Adjusters have traditionally been a critical part of claims handling… but can their role be eliminated today? With the combined use of modern technologies, field operations and remote analysis, it is now possible to radically redefine the entire claims workflow and get better results. As the processes get smarter, the traditional roles and responsibilities of adjusters also stand to be fundamentally changed. Genpact made an acquisition announcement today that gives it the potential to play a role in this transformation. Genpact bought Massachusetts based OnSource, a property, scene, and vehicle inspection specialist that has an insurance client base in the US.

Insurance carriers in the property and casualty market have a complicated relationship with their internal and independent appraisers and adjusters, resulting in a complex, lengthy and costly process to appraise the property and settle claims. The main scenarios where carriers feel the resource crunch include:

Catastrophe claims and adjusting are arguably the most distressing, where thousands of adjusters will spend weeks investigating affected regions. Not only is the damage inspection time consuming, it is often hazardous, as property inspectors need to brave floods, ice storms and worse to get the job done. This is where drone image capturing is starting to play a huge role.

Similarly, drones can be used for appraisals in large commercial properties such as factories that need a significant time to inspect in-person. This is an area where OnSource has combined drone image capture with 3D image rendering.

Auto insurance needs separate triage outlets for the higher volume of small, non-complex claims. Often, carriers club appraisal efforts for all exposure types, and end up hiring expensive independent appraisers to supplement their teams for these small claims. This is another area of focus for OnSource, which offers a self-service photo-taking app for customers to submit their data through their smartphones.

Onsource’s model allows carriers to customize the level of physical/digital connectedness in the process, as it not only offers the self-service app and drone options, but also a field inspection team and a “screen-sharing” type of virtual inspection service. The likely implications for a carrier, with a partner like OnSource is that the carrier can maintain a leaner appraisal and adjuster staff, rely less on external help, undertake more desk-based evaluations, provide more self-service options for customers and potentially create more straight-through processing for certain exposure types. Thinking about the future of appraisers and adjusters, we don’t see the roles disappearing, but they will be significantly altered. You will always need teams to undertake special investigations, liaise with intermediaries, customers, and witnesses, etc. What will change is the nature of work for some, e.g. not all appraisers will want to move from field ops to desk-based writing.

What is interesting is the possibility of what Genpact as a large-scale insurance operations partner can start to offer with the addition of OnSource. This is yet another example of a service provider who is thinking beyond legacy “BPO”. Taking a step back and evaluating the entire value chain of processes and service experiences, instead of just decoupling tasks that can be done offshore/offsite. The insurance business process services industry is so mature at this point, that we are staring at this step-change in roles for service providers. Who can help carriers with the messy “feet on the street” work that takes up so much time and resources and exorbitant costs to orchestrate the evaluations done by underwriters, adjusters and appraisers? Helping prepare underwriting case files, pulling information together using remote teams has some benefit, and was the story so far. Most providers hadn’t touched claims adjudication, and work around the processing and settlement areas instead. This acquisition follows similar moves made by competitors such as EXL that acquired underwriting support specialist Overland Solutions a few years ago (read our analysis here). Genpact faces tremendous competitive pressure from its closest peers such as EXL and needed to create more differentiation in a fairly commoditized market. What is different with OnSource is that Genpact is not just taking more ownership of the process value chain, but doing so in a forward-thinking way, using modern technologies to simplify the work and the experience itself for all parties involved.

We will continue to observe how Genpact leverages OnSource’s capabilities in coming months. The acquisition is part of Genpact’s strategy to provide more “end-to-end” solutions in insurance, in particular, in P&C claims. It has already acquired claims adjudication and support services capability with the addition of BrightClaim and National Vendor in the last year. Genpact is challenged in integrating all these capabilities together, as acquisitions haven’t been its strongest suit in the past. Further, the service provider will need to put significant focus on shifting its go-to-market strategy for insurance. Blending these additional capabilities will require Genpact to really move away from labor-based commercial constructs, which constitute more than half its insurance business today. Even if it does reorient internally to offer more business outcome-based models for claims adjudication, Genpact will need to recreate its perception, particularly for existing clients that see the provider primarily as a partner for backoffice processing. Overcoming these challenges is part of the solution to long-term growth for Genpact and all of its competitors in insurance operations. OnSource is a great start, as it brings more to the table by means of technology enablement in the claims management process, with the potential for better customer experiences that the P&C market so desperately needs.

There is only one Steve Rudderham (thank the Lord). One of the most traveled and fun guys in the world of operations and services over the last 15 years, who’s managed to somehow lead major BPO operations for leading service providers in both India and Latin America, run service delivery centers across the southern parts of the United States, before winding his way to the lovely Kalamazoo Michigan, where he today is devising the next phase of global business services for the Kellogg Company. And all this having grown up in the small cathedral town of Lincoln in the English East Midlands. So let’s pin Steve down for a little while to find out what he’s up to and where the world of global business services is taking us…

Phil Fersht, CEO, Chief Analyst, HfS Research: Good morning Steve, it’s great to have you on HfS for the first time. You’ve had a colorful career in and around the process and operations world, can you give us a very quick run-down of where you came from and how you got to where you are with Kelloggs today?

Steve Rudderham, VP Global Business Services:Absolutely, I grew up in GE Lighting in the UK, 17 years ago I moved over to Kansas, US, to work in their Insurance business. Started off within process excellence, I was a black belt there, then went over to India to run their back office operations for what is now Genpact. I moved over to Genpact to run Latin America. I’ve also had terms with CapGemini running the Americas then more recently within Accenture doing Finance and Accounting globally for them as their product lead. I now run the global business services for Kelloggs.

Phil:How do you feel about being client side, having spent so long on the other side?

Steve: It’s been very interesting coming over to the buyer side. I think the advantage I have is that I come with a lot of knowledge of what’s available and the best practices. I also have insight into what the providers have been doing for other companies, not just within the food industry, but outside as well. If you think about Accenture, they are very strong within oil and gas, you can bring a lot of best practices over and into Kelloggs. It is slightly different in that you don’t have multiple clients that you are looking after, you have your internal clients, but the focus is within one company and it’s a mixture of internal staff and leveraging third party providers.

Phil: The industry has been through quite a few inflection points in the last few decades, are we really going through another one, or do you think this is a product of too much hype and rhetoric on social media and conference topics?

Steve: I think the difficulty, from a client perspective, is how you get through that hype, there are a lot of conferences around and social media is driving a lot of content as well, people want to be out there talking about what is going on in the digital environment and automation and AI. The key is to understand what is real, and how you apply that to the global business services I run – that’s the difficult piece.

Phil: Coming at it from the client perspective is there a burning platform in our own environment to jump on RPA, digital and more technology based solutions. Is it something that has a strong velocity behind it, or is it more exploratory at this point?

Steve: For automation and cognitive computing there is a lot of exploratory work taking place. To answer your question around the hype – we hear a lot of how other businesses are doing it, for us, it’s how do we leverage that best within Kelloggs. We are similar to a lot of organizations, we have a lot of transactional processes, as well as the higher value ones. We want to be spending our time on the higher value pieces. We are exploring where we can leverage automation to drive accuracy. If you consider an order to cash process, we want to be spending our time at the front end with the customers developing those relationships, not spending the time working out how we code deductions when they come in. This will be automated to drive accuracy and then we can spend our time elsewhere.

Phil: Do you think this current state of hype is the new normal, or are we going through a transition period as people get more knowledgeable about what is out there, and everyone becomes an expert in everything?

Steve: it will be interesting to see how fast people can get up to speed. I don’t think it’s just this industry – you touched on earlier – social media as a phenomenon is driving a lot of content out there – it’s driving a lot of knowledge as well. Often you are spending the time trying to see the wood from the trees, how do you actually know what’s real? I think it’s the social media environment we live in – how do you get to the information that is relevant to you, in a timely manner.

Phil:For you personally having spent time at Genpact, Capgemini and Accenture, going over to the client side and getting stuck in with lots of your colleagues and very experienced GBS shared services professionals, what advice would you give to service providers on what they are doing wrong and what they could do better? What are they doing well as they look at what is facing them in the next 6-12 months?

Steve: I think within the client side there is definitely a hunger for information. The data analytic side is very important if the providers can show the value with that, but I am always asked for where companies have had successful implementations on innovation. If a provider can show examples, then connect people with references in those companies that you can talk to, this will result in a comfort feel that you are not necessarily the first and innovative partner, and a sense of safety in that it has been tried before, it is an approved process and we can go after it in a very timely manner. On innovation, the data analytics and bringing the examples through, regardless of whether that is analytics, RPA, cognitive computing etc, if they get that right it’s a much more powerful selling proposal.

Phil: There has been some debate in the industry – “Is there an obsession about companies scaling themselves on a technology backbone as opposed to a talent backbone?” Do you think this is a potentially damaging time and what advice would you give to your fellow professionals who may be feeling uncomfortable at the moment?

Steve: Going back to the comment around the hype, organizations are trying to understand what they can leverage on the technology side v’s the people side. You’re always going to want your people to do the higher value work as much as possible, but without a completely clear road map of how you get there from the providers and from the industry, that makes it difficult. I think that some of the clarity we need, certainly as a buyer and a consumer organization, is what is real, what can I leverage and where can I focus my people and my resources on. Technology is obviously an enabler for us to drive the improvements, but to what degree we use is still in the exploratory phase.

With regards to your second point, I don’t know if there is a focus away from talent. Technology gives us an opportunity to develop our talent a lot more. You are getting people to do the higher value work as well. If you have organizations that are looking to leverage the technology you have to get with advisory groups or providers that cut through all the smoke and mirrors. That comes back to my comment about best practices, examples and references, the more you can bring the more comfort client organizations are going to have.

Phil: As you look at the future for service providers there is a lot of pressure to maintain margins and growth. Do you think there’s enough business for them to keep solvent at this pace? What do you think will happen to service providers in the next couple of years?

Steve:Service providers in the last few years have spoken about innovation, what they can bring to a client, This has to be stepped up on the client side and I’d be more than happy to look at gain share models. We have been talking about gain share models on business outcomes for a long time, but I still don’t see a lot of them. Service providers seem to be a lot more comfortable talking about consultancy rates, hourly, or project costs, etc. I think for service providers to have skin in the game and they must really drive a true gain share model, I think that will gain the client interest. That’s certainly where I’d like to see them and see some growth of their own.

Phil: What do you think will happen to RPA software companies that have sprung up recently? Will they continue to be the flavor of the month, or do you think that industry is in for a rude awakening in the short to medium term?

Steve: Depending on how innovative and disruptive they are, I can certainly see some of the big BPO providers buying into that talent, so you will see a concentration of the RPA providers. The big 4 BPO providers have each got their own RPA arm. I think it’s very fragmented at the moment, but I see some consolidation ahead.

Phil:You think the BPO’s are going to become the services arm, more than the advisers and the big 4 at this point?

Steve:I think they are going to want to drive to that, yes.

Phil: Finally, you have been in and around the industry a while now, if you were crowned the Emperor of the Service Industry for one week, what one change would you implement to make this industry a better place?

Steve: Emperor for a week? That’s dangerous, I think getting to this clarity of what is out there and what is real. What people can say v’s what you can actually get. What is the true value that service providers can deliver. That would certainly get the client side more comfortable with the service industry. Being able to put out very clear benchmarks, what’s being delivered, being very transparent, that would be what I would push for.

Phil:How well is Lincoln City going to do next season, back in the football league?

Steve: Interestingly it’s a 10,000 seater stadium, they have sold 6,000 season tickets, 2,000 for the away supporters and I think about 1,500 junior tickets it’s almost a sell out every game now. So the City is definitely excited about it. If they can hold on to the players, I think it could be good season, there’s a lot of optimism.

Phil:Well let’s hope those Imps have a decent run at it! Cheers, Steve!

There’s nothing worse than being the “best-kept secret” in an industry… sure, it sounds cute at first, but after a while it gets frustrating as people aren’t learning about you. And there’s nothing worse than being a best-kept robo secret in a market obsessed with propaganda, ignorance and bad analysts, many of whom have no clue what they are talking about.

So let’s change this for one solution vendor, Redwood Software, which has quietly gone about helping enterprises automate processes around SAP workflows. When we bemoan rigid, poorly integrated processes, it’s often borne out of legacy systems and ERP that have the effect of pouring concrete into a firm’s operations. So what better than to develop both robotic and digital automation capabilities around SAP’s R3 finance platform, helping financial leaders renovate more of that they have, without the costly and disruptive need to invest millions in expensive system upgrades that often only succeed in delivering a whole new suite of integration problems. Sounds like a simple way to make money? Well, it actually takes decades of practice and experience, so let’s hear a bit more from the firm’s CEO and Founder, Tijl Vuyk. and his Chief of Staff, Neil Kinson, about how they got here and where they are taking this very well-kept, soon-not-to-be so secret Redwood product…

Phil Fersht, CEO and Chief Analyst, HfS Research: Good morning Tijl and Neil – it’s great to have both of you talking to us today. Perhaps we can start with a little background on Redwood, where you have come from and what you do?

Tijl Vuyk, CEO and Founder, Redwood (pictured left): Thanks Phil. Well it’s been about 25 years since we were founded and we started in the application space where we were building Oracle applications. We saw the need for automating these applications because there were a considerable amount of manual activities running all kinds of processes within Oracle, and later on with SAP. When we started, we created a tool that would help customers build their own automated processes. In the last five to eight years we discovered that building these automations were a challenge for many of our customers. So we tried to productize the whole idea of automating these business processes and now we call this robotics – where we use the application’s functions to automate the processes normally undertaken by humans. I think that’s where we are. We came from a technology background where we built enterprise strength applications to automate primary business processes, and now we are trying to make this as easy and slick as possible to implement those processes without having customers spend too much money on services and maintenance. There is more to say about what we do, but these are the highlights.

Phil: Sure, so you’ve been around for 25 years, how did you end up in this automation space? Was it a deliberate move or was it something that evolved over time?

Tijl: I wouldn’t say a deliberate move but I love automation. If I do something twice, I ask myself, “can I do this easier and faster or not do it at all?” And that is the attitude we have towards automation. We automate everything we can. When you see customers struggling to get things done because there are so many manual tasks, you ask yourself “can we do this better?” And yes, we can. It’s a mentality thing – you want to find better solutions that help you achieve those goals.

Phil: We hear a lot about companies like Blue Prism and UiPath, Automation Anywhere, Kofax and a few others. But you seem to be doing a lot more than just RPA basics for clients. Why would you say Redwood is different?

Tijl: I think it’s our heritage that makes us different and our approach to automation. Our heritage is around enterprise systems automation where you cannot afford any timeout. If the process stops our companies no longer operate. That’s the kind of environment we come from – enterprise class software for customers that have enormous demands, where RPA vendors are screen scrapers and you can give them any name you want, but they work through the user interface which is not really a solid basis from which to build automation.

If you think of business critical processes where failure as ‘not an option’, then basic RPA is not a solution. Only instances where failure is ‘not a problem’ (i.e it is not mission critical) is this basic RPA capability applicable. But if you are looking to replace people with automation then something you should ask yourself is “what happens if the robot stops working? If I don’t have those people anymore to do the work manually?” The feedback I get from RPA customers is that the robots do fail, and you ask what they then do, and of course, they rely on humans to take over.

At Redwood we look at process automation differently and if we automate processes then we automate them one hundred percent or as close to that as we can get. And they always run. There is no issue with our technology, it is more stable than anything. I think our customers sometimes forget it is there because it’s so efficient. If you talk to our references, there is also little or no maintenance required on the robots. That’s the big difference. It is basically the lower cost of the ownership, elimination of the risks involved in running a robotized enterprise and our approach to these problems.

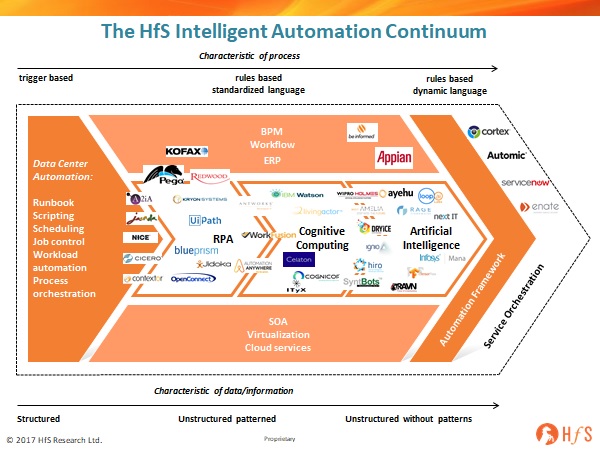

Phil: I think in the early days of this recent surge in automation when we started talking about the RPA concept, we talked a lot about the intelligent automation continuum, where enterprises could start with rudimentary RPA then gravitate to more mature automation. They could start automating the automation and evolve to a cognitive, then eventually an AI strategy. Do you think this is still a logical progression, or do you think clients can now experiment with all facets of the continuum at any time? How do you see this truly evolving in your experience?

Tijl: I think you are mixing up a couple of items. I think the role of AI, if it exists is maybe a step in the process. It is not ‘The process’. You will not have any AI that will do the accounting for you for example. AI is used in pattern recognition in some form. When the pattern is recognized it kicks off a process that can do whatever it wants. But all these processes are more or less set. AI will play a role in a step of the process. If you think “oh I am going to delve a little bit in automation” then you are destined to fail. What we see is that if automation is not put on the agenda at the executive level then it becomes just one project silo and then it stops. I think automation is a way of life, you need to give it constant attention because it is not over until everything is automated. But then business might change. So for me, it’s really about continuously automating and looking for the next thing to automate.

At the moment people run a project and they stop because the project is finished and they don’t continue with the next project or expand the current footprint. I think that is the biggest danger to the success of this idea of automation or robotization. If you start out with the wrong tool then basically you start out with the wrong foundation for future development. We have a more holistic view on the approach. We want to create an environment where people can automate at an enterprise level and don’t get dragged down by the cost of maintaining and keeping things running. It needs to be low cost, easy to get started, efficient automation.

Phil: Tijl, there’s been a lot of hype about job elimination in the industry. When we look at the operations business that I’ve come from – BPO outsourcing, shared services, captives etc. – we have essentially grown up on efficiency and cost reduction, and as much as we hate to admit it, that’s been the core of our industry for the last couple of decades. Do you think that the emerging concept of automation is going to move the conversation to more about business value, or do you think we are perennially stuck in a cost reduction job elimination scenario?

Tijl:I think that outsourcing is a mistake and automation is the way to fix that mistake. What happens when you outsource is that you lose control. You think you give the control to someone who does your menial jobs. But then people have the upper hand because you are dependent on them.

If you eliminate all your outsourcers, by automation, you gain full control of your processes and full flexibility whilst saving cost. For me, automation is a way to regain control of your primary business processes, whilst making them more efficient, more flexible and more supportive of the business instead of being dragged down by an outsourcer, and a long contract that is designed to make things difficult.

We have seen customers building these “hells” as they call them. They have created hell and now have to live with it. I think automation is a way to reverse the wrong decision of ten years ago and yes there is significant value beyond only cost reduction.

Phil: Looking into your crystal ball and thinking about where we have come from, the current state of the market and all the noise and conversation that we are hearing today – what do you honestly think we will be talking about, and where do you see the industry in three years time?

Tijl: This is where I like to introduce you to my crystal ball reader, Neil…

Neil Kinson, Chief of Staff, Redwood:Thanks Tijl – ‘Mystic Neil’ here…. we’ve talked a little bit about the dream of The Robotic Enterprise and if you think of a parallel in industries that are being disrupted effectively you see the notion of people doing repetitive mundane manual activities in a back office. This should be as unusual and as unthinkable as it is today to going into a shop to pick up a DVD or a video. My kids wouldn’t understand the idea that you actually drive somewhere, pick up a DVD, watch it, take it back – or take it back late and get a fine. You know that’s an industry that grew up and disappeared in 25-30 years. So is it three years? Probably not Phil. Probably longer than that. But you know that’s certainly the vision – we will see some organizations where that notion is frankly ridiculous and when you think about it in 2017, when you see hundreds and thousands of people doing activities that you can’t believe people still do today. Well that is something you see in the back offices of some of the world’s largest enterprises. So as we look into the crystal ball we see that changing and we see ourselves playing a big role in making that change.

Phil: Okay. This has been a good conversation, but I’d like to pose one final question about what you would ideally like to see change in this industry. If you had one desire that could change attitudes or focus in this industry, what would it be? What would you change to make your customers, partners, and competitors all think differently about the way we are looking at automation today?

Neil:The key thing for me is where is your ambition? If your ambition is to get marginally and organically better than automating a few arms, legs, fingers and toes in terms of driving out change then that’s fine. But if you really want to check the future of your organization by being truly world class and reinvesting in serving your customer, not through an automated agent, but actually through real people who are passionate about the success of their customer, then focus on that. Focus on the end-to-end, on what you are trying to achieve and how you can achieve that rather than building and just employing bots for the sake of it. I often hear the term ‘Center of Excellence’, which when you drill into it is actually a ‘Center of Expense’. Because people are moving the cost from one area to another and you are actually moving people who are experts in executing the process into experts into how do they deal with a situation when a robot fails.

That doesn’t improve customer intimacy. That doesn’t drive you towards continuous process improvement, and that doesn’t help you serve your customers better. Yes, it drives out some operational cost. But let’s take a step back and look at the end-to-end process. How can you improve the quality? How does that fit with your sourcing strategy and staffing strategy over the next ten years. You know you need to raise the level of ambition and you won’t get that truly by dabbling and saying “yes I’ve done robotics” or “we are looking at robotics .. we must buy some”.

Too many people are approaching this from the point of view “this is something we need to do”, not from the point of view “this is the outcome that we are looking to achieve within.”

Phil: Okay. A very good answer! Many thanks Tijl and Neil. I really appreciate your time today and I look forward to sharing our conversation with the HfS audience.

As the fog slowly lifts from our beleaguered world of operations, we can start to put the pieces together regarding where we truly are, when it comes to building the backbone for successful businesses of the present and the future:

No – not all our firms have been wiped out overnight by disruptive digital competitors (sorry all you hypesters who’ve been beating that drum, but most our ‘legacy’ firms are doing just fine).

No – not all of us have been replaced by robotic software that can mimic our rote behavior and render us useless (if only more customers will actually admit they are finding RPA a lot more challenging than they thought).

No – outsourcing isn’t dead, it’s just under pressure from commoditizing services, too many competitive service providers, greater global location choice and the emergence of specialist niche firms, which can do complex work at a much smaller scale than our juggernaut firms can afford to deliver.

In short, our enterprises are caught between innovation and renovation, where they need to make the most out of what they have, while making the shrewd investments in the innovation the need to stay relevant in their markets. So with whom better to chew the fat than a very old friend and great supporter of HfS over the years, Ian Maher, who’s been the dynamic busybody behind Hanover Insurance’s sourcing and operations activies over the last decade. You won’t meet many customer executives who deal with technology firms, automation vendors, outsourcing providers, procurement executives, HR, IT – you name it – and still always has a smile on his face. Maybe it’s his stubborn devotion to his under-achieving soccer team, Everton, which keeps the chap so positive and focused….

Phil Fersht, CEO and Chief Analyst, HfS Research:Good morning Ian. It’s great to catch up with you again. Could you tell HfS readers a little more about you and your background in the industry, where you’ve come from, and what you’re doing today?

Ian Maher, VP, Head of Sourcing, The Hanover Insurance Group: Phil, good morning, it’s great to catch up again. As you know, my background is on both sides of this interesting equation, from both a sales and a buy-side perspective. When I was originally in the UK, I spent the first decade of my career working for what is now Fujitsu. As the development of consulting services, on the back of technology solutions, I was fascinated by how firms created new revenue streams on the back of product sales. In the late ‘90s, I moved over to the States and joined Gartner. With roles, in account management support and financial services in the North East of the US, I then started to work more closely with the research leaders in Sourcing and especially BPO, spending a lot of time working with CIOs and similar leaders, helping them understand what was going on from the BPO point of view as it started to seep away from a technology space, into the realm of mainstream business decision makers.

One of my previous clients is the company I’m with today. I’ve been at Hanover for nearly 10 years. We are a growing P&C business, largely in the US but with a UK operation via our Lloyds of London syndicate. In this role, I look after a variety of functions, including, traditional procurement, contract risk and governance. But more interestingly, perhaps to me at least, is the role of trying to fix together how the ideas from the outside world can be brought to benefit, what is pretty much, a traditional insurance business. I’ve led a couple of major initiatives working with leadership about benefit realization from BPOs and in the last two years, really started to help familiarise and educate the organization as to the potential and perils of what we call Services Automation. In short, our venture into RPA, Cognitive and the step change function that Automation may offer operational excellence.

Today, I’m keeping the organization moving at a steady pace.

That’s the potted history and I’m speaking to you today from a very sunny Boston. So I’m happy about that.

Phil:Good for you. I think we’ve worked together as colleagues and friends for probably close to a decade, since you started at Hanover. You’ve been through a long process of educating your colleagues and stakeholders on the merits of BPO and I’ve observed you’ve become quite a mature adopter at Hanover over the years. Where is it all going now? Is it still the same type of value proposition that we were talking about three, four years ago? Or do you feel it’s really changing now, beyond recognition?

Ian:It’s interesting Phil. I sometimes think we jump to the next fad or area of excitement, and forget that at its very basic level a successful BPO program is, and should continue, to deliver massive benefits as long as it’s managed in the right way. It isn’t something that gets stale. We continue to reap major benefits economically, from a quality of service, which is really the primary driver and continues to be a point of differential with our agents and with our insureds. Caution should be taken not to throw away something, that while it’s sell-by-date might be fast approaching, it’s something that can still, year-on-year, give a consistency of service at a scalability of cost, and should be maintained.

We’re approaching 12 years in our relationship with our primary BPO provider, to support maybe 80 to 85 different functional areas across Hanover, and continue to deliver extremely well in a very, mature set of processes. Where is that relationship going? We’ve discussed how the BPO providers are moving towards the next evolution of service delivery and incorporating the digital aspect. I’m sure a part of me is a little bit frustrated, I would like to see the traditional pure-play BPO’s a little bit further along the path. But at the same time, I need to be confident that if they change their delivery model, I can still hold them accountable for both the people and the digital aspects of the solutions. I’m comfortable in biding my time a little bit as long as I get a 95% confidence level of the evolution of the BPO into this hybrid BPO, and its success. That’s probably where I am and what I’m saying to my senior leaders, don’t rush into something at a 40-50% confidence level.

Let’s make sure we get it right jointly. Let’s make sure that the vendor succeeds. Because if we fail, we fail jointly and there may not be a second chance in terms of going in the direction that we’re looking to go given the magnitude of impact of introducing automation into the delivery model.

Phil:It’s good to hear you talk about incremental change, at a pace that you’re comfortable with. We hear a lot of clients today and customers talk about, “Oh, my CFO just came back from another conference and apparently we have to find 40% cost saving through RPA, and we got to do it next week and we need a digital strategy.” Does your firm suffer from a lot of the startling new stats and new technology trends? Or do you feel you’re a bit more sceptical, at Hanover, as to the pace and the velocity with which things are moving?

Ian: No. You hit on the most common conversation I have, from a global business services or a shared services leadership point of view, there is no more important task than being a voice of reason, and often responding to CFOs latest airport lounge magazine article, in terms of what’s the marketing hype from the sell-side.

It is always possible to hit some unrealistic number in the short-term. But you’ll probably pay the cost through disruption or through a failure to really plan systematically for the next three to five years. Across the industry, and not just at Hanover, experiences of going through different delivery model changes can bring that realism to keep you ahead of the discussion. One of the things that I’m starting to take a lot of interest in, and I’m looking forward to discussing further at the HfS Summit in Chicago, is, are leaders ahead of the discussion or is the discussion ahead of them and they’re simply reacting to other senior leaders?

I think this is a great chance for the BPO leaders, the CPO’s, the SSO leaders to again reinforce value within their organization and to be ahead of these major changes. I’m interested in the views of the folks that are going to be in Chicago – where do they see themselves on the proactive vs reactive scale.

Phil: Yes, there was a lot of tension at a recent event we held in New York City, the stress levels between providers and their customers, have reached an all-time high. I think there is a lot of expectation on both sides and a lot of pressure on operations to really shift things along in many organizations. It’s interesting to hear what’s happening with Hanover. When we talk about a burning platform, you know insurance is an interesting industry. We’re looking very closely because there are a lot of disruptive competitors coming along, a lot of digitally driven insurance products and firms leaping into the space. Do you feel being in a more traditional firm like Hanover, there is more threat from digital disruption? Is this something you’re closely monitoring in terms of how you need to make a pivot? How are you viewing disruption in your space? Is it something that is changing your behavior when it comes to sourcing and operational relationships?

Ian: It really is and obviously my major area is the P&C side. I am vaguely aware of the Life and Health side as well. We are traditional, in so much as we still largely operate through a distribution channel of Insurance agents, because at the end of the day we’ve got a firm belief and understanding of the needs of the insured and this is best handled through a skilled individual – that’s our Agency channel. Clearly, we’ve got challenges within the industry. As companies can move into the insurance space with a fraction of the start-up or operational cost that we have, there is clearly a need to pay attention to those who are bringing in digital end-to-end solutions. We’re looking to build on the foundation of our value proposition, which includes intimacy of conversation and an understanding of “location”, and bringing in the smartest and most effective delivery model.

We typically see a progression through a legacy system being matured, and in some cases being replaced by package solutions. However, at the front end, what we’re starting to see is the widespread adoption of the digital based input processes, the submittal, the early inquiries and so on that come to us. They now typically come in with an expectation that a quote or description of the coverage areas, can be provided through any device, can be provided at any time of the day, can be provided without necessarily having to talk to somebody. So my focus is sourcing the enhancement of our sales activities as well as the delivery of operational services.

The other area that we’re seeing Phil, is clearly the development of certain products to actually take account of some of the emerging threats in the world of business. Most insurance companies, are looking at the development of cyber-related insurance products.

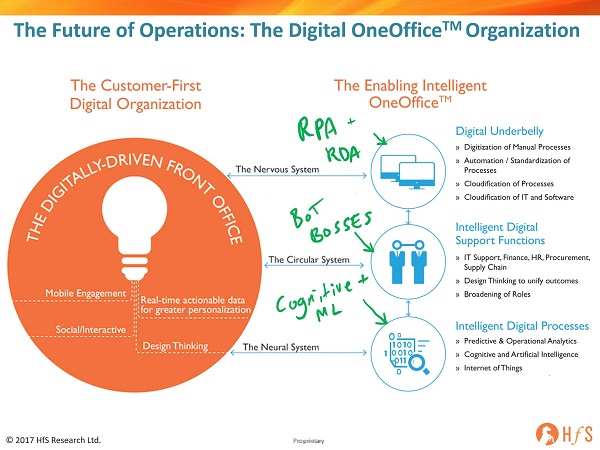

As we start to build those new products, we’re largely building them from a framework of digital first components. In the past, we have gone through a traditional underwriting compliance product development area. Most of us are more likely to look at a solution that’s a one-stop shop for underwriting in some of these interesting and extremely opportunistic areas for us to develop new products. I go back to my earlier question – is the sourcing leader involved in working with these types of solutions and integrating them into the portfolio of traditional BPO services? I think that typically sourcing leaders can bring in a rational and an understanding of how new vendors, new third-parties can be integrated into the bigger service offerings of the organizations that we represent. So definitely a change in mentality from back office through to front office differentiation, something akin to the HfS OneOffice vision.

Phil: It’s good to hear the evolution of your approach in this type of market as you look at your enabling support strategy, to be more flexible, nimble, scalable, cost effective with your delivery. One of the other analyst firms recently declared that 96% of clients trying RPA aren’t very happy. What’s been your experience? Are you one of the 4% or one of the 96%?

Ian: So we will refer to that “other firm” as, just as one of the others… I don’t think we’ve had enough time for anyone to judge happiness or success. I think we’re in the twilight of the first day of understanding just what the benefits or otherwise from the early ventures might be. Insurance is slightly a laggard as we don’t work in a real-time environment Phil, the wealth management and retail banking firms together with the micropayment functions are ahead of us in terms of benefits realization but we are starting to see how to deploy successfully, and how not to.

Our success, as opposed to happiness, has been in actually seeing from start to finish, the life cycle of Service Automation, including almost 10 to12 months of actual production environment. We’ve measurable results of a very, very key insurance process which has a minimum life cycle of a year because it’s involved with the market acquisition. I think the first sign of success is present but we won’t know for some time. I’m not in the camp of happiness, I’m in the camp of ‘enthusiastic observer’.

More than anything our success is about getting our organization ready for the next major initiative, as it is with the result of the first one. If your organization is primed and operating in an environment where the support services understand, articulate and are making the right commitments to plan for 2018/2019, I think that is success. But I don’t put that down to RPA. I put that down to good planning and leadership that we’re trying to bring to the organization.

Phil: We talk a lot about unlearning. You’ve been in a quite unique role as a sourcing lead, a governator type, for quite some time. Do you feel that you are learning new skills, new capabilities on the job and broadening your horizons? Or do you feel there is more of a defined curriculum here with everything that’s going on?

Ian:Well it’s a good question. I think in some ways the scope of what we try to do really hasn’t changed, but the pieces that we’re talking about clearly have.

From a sales background and now leading the buy-side, in many ways I’m part evangelist on behalf of the industry and some of the sales organizations, part pragmatist. I think that really hasn’t changed. The role that we play organizationally is about risk management, finance management and governance. But individually, I think you play a different role in terms of bringing the knowledge to the C-level that they require in order, to make decent decisions.

So from my own development, my ability to understand the ways of a changing C-suite is something that you’re never going to feel that you can take for granted. You go through the activity to establish and maintain relationships. You understand how the outside world forces changes in business direction for the senior leaders and you have to connect Sourcing to these changing needs. We’ve had the retirement of our CEO and the arrival of a new CEO with a very different outlook on the world. You need to be ahead of that individual thinking and bringing ideas as opposed to problems. Otherwise, you and your function that you look after might be relegated to a secondary position. In summary, while nothing has dramatically changed, you have to be consciously looking out and understanding and translating the marketing and the realities of the sale side. That is something we’re never going to be comfortable in saying that we’ve achieved, simply because the sell-side bring ideas at an ever faster rate.

Phil:We talk about the velocity of change and where things are shifting, when you look at your partnerships, with the other service partners in particular, would you say those are changing dramatically? Do you feel your current partners can innovate with you at the pace that you want to go with? Do you feel you constantly need to look out for new expertise and skills? How do you feel the service community is helping you get to where you need to get to?

Ian:I think I’m going to give a more general answer as opposed to a specific comment on my primary partner Phil. Knowing many of the folks in North America and a number in Europe as well, Many service providers have struggled somewhat with this reality of, “How do I protect my revenue but also generate future margin.” For some time I have been somewhat frustrated but also somewhat sympathetic to the business challenge that they’ve got. I’m not sure that I need to hold my primary BPO vendor to something that would cause them to act unnaturally or even put their capabilities in threat. I want to get a better deal clearly. I may want to get better quality but you have to figure out the solution together. I say that because I’m still going to hold my BPO partner accountable for both the digital and the non-digital delivery component. I’m not looking to change or reduce service levels. They’re only going to go up.

There is a degree of complexity, that you really have to think through on behalf of your vendor rather than just take a “two by four” and challenge them to take 60% of cost out. Because you’ll end up with an unbalanced and a somewhat immature solution. My wish though, and again I’m looking forward to speaking to some of the BPO vendors as well as the Automation vendors, is how well are they really teaming together not just to shift license, not just to get me to commit upfront, but to think through the reality of a deployment model including the HR aspects of workforce changes.

Providers need to think through a reality of a well built, highly efficient use of technology rather than just have a deploy bots that may just about meet a basic level of performance but fail to when integrated to the much bigger ecosystem of operations. The BPO providers need to take look at derivative rights solutions that combine technology and process knowledge into a reusable industry focused set of solutions. I’m surprised that this isn’t more widely talked about because your asset at the end of the day is your execution of your process. Whoever carves that out first and can create some competitive edge, maybe even protect that particular new product, I think has got a great opportunity to be competitive and more aggressive and go after other organizations traditional business areas. So a long answer but I think on the whole I’m a little bit more sympathetic in figuring the future out than I was.

Phil:That’s nice to hear. So you’ll go easy on everybody when you’re in Chicago in September I’m assuming, right?

Ian:I’m looking forward to the one-on-ones Phil, let me put it that way!!

Phil:And finally… what do you think about Wayne Rooney coming home to Everton?

Ian: Happy! A different player at 31 but will help galvanize the team. some very good signings so far, I’ll be doing nearly as many air miles as you this year, Phil

Phil: Excellent. I’m really looking forward to seeing you again. You’ve been a very good friend and supporter of HfS over the years and hopefully, you’ll get to meet many new folks in Chicago in a few weeks. Thank you very much for your time today Ian.

In a world of inflated hype around chatbots and where customer service interactions solutions claiming to be AI or cognitive are popping up at a feverish pace, it’s up to service providers to take a stance and articulate a strong value proposition. Most pure play contact center service providers don’t have much of a strategy for Intelligent Automation in general and in AI in particular. Many are exploring partnership options or allocating tiny budgets to develop their own chatbots and lower level machine learning tools. CSS Corp has decided to flex some muscle and use its own IP to develop a virtual assistant, “Yodaa,” claiming to be an AI tool capable of “human-like” interaction. Combining NLP and machine learning, the SaaS-based solution can be used as a standalone support interface across contact center channels or as a platform integrated with Amazon Echo, Apple Siri, Microsoft Cortana and Google Now. It also has the ability to understand customer intent and learn from its interactions. CSS Corp is piloting Yodaa across 3 clients and 1 client has already gone live with the virtual assistant.

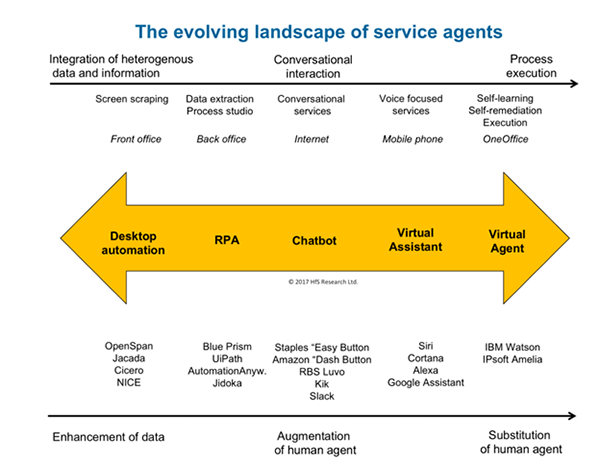

While the broader market gets excited about chatbots, the best way to discuss Yodaa’s capabilities is to look at the evolving landscape of service agents across a continuum (see graphic below) from more basic back office automation of processes all the way through to process execution on interactive channels. Without seeing specific use cases just yet, our best guess is that Yodaa falls somewhere on the spectrum between chatbots and virtual agents. It’s self-learning capabilities take it beyond the traditional bot to integrate with enterprise systems and learn from conversations, as well as combine both human and machine learning in what CSS Corp calls a “cotelligent” platform. Its multi-channel capabilities plus ability to integrate with existing consumer virtual assistants is another important feature. What remains to be seen is whether Yodaa’s capability extends to process execution the way that IBM’s Watson and IPSoft’s Amelia have demonstrated: to help front office professionals make better decisions with insightful, predictive data and analysis or routing customer requests to execution, or interact (in the case of Amelia) with some level of “emotional” intelligence.

Augmenting the agent experience: adding value to customer engagement

At the far right of the continuum, virtual agents are not only automating tasks to support the digitally-driven front office behind the scenes but also using cognitive intelligence to have meaningful, secure, and efficient interactions with customers. But, cutting through the hype, we’ve yet to see a virtual agent that really can replicate a true human interaction or execute processes the way a human can. IPSoft’s Amelia is the closest we’ve seen to be able to execute at a close to human capability.They’re getting more sophisticated, and ultimately these tools may replace some customer interactions, but not all. Ideally, virtual assistants and agents can help human agents do their jobs better to support the customer experience– by providing context and recommendations to agents, promoting more valuable interactions.This opens up the door for cross-selling and upsell opportunities, as well as promotes loyalty and satisfaction with customers, whereas lower level chatbots and automation simply replace repetitive tasks and automate basic functions without adding much value.

The Bottom Line: Virtual assistants have the potential to help transform the contact center if used correctly.

As Yodaa’s namesake famously said, “you must unlearn what you have learned.” Cognitive agents are not going to work well if they’re slapped on top of or inserted into broken and bad customer support processes. Customer service executives need to re-think and re-design the processes that contribute to customer experience across the board, which means “unlearning” bad habits, throwing away legacy thinking about “this is how we’ve always done it” to embrace making the contact center a much greater strategic entity within the enterprise– one which doesn’t continuously solve simple, repetitive issues (at great cost) but finds ways to build value. We explored this concept with CSS Corp in a POV last year, where we discussed the ways in which contact centers can transform from a cost center to a profit center—most notably, we looked at how enterprises can drive more revenue by analyzing their real-time customer interaction data and support contact flows. Virtual assistants like Yodaa contribute to this strategy by making data and context easily available and automated, becoming a valuable tool for marketing and sales as well, by learning from customer conversations to better understand their needs and expectations.

The lynchpin of success in the contact center for virtual assistants like Yodaa is the capability to fulfill a very important customer need for simplicity. It all boils down to making things easy for the customer while looking for opportunities to add value when appropriate.The Yodaa tool claims to understand customer intent and be able to learn from its conversations, which can provide a huge benefit to making customer service easier. CSS Corp’s Yodaa is onto something with its learning and integration capabilities, and looking forward we will see if customer stories pan out to show this is a capability which stands out amid the din that is the topic of service agents today.

In Q4 we will be exploring the world of service agents in more depth as we launch our first Cognitive Agents Emerging Market Guide.

With Natural Language Processing, Interactive Voice Response, cognitive virtual agents, Robotic Process Automation, the very essence of our corporate existence, the conference call itself, is in grave danger of going robo. I think we’re done folks…

Recently I attended the GSA Symposium to get to grips with what’s going on in the global sourcing industry. In a debate, the topic of robotics and automation and its economic impact was tackled head-on by a panel that included union leaders and automation luminaries including HfS’ founder Phil Fersht.

The core focus of the debate was the impact of these technologies on employment, and what could be done to mitigate them. The discussion was broad and covered a full spectrum of topics including universal basic wage and the plight of low-skilled labor. It is the latter that caught my attention.

The bulk of the argument was how organizations should protect low-skilled positions to avoid such sweeping economic change. One union leader argued that if low-skilled jobs were to leave his region, it could never possibly recover as the range of employment options simply weren’t available.

The trouble is, I disagree and do so with relatively little knowledge of the region in question. Simply put, I think the future looks bright for all workers, regardless of skill, for two key reasons. Paradoxically, technology is at the center of both – except where others believe they’ll make people redundant, I think they’ll empower them to do greater things.

Technology up-skills and empowers

In previous blogs, I’ve argued that technologies like automation free people to do amazing things by doing the tedious and low-value work that nobody wants to do anyway. This time, however, I want to look at things from the other side of the coin.

I believe technology empowers people to do high-skilled work, regardless of their experience and education. Historically, individuals found themselves pigeon-holed to specific forms of work because of their academic background or employment history. It may be that they didn’t study the course they needed to get the dream job, or hadn’t ticked all the experience boxes needed to get where they wanted to be. Now, technology can balance the field.

Take a car mechanic as an example. An enormous amount of training and experience is required to be successful in the role. Fixing a Ford Mondeo with a dodgy head gasket isn’t something you can just walk into after all. However, with new analytics technologies and the increased computerization of vehicles, it may be something that can be diagnosed by a relative novice. With the right integrated knowledge management system, it might be something they can fix while reading a walkthrough or watching a video.

What’s key here is that the technology available to us now provides us with opportunities that were historically never available. So, the fear of low-skilled labor taking the brunt of the automation fallout is unlikely to be as simple as people make it sound. The parameters of what is considered low-skill and high-skill are blurring significantly.

Technology makes us more mobile

Access to these opportunities makes the average employee more mobile, as long as they have the right tools and access to knowledge most doors can be flung open. But technology makes us more mobile in another way. I’m writing this piece from home, approximately 50 miles from my nearest colleague, Jamie. Nevertheless, I’m happy talking to Jamie right now using technology that’s available to pretty much anyone. I’m accessing documents and collaborating on a report with colleagues in three continents. Of course, some jobs and professions require a physical presence (even I’m struggling with the concept of a surgeon operating from home) but more and more will utilize new mobility and communication technologies to allow employees to work from anywhere in the world.

The future of work is a complex beast, but if one thing’s clear it’s that technology will play an enormous part.

So, will technology be a terminator or our salvation?

Both. Technology will make some jobs redundant, improve some and create others – as it has always done. When I discussed this blog with our Head of Research, Saurabh, he mentioned the example of candlemaking’s decline at the advent of electricity and the light bulb. Sure this was undoubtedly upsetting for those who had dedicated their lives to candle making and had little other skills to transfer into another role. But these days, when we’re surrounded by knowledge, tools and technologies, we have a much broader range of transferable skills.

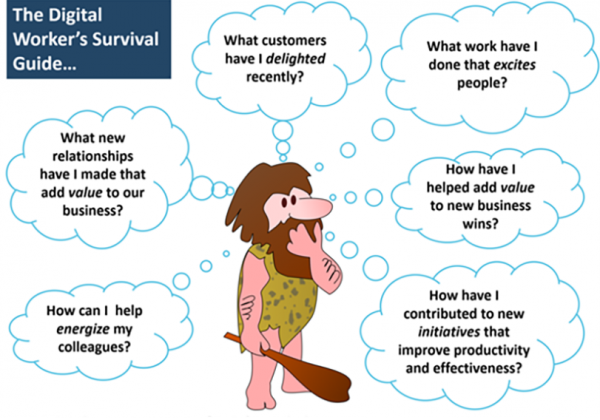

Crucially, as Phil Fersht has pointed out in his popular blog, the digital worker has a broader range of considerations rather than a particular strength in a craft – the key considerations are captured neatly in the image below which I’ve ruthlessly plagiarized from Phil’s original blog.

When did we start missing the point?

What I want to know is when did we start being so miserable? Everywhere I turn people are sharpening pitchforks for the imminent robot invasion. I answered a survey recently that asked if I was preparing for a world domination bid from an AI overlord. Amongst the hype and hysteria, we’ve lost sight of what’s really going on. By and large, technologies have been invented to improve on what we currently have. Sure, dependent on your perspective you can reel off a list of offenders that have been damaging, but for the most part, they improve how we live, work and play. And increasingly seek to secure the future of our planet.

Frankly, and if the hype is to be believed I may be in the minority, I’m looking forward to the future and what new and innovative technologies will bring.

Bottom Line: The truth is that technology may have a negative impact in some areas of the economy, but it will also have a positive impact on many more.

If you’ve been covering the legacy world of Business Process Management (BPM) software and the emergence of Robotic Process Automation (RPA) software for the past two decades, it’s fascinating to see the two solutions to mesh together, as customers need the full gamut of automation help: the digitization of manual work, the scripting, and integration of static data that provide the foundation for the automation of the digital processes.

Then you can get to the really exciting stuff of recognizing data patterns, taking advantage of machine learning to make systems self-remediating, and, ultimately, the injection of intelligence to make them absorb everything around them to become predictive and human-like in the way they operate. This is why we’re seeing the likes of Pega peering into the RPA space, Blue Prism partnering with Appian and AutomationAnywhere now partnering with IBM’s BPM software solution. We’re also seeing some novel approaches, such as intelligent automation provider WorkFusion donate free RPA software to the world to bridge the divide between the manual and the digital quandary.

Yes, people, there appears to be a fair bit of life left in the HfS Intelligent Automation Continuum. Despite some critics who believe RPA is a very separate solution than digital autonomics, machine learning, cognitive and AI, the fundamental thought-process behind the HfS Continuum model still rings true: all the approaches illustrated are both overlapping and interdependent:

Notwithstanding all the feverish excitement on RPA and Cognitive, we still need to include all the less exciting – but critical – activities, like runbooks and scripting, and how these approaches must be integrated into broader digital process workflows. True Digital OneOffice only works when all breakpoints and silos are effectively automated. If you truly want all touchpoints and processes across your organization focused on executing your vision of customer experiences and building foundational capabilities that support this entire philosophy, you have to address the entire Intelligent Automation Continuum if you want a data backbone that operates in synch across your customers, partners, and employees.

This is the context in which the announcement of IBM’s partnership with AutomationAnywhere comes in.

As part of the agreement, the two companies plan to integrate Automation Anywhere’s RPA platform with IBM’s portfolio of digital process automation software. The main focus will be on integrating Automation Anywhere with IBM’s Business Process Manager and Operational Decision Manager. Crucially, integration is meant to be on code level and therefore goes beyond more loosely integrated partnerships between BPM and RPA players. These enhanced products will be part of IBM’s software catalog. And lastly, both companies plan to build out a Center of Excellence around Automation Anywhere’s RPA capabilities. Condensed and in plain English, this means that IBM is planning to expand its BPM offering through RPA capabilities. Thus, it is a defensive move against Pega’s acquisition of OpenSpan that has seen the integration of BPM, RDA (Robotic Desktop Automation) and RPA. At the same time, we’re seeing the rise of more loosely integrated partnerships such as Blue Prism and Appian.

IBM needs to develop a holistic corporate strategy for RPA

While the partnership makes a lot of sense for IBM’s BPM division, from a narrow BPM angle, from a corporate and market facing point of view this announcement raises many questions. As part of its Cognitive Process Automation strategy, the GBS side of IBM has a focused and strong relationship with Blue Prism. It is unlikely that executives at Blue Prism (or GBS) are overly-pleased with these developments as it could curtail their mindshare among stakeholders. If anything, in contrast to most of its peers, GBS had chosen a single partner in order to scale its RPA deployments. Almost all of IBM’s peers have moved to a portfolio approach on RPA by offering and integrating a broad set of tool providers. In our discussions with IBM executives there appeared to be a lack of understanding as to the different RPA strategies of the various business units, let alone a nuanced understanding as to how RPA is being discussed in the broader market. In a nascent market with blurred market communications and relentless marketing rhetoric, this could add to the reluctance of customers to engage on a larger scale and a more holistic approach around RPA.

For those already engaged in RPA activities, questions begin to crop up about the firm’s current RPA engagements. Can clients expect to continue on their journey with BluePrism or should they anticipate a migration over to Automation Anywhere solution in the long-term? Of course, this is dependent on the level of exclusivity surrounding the partnership alongside other factors. In recent engagements with HfS analysts, the firm has championed its vendor and IP agnosticism, offering customers the opportunity to broker a broad range of solutions and services through them to find the best fit for the client business. We will continue to monitor this space to see if this partnership also signals a move away from this philosophy. If there’s one thing for certain, the deal may make commercial sense to IBM, but it opens them up to a lot of questions about current and future engagements for RPA, alongside broader IBM services.

And where does this really leave Watson? While the rest of IBM grapples with the digital underbelly of pulling the pieces together in a way that makes sense for the process wonks, the engine that is Watson, with all its cognitive analytics grunt, is nowhere to be seen in this story. Surely IBM needs to pull together all these internal factions (and from within the Watson group itself) to develop an integrated data orchestration story that the industry can actually understand. Talk to anyone about Watson and noone is particularly clear where this is all headed, even from within Blg Blue.

For Automation Anywhere it is all about scale

The RPA market is still lacking scale. Most deployments are client specific and on sub-process level. In a nascent market that might not be surprising, but more fundamentally there is a lack of education as to how to get to scale with deployments. Against this background Automation Anywhere could leverage IBM’s know-how and IP to understand better how data is being transported and what the critical bottlenecks are. This could provide a critical differentiation in a nascent market that lacks an understanding how those innovative toolsets are impacting process chains and workflows. The talent with such an understanding is extremely scarce and is difficult to keep in an organization. However, for Automation Anywhere scale is also important from another angle. The main strategic objective is still moving toward an IPO. Therefore, the leverage of IBM’s sales channel could conceivably reach many new customers which in turn would enhance Automation Anywhere’s valuation by financial stakeholders. To achieve that goal, Automation Anywhere needs to mitigate any potential negative reaction by its other main partners. Suffice it to say one could argue, that Blue Prism’s close relationship with IBM has not harmed its potential, yet with more scale and consequently value, the balancing of partner interests could become more intricate. Having said all that, should the partnership prove successful, M&A rather than an IPO might be on the cards.

The broader market is likely to get more confused in the short term

In a market blighted by smoke and mirrors as well as the mis-selling of RPA, without a focused and clearly articulated marketing push, this announcement is in danger of confusing the market at least in the short term. Many stakeholders don’t understand the differences between RPA and RDA, how cognitive is coming into play or even how RPA could be integrated into BPM toolsets. By adding BPM as another starting point to the RPA discussions on top of the front-office centric RDA approaches and the more back-office focused RPA engagements, further confusion is likely. Suffice it to say IBM has the marketing muscle to act as (a long overdue) educator. IBM’s BPM team should urgently leverage the robust insights and capabilities from its peers in GBS.

Bottom-line: The proof will be in the pudding, but the move could give Automation Anywhere real industrial scale

IBM urgently needs to develop buyer stories that demonstrate to the broader market the success of its strategy. A critical component in those narratives needs to be the depiction of how BPM and RPA work together. As it is sold as a product rather than a service, it could follow the many failed RPA projects that neglected a more consultative approach leveraging the specialist capabilities of organizations like the RPA pure plays such as Symphony Ventures, VirtualOperations or Mindfields. Automation Anywhere has less to lose yet more to gain. The understanding of how to scale deployments while simultaneously broadening its client reach is as tantalizing as it could be value enhancing. As the proof will be in the pudding, HfS will follow those developments with great interest.

The big questions marks with the likes of AA and other RPA solutions are whether these products will hold up in situations of industrial stress where they have to cope with very high throughput, high-intensive processing. If AA can prove it can delivery both the RDA and RPA grunt to power the broader IBM BPM solutions, then the firm will be in a strong position to increase its valuation as a bonafide enterprise class solution. Perhaps even IBM itself wants to have an up-close and personal experience of the AA software in these intensive client environments, before making its own acquisitive move… the future is unraveling, and this is just another piece of a much larger automation jigsaw that is quickly coming together…

Another year another top 50 list of service providers can be found on HfSresearch.com. We have included some new providers – including a couple of interesting BPO firms in Japan and adjusted for the recent wave of consolidation in the market.

I just wanted to repeat the advice I gave out last year about the report and the list – this report is all about the money. Being on the list or not, doesn’t make a service provider good or bad – hopefully market forces mean that better/cheaper providers rise through the ranks, but it isn’t necessarily so.

The Top BPO FAQ:

You’ve made a mistake can you correct it?

We are human and from time to time this happens – just send me an email and with your thoughts and we’ll correct. By all means, call me names on Twitter – but I may shout back…

We can miss companies from time to time and define where revenues go incorrectly. And, occasionally, spell your name incorrectly 😉 Also we may define things differently from you – we are trying to compare like with like as close as possible. Remember this is an estimate – so if you have further guidance, I’d be happy to have a conversation to let you know how we came up with any of the numbers.

I should be on the list / What do you have to do to get on the list?

Sending us evidence (a financial report or two, would help) that shows latest annual revenues. We use calendar years for our lists usually, so something that shows the relevant quarters would work. But happy to have a discussion with any private firms – just so we can properly establish position. I am not a miracle worker so private companies that don’t publish results and don’t provide guidance may not make the list.

How much do I need to bribe you to change my position?

It (still) pains me to say it but no – we just can’t. The pesky tax man (and our boring accountant) frown on it 😉

That said it is also free to be on the list – you just need to demonstrate that you have the revenues to make it. But I will check against public sources and validate.

I really want to be part of this but I just don’t have the revenues yet – is there anything I can do?

We are happy to engage regardless of the absolute market share if a vendor has an interesting service – we are interested in up and coming providers. And we may profile interesting firms.