Biden’s keynote could not come at a more opportune time. Agentic technology dominates business conversations, blurring the lines between humans and technology and between services and software. Under the monicker of “The Agentic President,” The former President will address the HFS audience of technology and business leaders to help them grasp these huge opportunities agentic AI presents for the US economy. Millions of jobs are pointed to be brought back onshore because operations will be executed by supercharged agentic humans, with their employers avoiding burdensome tariffs.

If you want to reserve your spot to hear the Agentic President’s Address, click here now.

Commenting on his keynote, Biden stated, “While it’s a tragedy I lost the election, I’m delighted I can give back to the US economy by promoting America as the agentic capital of the world. We’re teetering on the precipice of change to bring both white and blue-collar jobs back to the USA. It’s time to build back better and make America become super-charged once again.”

The Summit will be held at New York’s Apella Hotel, on 7-8th May situation right next to the UN Headquarters on the East River, where HFS CEO, Phil Fersht, hopes to send a strong message to world leaders: “The line between software and services is blurring, and we need to make sure the US stays on the right side of history as machines take over the back office”, he stated earlier today.

Biden’s agentic assistant, Gemini Joe, will deliver some of his key messages as part of his address. “I just wish I’d discovered Gemini before that darned debate, and we’d still be friends with Canada,” added Biden. Plus, I could have sent him to Greenland, and he wouldn’t complain about the cold.”

Maybe it’s my generation, but I remember when going to work was fun, and you actually wanted to take on new projects and assignments to gain more experience and impress your colleagues and bosses.

We’re living amid an abundance of work avoidance

Today, it feels like so many people have flipped a full 180 degrees where they expend all their energies looking to take credit for everything possible while claiming they are just so damned swamped to take on anything new. Why actually do work to impress people when you can just pretend you do?

We’ve somehow arrived in an era when many people seem content to spend a few hours a day sitting in a few virtual meetings while avoiding actually doing anything. Most people have figured out how to game the system, inserting themselves into conversations to make it look like they are super-productive and irreplaceable when, in reality, they do very little.

Too many of us have become AI imposters

There is no worse example than the last two years of utter AI nonsense we’ve been fed from the vast majority of senior executives, tech marketers, politicians, and even some academics. I’ve lost count of the number of imposters getting up on stage preaching to the world about how our jobs and very livelihoods are about to be replaced, augmented, agentified, and ultimately decimated by AI. But it’s all OK, folks, because we humans will find new jobs that AI will somehow magically create. ChatGPT pro is going to supercharge us into these amazing people who are going to be so much smarter than we are today. Just spend that $200 a month to feel ahead of the AI monster snapping at our heels, and all will be fine…

So what’s the actual point in working hard when we can do what we need with a few prompts and pretend we’re clever? What’s the point in being passionate about our jobs anymore when we can just fake success, turn on our “Out of Offices” and binge-watch White Lotus in bed?

It’s not that we don’t have the time, we just don’t have the passion

Seriously, I despair of the number of people these days who just refuse to take on new projects and invest time to train themselves to do their jobs better, all under the guise that they “simply do not have the time.” I call bullshit on this. People who claim they don’t have the time are really saying they don’t have the passion. If someone asked you to prepare a presentation for a client who was going to take you to a Taylor Swift concert that evening, I bet you’d magically carve out some precious hours and free up your evening… because that actually gets you excited.

The Bottom Line: It’s time for a big professional reset to escape our humanist recession

So how can we get excited about our jobs again and reignite our passion for what we do?

Let’s face reality, everyone. The world has changed, and we’ve found ourselves facing a humanist recession. We need to become less depressed about AI coming for our jobs, about that long-awaited recession, and about weird politics breaking apart families and friendships.

We have to reset our current work habits and refocus on our futures. Otherwise, we’ll withdraw more and more into a world where we’re becoming imposters. We must embrace change, refuel our passions, and tune out all the rhetoric and noise.

My advice is to focus on building closer work relationships, get out more, and meet more people. Working with people, locking heads, building friendships, sharing experiences… this is what energizes us. At the end of the day, we’re all mammals, and we need each other.

Let’s take the time to learn new things, new tools, and new business theories. Sitting behind a computer for 8 hours a day is burning us out and sapping our passion and enthusiasm for what we do.

So let’s make it real and lean into our colleagues, clients, friends, and partners. Let’s make work fun again!

Miss the good old days when everything was fine as long as the economy was good? Today we need to fight our inner FOBO… our Fear of Becoming Obsolete.

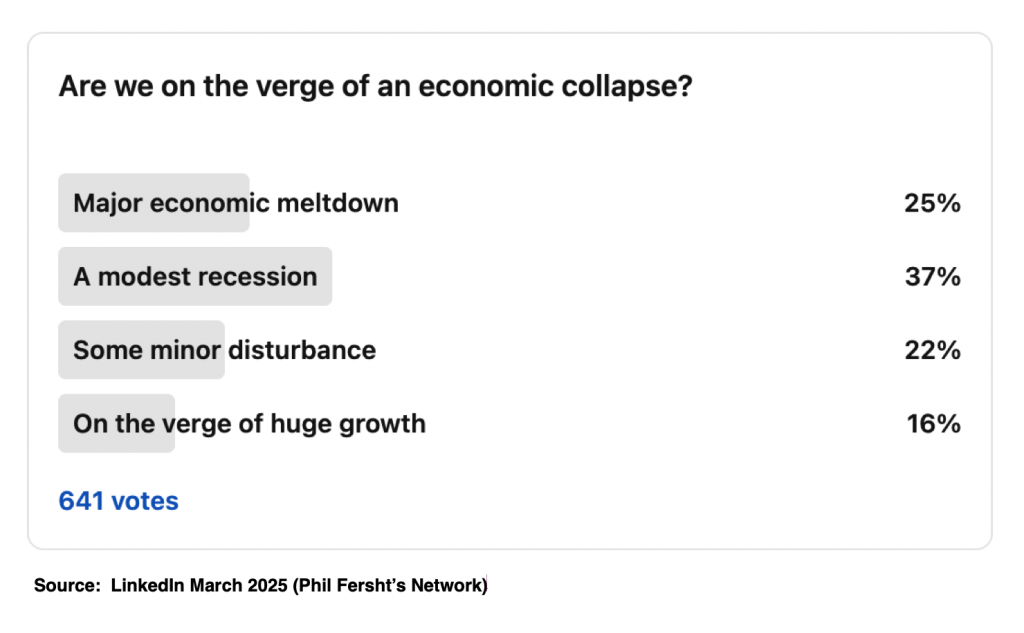

We hate to be the bearer of bad news, but we have far more to worry about these days than just the economy, where only 16% us are bullish about our economic future:

An overwhelming majority expect some form of economic turbulence in the coming months. Escalating geopolitical tensions, combined with unpredictable politics is making the world feel unstable, and that nagging feeling that a long-overdue global economic recession is surely looming, is weighing on our minds and causing many of us to spiral into a swirl of negativity. Today’s uncertainties are far more than economic. Political uncertainty, economic fears and the threat of AI taking over jobs has created a triumvirate of tension that is impacting our very psyches, dampening our excitement for the future and hovering over us like a dark cloud.

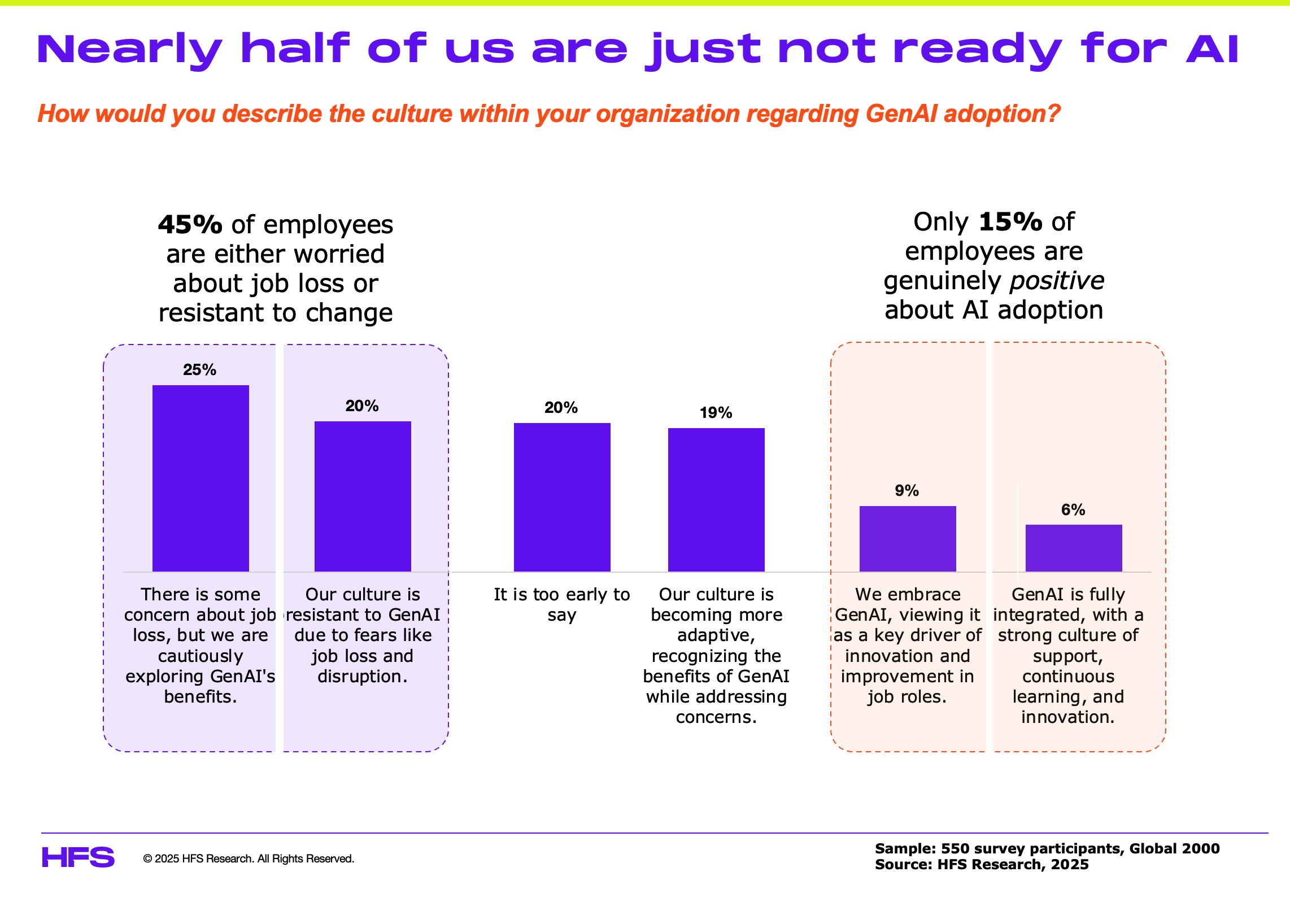

Be paranoid—we should be… as almost half of today’s employees are worried about AI in the workplace

When you think about all the stuff we wanted to do with RPA but couldn’t, which we can now do with agentic software, it’s getting easier and easier to realize that big chunks of our jobs can be replicated into software. As we advance along the AI continuum, the fear of being left behind is accelerating:

AI can either significantly enhance or completely automate tasks, such as pulling information from one screen to another, mining data and information to address issues, performing deep research, planning campaigns, reports, presentations, etc.

However, we are still aways from where we can confidently state that significant AI-driven automation has been achieved. Our recent study of 550 AI decision-makers across the Global 2000 details that almost half of us are simply miles behind in being ready to embrace GenAI, while only 15% are actually embracing it:

Fear AI making you obsolete… it’s smart to be AI paranoid. Embrace it and it may just open new doors for yourself. Ignore it, and someone more AI-literate than you is waiting to step into your job.

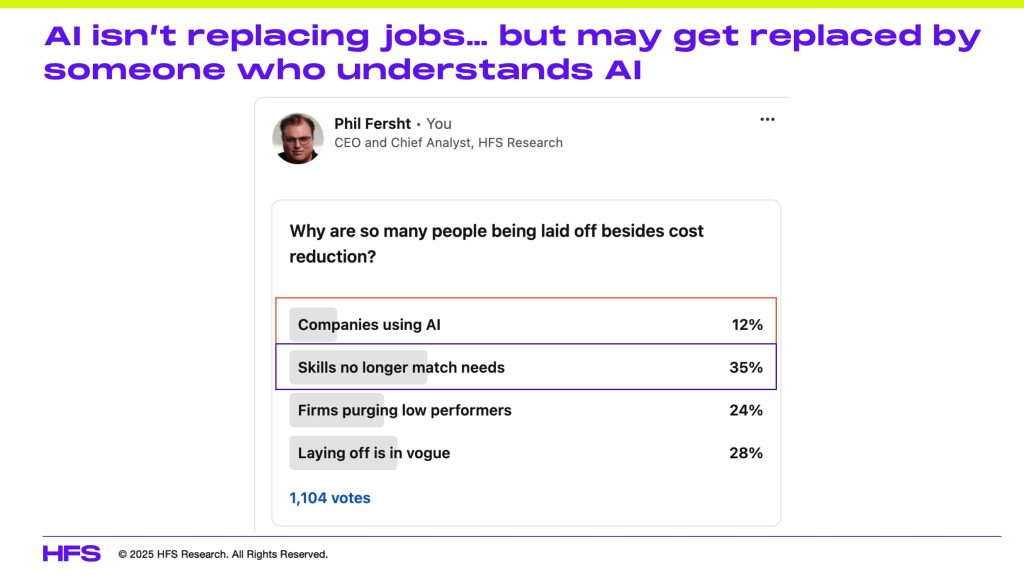

Let’s cut to the chase: If you give in to your FOBO (Fear Of Becoming Obsolete), you know you’re sitting on a ticking time bomb. Most F500 CIOs are under intense pressure to deliver genuine AI capability to their peers and bosses (per the 15% above), and executives who are failing to get with the program are under increasing scrutiny, as highlighted by a recent LinkedIn poll of over 1100 tech-centric executives:

Despite the realization that AI is here to stay and will have a significant impact on the future of the workforce as we know it, a large portion of investments around AI adoption are purely reactive rather than proactive; most are made without a clear understanding of where and how to apply AI for maximum gains – efficiency or cost – resulting in haphazard applications and unrealistic expectations. And what happens when these pilots fail to deliver or are unable to scale? Heads roll, projects are scrapped, and valuable time and resources are lost, bringing us back to the square one where cost-savings becomes number one priority while focus on innovation is lost.

Bottom-line: You can’t control geopolitics or the economy, but you can become an AI warrior to maximise your value and break out of your current predicament

You can blame your company’s culture or your management’s cynical approach to cost-cutting as being the key reason behind failed AI experiments, but ultimately, you need to train yourself to be an AI warrior, unafraid of the battles ahead, to stay relevant, creative, collaborative, and completely irreplaceable. You can’t control today’s volatile economics and politics, but you can control your relevance to your own organization, or to other firms if your current firm is fading into the past. So, invest in AI education – or go fund it yourself if your organization is too cheap. Make sure you understand these emerging GenAI and agentic tools tools, such as Perplexity, ChatGPT, Claude, Gemini, Moveworks, Beam etc, and how they can help you create content, analyze data, write code, design graphics, design cross-system orchestration, create action validation workflows.

Google has struggled for years to sink real teeth into the enterprise, but it may have just found its path to take on Microsoft and AWS as an AI cyber giant and gain real relevance as an enterprise cloud AI platform. This massive acquisition of Wiz also firmly positions Google directly against cyber vendors, namely Palo Alto Networks and CrowdStrike.

Google’s $32 billion valuation represents an exceptional premium, about 90x Wiz’s reported $350 million ARR. The significant valuation increase from Google’s $23 billion offer underscores both competitive urgency and strategic foresight, driven by Wiz’s rapid growth trajectory and market adoption and the Trump administration’s friendlier stance towards big M&A.

It is also worth noting that the US Administration deprioritizing its cyber focus on foreign actors means companies will need to be extra vigilant in protecting their data and assets. This acquisition could prove very timely for team Google, especially with the huge client list of Wiz clients it can try to tempt over to Google Cloud. If it plays this well, Google could end up closing this gap to both AWS and Microsoft in the enterprise AI platform market as cloud, cyber, and AI become completely intertwined. However, with AWS dominating a third of the global cloud market and Google barely having more than 10%, Google will have to tread carefully to avoid alienating the vast portfolio of Wiz customers. It has to prove to its new Wiz cyber clients it can be cloud-agnostic to optimize this massive investment.

Why are we bullish on this move?

Google’s biggest opportunity with this acquisition can be establishing itself as a leading multi-cloud security provider (leveraging Wiz’s advanced AI-driven technology and Security Graph, which identifies complex risk patterns across cloud environments). This will further support Google’s strategy to diversify revenue streams beyond advertising. Google has strategically focused on cybersecurity since 2022 (because of the acquisitions of two cyber firms). Google can deliver built-in security solutions without relying on third-party integrations, unlike its competitors (AWS and Microsoft Azure).

What are Google’s main challenges with Wiz?

On the tech side, one integration challenge will be migrating Wiz’s backend onto GCP. Wiz, as a startup, is hosted across many different clouds. Post-acquisition, it would make sense for many customers to run Wiz’s services on GCP for cost and synergy. However, if the migration is not handled carefully, it will disrupt existing customers. In addition, many Wiz customers will not want to move onto GCP, so Google needs to carefully manage its new portfolio of Wiz customers to allow them to use whatever clouds they want without risking alienating them.

The company’s previous largest acquisition, Motorola Mobility, for $12.5 billion in 2012, ultimately resulted in Google selling most of Motorola’s assets to Lenovo for $2.91 billion just two years later. This raised a question about Google’s integration capabilities. Google has allocated up to $1 billion in retention bonuses to retain Wiz’s critical talent, recognizing the importance of preserving the startup’s entrepreneurial culture and innovation velocity within Google’s more structured corporate environment.

Wiz’s strategic appointment of Anil Bhasin as India head underscores significant growth opportunities in India’s rapidly expanding cloud security market. Wiz’s proactive approach includes extensive local hiring and collaboration with regional enterprises and government initiatives, strengthening its position as a significant regional cybersecurity partner.

And the strategic rationale behind this mega acquisition…

Google’s strategic imperative centers around enhancing cloud security capabilities. This is driven by increased enterprise investment in cybersecurity, especially following significant incidents like the 2024 CrowdStrike outage, which heightened industry awareness of cloud vulnerabilities. Wiz’s Cloud-Native Application Protection Platform (CNAPP) significantly enhances Google’s offerings by integrating advanced AI-powered tools to identify and remediate complex vulnerabilities across multi-cloud environments, aligning with Google’s AI-centric approach.

This acquisition further supports Google’s strategy to diversify revenue streams beyond advertising, subtly positioning it against competitors such as Microsoft, whose cybersecurity business alone generates over $20 billion annually. Notably, Google’s strategic focus on cybersecurity was previously reinforced by acquisitions of Siemplify and Mandiant in 2022 for approximately $500 million and $5.4 billion, respectively.

The core technical and product integration challenges

Wiz’s unique Security Graph architecture is central to its differentiation. It comprehensively maps cloud infrastructures to identify and address toxic risk combinations and vulnerabilities that traditional security tools often overlook. As a Cloud-Native Application Protection Platform (CNAPP), Wiz effectively integrates Cloud Security Posture Management (CSPM), vulnerability detection, and identity risk analysis into one unified solution.

Wiz’s overarching platform is cloud-agnostic, developer-friendly, and deployable in minutes via simple API-based integration. This ease of deployment is critical for rapid adoption and effective management across diverse environments. Wiz’s multi-cloud posture management capabilities, comprehensive risk graph, and innovative AI-driven security services address significant gaps within existing offerings.

Integrating into Google’s ecosystem involves addressing multiple technical challenges, such as migrating Wiz’s backend onto Google Cloud infrastructure for cost efficiencies and operational synergies without disrupting existing services. Aligning Wiz’s advanced Security Graph and data models with Google Cloud’s existing asset inventory systems and services like the Security Command Center (SCC) will be complex. Google may rationalize overlapping functionalities within its current security offerings to ensure seamless user experiences, including unified login, authentication, and consolidated billing.

How does this impact the cybersecurity competitive landscape?

The acquisition significantly reshapes competitive dynamics. Google’s enhanced security capabilities put considerable pressure on AWS and Microsoft Azure. AWS, traditionally reliant on internal security solutions and third-party integrations, may need to accelerate improvements in its native security tools or pursue strategic acquisitions of similar agentless, multi-cloud security platforms. Microsoft Azure, with its extensive but traditionally more siloed security ecosystem, also faces intensified pressure to innovate rapidly, particularly in comprehensive risk analytics and AI-driven vulnerability management.

Cybersecurity vendors like Palo Alto Networks and CrowdStrike confront heightened competitive pressures. Google’s acquisition may prompt further market consolidation or drive independent cybersecurity firms to form strategic alliances with other cloud service providers or major technology firms to remain competitive. In the short term, we can expect a significant valuation jump for many of the cloud-native security vendors such as Eclypses, Crypto4A (creating quantum-safe keys that are NIST and Quantum approved), Wallarm (API security), Crowdstrike (even with their fumble, they are one to beat), Sysdig (microservices/container security) and a host of others.

The bottom line: All the major tech players need to up their cyber game and join this acquisition frenzy

Google’s acquisition of Wiz significantly enhances its competitive position in cloud security, providing advanced, AI-enhanced capabilities across multiple clouds. Successfully navigating technical integration challenges and regulatory scrutiny will be essential. Ultimately, the success of this acquisition will largely depend on the effectiveness of execution, potentially reshaping competitive dynamics across cloud computing and cybersecurity industries and emphasizing the critical role of innovative security solutions in enterprise technology ecosystems.

Cyber is very complex and AWS, Google, MSFT, Oracle, and IBM will likely all need to go on the acquisition hunt for solutions that can be embedded into their offerings. Apple, HPE, Dell Technologies, and Lenovo will all likely join the hunt as well.

Trade wars used to be fought with ships and embargoes. Today, they’re waged with tariffs, regulatory chokeholds, and digital sovereignty laws. The US and China have been throwing economic punches for years. Europe has fortified its own walled garden with GDPR and AI regulations, and the new US administration has intensified trade tensions with Canada and Mexico. However, amid the geopolitical chaos, ambitious CEOs and CIOs see a huge opportunity to rise above the noise and exploit the rapid advances in AI and automation technology (Services-as-Software) to ensure their organizations remain competitive, with agents supercharging their workforces.

Protectionism is reinventing how services will be delivered to your organization

As a CIO, you must prepare for the impact: rising costs for offshore/nearshore talent, imminent price hikes on technology hardware and software, delayed hardware shipments, and service providers suddenly subjected to new regulatory constraints. But protectionism isn’t just disrupting your current vendor relationships—it’s fundamentally transforming how services will be delivered to your organization.

The more governments try to lock down supply chains, labor markets, and data flows, service providers are left with no choice but to accelerate their shift toward Services-as-Software (SaS). By automating and digitizing service delivery, they’re reducing their reliance on people, physical goods, and traditional offshoring models, and this will change how you consume and integrate professional services across your organization. Savvy service providers will shift the delivery of software-based services to the US (or whatever location avoids financial penalties) to give their clients services unencumbered by government interference.

Isolationist policies force businesses to radically rethink their access to talent, technology and resilience

Governments pushing protectionist policies are stuck in a pre-World War II old-world paradigm, where economic strength comes from manufacturing dominance and self-sufficiency. But the world doesn’t work that way anymore. The Internet has woven supply chains and commerce so tightly together that there’s no undoing interdependence. Yet, leaders are doubling down on restrictions that force businesses to rethink how they access talent, technology, and supply chains.

Higher tariffs don’t just raise costs—they force automation. Companies aren’t waiting around for trade deals to stabilize. If importing materials, talent, or services becomes too expensive, they don’t just “buy local”—they digitize, automate, or move to neutral zones where protectionist policies don’t apply.

Global supply chains are too complex to rewind. Cutting off trade doesn’t make them simpler—it makes them unpredictable. Businesses are already restructuring operations around AI, automation, and nearshoring, not because they want to but because they can’t afford to be caught in the next tariff war.

Regulatory barriers don’t protect industries—they push them toward digital models. Businesses don’t wait for favorable policies; they engineer workarounds. The more fragmented the regulatory landscape becomes, the more companies rely on software-driven services that make national borders irrelevant.

The loudest advocates for economic independence are still deeply dependent on global markets. China pushes self-reliance but still relies on foreign semiconductors and global exports. The U.S. is doubling down on tariffs for key imports—steel, aluminum, electric vehicles—while still needing foreign critical minerals, pharmaceuticals, and offshore manufacturing.

Protectionism isn’t making industries stronger—it’s forcing them to become leaner, faster, and more reliant on technology instead of people. And that’s where Services-as-Software comes in.

Protectionism creates a compelling opportunity for CIOs with SaS

When governments raise trade barriers, service providers don’t wait for a diplomatic resolution—they adapt. Increasingly, the adaptation strategy is Services-as-Software—the shift from human-dependent services to fully automated, software-driven solutions:

We’ve seen this playbook before. The first industrial revolution mechanized labor, the second optimized mass production, and the third digitized processes. Now, we’re in the next phase—the automation of services, where routine work that once required people, physical goods, and often cross-border transactions is being rewritten as code. Professional IT and business services companies such as Infosys, IBM, Genpact, Cognizant, KPMG, and Accenture are already repositioning their strategies to align with this vision.

But this SaS shift isn’t just about avoiding tariffs or dodging supply chain constraints—it’s transforming how value is created and delivered. All these protectionist policies are doing is accelerating the development of SaS because of the following:

Weakening dependence on offshore labor: AI-powered services eliminate the need for massive offshore teams, cutting exposure to labor costs and visa restrictions. In many instances, scaled-down onshore teams supporting a SaS model can perform the same work at similar or even less cost and arguably increase analytical value.

Automated compliance at scale: Software-driven services embed compliance into the code instead of navigating country-by-country regulations.

Resilient, tariff-proof supply chains: Businesses that once relied on imports can now deliver services via cloud-based automation, skipping geopolitical bottlenecks entirely.

The old playbook—offshoring to low-cost regions—is likely being replaced with software-first service delivery. The big question is whether the human element of services remains offshore or if the cost benefits encourage services to move onshore or be eliminated. CIOs must rethink their vendor relationships because how they buy and integrate services are fundamentally changing. They need partners aligned with their needs to support their transformation path to SaS.

CIOs must adapt as services shift from people to code

When electric and hybrid vehicles entered mainstream consumer markets, dealerships needed to retrain their staff to understand how to sell and maintain them in addition to traditional gas vehicles. The same is happening with SaS models entering the enterprise equation. CIOs should adapt their knowledge and skills to program work types into software applications, work with their C-Suite counterparts to drive the process, and support the significant change management aspects involved. It’s one thing to move work from onshore people to offshore people. It’s an entirely different proposition to move work from people to computers.

CIOs must understand the implications for their operations, technology strategies, and vendor relationships:

Changing commercial models: Traditional FTE-based pricing structures are giving way to subscription and consumption-based models, which may require different budgeting, procurement, and governance approaches.

Shifting partnership dynamics: Relationships with consultants, systems integrators, and managed service providers are becoming more like SaaS vendor relationships, with significant implications for security, compliance, and integration.

New implementation challenges: As services become more automated, bridging business requirements and service outcomes requires different skills when platforms replace human intermediaries.

Integration considerations: Organizations need integration strategies for automated service platforms with embedded workflows rather than adapting offshore teams to existing processes.

New governance frameworks: When software—not people—delivers services, governance must shift from vendor relationship management to overseeing APIs, data flows, and automation.

Preparing for the SaS Future

CIOs should take proactive steps to get ahead of the shift:

Assess service automation potential: Identify which functions, processes, and services are primed for automation based on labor costs, regulatory exposure, and technology maturity.

Evolve procurement strategies: Redefine vendor selection and contracting models for SaS, shifting from FTE models to AI-driven service consumption.

Implement governance frameworks: Establish new oversight models focused on compliance, automation monitoring, and outcome-based service evaluation.

Develop integration capabilities: To prepare for a code-based service delivery model, build expertise in agentic AI, workflow orchestration, and automation-first architectures.

Align business expectations: Educate stakeholders on how service consumption patterns will evolve, ensuring that business units adapt to automation-driven service delivery.

Manage the AI fear and cultural impact:Recent HFS research shows that 45% of enterprise executives fear AI will take away their jobs and negatively impact company culture. CIOs must take charge by running AI boot camps to educate teams, showcase AI’s potential, and inspire a mindset shift toward AI-enabled roles.

SaS isn’t an island—enterprises still need ecosystems

Let’s be clear: while Services-as-Software may provide an escape hatch from protectionism, it doesn’t eliminate the need for interconnected ecosystems or people. AI and automation might replace some people, physical assets, and manual workflows, but they can’t substitute collaboration, shared data, and platform interoperability. No company operates in a vacuum, and no tech stack functions without dependencies.

The Bottom Line: CIOs must prepare for a world where many services are delivered through software, not people—protectionism is merely speeding up the inevitable

CIOs can’t afford to treat protectionism as just a policy shift—it’s fundamentally reshaping how services are delivered and consumed. The move toward Services-as-Software is accelerating, forcing enterprises to rethink vendor relationships, integration strategies, and governance models.

There has never been a time during the last three decades that the world has seemed less flat…

Thirty years of the Internet and the rapid development of ubiquitous data, coupled with the emergence of developing nations hungry to support bloated greedy corporations, had led us to a place where employment has seamlessly moved to low-cost locations to support these corporations at much lower cost and scale than employing people locally.

Until recently, these corporations primarily favored contracting with third-party outsourcers to deliver this lower-cost work, but we have seen a marked swing toward many of them opting to hire offshore people directly into their own labor forces as part of what they are marketing as “Global Capability Centers.”

However which way we look at this, the basic premise has been the same: moving work to low-cost locations that can rapidly scale up to deliver that work. Whether it is more beneficial to employ people directly in low-cost locations or contract to have them deliver work through third parties isn’t really that important. The big question now is whether these corporations are going to have tariffs imposed for exporting corporate operations outside of the country that could be managed at home.

Suddenly, we find ourselves in a world where moving work around the world carries a lot more risk… and cost

In the past, when economies got tight, and corporates panicked, there was always the constant of sending more IT and process work to India, more manufacturing to China, or more customer support to the Philippines to keep operating costs down and CFOs at bay. However, there is now increasing concern from industry leaders that all their exports of work outside the US will come under the spotlight as the tariff programs get rolled out. The impact would ultimately result in big hikes in costs, which could be as high as the 25% level, considering the current tariffs that are being set. Why stop at Mexico, Canada, China, and the EU?

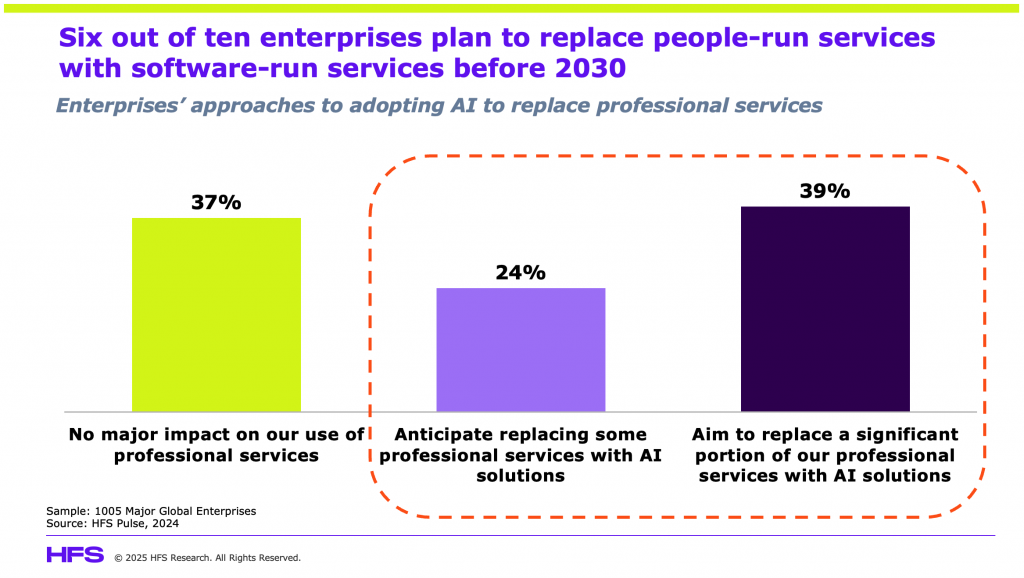

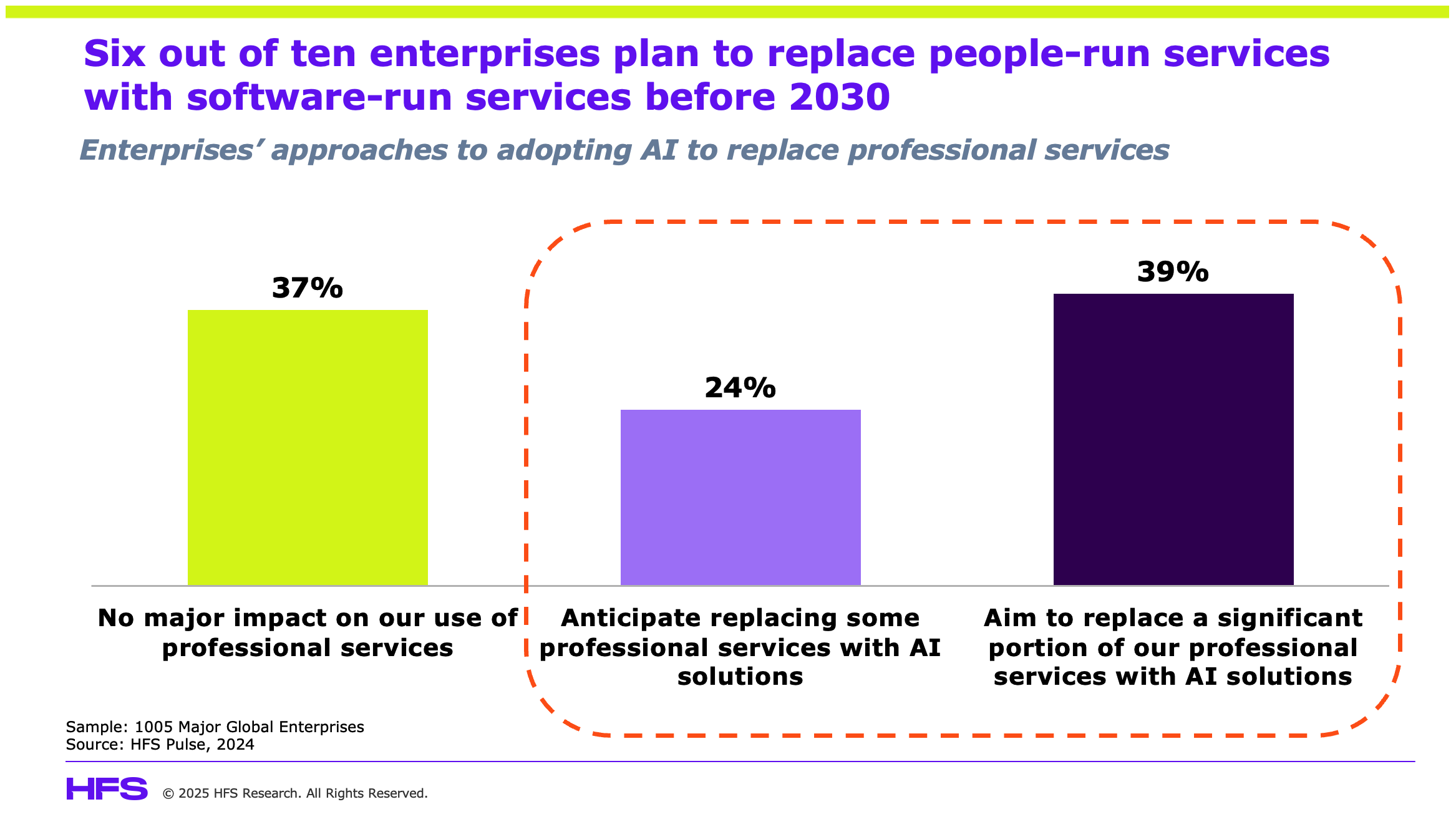

In our view at HFS, this will further drive the focus on AI-first services where increasing amounts of service provision are programmed into software platforms using agentic technology, generative AI, and other AI technologies. As we discussed recently, six out of ten enterprises are already serious about adopting an AI-first approach to professional services, so doesn’t this throw the whole location question out the window as the line between services and software increasingly blurs? If we are going to be buying supercharged agentic humans before long, so will the focus from people scale to outcomes:

We have already projected Services-as-Software presents a $1.5 trillion opportunity for both software and services firms, where enterprises stop buying static technology and people-intensive services and instead consume AI-powered, outcome-driven solutions that continuously evolve and adapt to changing business requirements. What we hadn’t projected were the locations that would benefit from this expenditure.

Why the US services option is becoming increasingly attractive

Already, Apple has announced $500 billion of investments in the US over the next four years as the firm seeks to get ahead of the political move away from globalization and the onset of these prohibitive tariffs. As we have seen with the succession of US-led enterprises renouncing their DEI strategies, surely we are poised for a wave of these corporations promising to move more of their jobs back to the US as they seek to curry favor with the Trump administration and also derisk their services supply chains exposed to global delivery strategies. Manufacturing, logistics, and retail sectors are already either slowing down hiring or shifting workforce priorities due to higher costs of imported goods. It is only a matter of time before other industries heavily reliant on global talent, such as financial services and hi-tech, seriously evaluate the penalties and risks of their globalized business operations.

Another factor to consider is the state of employment in the US, where a recent study from the Federal Reserve Bank of New York reported the widest unemployment gap between new graduates and experienced degree holders since the 1990s. In terms of MBA graduates, Harvard Business School has reported 23% of the 2024 MBA class remained jobless three months after graduation, a significant increase from 10% in 2022, while Wharton, Stanford, MIT, and Kellogg all report double-digit unemployment, well above previous years.

Bottom line: It’s time to brace ourselves as the future of global services may be about to go through some radical changes

Even if currently offshored services increase by ~20%, many will still be significantly cheaper than re-employing onshore as the wage costs are usually 30-70% higher. The short-term impact should be small, but we cannot ignore the longer-term effect, especially for areas requiring skilled workers that can be highly effective when boosted by AI tech. When services that may have required, for example, 100 people in India, can be run with 20 skilled workers onshore, there are both significant geo-political and straight-up business cases to consider. The changing nature of the US workforce supports the possibility of services coming to the US as anxious businesses look to get ahead of global risk and uncertainty. Only a fool would ignore the magnitude of what is happening in our geopolitical landscape.

We’ve been talking about the impending disruption facing BPO for well over a decade now, as maturing AI and automation technologies promise to replace the masses of humanity hired to deal with customer queries, move data from one screen to another, process reams of invoices, claims, and many other office tasks. However, are we finally on the cusp of genuine secular change in the industry commonly known as “BPO”?

Will UnBPO succeed where Robotistan failed?

In fact, we went as far as introducing Robotistan as the new BPO location back in 2012 as RPA solutions launched themselves upon the industry. Somehow, labor-centric BPO has managed to weather the storm as enterprises struggled to scale the technology to do anything beyond piecemeal task automation, hence our declaration of RPA death in 2019. However, as enterprises have gradually run out of excess onshore labor to be replicated offshore, the BPO industry has slowed down considerably, and the only room for further value in the model is to shift away from moving work from humans to lower-wage humans by moving that same work to software.

The industry has been ripe for this transition for many years, but it’s the rapid rise of agentic technology to mimic human work that is about to make the pivotal assault that finally forces the industry to change. The technology is finally here, and there is nowhere left to hide. In short, the rise of GenAI, automation, and digital-native competitors is making legacy BPO look like a relic, and the old model—offshoring, labor arbitrage, FTE pricing—is on life support. Firstsource is betting its future on a radical alternative: “UnBPO.”

CEO Ritesh Idnani, a BPO veteran who has lived and breathed every flavor of BPO for the last two+ decades, unveiled this bold vision at the Emergence customer event, making it clear that this isn’t just another incremental shift, it’s a demolition job on the traditional BPO model. The ambition is for AI-first, networked, outcome-driven operations that render legacy paradigms obsolete. The tenets laid out in the UnBPO playbook are well aligned with the guidance HFS has been giving the industry, and the seeds of real change are being planted with some of the shifts Firstsource is making to its organization and client engagements. But execution is everything. Can Firstsource and the industry make the leap, or is this just another rebranding exercise?

Firstsource CEO Ritesh Idnani unveils Firstsource as the UnBPO Company

The future workforce has to unlearn — there’s no patience for legacy thinking

Forget offshore, nearshore, or onshore. Work has no borders anymore. Firstsource is throwing out the outdated “location strategy” playbook, embracing a truly global workforce where AI, automation, and human expertise operate in sync. The new model isn’t cheap labor, it’s technology arbitrage.

The company’s AI-first mantra—”data for AI, AI in everything, AI for everyone”—signals a pivot from cost-cutting to value creation. This is about augmentation, not elimination. One radical example is how Firstsource now uses AI bots to conduct all first-round hiring interviews. That’s not just automation, it’s rewriting how companies think about talent acquisition.

But talent strategy isn’t just about who does the work, it’s about how they learn, and traditional training models are facing potential extinction. Firstsource is betting on hyper-personalized skilling and real-time learning as a talent game-changer. They are forgoing static training programs in favor of guided decision-making, dynamic prompts, and AI-driven agent support in the moment. Firstsource’s workforce will need to unlearn outdated processes and mindsets quickly to keep up. As Idnani put it, “The only metric we want employees to think about is what value did you add to your customer today?” That’s the kind of metric that forces transformation—or exposes the cracks.

AI translation is smashing the global talent market. Location no longer matters.

One of the most disruptive forces in the contact center industry today is the rise of AI-driven language translation capabilities. If companies can use AI to remove language barriers, they can literally hire anywhere. Firstsource is already deploying live agent voice translation, meaning an agent in Bogotá can seamlessly serve a customer in Tokyo. This flattens the global talent market, unlocking labor pools previously off-limits due to language constraints.

This has profound implications for the BPO industry. For Firstsource, this is a competitive advantage—if it scales. But it also introduces risk. AI-driven translation depends on data quality, compliance, and regulatory alignment. Firstsource’s mission will be scaling AI translation without introducing compliance nightmares or degrading customer experience.

Firstsource aims to kill headcount-based pricing, focusing the customer on value, not “effort”

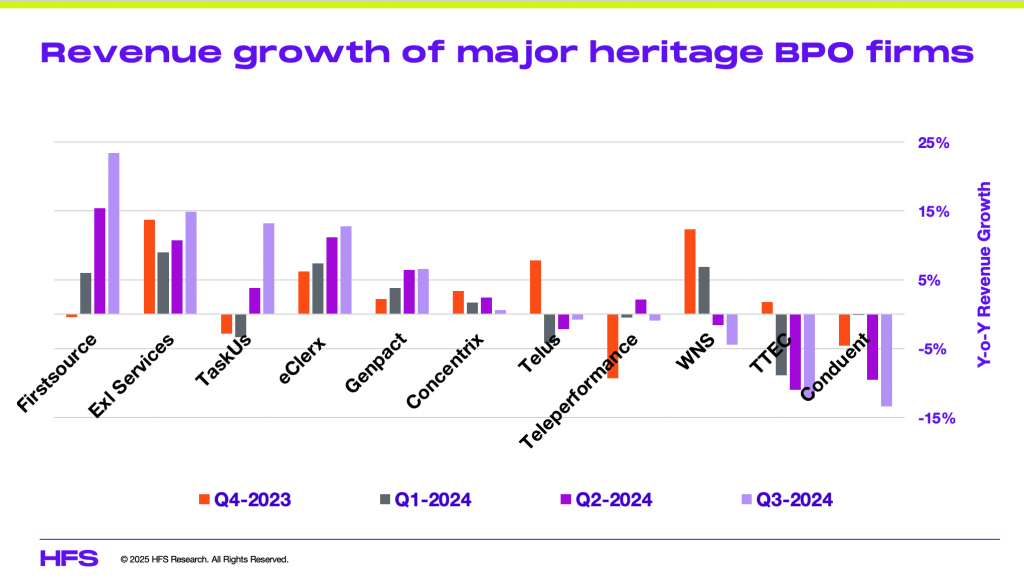

Perhaps the most aggressive part of Firstsource’s UnBPO model is its rejection of traditional BPO pricing. Firstsource is pushing for risk-sharing and outcome-based pricing—aligning revenue to value delivered, not hours worked. Firstsource is riding a wave of aggressive growth in 2024, outpacing struggling mid-tier competitors by doubling down on AI, automation, and digital CX (see chart below). Its strategic acquisitions—Ascensos, Quintessence, and AccunAI—signal a clear intent to lead, not follow. In our current market discussions, an increasing number of enterprises are far more open to an AI-first mindset to procuring services, with 6-out-of-10 declaring they are ready to move a large amount of their services into a services-as-software model by 2030. We are also seeing many enterprises start to value the services platform they are buying as opposed to the number of bodies required to execute for them. This is where the game finally changes for services as the customer focus shifts from effort to value.

This is surely the calm before the storm when enterprise customers are ready to UnBPO themselves

Furthermore, Firstsource’s rising headcount is a direct response to its business expansion, fueled by new client wins, strategic acquisitions, and an increasing demand for AI-augmented services. Unlike traditional BPOs that add headcount primarily for labor-intensive contracts, Firstsource’s growth strategy is tied to scaling its AI-first, automation-driven service model. But hypergrowth comes with high stakes. Scaling headcount while shifting to outcome-based pricing is a balancing act—one that introduces revenue unpredictability just as Firstsource is making massive bets on AI and workforce transformation. Clients love the concept, an many have declared they are ready to commit at scale. This is surely the calm before the storm when enterprise customers are ready to UnBPO themselves.

Firstsource’s UnBPO vision hits all the right notes, but the transformation is only just beginning. The growth tear that was 2024 indicates a good start. However, heavy AI investments, workforce restructuring, and non-linear revenue models create unpredictability. Investors and clients will be watching closely. The real test will be whether Firstsource can consistently deliver measurable outcomes enough to make this model viable in the long term.

The Bottom Line: AI is flattening the global workforce and upending BPO. UnBPO is a whole new way of thinking, working and partnering. Only the strong – and courageous – will survive.

Firstsource just put BPO on notice. It’s not just talking about transformation—it’s daring the entire industry to burn the old playbook.

AI is flattening the global workforce, killing off legacy BPO, and redefining what service delivery means. The challenge is execution. Firstsource’s vision is compelling, but it requires massive change to survive the brutal realities of enterprise adoption, financial sustainability, and workforce resistance. One thing is certain: BPO firms that cling to outdated models will be left in the dust. Firstsource has thrown down the gauntlet. Now the industry has to decide—evolve or be erased.

Prepare for a breakthrough year in the Generative Enterprise—powered by the potential of agentic AI to deliver end-to-end, self-improving, cross-silo processes to achieve business outcomes, the promise of deregulation, and greater access to the infrastructure of the Stargate program, and a new wave of LLM innovation exemplified by China’s DeepSeek.

There has never been more urgency to find the right services partner to match your firm’s ambitions. Our Generative Enterprise Services Horizons report 2025 identified several trends: how service providers are meeting enterprise needs, effectively training people, what enterprises need more of from their service partners, and what customers and partners have to say about their service experiences.

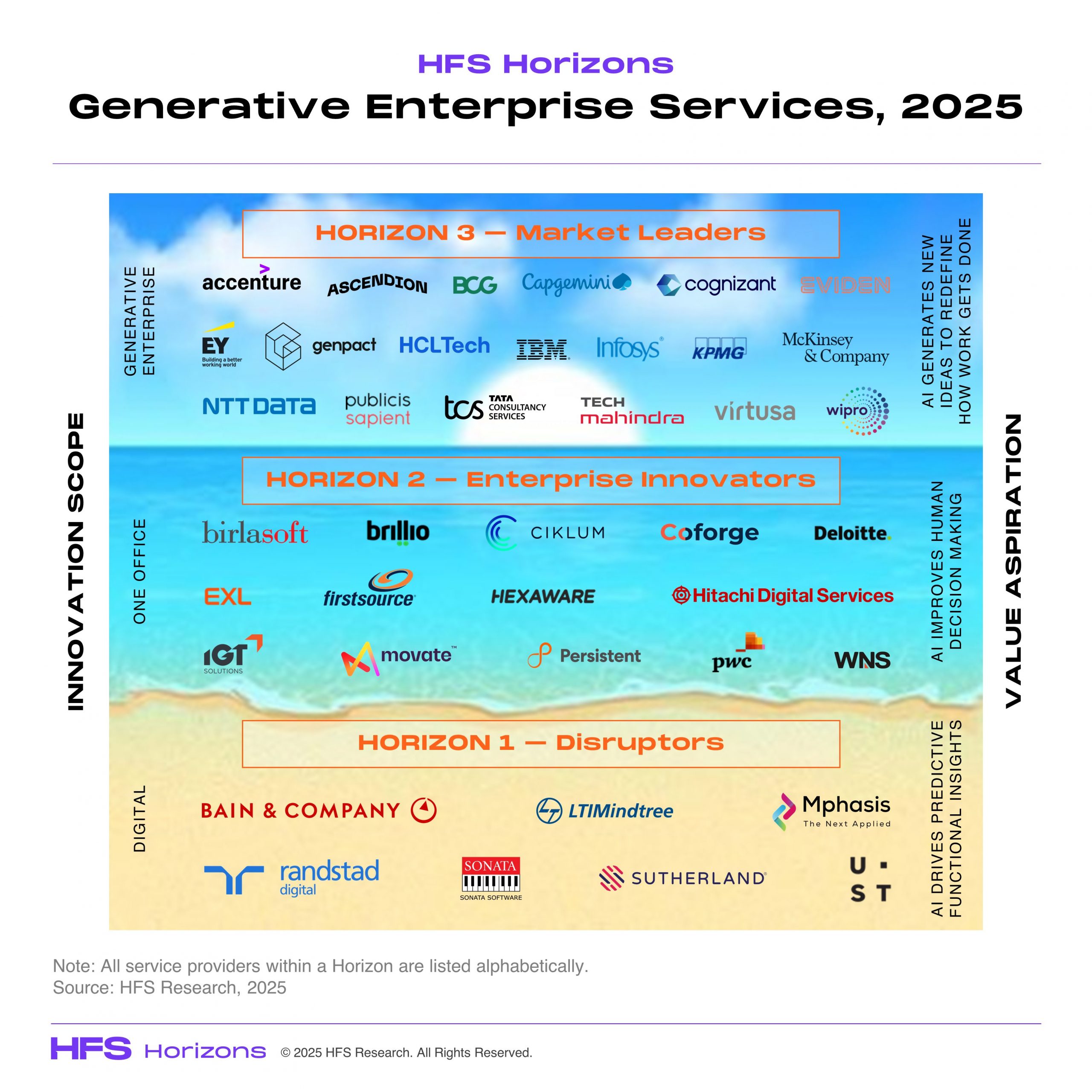

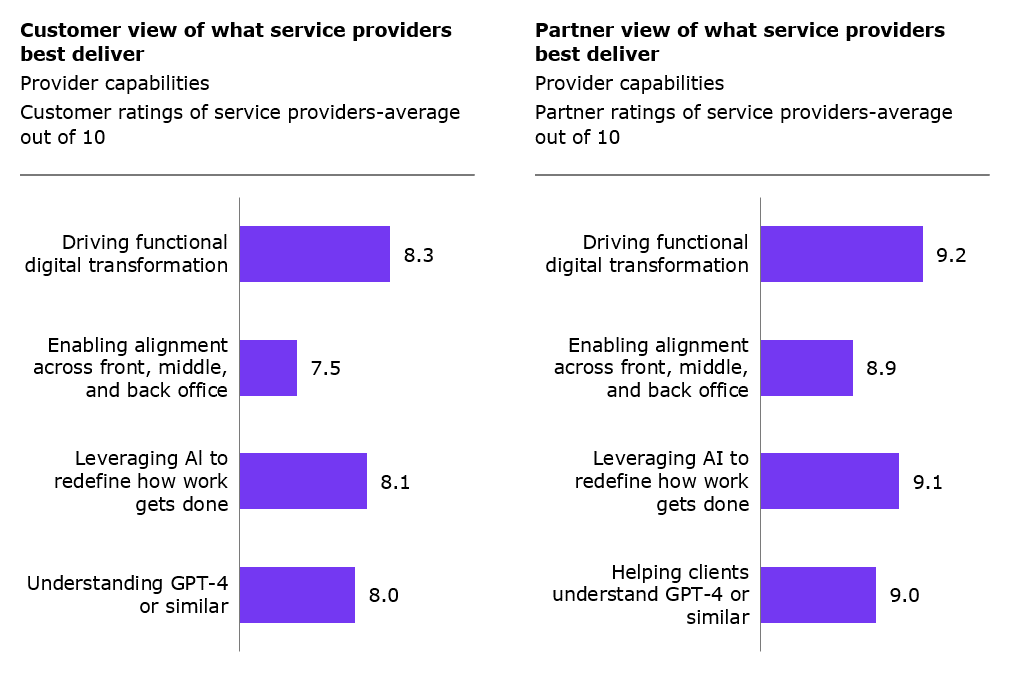

Who are the best Generative Enterprise service providers?

This report evaluates the capabilities of 40 service providers across the HFS Generative Enterprise value chain based on a range of dimensions to understand the why, what, how, and so what of their service offerings. It assesses how well service providers are helping their clients worldwide embrace innovation and realize value across three distinct Horizons: Horizon 1, optimization through functional digital change; Horizon 2, experience through end-to-end enterprise transformation; and Horizon 3, growth through ecosystem transformation (Exhibit 1).

Exhibit 1: The HFS Horizons model helps enterprises pick their service providers based on desired outcomes

We assessed these 40 service providers across their value propositions (the why), execution and innovation capabilities (the what), go-to-market strategy (the how), and market impact criteria (the so what). The Horizon 3 leaders (in alphabetical order) are Accenture, Ascendion, BCG, Capgemini, Cognizant, EY, Eviden, Genpact, HCLTech, IBM, Infosys, KPMG, McKinsey, NTT DATA, Publicis Sapient, TCS, Tech Mahindra, Virtusa, and Wipro. These service providers have demonstrated their ability to support various enterprises across the journey—from functional digital transformation through enterprise-wide modernization to creating new value through ecosystems. These leaders’ shared characteristics include deep expertise across the Generative Enterprise value chain; a full-service approach across consulting, IT, and operations; a strong focus on innovation, internally and externally with partners; co-innovation with clients and partners; and proven impact and outcomes with clients around the world.

A year is a (very) long time in the Generative Enterprise

When we published our 2023 Horizons report on Generative Enterprise Services (Q4, 2023), the gaps in capabilities and commitment across service providers were clearer. As we publish our 2025 Horizons report (Q1, 2025), those gaps have been compressed as demand for POCs and pilots has rocketed, and learning has been shared far and wide across the industry.

A year is a long time in the emergence of the Generative Enterprise. A year ago, agentic wasn’t even getting a name check. The LLM-capability arms race has continued with OpenAI, Meta, and Google all releasing multiple updates and new capabilities in text, image, and audio processing and taken a new twist with the arrival of DeepSeek. And now we have Trump’s Stargate for a boost to infrastructure, too.

Enterprises now demand business outcomes over experiments

Customers have shifted from initial experimentation to focusing GenAI’s capabilities on value outcomes. And that has led to the formalization of innovation pipelines in the enterprise – and integrated and repeatable offerings from service providers. But for all the formalization and standardization, there is no doubt we remain very early in this journey.

And while spending on GenAI is rising (HFS data suggests enterprise investment is rising by more than 25% on average into 2025), we start from a low base. We estimate enterprise spending on GenAI in 2024 accounted for less than 1% of global IT services spending. This is just one illustration of how far we still have to go.

Service providers are adding resources, expanding their ecosystems, and replacing labor with software

To help enterprises achieve the results they need with GenAI, services firms have continued to scale up their capabilities (by 250%) and extend their ecosystems.

Services firms are forming an increasing number of strategic alliances with large tech, cloud, and data companies such as NVIDIA, IBM, and Databricks to co-develop platforms, frameworks, and foundational capabilities; academic partners such as MIT and Stanford to further research the impact of GenAI; and niche AI players such as Hugging Face, Anthropic, Kore.ai, and Mistral AI to gain access to specialized AI capabilities such as fine-tuning.

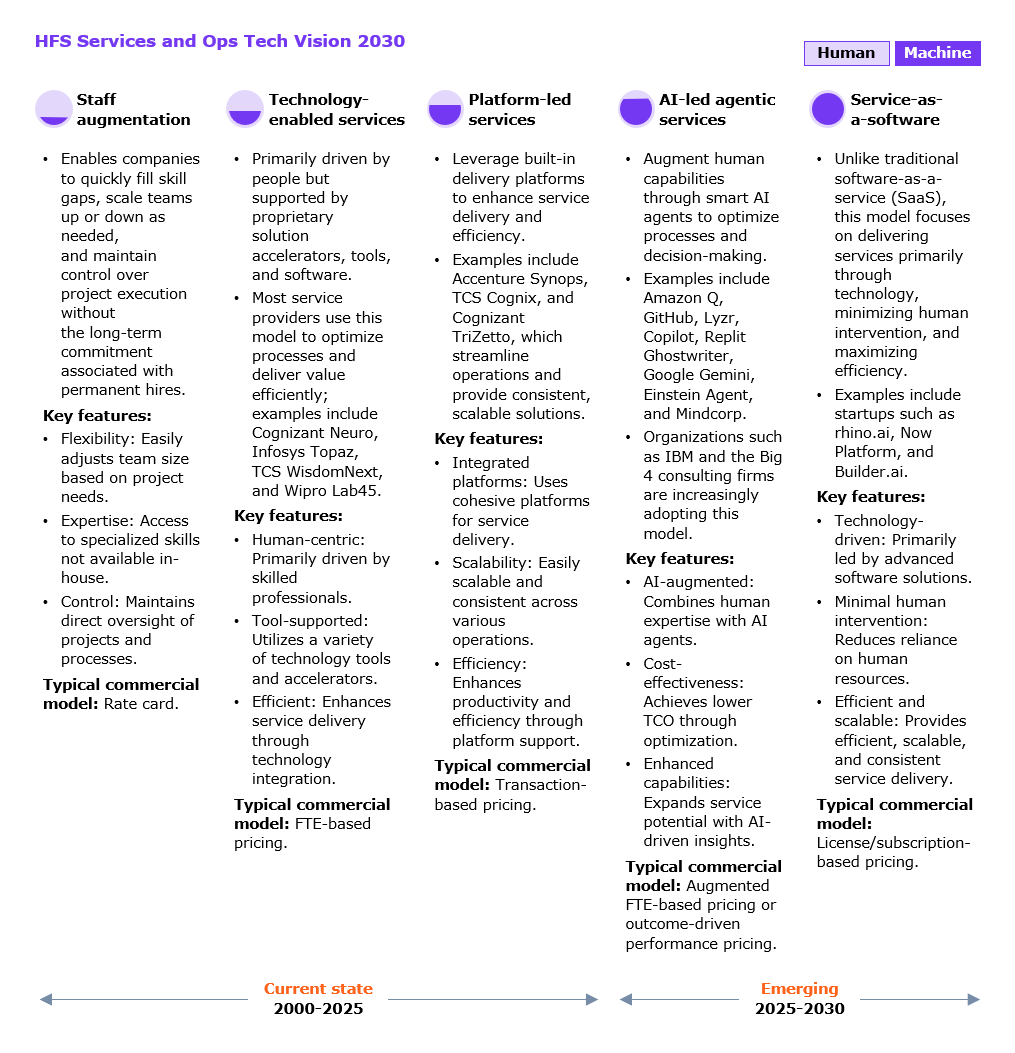

As services firms cozy up to tech providers, they become a little more like their tech partners—developing software solutions to replace work previously done by consultants. Examples such as SASVA from Persistent and Consulting Advantage from IBM illustrate the shift to the right HFS has been predicting in our Services-as-Software Vision 2030 (see Exhibit 2).

Exhibit 2: The lines between services and software are already blurring

Source: HFS Research, 2025

Enterprise-scale AI comes with new cost and control challenges

However, the examples of scaled success with GenAI remain scarce. Firms are stuck in a chicken-and-egg situation. Leaders must see ROI to take the leap and scale up their GenAI initiatives. Yet it is nearly impossible to prove value with just one or two POCs or pilots—such is the investment required to overcome data, privacy, and security concerns—let alone tackle the mountainous technical, skills, process, culture, and data debts accrued over decades.

The firms taking the leap to deliver at scale with GenAI soon hit cost and control issues—echoing the debates over the cloud. Many are learning that there is no single LLM solution to their enterprise needs—hence the rise of small language models (SLM) and models to support selection vs. accuracy, performance, and cost control, such as TCS’s WisdomNext platform.

DeepSeek is setting new expectations regarding training and related costs, and we expect market leaders to respond.

Data and technology debts restrict many firms to point solutions

Enterprise customers and service providers’ partners rate service providers strongest when driving functional digital transformations (see Exhibit 3). These transformations are mostly point solutions that help clients achieve greater efficiency or improved CX or EX. However, these point solutions rarely deliver new sources of value or redefine how work gets done, making it difficult to meet ROI requirements.

Data and technology gaps must be filled to enable the disruptive potential of GenAI to extend end-to-end across processes. Currently, service providers are rated less effective at delivering the alignment across front, middle, and back offices that cross-silo processes demand (see Exhibit 3). Enterprises must be prepared to tackle their data silos.

Exhibit 3: Service providers are rated weakest on enablingcross-silo alignment

Sample: 75 GenAI partners and 71 customer references as part of the survey for the report. Source: HFS Research, 2025

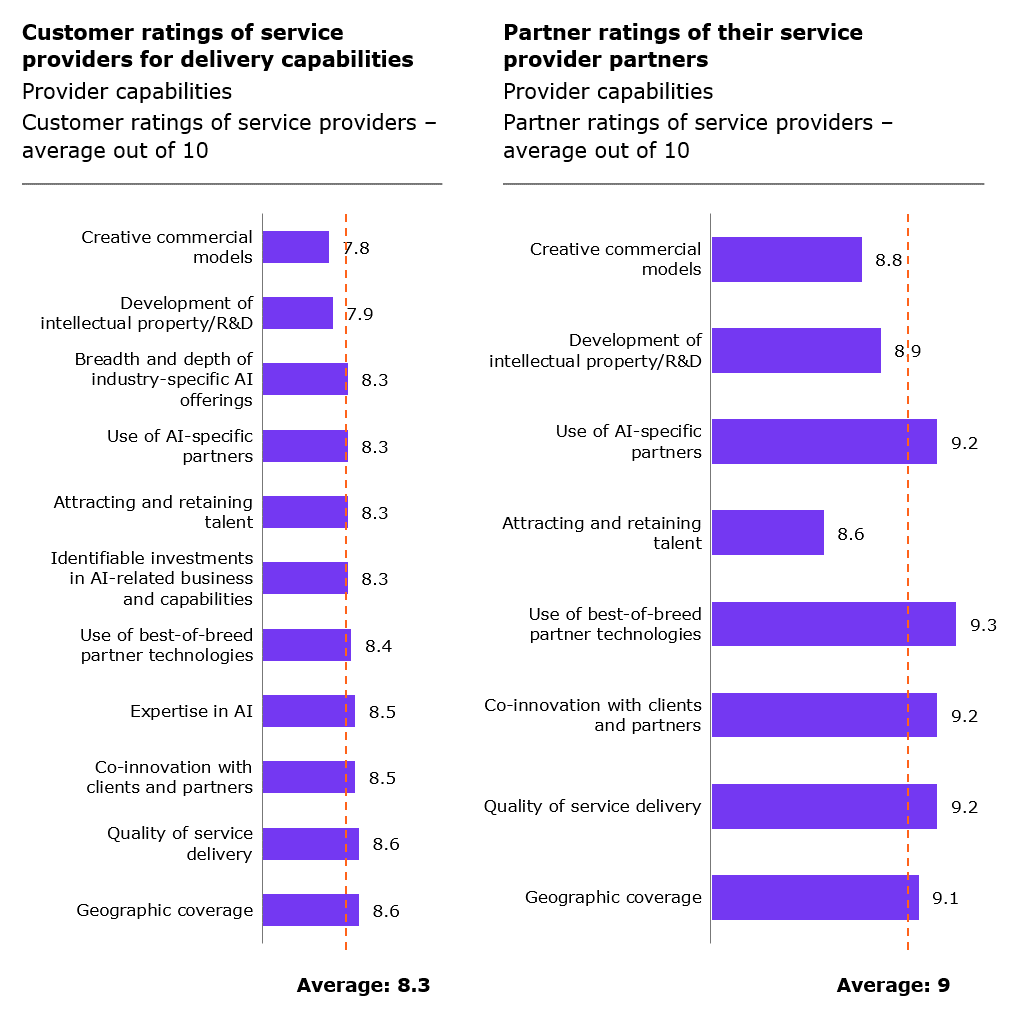

Talent supply is impacting the outcomes service providers can deliver for enterprises

Service providers have made huge investments in training employees on AI /GenAI; however, as seen in Exhibit 4, partners, in particular, have called out talent issues. The supply of AI / ML–experienced employees remains stretched, and a talent war is ongoing. Furthermore, customers and partners have indicated a greater need for creativity in commercial models and more GenAI-focused development of IP / R&D, including industry-specific AI offerings.

Exhibit 4: Service providers’ ability to attract the best AI talent is a concern for their partners and customers

Sample: 75 GenAI partners and 71 customer references as part of the survey for the report. Source: HFS Research, 2025

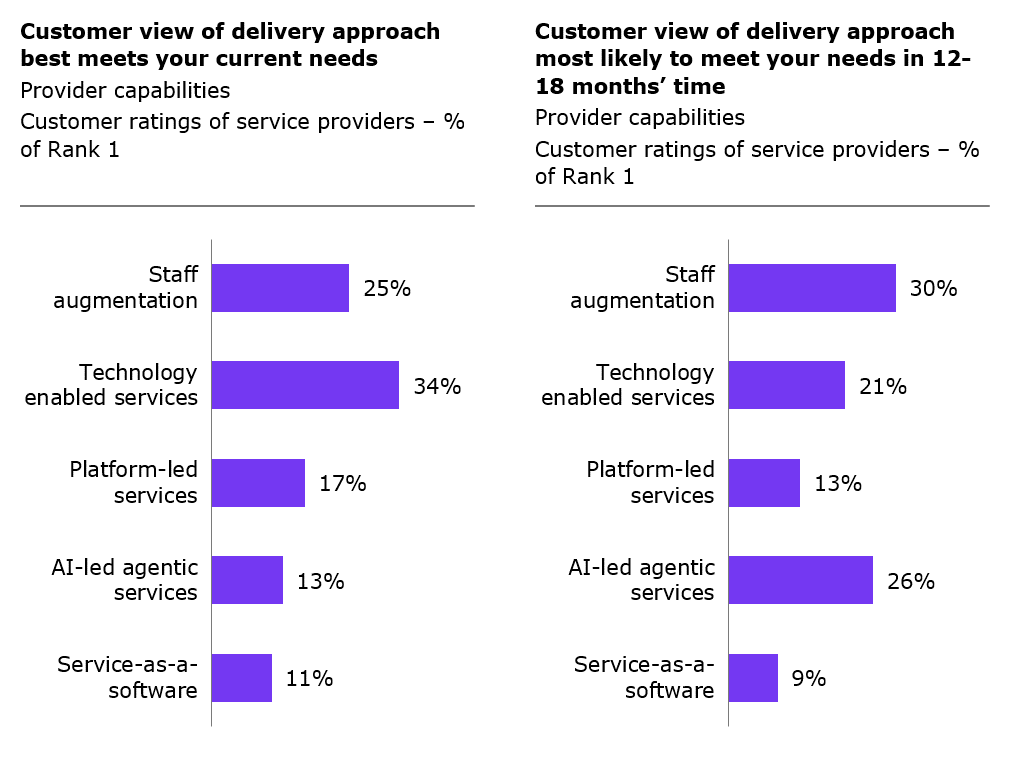

Agentic will be as essential as staff augmentation within 18 months

Currently, technology-enabled services and staff augmentation approaches are most in demand by customers. Within 18 months, customers’ service delivery preferences will shift, and autonomous AI-led agentic services handling complex decision-making tasks will be almost as important as staff augmentation (see Exhibit 5).

Services and software people come from different worlds and speak different languages, but they will need to come together—quickly—to align technology with business outcomes.

Exhibit 5: Customers expect agentic to play almost as large a part as staff augmentation within 18 months

Sample: 71 customer references as part of the survey for the report. Source: HFS Research, 2025

The Bottom Line: Choose a service provider that understands where your enterprise is on its Generative Enterprise journey—and is best positioned to meet you where you are.

It’s easy to be overwhelmed by possibility, excited by grand visions, and lose your way in pursuit of goals that are not within the current grasp of your organization.

When choosing your service provider partners, look for those who understand the business problems you face now. If your current problem is how to take the leap to scaling the impact of generative AI across the business, choose partners capable of supporting such ambition. But if you face more discrete and burning issues, be open to partners matching less ambitious outcomes. Solving the smaller problems is the route to preparing for the coming AI transformation.

Read our full Generative Enterprise Services Horizons Report 2025 – here to learn which service provider is best aligned with the results you want to achieve.

Have you been taking your FOBO pills? Because without a healthy Fear Of Becoming Obsolete, you will likely end up in a dark place, desperately searching for someone to buy what you’re selling.

Cutting to the chase, if you think enterprise software and services will look anything like they do today in the future, you’re delusional.

SaaS is a bloated, overpriced mess that forces companies to pay for features they don’t need.

IT Services and Consulting are a glorified human labor business masquerading as innovation.

CIOs are still spending billions on static tools and labor-heavy services when AI-first solutions can do far more for a lot less.

Talk to any C-Suite leader worth their salt, and they will tell you they are sick of spending more and more every single year on the same old software licenses and hiring more and more services people to make them work. This world cannot continue spending on low-value technology in perpetuity.

Why and how Services-as-Software will rewrite the enterprise tech playbook

Traditionally, software vendors have dominated the strategic sale of outcomes, while service providers have sold the tactical rollout of the software to reach these outcomes. The big challenge is for software firms to focus more on the tactical “how to” and services firms to be more relevant with the strategic “why.” This is an unprecedented time in technology history where outcomes, dreams, and tactical delivery are becoming one, and we don’t yet know who the clear winner will be.

Enter Services-as-Software—an AI-first, automated service layer that’s coming to obliterate everything in its path. No more billable hours. No more clunky SaaS.

That’s the HFS 2030 Vision—where we first coined the term Services-as-Software. A world where enterprises stop buying static technology and people-intensive services and instead consume AI-powered, outcome-driven solutions that continuously evolve and adapt to changing business requirements.

This isn’t a subtle shift. It’s a full-scale re-invention of enterprise technology as we know it. We’re already experiencing a secular change in how we buy, deploy, and consume technology, both in our professional and personal lives. The key is to stop clinging hold of the way we used to engage with tech and embrace the new before we become obsolete in the workplace. The old world of bloated spending on bad SaaS and bloated labor-based support deals is firmly in the past.

To reiterate this trend, HFS’s pulse survey of over 600 enterprise decision-makers reveals more than two-thirds of enterprises are frustrated with both their software and services investments and are primed to renegotiate their current contracts as they search for alternatives:

Enterprise software promised efficiency but delivered clutter for decades. Packed with unnecessary features, it overwhelms users instead of empowering them. Pre-configured workflows assume businesses operate in predictable, linear ways, yet real-world challenges demand adaptability and agility. And despite the never-ending hype of automation, most software still relies on expensive consultants to stitch it together—turning “plug-and-play” into “pay-and-pray.”

Services are a scam—overpriced, slow, and labor-heavy

Consulting firms claim to sell expertise, but too often, they peddle generic templates disguised as bespoke solutions. The game is simple: create complexity, then charge clients to navigate it. Efficiency isn’t in their business model—hours billed are the real product. Organizations don’t pay for results; they pay for human effort, endless PowerPoints, and the illusion of transformation. In short, complexity has kept consultants and C-suite executives in jobs for decades as they tacked decade-long ERP rollouts, cloud migrations, and data transformation initiatives.

In a world that demands agility, both software and services are holding businesses back. It’s time for something better.

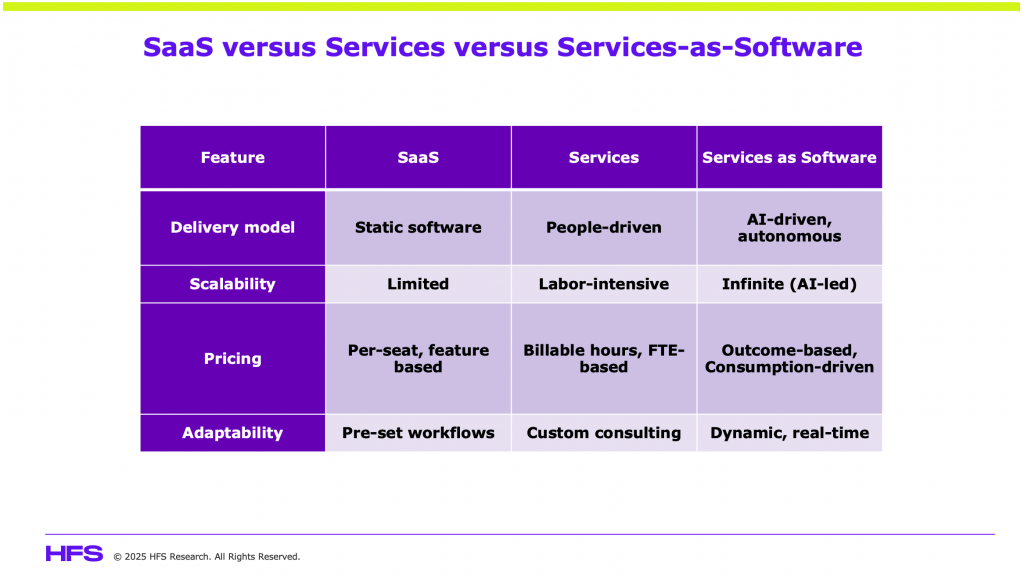

A brand new category of “Services-as-Software” is emerging

Services-as-Software eliminates this current BS—blending automation, AI-driven decision-making, and outcome-based pricing to finally deliver what enterprises need.

Like services, it delivers expertise and decision-making.

Like software, it is automated, scalable, and subscription-based.

But unlike traditional SaaS and Services, it is adaptive, continuously learning from data to optimize processes in real time.

No wonder 6 out of 10 enterprises expect to replace at least some of their professional services with AI-driven solutions:

Forget configuring software. Forget hiring a bunch of consultants. Services-as-Software is the new model. It’s AI-first, service-led, and autonomous:

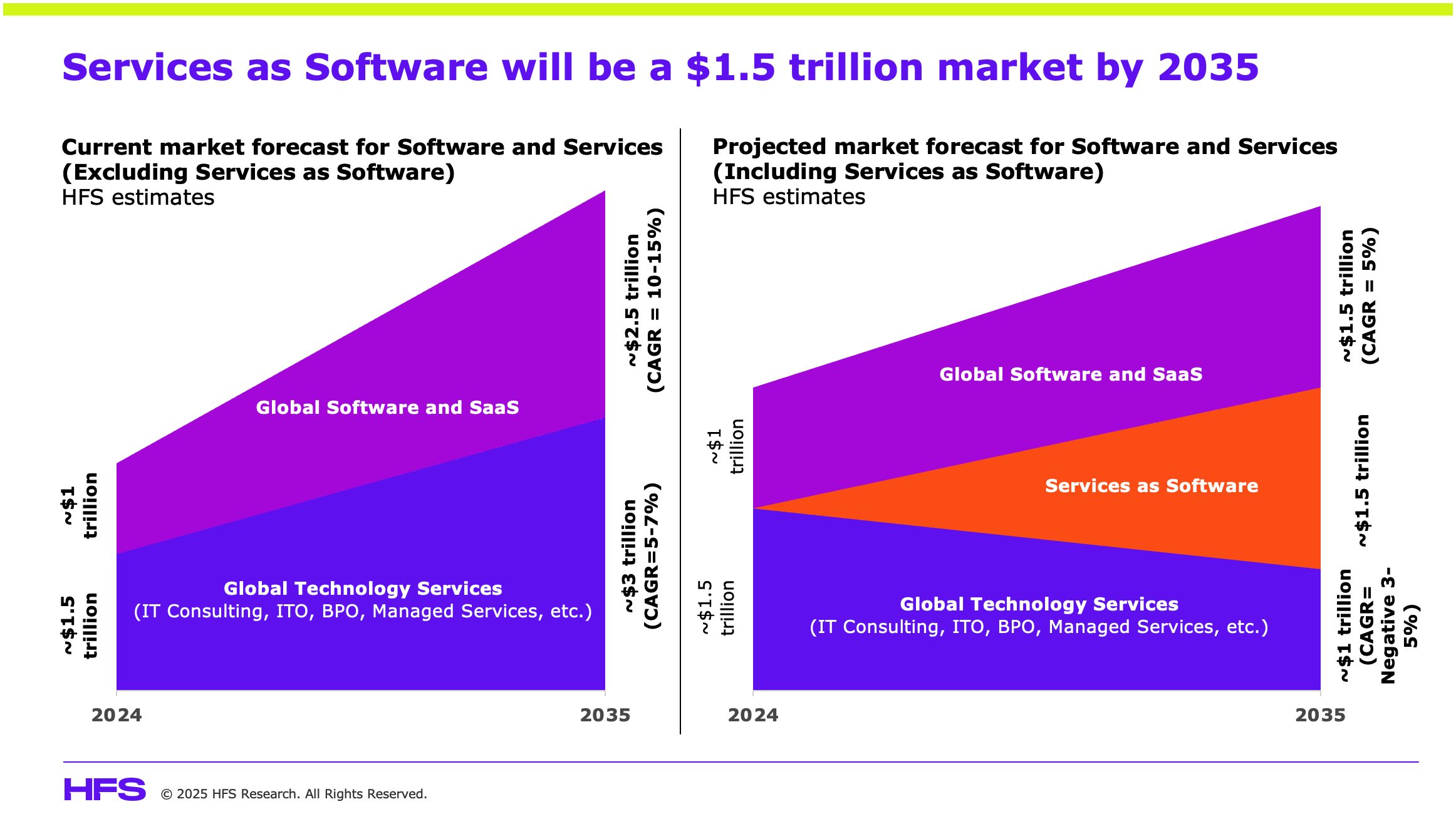

Services-as-Software will become a $1.5 trillion market by 2035, absorbing revenue from both traditional IT services and SaaS

By 2035, HFS projects Services-as-Software to grow into a $1.5 trillion market, absorbing revenue from both traditional IT services (which will shrink) and Software & SaaS (which will evolve and grow but at a slower rate):

These are our high-level projections based on several critical assumptions about enterprise technology adoption, AI progress, and industry transformation:

Services-as-Software will erode traditional IT services revenue. IT services revenue (around $1.5T in 2024) will decline as AI-driven services replace traditional labor-intensive work in areas like IT outsourcing, BPO, and consulting. Many traditional services will become productized and subscription-based, leading to fewer billable hours and lower revenue from human-led services.

SaaS growth will continue but at a much slower pace. SaaS growth (from around $1T in 2024 to $1.5T in 2035) will not just be from traditional SaaS licensing but from AI-powered, adaptive services. Software vendors will increasingly monetize AI-powered service layers instead of static software licenses.

Services-as-Software will become a $1.5T category. New spending will not be incremental but will come at the expense of traditional services and software markets. Enterprises will stop hiring as many IT consultants and will move away from feature-based SaaS toward outcome-based AI solutions.

AI innovation will drive down costs, increasing adoption. The cost of AI will continue to decline, making AI-driven services cheaper and more accessible for enterprises of all sizes. Open-source AI models will accelerate adoption of Services-as-Software by reducing development and implementation costs.

Agentic AI and “DeepSeek” inspired AI innovations will accelerate the shift to Services-as-Software

Agentic AI is emerging as the backbone of Services-as-Software. AI systems that autonomously take action make decisions, and continuously learn will drive the transformation of software and services into intelligent, self-operating solutions. Unlike traditional SaaS, which relies on pre-defined workflows and manual configurations, agentic AI learns, optimizes, and executes in real-time, eliminating the need for enterprise software licenses. Businesses will no longer need to buy and configure ERP, CRM, or other SaaS platforms; instead, AI agents will autonomously manage processes, analyze data, and take proactive actions (at least the easy ones) without human intervention.

The same shift will disrupt traditional service models like IT consulting, BPO, and professional services. Rather than hiring consultants to analyze data or outsourcing tasks to human workers, agentic AI will monitor operations, self-optimize workflows, and make business decisions in real-time—reducing dependency on billable hours and manual labor. The future of enterprise technology isn’t about AI-assisted work; it’s about AI-led execution. A future is emerging where businesses won’t need to buy software or hire service providers for everything—they will consume fully autonomous AI-driven solutions.

If you leave aside the geopolitics and the “AI cold war” between the US and China, DeepSeek’s recent AI advancements will also accelerate the movement toward Services-as-Software. DeepSeek’s underlying engineering innovations promise to make AI-powered solutions cheaper, more efficient, and widely accessible, accelerating the shift toward Services-as-Software. AI at lower costs enables cutting-edge capabilities at a fraction of traditional development expenses. Open-source AI is also democratizing access, allowing enterprises of all sizes to integrate powerful AI-driven solutions without prohibitive costs. Meanwhile, real-time expert reasoning is revolutionizing decision-making as AI increasingly replicates the expertise of human consultants, reducing the need for traditional advisory services. This shift levels the playing field, enabling even small businesses to harness AI-driven intelligence, accelerating adoption, and driving industry-wide disruption.

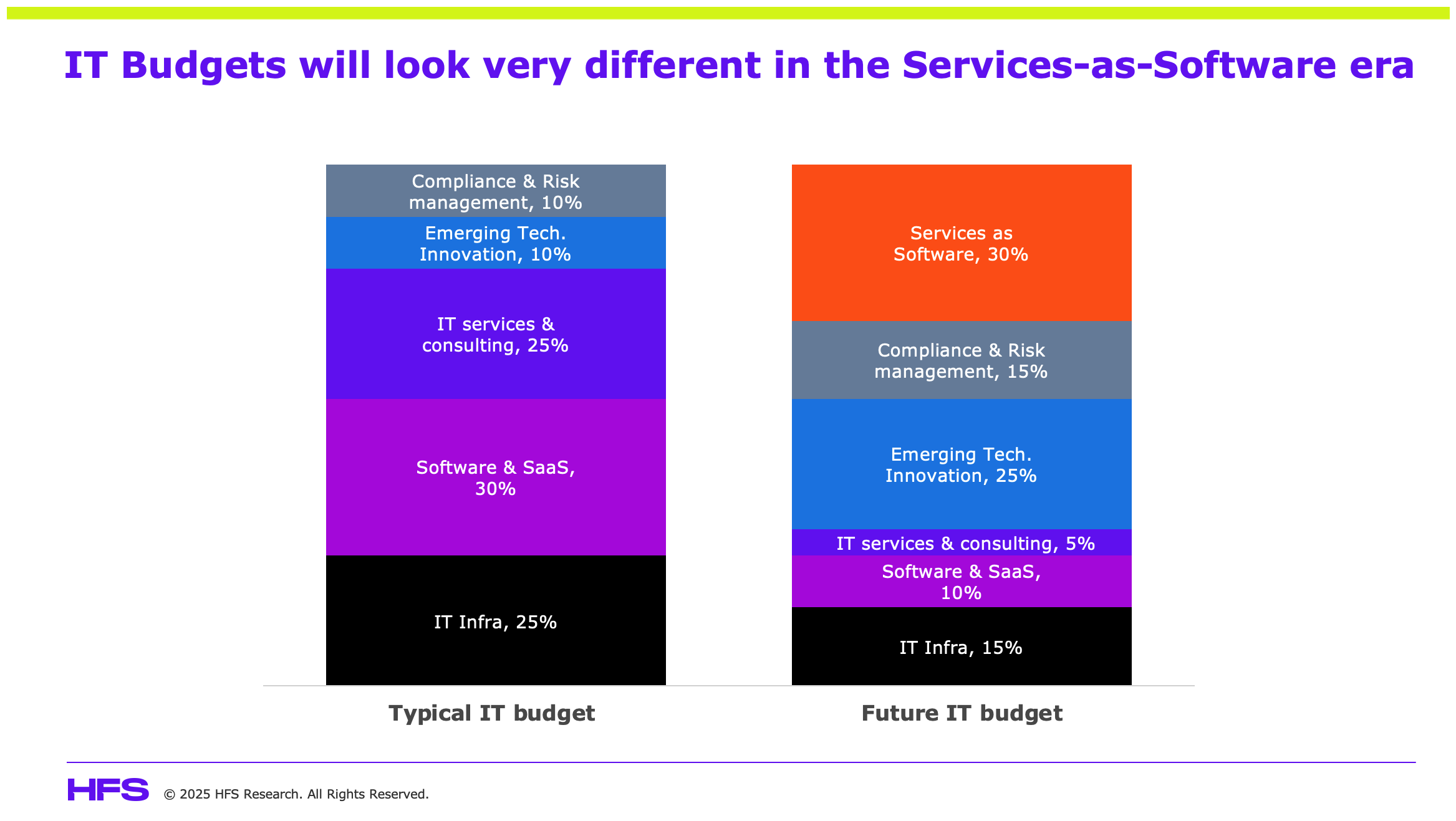

CIOs: It’s time to completely rethink your IT budget

A large enterprise typically allocates its technology budget across multiple categories, including IT infrastructure, software, services, innovation, and compliance. However, with the rise of Services-as-Software, this spending will shift from fixed investments in software licenses and human-driven services to AI-powered, outcome-based models (See Exhibit 4). AI-driven services will replace traditional workflows, dynamically adapting to business needs and optimizing processes in real-time:

Services-as-Software becomes a major IT spend. Nearly a third of IT budgets will shift toward AI-powered service layers that replace static workflows with real-time intelligence. Spending on AI-as-a-Service will grow, covering automated advisory, compliance, and decision-making. Investments in AI-native process automation will replace traditional SaaS workflows, with outcome-based pricing models replacing per-seat software licensing.

Increased investment in security, compliance, and governance. AI-enabled cybersecurity and automated compliance will become critical budget priorities. Regulatory technology (RegTech) spending will surge as businesses strengthen AI governance to meet evolving compliance requirements.

Growing budget for emerging technology & innovation, Enterprises will increase spending on cutting-edge technologies beyond AI, including quantum computing, edge computing, blockchain, IoT, digital twins, and who knows what else! The focus will be on integrating these technologies into AI-powered platforms to drive competitive advantage.

Key Areas of IT Budget Decline:

Shrinking IT services & outsourcing spend. AI-driven automation will significantly reduce reliance on traditional IT support, consulting, and application development. The demand for outsourcing contracts will decline as no-code/low-code AI solutions take over maintenance and customization.

Declining enterprise SaaS spending. Businesses will move away from large, rigid SaaS contracts (e.g., Salesforce, SAP, Oracle) in favor of AI-driven, flexible, outcome-based platforms that continuously adapt to business needs.

Infrastructure costs shift to AI-optimized cloud consumption. Traditional cloud spending will give way to AI-optimized compute environments, allowing enterprises to dynamically adjust workloads for greater efficiency and cost savings.

As AI and other emerging technologies reshape the enterprise landscape, IT budgets will prioritize intelligence over infrastructure, automation over manual processes, and outcomes over effort—accelerating the shift toward a fully AI-powered and innovation-driven operating model.

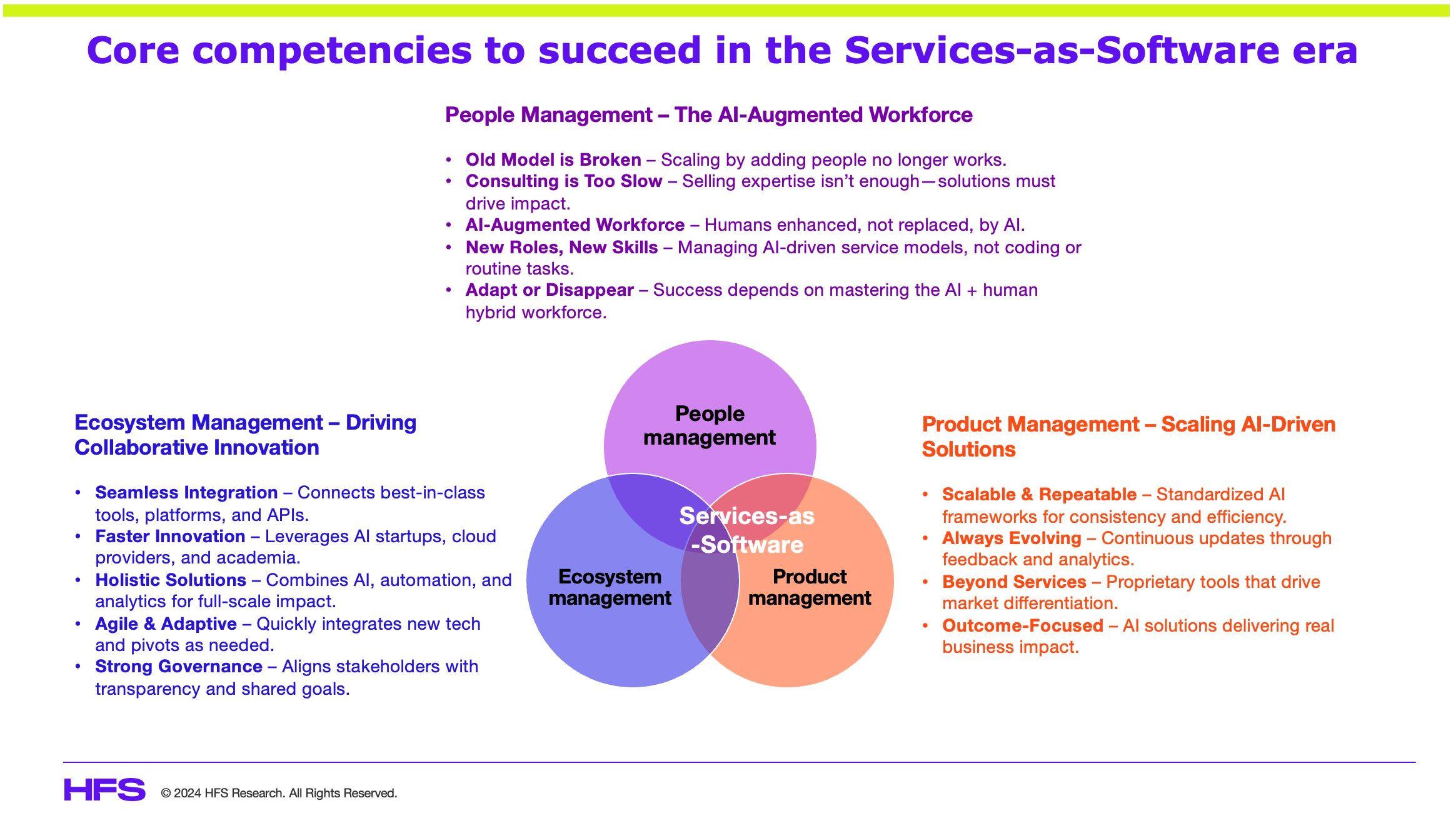

Who will win? The Providers who can master People, Products, and Ecosystems

Traditional IT services firms don’t know how to build scalable products. Traditional SaaS vendors don’t know how to deliver real-world services. Ecosystem building is not considered a core competency by either. The winners in the Services-as-Software era will be those who master all three core competencies:

The Bottom line: Services-as-Software is not a death knell for service providers and software vendors. It’s the $1.5 trillion opportunity of our lifetime

As the lines between software and services blur, traditional tech providers can finally crack open the $1.5 trillion services market, while service firms can escape the FTE trap and regain hockey-stick growth. But the winners won’t be those who cling to outdated models—they’ll be the ones who fuse AI, automation, and expertise into scalable, outcome-based solutions.

This isn’t the end. It’s the biggest revenue shift in enterprise technology history. A brand new category is on the horizon. The big question is—who will seize it? That is yet to be seen…

HFS research has found that the average time for a bank to onboard a new commercial customer is 32 days. Not hours. DAYS. The rapid and often real-time digital interactions and journeys enjoyed in the retail banking domain have not permeated the commercial banking realm – despite the fact that commercial clients are typically banks’ highest-value clients.

As commercial banks strive to meet the broad B2B needs of small and medium enterprises, commercial clients, and corporates, they need to seriously up their digital game. This means something totally different and far more complex in the B2B arena. A sexy app does not win the day in commercial banking. Commercial banks must balance foundational modernization initiatives between practical platform solutions and custom builds—all in the name of enabling 360 visibility of working capital and real-time everything. Service provider partners have a critical role to play in enabling this future reality.

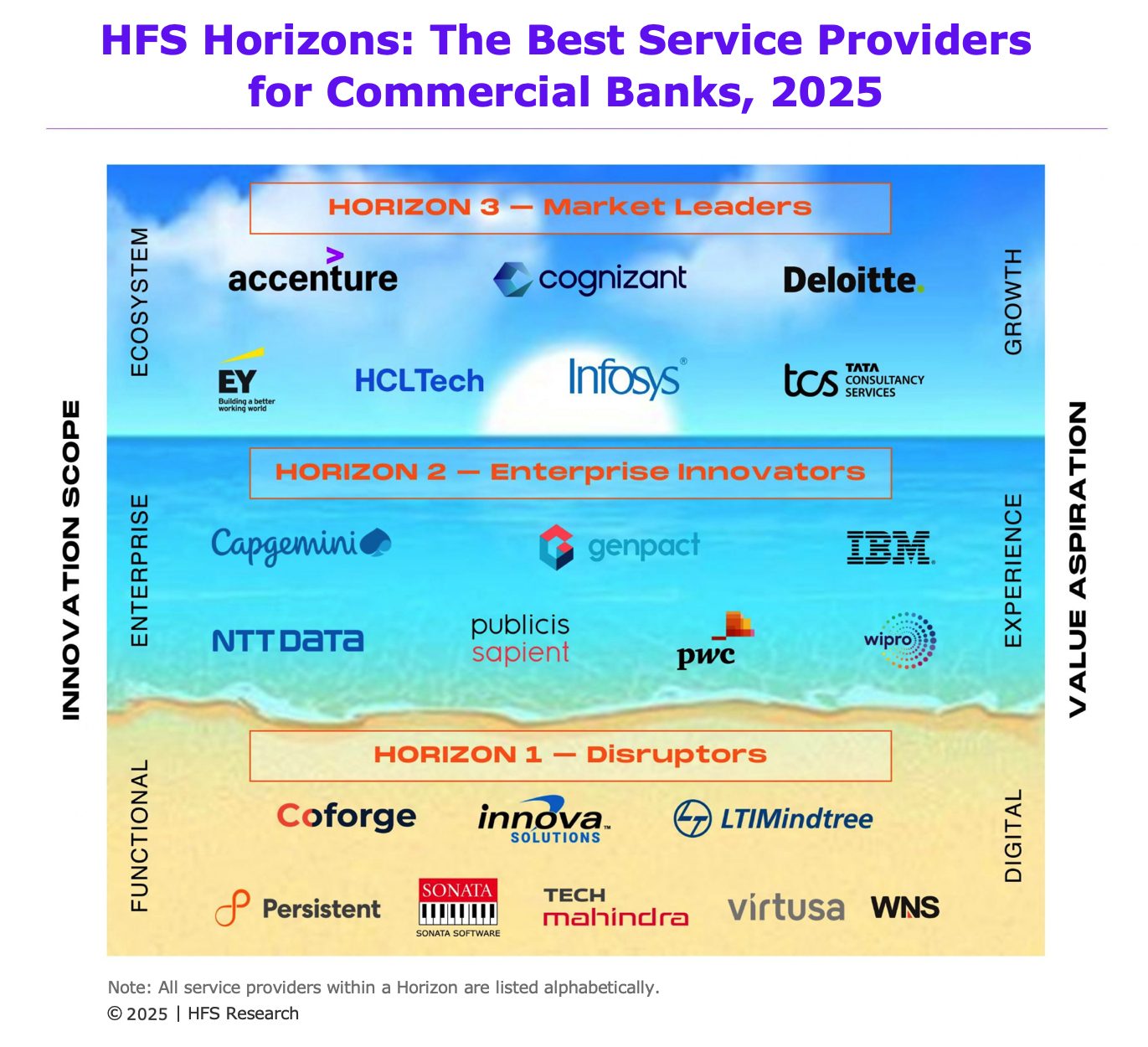

Who are the best service providers for commercial banks?

HFS conducted a deep-dive Horizons Study into the needs of commercial banks and the best IT and business process service providers to support them.: HFS Horizons: The Best Service Providers for Commercial Banks, 2025. This report evaluates the capabilities of 22 service providers across the HFS commercial banking value chain based on a range of dimensions to understand the why, what, how, and so what of their service offerings. It assesses how well service providers are helping their commercial banking clients worldwide embrace innovation and realize value across three distinct Horizons: Horizon 1, optimization through functional digital change; Horizon 2, experience through end-to-end enterprise transformation; and Horizon 3, growth through ecosystem transformation (Exhibit 1).

Exhibit 1: The HFS Horizons model helps commercial banks pick their service providers based on desired outcomes

We assessed these 22 service providers across their value propositions (the why), execution and innovation capabilities (the what), go-to-market strategy (the how), and market impact criteria (the so what). The seven (7) Horizon 3 market leaders are Accenture, Cognizant, Deloitte, EY, HCLTech, Infosys, and TCS in alphabetical order. These service providers have demonstrated their ability to support commercial banks across the journey—from functional digital transformation through enterprise-wide modernization to creating new value through ecosystems. Their shared characteristics include deep industry expertise across the commercial banking value chain, a full-service approach across consulting, IT, and operations, a strong focus on innovation internally and externally with partners, co-innovation with clients and partners, and proven impact and outcomes with commercial banking clients around the world. While these seven firms prevailed as Horizon 3 market leaders, we underscore the fact that there is value to be had at each horizon based on the needs and desired outcomes of commercial banking clients.

Key trends in commercial banking – change is hard and expensive

The enterprises and service providers interviewed for this study painted a clear picture of a market in need of modernization but mired in extenuating circumstances that impact budgets and solution extensibility. HFS notes three major trend themes:

Macroeconomic mixed bag. Inflation and high interest rates have yielded good news/bad news scenarios in commercial banking. The good news has been that there was money to be made in the first rising interest rate economy in the past 15+ years. However, volumes were down as the cost of loans was high. Combine this with the steep competition for deposits, which forced commercial banks to offer attractive interest rates, thinning their net interest margins.

CX in commercial banking is unique. Retail banking CX is flashy B2C. In commercial banking, it’s a B2B paradigm that requires 365x24x7 capital clarity. Commercial clients want simplified, connected access and straight-through transactions. Banks are meeting this need by balancing digitalization with personalized service—using digital tools to enhance in-person interactions, enable self-service, and deliver best-in-class onboarding among others. The 2025 wish list includes 360 liquidity across banks and real-time everything.

Build AND buy to modernize. No commercial bank wants to build a custom or highly customized lending platform for treasury or trade finance among other functions. Witness the rise of COTS (commercial off-the-shelf) in commercial banking. However, for modernization needs—where there is no easy platform upgrade—commercial banks are building various digital, API-enabled solutions to extend the functionality of legacy systems that are not ready to be retired.

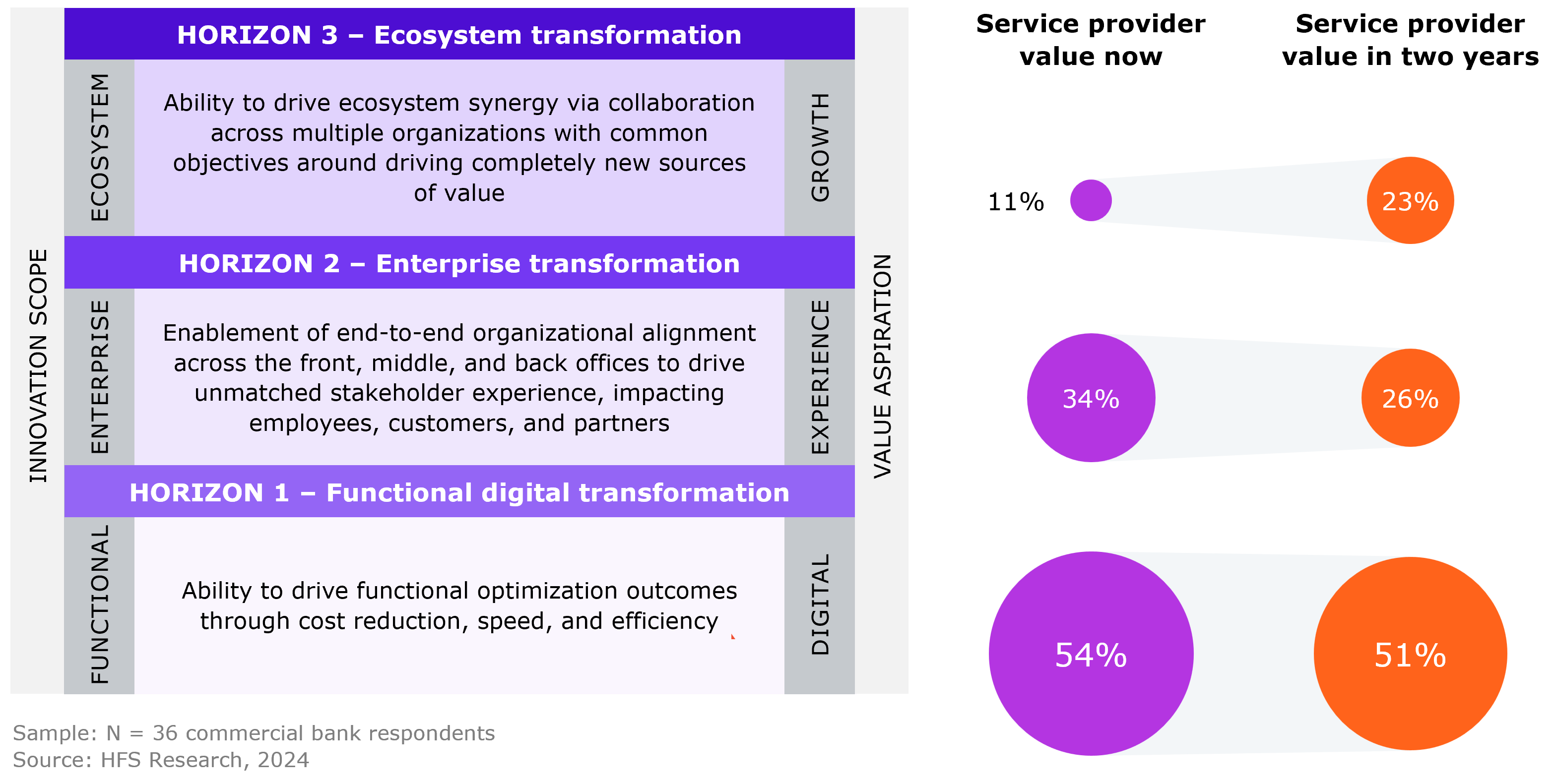

What commercial banks want from service providers

The HFS Horizons model aligns closely with enterprise maturity. We asked commercial banking leaders interviewed as references for this study to comment on the primary value their IT and business service provider partners deliver today and are expected to deliver in two years. Respondents indicated that the primary value realized today is largely Horizon 1—functional digital transformation focused on digital and optimization outcomes (54%). In two years, the focus will continue on digital and optimization outcomes (51%), as the industry strengthens its digital hygiene to better serve large customers while also expanding to effectively cater to small and medium enterprise (SME) clients (Exhibit 2).

About a third of commercial banks are currently tapping their service providers to support enterprise transformation (34%). While modernization needs abound, this focus will be downplayed in 2025. The biggest value shift in the next two years is to Horizon 3 initiatives. Commercial banks want to leverage their modernization initiatives to help them expand their footprint and increase their relevance to commercial customers with broader liquidity offerings, non-banking services, and other ecosystem plays. Commercial banks must choose their partners based on the value they seek; incumbents may be the convenient choice, but they must demonstrate updated and relevant value.

Exhibit 2: Commercial banks prioritize improving digital hygiene to reduce costs, improve operations, and elevate customer experience

How service providers are meeting the needs of commercial banks

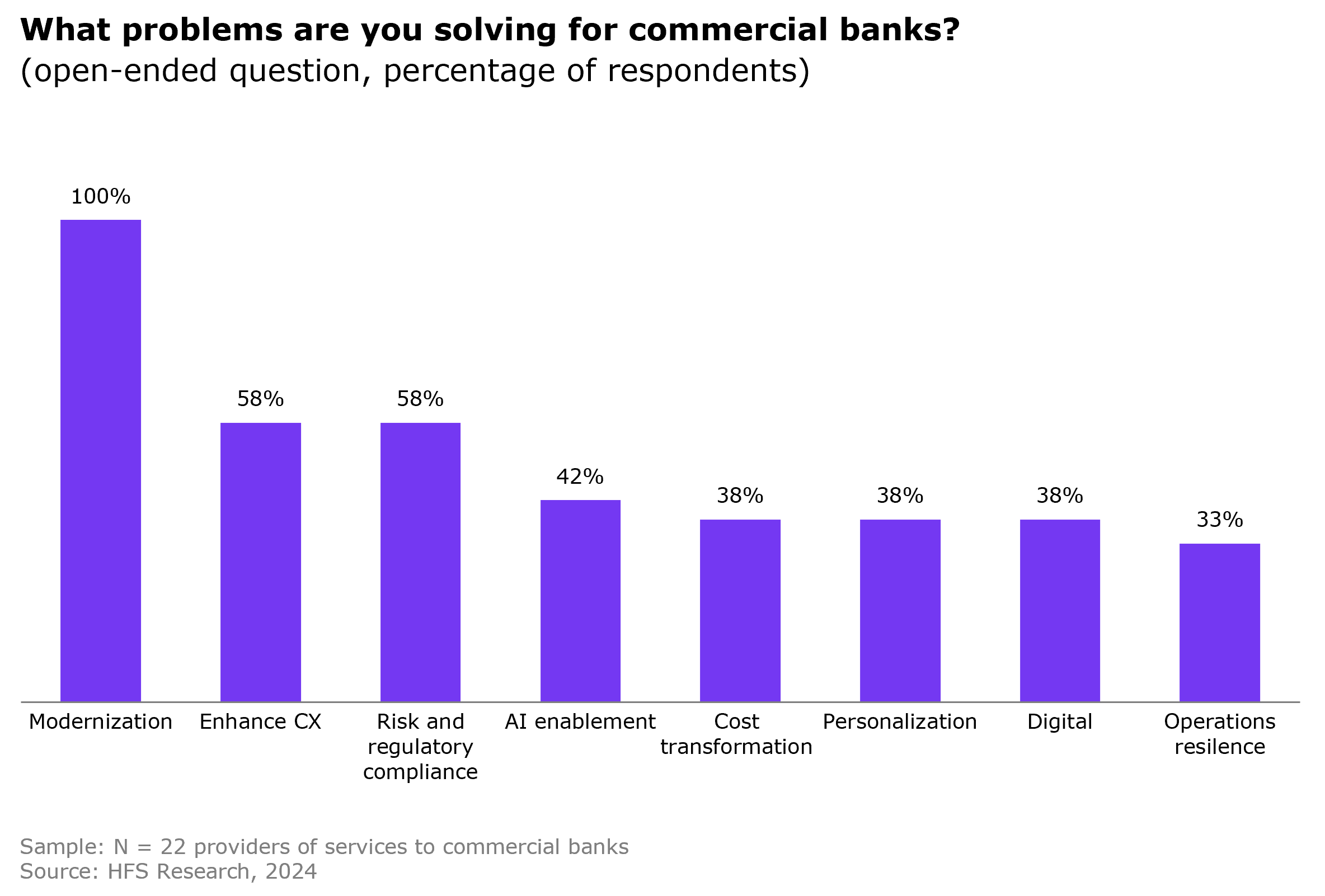

As commercial banks evolve and mature across the Horizons, service providers are on point to support these ever-changing needs. In our study, we found strong alignment between commercial banks’ digital and modernization initiatives (Horizons 1 and 2, respectively) and the fastest-growing service offerings from providers. Modernization, CX, and risk and regulatory compliance ranked as the top solutions meeting the needs of commercial banks (Exhibit 3). Modernization initiatives take many forms, but there is a strong focus on platform implementations for functions such as commercial lending and trade finance. CX in commercial banking is a B2B focus and requires more than great interactions—it includes elements such as faster customer onboarding, real-time payments, better cash management to enable real-time liquidity views, and faster credit decisions for lending. Enhanced customer onboarding was a top case study, as were nCino implementations for lending modernization. Risk and regulatory compliance is perpetual, and there’s still work to be done on optimizing these functions, particularly with AI. We’ll see what the incoming American federal government administration has in store for regulations in 2025.

Exhibit 3. Service providers’ top commercial banking offerings

The Bottom Line: Modernization is essential for commercial banking success in 2025

Commercial banking customers want digital experience: Commercial banks own the high-value relationships within their firms, but they must play catch-up with their retail banking siblings, shifting from manual processes and a people-led engagement running on legacy tech to seriously up their digital CX game. The competition is intense, with commercial clients diversifying their relationships across banking institutions and non-bank lenders and nimble fintechs gaining ground. Congruent priorities around customer experience, new business models, and enablement of better business transactions necessitate modernization to secure each bank’s future—goals that commercial banks can achieve with the help of their service provider partners.

{kind=link}