How can enterprises make automation core to their operations strategy and not merely a peripheral activity? Let’s be blunt here, many service providers have been automating routine tasks with their clients for years, yet as my HfS colleague, Tom Reuner, has noted, the innovations referenced by the notion of RPA and Intelligent Automation are “often at sub-process levels…not at the heart of a delivery backbone.” We are seeing the momentum pick up here, though, particularly when automation is a shared strategy between service providers and their clients. We heard one such case highlighted by Peter Quinn, Managing Director of Automation at SEI Investments Co., (NASDAQ: SEIC) a wealth management solutions company, at the recent NIIT Technologies Industry Analyst/Advisor Day.

Service buyers want to partner for automation, but where – and how – is it actually working?

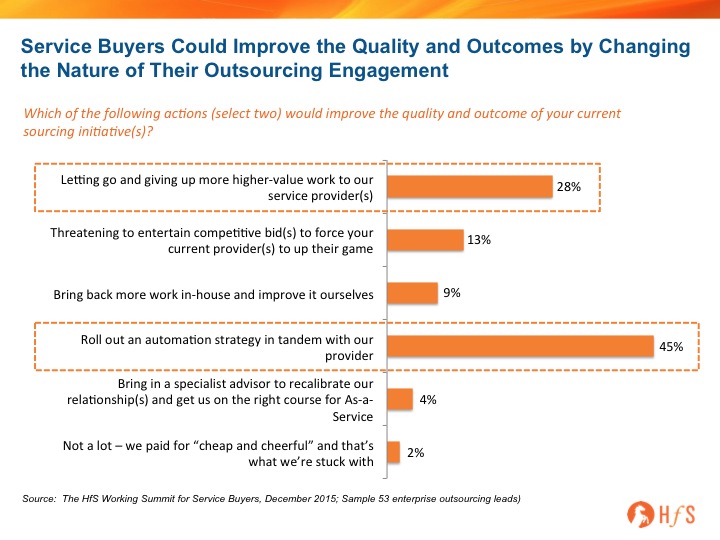

When we asked 53 service buyer executives what would improve the quality and outcome of their current outsourcing engagement, 45% of them selected “roll out an automation strategy in tandem with our provider.” (see Exhibit)

Exhibit: Service Buyers Could Improve Quality and Outcomes by Changing the Nature of Their Engagement

There are risks to be taken by buyers and providers – but is the greatest risk avoiding core automation?

For service buyers, challenges include getting the IT department on board and addressing concerns about data security while selecting and licensing the appropriate software. Service providers also face the investment challenge of taking hits to their existing FTE-based revenues and margins in order to safeguard existing clients and win new ones. So, how can buyers and providers truly get to a shared automation strategy that’s genuinely core to the engagement? It’s simple: both need to be willing to take risks to drive new business outcomes. But you can also look at the risk of not taking the risk – failure to achieve effectiveness through automation could ultimately lead to the buyer enterprise leaders falling on their swords, while those service providers clinging to the legacy FTE model will eventually be displaced by those with a genuine automation capability and offering.

The SEI and NIIT Technologies Experience with Governing Core Automation

Here’s one such story: It starts with SEI getting excited about the potential impact of automation on security, quality, speed to results, and employee engagement.

Peter Quinn, Managing Director of Automation at SEI, set out the expected outcomes for an extensive use of automation:

Improve SEI employee quality of work experience by eliminating the repetitive, mundane tasks, thereby transforming the culture and eliminating the revolving door in certain departments

Reduce risk of off-shore data privacy breach – corporate investment to ensure all offshore access to data is secure was still being met by the question of “what if”… no matter what the effort to address it

Eliminate risk of geopolitical event impact on BPO

Reduce human error and associated costs (financial, client impact, SEI industry image)

Achieve rapid deployment

Create instant and profound scalability: license robots versus on-board and train people

Achieve cost reduction through staff savings

“Yes, of course we are looking for lower cost,” as Peter Quinn, Managing Director of Automation, SEI says, “but if you can get rid of human error… that’s key, because errors have financial, client experience and brand impact.” A data security breach or other human error on an investment portfolio of a client can have expensive short- and long-term consequences on customer experience and brand loyalty, for example, for a company that builds its business on its clients’ trust. And it seems like no matter how much is invested in time, money, and resources on security, it’s never quite enough for regulators. Automation helps drive more predictable and reliable results.

To get full benefit from the use of robotic process automation, end-to-end processes need to be automated to the fullest extent possible. SEI would be evaluating all the work they do from end-to-end, including considering what is done in-house, what is outsourced, and where the hand-offs are. That means work that had been outsourced and managed by its partner, NIIT Technologies, would be in scope. NIIT Tech, for its part, typically evaluates the work it does, looking for opportunities to increase efficiencies, including the use of automation.

This is the point at which the two parties come together in a more strategic approach to automation

“We will automate as much as possible, and that includes potentially repatriating work that had has been outsourced for years,” Peter Quinn of SEI told NIIT Tech. Pause. The response from NIIT Tech: “How can we help?” This response may or may not have been immediate – perhaps there was a little surprise involved—but the point is that NIIT Tech took a step forward to stay involved. Yes, NIIT Tech would lose current work, but from their perspective, this move takes their efforts to the next level of efficiency and relevance to SEI’s business; it also gives their own organization the same benefits as those listed above by Peter Quinn regarding employee quality of work and business results. Participating in discussions about what and how SEI wants to run their business and the supporting operations also gives NIIT Tech the context and opportunity to share new ideas for their role going forward.

A critical part of the automation strategy – governance – includes representation from internal stakeholders and external partners

While as an industry we agree automation is increasingly integral to business operations and outsourcing roles and results, how to bring automation into outsourcing partnerships and engagements – from strategy and governance to contracting – is still a work in progress.

Quinn, reporting to SEI’s CIO, chairs the Automation Governance Committee, which includes NIIT Tech so that they can be an active participant in all discussions. It also has representation from all market, geographic, and operating units, and includes business managers, legal counsel, and IT. The committee serves as a forum to:

Exchange ideas and needs, find commonalities, and build the business cases

Assess new requests

Determine best tool / best fit

Prioritize 90-day inventory for each tool (e.g., company impact, ROI)

Review tool capacity saturation

Evaluate new products as the market changes

The intent of the Automation Governance Committee is to weave intelligent automation into the fabric of the company. Too often, we hear stories of automation being used piecemeal in different areas of companies, which can lead to the use of it being sub-optimized at a point in a process versus as part of an end-to-end strategy, and complicated and expensive with separate licenses and approaches. The automation strategy should drive the ecosystem of partners within and outside a company to ensure that all the participants supporting the operations of a business are aligned and integrated.

The Bottom Line: The challenge for service providers is pivoting to meet clients’ future goals

Can NIIT Tech develop the capabilities to achieve the clients’ goals, still deliver value as a long-term partner, and realize margin for their business by having “sacrificed” the FTE-based work? “I believe the days of FTE-based work are coming to an end,” says Dan Spaventa, NIIT Tech’s client partner for SEI. Looking ahead, the service provider is developing automation-based solutions in targeted market areas like “SmartTransfers” in financial services, to bring automation into the core as part of the regular cadence of work in the service industry. These are moves that NIIT Tech – and other service providers – have to make to be a viable service provider partner in the future of outsourcing in the As-a-Service Economy.

The stills from the James Bond movie, “From Russia With Love” flashed in my mind when Infosys SVP and Global Head of Engineering Services, Sudip Singh described the latest multi-million and a multi-year engineering services outsourcing deal with Ansaldo Energia. As part of the deal, Infosys will open engineering service delivery centers in Moscow (Russia) and Karlovac (Croatia) leveraging a rich pool of engineering talent in both these countries.

The Context of the Deal

GE acquired Alstom’s Energy business for €12.4 billion in 2015. The EU Commission and the US Department of Justice approved this acquisition conditional upon the divestiture of parts of Alstom’s R&D gas turbine projects. In 2016, Ansaldo Energia acquired these R&D gas turbine projects from Alstom.

Infosys has been a strategic partner of Alstom’s Energy business and has delivering engineering services to Alstom for the last few years. This merger and de-merger of GE-Alstom Energy business provided an opportunity to Infosys to upscale its engineering services engagements with both GE-Alstom and Ansaldo Energia.

Why Is this Deal Important for Infosys?

Strengthens engineering services footprint in Europe and Russia: Infosys is one of our As-a-Service Winner’s Circle service providers in our Engineering Services Outsourcing Blueprint. We advised Infosys to improve its business and footprint in Europe. We are glad that Infosys has acted on it.

Augments expertise in turbomachinery: Infosys has strong engineering services capabilities in turbomachinery with Alstom as its anchor customer. This acquisition augments Infosys’ turbomachinery capabilities with specific skills in heavy duty gas turbines, industrial gas turbines, steam turbines, etc. These are hard-to-find skill sets in the highly specialized industry and Infosys can leverage them to provide engineering services to other customers as well.

Additional skill sets in other engineering verticals: Turbomachinery Engineering is one of the most complex engineering skill sets. This deal allows Infosys to access high-end turbomachinery engineering skill sets, that augment Infosys’ engineering design and analysis capabilities in the automotive and the aerospace verticals (aero structures and aero engines).

Position Infosys to leverage Russia and Croatia: Infosys had no engineering delivery presence in Russia and Croatia. In fact, the broader Infosys operation had no major delivery presence in both these countries. Infosys only had a few support and business development professionals in Russia. This deal will change that and provide an opportunity for Infosys to leverage a delivery presence in Russia as well as Croatia to win more deals for both engineering services and larger IT services in the region.

Why Is this Deal Important for Ansaldo Energia and GE-Alstom?

Provides continuity and future proof engineering support: This deal ensures that Ansaldo Energia will have the engineering support of Infosys in providing continuity to the customers of GE-Alstom. Otherwise, it would have been a challenge for Ansaldo Energia to bring the dedicated focus to turbomachinery design and analysis, invest in future skill development, and manage spikes and trough in demand. There was always a danger of rationalization and right sizing but now under Infosys umbrella, engineering team can look for a long-term career option. Infosys will leverage this engineering team to provide engineering support to other customers too and overall grow Russia and Croatia operations.

Why Is this Deal Important for the Engineering Services Industry?

Leveraging manufacturing and technology mergers and de-mergers: The manufacturing and technology industries are going through global turmoil. A lot of the big mergers happening in the industry are subject to regulatory approval, such as Nokia-Alcatel, GE-Alstom, Dupont-Dow, Holcim-Lafarge, Electrolux-GE, Dell-EMC, Inbev- SABMiller, Halliburton-Baker Hughes, Shell-BG, Avago-Broadcom, etc. One of the rationales of the big mergers is synergies or consolidation in R&D and procurement spending where engineering service providers could be at the disadvantage. The corollaries of these big mergers are de-mergers or selloffs either for regulatory approval or for generating cash. These mergers and de-mergers can also provide an opportunity for engineering service providers to leverage discontinuity and build their strengths and move up in the value-chain as Infosys Ansaldo Energia deal shows.

Russia as engineering talent base for the engineering services industry: Russia has the incredible engineering talent and despite a good history of Indo-Russian relationships, Indian IT and engineering services has failed to tap it. This could be the start of one of many deals where Indian engineering service providers will augment their delivery capability in Russia.

The Bottom Line: This interesting deal gives Infosys an opportunity to drive its strong turbomachinery strength in engineering services and leverage its engineering delivery presence in Russia and Croatia to grow both engineering services and overall IT services business.

To close, I’d like to twist the opening line of one of my favorite songs – “From Russia and Croatia with love, Infosys provides engineering services to you!….”

Just one year after the industry’s first ever in-depth competitive intelligence report on the Workday Services market, HfS has just published the updated HFS Blueprint Report: Workday Services 2016. We analysed and positioned sixteen Workday service providers according to their execution and innovation capabilities.

So, what’s changed since last year?

What a year it’s been! Workday service providers have been busy investing in service offering expansion, tools and technologies development and talent retention programmes to remain competitive in this hot growth market. There’s also been some consolidation, including:

The Aon Hewitt acquisition of UK-based Kloud

KPMG’s acquisition of Towers Watson HR Service Delivery Practice

The IBM acquisition of Meteorix

And the Mercer acquisition of CPSG

And we’re sure the consolidation will continue!

Last year’s report focused heavily on service provider’s capabilities to deploy and support the Workday Human Capital Management (HCM) product, as that formed the majority of the market at the time. Since then the Workday Finance Management (FM) application has grown in popularity, with enterprises either deploying this in phase 2 projects, considering HCM and FM together as a platform deployment, and some enterprises even leading with the FM application deployment.

We have seen the focus of work shift. Last year enterprises were largely concentrating on implementing the applications, with lower demand for consulting or management services. Although the focus on implementation remains this year, with buyers still demanding fast deployment cycles, more additional service opportunities have appeared. Particularly, as buyers realize the importance of preparation prior to rolling our any SaaS initiative. We have seen a greater emphasis on Workday readiness services that provide guidance and some visibility of their Workday journey. Plus consulting work that positions Workday at the heart of their HCM and finance business transformation initiatives. Management services were hardly considered last year, but this year, buyers are realizing the need for ongoing, flexible support services to keep their deployments relevant to business requirements and outcomes.

So, all in all, the market has changed that much that it almost felt like doing a completely new Blueprint rather than an update.

So, which service providers stood out?

We should note that all of the providers we included were very strong, which is not surprising, given that Workday works very closely with each of its service partners to provide guidance and assistance. All service providers were either in the As-a-Service Winner’s Circle, High Performers or High Potential categories. In other words, they all had excellent vision of where this market is headed and are investing in services and solutions to meet the emerging demand. This remains however, an immature market, with client demands still largely focused on requiring fast technical deployments. Most client references across the board were unsurprisingly very positive. As a result we have a cluster of providers in the As-a-Service Winner’s Circle this time round. As the market matures and continues to change over the next year, we expect a few clear winners to break away from the pack and create some clear differentiation. DayNine, Aon Hewitt, Deloitte and Collaborative Solutions particularly impressed with their execution capabilities. We saw a lot of impressive innovation, at Accenture, Deloitte and DayNine, IBM, PWC, Appirio and KPMG. And OneSource Virtual continues to standout with its focus on BPaaS solutions.

What are we expecting next year?

More consolidation! The acquisition game is not over and we expect some more consolidation before we refresh this Blueprint in approximately 12 months. Those who acquired this past year, have a massive opportunity to integrate, market and deliver the combined capabilities to strengthen their position in this market. And we expect the service providers who invest in developing consulting and management services to do well as demand for these services picks up in the next year. We think there’s a high chance the grid could be very different again next time round! Stick with HfS to monitor the important changes in this rapidly evolving market!

If you had dropped by our new Bangalore office last month, you would have found fellow HfS Research analyst Tanmoy and me poring through loads of engineering services data for the Q2. The end result was that we prepared a comprehensive 29-page report (which even our Editor-in-Chief Mark Reed-Edwards had a hard time editing!) highlighting Q2 Engineering Services Trends with a large number of data points and charts.

I have picked three charts from this report to convince you that automotive is in the driving seat of engineering services growth.

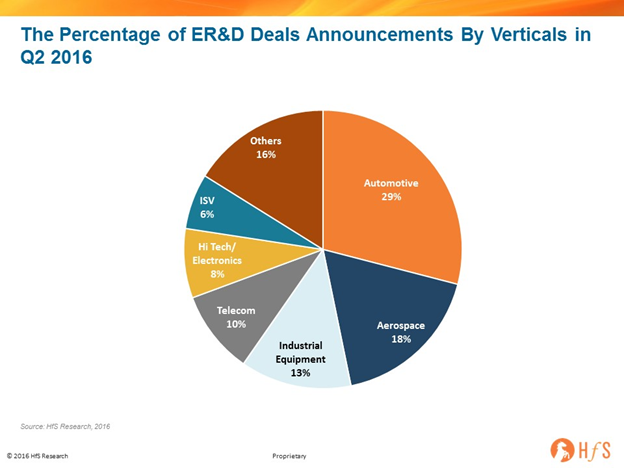

The first chart is the percentage breakup of the engineering services outsourcing deals announcements by verticals in Q2 2016 (see below). This chart shows that automotive vertical bagged the highest number of deals in the last quarter at ~30% of the total.

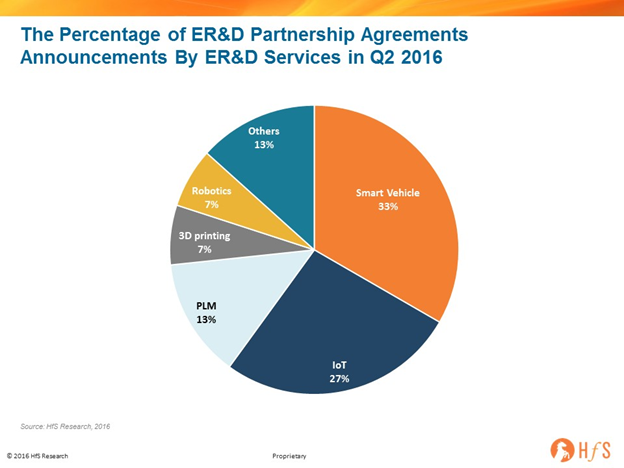

The second chart is the percentage breakup of the engineering services partnership announcements of service providers by ER&D services in Q2 2016 (see below). This chart shows that smart vehicle, at 33%, is the most preferred partnership area in the last quarter. There is a lot of investment in smart vehicles globally with the likes of Tesla, Google, Apple, Uber along with the traditional automotive OEMs investing in self-driving vehicles, connected vehicles, etc. Engineering service providers are developing their value proposition in this fast evolving space by partnering with other firms.

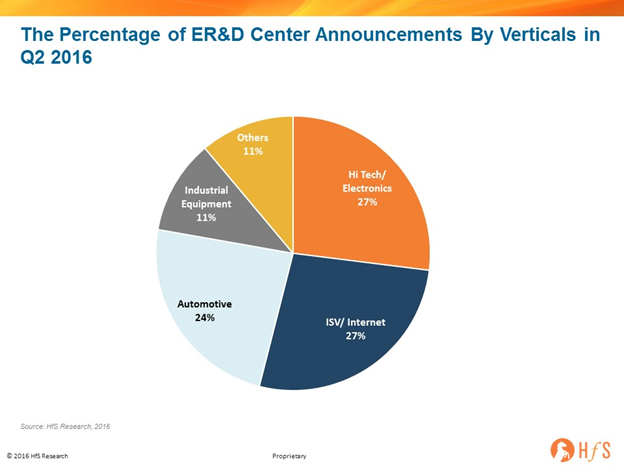

The third chart is the percentage breakup of the engineering services captive center announcements of either new centers or expansion of the existing centers in Q2 2016 (see below). This chart shows that though automotive vertical is at number three position, the gap between automotive verticals and other top two verticals is small. The top two verticals are from emerging areas such as software and high tech where R&D needs are higher. Among traditional industries, automotive leads all the way as there are a lot of R&D requirements in connected vehicles, self-driving vehicles, etc. which OEMs and Tier 1s will like to research and test in-house.

These charts show that automotive customers are actively outsourcing to engineering service providers and also setting up their own engineering centers across the world. Also, engineering service providers are augmenting their automotive capabilities with partnerships. These are all good signs for the automotive vertical. Also, in one of my earlier blog I discussed the spike in vehicle recalls and its implication on the growth of automotive testing, verification and validation services.

The Bottom Line: We believe that automotive may become the largest vertical in coming years as a result of the growing interest of automotive customers and engineering service providers.(In our Engineering Services Blueprint Report we discovered that automotive is the second-largest engineering services vertical after telecom and hi-tech)

HfS subscribers can click here to download the full POV on Q2 engineering services trends.

Don’t you just love being in Denial? That wonderful place where all you have to do is show up for work, do the same old, same old… and everything just keeps on ticking along. Isn’t it so cool to wake up in the morning and proclaim to the world that you’re just so excited to plonk your behind down in your tried and trusted swivel chair and keep those lovely green lights staying on?

Well, I have bad news for, Denial-lovers, because we finally all accepted, at the HfS Cognition Summit this week in Westchester New York, that we have to bid our fond farewells to that nice cosy place, where linear growth and green light happiness were taken for granted, where it was OK to have lots of manual workarounds to keep workflows going, when robots were visitors from the future, as opposed to appearing on your desktop to run repetitive loops on your invoice processing…

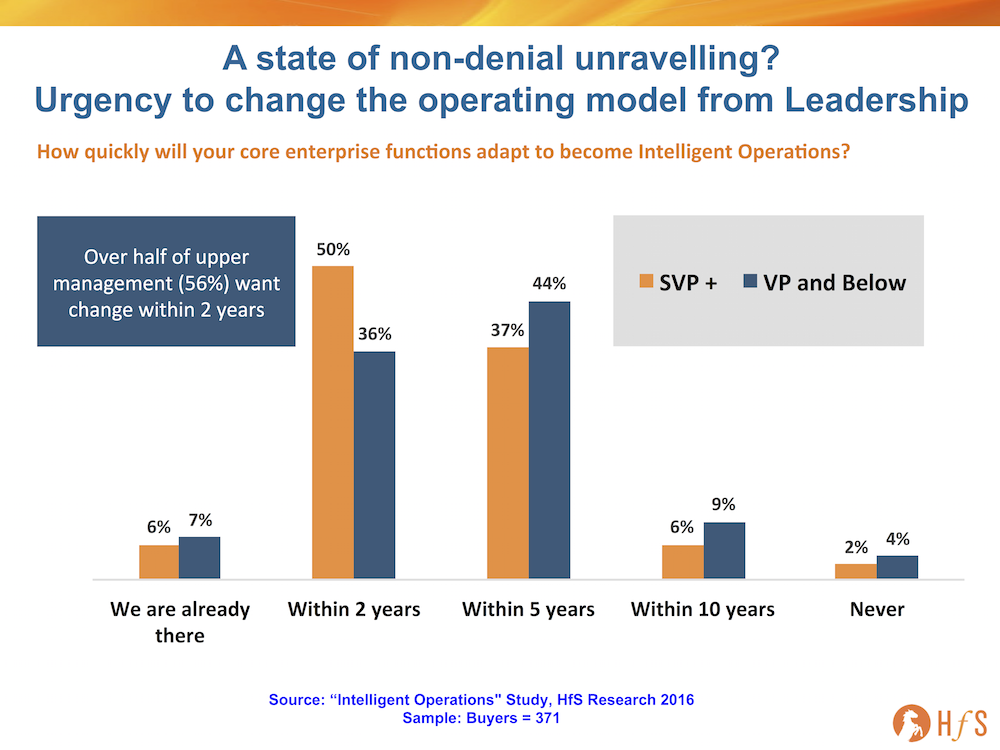

As our recent study of 371 major enterprise shows, well over half (56%) of senior leaders now expect to see major moves towards intelligent operations within two years. Compared to our 2015 study, where 70% were still looking at a 5 year horizon:

Two years is real, it’s a time span that impacts us all today, not one where we are procrastinating, or simply leaving the problem to someone else, once we have left our current job.

By why now? What’s wrong with a few extra years wallowing peacefully in Denial?

Social media is leaving us with nowhere to hide. Let’s face facts here – RPA technology, by and large, is nothing new – much of it has been around for the last decade and beyond. “Cloud” has been around for so long, we’ve almost forgotten about it. Cognitive tools are still largely smart macros and algorithms (again, nothing new), while Rolf Faste was harping on about Design Thinking to Stanford students in the 1980s. The reality, today, is that we’re educating ourselves (and hyping ourselves) at a breathtaking daily pace and, suddenly, if you don’t have an automation strategy, are tinkering with cognitive capability and have some clue how to make your enterprise behave more “digitally”, then you are officially legacy. The way we think, operate, manage and communicate is becoming brutally exposed – in almost every business situation with which we deal. If you are behind the curve, everyone knows it very quickly and you are typecast as the walking corporate dead. There is nowhere to hide, people… it’s time to purchase that one-way ticket out of Denial, before that long-awaited career move making sandwiches becomes your future.

Offshoring never was a permanent solution, it’s part of the gearbox of value levers. Remember all those times we debated the accidental “career” that is outsourcing? When shifting back office work to cheaper labor pools around the world was a special skill, a unique capability that only a very select group of us, endowed with this blessed experience, could boast? What we weren’t really considering, back in Denial-day, was that offshoring work was only the first phase in a quest for better efficiency and value. Just because you signed a five year deal to shift the work of 500 headcounts to a be carried out at lower cost elsewhere, didn’t mean you weren’t intending to search continually for new ways to innovate in the future? Most enterprises that have outsourced IT and business process work today are already putting real pressure on their operations leadership to commit to new, identified value levers, with an automation strategy being the prime lever that is the natural sequential transformation phase for most operations, whether or not they are outsourced.

Digital disruption is driving more urgency and paranoia among enterprise leaders. In many industries today, digital business models can completely take established legacy enterprises out overnight. If you are (for example) an insurance firm with 10,000+ people processing claims onshore using green screen computers, a bank which still has hundreds of branches employing tellers from the 1970s, or a retail outlet with no mobile app strategy, you are at dire risk of competition coming at you with a completely app-ified, user friendly, intuitive and cognitive business model, supported by low-cost sourced operations. If you have failed to see what could be coming at you, and do not have that salvage plan already in play, where you are ripping out that costly, unnecessary legacy, with a plan to compete against your potential “uberized” new competitor, you really are doomed. If you are a highly paid enterprise leader who is not aware of what could happen, without a plan to counter it, you might not be in a job for much longer…

The Bottom Line: Leaving Denial is one thing, but make sure you arrive successfully in Optimistic Reality

If there’s one thing that we all need to stamp out, it’s the pessimism and fear-mongering – most of it’s unwarranted, unfounded and irresponsibility created by people who should know better. The reality is, we are dealing with some disruption to jobs, as automation, when implemented well, can reduce some transactional headcount (which we predict as having a 9% negative impact over the next five years, and will be largely offset by natural attrition and workers evolving their skills into other areas).

In my view, the real threat comes in the form of disruptive competitors using digital platforms and cognitive computing that can wipe out your enterprise overnight. Imagine a new bank appearing, with a great mobile app, immediate customer service via chat / phone etc. Or a rival insurance firm that delivered everything you needed at half the premiums, but twice the usability? You’d switch in a heartbeat wouldn’t you? And these capabilities are here today, they’re not coming tomorrow.

And also remember that the threat of legacy extinction is with mid/advanced career folks, not our kids… they’ll always adapt and survive, as they have the digital skills and awareness to do what modern businesses need. It’s the 35+ generation that needs to get with the program and grasp how to manage automation initiatives, how to understand a cognitive workflow, how to determine and execute a digital business model. It’s the mature executives who have been basking far too long in the delights of Denial and must make a hasty exit to Optimistic Reality.

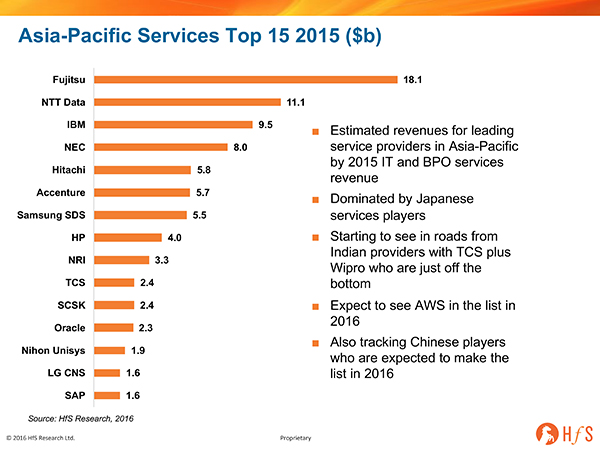

Over the last few weeks we’ve written a few blogs about the leading BPO/IT services players in EMEA, more recently the leading BPO/IT services players in North America. Now is the turn of Asia and the Pacific region. This region is more awkward, with a list containing a few familiar faces, but many less familiar to those outside of the region. The most dominant force in the Asian market are the Japanese players – Fujitsu, NTT Data, NEC ad Hitachi – with some notable players from Korea such as Samsung SDS.

Although most of the trends are familiar – the traditional players struggling to grow, while battling to gain mindshare in new As-a-Service business models like cloud infrastructure, BPaaS, and SaaS. Although

Perhaps surprising to many outside of the region is the lack of presence of the big offshore firms apart from TCS, no Cognizant, Wipro, HCL, or Infosys. Although they have significant revenues in India, this is still a relatively small market, and they have little elsewhere in the region, especially in the big markets like Japan. TCS has made bigger strides in gain a presence outside of India – with a sizable business in Japan and Australia. Wipro is second in the region, just off the bottom with success in Japan. Frankly, the key to scale in the region.

The large global integrators like IBM, Accenture and HP have never been as strong in Japan as the local players and so in spite of strong presence in China/Pacific are dwarfed by Fujitsu.

The biggest changes we expect over the next two years are the rise of more Chinese players – with firms like Digital China, Alibaba and Neusoft building on and offshore business. Additionally, we see AWS as a key player shortly, particularly given the recent investments made by the firm in the region with centers in India and Korea launched earlier this year.

Bottom Line: The AP market is poised for major change… but not just yet

There is still plenty of room for growth in IT services and BPO within the region. Particularly in emerging super economies like India and China – but the beneficiaries are likely to be local providers and international providers with a distinct value proposition – like AWS and its best in class cloud infrastructure. Although we anticipate stiff competition from regional champs like Alibaba.

The lack of success of the offshore firms in the region is mainly due to the reduction in their key value proposition – labour arbitrage. However, we may start to see other members of the Indian WITCH group rise the list as labor takes a less important role within the market and within these providers, some of which are making real efforts to develop “as-a-service” offerings that blend low-cost talent with automation capabilities.

It doesn’t really matter what part of the world we are in, the competitive landscape is pretty much being shaped by the same overriding forces – the endless client demand for productivity improvement, rapid technology adoption around client engagement and data, the drive to simplify infrastructure, whilst providing a more comprehensive service and the shift to more platform-based services. This means the criteria for success for the providers, particularly in the enterprise space will be the same. If anything when we survey Asian companies they are more progressive about technology adoption and business process change. So agility is the key differentiator for providers, the world over. Given the uncertainty across the world, we are sticking to our mantra: the main differentiators for any service providers is the ability to adapt to the market conditions and the capacity to deliver intelligent (and adaptive) solutions to clients.

HfS Premium Subscribers can download the full report here.

Translation Service LanguageLine Accents the Teleperformance Portfolio

Contact center outsourcing powerhouse Teleperformance has seldom ventured outside of its core of contact center services, so it was with great interest we learned of its recent $1.5 billion acquisition of LanguageLine Solutions, a provider of over-the-phone and video translation services. In today’s world of “going digital,” this acquisition is more about filling a market gap and increasing the value of non-automated interactions, and fulfilling the talent strategy that supports “OneOffice” than about enabling the automated or digital interactions themselves. This is a smart move that complements Teleperformance’s business and will help to better serve its clients.

Translation service fits well into a comprehensive talent strategy

LanguageLine fits well into Teleperformance’s portfolio, as one of the many contact center service providers trying to carve out a new value proposition and maintain relevance in a rapidly changing market. LanguageLine’s 8,000 interpreters, supporting 240 languages, are largely work at home employees; the home based delivery option is one we’ve watched grow in recent years as a solid strategy to find and retain better talent. Companies like LanguageLine have created a common market for interpreters, most of which are formerly self-employed contractors. It provides these contractors with a network, benefits, and corporate culture, but the flexibility of the work-at-home, and the satisfaction that comes with assisting customers with higher value services.

We can surmise that much of the translation service are of higher value than the average contact center interaction; the majority of the interpreters’ calls are over 10 minutes long, indicating more calls greater in complexity than average. LanguageLine is protected from (simple) automated interpretation services due to the majority of clients coming from highly regulated industries including healthcare and BFSI, supporting our that automation generally isn’t replacing contact center jobs, it is making them more challenging and interesting.

LanguageLine will help Teleperformance better serve the healthcare vertical

We see the greatest opportunity here in particular to increase the value of the service provider’s healthcare offerings (LanguageLine’s revenues are close to half from the healthcare vertical). Teleperformance has a sizeable and growing presence in the payer space, and we speculate that using the video translation services of LanguageLine could help create a unique value proposition at those sites where Teleperformance runs the interactions for people enrolling in health insurance. Healthcare organizations are highly sensitive about interactions with their constituents, and the context and finesse needed to handle these translations are great, so Teleperformance’s ability to handle these interactions well would be a big differentiator.

Taking the LanguageLine service and integrating it into Teleperformance’s already well rounded customer experience portfolio will be the key to success. Teleperformance is no stranger to adeptly integrating major acquisitions (i.e. TLS Contact, Aegis U.S.). LanguageLine has proven to be an adaptable organization, starting off as a translation service for Vietnamese refugees in 1982, and was owned by AT&T from 1990-1999, before being sold to a private equity firm. Teleperformance shares a number of clients with LanguageLine and partners with them on specific projects, something the service provider has proven works well through the TLS Contact acquisition. Teleperformance should in theory be able to position complementary services for business results with clients that overlap.

The Bottom Line: LanguageLine’s expertise helps Teleperformance further hone its already smart talent strategy.

The acquisition confirms the service provider’s focus on home based agent delivery and higher value interaction services. The fact that LanguageLine already has a well established remote video interpretation service shows that it is pivoting the business toward important trends and keen to serve the customer of the future. This acquisition takes a talent and vertical expertise focused approach to support OneOffice; it is a really smart move to fill a market gap, reaffirming Teleperformance’s commitment to sustained growth and serving its clients by developing and retaining the best possible talent.

EXL just announced its acquisition of IQR Consulting, a small but fast-growing marketing and risk analytics service provider to the banking industry. This follows EXL’s acquisition of RPM Direct early last year to augment its insurance data and analytics portfolio (read more in our coverage here), which it is also starting to use in healthcare. With IQR, EXL is continuing its focus on adding analytics and data assets with a vertical flavor.

On the surface, this looks like a typical acquisition to build scale, but IQR brings some interesting downstream opportunities for EXL:

Access to regional banks and credit unions: EXL has developed client relationships with some of the largest banks and financial services institutions in the world, providing them with much needed scalability for analytics and reporting functions over the years. IQR will help the service provider forge new relationships with smaller BFS segments, credit unions in particular. Regional and supraregional banks and credit unions have differentiated needs, challenges and levels of internal capability with analytics functions when compared to the BFS majors that EXL primarily works with. IQR has found a way to network and grow its presence in these segments, partly due to its board members’ industry backgrounds. These new categories of clients present EXL with new opportunities, not just for analytics work, but to cross-sell BPO and BPaaS solutions in the future.

BFS-specific marketing analytics to complement EXL’s breadth: EXL has comparatively more of a reputation and experience in the portfolio and risk analytics space in the banking and financial services industry. IQR will augment its BFS marketing analytics portfolio, in particular bringing data insights to formulate brand strategies, communication tactics, promotional offers and pricing strategies for banking clients.

Access to an analytics talent hub: This is an exciting one – Ahmedabad, India, where the majority of IQR’s workforce is based, is a new location for EXL’s analytics practice. As wage inflation for analysts soars across other metros, EXL will want to find newer locations for sourcing – and even shaping – analytics talent. IQR presents this opportunity with operations out of a city growing its engineering, math and statistics talent base.

The Bottom Line

We placed EXL in the Winner’s Circle for our BFS Analytics Services Blueprint this year, noting its interest in working with smaller players in the BFS industry (fintech clients, etc.), while its competitors go from blue chip to blue chip. This acquisition further outlines the service provider’s broadening of its BFS analytics portfolio to service different client segments. Overall, the combination of EXL and IQR brings regional banks and credit unions the opportunity to work with an analytics specialist that can bring both scale, process rigor and greater resources to invest in program development, as well as the domain experience to cater to their data and analytics needs to achieve business outcomes in the marketing realm – increasing member lifetime value, brand loyalty, and smart omnichannel servicing. The next step for EXL will be to further outline its vision for smaller BFS players, and how the amalgamation of these acquired and homegrown analytics and data assets help it address their unique challenges.

It’s time to end the hype and get real about the evolving world of digital! Later this month, I’ll be sending out Requests for Information for our forthcoming HfS Digital Blueprint where we will truly flesh out where this market is today, and the path we need to take to close the gap between Digital potential and the ability for ambitious organizations to achieve it.

‘Digital’ is a word which has been hopelessly mangled by market forces. The huge societal change wrought over the last eight years by the advent of the iPhone and Android and improved connectivity – the prime as catalysts for the proliferation of social network connections, conversations and data, has created havoc for the vast majority of companies, still firmly anchored in previous generations of technologies. Digital marketing has evolved very quickly to allow the positioning of products, services, buying opportunities, customer support and feedback, and digital marketing budgets have exploded in so many ambitous organizations eager to hop on this “bandwagon”.

Marketing, by its very nature, evolves and changes constantly to seek competitive advantages and differentiation, and these techniques have also been used to position countless companies as ‘digital’, much as previous generations added an ‘e’ prefix to everything (or Apple’s ‘i’ prefix)- so we had eShopping, eCommerce etc etc. In most cases, this posturing was to cover up the fact that the ‘e’ suffix was being added to tart up legacy offerings as market repositioning, and this is often the case today with ‘digital’.

While these digital branding activities can be highly effective for specific sales motions and targeting, it has arguably hurt broader digital evolution, creating mass confusion about what ‘digital’ actually is beyond marketing speak. A few years ago ‘SSMAC’ – Security, Social, Mobile, Analytics and Cloud – were considered core components of ‘digital’, floating offshore from IT on a sea of ever more valuable Data. Since then, legacy IT has soldiered on in a business climate made ever more complex by digital and budget pressures, while ‘digital’ has grown to become ever more ubiquitous.

Bymid-2016, and moving forward, many firms have high level ‘digital first’ imperatives in place, and some understanding of strategic goals and threats. What’s problematic is all those pesky legacy ways of doing things – the workflows, ring binders, filing cabinets/ Sharepoint, technologies and relationships that choke any sort of change management. Like ivy in a garden, the old ‘we know how to do this’ culture grows back fast. Add to this the reality of multiple vertical budget P&L’s, organizational politics and rivalries along with a percentage of management and most of HR sleeping on digital opportunities and threats, and we have a growing vacuum.

Fortunately, enterprise service providers have been tireless in creating and learning new ways of doing things in a digital world, having seen the threat to their livelihoods in continuing to merely servicing last century IT and associated business processes. Where a couple of years ago it was quite challenging to find scale resources to execute digital initiatives, today there is an appetite to help businesses compete in the ever more data and collaboration driven world.

I’m right in the middle of briefings with both providers and buyers of services for our upcoming ‘internet of things’ (‘IoT’) blueprint and having a fascinating time discussing approaches, projects, methodologies and business outcomes with scale vendors. Sensor-driven data flows are a critical dimension of digital, from real time industrial machine intelligence feedback (‘I’m going to need a new solenoid soon’) all the way to smart factories creating smart products that communicate regularly throughout their life, to both the seller, owner and manufacturer to be as efficient as possible.

During the coming months I’ll be meeting various industry luminaries to discuss the state of ‘digital’ – perceptions of opportunities, stresses and pressures, and what it takes for companies to take the leap and place big bets on a holistic, ultra interconnected digital framework to replace the fragmented, heterogeneous environment most IT infrastructure evolution grapples with. This takes vision, confidence and courage to achieve in mature companies, but the reality is that failure to grasp this opportunity will result in modern ‘full stack’ digital startups, rapidly superseding legacy firms and taking their markets.

Interesting times and this is going to be an interesting, timely piece of research in a fast moving world…