When we coined the term “The As-a-Service Economy” a year ago (remember our famous Ten Tenets post), we never quite anticipated we were helping define the future model the services industry would adopt for business, technology and operational service delivery.

When we coined the term “The As-a-Service Economy” a year ago (remember our famous Ten Tenets post), we never quite anticipated we were helping define the future model the services industry would adopt for business, technology and operational service delivery.

As-a-Service replaces Outsourcing

We’ve perennially debated the (toxic) term “outsourcing”, long vilified as the substitution of onshore jobs with cheaper offshore people. The outsourcing community has continually struggled to find new defining terminology, as NASSCOM replaced “BPO” with “BPM” and the IAOP has refused to shift from the past, staying true to the O word as its core identity.

The reason why we struggled with our identity was because outsourcing, by and large, has really always been about people. It’s hard to change processes, drive common standards across clients, build a utility model that can be scaled and made cost-efficient, when you’re really just moving work around the world with the goal of getting it done cheaper. And that’s really been the story of outsourcing to-date – service providers battling it out, at varying levels of effectiveness, to deliver people-based services more productively, promising delights of delivery beyond merely doing the existing stuff significantly cheaper and (hopefully) a bit better.

But outsourcing hasn’t failed. Only 13% of service buyers in our new Ideals of As-a-Service study believe there is no more value to be found in the current outsourcing model. Outsourcing is the starting point towards driving out bloated labor costs, centralizing the delivery staff within a service provider, and creating some basic common standards across processes. However, it’s not the end-solution for ambitious firms, it’s merely the start of the journey towards this future vision of “As-a-Service”.

We also hear a lot of hype about Robotic Process Automation, which is another accelerator towards As-a-Service, but like outsourcing, RPA isn’t necessarily the end-solution either – many applications have a lifecycle and are replaced over time, and many of today’s processes become obsolete as businesses evolve. RPA merely acts as a further conduit, coupled with outsourcing, to smooth the ultimate journey towards destination As-a-Service.

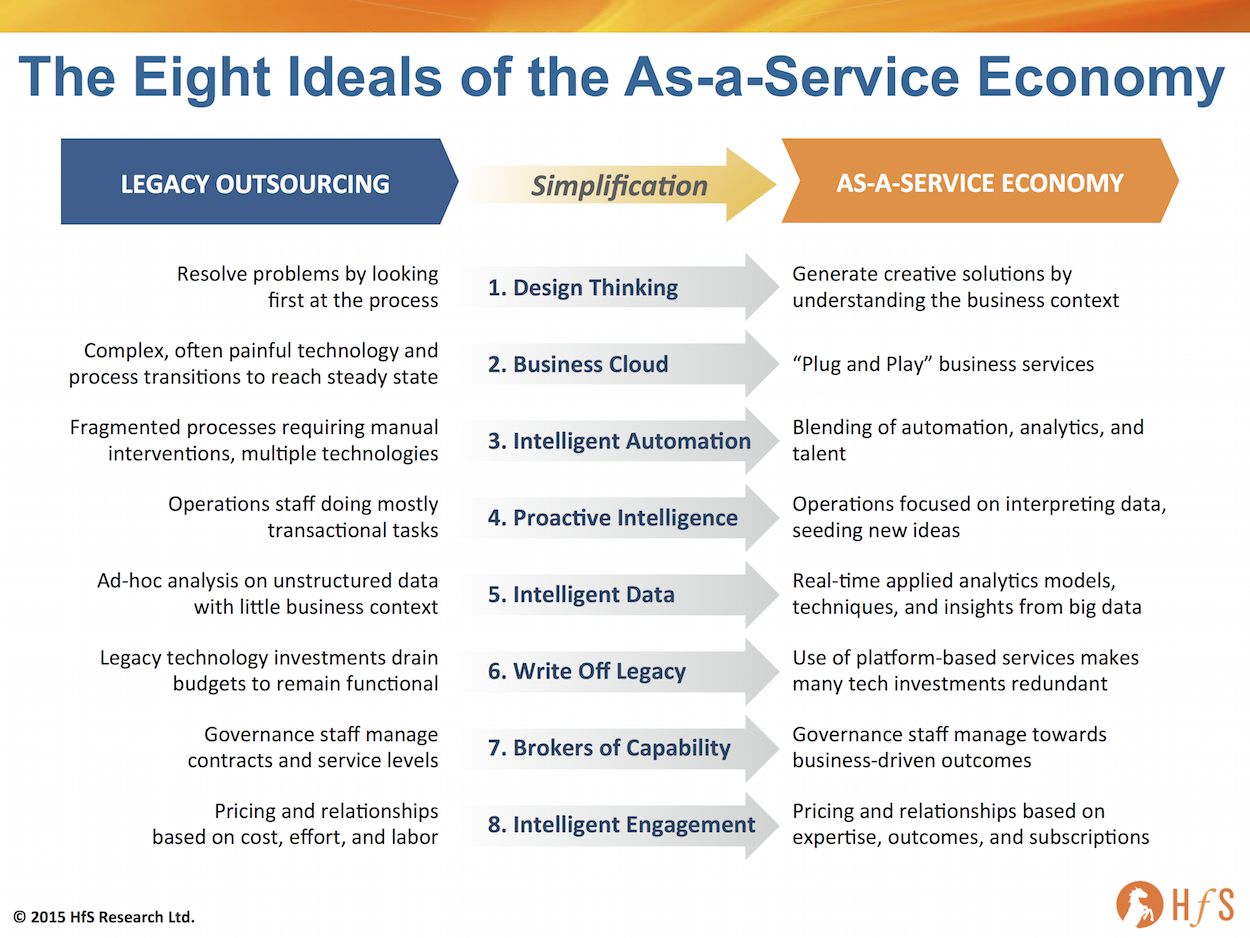

Defining the evolution to the As-a-Service Economy with Eight Ideals

The game-changer is centered on today’s services work gradually becoming a genuine blending of people-plus-technology that helps us inch towards an ultimate destination of services value, accessible on-tap, empowering service buyers to focus on proactive value-identification with help from their service partners through meaningful and secure data, enabled by intelligent automation and digital tools… all made possible by smart people working together.

So let’s examine the Eight Ideals of As-a-Service, into which we delve in-depth in our new defining report, “Beware of the Smoke: Your Platform is Burning“, that canvasses the views, dynamics, aspirations and intended actions of 716 service industry stakeholders:

Click to Enlarge

The journey to As-a-Service is all about simplification

Business services, today, are one of speed to business impact. They are about simplification. They are about removing the blockages and obstacles diluting this business impact. Anything less is not taking advantage of the experience and capability that has been developed in the global services market, over the past three decades. In this time, enabling technologies, talent, sourcing operating models, and macro-economic trends, such as globalization of labor, high growth emerging markets, new business models and consumerization, enable service buyers, advisors, and service providers to engage increasingly in a more flexible and collaborative manner. The ambition is to achieve renewed business results with speed, quality, and effectiveness. When we get there, we will be in the As-a-Service Economy.

The transition to As-a-Service is all about simplification — removing unnecessary complexity, poor processes, and manual intervention to make way for a more nimble way of running a business. It is also about prioritizing where to focus investments to achieve maximum benefit and impact for the business from its operations.

The emerging As-a-Service Economy will be more agile and dynamic, featuring on-demand plug-and-play services in a one-to-many fashion targeted to impact what matters to consumers as well as businesses. The two are increasingly intertwined as consumer insights, decisions, and loyalty carry increasing weight on the success or failure of an enterprise in any industry.

The Bottom-line: The As-a-Service Economy is a vision for the future, building on today’s achievements

It’s easy to deplore how poorly our business are run, how dysfunctional are our processes, how badly integrated are our technologies, how reactively and transactionally our staff perform. But this is the evolution of business, this is how we got here today. When you talk to service buyers, they are unlikely to tell you their businesses are running worse every year. In fact, most have improved immensely over the last five years with improvements in global scale delivery, cloud computing etc.

Survival in today’s global business environment, for most, is a marathon, not a sprint. Not every industry has been Uberized over-night – most are being disrupted with technology-driven business models that we can learn from, adapt, adjust and try to get ahead of. Most enterprises suffer from the same woes and face similar challenges to clear their path towards their desired As-a-Service Ideals.

The new challenge is to prioritize which Ideals really matter and how to work with the smart people and partners around us to get there. In subsequent posts to this theme, we will analyze our study findings further to understand the priorities, obstacles, expectations and anticipated dynamics to unravel how we will eventually arrive at the As-a-Service Economy, and what we can do as an industry to get there and prosper.

And Part II is now up – click here to read!

Please download a copy of our new Industry Report “Beware of the Smoke: Your Platform is Burning”, authored by analysts Phil Fersht and Barbra McGann, that analyzes findings from 716 service industry stakeholders in our new Industry study that defines the future of services and the emergence of As-a-Service Economy.

Posted in : Business Process Outsourcing (BPO), Cloud Computing, Design Thinking, Digital Transformation, Global Business Services, HfSResearch.com Homepage, HR Strategy, IT Outsourcing / IT Services, Mobility, Robotic Process Automation, SaaS, PaaS, IaaS and BPaaS, Security and Risk, smac-and-big-data, Sourcing Best Practises, Sourcing Locations, sourcing-change, Talent in Sourcing, The As-a-Service Economy, The Internet of Things, the-industry-speaks

Excellent analysis, Phil. Extremely thought provoking.

Rahul

Well said Phil! Excellent article.

[…] Hello As-a-Service Economy, goodbye Outsourcing, Part I – … our famous Ten Tenets post), we never quite anticipated we were helping define the future model the services industry would adopt for business, technology and operational service delivery. The reason why we … […]

… [Trackback]

[…] Informations on that Topic: horsesforsources.com/as-a-service-economy-defined_080915 […]

Very good insights. I like how you have articulated as-a-services as a continuum from the current outsourcing model, as opposed to something completely new we have to invest in.

Phil,

Enjoyed reading this article – you raise some important points. The focus on simplification is a key one, and a major challenge for the industry. There is short term gain to help enterprises simplify, but where is the revenue for providers after that?

Brian Lewis

@Brian – The billion dollar question (and a great one!). The simple answer is that money is to be made where value can be created. In the old (and current) model, there is value in the simplification of the back office. Enterprises want a standard, effective way to pay their staff, manage their suppliers, consolidate their accounts, pay their bills, process their claims, manage their data etc. When the value is in standardization and efficiency, the money is to made in achieving that for clients. There is still a long, long way to go just with the standardization of the back office, but advancements in technology platforms are certainly creating a new ceiling on finding an acceptable place for enterprises to aspire to reach. However, while that market continues to grow, prices are getting squeezed and demand is not as aggressive as it once was, as most major enterprises are maxing out their easily-achievable labor arbitrage opportunities and the focus moves more to automation and standardization. So being able to provide intelligent automation is definitely one avenue – and I see a 10 year runway there, being honest – this really is a marathon transition for most of today’s enterprises. However, where there is As-a-Service money to be made is with the new breed of “born in the cloud” companies (the F500 in 5 years’ time) and those ambitious companies embracing digital, where RPA is native in their processes, most operational areas are sourced externally and the core products are dominated by digital processes and capabilities. The means we need As-a-Service providers which can deliver middle/front office capability to clients in areas like marketing, sales operations, customer analytics, social media management etc. In short, the more the back office commoditizes, the more the focus will shift (and already is) to the front. That means providers need to be bold and make bigger bets and investments in these new areas if they truly want to be more than a back office player…

PF

Hi Phil, extending Brian’s billion dollar question. While I agree that the money will be made where the value is created, but given that the investment needed is long term in nature and the typical outsourcing contracts are mostly 3 ~ 5 years. How do you see service providers and clients committing to it.

Second part of the question. Unlike a B2C scenario where many new players have challenged the industry with disruptive innovations – e.g. Uber, In outsourcing service that is B2B, how can a new player remove the huge entry barriers. The earlier wave of labour arbitrage outsourcing was a result of a major disruptive development – the undersea fibre optic cables. What’s the next big thing in future.

Phil,

Great article and a spot on analysis of the changing landscape of BPO, at least from a personal perspective.

I would go one step further and add that a core part of ‘simplification’ is actually specialisation.

Why don’t Marketing agencies wrestle with the same broad industry branding challenges outsourcing providers face?

– They are an outsourced function, just like Finance, HR, IT.

– They are responsible for managing billions on behalf of their clients.

– They are service oriented, with a focus on delivering functional/corporate goals.

Yet, very few – if any – would actually be a part of this debate, let alone categorise themselves as BPO – a few thoughts why:

– Marketing agencies’ work is highly visible, their impact is felt across the business.

– They have progressively moved the discussion from workloads, quantity of outputs, ‘cost-per-million’ to customer journey, brand equity, shareholder value.

– They are able to deploy specialists into the client’s world, at the right time to focus intensely on that area, then move on again.

– The nature of this specialist approach means that the specialists are intelligent, agile, and adaptable – not restricted to just running a pre-defined process

– Design thinking is at the heart of their modus operandi, they always start with the client’s problem/challenge and adapt approach / strategies accordingly

– The transactional element of their work is rarely felt / shown to the client, they instead have a slick customer interface which is able to connect client’s demands with various parts of the agency

– And finally, in a lot of cases, they have been successful in moving from back to front office support – it is just as easy for a CEO to buy / work with a marketing agency as it is a CMO.

Phil, back to your article – the two critical differentiators between a marketing agency and a BPO provider are fundamentally the (a) operating structures and (b) the creative culture that empowers everyone within the agency organisation to understand value from the client’s perspective. It is this understanding of value that enables each of the specialists to better craft ideas, present new insights and offer new ways of working – not just follow a process flow for doing the same thing, faster.

Why raise a ticket, if the event can be avoided completely but still achieve (or exceed) the desired outcome?

In regards to monetising this model, yes – it will take a long time for established BPO providers to turn their mighty machines around and realign with this trend. But the risk of not doing so increases each year as more and more specialist service providers, challenger companies, enter the market – and large corporates start to look for value-additive partners, not just process managers.

Articulation of the topics first-class, I really enjoyed the article and contents surpassed my expectations of depth and inclusion of things that mattered. Yes, we continue to march towards this particular economy and as new technology makes quick work of old processes, in a true Microsoft fashion consumer requirements continue to grow as with expectation. I believe it’s impossible to accurately predict when everyone will function in a similar manner. Where our breadth of offering matches the demand of new services. look at the bundling of technology offering from a legacy telco as an example of either utilising your customer base in a different way or safeguarding new revenue stream as competitors disrupt. We have a long way to go, flexibility and innovative mean more than ever before!

@Chris – good rationale. You’ve actually articulated well the differences between the back office (traditional BPO) and the middle-to-front office (creative marketing and design thinking). The former is all about standardization, cost and scale; the latter re-imagining process to create new thresholds of value. However, the latter needs the former to provide the data and infrastructure to be effective. We’ve long-written about the potential of “marketing BPO” at HfS – many of the smart call center provders are already going down this path, within the delivery center, and reorienting their customer service staff (for example – as Durgesh points out – helping legacy telcos evolve their offerings across multiple channels). The same needs to happen in areas like F&A, Procurement provision, insurance, ICD-10 transition etc., but providers can only move as fast at their clients are willing to take them. And BPO providers need to figure out where to make their big bets – they don’t have the resources to be “front office” with everything, they need to pick where they are truly distinctive and can invest in the talent, technology and capability to be effective. This is a marathon, not a sprint, but the destination is clear where we’re heading and the old world will be very different in 5-10 years’ time…

PF

[…] For background reading, check out: Hello As-a-Service Economy, goodbye Outsourcing, Part 1 […]

[…] have achieved the maximum potential benefits from legacy BPO by this point. In our recent “Ideals of the As-a-Service Economy” research, just about three out of four participants (72%) from this industry indicated that […]

[…] has been considered an ugly word. The Horses for Sources analysts are saying the “As a Service” age is upon us. Outsourcing is a very acceptable way to […]

[…] outsourcing and risk-averse. However, we expect this model to change in the medium to long term as As-a-Service components make their way into the […]

[…] Provider-replacement therapy popular among three-quarters of the C-Suite. A staggering 77% of leadership want to see their legacy service providers replaced, compared with only 27% of their middle management. This is because corporate leaders have reaped the labor arbitrage fruits from legacy outsourcing, and know their middle layer is getting fat-and-happy meeting their SLAs and performance metrics. Nothing will change without forcing the issue – the incumbent provider has little interest reducing the predictable headcount-based revenue it is serving up, and automation threatens both the provider’s margins and the middle management’s job security. Ripping out the legacy is the only sure-fire cure to breaking the inertia cycle. Provider-replacement therapy worked when the C-Suite demanded the expensive ITOs were kicked out for the hungry India-centric providers (remember all that fuss the fat-and-fluffy middle then made about the perils of offshoring). Now, the C-Suite wants to replace this new legacy with automation-driven service solutions. This is a continuous cycle of cost take-out and better effectiveness and now we’re onto the next wave….The As-a-Service Economy. […]

[…] Provider-replacement therapy popular among three-quarters of the C-Suite. A staggering 77% of leadership want to see their legacy service providers replaced, compared with only 27% of their middle management. This is because corporate leaders have reaped the labor arbitrage fruits from legacy outsourcing, and know their middle layer is getting fat-and-happy meeting their SLAs and performance metrics. Nothing will change without forcing the issue – the incumbent provider has little interest reducing the predictable headcount-based revenue it is serving up, and automation threatens both the provider’s margins and the middle management’s job security. Ripping out the legacy is the only sure-fire cure to breaking the inertia cycle. Provider-replacement therapy worked when the C-Suite demanded the expensive ITOs were kicked out for the hungry India-centric providers (remember all that fuss the fat-and-fluffy middle then made about the perils of offshoring). Now, the C-Suite wants to replace this new legacy with automation-driven service solutions. This is a continuous cycle of cost take-out and better effectiveness and now we’re onto the next wave….The As-a-Service Economy. […]

[…] From this year’s proceedings, we have taken to heart the near ubiquitous discussion of “Digital enablement and Disruption” to construct a sentiment analysis of where the stakeholders in ILF currently find themselves in their transition from a world of legacy operations to delivering what HfS has termed the “As-a-Service Economy”. […]

[…] The bigger threat is with the offshore locations which deliver these services, as most are, by and large, very robotizable tasks that smart service providers are already figuring out how to automate using the various RPA and IT automation tools available on the market today. If I were Narendra Modi or Xi Jinping (perish the thought), I would be very concerned that a whole workforce generation needs reorienting to find jobs that are growing in demand, as we are fast approaching a time of oversupply for the demand coming from North America, Europe and ANZ. The shift has already happened, we are now experiencing the aftershock of the shift towards the As-a-Service Economy. […]

[…] The bigger threat is with the offshore locations which deliver these services, as most are, by and large, very robotizable tasks that smart service providers are already figuring out how to automate using the various RPA and IT automation tools available on the market today. If I were Narendra Modi or Xi Jinping (perish the thought), I would be very concerned that a whole workforce generation needs reorienting to find jobs that are growing in demand, as we are fast approaching a time of oversupply for the demand coming from North America, Europe and ANZ. The shift has already happened, we are now experiencing the aftershock of the shift towards the As-a-Service Economy. […]

[…] of the most significant shifts towards As-a-Service delivery, in recent times, has been the investments in delivering comprehensive IT and business process […]

[…] of the most significant shifts towards As-a-Service delivery, in recent times, has been the investments in delivering comprehensive IT and business process […]