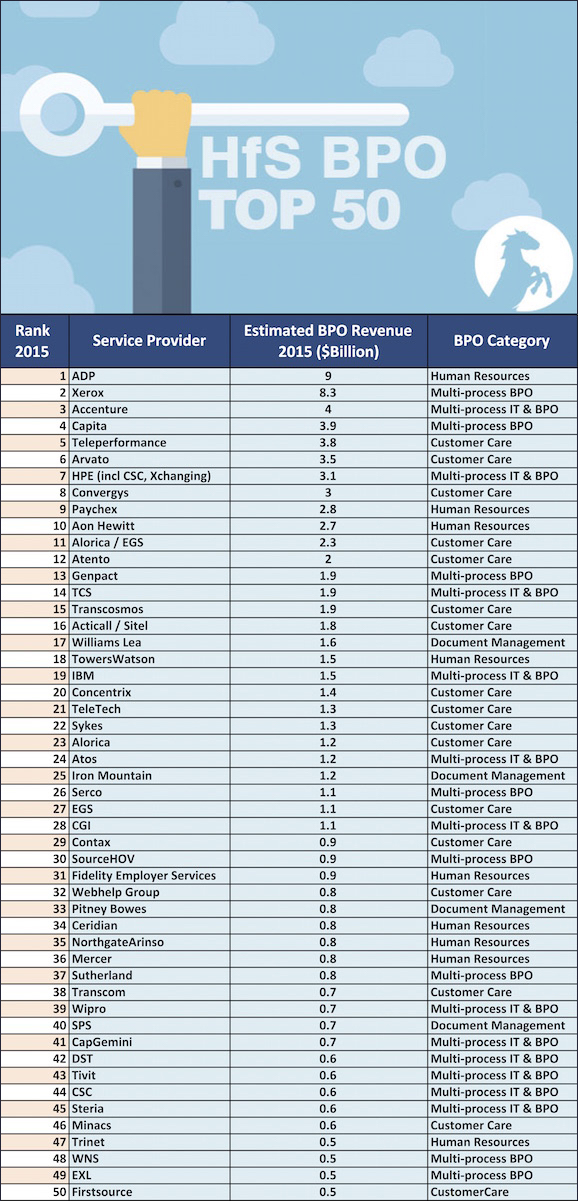

Ever wondered who the leading 50 BPO providers are across the globe, when we add up all relevant revenues? Well, you need look no further:

Source: HfS Research 2016 estimated from services provider financials. Revenues are fitted to nearest calendar year. We attempt to make the BPO services numbers as close to HfS definitions as possible. The market primarily used for this list is the horizontal BPO processes of F&A, HR, Customer Care/CRM, and Procurement. Some industry-specific back office processes are included but we have excluded specialist categories, for example, banking securities.

We have segmented the providers into 5 broad categories: HRO specialists, Customer Care specialists, Multi-process BPO, Multi-process IT & BPO and document management providers. The specialist areas: document management, customer care and HRO should be fairly clear—the vast majority of the services these company provides in BPO is related to this category. The IT multi providers and BPO multi providers—divides the companies that provide multiple types of BPO services into those with an IT heritage and those without. These categories are subjective; we based these splits partly on the type of services they provide and individual company background. For example, Accenture provides multiple types of BPO service and has a sizable IT services business so we have described as a IT multi.

HfS subscribers can download the full report, authored by Jamie Snowdon, Barbra McGann and Phil Fersht by clicking here

Paris headquartered Workday specialist service provider, everBe, recently announced the opening of a new ‘Global Excellence Service Centre’ in Bordeaux, France. everBe selected Bordeaux from a list of 10 locations, because, to quote the CEO, Jean Manaud:

“Finding a location where our staff could raise families and enjoy a quality life was a major criteria for us.”

I have read hundreds of press releases over the years of service providers opening delivery centers or Centers of Excellence around the world, to support local clients and/or be the hub for a particular solution capability. Typically, service providers highlight the ability to offer local support, with resources who understand local culture and language, and generally make local enterprises feel understood and loved. everBe will of course tick this off as well, but it recognizes that the most important element is to attract good people and retain them. everBe aims to support Workday Human Capital Management and Financial Management deployments and management services from this center, to which it wants to attract 30 consultants in the first round of hiring.

everBe has actually considered what people need to be happy in a job. It’s way beyond just having a stable job, the opportunity to advance skills, and getting a good salary. It’s also about actually liking where you live, and being happy there with your family.

Wow. The service provider pendulum is definitely continuing to swing towards focusing on its people.

I started playing Pokemon in college. More or less at the same time, I watched my first sci-fi movie Minority Report, which blew my mind and I started imagining the role of many futuristic technologies including augmented reality (AR). I could have never imagined, 14 years later, the combination of these two (Pokemon and Augmented Reality), Pokemon Go would become such a craze, adding $7 billion to a company’s valuation in just a couple of days. It also leads me to think again about the use of AR in engineering services.

Augmented reality has a 360-degree relationship with engineering services.

On the one hand, AR augmented the existing product design, analysis, manufacture and services capabilities and on the other hand augmented reality applications are built using software product engineering.

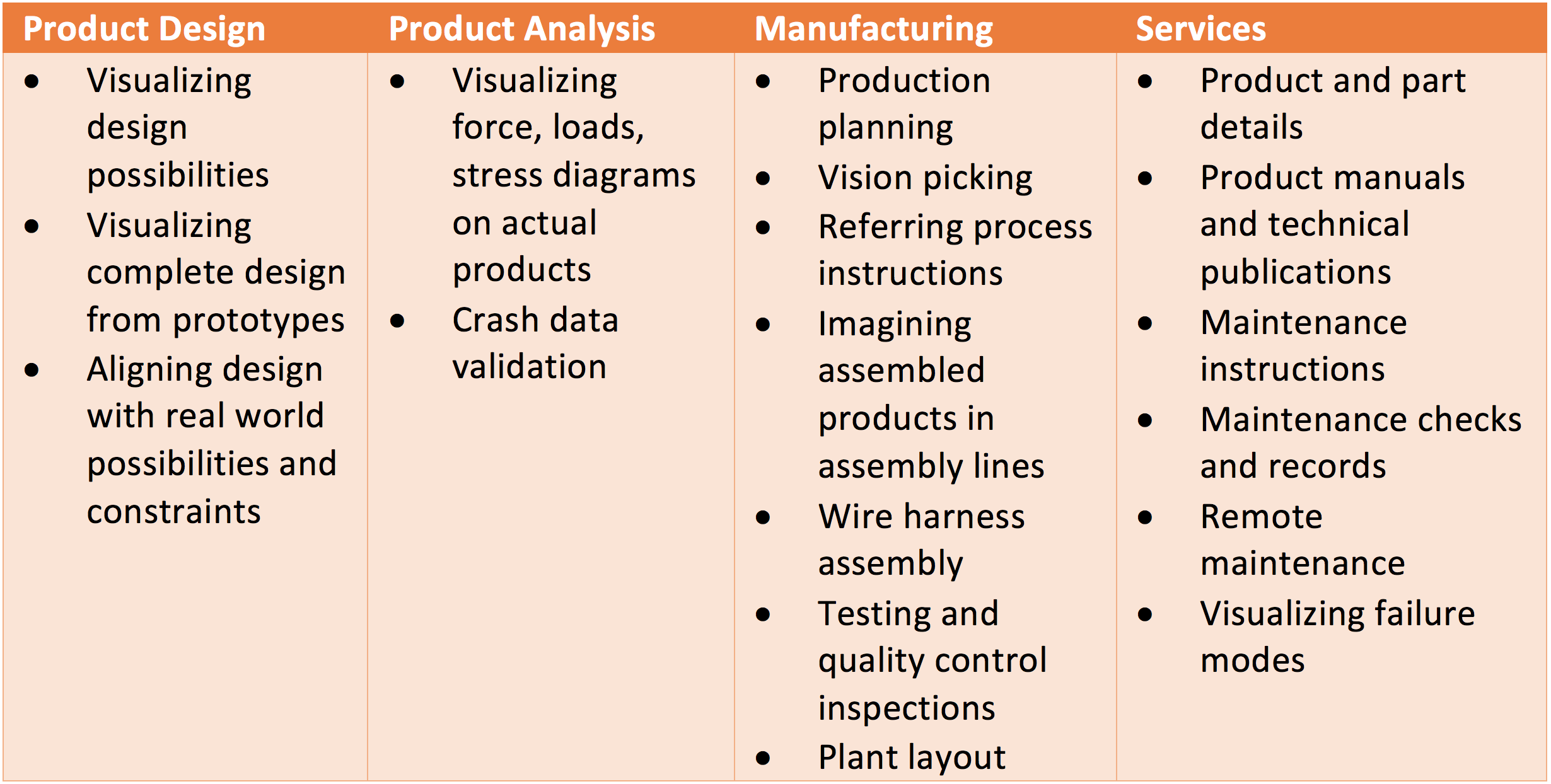

Augmented reality enhances engineering services by adding visualization capabilities and takes the concept of the digital clone to the next level. The capability to visualize real objects can be a very powerful tool across the engineering services value chain of design, analysis, manufacturing, and services and can reduce time and cost significantly, while at the same time improving quality. Some of the AR use cases across engineering services value chain are shown below.

Exhibit 1: Augmented Reality Use Cases Across Engineering Services Value Chain

Augmented reality is made possible because of software product engineering services. The ISVs rely on software product engineering support across design, architecture, development, testing, maintenance, integration, mobility, product management and localization for supporting AR applications. Apart from engineering, AR has strong use cases in tourism, government, entertainment, healthcare, construction, military, logistics, retail, internet, etc. which ISVs will like to capitalize.

AR also has strong use cases in engineering education. I remember how much pain it was, always looking for lab and equipment manuals in the middle of experiments and difficulty in imagining engineering objects from different angles in engineering drawing classes. Augmented reality can help future engineers in all these areas, and much more.

Okay Sherlock, what has Pokemon changed for augmented reality in engineering services? The two-word answer is “User Adoption.”

The augmented reality solutions mentioned above already exists both in labs as concepts and implemented in some of the advanced factories. Almost all CAD ISVs support AR applications. I have tested some of these solutions myself in the labs (the perks of being an engineering services analyst!), and the overall feeling was that it is still not intuitive, or user friendly. The limited success of Google Glass and other similar gadgets have reinforced the belief that user adoption will take time. It was similar to journey of mobile smart phones before iPhone era. And suddenly, the Steve Jobs iPhone moment changed everything and lead to the birth of mobile based unicorns such as Uber, WhatsApp, Instagram, etc.

The user adoption of augmented reality is a good opportunity for all three stakeholders – enterprises, ISVs, and engineering service providers to revisit their augmented reality strategies. Enterprises will have the confidence of higher user adoption among their employees, and can invest in augmented reality technologies further. ISVs can revisit their product roadmaps and prioritize augmented reality related features and applications. Engineering service providers can take the lead and develop/ enhance their augmented reality expertise and should even look at inorganic options too, with many potential AR startups emerging in the industry such as nGRAIN.

To conclude, this Pokemon phenomenon may be a fad or it maybe we are looking at that Steve Jobs iPhone moment which changed user adoption forever. Whatever the case maybe, we will be keeping track of AR developments in engineering services and include augmented reality as one of core areas in our upcoming Industry 4.0 Blueprint.

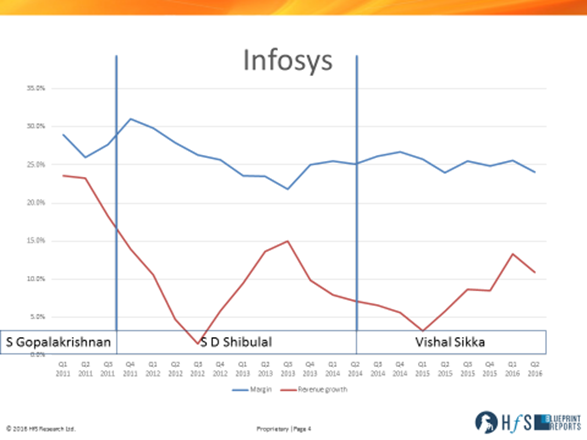

HfS produces a roundup of the quarterly financial results (see our recent one for Q2) – which means we have to wade through lots of financial data and listen to quarterly calls. We also read various bits of commentary around the performance. One thing that always surprises me is how much commentators make of one single set of results and even one small part of those results. I ought to say that I look at the results as indicators for the market as a whole and the individual supplier performance. I tend to focus on annual changes rather than quarterly changes. So I am always a little shocked when the bigger picture is lost. There’s nothing worse when investment analysts and market pundits take such a short term quarterly view of the world, so let’s take a step back and look at it long term.

When I looked at Infosys Q2 2016 results (I use calendar quarters not fiscal – I am referring to Q1 2017 fiscal) I thought they looked OK. Growth was OK, down from the predicted growth, but round and about on par with the overall market performance – and certainly better in market terms than the last two years, except last quarter. Operating margin looked OK / consistent with previous performance. While I understand there are other metrics to measure success – I think this shows a pretty good showing, nothing concerned me.

Then I see the commentary which seemed to suggest the CEO was doing a bad job and lots of quite negative thoughts, disappointing results, etc… – mostly concerning the forecast adjustment. I certainly get the value in accurate forecasting, and consistency in forecasting well is a sign of smart leadership. However, in a market that is going through the major upheavals seen in IT and BPO services at the moment, the ~10% growth year-on-year enjoyed by Infosys is at the top end of the scale in performance terms. To put this in context, Accenture’s last quarter was not as good, and neither was the stalwart TCS. We have yet to see other contemporary’s Cognizant and HCL Q2 results which may show an equivalent dip.

Because of the criticism leveled at Vishal Sikka – I looked at Infosys’ long-term performance and mapped against each CEOs tenure. Looking at the chart, the financial performance during his reign seems to be pretty good. With increasing revenue growth and stable operating margins. This quarter has shown a modest drop in growth of a couple of percentage points (from 13.3% or 15% in constant currency in Q1 to 10.9% or 12.1% in Q2), but it just seems too early to say this is a trend.

The bottom line: you cannot judge a provider’s performance effectively with one set of results.

Moreover, without seeing some of the other results, it is difficult to gauge – as success can really only be measured in market terms and is relative. However worrying any dip in growth is, we will not know if it is a problem until next quarter, after all the results are out.

Buyer: “This service provider delivered no innovation, thought leadership, or long-term best practice management advice for my business process.”

Me: “Did you ask them for any of this?”

Buyer: “Erm….no.”

Alright then. It’s funny how many times I’ve had a similar conversation with IT services clients over the years. Luckily at HfS we take into consideration that there’s usually two sides to every story – otherwise some service providers would consistently be scored badly in any innovation or thought leadership category in our research reports. So, why is this happening? It seems to come down to one of three reasons:

The beauty of hindsight: Buyers often don’t know what they need until the end of the engagement, particularly in a deployment project. At that point, they can very easily highlight all the processes, approaches, methodologies and advice that would have been fantastic to have had access to prior to implementing the solution. Service providers do however have a responsibility to explain all of their capabilities and all the points the buyer needs to be aware of before starting the implementation. It would then be up to the client to decide whether they want to contract the service provider for these skills, use in-house skills, cross that bridge at the appropriate time, or frankly ignore it.

Not required: Sometimes buyers engage in a detailed consulting project with a consulting provider, and then use a separate implementation provider. This is particularly true in the SuccessFactors services market. Clients assume that every possible eventuality has been considered in the consulting phase. The implementer is often selected based on its technical capabilities and its cost effectiveness. Complaining that this provider did not provide any thought leadership or viewpoint outside of specific module implementation is simply unfair. Often the service provider has successfully completed the exact work it was contracted for, which in my book counts as a successful project. Again, it’s probably wise for service providers to point out to clients exactly which skills and engagement levels to expect for the price the client is willing to pay.

It’s all Horses for Sources: Sorry for the pun, but frankly, every enterprise defines innovation or thought leadership in a different way. I once had a mid-sized buyer enterprise with zero sourcing experience tell me that their first engagement with an IT service provider was ‘out of this world! They put the stuff in, they were very nice, and it all worked!’ Whoopee. I doubt a large enterprise who has been outsourcing for decades would get as excited about this achievement.

So, buyers and service providers alike need to have the innovation, thought leadership, or whatever they care to call it, conversation upfront. That way the service provider knows exactly what they are required to deliver and the buyer knows exactly what they will get and what they’re paying for. Remember: if you want some value add, I’d tell someone.

So it’s finally happening. Enterprises are using SaaS applications to run important processes, such as CRM, HR and even Finance. Moreover, some even have an enterprise cloud strategy that requires departments to consider cloud options alongside on premise solutions, as part of process transformation projects.

Until recently, enterprises dabbled in SaaS applications to support specific, isolated needs. Did you hear about the Marketing Manager who purchased Salesforce.com on his credit card without any recourse to the IT department? We did unfortunately. Salesforce.com is one of the most established SaaS applications in the market, but initial deployments were seldom aligned to an enterprise-wide CRM strategy. Second waves of Salesforce.com implementations have been more strategic. Workday and SuccessFactors implementations have also taken off in the past few years as enterprises realize the importance of having a modern HR department running programmes to hire, motivate and retain the best talent. Workday’s Financial Management product is also increasing in popularity, with some enterprises deploying this before the HCM module.

But SaaS adoption brings with it many differences from the on premise world. Enterprises need to consider the organizational change management implications for one. Engagement models with service providers are also changing. The service providers, for their part, need to understand the different types of services required to effectively support SaaS applications. Some have invested early to be prepared. But for others, this all seems to have crept up on them rather quickly. The same might be said for research and advice for service providers and buyers alike in the SaaS services market.

Luckily, HfS has been tracking this market for some time and produced a wealth of information in just this past year to help both parties. This includes three Blueprint reports:

Clients with the necessary subscriptions are lucky enough to have access to all the detailed service provider profiles in these. But we have also published several Points of View and Soundbite notes that are FREE to anyone who cares to visit the site! These include:

I’ve been busier than I thought! And there’s more to come. The updated Workday Services Blueprint and the Salesforce Services Blueprint will be published before the end of 2016, with all the accompanying buyer and service provider oriented supporting notes – all free of course.

So stick with HfS. We’ll keep you posted as this hot market evolves over the next few years.

This is a question you expect to get as a forecaster, and it is not always the easiest to answer. It is always troubling to be asked to speculate on a market size where the outcome is so uncertain. However, this is not speculation upon speculation. This is not like forecasting the impact of Grexit (Greek exit from the EU) – even though this has not happened.

Brexit has happened, and we should have a position, even though the ramifications are far from clear, and it is still in its infancy. The current uncertainty is broadly focused on exactly what the terms of the EU departure are and the on-going relationship the UK will have with the EU. As forecasters, we have a choice to make as to which scenario we choose as the likely option or the middle ground. Our thought process is likely to develop over the next year, and this is going to change the forecast.

So, our workload is likely to increase as we will have to consider the Brexit model and adjust over the next few quarters (at least). Even the most confident of forecaster should reflect on what they have done and make adjustments as things unravel. The old maxim that the analysis is only as good as the best available data rings true here.

In short, how do we see the impact of recent events? We think it is safe to assume that the level of uncertainty currently is going to have an impact on the IT and business services markets, regardless of any eventual outcomes. We have already heard services firms mention Brexit in negative terms during financial calls. Although, Infosys CEO Vishal Sikka said it might lead to uncertainty in the near term, he said it would also lead to opportunities in the medium-to-long term. TCS’ position was similar, with its Chief saying his executives will be talking to their clients and watching what happens.

Typically, recessionary periods / periods of economic uncertainty impact the IT and business services market in two waves. Firstly, a slowdown in discretionary spend and some decision making is suspended/slowed. We are loathed to forecast a big delta at this stage as services buyers have weathered many economic issues in the last six years and this may just be seen as one more thing. If this were an isolated uncertainty, it might have had a larger impact, but in a stream of issues, the impact may not be as severe. It does not, as some observers believe, mean an automatic uptake in external services to augment the increased scarcity of internal resources or as a cost cutting measure. Any uptick is countered with the uncertainty. The secondary effect mean organizations are likely to make investments to make themselves agiler and less susceptible to economic issues in the future – this is where we see an increase in outsourcing, more adaptive operating models and, inevitably cost cutting.

Bottom-line: The short term impact is likely to be wracked in uncertainty. However, medium-long term opportunities could well arise. To conclude, our current position is that there will be a short-term impact on market growth in the UK, which will ripple across Europe, but this slowdown will be caused by some increased market uncertainty and – for the most part – the services market will continue to chug along unabated. We will see some opportunity as the buy side adjusts, but, given the process is going to take some time, it is too early to predict the timing or scale.

Two years after our inaugural Blueprint in Mortgage BPO Services, we took a fresh look at this industry…here’s announcing the findings of the HfS 2016 Mortgage As-a-Service Blueprint!

The concept of delivering mortgage As-a-Service, using plug and play digital business services is still in its infancy. We’re not quite at “push button, get mortgage” as an industry – and the verdict is out on whether this is the right message to send for a lending environment that is still rebuilding itself, seven years after the 2008 housing crash. How do you do this without raising eyebrows? You’ll have to ask Quicken Loans, as they learn from the backlash of their Super Bowl campaign with that very slogan.

Mortgage is complex, sensitive given its recent history, and needs to have a different approach and response to “digital disruption”.

Despite this sensitivity, other industry forces still march on; regulation, homebuyers and a new breed of disruptive fintech firms are steadily shifting the entire mortgage industry towards generally being more digitally enabled. Lenders have this big ask today: how to carefully balance their investments in new technologies, with changing consumer needs, volatile rate environments with rampant M&A, their company’s own appetites to write off/augment internal legacy systems, and all while continuing to remain compliant in an increasingly watchful regulatory environment.

Borrowers are increasingly looking for three key benefits in their interactions with agents, brokers, and lenders:

Simplification in the processes, handoffs and interactions

Transparency in the loan terms and costs, application progress

Control in document and information exchanges, decision making

The use of digital technology can greatly help lenders to achieve these experiences, in both facilitating interactions and in creating operational efficiencies at the back-end to speed up applications and free up loan officers’ time. In becoming digitally driven, lenders have a long way to go in thinking about e-mortgage beyond digitization, and borrower experiences that are built on new engagement strategies, especially as the market shifts to more purchase originations and persistent refinancing dictated by flat-lined interest rates.

What’s changed since the inaugural Mortgage Operations Blueprint in 2014…

HfS believes that the Mortgage Operations market for both residential and commercial loans is on the cusp of a significant transformation. Several lenders in our research described their mortgage processes as complex, broken and in need of help to compete with non-traditional lenders and faster cycle times. Said one, “Our industry needs to go through massive business process reengineering efforts…so many lenders don’t have processes documented still. We need to start there [with our providers], to find ways to improve cycle times and create better experiences for borrowers.”

There is a marked departure in the market dialogue, away from labor arbitrage and manual “lift and shift” processes, and towards using a combination of technology platforms, analytical insights, automation, digitization and other accelerators to redesign processes and drive more value in sourcing engagements.

Some areas that have changed since our last Blueprint include:

With greater purchase originations, we see the mortgage operations market more broad-based in the work sought from lenders. Accordingly, service providers have grown both their technology and process capabilities in originations and servicing in the last two years, with a few that have foreclosure and default management work today.

Great examples of service provider capability in creating and embedding analytical insights and data into different parts of the mortgage value chain, understanding the key triggers/outcomes in the process such as predictive modeling for loan origination to help prioritize underwriter time and understand likelihood to close.

New services and technology accelerators coming from service providers to address regulatory pressures such as the audit and due diligence reporting back to CFPB, which is increasingly getting more complicated and frequent. Clients expect more guidance and recommendations in regulatory changes and their impact on technology systems/processes/data to maintain compliance.

Service Provider Landscape and Blueprint Grid Performance

Our HfS Blueprint methodology assesses service providers based on two critical axes: Execution and Innovation. We gather data to support our analysis from client reference interviews, market interviews, RFI submissions and exhaustive service provider briefings.

In this Blueprint, we identified four As-a-Service Winners: Accenture, Cognizant, TCS and Wipro. These service providers have the strongest vision for As-a-Service delivery in the mortgage industry, and are driving collaborative engagements with clients to bring this vision to life. They are making significant investments in future capabilities in automation, technology and borrower experience to continue to increase the value over time.

The High Performers in this year’s Blueprint are a highly competitive set of service providers: Genpact, Infosys, ISGN/Firstsource, Sutherland Global Services and WNS. They have high execution capabilities and are growing their client bases as a result of investments in future capabilities and innovation. These service providers have the pieces in place for As-a-Service delivery, and need to focus on consistently bringing these capabilities to clients and scaling up with broad, multi-client solutions. We expect them to challenge the Winner’s Circle leaders in the next couple of years, with each building on unique strengths and assets in this vertical.

We see Unisys and Xerox as the Execution Powerhouses. These service providers are strong in operational excellence with ubiquitous technology platforms in their respective markets, and need to focus on value chain expansion and innovation in their services stack.

HfS Predictions for the Next 2-3 years of Mortgage As-a-Service

The biggest developments we see in the mortgage market in the next few years are:

Greater Alignment of Services Around MOS Platforms: Service providers like Wipro, Accenture and Genpact that have made investments in acquiring MOS technology vendors have goals of providing a broader, end-to-end portfolio in mortgage, including people, process and technology. This is an indicator of a vision for providing Mortgage As-a-Service. However, most of the acquisitions made were of independently branded software solutions, accompanied by their own branding legacies. Infosys took a different approach with its startup acquisition to create CreditEdge. In the next two years, we expect these service providers to further articulate and demonstrate how these technology buys change their value proposition, towards greater clarity and examples of delivering Mortgage As-a-Service.

Mainstreaming of Process Automation: It has taken a while for process automation to cautiously make its way to the forefront of conversations in mortgage operations, due to its troubled “robosigning” past. We are now seeing greater understanding by both service providers and buyers to start thinking practically and implementing different kinds of automation technologies (RPA, intelligent OCR, etc.) across various parts of the mortgage services value chain. Today thus represents the early vanguard and the arrival of RPA in mortgage, leading us to believe that adoption will be fairly rapid over the next 12-18 months.

Digital Driving Disruption at the Top: Several of the big lenders that HfS interviewed are still playing the “wait and watch” game on digital disruption, in particular the strides made by fintech startups and non-traditional banks in the mortgage industry. While “push button, get mortgage” as we discussed above might not be the path for all the Top 50 to go down, lenders are initiating more conversation and strategy around how digital components can help them look at traditional operations differently. Service providers will have a big role to play in this, from a process reimagining perspective, as well as ultimately configuring the digital components that link these activities back to onboarding and origination platforms.

For more detail –including visuals of the market activity and analyses of the service providers—click here to access and download the HfS 2016 Mortgage As-a-Service Blueprint.

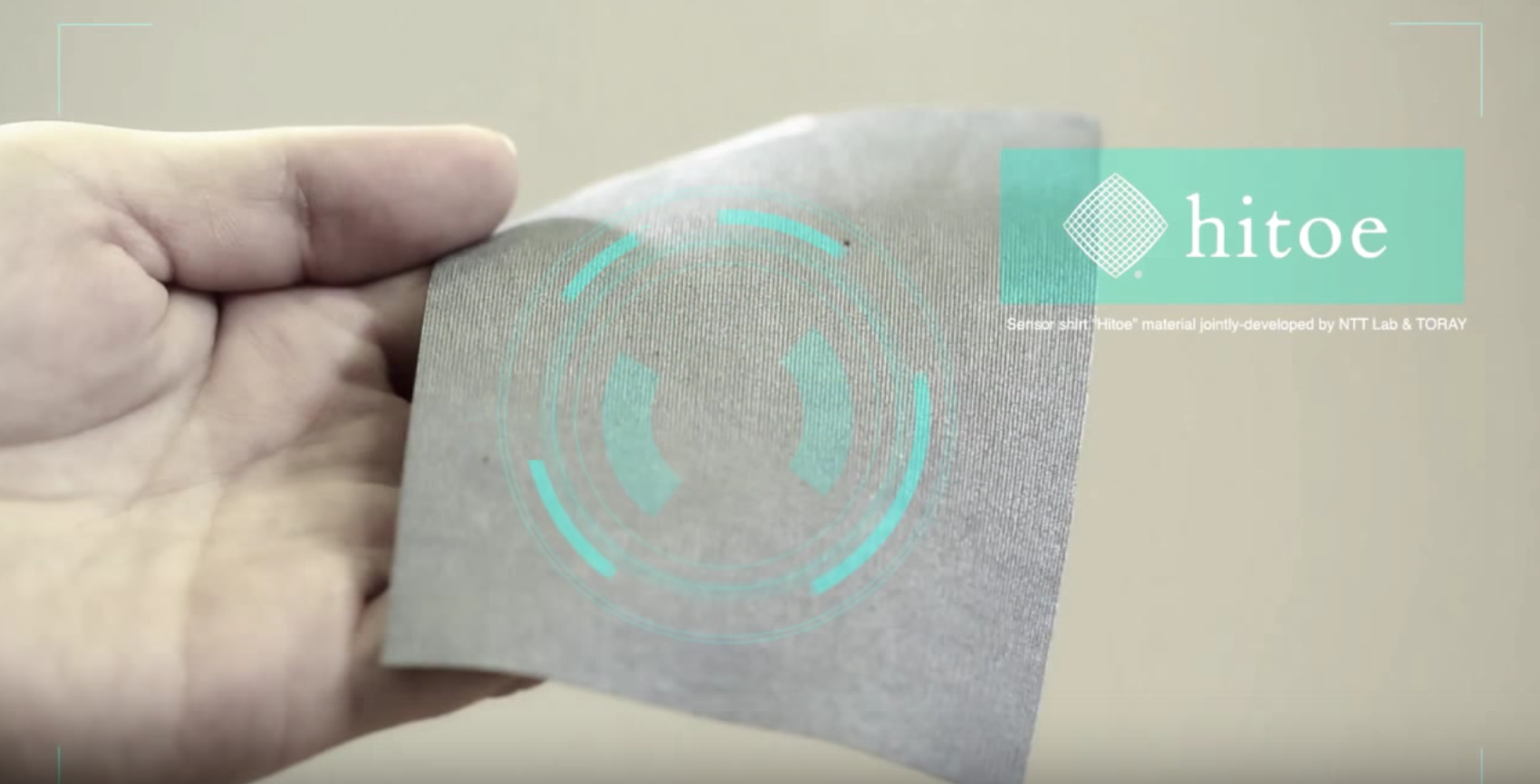

We hear a lot about the cost of healthcare, among these being the high cost of additional treatments or elongated stays when patients fall in hospitals, and of readmissions when people who go home after treatment don’t follow care plans. It’s amazing to think that a solution could involve something as simple, cost effective, and comfortable as clothing, such as a garment made with Hitoe® (That’s hee-toe-ay, not high-toe!).

Hitoe is a fabric that is also a sensor, contributing heart rate and brain and muscle activity to analysis for health and care analysis and plans

Earlier this week, Adam Nelson, VP Healthcare and Pharma at NTT Data, came by the HfS Research office in Cambridge, Massachusetts, with a shirt. This shirt is essentially “living data collection wear.” When someone wears it, the fabric collects and transmits data such as heart rate and muscle activity. Data transmitted from the shirt shows (as we saw firsthand, thanks to Adam’s clothing of choice that day) posture and movement through a 3D rendering, and heart rate through an electrocardiogram. The system it feeds can be programmed to send an alert, such as when someone makes a sudden dramatic movement like a fall, or even a change in posture that indicates getting up (picture a patient that shouldn’t be getting out of bed), enabling a care giver to intervene or provide help faster. It also shows data on muscle activity, helping to determine movement versus atrophy, as input for rehabilitation plans.

There are healthcare machines that capture and transmit the same type of data. But a garment made with Hitoe fabric could mean one less “hookup” during care and treatment. It also means that someone could be monitored remotely versus spending time in a hospital for the same reason. Also, compared to machines, the fabric seems pretty comfortable to wear, and is less expensive to buy and use at scale. So it could help address patient comfort, refinements in care plans, hospital and care costs, and even less waste in the environment. Hitoe, a partnership between Toray Industries and NTT, uses nanofiber technology, bringing the threads incredibly close together, with an electropolymer adhered, to monitor vital signs and send signals to the cloud (but it can also be put in a washing machine). Then, using something like the NTT DATA Optimum Exchange integration platform, the data can be combined with electronic medical records and other data input for patient data analysis to impact diagnosis, treatments, and care plans. And, by the way, creating a services opportunity too, for NTT DATA (and eventually, for Dell Services as the two come together).

A solution using Hitoe doesn’t require a lot of adjustment in a person’s life to use it, increasing the potential for engagement in their own health and care

This example of “IoT” caught my attention in particular because it is so approachable—it’s clothing, the most literal example for the new wave of “wearable” technologies that are becoming more commonplace. The fabric can also be sewn into a ball cap, for example, and capture brain activity, for use in diagnosis or treatment. While one version we saw fit snugly, to be used by fitness and sports programs, another looser fitting garment option (nylon) feels like the softest sheet with the highest thread count imaginable. The key is to find the balance of comfort and practicality—it has to consistently capture and transmit data that is uninterrupted by shifts in the clothing, and clinicians needs to trust this new data source. NTT DATA is working with an array of partners, including IndyCar driver Tony Kanaan whose team uses the heart rate and muscle activity data analysis to coach him during races, staving off fatigue and arm cramps. Hitoe-based clothing, worn comfortably and automatically transmitting data that can be combined with electronic medical records and monitored and analyzed, seems to hold promise for increasing the comfort and reach of health and care, as well as the impact.

We’ll wait to see how NTT DATA unpacks the potential that Hitoe represents for healthcare. In the meantime, here’s a video (link) of Tony Kanaan tearing up the IndyCar tracks as he tests out Hitoe in the field—transmitting heart rate and muscle activity that helps his team support his performance—that may provide greater inspiration that any description.

As such, organizations now need to take on more refined, able and focused hiring mechanisms to fill roles. The rise of employer-focused social media sites such as Glassdoor have added a further level of complexity to the game, with employer reputation now more important than ever.

So what does this mean for organizations out there trying to lure in and keep top performing Millennials? Well if the literature available is to be believed, you would have to include mobile and social enablement in your hiring practice that allows for one-touch functionality in processes including application and calendar coordination. While this is a great starting point, unfortunately it’s where many recruiters stop in their approach to Millennials.

Too often, Millennials are defined purely by the channels by which they engage the world.

This is a drastic over simplification of our generation and one that seems to miss the key point. This is a young generation roughly aged between 22 – 39 years of age. People in this age bracket, especially at the lower end, are in the first stages of establishing their position in the world regarding fashion, subculture and ideals. Why don’t recruiters appeal to this key element?

Consider some of the leading consumer brands in the world, Coca-Cola, Levi, Pepsi, Guess, American Express, Ralph Lauren. What do their (extremely successful) marketing campaigns all have in common? They very rarely sell a product, but rather they sell a lifestyle. Just think of Coca-Cola’s annual Christmas advertisements.

So why aren’t large organizations, desperate (or should be) for Millennial talent, doing the same in their hiring strategies?

I have friends who work in top end digital marketing agencies, working for some of the most visible brands in the world, who put out one-line job adds on LinkedIn that link back to a bland job description on a blank landing page. No wonder they can’t fill roles with the right people.

Companies need to market roles to Millennials that sell a lifestyle, not just a job description.

So what can organizations do in this regard?

Firstly, the marketing content behind a recruitment campaign needs to be on point, including images and language that speak to the lifestyle one would associate with working for the company. Put simple job descriptions in context and focus on the type of person (such as personality, interests, style, etc.) that succeeds in this role.

Secondly, internal company structures need to match this lifestyle. Organizations need to consider dress code, desk arrangement, hierarchical structure and internal silo’s making sure these match the lifestyle portrayed.

Thirdly, location, location, location. These are young people and at the younger end of the spectrum, many won’t commute in from any great distance. Therefore, office location needs to be attractive and also fit the lifestyle portrayed. Selling a young, hip, urban image can be challenging when your offices are based in Chipping Norton…

Overall, organizations need to better align with the candidates they are targeting. A focus on lifestyle is something the advertising industry has been doing for years and an area where hiring strategies need to catch up.