Usually when there is an acquisition in the tech/services space, you can always appreciate why the deal was done; no matter how cynical you try to be, there is always some gold in there to dig out.

However, in the case of Dutch staffing giant Ranstad buying the shriveled remains of a legacy resumé-based online recruitment firm that made its name during the dot-com days, my reaction is simply one of “Why? Just why?” The business was cratering (albeit slowly, but steadily) in a world where most people just don’t use Monster anymore to do their recruiting and job hunting—it’s a business from a bygone era. But there’s always someone out there ready and willing with the ego to resurrect a dinosaur (or a Monster in this case). So I asked the question to our HR-as-a-Service analyst, Mike Cook, to give us the answer…

Mike, Is there a Monet in the Monster or has LinkedIn already Rinsed the Shop?

Phil, Once Randstad blows off the dust from Monster, will it like what it finds? In the thrift shop of the recruitment market there are treasures to be found but in a market that has been turned on its head by the LinkedIn juggernaut, there isn’t much left.

In its strategic priorities for 2015-2016 Randstad aimed to capture positive growth opportunities as well as be in the top 3 scale positions in each market it participates in. Over the last 12 months this strategy has been bearing fruit—following the acquisitions of twago, Careo Group, Obiettivo Lavoro and RiseSmart.

However, these acquisitions have just been dwarfed with Randstad announcing the acquisition of one of the true veterans of the online recruitment market—Monster, for $429 million in cash. This represents a sale price of $3.40 per share, a premium of 63.7% over Monday’s closing stock price. But it’s worlds away from Monster’s $8 billion market cap achieved in early 2000. With much of the market questioning the 47% premium Microsoft paid for (a still extremely relevant) LinkedIn (see post), one should wonder about the wisdom of paying such a price for a site that is declining in popularity.

Monster was one of the original online recruitment leaders but has struggled to stay ahead of the pack and has lost significant market share in recent years. Direct competition is fierce in this industry and recent acquisitions, such as Indeed.com taking over Simply Hired, have highlighted this.

So what does this acquisition mean for Randstad?

Bolsters Randstad’s staffing and RPO capabilities: The increased footprint this acquisition gives Randstad should prove beneficial and provide improved service delivery to the provider’s staffing and RPO clients. However, the value of Monster’s candidate database is questionable. Unlike LinkedIn, which users update regularly, job seekers usually abandon job search site profiles when they’re not actively searching for a role.

Raise Randstad’s profile, particularly in the US: Currently Randstad’s US operation accounts for around 20% of its revenue. Considering its aim to be in the top 3 of each of its markets, the acquisition of Monster with its US-heavy revenue model (70% revenues from North American operations in 2015) may make sense.

Outside of these takeaways, it is difficult to see the value for Randstad in this deal. Monster looks to be the pensioner still wearing high tops, shades and a tank top, with its platform now largely outdated and its market share no longer what it once was. The likes of LinkedIn have disrupted this market to such a degree that legacy online recruitment sites are struggling to survive. This bid for survival is being played out in the massive consolidation currently taking place in this market. The one card that online recruitment sites still have to play is in the contingent workforce market, but with Microsoft is looking to steamroll its way into this area, through LinkedIn—and the forecast looks less than sunny.

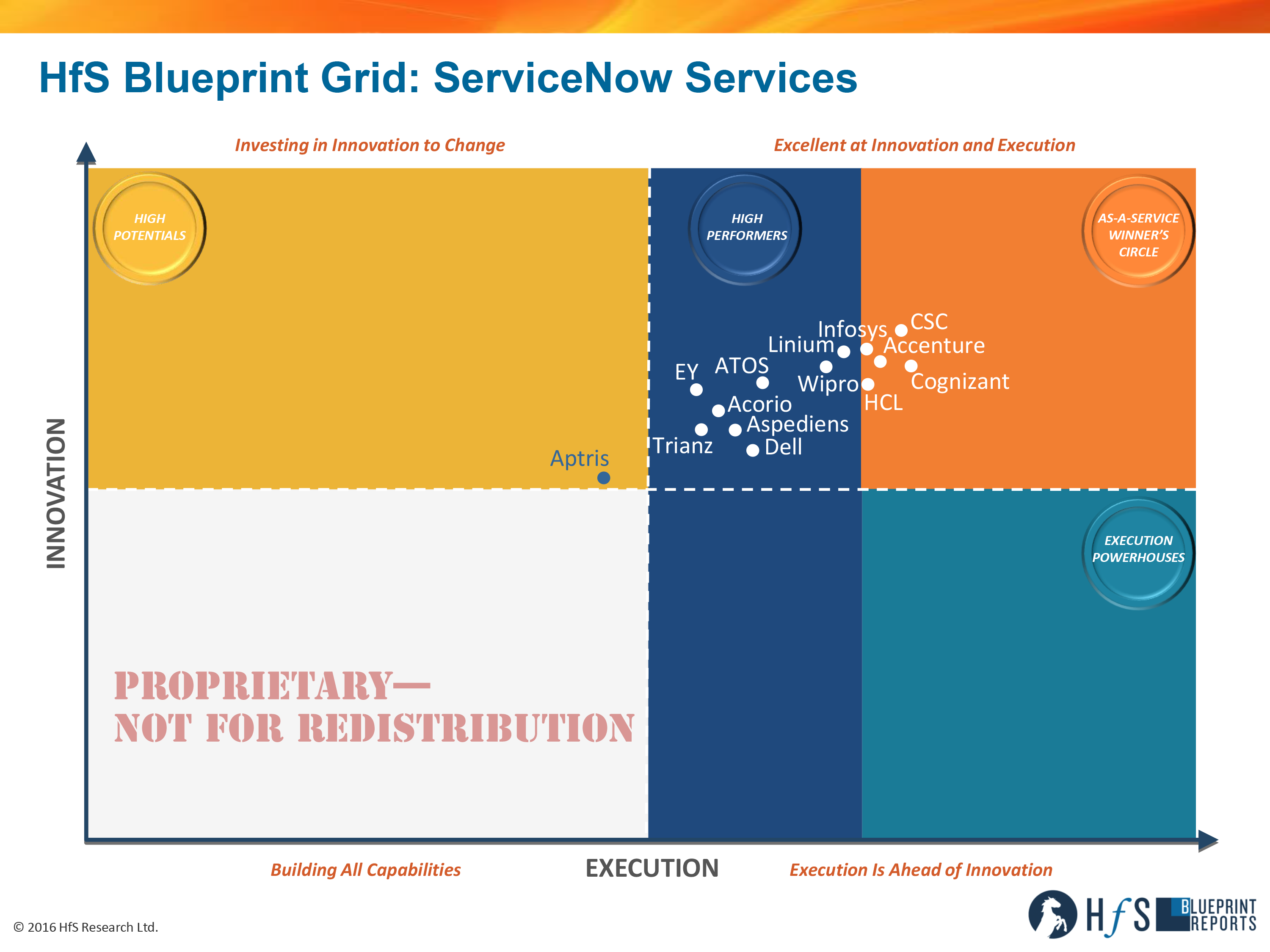

HfS readers are used to us relentlessly preaching the inexorable journey toward the As-a-Service Economy. And you still aren’t get familiar with the Eight Ideals, then you must have locked in solitary confinement for the last year…

But there are many missing pieces in that big jigsaw. Service management, while unspectacular, is a critical component of the digital underbelly of the OneOffice as HfS has termed it. As ServiceNow is aiming to expand the notion of service management to evolving into the “third estate between CRM and ERP,” providing a new cloud-based level of efficiency between front and back office, we have asked our Intelligent Automation expert in residence, Tom Reuner, to take stock as to where the ServiceNow ecosystem has advanced to.

Tom, there appears to be a buzz around ServiceNow in the industry? Is the hype justified and where does it fit in strategically for buyers?

Amidst the marketing noise in our industry, ServiceNow still stands out. And that, Phil, is quite an achievement as service management is really not among the sexiest of topics. You can see that in thousands of developers and partners having made their pilgrimage to Knowledge 16, ServiceNow’s customer event in Las Vegas this year. Crucially though, ServiceNow has expanded from the early focus on ITSM and from the slightly blurry yet smart positioning as “Enterprise Cloud Company.” Industry stakeholders are rather enthusiastic about the single data model, the embedded workflows and new ways of collaboration. As such, ServiceNow has the potential to evolve into one of the key building blocks for moving toward As-a-Service because its core value proposition centers on clients accelerating their time to value through faster actions and interactions, overcoming clunky legacy solutions like ITSM.

With that in mind, the focus is on working toward a real-time single pane of glass: The ability to communicate, collaborate and manage IT and operations in real-time is at the heart of ServiceNow projects and thus strongly aligned with the notion of the As-a-Service. Yet, only few providers articulate this as part of an innovation journey. Leading proponents that actually do this are Linium and Infosys. And this points to a broader challenge. As ServiceNow is expanding its capabilities, providers have to find a common language between IT and business: The marketing and go-to-market messaging is largely stuck in an ITSM centric mindset. The language is dominated by function, features and copious amount of jargon. However, the more ServiceNow is moving beyond the core ITSM capabilities, the more the messaging has to be adapted to this new set of non-technically minded stakeholders.

More broadly speaking, for buyers ServiceNow can help to make business alignment finally a reality: Several stakeholders we spoke to referred to ServiceNow as having the potential to evolve into the “ERP for IT.” Yet, business leaders rarely get involved in the planning process and often wait till “IT got its house in order.” Thus, there is a disconnect between the ambition to establish ServiceNow as the operational foundation and the implications to manage and run the business.

How are the winning service providers approaching ServiceNow services today? What are they doing beyond the bread-and-butter basic ITSM services?

Phil, the market is still in a nascent phase of development and therefore we see a fragmented service provider landscape: Revenues from ServiceNow Services for individual service providers are still below $100m from the leading providers, indicating a small fast growing market. There is plethora of start-ups and boutiques that will drive innovation and find their place in the growing ServiceNow ecosystem. ServiceNow aims to be the Third Estate between the front and the back-office. At same time it aims to expand toward the front office. Thus, comparison with Salesforce is unavoidable.

With that in mind, providers are evolving from the initial focus on ITSM capabilities toward what ServiceNow calls Enterprise Service Management. Thus we see them expanding into business functions such as HR, Facilities, Legal, etc., thus overcoming the traditional barrier between IT and business. Leading proponents are Linium, with CSC and Accenture catching up. But we see also ServiceNow being increasingly integrated into vertical offerings and well as frameworks and accelerators offered. Accenture is leading the space, with Cognizant catching up. Beyond that we would highlight innovative offerings around security and IoT. ServiceNow has acquired BrightPoint Security to close the gap between IT operations and security. As a result, CSC, EY and Acorio have started to build out capabilities. Similarly in IoT, While nascent and at proof of concept stage, providers like Aptris and EY are starting to experiment with IoT scenarios. And lastly, of course SIAM/MSI is the logical evolution from the starting point in service desk projects with Atos, HCL, Wipro and Accenture being the leading proponents.

Surely, it is not all plain sailing, Tom. Where are currently the main challenges around ServiceNow services?

Two issues are jumping to mind: The battle for talent and the lack of clarity for the direction of travel. As the ServiceNow ecosystem is still nascent, talent remains scarce. In many projects staff is being trained on the job with varying degree of success. Consequently, organizations have not always seen an alignment from sales process (and promises) and delivery. On the other hand the direction of travel remains a blurred picture: While an organization’s starting point is firmly rooted in ITSM capabilities with a view to overcome clunky legacy tools, the eventual destination is blurred at best. Crucially, the motivation for ServiceNow adoption lies more in embracing a single data model than the allure of cloud-based services. Yet, consulting capabilities that go beyond ITSM are scarce and many provider follow a “land and expand” approach. Many organizations we spoke to outlined that service providers fail to proactively propose innovation and help buyers with a clear outline of the future state.

The hype around Intelligent Automation keeps bubbling on days, to put it mildly. So where is ServiceNow fitting into that picture?

Phil, the disruptive element of Intelligent Automation is decoupling routine service delivery from labor arbitrage. Therefore, service providers remain comparatively and unusually coy on the topic, so I am struggling with the term “hype.” Rather, I see hesitation and confusion out there. Having that said, the market development is noticeably maturing. A reference point for that is the service orchestration around the notion of Intelligent Automation that is starting to set in. Providers like Atos, TechMahindra and Hexaware are starting to standardize service delivery on ServiceNow, link this up to orchestration engines like Automic or Cortex and put the plethora of Intelligent Automation on top of that. Thus, ServiceNow is becoming part of the broader discussions on service delivery and automation.

Does ServiceNow have the potential to move center stage in the As-a-Service Economy? How do you see the market evolving in the next few years?

As I have outlined, stakeholders suggest that ServiceNow has the potential to evolve into a critical building block for the As-a-Service Economy—not least because of its single code and data model. Yet, ServiceNow itself has been slow in embracing the notion of an ecosystem that goes beyond treating partners as mere sales channels. This is starting to change though, which is critical as the notion of the As-a-Service Economy is predicated on a collaborative partner ecosystem. Partners would like to see more investments in joint marketing and joint capability development such as vertical offerings.

In order to progress toward the As-a-Service Economy, the supply side needs to invest in consulting capabilities that go beyond technical consulting. In our discussions with clients the lack of proactive innovation and the struggle to provide guidance on the future state of operations have been as vocal as consistent. But we will see more M&A activities as the juggernauts will continue to build out capabilities. During the project CSC did acquire Swiss Aspediens and we expect to see many of the boutiques absorbed over time. Thus, we look forward to extend the discussions beyond the organizations that we have covered in this report.

HfS Premium Subscribers can click here to download their copy of the new Blueprint Report, ServiceNow Services 2016

It’s hard to overstate the importance of product support to software and high-tech companies. Good product support helps in customer satisfaction and influences purchase and repurchase decisions.

But what is good product support? Ideally, it’s where no support is required. Although companies should strive to develop products that require minimum product support, they should also look at improving the customer experience and reducing time spent on product support. Overall product support systems should be cognitive, intelligent and self-improving.

This is all the more important because most customers in the As-a-Service Economy are used to a customer-centric user experience and instant gratification. They expect the same for software and high-tech firms in both the consumer and enterprise segments. Companies need to minimize the need for product support, provide an improved customer support experience, and improve the effectiveness and timelines for product support.

Most companies outsource product support. But, whether in-house or outsourced, improving product support typically means adding headcount or seats, which will increase costs. Adding seats may improve responsiveness but may not improve customer support effectiveness.

There has to be a better way to do it. Enter the As-a-Service Economy, in which product support can be re-imagined and existing product support process can be disrupted.

Goodbye legacy product support and welcome cognitive product support

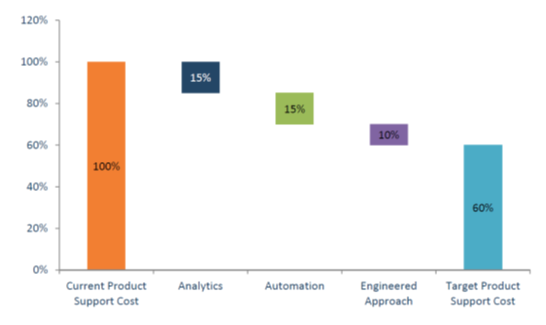

The product support process can be made cognitive or intelligent by leveraging analytics, automation, and engineering approach. The business outcome and productivity gains committed in the contract will drive the adoption of cognitive product support levers and deliver value to the enterprises. Our estimation based on case studies we discussed shows that software and high-tech companies can save about 40% of total product support cost by moving to cognitive product support as shown in the Exhibit. This 40% saving is over and above any labor arbitrage which service providers promise when they leverage offshore resources.

Exhibit: Value Proposition of Reimagined Cognitive Product Support Process

Apart from reduction in product support cost, cognitive product support increases customer satisfaction by

Reduce MTTR by increasing resolution accuracy

Reduction in invalid escalations to backline/frontline

Increase Self Service to maximum extent possible

Improve forecasting accuracy

Both users and enterprise will benefit from cognitive software product support but existing outsourcing relationships need to be revisited

In our research, we’ve found that biggest obstacle for software and high-tech firms in achieving cognitive or intelligent operations is their existing outsourcing relationships. Some of our buy-side customers believe that their primary service providers though are providing the good quality support they are still using legacy ways and nothing has changed in the product support process in the last ten years.

Enterprises should leverage cognitive product support if not for savings then for customer satisfaction. Phil recently had a very bad experience in customer support from a large high-tech enterprise. He had to speak to 16 reps to resolve the issue. No prize for guessing that this large high-tech enterprise will not be Phil’s first choice at the time of repurchase.

Net-Net, software product support is ripe for disruption. Progressive software and high-tech product companies will not hesitate to leverage cognitive software product support and futureproof their value-driven product operations.

HfS subscribers can click here to download the full POV, which details our research and recommendation on cognitive software product support

I have been an avid book reader for as long as I can remember. And when I look back, I am amazed how my process of book selection has changed over time from the wisdom of crowds to the wisdom of experts. There are parallels to the outsourcing industry, including sourcing advisors and analysts.

While I was a student, I had enough spare time (this was before the internet era in India), and I used to read a variety of books. I didn’t care about the advice of experts back then. I used to go to bookshops, browse the books and bought the ones I liked. When I say bookshop, I don’t mean likes of Borders or Barnes & Noble. In India, especially in Delhi, students hang around these kinds of weekly book markets that open on streets—only on Sundays, when regular shops are closed and are student-pocketbook-friendly. These markets have second-hand books, stolen books, pirated books, all in one place—and believe me you can’t tell the difference!

I was amazed at the risk these weekly booksellers would take and physical hardship they endured moving the books books in and out every Sunday. I asked a bookseller once how he decided on his book selection because he’d have to carry unsold books back home at the end of the day via not-so-friendly public transport. He said he asked people around in the trade which books are being sold in the big bookshops, and he tried to procure them in a cost-effective way. I didn’t ask details of his cost-effective procurement ways, but this bookseller—along with other booksellers in this market—relied on the wisdom of crowds.

Fast forward to the internet era: Amazon and its best seller rankings in different categories play the role of the wisdom of crowds. Later on Goodreads came along, which took the wisdom of crowds in book selection to an another level; Amazon acquired Goodreads in 2013.

By the time Goodreads came, I was few years into my professional life and had loyalty cards of many leading bookstores. I didn’t need to visit Sunday street bookstores any more. But my behavior remained same (i.e., I still relied on the wisdom of crowds). I was buying books using Goodreads/Amazon recommendations. But there was one problem—I didn’t have enough time to read.

Also, I was frequently annoyed when I realized that my precious reading time was often wasted on books that didn’t really interest me. I later realized, using analytics on my unread books, that I could now read only 5-6 books in a year. My risk profile has become bigger because my time was now a more precious resource, as I juggled my professional and personal lives. I didn’t want to waste a couple of months reading a potentially boring book. Also, unread books in my library were annoying me because reading them were becoming my to-do list—and I hate to-do lists. The pressure of reading was overwhelming the pleasure of reading.

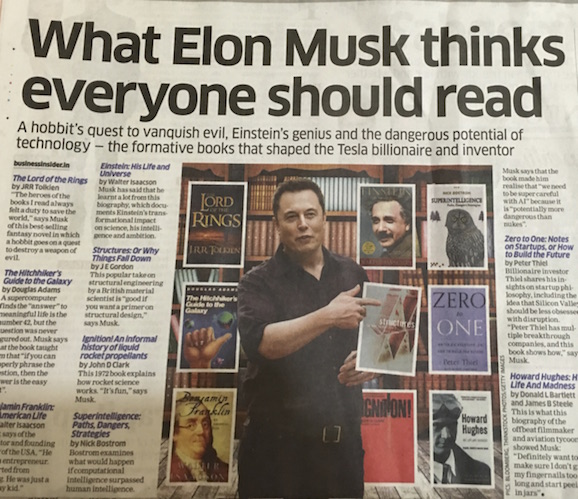

So I decided to rely on the wisdom of experts and not buy more than 5-6 books in a year. I now rely on book recommendations of few experts I admire, such as Bill Gates, Elon Musk, Warren Buffet, and Mark Zuckerberg. Also, there are a few more folks I know, who are not as famous, but nevertheless give equally good recommendations. I mainly select my books out of their recommendations.

In the outsourcing industry too, the wisdom of crowds and the wisdom of experts come into play but in a different way.

How does the wisdom of crowds play into the selection of service providers? The best example might be a service provider’s performance in the stock market. Service providers that are doing well in the stock market are better companies—at least according to wisdom of crowds. Who has not heard “No one ever got fired for buying IBM” in the last century?

But that was so 20th century! The companies performing well on the stock market might not fit an enterprise’s needs for a particular geography, industry vertical, service line or specific solutions. What about some of the companies that have are not listed in the stock market?

Here comes the wisdom of experts—or analysts and sourcing advisors. Analysts come first in the value chain and give enterprises the overview of the industry and help them identify good companies in their choice of industry, geography and service lines. The sourcing advisors come later. They advise enterprise on their specific needs and solutions and run the sourcing process. Enterprises that can afford to pay for analysts and sourcing advisors can rely on the wisdom of experts. The rest rely on the wisdom of crowds.

What if one firm can offer the wisdom of experts at the price of the wisdom of crowds? I don’t know if any of my sourcing advisor friends can do this (a disclosure: I am a former sourcing advisor), but analysts (not legacy) can do this, and that’s what HfS Research is trying to do by offering 75% of our research free. So enterprises/individuals who can’t pay for the wisdom of experts can also have a view of service providers better than the stock market!

Anyone with a real history in the services industry will be familiar with the insights of one Christine Ferrusi Ross, who spent many years leading the services and sourcing practice for Forrester Research, during the firm’s heighday. And in pre-HfS days, I used to enjoy meeting Christine for lunches when we would bemoan the state of the research analyst industry and what needed to be done to revitalize how analysts do research. Little did we realize back then we would be able to shake up the analyst industry together in an analyst firm not beholden to the whims of their paying suppliers and analysts confined to covering tiny slices of software markets. So when we got the opportunity to bring Christine, or “CFR” as her colleagues like to call her, to help shape our events and research strategies, it wasn’t a difficult decision… especially when you hear her views about moving to outcome-based contracts.

Welcome Christine! Can you share a little about your background and why you have chosen research and strategy as your career path?

Making a career of research and strategy, and then product development, came serendipitously. What I explicitly chose was being an analyst — because it seemed like an easy job at the time! When I graduated college I was working in a public relations firm for high tech companies. A big part of my job was convincing analysts to take briefings with my clients and then hopefully convince them to say something good about those clients to reporters. And I thought, wow, an analyst’s whole job is based on people being nice to them! PR people, tech execs, and reporters chasing analysts around like they were rock stars, who wouldn’t want that kind of a job? So I called some reporter friends who got me connected to some analysts and the rest is history. From the content side, I had done PR work for ERP companies and I understood how databases worked. So the application development and systems integration space was where I landed in my first analyst job.

Can I mention a competitor here? Because I started at Dataquest (now owned by Gartner) and was lucky enough to work with Allie Young, who taught me that the whole “rock star” thing was really not what the job was. She was the one who showed me that being an analyst meant doing good research and making sure you are as accurate as possible. Once I was at Dataquest, I realized I found my path — I love research, strategy, and I love the services space. From that first job, I’ve expanded into strategy and product development because I wanted to get deeper into helping clients solve problems in a tangible way and not just through research.

And why did you choose to join HfS… and why now?

Phil, I was joking with someone the other day that the real question is who thought it was a good idea for you to bring me on? It’s like taking the two kids causing trouble at the back of the classroom and letting them teach the class! That’s exactly what it’s like! You and I have had many conversations about where the IT services market is going, and where the research business is going. I’m not particularly bullish on either in their current forms. And HfS has a braver outlook than most when it comes to pointing out the flaws, but more importantly what hard changes have to happen if the businesses in these areas want to stay viable.

So with that context, why strategy and product development instead of fulltime analyst? I have spent a lot of time over the years with buyers who are frustrated. They have trouble negotiating with suppliers because deals are complex. But they’re also not getting the kind of help they need from consultants, advisors, and analysts. I’m excited to be working on some new products that will make buyers’ lives easier and hopefully make the industry as a whole more productive.

What are the areas and topics that you will focus on in your role?

On the “corporate” side, I spend most of my time on events and building new products. But I always say that analysts are born and not made, so I can’t really stop myself from looking at a few topics, at least. Right now, those topics include supplier risk and security, sourcing governance, contract negotiations, and improving the quality of life of people affected by our supply chains. There are a lot of good things we can do for the world — reducing human trafficking, for example — just by being responsible buyers and vetting suppliers properly. I talk about this more in my first blog post about being a superhero.

And what hot trends and developments are capturing your attention today?

Within the areas I mentioned, I’m particularly interested in compliance with supply chain and supplier risk requirements, as well as how contract negotiations are affected by emerging technologies. For example, it’s one thing to sign a contract with an automation software vendor. It’s another to think about how automation is applied to your services contract and the impact that has on the different cost levers. Related to that, I’m spending time on defining and contracting for outcomes. We’ve been on this ride before, but we really have to get it right. And once we get the definitions and the contracts right, what will be the impact on our industry?

So what do you do with your spare time (if you have any…)?

Hmm, a lot of things blend together in terms of work and personal for me. I’m very interested in fashion, and they have supply chain and sourcing problems too, in fact probably much worse than the tech industry. Especially problems like poor worker conditions and sweat shops, which I already mentioned is a hot button for me. I like music. You’ll hear a lot of my music taste at HfS Events actually, since I pick the playlists. I also go to a lot of concerts. My next concert is Steve Vai, and I’m really excited to see him since I’ve loved his music since college. In the past couple of years I’ve seen a lot of global musicians like Ed Sheeran, Stromae (from Belgium), One Ok Rock (Japan), Hozier (Ireland), Exo (S. Korea), BTS (S. Korea) and Block B (S. Korea.) The whole kpop industry is pretty fascinating. As someone who does product development and management, I was surprised how many product and marketing best practices we talk about in the technology that the kpop industry puts into practice. I love to discover singers from other countries, so if anyone has suggestions I’d love to hear them!

Welcome to HfS, Christine. Delighted to have you choose us as your analytical home!

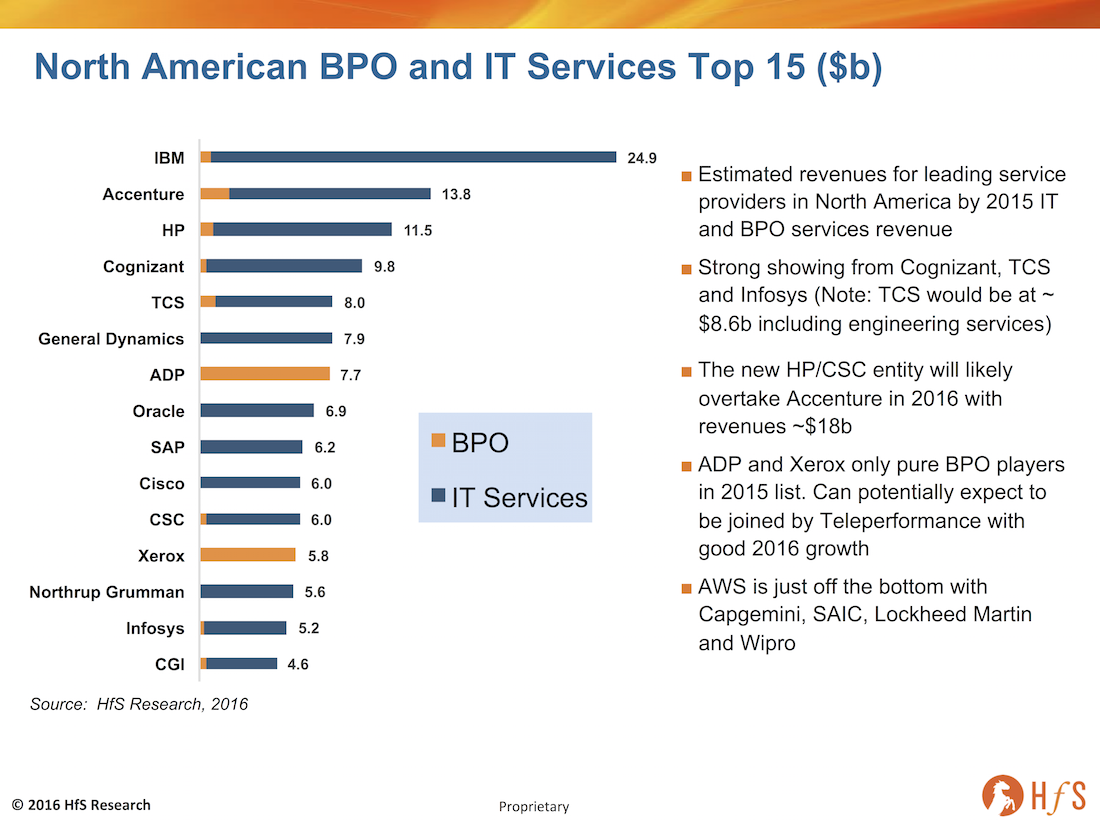

Last week we wrote a blog about the leading BPO/IT services players in EMEA, this week we’ll look at North America. Conveniently the headline is more or less the same: the Global majors: IBM, Accenture, and HP, still dominate the top of the list. Although the question here is… for how long?

Frankly, much of the same comment applies to the Top three in North America as it does to EMEA:

IBM is struggling to know what to do with its services business. The cash cow days of traditional large scale infrastructure and BPO deals are gone – with the remaining “traditional” large scale engagements much slimmer pickings and being very aggressively targeted by Indian-heritage competitive usually offering lower price points. Its pivot, like many of the technology players (but with more justification), is toward a more intelligent adaptive operations play driven by more advanced cognitive computing and analytics where clients pay for achieving business outcomes, not bill-by-the-hour labor rate cards. However, the industry is caught in a time lag between the old world scale deals and the coming intelligent deals, which could take several years to flesh out. How IBM (and its ambitious rivals) can bridge both old and new worlds of service delivery is a significant challenge.

The “New HP” – is pretty much an unknown quantity in services with the announcement of the CSC merger. Obviously, the new entity will be larger, and likely to be in the number 2 spot next year. However, while, HPE is making announcements about its future, we have heard little about the new services firm. We apologize slightly for still calling them HP, but we just keep thinking there is no point changing it until we know what the name will be, and people understand whom we are talking about even if it should technically be HPE right now. What concerns us about New HP is it appears it could be planning to compete head-on for bread-and-butter IT infrastructure business against the likes of Wipro, TSC, HCL, and Infosys. Brand India is popular among enterprise clients these days, especially for operational delivery at scale. Hence, New HP has its work cut out attempting to preserve its slide of the North American IT services pie.

Accenture has managed to balance the worlds of operational delivery and consulting to become the industry bellwether. The one service provider which has firmly established itself with its 144 diamond clients is Accenture, which expertly manages them through the forces of change at a pace which suits them. Accenture’s path is on the face of it a little smoother, partly down to its market performance, its deep C-Suite consulting relationships and its reputation to bring sanity to complex IT and business process worlds – its services seem as in demand as ever, with many clients boating their “we use Accenture” badge with pride.

The differences appear just after these three service providers. With the offshore-centric firms making a much stronger showing with Cognizant and TCS in number four and five positions, not forgetting Infosys at 12. Ignoring the shenanigans at HP, you could argue that Accenture, Cognizant, and TCS are the top three performing IT/BPO services firms in North America in recent times.

Over the next two years, there isn’t likely to be much change in the top three. Accenture is unlikely to be caught by Cognizant and TCS in that time. This is unless IBM makes a similar move to HP, hiving off another part or parts of its services business. Although there is a question mark, at least in our mind, on the exact final number attached to the new HP entity – and this will depend exactly on what is included and not included in the final deal. However, it is still likely to be significantly bigger than Accenture. So – even with big declines and fair winds behind the offshore players, it’s unlikely they will overtake in this time frame.

Not to spend too much time dwelling on the comparison with EMEA, the lack of the European giants Atos and Capgemini in the Top 15 is worth mentioning. Largely given their recent focus and acquisitions, this demonstrates the level of investment and determination required to make a dent in the North American market.

The US government contractors would have also dominated a similar list to this in the past – with Lockheed Martin, Northrup and General Dynamics all having significant revenues in this space. However, thanks to restructuring and slowdown in US government spend, Lockheed Martin has slipped off the bottom of the chart. General Dynamics and Northrup still have a place in the list, but revenues have slipped significantly for both firms over the last five years.

Amazon Web Services (AWS) remains just off the list, but is likely to overtake CGI next year if it continues its current market momentum, we could also see other cloud players like Microsoft and Google in the years to come.

Bottom Line: Agility to keep ahead of the market headwinds is still the critical X-factor

Although the global majors are likely to dominate the top of the list for at least the next couple of years. The direction of the market is largely being forged elsewhere, and unless they can tap into the zeitgeist more directly, most will end up as another CSC or EDS.

We have observed, in other blogs, that the competitive landscape was increasingly two-tier, with the main differentiator between the two categories being inertia, however, it is those companies that are reacting quickly to the changing market conditions that are growing, and not necessarily the low-cost offshore-centric providers. We are sticking by this fact that the x-factor for an enterprise service provider is agility – both regarding the provider’s ability to adapt to the market conditions and capacity to deliver adaptive intelligent solutions to clients.

A year ago, we took our first look at population health and care management business process outsourcing trends and service providers. This year’s update considers the increased focus and impact on health, medical, and administrative outcomes through BPO and BPaaS engagements. We cover the availability of skilled resources, increasingly intelligent automation, analytics, and improvements to and bundling with componentized, cloud-based platforms. It’s quite a list, and there are pockets of momentum that hold promise for delivering more effective healthcare operations for these changing times.

At the Heart of Healthcare

The healthcare industry is looking to put the people, their lifetime and lifestyle, at the heart of the business in order to drive better health and care experience at a lower cost. And healthcare organizations—payers, providers, and others in the ecosystem—are challenged to deliver on this set of outcomes, and bridge the old legacy world to the new As-a-Service Economy. As people take on more responsibility for their own health and care, they want quality, accessibility, and affordability. And every part of a healthcare operation—front, middle, and back office—has a role to play to make it a more “intelligent operation,” one that is consumer focused and results oriented.

A number of service providers are stepping in to help change the game, and partner to make healthcare business operations more effective, with an eye toward impacting these health, medical, and financial outcomes. We hear from service buyers that they are partnering increasingly for resources—to allow local clinicians more time and energy for interactions with healthcare consumers by rethinking what activity can be done remotely, through partners, or even automated.

In this blueprint, we take a look at the role of service providers in bringing together talent and technology to broker solutions through BPO and BPaaS engagements. The scope is:

Population Data Management and Analytics: identifying whom to target with what intervention

Consumer Engagement and Interaction: reaching out, engaging healthcare consumers

Utilization Management: processing authorizations, reviews, appeals and grievances

Care Coordination: coordinating care activity

Performance Management and Operational Analytics: program evaluation and assessment, quality and compliance reporting

Service Provider Landscape and Blueprint Grid Performance

As-a-Service Winners are service providers that are in collaborative engagements with clients, and making recognizable investments in future capabilities in talent and technology. These providers are also leading in incorporating analytics and BPaaS to deliver insight driven services:

Accenture: Sophisticated and innovative thought leader with a wealth of knowledge and experience looking to “change the game” in healthcare operations

Cognizant: Partnering and driving results with an increasing portfolio of BPaaS for population health and care management support

EXL: An operations management and analytics company that partners with the option of platform based and BPaaS services

Xerox: Coming out strong with refreshed focus on research-based population health that taps into healthcare heritage and recent acquisitions

The High Performers all execute well, are investing in future capabilities, but need to gain more consistency and traction among clients in defining and delivering against business outcomes, and using analytics in on-going services:

HGS: Building out a nicely comprehensive capability for enabling “healthy behaviors” and interactions between consumers, payers, and healthcare providers

Sutherland Global Services: Willing to align and invest in resources to partner with clients, creating a strong data-based starting point

Wipro: Using customer experience journey maps as a basis for helping healthcare address industry disruptions and drive outcomes

A new addition to the Blueprint this year, HCCA Health Connections (although not new to the industry) is a solid Execution Powerhouse with energetic, high quality clinical process outsourcing.

Dell has High Potential for increasing momentum for BPO/BPaaS for analytics and unique IP around imaging, social, and telehealth, and a strong ecosystem.

HCL shows innovation in enabling healthcare management through digital channels—mobility and telehealth—for the life sciences that could be used more in healthcare as well.

Picking up the Pace—What’s On the Horizon for Population Health and Care Management Operations?

In the year since the inaugural HfS Population Health and Care Management Blueprint, we have seen an increase in the use of automation, analytics, and software platforms, attention to talent development, expansion in the location of resources, and blending of talent and technology.

But the pace is slower than it could or should be, due to continued concerns about data privacy and security, locked legacy contracts, and “old habits that die hard” in procurement. Compliance both hinders and helps progress, with constant updates and requirements from the government, but also promotions and clarifications that are meant to increase interoperability, transparency, data access, and quality health care. We have to choose and commit to doing something in a different way to get a different result.

In Healthcare, more so than in other industries, service buyers are increasingly ready to switch out service providers that fail to help them evolve to a more flexible, automated, and insight driven operation. In our recent research, 66% of healthcare executive buyers—higher than any other industry—said they would likely look around when their contracts come up renewal. There is just so much at stake in the Healthcare industry now, between the driving forces of consumerism and compliance.

This side of the Healthcare Business Process Services Market—BPO and BPaaS addressing health and care management—is “poised to pop.” We have seen acquisitions and investments to get a handle on structured and unstructured data, change the mix in the workforce towards more use of automation and greater healthcare and analytics expertise, and momentum with one-to-many models and applications. We look forward to seeing how healthcare executives can partner with service providers to reinvent not just healthcare, but healthcare operations, and truly impact the health and care of consumers, driving toward higher quality, accessibility, and affordability.

The HfS 2016 Population Health and Care Management Blueprint covers market trends and direction as well as the analysis of 10 service providers: Accenture, Cognizant, Dell, EXL, HCCA Health Connections, HCL, Hinduja Global Services (HGS), Sutherland Global Services, Wipro, and Xerox. For more detail—including visuals of the market and contract activity and analyses of the service providers—click here to access and download the Blueprint.

You’re a hiring manager and you’ve just had an offer accepted from the ideal candidate. Now what? Well now the nail biting wait starts as to whether the candidate will turn up on his/her first day or indeed, last the first month.

This is a key concern for organizations today, as a candidate that drops out at this stage can cost between $3,000 to $18,000 to replace, and they haven’t even stepped in the front door yet! Therefore, the onboarding process (in this context “onboarding” will refer to both the pre-boarding and onboarding process of a candidate) is a key concern in today’s competitive job market. The reality is though that a bad onboarding experience might not just result in a candidate not arriving on their first day, but could have detrimental effects in the near and long term:

Dropout rate in the first 45 dayscan reach as high as 20%. Although this issue doesn’t end here as up to 86% of candidates make a decision to leave an organization within the first six months of their employment.

Underperforming employees who have not aligned with a company’s culture or processes are often a hidden cost. Studies have shown that keeping on underperforming employees costs the U.S. Economy around $37 billion a year.

Tools emerging on the scene will help “escort” the candidate to the starting line to increase the odds of a smooth transition on day one.

Since many companies provide various forms of booklets and induction courses, it’s not necessarily an issue of education or training about the company being joined. What is needed, is to establish a candidate within the culture of an organization from offer acceptance. Being able interact with line management and future colleagues, as well as easily access training materials on company “ways,” policy and procedure, will imbed a candidate within the organization prior to physically joining. For example, ADP has a tool for on-boarding new hires that uploads pictures and personal messages from new colleagues and managers, as well as providing online access to information.

These interactions do not have to be overly formal or heavily focused on training, as the candidate could be serving notice at a previous employer. Rather they can be regular “pulse checks” to make sure a candidate is up to date with pre boarding documentation and also that he/she is interacting with future colleagues. During this time mundane tasks such as laptop preference and tax filing should also be completed. The end goal is that the candidate can hit the ground running on the first day, already having an idea of the company’s policies and procedures as well as having already become acquainted with colleagues. Hexaware’s new ONe mobile application for example, enables interaction between management and a candidate from the time of offer acceptance through to first day, and also provides analysis on candidate’s state of mind to preempt potential drop out through a continuous mood assessment undertaken with the candidate.

A key take away here is for hiring and HR managers to move past the notion of employees only becoming part of the company on their first day, and then having to quickly assimilate or feel isolated or left behind. From offer acceptance a candidate should begin their induction, both through social interaction with management and colleagues through to light-touch training and administration. Think of a candidate as an employee even before they start their first day.

Most British people around my age will be familiar with Not The Nine a Clock News – a satirical sketch show on the BBC in the early eighties, which was one of the first vehicles for Rowan Atkinson. I remember a sketch where a customer was visiting an electrical retailer and asked a series of questions to one of the staff members about a Stereo’s features, like “does it have Dolby?” With the member of staff just parroting back affirmatives to every question, “yes it has Dolby.” The customer, with increasing disbelief asks if it could microwave chickens – with the “expert” answering with disinterest “yes it microwaves chickens.”

This is the type of response you get when you ask an “expert” about blockchain. What does blockchain do? Everything. Or so it seems.

I have the fortune (or misfortune depending on your perspective) to hang out a lot with IT and sourcing industry analysts – working in the industry they make up my colleagues and many of my friends. This means that, over the last couple of months, I have had to endure a whole spate of blockchain theses testing the boundaries of sanity. The issue with a topic like blockchain is it’s hard to understand what is real and what is not. Because blockchain is a difficult concept to understand, many of the people I have encountered talking about the benefits do not seem to understand what it actually is. Except that it will revolutionize lots of things – by making electronic voting a reality, electronic financial transactions perfectly secure, IoT actually happen and work, helping to enforce digital rights and combatting physical counterfeits. Which are all laudable aims, but I tend to lose confidence in people’s predictions about a subject, when they do not understand how it works. Just saying “well you know, it’s blockchain, of course it can (microwave chickens),” just doesn’t inspire.

What is more, this overblown confidence in blockchain’s ability to change the world is not shared by business leaders at the moment. Our recent research on achieving Intelligent Operations, which canvassed 371 major buy-side enterprises, showed interest in blockchain at a similar level to using drones.

When you look around and see the many options for pet services such as pet insurance, grooming and exclusive doggy spas, it’s pretty easy to see how our pets are considered part of our families (just ask my own pampered hound dog!). To stay competitive in the pet supplies business, Petco’s customer experience team is laying a foundation to cater to customers and the way they want to shop, often with their pets, which is also impacting the way the retailer engages with service providers.

Bentley the hound putting in a hard day at the office

Writing Off Legacy

Challenges on the surface are not just about meeting new customer expectations and bridging online and offline worlds, but about writing off legacy and building the back and middle office processes to support the front, essentially creating what we call an Intelligent One Office. Part of this includes moving away from old tools and connecting underlying systems to bring customer data together on an omnichannel platform. Despite the challenges in doing so, Petco is working with service providers to take these essential steps to future proof its competitive strategy.

Petco is also writing off legacy thinking, pivoting expectations of their service provider partners to be more aligned to the NPS and customer issue resolution that matters to their business results. Sutherland Global Services, one of Petco’s Integrated Business Process Outsourcing partners, has aided in the customer experience changes with certain areas of expertise, including handling phone, email, chat and social interactions as well as helping with some of the thinking about how to improve CX. Petco’s social customer care, for example, is run by trained and dedicated social-savvy pet enthusiasts. Using a “social media platform” that monitors and prioritizes comments, agents can respond to inquiries within an average of 30 minutes.

Applying Design Thinking

Sutherland is also doing some aspirational work to help Petco along its transformation journey. To get into the pet groove, Sutherland sent its own workforce along with Petco into the stores and neighborhoods to better understand what people want for their pets and fed it into the solution design. Using design thinking concepts, Sutherland consultants aim to improve the customer experience from the inside out—talking with groomers and understanding what can make their lives easier, using it to suggest what would improve the experience for customers.

One of the key focus areas of building out a digital customer experience strategy is evaluating whether the tools employees use are aiding or hindering good customer experience. It is all too frequent that contact center agents are toggling through many different screens to find the appropriate information. Petco is addressing this by investing in tools that will bring together the relevant information agents need, which also impacts the training and approach of key services providers to adapt to new systems quickly. Sutherland was one service provider which worked on a prototype platform connecting various pieces of customer information to create a more holistic “omnichannel” view of the customer. This creates a unified customer view using data sources such as web, loyalty info, chat, shipping info, social monitoring feeds—to generate customer intelligence that is actionable in real-time across channels. The unified view and analytically-driven intelligence helps optimize the customer experience by improving business and customer outcomes (e.g., reduced average handle times, increased first contact resolution, incremental sales, decreased attrition, improved NPS, increase customer satisfaction).

Petco’s efforts are taking a wise approach to move the needle on improving customer satisfaction, as well as the retention of loyal customers and their furry friends.

Usually when there is an acquisition in the tech/services space, you can always appreciate why the deal was done; no matter how cynical you try to be, there is always some gold in there to dig out.

Usually when there is an acquisition in the tech/services space, you can always appreciate why the deal was done; no matter how cynical you try to be, there is always some gold in there to dig out.

Most British people around my age will be familiar with Not The Nine a Clock News – a satirical sketch show on the BBC in the early eighties, which was one of the first vehicles for Rowan Atkinson. I remember a sketch where a customer was visiting an electrical retailer and asked a series of questions to one of the staff members about a Stereo’s features, like “does it have Dolby?” With the member of staff just parroting back affirmatives to every question, “yes it has Dolby.” The customer, with increasing disbelief asks if it could microwave chickens – with the “expert” answering with disinterest “yes it microwaves chickens.”

Most British people around my age will be familiar with Not The Nine a Clock News – a satirical sketch show on the BBC in the early eighties, which was one of the first vehicles for Rowan Atkinson. I remember a sketch where a customer was visiting an electrical retailer and asked a series of questions to one of the staff members about a Stereo’s features, like “does it have Dolby?” With the member of staff just parroting back affirmatives to every question, “yes it has Dolby.” The customer, with increasing disbelief asks if it could microwave chickens – with the “expert” answering with disinterest “yes it microwaves chickens.”