Am very flattered by how leading creative marketing strategy firm Antics Marketing Solutions has positioned HFS Research. Our simple goal is to empower your organization to be the disruptor in your industry 💪

As we collect our thoughts for the year and prepare for the next, one area I never want to compromise on is my desire to speak the truth and never be muted by corporate propaganda and pay-to-play bribery. Let’s just call it what it is, folks.

When I founded HFS 14 years ago, all we had was our honesty and reputation for calling a spade a spade. The more we kept true to this reputation, the more valuable our brand became, and the more money companies were prepared to pay for our insight and expertise. This was a terrific way to do business and feel proud of our work.

HFS does not do business with a handful of software and services businesses, which “canceled” us because we put out research that did not make them look as amazing as they were trying to portray themselves or we just called them out for poor practices. We also turn away business from several suppliers as we do not want money purely for puffing up brands with no proven research and customer evidence to back up the claims. These firms choose to work with other firms that are clearly more flexible to bend to their dollar bills. Like has anyone ever received an “award” in this industry they didn’t have to pay for? Like ever?

I won’t embarrass some of these firms here, as I do not want to play that game, but they know who they are…

In 2024, I will push my team even harder to be brave and speak the truth in this world of bullish*t marketing, relentless hype, blatant lies, and swirl of nonsense. We have more than doubled HFS since 2019, so there is one lesson to take away from this: Truth sells!

Sandeep Dadlani, Executive VP and Chief Digital and Technology Officer at UnitedHealth Group (UHG), the world’s largest healthcare enterprise with diversified businesses, has a long and deep technology experience across multiple industries on both the supply and demand side. His early days at UHG coincided with the explosion of GenAI on the global stage and has been shaping some of the thinking and doing for him.

In speaking with Sandeep, it is clear about the methodical and structured approach he is driving at UHG could define how healthcare leverages the latest technology miracle.

Our most recent candid interview – as part of our GenAI Leaders Series – is to learn how Sandeep fashions GenAI’s use and ways to realize its potential in healthcare and potentially beyond.

Pragmatic, excited, and responsible: the steps to get it done

While UHG is the world’s largest commercial healthcare enterprise with ~$360B (Sep 30, 2023) in revenues, it is also amongst the largest enterprises by workforce of some 440,000 clinicians, technologists, and market-facing professionals. An enterprise of this size with even greater implications for the health and well-being of over 150 million people must be deliberate when exploring new technologies. That is precisely the approach that is being considered while the world is abuzz with GenAI.

A pragmatic approach is to find the problem(s) to solve as the first critical step in being able to address it with any new technology. At UHG there is a bottom-up effort at identifying use cases that have led to piloting some 500 use cases while the top-down identified some 14 use cases. The approach to identifying the top-down use cases was an enterprise celebratory event called Tech-Tank involving tens of thousands of employees. While ideation and spitballing are part of the effort, UHG took a hard look at the business case and the ability to scale those use cases in their selection. Given the size of UHG, scaling means very different, and early indications are very encouraging.

The use cases are generally in the administrative realm of the value chain, which historically has accumulated suboptimal processes and is a rich target for technology transformation. These low-hanging fruits include processes used by thousands of call center agents to summarize their interactions with United’s members.

“…call summarization is a simple thing but has eluded the industry for a while but really eases the work for our call center advocates and has them focus on caring for the person who is calling” – Sandeep Dadlani

Never mind the cape GenAI wears, just focus on its superpowers

“…great synthesis and data extraction from structured and unstructured fantastically well, content generation very well and automates code writing…” Sandeep Dadlani

UHG’s selection of use cases keeps clinicians in the loop to ensure that they can practice at the top of their license and not replace them. This extends to all processes that may or may not include clinicians, that a human is always in the loop to help improve the outcomes and it is done responsibly.

And so, the notion of responsible AI does not have a stronger motivator than the use of GenAI in healthcare. In the context of life and death implications, be it for diagnosis, choice of therapies, or care delivery, responsible AI must become table stakes in action vs. narrative. There must be added urgency to ensuring fairness, eliminating bias, and clear explanations of results.

GenAI’s iPhone moment is more impactful than the Kodak moment

IT services are experiencing a flat revenue trajectory in 2023 after a quarter of a century of sequential growth. As a result, most of them are investing in GenAI to fuel the next era of growth. However, the philosophy of investments in healthcare could have long-term implications. There are two schools of GenAI investments in the context of the triple aim of care (reducing the cost of care, improving health outcomes, and enhancing the experience of care);

Positively improving the tripleaim of care by empowering clinicians to practice at the top of their license, incorporating ambient tech to be virtual caregivers, or accelerating drug discovery. This philosophy will take longer to pay off but will be sustainable and result in strong growth.

Maintaining the status quo by following legacy paradigms, including labor arbitrage, could see an immediate improvement but is unlikely to be sustainable.

The potential of GenAI is like the launch of iPhones in 2007 and the realization that it could not only replace the 36 pictures of a Kodak film role, but one could store thousands of pictures on the device. The notion of experimentation became common because one did not need to be precise in the shooting of a picture, photography expanded to everyone with a smartphone, and functionality expanded beyond pictures. In a similar vein, expect GenAI to deliver more technology faster with better outcomes.

Yet before IT service providers run the idea to the banks, it is important to address the improved productivity and how that will be shared. Early indicators suggest that we should expect 30-70% productivity gains, and enterprises expect that the productivity gains will be shared with them by service providers. Providers who figure out how they realize productivity gains and find an equitable way to share them with their employees and clients will likely prosper.

The Bottom-Line: A future of elevating work beyond the mundane, learning continuously and faster, while GenAI becomes a copilot aiding in better decision-making and improving outcomes many times over.

GenAI opens the door to interrogating data differently and smartly, leading to using data (structured, unstructured, images, audio, etc.) in ways perhaps only imagined. In a future where we are going to experience an acute shortage of clinicians, GenAI, being an able aid to a clinician, will help with speed and accuracy of diagnosis, reduce administrative burden, ensure gaps in care are addressed by engaging with health consumers, and the list goes on. The sky is the limit with GenAI, and that has some extraordinary possibilities in healthcare…assuming we make the right choices and deploy GenAI against the right problems.

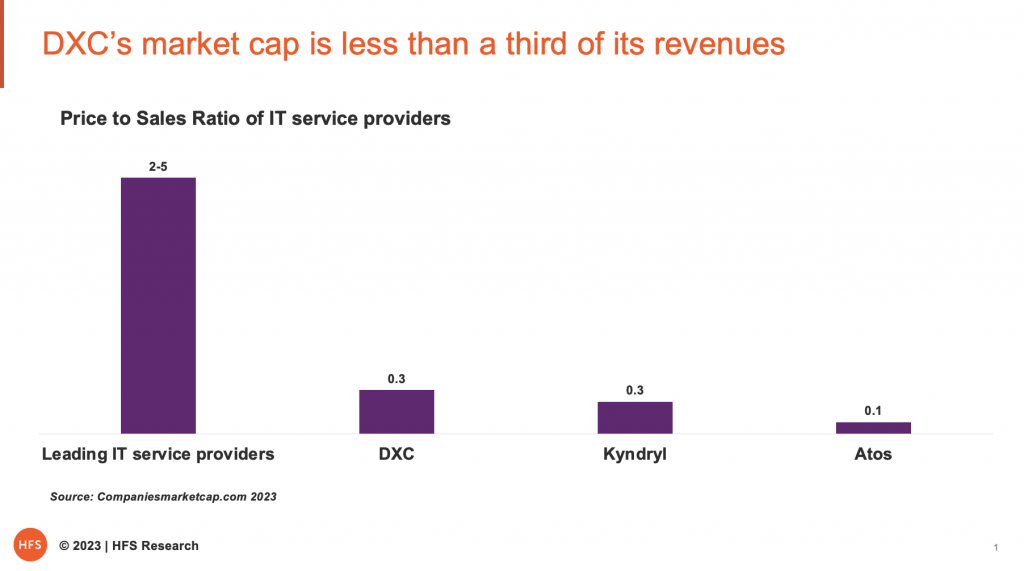

DXC Technology’s latest play is to bring Raul Fernandez off the bench as the new interim chief and move on from a difficult four years under Mike Salvino, who’s passing the torch. But when you look at the challenges facing this firm, you might just come to the conclusion that not even God can turn this one around.

Let’s not kid ourselves; this isn’t your usual passing of the baton – it’s more like handing off a ticking time bomb. The company’s market value is literally running on fumes at barely a third of its revenue numbers. And that’s not just a hiccup – it’s a full-blown identity crisis:

Let’s not forget our trip down memory lane from four years back, where we laid out the gauntlet of challenges and opportunities for DXC (remember this blog?).

So, where did Mike Salvino go wrong?

DXC made zero acquisitions under Salvino and gave all their money back to stakeholders to prop up the share price. He could have made acquisitions to bolster strengths in growth areas such as cloud migration, AWS services, analytics, Azure, etc., or double down on industries where DXC could have real differentiation, such as insurance, private healthcare, energy, and manufacturing. The Luxoft analytics business had real potential, and little was done to build on the firm’s insurance software and IP.

Sold a lot of pieces but didn’t build new capability fast enough. For example, its US State and Local Health and Human Services Business (Medicaid) was sold to Veritas Capital for $5 Billion, but that money was never reinvested.

Stabilizing delivery on infrastructure doesn’t mean people will buy transformation. Just look at the similar price-to-sales ratio to Kyndryl, another firm struggling to sell transformational services tied to its commodity infrastructure business.

Very limited diversity on the leadership team. DXC’s leadership is almost all US men… diversity wins deals, and many enterprises want to work with firms with a strong gender and cultural mix.

Very limited stability on his leadership team. Salvino hired and fired at least 15 senior leaders and churned through 3 CFOs in 4 years, one of whom publicly sold off his stock.

What challenges face Raul Fernandez?

Fight back in a cut-throat market. We’re in an IT services market that is suffering from flat to negative growth, and even the most successful IT service providers are reporting low single-digit growth at best (Accenture reported barely 3% growth yesterday). What Hail Mary can Fernandez conjure up to convince enterprise leaders to take a bet on this train wreck of a company? When you have aggressive outsourcing juggernauts, such as Accenture and TCS, to contend with, where can you realistically play when you’re this far behind?

Find some way to survive the GenAI revolution. Then there’s GenAI, the Chicxulub meteor that will result in wiping out the dinosaurs in the IT services industry. Will DXC dodge this extinction-level event, or will they be left behind like the dinosaurs? With Fernandez at the helm, it’s do-or-die time, and we are watching closely to see if DXC can pull a phoenix and rise from the ashes.

Find a raison d’être for DXC to reinvent itself. DXC has not been able to create a true brand association and find its mission. Financial restructuring to bring it back to life is also going to be hard. It has not even been able to find a buyer for its BPO business that it has wanted to divest for several years now. Simply put, there is no strategy, and investors have little confidence left in the firm. Maybe Fernandez will find a transformation acquisition or two to redefine exactly what DXC is and create a path forward to long-term survival.

The Bottom-line: Raul may not be God, but he needs to find a saviour

Raul Fernandez is only interim chief, so his task is most likely to search drastically for a path to salvation for the firm and install a dynamic leader to take them there. This may be the toughest tech CEO turnaround task since Steve Jobs returned as interim Apple CEO in 1997, faced with the task of making Apple profitable again after losing over $1bn in 1996. How did he do it?

1) Rebuilding the core products and value,

2) Prioritizing the customer experience,

3) Collaborating with rivals, and

4) Reinventing the company culture.

Perhaps these four areas are the best guide to follow…

In a recent Fireside Chat, I had the pleasure of sitting down with Nigel Vaz, the visionary CEO of Publicis Sapient, to delve into the burgeoning world of generative AI (GenAI) and its profound implications for the business landscape and the broader world at large. As we unpacked the complexities and potential of AI, Nigel’s dual sense of excitement and caution resonated with the current sentiment in our industry, as the GenAI hype and fear are reaching a fever pitch. Companies like Publicis Sapient are thoughtfully leading the GenAI charge by developing toolsets and talent, evolving their mindsets to embrace a culture of learning and unlearning, and being mindful of the risks and downsides so they can help their clients do the same.

From predictive to generative: GenAI is enabling a new wave of creativity to drive business transformation

Nigel’s enthusiasm was palpable as he described how GenAI goes beyond traditional predictive AI—potential outcomes based on data—and adds creation. This means, Nigel says, you get a powerful combination of decision-making and creativity, which will be a powerful catalyst for enterprise transformation. It could dramatically affect enterprise efficiency and growth, particularly how companies create new products, services, and experiences.

His excitement is tempered by a healthy dose of anxiousness fueled by ethical and regulatory issues and concerns related to how companies think through re-inventing business in the context of GenAI. Much like the advent of the internet and the mobile and social waves that followed, enterprises won’t get everything right with GenAI right off the bat. It’s creating a need to consider the risks and downsides as companies examine how this will play out within their organizations.

GenAI is here and now, and production at scale is on the horizon

At HFS, we’re cutting through the GenAI noise to understand what action is truly happening and what’s hype. Nigel tells us the difference between now and one to two years out is seeing GenAI move from primarily experimentation and prototyping to production at scale. He currently sees very real GenAI progress, particularly in content generation, software development, language translation, data augmentation, chatbots and conversational AI, and product design. These experiments are becoming increasingly optimized, meaning that proofs of concept get into production much faster. For example, in data augmentation, synthetic data based on an organization’s internal inferences can be used to train AI models to eliminate problems inherent in generic language models, meaning they can move to prototyping much faster. Publicis’ software developers now have tools such as a proprietary code library for all to contribute, significantly speeding up coding time. All of this means we’ll have a greater scale of GenAI examples in production at an increased level of scale in the not-too-distant future.

Perpetual evolution requires constant learning

To embrace these new tools and ways of working, Nigel urges a culture of perpetual evolution within organizations. Leaders must champion a cycle of learning, unlearning, and relearning to stay relevant. The strategic vision is paramount, but so is the seamless integration of AI into the business fabric. It’s about preparing for an AI-infused future where technology and strategy dance in lockstep. From a talent standpoint, everyone needs to learn the tools, accept that the tools are constantly changing, and get ready to learn again. Taking pride in being able to adopt new tools and learn quickly versus having knowledge is a cultural mindset shift. As Nigel says, Gen AI demands people who are “learn-it-alls” rather than “know-it-alls.”

So, how do you influence your people’s mindsets to embrace change? First, says Nigel, it is important to look at GenAI in the light of digital transformation, which means it is about way more than implementing new technology. You have to start with a vision of how you want things to look in the future to re-imagine how your business looks in the context of Gen AI.

This clear vision, which Nigel likens to a “North Star,” must be clearly articulated to employees so that they have the impetus to develop a common set of platforms and toolkits for people to experiment with. Publicis Sapient is creating these “sandboxes” of platforms and toolkits while being clear about the priority focus areas. The goal is to create a culture that embraces iterations as technology advances and goals and outcomes are achieved or missed. This is a constant evolution without a beginning or an end. At Sapient, Nigel and his team know that if they don’t embrace this change in mindsets and way of working themselves and embody the transformation, they won’t be able to help clients do the same.

Developing the right strategies to mitigate ethics, data privacy, and security risks is critical to success

While it’s easy to get excited about potential opportunities and cultural shifts GenAI offers, the risks are very real. Not having a robust strategy to evaluate and address these risks is a recipe for failure or even disaster. Ultimately, we must control AI in a way that is responsible, fair, and aligned with societal values. Nigel outlined the following key issues to consider:

Develop oversight and understanding of ethical and legal considerations. Companies need a framework to think about data privacy and security to address data protection regulations and ensure responsible AI guidelines and transparency in decision-making. This is a fundamental cornerstone for a safe and effective AI strategy.

Think about data in the context of bias and fairness. There’s a big issue around bias and fairness because the training models rely on potentially biased data. Particularly for hiring or bank lending, it’s essential to consider the implications for potential bias and carefully examine the training data for potential bias to eliminate it.

Enable transparency in AI systems. The “black box” nature of some AI systems can make it difficult to understand their decision-making processes. Ensuring transparency in AI models is essential for accountability, regulatory compliance, and ensuring you are building on datasets you want to propagate versus potentially biased data to avoid.

The future of tech and humanity is a platform effect fueled by increased computing power.

While GenAI is a transformative tool, like many other emerging technologies we’ve seen, it is only optimized in combination with other tech; Nigel sees an emerging “platform” effect. Technology such as 5G, cloud, and big data act as one layer of the platform, building on the internet and mobility, and now GenAI is an added layer for greater value. He predicts that the third wave to further expand AI to its full potential will be exponentially greater computing power, such as quantum. Adding this tremendous power will allow us to process and train models significantly faster, enabling changes such as the ability to focus on bigger problems, develop hyper-real augmented environments, and advance physical robotic capabilities.

Nigel’s future view of the platform effect is very optimistic for humanity in general; first, he mentions the increased ability to tackle big planetary and social issues like climate change and food security. He also thinks the platform will supercharge virtual and augmented reality, characterized by a significant increase in immersiveness and interactiveness, making the distinction between physical and digital experiences increasingly seamless. Lastly, he anticipates advancements in robotics and automation to extend the digital automation we’ve seen into the physical world, overcoming current physical technological limitations.

The Bottom-Line: Design your future state “North Star” and align your firm to navigate to it efficiently

Inevitably, GenAI’s evolution will not just change business; it will change how we live and work. It could also significantly impact our lives and the planet, but we have to shift our mindsets and be wary of the pitfalls to get it right. GenAI has ushered in the potential for us to become more efficient—and more creative and impactful. Nigel reminds us that we must develop a culture that embraces adopting new and changing tools, applies that new knowledge appropriately to realize the “North Star” vision, and remains willing to evolve once we get there.

Cognizant has made a significant investment in ServiceNow capabilities with the acquisition of Thirdera, one of the much-admired deep consultancies in the space. Eleven months into his leadership, Ravi Kumar has made his first major acquisition, which sets his stall out for large transformations, of which so many are built on a ServiceNow foundation. The big question now is whether Cognizant can absorb the new talent at its disposal to paint a real picture of technology arbitrage for ambitious clients wanting “more for the same” as opposed to “more for less.”

So, who better than our resident ServiceNow guru, Dr Tom Reuner, to share his viewpoint on the acquisition…

Despite the headwinds, ServiceNow continues to outgrow the market

There is an infectious enthusiasm across the ServiceNow ecosystem that has few bounds, even at a time when many organizations are grappling with the Digital Dichotomy of driving our cost while innovating at the same time. Looking at ServiceNow’s earnings (stock is up 65% this year), it is not difficult to see why the mood continues to be so bullish.

Despite the headwinds, ServiceNow continues to outgrow the market. If anything, it provides the building blocks to enable the Big Hurry to transform. Those engagements are around next-generation GBS, industry solutions, ERP modernization, and beyond – no longer just IT-centric implementations. (for details on the trends in the ServiceNow ecosystem, see: ServiceNow can become the digital foundation of the Generative Enterprise™.

Thirdera has the second-largest number of Certified Master and Technical ServiceNow Architects after Accenture

This provides the backdrop as to why we are hearing so much of late on potential M&A in that ServiceNow ecosystem. After months of rumors and speculation, Cognizant made the most significant move in the ecosystem to date by acquiring ServiceNow pureplay Thirdera. While not a household name Thirdera is the largest independent consultancy that adds significant muscle in the US but also expands Cognizant presence in Europe and APAC.

Perhaps the most important factor is that Thirdera has the second-largest number of Certified Master and Technical Architects after Accenture. This is crucial for being considered for complex transformations. On the other hand, its last acquisition of a ServiceNow pureplay has been a moderate success, and we are being polite here. Linium was meant to be a change agent for Cognizant, but not much is left of its culture. Thus, the key challenge for Cognizant is to learn the lessons and maintain some of the culture that has made Thirdera an attractive option in the first place. To assess the potential strategic impact, let’s peel back the onion. Let’s start with Thirdera, whose whole history tells the story of the development of today’s thriving ServiceNow ecosystem.

Thirdera was created in 2021 by PE Sunstone Partners by merging three acquisitions: Evergreen Systems, Cerna Solutions, and Novo/Scale, all focused on the North American and Latin American markets. Perhaps it shows my age, but the next move sounded like the Blues Brothers in the eponymous movie trying to “put the band back together.” Because Sunstone installed a management team that included CEO Jason Wojahn, who was the President of the ServiceNow Business Unit at Cloud Sherpas (formally Navigis, ServiceNow’s first services partner) – and after the acquisition of Cloud Sherpas by Accenture, the ServiceNow Senior Managing Director and Global practice leader there. Marc Talluto took over as Chairman of the Board, and he was the co-founder and CEO of Fruition Partners, acquired by CSC in 2015 (now DXC Technology). Many of the other leading executives have a history with these two companies.

Thirdera gives Cognizant global ServiceNow depth and breadth

Fast forward to 2023, Thirdera boosted its ambition to create a global ServiceNow pureplay through more acquisitions and achieved a presence in all key geographies. Thus, it maintained the cultural attributes of pure play whilst being able to compete with GSIs on scale. This is what sets them apart from peers like GlideFast, Plat4mation, Cask, or NewRocket. Furthermore,Read More

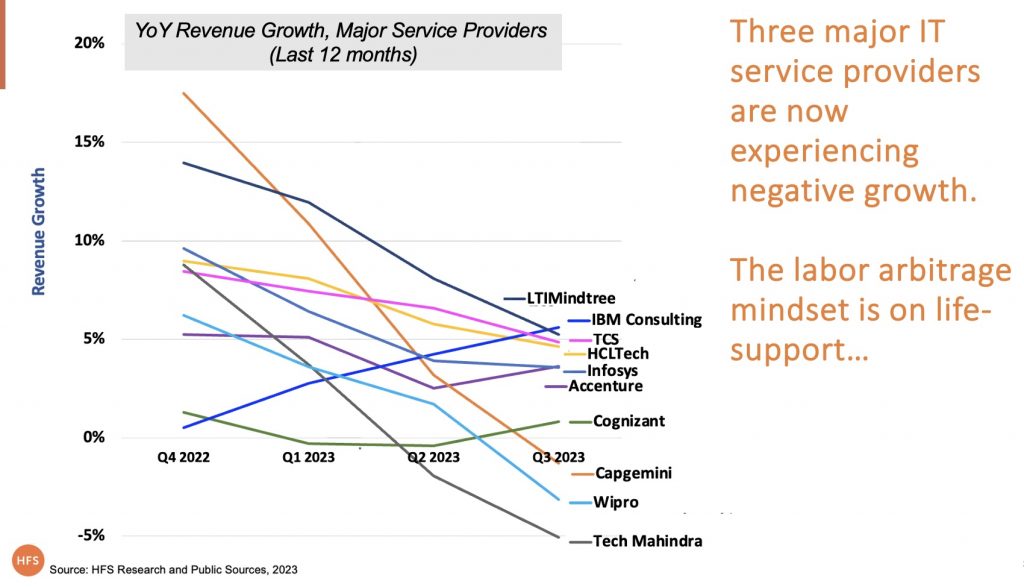

IT and BPO services have been on an incredible run for the last quarter of a century, enjoying the relentless double-digit growth of global delivery models fueled by skilled talent pools in more cost-effective regions of the globe.

Who’d a thought the Global 2000 would keep finding more and more reasons to keep spending more and more money on global service providers? Yes, they’ve had a lot of fat to keep trimming, but many have finally cut to the bone, and 2023 has seen a nosedive in growth from most of the major service providers:

Exhibit 1. 2023 has proven to be the great Reality Check for IT / BPO Services*

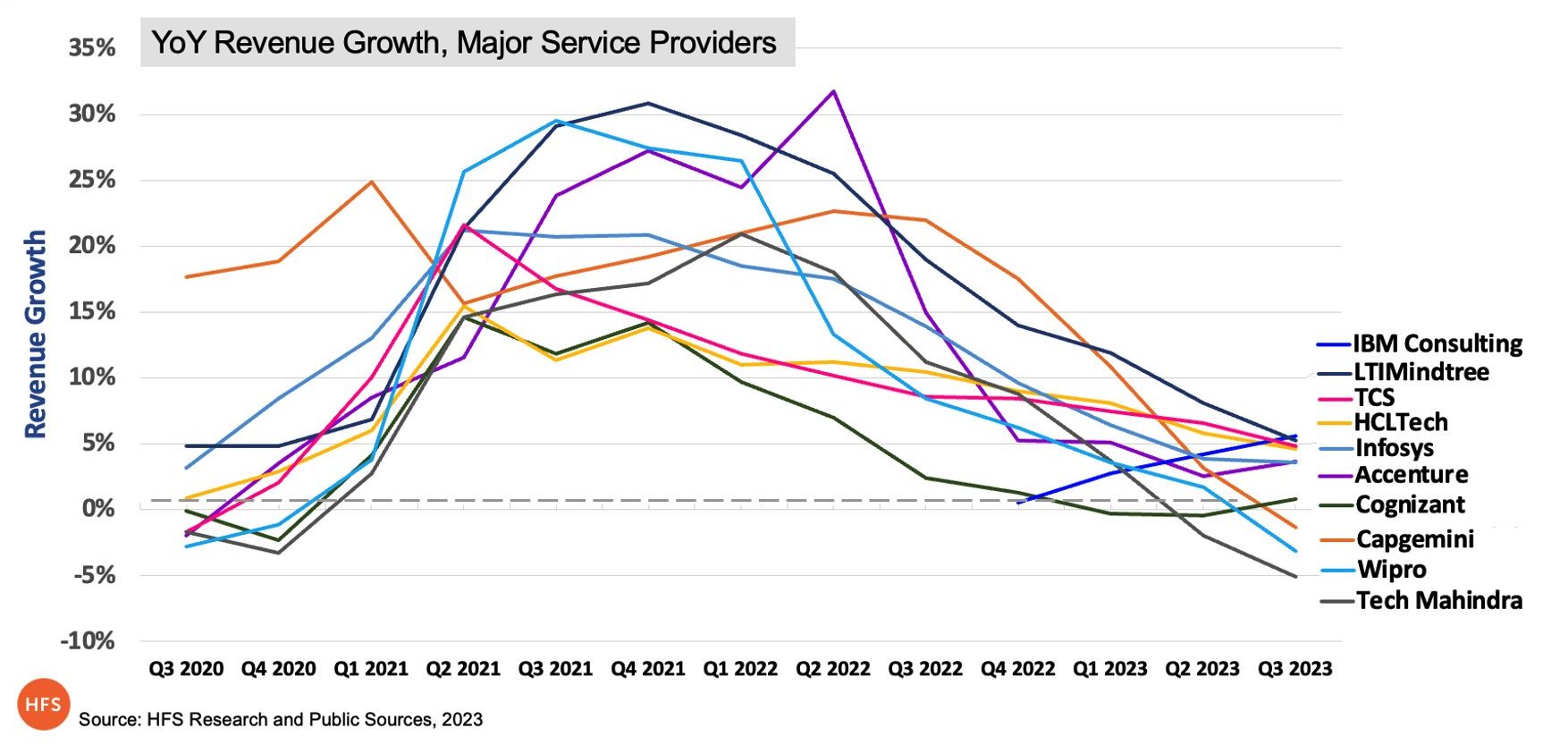

One can argue that the legacy labor arbitrage model was already running out of steam before the Pandemic, but the rush to the Cloud, driven by those pandemic-driven virtual business experiences, kept that spending on labor-intensive cloud migrations artificially high until everything came crashing down to earth this year:

Exhibit 2. The pandemic fueled the dying embers of Labor Arbitrage, but growth is flattening out

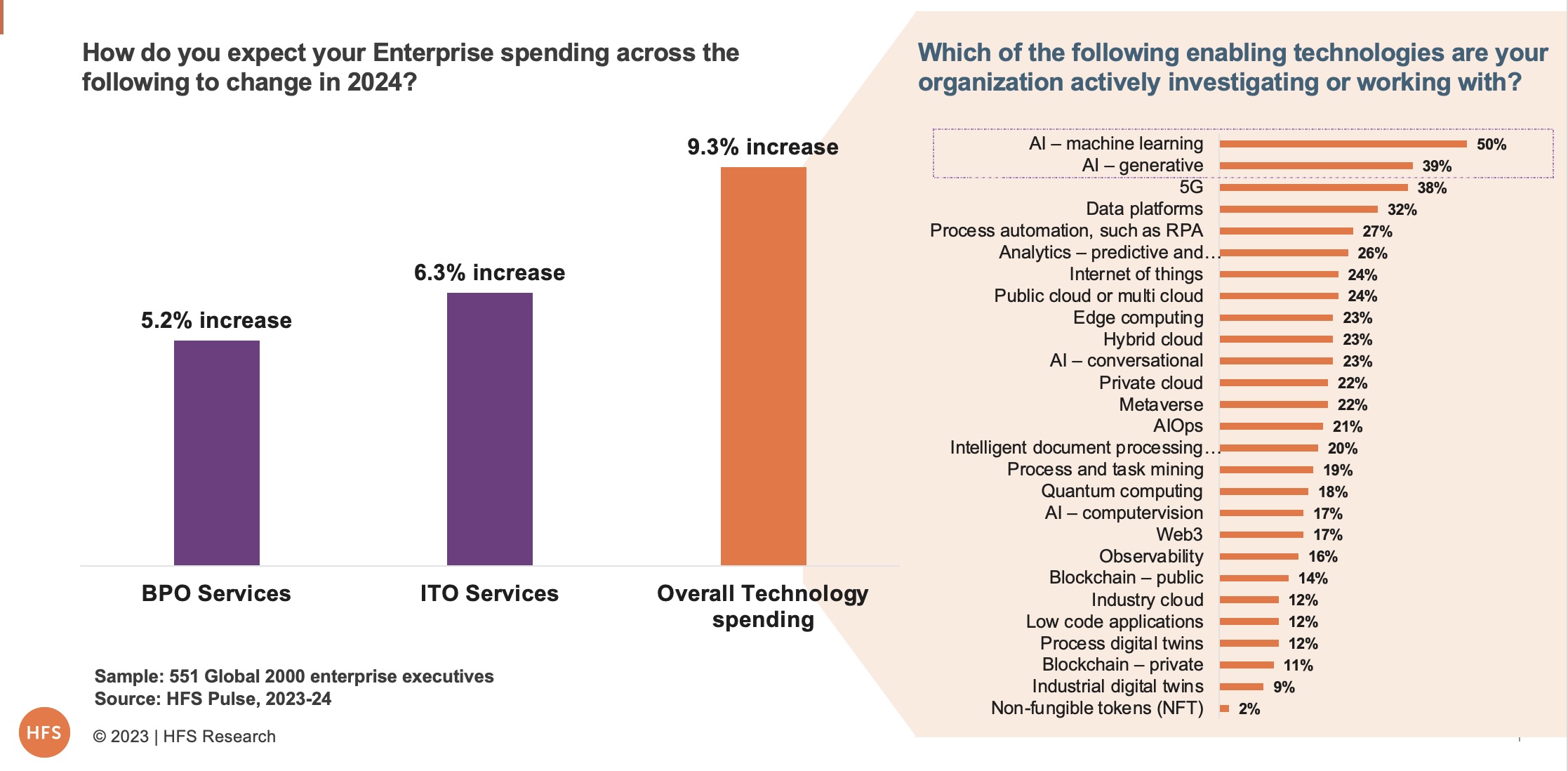

Our latest HFS Pulse data based on ongoing inputs from 600 of the global 2000 enterprises also suggests that labor-driven IT/BPO services growth is expected to be ~5% in 2024, and AI-driven technology spending is expected to increase at ~9% (See Exhibit 3):

Exhibit 3. Labor-driven IT/BPO services growth is expected to be 5%, but AI-driven technology spending is expected to increase at 10%

The industry has matured where most large enterprises (above $5B in annual revenues) have pulled the basic levers of offshoring either through in-house shared services and /or 3rd party service providers. And after playing for 3-5 years in the model, while there are incremental improvements that they can achieve, the transformational benefits start to diminish.

The reality is that costs are like hedges: they grow back after trimming, and the pruning shears are becoming blunt

Enterprises are running out of obvious places where onshore people can be replaced with offshore people, and they have no choice but to investigate new avenues of value that are less obvious. And those avenues are only to be found by exploiting technologies that can scale operations, provide rapid access to data that gives you a competitive edge, and grant you access to ecosystems to expand business opportunities. New technologies that enable you to run things faster, better, slicker, smarter, and cheaper than ever…

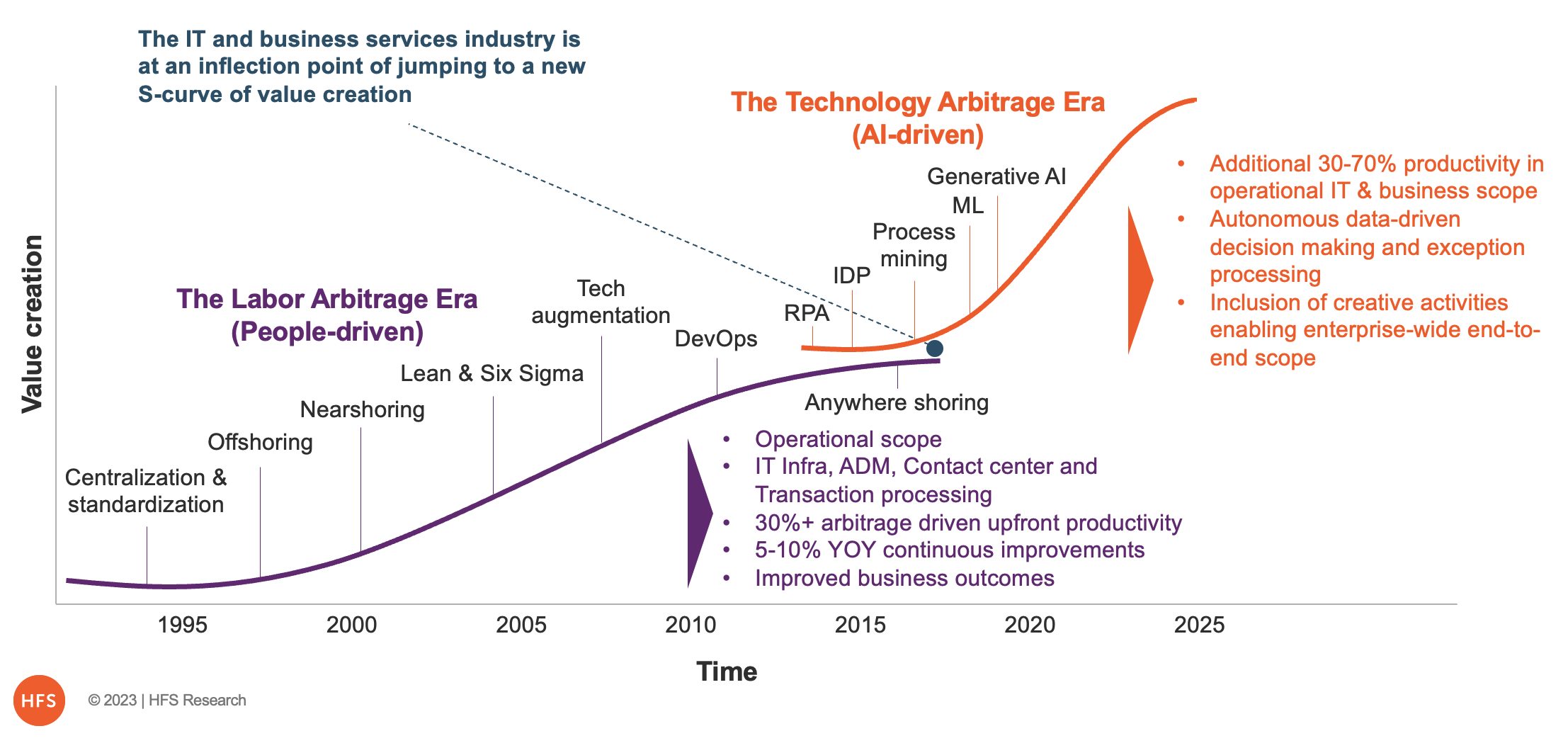

It’s past time for the IT and BPO Services industry to jump to a new S-curve driven by technology arbitrage if they wish to get back to another season of hockey stick growth:

Exhibit 4. The new S-curve of Value Creation will be AI-driven Technology Arbitrage

The “scale of technology partnerships” becomes far more important in the technology arbitrage era versus “the scale of people” in the labor arbitrage era.

The fundamental value creation lever in the legacy Labor Arbitrage era has been the centralization of people in a global delivery model. The fundamental value lever in the Technology Arbitrage era is all about architecting and orchestrating the rapidly changing technology ecosystem in line with the client’s business model.

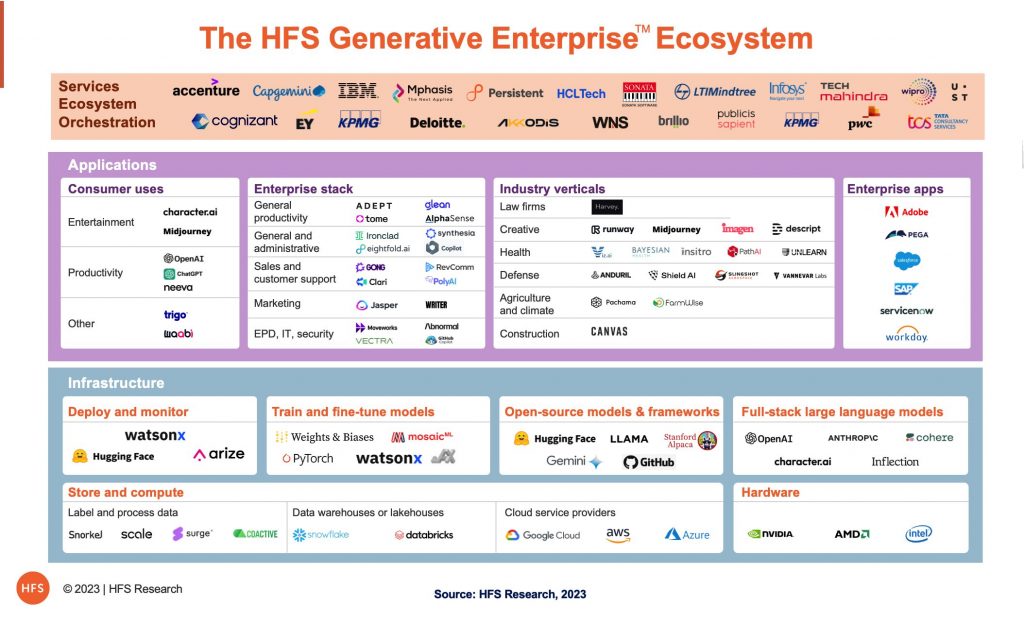

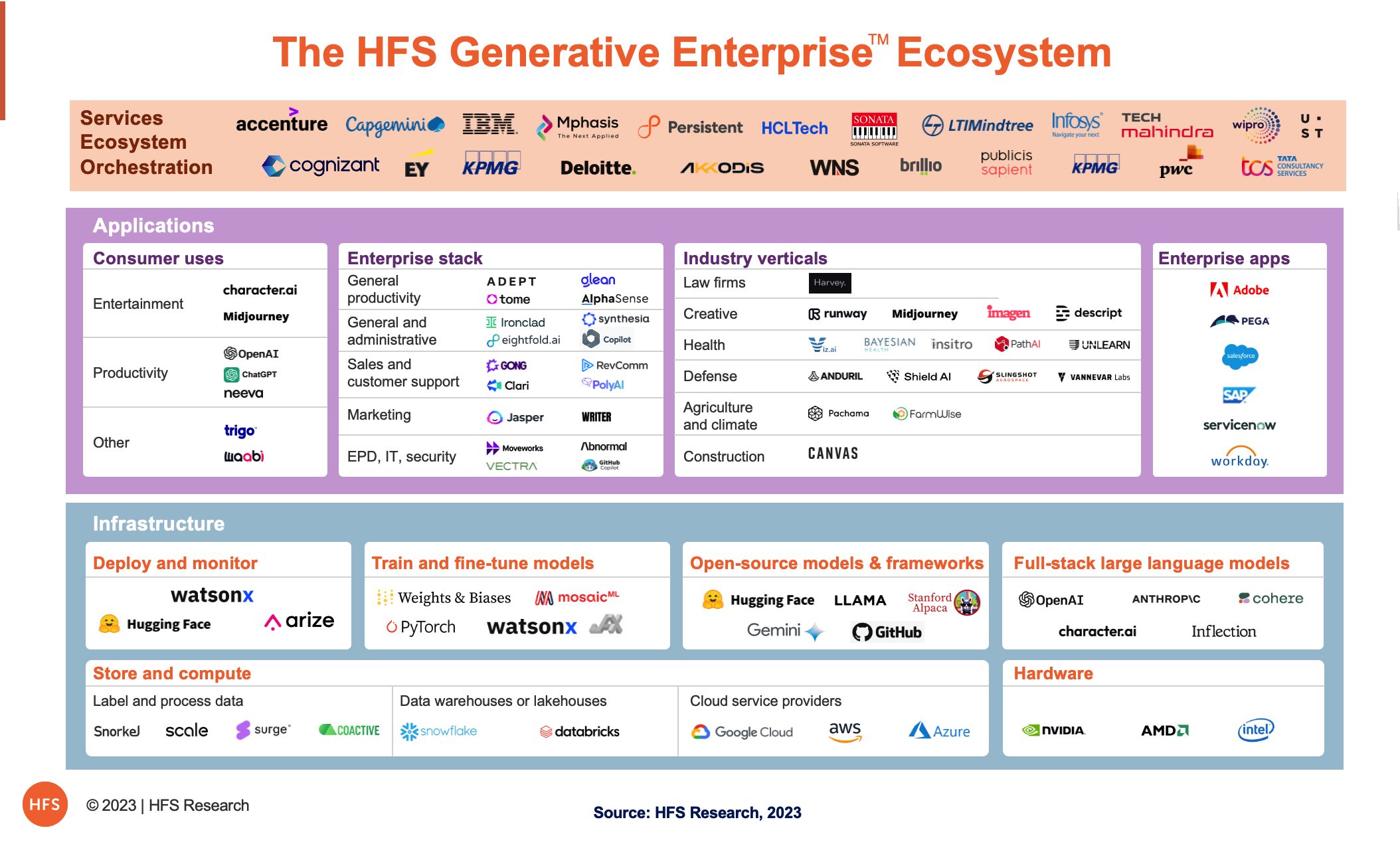

Let’s take the example of the rapidly emerging GenAI ecosystem (see exhibit 5) that an enterprise must build, manage, and keep updated on an ongoing basis as new players emerge, continually enhancing technology capabilities. This becomes too complicated and too costly very quickly, and consequently, the ROI becomes murkier.

Service providers have a significant value proposition to orchestrate this ecosystem to drive real business value for their core customers. Enterprises can’t exploit GenAI alone and need smart partners, which can really help them get ahead of the innovation curve. With GenAI, for example, there are real business pressures from the C-Suite to design AI capabilities that create genuine differentiation in the marketplace. Smart services firms that can engage at the senior level to bring their GenAI ecosystem to life will win in the emerging market, but they need to convince enterprise leaders to take a bet on partnering with them.

Exhibit 5: The technology ecosystem becomes too complicated very quickly (GenAI Ecosystem example)

With the advent of GenAI, this brand-new ecosystem is creating itself right in front of our eyes with new stakeholders that most enterprises will find difficult to engage and build relationships with. Ecosystem orchestration is a fundamental shift in the role that service providers can play in driving value for their clients.

The Technology Arbitrage era is not only about doing more with less but also generating actionable business value

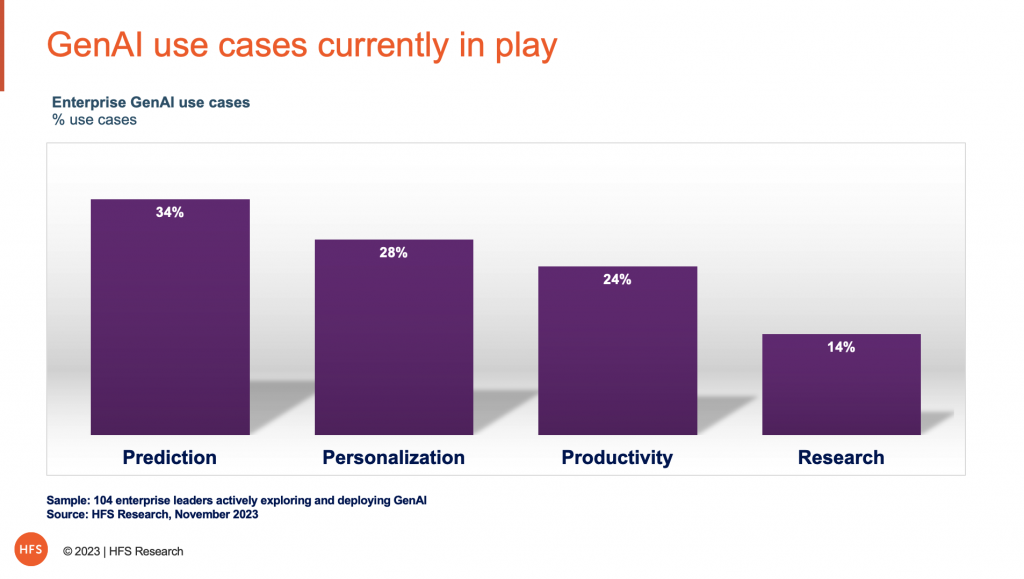

At HFS, we are wrapping up a research initiative where we reached out to 100+ enterprise leaders who are actually doing something credible with Generative AI and interviewing the executives actually leading the GenAI initiatives. Contrary to the popular media narrative, improving productivity is not the #1 use case for GenAI (see Exhibit 6); AI’s predictive capabilities and ability to personalize at scale are tickling the fancy of business leaders:

Predicting with Precision. The ‘Prediction’ theme emerges as the most popular and brings to the forefront use cases that deploy AI to anticipate, forecast, and devise estimations, playing a crucial role in strategic planning and decision-making.

The Age of ‘Me’. Personalization also dominates. Forget one-size-fits-all; we’re in the era of AI-driven, tailor-made experiences. The eminent theme of ‘Personalization’ has emerged as a dominant application area, underlined by use cases that harness AI to tailor experiences, content, and solutions.

Value isn’t all about Productivity. Productivity improvements must be augmented by Prediction and Personalization in the Technology Arbitrage era if they are going to drive real impact for enterprises. The legacy mindset of simply driving out cost as the core imperative has to change to a value mindset.

Exhibit 6: Prediction, Personalization, and Productivity: The 3Ps powering GenAI use cases for enterprises

Winners in the emerging Technology Arbitrage era will require strong business acumen.

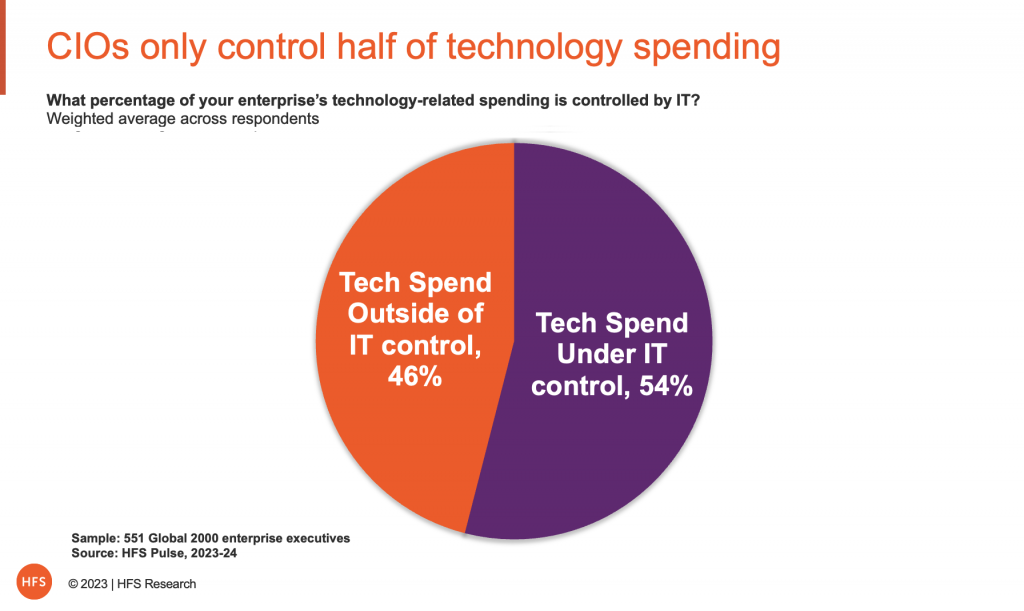

Nearly half of the new technology spending will be outside the CIO/CTO control – it’s with the business (See Exhibit 7). Past surveys before the Pandemic typically showed 70-80% of tech spending under CIO control, but the balance of tech power within major enterprises is clearly shifting.

However, our IT services industry keeps selling to the CIO/CTO. As traditional IT services growth flatlines, the IT service providers must develop a business narrative behind their technology services. For instance, every CPG company wants to go direct-to-consumer today – that is the challenge the business wants to solve. Now it’s obvious that the CPG companies will need to redesign entire business processes and integrate their data repositories in the cloud to make that intrinsic change in the business model. However, most of the current crop of IT service providers do not offer a solution to help them change their business model; they only propose how quickly and efficiently they can migrate workloads from legacy to cloud. This business acumen is exactly where Accenture outshines most other service providers, as it can redesign businesses to be effective in cloud ecosystems and manage them for its clients at scale:

Exhibit 7: CIO/CTO controls only half the technology spend

BPO service providers work with business stakeholders, so they should have more success in tapping into this tech spending. Right? WRONG! The BPO narrative has not changed for decades. Most enterprises leverage BPO for processing transactional, mundane, and frankly boring work. The tired old BPO value proposition is stuck with the labor model.

The first question when anyone discusses BPO is, “How many people?” The BPO model is so obsessed with FTEs that we’ve even converted automation initiatives to “number of digital FTEs.” Both clients and service providers just cannot get beyond this FTE model.

The Big 4 accounting firms (Deloitte, EY, KPMG, and PwC) have realized that they can give the BPO providers a run for their money with managed services offerings. They have C-level business connections in spades, but can they get out of their own way to be successful? EY’s failed Project Everest is a great reminder of how difficult it will be for the Big 4 to make fundamental GTM changes in their partner-led model.

The Bottomline: We need less “easy” and more “hard”. Bold enterprise leaders must stand up and create a new market paradigm. Service providers alone can’t do it.

“Labor arbitrage” in the 1990s was as novel an idea as “technology arbitrage” is today. Back then, it took British Petroleum to make a big bet by outsourcing its finance & accounting jobs on a large scale for the first time. Others then saw how transformational it was, and it created a whole new industry. We need a few bold enterprises to also take a risk with technology arbitrage. Unfortunately, we see most enterprises taking a very risk-averse approach to 3rd party services and persisting with the same old ways of operating.

We fear that this blog will die its own death of time as a potentially great idea that never took shape without any pioneering enterprise leaders who were willing to take a risk and take our industry to a new S-curve of value creation.

To conclude, the blame isn’t solely on the service providers for pushing the same old tired model. It’s also with the buyers of services who are too afraid to make complex changes to take full advantage of Cloud, AI, and automation technologies. Enterprises like easy – they really don’t like hard – but if they were to partner with ambitious service providers to share the risk, they would end up sharing significant rewards. As BP did with Andersen Consulting and PwC in the 90s to create the labor arbitrage model at scale, we need to see a similar risk being taken today by our major enterprises and their service provider partners if we are truly going to prosper in the Technology Arbitrage era.

*The service provider results reported above are taken from the earnings releases, where some are in constant and others in current currencies. For this article, we merely want to show the general trend in the industry, not zone in on individual performances

Retailers and CPG firms have never had it so tough. They are grappling with increasing costs of raw materials, wages and rising interest rates, in addition to the rapidly changing tastes of typical shoppers exacerbating the situation further.

The new-age shopper is tech-driven, environmentally conscious, convenience-oriented, has heterogeneous personal tastes, considers that CX trumps pricing, and engages via new channels, such as social commerce. The double blow of increasing operational costs and heightened customer expectations has created this digital dichotomy where enterprises need to innovate but don’t have the budget. Therefore, they are engaging in innovation projects to combat the digital dichotomy to get more value without huge upfront investments.

CPG and retail firms are working on both unique and common initiatives

In these challenging times, CPG firms focus on areas like supply chain command center solutions, digital engagement platforms, direct-to-consumer channels as extensions to their existing retail channels, and optimizing supply chain performance to reach customers at never-seen-before speeds.

In comparison, retailers want to create a seamless and similar CX across all engagement channels, working on customer loyalty, collaborating with their vendor partners to combat any future supply chain disruptions, devising community-driven brand strategy underpinned by purpose and ethics, and formulating multi-channel hyper-personalized experiences throughout the customer lifecycle. Read More

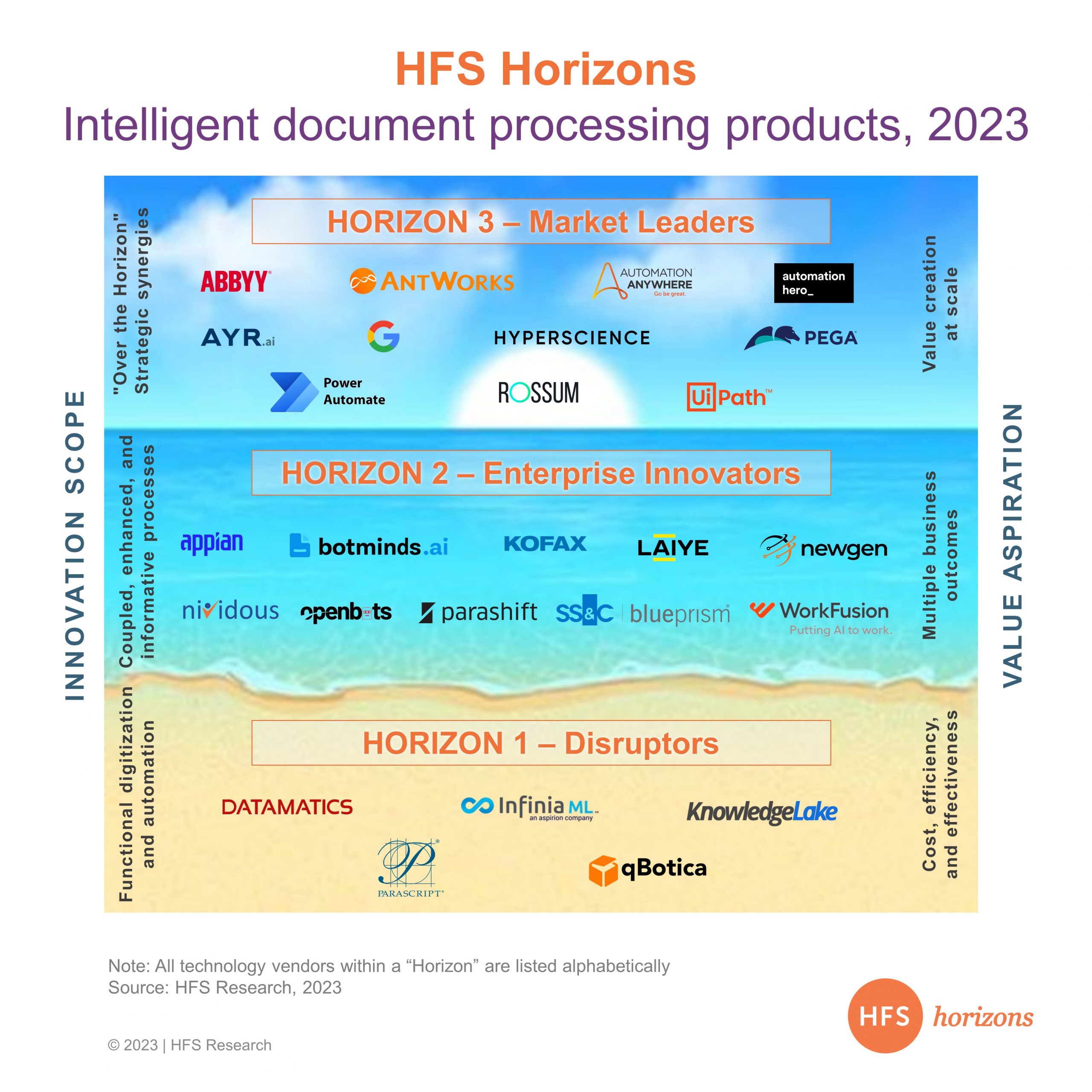

HFS has published its first intelligent document processing (IDP) Horizons report covering the broad landscape of IDP vendors landscape engaging with major enterprises. IDP is all about documents in the loose sense—extending beyond paper to include emails, digital forms, attachments, chats, and paper. It has quickly gained importance as a transformation enabler that uses automation to reduce manual effort and process the data present in documents faster and more accurately. IDP systems mimic human cognitive abilities to understand and analyze structured and unstructured data in documents.

However, that is only the primary use case for IDP. It can do much more, and through our analysis, we have seen how many IDP vendors link IDP with data and insights to drive enterprise decision-making.

Enterprises continue to struggle with making the most of their existing and new data, and IDP provides a base to extract data from documents and restructure it into more digestible formats. With the advent of generative artificial intelligence (GenAI), IDP has become an even more vital tool, giving enterprises higher accuracy and lower time to value.

Enterprises are building on the basics to target improved CX and EX

While efficiency gains and cost reductions are the essential outcomes enterprises seek, the intent for more mature results such as improved customer and employee experience (CX and EX), impact on top-line growth, and business model development are also gaining importance.

To deliver on these outcomes, IDP vendors have invested heavily in technology and internal IP or partnered with tech vendors to plug internal gaps and augment delivery. GenAI capabilities have become integral to most IDP initiatives; many vendors have already integrated them into their abilities.

The future of IDP lies in vendors using NLP (natural language processing) and image recognition to improve accuracy and efficiency, and—much in line with the outcome of combining IDP and large language model (LLM) capabilities—identifying patterns from data.

OCR is a thing of the past as IDP goes beyond document processing to unlock insights from masses of data

While efficiency gains and cost reductions are the essential outcomes enterprises seek, the intent for more mature results such as improved customer and employee experience (CX and EX), impact on top-line growth, and business model development are also gaining importance.

We assessed 26 key vendors (see Exhibit 1) in the HFS Horizons: Intelligent Document Processing Products, 2023 report.

Exhibit 1:Leading IDP vendors are building robust partner ecosystems, focusing on creative commercial models, and building internal IP to augment client delivery

Note: Service providers within each Horizon are listed alphabetically.

Horizon 3 is crowded with many vendors differentiating to deliver strategic outcomes to clients

Market leaders like ABBYY, AntWorks, Automation Anywhere, Automation Hero, AYR.AI, Google, Hyperscience, Pega, Microsoft Power Automate, Rossum, and UiPath are creating an ecosystem by partnering and working on tech advancements to help enterprises make that push toward getting more insight out of existing data and seeing them transform at an ecosystem level.

These vendors have a strong product roadmap planned and a vision and strategy aligned to achieve that goal. IDP for this group of vendors is more about being enablers to large-scale transformation efforts.

Horizon 2 innovators deliver outcomes beyond essential cost reduction and efficiency, enabling improved CX, PX, and EX

Appian, Botminds.AI, Kofax, LAIYE, Newgen, Nividous, OpenBots, Parashift, SS&C Blue Prism, and WorkFusion are the enterprise innovators driving enterprise-level outcomes.

These vendors work closely with partners to co-create and collaborate to bring a united front to enterprises in their transformation goals and work through loads of unstructured documents and data types.

Horizon 1 disruptors are enabling digital transformation at a functional level

Datamatics, InfiniaML, KnowledgeLake, Parascript, and qBotica are the IDP disruptors. These vendors are doing a great job helping clients get the basics right—an essential step in helping deliver clear functional outcomes. These vendors have robust IDP products and deliver fundamental value to clients.

The Bottom Line: Enterprise leaders looking to accelerate their digital transformation journey should seek an IDP vendor that matches their needs and maturity.

Don’t make your decision based on which vendor offers the broadest range of bells and whistles. Instead, choose the vendor that provides capabilities that align best with your enterprise’s needs and innovation scope.

Nearly 80 years before Edison invented the lightbulb, electricity had already existed. What Edison did through the invention of the lightbulb was to bring about a practical and accessible way to convert electrical energy into light. This innovation paved the way for widespread adoption in homes, businesses, and cities, fundamentally altering how people lived, worked, and interacted with their surroundings.

Similarly, while AI has been around for several years, what we are witnessing today is its increasing accessibility thanks to recent advancements in GenAI. We recently had the opportunity to sit down with Cliff Justice, KPMG’s US head of Enterprise Innovation, to delve into the transformative power of AI and its implications for individuals and businesses. Our enlightening discussion shed light on this exciting frontier.

Here’s a breakdown of our key insights from our conversation….

From Edison’s lightbulb to GenAI’s brilliance, we stand on the brink of unimaginable transformation.

During our discussion, Cliff drew parallels between GenAI’s impact and the electrical revolution ignited by Edison’s invention. At that time, electricity had existed for decades, but its practical applications were limited. However, with the advent of the lightbulb, a transformative shift occurred. As Cliff put it, “Once the practical light bulb came along and the average middle-class home could illuminate their house, and factories could install them, enabling 24-hour productivity, investment in electricity generation and the transmission grid followed, enabling many subsequent innovations adjacent to the lightbulb, like electric motors, electronics, and air conditioning.”

Much like the lightbulb, the development we’re currently experiencing has been unfolding over the past 5-7 years, where AI has transitioned from specific, tightly controlled use cases to becoming a practical and cost-effective tool with broad accessibility. This shift has led to a “network effect,” attracting more data, investment, and excitement, resulting in rapid progress—the implications of this progress span across various sectors, from education to fueling entrepreneurial ventures. ” in 2022, not many people knew what GPT was, and now it’s in your kids’ vocabulary and on their phones.”

While we witness its growing productivity capabilities, AI’s transformative influence will extend far beyond productivity. Cliff contemplated in our discussion, “What’s after GPT 4? What’s after the diffuser model? What comes next? There are a lot of potential technologies that come next. The innovation dollars flowing into these technologies will accelerate that.” The horizon is filled with unimaginable possibilities. It’s “going to happen a lot faster because we already have the electrical grid – it’s called the cloud.”

Geopolitical realities and human adaptation could throw a wrench in AI’s advancements.

Amidst this promising landscape, Cliff noted several limiting challenges. However, these challenges are less about the technology itself and more rooted in human factors and the supply chains that underpin it:

Legacy operating models: Established companies with entrenched operating models may need help adapting to AI effectively. “Organizations that are very traditional and have a deeply entrenched operating model will face challenges in making the necessary changes to compete with AI-native businesses.”

Reskilling the workforce: Achieving AI integration demands a workforce skilled in using AI technologies effectively. Cliff highlights the importance of this by noting that companies must quickly reskill their employees to work confidently with AI tools while ensuring policies are in place to prevent potential risks. “Talent and skillsets in this area are one of the pillars that you have to pursue, and you have to pursue it aggressively…. The companies that can do that faster will have an advantage.”

Geopolitics and materials: Geopolitical tensions surrounding the competition for rare earth materials, crucial for advanced chips and green energy technologies, pose a significant challenge. As Cliff mentions, “You’re competing with the same rare earth materials that are needed for green energy and like solar panels and electric motors, and there are geopolitical tensions right now which are impeding the importation of those materials at the scale.” To continue progressing at the current pace, new mining operations and chip manufacturing facilities need to be established rapidly – not a simple task by any means.

Overcoming these hurdles is essential for sustaining AI advancement in the coming decade. While navigating the complexities of geopolitics, intricate supply chains, and human adaptation, the pace of AI development may experience occasional disruptions.

Cliff envisions a quantum leap in AI…alongside some disillusionment.

During our discussion, Cliff hinted at three predictions on the future of AI, highlighting a forthcoming AI leap, empowered by Quantum computing, alongside the possibility of disillusionment driven by resource constraints and inflated expectations:

Advancements in AI and Kurzweil’s Predictions: Cliff discussed the progress of AI and its convergence with human interactions. He aligns his prediction with Ray Kurzweil’s predictions that by the 2020s, we’ll have interesting conversations with AI, and by the late 2020s, we will form relationships with AI. “he’s dead on in terms of interesting; You can’t argue that our conversations now are not interesting.”

Convergence of Quantum Computing and AI: Cliff anticipates Quantum’s advancements to potentially increase in the next five years or more, indicating it may become “usable, productive and economical.” It will be a “gradual…. gradual…. all of a sudden, quantum is here.” Cliff predicts that as quantum computing becomes more accessible and converges with AI, “that’s when you see the Ray Kurzweil type of AI, where it’s indistinguishable, maybe even smarter than human intelligence.”

Disillusionment Crash in AI: Cliff acknowledges the potential for a disillusionment crash in AI due to inflated expectations and computing resource limitations. He warns, “I think there will be a disillusionment crash because, as amazing as this technology is, the expectations can always get inflated.” He emphasized the challenges related to data infrastructure and chip shortages that could impact AI development.

Cliff’s insights reveal both the promise of a quantum-boosted future and the looming disillusionment, underscoring the need for a balanced and realistic approach to AI’s transformative journey.

The Bottom-Line: As we enter the promising world of AI, it is imperative to maintain a tempered perspective to unlock the full potential of AI.

Just as Edison’s lightbulb changed the course of history, AI has the power to reshape our world. With tempered optimism acknowledging the challenges ahead, we can unlock the full potential to illuminate a brighter future.

{kind=link}