We often ask this question. Customer quantity is a no brainer because more customers can bring more revenue. Similarly, customer quality is also important because the better the customer quality or size, the better the revenue potential for service providers. But what is more important—customer quantity or customer quality?

We all have the anecdotal answer to this question based on our experiences but what does the data say?

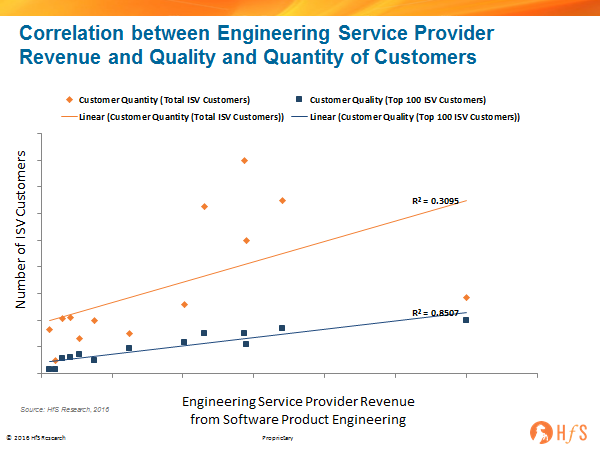

In one of our engineering service studies, we tested this on data and found interesting results. In our software product engineering services study, we correlated service providers’ software product engineering services revenue with the quantity and quality of their customers (see the Exhibit). For customer quantity, we took the count of service providers’ ISV customers. For customer quality we took the count of service providers’ ISV customers that are among the top 100 ISV customers by revenue because the larger the size, the better the potential of account mining.

We found that the correlation between service providers’ revenue and quality of customers is very strong (Correlation = 0.92 and R2=0.85) in comparison to the correlation between service providers’ revenue and quantity of customers (Correlation = 0.56 and R2=0.31): As a student of mathematics, I will be the first one to point out that correlation doesn’t mean causation. But it nevertheless gives us the opportunity to step back and ask ourselves the following: What if the quality of customer drives revenue more than the quantity of customers? What are the implications for engineering service providers and how can they position themselves to grow in a more future-oriented way?

Service providers should focus on the quality of customers and persistently target large customer accounts: This is a no-brainer as a strategy but sometimes difficult to execute. Getting a foot in the door of a large account and displacing incumbents can be difficult and requires persistence. Sometimes, with quarterly pressures mounting, service providers give up on these large accounts and target easier options. In my earlier gig, I came to know that it took seven years to penetrate a large customer account (Yes, seven!). In quarterly reviews, leaders sometimes lose focus on long-term targets, but in this example, leaders kept asking for an update on this particular account in every quarterly review I attended. What is happening in that account? Who has the account manager met with in the last quarter? Are there any RFIs or RFPs they’ve heard about? Any chances of proposing free PoC? Any firm they can partner with? And the list goes on. It requires the persistence of leaders to pursue this long-term strategy and luckily the business leaders in that firm were for the long haul (they are still working there when I last checked =) ).

Once the service provider has got a foot in the door, grow the account by making it real and not over-selling: In engineering services, especially at this time, service providers are competing more with the non-outsourced spend than with other service providers to grow the accounts. Service providers have told me that even after signing the contract and setting up the ODCs, the accounts just don’t grow. One piece of feedback I heard from the buy-side is that many product leaders are skeptical of outsourcing and somehow service providers need to convince them. Service providers typically approach this by hiring good sales and account managers. But the problem is most of the product owners or decisions-makers are technical guys and they don’t like sales guys or account managers showing their face every month. But they do like to know industry trends, what their competitors are doing, where the industry is moving. So, in my opinion, service providers will do better if they invest in “making it real” (something Phil Fersht has also written about in the larger IT services context). In other words: share prototypes, case studies, and demos. But don’t sell!

Mid-tier and emerging service providers should focus on smaller customers and develop their solution value proposition: The mid-tier service providers might not have the luxury of time and manpower to focus on the big customers. They will do better to focus on smaller customers that are not natural targets of the larger service providers. They should grind it enough to make themselves ready for the bigger customer later. The disruption often starts at the bottom and slowly moves to the top. Amazon has done the same with the cloud. Its initial value proposition was aimed at startups and SMBs. Now it is ready to compete in the bigger customer segment. One Fortune 100 buy-side customer told us that they gave a few projects to a mid-tier engineering service provider because it was more cost-competitive than many leading engineering service providers. Although the customer is satisfied with the service provider’s delivery quality and timelines, the customer feels that the service provider has limitations in domain knowledge, solutions, organizational maturity and the customer is unlikely to give that service provider any major additional work. In a way, this mid-tier service provider wasted the opportunity by entering the account early without sufficient capability. The mid-tier service provider should have defined its value proposition beyond cost reduction when they bid to enter large accounts.

The Bottom Line: Both large engineering service providers and mid-tier engineering service providers can use this correlation research to review their client acquisition and account growth strategies based on quality and quantity of customers.

Posted in : Procurement and Supply Chain