Enterprises adopting SaaS applications to run their business processes are often entering the unknown. They don’t know what moving to the cloud actually entails, both technically and organizationally. They don’t understand the migration and integration needs relating to existing systems and data. And they certainly underestimate the support requirements to ensure effective management of the solution that continues to align to dynamic business needs.

What’s more worrying is that, after decades of experience with IT services and outsourcing of legacy, on premises applications, there are lots of generally accepted approaches, issues and outcomes that some buyers assume will translate to the SaaS world. This means that buyers are just not asking the right questions upfront to ensure successful SaaS deployments. Moreover, as service providers and buyers alike are actually learning about the SaaS services market as it evolves, enterprises are still working out what the ‘right’ questions should be!

So, what should enterprises be doing about this? Generally, it’s about talking. Talking to peer enterprises and pushing the service provider to demonstrate their knowledge of the market. A few key approaches for buyers include:

Contract consulting services that provide business and process focused advice, preferably prior to any software platform selection. Select service providers who provide some sort of Cloud Readiness Assessment services that include technical and organizational elements. Ensure that you know exactly what is involved, and which resources you need to make it work. Deloitte has simulator tools, for example, that explain the go-live process to consultants and clients. Some service providers also offer important support readiness services that advise on how to support the SaaS application in-house for enterprises that do not want to outsource this. Aon Hewitt’s approach to helping clients to not just ‘go live’ but ‘Go Thrive’ is a fantastic example of assisting clients to be self-sufficient post-deployment.

Talk to other buyers to share best practice and experience. There is no substitute for talking to other enterprises that are implementing, or even better, have already implemented the same product. Also, identify which particular area is causing a problem and talk to enterprises that are facing that exact same problem. Remember, this could be an enterprise in a different industry or country, so broaden your horizons in terms of defining ‘peer enterprise’. Service providers are often good at bringing best practices learned to every deployment. They are typically less great at physically connecting enterprises to have the conversation. So, buyers need to demand these connections.

Talk to the software vendor. Often the software vendor connects clients too. Workday is excellent at doing this, and enterprises have opportunities to make some great contacts for the duration of the deployments.

Go to conferences, especially the big software vendor events to meet other enterprises and service providers. Buyers increasingly find this incredibly useful for service provider selection as well as important connections and best practice lessons. Buyers can also stay abreast of all new developments in the market to make more informed decisions. For example, did you know that Aon Hewitt acquired UK-based Kloud and now has European feet-on-the street?

Push the service provider to be proactive. At the end of the day, they are the ones with experience and if they don’t know how best to do something, no-one does!

Both service providers and buyer enterprises have to be proactive on keeping up the communication to ensure a successful SaaS deployment that meets desired business outcomes. So, pick up that phone, get out to those conferences and have those conversations in the hallways. It’s where you will likely get the most useful advice to help you on your SaaS journey.

In a recent podcast about omnichannel (see below), an interesting spin on the well-trodden omnichannel topic came up, posed by my colleague Fred McClimans: “Omnichannel applies to the internal business/partner operations just as much as the consumer side of the market – so why isn’t this given enough attention? Or is it?”

Is the Omnichannel truly Everywhere?

It’s a great question, and one that every company should think about. All organizations are dealing with BYOD and an increasingly mobile workforce that has various preferences depending on what we want to accomplish. We are omnichannel in our personal lives—just yesterday, I texted a friend about making plans to meet, later sent her a link to a funny video on Facebook messenger, and then called to tell her I was running late for said plans. It’s the same at work where sometimes we Skype, text, call or use social platforms depending on what we do. Of course, these are interpersonal relationships where we know one another and the context for seamless interactions is often inherent and certain technology implications aren’t quite as severe (think automated analyst briefings!) – but the concept is the same.

Where the internal omnichannel concept seems increasingly applicable, is within the contact center environment. Static FAQ style knowledge management systems are being replaced by dynamic social platforms where contact center employees can get the information they need and learn from each other to support the end customer experience. Gone are the days of contact center supervisors poring over reports in dark corner cubicles, they are roaming the floors with tablets giving them real-time performance updates while listening to and coaching employees.

It’s Tools and Talent!

All too often employees don’t have the tools at their disposal to effectively do their jobs – as we move toward OneOffice, it’s not just front line workers like contact center that need effective communications tools, it’s the back office and everything in between, as well as partner communications. It’s about how we work with each other, how that permeates through our company culture, and ultimately how that supports the end customer.

From a larger business, and cultural, perspective, supporting any type of omnichannel engagement costs money and takes time to implement, not to mention a new level of training. Already stressed by budget costs associated with digital transformation and omnichannel expansion, both talent costs and technology costs are watched very closely. Every dollar spent (or invested) is increasingly tied to customer-centric outcomes, while internal development (which may not immediately impact sales revenue) is often a second or third priority.

There is also a mindset shift that needs to occur within most enterprises – viewing employees as less “workers” and more “consumers and partners”. The truth is, employees are customers (users) of an enterprise’s internal systems and their satisfaction and consumption follows the general pattern of the larger consumer market. Employees are also partners, who must engage with various departments as part of an internal supply chain process). Failure to embrace omnichannel within an enterprise, while employees are living it at home, is like asking employees to leave their mobile devices at the door and not embrace BYOD.

The Bottom-line: Employees are Customers too!

So, to answer the question, why isn’t this being given enough attention (or is it)? It’s not, and the reason is a matter of maturity, and recognizing the influence that internal culture and organizational structure can have on business performance. Most of the marketing hype for omnichannel is being driven by tech vendors that are selling customer facing platforms, and thus the discussion leans in that direction. But employees are customers too. Time for us to change that dialogue, and start pushing enterprises and service providers alike to embrace the omnichannel in internal operations.

Here’s the podcast mentioned above, where we dive into the issues of omnichannel CX support within the global market, including the challenges faced by omnichannel within the enterprise:

Elon Musk released his master plan last week, which outlines his plans for solar roofs, trucks, buses, autonomy and business models for the ride-hailing economy. As a former business planner in a leading manufacturing firm, this gives me goosebumps. All companies can learn from the master plan. In fact, I would like to turn the clock back and have these kinds of discussions in our product planning meetings. But, apart from the effect it will have on Tesla’s competitors, I think the most important implications are for engineering service providers that aspire to disrupt and plan to have a long-term future in the industry.

These are the lessons from the master plan:

Start planning about engineering disruption in your customers’ industries: Do you want to wait for customers to come to you and ask for support in engineering projects or do you want to anticipate what support customers will require in future and plan it now? Do you follow end customer trends which will impact your customers (OEMs, Tier-1s, ISVs) in future and start building your capabilities in advance? It’s not about where the puck is now but where will it be next. (BTW, have you started thinking about Augmented Reality Engineering CoE post Pokemon Go?)

Fund your future ideas from the profit of current ideas: Money shouldn’t be the excuse not to build capabilities especially when some of the service providers are sitting on piles of cash. Tesla is able to disrupt the whole automotive industry with relatively small amount of money and used money generated to reinvest in further capabilities. Don’t expect customers to fund your innovation capabilities. Engineering services buy-side customers often complain that engineering service providers want to bill all PoCs, training, tools, etc., back to them. Service providers should at least show interest in funding innovation projects for their own good.

Challenge product and industry boundaries: Engineers are trained to think within boundaries. All engineering equations and theories have boundary conditions that need to be adhered to in order validate theories and formulas. The flip side is that engineers often don’t challenge existing boundaries—whether product or industry. Innovation happens when we question boundaries and long-held assumptions—as Tesla’s plan shows about challenging assumptions of different bus designs, point-to-point passenger drop of buses, etc. Also, industry or vertical boundaries are blurring and innovation is happening at the intersection of different industries. Is Tesla’s battery capability an automotive or energy capability? Similarly, in which industry is solar power combined with an electric car? Engineering service providers have experience in multiple industries and should be in a good position to help their customers in redefining industry boundaries.

Anticipate and support new business models: We all are tired of using Uber as a new disruptive business model example. But now Tesla is showing its vision of new business models, including a future in which an automated car can earn money for you when you are not using it. Another new business model will be easily generating, using, storing and selling excess solar power. Cars and solar power systems can transform from costly depreciating assets to revenue-generating productive assets for the average Joe. These models will require a good amount of engineering support at the backend to work well. Are you ready to support them?

Develop real value engineering capabilities: Though this is not listed in Tesla’s master plan, the real success of Tesla has been developing a game changing and cost effective car battery. How did Tesla do it? Tesla challenged existing constraints as discussed in earlier point but also value engineered it from first principles. Elon Musk, in this interview, said, “Somebody could say, battery packs are really expensive and that’s just the way they will always be. Historically, it has cost $600 per kilowatt hour. It’s not going to be much better than that in the future. With first principles, we say, what are the material constituents of the batteries? What is the stock market value of the material constituents? It’s got cobalt, nickel, aluminum, carbon, some polymers for separation and a seal can. Break that down on a material basis if we bought that on the London Metal Exchange what would each of those things cost? It’s like $80 per kilowatt hour. So clearly you just need to think of clever ways to take those materials and combine them into the shape of a battery cell and you can have batteries that are much, much cheaper than anyone realizes.” This is the essence of value engineering capabilities; your customer might expect from you in future.

Keep an eye on future leaders in your target industry: Engineering service providers that want to stay relevant for the long term should keep an eye on the future leaders/unicorns that are disrupting the industries. Don’t make the mistakes of the telecom industry, where yesterday’s leaders (Motorola, Nokia, Blackberry, Lucent, Nortel, etc.) were displaced by likes of Apple, Samsung, Huawei, etc. The bad news for engineering services providers is that new disruptors are not heavy outsourcers of engineering services. They needed to engage early. The same disruption in leadership might repeat in automotive, aerospace, medical devices, industrial equipment, energy, and ISV industries.

The Bottom-line: engineering services providers that aspire to be disruptive and innovative should avoid the following –

Digitization as digital

Developing a mobile app as a new disruptive business model

Building a version 1.1 product similar to other products as disruptive product development

Using same design library as rethinking existing industry boundaries

Substituting a cheap material or cost effective supplier as value engineering

All of those points are not bad strategies, but they push you into a downstream or mature phase, which is where you build scale and fund upstream activities.

But disruptors are the ones that get into upstream phase and shape the industry. This is similar to what Phil Fersht has said about two kinds of service providers group emerging in the IT services industry – OneOffice Enablers and BackOffice Outsourcers. The same will happen in engineering services. The difference in engineering is that the Teslas of the world are setting the bar a little higher!

If you run any type of business operation or P&L, you’re quickly realizing your number one challenge is getting your people to help you achieve the results your business needs to be successful. Your strategy has to be about promoting a mindset where people focus on what they are contributing to the business, not the amount of hours they spend “at work”.

Whether you are a workaholic slogging an 80-hour a week, or a 20-hour a week work-at-home mom/dad, you are going to be measured on what you are contributing to the business – so it’s really all about setting the right outcome expectations with your employer. Simply sending through a weekly timesheet with a bunch of vague activities is a waste of everyone’s time. Agree in advance with your boss what outcomes are expected of you and focus your time on meeting them… and if you can achieve them working 10 hours a week sitting by a pool in the sun, or slaving away for 100 hours in your basement really doesn’t matter anymore – it’s whether you delivered those outcomes expected of you. You just need to decide whether that job suits you and your own goals in life. Today’s successful working relationships are being defined by employers and workers sharing outcomes that both are motivated to meet. If those outcomes do not gel, then that working situation will not survive.

And this isn’t some fancy new vision for talent only a few businesses are adopting – this is the only way firms can really function today, if they want to be successful. Everyone on the payroll needs to add tangible, easy-to-explain value… otherwise why are they on the payroll? It’s easy to turn your PC on in the morning and forward emails around the place, but what is your real value?

The only six questions that matter when it comes to outcome-based employee performance

Which customers have you delighted recently?

What new relationships have you made that add value to our business?

What work have you done that excited people inside and outside of the business?

How are you helping energize your colleagues and exciting them with new ideas?

How have you helped add value to new business wins?

How have you contributed to new initiatives that improve productivity and effectiveness?

Cutting to the chase, if you think all you have to do is turn on your PC on at 9.00am and shut down at 5.00pm, mindlessly immersing yourself in forwarding and adding to chains of emails between your hourly Facebook visits, bi-hourly LinkedIn visits and your twice-daily moronic retweeting of some crap you never really bothered to read (but the title sounded impressive), then you’re pretty much done. Go check on your pension plan, because you may be hitting those funds long before you had anticipated.

As an employer myself, I gave up caring what staff do during the day – trust me, you’ll drive yourself insane if you go old-school with the old micro-management. New school management is simply asking staff those 6 questions – and requiring answers to them.

So what activities should outcome-centric employees do during the day?

Limit email activity to one email a time. Scan your messages and quickly decide which ones require a response. The pick them off one at a time. Do not click out and re-check them all again. Just answer then quickly one at a time until all the important ones are done. The minute you start trying to multi-task your email your lose focus and you’ll spend all day faffing around your inbox like packing up your hotel room with a hangover…

Call people who matter. Remember when you actually spoke to people? You got things done, you created friendships and new ideas. Something nearly always happens when you speak to someone. List the 5 people you need to talk to and focus on them for a couple of days.

Read something that makes you smarter. We all get loads of interesting stuff shoved at us and let’s face it, we probably ready 5% of it at best. Stop. Pick out the one article you know will make you super damn smart at your key work task at hand and read the damn thing. Make a decent cup of tea, go sit somewhere quiet and read it.

Turn off Facebook. Seriously – there is nothing in there to help you do your job better. Do it with a glass of wine in the evening if you have nothing better to do. If HfS did a productivity analysis impact on the global economy due to Facebook-faffers, it’s probably in the billions…

Write something. We’re all analysts now, so focus on writing something that your think you are expert in. It’s a great way to build credibility and if forces you to be a better communicator. We all went to school, we can all type, we can all read, we can all talk, so why can’t we put out thoughts to print? Just write like you talk, like you’re explaining your views on something to someone down the pub… or explaining to your Mom what you actually do. Everyone is an expert insomething… hell, if you’re not, you might as well give up now.

Exercise. Not much is worse for you that staring into a 12 inch laptop screen 18 hours a day while guzzling caffeine and noshing last night’s pizza… so pick out the best time of the day to get your heart pounding. It’s the best thing ever, but organize when you do it, otherwise you’ll hit 5.00pm and you know full well it’s just not going to happen…

The Bottom-line: we must change our work habits if we are to survive in this work-outcome environment

Personally, I never thought the work environment would reach some of the current depths it has today for so many people, but the impact of “digital” has not been very good, when it comes to the productivity and effectiveness of so many workers. So many people are just burned out from picking up terrible digital work habits (and many at quite a young age). So change how you work. Just do it, and you’ll start to experience a very old feeling you’ve probably long forgotten: job satisfaction.

Whenever the European Commission proposes legislation that relates to Internet companies or data protection, tensions flare and lobbyists have a field day. Suggestions of protectionism and stifling innovation quickly enter the public sphere.

Among the customary saber rattling, the General Data Protection Regulation (GDPR) became law on 24 May 2016, but the broader IT industry didn’t take much notice. Yet, the implications of the regulation are profound and could conceivably dramatically impact the way companies deal with cloud services and Artificial Intelligence. As the adoption of Intelligent Automation starts to accelerate with Cognitive Computing and Artificial Intelligence being critical building blocks, we sat down with lawyers at Squire Patton Boggs to discuss the repercussions for the broader IT industry.

What is the legislation all about?

The key elements as well as implications of the legislation include:

The GDPR is the European Union’s (EU) new data protection law; it replaces the General Data Protection Directive 95/46/EC.

It took effect on 24 May 2016 and becomes enforceable on 25 May 2018

The legislation imposes a uniform data protection law on all EU members, though national governments and Supervisory Authorities (SAs) retain substantial powers

Sanctions and penalties of up to €20 million, or 4% of global turnover, whichever is higher, for a variety of infringements, including:

Breaches of core data protection obligations (e.g., transparency, valid justification, accuracy, security)

Failure to comply with data subjects’ rights (e.g., to access, object to processing, be forgotten)

Failure to comply with rules on transfer of data outside the European Economic Area (EEA)

The GDPR regulates not only businesses with operations in the EU but also companies (whether controllers or processors) that have no EU presence if they are involved in monitoring the behavior of EU citizens or selling products or services to them

The GDPR regulates data processors directly for the first time. Processors must now maintain adequate documentation regarding all categories of personal data processing activities carried out for a controller. They must also implement appropriate security standards.

Major data breaches, such as the ones we’ve seen with corporate giants like Anthem and eBay or the infidelity website Ashley Madison, are well documented. We will not attempt to dissect the broader implications of this regulation in this blog post. However, two implications jump out.

First, the severity of the penalties of up to 4% of global turnover means that the regulators have the means to come down hard on organizations that are in breach of the legislation.

Second, and much closer to our research agenda, the last bullet point about regulating data processors goes to the heart of the As-a-Service Economy and applies to cloud providers, BPOs and Intelligent Automation providers in equal measure.

Service providers face direct responsibility for the data they are processing

So why is the regulation of data processors important? Because, for the first time, processors are directly liable for the data they are processing. Without wanting to drift into legalese too much, a data processor is an organization that may be engaged by a client to process personal data on their behalf (e.g., as an agent or service provider). In our industry, that could include cloud storage providers but also the burgeoning Artificial Intelligence segment. There are broad legal implications for processors, many of which are difficult to translate into simple English. But here’s a crucial one: processors must implement appropriate technical and organizational measures to ensure a level of security appropriate to the risk involved, which means that the processor must make itself aware of the types of data involved and the associated risk levels.

In addition, processors will have to maintain records for the processing activities under their responsibility. Critically, these records must be made available to the supervisory authority on request. At the same time, processors have to guarantee confidentiality and security. For any breach the processor may be directly liable if it has not complied with the regulation or has acted outside the instructions of its client. The focus of the regulation is all about ensuring that processors assist their clients in protecting the freedoms and the rights of the individual by requiring processors to take responsibility for securing the data that they handle. They must also contractually obligate any sub-processors to do likewise. And they must assist their clients in meeting the requirements of the regulation, including in responding to data breach incidents.

So what does that mean in practical terms? Take the example of UK mobile operator TalkTalk. Its data breach is well documented. Under the new legislation the fine could be up to 4% of its turnover, which is massive. At the same time, when Wipro employees working on the TalkTalk contract were accused of making scam calls from their call center, it is likely that Wipro would be directly responsible.

However, beyond the broader and more generic issues, the most challenging clause for the journey toward the As-a-Service Economy comes from a stipulation on automated processing. It is so important that we are quoting it in all its legal splendor: “The data subject should have the right not to be subject to a decision, which may include a measure, evaluating personal aspects relating to him or her or similarly significantly affects him or her, such as automatic refusal of an online credit application or e-recruiting practices without any human intervention.”

The legislation explicitly calls out that such profiling includes people’s performance at work, their economic situation, health, personal preferences and interests. This strikes at the heart of Artificial Intelligence and intelligent Automation at large. While fraud and tax-evasion monitoring are excluded, the thrust of Machine Learning could be seriously thwarted. However, it will probably take the first court cases to determine where statistical analysis of neural network and Machine Learnings ends and where personal data that potentially needs to be presented in court starts. Yet, the legal challenges for service providers become obvious as they have to able to answer to individual claims of breach of privacy.

HR processes and intentions of workforce reduction will be challenged

Let’s apply these stipulations to a couple of scenarios:

HR related processes will pose the biggest challenges. Many recruitment processes will come under scrutiny because the use of Machine Learning is widespread. To prove that many of these processes are not fully automated will be almost impossible. Similarly, using cognitive tools for performance management will come under the spotlight.

The use of cognitive and automation tools to assemble evidence to reduce staff can be challenged in court. Yet, beyond HR processes the impact will be also felt for broad customer onboarding processes where we already see broad use of RPA and Machine Learning. Profiling is not only used to enhance the user experience but to automate broad set of processes.

Organizations in the US—or the UK after Brexit—should be warned not to give this legislation short shrift. Because, as noted above, it applies to any company that markets goods or services to EU residents regardless of whether the company is located or uses equipment in the EU. To quote some sadly departed UK politician: “We are all in this together!”

Bottom line: The legislation needs to be enforced by national data protection authorities and, ultimately, in court.

Service providers need to evaluate the impact of GDPR on the way they deliver services. Suffice it to say, the legislation needs to be enforced by courts which can be cumbersome and costly. As with any data protection legislation, this will be a fluid process with continued lobbyism and with legal challenges. Thus, the legislation will not wreak havoc with the As-a-Service Economy but it will slow the journey down and make it more complex. And should you have specific questions, we will come armed with our lawyers.

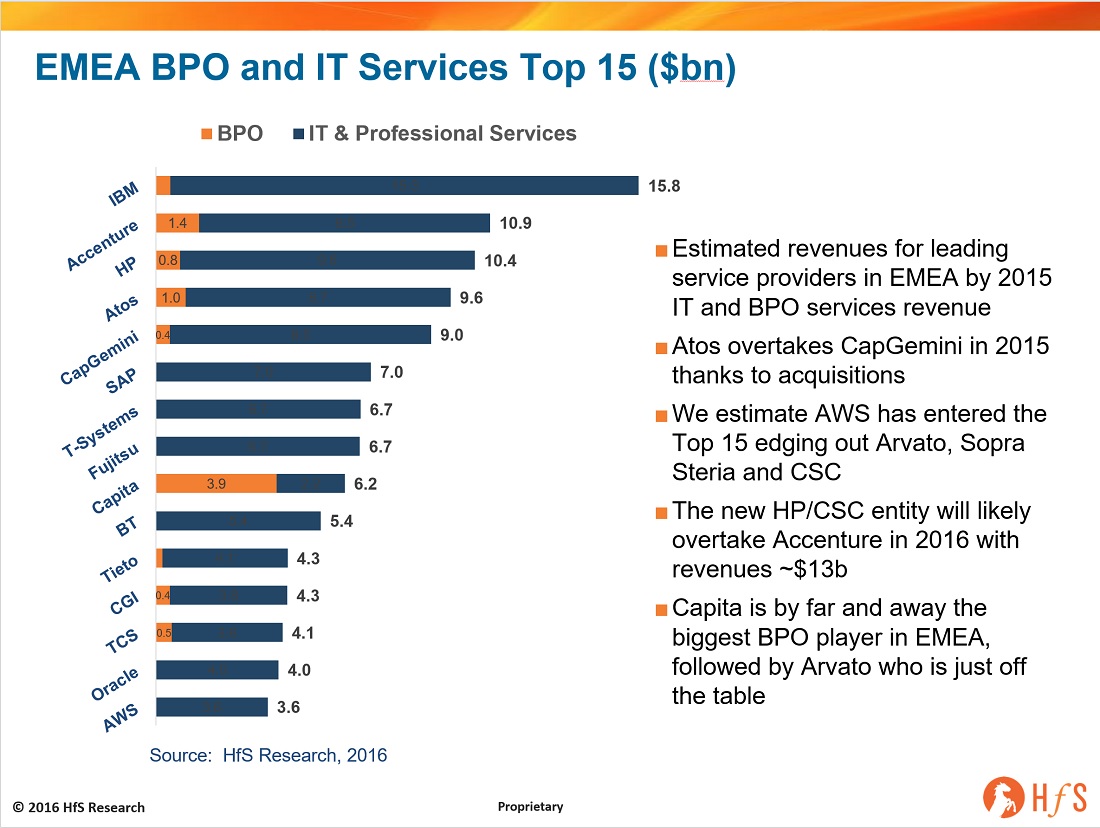

The Global majors: IBM, Accenture, and HP, still dominate the top of the list

These top 3 service providers are likely to remain in place in 2016, unless Atos and Capgemini can pull some more rabbits out of the hat, with additional acquisitions – this time focused on the EMEA market. This is not such a big leap of imagination, given the length of these firms’ recent acquisition trails. However, it is likely that HP (or whatever it becomes) will overtake Accenture when it adds in CSC’s and, let’s not forget, Xchanging’s revenues over the course of the next year. Although, given IBM and HP’s recent weak growth performance, we expect Accenture to be the fastest growing of the top 3 over the next year, particularly given its recent strong financial performance, most notably last quarter’s double-digit growth, and its broader set of digital capabilities, beyond bread-and butter IT apps and infrastructure.

Atos and Capgemini remain close in revenue terms in Europe, and both firms seem to share similar sets of challenges and goals, albeit from slightly different perspectives – both are focusing management effort on growth in the US. Atos is bearing down and trying to solidify its position in the infrastructure management space, with software defined datacentre led approach. Capgemini is building on its broad consulting skills by building out specific industry capabilities and leveraging its IGATE assets. Simply put,both are vying to be their customers’ guide to the digital promised land, but taking different routes to take them there. Both firms show strong growth in the first half of 2016 (Capgemini 15.6% and Atos at 17.9% constant currency) as they continue to integrate the finances of the recent acquisitions. Additionally, the providers grew organically, 1.9% for Atos and 3.3% for Capgemini.

Capita consistently remains the biggest BPO player in EMEA, although most of its revenues are from the UK and Ireland markets (we estimate >95% revenue). Recent half-year financials showed a 5% growth, over its 7% growth in 2015. Over the last couple of years, Capita has started to focus on expansion into Europe, with the acquisition of Avocis at the start of 2015 – its biggest commitment to this strategy so far. With the emergence of the competitive Genpact as a serious contender for European BPO deals, Capita is being forced to broaden beyond the English-speaking customer base to avoid losing further market share. Brexit has not dampened its enthusiasm for the expansion. Management comments regarding Brexit echoed those made by TCS and Infosys, some potential short-term uncertainty, but likely medium term gains and we all gain clarity of what’s in store.

There is a stark contrast between the EMEA provider list and the North American list (which we are publishing next week, so watch out for a blog). The EMEA list contains far fewer offshore-centric firms, which still depend on English-speaking centric services for the lion’s share of their business. Both Cognizant and TCS are top 5 players in the North American market, but in EMEA only TCS has managed to claim a Top 15 spot. The UK list would feature most of the big five players, as well as a strong showing from TechMahindra. Although there has been some emerging success outside of the UK for all of the other offshore firms, TCS has been the only one to gain genuine scale, thanks to its focus on localisation and more entrepreneurial approach to expansion. Although, all of the firms have had some success in the Nordics, most notably HCL with its huge Volvo and Nokia wins, but TCS has been the only offshore firm to generate significant traction in continental Europe.

Bottom Line: Europe is still a battleground for the Traditional Service Providers, but expect their Indian-centric counterparts to become more prominent as global markets consolidate

The EMEA market is still a hugely important market for all of the Global services firms, and there are plenty of opportunities given its non-homogeneous nature. The reality of the matter is simply that EMEA is not one market. Indeed, the European Union is not one market – look at the relative success of the offshore providers, outside of the UK and the Nordics. The differing national markets all have a distinct character and require different capabilities from their service provider organizations, such as local regulatory, compliance, data privacy, labour laws and accounting expertise. Many of the individual European countries have specific laws governing where data resides and whether processes can be executed outside of said country. This is especially evident when you look at smaller scale clients, which need specific attention the large providers simply cannot scale down to support profitably. So as experience in Europe increases we expect to see the other offshore providers, in addition to TCS, scale up across the continent, especially as the English-speaking markets becoming increasingly overheated for commodity IT and BPO services. For the top 15 list itself, we expect a few changes further down the list, including with the entrance of SopraSteria or Arvato in addition to the boost to HP from CSC and Xchanging.

The services industry, and technology industry, are full of ideas that keep coming around. And they often fail several times before they finally succeed. Cloud is a great example, as the groundbreaking successor to hosting and before that timesharing. Many pundits saw the value of renting capacity instead of owning it. The market just needed a few iterations before we found a viable technological AND business model for it.

So here we are, in the services industry talking about outcome-based contracts. Again. Outcome based is pretty important at HfS Research: we think it’s transformative enough to be part of one of the eight ideals of the As-a-Service economy (digital plug and play services require an outcome-based model.) And of course, my first reaction when outcome-based discussion arise is “what’s different this time?”

Here’s what’s NOT different. Outcome-based contract negotiations are a mess. Mostly for some really important reasons in order of when you’ll likely come across them if you want to try outcome based:

You have to know what an outcome is. Seems simple, and in some cases it might be. If you want to sign a BPO deal for claims processing, that’s not too hard. There’s a pretty standard definition of a claim, understanding of how to process it, and if it’s actually been processed. But if you’re going beyond basic transactional outcomes to broader issues like improved customer satisfaction or higher integrity in your supply chain, then you’ll need to spend a boatload of time defining an outcome properly.

Worse than point one, you have to decide what outcomes matter. As soon as someone gets the idea to do an outcome based contract, someone else in your company will come along and ask “why this outcome? Why not that one?” These kinds of discussions bring out some nasty internal arguments. Because sure, everyone can agree that raising the stock price is important and good. But once you get into more operational metrics, every business unit and every executive has different opinions and priorities to get there. Balancing everyone’s priorities to make sure your contract focuses on the right outcomes is a mess.

Then you’ll get into heated discussions about cause and effect. When you start to get into negotiations with your supplier, you’ll get into a debate about whether the supplier can claim victory in ALL instances, or only if the supplier can prove that the outcome was a direct result of its work. If an outcome happens, was it because of the service provider or external factors? Let’s say a supplier offers to reduce your supply chain costs by 15% through a consulting engagement and one of the categories in the engagement is fuel. The cost of oil drops and now your supply chain costs have dropped – having nothing to do with the supplier. This one will go around in circles for weeks.

What does an outcome even cost, exactly? If you’re paying for outcomes with little-to-no knowledge of the supplier’s cost structure then you have no idea what you should be paying for that service. It’s like cloud – take this price or leave it. So maybe the price seems fair compared to what you think you’re spending internally. During the negotiation, your only real negotiation lever will be if the bid is competitive and you can compare across suppliers.

Making services into a “black box” doesn’t wipe out your regulatory and legal obligations. During negotiations and continuously afterwards you have an obligation to vet suppliers for compliance to government regulation, making sure the supplier operates legally and ethically on your behalf, and follows appropriate security measures. You can’t wipe out this responsibility by saying you only get the outcome. If you only focus on an outcome, you can easily play the “I don’t care how you deliver it” card. But if your supplier achieves that outcome by using slave labor or being noncompliant with regulations, then you’re still liable since the supplier is part of your supply chain.

Post contract, you’ll start to resent your supplier BECAUSE THEY SUCCEEDED. Let’s say the contract agrees to pay on an outcome like volumes of sales and then every time sales goes up you have to pay your supplier. It won’t take long for you to decide you’ve paid them enough, in fact probably paid them two times over what you would have paid in a traditional contract structure. And you’ll turn on your provider – who’s doing an amazing job! (Maybe you put in a stop-clause that agrees to pay on outcome up to a certain amount of money, but that’s more likely for consulting/project contracts than ongoing outsourcing ones.)

Good luck during renegotiation. Remember the point about not knowing cost levers? Chances are your bargaining position will be even worse if you just want to renegotiate because without the competitive bids, you have no basis for comparison. Did the supplier use bots and completely automate the process to get the outcome? Are they primarily labor based? Some combination? If the supplier’s costs are going down, how can you know if you’re getting any of that savings back?

If that’s what’s the same, here’s what’s different: The As-a-Service economy depends on outcomes. Outcome-based contracts used to be something leaders did, and even then only in a few relatively rare situations. But now it’s becoming a requirement. Who has time in this fast moving world where everyone wants to just plug into partners and suppliers and go? Part of being plug-and-play means having an outcome pre-defined and ready to deliver.

No one has time for long complex negotiations. And even though today outcome-based contracts are long and laborious negotiation efforts, if we all keep working on them, we’ll get better at them. We’ll find ways to fix the problems I just listed. Just like timesharing, hosting and cloud, the idea is the right one. If we want to change our businesses and build a competitive future, then we need to start our contracts with the end in mind. We need to focus on what has to get done and not micromanage how it gets done. We’re getting closer as an industry all the time. HfS is working hard on research into this space right now. So when it happens, we’ll get there together.

Have you ever had a meal that tickled your intellectual curiosity, delighted your sensory perceptions and of course, sated your appetite? Challenged your concepts of what a restaurant should be and what it should deliver? That’s what Chef Grant Achatz and his team at Alinea, Chicago are trying to create— over and over again. Much as I would like to have had the actual experience, it was while watching an episode of Chef’s Table that I saw eerily familiar themes– concepts we talk and write about in the services outsourcing industry everyday.

Chef Grant and Alinea team at work

Here are three takeaways from Alinea that I put together that are meaningful “food for thought” for service providers, buyers and influencers alike:

The maker is as important as the consumer: Whether its for IT, business process services, call center operations, or analytics services, we are increasingly telling service providers that they have to think about the customer experience, and alter their service delivery metrics and workflows around delivering for the “customer first” organization. Sometimes its easy to forget that behind all the delivery are new generations of global workforces, that want to do meaningful work that “makes a difference”, instead of getting stuck in robotic, rote processes. Alinea sees the fulfilment of its team’s creative pursuits and experiences to be as important as those that it delivers to its customers. Chef Achatz describes, “Doing the same thing over and over again bores me. [My Colleague] will say, “Well, none of the guests that are coming in tonight have ever been to this restaurant before. So for them it’s all new.” And I go, Yeah, but…what about us?” We need better ways to link employee experiences to the work they deliver, and the ideas they continually generate.

Innovation and risk go hand in hand: With the As-a-Service Economy, and the evolution to the Intelligent OneOffice (or Dumboffice, as the case may be), we’re talking today about the eventual demise of the labor model, new opportunities for intelligent digital data, support and processes – and a transition period for an entire industry in the long run. Which ones will be able to make the shift, attract and motivate the right talent that “gets it”, make the smart platform and data buys, and articulate the most compelling visions for running the digital businesses of the future for their clients? Chef Grant takes reinvention so seriously, Alinea throws away perfectly good menus and starts from scratch on a regular basis. His colleague mentions on the show “We wanna lionize him [Grant] and romanticize him for creativity and innovation. But you can’t do it without being risky…What can you keep doing that’s new, that people will still like? And will you destroy yourself or destroy your reputation, or destroy the restaurant as a business…in the pursuit of doing something new?”

Three Michelin stars in, the idea of reinventing food and the restaurant experience is obviously still paying off for Chef Grant. Enterprise clients, by the same token, often state in our research that their hands are tied on innovation efforts with their service providers, for various reasons that have a lot to do with risk. Yet, we see a subsection of their peers succeed with collaborative engagements in place, creating joint innovation funds and chipping away at their legacy practices with their service partners. Innovation and risk – you cannot accept/expect one without planning for the other.

Reimagination is not a one man job: Alinea hit hard times despite all this success – in 2007 the press dubbed Grant as “the chef who couldn’t taste”, following his diagnosis of stage IV mouth cancer. A miraculous treatment saved his life, but took away his taste sensitivity. Grant powered through this phase with a renewed fervor to prove himself. He came up with even more provocative food concepts, and designed a system to communicate with his team on exactly how they were to be prepared (e.g. on a 1-5 acidic scale of pickles to bread…), and opened up other ideas for his sous chefs to experiment with more (how can we make food float?). This was revolutionary for an industry that thrives on “secret sauces” and ideas that chefs closely guard all the way to their graves.

We need to recognize that a lot of service providers today are in Chef Grant’s shoes – doing retail customer service without selling anything, running claims analytics without being insurance companies. This doesn’t exclude them from being innovative, or understanding the nuances of a particular industry. We need this caliber of human collaboration between buyers and service providers in the As-a-Service Economy, that can jointly contribute to executing on new ideas, without master-slave constraints.

These are seemingly broad, “soft” and intangible concepts, but they will dictate the level of success that service providers will have in either becoming OneOffice Enablers or left perfecting their backoffice outsourcing recipes. As for Alinea, they have just undergone renovations to rip apart and put together their well-run restaurant. In the episode, Chef Grant even wonders why plate manufacturers get to decide the canvas on which food is presented. He asks rhetorically, “Can we eliminate what we’ve been doing for the last ten years…and start over? And, uh… the answer is, “Yeah.” Sound familiar?

Fed up with 100 page profiles that focus on quantity as opposed to the key areas that really matter to you? If only there was something unbiased, concise, relevant and to-the-point that really helps us navigate sourcing providers’ key offerings and capabilities?

One question that crops up, time and again when we speak with outsourcing buyers, is the need for easy to use resources to help identify and select the right provider for the right task. HfS is launching a new type of report that delivers buyers a view of an individual service provider’s capabilities across both horizontal and industry vertical offerings. This is in addition to our flagship blueprint reports, which provide sourcing buyers with a view of the relative performance of providers in a particular offering space.

These Buyers Guides will be (as the name suggests) focused on the research needs of service buyers vetting potential IT/BPO service partners, providing in depth, referenceable insight. The Guides will include service provider people, process and technology capabilities, key financials, client examples, excerpts from published HfS Blueprints, strength, challenges, analyst insight as well as maturity modeling on the Eight-Ideals of the As-a-Service Economy. All factors that influence buyer’s decision-making today but more importantly, future-proof tomorrow.

So keep an eye, for the first of the buyer’s guides, starting with Genpact. They should appear on www.hfsresearch.com over the next two weeks. If you have any feedback or suggestions for buyers guides you’d like to see, please reach out as these are always welcome.

Long before it was turned into Hollywood film, Douglas Adams’ The Hitchhikers Guide to the Galaxy was one of my favorite books. It reminds me of the unburdened days of my youth when the book’s one liners and quotes were secret code among my friends. Among them was “42” as the answer to the ultimate question of life, the universe, and everything, calculated by an enormous supercomputer named Deep Thought over a period of 7.5 million years. To explain the meaning and the vision of Intelligent Automation, I wish I could throw a “42” at you.

Problem is, there are no simple answers.

To learn more about the complexity around the notion of Intelligent Automation, HfS has launched the inaugural Intelligent Automation Blueprint. Over the next several weeks I will share some of the learning from that project with you, starting with Capgemini today.

The HfS Intelligent Automation Blueprint assesses the delivery of comprehensive automation strategies

When HfS launched the Blueprint, there was broad encouragement and endorsement by the leading service providers, resulting in the project being oversubscribed. The stakeholders agreed that the main exam question should be how service providers orchestrate diverse sets of automation within the context of service delivery. How are they proactively transforming the processes for clients? Thus, the emphasis is not on task automation or isolated point solutions, but on automation from a business function or process point of view. The work through the Blueprint process is a litmus test for the state of industry.

The Intelligent Automation broader market is maturing

Capgemini is a compelling example how the industry is maturing. So far, Capgemini had built out some strong RPA capabilities and was starting to expand the Intelligent Automation skills to application management around its Autonomics PaaS platform. Fast forward to July 2016 and Capgemini just announced the Automation Drive suite of services that is aiming to leverage the disparate automation skills as well as four CoEs across the traditional business units. As a result, the company is addressing the issues we have earlier. The next logical step probably would be to organize those capabilities as one CoE on Group level. In practical terms Capgemini has expanded the RPA methodology to the broader notion of Intelligent Automation. Similar to many discussions on the journey toward the As-a-Service Economy, the key was a change in mindset as many delivery practitioners had to be introduced to the intricacies of Intelligent Automation. A further goal for the Automation Drive initiative is to progress to the next level of automating the automation, increasingly underpinned by a DevOps flavor. The ultimate vision is one to evolve toward a Digital Delivery Center where the capabilities of the automation CoE are overlaid with governance and control at the business unit level.

The Bottom Line: We urgently need a debate on the transformation of knowledge work

Two other aspects caught our imagination in the discussions with Capgemini. First, the company has started to deploy IBM Watson to achieve better management of the resource bench, more accurate staffing, and anticipation of gaps, rotations as well as the optimization of the “fresher” intake.

Second, Capgemini has launched an Intelligent Automation Academy to train and upskill staff so that they can move into consultancy and advisory, product selection, and proof of concept development among other things. If successful, the Academy is likely to be extended to broader Analytics and Cognitive skills. These two initiatives are important because they are part of the transformation of knowledge work that has been all too often neglected.

Data scientists and cognitive skills don’t grow on trees. Therefore, formalizing the upskilling process is a very sensible idea. The proof will be in the pudding of successful transformational projects. The answer might not be “42” but a much more holistic approach to Intelligent Automation.

Whenever the European Commission proposes legislation that relates to Internet companies or data protection, tensions flare and lobbyists have a field day. Suggestions of protectionism and stifling innovation quickly enter the public sphere.

Whenever the European Commission proposes legislation that relates to Internet companies or data protection, tensions flare and lobbyists have a field day. Suggestions of protectionism and stifling innovation quickly enter the public sphere.

The services industry, and technology industry, are full of ideas that keep coming around. And they often fail several times before they finally succeed. Cloud is a great example, as the groundbreaking successor to hosting and before that timesharing. Many pundits saw the value of renting capacity instead of owning it. The market just needed a few iterations before we found a viable technological AND business model for it.

The services industry, and technology industry, are full of ideas that keep coming around. And they often fail several times before they finally succeed. Cloud is a great example, as the groundbreaking successor to hosting and before that timesharing. Many pundits saw the value of renting capacity instead of owning it. The market just needed a few iterations before we found a viable technological AND business model for it.