In response to disruptive global events such as geopolitical tensions and continuously changing shipping guidelines, enterprises are increasingly prioritizing making their supply chains resilient and agile. There is a significant emphasis on digitalization, integrating AI, IoT, and analytics technologies to improve network transparency, efficiency, and security. Sustainability has also become crucial, as businesses aim to minimize environmental impact and uphold ethical practices in their supply chains. These changes not only address regulatory pressures but also align with consumer expectations for responsible business practices. Overall, these shifts are transforming supply chains into more dynamic, interconnected, and accountable systems capable of meeting the complex demands of the modern global market.

There’s a growing trend toward creating collaborative ecosystems that include suppliers, partners, and even competitors. This approach leverages shared technology platforms and data insights to collectively drive efficiencies and innovate supply chain solutions.

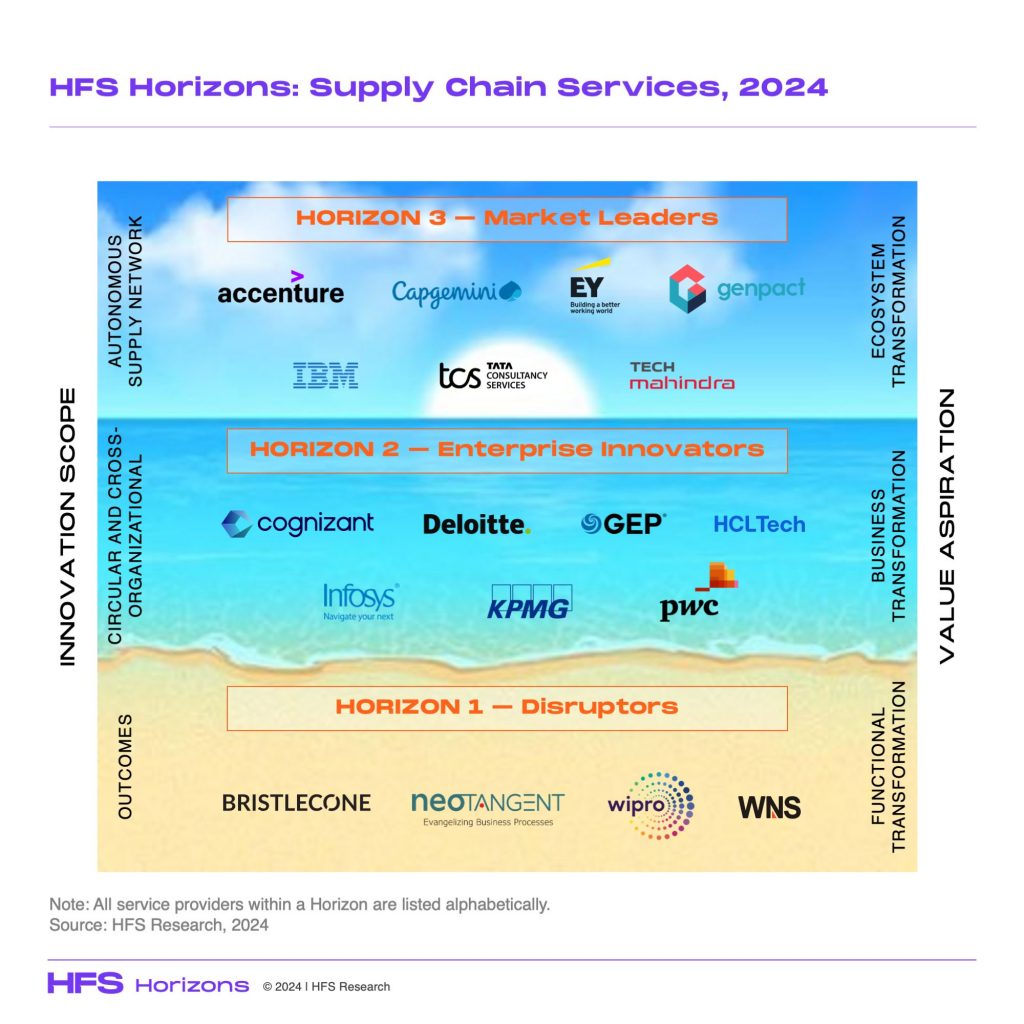

In the HFS Horizons: Supply Chain Services 2024 study, 18 supply chain services providers are analyzed and profiled. Seven of these providers are identified as leaders in Horizon 3, focusing on ecosystem collaboration. Seven are identified as innovators in Horizon 2, excelling in cross-functional alignment, and four are identified as disruptors, primarily working on function-level transformation.

Exhibit 1: 68% of upcoming supply chain investments in the next 2 years will be in Horizon 3

New service offerings coming into the fray

Generative AI integration: There’s a significant push toward integrating GenAI across various facets of supply chain management, from planning and logistics to customer interaction and compliance. This technology is expected to enhance automation, improve decision-making, and create more dynamic and responsive supply chain systems.

Sustainability services: Providers are increasingly offering services to achieve sustainability goals, such as carbon footprint reduction, lifecycle assessments, and sustainable sourcing strategies. These services are crucial for companies aiming to meet regulatory requirements and consumer demands.

Digital twins and advanced analytics: The use of digital twin technologies and advanced analytics is being expanded to offer more detailed insights into operations, enabling predictive maintenance, and optimizing supply chain resilience.

New buying patterns are surfacing

Shift toward subscription and as-a-service models: There’s a noticeable trend toward subscription-based and as-a-service purchasing models. These models provide flexibility, reduce upfront costs, and align with the increasing preference for OpEx vs. CapEx expenditures in corporate budgeting.

Increased demand for customized solutions: Enterprises are looking for solutions they can tailor to their specific needs, reflecting a move away from one-size-fits-all offerings. This customization is particularly prevalent in areas such as AI implementations and data analytics services.

New scope of work on the table

Global expansion: Organizations are increasingly designing supply chain solutions to support global operations, with a focus on integrating cross-border supply chains and managing international compliance and logistics challenges.

Focus on resilience and agility: Services are being developed to enhance the resilience and agility of supply chains, enabling enterprises to respond more swiftly to market changes and disruptions. This includes tools for better risk management and dynamic rerouting of logistics in response to external shocks.

New operating models being adopted

Collaboration across sectors: There’s an increasing emphasis on collaboration across different sectors and industries to optimize supply chain operations. This involves partnerships with tech companies, logistics firms, and even competitors to pool resources and capabilities.

Leveraging big data and IoT: The scale of supply chain operations is expanding with the integration of IoT and big data. These technologies enable teams to handle vast amounts of data across extensive networks, improving real-time decision-making and operational efficiency.

The Bottom Line: The shift toward deeper digital integration and an evolved operating model is transforming human-dependent supply chains into low-touch collaborative supply networks.

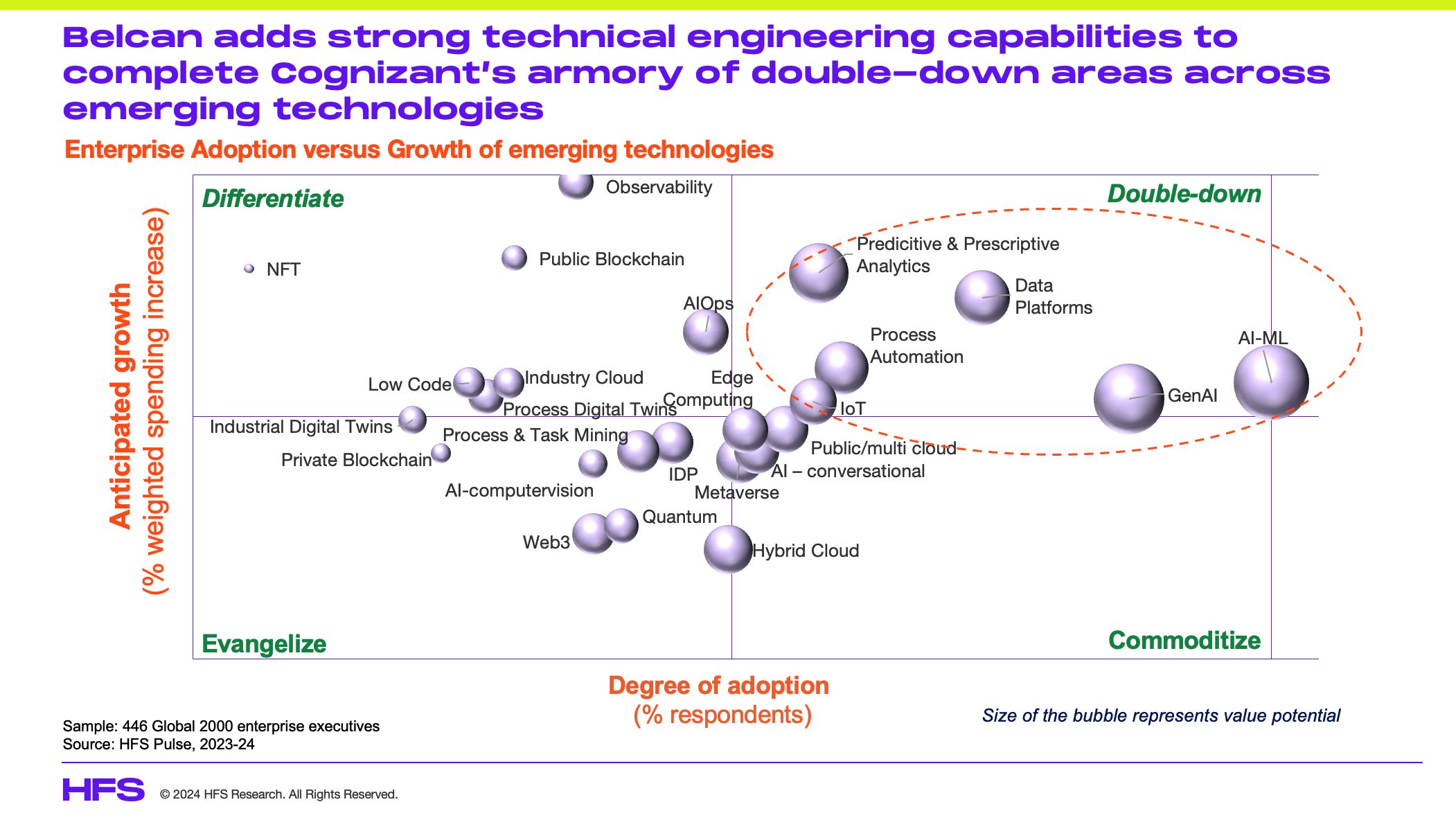

Cognizant’s bold $1.3B acquisition of Belcan isn’t just a headline grabber; it’s a game-changer in an IT services market that’s hitting a plateau:

Growth Catalyst: Engineering services, where Belcan excels, is the rocket fuel Cognizant needs. While IT services see modest gains or losses between -5% and +5%, engineering services are soaring with growth rates over 10%.

Tech Arsenal Upgrade: Belcan’s technical engineering services prowess adds serious firepower to Cognizant’s already robust suite of emerging technologies and digital engineering capabilities. With formidable AI, automation, and analytics capabilities, Cognizant now stands tall across all high-growth, high-adoption technologies:

Diverse offerings and domain expertise: Belcan brings expertise in both engineering and traditional IT development, testing, and integration capabilities across Aerospace and Defence, Automotive and Industrials. This strategic expansion and capability addition in global locations complements Cognizant’s existing technology expertise.

Niche Industry skills: Belcan brings deep technical expertise in high-precision sectors of Aerospace and Defence, Automotive and Industrial – industries where subject matter expertise is crucial to delivering complex projects. These industries are investing in digital threads, MBSE, integration of operations and enterprise technologies, building sustainable solutions and supply chain resilience which is Belcan’s sweet spot.

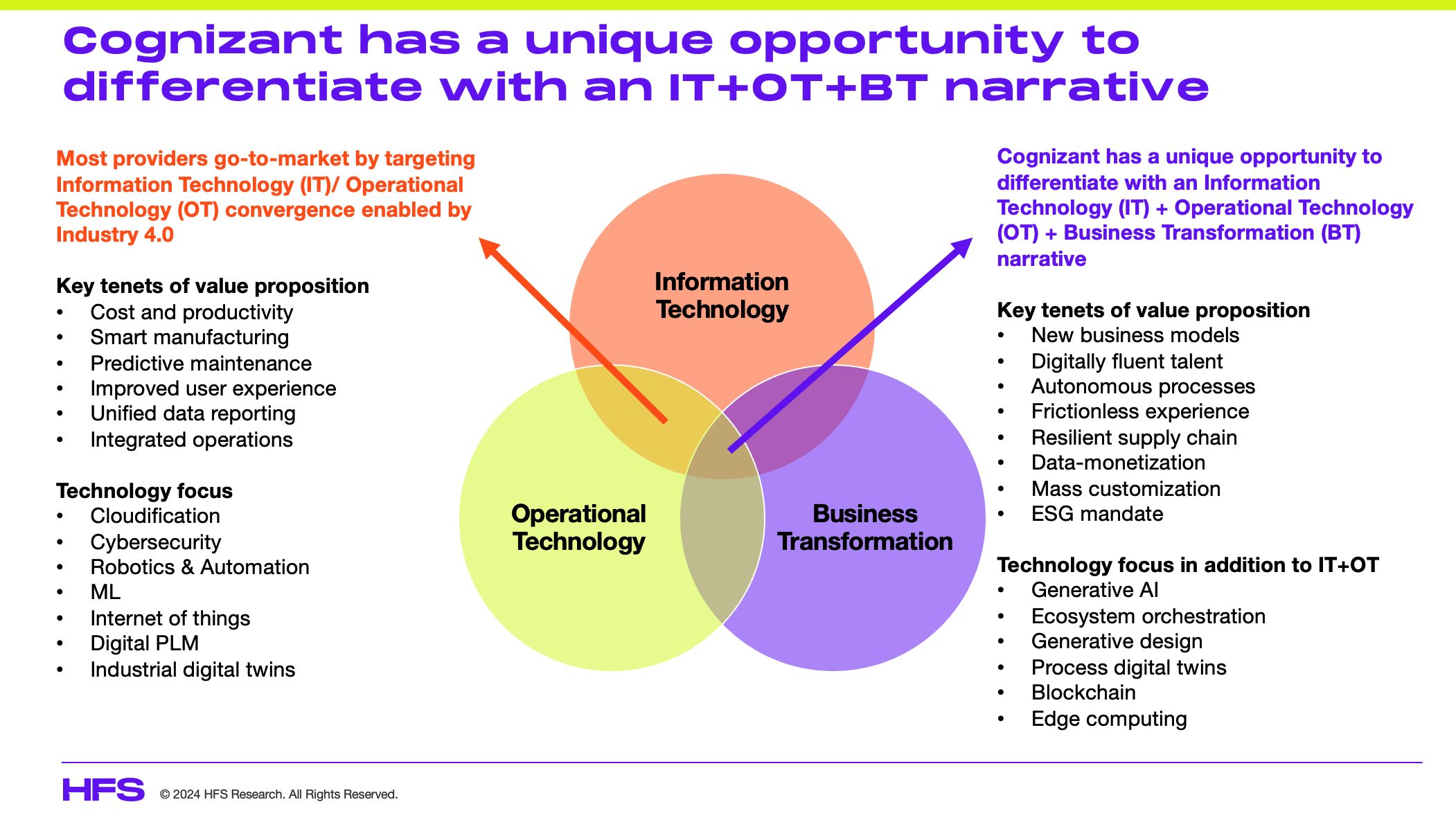

Strategic Differentiation: In these asset-heavy industries, Belcan’s expertise gives Cognizant a unique edge in large-scale transformational deals. This expands Cognizant’s digital transformation capabilities into aerospace and defense industries that are currently in a growth trajectory and are undergoing technology disruptions, compelling them to think of new product development, efficiency in operations, and business model transformation. This acquisition positions Cognizant as one of the few major players capable of seamlessly integrating IT (Information Technology), OT (Operational Technology via Belcan), and BT (Business Transformation) (See below). Only a few service providers, like Accenture, HCLTech, Infosys and Capgemini, can boast a similar trifecta:

Historically, Indian heritage service providers have struggled with large mergers. But if Cognizant can bridge these gaps, this acquisition could redefine the competitive landscape. However, all this hinges on seamless integration—no small feat given both firms are very different:

Geographical Divide. Belcan’s workforce is predominantly North American, while Cognizant’s strength lies in its substantial Indian presence. Although the value proposition is different, this integration should be similar to Capgemini’s integration of iGate, where European consulting norms were merged with an Indian IT culture.

Budgeting Clash. R&D budgets, Belcan’s domain, operate under different dynamics compared to IT budgets, which are Cognizant’s forte.

Reduce dependency on financial services and healthcare. Cognizant has a high revenue dependency on the financial services and healthcare sector—almost 60% of its revenue comes from these two highly regulated sectors. This deal will help Cognizant diversify its revenue mix. Additionally, the aerospace and defense sector is riding tailwinds due to the demand for travel and geopolitical conflicts.

Major opportunities this acquisition creates for Cognizant

The investment price is reasonable and the investment is almost 100% additive in revenues. The $1.29B acquisition price is very competitive, adding an estimated $800m in incremental revenues to Cognizant, of which 40% is in product engineering and 35% in embedded software. This broadens Cognizant’s offerings far beyond its mainstays of healthcare, life sciences and financial services, which are struggling for future growth in traditional IT services markets.

The post-investment merger is set up to drive synergies and continuity. Cognizant will now boast a $1.8B global engineering services practice under the leadership of renowned Lance Kwasniewski, which includes the acquisition of embedded software firm Mobica early last year. In a similar vein to Jason Wojahn becoming leader of Cognizant’s ServiceNow practice with the Thirdera acquisition, HFS sees this as the smart strategy for Ravi Kumar to expand his team by retaining key leadership talent to continue driving the businesses they built. This helps blend the cultures, retain key talent and ensure continuity.

The aerospace and defence market opportunity is spectacular. The aerospace and defense market is booming in terms of commercial, private, and government spending, which HFS estimates at surpassing $800B this year and $1T in two years’ time. There is also a strong demand in MRO services in the industry and because of Belcan’s OEM experience with clients like Boeing, Airbus, and Lockheed Martin. Belcan is able to service this demand effectively. Being in a position to deliver AI, technology, embedded software, and technical engineering services is a real additive area for Cognizant to exploit in this high-growth sector full of both large enterprises and hundreds of mid-sized subcontractors.

Seizing opportunities in automotive, E&U and industrials sectors, which are going through technology shifts. These industries are investing in new product development and optimizing their manufacturing process and their supply chain, which need industry domain and technical expertise as it is complex high-precision engineering. For example, to seize product engineering opportunities a provider must have capabilities in aircraft design, avionics, propulsion systems and defence technologies in the A&D industry. Similarly, capabilities in vehicle design, powertrain development, and autonomous systems are needed to grab opportunities in the growing SDV and electric vehicles market. The acquisition builds an industry-focused differentiator and is an opportunity to build next-gen technology solutions for Cognizant.

The offshore opportunity is still fledgling and positions Cognizant very strongly. Boeing, Airbus, Collins Aerospace, Pratt and Whitney, Lockheed Martin, and Thales in the A&D sector, and similarly, ZF, Hella, BorgWarner, Volvo, Hyundai, Stellantis, and Ford in the automotive sector have set up GCCs in India. There is also a significant focus on the expansion of engineering-centric GCC centers in India right across manufacturing and other verticals. The market is ripe for expansion, with Cognizant in a very strong position to take on these services.

The opportunity to take engineering and embedded software capabilities into other industries is clear. Huge industries such as medical devices, household electronics, and automotive technologies are rife with demand for embedded software, product engineering, and supply chains. With Cognizant’s focus on bringing Engineering, OT, IT, and BT together, there is a clear roadmap for growth, provided the firm can bring together the differing skills, cultures, and client needs effectively as a holistic and integrated capability.

Bottomline: Cognizant now has a seat at the engineer’s top table, but now needs to ensure it stays there

The deal strengthens Cognizant’s already existing technical expertise and deepens client relationships, creating major new market opportunities. This also puts Cognizant on the industry map for large-scale transformations with strong emerging technologies capabilities, making the firm a formidable player in the engineering services industry with domain and technical expertise. All Cognizant now needs is to cross the integration milestone seamlessly to build on this considerable momentum.

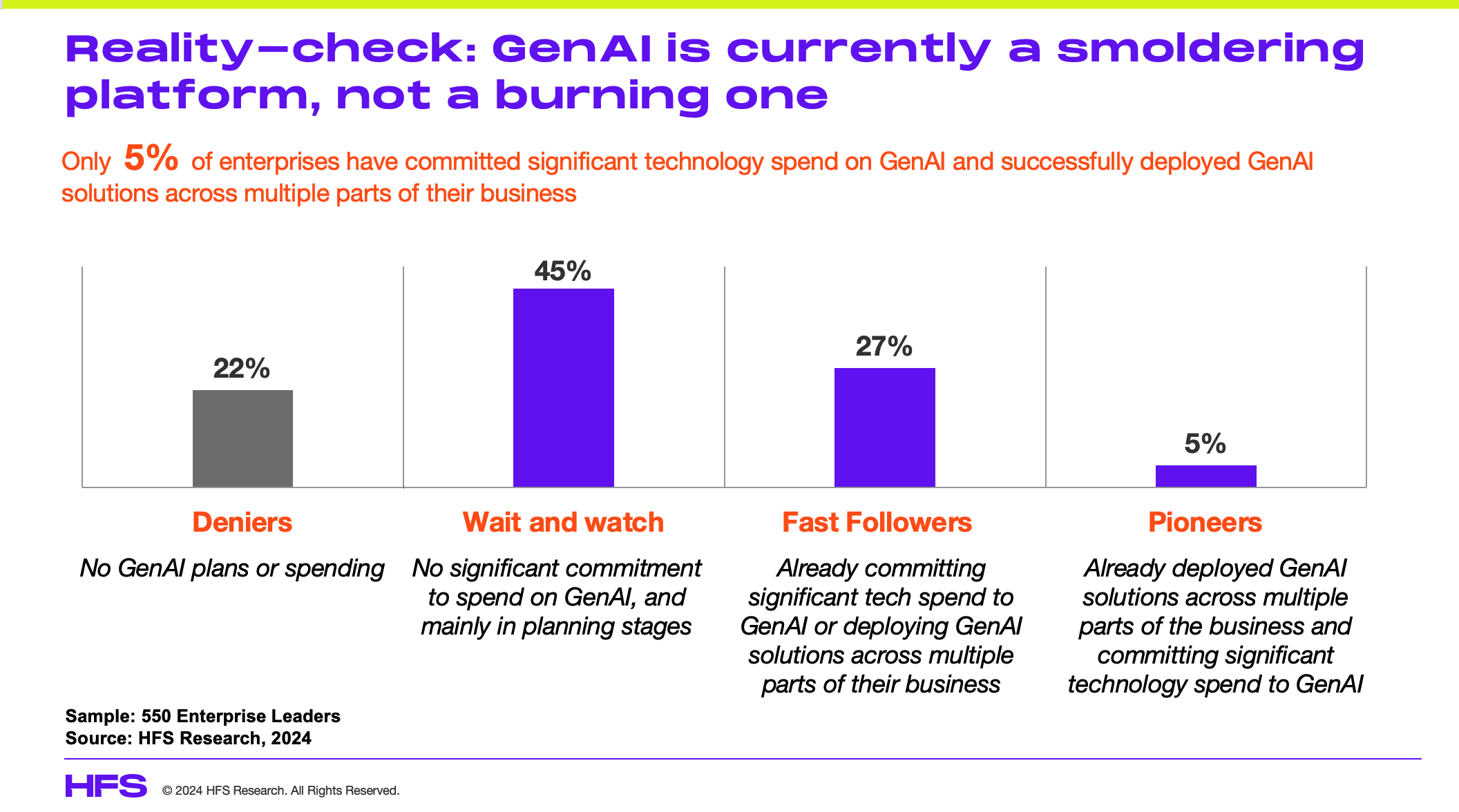

It’s hard to remember that the Generative Era is barely more than a year into its fledgling life since LLMs were cast upon us, and the tremendous excitement that GPT-4 started delivering with all the dramatic improvements helping us create new content and data.

However, our new research* covering a quarter of the Global 2000 shows things have not moved as fast as many of us were expecting, with only 5% of enterprises committing significant technology spend on GenAI and successfully deploying GenAI solutions across multiple parts of their business, and two-thirds doing practically nothing:

So, what will spark enterprises to move faster with GenAI and keep it from the graveyard of so many previous technology “innovations”?

The big problem with any type of new tech, since John Mauchly initiated modern computer programming in 1949 with Short Code, is that business folks dump it into the tech people to figure out and implement for them. While they get excited at the tech’s potential impact on their businesses to be slicker, smarter, and more competitive, they do not believe they need to get pulled deep into the technology to understand exactly how it can do it and what the business needs to do to exploit it.

This is why so many businesses got sold down the river with cloud migration during the pandemic and RPA just prior. They bought into the vision the technology firms were selling but gave it to technologists to implement that vision without changing how they ran their businesses to drive that change.

As Microsoft CEO Satya Nadella recently bemoaned, the uptake of AI “hinges on other companies doing ‘the hard work’ of changing their cultures.” Easier said than done, Satya, but perhaps Microsoft needs to invest in fast-track change management services to help your clients buy more CoPilot licenses?

Enter GPT-4o… another iteration of GenAI that just took things to a much more human level

The one thing that has been consistent since ChatCPT 3.5 was launched in November 2022 has been the continual proliferation of LLMs and the capabilities of the technology. However, it is the latest iteration of GPT that makes the biggest advancement yet and will surely wake up the majority of enterprise leaders as we pointed out when GPT-4 hit the streets last year.

Multimodal makes everything much more human. The thing I am loving about GPT-4o, apart from being twice as fast as GPT-4 is the “omni” or multimodal capability to bring text, vision and speech into the same neural network. With GPT-4, these were processed separately, with voice being transcribed into plain text, which erases the nuanced information from the LLM; so all the tone and emotion captured in an audio format are now reduced to plain boring text. Net-net GPT-4o can process images, audio, video, and text simultaneously. GPT-4 could only process text and images. In effect, old GPT was like texting a friend, GPT-4o is like calling a friend.

Real-time human-2-machine conversation is now possible. In short, we are able to converse naturally without first converting words to text, with real energy, emotion, and expressiveness. We’ll also be able to interrupt it, have it change its tone of voice, and respond with emotion. The whole nature of collaboration with machines has gone to a new level.

Enhanced multilingual support and capabilities. GPT-4o has greatly improved the quality and speed of ChatGPT’s international language capabilities compared to previous models. It can communicate fluently in dozens of languages, making it accessible to more users globally. The model demonstrates more robust performance in non-English languages and translation tasks. Combined with its human-like chat and collaboration, surely the excuses to invest in generative customer engagement are moot?

It really does have human eyes now. GPT-4o can read the expressions on people’s faces and judge their emotions by simply pointing your iPhone camera. This thing really does have eyes that process what we see beyond transactional images. While GPT-4 had optical potential, GPT-4o is making AI optical capability much more real.

It’s being incorporated into Apple’s iPhone and Google’s Android operating systems. The earlier version of ChatGPT Voice available in the iPhone and Android app allowed you to converse with the AI in a relatively natural way — but it wasn’t listening to what you were saying; rather, it converted it to text and analyzed that instead. Hence, Siri and Google Assistant should soon be becoming much more human than their current transactional forms, which most of us turn off because they’re just so useless.

Summaries are concise and relevant. GPT-4o provides summaries of conversations and searches that are very accurate in both tone and length, while GPT-4 often produces inaccurate language and tone which require a lot of supervision to get right. Is this finally the end of legacy Google search and bad call transcripts? Surely disruption of legacy text strings is now in full play?

Visual interpretation and data tables are much more usable and accurate, ready to support business needs. It accurately converts image data into a clean table format without misinterpretations. It is precise in converting text and data, while previous versions made a lot of inaccuracies. Research capabilities are more detailed, provide more accurate breakdowns of data and analysts, and provide real practical examples. Do we really need to keep relying on clunky old data and analytics tools that require so much manual manipulation to get what we need?

Image generation capabilities are just so much sharper. GPT-4o is more visually appealing and produces conceptually accurate images. It is much more usable for enterprise projects needing high-quality visuals than what we have experienced using the current versions of Dall-E (for example). GPT-4 gave us a taste but now we surely we now are seeing the potential to create content ourselves without the need for expensive agencies and outdated complicated software packages?

The cost of accessing its APIs is 50% cheaper. OpenAI has clearly realized its costs are holding back wary enterprises and is now pushing 50% less cost for many of its core APIs, such as Chat Completions API, Assistants API, and Batch API. Are we finally going to be freed from decades of legacy software, abhorrent license fees and meaningless code bases?

Coding is vastly improved. So far, many developers are lauding the improvements in GTP40’s ability to solve many coding projects, such as multiple thousand lines of code in under 10 minutes, which previously took prompt engineering processes many hours. It can also create multiple apps in Python that the previous version struggled with. According to one developer, “4o not only solved it and provided clear concise dissection of the solution. 4 can be easily tricked into going down a death spiral it does not know how to backtrack correctly. OpenAI did incredible improvements to 4o. I can see Model 5 gonna start to get rid of human programmers for good.” We recently discussed how GenAI is already making radical improvements to human-heavy legacy code development, and these new advancements are reinforcing the end to legacy coding as we know it.

The Bottom-line: Just as we were giving up the ghost on GenAI, it becomes more human than ever

I am one of the biggest cynics when it comes to tech innovation and business change because of one reason—there needs to be a bloody great burning platform to force businesses to adopt. With GPT-4o, many of the reasons for murdering the technology in this death spiral of a thousand pilots have been the inability to adapt it to so many business scenarios. Ambitious C-suites will clamor louder than ever to see this AI tech immersed into their organizations and will seek leaders to defrost their frozen middle ranks to make this happen for them. Your job may not be replaced directly by AI, but you will more likely be replaced by someone who knows how to use AI if you don’t wake up and get with the GenAI program.

To conclude, I will go back to the main excitement behind GenAI… it is disruptive because it helps us create new data and new content. But it needs to become an extension of our humanness to do that, not merely another technology tool that can add some value in bits and pieces. Having multimodal capability that brings speech, text, video, and content together in one neural network that we can communicate with in real-time and immerse into our day-to-day activities is the game changer we have been unwittingly waiting for. Now it is here, and we can only imagine how quickly this will keep evolving as OpenAI, Google, Anthropic, Apple, Microsoft, NVidia, and co keep pumping all their investments into this emerging tech.

* The survey was conducted in collaboration with Genpact. We will be releasing the full study on 5/22

The biggest issue I see within enterprises today is how smart executives can find common ground with their bosses to make great decisions.

I really enjoyed this simple, but magnificent advice from HBR’s Amy Gallo where she describes some simple steps on how best to achieve the right results at work without creating all sorts of bad energy:

There are some pearls of Gallo wisdom I took down:

Do a risk assessment – weigh the consequences of disagreeing

Chances are you won’t get fired or make an enemy for speaking your mind

What do you stand to lose… what could happen later if you don’t raise this issue now?

When and where you meet matters to have the conversation

Time can really help, perhaps you can find colleagues on the same page as you and their support and ideas may bolster your case

A private meeting may be a lot less threatening

Make it a chess game, not a boxing match

What to say and how to say it

Maintain a strategic focus… keep everyone’s integrity intact

Ask permission to disagree… allows your superior to opt in without feeling threatened

Explain, “I’d like to lay out my reasoning. Would that be OK?”

Connect your idea to a shared goal…. something you both care about such as company morale, quarterly earnings, etc

How to present your argument

Project confidence and neutrality…. anxious body language can harm your message

Breathe deeply

Stay humble and curious enough to hear critiques

Share only facts, not judgments

Always add, “I know you make the final call here”

The Bottom-line: Amy will be speaking at the HFS Summit next week!

And, of course, how could we resist not enticing Amy to come and keynote at the HFS summit next week with the topic… “Is it Me? Or Is it Them? How to Collaborate with Difficult People”. We’ll also be sharing a few copies of her book, “Getting Along: How to Work with Anyone (Even Difficult People)”.

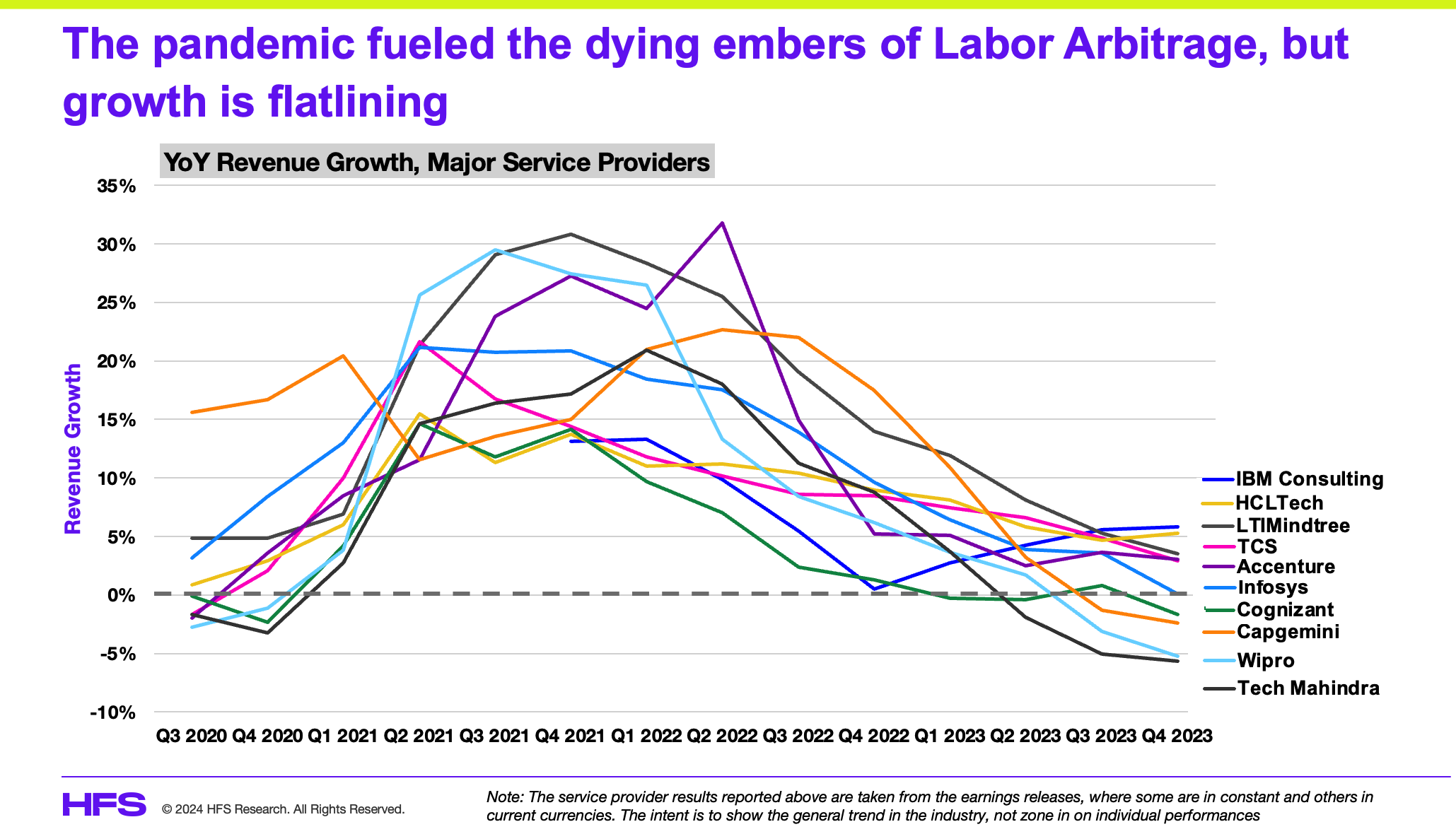

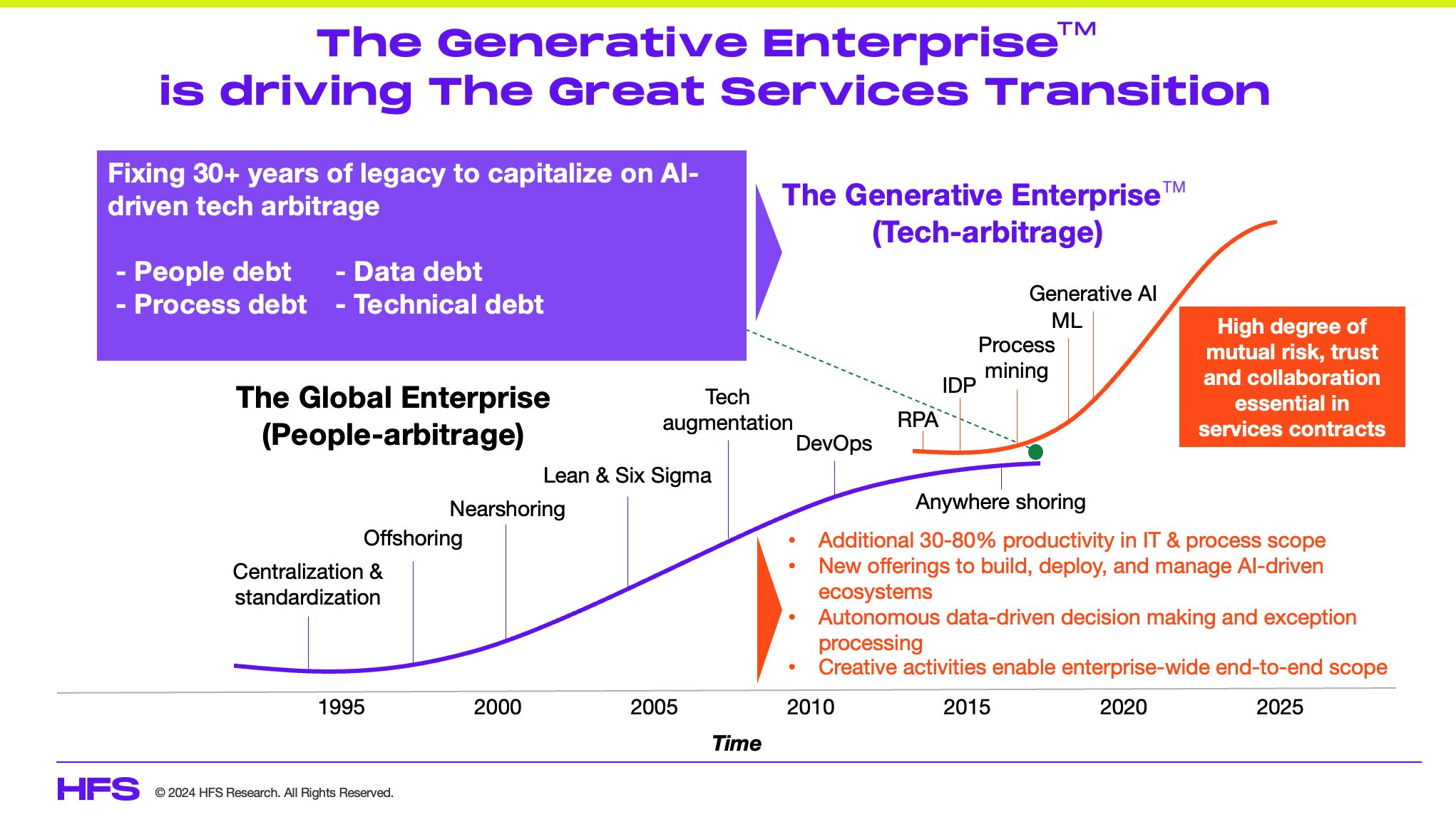

The IT and business services world has entered a crucial phase where the winners and losers will become clear in the next few months. Many are already getting left behind in the legacy services world of shopping low-cost labor, while the smarter ones are vying to become strategic partners to their enterprise clients, helping them write off decades of people, process, data, and technology debt to forge the path to the brave new AI world.

We are firmly along this S-Curve evolution from people to technology arbitrage that the Generative Enterprise demands. Welcome to this Great Services Transition, where the entire financial construct of services relationships is being reinvented to capitalize on the complex ecosystem of AI platform players, hyperscalers, data integration products, automation tools, LLM builders, and so on.

For example, services powerhouses like TCS and Wipro are digging deep into their tried and trusted past glories to (at least) restore some of the old energy and verve into their teams, but they won’t be able to rest on their laurels by simply placing popular leaders at the helm. They have to embrace the complex shift from people-based arbitrage to technology-based arbitrage if they are truly going to make it through to the other side – which we are calling this Great Services Transition.

Can today’s services firms really make the painful changes to reinvent their business models, or have their owners made so much money off the old model they simply aren’t motivated to grapple with painful change?

All these major providers, from Accenture, IBM, and Capgemini to the plethora of Indian heritage services firms and technology consultants such as Deloitte, EY, and KPMG, have to change their financial construct with their clients to one of shared risk, shared learning, and ultimately shared reward; otherwise, they face a race to the bottom.

This means changing the habits of a lifetime. You only need to look at the likes of Kodak, Nokia, Yahoo, Xerox, and even JC Penney, which simply failed to innovate with the times and were too late to play catch-up once they had woken up to the new reality. One could argue that many of the services firms in today’s spotlight are already too embedded in their legacies to turn things around. The continued cycle of providing people-based services will yield a modicum of modest growth as enterprises seek continued cost savings and invest in AI build-out initiatives. But as the model transitions to AI-led technology arbitrage, those left with hundreds of thousands of resources requiring decent utilization rates will see margins further degrade. The people-based arbitrage model is plateauing.

When your leadership is fat and happy, and the stock still holds up, why go through the aggravation of painful change when you can quietly ride off into the sunset with your cash pile? When your board and stockholders only care about your quarterly numbers, and you don’t have the time or trust to drive a long-term plan, what can you really do beyond chasing ever-decreasing deals and focusing on cutting costs to the bone? Sadly, it’s not always the fact that leaders fail to see the change coming; it’s more the casino that is Corporate America’s stock market that dictates which companies will survive or add themselves to the list of innovation failures.

However, as analysts who’ve covered this market for nearly 30 years, we steadfastly refuse to give up because many of today’s IT service leaders are too greedy, too risk-averse, or just too ignorant to find a path for survival and renewed prosperity. So let’s break down this Great Services Transition into four simple problems to solve:

To survive The Great Services Transition, there are Four Problems to Solve:

Solving problem 1). Enterprises and service partners must be aligned on the change mandate

What service partner has a culture you want to work with that will blend well with yours? Ambitious enterprises and their service partners are both striving to be effective in the emerging world of AI-driven business models and operations. This means this transition only works when there are two parties ready to tango and change together. To this end, service providers must become partners of change for their clients to help them understand the sheer noise of technology change going on around them. Clients need internal alignment to ensure that its time to make the move.

Solving problem 2). Services must provide access to affordable talent with real expertise

The shift from labor to technology doesn’t take away the need for people; it actually necessitates experts who can shepherd their clients along to help them change. They must provide continuous education on how to manage organizations’ fast-moving technology ecosystems and work with them to create business roadmaps based on emerging tech to make them slicker, smarter, more efficient, and less bloated.

Solving problem 3). Determine the people, process, data, and technology debt to address

In the Great Services Transition, enterprises are buying services solutions that improve performance, drive speed to market, reduce cost, and create new content and data.

You must address your debt in these four areas which your firm has likely collected over the last 30+ years:

1. Fixing your skills debt: Develop new skill sets that can support the transition to embracing emerging technology and AI-driven business models.

2. Fixing your process-debt: Recreate new processes process to determine what should be added, eliminated, or simplified across your workflows to support your slicker AI-led operating model.

3. Fixing your data debt: You must align your data needs to deliver on your AI-centric business strategy. This is where you clarify your vision and purpose. Do you know what your customers’ needs are? Is your supply chain effective in sensing and responding to these needs? Can your cash flow support immediate critical investments? Do you have a handle on your staff attrition?

4. Fixing your technology debt: IT spending just keeps increasing and only keeps swelling with each new platform and coding change. Stop buying tech for the sake of tech—this has been the failure of so many previous investments, such as the two-thirds of enterprises left struggling with their cloud migration journeys signed during the pandemic. The Great Services Transition is where you proceed through steps one to three before making bold decisions on your technology investments of the future.

Solving problem 4). Restructuring your services engagements to shift from labor arbitrage to technology arbitrage

Enterprise leadership has always been – and still is – obsessed with cost reduction. This is what they understand more than anything, and they view innovations such as GenAI as another lever to justify investments based on yet more cost take-out. The best approach is to reduce overall delivery costs by 20-30%, apportioned over 3-5 years. This is offset by the increased value and reduced labor costs driven through effective investments in change, processes, data, and technology. Clients MUST sign up for process reinvention and data transformation as part of it. Clients need to TRUST their partners to get them there. Providers need the TALENT to work with their customers, or the whole thing simply erodes to the bottom.

The Bottom Line: Change the habits of a lifetime, or crawl away, as this S-Curve is the biggest people and technology challenge we’ve ever faced

As human beings we’ve already grown comfortable with what is familiar to us and avoided doing things differently until we have literally no choice. This is the case with the services industry, which has ballooned in growth and home comforts for three decades. The stark reality today is that enterprises do not need to keep spending on low-cost people-based services – they have what they need, and there is so much supply they can look at many providers to get it. What enterprises desperately need are partners to work with them who share similar desires to learn new methods, unlearn old habits, and to teach them to exploit new technologies and new data methodologies and work with them to attack new markets with these capabilities.

This is how to survive the Great Services Transition. The big question now is whether enterprises and their services partners have the appetite to fix their skills, processes, data, and technical debt? Can they really learn new ways of operating, change their cultures, and embrace emerging technologies? Everyone needs to dig deep and decide whether they want to be a footnote or the future

Operations leaders face unprecedented challenges. They have to manage the new complexity of becoming cloud native and anticipate the implications of GenAI. If that’s not enough, they also have to find answers to the Digital Dichotomy, balancing the macroeconomic “slowdown” with the “big hurry” to innovate to keep up with innovation pacesetters. Yet, it is not a question of doing one or the other—they must address all those challenges simultaneously.

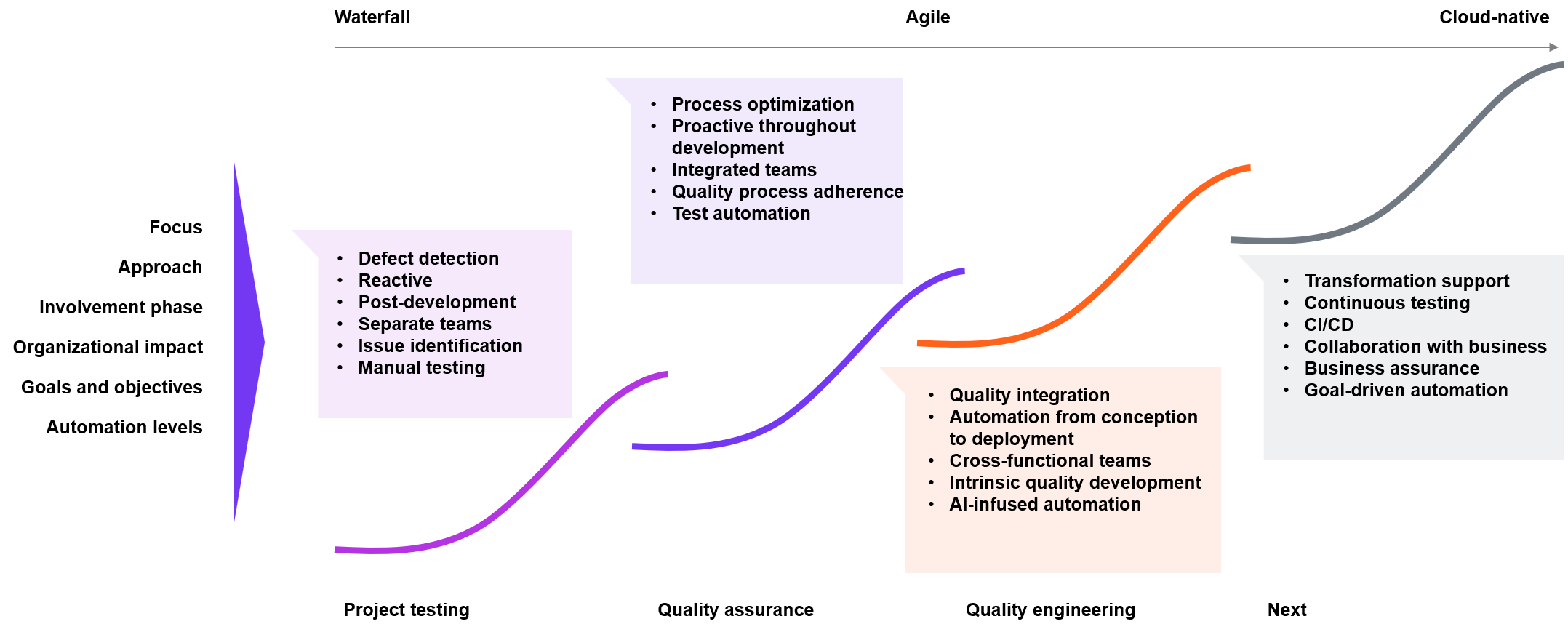

Against this background, quality assurance (QA), or simply “testing,” as it was called in the old days, can no longer be a reactive afterthought coupled with an unwillingness to invest in quality. Instead, it must become an integral part of the software development lifecycle (SDLC) and take on a much more holistic responsibility for assuring transformational outcomes.

This is the context for HFS’s seminal study on assuring the Generative Enterprise™ (HFS Horizons: Assuring the Generative Enterprise™, 2024). We sought to understand better where organizations are with their QA efforts and how they are trying to ensure transformational outcomes. We also explored how they assure change agents such as automation, AI, and blockchain. Finally, we looked at the adoption of GenAI through the lens of QA. In the following, we share the insights gleaned from our study.

Lofty aspirations for quality assurance

Finding your bearings on all things QA is difficult because there is a massive gap between the aspirations (and lip service) for QA and QA functions’ maturity and enterprises’ willingness to invest in them. While the mature end of the market is pivoting toward quality engineering (QE) with a focus on achieving continuous testing, data-driven decision-making, and cross-functional collaboration, two-thirds of the market is stuck at a lower maturity level, often still working with a Waterfall methodology, as Exhibit 1 depicts. Simply put, most organizations are on the left-hand side of this infographic.

Exhibit 1: Pivoting to quality engineering is about aligning quality assurance to customer journeys

Source: HFS Research, 2024

Yet, we might finally see organizations embracing the transformation of their quality assurance functions. According to our study’s reference clients, 95% described the primary value delivered by their service provider today as the ability to drive functional optimizations with selective quality assurance capabilities. Simply put, they expect services on the left-hand side of Exhibit 1. However, in two years, most of these organizations expect a transformation of their quality assurance functions, intending to drive experience-led outcomes and stakeholder experiences while creating new sources of value through ecosystem synergy.

“Shift right” is starting to augment “shift left”

Discussing these issues with QA leaders, technology partners, and service providers could crystalize more nuanced market dynamics. Most organizations have embraced “shift left” principles emphasizing the early and proactive involvement of quality assurance activities in software development. We are seeing mature QA functions augment this with “shift right” principles advocating quality activities also at the later stages of the SDLC.

Regarding organizations’ QA priorities, four clusters jump out for us: First, carving out a budget for QE architecture modernization and transformation. This goes back to the discussion of the Digital Dichotomy and the need to self-fund innovation. Second, solving the conflict of production quality versus speed to market. Not least, with innovation cycles dramatically compressed with the ascent to GenAI, this is a hard nut to crack. Third, overcoming a new complexity to provide integrated assurance for apps, infrastructure, and platforms or progressing toward the OneOffice™, as HFS would put it. And fourth, driving change management to foster transformation. Yet, large chunks of the QA community are stuck in a tools and technology mindset.

There is much noise but little assurance on GenAI

Let’s zoom in on the topic that comes up in every discussion we have, regardless of the context. While many providers hype use cases around domain knowledge and code creation, grown-up discussions about how to assure GenAI are sparse. As such, Cognizant’s Artificial Intelligent Lifecycle Assurance (AILA) and Infosys’ AI Assurance Platform are more exceptions than rules. This provides indicators for the enterprise adoption of GenAI. We are still at the very beginning of enterprise adoption. The core value proposition of GenAI use cases in QA is having a higher accuracy with less data. Thus, providers can drive new levels of automation to generate test scenarios and test cases.

While we had many discussions on the infusion of QA with GenAI, deliberations on governance on GenAI are still nascent. Where we had honest discussions, providers reflected that large language models (LLMs) are largely unfamiliar entities. One executive framed this aptly: In the context of GenAI, we must show humility to the unknown. Thus, the predominant way to engage is through experimentation. However, there is no beating around the bush that we were a tad underwhelmed by the discussions of assuring GenAI outcomes; outside of the service providers, we had some stimulating conversations. For instance, MunichRe provides insurance for AI, while German start-up QuantiPi blends quality assurance with governance for GenAI.

North Star (autonomous) persona-based testing

Beyond the broader pivot to QE, what have we learned about the evolution of quality requirements? Like cloud-native operations are shifting toward persona-based solutions, QE is shifting toward persona-based testing, requiring capabilities to support better specific stakeholders such as product teams, site reliability engineering (SRE), DevOps engineers, and beyond. But to be clear, this is the North Star, and only a few organizations have it on their roadmap. Looking at these requirements in the context of GenAI, the key is blending prompt engineering with specific persona scenarios. Using prompts to generate automation scripts such as Selenium can significantly enhance the scale of automation. Lastly, using the input from one prompt to generate another prompt can leverage GenAI to industrialize offerings.

Horizon 3 market leaders blend a compelling vision of transformation QA with nuanced approaches to assure change agents such as GenAI

Last but by no means least, congratulations to the Horizon 3 market leaders. These leaders’ shared characteristics include blending a compelling vision of transformational QA with nuanced approaches to assure change agents such as GenAI. The wheat separates from the chaff when providers ensure transformation outcomes are enabled rather than depicting functional testing and an overreliance on tools and technology. The leaders are pushing the envelope on transformation with new themes such as cross-functional testing, zero-touch testing, black-box testing, and beyond. Exhibit 2 outlines the detailed rankings of our research.

Exhibit 2: The vanguard of the quality assurance services ecosystem

Accenture and Wipro stand out, clearly outlining the evolution to QE. They shift the focus of their narratives by depicting transformational journeys and outcomes rather than getting stuck in tools and technology. Infosys supports clients’ pivots to product-centric delivery and intelligent ecosystems, while TCS infuses emerging technologies into QE and embeds them at the core of transformation. Capgemini surprised us with a nuanced and thoughtful narrative on adopting GenAI. Cognizant was demonstrating test automation chops and strongly emphasized customer experience assurance. Perhaps surprisingly to some, Persistent is going deep on cloud-native transformation by investing ahead of the market in digital engineering and GenAI capabilities.

The Bottom Line: The QA community needs to emancipate itself

The innovation delivered by the QA community continues to be stupendous. Yet, the community does a modest job articulating the goals and outcomes those change agents achieve. Without snapping out of this tool- and solution-centric view of QA, it is difficult to articulate a more value-driven approach, where QA executives get the limelight they crave to discuss and decide the significant sourcing issues. Stepping up to QE transformation and putting QE at the heart of transformation and software development is an opportunity for the community to emancipate itself from being boxed in a technology and tools mindset. Discussions with the market leaders in Horizon 3 gave us some hope that we are getting closer to this.

HFS subscribers can download the report and find many more details here.

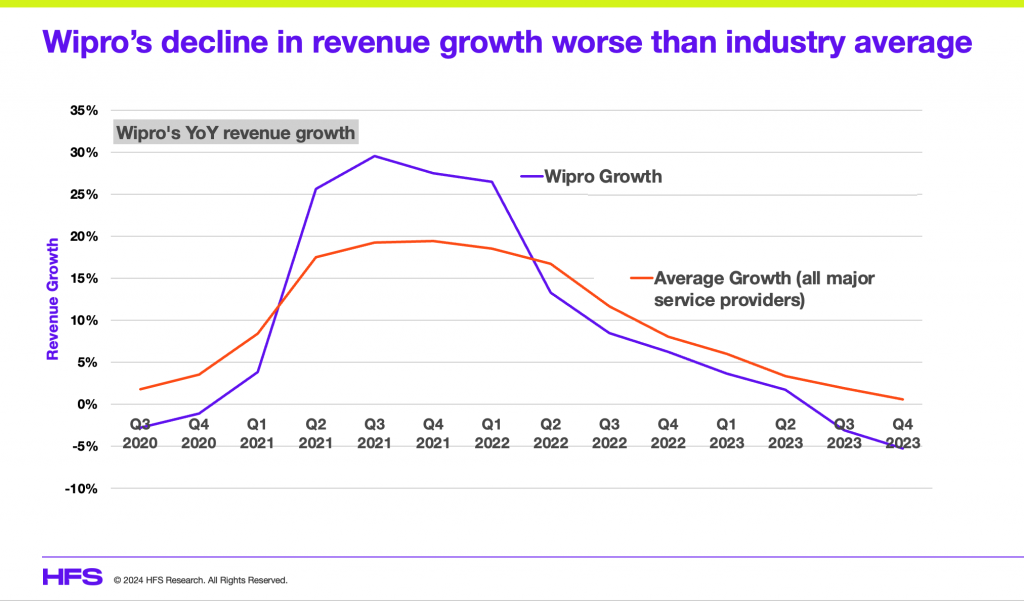

So, the worst rumor in the industry finally came to fruition: Thierry Delaporte finally fell on his sword at struggling Wipro to be replaced by an internal Wipro-ite and 32-year veteran, Srini Pallia. This is Wipro’s first internal candidate to take the helm since T K Kurien’s appointment in 2011.

Delaporte came into Wipro as the pandemic was kicking in and used his remote advantage to pull the company together, speaking with a multitude of clients and giving the firm some strategic direction during that difficult time, especially with the bold acquisition of financial services consulting powerhouse Capco. In addition, Wipro enjoyed a strong 2021 as dollars flowed into cloud modernization, and many of Wipro’s large clients, such as AT&T, Citibank, ABN Amro, Levi’s, Metro AG, Dell, and Este, all kept faith in the firm. However, when the momentum was there to kick on and compete for some of the choice deals, Thierry took his eye off the ball.

Sadly for Wipro, the post-pandemic period has been one of the worst times in the company’s history:

Delaporte rarely left his Paris base, while his CEO counterparts have been regularly rallying the troops across India and the US. You can’t run an Indian-heritage business during tough economic times when you’re not physically present to boost morale and represent the firm. Being seen at Davos and not rallying the leadership while the revenues are tanking is not a good look.

He brought in many executives from outside of Wipro and neglected the loyal Wipro-ites who had built the company. This has resulted in many A players leaving the firm such as Rajan Kohli (CitiusTech) and most notably losing its well-respected CFO, Jatin Dalal to Cognizant.

His large deals team, spearheaded by Stephanie Trautman, struggled with the internal fiefdoms Thierry failed to address, and was shut down at the end of last year with Trautman, a popular figure with clients, leaving the firm.

The Capco acquisition has been a major struggle to bear fruit, which was Delaporte’s big bet, as we discussed recently.

The morale has been sapped out of Wipro for a year now, and this change in leadership is at least six months overdue.

So what’s the deal with Srini, and can he bring Wipro’s mojo back?

While several external candidates were mooted, Rishad has opted for a popular internal candidate based in New Jersey the heartland of IT services decision making. Srini has the respect of the guys who built the firm (those who are still there) and well-liked by key partners Microsoft and SAP. He knows the company, he knows many of the key clients, especially ones like Este and Tapestry he personally let for Wipro.

What are the big things he needs to do quickly?

Restore morale. Simply put, the firm is bleeding talent, and morale has never been lower. He needs to nail down his plans quickly, give the firm renewed direction, and convince key stakeholders he is the right choice during perhaps the darkest period in Wipro’s history.

Retain key leaders. Significant talent, such as Suhba Tatavarti, Suzanne Dann, Nagendra Bandaru, Anis Chenchah, Harish Dwarkanhalli, and Jo Debecker, remains in the firm. He needs to pull together and ensure they stay.

Breakdown the fiefdoms. This is where Thierry struggled, and Srini can succeed by ensuring they go after new clients as one Wipro team, not a broken group of silos. Srini is at the coalface of many deal pursuits and should be in prime position to fix these issues.

Fix Capco. As we recently discussed it makes no sense to keep these entities so separate with separate brands. It’s not too late to reverse this and get this moving in the right direction, especially with financial services over the worst of its difficult times.

The Bottom-line: Better late than never, but this is no easy task for Pallia as Wipro turns back time

After the failed experiment to make Wipro like a Big 4/Accenture-like firm, Wipro is going back to its Indian-centric 80-year heritage to deliver cost-efficiency, but with capabilities to support transformations, Cloud and GenAI (Wipro is performing well with several GenAI pilots and rollouts, for example). However, the firm has to play catch-up during the toughest time facing Indian-heritage outsourcing, and Pallia needs to weather more challenging quarters, impatient shareholders, and unrealistic expectations. Thierry hasn’t left a great legacy to build on…

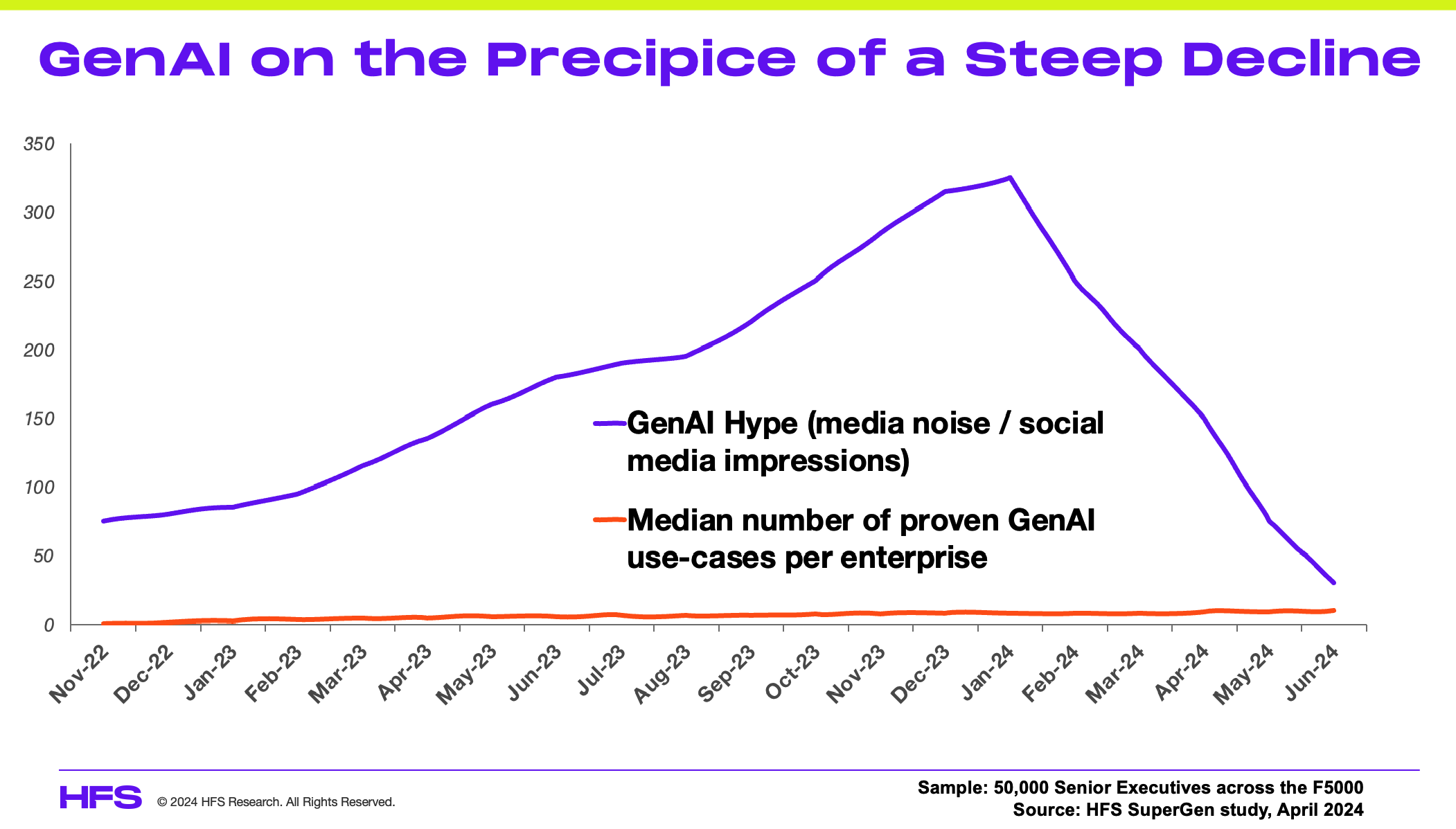

We’re sad to inform you all that the GenAI we have grown to love with such intensity will shortly crash and burn. We’ve been here before, folks, when we called the death of RPA five years ago… and we are today calling the death of GenAI:

GenAI has simply become the new Digital. The many billions every tech and services firm has claimed to be investing in GenAI has now evaporated in a puff of press releases, turgid conferences, and soul-crushing webcasts. They’re now claiming everything they once painted as digital is now getting a second coat of paint called GenAI.

Suddenly, every single executive from every single organization is talking as incessantly about GenAI as they used to about Digital. And they are keeping a straight face while they do it.

But “What is the problem with this, Phil? AI is changing everything about our world.” I hear you all collectively cry… so without further ado, let’s analyze brand-new data from our SuperGen study of 50,000 senior executives in big companies in the F5000.

HFS’ SuperGen study finally reveals the real truths behind the last 16 months of AI hysteria

Not content to simply jump on this hysterical AI bandwagon, HFS’s stubborn analyst team took it upon itself to launch the largest-ever study of GenAI adoption known to humankind. Here are some key highlights from the data findings we can exclusively reveal today:

98% of executives claim to be rolling out GenAI initiatives.

76% believe their GenAI initiatives are game-changing but won’t disclose what they are.

91% of senior executives do not have a paid ChatGPT account.

84% of senior executives with a paid ChatGPT account haven’t actually used it yet.

85% of senior executives have only performed one prompt, which is to find out what ChatGPT says about them.

97% of senior executives can’t actually define GenAI.

63% believe Elon Musk and Jensen Huang are developing GenAI to control people’s minds with embedded Nvidia chips.

34% believe Donald Trump will soon launch his own GenAI tool branded MagaGPT.

88% believe President Biden would benefit from a GenAI chip implant.

Bottom-line: With GenAI hitting the skids, what’s next?

We decided to consult the experts on what will replace GenAI and these many billions of dollars we’ve seen expended into the ether.

Jensen Huang and Jesse Lyu weigh in on the demise of GenAI

Firstly, we spoke to the new Steve Jobs… Rabbit’s Jesse Lyu has sent a thunderbolt of excitement into the industry with his revolutionary handheld product, RI. “LLMs asked the questions, but LAMs will provide the real actions. Fortunately, we’ve only just shipped out the first batch of Rabbits, so it’ll take a while for you all to realize the thing just adds yet another useless layer of application management. But it’s a cute bunny, and I got you all excited and very rich at the same time, so what the hell.”

We then managed to get Nvidia CEO Jensen Huang himself to talk to us, and he was pretty candid, “We’ve made so many billions from GenAI that I realized it may evaporate once I ditched this leather jacket I’ve been wearing continuously the past few years. So I’ve decided to invest in a super cool new bomber jacket to prepare for the next big thing… stay tuned, folks!”

Well, there we have it, everyone. With GenAI about to die, we can only ask why….

In March 2021, Wipro closed the largest acquisition in its history, Capco, a BFSI-focused consulting firm, for $1.45B. HFS wrote glowingly about the transaction, with our positive assessment fueled by a confluence of circumstances including a new, unlikely pick for CEO (Thierry Delaporte) who brought a strong pedigree in integrations of significant acquisitions, driven by his experience of the successful merger of IGATE into Capgemini and his respected leadership within the financial services industry.

In addition, the IT services industry was enjoying a massive pandemic-fueled spike in digital and modernization spending, and there was some optimism that this acquisition would finally anoint Wipro as a true end-to-end transformation partner.

As we examine what Wipro has achieved in the three years since the acquisition, we regretfully opine that things have not gone well, as clearly outlined here:

What went wrong – market headwinds, culture clashes, and lack of integration

The potential to be a great acquisition was there. “Strategy-led execution” was what the combination of Capco and Wipro could yield. Capco brought deep BFSI consulting capabilities and strong C-Suite relationships outside the CIO’s office, which so many of Wipro’s competitors lack. Wipro brought extensive delivery and execution capabilities in IT services. This limited overlap was viewed as a benefit, with the game plan being to integrate the elements to drive end-to-end services capabilities “from think to design to build to operate”. The integration plans were executed – lots of great and well-intentioned account-specific plans were drawn up. However, Wipro grossly underestimated the cultural differences between their firms, namely Capco’s Western-heritage consulting versus Wipro’s India-heritage delivery mindset. This cultural mismatch was further exacerbated by keeping the brands separate.

Wipro additionally could not have planned for the inflation and associated market headwinds that torched many a bank in 2023. The combined result has been a massively detrimental slide in BFSI revenues which, as its largest reported industry vertical contributing about a third of revenue, has most definitely left a mark.

At HFS, we acknowledge Wipro’s revenue challenges are bigger than the Capco conundrum, however this was Thierry’s big bet and it’s clearly struggling. All services firms are battling continued market headwinds and even Accenture sent alarm bells across the industry with its bleak demand forecast for the year.

But the fact remains that Wipro made its largest-ever acquisition and has little to show for it other than the somewhat nominal addition of Capco revenues to its topline.

Despite adding a supposedly margin-rich consulting business, its operating margins are in fact lower than they were pre-pandemic. The following graphic puts a fine point on the state of Wipro vis-à-vis its competitors. Those that are staying above water are doing so due to heavy prioritization of technology arbitrage.

Why large consulting firms and offshore-centric outsourcing providers struggle to blend

There was a cheesy relationship self-help book from the 90s called “Men Are from Mars, and Women Are from Venus – a Guide to Understanding the Opposite Sex.” Apparently, BFSI strategy consultants and IT delivery and execution resources are also creatures from different planets. At least at Capco and Wipro, but the cold reality is there have been few successful large mergers between large onshore consulting firms and India-heritage service providers. The one exception is Capgemini and IGATE, where there was very limited client overlap, and Capgemini already had deep consulting capability. Plus Capgemini had learned from several past acquisitions which hadn’t fared as well.

There is a fundamental underlying reality: strategy consultants are in the business of paid ideation and hand off to execution resources to build and implement their recommendations. Basically, consultants sell the dreams, and service providers provide reality, which is sadly where this Capco/Wipro merger has found itself.

IT delivery and execution resources are paid to build, implement and manage business as usual operations. These should be complementary capabilities, as was the plan for Capco and Wipro, but the breakdown comes from a mismatch of enterprise buyers, Capco’s view of Wipro’s capabilities as commoditized delivery, and Wipro’s view of Capco’s consulting as pre-sales.

1+1 = 1.5

The idea of Capco as the tip of the spear for Wipro’s capabilities fell apart as Capco’s relationships with non-CIO leaders did not translate well to downstream Wipro engagements. HFS heard numerous reports of Capco consultants disparaging Wipro delivery resources as the “C-team”. Wipro in turn has its own cultural challenges – best described as a bad habit of treating consulting as cost of sales investments to land large build and run deals. Neither of these orientations lend themselves well to end-to-end transformation deals.

The Capco and Wipro teams were culturally opposed and never found a great working groove. The most damning evidence of this is the various conversations HFS has had with clients of each Capco and Wipro, where we inquired about the impact of the integration. Capco clients generally indicated they are interested in the build and run “bodyshopping” resources of Wipro, but have not been impressed with the caliber of their people. Wipro clients have generally indicated they often work with Capco in other parts of their firms, but have not had the need to bring them in for their IT build and run engagements.

The net-net is Capco and Wipro sell and run separate engagements, usually with different levels of executives on the client-side. Sure, Capco’s revenue accrues to Wipro, but there has been limited exponential impact from combining the two entities. Strategy-led execution deals have not materialized.

Sub-brands are the antithesis of integration

So Wipro basically has a strategy sub-brand. Capco continues to operate as Capco, now branded as a Wipro company. They have lost some of their talent, most recently Lance Levy, the longtime CEO of Capco who will now serve as a “strategic advisor”. But retention bonuses paid early on have helped keep some of their key operators. Although, as with Levy, the three year mark is often when golden handcuffs are released. What is ultimately keeping Wipro from realizing the value of its acquisition of Capco has been the lack of integration.

We truly thought Wipro’s CEO, Thierry Delaporte, understood the criticality of integrating acquisitions. After all he was the maestro behind Capgemini’s successful integration of IGATE, an eerily similar combination of consulting plus Indian IT services capabilities. However it was the reverse order of operations – a consulting company acquiring an execution firm. We’re not sure it matters though. As Capgemini has more recently demonstrated with its 2019 acquisition and integration of Altran, the name of the acquired entity must be put to rest otherwise the master brand loses equity. Altran has been known as Capgemini Engineering since early 2021. Why Delaporte and his team lacked the confidence to roll its newfound consulting skills under its own brand effectively undermines the value of Wipro. And with the announcement of new CEO Annie Rowland as Lance Levy’s replacement you’d have thought this an ideal time to fuse the brands together with the old guard finally leaving the building.

Other proof points include the highly acquisitive Accenture – arguably the master of acquisition integration – nearly 300 of them since it split from Arthur Andersen – with most acquired entities folded in and accruing to the master brand. Although even Accenture struggled with some earlier acquisitions as it was building out its brand as a digital and advertising business.

NTT DATA has finally seen the light after years of fragmented operations and the awkward co-existence of multiple brands. It recently announced the consolidation of all operations outside of Japan. The result is a $30B powerhouse slightly bigger than TCS.

The Bottom Line. The writing is on the wall. The Capco brand needs to be retired if Wipro has any hope of truly integrating and realizing the vision of strategy-led execution

HFS refers to 2023 as the year of the digital dichotomy, where enterprises across all industries struggled to balance market headwinds with the palpable need to drive progress and impact with innovation. No sector was harder hit than banking and financial services. A gigantic entity like Credit Suisse went down. The 2008 financial crisis was a long time ago, but banking is an old industry and everyone still remembers like it was yesterday.

So there was zero confidence in banking investment last year. Every service provider, most of which have BFSI as their largest reported industry group, are feeling the pain of massively elongated sales cycles, teeny contracts, and cut-throat competition. For Wipro, the firm needs to reign in its sub-brands (let us not forget DesignIT and TopCoder) and get down to the business of offering, delivering, and finally realizing its potential of providing end-to-end transformation services. The cost-to-income ratio of banks has been stagnant for twenty years. The need for change is there, and there,is no better time than now to make a bit bet on itself.

In most of today’s Global 2000 enterprises, stodgy shared services are failing to deliver value beyond back-office support, provide exciting career tracks for ambitious professionals, and rarely provide anything to support the growth and innovation their companies so desperately crave.

The GBS model has had its time and is no longer relevant for ambitious enterprises

For more than two decades, Global Business Services (GBS), the centralized service delivery model leveraging a mix of internal shared services and/or 3rd party outsourcing, has been a tried-and-tested modus operandi for large enterprises to save costs, drive process discipline and improve compliance.

However, with the rapid advent of real generative AI capability, the current GBS model is dated, fails to deliver much (if any) value beyond cost and efficiency and has struggled to create viable career opportunities for ambitious talent. Let’s face it, GBS is still stuck squarely in the back office and fails to provide a career track for the best and brightest to pivot their firms into the generative AI era.

The GenAI era is finally driving much-needed change in business operations

After persisting with this tired old business operations model for so long, GenAI is forcing a major shift for ambitious enterprises striving to attract the talent they need to remain competitive and innovative. Many enterprises firmly glued to the old GBS model are in real peril of being left behind, lacking the culture, mindset and direction to remain relevant, viable businesses.

The ability for generative business services, where advancing AI technologies such as Large Language Models and autonomously-capable apps are driving the speed and predictive capability of enterprises to function with so much more agility, creativity, and intelligence.

Simply put, the time to make the move from back office to OneOffice is finally upon us (we introduced OneOffice seven years ago) and GenAI is the catalyst to force this change.

However, at HFS, we see two massive problems the current GBS proposition must overcome:

Problem #1. Cost and efficiency are now hygiene. Enterprises are on a mission to find new sources of value

How often does your CFO tell you, “We loved that 30% you took off the bottom line last decade; just relax and enjoy life”. With the advent and maturity of ERP platforms and outsourcing/offshoring, the role of shared services and GBS has been largely centered on the centralization of processes to drive efficiencies and partnering with outsourcing service providers to exploit lower-cost labor to reduce costs.

However, with most GBS organizations having maximized the cost and efficiency levers in recent years, the onus is now firmly shifting to genuine business transformation to provide faster, smarter data to drive rapid decisioning. That is the new lever that must be pulled by GBS to keep driving new thresholds of performance out of the business and support the growth agenda.

Cost savings are important but no longer sufficient to keep most operations leaders in their jobs. Minimizing costs to a desired level is one ceiling of achievement, but ambitious enterprise C-Suites have to keep striving for new sources of value to stay competitive in today’s era of rapid AI deployment.

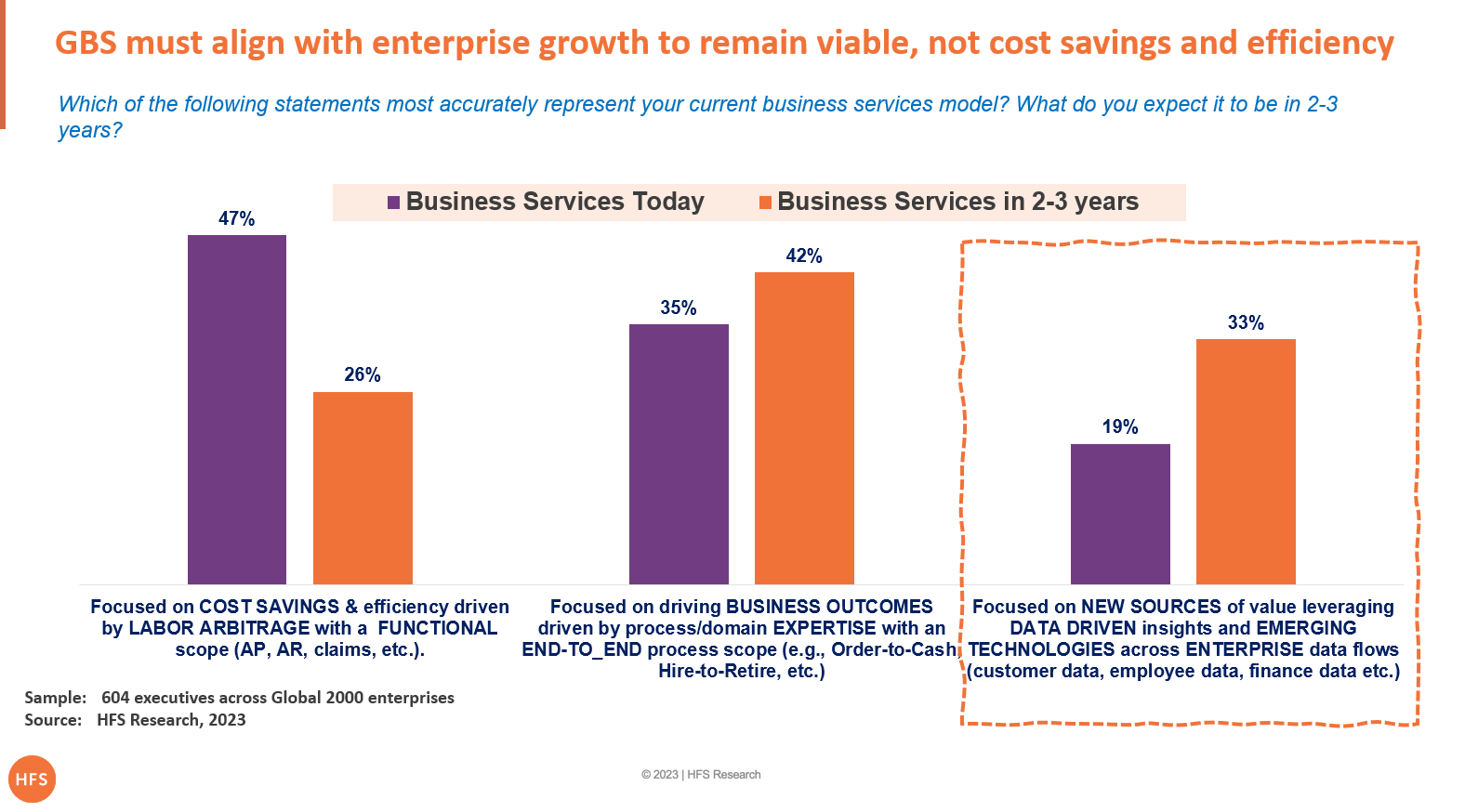

Our research of over 600 business services decision makers across the Global 2000 reveals nearly 50% GBSes are happily focused on cost savings today. However, it is expected to halve in the next 2-3 years (See exhibit below). GBS services of the future must align with the enterprise growth agenda, not just better, faster, and cheaper operations.

GBS has a critical role in helping organizations balance the current digital dichotomy that nearly every enterprise faces: balance the macroeconomic “Slowdown” with the “Big Hurry” to innovate.

Problem #2. Young people don’t see GBS as an attractive career. It’s just not sexy

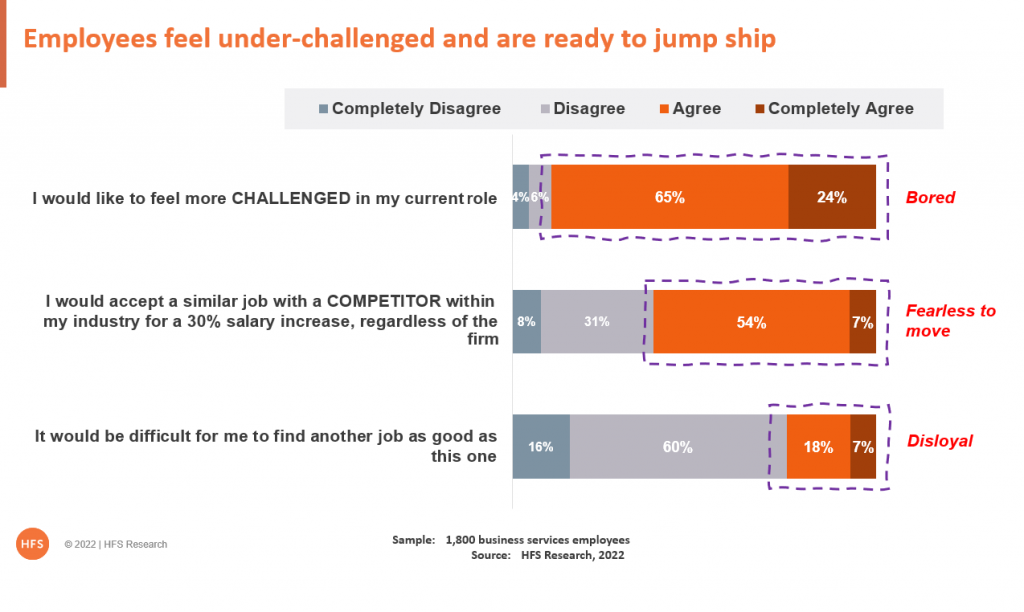

Research we conducted on employee experiences of 1800 business services staff shows close to 9 out of 10 want to feel more challenged (and are bored), 61% will jump to a competitor for a pay hike, and 75% believe they can easily find a job as good as the one they currently have:

It’s no wonder business services staff are quitting in droves in search of something more challenging when there is so much demand for workers to perform elsewhere. Now that next job may turn out no more challenging than their current gig, but if there’s 30% more money for doing it, why not?

Now we can moan and groan about the attitude and self-entitlement of some Gen-Zs and Millennials who have no loyalty, don’t care about longevity on their CVs, etc., but put yourself in their position: you’re ambitious, and other companies are offering you more challenging work, more money, and are simply more exciting places to work.

Why would you want to suffer a life of soul-crushing work for a company that still operates the same way it did 30 years ago? And can you blame staff for preferring to work from home than suffer from the monotony of a stuffy cube kingdom where most of the management isn’t even there? Let’s be blunt: it’s often the management who have become self-entitled, not the staff. The problem ultimately lies with bad leadership, not bad working attitudes, which is the reason why GBS has failed to provide real career options for our best and brightest.

The dawn of GenAI creates a once-in-a-lifetime opportunity for GBS to pivot

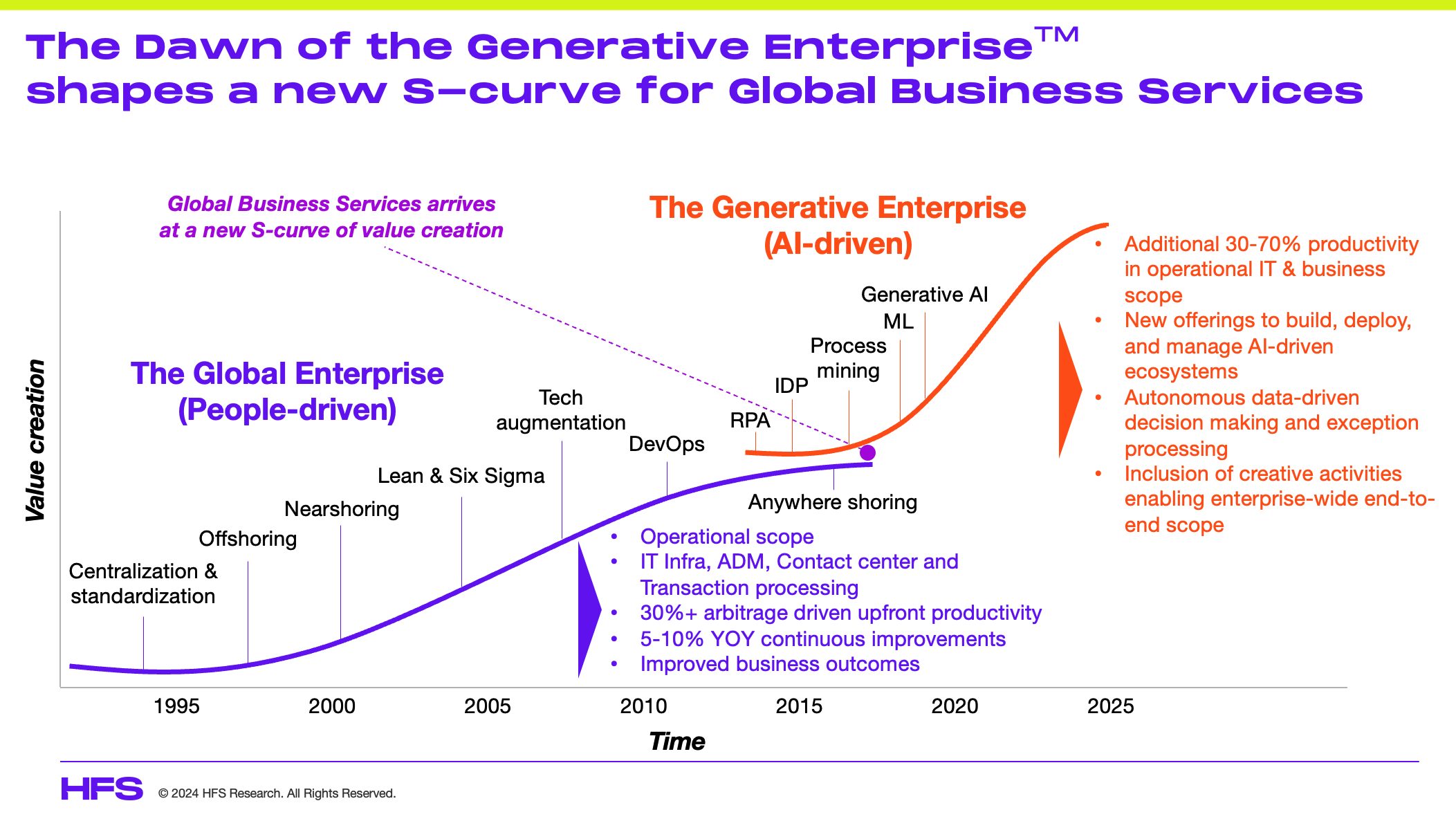

Global talent is what created the GBS model. Centralization, standardization, lean/six sigma, offshoring, nearshoring, technology augmentation and, more recently, anywhere shoring have been the pillars to drive down costs and improve productivity. The core business case for GBS revolves around 30%+ upfront arbitrage-driven cost savings and 5-10% YOY productivity with a veneer of better stakeholder experience and improved business outcomes. For enterprises that have been at it for decades, start realizing there is a limit to how much juice you can squeeze from a lemon and start witnessing diminishing returns. As we mentioned already, your C-Suite has long since stopped celebrating the costs you trimmed in the past, they will soon be demanding new thresholds of value that aligns with their innovation agenda (if they are not already).

GenAI is driving a whole new innovation agenda and GBS leaders must be part of the conversation

GBS leaders searching for the next big thing after “offshoring” may have their prayers answered with the dawn of GenAI. It promises a significant productivity improvement (not just incremental) on voice-based work, coding, testing, and transactional processing – the core of any GBS operation. What’s even more interesting is the ability of AI-driven operations to support autonomous decision-making, exception processing and the capability to handle a more creative scope of work (think art, writing, design) beyond mundane and boring activities.

The dawn of GenAI has created an inflection point for GBS to jump to a new S-curve of value creation:

The S-Curve we once knew as linear now has a huge kink in it: where we could save 20% here or 30% there with the use of smart automation, chatbots, and simply using better software and cheaper labor aligned to better processes is now up having a major shake-up – and this will happen quickly.

For example, one onshore call center operation has hooked up a GPT-4 bot to its Salesforce system and can already see how 50% of its staff can be reduced within months. There are many, many other cases quickly emerging – they are emerging almost daily as we all tinker with the disruptive potential this is going to have.

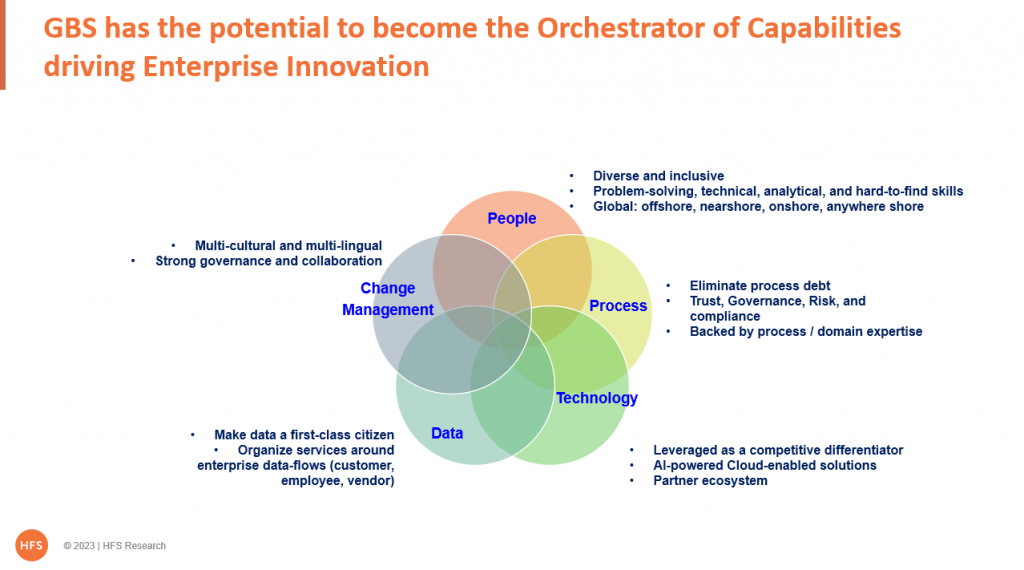

It’s time to stop underselling GBS as a large-scale operational entity. GBS has the potential to be an innovation capability orchestrator

The common perception within most enterprise stakeholders of GBS is associated with large-scale and process efficiency. GBS leaders must market their capabilities better. GBS can become the orchestrator of capabilities required for enterprise innovation if it stops underselling itself around running transactional processes for the enterprise:

The winning mantra for GBS is EX+PX = CX. In our obsession to deliver the best CX, we ignored EX for far too long. Thankfully, the “Great Resignation” of 2022 created the burning platform to at least try to resolve our talent equation. However, we are still missing an important stakeholder – the PX (Partner Experience). No-one-can-be-everything-to-anyone and more organizations are now realizing that they need an ecosystem strategy to be at the forefront, along with customers and employees (See HFS’ POV on OneEcosystem).

The bottom-line. Focusing on the old way of doing things is no longer the way forward for GBS

Successful GBS of the future needs to be training grounds for talent, data, and AI business models. GBS needs to be generative… by driving and promoting new ideas and ways of thinking and operating. The back office perpetuated by tired old GBS models has held back enterprises for far, far too long. The tools, know-how, and competitive realization are forcing the move to a generative mindset for those companies desperate to propel themselves forward into the GenAI-era. Don’t get left behind…

{kind=link}

{kind=link}