When an industry is enduring a secular shift that is literally redefining how we do work, it’s pretty important to get some real, unfettered dialog going among all the key stakeholders this impacts. We need to break free from the glitzy paid-for sales presentations, robot keyrings, stress balls, nasty logo-ed leather notepads and greedy events firms vying for a quick buck from vendors eager to part with cash to promote themselves to all their competitors.

That’s why we’re assembling 100 of the industry’s finest leaders in a single room for a whole afternoon to thrash out the mandate for the future of operations in the robotic age for our inaugural FORA council session in Chicago, 19th September. And we promise no sponsors, stress balls or bad white papers to take away…

Here’s just a sample of the industry robo dignitaries who’ve already committed:

Alastair Bathgate, CEO, Blue Prism

Chetan Dube, CEO, IPsoft

Chip Wagner, President, Emerging Business Services, ISG

Cliff Justice, Partner, US Leader, Cognitive Automation and Digital Labor, KPMG

David Poole, CEO, Symphony Ventures

Daniel Dines, CEO and Founder at UiPath

Jesus Mantas, Managing Partner and General Manager, IBM Business Consulting, IBM US

Lee Coulter, Chair for the IEEE Working Group on Standards in Intelligent Process Automation

Dr. Mary C. Lacity, Curators’ Distinguished Professor of Information Systems, UMSL, and Visiting Scholar MIT

Max Yankelevich, CEO, WorkFusion

Mihir Shukla, CEO, Automation Anywhere

Peter Lowes, Partner, and Head of Robotics & Cognitive Automation, Deloitte US

Shantanu Ghosh, SVP, CFO Services and Consulting, Genpact

Thomas Torlone, U.S. Leader of Enterprise Business Services, PwC

Tijl Vuyk, CEO and Founder, Redwood Software

Weston Jones, Global RPA Leader, EY

We also have leaders of cognitive and automation initiatives from the following buyside firms already signed up to get stuck into the debate:

So let’s cut to the chase – it’s time to have the real, hard conversation about where we really are as an industry. Why aren’t those 40% cost savings happening, each time someone slams in some software and hopes it somehow eliminates manual labor because they can access a bot library? In fact, why are a third of RPA pilots just left hanging with no result? Yes, people, it’s time to wake up and smell those robotic roses and have those really tough conversations about what is real, versus why so much of this stuff just isn’t working – and why we’re not putting together properly governed RPA rollout plans like we do with ERP software and SaaS platforms. Why are we making such a mess with this, when we could have so much to benefit from?

So join us in Chicago this September 19th for FORA the inaugural council meeting that finally debates the true Future of Operations in the Robotic Age

FORA is the very first industry council established to bring together buyside operations leaders, service providers leaders, expert advisers and technology developers to steer industry’s transition to the Digital OneOffice™.

FORA’s mission is to bring together the leadership from senior buyside operations leaders, service provider leadership, expert advisers, and technology developers to set the agenda for the transition to the Digital OneOffice™, and to develop an industry mandate for navigating and managing the creative destruction that looms. Supporting the FORA initiative is the IEEE’s Intelligent Process Automation Standards initiative that will encourage further research and investment, leading to powerful and attractive new service offerings. But the commercial frameworks needed to encourage and sustain wider deployment of these technologies are lagging because they fundamentally threaten established models.

In order to communicate the learnings from the FORA meetings, the group will produce a quarterly “FORA Mandate” that communicates core recommendations to the industry from the group meetings that will be held at quarterly HfS Summits.

So how can you get considered for Council Membership?

HfS will consider applications to the FORA Council based on seniority and relevance. Are you interested in participating? Just email us at [email protected].

This is a really important development as we consider the future of services and operations amidst all this creative disruption. I hope to greet many of you personally in Chicago this September.

Earlier this week, Cognizant announced its intention to expand its footprint to support U.S. Government health operations through the agreement to acquire the TMG Health subsidiary of Health Care Services Corporation (HCSC). On the flip side of that announcement, HCSC has carved out its Government health support function to be run by a partner – Cognizant. HCSC can benefit from Cognizant’s dedicated, prioritized, and leveraged (cross-client) resources to manage the operations services. However, to impact the health, care, and financial outcomes of its healthcare consumer base, HCSC will need to partner with Cognizant in a way that creates the OneOffice™ – a seamless flow of data, insights, and infrastructure for the front, middle, and back office.

TMG Health’s relationship with HCSC started back in 2005 when HCSC selected it to provide BPO services in support of its entry into the Medicare Advantage market. At the time, TMG Health provided some measure of enrollment, eligibility, claims, and billing support to a total client count of 30 plans covering 2.8 million lives. In 2008, HCSC acquired TMG Health for $100m, tucking in the BPO provider as a subsidiary. TMG Health has since added support for Medicare and Medicaid claims processing and member services and has local resources in Pennsylvania and Texas – for 32 health plans (+2 since 2009) and more than 4.3 million lives. TMG Health has not really grown its portfolio of clients although the footprint of services has expanded over time. And public health programs continue to grow – in numbers and complexity as the industry moves to greater coverage and value-based care. The changes in the healthcare market driven by consumerism and compliance are driving healthcare plans to “rethink” their business and operations strategy.

By exiting the “back office business,” HCSC can focus its investment and resources on becoming a more consumer-oriented company.

While retaining a partnership with Cognizant for its support/back office services, we expect HCSC to focus on becoming more consumer-oriented; to channel its resources to becoming insightful, tech-enabled, and overall “savvy” to impact health outcomes for its constituents. In the meantime, it can rely on Cognizant to provide a steady and increasingly optimized rules-based foundation. We expect Cognizant to tap into the Medicare/Medicaid COE it told us about in our last Healthcare Operations Blueprint research. The consolidation of its subject matter expertise, IP, and tools in the COE is to help manage the tricky business of complying with government policies and the continued growth of Medicare, Medicaid, Medicaid Advantage, and Dual-Eligible consumers – providing support for eligibility, enrollment, billing, claims, and applying its solutions around quality and reporting (e.g., STARServe). Cognizant has the right experience plus industrialization and scale and has the Trizetto and RPA capabilities to drive increased efficiencies and free up resources to support new growth in the Government Health operations business.

The Bottom-line: HCSC and Cognizant will need to partner to keep – or establish – integration between front and back office to impact health, care, and medical outcomes.

One place this arrangement could break down is if the back office support that Cognizant provides is not integrated with the front- and middle-office of HCSC (and its other clients). In order to impact health, care, financial, and quality outcomes, healthcare payers need to be healthcare-consumer oriented – understand the health, financial, economic, and social determinants of their constituency. A lot of that data is part of those back office systems and processes, so HCSC and Cognizant will need to be partners in defining workflows of the future that will support an insightful, consumer-oriented business that complies with government standards and also enables HCSC to better manage the health, care, medical, and financial outcomes of its public health base.

A question I get asked a lot is what do I think about the future of outsourcing? In this case in a few hundred words. I thought I’d share, but forgive me if it becomes evangelical:

The future of outsourcing is linked very strongly to the future of technology and its use in the enterprise – often it’s very hard to distinguish between the trends of these two things. Essentially outsourcing is the commercial arrangement between technology (and business services) organizations and their customers – it’s how you put a price on an operational service between the two.

The big shift will be the level at which you quantify an amount of service. The most popular way to quantify outsourcing arrangements has been by the number of people, per FTE models. But over time these transformed into a hybrid of FTE, transaction/consumption based and the slightly misleading outcome based pricing – which was often just an emphasis shift toward an achievement or variant of the first two, essentially the same but with a stricter KPI focused on a specific goal.

Cloud and as-a-service types of the contract have made consumption/transaction based pricing the norm for IT and IT services – we expect this to pretty much remain. The twist in its tail will be the unit being consumed will not be an IT measure. The unit of consumption will start to be linked more directly to a business metric, not an outcome. So, for example, all of the costs associated with hiring a bicycle from a city-wide hire scheme could be paid for in bike hire units – the provider only gets paid when a bike is hired – irrespective of the technology being consumed. This is a simple example – but as we see better use of automation and AI within IT and within transaction management, which reduces idle costs and we will reach a point where this type of deal has little risk. The cost of keeping the IT running could be negligible – this won’t be risk/reward in the traditional sense as the IT firm carries very little risk if the client doesn’t achieve the desired volume. The build and run deal, where the client doesn’t pay for the implementation will require the same type of calculation as current build and run deals – but the measure used for payback will be different.

Additionally, as these models develop we expect the level of risk within the contract to be better understood. This means the risk equation can be better calculated into the mix as analytics dictate the acceptable level of risk and the appropriate price points.

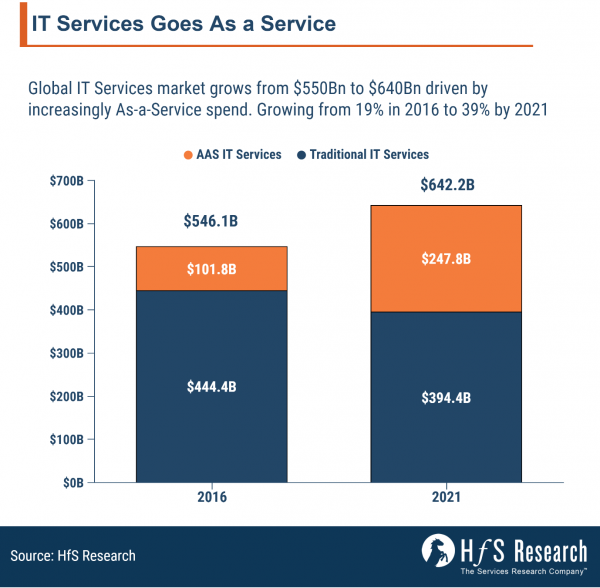

We have quantified this shift to more consumption-based services in the chart below – if you look at the proportion of IT services contracts that will be as-a-service by 2021, it is jumping from its current 19% level to almost 40% by 2021. We define AaS is a turnkey managed service solution based on a standardized platform delivered via the Internet – uniform standards across clients with relatively low levels of customization (<25%) – not lift and shift, but adopt, change and adapt. The price of the service is directly proportional to a transaction or measure of consumption. We also include consulting and professional services that advise upon and wrap around this type of service.

Another shift, particularly in IT outsourcing will be the merging of applications and infrastructure – which we have already seen to a certain degree. Cloud and DevOps have helped to break the silos between applications and infrastructure intrinsically linking these two pieces – making separate outsourcing deals for these two parts of an organization increasingly unlikely as the applications and infrastructure continue to merge. This will be particularly true in industries where applications are developed for customers, and the infrastructure requirements are linked to the success of the application. The adoption of the app dictates the scale of the infrastructure – which increasingly means monolithic, inflexible infrastructure deals fade away. Replaced by more application focused deals including the infrastructure paid for based on consumption linked to business use.

Bottom line – outsourcing will continue to exist, but the variable won’t be as directly linked to the cost of people. It will use technology to form new blocks of consumption.

Outsourcing is one of the commercial wrappers for consuming technology and business services. As these services become more software and platform based, the commercial models will become more As-a-Service. So consumption based models will be and already are becoming the norm. However, the most critical shift in will be the commercial parameters changing to fit the technology being outsourced. Automation and AI technologies will be used to allow outsourced IT (and business services) to split into new blocks of consumption, more linked to business requirements. With AI even helping to match risk levels to specific price points. True As-a-Service outcome pricing is born.

The windy city will get extremely blustery this September 19-21, when HfS stages the inaugural FORA Council session, immediately followed by our annual HfS Summit “The Digital OneOffice: Redefining How We Get Work Done”

Friends,

Someone just described going to an HfS event as the whole industry being bludgeoned with a blunt instrument… how dare they? Yes, friends, it’s nearing the time for the next, immense iteration of that HfS summit, where we’re cementing together the biggest, boldest and baddest crowd yet to mix some serious debate with a good sprinkling of humor and networking.

Indeed, the way we get work done really is being completely redefined before our very eyes. However, while it’s one thing to redefine how we do things, it’s another actually to execute in the reality of the workplace. This is where we turn the traditional outsourcing model on its head as clients demand a piece of the automation action. This is where we talk about end-to-end processes that include both RPA products and cognitive tools. This is where we talk about the Digital OneOffice, where the barriers between front, middle and back offices are forever eroded to meet common business outcomes.

Please join me and the HfS analyst team in Chicago, September 19-21, for two amazing days of debate and collaboration, where we put our egos aside and make some key recommendations to the world.

Apply now for the full program consisting of compelling keynotes and discussions, case studies, workshops, and networking. Find the full agenda here and apply for your seat now while we have some spaces left.

Cheers,

To name a few companies which will be represented…

I have refrained from political commentary since Trump took office because so much has been unclear. Not that his stated views during his campaign that climate change is a Chinese hoax and climate rules are designed to hurt American businesses or his appointment of staunch climate change-deniers to the EPA and Department of Energy, promised anything good. But now the long awaited, reality TV decision about the Paris Climate Agreement showed the real Donald Trump meant what was really going to do what he promised: The United States will “withdraw from the Paris Climate Accord,” “seizing all implementations right away.”

Trump frames the climate change fight, not as one of our world’s biggest challenges but an economic zero-sum game of the US against the rest of the world. In his speech, Trump tried to tie leaving ‘Paris’ to the protection of the American people. This is a narrative weaned from reality.

Here are some sobering facts to put Trump’s decision in context

Withdrawing from Paris doesn’t impact much in the medium term, regarding real climate policy and action. Withdrawing from the agreement will take a full four-year period. Ironically the US can only officially withdraw the day after the 2020 presidential election.

Paris is a voluntary agreement, of which many critics claim lacks teeth. Every nation sets its own goals. Obama pledged to reduce carbon emissions by 26 percent during the 2005 – 2025 timeframe. The US could have simply adjusted its ambitions and goals if it felt Obama’s goals are unattainable. Trump has already gutted the Clean Power Plan, an essential part of Obama’s efforts to reduce emissions by fossil fuel burning electricity plants and increase the use of renewable energy and energy conservation.

Many “legacy” energy jobs are already gone. Coal jobs won’t come back, nor will the jobs in Oil & Gas that were lost in the downturn over the last three years. Coal has lost its ground and competitive edge to natural gas, solar and wind. Mostly for competitive pricing reasons, not policy reasons. Coal companies acknowledge this, saying they don’t see a future for coal and jobs will continue to diminish. The production of oil and gas has rebounded from the slump of 2014-2016, but jobs have not. This is due to new efficiencies in the field, primarily driven by automation.

The new jobs re in clean energy and Paris promotes their creation. The jobs Trump is so eager to create are not in the fossil fuel industries but in clean energy. The solar industry is the biggest engine of job creation in America. In 2016, one in fifty new jobs was in the solar industry. Grid modernization driven by renewable energy has created 100,000 new jobs in 2016, according to the Department of Energy. The Paris Agreement created a lot of momentum for the adoption of clean energy. For the first time in history, the world united to curb emissions and set a framework to act against climate change. The Paris Agreement provides a big push for the energy transition that is underway across the globe, a transition that some experts expect to create a ten-trillion-dollar economy for renewable energy and is already creating large numbers of blue-collar manufacturing, installation and service jobs in the US.

Any deal on climate change is terminal while Trump is in power. There won’t be a new deal of a re-negotiation of the current agreement, as Trump alluded to in his Rose Garden spectacle.

Will it change US progress in the inevitable move to renewable energy?

The simple answer is no. Besides the damaging effects of Trump’s actions at the federal level, for businesses, states, and cities, the only common sense course of action is to continue down the path of renewable energy. Directly after Trump’s decision, California, Washington, New York, Connecticut, Massachusetts, Rhode Island, Hawaii, Oregon, Vermont, Minnesota, Delaware, Virginia and Puerto Rico – representing roughly 35% of the US economy – formed the United States Climate Alliance, vowing to uphold the Paris Climate agreement within their borders. Eleven other states, including Maryland, Ohio, North Carolina and Illinois, have also supported the Climate Agreement.

The historic Paris Climate Agreement has already been ratified by most parties to the treaty and was signed by all countries except Nicaragua, who find the agreement not far-reaching and aggressive enough, and Syria, for obvious reasons. The Paris agreement is an agreement with intentions, not with automatic actions. The interpretation and subsequent actions heavily rely on industry and civil society. And they are now further encouraged to take action. While the Trump administration is doing everything to shut down forward-looking energy policy and climate change policy on a federal level, such as overhauling Obama’s Clean Power Plan, on a state and city level, the majority is acting; investing in renewable energy resources, adhering to the Paris Agreement guidelines. Since Trump’s announcement, governors, mayors and business leaders have spoken out and showed their intentions to stick with ‘Paris.’ California’s governor flew to China to sign an agreement with the Chinese to collaborate on climate and clean tech, emphasizing the resolve from states to act and move forward.

A symbolic policy shift with diplomatic and reputational impact first and foremost

The announcement to withdraw from ‘Paris’ is a symbolic move more than anything. And it is symbolic for all the wrong reasons

The backlash is starting to show; there is a negative impact on the reputation of the US – the rest of the world effectively sees Trump’s move as the withdrawal of the US from the world stage. The diplomatic backlash will be felt beyond the climate realm.

Impact on American businesses – US businesses fear they will be at a disadvantage seizing the opportunities in the renewable energy market, while they, until Trump’s decision, where well-positioned to lead in the global clean energy market.

It highlights the missed opportunity to jump on the renewable energy train. Trump is missing a great opportunity to make a concerted effort on infrastructure and the job creation in the renewable energy market. Last year, one in fifty new jobs in the US was created by the solar industry. Think about that. And only 50.000 people work in coal. Pick your battles, Mr. Trump. Instead of trying to save a small number of coal mining jobs with the red herring of ‘clean coal’ and withdrawing from Paris, focus on re-training coal miners for the manufacturing, installation and service jobs in the wind and solar industry.

The bottom-line: Trump will be gone when Mar-a-Lago is swallowed by the sea

As Oscar Wilde famously said: “With age comes wisdom, but sometimes age comes alone.” Trump’s announcement was short-sighted and removed from reality and science, catering to a small fraction of people with extremist and ancient views on climate and energy

The good news is that the clean energy transition is well underway and won’t be stopped by the Trump administration, not in the US and certainly not abroad. But, as many critics of the climate agreement emphasize, it might be too little too late. The Paris deal was a strong message from all nations, coming together in the endorsement of curbing global warming and the impacts of climate change, but the climate fight needs more ambitious goals and most importantly actions. The world can’t wait any longer and play an economically motivated game of chicken, with the well-being of our planet at stake.

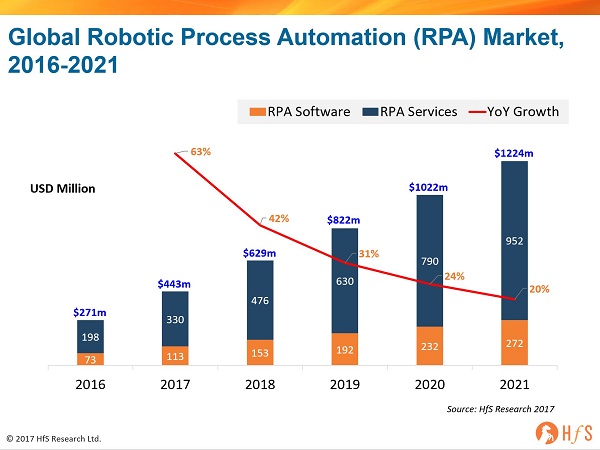

Have we ever got so excited about a market that isn’t even yet past the half-billion dollar spend level? Are we getting over excited about solutions because of their potential before they are fully tried and tested in reality? Let’s get to the realities of RPA by examining the size and five-year forecast for software and related services expenditure:

The global market for RPA Software and Services reached $271 million in 2016 and is expected to grow to $1.2 billion by 2021 at a compound annual growth rate of 36%. The direct services market includes implementation and consulting services focused on building RPA capabilities within an organization. It does not include wider operational services like BPO, which may include RPA becoming increasingly embedded in its delivery.

RPA describes a software development toolkit that allows non-engineers to quickly create software robots (known commonly as “bots”) to automate rules-driven business processes. At the core, an RPA system imitates human interventions that interact with internal IT systems. It is a non-invasive application that requires minimum integration with the existing IT setup; delivering productivity by replacing human effort to complete the task. Any company which has labor-intensive processes, where people are performing high-volume, highly transactional process functions, will boost their capabilities and save money and time with robotic process automation. Similarly, RPA offers enough advantage to companies which operate with very few people or shortage of labor. Both situations offer a welcome opportunity to save on cost as well as streamline the resource allocation by deploying automation.

The bottom-line: RPA provides the building blocks for digitizing rudimentary processes in the digital underbelly, but the broader market for intelligent process automation is more than 10x the size

Stay tuned for our broader forecast for the global Intelligent Process Automation market, which is in the final stages of its fine-tuning, as the expenditure enterprises and service providers are making their internal teams to learn how to automate business processes intelligently, the internal training and development, pilot projects and trial implementations, is so much larger than simply software licences and third party professional services to work the software effectively.

Net-net, we have to be realistic about the value RPA brings to enterprises today, versus its potential for the future. RPA’s value for most of today’s early adopters lies in the digitizing of rudimentary manual processes. It’s a starting point for designing the underbelly that enables a digital OneOffice environment:

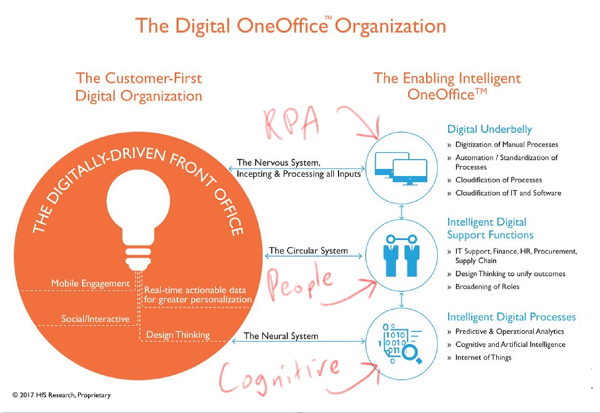

Digital effectiveness is all about organizations enjoying real-time process flows forged through the elimination of manual process break-points and intelligent linking of data patterns across the front and back offices. RPA is a critical building block in facilitating this journey, but ultimately it’s the whole OneOffice, not the sum of the parts, that matters for true real-time effectiveness. This is about one integrated organization unit, where teams function autonomously across front, middle and back office functions and processes to promote real-time data flows and rapid decision making, based on meeting defined outcomes. In the future… front, middle and back offices will cease to exist, as they will be, simply, OneOffice, and RPA has a critical role to play supporting the building blocks. However, the market is still very young and we’re only at the start for so many organizations, so let’s not get too carried away until we see really robust solutions with proven ROI and long-term business value.

In short, every siloed dataset restricts the analytical insight that makes process owners strategic contributors to the business. You can’t create value – or transform a business operation – without converged, real-time data. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embracing the cloud in a way that enables genuine scalability and security for a digital organization. Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities. This is where RPA adds most value today… however, as more processes become digitized, the more value we can glean from cognitive applications that feed off data patterns to help orchestrate more intelligent, broader process chains that link the front to the back office. In our view, as these solutions mature, we’ll see a real convergence of analytics, RPA and cognitive solutions as intelligent data orchestration becomes the true lifeblood – and currency – for organizations.

Fractal Analytics’ bets, on AI and machine learning as its future, are set to be bolstered with its new acquisition of consulting and analytics firm 4i Inc.

We noted in 2014 in Profiling An Analytics Rising Star: Fractal Analytics, that “Fractal is now more bullish about its analytics consulting presence onshore, and its technology investments – a clear aspiration to move away from the offshore analytics model”. Our interactions and observations of the service provider since that time – including this latest announcement – seem to confirm our hunch about this pivot.

As one of the last few pure-plays left in the analytics services business, Fractal has come a long way from 2000 when it was set up in Mumbai, India to tackle niche analytics projects for U.S. based banks and consumer goods companies. It now has a global presence in 12 locations, serving well-known global brands such as Philips, Kimberly Clark and P&G. Fractal was already growing rapidly (e.g. it has grown at 60% CAGR over the last six years). We expect this move to add to their topline growth with an expanded base of U.S. clients and front-end consulting capabilities to aid sales efforts. In the last few years, it has aligned resources towards a long-term growth strategy focused on high-touch client interactions and machine learning and AI technology-led solutions.

Increasingly high-touch local interactions supported by global network

Along these lines, Fractal’s acquisition of 4i is interesting because it:

Brings CPG consulting chops: Analytics consulting was the critical missing piece for Fractal as it rounded out its services portfolio. With clients like Colgate, Kraft foods, Post, and Del Monte, 4i’s focus on CPG is evident. Its “foresight-driven approach” will align well with Fractal’s focus on predictive analytics that can help clients be more proactive vs. reactive with their analyses and decision making.

Improves client collaboration: 4i’s capabilities add to the high-touch client interactions that strategic analytics initiatives need to be successful. Fractal’s clients love the attention they get from the service provider’s management team and its long-standing relationships are a testament to this culture. 4i’s presence in a central location in the U.S. (Chicago) will help deepen client relationships. More importantly, this onshore presence will help Fractal’s analytics services be more impactful. A lot of analytics clients value “high touch” engagements where analysts can spend more time on-location to really understand business context and priorities and with the operations teams to get the best results.

Extends the delivery network: 4i brings operations presence in Ukraine and Mexico, which Fractal will need to build out a diversified and global delivery backbone. Analytics talent in India is increasingly in short supply as every IT service provider, analytics startup, and enterprise IT organization tries to scoop up analysts, statisticians and data scientists in the major cities. Add to it the smaller subset of machine learning and AI specializations that Fractal will need going forward, and you can see why tapping other talent hubs around the globe makes sense.

How this local/global expertise is complemented by artificial intelligence

These factors will bring some significant advantages to Fractal, particularly as it rolls out its strategy for incorporating machine-learning into its analytics solutions. Fractal has spent the last two years building out its product portfolio of machine-learning solutions and even reorganized its management structure to give it more focus. Its solutions present “here and now” practical applications to enterprise challenges around infusing insights into every business decision. For example, Fractal Analytics’ Trial Run solution helps teams run experiments on their existing datasets, to see the potential benefits before rolling out to a wider base. Its Customer Genomics “hyperpersonalization” platform is helping companies target customers with more relevant and meaningful dialogues based on individual wants and needs. Enterprise clients that are working with Fractal on these solutions have mentioned to us how valuable their partnership is to access and explore machine learning technology together in these early days.

That word – partnership – is a great way to describe the type of engagement that enterprises need with their technology and service providers to build out AI applications today. As my recent blog post on IBM Watson services pointed out, “Cognitive technology falls in the ‘innovation’ realm for most enterprises. It requires thorough experimentation, risk/opportunity assessment, project prioritization, steep learning curves on skills development, and above all, education and change management for the employee/customer base that is involved in the process.” Consulting capabilities are thus a critical part of this journey for any hopeful AI service provider. With this tuck-in acquisition, Fractal is playing catch-up to its competitors such as Mu Sigma and Accenture, whose consulting capabilities are at the forefront of their analytics services businesses.

The outstanding challenge is just that: how to stand out, particularly against better-known brands with similar capabilities

Fractal has already made investments in the actual technology, including its own R&D, and acquisitions of Imagna and Mobius Innovations in the last couple years. It has the foundational client relationships that it can leverage. 4i will help it bring all these capabilities together. However, there are several emerging AI-based personal assistants, personalization platforms, etc. that Fractal is competing with through its product group. Its key challenge will be differentiating itself in this new and increasingly crowded market.

What Fractal needs to do next is craft a vision for its AI applications and services specifically within its key verticals of CPG and BFSI instead of the familiar trap of becoming a generalist. 4i has complementary vertical strengths and Fractal will do well to leverage these and build out what HfS calls vertically-infused insights. Overall, we give this acquisition a “thumbs up” verdict at HfS, with an eye on how Fractal articulates its value as a more comprehensive analytics services provider going forward.

Whether you have successfully started working with Watson, are evaluating it, did a PoC 18 months ago and swore off it, or have an enterprise license sitting around, you have realized that Watson is not your average prepackaged software application. As IBM’s umbrella brand term for all things cognitive, Watson capabilities range from analytics to cognitive solutions and virtual agents, available as individual APIs or prepackaged products to develop Watson applications. As cognitive technology like Watson falls in the “innovation” realm for most enterprises, it requires thorough experimentation, risk/opportunity assessment, project prioritization, steep learning curves on skills development, and above all, education and change management for the employee/customer base that is involved in the process.

When you’re working with a service provider through this journey, chances are they are on the same learning curve because of the newness of the cognitive market for business use. While IBM is taking Watson to market through its GBS organization, Watson APIs and products are being used by business and technology services providers in a variety of ways (see our POV paper on this subject here). IBM Watson technology has been around officially for a few years, and PoC projects are the norm so far. However, HfS hears a lot of industry optimism and “gearing up” for 2017-2018 being the years of more substantive implementations through this growing network of services partners.

Considerations for using Watson services

As you explore Watson in your organization:

Understand where and how your service provider is investing in Watson to offset cost: Perhaps the biggest barrier to Watson adoption for enterprises has been its high price tag for entry. Service providers have been trying to circumvent this by exploring options to host the Bluemix and Watson licenses plus external databases. Their clients can then access both the technology and data, particularly for proprietary solutions where cognitive APIs are being leveraged. Enterprises that already have access to the Bluemix cloud computing environment are getting started with Watson on it as an incremental investment. As Microsoft Azure, Amazon AWS and other competing cloud environments all have their own machine-learning technologies, the decision to which cognitive ecosystem you go with will likely be influenced by these larger technology-buying decisions.

Find the provider that Is collaborating with IBM in areas that matter to you: Watson APIs and products are being constantly revamped, retired, and regrouped and it will help to have advance knowledge from a service provider that is deeply involved with IBM in advancing specific areas. We heard instances of how by providing feedback to the IBM Watson product development team and working collaboratively, some service providers influenced the release of new functionalities that benefitted their clients’ projects directly. Look for the connections that your service provider team has been able to establish that could impact your particular use cases.

Find the Service Provider That Is Investing in Your Vision – Or Using Design Thinking to Help You Develop One: Even in these early days, we see industry, functional, and technological strengths developing among service providers. The experience gained and customization achieved with specific solutions – like Hexaware’s superannuation bot or Accenture’s mortgage advisor Collette – are valuable to companies that have already outlined these areas for Watson or are looking for new levers for value to their business and customer base. In areas where there is not a relevant standard solution, your leadership team will often have competing priorities. Consider service providers that offer Design Thinking workshops to establish the top business priorities, the process and technology roadmaps, and the definition of your own version of a future-state with an “augmented workforce”.

Don’t Underestimate the Power and Influence of Naysayers – Educate Them First: As shared by a financial services VP, “Internal stakeholders require fundamental lessons on what Watson is and isn’t…Our skeptics didn’t fully understand what cognitive or data mining benefits Watson brings; we should have expected it earlier on and addressed it head first”. Without aligning organizational buy-in, companies in our research have seen significant slowdowns in each stage of their projects. Make sure your key representatives understand the breadth of the technology and its suitability to your use case before kicking off and then check in regularly.

The ripple effect of Watson services

With these considerations in mind, do note that whatever cognitive initiatives you undertake will invariably impact more than one part of the business and way of working. As a department undertakes the required data curation, reference architecture, process remodelling, and rollout, it will interact with and influence other departments or processes and advance their maturity toward more intelligent operations as well. For example, a retailer could go from a production pilot in personalized shopping on its website into cognitively determined best next actions for its sales channels, then on to cognitively driven merchandising and supply network on the back end to better predict demand. The core customer and product data can be leveraged across these functions and can become a powerful way to reinvent the entire customer engagement process.

The focus on better enabling the customer and/or stakeholder experience is driving significant enterprise interest to explore Watson services.

In our latest report, HfS Emerging Market Guide: IBM Watson Services, we further explore this theme of getting started with IBM Watson – the use cases so far, the progress on and beyond PoCs and pilots and the emergent role of service providers. The investments today are helping establish new norms for people, processes, and technology that will pave the way for “industrial scale” Watson in the future.

I am proud to announce we’ve unveiled a very exciting analyst talent to lead our global research team, based in Chicago US, as our Chief Strategy Officer (see bio).

Saurabh Gupta worked with me at Everest over ten years ago where I helped train him up to help lead the firm’s BPO research team. After a distinguished career at Everest, where he earned a very strong reputation as a highly focused and respected analyst in the areas of BPO, banking, F&A, procurement, analytics and the underlying technology platforms, he went onto the buyside with AbbVie (the spin off shared services for Abbott Labs), where he helped craft the firm’s BPO and shared services strategy, working across various service lines and service provider relationships. He then had a spell with Genpact, where he has been instrumental helping them devise and shape the firm’s CFO service offerings and digital strategy.

Saurabh has long eyed a return to the analyst fold and coming onboard HfS is the ultimate challenge for him, where he’ll be leading our global research team and working with all of us to write about real buyer experiences and mapping where enterprises are on their Digital OneOffice journeys, how fast they need to move and what is preventing them getting to their ideal states. I caught up with Saurabh this week to share more with you all what you can expect…

Phil Fersht, CEO and Chief Analyst, HfS Research: Saurabh – it’s just terrific to be working with you again after a decade since we were at Everest together! What took you back to the research industry after your recent years on the buyer and supplier side of services life?

Saurabh Gupta, Chief Strategy Officer, HfS Research: Thanks Phil. I am thrilled to be here. I am passionate about business research and being an analyst was the best thing that happened to me. However, I did want to experience and appreciate the perspectives of different stakeholders in our industry. So after Everest Group, I spent time with AbbVie helping shape their business process services strategy as well as Genpact as their strategy leader for CFO and transformation services. I think…or I hope that getting into the shoes of a buyer and a vendor helps me become a better analyst. Plus, this is an exciting time to be a researcher in our industry. On one hand, we live in this VUCA environment and on the other, we have finally unearthed the next big value creation levers after offshoring in Robotics, AI, and blockchain. So I feel the role of an analyst is extremely important in today’s world.

Phil: So why did you choose HfS? I think we were just a little bootstrapped operation when you were last in the analyst biz….

Saurabh: Where else? HfS has turned the analyst world upside down with its thought provoking, leading edge and futuristic research. With the pace of innovation and change, all stakeholders (buyers, suppliers, tech providers, investors) need to make important bets and decisions about their future. I’ve seen this first hand in my last two roles. And they cannot just rely on past data and trends to make those calls. HfS is the only analyst firm that I know who can help clients with “what is going to happen” versus “what happened in the past”… so this decision was a no-brainer for me.

Phil: Where is the industry right now, Saurabh? Do you see us in a transition state, or is something else bubbling to wake us all up?

Saurabh: As I mentioned earlier, this is an exciting time for our industry…perhaps the most interesting time in my career. It has reached an inflexion point after very long time where it is about to jump a S-curve. The offshore-led value proposition has dominated our industry over the last 15 years. RPA and AI is finally adding a new value lever that can make a difference and turn the game on its head. At the same time, we also have guard against the hype and be realistic in our expectations. We (and that includes analysts, advisors, buyers, and suppliers) also must learn to unlearn. And then watch out for blockchain and distributed ledger….while everything that we just talked about is about shrinking the pie, blockchain promises to remove the pie altogether…can you imagine what will happen if we don’t need system of records after all?

But the even more interesting thing to solve is the puzzle on talent. If I can ever get to influence my daughter, I will be pushing her towards humanities (arts, communications, psychology, creativity) and problem-solving versus left-brain stuff. I think that’s the future!

Phil: So what can we expect to see from you at HfS… what are your plans with our research strategy – can you give us a little snippet of what we can expect?

Saurabh: We already have such a great core in terms of thought leadership, coverage areas, clients and readership, brand, and data that gives us the ability to influence and shape the market. So I want to leverage our assets and IP to focus on serving our clients…understand their challenges and provide relevant and real insights.

Our focus should be on making research ‘real’ for our clients especially concepts such as RPA, digital, AI and blockchain. Help them differentiate between a pitch and delivery, go beyond the hype, be realistic yet provocative. We should complement our in-depth blueprint reports and vendor analysis with real-life client experiences, go deep in a set of chosen coverage areas, and expand coverage of niche and emerging players with a potentially disruptive value proposition. I also think we could help our clients across three horizons: “act now”, “watch out”, and “investigate”. I want to drive our agenda to do just that.

Phil: And finally, is the analyst industry as exciting as it was 10 years’ ago?

Saurabh: Perhaps even more exciting but this is just day 2 for me…

Let’s turn that common lament we hear of a “talent shortage” on its head. What if you created a pipeline of talent that fit the needs of your business as it is growing and changing? While at the Infosys Confluence event recently, I heard about how AT&T has been taking steps for the last two years to create the very workforce it needs to achieve its vision.

First, determine what skills and capabilities your workforce will need in the future

“Based on industry and corporate direction, we chose six areas, including big data, IP networking, and software-defined networking, that we specifically want to attack as the skills of the future,” shared Candy Conway, VP, Global Managed Services Operations, Business Solutions and International at AT&T.

AT&T defined a set of roles that map to these areas, determined the associated competencies, and evaluated employees against the future landscape. They identified over 100,000 employees who will need to have a different or a more varied or developed set of competencies than they have today. “We then developed a roadmap and plan for getting these professionals into a relevant and meaningful career path that maps to the future of the company and the industry,” said Candy.

AT&T is a little over two years into this program. At this point, each employee has a prescriptive program managed through a learning portal – it identifies the role they are in currently, the one they target the future, the associated competencies for each role and the learning and education path to get there. For example, an employee could be in the network center and want to be a software engineer, and has a learning path mapped out.

The nuances of the skill areas also change quickly. “It used to be that skills would change a decade at a time, and that’s now accelerated,” said Candy. AT&T designed a program that would offer a number of options and flexibility – from internal designed and led courses, to “nano-degrees” in niche areas like web development and virtual reality to online master’s degrees from Georgia Tech and social-media based programs with badges (157,000 options) awarded as people complete courses.

Investing in future skills is of value to the employee and the company

This plan is mapped to what roles that AT&T believes it needs to have in the future…. so employees can look for open roles and bid on the ones they want to fill. There are no guarantees that these roles will be filled by employees desiring them at AT&T, but the program still provides an advantage to the employee since AT&T is defining these roles (such as data scientist) with a forward-looking view, and therefore helping employees develop these competitive and marketable skills. Certainly, having invested in the person’s training, AT&T has an interest in keeping these people in-house and this is a way of creating loyalty, stickiness and a workforce of the future.

This kind of investment can help a company attract and keep the “best and brightest” with the most potential for helping grow a company. Individuals who feel a company cares enough to invest in their talent development, keep their skills relevant (and competitive), and give them options in a career are more likely to stay with that company. AT&T also will have skills relevant to the future – the future workforce – without having to go out and ‘find them’.

The bottom-line: Become a learning organization in order to be relevant to your customer base, stay competitive, and grow.

Take a look at the vision for your company. What do you want to be able to deliver to your customers? What experience do you want to create for them? What outcomes matter over time? Determine what roles and competencies, and what training, education, and mentoring will develop your workforce to achieve it.

Businesses need to be increasingly agile to address the rapid changes driven by consumer expectations and digital technologies. That means employees also need to be agile – and managed in a way that encourages and rewards-based learning. The market is increasingly competitive for candidates who have future-oriented “soft skills” like critical thinking, problem-solving, and creativity, and the ability and interest in learning. This program provides a model for how a well-established, “legacy” brand can embrace a learning culture to enable an agile workforce relevant for competitively positioning the company for growth long-term.