We’ve spent the last decade-plus romanticizing automation and AI, and now the hangover’s (finally) kicking in. Most of us are avoiding CoPilot like the new Clippy, while GenAI and Agentic get tossed into PowerPoint decks like fairy dust. And meanwhile, our businesses still run on Excel macros, spaghetti code, and tribal knowledge.

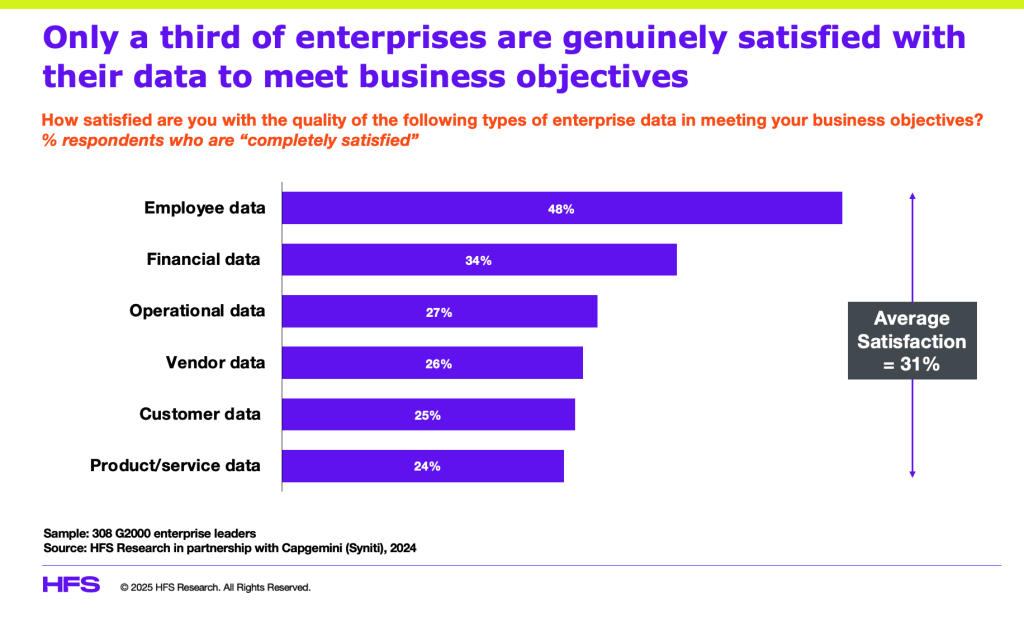

Bad data is killing businesses

The truth? Enterprises that win are the ones who treat data as their strategy, not just some exhaust from the grind of their broken workflows and systems that no one trusts to base decisions on. A major study we conducted across global 2000 organizations reveals just how poor our data is right across the enterprise:

The HFS OneOffice model initially laid the groundwork in 2016 to define how businesses need to operate. We just didn’t realize back then it would take another decade via a pandemic, rampant inflation, several geopolitical conflicts, and daily economic uncertainty to create the burning platform where enterprises have to be autonomous, less border-sensitive and much more cost-conscious, with capable talent and partners to help them function in these emerging business ecosystems and across convoluted supply chains.

OneOffice inspired a new enterprise mindset in 2016

“HFS in 2016: The onset of digital and emerging automation solutions, coupled with the dire need to access meaningful data in real-time, is forcing the back and middle offices to support the customer experience needs of the front. Consequently, we’re evolving to an era where there is only “OneOffice” that matters anymore, creating the digital customer experience and an intelligent, single office to enable and support it

Today’s college graduates are simply not coming out of school willing to perform mundane routine work: operations staff proactively need to support the fast-shifting needs of the front office. So the focus needs to shift towards creating a work culture where individuals are encouraged to spend more time interpreting data, understanding the needs of the front end of the business, and ensuring the support functions keep pace with the front office.”

Fast-forward to today, and we finally have an injection of rocket fuel from Generative and Agentic AI to create intelligent agents that can sense, decide, and act with autonomy… as long as we have our data strategy right. To be a truly autonomous organization, the principles of OneOffice hold truer than ever: workflows executed in real-time between customers and employees that engage partners right across our business ecosystems.

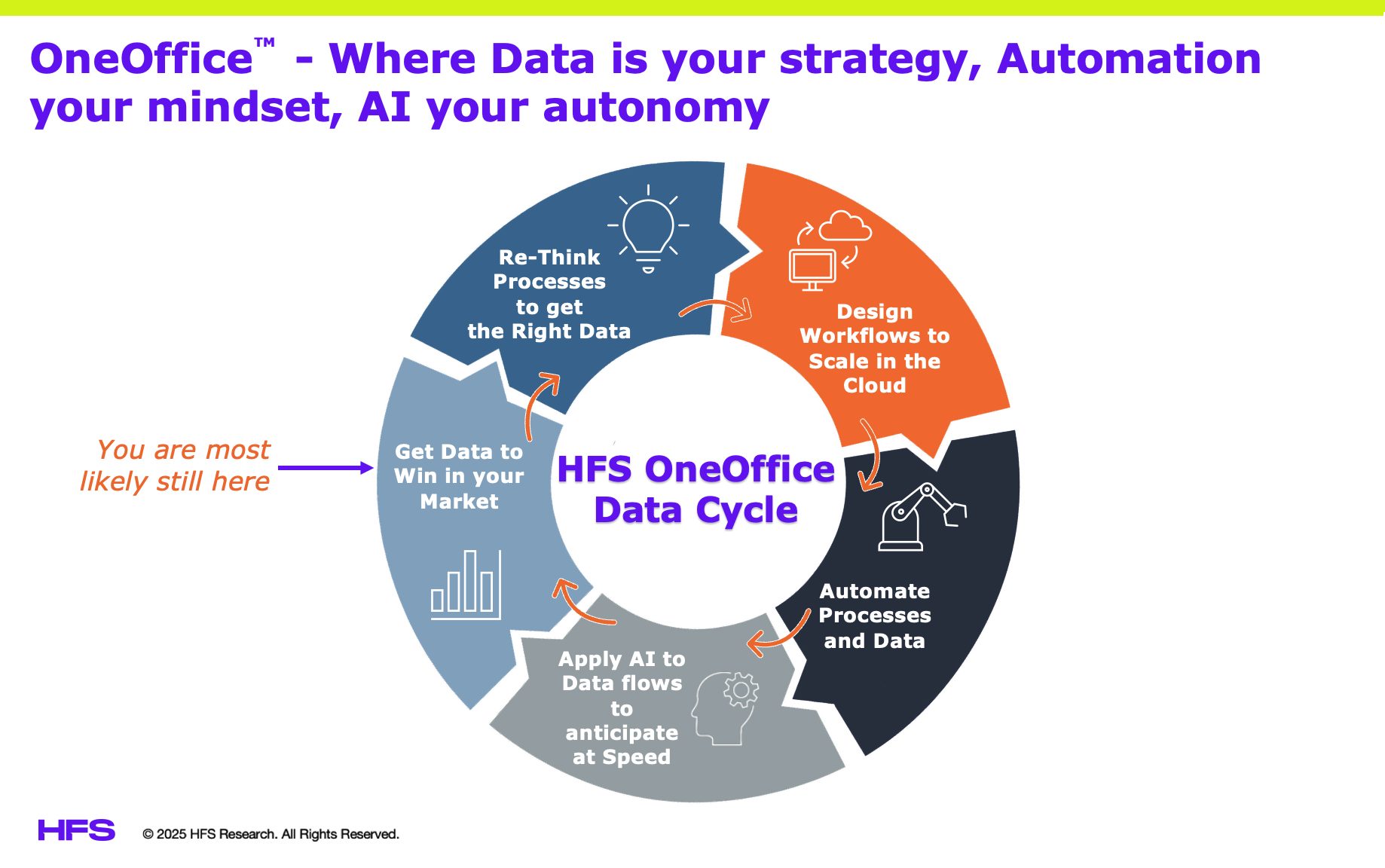

The OneOffice Data Cycle in 2025 places data at the core of enterprise effectiveness

OneOffice is HFS Research’s enterprise model that breaks down traditional silos between front, middle, and back offices to create a single, digital, customer-centric enterprise. It’s where automation, AI, and data converge to create real-time workflows between customers, employees, and partners—without handoffs or latency. A OneOffice model creates one intelligent enterprise that operates in real-time, adapts to change, and delivers seamless customer experiences. Data is the lifeblood of OneOffice: it fuels decision-making, powers AI models, and ensures every function is aligned with customer and business outcomes.

Let’s walk through this OneOffice Data Cycle, powered by the actual technologies and companies that are making it real.

We need to understand how the data cycle works to get us ahead of our markets. Here are five steps we must take with examples from enterprise clients, service providers and technology firms:

1. Get data to win in your market.

This is where you must align your data needs to deliver on business strategy. You can’t manage what you can’t measure. This is about aligning data capture with business priorities: customer behavior, operational bottlenecks, talent churn, and cash velocity.

Examples where AI is being effectively applied:

Unilever uses Microsoft Azure OpenAI to analyze internal and external datasets, including consumer sentiment, to adjust brand strategies in near real-time.

Anthropic’s Claude is being embedded by data-rich enterprises to run secure, real-time analysis agents that summarize, flag anomalies, and interact with humans when decision thresholds are crossed.

Stitch Fix leverages OpenAI GPT to extract signals from customer feedback and style preferences, improving product recommendations and inventory decisions.

Siemens uses Braincube’s agentic AI platform to monitor industrial IoT data, detect deviations in production, and adjust machine behavior—without waiting for human commands.

Infosys Topaz integrates GenAI with real-time analytics to help clients personalize digital banking experiences based on behavioral data.

LTIMindtree applies autonomous agents to enable real-time tracking and predictive inventory management for retail clients, eliminating stock-outs.

Publicis Sapient uses GenAI to analyze large-scale customer journey data, surfacing real-time behavior patterns to inform digital product strategy.

Movate integrates agentic AI into CX analytics platforms to proactively detect churn signals and initiate retention playbooks autonomously.

Firstsource integrates GenAI-powered document understanding to extract structured data from scanned medical records and billing forms—feeding analytics for healthcare payer and provider decision-making.

Net-net: If your data signals aren’t tied directly to how you win revenue, you’re running blind.

2. Re-think processes to get the right data

If your processes don’t capture useful data, they’re not processes—they’re liabilities. You must re-think what should be added, eliminated, or simplified across your workflows to source this critical data. Do your processes get you the data you need from your customers, employers, and partners?

Examples where AI is being effectively applied:

Chubb Insurance applies Amazon Bedrock to re-engineer underwriting and claims documentation workflows—turning dense PDFs and call transcripts into structured, searchable insights.

Capgemini has embedded Google Gemini into supply chain operations to automate root cause analysis and recommend corrective actions across vendor networks.

Publicis Sapient reimagines customer experience and marketing processes using custom-built GenAI copilots that generate real-time campaign responses based on audience behavior.

UnitedHealth Group is developing a concierge bot developed with both GenAI and agentic technologies to support medical patients dealing with the complexities (and huge inefficiencies) of the US healthcare system.

UiPath Autopilot now combines GenAI with autonomous agents to observe process execution and propose optimizations—cutting down rework loops by over 30% in pilot enterprise clients.

Wipro’s ai360 platform deploys agents to continuously optimize procurement and finance workflows by identifying anomalies and recommending improvements.

NVIDIA partners with major automotive and manufacturing firms to deploy AI agents on its DGX Cloud infrastructure—allowing real-time model training, simulation, and inference at the edge.

Cognizant’s Neuro agent-based modules continuously scan workflow telemetry to self-heal and recommend business rule updates.

Coforge is leveraging agent-based automation to dynamically adjust airline booking flows based on real-time seat availability and fare rule compliance.

Net-net: If the process doesn’t give you valuable data, kill it or fix it. Preferably both.

3. Design workflows to scale in the cloud.

Moving legacy sludge to the cloud without rethinking the model just means faster dysfunction. We’ve seen billions of dollars wasted on botched cloud migrations in recent years because underlying data infrastructures were not addressed effectively, and bad processes became even less effective or completely dysfunctional.

Examples where AI is being effectively applied:

Ford Motor Company deploys agentic AI agents built on OpenAI, Anthropic, and Nvidia GPUs to convert 2D sketches into 3D models and run rapid stress analyses—shortening simulation from 15 hours to 10 seconds

ServiceNow’s GenAI Workflow Studio lets ops teams redesign service flows using natural language—automating ticket routing, approvals, and data handoffs in cloud-native apps.

Workday AI uses GenAI to automate job description creation, compensation modeling, and hiring workflows—all in cloud-native HR suites.

Tech Mahindra uses Google Cloud’s Gemini to enable telecom clients to deploy conversational agents across cloud-native CRM and support systems.

FedEx is using DataRobot agents to orchestrate cloud services across route planning, weather modeling, and fleet management—autonomously shifting strategies on the fly.

Accenture SynOps embeds agentic capabilities to autonomously orchestrate and optimize cloud-based workflows in finance and customer operations.

Anthropic Claude is embedded in some cloud-first healthcare platforms to provide HIPAA-safe, autonomous intake triage for patient engagement.

Publicis Sapient enables retail clients to run full-funnel autonomous campaign workflows across cloud stacks, where agentic bots optimize audience targeting and message testing.

Uber built a near-real-time data infrastructure processing PBs of user and driver data—supporting instantaneous pricing, fraud detection, and dispatch decisions across its platform

Birlasoft has deployed cloud-native agent frameworks that autonomously monitor SAP-based operations for global manufacturers—streamlining issue detection and resolution across procurement and logistics.

Genpact leverages cloud-based GenAI models to power finance-as-a-service workflows, dynamically updating reporting logic and dashboard content based on real-time operational data.

Net-net: If the cloud is your warehouse, AI is your forklift driver. But you still need to design the blueprint.

4. Automate processes and data.

Automation is not your strategy. It is the necessary discipline to ensure your processes provide the data – at speed – to achieve your business outcomes. This is where we separate real automation from Franken-bots duct-taped to bad data.

Examples where AI is being effectively applied:

Morgan Stanley has deployed OpenAI-powered advisors internally via GPT-4, enabling wealth managers to get instant access to decades of investment research—automated, summarized, and contextualized in seconds.

SAP Joule helps automate business insights from ERP data across finance and supply chain, using GenAI to generate insights that would’ve taken analysts days.

Cognizant’s Neuro Agent Framework is being used by Fortune 500 firms to automate backend processes across billing, collections, and claims management—learning and adapting with each data cycle.

Sonata Software integrates GenAI into its Harmoni.AI platform to automate customer service and backend documentation in manufacturing.

TCS Digitate’s Ingio platform uses agentic AI to resolve IT incidents automatically by sensing anomalies, identifying root causes, and executing fixes autonomously.

Capgemini’s Perform AI framework deploys agents to dynamically rebalance workloads and scale automation across insurance and telecom.

Microsoft uses AI builders in Power Automate at Eletrobras Furnas to detect electric grid anomalies and trigger alerts—minimizing regulatory risk.

WNS deploys an agentic-based solution called Travel Buddy to supports it clients’ needs for corporate travel bookings without the need for constant human oversight.

Net-net: Automation that doesn’t learn is just glorified scripting. Intelligent automation enables intelligent outcomes.

5. Apply AI to data flows to anticipate at speed.

This is where the magic happens—predictive, adaptive AI running on clean, automated, cloud-native data. Welcome to the self-optimizing enterprise. AI is how we engage with our data to refine ourselves as digital organizations, where we only want a single office to operate with agility to do things faster, cheaper, and more streamlined than we ever thought possible. AI helps us predict and anticipate how to beat our competitors and delight our customers, reaching both outside and inside of our organizations to pull the data we need to make critical decisions at speed. In short, automation and AI go hand in hand… AI is what enables a well-automated set of processes to function autonomously with little need for constant human oversight and intervention.

Examples where AI is being effectively applied:

Pfizer uses IBM Watsonx to accelerate clinical trial discovery by analyzing academic papers, medical literature, and trial results, surfacing new therapeutic targets in record time.

JPMorgan Chase is applying GenAI to risk models—feeding real-time data from markets, news, and internal portfolios to simulate potential exposures and make split-second adjustments.

Accenture leverages agentic AI for proactive customer churn prevention—automatically adjusting engagement models based on behavioral and transaction patterns.

Telefonica has deployed Aisera’s agentic AI to manage internal IT and employee service requests—handling over 80% of Tier 1 tickets autonomously.

Shell uses agent-based digital twins to simulate field operations and adapt to variables like pricing, weather, and inventory—helping them model and tweak operations in real time.

Inflection AI’s Pi assistant is being explored for continuous learning across enterprise L&D platforms to nudge workforce behavior in real-time.

Genpact applies AI-powered forecasting to proactively adjust finance and accounting workflows for large clients, predicting anomalies in receivables and dynamically adjusting credit risk scores across markets.

Anthropic Claude is embedded in financial services platforms to act as a proactive co-pilot for risk monitoring, triggering alerts and recommendations autonomously.

Coforge is piloting predictive agent-based maintenance for airport ground services using IoT sensor data and historical patterns.

Bridgewater Associates launched a multi-agent system (“AIA Labs”) that breaks investment queries into sequential agent tasks—an early-stage agentic AI demonstration

Net-net: AI isn’t the cherry on top—it’s the engine room. And it only runs on connected, clean, automated data.

Bottom-line: GenAI is the Brain, Agentic AI is the Muscle. As long as you have good data.

Let’s be clear: GenAI generates. Agentic AI executes. Together, they transform OneOffice from a strategy into an operating model. However, if your processes can’t capture good data, you’ll automate the wrong things. If your cloud isn’t built for agility, you’ll scale chaos. And if your talent isn’t empowered with intelligent tools, they’ll become blockers, not drivers. Your employees are now your most important customers. Treat them like it—or watch your best data (and people) walk out the door…

Cyber conflict is no longer a niche concern for defense departments, it’s a pervasive, persistent threat reshaping the security posture of every enterprise. As global tensions escalate—from Ukraine and Israel to rising flashpoints in South Asia—cyberwarfare has emerged as the new frontline. It targets not just military infrastructure, but also cloud platforms, supply chains, tech ecosystems, social media feeds, and the smartphones of your employees.

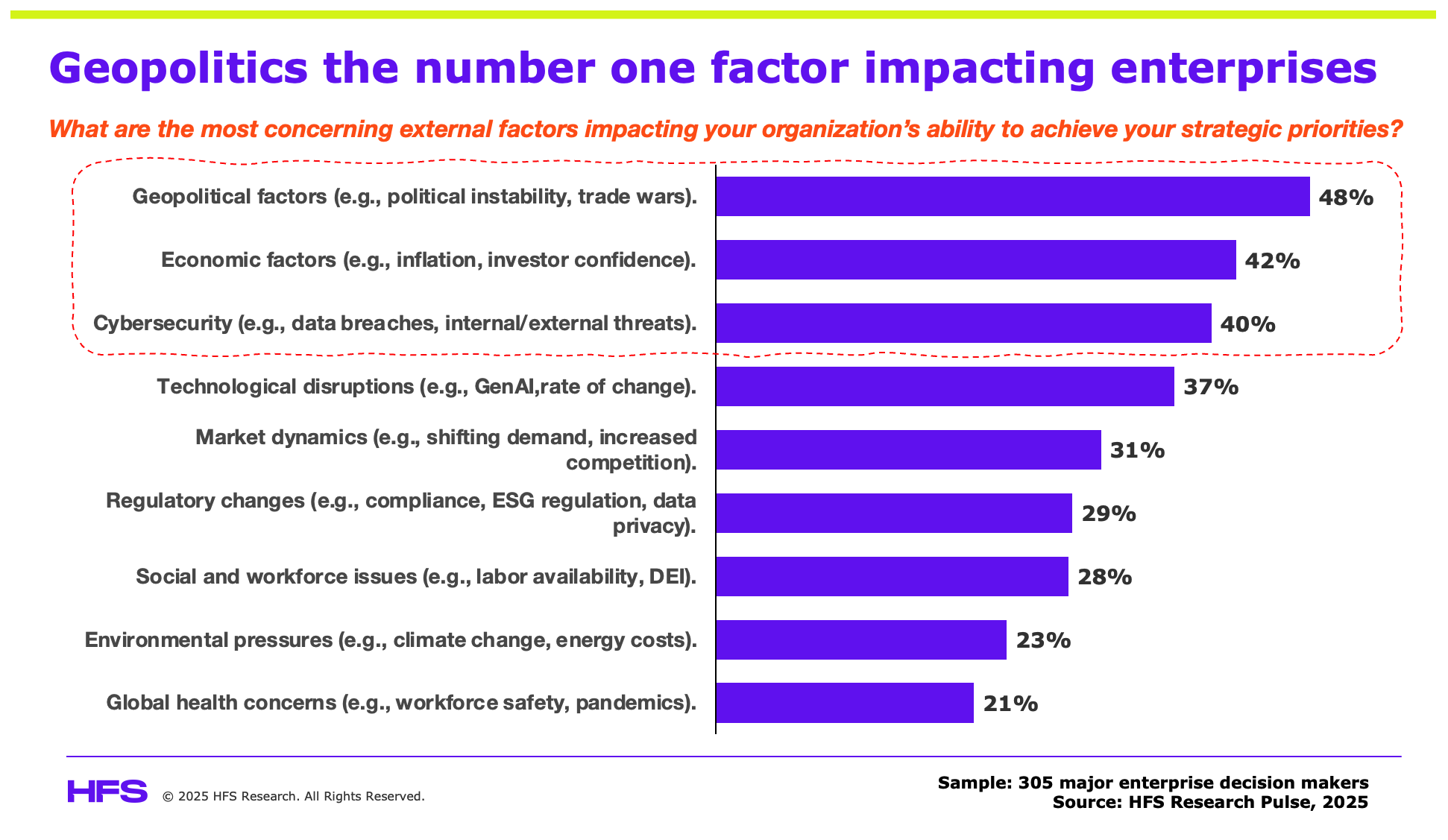

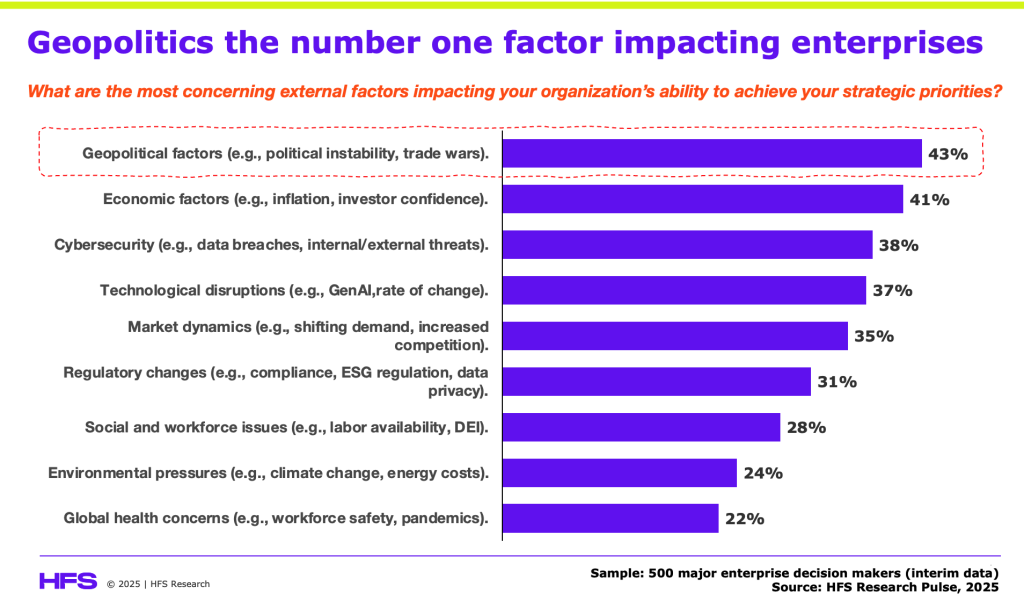

It is little wonder our latest research shows the combo of geopolitics, economics, and cybersecurity as the dominant external factors on the minds of G2K enterprise leaders:

This is not just about ransomware or phishing; it’s an emphatic focus for the CIO

Cyber conflict today includes information warfare, infrastructure sabotage, and financial system disruption, all designed to paralyze confidence and destabilize economies.

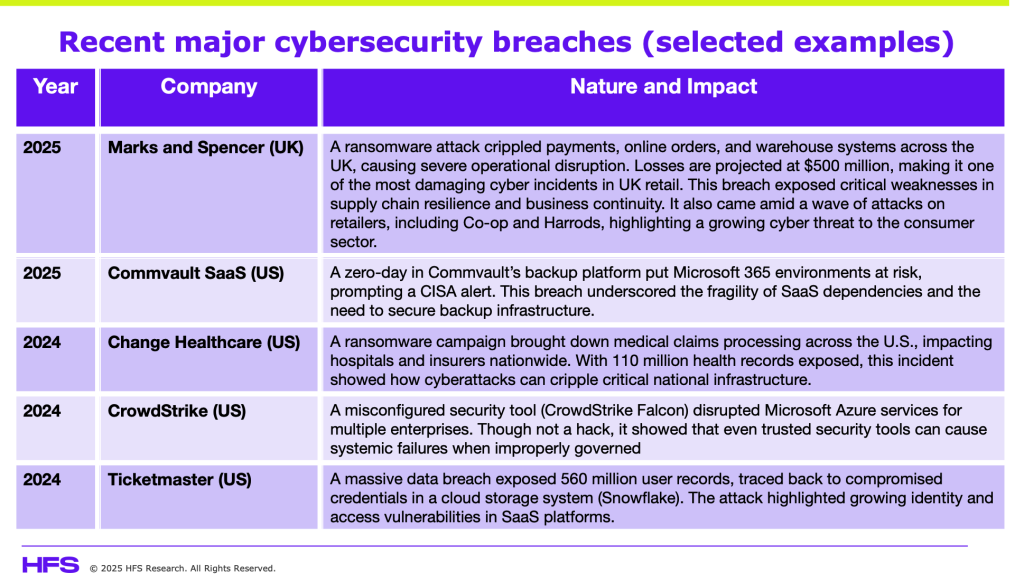

The pressure point has become the CIO, who not only has to manage significant pressures from their boards and leadership peers to deliver an AI agenda, but they also have to balance this with a proactive, holistic cybersecurity approach that business leaders can comprehend. Mess up your cybersecurity, and you’re not only fired, but your entire firm may just sink with you. And for every cyber-attack that goes public, we estimate another six are kept under wraps to avoid negative publicity, remaining unreported or even undetected:

Enterprise leaders must treat cybersecurity as a strategic boardroom issue, not merely an IT function

This is why we do not believe a CISO should report to the CEO, as the CEO really needs to understand the risks and how to proactively get ahead of them. CISOs tend to be too technical, whereas the CIO is evolving as the hybrid executive who can translate technical issues in plain business terms. In addition, with all the pressure to deliver on AI, the CIO is best placed to bring the cyber strategy into the conversation, as there simply won’t be successful AI without an effective cyber strategy.

This paper unpacks the modern cyberwarfare playbook, outlines its enterprise implications, and provides a security readiness agenda that organizations must prioritize in an era of digital warfare.

Cyber tactics are now strategic weapons of war

Before diving into each tactic in depth, the table below summarizes the most common cyberwarfare methods, their typical targets, intended impacts, and real-world examples observed in recent conflicts.

Let’s now examine these threats in greater detail:

Cyber Espionage Is a Silent Strategic Weapon

Cyber espionage is among the most insidious tactics in modern cyberwarfare. It involves stealthy infiltration into government networks, defense systems, and critical infrastructure to extract sensitive information—military strategies, diplomatic communications, or classified research. These campaigns are often the work of state-sponsored Advanced Persistent Threats (APTs). The long dwell times and covert nature of these breaches make them especially dangerous, and they can unfold undetected for months, quietly eroding national security.

Sabotage of Critical Infrastructure

Attacks on critical infrastructure are no longer speculative, they are documented weapons of war. Power grids, water supply systems, transportation hubs, telecom, and financial institutions are prime targets due to their symbolic and systemic value. Disabling such services can incite public panic, disrupt military logistics, and hobble a nation’s economy.

Denial-of-Service (DoS/DDoS) Attacks

Distributed Denial-of-Service (DDoS) attacks involve flooding a target’s servers or websites with overwhelming traffic, making them inaccessible. These attacks often aim to paralyze essential services like banking, government portals, or emergency response systems during times of peak demand. In recent conflicts, banks have established “war rooms” to monitor and neutralize such attacks on financial infrastructure, recognizing that even temporary outages can cause economic damage.

Disinformation and Psychological Warfare

Modern cyberwarfare also weaponizes information. State-sponsored troll farms, fake social media profiles, and AI-generated content flood platforms with misinformation designed to erode public trust or manipulate opinion. During active conflicts, fake videos, doctored images, and viral rumours often circulate faster than facts. The goal is not just confusion—it’s psychological destabilization.

Ransomware and Wiper Malware

Ransomware typically locks critical files and demands payment for their release, while wiper malware is designed purely to destroy data. In war zones, these tools can disrupt media outlets, hospitals, transportation, and public sector databases.

Fake Domain Attacks and Social Engineering

Threat actors often register lookalike domains, like “gov[.]in” clones or fake military emails to deceive targets. These are used in phishing attacks to steal credentials or implant malware. These tactics, as seen with actors like APT36, exploit human trust as much as technology. This reinforces that cyberwarfare doesn’t always involve zero-days or advanced code—human deception remains one of the most effective vectors.

Cyber risk now reaches every node—from the boardroom to the smartphone

The broad reach of cyberwarfare means that no one is immune—not just governments and militaries, but also hospitals, utilities, media, private enterprises, and ordinary citizens.

Governments and National Security

Defense ministries, intelligence agencies, and critical infrastructure operators are prime targets. The need for robust cyber defense postures, including threat intelligence sharing, rapid incident response, and sovereign cloud strategies, has never been more urgent. Enterprises must integrate with national threat intelligence initiatives and not operate in silos—public-private cyber cooperation is now survival, not strategy.

Financial Institutions and Corporations

Banks, payment processors, and fintech firms are increasingly in the crosshairs of both nation-state actors and criminal proxies. Disruption of financial services not only causes direct economic loss but also undermines national morale and investor confidence. CISOs and CFOs must jointly model the impact of multi-day outages—not just from a tech standpoint, but investor confidence and liquidity.

Citizens and Civil Society

Ordinary users are not exempt. Malware-laced videos, phishing messages on messaging apps, and spyware hidden in mobile content put smartphones and personal data at risk. These devices can also be hijacked into botnets or used as entry points into corporate systems.

Security can no longer be just a defense—it must be a digital war doctrine

The shifting cyber risk landscape demands more than patchwork defenses—it requires holistic, governance-driven frameworks across all levels of society.

For Individuals:

Individuals are no longer bystanders in digital conflict. Practicing basic cyber hygiene—strong passwords, MFA, regular updates, and healthy skepticism on social media—must become habitual. Each personal device is part of a nation’s cyber terrain.

For Organizations:

Operationalize war-room readiness: Crisis simulations and red-teaming must become part of quarterly risk oversight.

Elevate employee awareness: Training must go beyond phishing modules—employees must understand geopolitical vectors and supply chain infiltration.

Audit digital supply chains continuously: Most vulnerabilities now enter through cloud vendors and third-party platforms.

Backups are not optional: They must be segregated, immutable, and tested frequently.

For Boardrooms and Policy Leaders:

Leadership must stop asking if cyberwar will affect them—and start preparing for when it does. Key questions every board must ask today:

Do we have strategic visibility into our cloud, SaaS, and geopolitical risk exposure?

Can we maintain operations during a symbolic, high-profile cyberattack?

How will we defend brand trust if misinformation targeting our leadership goes viral?

Global cyber instability demands enterprise engagement in rulemaking

In the absence of attribution standards, the private sector is often left to interpret silence as safety. Enterprises must advocate for clearer norms and participate in attribution consortia and not wait for government-led rules to trickle down. Enterprises cannot wait for digital Geneva Conventions. Industry coalitions must take the lead in defining cyber accountability protocols, especially in cross-border supply chains and critical services.

These costs are cascading to enterprises through compliance mandates, insurance premiums, and operational disruptions. Leadership must start quantifying cyber conflict readiness as a financial exposure in annual reports and audits.

Bottom Line: Cyber conflict is now a business continuity threat, a brand risk, and a geopolitical wildcard.

Cyber conflict is now a business continuity threat, a brand risk, and a geopolitical wildcard. Enterprise leaders must treat it with the same urgency and discipline as they do financial risk or regulatory exposure. It’s time to move beyond firewalls and frameworks to establish a living cyber doctrine—one that includes red-teaming, board-level risk modeling, threat-sharing participation, and scenario-based preparedness.

The question is no longer if you’ll be targeted. It’s whether you’re prepared to respond at the speed of a nation-state actor.

Act now: appoint a cyber conflict readiness officer, fund cyber resilience as an innovation stream, and demand geopolitical threat briefings at the board level. Because resilience in the age of cyberwar isn’t just technical—it’s cultural, strategic, and existential.

Visa and Mastercard just escalated the war for the future of commerce—not with another app, but with autonomous AI agents that buy on your behalf.

These aren’t lab experiments. Visa’s Intelligent Commerce and Mastercard’s Agent Pay are foundational shifts designed to embed payments into AI platforms that consumers already trust.

The implications for enterprise marketing are nothing short of seismic, and the following class of applications is under threat:

Ecommerce platforms like Adobe Commerce, Shopify, and Salesforce as AI agents bypass frontends entirely by making decisions and completing purchases autonomously.

SaaS tools for behavioral analytics and personalized product recommendations (e.g., Dynamic Yield, Monetate, Nosto)

Commerce Is Becoming Agentic—and SaaS Is Losing Its Grip

Visa integrates tokenized payments into agents OpenAI, Microsoft, and Anthropic developed. Mastercard is launching Agent Pay to handle secure transactions via AI, using a system of agentic tokens to verify trust and authorization. These aren’t front-end bells and whistles—they are backend rails designed to replace the shopping cart, the e-wallet, and potentially the SaaS commerce stack itself.

Forget clicking, browsing, or tapping. Tomorrow’s consumers can offload their entire shopping experience to trusted AI agents: searching, choosing, transacting.

Six months ago, we at HFS outlined precisely this vision (see our previous POV, “Reimagining e-commerce with AI: the dawn of interactive commerce“), emphasizing AI-driven personalization, real-time recommendations, and autonomous purchasing as the future of digital commerce (see below). These recent moves by Visa and Mastercard directly support that bold prediction.

We’ve Been Here Before—But This Time, the Tech Can Deliver

Skepticism is warranted. We’ve seen overhyped commerce experiments flop before. Voice commerce flatlined. Chatbots collapsed under their own UX failures. Even Amazon’s Dash Buttons died quietly, abandoned by customers who preferred frictionless app-based buying.

But generative AI isn’t Alexa. Today’s GPT-class agents don’t just react—they reason, personalize, and adapt to individual behaviors in real-time. Visa and Mastercard are embedding commerce into agents consumers trust—Microsoft Copilot, OpenAI’s ChatGPT—and are not trying to build new destinations. The Apple Pay strategy is reborn but with an intelligence layer on top.

Trust Is the New Commerce Interface

Here’s the rub: none of this works if enterprises don’t aggressively confront the trust equation. Consumers will not adopt agentic commerce if transactions feel opaque or risky. Visa and Mastercard offer spending limits, granular controls, and advanced fraud protection—but enterprise leaders can’t outsource this responsibility.

Enterprise leaders must now ask:

How do we expose our catalog, pricing, and inventory to AI agents?

How will we audit and verify agent-led purchases?

What is our liability if an agent misfires?

Failing to answer these questions risks marginalization. In a world where AI agents filter and finalize purchases, invisibility equals irrelevance.

Enterprise Leaders Must Act Now to Stay in the Game

Don’t wait for agentic commerce to go mainstream. The fundamental shift in how platforms manage transactions and data flows is underway. The new power brokers—Visa, Mastercard, OpenAI, Microsoft—are building commerce ecosystems where SaaS apps and digital storefronts may no longer be the primary interface.

Enterprise leaders must:

Pilot AI-agent exposure: Experiment with exposing products to agent ecosystems (e.g., integrating with GPT plugins or Microsoft Copilot).

Design for machine-first buying: Rethink UX, metadata, and taxonomy to serve AI agents—not humans.

Double down on trust infrastructure: Build transparency, consent, and explainability into every touchpoint—because the agent is now the user.

Bottom Line:AI agents are not another channel—they are a new species of consumer. Enterprise commerce leaders must prepare for a world where decisions are outsourced to autonomous systems, not influenced by UX or loyalty programs.

Enterprises must build trust into every AI-agent interaction because, without transparency and control, agent-led commerce dies before it scales. The winners will be those who operationalize agentic commerce today—exposing product data, managing liability, and building trust before Visa and Mastercard become the invisible middlemen behind every transaction. Waiting means disappearing from the decision-making process entirely…

The energy and utilities (E&U) industry must transition while it’s still an option. AI is proving value in an old sector during the push for optimization and continued (yet too slow) decarbonization. However, transition planning is nowhere near the level it should reach (see our call to action). There’s still time to lead as an individual, team, or firm across emerging tech and sustainability. Make it personal. Be part of the systems change, whether you’re an E&U individual, team, or whole organization in an enterprise or service provider.

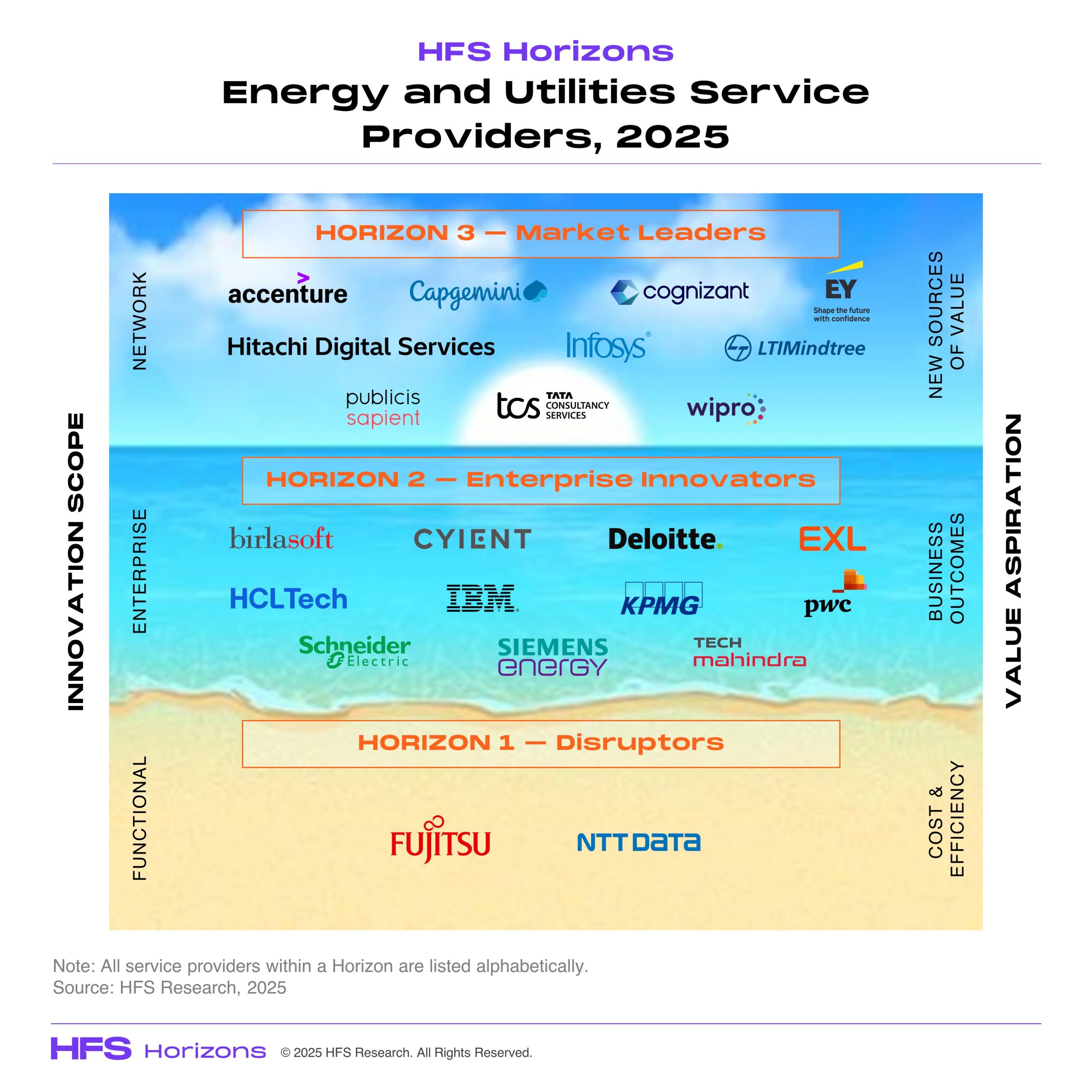

The 2025 HFS Research Horizons study for the E&U sector assessed 23 leading consulting, technology, and business service providers (see Exhibit 1). That study examined the providers’ value propositions (the why), execution and innovation capabilities (the what), go-to-market strategy (the how), and market impact criteria (the so what). Horizon 3 firms show market and systems-changing leadership. Horizon 2 firms powerfully work across organizational silos. Horizon 1 firms execute efficiently. The E&U services market is also growing: revenues, headcounts, and client numbers grew 44%, 36%, and 17%, respectively, over the past three years.

Exhibit 1: E&U’s technology and sustainable transitions mean an economically, socially, and environmentally pivotal role for consulting, technology, and services companies

The E&U industry is being reshaped and it’s a bumpy process—sometimes it seems rapid; other times, much less so

That disruption goes beyond addressing the climate emergency and energy transition. Emerging technologies, including AI, physical-digital combinations such as grid upgrading, and outcomes such as creating genuinely positive customer experiences (CX) are also top of mind for enterprise business and technology teams.

The sphere of influence is massive for all services firms. But does the ambition match?

The Horizons report includes detailed profiles of each service provider, outlining their numbers, strengths, and development opportunities. The report is global in scope and helps enterprises of all shapes and sizes, service providers offering E&U services, and ecosystem partners.

The CIO agenda and how efficiency drives AI, emerging technology, and the energy transition

The E&U industry is focused on efficiency above all else. This clarity is an unmissable opportunity to align the technology suite, including AI in its various forms, toward shared goals throughout organizations and ecosystems such as optimization and decarbonization (we deep dive here). The industry also needs clarity from its CIOs. To target efficiency, tech, systems, and processes must connect, with security ensured and innovation maximized (we outline this agenda here).

The industry talent crisis continues—it must transition while still being an option

E&U enterprises are calling for transition planning across sectors (we highlight here). The industry should transition while ‘leading’ is still an option (we called for this in launching the study). Collectively, as an industry, we must improve our ability to communicate the benefits to the planet, people, and business. The energy industry has also faced a decade-long talent problem connected to its unsustainability. The sector is not seen as high-tech either. Energy needs new, ambitious, and diverse talent to address the climate and sustainability emergency and adapt to technologies such as AI (we assess how E&U can find its best self here).

The utilities vision is a positive, proactive CX; digital grids also see investment but need collaboration

Utilities must go beyond providing a neutral CX. Combinations of emerging technology, including smart meters and GenAI, will win out by producing new positive CX and outcomes for customers—and doing so proactively. Enterprises—from water to electricity providers—are incorporating these technologies and new processes to move toward better experiences, but none are yet truly in the positive camp. Some are gearing up to target that camp. But most utilities are struggling with their existing systems that a net-neutral CX is the best they can currently hope for.

Demand is also not reaching a critical mass in EV or broader distributed energy networks. Governments are struggling to find the necessary investments for grid infrastructure. E&U enterprises will have to pick up the tab. Better that tab be picked up in public-private partnerships to make sure the upfront cost of the energy transition does not fall on the least advantaged through large increases to energy and water bills. History suggests that a monumental change in approach is needed to avoid such an unjust outcome. A lack of system collaboration among tech, regulators, industry, and consumers hampers new successful market design.

DeepSeek is setting new expectations regarding training and related costs, and we expect market leaders to respond.

Voice of customers and partners

Co-innovation with major industry clients is a clear differentiator for leading services firms, alongside expected themes such as execution and existing relationships. The depth of domain knowledge stands out among providers that use a similar language. Ambition for systems-changing AI and sustainability also separates the best from the good.

The Bottom Line: To ensure a successful transition, E&U enterprises must attract the best talent before they’re dragged by systemic change. The services market is expanding to meet this challenge but has much more orchestration and collaboration to master.

This Horizons study examined the E&U industry’s overall story: enterprises must improve their transition plans and ecosystem collaboration; maximize innovation and ensure security through new, clear governance; address a continued talent crisis; and find new positive proactive customer experiences.

The analysis also outlines how the consulting, technology, and services industry must enhance its ecosystem orchestration and co-innovation with systemically important companies that can drive the systems change that technology and the energy transition need.

If you’re an enterprise leader staring down ballooning tech debt, rising pressure for AI transformation, and daily new product drops that all scream “innovate now or be left behind,” stop. Take a breath—and read this wide-ranging Q&A between Cognizant CTO for AI, Babak Hodjat, and HFS Executive Research Leader David Cushman.

Babak has agentic AI cred in spades and has been operating in this space for three decades. He was the main inventor of core massively distributed evolutionary computation technology as co-founder and CEO of Sentient Technologies. When Cognizant acquired Sentient’s IP assets in 2019, Babak came along for the ride. Sentient’s platform combined evolutionary computation, which mimics biological evolution, and deep learning, which is based on the structure of nervous systems. His patented work on artificial intelligence led to the technology used by Apple for its digital assistant Siri. In short, Babak’s entire career has been rooted in the humanization of technology, which forms the basis of what we today call Agentic AI.

However, it wasn’t until Ravi Kumar took the reins at Cognizant that he quickly unearthed this gem and encouraged Babak to energize the firm’s multi-agent strategy under its Neuro AI brand.

The conversation cuts through the agentic noise to tackle what enterprises need to do today. Chasing a “god model” of general-purpose, all-knowing AI is a distraction. The real opportunity lies in engineered agentic systems—practical, modular, governable, and already delivering enterprise value.

This is how AI becomes real.

From Siri to agentic systems: the long road to a practical AI future

HFS: It’s striking how far back your work in this space goes.

Babak: Yeah, I got into agents in the mid-90s. I wrote about agent-oriented software before it was a thing. The code that led to Siri was multi-agentic. Each component understood a piece of context. Plug in a new DVD player to your entertainment ‘stack’,Read More

Apple’s pivot to shift its US iPhone manufacturing from China to India by 2026 isn’t just significant—it’s monumental, and it’s happening at warp speed for such a huge manufacturing shift.

This also signifies the deepening links between the US and India as these global trade wars gather pace. Apple is expected to create over 600,000 new jobs in India through its supplier ecosystem and also help fund its broader $500 billion investment plan in the U.S., strengthening its dual commitment to global resilience and domestic innovation.

The impact of geopolitics at the core of Apple’s move

Think about it: we’re witnessing the strategic decoupling of one of the world’s largest tech titans from its longstanding reliance on China, driven by geopolitical tensions, tariffs, and a desire to insulate against future disruptions. This isn’t just supply chain optimization; this is Apple’s full-throated acknowledgment that geopolitical risk is now the primary disruptor of global tech, as revealed in our current HFS Pulse research covering the dynamics of Global 2000 enterprises:

Let’s not underestimate the size of this operation. One million workers in China are involved in the manufacturing of iPhones through Apple’s suppliers, notably Foxconn and Pegatron. Specifically, Foxconn’s Zhengzhou Technology Park, often referred to as “iPhone City,” employs around 350,000 workers dedicated to iPhone production. Additionally, Foxconn’s Longhua Science and Technology Park in Shenzhen employs between 230,000 and 450,000 workers, many of whom are engaged in assembling Apple products, including iPhones. These figures underscore the extensive labor force required to meet global iPhone demand and highlight the significant role China has played in Apple’s manufacturing operations.

India becoming the “New China”?

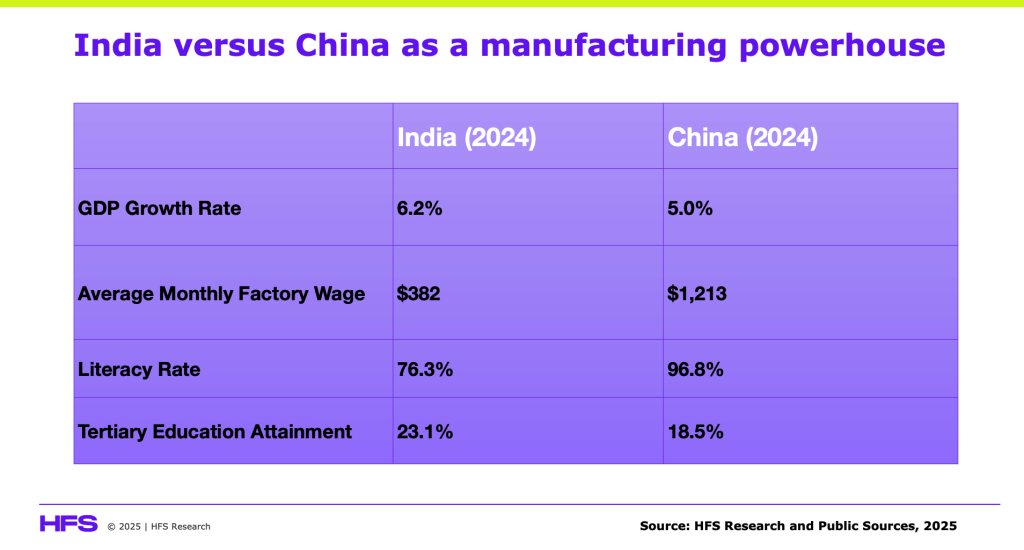

This strategic realignment underscores a broader trend: India emerging as a viable, large-scale manufacturing alternative to China. But let’s be clear—this isn’t simply about swapping flags on factories. India’s ambitions to become a global tech manufacturing hub are clear, yet the journey won’t be without friction. Production costs remain higher, infrastructure still poses major challenges, and the complexity of achieving quality and scale comparable to China is significant.

India is increasingly being dubbed the “New China” for several compelling reasons. Firstly, its demographic advantage—characterized by a young, skilled, and abundant workforce—provides a sustainable competitive edge. Secondly, the Indian government has rolled out aggressive policy measures, including tax incentives, streamlined regulations, substantial infrastructure investments to attract all the global tech companies, and a huge expansion of the Global 2000 into Indian cities, with 1.6 million Indians being employed in global capability centers. HFS estimates over 2.7 million people will occupy India’s GCCs by the end of 2026, which could top 4 million staff by 2029

With approximately 248 million students enrolled in over 1.47 million schools, India offers a massive future labor pool. Moreover, India’s commitment to digital transformation and innovation, supported by a vibrant tech ecosystem, positions it as an attractive destination for high-value manufacturing:

Bottom line: We’re arrived at a defining moment in India’s future as the world’s emerging manufacturing/tech powerhouse

Apple’s decision sends a resounding signal. It validates India’s potential and puts a bright spotlight on the Indian government’s proactive stance on incentivizing tech investment. This move could catalyze an industry-wide rethink about supply chain resilience, shifting the narrative from cost-driven globalization to geopolitically-driven diversification.

Challenges will be inevitable, but Apple’s bold move to India is undeniably a bellwether. Other tech hardware giants watching from the sidelines will inevitably reconsider their strategies. Apple’s India pivot isn’t just strategic—it’s transformative, reshaping the tech supply chain landscape profoundly and permanently.

This also raises the debate over $500 billion Apple has declared to be invested in advanced manufacturing in the US over the next four years to support Apple Intelligence with domestic workforce expansion, education initiatives, and datacenter expansion. If effective, we will end up with a cohesive US/Indo global operation that powers 1.4 billion iPhone users.

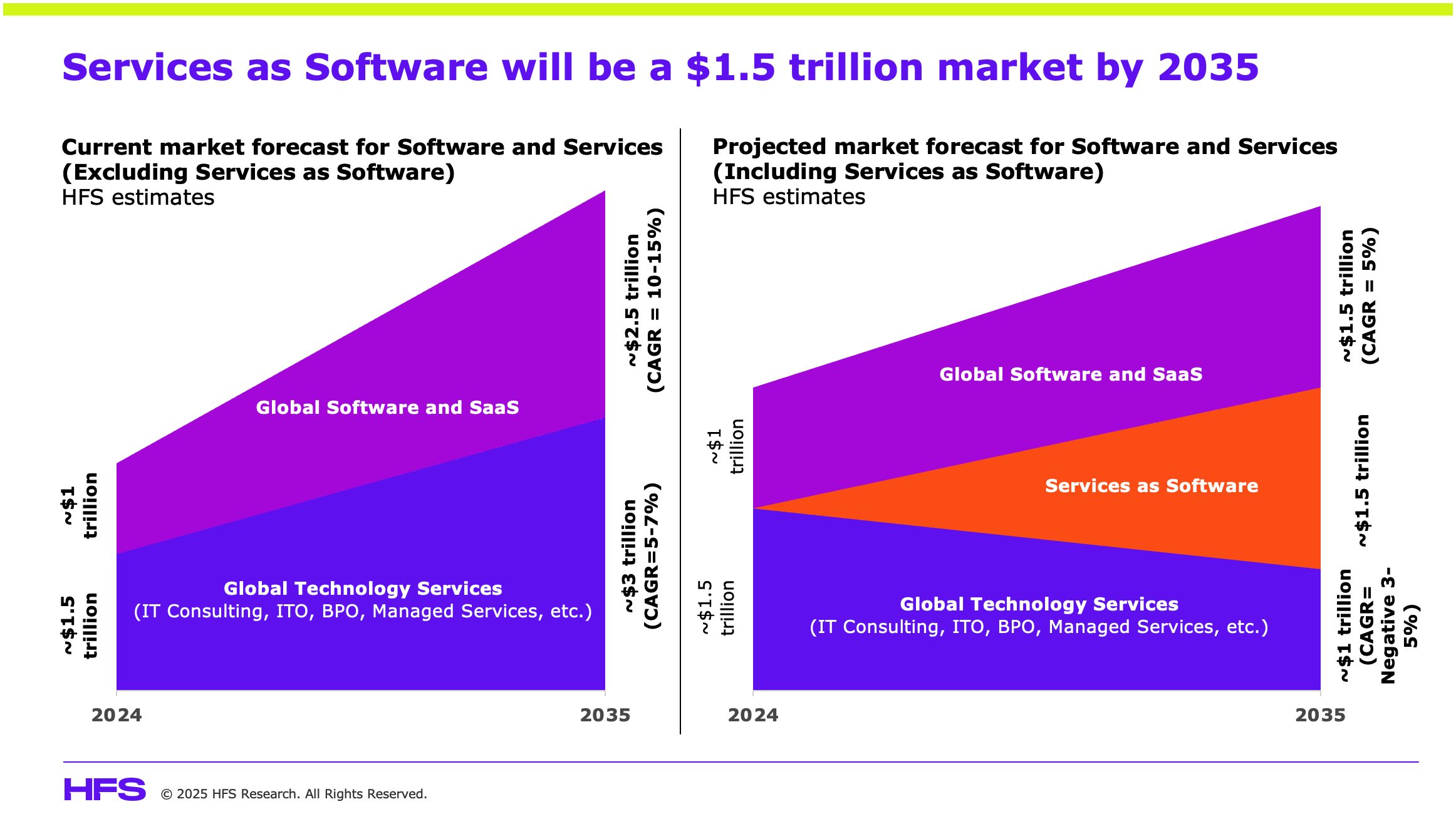

As speculation of a Capgemini takeover of WNS heats up, you have to question the future of BPO specialist firms as the worlds of services and software continue to blend together in this rapidly emerging $1.5 trillion market, which HFS last year termed “Services-as-Software”.

It’s been years since there has been such a significant merger of services at this scale, in fact, you have to look back exactly a decade to the Capgemini acquisition of iGATE to compare a services marriage at this scale and market impact. However, this potential acquisition is different as it represents a BPO powerhouse adding significant process domain and scale to one of the major IT services firms, which would boast one of the largest BPO portfolios in the industry, estimated at more than $2.5 billion.

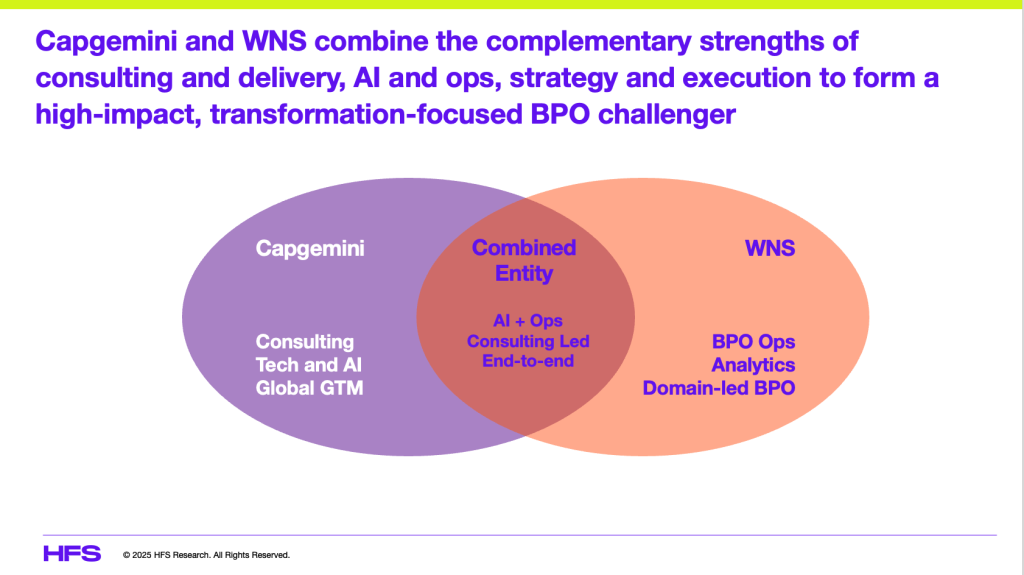

With Capgemini’s sheer global scale and depth of technical capabilities, the addition of WNS could create an ideal incubation business to develop leading-edge Services-as-Software solutions to attack this huge emerging marketing opportunity:

Enterprises’ adoption of Generative and Agentic AI solutions eliminates manual efforts, which threatens the revenues of pure-play BPO companies.

However, the technical sophistication required to deploy enterprise-class Services-as-Software requires substantial technology expertise not traditionally found among BPO specialists.

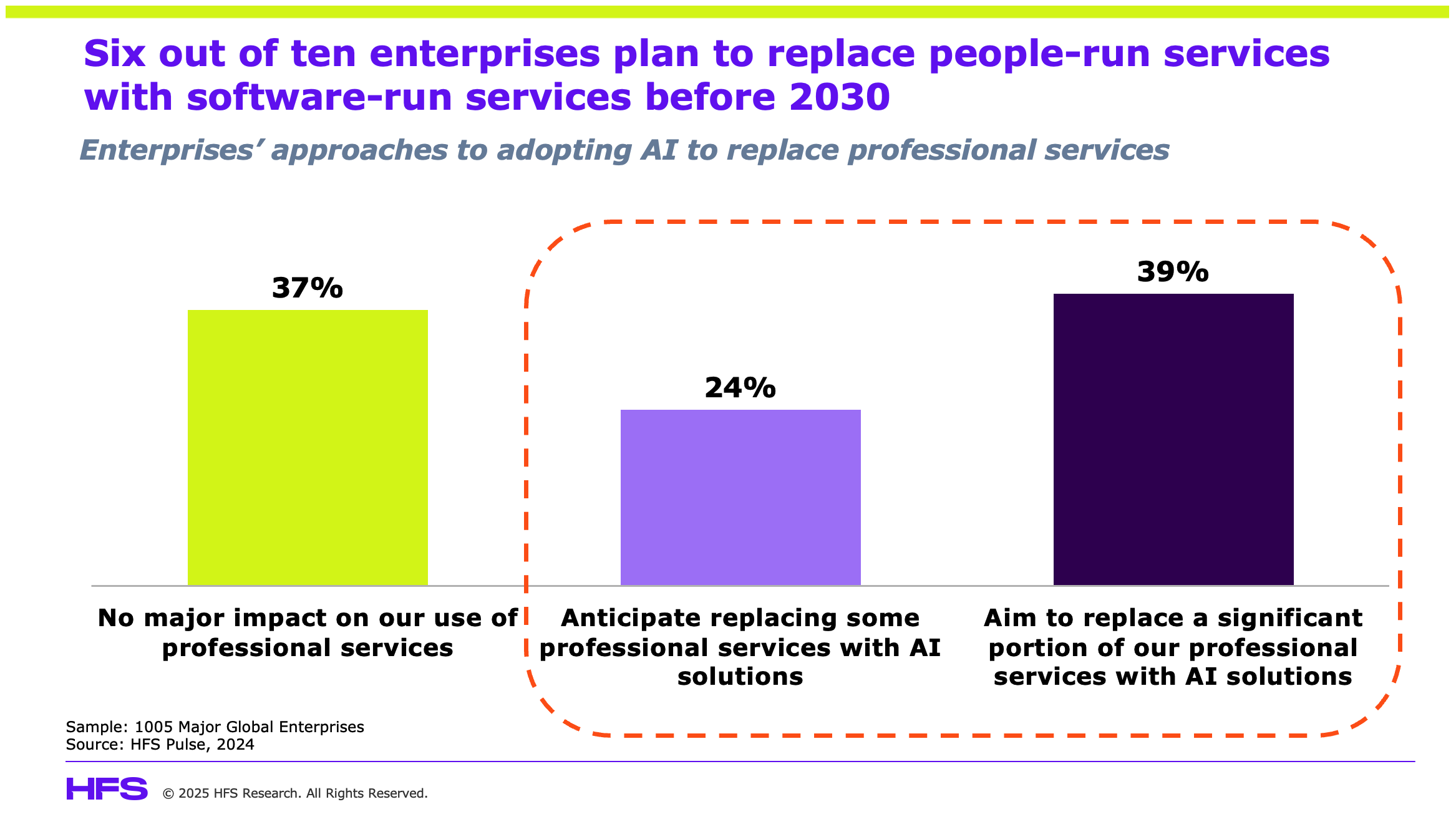

Enterprise appetite for pure-play BPO solutions is rapidly waning as enterprises advance Services-as-Service agendas with lesser dependency on armies of people to execute processes. Our recent research of over 1000 major enterprises already shows 6-out-of-10 enterprises expect to replace professional services with AI-driven solutions over the next five years:

Likely seeing the strengthening preference for technology-centric solutions over cheap “butts-in-seats”, WNS’s potential purchase by Capgemini provides shareholders with a perfectly timed exit. In turn, Capgemini acquires WNS’s deep vertical process experience and the ability to mine WNS’s vast client base for sales opportunities focused on buyers’ strongest preference: replacing BPO solutions with Services-as-Software, one of Capgemini’s emerging strengths.

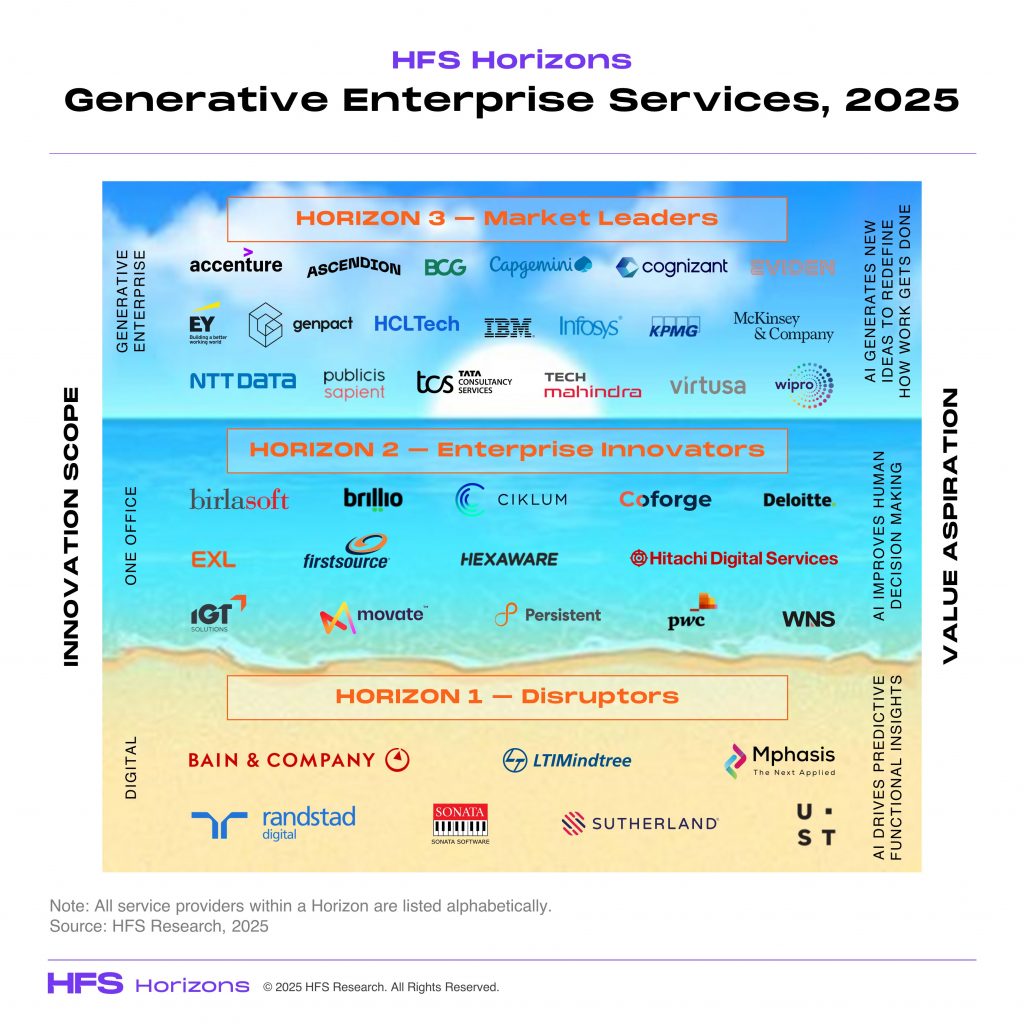

Capgemini has always stood out for its global consulting capabilities, and it strengthened its US presence and technology capabilities with its 2015 $4B acquisition of iGATE. Since then, Capgemini’s technology leadership has accelerated. In 2023, Capgemini announced a 3-year €2B investment in AI capabilities, leading to the development of the Reliable AI Solution Engineering (RAISE) operational accelerator, IDEA, and the “Trusted AI framework” for the industrialization of GenAI projects. In 2022, 2023, and 2024, Capgemini acquired Quantmetry, BTC, and Syniti, respectively, to bolster its AI and data capabilities. Further, Capgemini built class-leading ecosystem relationships with hyperscalers, data management firms, and AI-specific companies (like Mistral AI and Liquid AI). By early 2025, these capabilities had won the firm 350+ projects with large enterprise customers spanning all major industries. HFS Research placed Capgemini squarely in the Horizon 3 tier in our 2025 Generative Enterprise Horizon study:

Yet, winning new enterprise customers in a tightly competitive market has become more competitive and challenging. Business process expertise is required to fully implement Services-as-Software capabilities. Thus, Capgemini’s potential acquisition of WNS is focused on two key strategic factors: WNS’s vast industry-specific process experience and the opportunity to mine WNS’s piles of legacy BPO deals that enterprise leaders want to convert into Services-as-Software.

WNS offers enterprises deep domain expertise and operational excellence

WNS is a clear leader in providing domain-specialized BPO services, with crown jewels in BFS, insurance, healthcare, TMT, procurement, F&A, and travel and hospitality, leading to a $1.3B BPO client portfolio mix of large and medium-sized clients. Enterprise customers laud WNS’s flexibility and creative commercial contracts that align innovation incentives, and clients have confirmed WNS soundly delivers on its skin-in-the-game promises. That said, WNS’s advancements in Generative AI have not been as substantial as those of other competitors. While it has invested in 80+ AI assets and partnerships, its capabilities only earned it a Horizon 2 rating in our 2025 Generative AI Horizon (see above). As a largely BPO-centric firm, WNS’s technology and Generative AI capabilities just aren’t as deep as those of other companies.

To a firm like Capgemini, WNS’s high-quality client base is a gold mine of sales opportunities: client operations executives who want to replace BPO services with Services-as-Software. Further, WNS’s deep domain expertise, the cornerstone of its client growth rate, provides Capgemini, which has historically lagged behind other companies in terms of domain-specific operational BPO delivery, with both a vast BPO capability and thousands of industry business process experts that can be teamed with its consulting and technology staff to deliver next-generation client solutions.

Capgemini + WNS Would Be More than the Biggest IT + BPO deal in a decade

At $1.3B in revenue, Capgemini’s potential acquisition of WNS would result in a paltry 5% increase in Capgemini’s $25.5B business. Yet, the total headcount increase of the combined entity is a whopping 19% – which speaks to the underlying manual nature of WNS’s client-base. Capgemini’s industry-leading consulting teams will have the opportunity to mine WNS’s clients for transformational opportunities while also leveraging WNS’s class-leading process domain expertise to expand Capgemini’s largely consulting and technology-centric client base to operational capabilities clients, where clients are focused on slashing people-centric costs and improving process outputs through technology-centric solutions. It’s an AI + Operations win-win for the collective client base of both firms, positioning Capgemini as the incumbent for hundreds of operations clients looking for Services-as-Software solutions.

From a competitive perspective, another potential big win for Capgemini is its new positioning against the Big 4 (Deloitte, PwC, EY, and KPMG), which have traditionally dominated consulting and technology services. With WNS’s operational expertise integrated into its offerings, Capgemini could deliver end-to-end transformation services that the Big 4 cannot – and at lower price points.

In some cases, like procurement services, Capgemini acquires a well-established strategic sourcing capability built on WNS’s 2017 Denali acquisition, strengthening Capgemini’s F&A and procurement capabilities. Finally, WNS’s North American and UK-centric client base allows Capgemini to expand its geographic footprint.

Can pure-play BPO players take on consulting-led, technology-centric transformations?

The potential of a Capgemini acquisition of WNS also highlights the challenge all pure-play heritage BPO providers have: can BPO-centric providers, like Genpact and EXL, take on the Services-as-Software transition? Lacking deep consulting and technology chops of Capgemini, Accenture, IBM, and the Big 4, how can companies lacking best-in-class capabilities win the hearts and minds of enterprise customers hell-bent on slashing operating costs through Services-as-Software capabilities?

The big deals of the future won’t be focused on 500-1000 seat ITO and BPO deals. Rather, the enterprises’ focus on real transformation will force service providers to come to the table with deeper skills and capabilities than ever before. This may leave traditional BPO companies picking up smaller BPO-centric deals while losing their larger client base, which is making a dramatic shift towards Generative and Agentic AI solutions.

As the following chart exhibits, only a handful of these heritage BPO firms are continuing to operate in growth scenarios and desperately need to reinvent themselves to evolve in the Services-as-Software era:

WNS’s evaluation of a strategic exit may be the dying canary in the coal mine, announcing the death of BPO-centric deals and pressure from existing clients at renewal time on true transformation. Given the shift in demand, their potential valuation may never be higher, which may put yet more pressure on BPO pure plays.

The Bottom Line: Capgemini + WNS is a bold statement about enterprise demand shifting from FTEs to Services-as-Software, creating a combined entity that could compete on an equal footing with Accenture and outcompete the Big 4.

The Capgemini-WNS acquisition is a pivotal opportunity to lead the shift to Services-as-Software. By combining consulting, technology, and domain-driven BPO, Capgemini + WNS has the potential to lead AI-powered business transformation, with a robust incumbent WNS client base hungry to replace FTEs with technology solutions.

If Capgemini succeeds, it will send a chilling message to the BPO market: without consulting and technology capabilities, you’ll be left picking up table scraps. And to the Big 4, Capgemini sends a message of operational savviness and incumbent positioning that the Big 4 simply don’t have.

While the US administration obsesses with pointing DOGE at relatively small levels of governmental expenditure in areas such as USAID and the Department of Education, when it comes to US healthcare, there are levels of cost inefficiencies and improved outcomes that could reach trillions of dollars if managed effectively.

In fact, if US healthcare were its own country, its annual spending of $5.2 trillion would make it the world’s third-largest country by GDP. Yet, the US has amongst the worst health outcomes among OECD countries, with the lowest life expectancies for both men and women, and has not been able to address obesity and mental health epidemics:

At the same time, the prevalence of chronic conditions rises without checks. So, in some ways, DOGE hacking away at what it considers wasteful spending of taxpayer’s money is welcome. In that context, we provide DOGE recommendations on where such cuts should be in healthcare.

These three main categories drive the cost of healthcare in the US:

Compensation for everyone in the healthcare ecosystem (doctors, nurses, administrators),

While compensation and therapies have opportunities to be streamlined and reduced, the administration cost can be hacked with DOGE recklessness without legislative action and yield better outcomes:

US healthcare admin costs double that of comparable countries with worse health outcomes

According to an analysis by the Mercatus Center, the US had upwards of 42,000 regulations instituted by the Department of Health and Human Services as of 2020. These regulations are additive to state and local regulations. No wonder the US spends about 7% of its per-capita healthcare spending of ~$15,000 (2024) on administrative processes, twice that of comparable countries (Austria, UK, France, Germany).

While regulations are essential to ensure rules are applied evenly, health consumers are protected, proper care is rendered, and payers, providers, pharma’s, and other ancillary organizations deliver their services as health fiduciary agents. However, when those regulations add costs materially and inhibit or delay care, it is time to eliminate them.

There is a laundry list of regulations that have done nothing but add costs and risk to human life. Some that require immediate attention are:

Prior authorizations (PA): This process requires providers or consumers to seek approval from health insurers before getting treatment. PAs lead to delayed treatments and often abandoned treatment, causing health risks to patients. They also require providers to add staff to manage PAs. Analysis of 2021 Medicare data shows that 95% of all PAs were approved. This reflects the enormous cost and health risk burden being unnecessarily imposed on the US healthcare system.

HIPAA: While the 1996 law’s intention is still valid, its overuse has added cost and made data sharing unnecessarily complicated. Given that pre-existing conditions cannot be factored into underwriting risk, it is time to readjust how HIPAA is utilized…privacy is different in the 21st century than in the last one.

Interoperability: CMS rules to drive interoperability are based on a fundamentally wrong premise. Healthcare data belongs to consumers, not the government or health insurance companies. Consumers alone must decide who, when, what purpose, and for how long their health data can be used. CMS or other healthcare entities have no business in determining these rules. Elimination of interoperability rules should release significant resources and administrative burdens. Instead, private-public efforts must create a consumer-facing healthcare data aggregation solution…my data on my mobile app.

Recommendation to DOGE: Eliminate any regulation that does not explicitly reduce cost and improve health outcomes within 12 months.

There is nothing valuable about value-based care

Since the 1960s, the US has been experimenting with value-based care (VBC) with little to show. CMS defines this concept as designing care to focus on quality, provider performance, and the patient experience. Over the last 60 years, CMS has driven countless programs (see Exhibit 3), yet estimates suggest that less than 25% of all Medicare contracts are aligned to some form of VBC. VBC is a dead concept, given that it seeks to impose an insurance construct on care delivery, which has no proof of working consistently and at scale over time.

While the idea of holding everyone in the healthcare ecosystem accountable for costs and outcomes is important, there is no precedent for it in any part of the world…yet. There may be private-public options to achieve a capitated model based on social determinants of health; however, those are in the realm of possibilities rather than current realities.

Recommendation to DOGE: Sunset all CMS VBC programs immediately.

DHHS needs organizational simplicity and 21st-century purpose

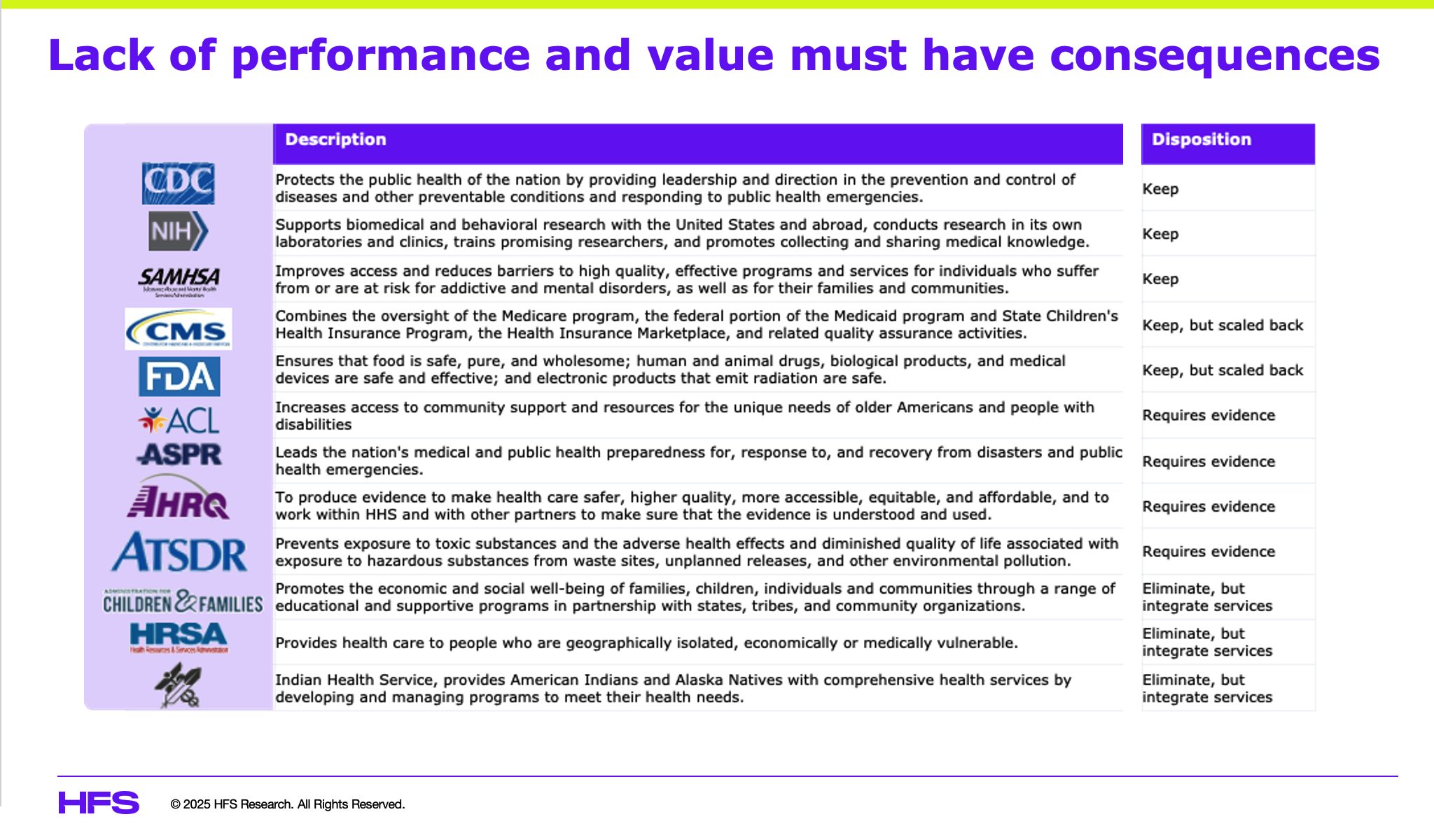

According to the US Department of Treasury, in fiscal 2025, the Department of Health and Human Services (DHHS) will account for 26% of all US government spending. It is the largest agency by budget and influences the largest category of spend. Yet, the US health outcomes continue to decline and are a laggard amongst OECD nations seen through the lens of life expectancy, prevalence of chronic conditions, and epidemics (opioid, obesity, mental health). This is an unacceptable story requiring an organizational overhaul (see Exhibit 3) to reduce costs by simplifying and eliminating what does not work.

DHHS has 11 sub-agencies, three focused on human services and eight on health. The purpose of many of these sub-agencies either overlap or are not relevant anymore. Changing demographics, challenges of the 21st century, and advanced technologies justify rationalizing these agencies. There are three categories for the disposition of DHHS agencies:

Keep: These are agencies whose purpose is central to critical programs that prevent pandemics or epidemics while allowing the US to keep leading on disease management, such as CDC, NIH, and SAMHSA. Other agencies should be allowed to function but scaled back through the elimination of wasteful administrative functions. Agencies like CMS and FDA can leverage technologies and streamlined processes to address their mandates.

Requires evidence: These are agencies whose purpose needs validation through outcomes they delivered or influenced over the last five years. Agencies like ACL, ASPR, AHRQ, and ATSDR may have fulfilled their mission, but they may need to be sunset.

Eliminate: These are agencies whose purpose does not support a stand-alone focus but can be folded into other agencies for services. Indian Health Services or Health Resources and Services Administration (HRSA) must be folded into CMS, given that the beneficiaries could use Medicare or Medicaid.

Recommendation to DOGE: Eliminate agencies that can not quantify their impact on lowering healthcare costs or improving health outcomes.

The Bottom Line: Addressing the low-hanging fruit of US healthcare can yield immediate cost relief while improving health outcomes

It is unconscionable that the US spends ~20% of our GDP, the highest both in aggregate and as a percentage of GDP, yet delivers amongst the worst health outcomes (life expectancy, infant mortality, prevalence of chronic conditions, substance abuse). To blame is the healthcare ecosystem’s complexity (administration, cost of care, clinical expertise) in terms of costs and outcomes. It is due for another transformation but must be a private-public partnership. While that level of collaboration may take some doing, the low-hanging fruits of reducing admin processes, eliminating the delusions of VBC, and rationalizing DHHS can bring some relief.

In the late 19th century, the US didn’t have an income tax and relied purely on tariff revenues. Now, the fate of the global economy lies with one “big beautiful bill” of income tax cuts, which President Trump believes will stimulate an economic surge for the country. Economics and analysts are highly skeptical that this will work.

At HFS, we see the very foundations of the IT services industry being rattled to the core. We had anticipated a hike in Indian exports to the US of 20% at worst, but this is even higher at 26%. Those recession odds are rising significantly now, and so with it is spending on IT services.

Goldman Sachs had put a 30% expectation of an economic recession before President Trump’s “Liberation Day” announcement of tariffs, which are far more severe than expected. These expectations are now over 50% and there will be a rapid domino impact on the IT services industry by immediately slowing down enterprise decision-making and increasing immediate focus on cost controls.

Expect lower innovation and more focus on AI to protect productivity

This new wave of Trump-era tariffs is aimed at foreign goods, but people everywhere will feel the aftershocks as they will constrain trade and create imbalance at a rate not witnessed since COVID-19 wrought havoc on global markets and societies.

Businesses in the US are shielded by this steep tariff war, which lowers the incentive to compete and innovate when there is less intense competition from abroad, which is undermining the US’s position as the world’s most innovative economy. The focus of a lot of US business is going to be squarely on cost reduction, and this will have a direct impact on the global IT and BPO services industry. This will result in a double whammy hit for the India-dependent service providers and consultancies as US firms will be incentivized to reshore services work back to the US and also to invest more heavily in AI to reduce reliance on support staff in areas like application development and business services.

What began as a populist policy move has become an anti-globalization movement that threatens to reshape the fabric of society and upend enterprise priorities across products, people, and profits.

Consumers say: “I won’t buy—it’s too expensive.”

Tariffing China at an effective 54% will raise the prices of goods. In 2024, the US imported $462.6 Billion in goods from China. The proposed increase will make many Chinese goods extremely expensive for the average customer, thus cooling consumer demand rapidly. China isn’t alone. Large trading partners like India, Vietnam, and the EU have also been hit with numbers that will force retaliation and restructuring of producing goods away from the US consumer.

With tariffs being applied globally, the US consumer – the world’s largest buyer of goods – will be forced to curtail spending at a rate not seen since COVID hit the markets in 2020. While there won’t be long lines for toilet paper, the travel, tourism, retail, and hospitality markets can be expected to see double-digit drops by Summer.

As the threat of unemployment looms, the new jobs promised by these tariffs to Americans are likely to never materialize as the knock-on of a double-digit drop in consumer spending, financial concerns, and a decline in government programs (typically used as stimulus but now hobbled by DOGE and Trump’s executive orders) are likely to accelerate a recession.

IT services and advisory firms will need to act quickly to address these consumer impacts by getting into war room footing with companies to seek out where manufacturing and imports that are tariffed less can be moved. There will be no free trade zones. This won’t withstand the changing economics of this new world order, but it may allow savvy firms to help their customers shore up contracts and services needed to deliver goods as they lean out their operations.

Enterprises respond: “We need to cut costs—fast.”

As consumer and business demand declines and margins tighten, businesses are expected to turn to cost-cutting levers.

While the Trump administration heralds these tariffs will force companies to reevaluate supply chains, repatriate manufacturing, and rethink cost structures to stay competitive – building a new multi-billion dollar manufacturing industry that can’t afford the steel and other building resource imports needed (thanks to high tariffs on neighbors like Canada) will make it these promised national investments impractical.

The expected outcomes will be a significant drop in consumer spending, double-digit inflation, and a likely doubling of unemployment. Companies facing this type of market will quickly cut consulting costs and technology investment costs and lean out supply chains to few products and goods – focusing on durable goods at lower margins.

Services firms will need to shore up contracts and reevaluate their IT and operations quickly—often viewed as back-office or non-core—become the first to become collateral damage as trade wars escalate.

IT Services: Collateral Damage in the Trade War

IT services are a mix of labour and technology arbitrage and have been adapting to a new economy post-COVID with more remote work, more AI, and an increasing dependence on the cloud and real-time data. Where COVID forced product and business model innovation, a global trade war will be about circling the wagons, constraining costs, and slowing product innovation as consumers and other businesses will no longer be looking to buy these new products.

The blow to IT services is indirect—but decisive:

Digital nationalism intensifies: As political pressure to localize services gains ground, offshore delivery will face new skepticism. Despite not being directly tariffed, a view that a country’s workforce may benefit while US workers lose jobs won’t be popular. Expect companies to accelerate the use of data, automation, and AI to reduce any dependence on outsourced overseas jobs. GCCs may be heavily impacted.

Margin pressure escalates: US firms will demand more value at lower cost. Services firms will be expected to absorb pricing pressure while delivering faster, smarter, cheaper outcomes. However, the longer the trade war lasts, the significant risk of many companies cutting IT services or not renewing contracts will increase. Large IT contracts will be cut drastically without a need to develop new products or services in a recession and with buyers needing less support for new products.

Delivery shifts inward: The intent of tariffs is for US enterprises to undergo supply chain reengineering, onshore manufacturing, and create a closed-loop economy. However, the administration has created labor constraints that will make hiring workers, procuring materials to build new factories, and technology costs very expensive. Delivery will shift inward, but cost-cutting measures will be aggressive as many firms likely take a wait-and-see approach to how long these trade wars will continue.

Agentic AI becomes the burning platform: Technology investment has been the means to find a new S-curve of productivity and competitive edge. However, as experience-led transformations (EX, CX) are deferred, AI risks, governance, and cybersecurity investments are expected to rise to the top. Yet, while these technologies might soften the blow – their cost models and the lack many companies have had in scaling these don’t mean these technologies are a slam dunk for services firms to bet their futures on.

Delivery model realignment raises costs: As offshoring practices come under political and public scrutiny, firms will be forced to hire IT resources locally. This may require IT services firms to acquire U.S.-based firms or enter regional partnerships for increased nearshoring. But all these moves erode the economics of the global delivery model. And due to rising inflation will make any such investments very costly.

Bottom Line: The Trump administration has launched a series of tariffs on goods, triggering a chain reaction that will destabilize the global IT services industry and economies.

As firms are forced to determine how they’ll survey the impending economic uncertainty or decline, the IT services industry has no option but to double down on AI-led productivity gains and deep domain expertise to help clients weather the storm. The best case will be a harsh but brief storm, as we hope a sudden economic downturn can bounce back in late 2025. But this summer will likely be one of frozen spending, cost cutting, and restructuring.

IT services must get ahead of contracts and work with their customers to ease the burden of costs by offering terms that can adapt to the potential short and long-term scenarios. These may include:

Where possible, IT services firms can help by proactively taking on business support teams and technology areas at more aggressive rates, targeting a near-term cut in services costs (and their profitability) in hopes that the rebound will make them more indispensable in the future.

IT services firms will need to help companies refactor their ecosystems and make the procurement of goods from countries with better production costs than those being taxed the highest.

Help companies switch from innovation and growth models to responsible cost management and workforce realignment.

The IT industry transformed itself to survive COVID. It must now do so again—this time, to outlast the era of tariff wars.

Tariffs are back in fashion — again. Some politicians love them. Pundits love to debate them. They’re tough-sounding, crowd-pleasing, and give the impression that someone is finally standing up for American workers.

There’s just one problem: they don’t work — at least not the way we need them to.

Sure, tariffs sound great in campaign speeches. “Let’s tax foreign imports, bring factories home, and rebuild the middle class.” The rhetoric is nostalgic, nationalistic, and — unfortunately — economically naive. In my view, tariffs are a place where politics and economics just do not gel together, no matter how well-intentioned.

Let’s be clear. Tariffs aren’t inherently evil. In limited, strategic use, they can buy time for critical industries. But when wielded as a broad, blunt policy — as a primary economic lever — they just don’t deliver results. They create a cascade of consequences that hurt far more than they help. Sure, there can always be a few modifications here and a consensus agreement there, but when they are designed to choke the life out of a trading relationship and load costs onto the consumer, the ramifications rarely read to achieving lofty political goals.

Here’s what really happens when you build a wall around the economy instead of investing in its foundation:

1. Tariffs won’t fix the trade deficit

Yes, they reduce imports. But they also reduce exports, leaving the balance largely unchanged. Why? Because other countries retaliate, and a stronger dollar makes US goods even more expensive. You don’t “rebalance” trade by slowing everything down. That’s like fixing traffic by banning cars.

2. Manufacturing won’t come roaring back

We’re not living in 1955 anymore. US factories can’t just reopen and start making TVs and sneakers. Modern manufacturing is capital-intensive, automated, and globally distributed. Tariffs raise the cost of doing business — they don’t attract it.

3. US exports lose their edge

Tariffs also make it more expensive to produce goods in America. Pair that with a rising dollar, and you’ve priced yourself out of international markets. Suddenly, the “Made in the USA” label looks more like a premium surcharge than a selling point.

4. Consumers pick up the tab

Tariffs are a tax — and not on foreign producers. They are on you. Everything from groceries to electronics goes up in price. You may not notice it at first, but your wallet will. Inflation certainly doesn’t need much more help these days, but tariffs are happy to pitch in.

5. Other countries will punch back — and aim to hurt

Trade wars aren’t fistfights — they’re chess matches. And other nations will go after US exports where it hurts: agriculture, aerospace, microchips, tech, etc. Tariffs don’t just invite retaliation — they guarantee it.

6. Store shelves get thinner — and more expensive

Say goodbye to cheap imported goods and hello to smaller selections and bigger price tags. Some items vanish entirely. No, it’s not a supply chain apocalypse — it’s just tariffs doing what they do best: making things harder to get hold of… and costlier too.

7. Export-reliant jobs disappear

Industries like manufacturing, life sciences, technology, and agriculture rely on global markets. Tariffs reduce their access, kill demand, and shrink payrolls. We’re not just talking about a few jobs here and there. Entire regions could see economic fallout.

8. Supply chains start to crack

Modern business runs on global supply chain inputs. Tariffs disrupt the flow, raise the costs, and force companies to scramble for alternatives. Often, those alternatives are slower, more expensive, less efficient and production plummets. Sometimes, companies just pack up and go elsewhere because they can’t function competitively anymore.

9. The economy slows — or worse

Put it all together: higher costs, weaker exports, lost jobs, reduced investment. That’s not “taking back control.” That’s how you drag your economy into a slowdown — or kick off a recession if you’re really ambitious. Recessions aren’t caused by singular shocks — they come from dominoes falling in sequence. Tariffs could tip the first one.

10. AI gets weaponized, not optimized

Rather than embracing AI to augment human capabilities, enterprises will use it as a weapon to remove workers and replace them with technology. AI will become a smokescreen to downside organizations, not improve them.

11. Even if factories come back, workers won’t

Let’s assume — generously — that tariffs succeed in nudging companies to bring some manufacturing home. There’s still a problem: we don’t have the workforce. Skilled labor in the US is in short supply. We’ve spent decades underinvesting in vocational training and tech education. You can build the factory, but who’s going to run it? Maybe start investing in building the workforce of the future before living in the past?

The Real Problem Isn’t Imports. It’s Incentives. More carrot and less stick, please…

The US doesn’t need more barriers — it needs better magnets. If we want to rebuild our industrial base, we need to make America the best place to invest, build, and hire.

That means:

Modernizing infrastructure so supply chains can run efficiently

Incentivizing domestic production with smart tax policy, not tariffs

Training a skilled workforce through serious investment in vocational and technical education

Stabilizing regulatory and trade policy so companies can plan for more than 18 months at a time

Supporting R&D and automation that drives innovation, not job loss

In short, the US needs a carrot, not a stick. You don’t grow a competitive economy by punishing everyone who isn’t domestic. You grow it by building the kind of environment where global businesses want to stay, invest, and scale.

Bottom Line: Tariffs don’t make things — they break things

They disrupt supply chains, confidence, and growth. While they may win applause at rallies, they lose traction in the real economy.

If the US wants to lead the next industrial revolution, we need to stop weaponizing policy and start investing in capability. We must compete smarter, build stronger, and attract better talent.

Tariffs are a headline. Strategy is what comes after.