You know what we’re sick and tired of at HFS? Ridiculous empty-promise press releases touting GenAI capabilities with no in-production use cases or substantiated benefits.

You know, the ones boasting “widget ABC now with generative AI”. A close second on the naughty list is press releases purporting to showcase generative AI capabilities but are really promoting the same non-generative AI capabilities they already had. Then there are all the promises of billions of dollars of “investment in GenAI” without any sort of accountability they’ll ever be held to it.

Let’s be honest, the entire marketplace is exhausted by genAI-washing, where everyone can pretty much claim whatever they want and never be held to account. This is such a shame because the potential is massive as we explore the seemingly limitless possibilities of GPT4 technologies.

So when we do manage to find actual GenAI use cases that are in production with real live customers and delivering benefits, we move like the BS-busting analyst cheetahs that we are, and we cover them! This was the case when Genpact briefed us on its newly developed anti-financial crime (fincrime) regulatory risk and compliance GenAI capabilities (see news release here). We approached with an appropriate level of “show me the outcomes” cynicism and were pleasantly surprised to find that despite its shiny newness, its capabilities were developed with not one but two actual clients (gasp), and they were showcasing in-production use cases.

Anti-fincrime regulatory compliance – super important, super manual

Despite financial services firms being the early adopters and now long-time poster children of applied automation and AI, these capabilities have not been adopted consistently across all business functions. Areas like shared services, risk modelling, and customer service have benefited substantially from intelligent automation beating down the manual processes caused by compounded legacy tech debt. But many processes within anti-fincrime functions like fraud, know your customer (KYC), and anti-money laundering (AML) have proven to buck the trend by being non-standard, requiring humans to make final decisions, and/or not being sufficiently explainable to satisfy regulators. The current state reality of many fincrime groups within financial institutions is loads of humans generating content to enable or justify decisions. This is intense, detail-oriented work in a specialized domain with a high burn-out rate.

Genpact, some edgy riskCanvas clients, and AWS came together to make fincrime compliance less soul-crushing

Genpact acquired riskCanvas, a software suite of AML solutions and a related consulting practice, from Booz Allen in 2019 to help enhance its fledging risk and compliance practice. A couple of Genpact’s riskCanvas clients, including Apex Fintech Solutions, were excited about the potential of GenAI and agreed to a discovery session turned hack-a-thon with Genpact and its partner AWS to road test AWS’ Bedrock foundational AI model capabilities. Genpact and its clients leveraged their respective private and secure data from riskCanvas, chronicling years of AML events, to feed various foundational GenAI models. The initial results were so encouraging they transitioned to a full-on hack-a-thon at the Amazon2 headquarters. From the event, two use cases rose to the top as offering the greatest immediate impact:

Automated sanctions screening alert decisioning – potential sanctions match data is automatically analyzed and compared against thousands of previous alerts, resulting in a detailed explanation of findings and suggested decisions. Human analysts make the final decisions. The benefits impact is 70% reduced handle time.

Suspicious activity report (SAR) narrative writing – automating the time-consuming summarization of SARs, including filing details, subject information, transaction patterns, and activity analysis, all based on an institution’s established standards and languages. Human analysts provide final review. The benefits impact is 60% reduced handle time.

It is critical to note that the generative capabilities of GenAI are also used to produce explainability statements. The hack-a-thons took place in July 2023. These production use cases were hardened and put into production quickly because the necessary data was available and already hosted securely on riskCanvas in the AWS cloud. Also critical to note – these are publicly available models used privately in a static format to ensure privacy.

Other use cases have also been identified – all loosely in the ilk of fincrime functions with loads of content documentation that needs to be produced and is currently heavily manual – like customer due diligence review and summation, case review and summation, fraud alert decisioning with detailed explanation, transaction monitoring alert decisioning with detailed explanation. You get the picture.

The bottom line. Genpact makes a bold step forward to make GenAI real and impactful in fighting financial crime. Banks tired of analyst burn-out take notice!

Nothing happens if you don’t try. Failing fast is a great mantra, but it requires effort. Kudos to Genpact, its intrepid clients, and AWS for experimenting and succeeding in building in-production GenAI models that can legitimately help better fight financial crime and improve the harried lives of fincrime analysts. The regulatory burden of documented proof of decisioning is a heavy lift for firms of all sizes. But it is a problem screaming for GenAI solutions – literally, the power of generative content trained on private data from past reports – is an ideal fit.

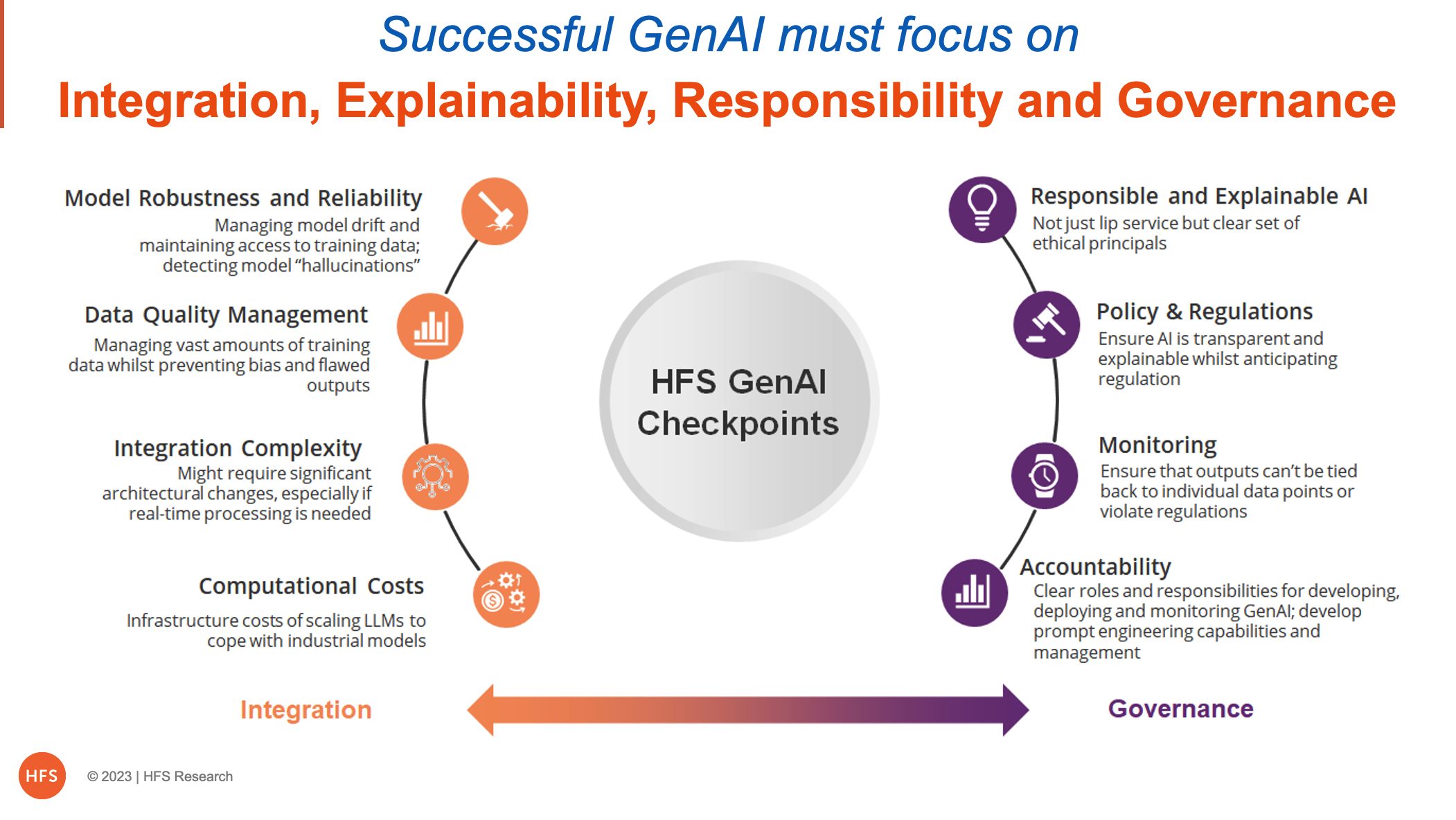

The rub for fincrime compliance typically is unhappy regulators. The critical nuance here is GenAI enables the humans, with humans taking all final decisions with full explainability documented. Here are our critical focal points for successful GenAI:

While this is a real and decent step forward, as with so much of applied automation and AI – it is focused on making existing rule-based processes less manual – rather than changing the processes. While the industry works towards a future of less rules-based fincrime compliance processes, Genpact’s riskCanvas GenAI is a much-needed step in the right direction.

Unlike most other technological breakthroughs in our history, Generative AI has caused a tidal wave of excitement and fear in our personal and business lives. In many ways, it feels like it’s 1998 all over again when the early days of the Internet dominated the lion’s share of both business and tech conversations and became embedded into the fabric of society.

While AI has been a fundamental part of our technological landscape for over a decade, GenAI represents a substantial leap forward, revolutionizing the way that we work, learn, and interact with technology and one another – especially the major enhancements between the ChatGPT 3.5 version that was launched last November and the recent upgrades to GPT4.

We caught up with someone who’s been a bastion of AI for well over a decade now, Paul Daugherty, the Chief Technology and Innovation Officer at Accenture, on the potential impacts of GenAI on enterprises and the workforce. Paul has been CTO of Accenture for over a decade and became Chief Executive of the $60bn firm’s technology business in 2020..here are some key insights from our discussion!

GenAI isn’t just eating software, it’s dining on the future of work

In this evolving landscape of technology – a new paradigm is dawning, one where GenAI is not just impacting how we use technology; it’s fundamentally changing the nature of work. As Paul aptly put it, “We used to talk about how software is eating the world, and now the new analogy is that generative AI is eating software, which means that we have much more powerful ways of interacting with technology than we had before, which stands to benefit the way we work.”

In this reality, it’s not just an incremental improvement on existing AI capability but a leap that has the potential to fundamentally alter our approach to work. While previous technological advancements optimized and streamlined processes, GenAI seeks to redefine the very nature of what organizations do and how they do it. “Whether it’s reimagining content creation in media companies or streamlining regulatory filings in financial and life sciences institutions, GenAI is about reshaping enterprises’ core processes and workflows.” It empowers organizations to rethink how they function – making it a game-changer in the tech landscape.

We’re entering an era of ‘no-collar’ jobs—where AI and humans collaborate to create new jobs

As we step into this transformative era, the concept of “no-collar jobs” takes center stage. Paul introduced this idea in his book “Human + Machine,” where new roles are expected to emerge that don’t fit into the traditional white-collar or blue-collar jobs; instead, it’s giving rise to what he called ‘no-collar jobs.’ These roles defy conventional categories, relying increasingly on digital technologies, AI, and automation to enhance human capabilities. In this emergence of new roles, the only threat is to those “who don’t learn to use the new tools, approaches and technologies in their work.”

While this new future involves a transformation of tasks and roles, it does not necessitate jobs disappearing. To Paul, AI isn’t replacing us; it’s giving us superpowers in our own domains. While technology can streamline the workforce, history has shown it often enables people to work more efficiently. According to an Accenture study, approximately 40% of working hours across industries will be impacted in some way by GenAI, but “that doesn’t mean that 40% of jobs go away because, in most cases, GenAI is impacting a part of a task somebody does. It’s making their overall job more effective, and often more fulfilling by removing some of the detailed work they needed to do – that can now be done by AI.”

In this reality, reskilling is a critical mandate. Paul emphasized the need to develop both AI development and AI usage skills are critical. He encourages companies to set up dedicated training academies and learning processes to help reskill their employees.

Paul’s predictions point to the next epoch of enterprise evolution

When asked to peer two years into the future, Paul made four predictions about GenAIthat signal a seismic shift in the evolution of the enterprise – alongside some cautions:

Accelerated Experimentation and Scaling: In a year, companies will shift from experimenting to scaling AI solutions, with more focus on specific use cases for widespread deployment. Traditional enterprise software companies will increasingly incorporate generative AI into their products, making it a standard part of operations.

Integration into Enterprise Software: Just as AI has become an integral part of enterprise software today, GenAI will follow suit. In the coming year, we can expect to see established software companies integrating GenAI capabilities into their products. “It will become more common for companies to use generative AI capabilities like Microsoft Dynamics Copilot, Einstein GPT from Salesforce or, GenAI capabilities from ServiceNow or other capabilities that will become natural in how they do things.”

Intelligence as core to enterprise architecture: Paul believes “embedding intelligence as a core component of the enterprise architecture” isone of the most significant changes businesses will experience since the internet. Accenture now calls this the “modern digital core, which businesses must develop so that they can integrate new capabilities like GenAI, operate more effectively and set the stage for new growth..”

The Inevitable Backlash: With great innovation comes a (healthy) dose of skepticism and backlash. GenAI will face its share of challenges, including managing expectations. Over the next year, some may be disappointed when they “realize that generative AI doesn’t solve every problem as easily as they thought.” Paul cautions that careful consideration of the business case, costs, and scalability will be essential for a successful transition – “We’re encouraging companies to start even at the experimentation stage with a business case-driven view.”

We’re at the tipping point of one of the most significant enterprise shifts ever, and there is much more to come (that perhaps we are yet to fathom). As Paul put it, “I believe we haven’t seen some of the significant innovations yet from an enterprise tech perspective where it’s entrancing to watch AI ecosystem players that are innovating in the models themselves.”

Responsible AI isn’t just a push from the Tech community anymore, it’s a market-driven requirement.

As organizations gear up to integrate GenAI into their operations, Responsible AI has moved from a push from the tech community to a market-driven requirement. In our discussion, Paul noted that while the foundations of fairness and ethical AI have remained consistent over the last few years – the approach has shifted. In the past, efforts were focused on pushing to educate people about these concerns; however, today, “what’s different now is that there’s a pull to find information on responsible AI because they understand the importance…and heightened risks of GenAI”.

With the escalating risks concerning intellectual property and the emerging concerns related to misinformation at scale (including the potential creation of GenAI-generated deep fakes) – a set of unique challenges has arisen with GenAI. These challenges have been instrumental in driving the demand for Responsible AI. Paul stressed the urgency for organizations to promptly establish a systemic foundation for responsible AI practices.

Bottom line: We’re at the tipping point of one of the most significant enterprise tech shifts ever. The first movers are the ones that will have an advantage…

No one is immune from the impacts of GenAI, and conversely, everyone has an opportunity. “What will make a difference is that the first movers will have an advantage. Those who now understand the technology and models, and look critically at their data estate, will establish a solid digital foundation and will have a sustainable competitive advantage.”

There you have it, folks. It’s a brave new world; are you ready to seize it?

Do you work for a firm selling a successful product that just requires staff to push rocks and turn widgets, where you’re unaffected by technology disruption and innovative competition? Where all you need to do is to turn up for work when your boss is looking, and you’ll get your annual payrise and bonus? Where can you just take off on holiday / go to whatever conferences… and all you need to do is slap on your “out of office,” and no one will bother you or dare stress you out with any work demands.

My guess is you don’t… although it was probably like that during the recent pandemic years and recent return to quasi-normality when most people took full advantage of the Great Resignation to put lifestyle very much first in their lives.

Over my career experience, a company is all about its people. If your colleagues aren’t passionate about your brand, barely enjoy working with each other, are struggling to delight your customers, or grow your partnerships, this post-pandemic business climate could well see your business fall away as more adventurous, disruptive, and passionate businesses steal your mindshare and usurp your competitive position.

Today’s business climate is not for the faint-hearted, and settling for a cushy lifestyle job is something you need to think very hard about as we all venture into a business environment demanding passion and focus.

Even Zoom is losing faith in the remote work ethic it helped create

The sad reality is that nearly half of companies are struggling to get their work ethic back to pre-pandemic levels – and when you consider that even Zoom is mandating staff back to the office, we clearly have a work motivation that is getting worse… not better. Zoom and most of the G2K are calling staff into the office 2-3 days a week (at a minimum) because they have lost the trust they are motivated, are putting the needed time into their jobs and have lost interest in collaborating with their colleagues.

Net-net, many companies’ leaders are struggling to motivate a dispassionate workforce and want to bring their teams back together physically to retrofit some form of the work culture they can remember from pre-pandemic times. Their problem is you can’t force people to be passionate and focused; you must show them the way and inspire them with great ideas and your vision for taking your company into a leadership position in your market. If you can’t do that, then you’re either working for a company living on past glories or you’re struggling to motivate yourself as a leader. Or both…

As our talent survey of service provider employees revealed last year, close to 9 out of 10 staff want to feel more challenged (and are bored), the only saving grace being that 90% of employees are passionate about the impact they can have on enterprise clients. So corporate leaders have to make sure their staff has that chance to challenge themselves if they want to avoid their firm slipping into the abyss of commodity work and demotivated staff.

Whether we like it or not, the vast majority of today’s companies rely massively on a motivated workforce to stay ahead of their markets during a time of genuine technological disruption and significant cost pressures from years of inflation and a tough economy.

Only a quarter of firms are going in the right direction with their people… make sure you work for one of them if you can’t fix where you are

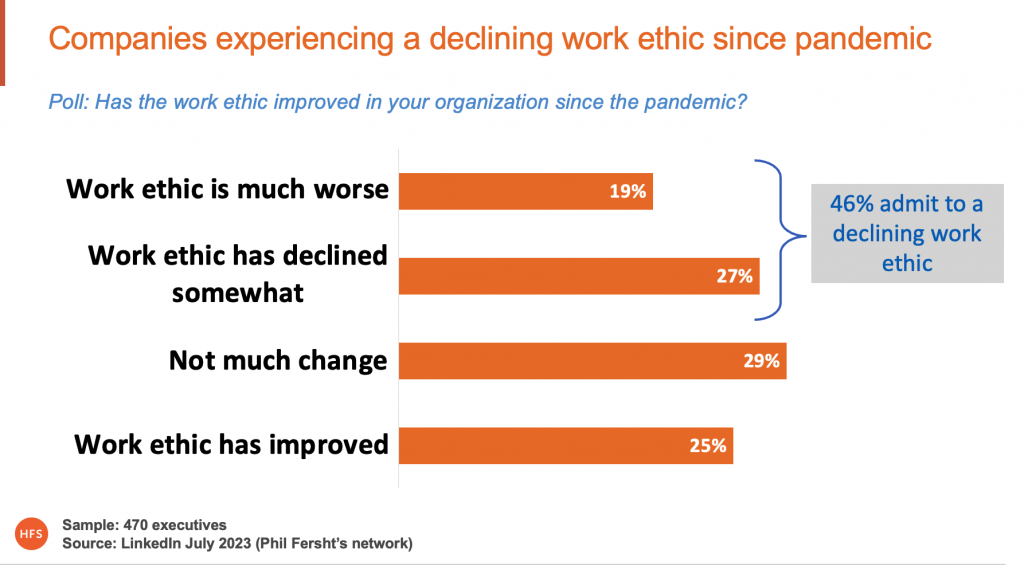

Most people in my network are associated with the tech industry – either selling/advising on technology services and products or implementing and managing them as part of their tech/operations leader role. So I thought I’d poll my network to gauge whether their companies’ worth ethics were improving or in decline:

When you consider most people on LinkedIn tend to give a more rose-tinted view of their business world, the fact only 25% see an improvement in work ethic is a pretty damning verdict of where we are. On top of that, close to half (46%) actually admit their company’s work ethic is bad or very bad.

This data does not bode well, with people getting laid off almost everywhere as the Great Resignation becomes the Great Freakout, and many companies are desperately seeking to offload the deadwood. So make sure you are not seen as deadwood…

Bottom line: Are YOU motivated to be part of a successful business, or do you just care about your lifestyle where a “job is a job”?

In short, you need to evaluate your own career trajectory and decide whether you have the appetite to be on the winning side in this emerging AI economy or if you prefer to meander around today’s strugglers where the work ethic dissipated away somewhere in 2020 and are still clinging to the memories of pre-pandemic days when their brands had real meaning and direction.

Only YOU can honestly answer that question for yourself. But don’t dwell too long deciding what trajectory you are on, as you may get left behind on the scrap heap of lethargic legacy brands that aren’t going to make it much past the next couple of years in this new economy.

Please stay true to your inner work mojo that got you here in the first place…

Barely ten months after its birth changed the world of technology, OpenAI unleashes ChatGPT Enterprise, where enterprises now have “Enterprise-grade security and privacy, unlimited higher-speed GPT-4 access, longer context windows for processing longer inputs, advanced data analysis capabilities, customization options, and much more.”

Assuming the 20 enterprises that road-tested ChatGPT Enterprise experienced these benefits in double-quick time, you have to take a serious look at scaling up GenAI tools or risk getting left behind with the most hyped technology since the Internet came to be…

The market is awash with BS about GenAI – and you already know it

As Kurzweil’s 2029 prophecy that AI will pass a valid Turing Test and draw level with human intelligenceappears less improbable, it’s vital we take a reality check to balance fantasy with reality.

Firstly, you gotta love the discussions of the displacements of jobs from AI. It feels like the whole narrative on equating automation and job losses just got reloaded with a GenAI sugar frosting.

Yet, at the same time, the build-out of capabilities on the service provider side is equally mindboggling as everyone claims deep capabilities of talent and solutions in barely a few months. To this end, HFS is currently engaging with the leading service providers to learn about their strategic objectives and capabilities to release our inaugural Generative Enterprise Horizon study on the topic.

Simply put, the whole enterprise world is absorbing GenAI information overload, and we need to take a deep breath and crystalize some issues that will drive enterprise adoption:

Take a long-term view on technology adoption: Technology and capabilities are continuing to evolve at an astounding rate, and their hype phases are shortening – we’ve only just come through the excitement of IoT, blockchain, RPA, Cloud, etc., and adoption of these technologies is still relatively immature and only just realizing their potential. ChatGPT was only released to the public last November 30th, and the GPT 4 series of foundation models later in March of this year, which already demonstrated a 10-fold increase in synthesis power among a host of other significant improvements and potential. However, enterprises are still struggling to adopt cloud! And we should remember that progress with GenAI is only possible when you fix your data infrastructure and integrate cloud and your other AI tools. With that, you have to digest all those surveys with data on adoption rates with a big pinch of salt as consultants and tech firms vie to lead the GenAI narrative. For example, many traditional NLP projects are getting relabeled as GenAI to make them sound more appealing among many other initiatives using older AI tech.

It is about the enterprise, stupid! GenAI has not infiltrated the enterprise in the traditional “vendor push” manner as most technologies – it’s being brought into everyone’s daily lives by users, especially the younger generation, for education purposes. Most GenAI examples are not enterprise-centric, and only a handful of projects have reached production. We must acknowledge that enterprise environments are not a smartphone. Enterprises are not closed systems but systems that have to deal with complexity and scale as well as the old foe that is legacy.

There will be big winners and losers in the AI arms race, and there is nowhere to hide. Whether you sell, advise, buy or use technology, there is an arms race to build out foundational GenAI models with these fresh dollops of crazy capital influx. If and when the hype bubble bursts (which they always do), the technology will be blamed. And, of course, it is the typical analyst question: Who are the winners and losers? Luckily we are not financial analysts. Our job is to guide on enterprise adoption not financial gain, but ultimately there will be winners and losers in the GenAI era, and you can’t hide from it.

Beware of the hyperscalers ringfencing their oligopoly: In our view, more – not less power is getting concentrated with hyperscalers, such as Amazon Bedrock, Microsoft Copilot, and Google Cloud generative AI. Just like cloud GenAI will be foundational. Yet, enterprises are already frustrated with the oligopoly. Both in terms of vendor lock-in as well as spend. Only with clear objectives can enterprises justify the costs.

Engage with the cool kids on the block like Nvidia, Databricks, and Hugging Face: Brand new ecosystems, including Nvidia, Databricks, and start-ups, are emerging. Enterprises don’t know how to navigate this. Everybody is trying to be the new best friend of Hugging Face, who could become the new RedHat. At the same time, who is getting hold of Nvidia’s GPUs as the key building blocks for GenAI have become a scarce resource? But

Your governance and explainability focus is critical. Most data privacy laws are trying to take a black-box approach with limited explanation or visibility, where something goes inside a black box, and something comes out and no one understands what happened inside the box. Yet, most Machine Learning is a black box with no explainabilty, but this largely went unquestioned until the recent explosion of focus around LLMs. To protect civil liberties, bias and other issues you need explainable AI. To this end, major legislation is looming: US AI Bill of Rights, and the EU AI liability directive as examples. And we are already seeing AI litigation is starting to kick-in. For instance, the FTC has opened an investigation into ChatGPT maker OpenAI over the potential harm it could cause and the company’s security practices. Lastly, responsible AI legislations around the world are not yet aligned on a common reporting format, thus, it is adding to confusion and delaying the initiation of responsible AI compliance by companies.

Get on top of enterprise data management. Anything touching our customer or employee data is more scrutinized than ever, and GenAI opens up a whole new can of worms when it comes to immersive it into the enterprise. Most Generative AI use cases use public data today. Getting enterprises to share private data will be challenging, if not impossible. We hear about approaches for data anonymization and for data impact assessments. But as we could see with GDPR, in the end, the courts will be the arbiters of the effectiveness of those approaches. Equally, how can enterprises deal with model drift and eliminate the randomness from these models’ outputs? Their responses evolve due to updates from new data. It is about the integration into complex enterprise ecosystems.

Scaling your GenAI is expensive – start building the business case now: Forget ChatGPT 3.5. For enterprises, GenAI is not free. On the contrary, to attract talent for data management, the rare breed of prompt engineers, or even to run your foundational model, requires deep pockets. And that is before the debate around Carbon Footprint of AI is getting started. In addition, getting access to the IT infrastructure to build and develop these language models gets expensive, and building business cases and longer-term viable cost models is going to dominate sourcing discussions in the coming months.

You must avoid a myopic view on productivity: The singular focus on productivity is misleading – remember how replacing people with techdestroyed the RPA phenomenon. We are hearing from service providers that they intend to shrink their talent pyramid by leveraging GenAI. Yet, what we need to focus much more on is the value creation. We are hearing about fantastic breakthroughs in science, but we have yet to hear about compelling examples of value creation in the enterprise.

Understand what GenAI is… and what it isn’t: GenAI is Machine Learning, and it is being trained on information that disparate sources have provided. So don’t expect a “42” thrown at you as the answer to life, the universe, and everything. And the last time we checked, it wasn’t sentient either. The next frontier for AI is becoming objective and goal-driven. Yet, we are early in terms of foundational research. It will be intriguing to watch the progress of Google with its Gemini project, which aims to add planning and problem-solving to the capabilities of LLMs.

From an enterprise point of view, what all of this boils down to is integration and governance. In the exhibit below, we have highlighted the critical elements. It is about building on and expanding all the hard work at the intersection of cloud, data, and AI. GenAI is not supplanting all this. All the noise about the democratization of AI is misleading, as we still need the infrastructure and the talent to run all these models. Talent that understands GenAI is not growing on trees. Thus, it will not only be an arms race for AI capabilities but for talent. And we should remind ourselves of the learning of cloud adoption. Cloud-native talent remains scarce, and many cloud transformations fail. It is all about the learning from those experiences. Therefore, we have to learn so much more about GenAI and beyond. Cutting through the market noise is an essential early step on that journey.

The Bottom Line: Enterprise adoption of GenAI is all about integration and governance; therefore, operations leaders need to take a long-term view focused on value creation

The development of GenAI is demonstrating an unparalleled compression of innovation cycles we’ve never before seen. Yet, all those headline-grabbing reports on enterprise adoption are focused on capabilities (and sales ambitions) rather than the critical issues of integration and governance. Therefore, we urgently need to learn more about the real experiences from the early deployments to drive more nuanced and relevant discussions. As far as we can tell, the Singularity is not yet nigh. But stay tuned for our inaugural Horizon!

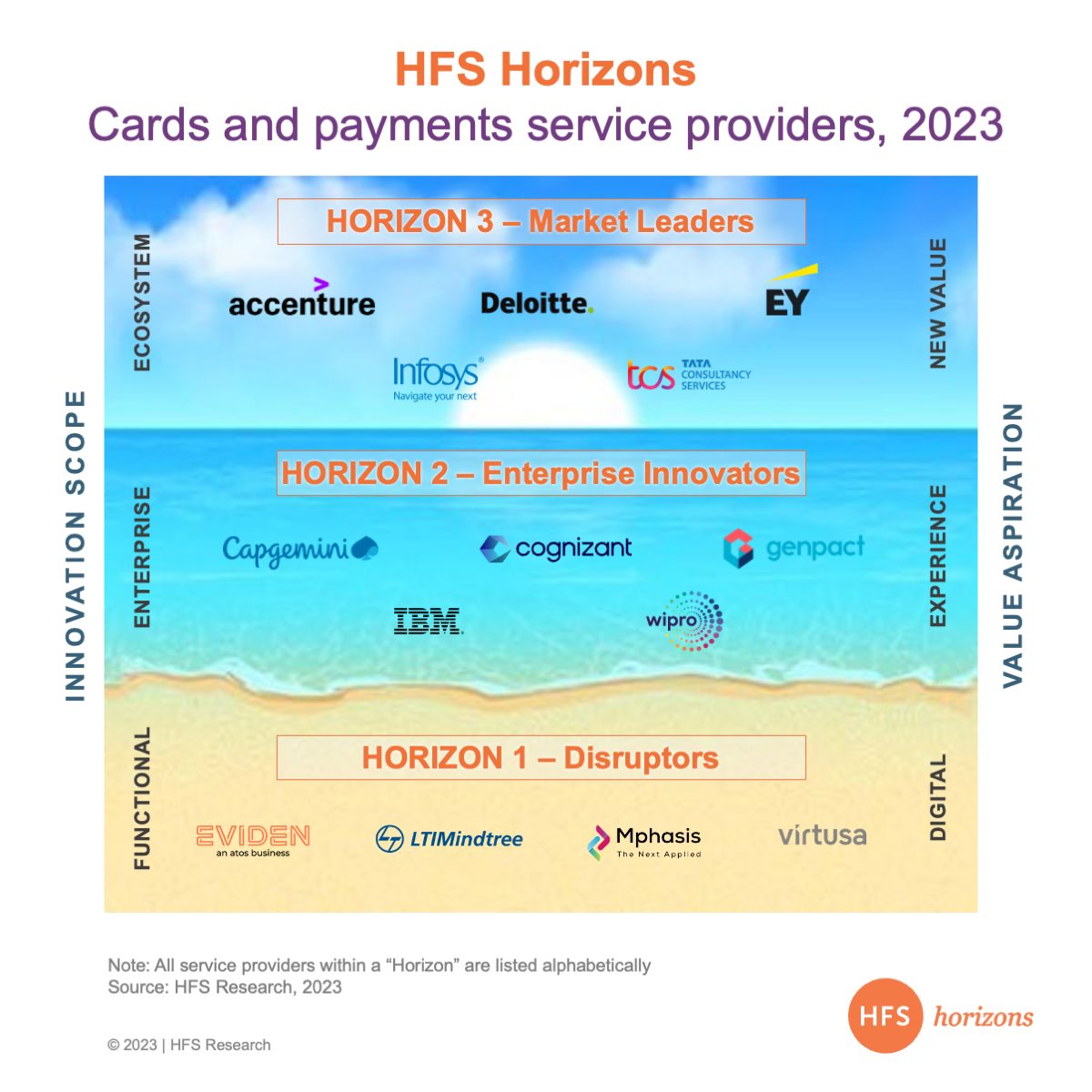

HFS launches its first-ever cards and payments Horizons report. Payments demonstrate the fastest innovation cycles in BFS and are in a constant state of disruption as digital models decimate the cost and data intelligence capabilities of legacy systems.

Payments were once perceived by the world as largely tangential to the banking and financial service industry (BFS), but today they have morphed into a melting pot of innovation and one of the most compelling areas of activity and investment in new capabilities within financial services.

The effects of developments in payments are far-reaching, with a broad impact across consumers and businesses. Payments-industry shifts are forcing incumbents to work harder to capture growth, pick up the pace of digitization, gain economies of scale, and manage risk—all while contributing to innovation. These demands can be overwhelming, but the potential for growth and innovation in the payments space is real. Therefore, attracting new players in great numbers, crowding the market, and raising the competitive stakes.

The payments ecosystem is more dynamic than ever with multiple forces at play, and smart service providers are seizing the opportunities

We took an all-hands-on-deck approach to understanding the changing landscape and role of service providersfor our2023 Horizons report oncards and payments, where we evaluated14 service providers (Exhibit 1) and interacted with 40 enterprises that contract with them. Here are the top payment marketplace takeaways.

Exhibit 1: Seeing the opportunities emerging from payment evolution is not the same as being able to seize them, need the help of service provider partners to seize the opportunity

Note: Service providers within each Horizon are listed alphabetically.

The many manifestations of digital payments

Digital payments take many forms; high-profile payment vehicles include digital wallets, real-time payments, buy-now-pay-later, blockchain, super apps, and crypto payments. The most recent incarnation is mobility payments. Here, one size doesn’t fit all; different markets and regions have had success developing payment business models for specific demographics with strategies embodying the elements defining them. Common elements of a winning model include a connected infrastructure, a forward-looking regulatory view, customer intuitiveness, leveraging emerging technology, and a compelling value proposition rather than just cool technology. All digital payments have exhibited a promising future; however, players that can monetize services and data are poised to capture a larger share of revenue pools.

The promise of multiple monetizable opportunities

Nontraditional players are jostling with banks and payment service providers to become issuers, providers, processors, or partners of choice, causing a proliferation of payment providers. The promise of monetizing across various touchpoints of consumer and commercial customer journeys has everyone excited. And we can’t leave out the payments-adjacent revenue pools, such as unlocking data to capture personalization and marketing opportunities, the ancillary prospects of open banking and embedded finance, and software, platforms, and services surrounding the payment. The payments space is becoming crowded, so market participants must work hard to create differentiated value positions to win in the marketplace.

Modernize or risk disintermediation by customers

It’s time to retire legacy monolithic payments architecture in favor of more flexible systems to accommodate digital payments, integrated services, and related new payment technologies. The archetypes of modern payments architecture include cloud or hybrid models using a modern microservice-based framework, scalable data platforms to access data through standardized APIs, a nimble and adaptive ecosystem, and decoupling legacy workflows and augmenting them with new workflows powered by emerging technologies while supporting seamless integrations with external software and platforms.

The Bottom Line: There is no silver bullet that solves all payment challenges; however, there are clear action steps that participants can take to improve their positions and gain or maintain competitive advantage

TheHFS Horizons: Cards and payments service providers, 2023report includes detailed profiles of each service provider supporting the cards and payments ecosystem, outlining the service provider’scapabilities, strengths, provider facts, and development opportunities.

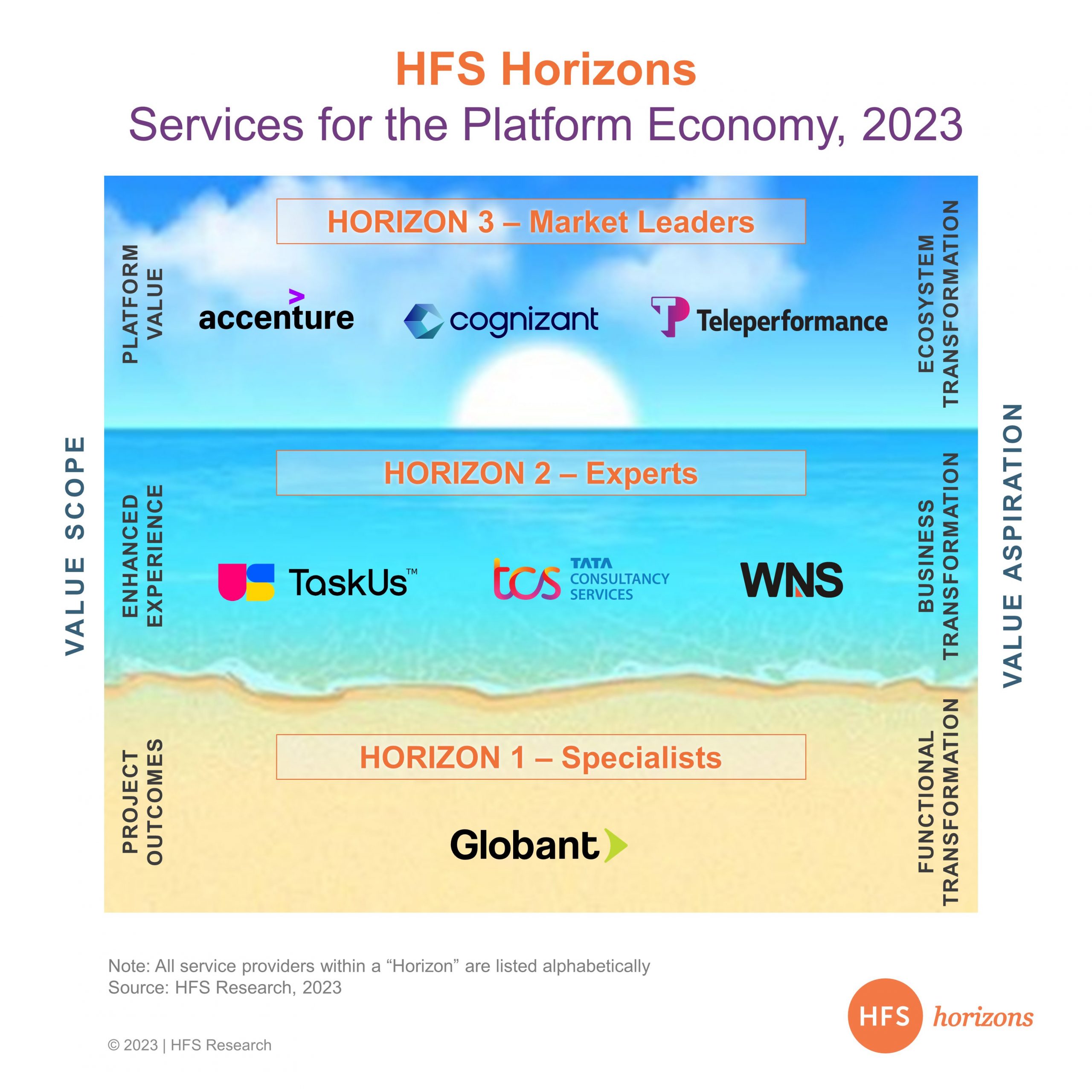

The last decade-plus has seen the ascendancy of platform businesses like Uber, Netflix, Amazon, Facebook, Google, and Spotify… and today, six of the top 10 global businesses by market capitalization are platform businesses.

These businesses have changed how consumers and producers interact, companies compete (customer acquisition becoming more important than profits), and value is created in the economy. These platform companies with new rules of engagement, reimagined value chains, and non-conventional business models constitute the platform economy.

These companies rule the roost in market share and technological advancements. For the past few years, many leading platform companies, including Amazon.com and Meta, have been working on and incorporating recently introduced technologies such as LLM and Generative AI.

The opportunities for service provider partners continue to proliferate

The platform companies, especially start-ups and next-generation platform businesses, are constantly looking for providers that can respond to their platform’s network effects, understand the multi-sided nature of clients (providers and consumers), play the role of an orchestrator in ecosystem building, show preparedness to handle rapid scaling, and help in geographic expansion. Correspondingly, the platform economy has become an irresistible customer segment for IT and business process services (BPS) providers. However, few providers have been able to crack the code required to work with platform businesses.

The Services for the Platform Economy, 2023 Horizons report covers seven notable providers helping their platform clients efficiently run operations, expand business, and realize value. Horizon 1 constitutes niche and specialized services catering to specific aspects of a platform business, such as digital engineering or digital marketing. Horizon 2 retains the values of Horizon 1 plus looks at a diverse portfolio of services and core competence in working with platform clients with varying business models. At the pinnacle is Horizon 3, encapsulating all values of the previous Horizons plus a focus on an innovative portfolio of tailored services and instances of co-innovation, driving completely new sources of value with the HFS OneEcosystem™ approach.

Exhibit 1 summarizes the Horizons philosophy and key underlying dynamics, showcasing the providers across the three Horizons.

Exhibit 1: Accenture, Cognizant, and Teleperformance are driving value with the HFS OneEcosystem™ approach

Note: All the service providers within a Horizon are listed alphabetically.

According to the report’s lead author, Ashish Chaturvedi, “The ascendancy of the platform economy ushers in a transformative era in the enterprise world—six of the world’s top 10 companies by market capitalization are now platform businesses. This dynamic shift redefines traditional business boundaries, compelling the market to embrace eco-system-driven opportunities, multi-sided customer lifecycles, and manage hypergrowth phases. Service providers are pivotal in fostering this growth and innovation by sharing and managing their platform clients’ critical business and IT activities.”Read More

When every tech firm is pounding out an identical narrative to seize their pound of GenAI marketing flesh, who better to turn to than Don Draper to unearth that golden nugget that makes them special in the mind of the buyer?

The greatest marketing opportunity since the invention of cereal…

Tech providers… when it comes to differentiating your capabilities, you need to resonate with the audience you’re targeting, not simply scream more noise into the ethernet. Do you really think anyone wants to hear about your new suite of GenAI tools that just appeared from nowhere and sound suspiciously like your usual crop of offerings with “GenAI” simply glommed on top?

The answer is no – people are excited by the potential impact of GenAI on their lives – both their work and their personal experiences. They want to know how they can be better than they are – and how to make others around them better. They want to know how to keep enriching their experiences because of the promise of GenAI… not simply how they may become so programmable they will lose their job or the huge productivity gains that will make their corporate money people happy.

In short, we must stop making the same old mistakes of viewing anything new and shiny as the next productivity tool… this is what killed RPA (remember that?). The beauty of GenAI is the simple reality that it brings human-like intellect into our technological lives… it’s about extending the brilliance and creativity of ourselves, not about replicating and subsequently eliminating our minds.

The key is for tech providers to convince you to take a bet on them

You must avoid creating panic and desperation to sound as credible as everyone else or make out you’re spending more money than everyone else. Ultimately, you want your clients and your competitors’ clients to find you compelling enough to talk to you about this and view you as a partner worth taking a big bet on… and they’ve all got some very big decisions to take and some very big risky bets to make.

We all know by this point that GenAI promises the first seismic business-tech inflection point since the advent of the Internet in the mid-90s. GPT-4 is real; it is a whole new way to interact with the Internet, to learn, to collaborate, to program, to design, to re-invent, to make us happy. It’s not just disruptive; it’s positively destructive. It’s really, really personal.

GenAI is powerful because it is personal… it can make smart people happy

So the whole tech industry needs to get away from this press release disease of copying each other’s fluff and actually change the whole conversation to make it meaningful – and make it personal. Unlike most technologies, GPT is being driven by consumers, not corporations pushing out the next productivity tool, which can help penny-pinching CFOs cut staff and shift work to cheaper locations.

People are bringing ChatGPT into their enterprise in a similar fashion to the way Apple Macs were submerged into enterprise environments… employees demand superior technology when it raises the quality of their work and their personal experiences. And savvy corporate leaders will support tech investments when they see how the improved experiences stimulate employee morale, and their improved happiness and passion result in better competitive performance.

Bottom-Line: Most people are turning off GenAI and will only pay attention when someone can make it all about THEM

Back in the 60’s, you had six tobacco giants trying to convince the world that cigarettes were not bad for your health, as more and more evidence gradually unfolded linking smoking to cancer. Fast forward to today, and it must be similar to convince people about the threat of climate change and actually doing something about it while various politicians and big businesses attempt to sow doubt into people’s minds (even though only the most ignorant are still in denial).

If only we had Don to spur us into climate change action with another brilliant campaign idea. If we made climate change about how it impacts you personally, then perhaps more people will actually do something about it, rather than confuse us with Net Zero targets and thrusting intellectual elite snobs on us, jet-setting to their latest fancy conference, to make us feel very stupid and unworthy.

It’s also the same with GenAI… the tech world must convince people how amazing the experience is to them, genuinely demonstrating how they can immerse themselves in a new technology that everyone can immerse into their daily lives. GenAI may not be toasted, but it can make you happy…

New TCS CEO K Krithivasan (left) taking the reins from Rajesh Gopinathan

So new(ish) TCS CEO MD K Krithivasan (or just “Krithi” to those who know him) has made his first move in his new role – to re-jig the familiar cast of TCS characters and move back to the more industry-centric structure that made TCS so successful in the past, including Krithi himself as their financial services leader. As expected, no one new is brought in, and it feels very much like a TCS re-org… focusing on the familiar tenured gentlemen and focusing on what worked in the past.

Is this new structure really going to propel the company forward in the AI-driven era where scarce skills in areas such as GenAI are at a premium and intra-company collaboration and training are more critical than ever? Does having an all-male leadership team send the right message to clients and employees, where diversity is so important to its culture and enticing the best young talent?

Krithi is doubling down on an industry-led go-to-market

TCS announced a new operating structure for the company that organizes its 40+ Industry Solution Units (ISUs) into seven verticalized business groups – BFSI US, BFSI RoW, CMI, Life Sciences & Healthcare, Manufacturing, Retail, and Technology and Services. With this change, Krithi has pretty much wiped away Rajesh Gopinath’s (his predecessor) 2022 re-org, which was structured mainly by client size categories and has returned TCS to a tried-and-tested model.

Going back to familiarity can paper over the cracks

For TCS, the recent structure has caused a lot of internal politics and issues with access to scarce resources, so going back more to what they are familiar with should help calm the waters as they target more client wins and expansions.

The pros are increased specialist skills in certain industry verticals where TCS is well-resourced to win smaller deals as opposed to accessing a generic talent pool – assuming each vertical has an adequate scale of talent.

Going back to industries spells a re-emergence of old-world fiefdoms, which can stifle collaboration and neglect emerging business opportunities

The cons of this structure are that specific industry units get preferential access to talent, making it harder for emerging industries to have the investment needed to be competitive. In addition, industry segmentation like this can lead to fiefdoms and poor collaboration, which ultimately could stunt the growth of TCS. Moreover, reverting to the old “vertical fiefdom” approach doesn’t bode well for TCS investing in smaller-scale opportunities with emerging clients, which could deliver longer-term growth potential, and places the emphasis on the same old slow-moving juggernaut clients which suck up resources and often do not want to move beyond the butts-on-seats Walmart model.

While it’s understandable Krithi wants to revert to a structure that made him very successful, this signals a sideways move in contrast to the likes of Accenture, which focuses its structure heavily on geographic localization of resources that has spurred huge growth for the firm over the past couple of years.

This latest re-org doubles down on execution focus versus innovation focus.

The industry focus allows them to be close to their clients, understand their context, and ensure delivery is flawless. But to drive innovation, you need a OneOfficeTM model – where they need to seamlessly integrate their IT, business, engineering, and consulting services in an easy-to-understand and simple-to-consume way. Accenture is driving this with “One Accenture for shared success,” and Wipro’s latest re-org is trying to achieve this OneOffice mindset.

For TCS, creating the OneOffice will be difficult to achieve in its new (or back to the old) industry-led model where the biggest verticals get the brightest resources and drive innovation in silos. It is also complicated for clients to navigate.

We’ve interviewed nearly 50 TCS clients over the last 2-3 years for our Horizon studies. Their clients’ average scores is a strong 8.7/10 for execution but drops to 8.0 for innovation. We doubt if that will change significantly with this new model.

With Generative AI promising to change how services are consumed and delivered, we were expecting a bit more forward-thinking from TCS versus going to back to a decades-old tried and tested model.

The re-org does nothing to drive forward TCS’ gender diversity while promoting long-time company servants

Executives like Abhinav Kumar, Ashok Pai, and Harrick Vin are very strong leaders in their own right and will surely do well in the new regime. However, it’s very disappointing to see the lack of gender diversity in the appointments, and Rajashree has performed very well as CMO, with some smart branding, especially the extensive sponsorships of marathons which has gained real visibility and alignment with health and wellness across the world.

With Rajashree’s demotion, TCS now has an “all-Indian male” leadership team. This does not augur well for a company that is considered by many as the bellwether for the IT services industry.

Bottom line: This structure is designed to embrace the tried and tested ways that have yielded success for TCS in the past. However, it is likely to create vertical stove pipes and stifle innovation required for changing the status quo

Will the TCS factory model continue to roll on? Most likely. But is it going to be an exciting journey? No way! The dawn of GenAI has created a unique opportunity for the IT and business services industry to jump to a new S-curve of value creation for enterprises. We wished TCS looked at this as an unmissable opportunity to create a forward-looking org structure versus a conservative back-to-the-past re-org.

While we’ve been very busy weaving lots of GenAI into our research model, we haven’t ignored our primary strategy of hiring great human talent. As we evaluate people with diverse backgrounds and personalities, we’ve landed on a very smart analyst in Toronto who’s into pottery, sculpture, drawing, photography, and roller skating. Yes, this is exactly what we needed when looking for someone to help drive our Employee Experience research with deep technology chops.

With a background in Anthropology and IT, Dana Daher brings a unique human-centered perspective to the world of technology. In her new role, she will collaborate on key research areas impacting clients across Employee Experiences, including HR technology, EX services, automation, generative AI, DEI, and sustainability.

So let’s learn a bit more about Dana Daher and what she brings to the table after her experiences with the likes of Unisys and Info-Tech Research, and of course, roller skating…

Welcome to HFS, Dana! So, what gets you up in the morning besides a good roller skate?

My mini cockapoo Junie! Her morning routine is always the same, and it never fails to make me smile. As I open her crate door, her tail starts wagging with infectious enthusiasm. Her joyful trotting echoes through my apartment as she jumps to the couch, waiting to greet me for morning cuddles. Her morning rituals shape mine, and with a warm cup of coffee, I am ready to start my day.

What keeps me inspired throughout my day is my passion for understanding the technical and human aspects of the digital world! With a background in anthropology and a career in IT research, I am fascinated by how technology shapes and is shaped by human behaviour, beliefs and practices. Where possible, I find opportunities to instill anthropological inquiry and practices, striving to contribute to a more human-centered and socially responsible approach to technological innovation.

Your diverse background is fascinating! How has the combination of your experiences influenced your career journey so far?

Because of my diverse background, my career path has never been straightforward. From consulting in vendor management, data analysis and validation, leading research and advisory in digital transformation, to driving a research practice in a technology organization, I have acquired and practiced numerous approaches to pinpoint systemic trends and client opportunities.

I always thought of my skillsets as a formidable trio on a battleground – each complementing the other seamlessly. My training in anthropology enables me to closely observe and interpret behaviours, patterns and cultural nuances – granting me insights into strategies and decision-making patterns. My expertise in data analytics allows me to analyze vast datasets to discern patterns and predict moves. Last, with a passion for all things digital, I explore the exponential stretches of technological innovations to navigate their trajectory. My wide range of passions and skill sets allow me to help clients wield data-driven intelligence and technological advances to conquer the challenges of operating in an ever-changing landscape. Throughout this process, my focus remains on prioritizing the needs of people at every step of the way.

And why choose HFS? What will you be writing about? What is it you care about?

I’ve been fortunate to work with HFS folks from a vendor-client perspective and in prior roles. I’ve found that, undoubtedly, HFS boasts a team of brilliant individuals who bring their unique perspectives and expertise to the table. One thing I’ve admired – and is certainly a key differentiator amongst analyst firms – is the no BS/nonsense approach to research and writing. It’s an approach that cultivates an environment of transparency and honesty which I find refreshing.

In my new role, I will be leading research in Employee Experience. I will explore how employees engage with their work environment – capturing the tools, culture, and physical environment. I will explore best practices, emerging technologies and their impacts on shaping an employee’s journey through an organization. To kick off this role, I will be building out the Employee Experience Horizon – diving into the needs of enterprises when it comes to EX and how providers are addressing them.

Dana was recently in Edinburgh, trying not to look like an American tourist…

So, finally, Dana, what do you think we’ll be talking about in a year?

Looking ahead, the discussion will continue to center on how organizations are coping with economic volatility and the increasing need to do more with less. One prominent solution in the tech world that continues to dominate today’s discourse is AI and generative AI. I’m keen to expand on the Generative Enterprise concept from HFS as it relates to EX – exploring how AI can elevate employee experiences, augment work, enable worker autonomy and generate new efficiencies. I will explore the impacts of AI on employees through an ethical and human-centric lens that sustains a level of empathy.

Beyond this, whenever I think about what I will be talking about in one- or five-years’ time, I start with mega-trends. These are trends that happen on a large scale, are linked to our past and unfold over an extended period. Several megatrends around us will impact everything we know today, including climate change, demographic shifts, increased connectivity, and blurred digital and physical realms. Each of these megatrends poses questions about their impact on the workforce. They lead to questions like: How will climate change influence an organization’s operational costs (e.g., energy consumption, resource management)– and how will that impact its workforce? Will there be changes in work demands or job responsibilities due to wider ESG measures? How will digital-native generations influence the organization’s technological capabilities and digital transformation efforts? What are the skills required for the future digital workforce? and much more.

As populations grow and the world begins to feel much smaller, the modern enterprise must adapt and ensure it meets the evolving needs of its workforce to thrive. There are many topics to discuss within these mega-trends; you’ll have to wait to see what we focus on!

Well welcome to HFS, Dana – we can’t wait to read your insights!

Thanks, Phil! I’m looking forward to this new journey!

There appears to be a strong whiff of Zeitgeist in IBM’s intention to acquire Apptio. Macro headwinds are putting brakes on budgets. Cloud costs are rising – so where better to drive value to enterprises than help them manage their technology investments?

HFS strongly believes these mega-software compilations can only fulfill their potential when combining transformation services with the software. The days of selling expensive software to CIOs without a real business plan to integrate them effectively across the enterprise and then develop and manage them are fast fading. And there is no greater example of this than IBM’s acquisition of Apptio. It looks great on paper, but this investment will come nowhere near achieving its objectives if the platform is not developed to deliver a holistic view of IT spending, with a services alignment to help them achieve this quickly for needy enterprise clients.

Apptio addresses the first half of the Digital Dichotomy – reducing costs. Now it needs to help enterprises innovate at speed

2021 and 2022 have been dubbed by many as the “Big Hurry” years, where so many enterprises were desperate to transition to their desired cloud states and worried less about some of the cost and transition work it entailed to get there. 2023 has turned into a “Digital Dichotomy” where cost pressures have become massive for so many enterprise businesses, but they still need to move at real speed to benefit from the cloud outcomes that will keep them competitive.

This is where the core value is for the future of an IBM-led Apptio solution… to manage costs while supporting innovation investments at speed. Operational leaders have to accept that cloud transformation is not a cost-reduction exercise. The benefits lie in cultural change leading to the capture of new sources of value. With that, the value proposition of any spend management tool has to be expanded to enable transformational change. In our this view, this is the context for the Apptio acquisition.

Additionally, IBM’s growth rates are slowing, and Apptio has reached another plateau in its corporate development as it has struggled to expand its sales reach. By paying a substantial $4.6bn, IBM is looking to create a new software category that, in the words of Rob Thomas, SVP Software and Chief Commercial Officer, “will give customers a virtual command center to understand their technology spend, their cloud spend, and their labor spend.” An elevator pitch that should echo the thoughts of many leaders in these challenging times. But it has to be filled with proof points, not only compelling narratives.

Apptio’s progression from IT cost management to FinOps

Let’s rewind. Apptio, founded in 2007, created a new software category Technology Business Management (TBM). The goal was to run IT like a business where you manage cost. Basically, by providing CIOs and senior IT operations executives with the necessary tools and insights to optimize IT costs, align IT with business objectives, measure performance, and drive value for the organization as a whole. Core IP is based on a “standardized” cost attribution model for shared platforms across infra/apps/services, which could be used to run a chargeback model for all IT Services delivered to a line of business entity. At the same time, innovative Apptio did hit a plateau. Its initial focus was on-prem, but a series of acquisitions (e.g., Cloudability) led to extending this approach to cloud-native platforms, predominantly the hyperscalers. Yet, Apptio could never progress beyond financial management and strategic planning. For many, Apptio has become a leader in FinOps; nonetheless, it is easy to forget its roots.

Spend data meets telemetry data which ultimately becomes aligned with AI

Fast forward to what both companies had to say in the announcement. The intent is more significant than either TBM or FinOps, much bigger. IBM intends to bring automation and FinOps together. Put another way; the ambition is to link spend management data with broader operational telemetry data. Not only this, but the acquisition will be a conduit for enabling actions and, ultimately automations, for a multitude of inputs from AIOps, Observability, and beyond.

This is about expanding the integration of Watson capabilities into the various Cloud Paks. From a product point of view, the plan is to blend Apptio with the capabilities from the newly-launched Watsonx platform and acquisitions like Turbonomic, Instana, and MyInvenio. AI is meant to be the glue and the catalyst for an expansive suite of IBM-owned assets. As so often, the proof will be in the pudding.

IBM describes Watsonx as full technology stack” for training, tuning, and deploying AI models, including foundation and large language models, while ensuring tight data governance controls. With that, Apptio conceivably will be heavily aligned with GenAI. Additionally, the data from IBM’s multiple acquisitions provides a large set of telemetry data to bolster the spend data provided by Apptio.

Take Turbonomic, which helps customers overcome silos in IT Operations as it brought together applications resource management and network performance management. To progress toward cloud-native operations, organizations must develop the ability to convert insights from logs, metrics, traces, and dependency maps into actions across the enterprise. For most organizations, the progress has stopped at insights. And those insights are often confined within siloes rather than providing an enterprise-wide view. The North Star is the ambition to run operations across the boundaries of IT and business. Apptio never progressed beyond providing insights, while IBM needs to demonstrate the proof points for integrating its disparate capabilities as well as progress from insight to action and, ultimately, automation.

IBM Software must work with IBM Consulting transformation more effectively

So how can the worlds of telemetry and spend data come together? IBM’s AI assets are meant to improve Apptio’s already decent ability to ingest and classify data, detect anomalies in data or operations, and create recommendations. It is here where the integration of those disparate data assets is meant to happen. In essence, if successful, the ability to act on – and ultimately automate – all those insights is pretty much the operational Holy Grail.

Just for transparency getting expansive spend management and FinOps capabilities in itself will be a solid asset for IBM. However, any new and bolder proposition aiming at the bigger transformation price must move beyond technology and include stakeholders and change management. The ambition could be a broader business assurance where spend data, operational insights, and governance get tied to business objectives. In our view, this provides a significant alignment opportunity with IBM Consulting as it seeks to differentiate itself from the likes of Accenture Operations and Genpact. Having a deep services alignment with Watsonx and Apptio will bridge together the ability to manage the cost and value of both cloud transformation and AI investments – provided it gets it right with its global talent base of technical and process domain specialists.

Apptio must prove to be more than just FinOps

Foremost the value proposition must be broader than the narrow cost focus of FinOps. As Kareem Yusuf, SVP Product Management and Growth at IBM Software, explained: “FinOps is just one use case of the overall proposition. We probably might need a new terminology to capture the value proposition”. In our view, this should not just be about a new terminology but a new way to manage transformations enabled by cloud. As clients progress toward becoming cloud-native, IT and business operations must move together. Clients want end-to-end process insights and the efficiency to react to any incidents. Whether we need to create a new moniker to capture those capabilities is debatable. What IBM is proposing is as bold as it is complex. We look forward to seeing the first proof points…

Bottom line: The contours of a new value proposition for managing transformation are bold, but as always, the proof will be in the pudding

Net-net, it is a good deal for both IBM and Apptio. IBM didn’t have much spend data; therefore, there is little overlap in terms of products. The ambition is bold. But the Holy Grail of operations is having an operational single pane of glass that includes automation and AI. If IBM can integrate all those acquisitions and get all that telemetry data out of its often highly specific domains, it can achieve strong differentiation in the market. Conversely, Apptio had hit a sales plateau as it struggled to scale its sales reach. Getting $4.6bn for hitting a plateau is too good an opportunity to turn down.

The rationale behind the deal is built on aspirations. It must be because $4.6bn is no peanuts. We have heard the sales pitch, but now we need to see concrete outcomes. But we have heard many claims from IBM over the years. Top of my mind is the claim that IBM is winning big AMS deals because they allegedly had linked RPA with AIOps. However, we still must see the proof points. IBM’s Apptio bet is to drive a new value proposition of an end-to-end operational single pane of glass linking technology performance and spend data. If successful, such a proposition will create high demand in today’s challenging macro headwinds.