One of the business mantras we hear far too often is the concept of “fail fast”, but like other all-or-nothing business slogans, it’s majorly flawed. Although digital technology is disrupting many industries and business processes, “failing fast” is not a great approach to decision making: yes or no, or on or off is too simplistic. Decision making needs to be more analogous, much more nuanced, based on real context, and, most importantly, real-time data.

That said, failing is vital to any business, but simply failing and moving on to the next idea? Throwing your business thoughts against the wall and seeing what sticks, like some perverse infinite monkey approach, is not smart. Failing and limiting the damage from a dead-end pursuit is a good idea, but the real value of failure is what you learn , and how your subsequently apply that learning experience to your business. This is what provides the value.

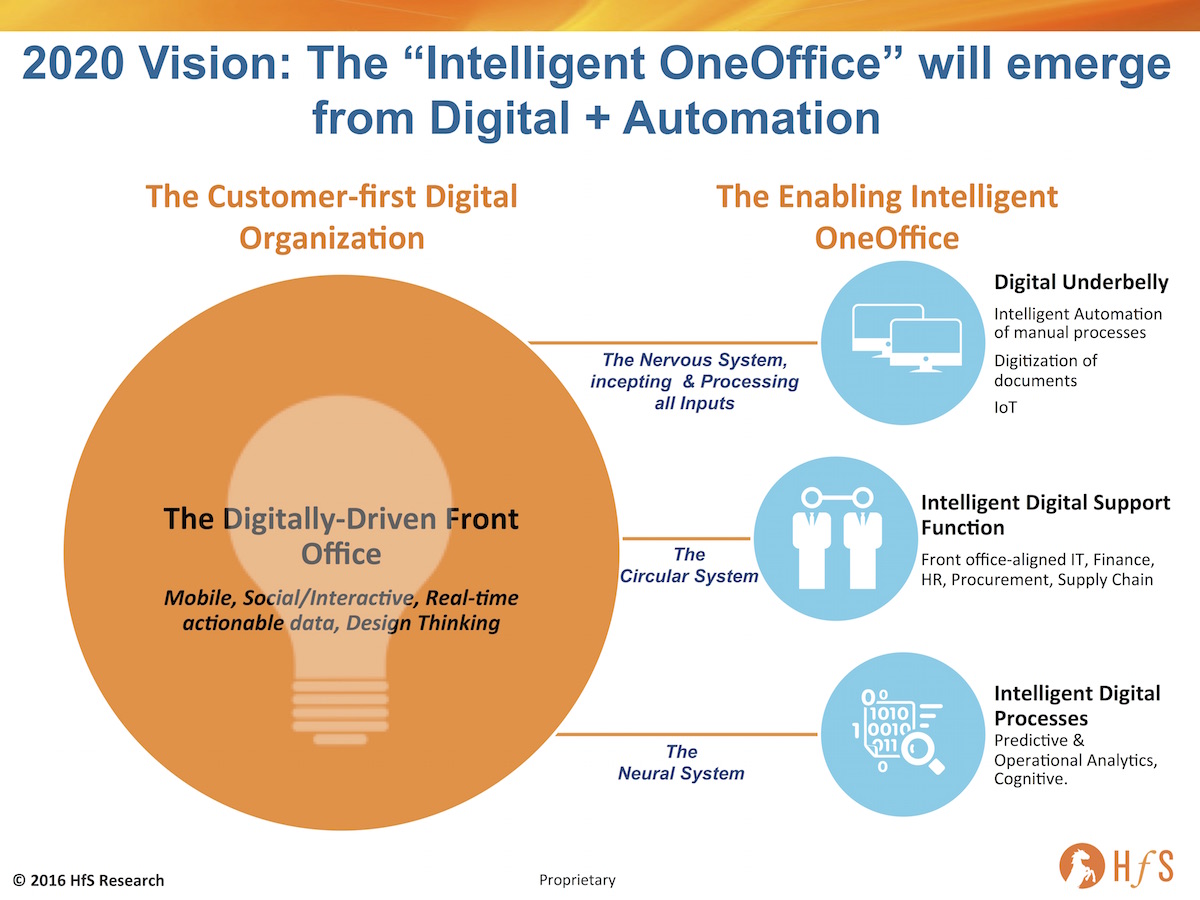

You may have seen the OneOffice operating model that Phil has shared on his blog here.

The goal of the OneOffice is to engineer processes to ensure that the whole of an organization is greater than the sum of its parts. Any system, within any organization, is likely to become inefficient or will require maintenance or over haul at some point. The issue with current business practices in many industries, is their systems and processes have typically been operated using closed feedback loops.

The “innovation cycle” in legacy traditional business models has been driven by the experience of business leaders who have not had the benefit of accessing and interpreting the vast amount of data – particularly around the cause and effect of changes to business practices. The biggest change driven by Digital is not the better interaction or access to new markets, but analyzing real-time data from interactions right across the customer, supplier and employee value chain to make informed decisions on the future. It gives companies instant (or near instant) feedback on its decision making loops – which can be used to create a massive open feedback loop for decision making that helps business leaders create their markets, not simply react to historical facts.

In such a feedback loop, the impact of changes made, at any part in the system, can be tracked and analyzed. This data can determine, for example, when and how products are launched, the level of training a new product will require – and perhaps, more importantly, whether this strategy was correct. The open feedback loop is the heart of Design Thinking and the key to successful OneOffice schema. All parts of the organization are joined so cause and effect can be judged. Failure can be measured and learned from. Equally, the real reasons for success can be measured and replicated.

The Bottom Line: Embrace your mistakes – and Learn from them

The most important feature of Design Thinking, or any business system designed to drive data driven decisions, is to create a culture where mistakes are embraced and learned from, rather than hidden and repeated. A good example of this is the “Aggregation of Marginal Gains” ethos used by the British Cycling team, which helped it go from 2 medals in the 2004 Olympics to 12 in 2016 (6 of which were gold). The assumption being that any process can be improved. When you look at a system as a whole it’s hard to see how to improve it, but if you look at the components it’s easy to see how small improvements can be made. When a customer outcome isn’t as good as it could be, what can be done to make it better?

Refusing to change our ways in today’s energy sector is a certain recipe for failure. There are a lot of inefficiencies in Oil & Gas, which in times of high oil prices and high margins, are largely hidden and/or ignored. In today’s continued low oil price environment with low margins and profitability—what we believe to be the new normal—Oil & Gas companies need to take out inefficiencies and find new ways to optimize production and bring down operating costs like never before. Our Energy Operations Blueprint highlights the way Oil & Gas companies are looking at digital technologies, automation and outsourcing as avenues for change, and levers to pull to drive new efficiencies and value creation.

Sustaining the current momentum of change in today’s environment is a huge challenge for Oil & Gas companies and their service providers. Changing for new results requires progressive change from within, not just rearranging the deck chairs hoping for a different result. The Blueprint identifies eleven trends that are currently taking place, and while they all serve a purpose to address the trends impacting their world, there are a few that bubble to the top.

Four trends that we see as an opportunity for focus by service buyers and providers to increase the value of their engagement over time:

Evolve analytics capabilities to cater for energy-specific applications. Analytics offerings have started to progress from being based largely on access to data science talent and unique algorithms to include industry specific analytical applications delivered by service providers that deeply understand a client’s enterprise and marketplace. We see good progress in analytics that improve the drilling process and analytics capabilities underpinning the 24/7/365 monitoring of thousands of units of critical equipment from a central support center in Exploration & Production.

Leverage data to look into the future, not the past. Predictive and prescriptive analytics are starting to enable more real-time decision-making and continue to have a huge impact on the operating models in the industry. The industries’ strict requirements for safety, reliability and uptime in operations, often in harsh circumstances and remote locations can be better met with advanced analytics capabilities offering real-time and actionable insights. Knowing what went wrong through descriptive analytics simply doesn’t cut it.

Put IoT at the heart of your planning. The (Industrial) Internet of Things holds tremendous promise and we expect adoption to accelerate as there are already huge numbers of connected assets in the industry and providers and Oil & Gas companies have to focus on connecting those assets to the internet to bring tremendous value. Think about how in Midstream, pipeline sensors providing data on transportation of product and the health of the pipes replaces the need for field workers to get sensor readings in person. And using drones and connected sensors to inspect the gigantic stretches of pipeline in difficult terrain instead of visual inspections by field workers.

For future effectiveness, focus on IT/OT integration and the Digital Oilfield. The digital footprint is increasing in Energy Operations, bridging the gap between Information Technology and Operations Technology. In Upstream, advanced analytics improve operations in drilling, reservoir modeling and engineering and remote monitoring.

Bottom Line: It’s time to dare the industry to build—not inhibit—momentum for change

Here are two dares I want to put forward to Oil & Gas executives and service providers respectively, both of them critical to sustain the change momentum and achieve the innovation that is so desperately needed:

Energy Buyers – Dare To Reinvest Cost Savings into Innovation Funds: It is very attractive to put cost savings achieved by outsourcing in the hands of the CFO. However the CFO isn’t going to turn around and say “great job, let’s all sit back and celebrate that 20% off the bottom line”. We recommend to reinvest these savings in further innovation, perhaps make it a part of a Collaborative Engagement arrangement: “Service provider, save us 20% and we can both reinvest the 20% as next year’s innovation budget”. For example, saving driven through the offshoring of application development and accounting work could be funneled into a digital oilfield project.

Energy Service Providers – Put Your Money Where Your Mouth Is: Pro-actively and aggressively push the innovation agenda around automation, analytics, drones, 3D printing for MRO, simulating with digital twins, machine learning, deep learning, cognitive computing. Present clients with use cases, examples and capabilities to “unfreeze,” inspire and build credibility in innovation.

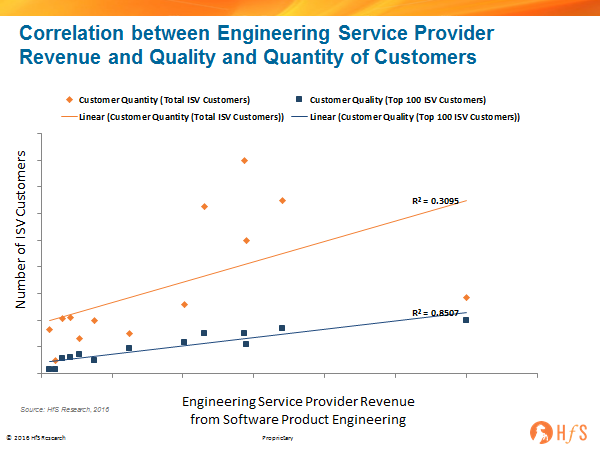

We often ask this question. Customer quantity is a no brainer because more customers can bring more revenue. Similarly, customer quality is also important because the better the customer quality or size, the better the revenue potential for service providers. But what is more important—customer quantity or customer quality?

We all have the anecdotal answer to this question based on our experiences but what does the data say?

In one of our engineering service studies, we tested this on data and found interesting results. In our software product engineering services study, we correlated service providers’ software product engineering services revenue with the quantity and quality of their customers (see the Exhibit). For customer quantity, we took the count of service providers’ ISV customers. For customer quality we took the count of service providers’ ISV customers that are among the top 100 ISV customers by revenue because the larger the size, the better the potential of account mining.

We found that the correlation between service providers’ revenue and quality of customers is very strong (Correlation = 0.92 and R2=0.85) in comparison to the correlation between service providers’ revenue and quantity of customers (Correlation = 0.56 and R2=0.31): As a student of mathematics, I will be the first one to point out that correlation doesn’t mean causation. But it nevertheless gives us the opportunity to step back and ask ourselves the following: What if the quality of customer drives revenue more than the quantity of customers? What are the implications for engineering service providers and how can they position themselves to grow in a more future-oriented way?

Service providers should focus on the quality of customers and persistently target large customer accounts: This is a no-brainer as a strategy but sometimes difficult to execute. Getting a foot in the door of a large account and displacing incumbents can be difficult and requires persistence. Sometimes, with quarterly pressures mounting, service providers give up on these large accounts and target easier options. In my earlier gig, I came to know that it took seven years to penetrate a large customer account (Yes, seven!). In quarterly reviews, leaders sometimes lose focus on long-term targets, but in this example, leaders kept asking for an update on this particular account in every quarterly review I attended. What is happening in that account? Who has the account manager met with in the last quarter? Are there any RFIs or RFPs they’ve heard about? Any chances of proposing free PoC? Any firm they can partner with? And the list goes on. It requires the persistence of leaders to pursue this long-term strategy and luckily the business leaders in that firm were for the long haul (they are still working there when I last checked =) ).

Once the service provider has got a foot in the door, grow the account by making it real and not over-selling: In engineering services, especially at this time, service providers are competing more with the non-outsourced spend than with other service providers to grow the accounts. Service providers have told me that even after signing the contract and setting up the ODCs, the accounts just don’t grow. One piece of feedback I heard from the buy-side is that many product leaders are skeptical of outsourcing and somehow service providers need to convince them. Service providers typically approach this by hiring good sales and account managers. But the problem is most of the product owners or decisions-makers are technical guys and they don’t like sales guys or account managers showing their face every month. But they do like to know industry trends, what their competitors are doing, where the industry is moving. So, in my opinion, service providers will do better if they invest in “making it real” (something Phil Fersht has also written about in the larger IT services context). In other words: share prototypes, case studies, and demos. But don’t sell!

Mid-tier and emerging service providers should focus on smaller customers and develop their solution value proposition: The mid-tier service providers might not have the luxury of time and manpower to focus on the big customers. They will do better to focus on smaller customers that are not natural targets of the larger service providers. They should grind it enough to make themselves ready for the bigger customer later. The disruption often starts at the bottom and slowly moves to the top. Amazon has done the same with the cloud. Its initial value proposition was aimed at startups and SMBs. Now it is ready to compete in the bigger customer segment. One Fortune 100 buy-side customer told us that they gave a few projects to a mid-tier engineering service provider because it was more cost-competitive than many leading engineering service providers. Although the customer is satisfied with the service provider’s delivery quality and timelines, the customer feels that the service provider has limitations in domain knowledge, solutions, organizational maturity and the customer is unlikely to give that service provider any major additional work. In a way, this mid-tier service provider wasted the opportunity by entering the account early without sufficient capability. The mid-tier service provider should have defined its value proposition beyond cost reduction when they bid to enter large accounts.

The Bottom Line: Both large engineering service providers and mid-tier engineering service providers can use this correlation research to review their client acquisition and account growth strategies based on quality and quantity of customers.

Clients are being subjected to such a load of nonsense about the impending impact of robotics and cognitive computing on enterprise jobs, many are literally terrified. Conversing with the “head of automation” for a F500 organization today, is akin to meeting a Secret Service agent in a clandestine alleyway. These people do actually exist, but most have to conduct their work under a veil of secrecy, due to the level of discomfort and panic our robo-commentators are making in the presses.

Remember the panic about jobs getting shipped offshore? Well, that is child’s play compared to the emerging tumult of fear being generated by jobs being completely eliminated by robotics. Net-net, people are frozen stiff with fear, and it’s the responsibility of respected analysts, consultants, academics and journalists alike to educate and world using real, substantiated facts. Sadly, the likes of Gartner, McKinsey, Oxford University and our beloved Stephen Hawking, all seem hell-bent on capitalizing on the panic to grab the headlines (read my post earlier this year) as opposed to dispelling much of the ridiculous scaremongering about the impact of automation on job losses.

At HfS, we published a very thorough analysis on the impact of automation on global services jobs, showing there is likely to be modest downsizing of ~9% over the next five years as low-end tasks are increasingly automated across major service delivery locations. And this 9% will be immersed in natural attrition and redeployment of workers to other industries, as global services streamlines and matures as an industry. Yes, there will be impact, and it will be somewhat painful to absorb for some enterprises, but it’s not the impending workforce apocalypse these people are predicting.

So why, pray tell, is Gartner, a respected voice in IT research, continually pounding us with continual scaremongering that we’re all doomed to the will of the robot, and we may as well start preparing for a life of unemployment, or sandwich making? Oh wait, robots can even make sandwiches, right?

Peter Sondergaard, Gartner’s Head of Research, predicted one in three jobs will be converted to software, robots and smart machines by 2025. OK, that’s so far out in the future, I think Peter’s on pretty safe ground here – he’s probably going to have cashed in his Gartner stocks long before then, in any case, and be on a golf cart somewhere, when one very earnest soul decides to dig into the Gartner archives of previous decades to read very old research, with very dodgy predictions, that absolutely noone care about anymore. So we’ll let Peter off the hook here – he wanted to make a splash at his Symposium and he achieved exactly that.

But then we get treated to this almighty whopper from Fran Karamouzis, a vice president and distinguished analyst at Gartner…

By 2018, more than three million workers globally will be supervised by “robo-bosses”. Wow – isn’t this barely more than a year away? Excellent, so Fran’s going to be around to declare automation glory when global employment goes through a robo-geddon so seismic, it’ll be like all three terminators visited from the future at once to change the world? My god – what is going on here? The suggestion that an employee will be supervised by a machine simply cannot be corroborated by any meaningful research…

So why do we, at HfS, view claims like this as factually incorrect and irresponsible?

There is only one very shaky example of “robo advisors” in the industry. The most cynical implementations of automation that HfS has come across, thus far, where direct replacement of human labor by robots is the declared outcome, are examples such as Royal Bank of Scotland, where virtual agents, deployed as “robo advisors” are solely deployed to replace FTEs. We’ve also witnessed a service provider radically downsizing some delivery staff claiming success of its robotics strategy (only to find out later these staff were simply redeployed elsewhere). Let’s be honest here, the onus so far seems to be about firing people and using “robotics” as the smokescreen. While Intelligent Automation decision-making will undoubtedly increase (view our Continuum here), we see no examples of employees being supervised by bots. At HfS, we are covering every deployment in the industry, and are just not seeing it.

We still haven’t had a real debate on the ethics of automation and cognitive computing in the B2B environment. Suggestions that employees will be supervised by bots can be traced to the broader discourse on Artificial Intelligence, where more consumer-facing technologies are discussed with undercurrents of movies, such as the Matrix. These discussions tend to focus on technology capabilities of providers like Google and Facebook. However, we haven’t seen a similar debate in the B2B space. If anything, the B2B urgently needs a debate on the ethics of automation, in light of these nascent cognitive capabilities. But to surmise that robobosses will be so prevalent in barely over a year before we’ve even had these debates is quite absurd.

The speed of internal organizational change is painfully slow. The tendency from clients with automation is to pilot first, rather than to go full scale, and every ambitious forecast is always waylaid by the reality of interacting with legacy systems. Most of today’s Robotic Process Automation(RPA) tools are simply being retrofitted into smoothing over manual processes within legacy technology environments with obsolete processes. They are adding efficiency to broken operations, which may, in the future, lead to a lesser need for headcount in low value work areas. Talking about today’s enterprises being so close to investing in Robo bosses is just very wide of the mark. What’s more, much of this RPA technology has been around for more than a decade – this stuff isn’t exactly revolutionary, it’s just becoming more popular as enterprises figure out further efficiencies beyond initiatives such as offshore outsourcing and shared services

Cognitive tools are only just emerging. While IBM has done a stellar job aligning its Watson capabilities with the healthcare industry (read our report here) and software experts such as IPSoft’s Amelia and Celaton have some compelling client stories to tell, the focus on self-learning and intuitive cognitive solutions are mainly confined to customer service technology and virtual assistant chatboxes. Talk to the call center BPO providers and they’re really only just figuring this out…. forget robobosses, we’re still just trying to figure out some basic software to make chatboxes work better these days. Moreover, with Watson, our research shows it’s best application today in the medical field is helping flesh out the bad science and saving scientists serious amounts of time doing their research. Meanwhile Celaton, in the UK, has created a really cool tool to help Virgin trains handle emailed customer queries. But the long and short, here, is that Intelligent Automation solutions today are great at augmenting processes and unstructured data pools, not replacing real people who make real decisions doing real jobs.

The definition of robo bosses, and the potential value, of robobosses is missing. There is, however, something to be said for the value of increased automation combined with analytics to better understand the impact — measured by targeted business outcomes — in a more realtime way during a contract with a “gig economy” worker (or any worker). Such knowledge can help us intervene and train/coach a project “going south” sooner, or catch fraud fastest, or identify a worker to “gets it faster”. Along these lines, we see value in “robo advice”, but the point also needs to be made that these “robobosses” (give me a break) do not work alone, such as with Watson and health / medical diagnosis and treatment, they work in tandem with doctors / clinicians, changing and refining the dr/clinician job (freeing up that person to be more targeted and more of a coach than a statistician) with the intent of better medical results. These robo tools (or whatever we call them) do not replace the doctor / clinician.

Monitoring software has existed for decades… so when does it become a “Roboboss”? Currently, there are probably a million or more workers just in the UK (for example) managed by extreme monitoring of some kind. The Amazon style warehouse pickers, fast food cooks, many call center agents, delivery drivers, assembly line factory workers are subject to time monitoring and computers giving them tasks. We’re just not sure when this turns into a roboboss?

Bottom Line: The real “roboboss” is the human worker who can use Intelligent Automation tools effectively

It today’s swirl of gibbering noise around the social media presses, it’s the responsibility of leading analysts, advisors and academics to be the voices of sanity and reason, when it comes to topics as critical as the future of work elimination through Intelligent Automation technology. The vendors love the hype as it gets them attention with clients, but analysts who like to take money from these vendors have a responsibility to articulate the realities of these technologies to their clients. They are great at augmenting work flows, and even aiding medical discoveries, but this is the real value – it’s not about sacking people. It’s about making operations function better so people can do their jobs better. The real “roboboss” is the human enterprise operator who can use smart Intelligent Automation tools to enhance the quality of their work.

Net-net, industry analysts, advisors, robotics vendors, academics and service providers need to engage with clients around how all these disruptive approaches will affect talent management as well as organizational structures. Even without these apocalyptic scenarios, some job functions are likely to either disappear or be significantly diminished (as our 9% forecast reveals). Equally, we need to talk about governance of these new environments, touching upon ethical, but also practical, issues. This is not only a necessity for the broader adoption, but also offers high value opportunities.

I’ll probably get a few nasty messages as a result of this piece, but I sincerely hope this has the outcome of steering our industry conversation in a more realistic direction, backed up by real data and experts who prefer realistic conversation that mere headline-grabbing and panic creation.

A special shout out to Cartoonist and Innovation evangelist Matt Heffron for penning this little gem:

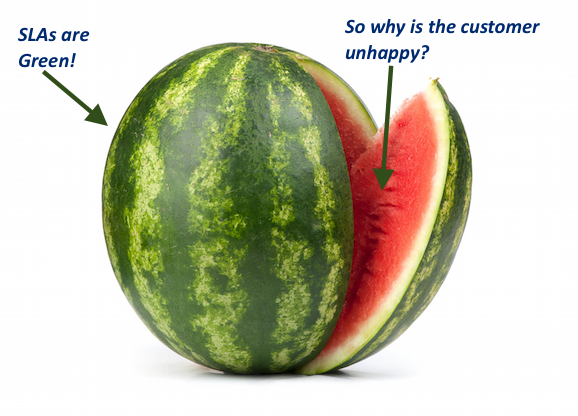

In her recent blog on outcome-based contracts, Christine Ferrusi Ross challenges the industry with Outcome-based Contracts Are A Nightmare –Do Them Anyway, and offers guidance and experience to rally the troops. What is also intriguing about this outcome-based approach is the potential to shatter the so-called “watermelon effect” that often takes shape in an outsourcing engagement that is based solely on key performance indicators (KPIs) and service level agreements (SLAs)… and use those traditional metrics as seeds for new value-based engagement.

What Is the Watermelon We Want to Shatter?

The outsourcing industry grew up on contracts that clearly articulate KPIs and SLAs, providing an agreed upon set of targets for the service providers to get the work done at a level that is satisfactory to the client. As transitions take place and Lean, Six Sigma and continuous improvement methods iron out processes and make them more efficient, these metrics regularly appear “green” on the scorecard. But, even when all the indicators are green, service buyers can be left feeling red—the so-called watermelon effect of green outside and red inside. There is often a sense that while all the targeted metrics for turnaround time, uptime, and transactions processed are being met, clients and service providers “feel” value is still missing.

This effect often leads to questions about the value of the contract and challenges for achieving innovation, price reductions, and competitive re-bids. The key issue is that perceived value changes as relationships evolve; therefore, the benefits received and the associated metrics to measure and manage real performance need to change with it. We once joked that “if outsourcing was an employee it would be fired,” meaning if you took a job and were judged on the same performance metrics every year, you wouldn’t last very long!

There is a Step Along the Path to Outcomes-Based Contracts

As Christine’s blog points out, outcome-based contracts can be incredibly difficult to create, but you can still address the watermelon effect right away while sorting out the outcomes desired. In one such example, we heard of service buyers and providers addressing this point by including a metric and payment based on Net Promoter Score in the contract. That way, all parties in the engagement have to figure out, and proactively address, that feeling of missing value. An example is a simple performance evaluation, on a regular basis, that asks for a rating of partner satisfaction on a scale of one to three. If the feedback comes back as a one, a percentage of the payment is held back, if a two, no movement of money, and, if a three, then a percentage bonus.

The intent is to drive the right attitude, behaviors and cadence of interaction and measure, not just the service levels and performance indicators, but that “feeling.”

Yes, it’s subjective, but isn’t any relationship subject to “feelings”? This “feeling” can be an indicator that the engagement is at a stalemate—that the engagement is no longer driving step change, helping the business to improve or address what matters to their customers today.

Using KPIs and SLAs As Seeds to Grow Outcomes-Based Contracts

How does a business outcome differ from a KPI or SLA? In practice, a business outcome often encompasses multiple KPIs and SLAs. For example, a business outcome in retail could be “increased sales closed by visitors that start a shopping cart,” versus an SLA which could be “ensure website has availability of 99.999%.” In healthcare, “decreasing the cost of care for a targeted population” could be a business outcome, while a KPI may be “percentage of targeted population enrolled in a relevant wellness plan.” They are not mutually exclusive, and when used together, can help advance an outsourcing engagement towards a structured, but more interactive and flexible arrangement for today’s dynamic business environment.

Looking at business outcomes puts the focus of the outsourcing engagement directly on the client and the client’s customers and stakeholders—the ones who are judging and measuring the client’s performance. The business outcomes for an outsourcing engagement in operations are broader than simple transactions, like website uptime or number of bills, invoices or claims processed. Using a healthcare industry example, what matters to a healthcare payer today could include retaining members in their plans, and that means KPIs that could include member satisfaction scores, and SLAs like payer web site uptime, claims processing throughput, and accurate provider data.

The Bottom Line: The point is not to move away from KPIs or SLAs in a contract, but to use them as building blocks for achieving real outcomes that make a difference to the client’s business goals… and in a way that can flex and change in order for the partnership between the service buyer and the service provider to stay relevant over time.

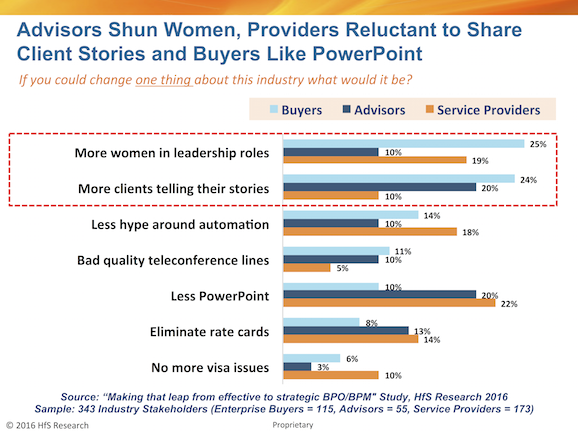

We set out a few weeks’ ago, with support from NASSCOM, to test the views of service buyers, advisors and providers on what the BPO industry needs to do to make the leap from delivering mere efficiency to one that can provide genuine strategic value to clients (if this is indeed possible).

As we filter through the first results, what immediately leaped out at me was the following:

Clients want more women leaders and real case studies… more than anything else

“Why are these providers and advisors dominated by boring men in gray suits?” bemoaned several clients at one of our HfS Summits recently (where more than half the buyers executives present were actually female). This is a serious issue, folks. Our industry has – somehow – become dominated by too many dinosaur service provider executives with their lavish air-miles accounts and two iPhones* (why do some people insist on having more than one iPhone? Are they really that popular?), who have, at the same time, somehow lost all records of actual client success stories that justify their new vernacular around “digital transformation” and “automation”.

In fact, during one service provider briefing last week (which will remain nameless), we asked an executive to explain how he defined “Digital Transformation” (after many utterances of said phrase) and the poor chap was positively floored that he was asked to define what he was talking about. These people seem to be obsessed with recanting the vogue buzz phrases, without the need anymore to know what they really are. Can we just call it “technology” again and go back to sharing real examples of how technology can enable and transform client performance? Can we just explain what all this hype is surrounding automation and emphasize that most of today’s RPA technology has actually been around for more than a decade in many shapes and forms?

Here, it’s abundantly clear that we need to see more women – and, dare I say it, more youthful executives, who can simply connect better with the clients. Everything has become so dominated by the men in gray suits, who talk in increasingly more impressive riddles that are becoming increasingly distant from reality. Moreover, we need to dispel much of the hype surrounding automation and jobs impact: Gartner’s unsubstantiated claim that “more than three million workers globally will be supervised by robobosses in just 18 months’ time”, is simply irresponsible and unprofessional. It’s time to make it real and drop the hype and scaremongering…

The Bottom Line: It’s time for progressive change from within to break ourselves out of this legacy holding pattern

The industry has spoken, and it’s not pretty – clients are fed up with the same old selling, the same old unsubstantiated hype and the same old cronies dishing it out. Change only comes when we look at progressive change, not successive change. This means we must stop making the same old mistakes by replacing jaded middle managers with more faceless middle managers with a hype-upgrade; this means we must stop plastering out turgid marketing that was really a rip-off of the other ten competitors, with a different logo slapped on it.

We need real people selling and delivering our solutions, who can listen to what clients need and can really empathize with them, who are diverse across the genders, the age groups and the ethic backgrounds. We need to start talking real English again, and less of the manifested garbage we can’t resist spewing out to mask our insecurities. As our whole 2017 research theme at HfS is centered on… it’s simply time to start making everything real again and redefine our industry as something that is geared up for our clients’ real needs, not needs we are trying to convince them they have!

*In full disclosure, the author of this article has been seen once sporting a gray suit and did possess two iPhones for a brief period of time. He has since changed his ways…

One thing about testing services that continues to strike me is that the development is largely out of sync with the broader IT market. That is not to suggest that the testing community lacks sophistication or innovation, but we cannot just use the usual mindset, concepts and monikers without adaptions when we discuss testing services. Much of that has to do with the reluctance of buyers to invest in testing. For many organizations, testing services remain a secondary concern when setting strategic IT goals or embarking on transformation projects. Yet, as organizations journey toward to the As-a-Service Economy is accelerating, and in particular Intelligent Automation is fundamentally changing the way we deliver services, the discussions on testing have to move center stage. HfS had the opportunity to sit down with executives of Capgemini and TCS to discuss their strategies for test automation and how the notion of Intelligent Automation will shape the future of testing services.

Desperately seeking an organizational model for testing

Testing services have never fully mirrored the broader IT market in the way it was seeking to optimize its organizational models. Be it aiming to centralize large parts around the notion of shared services or be it by embracing large-scale outsourcing. The build out of Test Centers of Excellence (TCoE) has always been a litmus test for the progress with centralization efforts in testing. However, as executives at Capgemini put it:”TCoEs have flat lined”. The reasons for that a likely to be twofold. First, the lack of maturity on the buy-side. Second, the traction of Agile and DevOps methodologies. The latter has two direct consequences: On the one hand the requirement for more co-location, yet as Capgemini put it with more intelligent solutions than just aligning delivery teams. On the other hand, both executive teams agreed on the rise of Distributed Agile. While Agile is intrinsically aligned with the journey toward the As-a-Service Economy, the testing community has to articulate and demonstrate what the concept exactly means. Not least in the context of vastly varying buyer maturity, or in the exasperated words of a Capgemini executive:”99% of the market is still Waterfall.” As a result, both Capgemini and TCS see Distributed Agile as the next key development phase for testing services.

Deconstructing Test Automation

Distributed Agile is the logical evolution of testing services to support the journey of organizations toward the As-a-Service Economy. Yet, as we have suggested, we need clarity around the different methodologies and monikers compared to the broader market. Historically the notion of Test Automation was largely defined as test case automation, and to a lesser degree as the automatic provisioning of test environments. For Capgemini, the direction of travel is toward the notion of a Virtual Test Factory (VTF) that can be embedded in heterogeneous test factories through virtual delivery management and governance. Over time it will also be key for the alignment with Automation Drive suite of services that is aiming to leverage the disparate, broader automation skills as well as four CoEs across the traditional business units. Thus, progress with VTF is crucial for pushing competitiveness and distributed agile as well as moving toward the As-a-Service Economy. The two key building blocks for that journey are Smart QA, an end-to-end ecosystem that includes smart assets, zero touch testing, smart environment provisioning, 360 degree view insights and smart analytics to drive down cost of delivery and cycle times significantly while improving customer experience. Furthermore, the Intelligent Test Automation Platform (ITAP), comprising of intelligent frameworks and robotic agents that underpin analytics and rules driven smart test strategy, quality gates, job chains with no manual intervention leading to continuous testing and delivery. Both platforms are centered around end-of-end life cycle automation along with smart dashboards to offer a service catalogue as well as a heat map of critical issues. Consequently, these platforms are evolving toward notions of self-remediation. However, in this context self-remediation means more providing knowledge-based solutions for business agents than self-remediating engines.

TCS is echoing many of the sentiments on Distributed Agile. To adapt its existing client relationships to this methodology the company is creating “virtual rooms” on the account level. Thus, assuring that the “distributed” work streams are being aggregated to support business processes. Therefore, the vision for its 360 Degree Assurance Platform is to evolve into an Adaptive Assurance Ecosystem. To progress toward the notion of “adaptive”, TCS is aiming to leverage Machine Learning and AI to evolve into self-healing capabilities. This is predominantly done by leveraging a set of neural networks (i.e. beyond its flagship platform ignio). Use cases are test suite optimization, automated defect analysis and the prediction of outcomes through linear regression algorithms. TCS executives were pointing to the fact that customers are starting to look for value chain execution rather than just test case execution. Another reference point that testing services are starting to move up in the value chain.

What are the testing strategies for Intelligent Automation?

While the two discussed approaches indicate that the testing community is closing the gap to the broader IT market both in terms of development as well as maturity, one obvious question has still not been answered: What are the testing strategies for Intelligent Automation? When we put this question to the supply side, the standard answer tends to be pointing to the broad portfolio of existing testing services. Yet, are these service sufficient to test Deep Learning and broad scale Cognitive Computing? Traditional approaches can look at outcomes or deal with user acceptance testing, but how should we deal with the ever more sophisticated algorithms that underpin those concepts and how can we assure that those algorithms are crunching the right data sets? If the testing community wants to be included in the decision-making for the large transformational projects it has to find answers to those questions.

Bottom-line: The testing community has to find its voice – one that is being understood by the business

The more the market is moving toward the As-a-Service Economy and outcome based models, the more the testing community has to find solutions as to how to support those strategies. While we see a clear maturation in testing services, the community has to change its mindset and embrace business-led discussions. Thus, the supply side has to move beyond conversing in jargon around function and features to align itself with the broader IT stakeholders. In Q4 we will launch a Blueprint on Application Testing for the As-a-Service Economy and look forward to exploring these themes with stakeholders.

Perhaps the best example of the evolving As-a-Service delivery model that immerses all the value levers of global delivery; namely offshore talent, cognitive automation tools, analytics and the digital customer experience, can be found in the burgeoning mortgage processing industry. With banks going all out to sell highly competitive mortgages at record low interest rates, the onus to manage the whole process both efficiently and intelligently, while battling all the regulatory demons, has never been so great.

Two years after our inaugural Blueprint in Mortgage BPO Services, we took a fresh look at this industry… here’s announcing the findings of the HfS 2016 Mortgage As-a-Service Blueprint, led by HfS banking analyst, Reetika Joshi.

The concept of delivering mortgage As-a-Service, using plug and play digital business services is still in its infancy. We’re not quite at “push button, get mortgage” as an industry – and the verdict is out on whether this is the right message to send for a lending environment that is still rebuilding itself, seven years after the 2008 housing crash. How do you do this without raising eyebrows? You’ll have to ask Quicken Loans, as they learn from the backlash of their Super Bowl campaign with that very slogan.

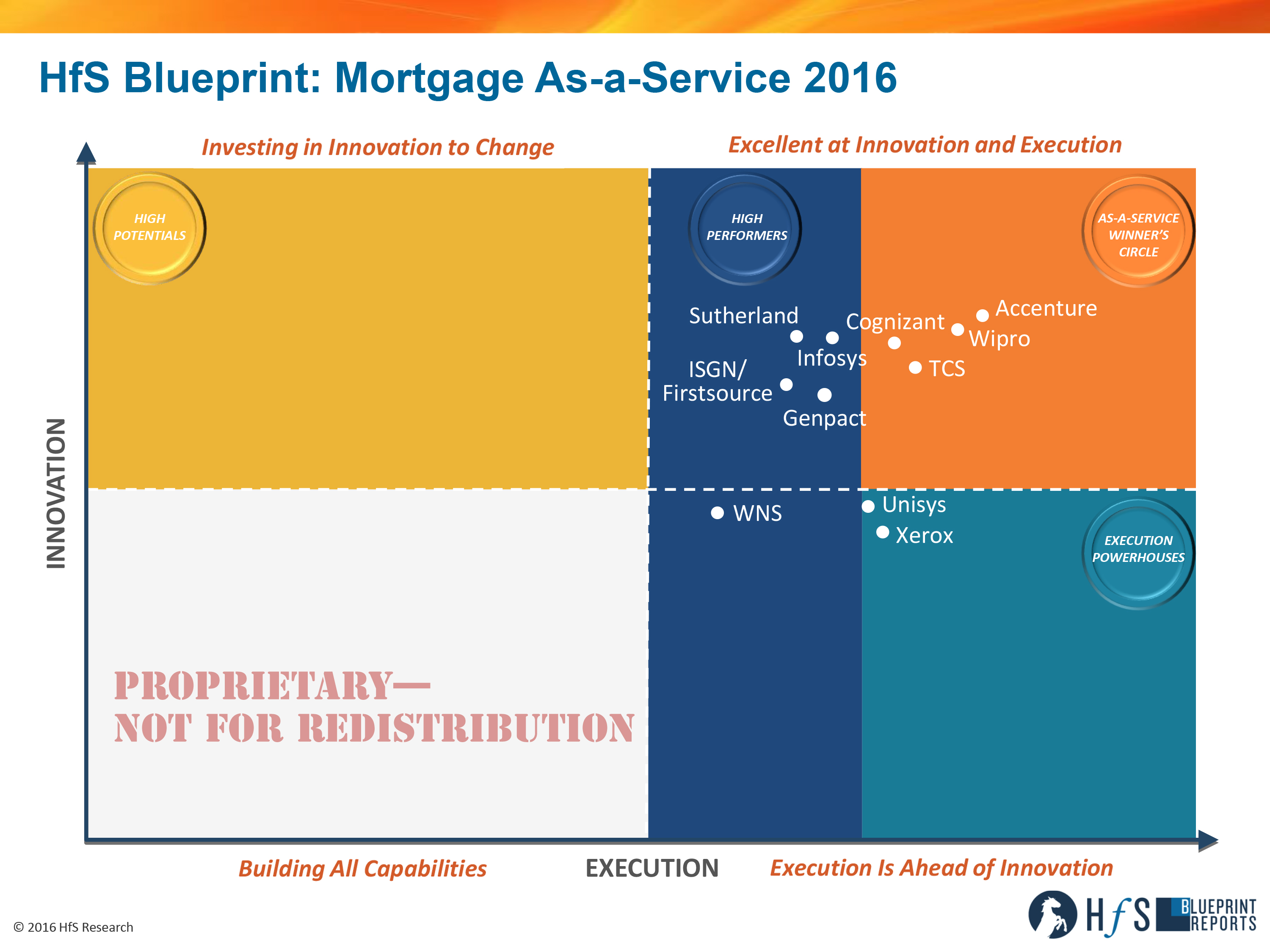

Reetika, how do you view the 2016 Service Provider Landscape?

Our HfS Blueprint methodology assesses service providers based on two critical axes: Execution and Innovation. We gather data to support our analysis from client reference interviews, market interviews, RFI submissions and exhaustive service provider briefings.

In this Blueprint, we identified four As-a-Service Winners: Accenture, Cognizant, TCS and Wipro. These service providers have the strongest vision for As-a-Service delivery in the mortgage industry, and are driving collaborative engagements with clients to bring this vision to life. They are making significant investments in future capabilities in automation, technology and borrower experience to continue to increase the value over time.

The High Performers in this year’s Blueprint are a highly competitive set of service providers: Genpact, Infosys, ISGN/Firstsource, Sutherland Global Services and WNS. They have high execution capabilities and are growing their client bases as a result of investments in future capabilities and innovation. These service providers have the pieces in place for As-a-Service delivery, and need to focus on consistently bringing these capabilities to clients and scaling up with broad, multi-client solutions. We expect them to challenge the Winner’s Circle leaders in the next couple of years, with each building on unique strengths and assets in this vertical.

We see Unisys and Xerox as the Execution Powerhouses. These service providers are strong in operational excellence with ubiquitous technology platforms in their respective markets, and need to focus on value chain expansion and innovation in their services stack:

Why does mortgage needs to have a different approach and response to “digital disruption”?

Despite this sensitivity, other industry forces still march on; regulation, homebuyers and a new breed of disruptive fintech firms are steadily shifting the entire mortgage industry towards generally being more digitally enabled. Lenders have this big ask today: how to carefully balance their investments in new technologies, with changing consumer needs, volatile rate environments with rampant M&A, their company’s own appetites to write off/augment internal legacy systems, and all while continuing to remain compliant in an increasingly watchful regulatory environment.

Borrowers are increasingly looking for three key benefits in their interactions with agents, brokers, and lenders:

Simplification in the processes, handoffs and interactions

Transparency in the loan terms and costs, application progress

Control in document and information exchanges, decision making

The use of digital technology can greatly help lenders to achieve these experiences, in both facilitating interactions and in creating operational efficiencies at the back-end to speed up applications and free up loan officers’ time. In becoming digitally driven, lenders have a long way to go in thinking about e-mortgage beyond digitization, and borrower experiences that are built on new engagement strategies, especially as the market shifts to more purchase originations and persistent refinancing dictated by flat-lined interest rates.

So what’s fundamentally changed, since the inaugural Mortgage Operations Blueprint in 2014?

HfS believes that the Mortgage Operations market for both residential and commercial loans is on the cusp of a significant transformation. Several lenders in our research described their mortgage processes as complex, broken and in need of help to compete with non-traditional lenders and faster cycle times. Said one, “Our industry needs to go through massive business process reengineering efforts…so many lenders don’t have processes documented still. We need to start there [with our providers], to find ways to improve cycle times and create better experiences for borrowers.”

There is a marked departure in the market dialogue, away from labor arbitrage and manual “lift and shift” processes, and towards using a combination of technology platforms, analytical insights, automation, digitization and other accelerators to redesign processes and drive more value in sourcing engagements.

Some areas that have changed since our last Blueprint include:

With greater purchase originations, we see the mortgage operations market more broad-based in the work sought from lenders. Accordingly, service providers have grown both their technology and process capabilities in originations and servicing in the last two years, with a few that have foreclosure and default management work today.

Great examples of service provider capability in creating and embedding analytical insights and data into different parts of the mortgage value chain, understanding the key triggers/outcomes in the process such as predictive modeling for loan origination to help prioritize underwriter time and understand likelihood to close.

New services and technology accelerators coming from service providers to address regulatory pressures such as the audit and due diligence reporting back to CFPB, which is increasingly getting more complicated and frequent. Clients expect more guidance and recommendations in regulatory changes and their impact on technology systems/processes/data to maintain compliance.

And what are the HfS Predictions for the Next 2-3 years of Mortgage As-a-Service?

The biggest developments we see in the mortgage market in the next few years are:

Greater Alignment of Services Around MOS Platforms: Service providers like Wipro, Accenture and Genpact that have made investments in acquiring MOS technology vendors have goals of providing a broader, end-to-end portfolio in mortgage, including people, process and technology. This is an indicator of a vision for providing Mortgage As-a-Service. However, most of the acquisitions made were of independently branded software solutions, accompanied by their own branding legacies. Infosys took a different approach with its startup acquisition to create CreditEdge. In the next two years, we expect these service providers to further articulate and demonstrate how these technology buys change their value proposition, towards greater clarity and examples of delivering Mortgage As-a-Service.

Mainstreaming of Process Automation: It has taken a while for process automation to cautiously make its way to the forefront of conversations in mortgage operations, due to its troubled “robosigning” past. We are now seeing greater understanding by both service providers and buyers to start thinking practically and implementing different kinds of automation technologies (RPA, intelligent OCR, etc.) across various parts of the mortgage services value chain. Today thus represents the early vanguard and the arrival of RPA in mortgage, leading us to believe that adoption will be fairly rapid over the next 12-18 months.

Digital Driving Disruption at the Top: Several of the big lenders that HfS interviewed are still playing the “wait and watch” game on digital disruption, in particular the strides made by fintech startups and non-traditional banks in the mortgage industry. While “push button, get mortgage” as we discussed above might not be the path for all the Top 50 to go down, lenders are initiating more conversation and strategy around how digital components can help them look at traditional operations differently. Service providers will have a big role to play in this, from a process reimagining perspective, as well as ultimately configuring the digital components that link these activities back to onboarding and origination platforms.

HfS readers can click here to view highlights of all our HfS Blueprint reports

HfS premium subscribers click here to access the new HfS Blueprint: HR Mortgage As-a-Service 2016.

Who Are the As-a-Service Winners in Energy Operations? HfS’ inaugural Energy Operations Blueprint reveals frontrunners Accenture, EPAM, Infosys, Wipro and TCS

Why An HfS Research Blueprint for the Oil & Gas Industry?

Tumultuous times in the Oil & Gas industry. Understatement of the day I hear you say… Time for a rigorous look at the role service providers play to help Oil & Gas clients battle adversity.

The Oil & Gas industry is on the cusp of a significant transformation. Economic, societal, market, political and regulatory pressures are coming together bringing immense challenges for companies to solve through more effective and lower cost operations.

HfS sees a significant role for next generation services providing flexibility to scale up and down, agility to deal with a volatile environment and fully leverage digital technologies and digital enabled business and operating models now and in the future.

What does this Blueprint cover?

This is not a beauty contest about size, revenue and global scale. There is a place for smaller providers that excel in a niche and help clients on their As-a-Service journey.

One of the key attributes we looked for in this Blueprint process was if the service provider has a real Oil & Gas practice, not a collection of contracts with a sign “Oil & Gas Practice” slapped onto it. In this light we are interested in the way service delivery is organized, the availability of industry domain expertise, investments in industry talent, acquisitions of companies with industry specific capabilities and partner ecosystems. Another point of emphasis in our research is the move to As-a-Service, how service providers are enabling new ways of working, how automation and analytics are used to tackle industry specific challenges and the level of innovation brought to clients.

Key Market Dynamics

Two dynamics jumped out at us during the Energy Operations Blueprint process:

Oil& Gas Companies Looking for NewLevers: As the focus of the industry is on cost reduction, production optimization and operational efficiency, automation and outsourcing are two principal levers available to the industry. The name of the game for Oil & Gas is: Fix the basics and leverage new technologies. Oil & Gas executives are forced to have a good look at their strategy. Key questions include:

What is the core of our enterprise?

What do we need to do internally, what differentiates us from the competition?

What parts of our processes can we automate?

Can we outsource what we can’t automate?

Buyers Perception of Service Provider Becoming More Strategic: A pivotal changing dynamic in the market is how buyers look at their service providers. With the renewed focus on outsourcing as a lever to deal with the pressures in the volatile business environment, Oil & Gas clients tell us they look beyond labor arbitrage and see service providers as an extension of their organization. They want deeper relationships with their providers and forge stronger ties between internal and external staff. They look at their service provider(s) to help the organization become more flexible and scalable, ramping up and down in the cyclical business of Oil & Gas.

Who is Standing Out? The Service Provider Landscape and Blueprint Grid Performance

All of the 13 service providers that participated in this Blueprint share the conviction that innovation is crucial to helping their Oil & Gas clients through this volatile environment. Most of them have a unique set of offerings and capabilities. There are a couple of clusters of expertise. For example, KPIT and HCL, focus on a specific area of the value chain; TCS, Infosys, Wipro, Accenture, IBM and Cognizant, focus on strong domain expertise and consulting-led delivery; and EPAM, Atos, Luxoft, Harman and Tech Mahindra, lead with engineering or Digital Transformation with credible experience from other industries.

As-a-Service Winners are service providers that are in collaborative engagements with clients, and making recognizable investments in future capabilities in talent and technology. These providers are also leading in incorporating analytics and BPaaS to deliver insight driven services: Accenture, EPAM, Infosys, TCS and Wipro. I’ll highlight two Winners here:

Accenture has tremendous breadth and depth in its capabilities and experience serving the oil and gas industry. Its commitment to innovation in technology and service delivery and bringing digital platforms to the industry make it one of the leading service providers in the move to the As-a-Service Economy.

Wipro’s Oil & Gas practice holds a lot of domain expertise, which Wipro combines with innovation in digital, cognitive computing and automation (Holmes) and commercial models. What stands out is Wipro’s ability to bring valuable, new As-a-Service propositions to the market, enabling the introduction of clients’ new reimagined digital business models, a crucial capability for success in Energy Operations.

High Performers show solid performance in either technical execution or services innovation but may not show an innovative services vision or lack execution momentum against what is potentially possible: Atos, Cognizant, HCL, KPIT and Tech Mahindra. Atos impressed us with their vision on Holistic Security and Industry 4.0 experience, two key areas for the future of Oil & Gas.

Harman, IBM and Luxoft are ranked as High Potentials, emerging players bringing highly innovative approaches and overall vision to the market, but lacking in the complete build-out. IBM is struggling to transition from being firmly entrenched in ‘traditional’ services, and has been on the wrong end of consolidations in the industry. However, what caught our attention is IBM’s capability that puts it on the forefront of advanced analytics services, with heavy investment in cognitive capabilities. We have seen a number of interesting applications of Watson with Oil & Gas clients, for instance using predictive data science to leverage more than 30 years of collective knowledge and experience in a cloud based knowledge platform. With the Big Crew change firmly underway, this an important area for Oil & Gas companies.

What is Next? Sustaining the Momentum of Change The downturn in the Oil & Gas industry and sustained low oil price has created a momentum for change in the industry. But will it continue if the oil price goes up again—what happens when it hits $60 per barrel? Many industry executives shared a concern that without the economic necessity of cost cutting, the industry will return to a complacency that will slow the pace of innovation and change.

This Blueprint shows that, in addition to cost reductions, the industry needs to be focused on business outcomes relating to talent, operational efficiency, organizational flexibility and scalability and time to market. The way forward is through more collaborative engagements that incorporate the achievement of these business outcomes. The Energy Operations Blueprint provides a comprehensive overview of the industry and identifies ingredients for long-term business value along the As-a-Service Journey.

I’ll wrap this up by emphasizing again the importance of true partnerships. To survive the oil price slump and come out stronger Oil & Gas companies need partners that proactively bring innovation and are willing to co-invest in technology, collaboration and talent.

HfS Premium Subscribers can click here to download their copy of the new 2016 Energy Operations Blueprint Report.

As someone who has profited very nicely from social media (I helped build an analyst company with blogging and social at the heart of our culture), I am probably not the most appropriate person to speak out against the negative side of social media’s impact. But, as Gerald Ronson once famously espoused to the editor of the Guardian newspaper, “Opinions are like arseholes, everyone has one”, I just can’t help myself, so I’ll give you mine…

2008 was a financial disaster fueled by greedy bankers; 2016 a political disaster fueled by social media wankers. Opinions on politics. My god – back in the day, people pretty much kept quiet on their views until they had some facts to back them up. Today, they just have a bloody opinion and want to get it out there, regardless of whether they can justify it or not. When they get into an argument, they just try and shout louder, rather than listening to reason. David Cameron has been guilty of one of the biggest political snafus of modern times, where he went to the public with a complex decision to be made. Instead, all he succeeded in doing was allowing every opinionated idiot with a twitter account to air his or her views on society at large, until the vote become one about him and the establishment and not whether Britain should remain in the EU. (And you wonder why Hitler loved referenda…)

All social media has achieved is providing a platform for people to spout off unsubstantiated rubbish, as opposed to a collaborative opportunity for them to learn more about what’s truly going on in the world. Then we advance to the lovely US media and the most insufferable election in history, where reality got somehow lost in a maelstrom of hype, tweets and many unsubstantiated facts that really dumb people actually believe. All I can say is that I cannot wait for the election to be over so we can actually get back to some normalcy of running a country again.

The tech and services industry has complete lost itself in the socially-driven hype. So let’s reflect on what happened to our industry over the last couple of years. For a while, social media was fun – we could debate the trials and tribulations of real services and real technology and how to improve ourselves. Suddenly, the facts have got lost somewhere are we’ve arrived at this dark place where it’s more about who’s making the loudest noise than who’s talking the most sense. Every supplier of tech and services talks up “Digital” but never defines it – with few to no clients to reference their capabilities. They talk “automation” with little clue how to do it, with (again) no clients as reference points. Myself and my team have sat through hours and hours of deathly dull briefings where we’ve actually had analysts bemoaning the fact that the providers failed to brief them on the subject at hand. It’s really that bad.

The Bottom-line: It’s time to find our way (somehow) back to reality

Let’s be brutally honest – we’ve all lost the plot. Why are tech and service providers so obsessed with sounding the best as opposed to proving they’re the best? Why do so many analysts and consultants just parrot each other, as opposed to having real opinions and real substantiated viewpoints? Why have so many enterprise buyers buried their heads under the bedcovers, scared to come out until someone dared to explain to them what this new bullxxxt was all about?

It’s time to make things real again… we owe it to ourselves and our clients to talk about how buyers/end-users adopt these emerging solutions – what are they doing, which processes are being impacted, what outcomes are being achieved. We need to focus on real industry dynamics to learn why is digital so relevant to retail; omni-channel to travel; block chain to banking; cognitive to healthcare etc. We need truly to understand and articulate how today’s workforce grasps these emerging concepts and drives them in practice – how can experienced professionals reorient their capabilities, and the younger generation be embraced into the workforce? What are the career progression plans in these areas? While technologies advance, how are staff advancing (or failing to advance) with them?

Unless we really dig deep to stop using our social foghorns to spout the loudest and start focusing on being the more real, we are truly doomed to a future of increased stupidity, naiveté and confusion. It’s time we all broke form these habits and refocused on what is really happening in the world.