Tired of the Blockchain hype? You should be, but the emergence of Hyperledger Fabric 1.0 gives us a sense of the reality to come and where this is all heading. Let’s dive in…

Hyperledger announced the release of Hyperledger Fabric 1.0 yesterday (see press release). Hyperledger Fabric is an open-source platform, hosted by the Linux Foundation that allows organizations to develop Blockchain applications. Version 1.0 marks the release of a production-ready platform that goes beyond pilots and proof of concepts. 159 engineers from 28 organizations collaborated over a 16-month period to make this happen.

There are multiple Blockchain platforms that exist today. Ethereum is the most mature public platform (besides Bitcoin) with tremendous potential and over 500 use-cases in various stages of development. There are multiple other private or semi-private platforms such as Ripple and Chain. Hyperledger Fabric is younger than many others, but there are three characteristics that make it important for enterprises that want to solve business pain points, leveraging Blockchain:

Flexible. The architecture of Hyperledger Fabric can run like a private or hybrid or public platform, making it potentially more secure from a data-privacy standpoint thus rendering itself enterprise ready

Open-Source. Hyperledger is an open source collaborative effort created to advance cross-industry blockchain technologies. It is a global collaboration, hosted by The Linux Foundation, including leaders in finance, banking, Internet of Things, supply chains, manufacturing, and Technology. This structure gives it the potential to become the de-facto standard which will become an important adoption criterion going forward

Not crypto-currency based. Hyperledger does not have a crypto-currency (such as Bitcoin or Ether) which potentially renders it more usable for business applications as not every potential use case needs a currency

The announcement marks a significant move forward to leverage Blockchain for business use cases. The Hyperledger Fabric project started in March 2016 based on merged codebases from IBM and Digital Assets Holding. It moved out of incubation 12 months later and was ready for pilots and POCs. Now four months later, they have released Hyperledger Fabric 1.0 – a production ready version.

Does this mean that Blockchain can now become mainstream for enterprise adoption? No.

These are the three challenges the Blockchain pioneers must address to make the technology truly enterprise ready:

1) Technical challenges. Blockchains by design will never be able to complete thousands of transactions in a second, but the technologies do need to be able to scale up for enterprise-grade performance, efficiency, and costs. Hyperledger Fabric promises to solve this by not using consensus-driven Proof of Work (PoW) that most other Blockchains are built upon and requires major computing power

2) Policy challenges. There are no Blockchain standards, there exist multiple platforms with no interoperability, and there are no regulations in this space. And these are not easy questions to solve. For example, given that all Blockchains are Distributed Ledgers, which geographical jurisdiction will be applicable?

3) Nascency challenges. Several challenges stem from its nascency and novelty. Lack of proven use cases, limited understanding of technology and its potential, limited talent and skill-sets shortage across IT and business, etc. The inherent power and potential of the concept with the help of some pioneering risk-takers will help pull it through such nascency challenges, but it will take time

Bottom-line: There is still a long road ahead for Blockchain, but real progress is being made.

Notwithstanding these challenges, the advancements in Blockchain technology are happening at a frenetic pace. Market developments such as this Hyperledger Fabric 1.0 release are important milestones in the development of this space. It’s important for enterprises to take notice and start investigating.

One of the leading service providers is also one of the most understated: Hindustan Computers Limited, or its better-known abbreviation, HCL. This company has grown its revenues by more than 75% in the last 5 years and maintained its profitability to surpass $7 billion this year, while running Wipro close to being the 4th largest Indian heritage IT services firm. Its reputation is one of having a very strong engineering pedigree, a “roll the sleeves up” attitude and a no-nonsense approach to business. The fact it has never bothered to spend millions on a fancy new logo, or glitzy marketing posturing, speaks volumes for this determined, humble and very focused firm, quietly – but aggressively – going about its business as becoming one of the heavyweights of the IT services industry, and one of the best positioned to weather the current malaise caused by flagging demand, too many competitors, and creeping automation.

So when I got a chance to spend some time with its new, young dynamic CEO, C Vijayakumar, or “CVK” as everyone calls him, I just had to share some of our conversation with the HfS community…

PhilFersht,CEOand Chief Analyst,HfSResearch: CVK, tell us about your journey to becoming the CEO of HCL Technologies? What is your secret sauce?

CVijayakumar(CVK), President and Chief Executive Officer, HCL: More than the secret sauce that I bring to the table, the question is, what is really special about HCL, and what is that secret sauce that has developed a range of leaders within the company. They may seem different and diverse on the surface, but all our leaders embody a core culture within, and that’s fairly constant. I have had the good fortune to be part of some great milestones and worked with some excellent teams at HCL. I have also worked across multiple business functions – strategy, practice, product management, sales, business development and delivery. This has helped me to get a well-rounded view and brought me to this position today.

Phil: So what is the number one issue with HCL and the business… what is keeping you up at night?

CVK: The number one issue is the speed at which we can evolve our next generation of services. I believe if 40% of your revenues are from next generation services, then we have crossed a threshold to be relevant and do well. 20% of our current revenues are coming from next generation services. How can we get this up to 40% in the next 2-3 years? Or how fast we can get there? That’s what we are working on and that’s what keeps us up at night. We have a strategy, our “Mode 1-2-3 strategy” we are driving on a three-lane highway where we need to maintain a steady pace in the lane we are driving on, Mode 1 – our core services. Moving to the adjacent lane, Mode 2, we have an opportunity to overtake and finally working our way to the high-speed lane which is Mode 3. That’s how we and a lot of global leaders look at it, especially in the IT industry. Technologies themselves may not be the big things you are worried about, I think every business is trying to reinvent themselves, reimagining and rewiring their business using new technologies. Every aspect of the IT industry, infrastructure, application, business services, even the talent, and skill is undergoing significant change or disruption. My focus is to evolve the business in line with the changing dynamics and rapidly changing customer dynamics. That’s where the focus of the company and the leadership team lies. Our Mode 1-2-3 strategy has been built to address theses issues:

Mode 1 – is our core services: infrastructure, applications, BPO and engineering services. They contribute 82% of our revenue as measured in the last quarter. The differentiator is the industry leading autonomics platform called DRYiCE. We are still the most significant player in these services offering practical benefits for our clients.

Mode 2 – our experience-centric digital services or outcome orientated IoT services enabled by a foundation of cloud and security, leveraging what we call DRYiCE orchestration. This is where cloud and security are already enabling digital which offers a great growth opportunity for us.

Mode 3 – this is unique to us and is about using the ecosystem to future-proof our business. Building a products and platform business, by creating innovations enabled by creative partnerships. The products are stable, long-standing products and we make them relevant for the new world. This is different from creating products from scratch. You buy the IP and see how you can modernize and make them relevant. A good example would be our work with Workload Automation, we bought the source code license from IBM and created a cloud Workload Automation solution which is very relevant in data centers, which are becoming hybrid cloud solutions. This strategy is working very well. We have numerous products in the pipeline, they are all traditional products but they are being reinvented to be relevant in the modern world. That’s the Mode 3 strategy, we not only have this on the technology side, we are doing this on the business functionality as well. We have a few things in the pipeline that we will announce shortly. We are building a strong products and platform business. This is an in-depth answer, but technically this is what is keeping us up at night.

Phil: Very well-articulated! What do you think, CVK, is going to have the biggest impact in the next 3-5 years? Is it blockchain, automation, cognitive or something else?

CVK:I think it’s a confluence of all these things, not just one thing. These and some more things will all have an impact. We have now identified 5 distinct areas that will have a huge impact on the services industry and they are: Digital, IoT, Automation, Cloud and CyberSecurity. There could be many sub-themes in and around these areas, but broadly these are the 5 key themes. We recognize that clients’ ability to adopt these will vary based on the maturity of their existing environments, hence we have created separate focus groups with a leeway to invest adequate management support to the three Modes that we are operating in. I believe having the right investment and right management across all the various aspects of operation is critical to our Mode 1-2-3 strategy.

Phil:A lot of this is going to require ‘unlearning’, changing the way things have been done in the past. When you look at your company and where you are going, how can you unlearn the last couple of decades to make yourselves truly relevant for the next decade?

CVK: I open a lot of presentations with a quote from Alvin Toffler – “The illiterate of the 21st century will not be those who cannot read and write, but those who cannot learn, unlearn, and relearn” – I keep emphasizing this to our business leaders and the technical talent – learn, unlearn and relearn – is a very important aspect. The outsourcing business is definitely changing. Even if for a moment we believe it’s not changing dramatically, it’s always good to believe it’s changing dramatically, which will propel us to do the right things and be ready when these changes have to be implemented for a client, or to change your business model. I believe the industry is changing significantly and we have to change ourselves. Traditionally there were many subject matter experts with in-depth knowledge in technologies, but today the silos have broken down and IT is a vast horizontal plain, cutting across technology, businesses and different functions. The challenge is to create a breed of inter-connected specialists who can traverse different domains. This is where we need to focus our talent – continually building capabilities that will make them a full stack engineer or a converged engineer who can look at not just running infrastructure but who can program application API’s and micro-services etc. Creating talent that has a broader view than the siloed view of the last few years.

From an industry and services perspective, it’s no longer a labor and a cost arbitrage game, it’s about how you can deliver a business outcome and encourage your teams to have skin in the game, by committing to a solution, committing to an outcome, that will deliver through that phase and ensure the outcomes happen. Customers today are looking for a partner who will have skin in the game and ensure business outcomes. We are therefore encouraging our teams to take some risks, learn something on the way and deliver outcomes.

Phil:That’s great to hear, and it’s difficult to have a conversation like this without talking about the impact of politics. For the first time politics and technology are becoming entwined in a business model. In terms of HCL business have you seen a major impact on your own financial performance, as a result of some of the political changes and noise that we have had in the last few months?

CVK:Yes, due to the political changes, I think some decisions have been delayed, people are reviewing their decisions a lot more carefully and thoughtfully. Everyone is worried about being visible. It has definitely slowed down the flow of some new deals. But most customers strongly believe in the business model, the outcomes that they expect in the services outsource space. There is some delay but I don’t think that people are fundamentally rethinking this. They are being a little bit more cautious, so it has an impact to that extent but I do not believe it will fundamentally change the way customers are thinking about a business case.

Phil:So, my final question, if you were to be anointed the ‘Emperor of the Service Industry’ for a whole week and you can make one change, what would that be?

CVK:We have an internal communication platform called MEME where I communicate directly with all HCL’ites every day and I actually posted this question there. There were lots of very interesting responses, some of them very closely aligned to my own thoughts on this subject. I believe the IT industry is an open source world and cannot have one Emperor, but to answer your question I would probably aggregate the forces of IT to really use them for the less advantaged and unleash its benefits to the common man – in today’s world that is not the central piece which drives investment. We could really leverage IT in unimaginable ways – help the disadvantaged, help to fight crime in a very meaningful manner. The other decision would be around AI. Currently, there is a lot of nervousness about automation and AI. I am a strong believer that if you use Automation and AI in a thoughtful manner, it will give more benefits to humanity. But how do you get that done in a very thoughtful and disciplined manner? There’s a very good analogy that we can draw from the ‘Nuclear non-proliferation treaty’, signed across many countries in the world. Something like that should be done for AI, an AI treaty that mandates the use of AI in a meaningful manner to augment what humans can do and improve lives. I hope that makes sense.

Phil: This is the most thoughtful answer I have had from this question and it makes a lot of sense. It’s been a great interview and good to hear what HCL is doing to continue to be successful… excited to share with our audience, CVK!

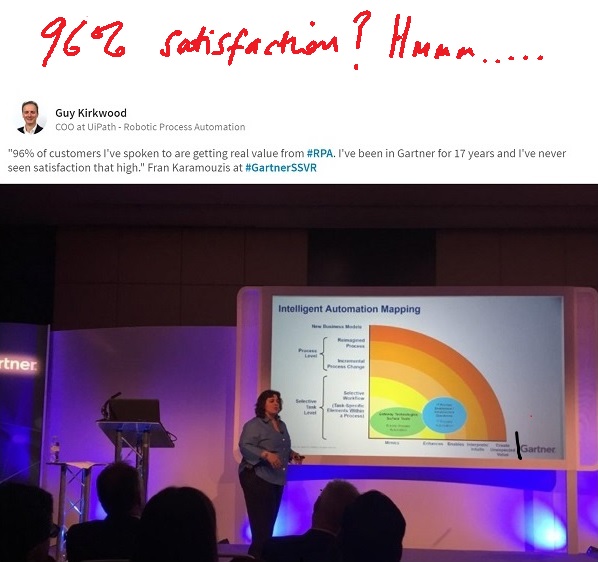

When we revealed Gartner’s bullish 96% of clients are getting real value from RPA bombshell (see post) six weeks ago, everyone close to the action was incredulous:

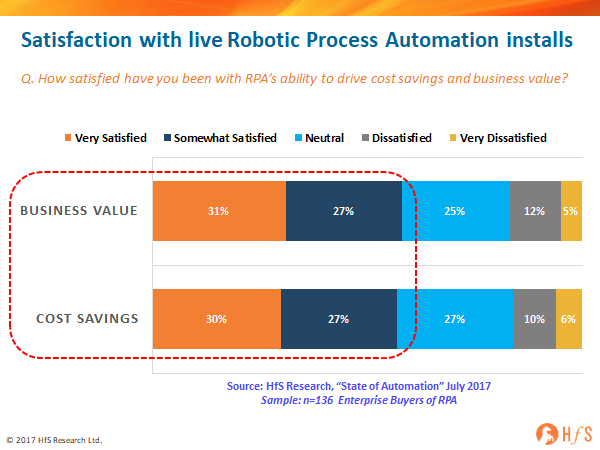

Now we have the real data to prove where satisfaction levels currently sit, where we interviewed 136 major enterprises currently experiencing RPA installs:

My personal experience has tended to be about half of enterprise RPA clients today are experiencing positive progress, while the other half are struggling or aborting RPA projects altogether, so this data is pretty positive, especially when you consider that the same number are positive about both the cost and business impact of RPA.

The Bottom-line: RPA is making sense in this era of renovation and the current satisfaction results reflect this

What I love about RPA is the fact it’s making us fix a lot of the systems we’re currently stuck with, using sensible, affordable technology. We spent years bemoaning the fact that enterprises couldn’t just “saw off” their broken processes and replace with costly new systems and services, but the reality is that most enterprises are not ready to write off their technical debt and invest in change, especially when the outcome is not particularly clear. What is clear is that most enterprises prefer to invest in making their broken processes function better, operating in a digital fashion where they can manage the change themselves and the cost isn’t abhorrent. Taking it one broken process at a time, fixing it, proving the ROI then onto the next one is the step change strategy that is working for the majority.

Yes, RPA is predominantly operating as a retro-fit solution for most enterprise clients, getting rudimentary processes functional by eliminating high-throughput, high-intensive manual interventions and helping applications and systems manage digital workflows effectively. Yes, RPA keepslegacy alive for many organizations, but in a way that you can build digital overlays over these systems, once the manual elements are eliminated and workflows are joined up effectively. Our emerging conversation, beyond RPA, is all about automating the automation and deriving the right data patterns to promote more intelligent machine learning and cognitive capabilities.

The good news is the general adoption of RPA is on the right path and the next challenge for enterprises is to figure out the next wave of digital building blocks to drive more intelligent and predictive capabilities into their data backbone. Software firms, advisors and service providers alike all have to create much more dynamic partnerships to help enterprise their clients get to this stage – this is much more about how to start innovating together and understanding each others’ capabilities. Just talk to any services provider, such as an Accenture, Genpact, IBM, TCS or Wipro etc., and they will tell you a whole new plethora of smart digital competitors are emerging and you just can’t afford to acquire them all – you need to learn how to work with them and give them some skin in the game.

We’re in an era when technological needs are complex, and there is no defined rulebook explaining how to develop a holistic data strategy. We’re in an era of discovery and making the most of what we currently have, before we can truly understand what we will need to be successful at some far-flung point in the future. In my view, being “disrupted” is when you don’t collaborate and explore… being a disruptor is being forever bold and unafraid, in order to define your own curriculum as this digital future unravels. Stay tuned for a lot more analysis from this study…

Last week, Accenture announced the latest in its 2017 $1.8 B shopping spree with Boston-based mobile design and development company Intrepid. This is a part of Accenture’s strategy to dominate the Digitally-driven Front Office with the vision to offer its clients a model with no business silos where the barriers between the front and back office are removed forever; as described in HfS’ Digital OneOfficeTM. Accenture’s strategy goes beyond the ambitions of growing and maintaining the largest digital agency in the world. It’s about building capabilities to impact its clients’ transformation, finding unique capabilities in opportunistic Geos, opportunities for pull-through with its other services, and a keen focus on impacting the customer experience.

Intrepid’s 150 employees will join Accenture Digital, the division where many of Accenture’s customer experience focused services reside. Intrepid’s engineering talent and capabilities, such as it’s work with Saucony Stride lab — an app that helps runners analyze their stride for better performance– falls right in line with the kind of digitally-driven customer experiences Accenture is looking to help its clients achieve. There are also great client synergies between Accenture and Intrepid, in particular around P&G, Accenture’s marquee client for front office services and an organization which is at the forefront of value creation from front office services.

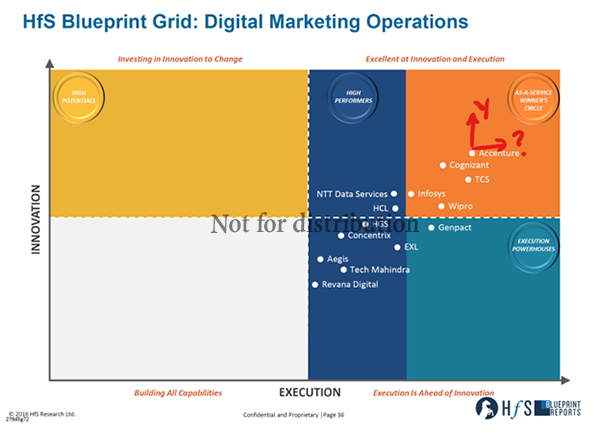

Accenture was recently placed in the Winner’s Circle of our Digital Marketing Operations Blueprint. This acquisition will further solidify its position, in a space where Accenture’s ability to replicate its Digital Front Office services across industries is also emerging as a competitive differentiator. The ‘string of pearls’ M&A strategy across the core pieces of digital transformation is illustrative of the service provider’s forward thinking vision for the evolution of this market. These acquisitions span across various core pieces of digital transformation, such as include aVVenta for content, Cimation for IoT consulting and Chaotic Moon for digital technology design and prototyping, complementing customer experience services and helping the service provider double its digital marketing operations business over the last two years.

Accenture is putting together a differentiated and bold story for the digitally-driven front office. In fact, Accenture accounts for approximately 50% of the M&A activity since January 2017. Let’s look at some of the more recent Accenture recent acquisitions in 2017:

MediaHive, May: Digital commerce strategy and design to platform delivery and managed services

Monkeys and Maud, May: Creative ad agency, Australia and New Zealand

Kuntsmaan, April: Belgian communication agency focused on customer experience

SinnerSchrader, February: German digital agency

What is the common theme in each of these selections? A clear focus on digital customer experience and design. Accenture also stands apart from the competition in the sense that it seems to avoid falling to the temptation of talking immediately about technology and software (in spite of the strength of its technology assets and partnerships), and instead focuses on the business value. This management consulting legacy and mindset is part of the company’s DNA and a big part of how it builds trust with its clients.

This flurry of M&A activity is bold, but not without risks and potential problems. One of the greatest potential issues is addressing the clashes of so many disparate and vastly varying organizations both operationally and from a cultural perspective. Accenture’s culture is built on thought leadership, delivering operational excellence, and not necessarily in sync with more “creative type” cultures that will inevitably come with the acquisitions, it’s been targeting. For now, the strategy seems to be running these entities independently, almost using them as R&D centers wherein their original cultures remain intact. But inevitably over time, some cultural transformation will occur, morphing the digital giant and its entities into something new-the question is whether legacy Accenture becomes a more creative, innovative organization-or it’s subsidiaries turn more corporate, potentially snuffing out some of the creative fire and losing key talent in the process. It also risks its size becoming a deterrent for buyers who prefer the niche specialized agencies and the attention, flexibility, and experience they receive from a smaller player.

Another potential threat is that Accenture might become complacent in delivery and execution given its dominance from a capability perspective in this space. This acquisition moves it up on our innovation versus execution grid, but will Accenture also move toward the right? We will be watching that as Accenture continues to enhance its capabilities with these innovative firms.

As Anatoly Roytman, head of Accenture Interactive for Europe, Africa, Middle East and Latin America said (of the Kuntsmaan acquisition): “Together, we’re bringing our unique model to the market: part creative agency, part business consultancy and part technology powerhouse – all laser-focused on creating the best customer experiences on the planet.” The refrain we hear constantly from service buyers — Accenture’s included—is “more innovation!” Accenture has certainly amassed an array of building blocks to address this demand globally; now the hard work begins to pull these pieces together – a ~$10B digital agency with many moving pieces, specialized skills and domain capabilities – to execute on transforming the digital customer experience for its clients.

Now available in select “HR supply stores”: IoT (Internet of Things), one of the five tools discussed in my latest POV – “The HR Power Tools 6-Pack for High-Impact Service Delivery.” Much like the double-edged sword nature of its companion power tools, IoT in workforce management can usher in unprecedented and significant business benefits, but only when the right capabilities are selected and potential risks and adverse outcomes are accounted for.

IoT is a process in which people, machines, and devices are connected to one another via a single network in order to automatically exchange data without any manual involvement. IoT can, for example:

track the productivity of workers in the field

confirm overall fitness or fatigue when relevant

assign tasks based on the nearest worker

tie scheduling real-time to customer flow

offer real-time training based on an employee’s time on job, credentials or performance

All of this sounds pretty compelling, but a couple words of caution. The first word: Volkswagen, whose engineers illegally programmed IoT-like software to sense when the car was being tested during an emissions inspection, which then activated more costly equipment that reduced emissions. This resulted in a roughly $3B fine this year. Additionally, IoT solutions will generate lots of new, often very valuable data related to people and how they perform their jobs, and not every HR Department is adequately staffed to handle the current explosion of people data or supported by data scientists.

Cause for Optimism with Early Adopters of IoT in HR

While not many HR Technology solution providers are occupying the IoT market category just yet, one company caught our attention: Triax Technologies, and specifically with their “spot- r” solution for companies with workers in the field, particularly on constructions sites. Certainly, accidents are more common there. My briefing from Triax’ COO Peter Schermerhorn enlightened me that U.S. construction companies pay out $1 billion annually for claims related to slips, trips or falls; that the construction industry pays more than twice the national average for workers’ compensation insurance; and that an estimated $7.2 billion in fraudulent workers’ compensation claims are filed annually in the U.S.

spot-r by Triax provides data-driven, real-time visibility into construction operations and safety incidents, leading to an improved safety culture on site and can result in reduced insurance costs. Automatic, geo-tagged “slip, trip, fall” alerts improve response time to accidents and record surrounding conditions (temperature, height, location of witnesses in the area, etc.), self-alert buttons empower construction workers to stop working due to unsafe conditions and alert supervisors to hazardous conditions, and high-decibel evacuation alerts are included in the mandatory wearable devices used on many of the company’s pilot projects with customers. Peter also offered a glimpse into the near future when the company’s sensors will be used in new ways to promote safety and visibility on the job site. Imagine knowing in real-time where your workers, equipment, machinery, and tools are onsite and how they’re interacting with each other.

Who said technology innovations related to HR and workforce management usually lag other business areas?

Bottom Line: As with all the other power tools (i.e., sophisticated capabilities) recently added to the HR practitioner tool belt, IoT’s potential to be a game-changer cannot be overstated, but neither can the surrounding considerations for avoiding possible misuse or sub-optimal deployment.

One of the things I’ve been at pains to convey is the critical link between digital transformation… and the role RPA plays it making so much of it possible. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embracing the cloud in a way that enables genuine scalability and security.

Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities.

So click here to download my full session at the recent packed-out Blue Prism World in London town:

I was struck by the similarities between Global Business Services (GBS) and Empires after reading ‘Sapiens: A Brief History of Humankind’ by Noah Harari. He says:

“An Empire is a political order with two important characteristics. First, to qualify for that designation, you have to rule over a significant number of distinct peoples, each possessing a different cultural identity and a separate territory….Second, empires are characterized by flexible borders and a potentially unlimited appetite…”

These two characteristics of an empire are uncannily similar to Global Business Service (GBS) organizations. GBS is:

Multi-function. GBS organizations aim to deliver services across multiple business functions (aka distinct peoples with different identities) such as F&A, HR, IT, procurement etc. all under one organizational umbrella.

Multi-geography. GBS organizations also aim to deliver its services across all regions and countries (aka flexible boundaries) that a company operates in.

The basis of the creation of Empires and GBS also has similarity. For Empires, it is about basic unity of the entire world around a central ideology. For GBS, that ideology is around standardization, collaboration, and effectiveness.

This all becomes troubling when you realize that we all have a very negative connotation around the word “Imperialism”. We tend to associate wars, brutality, coercion, oppression, and so on when we talk about imperialism.

So, is GBS also this brutal? I think it depends on what lens you view it from:

People lens. GBS makes total sense if you are sitting in the corporate headquarters but will be a bitter pill to swallow if you are the one who loses your job because of what you and many others consider to be some corporate mumbo jumbo and the latest consultant gimmick

Time lens. It feels like an achievement in hindsight but it is really challenging during set-up. Have you thought why almost everyone describes their experience of setting up a GBS as ‘war stories with battle scars to prove it’? I’ve not met anyone who has told me that the journey was smooth and they did not meet any resistance.

Bottom-line: GBS will work as long as we keep people at the core, define our outcomes and keep an eye on the future

However, I don’t think there is any value in painting GBS as black or white. Like almost everything in life, it has shades of gray. The most important question is ‘how can we make it better?’ And I think this is where GBS organizations can learn from the rise and fall of Empires.

Lesson #1. Focusing on developing talent is at the crux. GBS is about people and will not succeed without buy-in from people. The tone from the top helps but cannot be the only driver for sustainable success. Phil’s recent rant on this subject is spot on – too many enterprises are obsessed with achieving a scalable operational backbone centered on technology, as opposed to talent

Lesson #2. Make sure you know what “success” looks like. Balancing efficiency with empathy is an important concept to keep in mind. Also, there is a diminishing return to efficiency improvements and cost reductions. After a certain point of time, it really does not matter. What matters is business outcomes and for that, you need motivated talent.

Lesson #3. All good things come to an end. Every empire eventually falls. GBS is the concept that we are all rallying behind in recent times, but you can be pretty sure we will come up with an even better framework for organizing ourselves to deliver work in future (such as the HfS framework, the Digital OneOfficeTM). The life expectancy of ideas is coming down dramatically, as we jumpS-curves in years not decades. So it is extremely important that we keep looking out at the future. Keep testing, keep piloting, keep investigating. This is how we at HfS Research are designing our future research agenda – but more on that later!

Disclaimer: I am a firm believer in the value and concept of GBS. My sole objective of this post is to make it more human.

Our industry requires a shift in mindset from providers, buyers, AND investors. We need to rethink shareholder value and the integral link it has with the very element it seems to be bent on eliminating – people. In a thought-provoking post, my colleague Phil Fersht called out the fact we are in the people elimination business, wondering how it got so bad. My take: there are two key aspects in this debate; the way we view talent and the (unintended) consequences of decades of shareholder value doctrine.

The importance of talent for the future of services

Buyers need to deal with their cost reduction obsession and recognize talent is still the differentiating factor for their business success – and will be for the foreseeable future. Domain expertise, talent, and local people are critical components of the value service providers produce. This is true in any industry, but for example in oil & gas and the utility industry, the service providers that are perceived as delivering the most value by buyers are those that invest in talent, local people with deep industry expertise, and innovation prowess. These folks are not the cheapest, but bring exponentially more insight and impact on results. Buyers have shared ample examples of service providers that help them tackle the sticky industry problems by bringing the talents of industry experts, data scientists, technology experts and the client’s domain experts together. This teaming leads to multidisciplinary cross-pollination to design and deliver solutions that combine technology, industrial process and ideas and proven concepts from other industries.

We are on the verge of a shift in the way we work, and the outcomes we produce

The future value delivered by the outsourcing industry won’t be people running the accounts payable process, but in knowledge-intensive, decision-rich processes. You need the talent to make the technology work effectively – to drive the results and business outcomes. If we again look at the oil and gas and utility industry, organizations are starting to recognize the talent they need to compete in the new economy aren’t smitten with the work and reputations of the oil & gas industry or utilities. The reality is that the competition for data scientists, for instance, is not Shell versus Exxon Mobil, but Exxon Mobil versus the likes of Apple, Google, Facebook and a host of start-ups. Service providers can offer more interesting career paths and are a source of talent that can plug the quantitative and qualitative skills gap these industries face. Long story short; focusing on talent, continuous education and business value creation is the viable path forward for service providers.

The creed of shareholder value and its disconnect from reality

Too many people are still worshipping the totem of shareholder value, a theoretic and flawed notion from its conception. We are in a slow transition to more stakeholder value focus, more fitting our interdependent world that needs more cohesion and inclusiveness.

Ever since the invention of the term shareholder value, it was adopted as the dominant discourse by Wall Street and institutional investors. It, among other factors, has led to a short-term, myopic circus that reduces the horizon of executives to 90 days, de-humanizing our enterprises. It’s a fact that we are richer than ever before and there is less sickness, famine, and war (you wouldn’t say it if you watch the news). But there are still large swaths of the world struggling to improve the standard of living. And even in the world’s richest countries, large groups of people don’t feel better off. They feel left behind, disenfranchised and powerless. This is about half the population in countries like the US, the UK and France, evidence Brexit, Trump and Marine Le Pen’s rise.

We need to go full circle on shareholder value Coming back to shareholder value; it’s time to go full circle. Take a minute to think who is behind the vast pools of capital institutional investors manage… It’s us, the people saving money for their pensions. Shareholder value is a construct that served the money managing industry well but forgot to look at the wider interests of the actual owners of the money…. those shareholders are also your employees. Shareholders are not the clever folks on Wall Street, they are the representatives of the ‘normal people’ in your neighborhood and your company, the people who save their money in a pension fund or 401k.

If you take a narrow interpretation of ‘fiduciary duty,’ you can get away with the fallacy that returns on investment is the only metric of interest. But what if you fail to let that money you invest create prosperity for the people you invest it for in their real life? If your addiction to dividends and higher share prices is ruining the jobs of your future beneficiaries? It is time to bring the financial economy and the real economy closer together.

We can’t ignore the externalities of business any longer. People elimination is one of the challenging externalities that is a short-term lever executive in our industry seem to see as the inevitable answer to competitive pressures and new technologies (RPA, AI).

The Bottom Line – Taking social responsibility seriously is a critical and foundational aspect of doing business anno 2017

Only ten years ago, when I was doing research about investment preferences of pension fund beneficiaries and their ability to influence pension fund investment policy, corporate social responsibility and socially responsible investing were a theoretic discussion, often painted as the domain of idealistic, money-hating tree huggers. Not anymore. Since the 2008 financial crisis, everyone understands CSR is a real thing, a source of durable value creation, competitive advantage and not a fad you only use as window dressing. CSR has come a long way since. It’s time for service providers and buyers, along with governments, to come up with credible policies to make sure talent is up for the new tasks at hand, to truly augment people with the new technologies instead of using this as an excuse for the next round of layoffs.

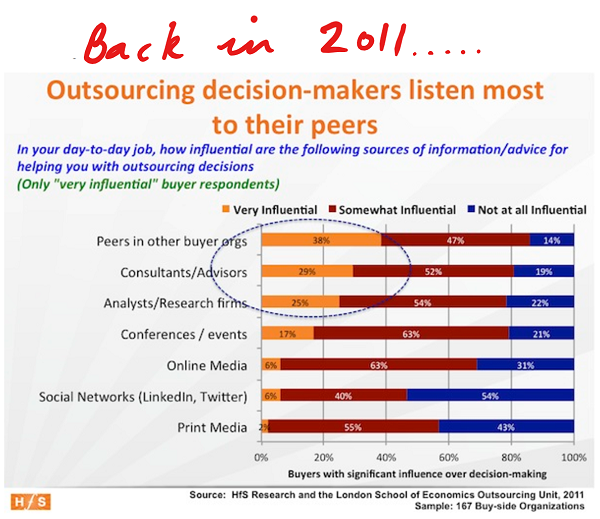

Remember when sourcing advisors has become the “new analysts” and dominated so many outsourcing discussions? Remember when it was the norm for clients to bring in the sourcing specialists whenever they needed a deal done, not only to get a good price, but also to make sure they selected the right partner and had a strategic view of the future? Remember when most advisors were not only contract experts, they were also strategists, researchers, sounding boards and respected brands you could hang your hat on… Just look at our 2011 study when advisors lorded the influence over everyone bar direct peer feedback:

Fast forward to today, with all the sourcing advisors doubling-down in RPA to compensate for the drying up outsourcing deals and confidently hoping their outsourcing clients will immediately turn to them to help them grapple with the new outsourcing-cum-automation model. Surely their ability to craft deals for clients will put them in pole position to take their clients down the RPA path…

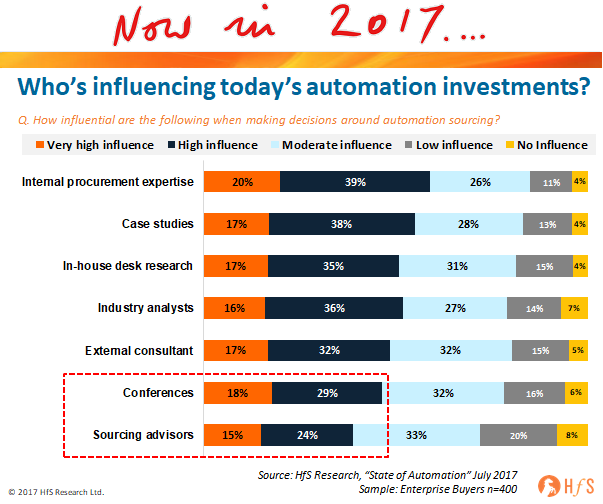

Let’s visit our brand new (still-in-the-field) study on the 2017 State of Automation, and it’s telling us a very different story when we spoke with 56 enterprises actually deploying RPA:

Less than half the RPA buyers view either consultants of sourcing advisors as influential in their automation sourcing. Even conferences are impacting automation buyers more.

So what’s gone so wrong with advisors in automation?

Credibility. Suddenly many advisors who were previously hawking their deep understanding of HCL versus TCS’s FTE rate cards are now suddenly adding their names to white papers on automation and trying to insert themselves into serious client conversations about said topic. It’s just not credible.

Smarter clients. The swirl of information over social channels is so intense these days that most clients’ knowledge isn’t that far behind the experts. In many cases, you’ll learn more about RPA talking with a client in beta mode than an advisor or analyst trying to impress you at a conference. That is why internal channels, such as procurement and plain old desk research is such an influence factor these days.

Archaic focus on headcount reduction. Just because you could create simple cases for headcount reduction with “take the people” outsourcing, doesn’t mean you can deploy the same draconian strategy to automation. Even the most clueless governance executive knows you can just fire people before you programmed some manual activities into a piece of software. Sure, there are serious productivity gain to be gleaned over time through the digitization of manual processes, but to tie this to immediate headcount takeout just doesn’t work.

Competition from service providers. For the first time, sourcing advisors and service providers are going head to head, and automation is the promoter of the fight. When clients want to understand RPA and a partner so help them roll it out, they need people who are in the game for the long haul, not a broker to dip in and out and get a deal done. Many of the sourcing advisors are just not transformation people – they are great at helping clients plan their outsourcing weddings, but marriage guidance councilors they truly are not. Service providers depend on long-term, complex and often messy relationships to keep them employed and busy… and RPA really fits the bill. While it poses significant threats to their margins over the long term, they cannot afford to be not playing in the automation game. What’s more, most the BPO service providers are rapidly running RPA in their own delivery organizations, which is giving them the experience and lower cost base to be effective.

The traditional consulting model doesn’t work with RPA. The advisors are struggling to scale up talent bases that can understand the technology and deal with the considerable change management tensions within their clients. RPA is murky and complex, and not something you can train bus loads of 28-year-old MBAs to master overnight. Meanwhile, we are seeing some advisors simply do some brokering of RPA software deals for small fees, only to make a hasty exit from the client as they do not have the expertise to roll-out effective implementation and change management programs.

RPA specialist consultants few and far between. Pure-play RPA advisors are explaining this is not quite so easy and requires a lot more of a centralized, concise strategy. There are simply not enough of these firms in the market, especially with Genfour having been snapped up recently by Accenture. With only a small handful of boutique specialists to go around, these firms can pick and choose their clients and command high rates. Quality RPA advisory boutiques, such as Symphony Ventures, are literally turning business away as they cannot scale fast enough to cope with the demand.

Advisors are not producing research. There’s a reason why procurement folks, analysts and simple desk work actually sit above advisors in the new data – clients want product specific benchmarks and real experienced advice that they are simply not getting from the advisors. All the advisors are putting out is the same of tired “drama” about robots replacing workers, and how to think “strategically” about RPA. While I like some of the stuff I see coming out of the likes of McKinsey, KPMG and EY, it’s just not giving me the real deal about which RPA vendor I need to be working with, how these tools truly stack up against each other and how I can actually build a bloodybot. That is why many clients are getting more reality from attending a conference than the lovely lunch they just got bought from their nice friendly consulting partner.

Turgid, hackneyed marketing doesn’t work anymore. Cheesy pictures of robots and the same endless stream of 300-foot view puff that sounds just like the last piece you read on LinkedIn by some weird dude who you can’t actually recall allowing into your network, isn’t helping matters. These advisors are relying on their brand and past reputation for credibility in a world where clients want to see some meat on the bones.

The Bottom-line: Advisors need a vastly different approach to automation to avoid complete irrelevance in this market

This industry has literally entered into a destructive war over automation, and the need for credible, independent and experienced advice has never been so in demand from customers. The skills to make automation a feasible profitable reality are few and far between, while greedy corporate leaders demand cost savings that simply are not achievable if their organizations fail to make the necessary investments and partnerships. Did companies become world class at HR overnight because they bought an expensive Workday subscription? Or stellar at sales and marketing because they slammed in a Salesforce suite? So why should they become amazing at cost-driven automation simply because they went and bought some licenses from an RPA vendor promising bot farms and virtual labor forces?

RPA and Intelligent Automation have sparked a major war in the worlds of outsourcing and operations, where many battles are being fought – and the winners will be those who are in this for the long haul, who can absorb some short-term pain in order to benefit from the larger spoils further down the road. While automation is killing outsourcing today – costing many people their jobs, their reputations and destroying the profitability of legacy engagements, those who can hunker down, focus on self-contained projects where they can fix one broken process at a time, can get stakeholders onside by demonstrating meaningful, impactful outcomes without major resource investments, will be the winners.

Advisors who can win out are those who can take their clients through this journey – one process chain at a time, evaluating all the right solutions and developing milestones that are realistic. Sadly the easy gigs where you could roll out of bed for a couple of million in billings are now extinct. The key is to play the long game, invest in the new skills you need to be truly credible in this market, and produce credible research that gets down and dirty in the weeds, not that 300 ft helicopter view that everyone’s heard over and over again…

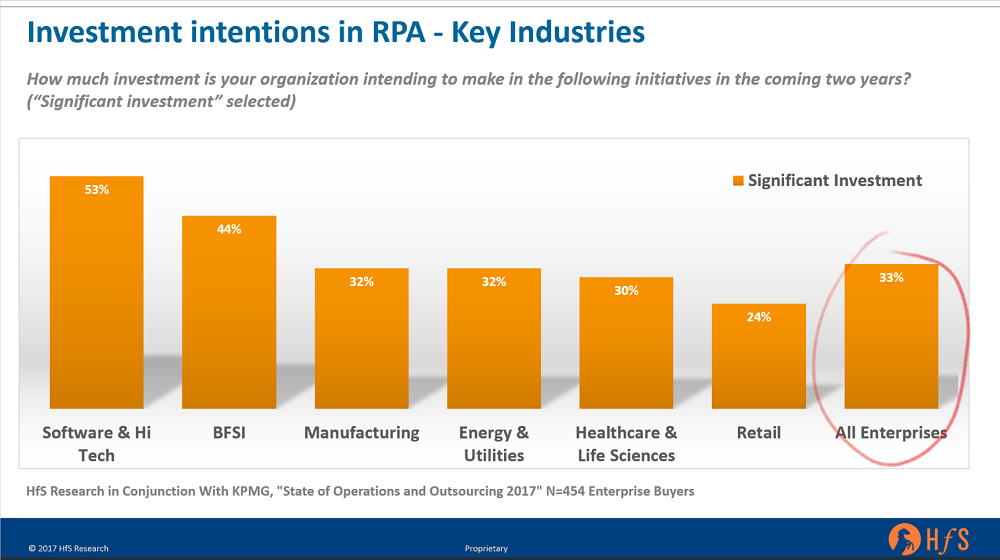

Tired of the RPA hyperbole? Well, you’d better get used to it continuing, as key industries have already made significant short-medium term commitments:

Our 2017 State of Operations and Outsourcing study with KPMG, covering 454 major enterprises, shows the hi-tech and financial services industries leading the way with, respectively, 53% and 44% already making significant investments in RPA over the next couple of years. Only retail falls below 30%, which may be a result of highly distributed organizations finding it if challenging to find high-throughput, high-intensity process where there is real tangible ROI for the investment.

The Bottom-line: The more digital your firm need to be, the greater the onus on digitizing and automating your manual processes

Quite simply, you can’t be an effective digital organization if you don’t have your manual processes digitized and automated. That’s what RPA does. All software and hi-tech firms have to transact their services over digital channels, and most tend to be further along the change curve when it comes to automation. Net-net, hi-tech’s DNA is all about automation, so having a digitized back-end just fits with how they view the world. For banks, these companies are plagued by manual processes and many have taken the plunge in recent years with large RPA teams to help them meet compliance deadlines and standards – almost every major bank has an RPA story unfolding. Insurance is catching up too, especially those with archaic claims processing workflows. Moreover, many insurers were among the first to exploit offshoring over the last 10-15 years, and moving along an RPA path is a natural progression for many of them. Energy and utility firms are all about cost control these days, while healthcare orgs are among the most backward when it comes to legacy technology and process. As patient care moves into the digital era, the need to digitize those manual records has never been more dire.

However which way we look at it, RPA is on a major growth trajectory… our forecast may be too conservative, but we believe many organizations will be surprised at how much time it will take to get their act together to adopt RPA in the right way. However, the newbies should be able to learn from the pain of the early adopters to move along the RPA adoption cycle faster.