As we famously declared in 2019, standalone RPA is dead, and the only way to derive real value from process automation and data is to adopt an integrated approach that breaks down silos and produces the data executives need to make rapid decisions. Our autonomous enterprise principles clearly outline the steps needed to define the data needed, the transformation to collect and access it, and the governance capabilities to arrive at the decision points along the way.

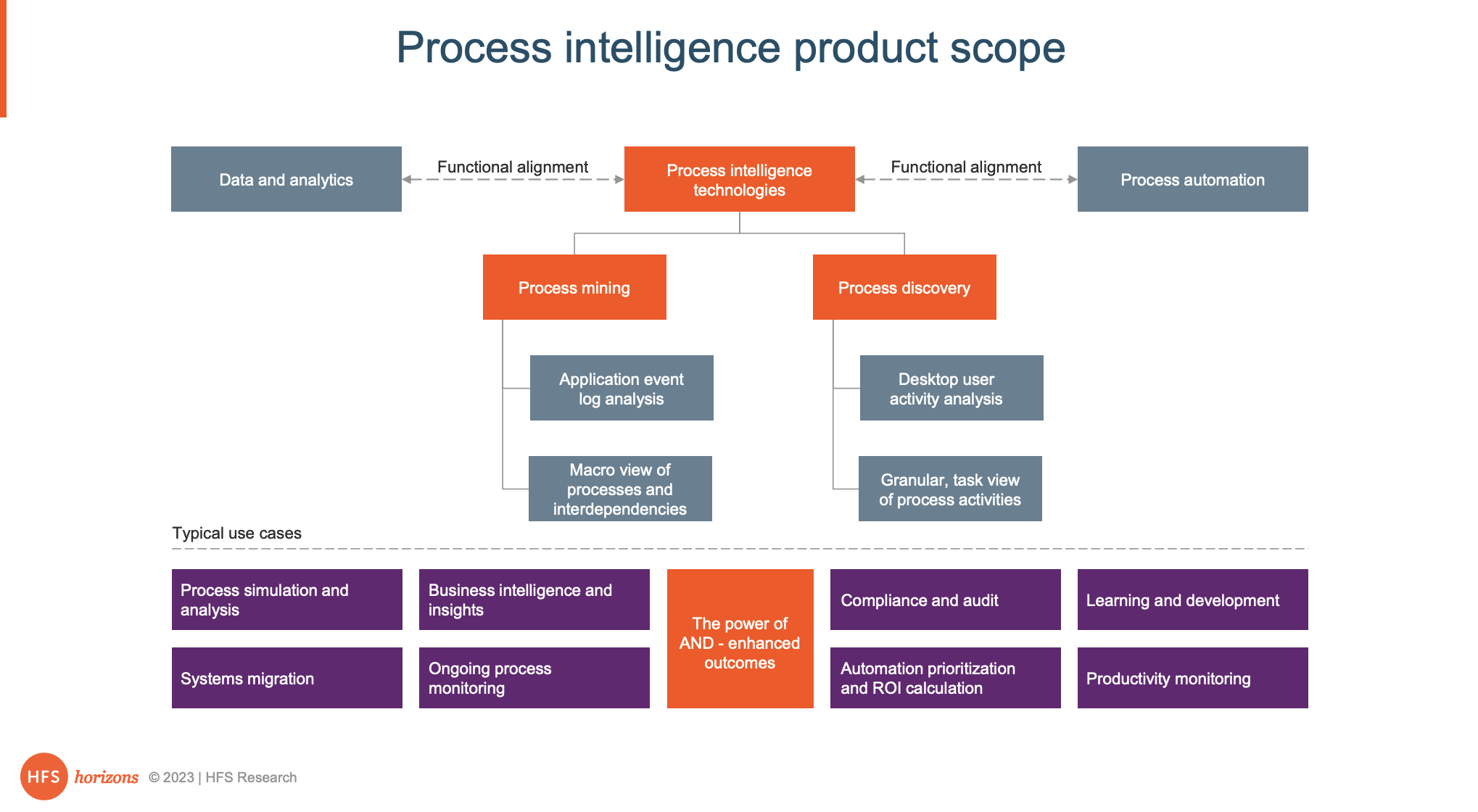

Enterprises can either use a multitude of specific software tools to support their needs or opt for a single platform approach that encompasses the functionality they need. We categorize software platforms that support this integrated approach as “Process Intelligence”:

To this end, HFS published its latest HFS Horizons report delving into the world of Process Intelligence Products. Rather than being a ranked Top 10 list, the assessment methodology provides a Horizon view comprising a full market landscape of vendors bringing different sets of technologies and focus to help enterprises understand how their work gets done.

Much like our previous assessments, we grouped process and task-mining vendors in this analysis for several reasons:

HFS focuses on the use cases and business values being derived from this set of technologies rather than the specifics of data capture and analysis techniques. In fact, our research proves that enterprise clients are applying a combination of process and task-mining tools toward similar and distinct use cases.

There’s a significant amount of convergence in this space. The market is full of acquisitions, investments, partnerships, and inhouse development to offer integrated solutions to combine both process and task data to deliver combined value – and it’s a trend we expect to see grow in the coming years.

The process intelligence market continues to grow exponentially and transform equally as fast.

Organizations are battling decades of technical and process debt, and as we immerse ourselves further into the digital economy, it will be enterprises with efficient operations that will succeed. To that end, we expect to see the impressive growth of process intelligence to continue – and the data in this HFS Horizons report confirms it, as we report that the majority of enterprises are predicting a ‘significant increase’ in spend on the technology over the next 12-18 months.

On the vendor side, we’ve witnessed the process intelligence market transform radically in recent years. A handful of vendors have been acquired by large enterprise technology platforms, automation, and workflow vendors. Meanwhile, new entrants are coming to the market armed with fresh approaches to gathering information and analyzing how people work. For enterprises, this makes it even more difficult than ever to select their preferred process intelligence partner – but they are also spoiled for choice.

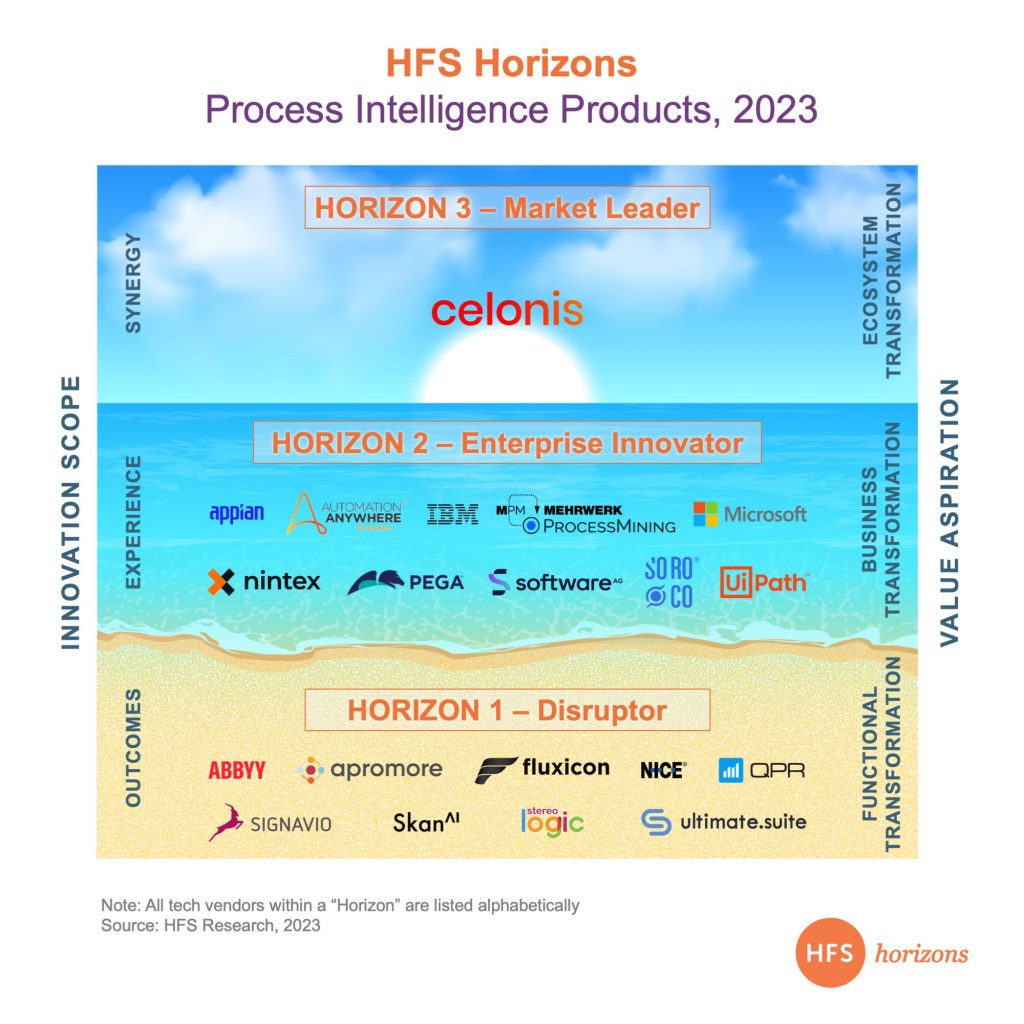

HFS evaluated 20 technology vendors

We assessed 20 technology vendors across four key dimensions: Why, What, How, and So What, allowing us to categorize vendors into three horizons: delivering cost and efficiency transformation (Horizon 1), driving enterprise business transformation at scale (Horizon 2), and creating new sources of value and creating an ecosystem impact (Horizon 3).

Note: All service providers within a “Horizon” are listed alphabetically

We identified one clear Horizon 3 market leader – Celonis

Celonis emerged as the only clear Horizon 3 market leader thanks to its ability to deliver ecosystem-based, data-driven transformation today. Horizon 2 hosts 10 fast-growing vendors whose clients are seeking enterprise-wide, data-driven initiatives – and it includes a combination of pureplay and acquired process intelligence vendors.

Horizon 2 plays host to 10 innovative vendors who are driving real business outcomes and improved stakeholder experiences. These vendors are putting an increasing amount of pressure on the likes of Celonis and are beginning to assemble a compelling end-to-end proposition, which we expect to see come to fruition in the next 1-2 years.

In Horizon 1, we identified 9 disruptive vendors helping enterprises make focused investments in the space. In particular, Horizon 1 disruptors excel when helping organizations with limited process intelligence experience and those focused on project-based functional transformation.

This report included detailed profiles of each service provider, outlining their placement, provider facts, as well as detailed strengths and opportunities.

HFS subscribers can download the report here (available free for a limited time).

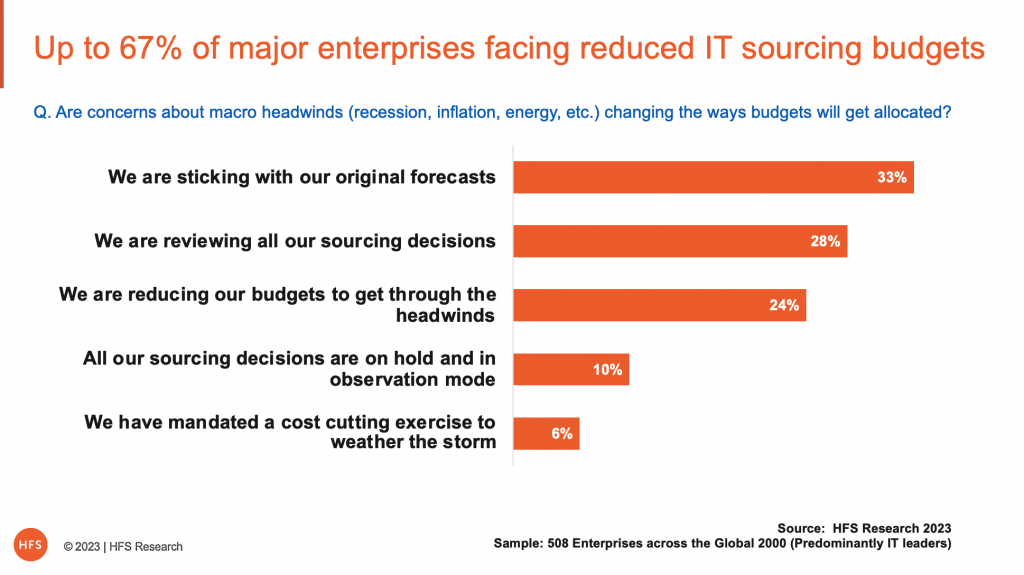

We thought the Y2K IT spending trigger was one-time bonanza… until we experienced the pandemic trigger, which saw IT investing bulge beyond our wildest dreams. Not only were we blowing cash on any collab app that seemed viable, any overpriced webcam on Amazon that would (surely) make you look amazing, but enterprise heads were also convinced they had to go on an insane rush into the cloud, even though their legacy systems and siloed 1960s processes were nowhere near ready.

Sadly, all good things come to an end as the majority of enterprises tighten their belts

Firstly, appreciate 2021 and 2022… we won’t see the likes of growth like it in IT services again. Or not until another trigger gets pulled, and we don’t know what that will look like – or when it will be. However, 2023 is going to be choppy, uncertain, and complex as we grapple with rampant global inflation and a recession everywhere except the US, which only decides to be in recession when Fox or CNN decides it’s time to be in one, based on whatever numbers can be spun to suit their agenda. Or when the government decides not to keep bailing out inept unregulated banks.

As soon as CFOs hear the “R” word, their hair-trigger response is to freeze all spending and gradually unfreeze items that are “critical” once they realize they were overreacting. Everything gets caught up in their web of austerity (except maybe some nice dinners with the auditors), and the humungous sums being lavished on all these expensive cloud migrations are under intense scrutiny as projects are either scaled back, accelerated to fruition, down-sized or even scrapped altogether.

Brand new data from over 500 IT leaders across the global 2000 tells an ugly story of how quickly the cloud bingeing is grinding to a halt, with only a third of enterprises currently staying the course with their current IT sourcing investments:

As startling as these factors are, market indices such as the S&P500 and the FTSE100 continue to trade at record highs. None of the leading service providers or bellwether ISVs like SAP, Salesforce, and ServiceNow have talked about a fundamental change in the market conditions.

Against this backdrop, the data from the survey tells us that discretionary spend is disappearing fast. This is neither the time for fancy innovation projects nor lavish client entertainment. However, spend for managing the core operations of organizations is holding up. We haven’t come across indicators that would suggest a softening in sourcing activities beyond service providers privately complaining deal cycles are lengthening and harder to close. So let’s examine these conflicting views…

We have seen a rapid shift in focus from top-line to bottom-line

One way to read into these data points is that we are seeing a reversal of buying trends triggered by the pandemic, where lengthy project lifecycles with opaque objectives have been billed to enterprises like there is no tomorrow. What has rapidly changed is tech and operations leaders expect a commitment from their service providers to deliver tangible outcomes in clearly defined timeframes. We are seeing an increase in many projects shifting to quarterly budgeting – and being placed under considerable scrutiny to reach their desired conclusions on time and on budget.

The macro headwinds that we did describe will force service providers to deliver outcomes that drive efficiency and automation. They also have to demonstrate an understanding of their clients’ data requirements and processes to ensure workloads can be migrated to the cloud effectively; otherwise, these projects will be expensive, long and painful.

At the same time, those headwinds could spell trouble for innovative startups that require PoCs to show the proof-points of their capabilities. Enterprise leaders want certainty at predictable costs and to minimize their exposure to project failure.

How should both CIOs and cloud providers address this dramatic change in enterprise focus and spending in 2023 and beyond? Can they find new fizz by approaching the cloud differently?

SaaS providers must show more flexibility in their contractual agreements and go beyond standardized seat-based pricing to support broader transformation initiatives.

Service providers must align technology with business objectives to (finally) capture business value for their clients

CIOs must change their mindset from cost to business value. Thus, FinOps must be expanded to governance and, ultimately, business assurance.

CIOs and Ops leaders much work together to map out their underlying data infrastructure to ensure it is cloud-ready

The cloud discussion has to shift to business value.

In just a few days, Silicon Valley Bank (SVB) fell from grace so swiftly that it still holds onto ‘buy’ ratings from most analyst firms. A month ago, stock pundit Jim Cramer urged investors to buy the stock—a clear warning sign to anyone familiar with inverse-Cramer investments. Tomorrow, an estimated 1000 tech start-ups will be unable to make payroll, and a further 2000 will be clinging on to liquidity for dear life. The future of America’s innovation – and the world’s innovation – is hanging by a thread.

So what actually happened with SVB?

Simply put, SVB piled loads of customers’ cash into long-term illiquid assets that, at the time, were safe but tanked as interest rates increased. That meant they couldn’t lay their hands on enough cash quickly enough to meet withdrawal demands. Word got out; more withdrawal requests came in. Eventually, the whole thing collapsed—a classic run on a bank.

Most of us have seen a run on a bank before. But for those new to the rapid demise of a financial institution, here’s a deeper analogy. Let’s say you’re kicking off a tech startup. SVB’s wooed you with their compelling investment offer for £1m in funding and all the goodies that come with it. Part of that deal involves putting your cash in SVB. They are your bank of choice. SVB, for its part, bought a lot of bonds, dishing out 1.5%. It’s not a bad deal on the face of it, given historically low-interest rates. But then, interest rates started rising. 3, 4, 5%. So those bonds paying out 1.5% suddenly look less attractive than newer bonds getting 4.5%.

Understandably, people aren’t keen on buying them anymore or want a much lower price. These factors combined (SVB pulling below-market yields on its bond portfolio, and the corresponding reduction in the value of bonds) pushed SVB to cash out on billions of bonds at a loss. Then, apparently to reassure the market, they chose to raise new funds from VC firm General Atlantic, alongside a public-facing bond. Rather than reassuring the market, panic set in. Their customers started pulling cash out.

So now, depending on where you are in the queue, getting your cash out of the bank becomes pretty hard. If you’re close to the back of the queue, it becomes impossible.

Some of it’s insured, and some SVB promises to pay back. But, for now, billions of dollars sit in an uncomfortable limbo. Leaving the CFOs of SVB clients to work all weekend as they develop a fiscal survival plan.

Multiply that $1m example a few thousand times, and you have the true scale of the challenge. And that’s assuming it’s just SVB. Global stocks took a kicking at the end of last week, with bank stocks leading the charge. The market is betting that the contagion will spread beyond SVB’s four walls. Most likely due to wary depositors racing to redeem their cash.

Another dent in the tech industry: The ecosystem effect will ripple far beyond tech startups

Now that may be a bit of a simplistic explanation—and economists and equity analysts will no doubt offer countless superior answers—but it gives a flavor of the crisis at hand. Now let’s zoom in on the impact of the SVB crisis on our industry.

Let’s start with the obvious: SVB clients. Firms with cash tied up in SVB face a tough few weeks or months as regulators figure out how to compensate clients and distribute SVBs remaining assets. Already, there are countless stories of tech firms of varying sizes warning that they’ll struggle to make payroll next week.

Few big names have announced any issues, but given its prevalence in the sector, it’s almost certain we’ll see some major enterprise software and services firms touched by the crisis. And, dependent on the direct exposure, we’ll see a ripple effect across the industry.

That’s because SVB’s clients in the enterprise space don’t sit in isolation. Take cloud observability company, Datadog, which is a known client (at least regarding SVB’s published case studies). Amongst their partner ecosystem, Datadog boasts IT Services giants Accenture, Fujitsu, and IBM. If Datadog encounters business continuity challenges—and there’s nothing to suggest they are—, then the ripple effect can swiftly spread across marquee outsourcers and into client engagements.

Of course, larger cornerstone companies (think the big SaaS giants now deeply embedded in most major businesses) will cause significantly larger problems for the industry, particularly as many are already grappling with rightsizing initiatives to drive down unsustainable costs. We could see some significant operational challenges if even a portion of their cash is locked away.

A bigger dent to innovation: A new funding winter

The immediate impact aside, we can expect a more damaging aftershock – a hit to innovation. SVB, as a financial institution, is a crucial source of funding for many high-potential tech firms—many in the consumer space but also a large cohort targeting real-world business challenges. Many will likely struggle to fight through the next few months without access to capital.

These firms may be small and nameless today but could be tomorrow’s enterprise tech giants. We may never know.

The impact is global. For example, TechCrunch reckons 60 YC-backed Indian Startups are struggling to redeem cash stuck in the failed bank. Encapsulating the issue, a founder told the India Express, “It is 4 am now and we have been on hold at the toll-free number given by the FDIC for over half an hour. We have around $2 million in our SVB account and need that to create payroll.” Meanwhile, in the UK, the Chancellor is working on a rapid intervention to provide cash to companies impacted by the crisis and give them some fiscal breathing space.

Smaller companies, or those earlier in their journey, will be the hardest hit. For instance, they’ll find it harder to lean on clients for early payments to help cashflow. And are far less likely to have followed risk best practices by spreading funds across multiple banks. They are also, on average, the source of the greatest industry innovation (today’s SaaS giants, for example, all started somewhere, very few are homegrown in already giant companies).

Bottom Line: The collapse of SVB isn’t just a banking crisis; it’s an innovation crisis

While many look to the collapse of SVB as an inevitable outcome of Silicon Valley excess, perhaps there’s some truth to the characterization. But below the surface, what we have here is the start of a potentially painful period for a tech sector already struggling to make sense of a world alien to their upbringing oriented around cheap cash. But worse, this could be the final nail in the coffin of innovation-focused funding for some time.

While the last decade of easy money deserves a degree of criticism, the inability of traditional investments to offer any meaningful return saw capital flow into startups and innovators. Now, why risk it? When the risks seem much higher, and the comparative returns much lower? And while there are already efforts underway to save SVB, it’s possible the damage to the tech sector is already done.

Retail banking remains the most visible segment of the global banking market with the greatest alignment (and exposure!) to consumer behavior and sentiment. This perpetual tension between what consumers want and what banks provide has driven nearly a decade of sexy front-end somewhat superficial digital investment to help banks defend against fickle customer loyalty. In our post-pandemic world, the top imperative for retail banks has shifted from digital engagement to front-to-back modernization. To succeed, digital innovation must permeate throughout banking operations and modernized core systems to enable new forms of value for end customers. Retail banks will get there with the help of their ecosystem partners.

The Best Service Providers for Retail Banks, 2023—Disruptors, Enterprise Innovators, and Market Leaders

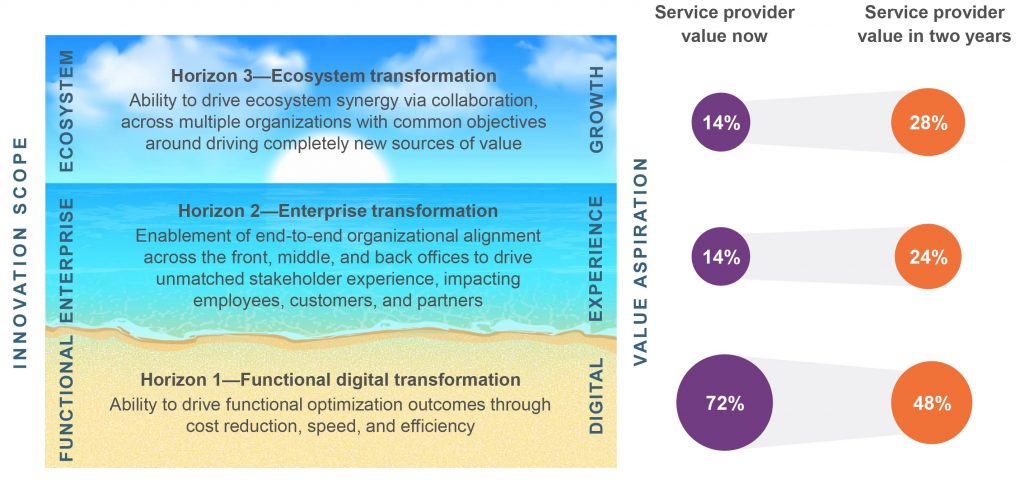

Horizon 1 is digital: Ability to drive functional optimization outcomes through cost reduction, speed, and efficiency

Horizon 2 is experience: Horizon 1 + enablement of the OneOffice™ model of end-to-end organizational alignment across the front, middle, and back offices to drive unmatched stakeholder experience

Horizon 3 is growth: Horizon 2 + ability to drive OneEcosystem™ synergy via collaboration across multiple organizations with common objectives around driving completely new sources of value

The purpose of the HFS Horizons model is to align enterprise objectives with service provider value. We assessed 21 service providers across their value propositions (the why), execution and innovation capabilities (the what), go-to-market strategy (the how), and market impact criteria (the so what) to best understand and plot the value they offer to their retail banking clients. Here are the results:

Note: All service providers within a “Horizon” are listed alphabetically

The Horizon 3 leaders are, in alphabetical order, Accenture, Deloitte, EY, Infosys, TCS, and Wipro. These service providers have demonstrated their ability to support retail banks across the journey from functional digital transformation to enterprise-wide modernization to creating new value through ecosystems.

These leaders’ shared characteristics include deep industry expertise across the retail banking value chain, a full-service approach across consulting, IT, and operations, a strong focus on innovation, internally and externally with partners, co-innovation with clients and partners, and proven impact and outcomes with its retail banking clients around the world.

Retail banks should select their partners based on the value they seek.

The HFS Horizons model aligns closely with enterprise maturity. We asked the retail banking leaders we interviewed as references for this study to comment on the primary value delivered by their service provider partners today and in two years. Overwhelming, respondents indicated that the value realized today is Horizon 1—functional digital transformation focused on digital and optimization outcomes (72%). Two years from now, the story changes with an enhanced focus on using service providers to help achieve enterprise transformation (24%) and a heavy focus on driving growth and new value creation through ecosystem transformation (28%). Retail banks should select their partners based on the value they seek. The most effective service providers of the future need to enable the growth and transformation of retail banks across the ecosystem continuum.

Which of the following statements best represents the primary value delivered by your service provider today? And in the next two years?

N=41 retail bank respondents Source: HFS Research, 2023

The Best Service Providers for Retail Banks, 2023—Disruptors, Enterprise Innovators, and Market Leaders report highlights the value-based positioning for each participant across the three distinct horizons. It also includes detailed profiles of each service provider, outlining their provider facts, strengths, and development opportunities.

HFS subscribers can download the report here (available free for a limited time).

The latest Sourcing and Procurement Horizons report is a snapshot of leading procurement service providers’ sourcing and procurement services capabilities. The aim of ambitious CPOs is to realize the value of procurement beyond costs and savings if they want to avoid back-office irrelevance in today’s unforgiving era. And partnering with deep procurement experts to create and manage their critical sourcing data, develop their sourcing ecosystems, and constantly fuel them with new ideas and methods can really drive impact for them.

Disruptors, Enterprise Innovators, and Market Leaders

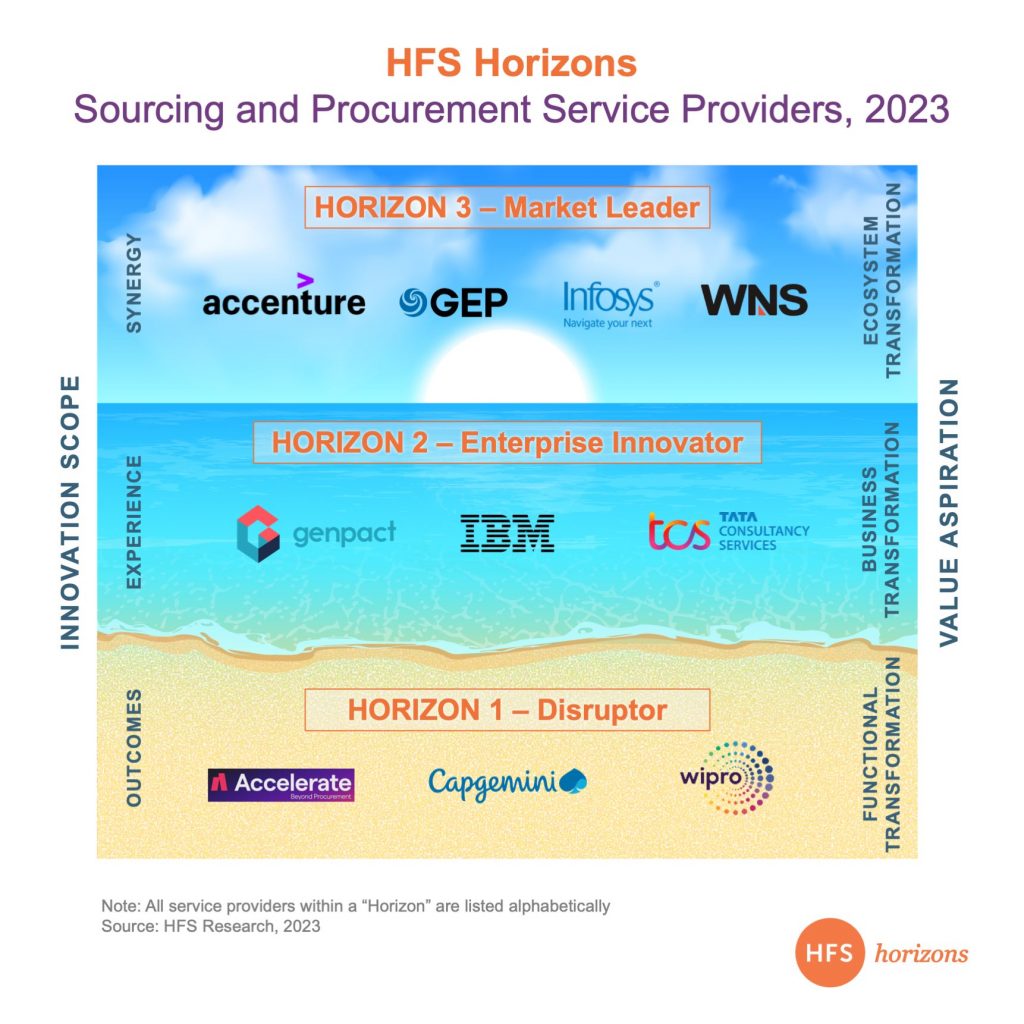

We assessed 10 service providers on their capabilities across a defined series of value propositions, execution and innovation, go-to-market strategy, the voice of the customer, and alignment with the HFS OneOffice criteria. The new Horizon landscape (below) demonstrates the providers’ positions within the three horizons. Horizon 1 (“Disruptors”) refers to those providers who have been able to drive functional procurement transformation, Horizon 2 (“Enterprise Innovators”) includes those who have reached the level of business transformation, and Horizon 3 (“Market Leaders”) includes all those providers who have closed the gap and moved towards ecosystem transformation.

The HFS Horizons report is aimed at evaluating the capabilities of service providersto deliver to the needs of enterprise buyers

With global competition intensifying and new technologies emerging, we are seeing a shift towards more automated and data-driven procurement processes and investments in category management to keep pace with changing markets. At the same time, enterprises must also navigate a complex regulatory landscape and manage a wide range of risks, including supply chain disruptions and changing customer demands. Service providers hoping to play a role in their procurement clients’ businesses thus require a deep understanding of their industries and a commitment to ongoing innovation.

Also, with the recent global assault impacting businesses greatly, in many organizations the procurement function has led organizations out of the crises. The face of procurement is no more a cost-saving function, but a strategic business enabler sitting at the intersection of the organization and its external connections. The service providers supporting this function are helping procurement reshape their role by reimaging their talent, technology, and process capabilities to build this function as a value enabler for the business.

Reshaping procurement role to realize its value beyond costs and savings

Driving down costs and reducing spending continue to be top priorities for procurement. Procurement’s role is changing given its responsibilities in managing third parties. It now includes new accountabilities like risk, diversity, sustainability, and social performance of third parties. Procurement assembles the resources to create the services and products the enterprise brings to market, and it arguably has the closest lens on differentiated value propositions that external stakeholders and partners can offer. Enterprises need and expect to fully capture the benefits a portfolio of external partners may have. To help procurement realize its evolving role, service providers are reimagining their skills and capabilities, designing, and delivering solutions around technology, and consulting to truly build this function to become a value enabler for the business.

Helping CPOs build ESG into the organization’s sourcing DNA

Effectively implementing the envisaged sustainability goals is an overarching organizational challenge, and it often means change for the product portfolio and the organization, including its culture. Service providers recognize the scope involved and are helping organizations with not just a sporadic launch of individual initiatives but rather a transformation of companies’ operations spanning the entire supply chain network. To ensure success and support the organization’s ESG (environmental, social, and governance) priorities, service providers are building core ESG teams, recruiting ESG leaders, and developing technologies and tools to monitor ESG markers.

The HFS Horizons: Sourcing and Procurement service providers, 2022report examines the capabilities of 10 FP&A service providers.

These service providers (in alphabetical order: Accelerate, Accenture, Capgemini, Genpact, GEP, IBM, Infosys, TCS, Wipro, and WNS) are offering differentiated approaches to meeting the transformation needs of clients. This research effort will assess how well service providers are helping their clients to envision and deliver sourcing and procurement transformation outcomes.

We assessed and rated the transformation capabilities of these service providers across a defined series of value propositions, innovation capabilities, go-to-market strategies, and market impact. This report also includes detailed profiles of each service provider, outlining their placement, provider facts, as well as detailed strengths and opportunities.

HFS subscribers can download the report here (available free for a limited time).

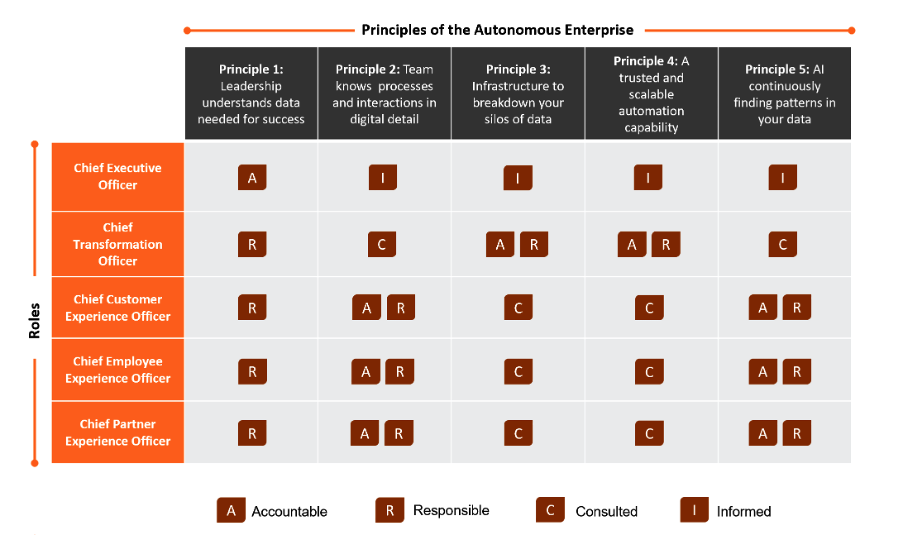

In our recent post discussing “The Six Principles of the Autonomous Enterprise,” we touched on all the key behaviors and technologies that must come together as smart leadership continuously seeks to refine the data it needs, in real-time, to be successful. We need to delve much deeper into the roles, traits, and responsibilities enterprise leaders must develop if autonomous enterprises are going to be effective in their emerging ecosystems:

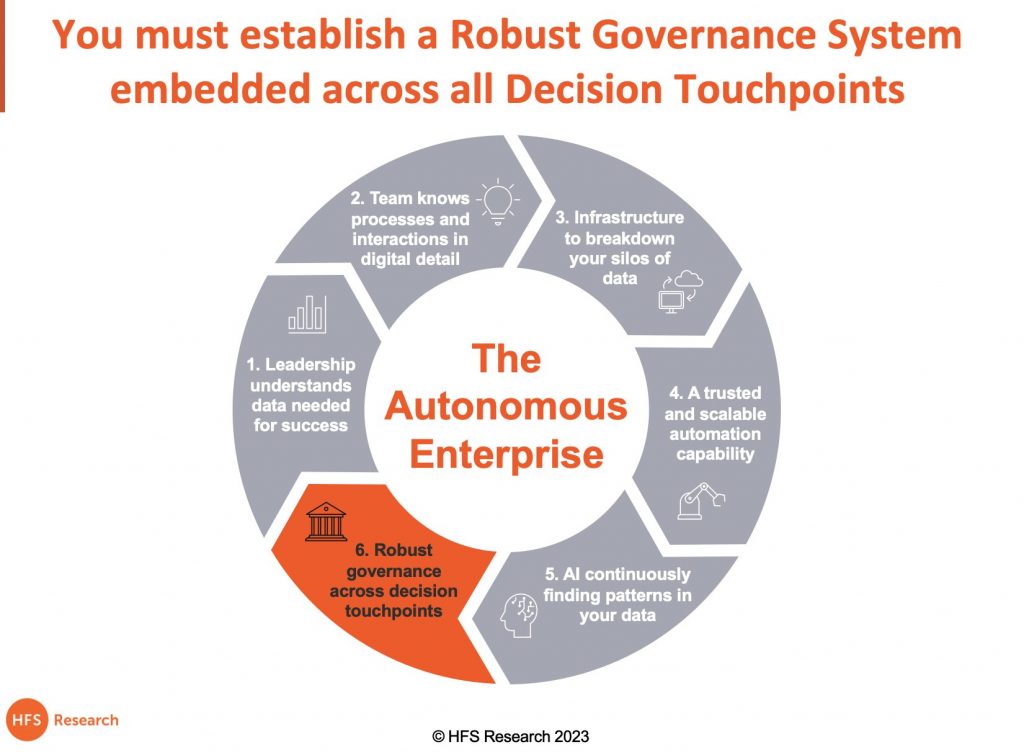

A robust governance system embedded across all decision touchpoints guides the effectiveness of your autonomous enterprise

A strong governance capability has the talent, tech infrastructure, automation, and AI to deliver the data that will drive success with minimal manual interventions that impede progress and speed. The ultimate goal of an autonomous enterprise allows us humans to remove ourselves from some parts of the system so that we can make continuous improvements to the ecosystem as a whole.

Ultimately this is about machines making decisions where we previously had humans and removing humans from loops that don’t need humans anymore. Leadership must understand the data they need to be successful and assemble and govern the right system to deliver success. Hence great governance is about maximizing the ability of talent to understand and access data, make rapid decisions based on that data and have a seamless infrastructure that houses that centralized data, and embed an effective risk management framework. Bringing together those processes and interactions with trusted and scalable automation frees humans from slowing down decisions and operating effectively in fast-changing ecosystems.

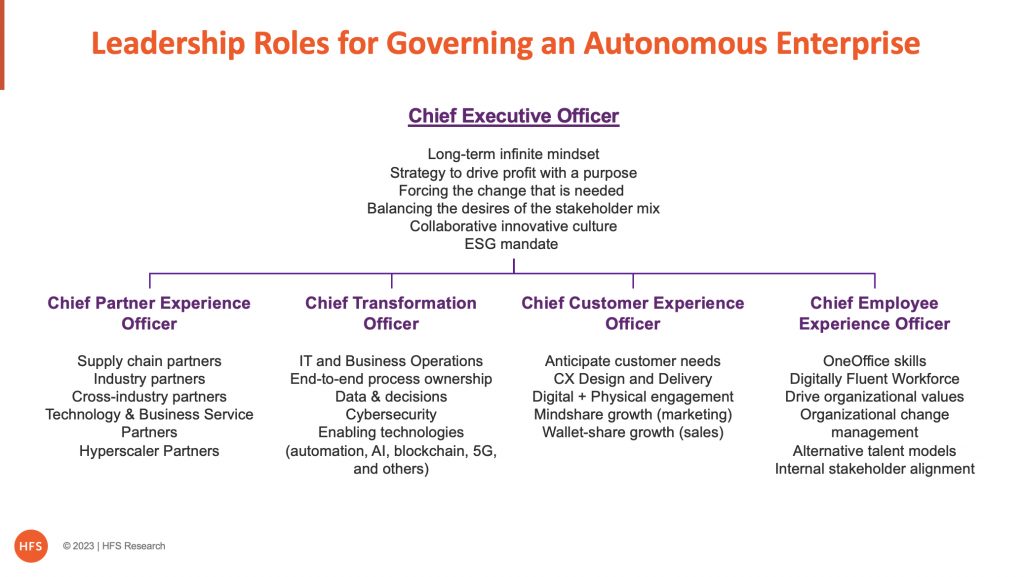

What are the leadership roles needed to understand the data they need? How can we build the right internal teams and external partnerships to support an autonomous enterprise? And how can we design smart governance to manage key decisions faster with some degree of confidence? It really boils down to breaking down internal silos and designing leadership roles to drive better decisions and support talent.

These are the roles – and leadership traits – that will optimize the value from autonomous enterprise models

The Chief Executive Officer: The CEO should be the leader who drives the infinite mindset across the organization. He/she must continuously define the purpose of the organization and relentlessly drive a fearless collaborative culture that values stakeholder value beyond shareholder value. As a leader, it’s so easy to obsess with operational functions of the business during times of disruption or distress – in this case, a global pandemic – that it can create knee-jerk, often short-term decisions that could inherently damage your long-term vision, your business’ culture and your raison d’être. With no defined time horizon, no clearly-defined rules, and with players that may enter and exit at any time, the primary objective of an infinite game is quite simply to keep playing. The goal for businesses is to have the will and resources to stay in the game through thick and thin. And none more so that the current unpredictable and challenging business environment.

Having lived and worked through four recessions, I personally understand the rapid change in leadership mindset that can occur when a firm goes from peacetime and growth to one of survival and all-out war. According to author Simon Sinek, people look to leadership to serve and protect, to “set up their organizations to succeed beyond their lifetimes.” But in the modern landscape, most organizations place an unbalanced focus on near-term results that may ultimately prove to be self-defeating, like casting aside your umbrella in a storm because you haven’t been getting wet. In short, business is no finite endeavor. This pandemic lays plain for all to see the game we are really playing.

The CEO is the ultimate collaborator, forcing the change that is needed and balancing the desires of the various stakeholders (the board, key clients, key partners, the employees). His/her/their team to make this happen, must be responsible for the full gamut of their customers, employees, and partners, working with a transformational wizard to bring together the process and technology with the real innovation ingredient: the people. Taking people out of routine work that should be automated or digitized and refocusing them on responsibilities that require real innovation and cultural affinity is so valuable.

Chief Transformation Officer:Any transformation leader worth their salt must be able to drill an autonomous mindset into their teams and work out a plan to implement the right technologies to form the baseline to break down silos and centralize critical data.

This leader must link front to back office and ensure processes run smoothly across functions to deliver the data/outcomes the organization needs. This should ideally be someone who understands the challenges of enterprise operations and how to align them with the market-facing/client-impact areas of the firm. Forget the old GBS head / shared services head role, as this just has repeatedly failed to get out of the transactional back-office world and the “finance factory”. This person must oversee both technology and operations, understand the value of automation and AI, be able to design and implement change programs and work closely with the employee experience leader to eliminate the back office mindset from antiquated business functions into one that is aligned with the direction of the business.

Chief Customer Experience Officer: This is the leader who lives and breathes the world of the customers and obsesses with how to engage them as effectively as possible – right across the entire customer life-cycle – both with talented humans and autonomously where humans are not necessary. Ideally is someone who understands how to design customer interfaces, how to service customer needs leveraging both digital tools and physical support, and ensuring the entire employee base is unified around (and incentivized on) driving customer impact. In addition, the CCXO must ensure the marketing mindset is to communicate with the customer, educate the customer, and develop specific programs that have a real impact on driving customer engagement and business growth.

Chief Employee Experience Officer: Forget transactional HR, the employee experience leader is the person responsible for making the company a great, energizing place to work, where staff of all backgrounds, ages, experience levels cultures are energized by the values and desired outcomes of the firm. The CEXO must drive trust across managers and staff to embrace autonomous technologies and craft roles that maximize human interactions. Noone wants to be stuck in zombie roles in this environment where ambitious leaders demand value from their talent, delighting customers, colleagues and key partners. Never has there been a time when people skills are more important, supported by trusted and robust technologies and data infrastructures.

This individual must be the person who can manage the expectations of the board, the CEO, and the shareholders to create a company culture and values that everyone believes in. Moreover, the CEXO must be intimately involved in the creation and execution of training programs across the firm to attract talent who want to work for a company that will develop them, as well as establishing a culture and values they can identify with. This should ideally be a strong leader with broad experience in the business and staff development, who knows what it takes to be successful, and who understands how to motivate people beyond pure compensation. The best leaders today are also great people managers – and the CEXO role must be at the core of the business leadership, not some ancillary executive painting lip service and not having any real impact.

Chief Partner Experience Officer: As the OneEcosystem environment evolves, the need to collaborate with entities with common objectives across the entire customer value chain has never been so prominent. Partners are no longer just your suppliers. Suppliers are essential partners in delivering your goods/services. Still, the OneEcosystem looks at partners more holistically – partners in the ecosystem involved in providing the customer experience across the entire customer lifecycle.

An autonomous enterprise needs to function autonomously both internally and externally. Essentially, the OneOffice and OneEcosystem are effective when processes and interactions require fewer manual interventions and data can be accessed in centralized repositories. It requires leadership to have the ability to continuously refine the data it needs in real-time to be successful right across both internal and external ecosystems and the CPXO is the leader to drive this mindset into practice.

In the age of transparency, these roles must be codified to ensure accountability

It is not enough to provide a high-level description of the key roles that will govern an autonomous ecosystem – enterprises must codify the responsibilities of each one of them to ensure transparency when measuring their effectiveness.

As highlighted below, adherence to each principle of the Autonomous Enterprise comes with different responsibility levels across the leadership roles.

We believe the CEO should ultimately be accountable for understanding data needed for success. Thinking about data as an “ecosystem builder” requires a mindset and cultural change – if the CEO does not show the way, nobody will. The CEO’s mandate is to lead the way and be directly accountable for the overall performance of transitioning into a data-driven enterprise.

The Bottom-line: The old way of running businesses is fast eroding as we rethink what constitutes success and ambition. Bring on autonomous principles to drive the next wave of innovation

We launched the “HFS Enterprise Innovation Framework” in 2022 that enables organizations to survive (Horizon 1: Digital), thrive (Horizon 2: OneOffice), and ultimately lead (Horizon 3: OneEcosystem). One of the six distinct organization characteristics for enterprises to successfully create the OneEcosystem will be “autonomous processes” which allow firms to operate with less inefficiency in order to make faster decisions.

Did you ever think your enterprise could move to a 100% work-from-home environment with less than three weeks’ notice? This era of constant change has forced businesses to flex – vastly accelerating the OneEcosystem environment, dramatically cutting redundancies and improving processes at scale. Essentially OneOffice and OneEcosystem are effective when processes and interactions require fewer manual interventions and data can be accessed in centralized repositories. Hence leaders need to understand the data they need, have the right teams/partnerships to support them, and have smart governance in place to manage their decision points. The Autonomous Enterprise principles, if followed by smart, ambitious leaders, will enable the OneEcosystem mindset to prosper and provide the discipline and clean data needed to be effective.

There is a massive amount of change happening, and out of change comes real transformation. After years and years of complacency due to the relentless growth (and papering over the cracks of 2008), all of today’s organizations now finally have a burning platform to change how they operate globally. In fact, the autonomous platform is positively on fire!

When we look at the now-famous Cognizant CEO factory, probably the best-known of the bunch is Debashis Chatterjee (known simply as “DC” to everyone in the biz), who now finds himself leading the new $4.2bn powerhouse that is LTIMindtree. He’s also one of the calmest and easy-going guys you can hope to meet in this business.

DC originally took the helm at Mindtree in August 2019, and soon found himself contending with a “non-merger” as LTI decided to keep Mindtree separate, and then a pandemic followed. But that all changed in November last year when DC was announced as the first CEO of the newly (and finally) merged LTIMindree entity. So let’s hear directly from DC… what makes him tick and what’s next for the new 7th largest Indian-heritage service provider…

Phil Fersht – CEO & Chief Analyst, HFS: It’s great to see you again, DC. I mean, you’ve been around the IT services space since before the internet. Right?

Phil: I can also remember the world before the internet, as well, so you’re not that old 😁. But let’s hear a bit about you, DC. What gets you up in the morning these days? And, as you look back over your career, was running a multibillion-dollar IT services shop what you always wanted to do when you started?

DC: So, Phil, my background is I am a mechanical engineer, by education. I used to be a very avid sportsperson in my school and college days and played a lot of sports, including cricket, which is my favourite sport. And if I was not pushed hard, I would not have become an engineer; I would have rather liked to continue in sports.

And having done my mechanical engineering, I joined an automobile manufacturing firm, spent two years over there, then – and I’m talking about 1989 – that is when I got an opportunity to work in TCS, which was a great opportunity at that point in time. I think IT happened to me by accident because it was just that everybody said, “IT is the future,” so I jumped onto it, and since then, I haven’t looked back.

We went through various S-curves within the industry, whether it is the initial mainframe era, or the client-server, or the internet, and then, subsequently, cloud and Digital, and went through various inflection points as well, like Y2K and the global financial crisis in 2008, in which I was right in the middle of, because I was running the Financial Services vertical at that time. So I think it has been a pretty exciting journey.

And if you ask me what it is that I think, getting up in the morning now, is these two organisations coming together, erstwhile LTI and erstwhile Mindtree, creating LTIMindtree. I think this is the first time, and a very unique scenario, where two listed entities are coming together which are almost of similar sizes, and bringing these two organisations together, the entire integration, and ensuring that we can create value over a period of time – one plus one equals more than 2, you know. I am always thinking about how to make that happen as we go along. I mean, we already have some plans, but how do you ensure that the plans can translate into execution? That’s something which I’m always thinking.

And, to your point, running a multibillion-dollar IT services company – who would not like to do that?! Not that it was the desire when I was studying my mechanical engineering, but definitely, as I went along, I felt if you are in the industry, you need to learn how to run scale, and how do you manoeuvre at scale. And scale is not something that I have not done before, and it’s really not just the scale, it’s the question of how do you leverage the scale, and get the best out of that scale? And that’s what I have been trying to do for several years.

Phil: It must be tremendously satisfying, DC, having spent such a significant career working in some of the biggest IT services companies in the world, actually to run your own shop, and drive some areas that are special to you. I mean, I was an analyst for 15-20 years, and I always had a personal view on how an analyst firm should be led, and getting the opportunity to build my own company, and add my own stamp, was tremendous. So who influenced you along the way as you built your career, when you started to build this vision?

DC: Well, I think there are many people who influenced me; people whom I have met,Read More

Managed services markets in functions such as finance, procurement, and HR have matured over the years, and it’s increasingly hard to differentiate across service providers… most deliver via an effort-based FTE model; they all compete for the same pool of talent, and they all have similar issues controlling attrition in this environment. However, enterprise leaders are increasingly desperate for rapid access to centralized data to make critical decisions in a hugely unpredictable and complex business environment.

Helping firms access centralized data at speed is critical to growing value-based partnerships, and none more so in financial planning

Hence those providers engaging in financial planning and analysis (FP&A) managed services, where they are supporting these critical data and planning decisions for their clients, are getting much deeper into the high-value controllership areas for them. This is where the whole relationship shifts from one of providing effort to one of performance and purpose.

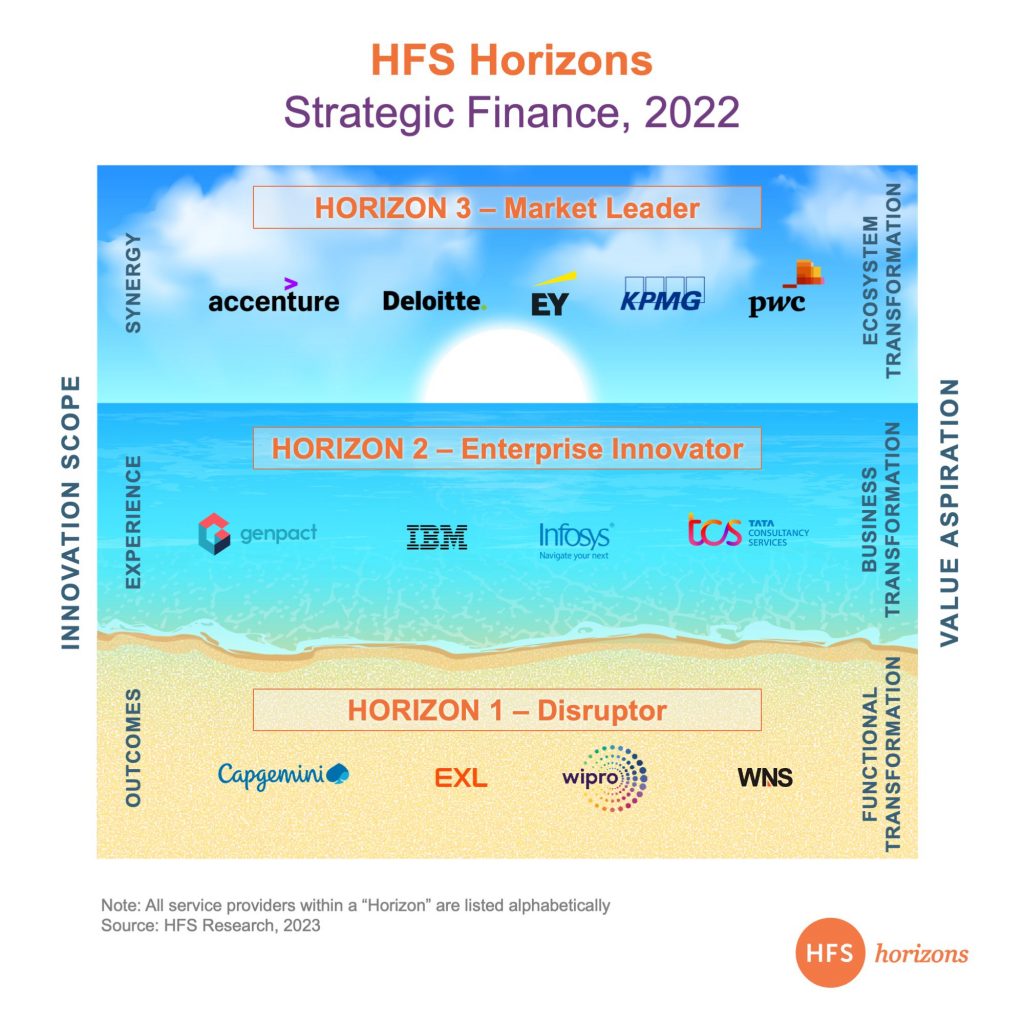

The HFS Strategic Finance Horizons report analyzes services provider capabilities shaping the financial planning and analysis industry and their proven capabilities to help their enterprise customers access critical financial data at speed. HFS assessed 13 major service providers’ prowess in the strategic areas of FP&A, based on the “Big 4” who are leading in some of the more specialized pieces of strategic finance and delivering managed services programs, and the F&A service providers with proven ability and scale to deliver FP&A work.

The new Horizon landscape (below) demonstrates the providers’ positions within the three horizons. Horizon 1 refers to those providers who have been able to drive functional FP&A transformation, Horizon 2 includes those who have reached the level of business transformation, and, Horizon 3 includes all those providers who have closed the gap and moved towards ecosystem transformation.

Agility and an evolving mindsetare key in this ever-changingfinance landscape

The last few years have shown us just how much enterprises need to focus on staying agile through uncertainty, change, and disruption. Financial planning and analysis strategy, technology, talent, and processes must evolve to keep up with finance leaders’ aspirations for helping the business navigate uncertainty and create long-term business value. In their quest for agility, we see finance and risk leaders engaging with third-party service partners not just on traditional FP&A activities but starting to move into strategic finance and performance management.Read More

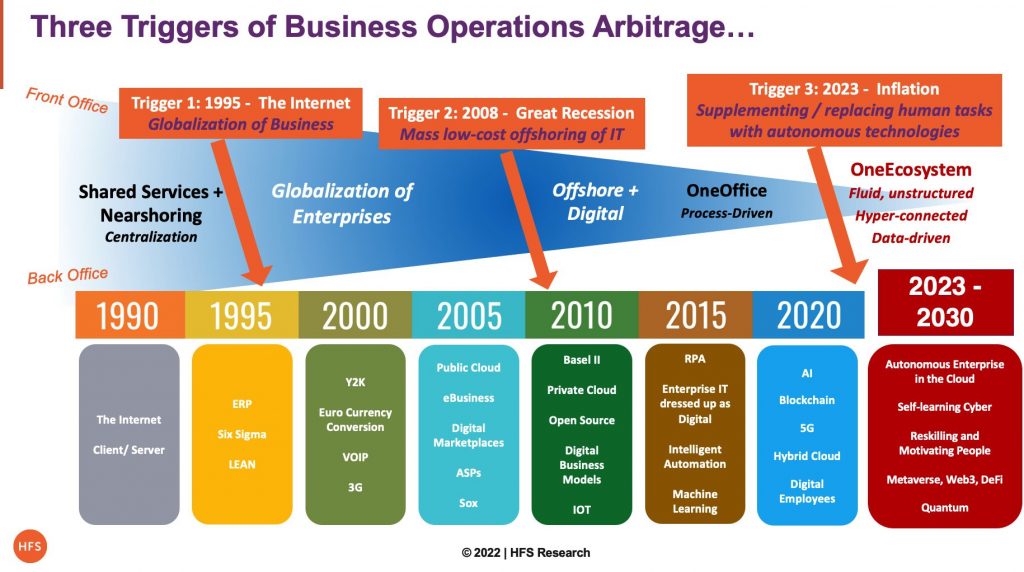

Nothing dictates real secular change to enterprise operations than financial pressures, and we are rapidly arriving at a third major trigger that will lead to the evolution of many autonomous enterprises where leaders have no choice but to drag their operations out of the dark ages:

Trigger 1: 1995 – The Internet drives globalization. The advent of the Internet at the turn of the millennium drove the first major wave of globalization of business and operations.

Trigger 2: 2008 The Great Recession brings about mass low-cost offshoring of IT. In 2008… the Great Recession drove a 15-year wave of tremendous offshoring growth… based on lower-cost labor to slash costs.

Trigger 3: 2023 Inflation drives organizations to supplement or replace human labor with autonomous technologies. In 2023… wage inflation, recession, and people refusing to return to the office will drive a considerable wave of autonomous enterprises… based on technology to perform the tasks of humans to stay afloat.

What is an “Autonomous Enterprise”?

An autonomous enterprise is one whose leadership continuously seeks to refine the data it needs in real-time to be successful. Its governance capability ensures it has the talent, tech infrastructure, automation, and AI to deliver the data that will drive success with minimal manual interventions that impede progress and speed. The ultimate goal of an autonomous enterprise allows us humans to remove ourselves from some parts of the system so that we can make continuous improvements to the ecosystem as a whole.

Ultimately, this is about machines making decisions where we previously had humans and removing humans from loops that don’t need humans anymore. Leadership must understand the data they need to be successful and assemble and govern the right system to deliver success (see our Six Principles of the Autonomous Enterprise).

We are on the verge of the third significant trigger of business operations arbitrage – autonomous technologies at speed and scale

The advent of the Internet at the turn of the millennium drove the first significant wave of globalization of business and operations. Still, it wasn’t until the Great Recession of 2008 that sparked the first massive wave of IT offshore outsourcing saw the likes of Infosys, Cognizant, Wipro, and TCS enjoy enormous growth to become the multi-billion dollar firms they are today.

During the last decade, we have flirted with the advent of automation, where the rudimentary screen scraping, process, and system patches of RPA sparked the dreams of many CFOs and investors to “Automate the Enterprise.” The reality was that real progress with automation was never going to happen, while business unit leaders refused to make fundamental changes to their underlying processes and data. Plus, the fact that the global economy has been on a constant upward growth curve in recent years, and no one really drives painful, transformative change until economics forces them to.

Inflation-driven pressures will likely culminate in a huge wave of job reductions, sparking the demand for autonomous technologies to fill the void

In so many recent HFS roundtable conversations with enterprise leaders, there is one constant topic dominating proceedings: how to keep businesses functioning effectively when most staff are not willing to come to the office, when it’s impossible to coordinate complex process and workflow changes to the business, all while there is huge pressure to reduce inefficiencies, drive down costs and improve the quality of data.

In short, many businesses are limping out of the pandemic confusion, still struggling to pull themselves together, and in many cases, are slipping backward in terms of cementing their digital foundations and joining up key workflows across front-to-back offices.

Many organizations face significant staff reductions and have to figure out how to deliver on their operations and achieve their business outcomes with fewer people.

Operations leaders who cannot deliver on automation will become obsolete – it is now an expectation. Losing people will force smart managers to rethink how they can achieve more with less – you’ll simply have zero choice but to act. You’re running a finance department of 500 people, which is reduced to 250. How do you get stuff done now? You’d better reconfigure how processes work so you can take advantage of automation that can interact – via voice and digital – with self-learning capabilities that don’t need constant human supervision.

On the flip side, less people will make it easier to identify areas that demand urgent changes, and as they identify the critical data they need to be effective: do they know what their customers’ needs are? Is their supply chain effective in sensing and responding to these needs? Can their cash flow support immediate critical investments? Do they have a handle on your employee morale and performance?

Where technology can deliver routine tasks via simple automation and self-learning AI is becoming critical. HFS is using the team “digital employees” to describe how smart bots can function autonomously, can respond to both voice and digital interactions, can develop both short and long-term memories, can genuinely replace or supplement human activities to deliver workflows and processes that can provide the data company leaders need – at speed and at scale.

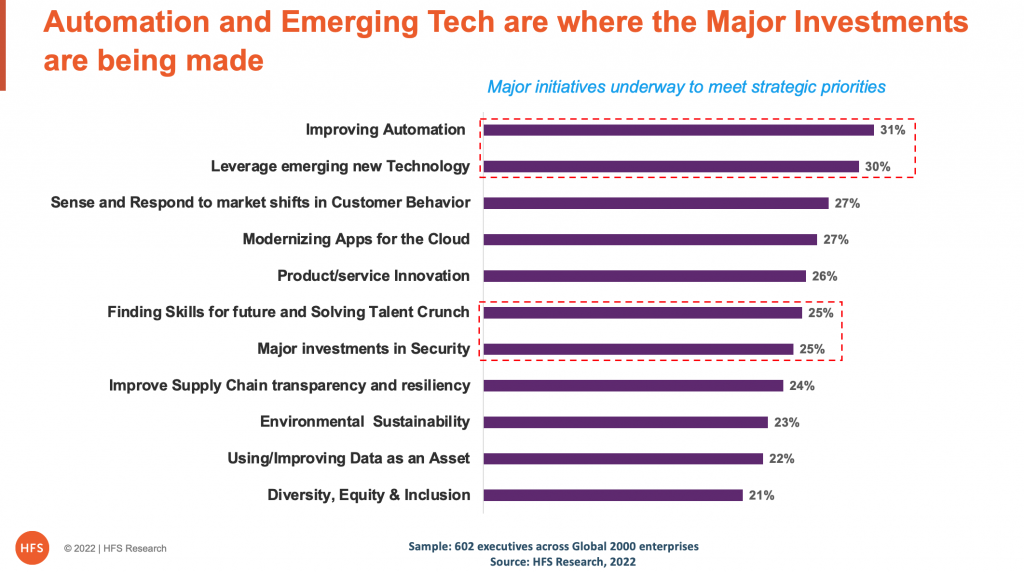

Automation is the leading tech investment being made among Global 2000 enterprises

10 years since HFS introduced RPA to the industry (see link), and we’re finally focusing on automation as a value-lever that drives business outcomes, as opposed to mere cost takeout in the back office.

The pandemic has shifted the automation focus from creating efficiencies in the back office to delivering immediate business impact, where talent shortages can be overcome, where digital workflows can operate despite broken supply chains, and where businesses can find new opportunities in their virtual and hyperconnected ecosystems.

Our recent pulse data of 602 enterprises proves beyond doubt that automation is the number one initiative currently underway to support enterprises in meeting their strategic priorities:

Automation is a discipline and a mindset

Automation is becoming so increasingly important to businesses as it helps solve so many of these endemic problems being caused by labor shortages, wage inflation, and poorly integrated systems, workflows, and processes. Simply put, if you get better at automating, you’re solving a lot of these other problems at the same time.

Smart business leaders have realized that automation is a mindset and a discipline that needs to be ingrained into every business practice. It is not why we do things; it’s how we do them. Automation makes what we have function effectively without needing constant human attention and manual workarounds. And the better we understand automation, the more autonomous it can become to drive genuine artificial intelligence interactions and processes in the future. AI and automation are becoming increasingly synonymous as we figure out how automation can really work within a business operation.

If there’s one thing the pandemic taught us, it’s been the necessity to re-think processes to get the data; what should be added, eliminated, and simplified across our workflows to source this critical data. And there is simply no option but to plan to design processes in the cloud using web-architected applications. In this virtual economy, our global talent must come together to create a borderless, completely digital business ecosystem where we can connect with other organizations that share common goals and purposes. This is the true environment for real “digital transformation” in action.

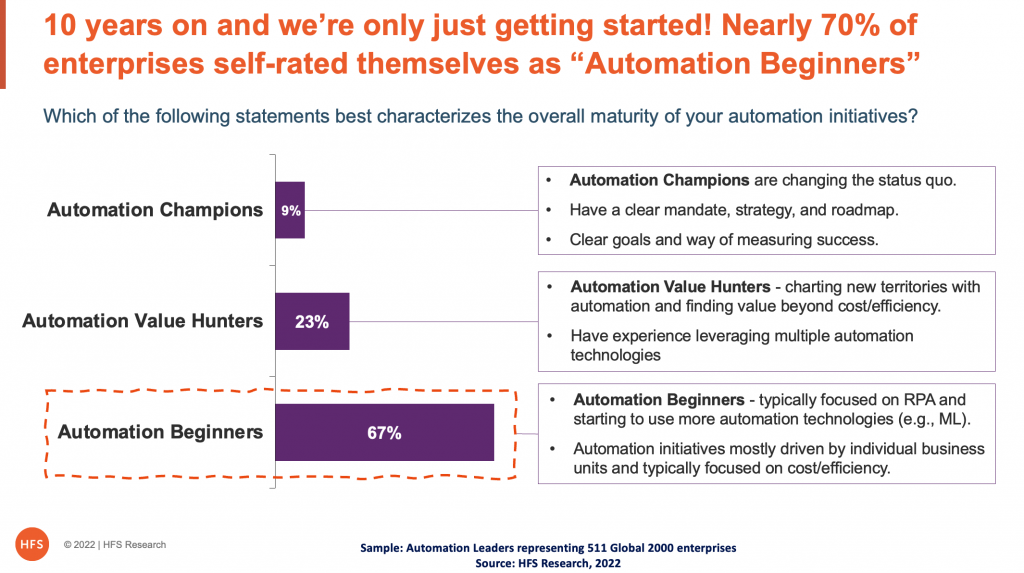

The Bottom-line: Most enterprises are only at the start of the real autonomous journey

As we reflect on our research covering over 500 automation leaders of major enterprises, what hits us the most is that 70% admit they are still novices. It seems the more they learn, the more they realize they need to know. We’re only at the start of a long journey for the majority of today’s ambitious organizations, and selecting the right partners along the way to help them design, implement and learn from automations across their businesses is so important. As one CIO delightedly pointed out to me recently: “I’ll keep finding automation ’till I die”… now that’s the attitude that is changing the whole approach to automation as the new IT mindset.

There is major rethinking taking place for 2023, where many firms are simply struggling to navigate this current maze of complexity and cost. The Autonomous Enterprise vision is where the survivors are looking, but getting there requires fewer people, politics, resistance to change, and great partnerships…