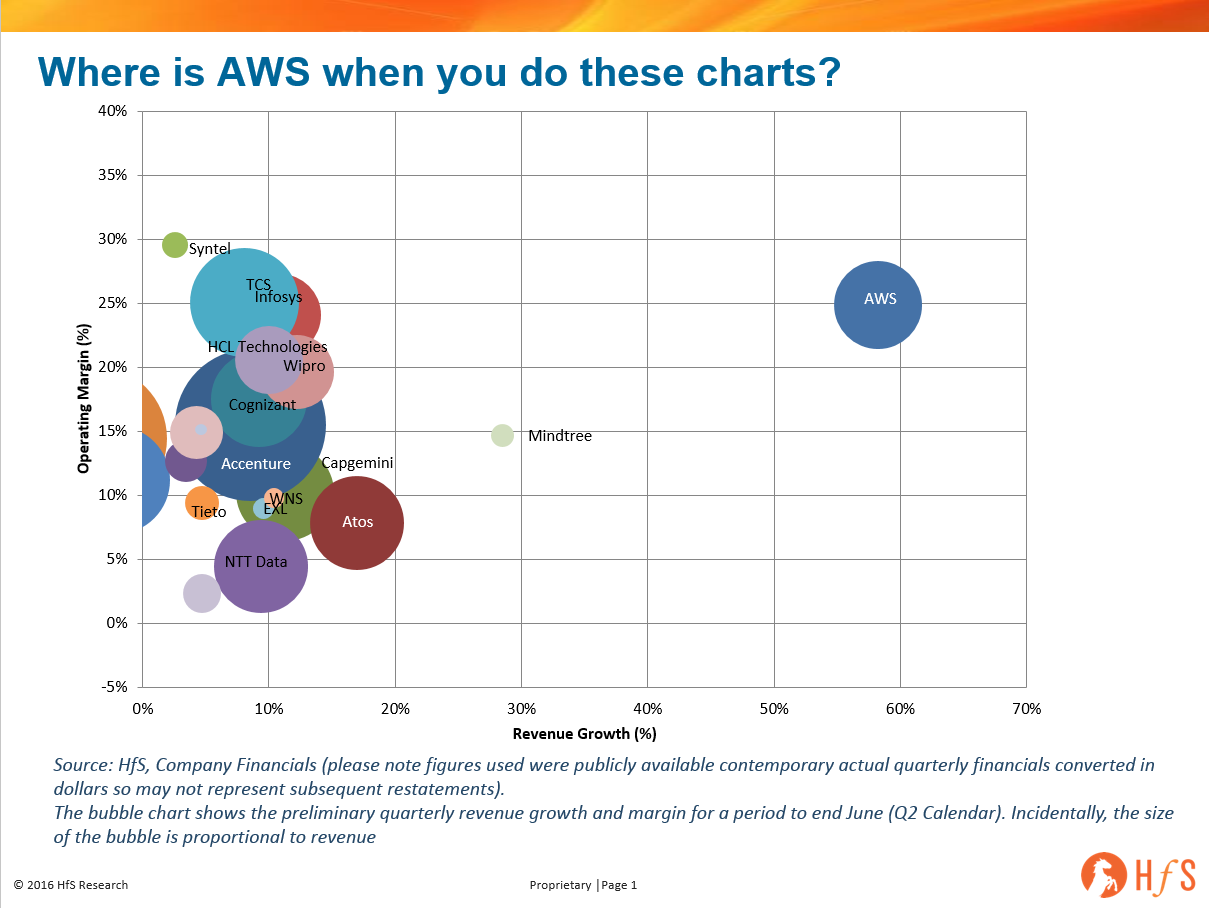

Sometimes it’s all in the fine print. We often put a small comment at the bottom of our charts that gives additional details about the data and a note of anything which specifically impacts the chart. A note we often add to the quarterly bubble charts we do is that we haven’t included one provider or another because if we added them it would skew the chart. One question I get asked fairly frequently is where AWS would feature on the chart.

The chart speaks for itself, demonstrating why we tend to leave AWS off the chart! Frankly, if we include them it’s hard to see anything going on with the other providers. The growth rates of the other firms just blend into one another. Because this chart is limited to financial results there are few sizable IT or business services firms that operate at that level for any sustained period. So it would be great to show Microsoft cloud and Google bridging the gap between the groups. However, neither provider publishes a clean revenue / margin statement for this part of its business. However, Microsoft has started to report some information about its public cloud business, Azure, stating that its revenues grew over 100% in the same period, albeit from a smaller base than AWS.

Another part of this preliminary data which is interesting is the clustering around the 10% growth mark – with the left shift of the offshore providers (see in this blog) and Atos, Accenture, Capgemini, and NTT Data all moving into this space – we are seeing a cluster of providers around the 10% growth mark.

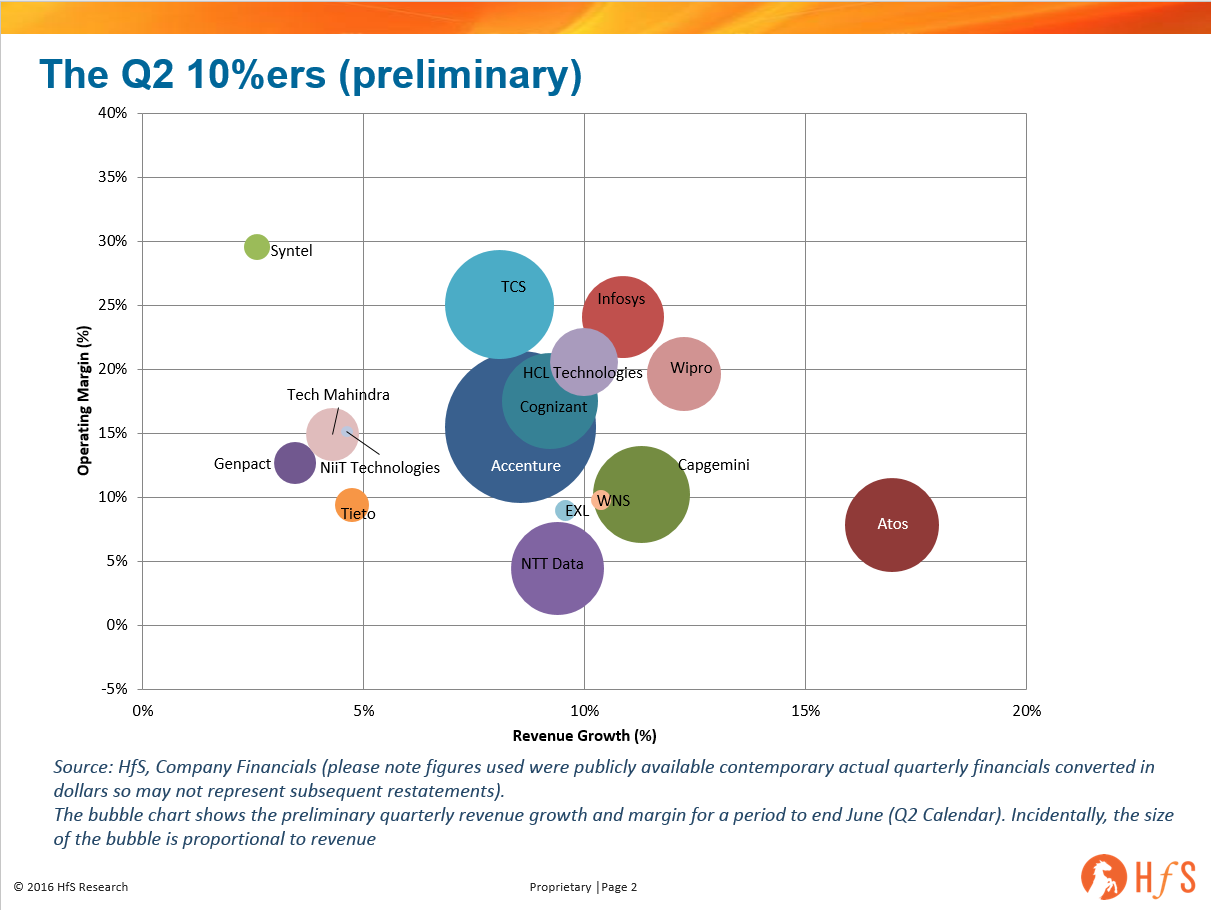

Zooming in on the 10% growth mark shows the phenomenon more clearly. The shift left of the offshore and a shift right of some on-shore players – we are seeing a convergence of some players around the 10% mark this quarter. This adds to the arguments made in the offshore blog last week, that the shift left isn’t merely an indication of a slowdown in the market overall, with an acceleration in Q2 2016. Given the good performance of many of the on-shore traditional providers.

We will be publishing our full review of the results in the first part of September and we will add a blog about the final positionings in more detail.

As the leading authority on Intelligent Automation, HfS gets inundated with requests to size and forecast the market.

Our standard answer continues to be another question: “How can you size a market that is not defined?” Suffice it to say, we have seen some of our peers put numbers out. Yet, how do we actually size the market? Do we aggregate licensing revenues by the tool providers? Do we draw a big mind-boggling number on AI into the sand? Or can we assess the addressable market beyond the bleeding obvious that every IT or business process is conceivably an opportunity for providers?

Until we have clearly segmented and defined markets, the value of market data is probably on the limited side. But don’t get me wrong, my learned colleague Jamie Snowdon can model any of those markets. He not only publicly declared his love for market sizing and forecasting but his Twitter handle is statement of modesty: he is one of the best in the business. And where it makes sense, we draw very visible lines in the sand, as in the case on the impact of automation on talent and jobs.

While we are shying away from confusing the market even more with bold claims on data points, we have very strong views on how the market is evolving. We share those regularly with our clients in strategy sessions and help them optimize their investments and fine-tune the marketing messages. Increasingly, those discussions get extended to investors who are trying to assess the opportunity. Intriguingly, those conversations are not confined to individual companies but comprise discussions on building strategic portfolios. On top of that, a spike in the share price of Blue Prism did fan rumors that were flying around already. Enough reasons for HfS to take stock where the market is—but more importantly to look at a couple of scenarios that could transform the provider landscape.

The market is moving toward exponential growth

HfS is just at the tail end of our research into the inaugural Blueprint Report on Intelligent Automation. Thus, the plethora of discussions with providers and customers provide a litmus test as to where the market development is at. The key exam questions for the project are how service providers are moving the discussions on Intelligent Automation from a narrow focus on RPA toward a more holistic approach. Similarly, how are providers moving beyond a stovepiped view from the traditional business units? Here is just a sneak preview of some of the insights we’ve gleaned.

Despite the blurred perception on the state of Intelligent Automation, the market is headed toward exponential growth. We see significant scale in the deployments both in business processes as well as in IT centric scenarios. These deployments are increasingly underpinned by automation frameworks and the notion of service orchestration. The leading providers are moving beyond the obvious buckets of RPA and Autonomics by building offerings around virtual agents and by getting ever deeper into cognitive scenarios. So stay tuned for the final results and insights!

Four market scenarios

Against this backdrop of a burgeoning and maturing market what could be shifts in the provider landscape that could conceivably disrupt or accelerate the market? Four scenarios jump to mind.

M&A through ISVs: Having just had the opportunity to catch up with the CEO of OpenSpan who has just been acquired by Pega, their example provides the Blueprint for such a development. Similarly, we hear of automation juggernauts circling for opportunities to prepare for catapulting themselves into new era, having heard enough about the Innovator’s Dilemma.

VCs and private equity firms demonstrate an at times remarkable knowledge about the space: We hear about scenarios akin to what General Atlantic did in the heydays of BPO in contemplating a portfolio approach, generating synergies between portfolio assets.

The emergence of an Automation Ecosystem: We already have seen the impact of Watson. Suffice it to say, IBM could be the driving force to extend those capabilities, as my esteemed colleague Phil mused some time ago. But it could equally be one of the tool providers significantly expanding its reach.

A new set of data centric partnerships: To build out cognitive and AI capabilities and to optimize the engines, access to data is critical. As many customers remain coy giving provider access, we might see a new set of partnerships accelerating these capabilities. While it might sound trite, datareally is the new currency. Obviously, these scenarios might overlap. Equally, M&A is often not rational. Thus, I am sure the market will continue to spring many surprises on us.

The Bottom Line: The discussion on Intelligent Automation has to move to center stage

In light of the strong growth and maturation of both service provider and tool provider, the discussion on Intelligent Automation has to move center stage. Despite the blurred perception the fundamental question is how do we align service delivery to accelerate the journey toward the As-a-Service Economy. To really fast track this transformation, we need to address issues such as governance, testing and the transformation of knowledge work. And as always I would love to hear your views on all this.

We’re excited to fly over some of the HfS star analysts to meet with the delegates at this year’s NASSCOM BPM Strategy Summit, where HfS is the exclusive content partner with the theme “The Next Big Goal – From Effective to Strategic, can BPM get this one Right?”. And the more discerning of you will notice that the theme is centered on HfS’ own Eight Ideals of the As-a-Service Economy.

So what are you waiting for? Book your flight and place now!

Venue: Hotel Leela Bangalore

Date: 22-23 September 2016

And if you’d like to meet with some of the HfS team, drop us a quick note and we’ll see what we can do.

When I was in college, I heard an incident involving Bill Gates and his comments about innovation in the automotive industry in the late 90s. Later, I found that Bill Gates comments were extrapolated and converted into a then very popular joke among automotive engineers. The irony is that joke is coming true now for car makers, but it is a good opportunity for engineering service providers.

It goes like this–

Bill Gates: If the automotive industry had kept up with technology like the computer industry has, we would all be driving 27 dollar cars.

Automotive Industry: Yes, but would you want your car to crash twice a day?

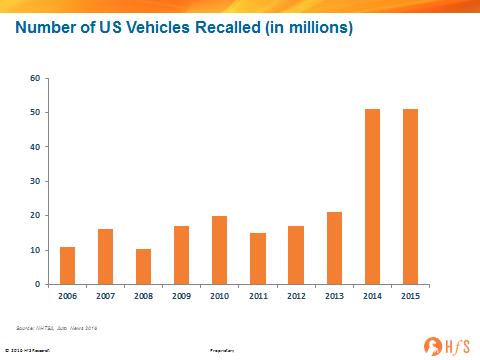

And guess what? Two decades later, cars have become more like software and vehicle recalls have skyrocketed.

High-end cars now have about 100 million lines of code, a steep increase from about 1 million lines of code in 2000. The code volume per car will grow further and expected to reach 300 million lines of code in the next few years. In fact, in 2016, the new Ford F150 pickup has 150 million lines of code. In comparison, Facebook has only 60 million lines of code (see infographics).

Parallel to the growth of lines of code in cars is the growth in vehicle recalls in the US. The recalls, which were in the range of 10-15 million per year a decade back, have skyrocketed to over 50 million per year in the last two years.

The above recall numbers are just for US but I am sure situation will be no different in other regions.

These recall numbers highlight there is something seriously wrong with the testing process. And one of the major culprits in recalls is software.

Beyond recall numbers also we have heard about disturbing stories in automotive sector such as the Volkswagen emission scandal, where the culprit was software. Even Tesla’s recent autopilot crash was related to software. As it turns out, the Tesla’s braking systems radar and camera may have failed to detect the tractor-trailer.

Where does this software code go in the car? It is in all the cool features, such as air bag system, anti-lock brakes, automatic transmission, climate control, communication system, dashboard control, engine control, entertainment system, power steering, etc. Also, the possibility of so many variants and consumer choices creates volume and complexity in car software.

The core expertise of automotive OEMs and tier 1s is mechanical engineering. They need help and external expertise in embedded engineering in design, development, testing, and manufacturing. The embedded software has been a growth driver, especially for Indian engineering service providers.

For car manufacturers, the pressure to push the products early creates pressure on testing. Now, amidst vehicle recalls, emission scandals, and auto pilot crash the importance of vehicle testing will increase further.

As software is eating up the car, the automotive industry needs all the help it can get in testing, verification, and validation. The testing requirements will only become stronger with self-driving cars. And we are still not talking about mass customization, where OEMs can design and manufacture car in the lot size of one economically. This will be a testing nightmare for OEMs but a goldmine for engineering service providers. (And don’t get me started on the fear of hacking and make you paranoid, but testing requirements will only increase!)

The major engineering service providers in the automotive vertical offer testing, verification and validation services. My observation has been that the current approach to testing is more at the compliance level. Service providers I talk to tell me that they help OEMs and tier 1s in getting certain certificates in few countries (the technical term is homologation). The providers want to be able to crow about their testing being recognized by OEMs and certification authorities.

This is all good and that’s why majority of testing outsourcing is being done. But today, we need to think beyond compliance level and instead think about how to prevent vehicle recalls, emission scandals, autopilot crashes and even support mass customization.

Service providers need to think what kind of testing services they can provide to the Teslas of the world. The compliance approach will be table stakes. How can they help Tesla in preventing another autopilot crash? (Read Lessons from Tesla’s Master Plan)

Currently, the percentage of the engineering services providers’ revenue from automotive testing is in single digits, which we think has the potential to go into double digits in the next few years if service providers move from compliance to solutions. This is no joke!

Most of the coverage of the Walmart/Jet.com deal has focused on whether this helps the firm compete more effectively with Amazon. Speaking as an Amazon addict, ahem, loyalist, my initial thought was there is no way this deal even comes close to having the intended impact. But as I dwelled on it further, I realized the more interesting facet of this news is how ecommerce competition is driving a fundamental change in the retail business model to support today’s digitally savvy customer; namely to architect a digital strategy that carves out a new value proposition for traditional retailers.

Walmart brings “digital brain” Marc Lore into the fold as its architect

This acquisition is as much about platform, relationships and customers as it is about the experience and savvy of Marc Lore, who also launched Diapers.com, which was acquired by Amazon in 2010. This is a tangible sign of Walmart looking to “get digital” in the core of the company—hiring someone who has turned boring legacy markets upside down by making the unsexy task of shopping for products like diapers and laundry detergent easy and appealing to yuppies and millennial shoppers.

The biggest part of this strategy is about better serving and understanding the customer. Retail, arguably more than any industry, has a real competitive need to move away from general segmentation to individual personalization. Jet.com leverages technology in a way that enables lower cost and greater personalization with its dynamic pricing engine. The retailer has also grown substantially in terms of membership and product availability and has been hyped as a potential Amazon disruptor since its inception.

Retail self-disruption is critical – where does the store fit in?

Emerging digital business models are disrupting retail in a way that legacy companies like Walmart simply cannot respond to fast enough and remain viable. Headlines of store closings are ubiquitous, while others scramble to leverage stores more effectively and invest in digital (such as Kohl’s use of ApplePay). For legacy brick and mortar retailers, the key is finding the right balance of in-store and online shopping capabilities, and ensuring a seamless experience between the two. In terms of physical real estate, writing off legacy isn’t necessarily the best approach- it’s about morphing and shaping that legacy into something that meets customer demand and supports the digital customer. Retailers like Macy’s, which has just announced significant store closings, may be missing out on an opportunity to use their real estate legacy to their advantage by making those stores points of shipping, pick up, or experience. And let’s not forget that today online sales are still a very small percentage of retail sales overall. One advantage of the Jet.com acquisition (over say Diapers.com being absorbed by an online native) is that it can leverage Walmart’s massive brick and mortar presence as a point of shipment for products.

The Bottom-line: You don’t have to completely write-off legacy – it’s about morphing legacy businesses to meet customer demand. Digital architects can save traditional retail if they adopt this approach

Retailers need to have leadership that addresses the overarching digital picture—a digital architect. They also need to master personalization in the same way that ecommerce natives have. This is no easy feat. In the case of Walmart/Jet.com, it is just one more example of on how difficult it is to redefine and recreate an existing legacy company into a digitized company, and addressing the need to understand the digital customer more effectively. Walmart has recognized that it cannot rest on its laurels—a company that was once seen as innovative because of its supply chain practices, but lost its edge over time, is making a bold move to revitalize the innovation. The challenge lies in integrating these two very different creatures. The acquisition is bold, and the market is taking notice—now begins the tough job of making it work for the digital shopper.

For the first time since Al Gore and Donald Trump founded the Internet, I am braving a few days in the analog world on a camp-site up in Canada somewhere. In fact, I don’t think this place has even undergone analog disruption yet…

At HfS, we’re growing fast in a very competitive and volatile market… and with growth comes change – but change is always good if you ask me! The most fun in jobs is when you have changes – you learn new things, get new ideas and you meet new people to help accommodate the change.

HfS is always on the lookout for serious talent that can help our clients become even more successful. So happy days when I heard that some serious quality was on the lookout for some new chapter in his life. Sunjeet Ahluwalia has joined per August, and today I wanted to give you a little more background about him.

Bram Weerts, Chief Commercial Officer, HfS: Sunjeet, can you share a little about your background and why you have chosen sales as your career path?

Sunjeet Ahluwalia, Senior Director, Global Business Development, HfS: Having completed my Course in Metallurgy and Material Science, I took up my first job in 2001. Traveled all over India and experienced the diversity this great Nation has to offer. Sales were fascinating, and I met various interesting people all during my life.

With a sales career, you have a high level of accomplishment as you are directly the person responsible for making things happen. It is quite an adrenalin rush when you close a sale. You also get the satisfying feeling of providing your customers with products that they truly want and need, and you had a large part in facilitating and meeting their needs. Some jobs can be really redundant, and you might feel that you have not accomplished anything, but with a sales career, every sale is a direct result of your efforts.

Bram: Why did you choose to join HfS?

Sunjeet: While in Gartner, came across clients who spoke highly of this new upcoming company called HfS. I did spend some time to understand HfS and was very impressed by the depth and knowledge they bring to the industry. Two things that stood out were Social Media Impact and premium research that set HfS apart from others in their peer group. I wanted to be a part of this growth and contribute significantly to their success in APAC.

Bram: What are the areas focus on driving in your Sales role?

Sunjeet: Relationship and trust are two key pillars of Analyst and advisory industry. Aligning yourself to your client’s goal and priorities will help you become more credible. Being relevant to what your client needs are and trying to always provide them with superlative value surpassing their investments will be my key focus.

Bram: What trends and developments are capturing your attention today?

Sunjeet: Automation, AI, and Data-driven Analytics Capability are in my opinion redefining the way industries do and conduct businesses. Innovation isn’t mere a fancy term now; rather it is the necessity if you intend to keep the Brand high and retain your clients.

Bram: And what would you like to see different in the research / services industries?

Sunjeet: I wish research / services industries have a wider reach within the audience. It should be able to impact the way people work within their teams and hence enable them to achieve their personal and business objectives. Key decisions are formed using insights and hence its key to be very relevant and objective while we work with clients.

Bram: And, what do you do with your spare time?

Sunjeet:I enjoy reading poetries and listening to music. If I have more time, I probably will go for a swim or cycling.

Bram: If you could change one thing in Sales what would that be?

Sunjeet: People buy from people, and hence we should aim at superior trust based value added relationships. Discounting reduces credibility and hence that should not be a driver for a sales guy’s success.

Bram: Thank you for your time Sunjeet, it’s a real delight to have you onboard and work with you in these fascinating times!

Q2 2016 has been an exciting quarter of results so far, with a few surprises particularly amongst the large offshore providers. We commented on the pressure on Infosys caused by its results last month.

We see a real change in fortune amongst the big players, certainly over the last two quarters. With the players with strongest growth rates over the last three years, TCS and Cognizant dropping year on year growth to single digit.

If you look longer term, the shift left of the big offshore players is accelerating—with these latest results accelerating this trend.

TCS, HCL, and Cognizant will see revenue growth slow dramatically over the last three years. The bubble chart shows the Trailing Twelve Month revenue growth and margin for a period to end June for the last four years. So the TCS 2016 bubble gives aggregate revenue growth and operating margin for the last four quarter to June 2016. Incidentally, the size of the bubble is proportional to revenue.

All of the providers have managed to keep operating margins within a fairly narrow range—certainly better than most of the traditional onshore IT and BPO players.

The reasons for the shift are complicated and intertwined. It is tempting to see the most consistent providers, in this case Cognizant and TC,S as bellwethers of the market—so the slowing down of these firms growth is a strong indication of a slowdown in the market overall. Although this, particularly when you look at Q2 results so far, isn’t borne out by other provider’s results, particularly Accenture, which had a bit of a barnstormer certainly compared to its recent results.

Another possibility is that the scale of these firms is getting to point that maintaining double-digit growth rates is such a large amount of actual dollars that these providers sales engines cannot fuel level of client acquisition. There is probably some truth in this and getting the size and shape of your sales team right is a major challenge for service providers at the moment—particularly given the current uncertainty in the market. However, given that both Cognizant and TCS achieved higher levels of dollar growth throughout 2010 and 2011—while they were half the size—makes this theory less appealing, and certainly isn’t the whole truth. In Q4 2010 (calendar to end December 2010) Cognizant added $408 million in revenue, and TCS added an impressive $607 million year on year. This is compared with $285 million and $326 million, respectively, in the latest quarter Q2 2016.

What has changed most is the market itself. Partly with the size of the engagements, we have seen the outsourcing bills in IT infrastructure tumble by 40-50% and in some cases 60%, which means renewals come in at reduced rates and expectations around cost savings continue to ramp up, especially since automation starts to add another lever to the cost saving toolkit. This is particularly crucial as Tier 2 offshore firms focus efforts on combining savings from even cheaper locations and automation to lick the remaining cream off many deals.

Although outsourcing was the example used, this is also impacting professional services, mainly implementation services. The increasing emphasis on technology driven by digital and customer centric solutions has produced many opportunities, and while the number of deals may have increased, the contracts remain relatively small. Reengineering a bank’s core applications is, in scale terms, 20 or 30 times the design and implementation of a mobile app. Additionally, digital deals are often more involved and have more complex requirements that draw on a broader set of skills. This is undoubtedly slowing the sales cycle and means the upfront effort to engage with these small deals is higher. The promise is that demonstrating competence and the ability to deliver value within these often high-profile engagements will bring further work downstream. The market is still awash with proof of concept digital deals and the converting these into more meaty engagements is taking its time. So, rather than a lack of absolute capacity in the offshore provider’s sales teams, it is the makeup of these teams that is taking the time to adapt to these new types of deal.

The Bottom Line: The market sands have shifted, and the impact is now being felt by offshore firms

OK—so we may start sounding like a bit of a broken record. However, long-term success in the services market is dependent on inertia or the lack of it. Providers that are reacting quickly to the changing market conditions are growing, and they’re not necessarily the low-cost offshore-centric providers. We are sticking to this message: the x-factor for an enterprise service provider is agility—both regarding the provider’s ability to adapt to the market conditions and capacity to deliver adaptive intelligent solutions to clients.

These firms are having to adapt to these changing conditions on the fly. Unfortunately, there is no timeout to use while you have to adjust your processes, bring in new skills or reenergize your sales teams.

We are keeping an eye on all the players in the market and are looking for signs of this agility being reflected in financial results—halting what seems like the inevitable shift left.

But all is not lost! I see some very powerful paths Procurement can take to become a more appreciated and valuable business function in enterprises.

Procurement is suffering from a reputation problem

Many executives express their frustration with procurement frequently claim, “they just don’t understand what I need, and obstruct me from achieving my goals”. Procurement is often seen as that last hurdle before reaching the finish line like a police officer trying to find holes in your story, looking to give you a slap on the wrist if they can. Everyone tries to circumvent Procurement when they need to buy products or services.

The underlying issue often lies in the emphasis on the transactional side of procurement in enterprises. People are subjected to procurement processes and form-filling that are very time-consuming, valueless and inefficient, feeling like they’re being sent from one desk to the other.

Of course, there is a role for Procurement. Of course an enterprise needs to have expertise and capability in contracting, buying and using services from third parties. And of course rogue spending is an issue for enterprises. But it’s time to take the next step. If being restrictive didn’t bring you the seat at the table you envisioned, if ‘the business’ still doesn’t ‘get’ you and doesn’t take you serious, its time to change the tune. But how?

Guides of the As-a-Service Journey

I want to argue Procurement is in a unique position to reinvent itself and that we should love Procurement.

HfS sees a dramatic shift in services towards the As-a-Service Economy. Key characteristics of the As-a-Service Economy are:

More and deeper collaboration between suppliers and buyers

A focus on business outcomes

Usage of digital platforms, analytics and automation to facilitate the convergence of people, technology and process

Services that are multi-client, leverage new opportunities for efficiency and quality and focus on the customers’ customers.

Procurement can be the enabler of the As-a-Service Journey. Don’t look further…. Procurement should be the broker of capability. Haven’t you noticed how “IT Services” and “BPO” and “software” have become procurement categories in so many buyers today? As services and technology become increasingly commoditized, standardized and commonplace, the greater the opportunity for Procurement to take the lead in adding value beyond merely negotiating price points.

The future of the supplier-buyer relationship is collaborative engagement and that starts in the contracting phase. Procurement should have a clear vision on the way the enterprise wants to form relationships with suppliers, what the nature of the collaboration should look like and how contracts facilitate collaborative engagements.

Procurement Brokers of Capability

The key to becoming a broker of capability is to be the spider in the web. In my years as a consultant, I often didn’t have a formal team. I went out into the organisation, identified the people and capabilities I needed to tackle the problem, formed informal teams of the right people and made it happen with them. I was a fixer more than anything, understanding the problem, limitations, possibilities and I knew the right people and brought them together. Not always easy, but a lot of fun. This is how I envision the future of the procurement professional. Identify business needs (you do this by actually talking to these people, understanding what they have to achieve), dive into your network and get the capabilities together that are needed. If you take a partnership approach, look at relationships long-term rather than short-term transactions, people are willing to do a lot for you.

So what is needed to truly become Brokers of Capability?

Be a business function, not a finance function – Procurement should be immersed in business units to understand the business, understand the needs, understand the market. Business executives have to allow Procurement into their world, Bram was right to point to business executives as a source of Procurement’s woes.

Category Expertise – One of the hardest areas to fix for procurement is strategic sourcing and category expertise, especially in the tail of indirect spend. This requires deep expertise of the category and the market, which is a challenge for enterprises to build in-house.

Information – At the heart of every buying decision lies information. Procurement has more data at its disposal than ever before. Information and insights derived from all this data is critical for the evolution of the profession. Digital platforms have emerged and are quickly growing in adoption and capability. Advanced analytics are drastically improving the insights and decision-making processes for Procurement.

Relationships – Building and maintaining relationships, internally and externally, is critical for modern Procurement. Price isn’t everything and it’s definitely not a predictor for the willingness to go beyond the contract and take a relationship approach to the engagement. Time and time again in reference calls for HfS Research Blueprints and in our discussions with services buyers at HfS events, the best service providers are perceived to be the ones investing in the long-term relationship, going above and beyond expectations and contractual obligations to deliver real business value to the client. Incorporate these tenets in your sourcing practices and your enterprise will benefit.

End-to-end focus – Key to realizing business outcomes and benefits of good procurement are closed loop processes and follow through after the ink on the contract is dry. Turning theoretic savings into real ones is still pretty hard to achieve.

Tech savvy – Technology platforms with embedded process automation and advanced analytics are emerging at the core of Procurement. Procurement professionals need to be more tech savvy than ever before to make sure they use and leverage the available technology platforms.

Ok, we agree it’s Procurement’s job to know what is out there, what the quality of products and services are, what going rates are and which terms are acceptable. They are the ‘go to guys’ when you as a business executive need something to achieve your goals.

I’m not naive. I know there are still a lot of people in Procurement hiding behind procedures and forms, terrified of becoming obsolete without them, clueless what your business goals are.

The Bottom-line: It takes two to tango

Friends in Procurement, if you don’t have a vision of Procurement being a business facilitator, now is a good time to get one. And “business”, this asks for different behaviour from you as well.

Question: Why are we becoming so obsessed with Automation and As-a-Service relationships?

Answer: Because outsourcing has worked so effectively, we can now look to new levers to pull to find that next threshold of value

Question: Will the next person who says “Outsourcing is just so Passé” get a punch in the face?

Answer: Yes

Barely three years’ ago, we were still lamenting that nagging lack of innovation in outsourcing relationships and the inability of service providers to deliver those transformational delights to their clients after they had come through with their promised cost savings. But let’s face it, the FTE-based labor arbitrage model has really worked – and a lot better than we thought it would, during those heady days of offshore screw-ups. I can barely remember the last time I sat on the receiving end of a group of clients throwing their service providers under the bus because they couldn’t get the procure-to-pay transition right, or got caught sneaking through change-orders to fix their dodgy coding.

Service relationships are more stable than ever, but focus is shifting to As-a-Service delivery and Intelligent Automation

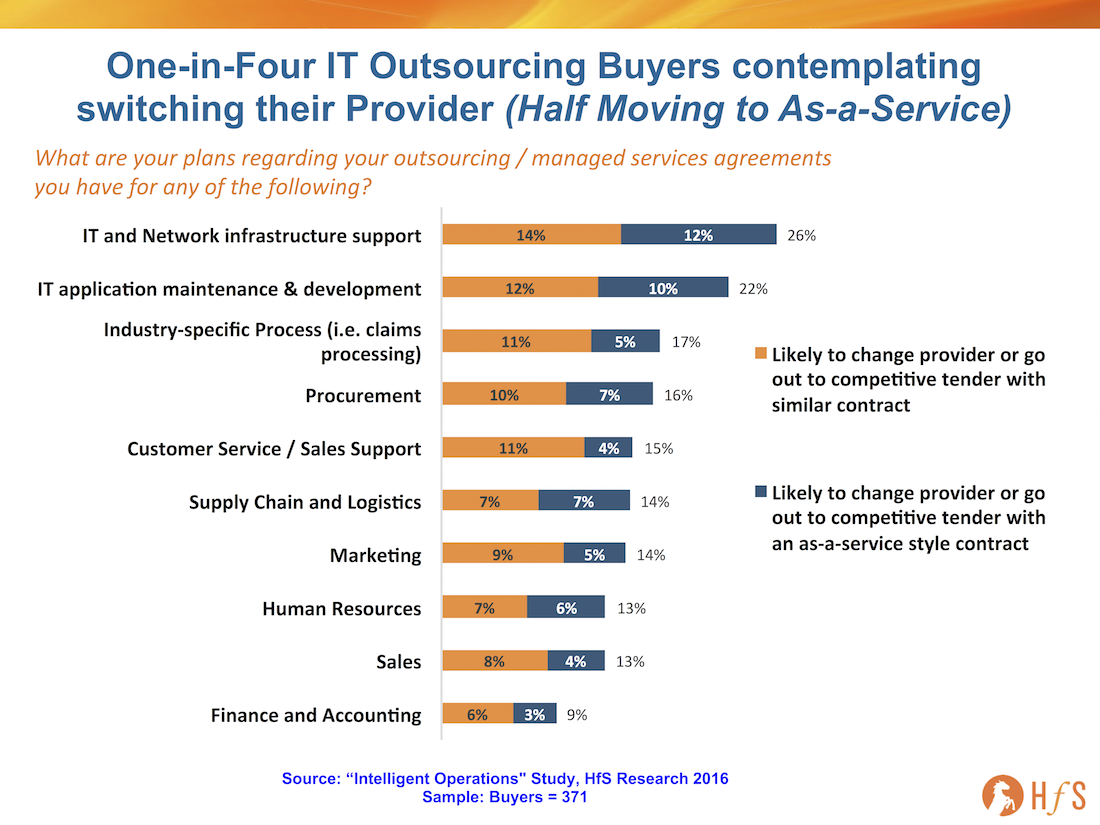

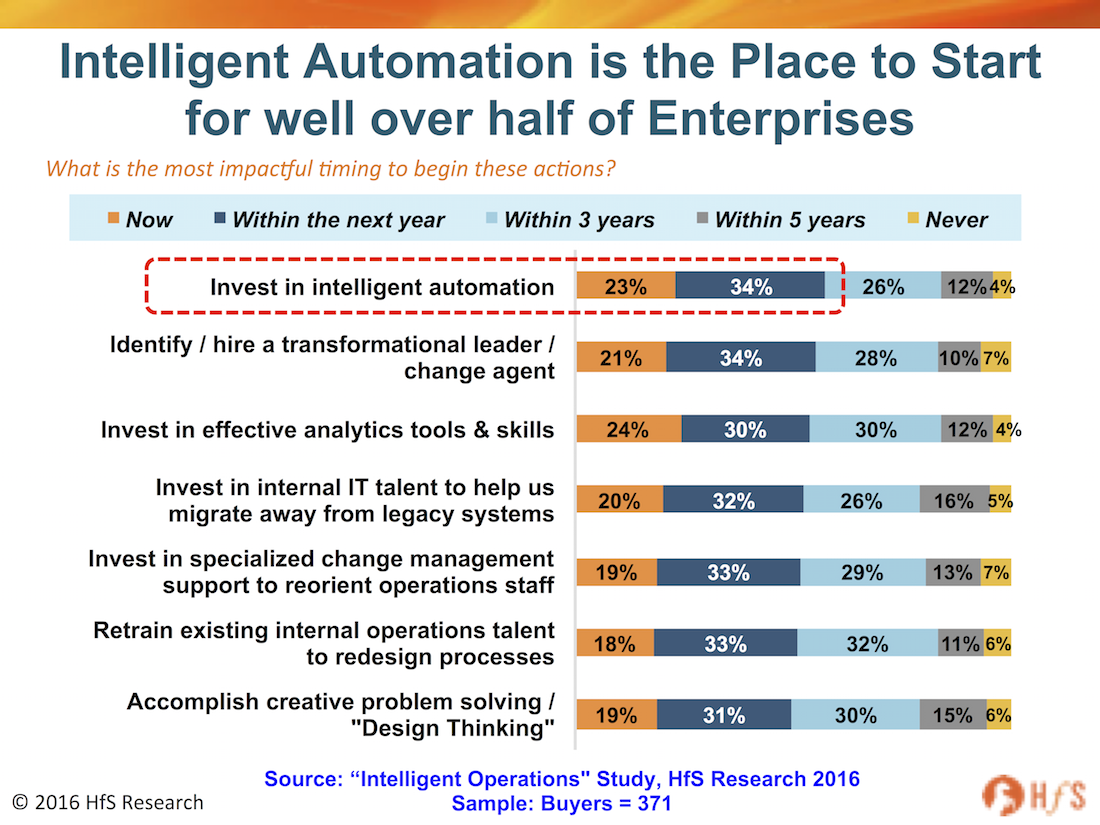

You only need to look at the intentions of 371 major enterprise buyers towards their outsourcing contract renewals from our new Intelligent Operations Study to get the picture that this isn’t an industry in delivery turmoil, about to self-combust because deal flow isn’t growing at quite the clip it was a couple of years’ ago. In fact, only one-in-four IT services clients today are even considering ditching their current partner, and a even lesser proportion with their BPO provider. However, many do want to make the switch to As-a-Service contracts:

The focus on automation is the logical next phase of value once stability of global service delivery has been reached.

The availability of smart automation tools and platforms from the likes of Automation Anywhere, BluePrism, IPSoft, Nice, UIPath, WorkFusion and Redwood have really been conversation catalysts to get the automation conversation to the table. In fact, most of the buyers we’ve been interviewing in our current Intelligent Automation blueprint are still in the early strategy and roll-out phases of their automation experiments. Moreover, as our research clearly shows, well over half of today’s major enterprises have automation plans firmly in play over the next year:

Bottom-line: From offshoring to efficiency to automation, it’s all a natural evolution

Let’s face facts, when your company hires an outsourcer to provide you with 500 staff to deliver back-office transactional operations, do you really expect this 500 number to stay constant for ten years? Of course not… as operations stabilize, as better technology helps streamline processes, your expectation is always to get the same work done for less hired effort. It’s like when you upgrade your accounting software – do you really expect to have to hire more people to operate it for you? Of course you don’t… you expect better quality for less effort.

So let’s stop berating “outsourcing” as some archaic practice that went out of fashion with the Blackberry. It’s a practice of globalizing operations that we’ve got really good at – and the fact that we’re now obsessing with getting into the weeds of automating processes, is testament to our progress that we’re running our businesses much more efficiently – and digitally – these days.