- Search

The Services-as-Software™ Framework: Building Sovereign Intelligence in the Age of Rented AI

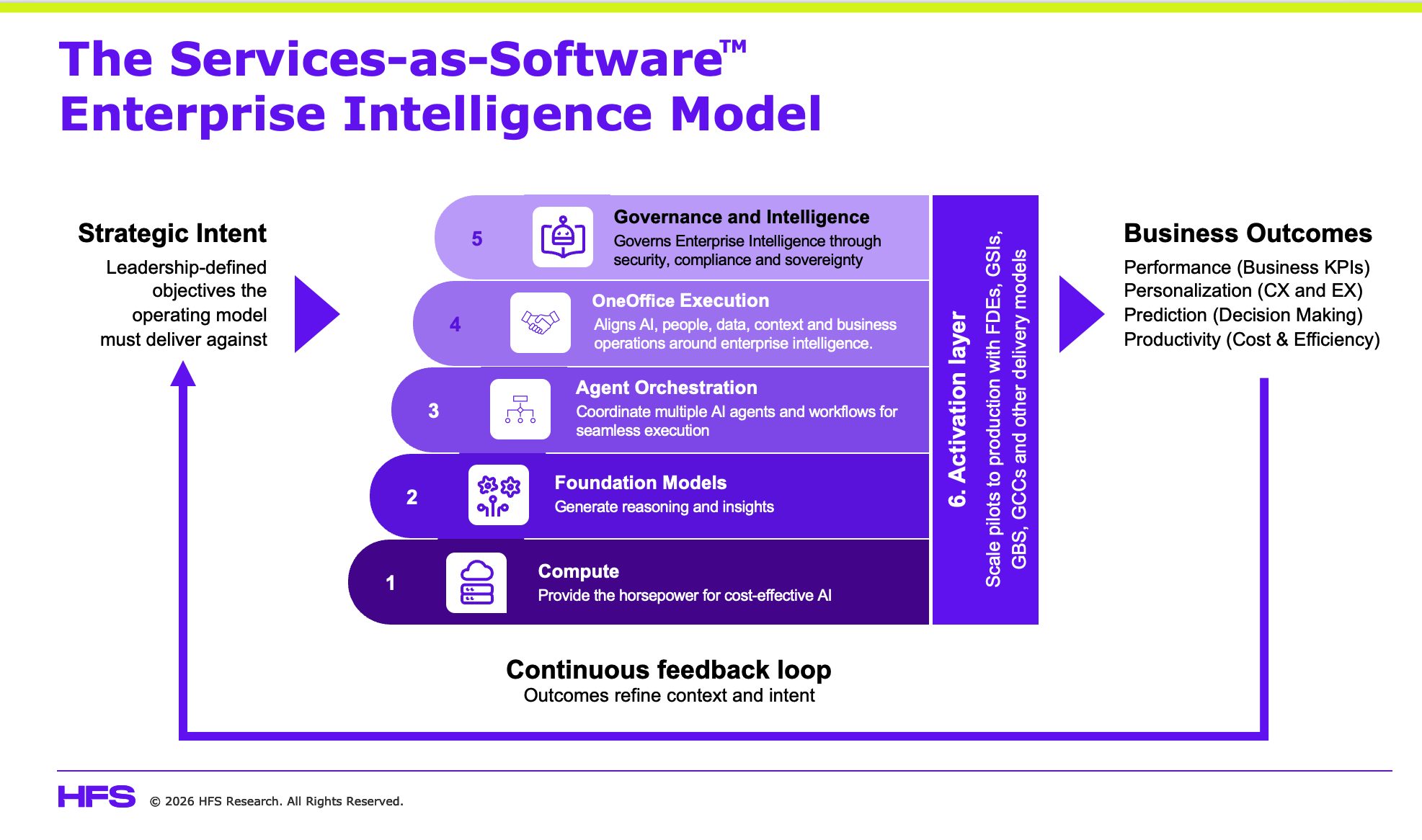

Services-as-Software™ is the HFS operating framework that enables enterprises to build Sovereign Enterprise Intelligence by capturing and codifying human expertise, then continuously improving it through execution.Our Services-as-Software™ Enterprise Intelligence Model connects leadership intent with business execution through six tightly integrated layers, all guided by a clear strategic objective. Every organization begins with an outcome it is trying to achieve, whether improving customer experience, accelerating product innovation, reducing risk, or transforming operational performance. Read More

The AI balloon is bursting and services must be ready to pick up the pieces

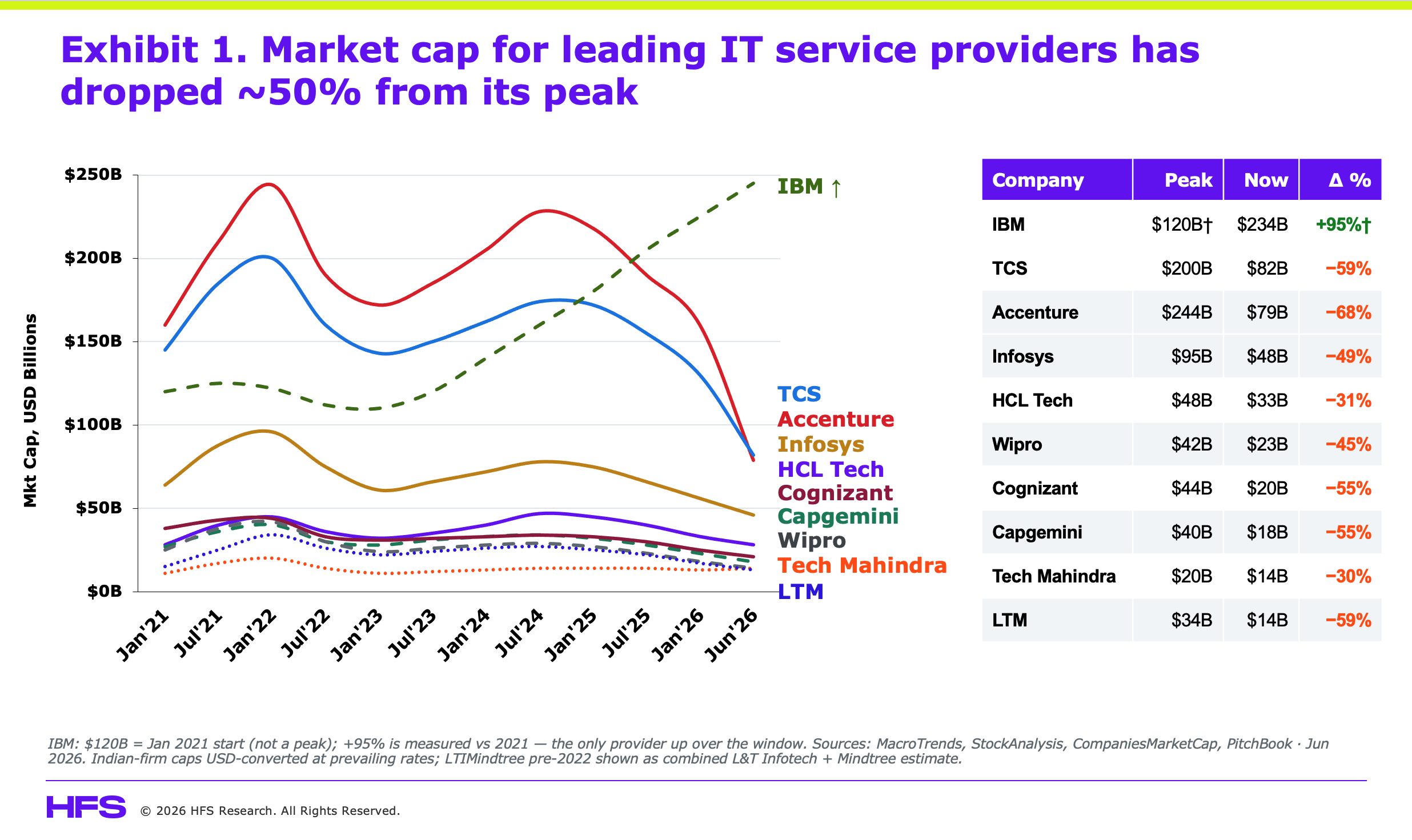

Wall Street has drawn a remarkably clear line between winners and losers, with AI-native companies representing the future and traditional IT services firms increasingly seen as part of the past. One side now commands price-to-sales multiples of 60x to 100x, while the other is steadily drifting towards 1x as investors bet that AI will replace the labor-intensive services model that has dominated enterprise technology for the last three decades.The problem with that narrative is that it only works if enterprises can actually deploy AI at scale, and today they simply cannot. Until organizations resolve their technology, data, process, and talent debt, AI will remain trapped in pilots and proofs of concept rather than fundamentally changing how businesses operate, which means the AI balloon won't burst because the models fail, but because enterprise adoption never catches up with the expectations already baked into today's valuations.Net-net, Wall Street will soon feel the agony of this AI balloon bursting if today's smartest services firms are not deployed to prepare Main Street for this AI future our whole economy is gambling on. Folks, services-as-software needs to be valued as the balance between success and failure. Read More

Stop treating enterprise AI like a Silicon Valley startup: Aaron Levie tells you why

We haven’t removed humans from the loop, we’ve just changed where they enter the loop. If you want to understand why most enterprises are still stuck in AI pilot purgatory, you can do a lot worse than listen to Aaron Levie. The Box CEO recently delivered one of the most lucid, unsparing conversations I’ve heard on what agents actually mean for large organizations, and almost none of it matched the breathless narrative coming out of the labs and the VC echo chamber. Read More

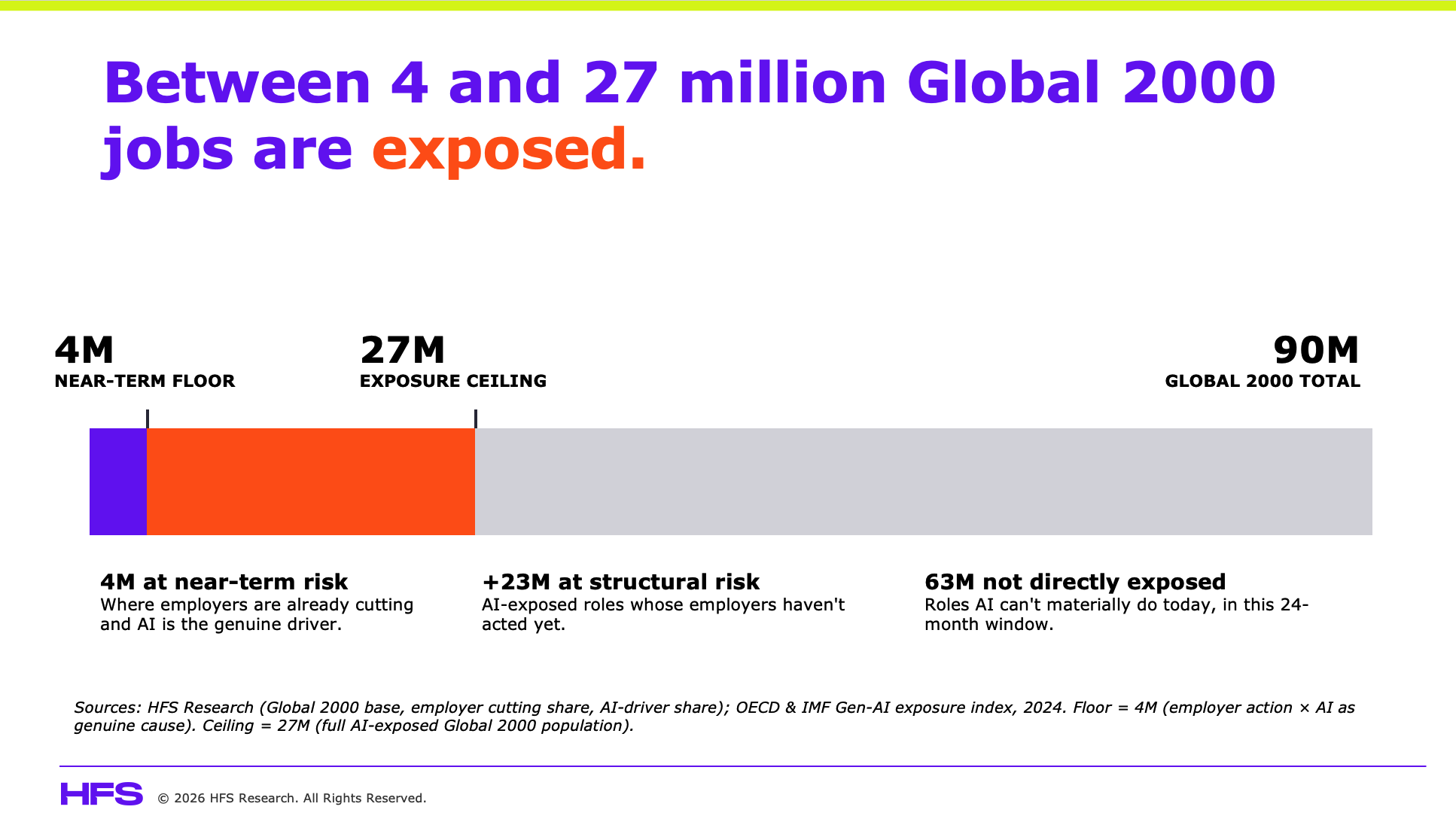

Over 27 million jobs are exposed to AI-evaporation across the Global 2000

Twenty-seven million. That is the number of corporate roles across the Global 2000 that HFS Research identifies as meaningfully exposed to AI-driven elimination, displacement, or fundamental redesign over the next three years. Not factory-floor jobs or gig roles, but 27 million white-collar, salaried, benefits-eligible positions held by people who built careers on the assumption that their employer had a plan for the future. Sadly, most employers do not, and the workers carrying the most exposure are the ones least likely to know it. Read More

Anthropic just weaponized the Palantir model. The entire services industry is now in the crosshairs.

Anthropic has announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs to launch an AI-native enterprise services company. This is not a services land grab, but a play to own the execution layer before service providers understand what they are about to lose. Read More

How Anthropic is devouring IT services

Accenture has 30,000 Claude-trained practitioners. Deloitte rolled out Claude to 470,000 employees while Cognizant deployed it to 350,000 more. Infosys signed its own major Anthropic deal last week, covering regulated industries. That is over one million practitioners already committed to Claude delivery, while most of their competitors are still reviewing governance frameworks and unsure where to place their agentic bets. Read More

Forward Deployed Vibes are now a thing. The Vibe Coding Council made it official.

A cohort of Y Combinator startups, operating in quiet coordination with the newly-formed Vibe Coding Council, has declared Forward Deployed Engineering obsolete. The replacement? Forward Deployed Vibes. Read More

Are Global Evaporation Centers next? Your GCC will likely be agentified in 18 months if your board is already questionning its value

We’ve already called out that the next 18 months will witness the dying embers of labour-intensive services. That includes your GCC. If your GCC focuses predominantly on repetitive manual tasks it’s little more than a transaction factory, and it’s the first thing the board will look to automate next. It won’t gradually downsize or pivot, but will likely experience rapid, devastating headcount reductions. Just because the labor costs are lower doesn't negate the fact that these are still costs. Read More

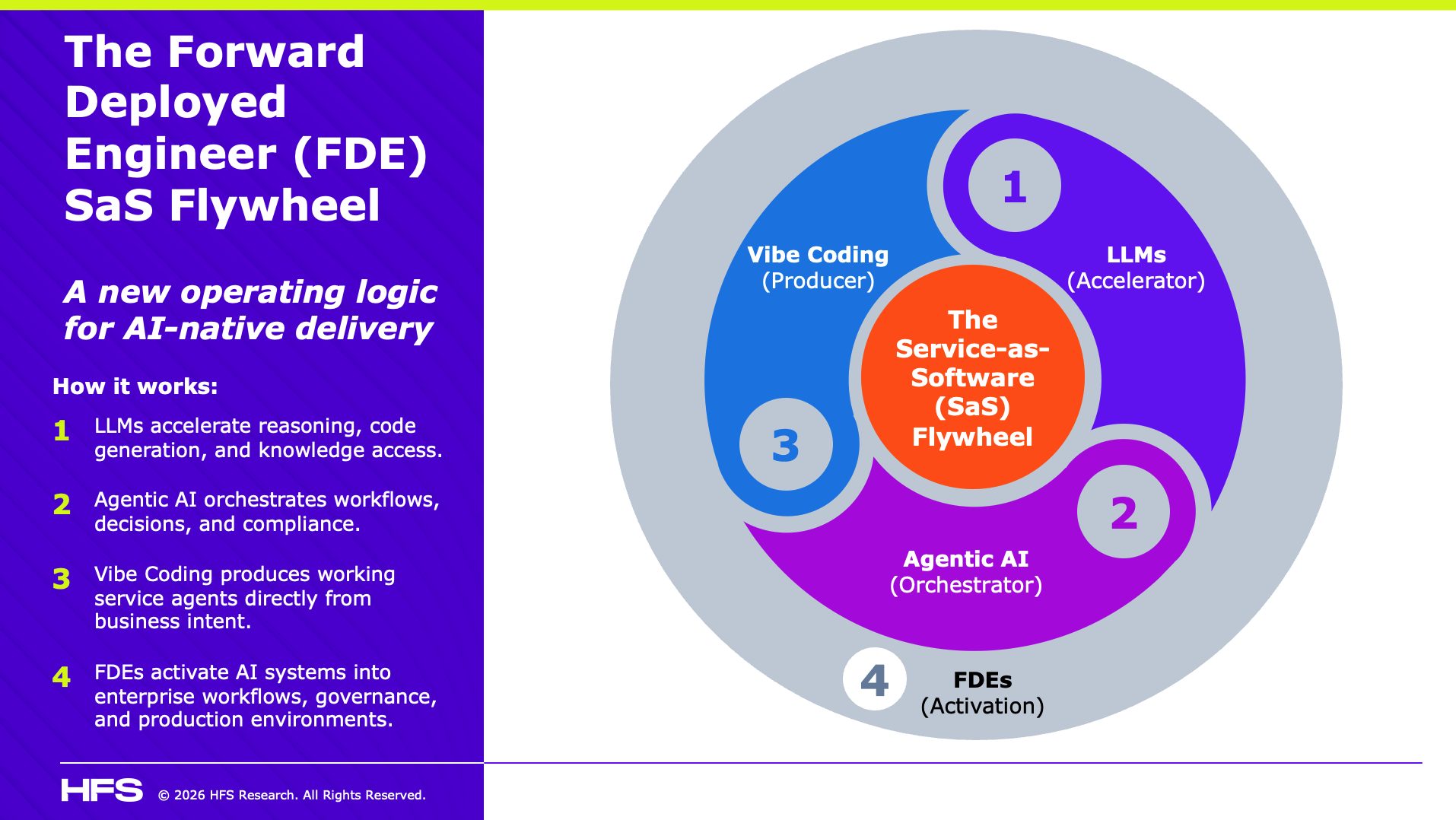

Stop treating FDE as optional: Your AI Flywheel will not spin without it

Who actually wires AI into your live systems, governs it in production, and makes it keep working when the AI software vendors leave the room? The answer is Forward Deployed Engineering (FDE). If your transformation strategy does not have it, you are building an AI theater, not an AI operating model. Read More

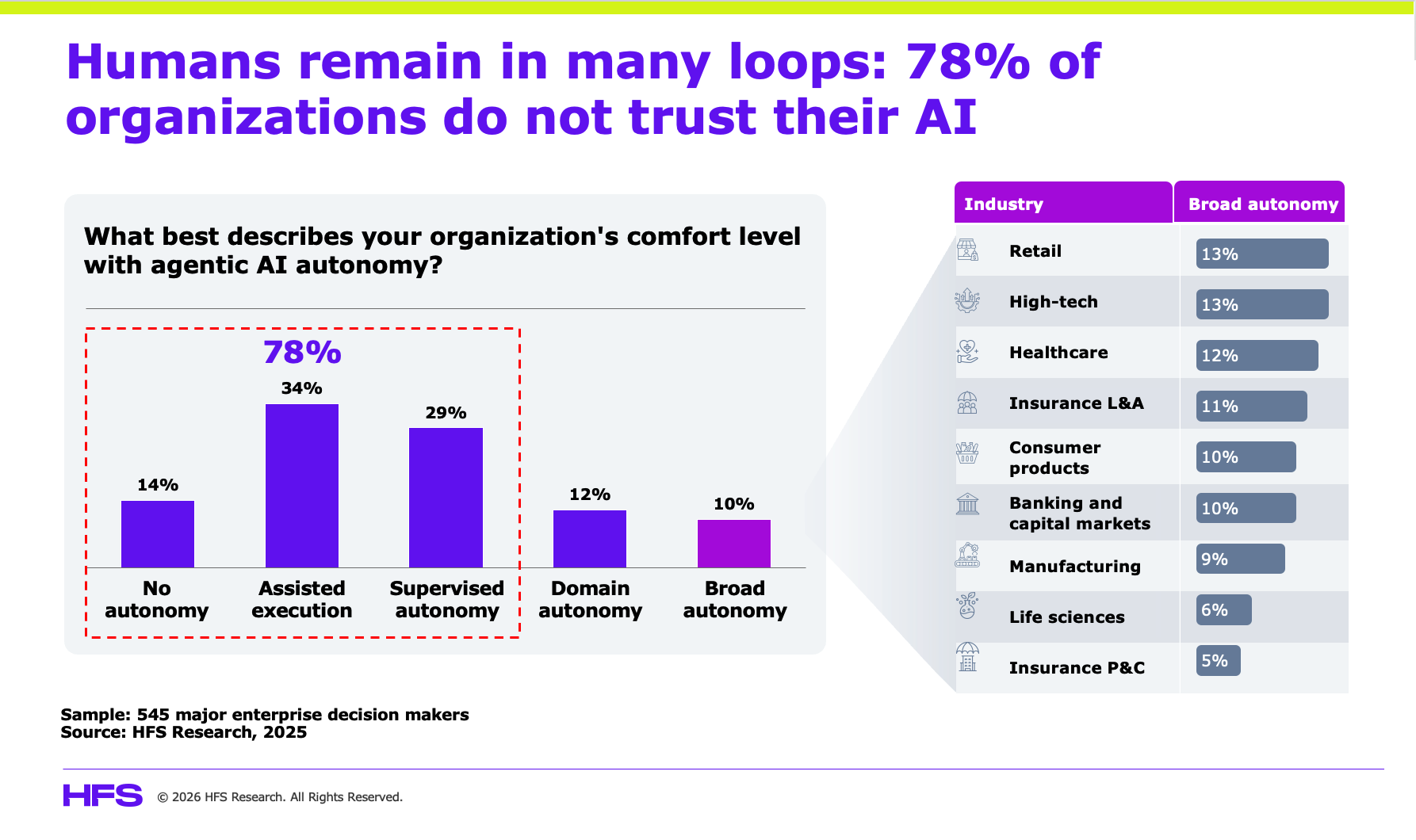

The HFS AI Trust Curve: AI isn’t failing… leadership is

The HFS AI Trust Curve rewards an organization that achieves an outcome in which AI can influence decisions. The firms breaking through the curve are not doing so because they have superior algorithms. They are doing so because leadership has resolved the human questions: Who owns the data? Who owns the insight? Who owns the outcome? Until those answers are explicit, AI remains advisory theater. Read More

Meet the Founder