A decade on from the trials and tribulations of IBM Watson, IBM unveiled its multi-model and multi-cloud Watsonx to drive AI-first enterprises – what we are calling “The Generative Enterprise” at HFS.

IBM is describing the platform as a “full technology stack” for training, tuning, and deploying AI models, including foundation and large language models, while ensuring tight data governance controls. Watsonx.data focuses on the data scientist; Watsonx.ai the application developer; and Watsonx.governance is then used to deploy the model using a data model factory to ensure that AI is used ethically and responsibly.

In our view, Watsonx is the first enterprise-grade offering to address the Generative Enterprise holistically. Here’s our interpretation of Watsonx:

Watsonx.data helps you create the data model. It focused on the data scientist leveraging Red Hat Open Shift to prepare, tokenize, train, and validate internal and external data.

Watson.ai helps you ask the relevant questions (design prompts). ChatGPT, for example, never gives exactly the same response twice. Learn how to prompt your LLM more intelligently with both short and long prompts to compare quality and accuracy. One of the key benefits of GPT4.0 is the ability to absorb very long prompts (as large as 1000s of words) at rapid speed.

Watson.ai also helps to iterate. Try asking the same question in different ways, exploring multiple responses to the same prompt, and then comparing the results, detecting bias, and being aware of it.

Watsonx.governance evaluates responses which is as critical as much of what we have experienced so far as how ChatGPT gets it wrong. Asking questions in different ways, discovering contradictions, and asking to self-assess, is a key aspect of GPT4 that has improved significantly since the prior version.

Watsonx.governance helps eradicate bias by constantly expanding our understanding of bias in LLMs. ChatGPT, for example, is biased based on the underlying approach used to build the LLM and the data used to train it.

Watsonx overall fosters the generation of new ideas (Generative Thinking). The big challenge now confronting us as we pursue becoming a true Generative Enterprise is to constantly seek new ideas beyond the constraints of our current LLM. You should ask ChatGPT to summarize, synthesize and find the contradictions in the result it creates. Invest time in learning how conceptual blending approaches are evolving.

The Bottom-line: IBM could have been at the center of the AI revolution but was left out as a bystander. Watsonx has the potential to put IBM front and center of the Generative Enterprise

Watsonx seems very well thought through for AI-powered enterprise use cases, especially for horizontal call centers, HR, and F&A. IBM seems to have learned from its original Watson launch by deploying it internally first, launching an apps development platform to demystify the technology. However, the IBM narrative for Watsonx continues to be more technology-centric versus business-centric, which they need to address with their Watsonx narrative.

IBM still woos the CIO budget, but that’s only a third of the total enterprise tech spend. We believe IBM runs the risk of missing out on the broader CXO budgets but polarizing itself around the CIO.

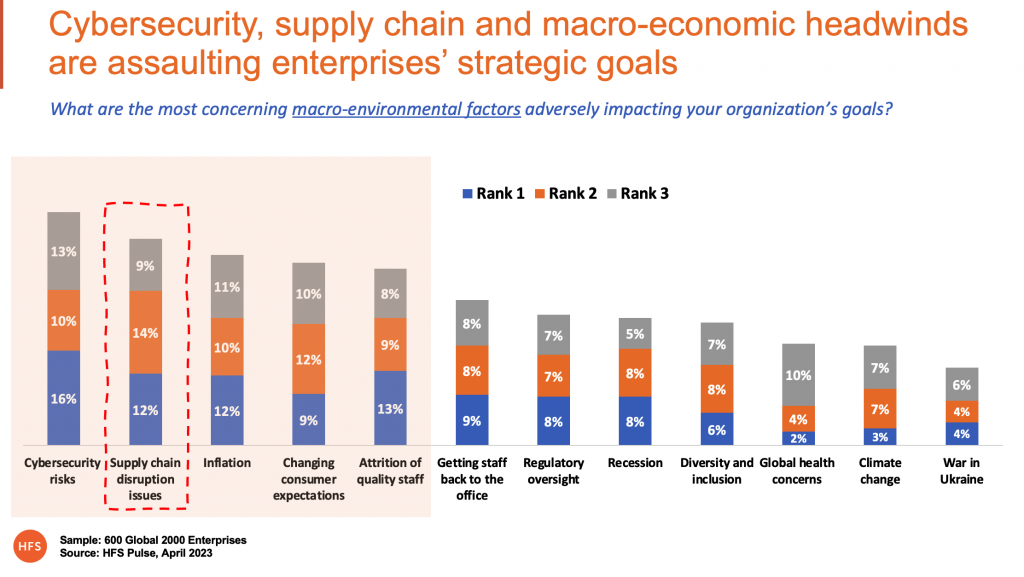

The health of most enterprises depends on the robustness of their supply chains, and our latest Pulse study of 600 G2K orgs shows supply chain disruption is posing the second-greatest challenge to enterprise leaders after cybersecurity:

Today’s enterprises grapple with unprecedented challenges, including disrupted supply from hubs like China, heightened sustainability expectations, a lack of resources, and increasing raw material and fulfillment costs. Service providers help enterprises improve inventory allocation through artificial intelligence (AI) and machine learning (ML) algorithms, optimize supplier management through dynamic supplier management systems, improve visibility by building advanced control tower solutions, and reduce people dependency by introducing automation across processes. The objective is that enterprises should be able to detect and react to “change” quickly, transforming from linear to circular to eventually autonomous supply chain networks.

The HFS Horizons report on supply chain services features 18 providers across three Horizons manifesting incremental business value for enterprise clients. Horizon 1 focuses on a linear supply chain driving functional optimization, followed by Horizon 2, which retains the values of Horizon 1 plus drives circular supply chains with end-to-end transformation capabilities, creating unmatched stakeholder experience with a “OneOffice” mindset. At the pinnacle is Horizon 3, which encapsulates all values of previous Horizons plus encompasses a networked and autonomous vision of the supply chain, driving completely new sources of value with a “OneEcosystem” approach.

The chart below summarizes the Horizons philosophy and key underlying dynamics, showcasing the providers across the three Horizons.

Note: All providers within a Horizon are listed alphabetically

According to the report’s lead author, Ashish Chaturvedi, “The pandemic coerced enterprises to prioritize resilience in their supply chain management and modernization programs. They are achieving this by increasing supply chain visibility, limiting human intervention, and creating multiple fallback options at a process level, such as source-to-pay (S2P). This newfound focus transcends the traditional linear, albeit constrained, supply chain management approach. Gradually, the industry is inching toward a connected, autonomous, sustainable, and collaborative supply chain paradigm.”

Report highlights include

Supply chain resilience has become the central theme of contemporary supply chain engagements. Service providers are helping move enterprises from just-in-time to inventory overstock and single-supplier–single-country sourcing to multi-supplier–multi-country sourcing, demanding more dynamic control tower solutions and a higher degree of automation in demand planning, warehousing, and fulfillment. The objective is to have more control and visibility of the supply chain to navigate unforeseen disruptions.

Sustainability offerings have evolved but not baked into engagements. More than two-thirds of the providers participating in the study have formulated offerings around sustainable sourcing, circular economy, green logistics, and decarbonization metrics. Interestingly, most of the cases discussed were standalone sustainability engagements with a supply chain angle rather than the other way around. It came to light that enterprises are also putting a half-hearted effort into baking sustainability across the supply chain.

HFS assessed 18 leading supply chain service providers. Of these 18 providers, six are positioned in Horizon 3 as leaders, nine in Horizon 2 as innovators, and three in Horizon 1 as disruptors. The services firms that lead the market and ecosystem-level change in Horizon 3 are Accenture, Capgemini, EY, IBM, TCS, and Tech Mahindra. The services firms innovating across organizations and supply chains in Horizon 2 are Cognizant, Deloitte, Genpact, GEP, HCLTech, Infosys, KPMG, PWC, and Wipro. The services firms disrupting and transforming business processes and functions in Horizon 1 are Atos, Hitachi Vantara, and Zensar.

The report includes detailed profiles of each service provider, outlining their capabilities, strengths, provider facts, and development opportunities.

To paraphrase Freddie Mercury, “Another bank bites the dust.” This time it’s First Republic Bank – the latest financial institution that was unable to sufficiently rebound from the liquidity crisis borne out of rising interest rates. J.P. Morgan scooped them up on May 1, with its Chairman and CEO Jamie Dimon widely quoted in the press insisting that this is not a global financial crisis repeat.

HFS tends to agree with him. Central banks and the financial services community have too much at stake to let that happen. It was a long road back from 2008. Trust in banks is still dicey at best. We expect we’ll see continued regulatory oversight, financial support and rescue buy-outs if needed to keep the global banking system functional.

While there is an undeniable crisis of confidence at play fueled by various macroeconomic factors and exacerbated by the spate of bank failures, crisis begets opportunity for the bold. Here are three recommended actions that growth-minded banks should take immediately to ensure survival at a minimum and potential leadership if done well.

Continue investment in critical modernization initiatives.

Digitize your commercial banking offerings

Create actual offerings for small and medium enterprise clients, inclusive of start-ups and scale-ups

Let’s break these down…

1. Continue investment in critical modernization initiatives

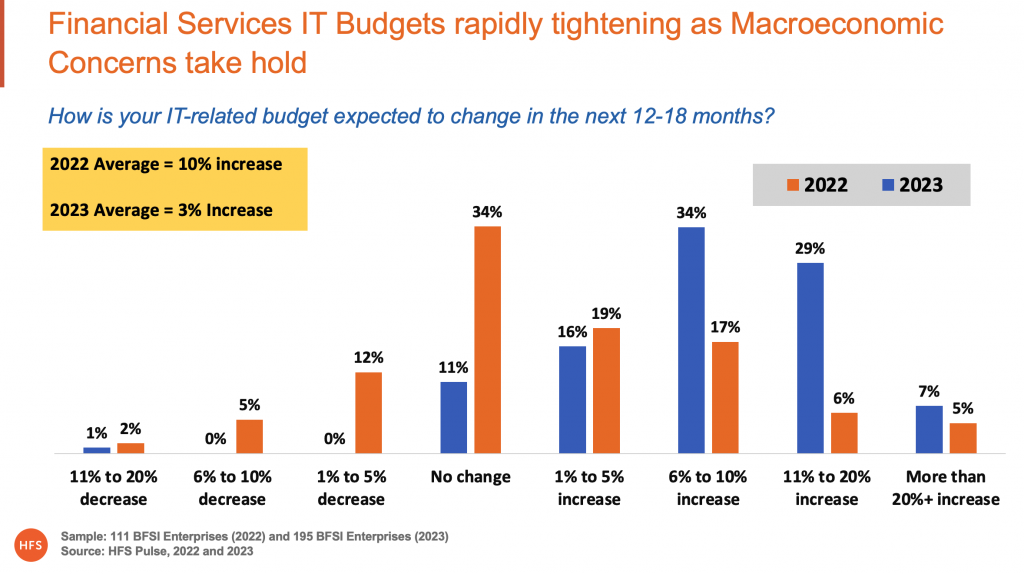

Before Silicon Valley Bank went belly up, global IT spending was already in a death spiral from the strain of ongoing macroeconomic conditions. With the pandemic largely at bay, everyone was forced to now pay attention to all the other contributors to macroeconomic malaise – global conflict, inflation, recession, talent challenges, and heightening cybersecurity risk. HFS saw this crisis of confidence reveal itself through a massive year-on-year slowdown in projected IT spending. As the below chart showcases, BFSI spending went from 10% projected growth in 2022 to just 3% in 2023, with the greatest portion of spending now sitting in the “no change” bucket.

This will further slow enterprise spending and related deal closures for services firms. This will persist for at least a quarter with the potential for stabilization and turnaround when banks fail and interest rate hikes quiet down, possibly in Q3 or Q4 2023.

As banks navigate the current mess, we beseech you – do not fall prey to the cost reduction path to perpetual mediocrity. While digital native competitors may be loads smaller than established banks, their technology nimbleness is real, enabling their ability to swiftly spin up new personalized offerings, use data to not just have a 360 views of customers but also to do something useful with the data immediately, and they can and are driving interesting new business models built on open banking and embedded finance. Smart banks need to have a firm understanding of which modernization initiatives are essential to enable growth. Core banking modernization and data migration to the cloud are two likely candidates that are well worth staying the investment course.

2. Digitize your commercial banking offerings

The four fallen banks of 2023 thus far – Silicon Valley Bank (SVB), Signature Bank, Credit Suisse, and First Republic Bank all had varied portfolios and customers. Still, they all offered a significant commercial banking proposition. These failures have already sounded the alarm for updated regulatory standards pertaining to interest rate risk. But they should also serve to raise awareness about the shoddy state of commercial banking – built for large enterprises and starved of digital investment. Smart banks should turn this so-called crisis into an opportunity to finally modernize their aging commercial banking capabilities. The impact will be better quality of service for existing clients and realization of the growth potential in SMEs.

A recent HFS survey of 150 commercial banking leaders revealed investment in offering expansion is heavily focused on enhancing existing capabilities not spinning up sexy new offerings:

The same but better. The top three areas for commercial banking offering expansion are lending and lines of credit, deposit accounts, and commercial cards. Treasury services rolled in at number four. The emphasis is less on new offerings and more on better versions of existing offerings.

Customer onboarding time takes too long. Respondents indicated the average time to onboard a commercial customer is 32 days. The leading factor slowing onboarding is implementation or integration requirements.

Host-to-host connectivity still rules customer access. 65% of respondents indicated that host-to-host connectivity is still the primary standard for accessing products and services. Commercial banking leaders expect strong growth in API connectivity in the next two years.

Current investments favor operations automation. Commercial banks indicated their current top area of investment is in intelligent automation of transaction and operations management. The top areas of investment in two years’ time shift from process optimization to international enablement with trade finance and embedded finance opportunities.

As banks consider their paths forward in the low-confidence economy, there is a clear need and growth potential in commercial banking that can be unlocked with appropriate investment.

3. Create actual offerings for small and medium enterprise clients, inclusive of start-ups and scale-ups

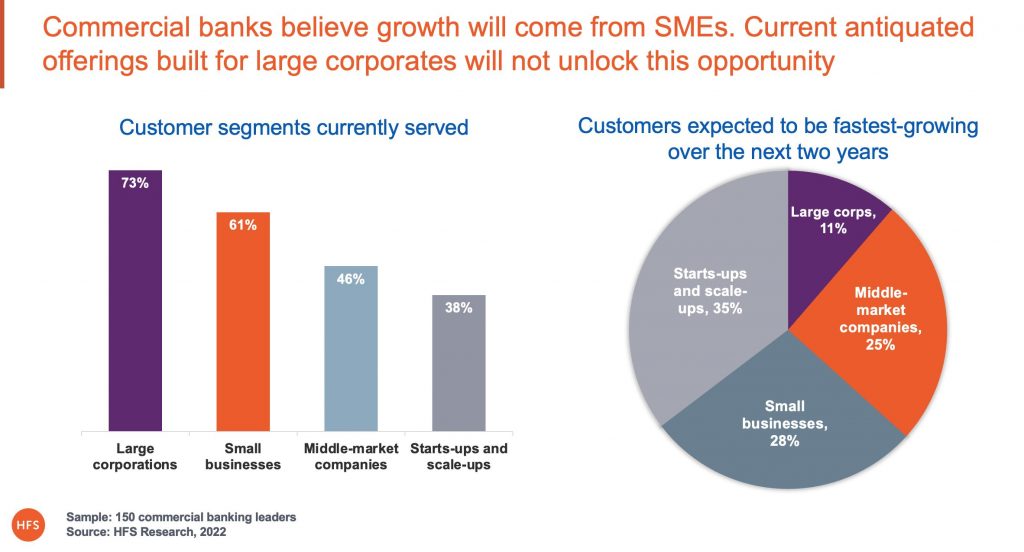

Commercial banking has largely been built for large corporates. The definitions of “large” tend to change based on the size of bank, but the customer baseline is very consistent – with large corporations making up the lion’s share of commercial customers served (see below). SMEs, start-ups, and scale-ups are represented, but often these segments are clubbed with and supported by retail banking businesses rather than being treated as commercial clients – or as their own unique customer segments. This is a missed opportunity to support and enable the growth of SMEs.

As Exhibit 2 also shows, commercial banks realize future growth will come from SMEs. The conundrum, though, is how to truly cater to these segments. The gaps left in the market by SVB, Signature, and now First Republic – all firms that were notable backers and supporters of SMEs – raise issues of bank choice, who is willing to support SMEs and innovative start-ups, and how to do so. As we suggested earlier in this piece, banks supporting commercial customers must invest in digitizing their offerings to deliver better services to existing clients. But it is also a critical ingredient to customer expansion. SMEs want the digital capabilities they’ve been enjoying on the retail side of the house with the benefit of traditional commercial services like various treasury services, lending and lines of credit, and merchant services – but done digitally. SMEs and start-ups, and scale-ups need to be treated as a distinct business segment.

The Bottom Line. Despite the crisis of confidence, there is a glaring opportunity in the face of the banking mess – better commercial banking

Banks should clearly shore up their balance sheets in the face of the liquidity crisis. Those not on Moody’s or other watchlists should consider seizing smart opportunities The need for better commercial banking is not new. But the recent bank failures have put a spotlight on banking choices and the options available to SMEs and innovative start-ups and scale-ups. There is a clear need and opportunity for digitization in commercial banking. As part of this investment, banks need to consider the needs of the SME community – typically representing over 99% of business in most country markets. These are your future growth customers, and they want offerings designed for them.

Anyone tracking HFS will have noticed some terrific new brains join us over the past couple of years from all over the world, but one area we have been really keen to bolter is engineering services. And we’ve been lucky enough to hire a smiling insomniac in Nandini Tare, who’s helped us grow our practice and coverage significantly, especially with her recent flagship Horizons report on Digital Engineering Service Providers.

So let’s hear from her directly what makes her tick and her views in the industry…

Hi Nandini – you’ve been causing quite the excitement for HFS over in India in the year you’ve been with us. Can you tell us a little bit about yourself? What gets you up in the morning?

On the professional front, Phil, I have been in research and consulting for almost 15 years. I started my research career in the automotive sector and now have about 3 areas of expertise under my wing. It has been an exciting journey so far, engaging with business leaders and talking about changing technology landscapes. The world is moving at such a fast pace, and everyone is trying to play catch up. I can’t help but quote Leena Nair the global CEO of CHANEL, ‘Don’t wait for the storms to pass, learn to dance in the rain.’

On a personal front, travel is my weakness. I find traveling an opportunity to engage in experiences that bring me inspiration and keep me motivated. I recently started on a fitness journey that has me up and running in the mornings. The endorphins keep me going. I am hoping to get certified as a coach in the future hopefully! And when I manage to get some free time, I ride my Royal Enfield Classic 500.

So why an analyst? Is this something you always wanted to do as a profession, or did you just fall into it by circumstance?

I believe I had the skills but didn’t tap into them early, but I forayed into industries accidentally. By no means am I an engineer, but I know how engineering impacts businesses. After experimenting with various roles from pre-sales to operations to consulting in my early career, I later chose to play by my strengths. It was a wholesome transition. The early experiments in my career gave me first-hand experience and widen my thought process. This experience has helped me analyze a subject or a topic from all angles and then conclude my opinion.

So what makes a good analyst, in your opinion?

An independent voice and an ability to be unbiased. I feel these two qualities can set an analyst apart from the regular crowd. Believing in the research and methodology one has created and proudly owns it. One can develop skills to be an SME, but providing an unbiased opinion is a conscious effort.

You’ve clearly demonstrated an aptitude for covering engineering markets… what’s so exciting about them, Nandini?

The whole ecosystem is getting connected. Businesses now have access to the latest and greatest technologies to reduce costs and make themselves profitable. The influx of IoT, AI, Robotics, 3D printing, 5G, Cloud, and emerging technologies like Blockchain, Metaverse, Digital Twin, etc. are impacting the consumption side and changing the way traditional business functions. Businesses are now spending on R&D to identify early-stage use cases and commercialize them to bring themselves to the forefront of the industry. All these changes must be a steady progression. ER&D is set to expand as it further gains acceptance in outsourcing and digital engineering. While all of this has me excited, I have intentionally kept generative AI out of this conversation as we would never stop discussing it and arrive at a conclusion on its influence on the ways of working.

And what do you think we’ll be talking about in 2 years time in this space?

Digital engineering services, as most of us would agree, have largely been known for building new products and solutions, Phil. The current set of available technologies has improved business efficiencies, augmented the speed at which a product is brought to the market, and aided product as a service. There is a small portion of the industry that is already talking about how digital engineering is advancing digital transformation strategy to business transformation. One would see a reduction in the lift and shift process and an increase in well-thought-through utilization of technologies to bring true value to the business. It would be interesting to see how service providers and enterprises develop a purpose-led ecosystem and outcome-based pricing. One would also see businesses engaging with niche players to build capabilities to provide enhanced customer experience. Overall, I see this space growing in the next few years.

Thanks for your time today, and looking forward to the next big insights, Nandini!

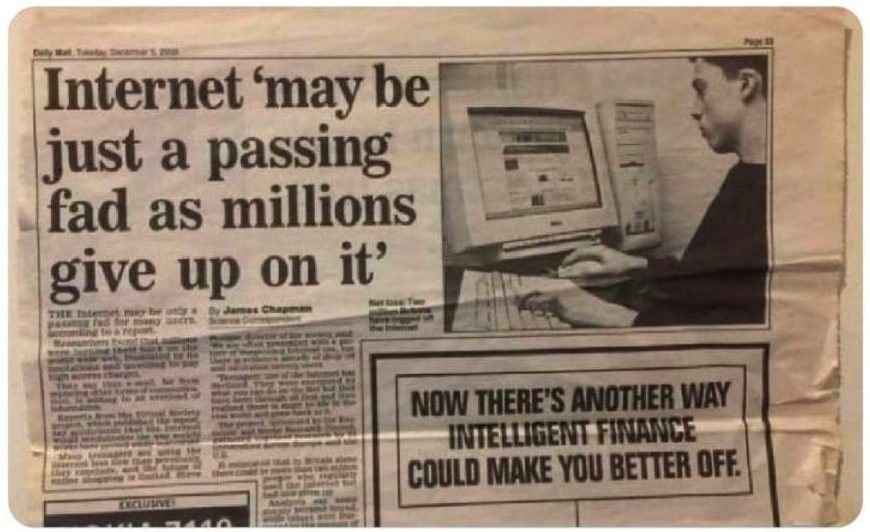

Recent headlines such as those in the WSJ (The Metaverse is Quickly Turning Into the Meh-taverse), and similar in the FT, remind us of such classics as ‘Internet may be just a passing fad as millions give up on it’ from the year 2000 edition of the UK’s treasure trove of fact, The Daily Mail. Such black-and-white premature pronouncements are typical of headline hunters. As leaders planning their investments and ensuring we extract the advantages we need from technologies as they emerge, we must take a more measured approach and a longer view. The Metaverse is so much more than Zuckerburg’s stumbling business model; it’s the complete immersion of augmented experiences enabled by AI and, ultimately, by Web3.

Anyone who thinks Disney has given up on the Metaverse has lost the plot

The headlines are being made by what are largely corrections in investment in the consumer Metaverse. For example, Disney is reported to have shut down the division, which (among other things) handled Metaverse strategies.

But these layoffs are part of a broader effort to reduce corporate spending and boost free cash flow. Disney is cutting $3 billion in content spend. No one is saying that’s the end of Disney content.

Let’s be real here. The idea that Disney has entirely shelved its Metaverse ambitions just does not ring true. Their ambitions “for storytelling without boundaries in our Disney Metaverse” have not gone away.

Meta’s rollback is no surprise and is likely to encourage investment from others

Mark Zuckerberg may be playing bait and switch with AI on his most recent earnings call rather than with the Metaverse, but then again, who isn’t? ChatGPT is investors’ latest drug of choice; why wouldn’t he play up Meta’s capabilities in it? Frankly, Meta distancing itself from the Metaverse landgrab will be welcome in a community that prefers decentralization and cooperative collaboration to the Zuckerberg monopoly any day of the week. We expect the Meta roll-back to encourage investment from elsewhere.

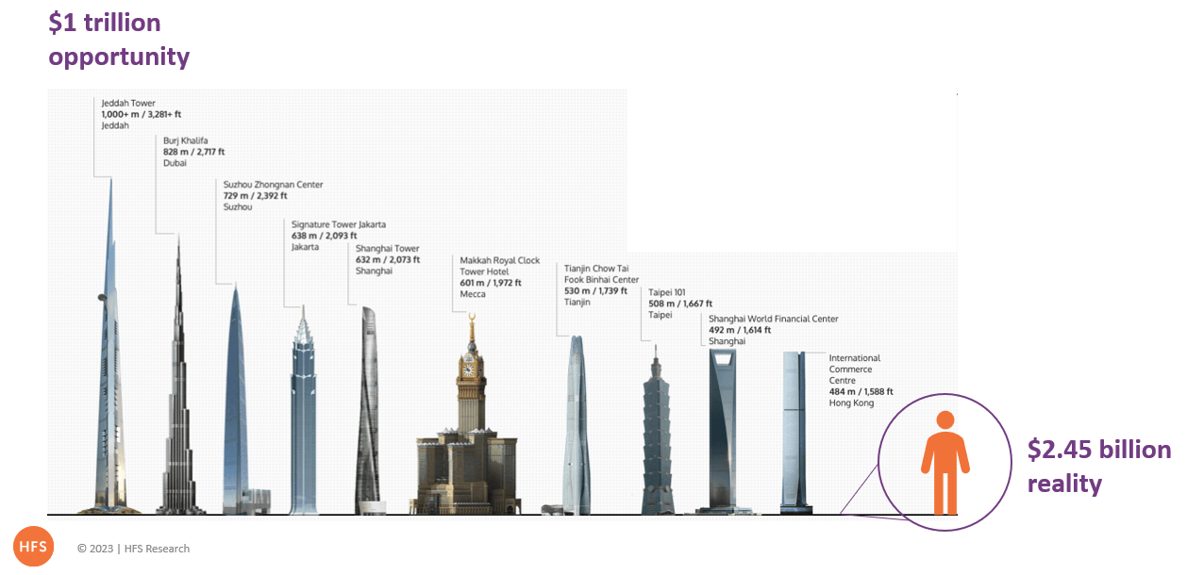

So what is really going on? A figure of $1 trillion for the Metaverse economy was reported at Davos just a few short months ago. Where did that come from? The answer: a global survey of CEOs who were asked roughly what percentage of their revenues they expected to come from Metaverse-related activities by the end of 2025. For context, this represents less than 1% of global GDP (which is predicted to deliver $118 trillion in 2025 – source, Statista).

The predicted opportunity equates to the size of a 1000m high skyscraper in comparison to the current reality – which at the same scale would appear just 2.45m tall

Source: HFS Research 2023

The $1 trillion opportunity is one Accenture takes seriously and CEO Julia Sweet has referenced it in public. Accenture is investing heavily in the Metaverse and believes it is one of five pillars of success for the enterprise over the next decade.

18 Metaverse services providers expect, on average, to see 15% growth this year

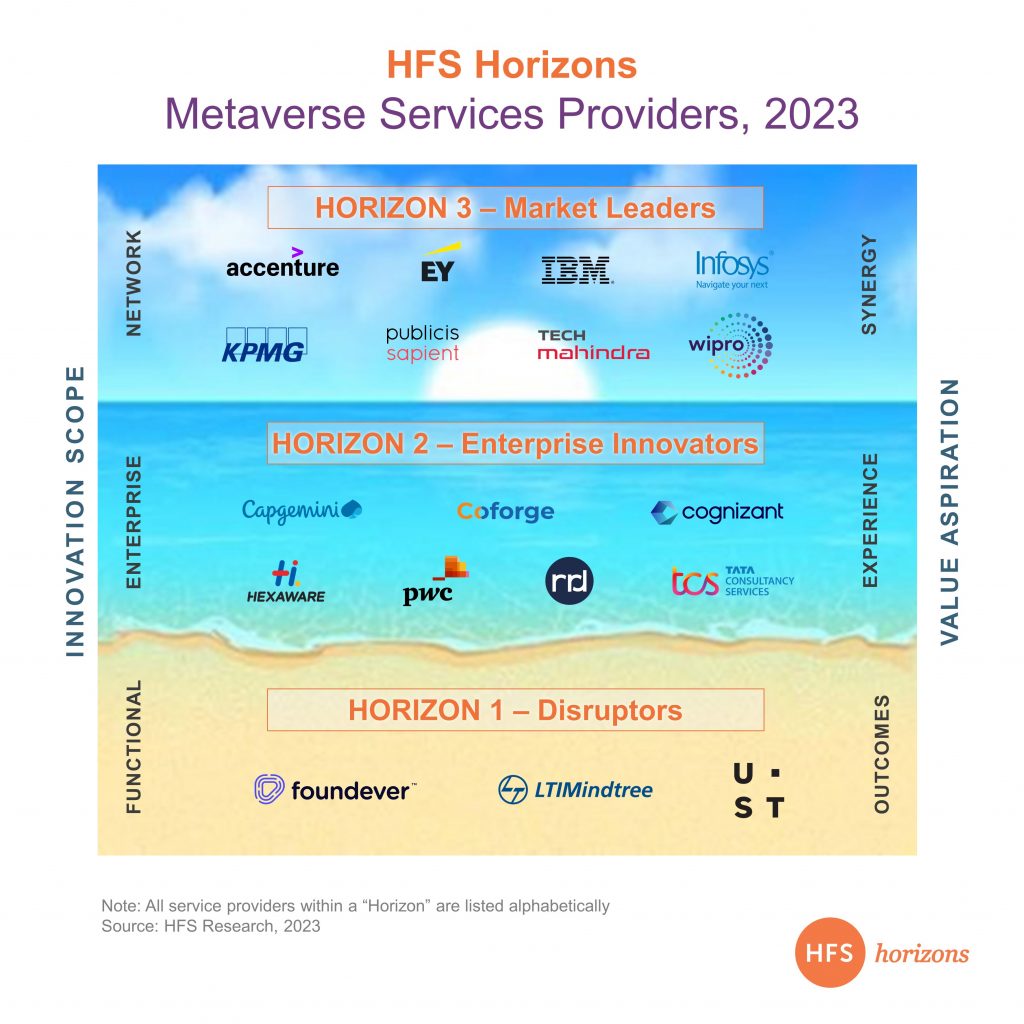

Accenture is far from alone in believing there is a very real and present opportunity in the Metaverse. Our recently published – and inaugural – HFS Horizons Metaverse Services report 2023, includes profiles of 18 leading services and consulting businesses who are designing and delivering Metaverse services and products right now. HFS estimates they are collectively generating $2.45 billion from these services – and across the board that is expected to grow by 15% this year.

Exhibit 1: 18 leading service providers and consultancies feature across three value horizons in our inaugural Metavese Service report

These include (exhibit 1) Accenture, Capgemini, Coforge, Cognizant, EY, Foundever, Hexaware, IBM, Infosys, KPMG, LTI Mindtree, Publicis Sapient, PWC, RRD, TCS, Tech Mahindra, UST, and Wipro.

Enterprises are continuing to increase Metaverse investments

We also found that Metaverse spending, along with low–code investment, were the only two areas in which enterprise investment in emerging tech is not being cut. Metaverse investments showed the greatest increase in investment, with 87% of enterprises committing between 5% and 20% more spend in 2023. The important caveat to this is that most are starting from very low bases.

The Bottom Line: Investment, services, practices, and products prove the Metaverse is not going away. Join investors now or scramble to catch-up later

Enterprise leaders should not allow knee-jerk headlines to distract them. The Metaverse is not going away, as proven by the investments continuing to be made and the practices, products, and services being established by leading service providers and consultancies. Your rivals are increasing their investment in the Metaverse. Your choice is between joining them now or scrambling to catch up later.

One of the most talked about sessions at the HFS Super Summit in New York was my on-stage 1-1 with one of the IT and business services industry’s most revered voices, Ravi Kumar. When he’s not getting invitations to the White House to advise on expanding IT talent development in the US, he’s often spotted on stage at the Milken Institute or Davos – all the while working many major customer engagements – and some of the largest in the history of services. Not many people have been as steeped in the development of global IT services over the last couple of decades as Ravi

So getting Ravi to talk candidly to a senior audience of IT and operations leaders at the recent HFS Summit was a terrific opportunity to get his perspective on the current crisis engulfing tech services to attract the best and brightest – and reverse this depressing drift towards becoming a commodity business.

Phil Fersht: Well, Ravi, do tell the audience a bit about yourself. Because you’ve kind of grown up with this industry, you’re still fairly young, as well, so you have a good affiliation with younger staff, as well as senior management, being one yourself. So maybe you could share a little bit about how what used to be sexy about this industry and maybe where it’s lost its sheen a bit.

Ravi Kumar: Phil, thank you so much for the opportunity to talk to you and the audience here.

When I joined this Industry two+ decades ago, I would say the tech services industry, in general, hired from tier 1 schools. Twenty years hence, I think this industry hires from lower-tier schools. So it’s a significant shift. I think the classical economics of when demand outstrips supply, you think the billing rates are going to go up. That’s not happened. And because the rates have not gone up… I think somebody in the audience mentioned that their son didn’t join one of the tech services companies because it’s not an innovation industry. I think, historically, the industry has been a fast follower in that way. So you fast follow tech cycles, tech waves, and you monetize on it.

And I would also say, Phil, that for the last 30 years, Global 2000 firms used system integrators for enabling technology in the non-core; building HR systems, building CRM systems, building financial systems, etc. So when tech is non-core – and for the last 30 years, the Global 2000 went global, and they used technology to make their operations efficient – it wasn’t so critical, honestly. It was critical to scale, technology was the enabler, but it wasn’t like technology was core.

So every time there was commoditization, it actually hit the tech services industry the most, and the tech services industry held up the margin, and to hold up to the margin, they actually went down the chain to lower-cost schools and hired talent in addition to building productivity improvement cycles. And that actually is the reason why it went from being a sexy business to where it is today.

Phil: Ravi, so how do we reverse this depressing cycle down the service value chain?

Ravi: Phil, we have this unique opportunity to change that. Tech has gone from non-core to core. The Global 2000 today want to use technology not just to build HR and CRM systems; they want to use technology to get extended reach to their consumers through digital platforms. Now, they actually want to embed technology into their products and services. So tech is going to go core. Every Industry today is in the technology and software business. When tech is core for a company, the kind of talent you need is going to be extraordinary, and the rates you are going to get are going to be elastic. And therefore, we have this unique opportunity to repivot. And I would say that the ones who will really make it are the ones who can pivot from enabling technology from the non-core to the core.

There is a new segment of customers that is showing up, which is digitally native companies. Digitally native companies did not outsource for the last 20 years or so. They had a free runway on EBITA, capital was freely available, and they hired talent at an abnormally high cost, which is why they are attractive as employers. Now, the cost of capital is high, and there is accountability to EBITA. So these same set of companies are outsourcing, but they were born digital, so they are outsourcing for core work, and therefore they’re willing to pay more money for high-quality talent. So we could repivot if we want to. So that’s the second shift. Tech is core, and we have a new segment of clients.

And the third is the universe for tech services companies was 2 to 7% of the revenue ofRead More

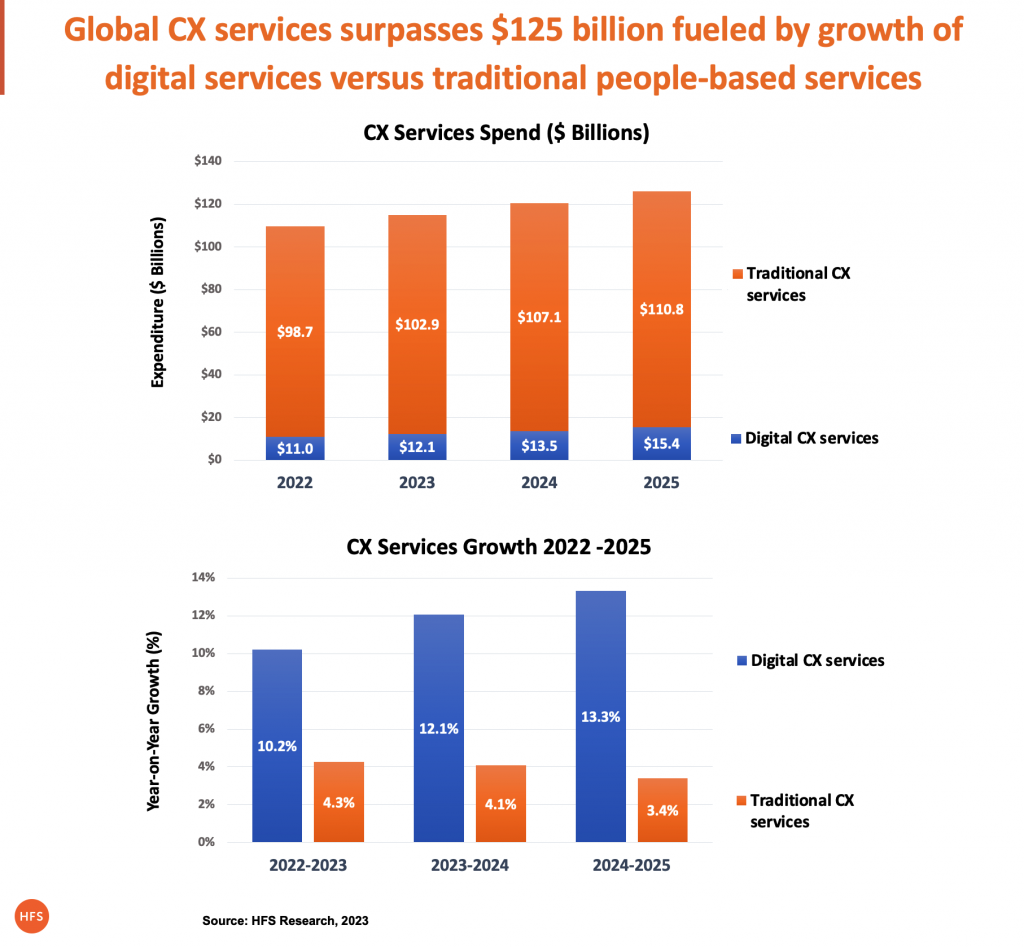

Every couple of years, we’re due a large-scale call center acquisition play, and the latest is Concentrix’s announcement to acquire Webhelp. With combined revenues of $8.3bn, Concentrix is now nipping at the heels of Teleperformance for position as the largest contact center business globally. Yes, it’s time for even more big traditional analog call center – and lots of it!

So has the $125 billion world of call centers really become so dull that the only thing left to talk about is who’s the biggest? This reminds us of the days when ADP swallowed up every payroll firm imaginable to ensure it controlled the global payroll market, making it an extremely unattractive market for others to enter. This speaks volumes for a service provider seeking to protect its legacy business and maintain the legacy way of pricing deals where scale means more butts on seats… and more revenue.

At first glance, it seems that Concentrix, Teleperformance and Foundever have locked down the CX services market… but they are actually creating a whole new one that will hurt them in the longer-term

However, there is one major difference here – traditional call center services are extremely ripe for disruption, with huge costs to be saved with the smart deployment of autonomous technologies. There are ample opportunities for tech-capable service providers to attack the CX space with digital offerings that are not dependent on voice-based butts-on-seats.

We are living through this Third Trigger of Change, where enterprises are seeking to slash costs, avoid wage inflation and enjoy the benefits of autonomization at the same time. Removing humans from loops where they are no longer needed is the game, but this seems to be counter to the business models of several traditional call center providers, still depending on selling more butts to keep growing their revenues. However, while traditional call center services are stagnating at a lower-than-inflation 4%, digital CX is growing at three times the clip (12%):

Just look at the growth services providers such as Tech Mahindra, Wipro, Genpact, and WNS are already enjoying adding CX-related services based on non-voice delivery to their client engagements. For example, Tech Mahinda has doubled its BPS business in three years (to over a billion dollars), wheeling in CX-related work in sectors like telco without this huge dependency on Manila. We fully expect other tech service providers with deep relationships in the CX domain to enter this market soon, such as IBM, Cognizant, and Accenture, all pushing business services with strong CX automation and AI elements.

For many industries, the need to house armies of increasingly-expensive customer service agents, either onshore or in locations like the Philippines, is decreasing as more and more customers simply do not have the time or inclination to talk to a rep, and enterprises want to cut out the costs of paying for them.

Concentrix hopes bigger is more beautiful for Webhelp’s customers

While service providers in other services, such as IT and F&A have been openly against scale-based acquisitions for several years, it seems that the leading call centers are opting for greater scale, more global presence, and more people to get ahead in their markets.

Recent consolidation of the largest providers in this market included Sitel/ SYKES (now Foundever) in 2021 and Concentrix/ Convergys in 2018. While this appears to be largely a scale play, Webhelp brings some unique features to the table. For example, its recent Sellbytel acquisition bolstered its ML/AI capacity. Its NEST offering is a business unit dedicated completely to helping startups scale their CX businesses, something we’ve not seen formalized in any major competitors (and probably will not until that market eventually recovers). Plus, the firm brings a strong ESG game, particularly with regard to its impact sourcing credibility.

Bolstering its geographic presence is clearly one of the advantages Webhelp brings to Concentrix, and its addition of 25 countries is appealing at a time when CX clients are very keen to pursue new locations that offer services and lower costs. Webhelp’s European, nearshore and South African presence will be particularly useful to complete Concentrix’s global jigsaw.

Whether Webhelp’s customers will be happy being serviced by a much larger beast is in question – will they get the same attention as before? Will Concentrix hike up prices safe in the knowledge the switching options have become fewer?

Concentrix is refocusing on traditional call center growth, despite earlier acquisitions of Tigerspike and PK

Much of the appeal of large-scale call center services acquisitions is to drive down pricing with fewer players, consolidate accounts and real estate, but it sometimes seems at the cost of innovation. This was the reason BPO giants like IBM exited the market several years ago (it actually sold its CX business to Concentrix a decade ago) and Capgemini deemphasized the CX space. They saw this market as a race to the bottom that was becoming harder an harder to maintain margins.

Webhelp signifies the direction Concentrix is going as a company, which is to edge out its other giant call center competitors with added scale and resources. When Concentrix acquired Tigerspike in 2017 to add digital design capabilities, it seemed that the firm wanted to broaden beyond CX into higher value areas to impact customer experiences. And its sizeable acquisition of PK Consulting early last year seemed like an attempt to make a more concerted effort into digital design after Tigerspike failed to impact Concentrix clients at scale.

However, the problem is simply that call center services and digital marketing services are acquired by different people within enterprises, and the client leads in services firms cannot sell to marketing leads as well as call center leads. You can’t blend the two skillsets the way most enterprises have developed over the years.

For example, the Sitel acquisition of Sykes saw a massive clearout of staff to remove redundancies, and strategic investments like its Symphony automation play have long bitten the dust. While the vision is lofty, the reality of the mega-mergers often seems focused on lower costs and higher margins while squeezing out cheaper smaller players. Overall we see a lot more call centers, and bigger call centers, than any significant technological advancements.

The Bottom-line: The future of CX is shifting to autonomous digital delivery, driving the need for call centers and IT integration providers to merge

Bigger isn’t always better, but other large providers are growing at faster rates, with both Teleperformance and TELUS both growing in the double digits. Both of these firms have made significant investments in technology capabilities and digitalizing their solutions, such as TELUS International grabbing up IT services firm Xavient and, more recently, digital engineering firm WillowTree.

Offshore-heavy IT-centric providers actively vying to move more into CX, having the tech capabilities to connect integration points, adding security around data repositories, and implement AI-bots to cater to autonomous customer contact. It seems that finding the right balance between technology and front-office capabilities will be the recipe for future CX success.

So why doesn’t Concentrix look to acquire an IT services firm to equip itself for the autonomous enterprise? Surely balancing the physical delights of the call center with digital integration capabilities to balance cost and speed will answer this digital dichotomy facing enterprises…

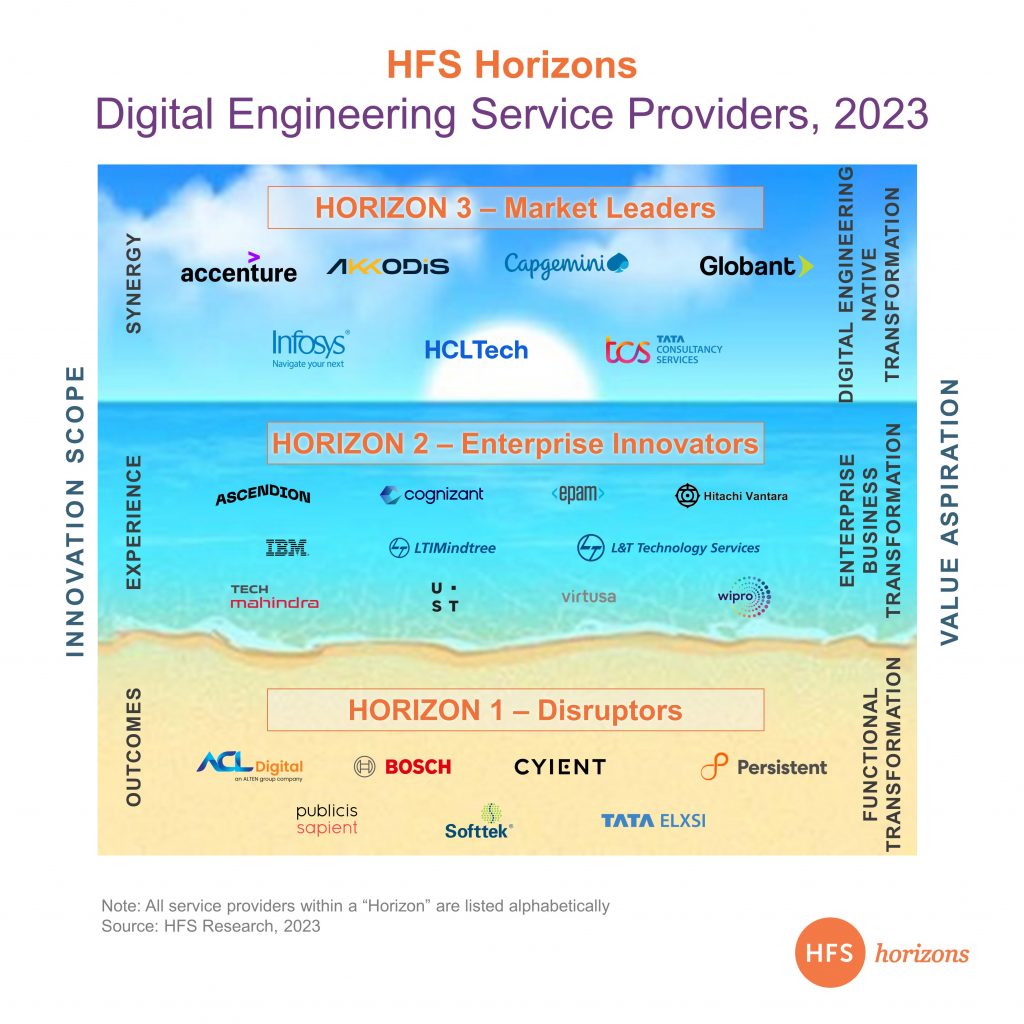

The new HFS Digital Engineering Services (DES) Horizons report provides a snapshot of leading digital engineering service providers’ capabilities in a rapidly changing market as more companies adopt digital technologies in product development and engineering processes.

Ultimately, the goal is to bring together siloed digital initiatives and look at a holistic picture of the business

Advanced technologies like artificial intelligence (AI), machine learning (ML), the internet of things (IoT), 5G, robotics, cloud, automation, data and analytics, blockchain, and alternate reality and virtual reality (AR/VR) are revolutionizing product design and development. As these new technologies emerge, there is a need for skilled talent, particularly in areas such as AI, ML, and data analytics.

Additionally, the rise of new business models such as product servitization (traditional episodic encounters being replaced by continuous personalized interactions) and platformization (making platforms data ready to drive commerce and interactions between buyers, sellers, and suppliers) has further fueled the need for providers to offer expertise in business design, marketing, customer and supplier engagement to stay relevant. This trend is driven by enterprises’ needs to optimize data use, digitally enable processes, accelerate growth, achieve customer intimacy, and become true ecosystem participants.

Disruptors, Enterprise Innovators, and Market Leaders

The HFS Horizons: Digital Engineering Service Providers, 2023 report examines service providers’ roles in digital engineering. The HFS Horizons model aims to align enterprise objectives with service provider value. We assessed 25 service providers across their value propositions (the why), execution and innovation capabilities (the what), go-to-market strategy (the how), and market impact criteria (the so what) to best understand and plot the value they offer to their digital engineering clients.

Here are the results.

Note: All service providers within a Horizon are listed alphabetically

The new Horizons landscape demonstrates the providers’ positions within the three Horizons:

Horizon 1 (Disruptors) refers to those providers who have been able to drive functional transformation with ecosystem partners and co-innovate solutions.

Horizon 2 (Enterprise Innovators) includes those creating end-to-end organizational alignment to drive unmatched stakeholder experiences.

Horizon 3 (Market Leaders) includes all providers with OneEcosystem™ synergy via collaboration to create completely new sources of value.

The Rise of Smaller Players in the Booming Digital Engineering Services Industry

The digital engineering services industry is a dynamic and rapidly evolving field, with many players offering a diverse range of technology and services. These players tend to be smaller, focusing on specialized niches within the industry. Despite their smaller scale, these service providers are experiencing impressive growth, with an average growth rate of 25%. Much of this growth can be attributed to North America’s booming market for digital engineering services. As this industry expands and develops, it will be interesting to see how these smaller players adapt and differentiate themselves from their competitors to remain competitive and relevant.

Strategic Partnerships and M&A

The digital engineering services industry is competitive, and service providers consolidate through mergers and acquisitions to expand their capabilities, enter new markets, and gain a larger market share. They also partner with startups and other players in the ecosystem to develop new capabilities and technologies to better serve their customers. This reflects the evolving nature of the industry and the need for service providers to continuously seek new partnerships and growth opportunities to remain competitive and meet the evolving needs of their customers.

Innovation Is the Key to Success in Digital Engineering Services

In the digital engineering services industry, service providers need to invest in innovation and R&D to remain competitive as new technologies emerge. Technologies like the metaverse and blockchain are garnering interest for enabling new business models and revenue streams. Service providers must adapt to changing client demands and explore co-innovation and value-creation partnerships to develop comprehensive and integrated solutions. Joint ventures, strategic alliances, and co-innovation programs allow service providers to leverage their expertise for growth and value creation.

The HFS Horizons: Digital Engineering Service Providers, 2023 report highlights the value-based positioning for 25 service providers: Accenture, ACL Digital, Akkodis, Ascendion, Bosch, Capgemini, Cognizant, Cyient, EPAM, Globant, HCL, Hitachi Vantara, IBM, Infosys, LTIMindtree, LTTS, Persistent, Publicis Sapient, Softtek, TATA Elxsi, TCS, TechM, UST, Virtusa, and Wipro. It also includes a detailed profile of each service provider.

HFS has successfully road-tested the capability with several research customers, who universally declared their whole research experience had been transformed. “It was like the research had come alive, and I was actually living it,” stated one customer. “I asked about the Metaverse and finally understood that it won’t be anything until Web3 is incorporated”.

To help customers navigate the HFS Web, HFS has developed an Avatar called Hillary, based on the firm’s popular Horse logo:

“With GPT, if you win, you win. If you lose, you still win”, stated HFS CTO Jake LaMotta. “When we tested Hillary with our customer focus group, we discovered our customers wanted to ‘Holler for Hillary’, so we have opted for a non-binary horse to guide everyone. We think this is going to be very popular.”

Another HFS customer, Tony Montana, was not quite so convinced. “Why do I need a damn horse to tell me about UiPath’s long-awaited admission that RPA is dead. Everyday above ground is a good day.”

HFS CEO Phil Fersht, commenting on the launch, added, “We disrupted with free research and loads of brash views on the market. Now we’re disrupting with a hollering horse. It’s what I dreamed of as a young entrepreneur. GPT-6 is the future, and it’s part of us now.”

2022 was the year where many peoples’ lifestyles trumped their commitment to their jobs; however, that attitude today might just get you the sack.

Just when it seemed that a hybrid work model, which is primarily home-based, had settled in as the status quo, the global economy enjoyed its post-pandemic bounce, and people were coasting along in their cozy hybrid habitats; 2023 hit us with a thumping jolt.

Massive tech layoffs, back-to-office mandates, a highly-uncertain economic and political climate, and an epidemic of banks almost collapsing dominate the headlines, and suddenly the workplace power dynamic has shifted squarely from the jaded employee-fuelled Great Resignation to something resembling a great workplace freakout.

In the current challenging economy, many employers are pointing fingers at remote workers as a reason for underperformance

There are many high-profile organizations now mandating in-office policy that is more “office-first” than “remote-first”. For example, Disney has mandated four days a week in-office and General Motors and Starbucks three days a week at their main headquarters and regional centers. Social media firm TikTok has mandated two days per week and threatened employees with termination if they do not comply. Many more enterprises are following suit, with three-day-a-week in-office mandates becoming commonplace. Moreover, the proportion of remote jobs being advertised on LinkedIn has decreased from a high of 20% a year ago to just 13% today.

Net-net, work-from-home entitlement is out the window, and uncertainty is high across the board. Our recent study (with the support of Unisys) of 2,000 employers and employees across the U.S., U.K, Germany, and Australia laid bare all discrepancies between staff and managers’ perspectives of hybrid work and also pointed to some ways to bridge the gaps and avoid the pitfalls that this freakout is threatening.

Hybrid work is breaking down, but finding that right balance is like walking a tightrope

While the power pendulum has swung back from employee to employer, enterprises struggle with keeping their employees happy while demanding the motivation, presence, and productivity that business performance requires. Our study showed employees are much more confident in hybrid work, with over half indicating they work in a ‘very effective’ hybrid environment, compared to only 1/3 of employers.

Employees reported enjoying the work/life balance that hybrid affords, but managers struggle to know whether the staff is engaged and productive. Employers are also struggling to justify real estate investments, high-security risks for remote work, and a lack of collaborative culture. Enterprises want to retain top talent, but not at the expense of financial results. Case in point, to kick off Meta’s “year of efficiency,” leadership used poor employee evaluations to try and weed out the low performers before announcing its 10,000 staff layoff last week.

Poor IT experiences and security setbacks are threatening staff efficiency and morale

While the pendulum may be swinging back toward in-office protocols, the reality is that hybrid, in some shape or form, is here to stay for the foreseeable future. Our study found some very specific pain points that employers must address to improve hybrid functionality. One mammoth issue we found is that 49% of employees lose between one and five hours of productivity per week dealing with IT issues. Not even half of employers are not measuring productivity loss due to IT support issues, meaning many are woefully unaware that their staff are losing this much time in the week. And cybersecurity, while the top enterprise concern for 2023, poses another major issue impacting worker productivity. 1/3 of employees report their ability to work effectively being negatively impacted by security policies regularly. The survey showed that positive IT experiences are a main factor in employees’ choice to leave or remain with a company; employers must provide a smooth experience or risk losing staff.

These issues are not insurmountable. Making investments in systems and technology that can proactively identify and quantify IT issues before they impact users can go a long way to improve workplace efficiency (about half of the employers surveyed currently have these in place). And 92% of employees report that they are willing to share more data (such as app/device/network usage and performance) if they can receive more proactive IT support in exchange. This statistic points to a win-win scenario if employers have the foresight to invest in systems that will measure and predict these issues.

Investing in EX: empowerment, recognition, and flexibility trump the old motivators

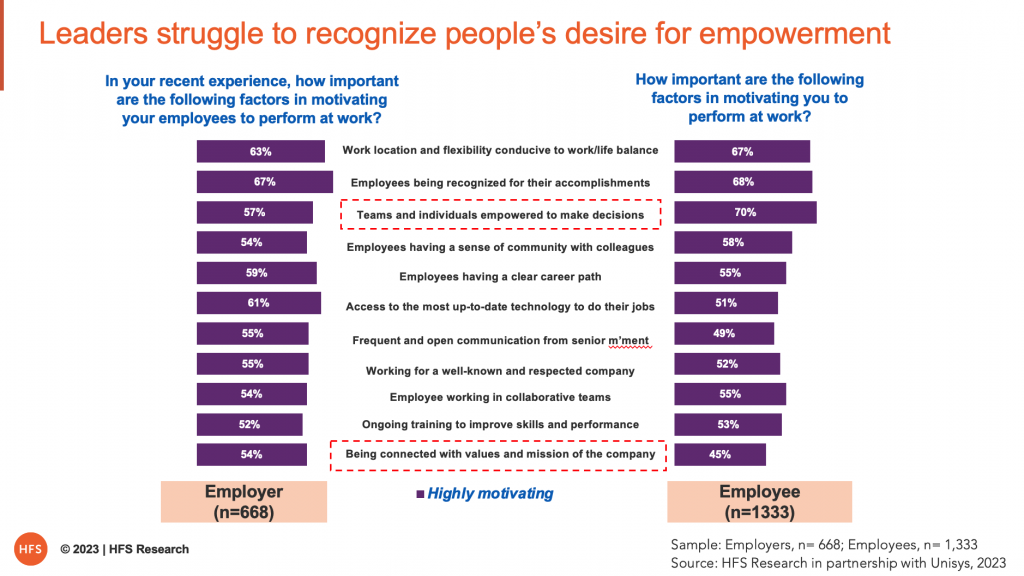

We covered some of the tactical issues impacting experience, but culture and engagement have a huge impact on how employees perform and are motivated at work. Any decent leader knows that EX is important, but do they know what their employees need and how to deliver on that? What motivates employees vs. what their managers think motivates them is quite a chasm across several key areas, particularly with employers not recognizing the importance of empowering employees to make an impact:

Employees are much more focused on their ability to have an impact and be recognized than the corporate brand

Employee motivations have changed, and employers need to pivot to enable better EX. The whole in-office culture was much more about belonging to the big corporate brand where you got a window cube when you got promoted. Now it’s less about the big company prestige and more about autonomy to make decisions, the recognition of doing your job well, and the flexibility to manage work/life balance. The big company rhetoric about mission and value is actually at the bottom of the motivational factors. Clearly, enterprise leadership is struggling to resonate with staff, many of whom must be losing their pride and identity with mothership as they lose touch with in-person interaction with their colleagues and managers.

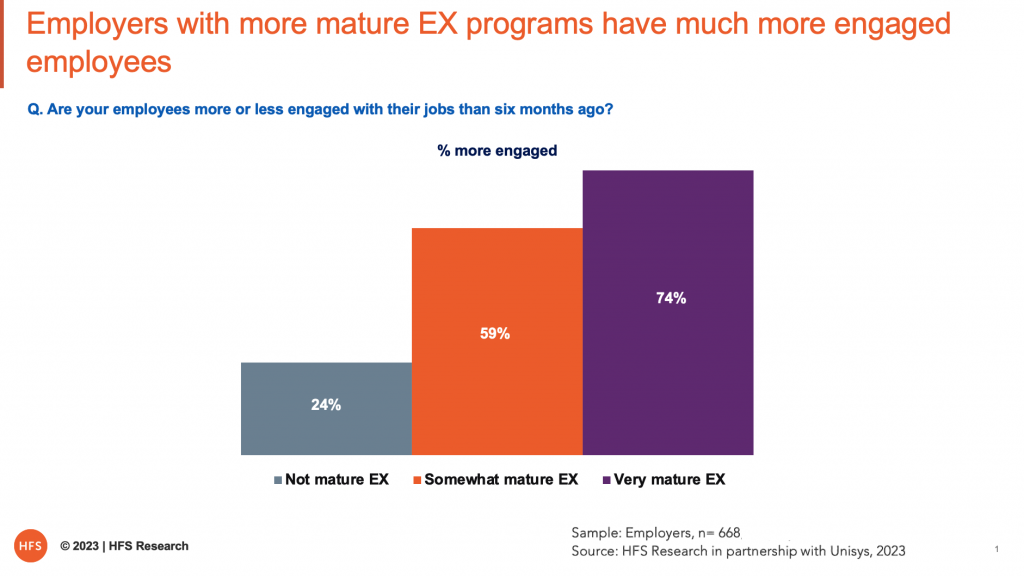

So how are companies investing in ways to better understand staff and deliver on their needs? Enter the EX program: including specific methods and metrics to measure EX, a centralized function that measures and informs EX policy, ways to solicit and incorporate feedback and manage against business outcomes, to name a few initiatives. Companies with very mature EX programs find their employees more engaged at a rate of 74%, compared to those with somewhat mature EX programs (59%) and immature EX programs (24%) (Exhibit 2). What’s more, employers and employees agree that EX programs also have a strong impact on business outcomes, including productivity, customer experience, and even financial performance.

The Bottom Line: Invest in creating the right conditions to shift from employee engagement to employee empowerment. You must understand employee frustrations and motivations to make hybrid work effective in this next era of the digital workplace.

The Great Resignation is in the rearview mirror, but we could have a messy freakout ahead if leaders don’t prepare accordingly. Many employees are increasingly citing an “edgy” culture is unsettling their enterprise, where most staff have no idea if layoffs are imminent and which staff will be targeted. We are not far from a Great Freakout engulfing enterprises as banks struggle to cope with increased interest rates, tech firms are radically addressing their cost structures, staff wages are not aligned with the current inflation rates due to a tough economy, and firms grapple the unprecedented situation of a shortage of low-income workers.

Last year there was a mistaken belief that by getting people the ability to work from home, we have achieved hybrid work, but our study shows we have not really figured out hybrid work. The good news is that there are enough synergies between employer perceptions and what employees want to create much better experiences; it is a matter of informed planning and execution to capitalize on the positives. The data is clear that investing in EX leads to better employee engagement. Tying this engagement to business outcomes is the next frontier and a critical one to brace for the uncertain days ahead in 2023.

In addition, companies have to address the cultures they want to create – and fast. They need to instill more urgency into their workforce and ensure their workers, whether remote or in the office, are accountable and still take their jobs seriously – and an effective EX strategy will go a long way to creating and maintaining that culture and settling employees’ nerves, providing your leadership takes it seriously and you have an empowered executive to drive it.

The days of hiding in our caves are over… it’s time to get out and face the world and fix our businesses. What worked in 2019 may no longer work in 2023, but if we don’t pull our teams together, we may find that out too late… and then it will be time to freakout!

A decade on from the trials and tribulations of IBM Watson, IBM unveiled its multi-model and multi-cloud Watsonx to drive AI-first enterprises – what we are calling “The Generative Enterprise” at HFS.

A decade on from the trials and tribulations of IBM Watson, IBM unveiled its multi-model and multi-cloud Watsonx to drive AI-first enterprises – what we are calling “The Generative Enterprise” at HFS.

One of the most talked about sessions at the HFS Super Summit in New York was my on-stage 1-1 with one of the IT and business services industry’s most revered voices,

One of the most talked about sessions at the HFS Super Summit in New York was my on-stage 1-1 with one of the IT and business services industry’s most revered voices,