Have you taken a step back to reflect on the impact of social media, AI, and the pandemic on today’s employee mindset? A work environment where isolation, loneliness, and self-entitlement have become the norm… an environment that is losing its connectedness and is becoming increasingly dehumanized.

What’s it like being in a “ME” work culture?

We live in a world that’s all about ME. We want to be loved, appreciated, adulated, respected, and credited for literally everything we do.

We want to earn lots of money, work when we want to, do what we want to, and not have a boss watching over our shoulders every day. We want ME in charge.

We want to have an opinion on pretty much everything and choose where we get our knowledge. ME has an opinion, and that’s all that matters.

We need these constant little endorphin hits when someone gives us attention, whether it’s a social media post or a call out at work. It’s all about ME… and as much as possible!

We communicate most of our time over text and talk to people less and less because we hide in our little ME cocoons. Talking to people requires effort and our full attention, and it’s not all about ME.

We have become super-sensitive to criticism. The slightest accusation or hint of negativity toward us makes us get very defensive. How dare you accuse me of not being perfect!

We repeatedly tell people all the amazing things we do so we can constantly get credit. Why wait for praise when we can just praise ME?

We invest our time in people who can advance our ME agendas.

We avoid people who have little to offer ME.

We spend less social time with our colleagues because team bonding is not very important to ME.

We spend time learning new things that interest ME, not things we need to learn about to further our work skills and knowledge.

We rarely work evenings or weekends anymore. ME doesn’t need to go over and above unless it benefits ME.

We “like” things on social media to further our ME network and never bother to read the articles. The authors should be genuinely grateful for our endorsements because they are from ME.

It’s really all just about ME, ME, ME!

“ME” is the world we live in, but we need to focus more on “US” to improve work culture

Can you really blame employees for feeling dehumanized when their bosses keep pontificating about bots and agents replacing and augmenting their work activities? Can you blame them for feeling lonely and isolated at home, performing mundane activities with little outlet to enjoy themselves? Can you blame them for needing recognition and appreciation for being human in an environment where there is so much focus on meeting metrics, reducing costs, and sucking the very humanity out of the workplace with constant technology upgrades and new deployments?

People don’t suddenly decide to become selfish. This is a product of these dehumanizing dynamics in the work environment, which results in people crying out for affirmation and a sense of connectedness that is missing from our work lives.

Bottom-line: We must reverse this culture, but it will take a lot of refocusing

I would love to provide a definitive guide to employers and employees on how to make our work environments more connected, but this is a blog, not a detailed guide to HR, so I’ll leave you with three simple activities to get back on the right track:

Let’s get to know each other better. Get off the Team, Zoom, Slack, whatever text system we use for company communication and call each other up. Get to know each other as HUMANS again and not as mere work colleagues who provide a means to an end. We don’t even need to like each other but just behaving like humans and not text-generating cyborgs is a huge step to improving our connectedness and work culture.

Focus on work as a positive, not a negative experience. It’s so easy to be negative; we all go there, and it’s not a great place to be. When you feel negativity coming knocking, take a step away and rethink why you are feeling this way. Staring at a screen 10 hours a day is just bad for your brain, your eyes, and your health and saps your energy and enthusiasm. So take more breaks in the day, go for a walk, hit the gym, or just call someone up to talk.

Spend less time on social media. I am not the patron saint of this, but so many people are wasting an inordinate amount of time seeking their little endorphin hits and not getting any actual real value from this. Unless you have something profound to share with the world, why spend half your day just trawling through digital junk when you can spend more time improving your own work or client relationships just by talking to them? Social media can be a great thing for developing your network etc., but there is a line between some networking and just wasting hours a day on this mind-numbing activity.

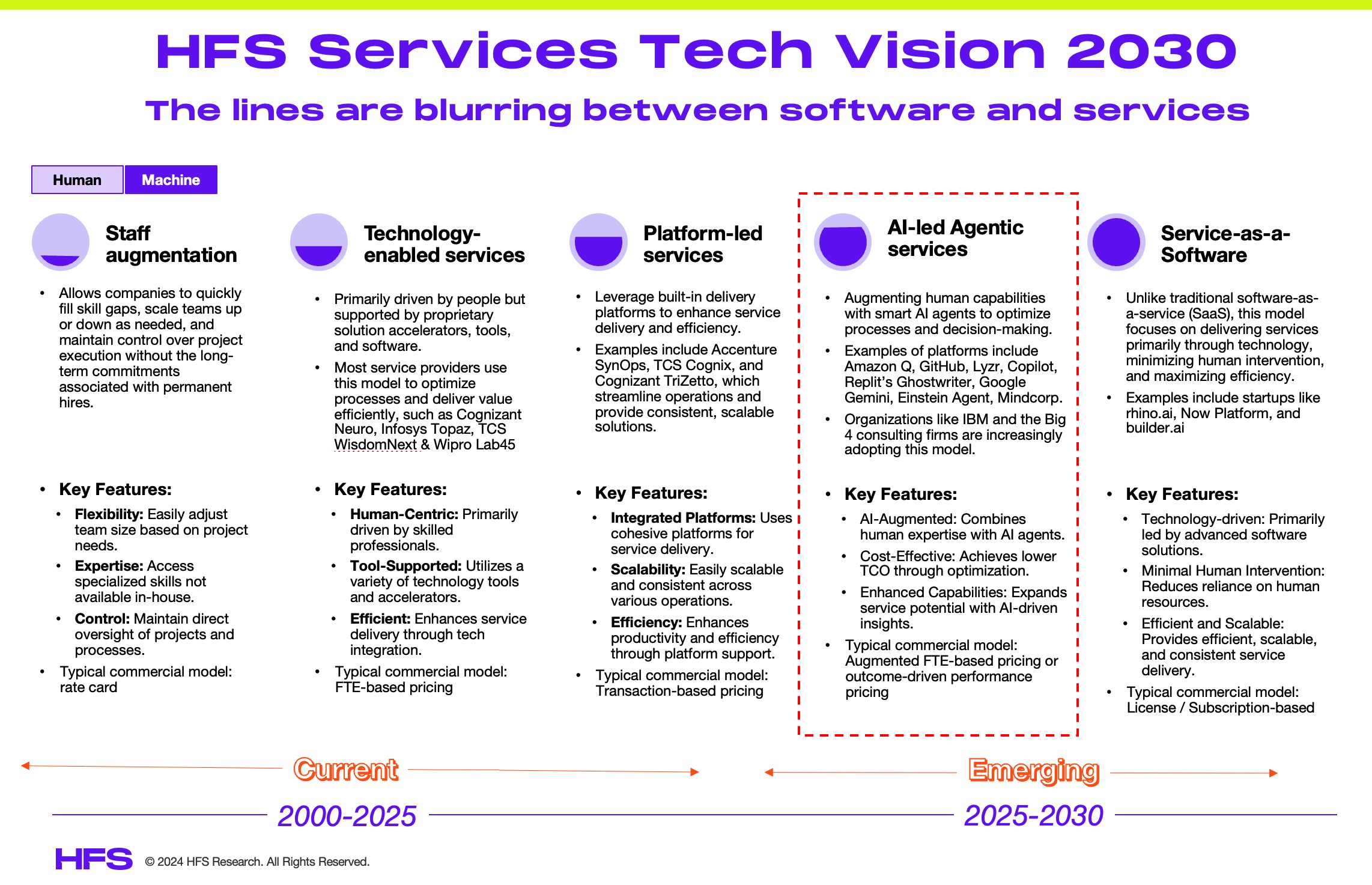

Two very different worlds, one based on humans and the other on technology, are becoming one blended, scalable solution we are calling Services-as-Software. In short, the line between services and software is blurring and eventually vanishing, and this progression has become more crucial than ever.

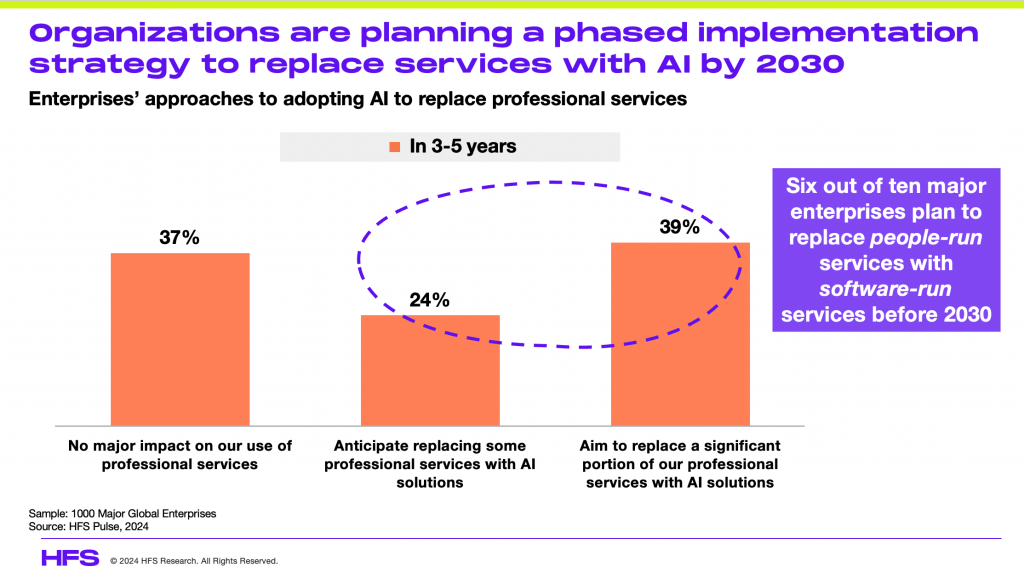

Sixty percent of enterprises are already looking to procure services as technology offerings

A recent HFS study of 1000 major global enterprises reveals what is happening with stark brutality: Six out of ten enterprise leaders plan to replace some or all of their professional services with some form of AI within the next 3-5 years.

Services will continue to reduce their reliance on labor as automation creates more efficiency and productivity

The reality is that most people-based services, once they become predictable and routine, eventually become automated. This increasing sophistication of AI tools is enhancing the whole service efficiency and personalization experience. Once implemented effectively, these Services-as-Software solutions become faster to manage, cheaper to maintain, and more scalable to cope with volumes of demand.

For example, fully automated passport gates at airports now allow for higher volumes of passengers to clear immigration much quicker than previously and for more airlines to land their planes at the airport. This leads to more profitability for the airport, more business for the airlines and people to enter the country more expediently. Similarly, self-checkouts at grocery and convenience stores are enabling many more customers to have their purchases processed simultaneously, securely, and faster, which creates the ability to handle volume spikes without layering on unnecessary staffing costs to cater to demand.

Software-driven services can also improve the customer and employee experience

Now the airport can redeploy its people to manage issues at the passport gate when needed, to help shepherd them into the right lines, and also to provide assistance to elderly or disabled people. The whole experience is improved. Similarly, the convenience store can redeploy its staff to help customers find the products they need, to ensure inventory is better managed, to help manage in-store promotions, and to ensure the store is kept clean and presentable. Again, the customer and employee experience should be vastly improved, and the automation of the rote work allows more focus on improving the speed and quality of the whole business proposition.

While fairly simplistic, these are current real-world examples of how software embedded in enabled machines can not only replace the dependence on people to meet outcomes, but also enable organizations to scale their services without adding linear cost. The only differences with the emerging Services-as-Software model are the improvements in botifying routine white-collar work that was previously too challenging to automate due to limited technologies such as RPA and the absence of our ability to mimic and predict human behavior with the increasing sophistication of GenAI and Agentic software.

Services and software are equally exposed to full automation and AI

Enter the world of IT and business process services, and similar trends are in play as routine IT maintenance, HR, procurement, accounting, and customer service work are becoming much easier to replicate in advancing GenAI and Agentic software, supported by public and private cloud capabilities to secure and scale transaction volumes.

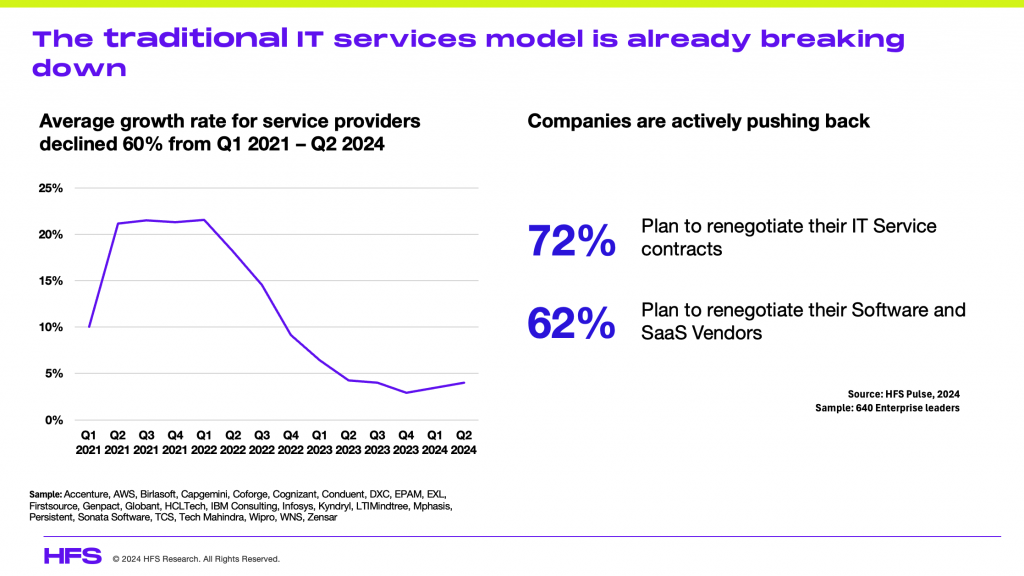

You only need to observe the rapid decline of growth in the labor-intensive services sector and the determination of enterprise customers to renegotiate both their services and software contracts to understand this dynamic is now in full swing:

Organizations face mounting pressure to deliver results faster, at scale, and with limited resources—all while managing increasingly complex technology ecosystems. The convergence of services and software meets that demand by transforming traditional consulting and outsourcing into scalable, automated solutions.

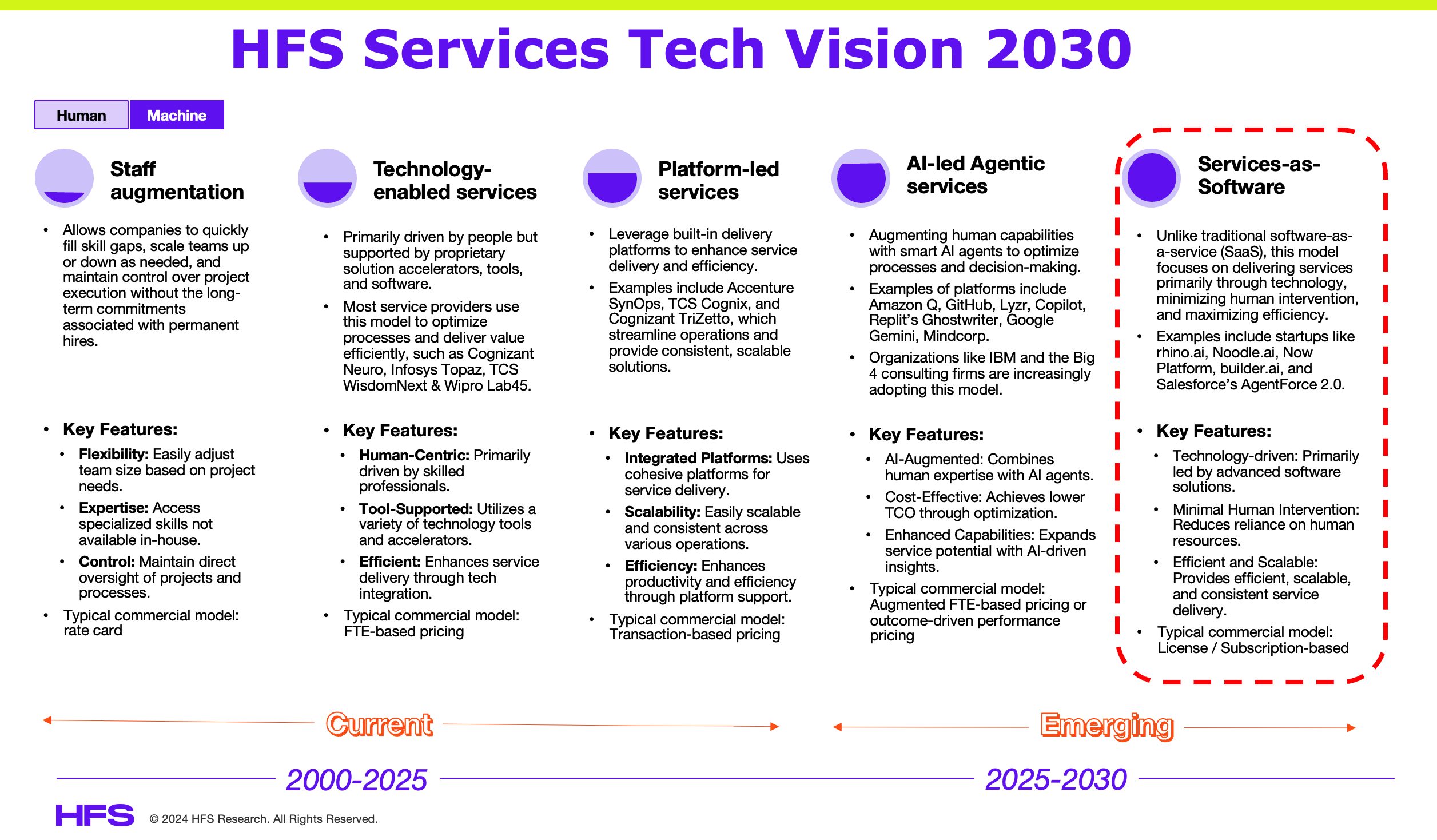

The 2030 destination is Services-as-Software, where the focus is on service provision performed by AI, not people

With the application of software platforms, Agentic solutions, and, ultimately, autonomous services mimicked by software, we believe we are on a fast track to reach an autonomous, human-lite nirvana of scalable, profitable, and affordable services by 2030:

These five phases of services tell the complete story of the industry’s evolution from adding people to perform work to scaling these same people with the smart use of platforms, AI-driven Agentic tools, and ultimately fully autonomous technology-led services where work is effectively replicated at scale with embedded intelligence.

In short, we are getting more of the same work without having to spend more on that same work. Instead, we can invest that money in value-added areas that cannot be mimicked by AI. Enterprises must adapt quickly to this shift as Agentic AI can autonomously handle complex decision-making tasks. This will impact both workforce roles and the enterprise software landscape, reducing the need for repetitive, decision-heavy positions and consolidating software functions under AI-driven platforms.

How the lines between services and software are blurring

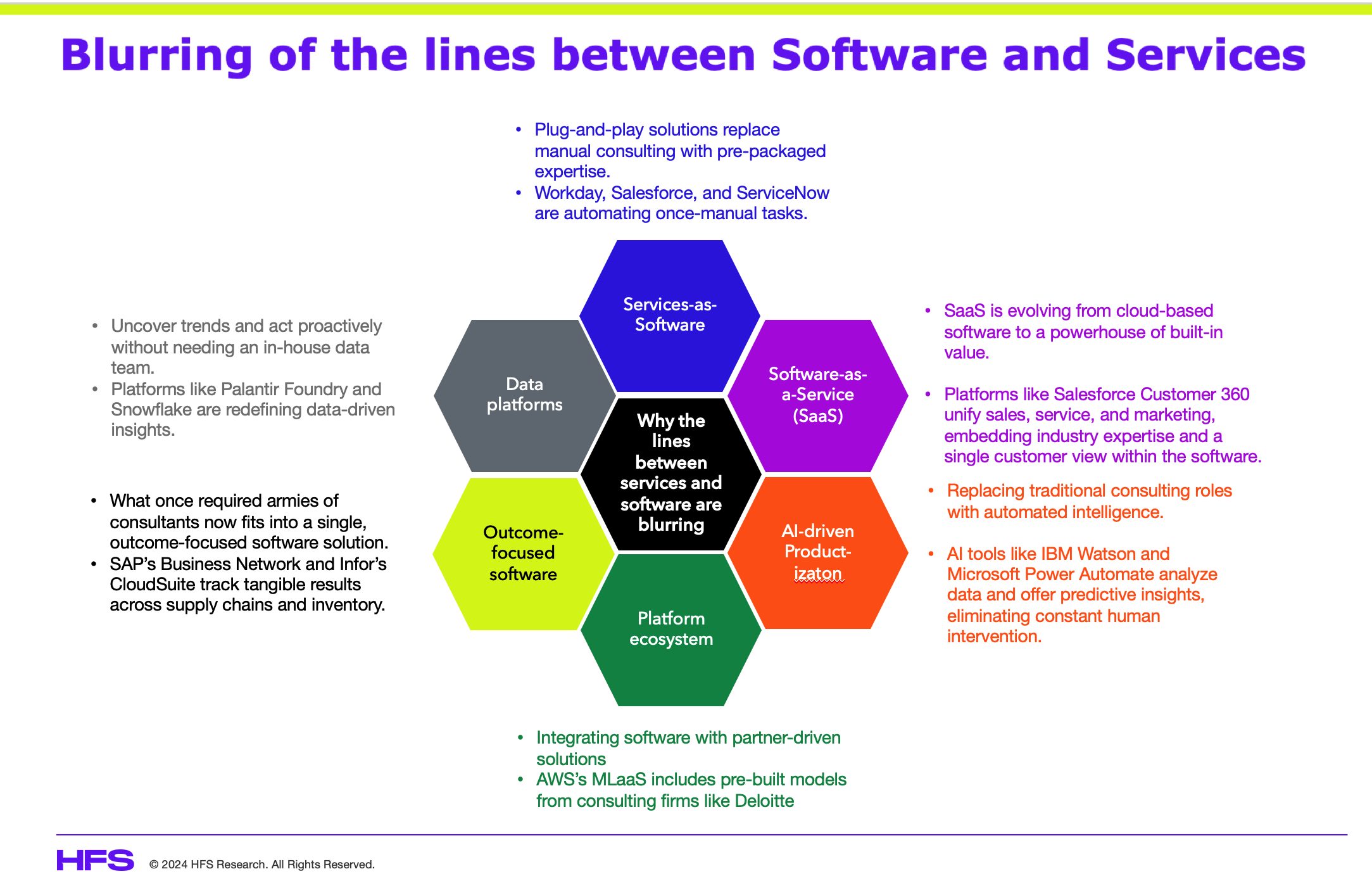

This new model (see exhibit below) allows businesses to access continuous insights, predictive analytics, and outcome-driven solutions that adapt in real-time. It’s not just about streamlining operations; it’s about fueling growth and resilience, accelerating companies ahead in a world where speed and adaptability are critical to success. Let’s explore how this is already happening at speed:

Services-as-Software (SaaS 2.0): Providers like Workday and ServiceNow are shifting from traditional consulting models to plug-and-play solutions that automate once-manual tasks. Workday’s People Analytics and ServiceNow’s ITSM are prime examples—what once required hours of consulting is now pre-packaged expertise delivering instant results.

SaaS as the New Backbone: SaaS is evolving from cloud-based software to a powerhouse of built-in value. Platforms like Salesforce’s Customer 360 bundle sales, service, and marketing insights into one, reducing the need for external CRM optimization by embedding industry-specific expertise and a single customer view across the lifecycle right within the software.

AI-Driven Productization: AI tools like IBM Watson and Microsoft Power Automate are replacing traditional consulting roles with automated intelligence. IBM Watson isn’t just a chatbot but a full-scale AI ecosystem that analyzes data and offers predictive insights, eliminating constant human intervention.

Platform Playgrounds: Ecosystems like AWS and Google Cloud go beyond tech infrastructure by integrating software and partner-driven solutions. AWS’s MLaaS, for instance, includes pre-built models from consulting firms like Deloitte, allowing its enterprise clients to tap into sophisticated AI solutions without custom builds. KPMG has invested significantly in the GenAI platform Rhino.ai to modernize legacy applications, while, and IBM has been developing out its watsonx platforms to replicate many routine business services in a one-to-many scalable delivery model.

Outcome Obsession: Companies like SAP and Infor focus on outcome-driven solutions, with SAP’s Business Network and Infor’s CloudSuite tracking tangible results across supply chains and inventory. What once required armies of consultants now fits into a single, outcome-focused software solution.

Data as a Weapon: Platforms like Palantir Foundry and Snowflake are redefining data-driven insights. Palantir Foundry continuously analyzes business data for actionable intelligence, while Snowflake’s Data Cloud empowers companies to uncover trends and act proactively without needing an in-house data team.

The Bottom-line: In this new service-as-software era, the distinction between service and software is practically erasing.

Businesses now access pre-built solutions, automated workflows, and data-powered insights, creating a seamless and scalable experience that puts the power of technology and expertise directly at their fingertips. Services firms will increasingly look to their software partners and investments to streamline and provide greater value to entrprise clients, as this GenAI ecosystem unfolds. This model doesn’t just support business goals—it accelerates them, transforming how companies achieve impact in a world where speed and adaptability are the ultimate competitive advantage.

The challenge we all face – whether we buy, sell, advise or analyze this merging of markets is changing how we articulate, commercialize and deliver outcomes. Services and software people come from different worlds and speak different languages, but now these need to come together in a way we can all understand and develop. We can’t simply buy shiny new S-a-S solutions and plug them in like we did with an ERP solution. This is where we need to define real business value, which can be delivered by AI technology and price according to that value and the desired outcomes we expect. There is a huge opportunity for service providers to guide their clients to a state where they are ready for S-a-S solutions. There is also the potential for services and software firms to merge together as this new market emerges – there are already multiple discussions and partnerships taking place that are readying for 2025 and beyond.

Welcome to the era of uncertain change, everyone… where uncertainty will breed opportunity!

Salesforce’s AgentForce 2.0 signals a new era of digital labor, redefining how enterprises manage productivity, outsourcing, and internal workforce models. By integrating AI-driven Digital Workforce Equivalents (DWEs) into its platform, Salesforce positions itself as a cornerstone of the agentic AI revolution, challenging traditional IT and outsourcing paradigms. We believe this release signals a clear path toward the services industry’s shift toward Services-as-Software:

Digital Workers at Scale: What’s New in AgentForce 2.0?

The AgentForce 2.0 release promises:

An End-to-End, “Skilled” Digital Workforce: Simplified agent creation using the Agent Builder that automatically generates “digital workers” from natural language descriptions, allowing businesses to scale their digital workforce with minimal technical expertise. This includes MuleSoft’s connections to 40+ platforms like AWS, SAP, Workday, Adobe, and Oracle, streamlining data and task orchestration across ecosystems. Enterprises can add “skills” to the digital workforce, which are pre-built or customizable capabilities, allowing for easy deployment of agents for common sales, HR, customer service, IT, and industry-specific actions with minimal configuration.

Digital Workforce Deployment to Slack: Agents can operate directly in Slack, enabling enterprise-wide search, workflow execution, and contextual task management. Collaboration and communication are reimagined as agents seamlessly interact with human teams in channels and DMs. This is a direct attack on Microsoft 365’s CoPilot capability but it also creates a built-in ecosystem expanding the promise of Slack’s collaboration capabilities with an expanding digital workforce.

Enhanced Atlas Reasoning Engine: Atlas upgrades by differentiating between faster simple queries and slower complex reasoning. Improvements in metadata chunking, query reformulation, and future inline citations will improve the quality of the digital workforce’s responses and ensure transparency and trust. Atlas includes enhanced governance and security through improved policies, as governance ensures compliance, secure data access, and trustworthy operations.

Outsourcing in Crisis: DWEs Reshape Enterprise Labor Models

DWEs Can Replace FTEs: As HFS has already forecasted, Services as Software is the future of the service industry. Salesforce’s new capabilities provide for a more capable agentic AI solution to replace outsourced and in-house FTEs with a digital workforce. If workers are not completely replaced, fractional DWES will soon reduce manual workloads and support the remaining FTEs. Net result: fewer FTEs on payrolls, and more DWEs on Salesforce’s invoices.

The New Default for AI and Automation: Agentforce 2.0 positions Salesforce as a go-to platform for scaling AI across enterprises. By consolidating AI tools into one existing solution, Salesforce reduces the complexity of managing multiple service providers. Traditional development and outsourcing firms specializing in repetitive business processes, ITSM, and application maintenance will face declining demand as enterprises turn to digital labor – Marc Benioff, Salesforce’s Founder, and CEO, has pledged not to hire new development staff but instead rely on its Salesforce capabilities.

Salesforce Becomes a Vital New Ecosystem Provider: IT services already have relationships with Salesforce, and those will become more important. However, business process outsourcing vendors, especially call centers, sales teams, order entry teams, and digital marketing teams, will need to build formal partnership relationships with Salesforce to enhance their Salesforce offerings instead of building their own solutions that have a fraction of the R&D funding that Salesforce is pumping into their solution.

Salesforce Challenges Tech Giants with Integrated AI Workforce

The AgentForce 2.0 release challenges existing norms in the technology sector, creating ripple effects across software vendors, service providers, and IT ecosystems.

A Redefinition of Enterprise Platforms: Salesforce is no longer just a CRM enterprise SaaS provider—it is positioning itself as an operating system for the digital workforce. This shift forces other vendors, including AWS, Microsoft, and Google Cloud, to rethink their strategies. For example, SAP’s Joule, while included in some of its cloud offerings, is not included in its customers’ proprietary SAP HANA S/4 environments, requiring custom installation for all of its clients. If a client has Salesforce and SAP, Salesforce may be the more capable and easier implementation, relegating SAP to being a system of truth but not processing.

Platform Stickiness: By deeply embedding AgentForce 2.0 in the Salesforce ecosystem, the company strengthens customer loyalty and makes it harder for enterprises to switch to other platforms.

Shift Toward Unified Platforms: Salesforce’s ability to integrate its ecosystem (Customer 360, Data Cloud, MuleSoft, Tableau, Slack) into a single, cohesive solution sets a new standard for enterprise platforms. Competing providers with fragmented specialty tools must offer deeper integrations and more comprehensive solutions.

Pre-Built Capabilities Reduce Time to Value: With a GenAI-driven Agentbuilder and a growing list of pre-built skills, enterprises can implement AgentForce without the need for extensive coding or consulting services. While the implementation does mean new revenue sources, the ease of implementation requires fewer billable hours. It is imperative that Salesforce “global system integrators” build accelerators that Salesforce currently does not have, like industry-specific action, legacy system actions leveraging MuleSoft, and Data Cloud integrations.

Why AgentForce 2.0 Still Faces Major Hurdles

Everyone is a Microsoft Client, but Not Everyone Uses Salesforce: Salesforce has faced heavy pressure from CRM ecosystem competitors. This foray into providing enterprise-wide agentic AI drives into the heart of Microsoft, Google Cloud, and AWS’s strategies, as nearly every company has one, if not more than one, of these solutions. The hyperscalers, while leaders in cloud services and AI models, rely heavily on enterprises to build their own solutions. Salesforce’s pre-built, low-code approach drastically lowers the barrier to entry for companies, presenting a direct competitive threat – and will not go unanswered, either through direct response or through SAP and Oracle ecosystems.

Cost Model Evolution: With pricing at $2 per conversation (list price), Salesforce makes AI-driven digital labor accessible. However, questions remain about how costs will scale as usage increases across autonomous, non-conversational use cases (back office agents). Furthermore, calculating the number of transactions per DWE requires significant business governance investment.

Ecosystem Lock-In: Of course, with unparalleled convenience and integration, enterprises that adopt AgentForce heavily will become deeply entrenched in its ecosystem, raising switching costs over time. Salesforce customers are quite vocal about their escalating licensing costs.

Industry-Specific Solutions Still Lag: Salesforce still remains a largely generic set of horizontal solutions with limited industry-specific “skills.” Salesforce must continue to develop in-house capabilities to suit the needs of healthcare, insurance, banking, pharma, and many other industries, or they must develop an ecosystem of “plugins” that bring industry-specific understanding to Agentforce 2.0. In the meantime, this becomes an excellent place for service providers to invest, as they have the industry acumen Salesforce lacks.

The Bottom Line: Agentforce is Accelerating the Future of Services-as-Software

As Salesforce brings AI-driven digital workers to market, enterprises must evaluate their workforce models and outsourcing strategies. Leaders should assess how DWEs can augment their operations, drive productivity, and reduce costs—or risk being left behind in the digital labor force revolution. Furthermore, AgentForce 2.0 is not just about scaling digital labor; it’s about reshaping the technology landscape. Salesforce is positioning itself as the backbone of the AI-driven enterprise, combining ease of use, deep integration, and scalability to drive adoption – a landscape long held by hyperscalers and ERP providers. Regardless of where you sit in the ecosystem, the enterprises and the entire services industry has been served notice: service as software is coming faster than most predict. . AgentForce 2.0 is a blueprint for the future of services as software —and Salesforce is leading the charge.

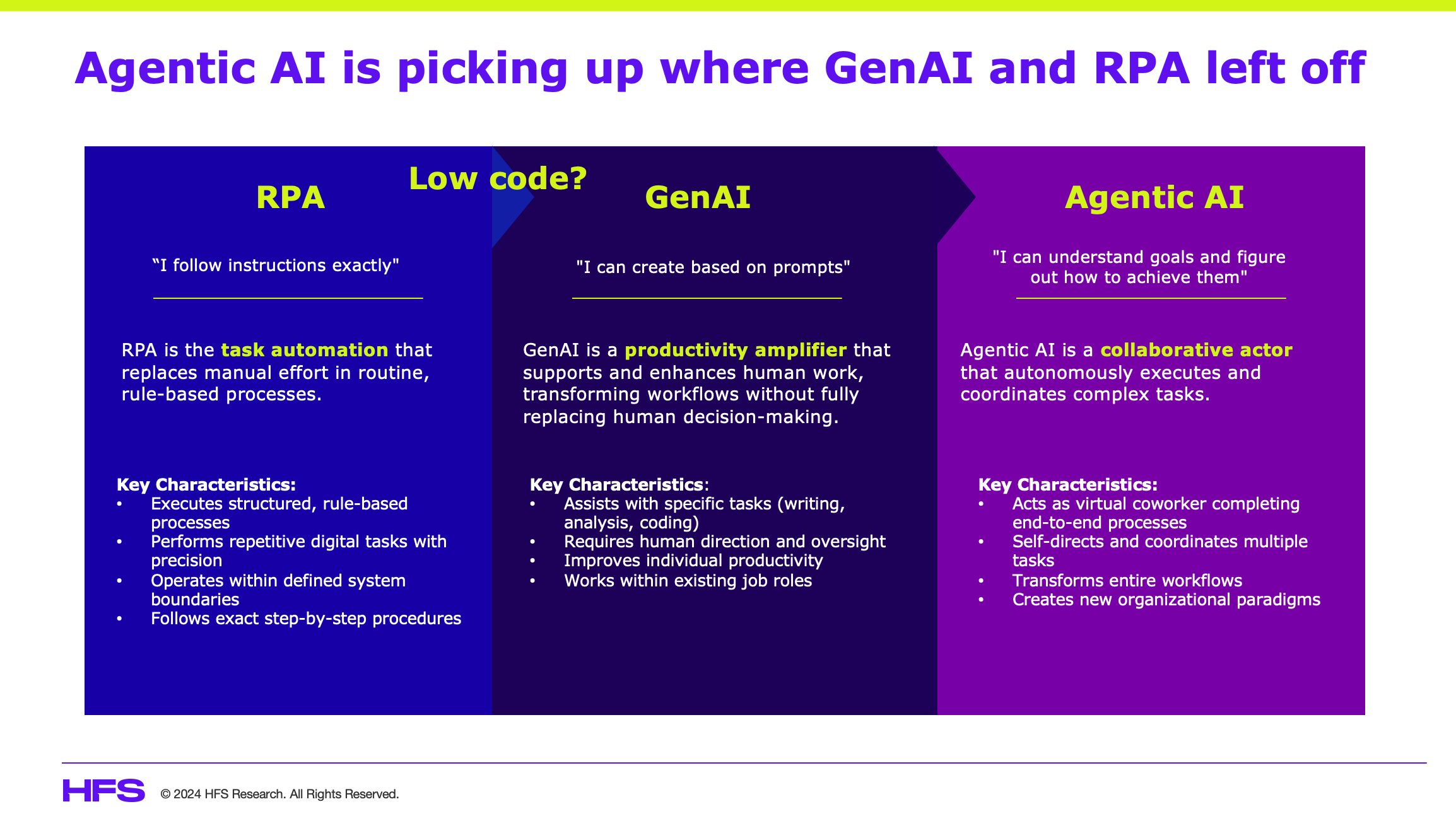

This early wave of RPA firms targeted repetitive low-risk jobs in areas where large amounts of human effort could be replaced with script-driven process recorders, screen scraping, and document scanning. Marketing slogans such as “automating the enterprise” and “a bot for every employee” fueled feverish excitement among many operations executives eager to have automation expertise on their CVs. The whole concept of mimicking human tasks with software bots had been born.

RPA failed, but the concept of a Post-Human organization was conceived

Rather than exciting smart enterprise leaders that they could refocus their talent on more creative, value-add, human-centric, and non-automatable activities, many quickly leaped at the prospect of slashing headcount costs either within their own companies or replacing the costs of their contracted outsourced labor with much cheaper software licenses. Nothing excites cost-cutting CFOs and Wall Street investors more than software that drives immediate productivity improvements via workforce reduction, and many people got very wealthy off the hype.

The problem with RPA was that without enterprise executives actually addressing their processes and data, you can’t simply lob work into software scripts when the software itself was brittle and very hard to scale, not to mention the security and compliance risks that needed addressing. The other big problem with RPA was that it was focused on mundane, low-value work, and the only real incentive to deploy it was if there were enough easy cost savings on offer. The actual deployment of RPA was not sexy or exciting, and it quickly got dropped on lower-level processes and IT staff to fix, which is where most overhyped software solutions go to die.

We’ve evolved from task-centric bots to dynamic agents that perform tasks on behalf of your workers

Fast forward to today’s world, and we suddenly have software that can impressively mimic not only human work but also human faces, voices, and expressions. Not only that, Agentic AI advancements are already proven to replicate human tasks, activities, and behaviors into real value-added work such as marketing functions, customer and employee experiences, supply chain operations, and sales processes. Agents are suddenly offering value far, far beyond mundane back-office efficiency… they are promising an injection of fake humanity into your enterprise.

Enterprise leaders are rushing headlong into a new era where AI doesn’t just assist—it acts.

The meteoric rise of Agentic AI is fundamentally reshaping workplace dynamics as these systems evolve from basic automation tools into autonomous digital workers that can execute complex tasks, make decisions, and even mimic human collaboration patterns. In short, after all the noise about bots replacing workers in the workplace over the past decade-plus, we now have technology that is still being positioned by many tech vendors to do just that.

Your agentic strategy will fail if you de-humanize your work culture

This evolution poses a double-edged challenge for enterprise leaders. While Agentic AI promises to unlock massive productivity gains and operational efficiencies, it also threatens to erode the human elements that drive innovation and organizational resilience. Meanwhile, employees face growing pressures to compete with tireless digital counterparts and productivity-obsessed work environments, further straining workplace culture.

The stakes are clear: without a thoughtful balance, organizations risk creating a “post-human” workplace—where efficiency wins, but humanity is lost. Moreover, in order to create effective agentic workflows, you need to encourage your workforce to create them for you with a positive mindset, not one where they are in fear of their jobs. Simply put, you are asking your people to trust you to replicate their day-to-day work functions into software programs and engage with those programs while expanding their own activities and capabilities. This will likely be the most challenging exercise in change management many workplaces have experienced, especially when you consider that close to half of workers are resistant or worried about the impact AI is having on their jobs:

At the heart of modern AI development lies a relentless pursuit to replicate and eventually surpass human intelligence

The enterprise technology market is charging full speed toward a controversial goal: creating machines that not only match human intelligence but render it obsolete. This isn’t just about better algorithms or smarter chatbots. From IBM Watson to today’s GPT models, every breakthrough in AI development has been driven by our relentless pursuit to recreate and then surpass human cognitive capabilities digitally.

We’ve always had a peculiar habit of humanizing our tools—from ancient myths to Alexa’s friendly voice. But today’s push toward Artificial General Intelligence (AGI) — and potentially ASI — represents something far more ambitious. These aren’t just tools; they’re attempts to build digital beings that can outthink, outwork, and outperform their creators across every cognitive domain.

This obsession with creating human digital intelligence reveals an uncomfortable truth about the enterprise AI market: we’re not just building better tools—we’re trying to rebuild ourselves.

Silicon Valley wants you to believe your next teammate is a software agent

The latest wave of Agentic AI vendors has perfected the art of anthropomorphic marketing, transforming what should be straightforward automation tools into “digital employees,” complete with names, personalities, and backstories.

Take startups like Artisan, Newo.ai, Knovva.ai, 11x, and Roots Automation, which don’t just offer automation but pitch “Elijah in customer support” or “Helen, the HR Rep.” Even tech giants like Microsoft are following suit, introducing AI agents with specific job titles like “Facilitator” for meeting management and “Project Manager” for task execution. These aren’t faceless algorithms—they’re marketed as perpetual team members, creating the illusion of a collaborative peer.

This humanization appeals to buyers and users alike. AI framed as a “coworker” is easier to justify in budgets, align with workflows, and trust decision-making. For example, an AI agent with a friendly voice or personalized responses creates a sense of collaboration.

The anthropomorphic framing also makes it easier for managers to justify budgets and evaluate performance, aligning AI agents with familiar job functions. In some cases, this can be used to make the replacement of traditional roles and functions more palatable to a workforce that may otherwise fear this technology. Given that 45% of employees (see above) are either concerned about job loss or resistant to GenAI, it makes sense to make these bots more human-like (See above).

As bots are humanized, human workers face growing pressures to compete with their tireless, hyper-efficient digital counterparts

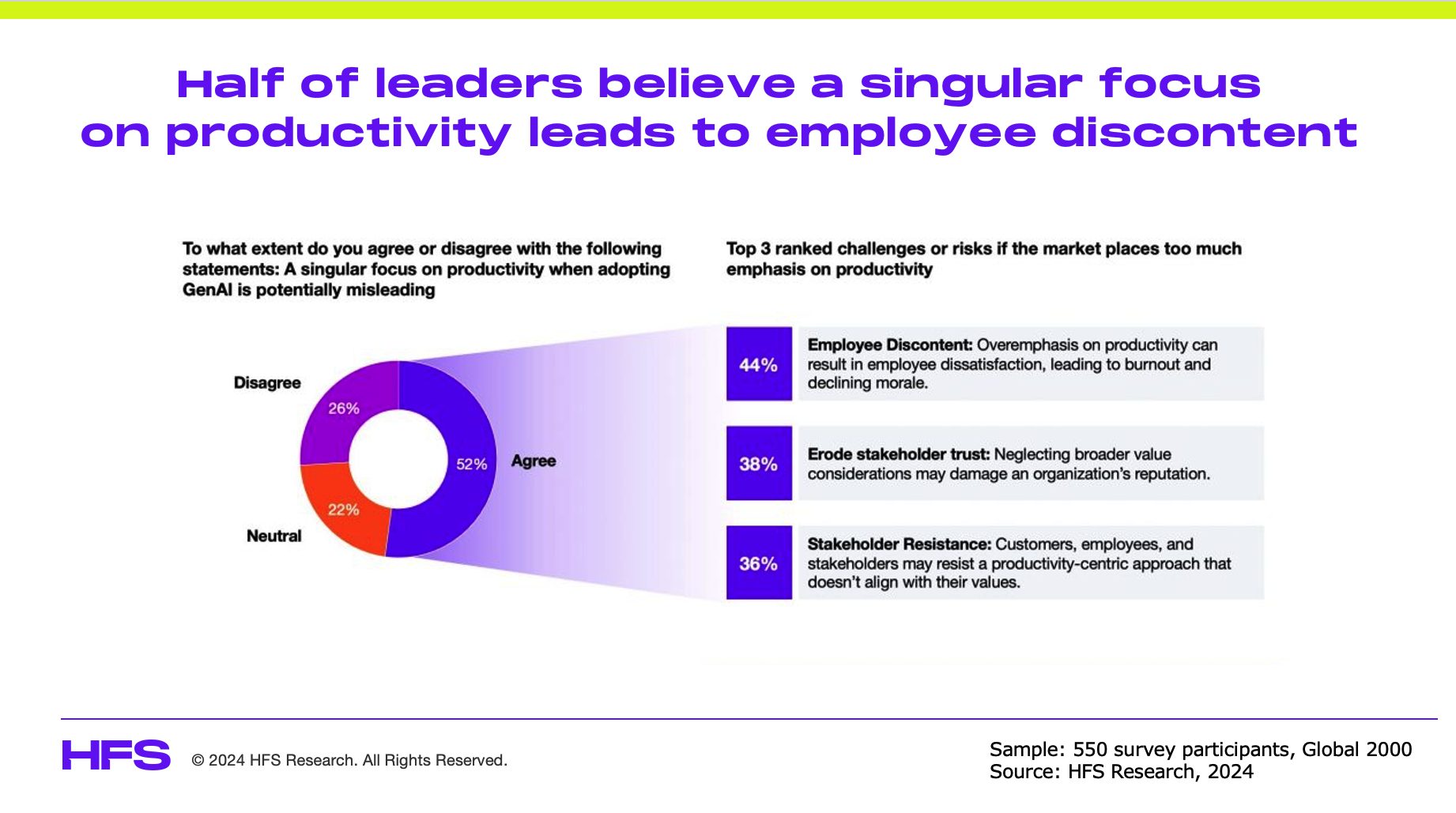

The rise of Agentic AI coincides with an enterprise-wide obsession with productivity, where every role is scrutinized for its efficiency. This shift is exacerbated by a workplace obsessed with productivity gains through AI. An HFS study found that the top driver of GenAI adoption was productivity, yet 52% of leaders also admitted that a singular focus on productivity could erode employee morale and trust.

Startups like Artisan are capitalizing on this moment with increasingly brazen messaging. Their “Stop Hiring Humans” billboard campaign in San Francisco perfectly captures this stark shift – openly suggesting that digital workers are preferable to human employees. It’s no longer about augmenting human capabilities; it’s about replacement (See Exhibit 3).

Artisan’s anti-human marketing campaign

The result is a workplace that will steadily transform into a transactional environment, where qualities like empathy, creativity, and collaboration—already strained in the post-pandemic world—are sidelined in favor of output and efficiency.

Employees may now face twofold challenges: the psychological burden of competing with machines and the cultural devaluation of human-centric skills.

The profit problem with post-human enterprises

Companies rushing to replace human functions with AI are missing a crucial point: the path to sustained profitability requires human insight, not just computational efficiency. Here’s why:

Market blindness: When enterprises lose touch with human experiences, they lose their ability to understand and predict market behavior. AI can crunch numbers all day but can’t grasp why customers buy your products. Strip out human insight, and you’ll miss every cultural shift and emotional driver that affects purchasing.

Innovation dies. Companies that over-automate find themselves stuck in optimization loops, perfecting existing processes while missing breakthrough innovations that come from human creativity and real-world experience. Tesla’s early automation failures in Model 3 production serve as a stark reminder—over-automation led to production delays and increased costs, forcing a return to human-centered manufacturing.

Commodification: While AI can handle transactions efficiently, businesses are learning that customer loyalty and premium pricing power come from emotional connections that only humans can forge.

Overreliance on AI creates dangerous uniformity across business processes and decision-making. When every competitor uses similar AI systems trained on similar data, they risk converging on identical solutions, creating a “race to the bottom” where price becomes the only differentiator.

Organizations must recalibrate their approach to navigating this complex landscape, recognizing that human qualities like empathy and creativity are not inefficiencies but essential drivers of success. Without this balance, the promise of Agentic AI may come at the cost of a disconnected and disillusioned workforce.

Recommendations for human-centric AI integration

Organizations must rethink their approach to AI integration to mitigate the risks of a “post-human” workplace. The solution lies in reframing AI as a tool rather than a counterpart while fostering a human-centric workplace culture that prioritizes collaboration, creativity, and well-being over metrics alone.

Reframe bots as tools: Maintain clear boundaries between AI and human roles. Anthropomorphized AI can enable productivity, but its purpose should remain as an enabler, not a substitute for authentic human connection.

Prioritize human-centric metrics: Balance productivity with engagement, creativity, and collaboration to create a workplace that values human contributions alongside AI capabilities.

Ethical deployment: Go beyond compliance with regulations like GDPR to address humanized bots’ societal and psychological impacts, ensuring transparency and fairness in AI use.

Foster engagement and trust: Invest in initiatives that enhance employee well-being and morale, such as flexible working models, upskilling opportunities, and programs that promote creativity and innovation.

The challenge lies not in choosing between humans and machines but in creating a workplace where both thrive in harmony.

The Bottom Line: Humanizing bots while dehumanizing humans risks creating a soulless enterprise in which efficiency wins, but humanity loses.

As we push the boundaries of AI to replicate and surpass human intelligence, the line between tools and colleagues blurs, raising profound ethical and cultural challenges. To thrive in this new era, organizations must balance leveraging AI’s potential with preserving the human values that foster sustainable success.

Donald Trump’s announcement of steep import tariffs on goods from Canada, Mexico, and China has rekindled concerns about a volatile trade landscape. His proposed 25% tariffs on Mexican and Canadian goods and an additional 10% on Chinese imports represent a significant shift from multilateralism to unilateralism. These actions threaten the integrated North American supply chain and global trade stability if implemented. Businesses that rely on cross-border trade must prepare for increased costs, potential supply disruptions, and retaliatory measures from trading partners.

For instance, the National Retail Federation estimates that U.S. consumers could lose up to $78 billion annually in their purchasing power due to such tariffs. Sectors heavily dependent on imports, such as electronics and apparel, are likely to experience more significant impacts, as the exact percentage decrease in profits varies by industry and company.

The proposed arrangement will have deep and varied ramifications on the current supply chain model

Cost Pressures and Inflation Risks:

Immediately, tariffs will raise the cost of imports, forcing manufacturers to absorb losses or pass costs onto consumers. The automotive, agriculture, and electronics sectors—heavily reliant on North American and Chinese imports—will be particularly affected. For instance, General Motors and Stellantis have already seen their share prices drop due to concerns about rising costs. This could lead to a 0.4–0.9 percentage point increase in consumer prices, straining household budgets and potentially reducing demand.

Disruption of Integrated Supply Chains:

North America’s deeply integrated supply chain relies on seamless cross-border trade. Key industries, such as automotive, heavily rely on just-in-time inventory systems across Canada, Mexico, and the U.S. Tariffs will disrupt these flows, causing production delays and necessitating costly reconfigurations. Companies may resort to stockpiling, leading to temporary surges in logistics demand. For example, in November, import volumes increased by 14% year-on-year.

Shift to Regional Sourcing:

Companies will expedite efforts to diversify their supply chains and reduce dependency on geopolitically volatile regions. While this may benefit nearshoring initiatives, such shifts require time, capital, and substantial operational adjustments. Mexican officials have already proposed decoupling Chinese inputs from their supply chains, but these changes could temporarily disrupt production.

Indian Engineering Sector is likely to reap the benefits of Trump-Modi camaraderie

India, with its burgeoning engineering services sector, stands to gain as companies seek alternative suppliers. The escalating U.S.-China trade tensions have already heightened interest in Indian products, and India’s robust diplomatic ties with the U.S. could further accelerate this shift. India’s potential to fully capitalize on this opportunity hinges on its ability to scale up production and meet the stringent quality standards set by US companies.

Retaliatory Measures and Trade Uncertainty:

Retaliatory tariffs by Canada and Mexico will further strain trade relations. Industries that rely on North American trade, such as agriculture, where over half of U.S. fruits and vegetables come from Mexico, will likely face supply bottlenecks and reduced profitability.

Agriculture: U.S. agricultural exports have been severely affected by retaliatory tariffs, resulting in substantial losses. Between mid-2018 and the end of 2019, the US experienced losses exceeding $27 billion due to retaliation from six trading partners.

Manufacturing: In the past, industries such as automotive and machinery have faced reduced competitiveness abroad. These tariffs have negatively affected their export volumes and profitability.

Enterprises can take the following steps to reduce the ill-effects

Scenario planning and risk diversification can help companies model multiple scenarios, including worst-case tariff impositions, to prepare for potential supply chain disruptions. Diversifying supplier bases and sourcing alternatives from unaffected regions is crucial. For instance, an apparel company sourcing fabrics from Canada might explore Asian or European suppliers.

Investment in tech or outsourcing to engineering firms can be a strategic lever for mitigating tariff impacts on supply chains. These firms can redesign processes, optimize production, and enable regional sourcing to reduce reliance on tariff-affected imports. They also help implement advanced technologies like robotics and Industry 4.0 to lower costs and enhance efficiency. Engineering partners bring expertise in trade compliance, such as reclassifying products or qualifying under trade agreements like the United States-Mexico-Canada Agreement (USMCA). Digital twin models, developed by engineering firms, allow businesses to simulate tariff impacts and adjust strategies proactively.

Engaging policymakers and industry groups through collective lobbying through industry associations can amplify concerns and push for balanced trade policies. Companies must advocate for exemptions or delays in tariff implementation to mitigate immediate impacts. Several influential trade associations in the US actively engage in lobbying and advocacy to shape trade policies. U.S. Chamber of Commerce, National Association of Manufacturers (NAM), American Farm Bureau Federation, and National Retail Federation (NRF) are a few examples.

Enhancing resilience with strategic stockpiling of critical inputs and goods can cushion short-term shocks. Retailers have already adopted this strategy, with imports surging in anticipation of potential tariffs. In anticipation of anticipated tariffs, companies often expedite imports to stockpile goods before the tariffs come into effect. For instance, in November 2024, U.S. ports witnessed a substantial increase in activity, with import volumes surging by 14% compared to the previous year. Retailers promptly advanced their purchases to avoid potential tariffs and minimize disruptions to their supply chains.

The Bottom Line: Trade volatility has become the new normal, and businesses must navigate an era in which geopolitical factors overshadow economic rationality. Strategic diversification, investments in technology and engineering, and fostering strong government relations will be crucial to mitigate risks in regionalized supply chains.

For enterprises, these tariff threats emphasize the urgency of adopting proactive and agile supply chain management strategies. Tariffs, whether wielded as leverage or as policy, are blunt instruments that jeopardize the efficiencies achieved through decades of globalization and cooperation. Enterprises must respond swiftly, but policymakers are also responsible for stabilizing trade environments. Free trade agreements like USMCA are cornerstones of economic integration and should not be undermined by unilateral actions.

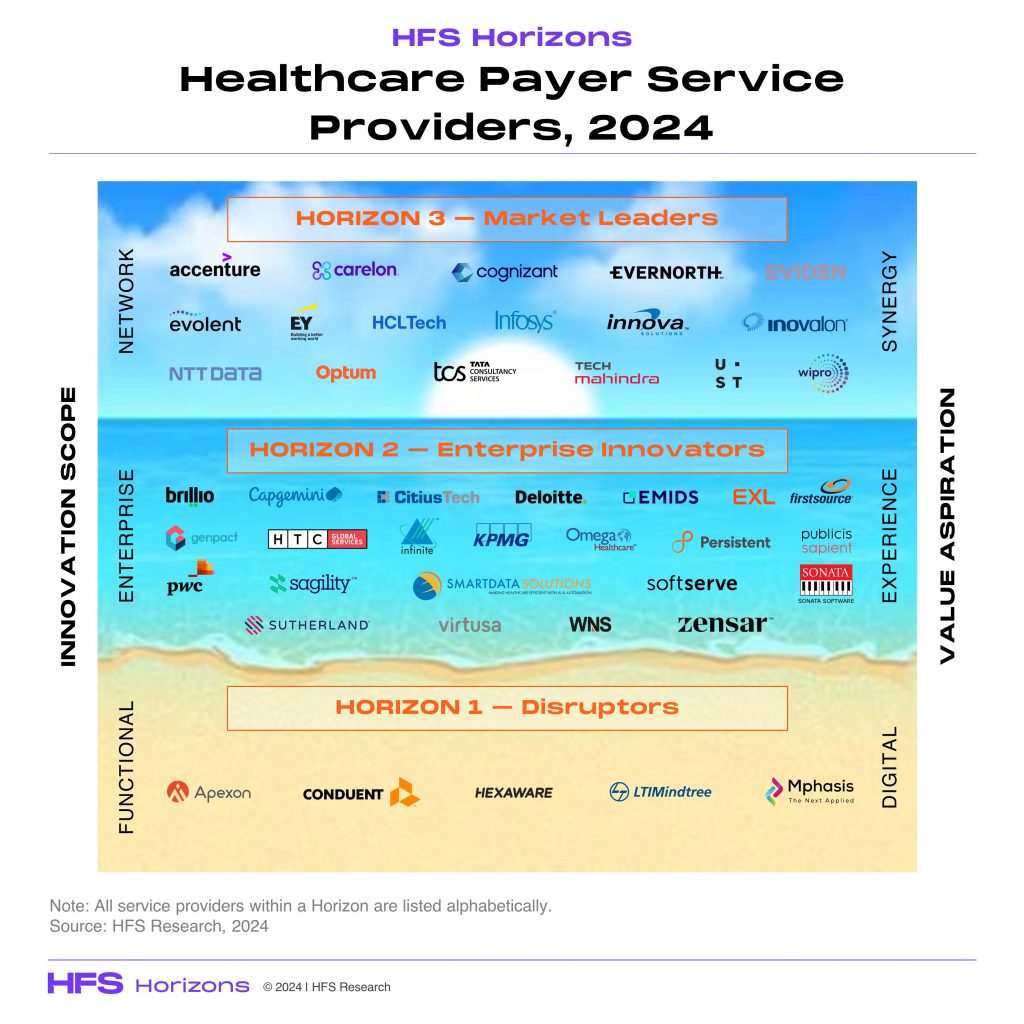

Global coverage for healthcare continues to shift away from commercial underwriting to governments as the quadruple aim of care (cost of care, experience of care, health outcome, and health equities) is challenged. This shift indicates a complex set of challenges and opportunities across the market, making a clarion call for a new generation of disruptors and innovators.

In the HFS Horizon:Healthcare payer service providers, 2024study, we evaluated 45 service providers for their ability to address the cost of care(Horizon 1), experience of care (Horizon 2), and health outcomes (Horizon 3) for health consumers globally. We also began to explore service providers‘ efforts to address health equities. This study reflects inputs from more than 300 healthcare enterprises, over 80 enterprise references, and approximately 80 supplier partners.

45 service providers reflecting a variety of heritages attempt to address the quadruple aim of care

It’s a jungle out there, with new big game that’s been ignored in the past

The significant legacy commercial group insurance that contributed to high marginscontinues to decline.Medicaid lives are plateauing, Medicare reimbursements are declining, and ASO is under unprecedented pressure as employers seek other avenues for services. So, health plans have increased outsourcing and offshoring to overcome their financial challenges, driving service provider growth. Outsourced services include new (health equity) and traditional (customer service) services. Service providers are also exploring newer insurance markets in the Middle East and Latin America as they optimize their value proposition and diversifytheir revenue mix.

Costs and margins will headline the story more prominently than before

Largeto mid-sized vertically integrated healthcare enterprises are reflecting 1-3% margins, while stand-alone health plans are showing closer to 1% margins, which is not sustainable or acceptable to their stakeholders. Despite the top-line growth reflected by service providers, they will see margin deterioration over the next three yearsregardless of claims that AI will aid in margin expansion. That tech–enabled growth movie has been played out in the past under banners such as automation and RPA.

Bigger ain’t better…a lesson that remains unlearnt

Top-line and bottom-line challenges have forced more than 50% of health plans to acquire non-similar businesses such as health systems, pharmacies, and health services. There have been signs of some successful financial integration, though not consistently, but certainly no evidence of success with operational integration. Most service providers can address both payer and provider needs independently but have yet to make the transition to integrated offerings to address vertical integration challenges, choosing instead to sell to legacy buyers. It certainly does not help that integrated healthcare enterprises continue to buy in silos, missing the benefits of integration.

Employers will drive the next apolitical healthcare transformation

Employers are underwriting the health of ~30% of all lives in the US, increasingly seeking new models and channels to address their employees’ shifting demographics and needs globally. Services providers remainon the sidelines of this market, unable to wrap their heads around this opportunity, assuming that servicing ASO is servicing self-insured employers. The fastest and largest segment of the market is getting the cold shoulder from most of the incumbent service providers, allowing a new generation of service providers to take pole positions.

Equity is not just nice to have…it’san economic imperative

CMS added the Health Equity Index to Medicare Star ratings, which will be used in the 2027 rating calculations. So, the days of well-meaning health equity narratives must now translate into action on the ground. Consequently, service provider solutions for data aggregation and analytics to address equity are gaining some traction, but solutions to drive sustainable and stronger impact have not seen much daylight yet.

The Bottom Line: Although the buy–side market dynamics haveshifted significantly, the sell-side remains biased towardthe legacy.

Payers have morphed into service providers themselves and are stumbling about to craft a viablefuture path. So, service providers that have gained success by answering the mail and plainly addressing the needs of payers should rethink their success levers in the future. The game has changed, and so will the way it is going to be played.

It’s been exactly two years since ChatGPT 3.0 hit the streets and dramatically changed the AI conversation. One of the key beneficiaries has been Microsoft Copilot, which, in barely one year, has generated a remarkable $1 billion in revenues and created a vehicle for CIOs to claim early “AI victory” to their corporate leaders hungry to exploit the delights of this AI revolution. So, with Microsoft positioning Copilot as the new “UI for AI,” what do CIOs and their C-Suite counterparts need to do to achieve more value than a glossy AI veneer?

To answer this question, some of HFS’ tech research brain trust attended Microsoft’s Virtual Analyst Day to get an advance view of major announcements and its plans for the year ahead. The overarching theme was… Copilot; what Microsoft achieved in one year of Copilot and where it is going from here.

HFS’ lens for all of our tech research is ultimately what realistic value it offers for enterprise users, beyond all the glamorous AI rhetoric and marketing wizardry. In this vein, we were struck by just how little adoption there actually is and how the value and benefits are still squarely being focused on productivity versus personalization and insight. For example, a recent HFS study into AI adoption shows that only 8% of Global 2000 enterprises adopt GenAI on any scale. We felt like we were at a UiPath event circa 2018 given the number of enterprise leaders discussing use cases and strategies to encourage utilization and drive Copilot and agentic technology adoption at scale.

Why will Agentic be any different from RPA when it comes to delivering on the hype?

HFS’ big question is, “Why now?”—what’s really changed to allow GenAI and Agentic technologies to genuinely change how work gets done, how businesses can be more disruptive and competitive, and how the human experience in the workplace can be enriched?

Microsoft’s answer is agents and the ability to use them safely, orchestrate them, and govern them. It wants Copilot to “be the UI for AI” – creating a “constellation of agents”. Maybe, just maybe….for Microsoft products. The big challenge now, similar to UiPath in the RPA days, isn’t so much selling licenses tied to a corporate dream, it’s getting leaders across the lines of business units to actually understand their real value and deploy them at any sort of meaningful scale.

Microsoft Copilot hit general availability on November 1, 2023. It was a hell of an inaugural year with a massive proliferation of Copilot licenses as enterprises hoped to leverage “safe” AI in the secure cocoon of their Microsoft product ecosystems. We got Copilots for 365, GitHub, Power Platform, Dynamics, Windows, Stream, Azure, and more announced at Ignite this week. We also got Copilot Studio to help build custom AI agents. We’ve seen a number of out-of-the-box agents announced at Ignite this week as well. From all this, Microsoft generated an estimated $1 billion in Copilot revenue within eight months of its launch, used by 70% of Fortune 500 companies. The speed is notable. The utilization is not.

Copilot as the fast answer to the CEO question, “What’s our GenAI strategy?”

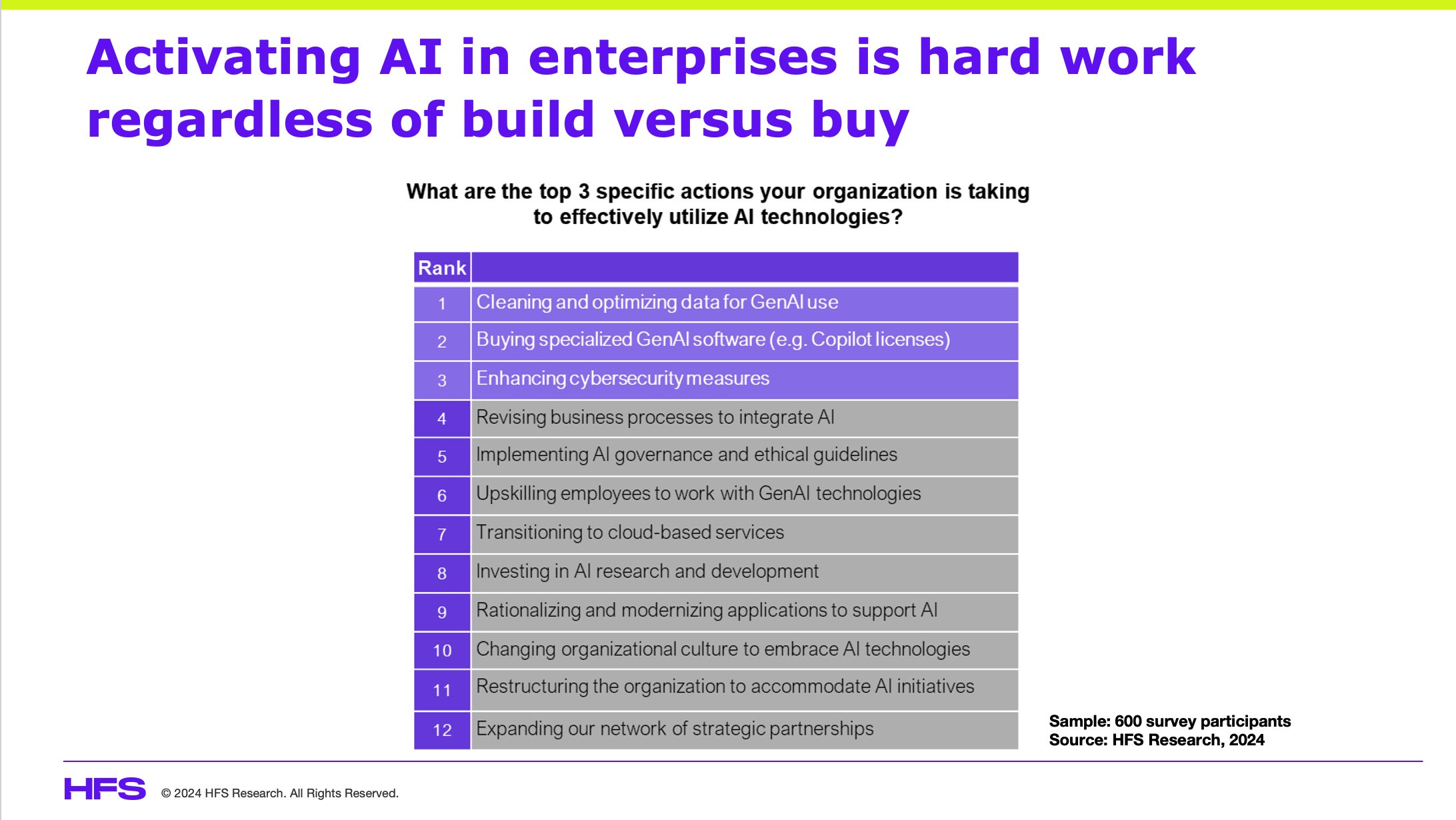

When ChatGPT3 was launched in November 2022, enterprises quickly stepped up to determine their path forward, commencing what HFS calls “death by 1000 pilots”. AI is not new, but determining how to best safely leverage, govern, and manage GenAI was a major challenge for all. And there were no planned budgets for GenAI in 2023, with most projects being funded through loose change from other present budgets.

2024 brought planned budgets but also extenuating economic conditions that left discretionary IT spending very thin. Enter Copilot. As shown below, a recent HFS study of Global 2000 enterprises indicated that licensing GenAI software like Copilot rated as the number two option to drive AI use, behind data optimization and notably ahead of enhancing cybersecurity measures. But even if enterprises opted to buy versus build, all the hard work related to the other 11 options in the below chart are still required.

Despite all the hype, the value and outcomes of Copilot squarely point to productivity

At the event, Microsoft featured various enterprise leaders discussing their use and achievements with Copilot. What they all had in common was that they were, by and large, tech leaders. They were all rightfully proud of the exciting use cases they have developed, and they all, sort of regretfully, indicated that the primary benefit realized thus far is productivity. Examples include:

Blackrock has embedded Copilot into its Aladdin risk platform but indicated its “primary benefit today is productivity, but we are looking farther”

Textron showcased its Textron Aviation Mechanic Intelligence (TAMI), which is designed to help combat knowledge loss due to retiring mechanics and amp learnings with new mechanics. It is now in pilot mode with 1500 mechanics and yields about 93% accuracy.

Dow is working across “offense and defense” approaches trying to drive topline and bottom-line impact. Its latest and most exciting is tied to the payment revenue process tied to freight optimization, and it will save millions in its first year.

Bank of Queensland is using Copilot to drive productivity in software development and customer service. It is piloting in other areas like HR and commercial lending.

RPA failed because it was focused entirely on productivity. CoPilot must avoid this blackhole if it’s going to succeed

In all cases, these firms and many other examples shared anecdotally by Microsoft leadership point to exciting use cases, with some in production and all currently focused on productivity benefits. The challenge with productivity is that when it is expressed in saved hours, enterprises run the real risk of not reclaiming that time. It’s incredibly hard to systematically guide human workers about what and how they should leverage extra time. We all state it should be used “for more strategic pursuits,” but unless it’s defined and prescribed, it’s potluck. This was the issue with RPA where its value was tied to dollars gained through productivity savings, and if customers couldn’t demonstrate real headcount reductions or actual monetary benefits from time “reinvestments”, all CFOs got to see were the millions spent on licenses and little else of value to them.

The progress so far is fast and exciting, but it’s low-hanging fruit. The real promise of GenAI and agentic technologies is the potential to change how we do work, not just reduce manual toil. In HFS’ vision of the next few years of technology innovation, we see a distinct blurring of lines between software and services. As we rapidly embrace agentic technologies, with rote manual processes getting automated, businesses will increasingly consume services as software. Copilots, other GenAI tooling, and assorted autonomous agents will combine to help enterprises work smarter. Read here for more on HFS” “Services as Software vision”.

Copilot had a brilliant inaugural year, but let’s also consider the reality that this also represents the proliferation of an unknown quantity of AI agents into major enterprises doing bespoke work at the individual user level without appropriate governance, alignment with enterprise-wide AI strategies, orchestration, training, or adoption plans. What could possibly go wrong? This is Microsoft’s big learning of 2024 – it can’t really tell enterprises what to do with Copilot, but it (and its partners) can help them build and use a ton of agents safely, with solid governance and orchestration. This is critical to Microsoft’s Copilot growth strategy as well as to answering HFS’ aforementioned question ”why now”.

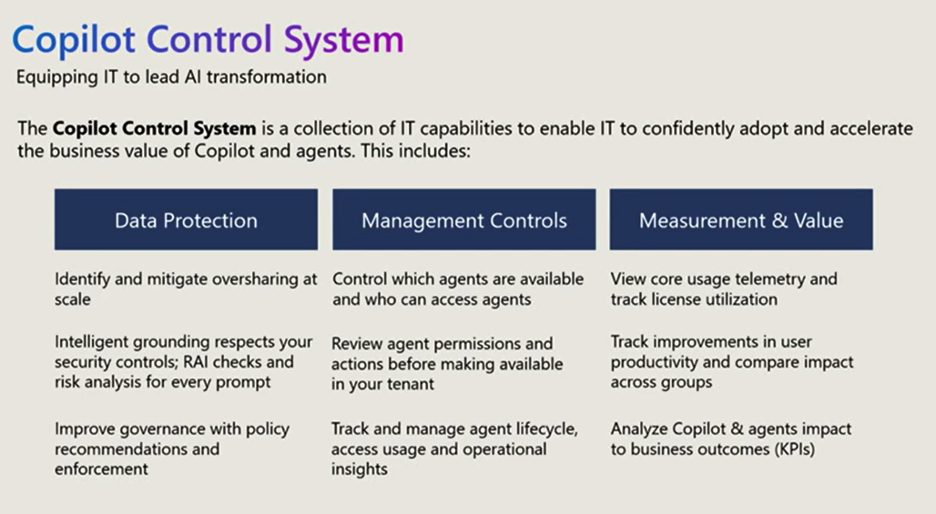

As shown below, Microsoft has just announced its Copilot Control System, which is designed to help enterprise IT scale armies of Copilots and agents. It is designed to complement the existing Copilot dashboard. As Copilots and custom and out-of-the-box agents grow in numbers, enterprises need a sane way to manage this new workforce while protecting themselves and downstream customers and partners. HFS views its launch as a positive but necessary step forward. Microsoft envisions a network of autonomous agents that can execute complex workflows independently while being orchestrated through the Copilot Control System. This is critical to extending Copilot’s role from a personal productivity widget to an enterprise-wide process transformation beast.

Microsoft announces Copilot Control System, a critical missing element in achieving GenAI scale

Source: Microsoft, 2024

The Bottom Line: Year two of Microsoft Copilot must amp data protection, agentic orchestration, and value beyond productivity

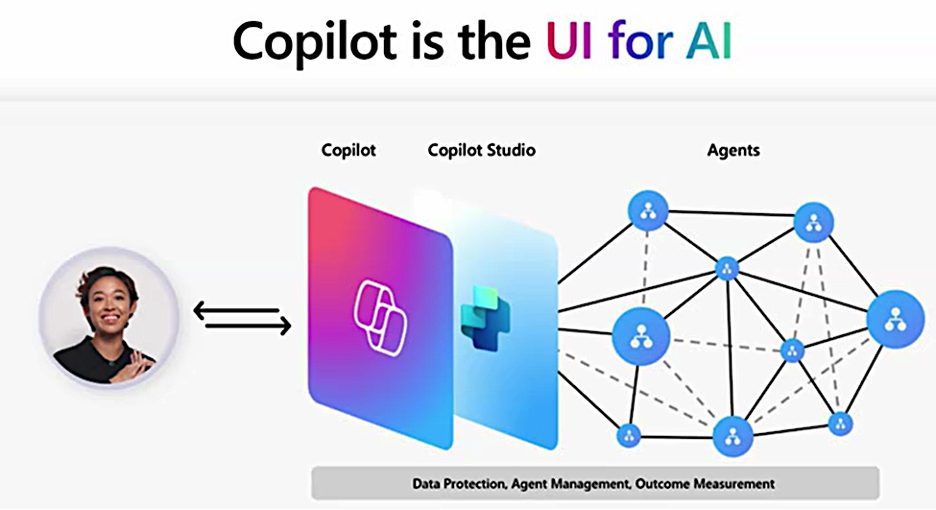

Bravo Microsoft. A year of Copilot has yielded license sales and some productivity gain. Year two must tackle safe, agentic expansion, adoption and education, value beyond productivity, and effective governance and orchestration. Its vision of serving as the “UI for AI” is quite plausible, but only in the context of the greater Microsoft ecosystem (see below).

Source: Microsoft, 2024

SAP, Salesforce, ServiceNow, Oracle, and other critical enterprise applications have their own plans for agentic domination. However, given Microsoft’s global footprint, its orchestration potential is meaningful.

Enterprise users of Copilot must demand more training, further investment in domain and industry-specific use cases and solutions, and simplified integrated pricing. Above all, enterprises need to think more broadly about their enterprise-wide AI strategies and how Copilot and other GenAI and agentic technologies fit into them. Don’t make GenAI and Copilot more hammers looking for nails. Think boldly about changing how work is done and the actual value of humans as we progress toward the age of Services-as-Software.

Some technologies struggle to fulfill their potential and need to be laid to rest. However, there are technologies that simply came into the world before their time because if they are truly capable of delivering real business value, they will eventually find their time and place in the enterprise spotlight.

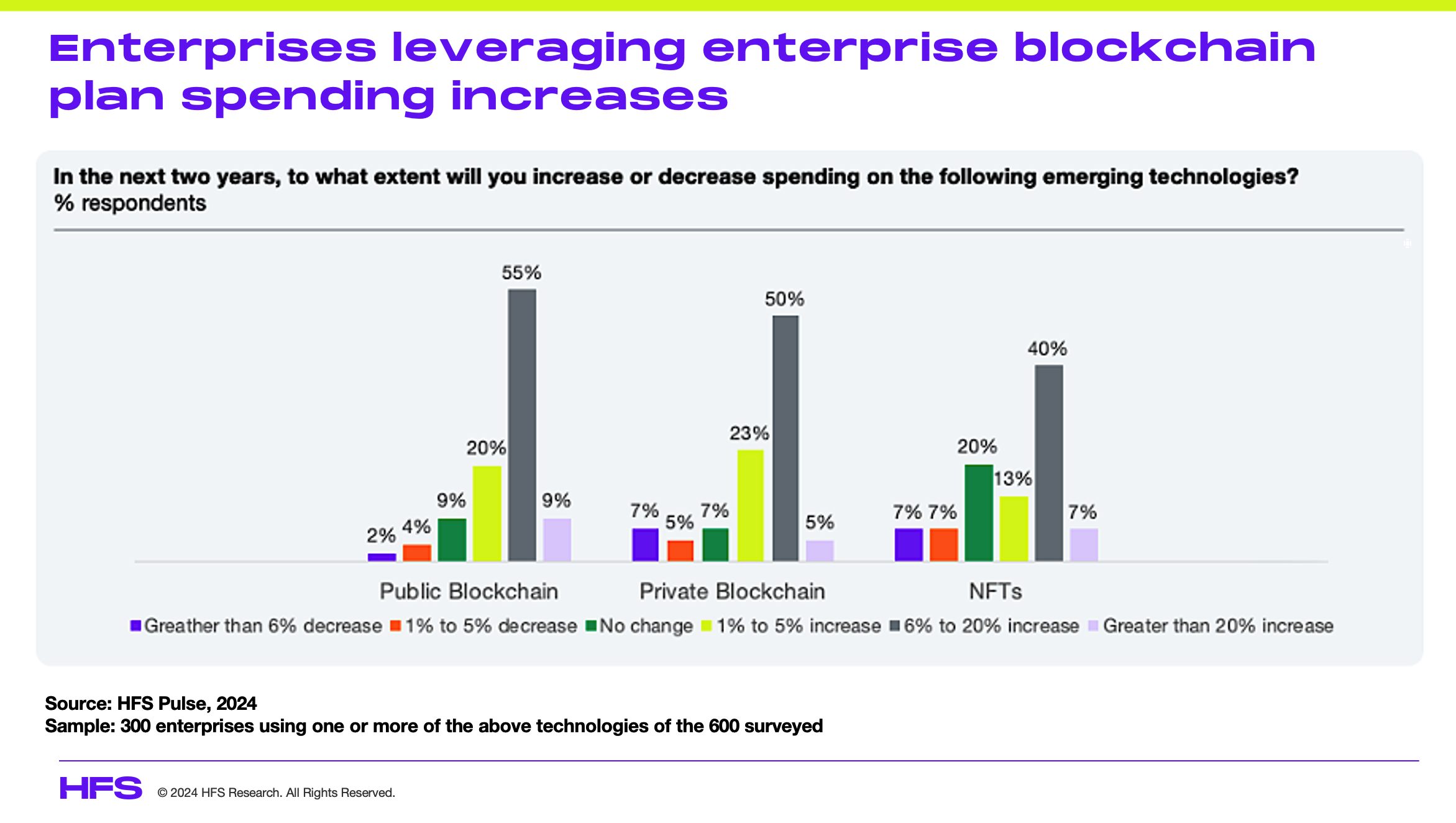

Blockchain was once the shiny object that captivated the tech world, a supposed cure-all that promised to revolutionize everything from finance to food safety. Then came the crash—overhyped promises fizzled, ICOs tanked, and blockchain’s media buzz was silenced except for the speculation around Bitcoin’s value. But guess what? Blockchain isn’t dead. The technology has evolved, grown tougher, and found its niche in critical industries. This is more than just a simple opinion – there’s data to support it. As our HFS Pulse data below reveals, the vast majority of enterprises still using blockchain today plan to increase their spending in the next two years – they wouldn’t do that without experiencing real value:

The blockchain hype machine kicked into overdrive around 2017, with headlines screaming about disruption and revolution across industries. Companies scrambled to plaster “blockchain” on every proposal, hoping to ride the wave of optimism. But much of that early enthusiasm was built on shaky foundations. As we pointed out in our infamous Blockchain Bullshit Buster (See our 2018 piece “Is blockchain a giant digital joke?”). Too many businesses leapt in with little understanding of the technology, banking on the promise without considering its practical use cases.

The inevitable happened: projects failed, the ICO bubble burst, and the market came crashing down. The blockchain-is-dead narrative took hold – using blockchain shifted from a badge of honor to one of shame – but it was an oversimplification. The hype died—but the technology didn’t. What came next was an evolution: businesses became smarter about where and how they deployed blockchain, shifting from broad, unrealistic ambitions to specific, high-value applications – all behind closed doors.

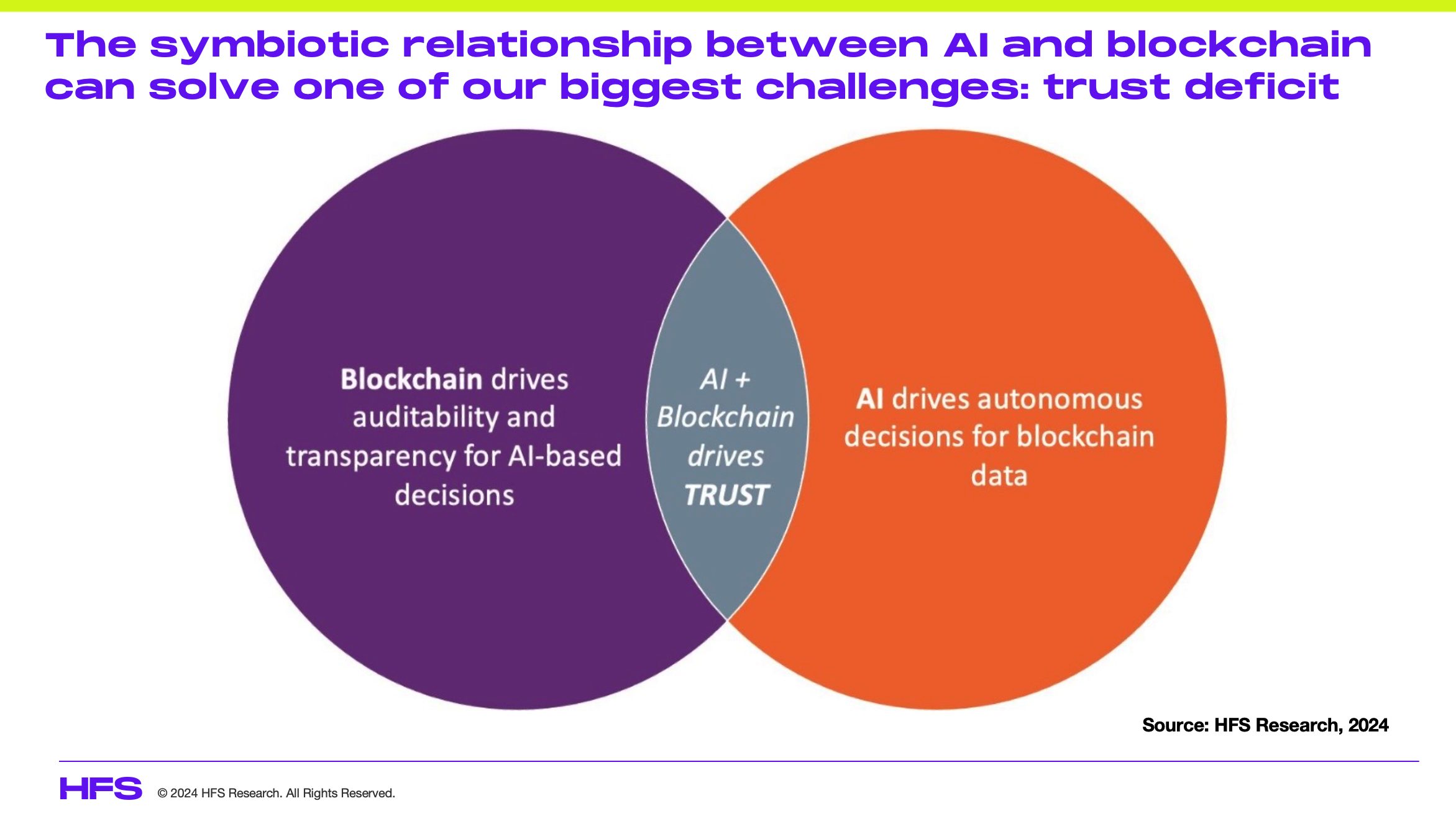

The symbiotic relationship between AI and blockchain can solve one of our biggest challenges: trust deficit

Now we’re almost two years into the GenAI revolution, one of the biggest benefits is the renewal of permission to consider technologies such as blockchain, which lost their way because of trust issues where enterprises simply weren’t prepared to open up their data to new innovative possibilities. Executives were more in fear of getting fired for experimenting with tech than they were in fear of being perceived as rejectors of innovation. AI is changing all of that in many ambitious organizations where C-Suites are challenging their colleagues to embrace a change culture and drive new AI innovation possibilities.

The intersection of AI and blockchain holds incredible potential, particularly in addressing one of society’s biggest challenges: trust. AI’s capabilities to analyze large amounts of blockchain data, paired with blockchain’s decentralized and transparent nature, could significantly reduce the trust deficit between consumers and corporations, as well as citizens and governments. Imagine a world where technology itself fosters greater confidence in systems that have long struggled with credibility issues. However, before we can leverage these advancements to build trust externally, we must first trust the technology itself—ensuring that it’s reliable, secure, and ethical. This is where the true power of this intersection lies:

Blockchain Thrives where Trust, Traceability, and Transparency are non-negotiable

Blockchain has matured, and those in the know recognize that it’s making strategic inroads in industries where trust, transparency, and traceability are non-negotiable. Here are our top 10 favorite real-world examples of how enterprises are deploying blockchain today:

Walmart & IBM (Supply Chain Transparency): Blockchain’s ability to create transparent, tamper-proof records is revolutionizing supply chains. Walmart has partnered with IBM on its Food Trust blockchain, which tracks the journey of food products from farm to table. The result? In cases of contamination, Walmart can trace the origins of food products like leafy greens in 2.2 seconds, a process that used to take days. This not only enhances food safety but also reduces the impact of recalls, lowering operational costs for Walmart.

JPMorgan & Liink (Banking & Finance): In the financial sector, JPMorgan’s Liink platform, part of its Onyx blockchain division, connects more than 400 financial institutions to streamline cross-border payments. Liink enables banks to securely exchange payment-related data, reducing delays and improving transparency. This is critical in addressing the inefficiencies in $30 trillion worth of annual cross-border payments.

Mastercard has launched its Provenance Solution using blockchain to trace the origins of goods along supply chains, ensuring authenticity. Through this platform, Mastercard tracks the source of goods like luxury items and pharmaceuticals, allowing retailers and consumers to verify the legitimacy of the products.

Ripple (Cross-Border Payments): Ripple’s blockchain technology is used to handle cross-border payments efficiently, challenging the SWIFT network. Banks like Santander and American Express have partnered with Ripple to process payments faster and more cost-effectively. RippleNet, Ripple’s global payment network, allows financial institutions to process international payments in seconds instead of days, reducing operational costs and improving liquidity.

Pfizer & MediLedger (Pharmaceutical Supply Chain): In healthcare, Pfizer and other pharmaceutical giants are using the MediLedger blockchain platform to improve the transparency and security of the pharmaceutical supply chain. With counterfeit drugs representing a major challenge globally, blockchain ensures the authenticity of drugs from manufacturing to delivery. This guarantees that medicines prescribed to patients are genuine, thereby improving safety and compliance.

Procter & Gamble & Plastic Bank (Sustainability): Procter & Gamble (P&G) is partnering with Plastic Bank, a blockchain-powered social enterprise, to encourage recycling in coastal communities. Blockchain ensures transparency in the collection and recycling of plastic waste by giving communities access to a digital ledger that tracks plastic collection and recycling rates. Collectors are paid in a digital currency through the blockchain, fostering a circular economy while reducing ocean-bound plastic waste.

Nestlé & OpenSC (Food Safety): Nestlé uses blockchain to track the entire journey of its sustainably sourced coffee and milk. The company partnered with OpenSC, a blockchain platform, to give consumers visibility into how their food is produced and shipped. Nestlé’s blockchain initiative enables customers to verify the source and sustainability of their products by scanning QR codes on packaging, providing unparalleled transparency in the food industry.

Siemens (Energy): Siemens is leveraging blockchain technology for energy trading in microgrids. Siemens is piloting a blockchain-based energy trading system that allows decentralized energy producers (such as homeowners with solar panels) to sell excess energy directly to their neighbors. Blockchain simplifies transactions, ensuring transparency and reducing reliance on traditional utilities.

De Beers (Diamond Tracking): De Beers, the world’s largest diamond producer, uses blockchain to track diamonds from the mine to the consumer. Through its Tracr platform, De Beers guarantees the authenticity and conflict-free status of its diamonds, providing end-to-end visibility in the diamond supply chain. This helps reduce the prevalence of “blood diamonds” and ensures ethical sourcing.

Unilever (Sustainability and Supply Chains): Unilever has been piloting a blockchain platform to track the sustainability of its palm oil supply chain. The platform ensures that the palm oil it sources comes from sustainable farms and adheres to environmental and ethical standards. Blockchain helps verify that suppliers are compliant with Unilever’s sustainability goals, reducing deforestation and improving transparency for consumers.

Even governments are getting in on the action, exploring blockchain for applications like digital identities, land registries, and voting systems. These are high-stakes use cases that can’t afford failure, and blockchain’s decentralized and transparent nature is exactly what’s needed. The backing of public institutions is further proof that blockchain’s longevity isn’t in question—it’s inevitable.

The hype needed to die so that blockchain could get real.

It’s easy to mistake the cooling hype for blockchain’s failure, but this couldn’t be further from the truth. The technology is now living up to its potential—not as a universal fix, but as a tool with targeted, high-impact applications with trust, traceability, and transparency at the core.

Blockchain’s early downfall came from misaligned expectations—companies that treated blockchain as a solution in search of a problem quickly saw their projects fall apart. But today, we see real deployments that address industry-specific pain points. The so-called “blockchain winter” didn’t kill the tech, it forged it.

One reason blockchain was written off too soon was because of its early scalability and privacy issues. Bitcoin and Ethereum, the poster children of the blockchain movement, struggled to handle high transaction volumes and a perception that a technology built on transparency couldn’t offer any level of privacy. Critics were quick to pounce, labeling the technology impractical for large-scale use. But those issues are fading. Layer 2 solutions (think Ethereum rollups) and cross-chain interoperability protocols have unlocked blockchain’s potential for larger-scale applications and enhanced privacy – we highlighted these innovations here. And it’s happening right under the radar—while the media stopped talking, the developers are still building.

Improved interoperability between different blockchain networks means enterprises no longer need to be shackled to one platform. We’ve seen partnerships between tech giants, including Microsoft and Amazon, offering Blockchain-as-a-Service (BaaS), making it easier for companies to experiment and deploy blockchain in a modular, scalable way.

Failure is a Part of Blockchain’s Evolution

As with any new technology, blockchain has had its share of failures. However, these failures don’t signify the end of blockchain’s potential—they are part of its evolution. High-profile projects may have struggled, but these are valuable lessons that help drive the technology forward. It’s important to understand that blockchain isn’t a magic bullet—it needs to be deployed strategically with realistic expectations and a clear understanding of the problems it solves.

Some high-profile blockchain initiatives, such as TradeLens, have not lived up to their initial expectations – and we covered this specific example in January 2023. In late 2022, Maersk and IBM announced the decision to shut down TradeLens, citing the platform’s failure to achieve the necessary commercial viability and collaboration needed to scale across the industry. The demise of projects like TradeLens sheds light on some critical factors:

Adoption and Network Effects: One of the biggest challenges for blockchain platforms like TradeLens is achieving widespread industry adoption. While TradeLens signed up some major shipping companies and port authorities, it didn’t bring on enough players to create the necessary network effect. Blockchain, especially in supply chain and logistics, thrives on collaboration between multiple stakeholders. Without critical mass, the benefits of transparency and efficiency diminish, making it harder for the project to sustain itself.

Legacy Systems and Industry Resistance: Blockchain often has to compete with deeply entrenched legacy systems. In the case of TradeLens, many logistics companies and customs authorities were hesitant to abandon their existing systems, which were highly customized for their needs, in favor of a new technology that required significant changes in infrastructure and operations. The same applies to other industries where blockchain has to integrate with or replace complex legacy systems.

Cost and Complexity: Implementing blockchain solutions can be costly and complex. TradeLens required significant resources for integration and maintenance. In industries with thin margins, like shipping, companies may be reluctant to make these upfront investments, especially if the long-term value proposition is uncertain. Blockchain platforms also demand interoperability between various players’ technologies, which adds to the implementation burden.

Ecosystem and Trust: Blockchain projects, especially those like TradeLens that rely on multi-stakeholder participation, can fail when there isn’t enough trust between parties. TradeLens needed buy-in from competitors, governments, and intermediaries, but in many cases, these parties were reluctant to cooperate, citing concerns over data sharing and competitive advantage.

Failures provide insights on what doesn’t work, but they also highlight the areas where blockchain has the potential to thrive. Businesses are learning to focus on practical, industry-specific applications that address real problems, rather than using blockchain just because it’s the trendy thing to do.

Bottomline. Blockchain winter has forged a stronger, more focused technology that is now solving critical challenges across multiple sectors.

The early frenzy around blockchain may have passed, but that’s not a death knell—it’s a sign of the technology’s maturity. Blockchain is now in its proving ground phase, with tangible, transformative use cases emerging across industries like finance, supply chains, and healthcare. The death of hype isn’t the death of blockchain; it’s the beginning of a more grounded, valuable era.

Blockchain isn’t about spectacle. It’s about solving real business challenges, and it’s already doing just that. So, while the headlines may have moved on, blockchain hasn’t—it’s here, it’s scaling, and it’s delivering results.

We are hurtling towards a US presidential election in which only a small proportion of people are fully aware of the consequences, whether it be the economy, immigration, healthcare, education, the climate emergency, and so on. While Kamala Harris has been specific regarding her policies, we need to examine Project 2025 to understand where policies are likely to be set under the Republican administration.

What concerns me a great deal is the proposed removal of the Patient Protection and Affordable Care Act (ACA)—previously called Obamacare—by the Heritage Foundation that we fully anticipate this Republican administration to execute, especially after President Trump’s determined -(but failed) attempts to repeal the ACA during his previous term. Essentially, when we remove the ACA, we will reverse history back to before 2010, when citizens could be refused insurance coverage for a pre-existing/chronic condition, which today impacts six out of ten citizens, according to the CDC. This will have a huge impact on both citizens and their employers as so many people struggle to access the urgent care they need.

HFS’ lead healthcare analyst, Rohan Kulkarni, has endured the US healthcare system for 16 years as a CIO, strategist, consultant, market maker, and now an analyst who has delved deep into the consequences of Project 2025 on US healthcare to understand what to expect. Over to you, Rohan…

The US presidential elections could reshape healthcare across the quad-aim of care

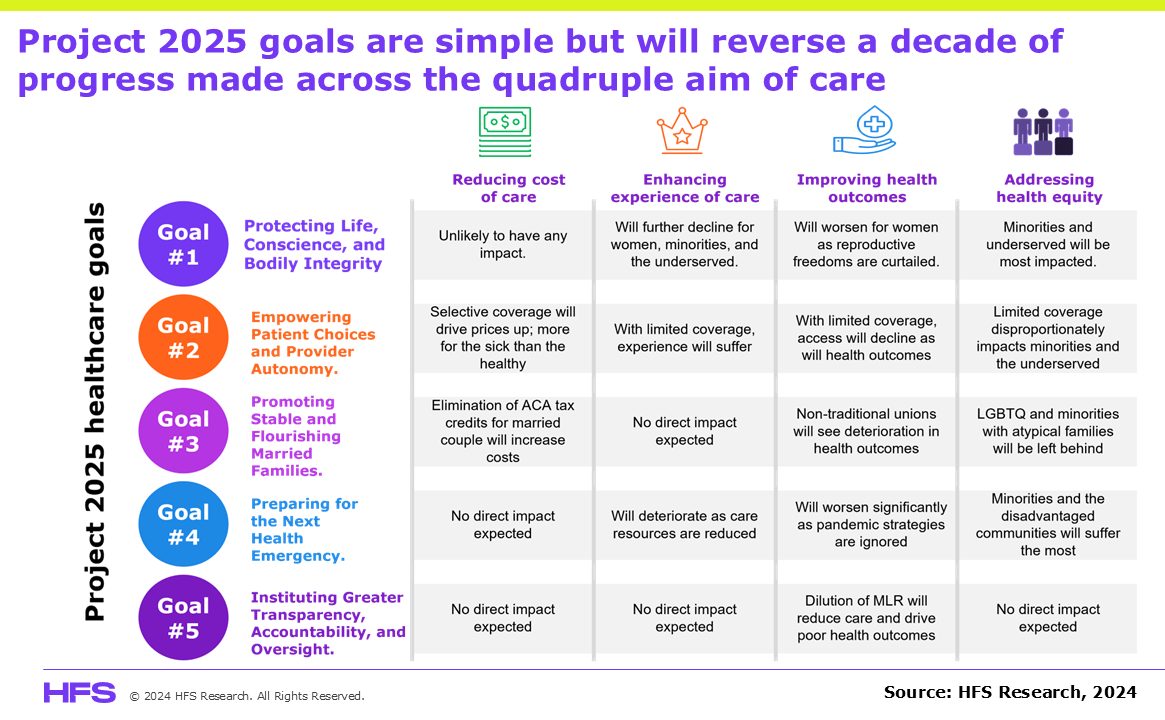

Elections always have consequences; this one in 2024 will impact life and death, particularly for certain population demographics. The choice in the 2024 election is between improving the Patient Protection and Affordable Care Act (ACA), the law of the land, or significantly diluting it with Project 2025, the conservative agenda published by the Heritage Foundation. The exhibit below reflects Project 2025’s healthcare goals and its impacts on the quadruple aim of care (reducing the cost of care, enhancing the experience of care, improving health outcomes, and addressing health equities), which will reverse the progress made over the last decade relative to the cost of care ($0 premium Medicare Advantage, exchange plans), health equity, access to care (lowest uninsured levels ever), and even health outcomes in some limited contexts.

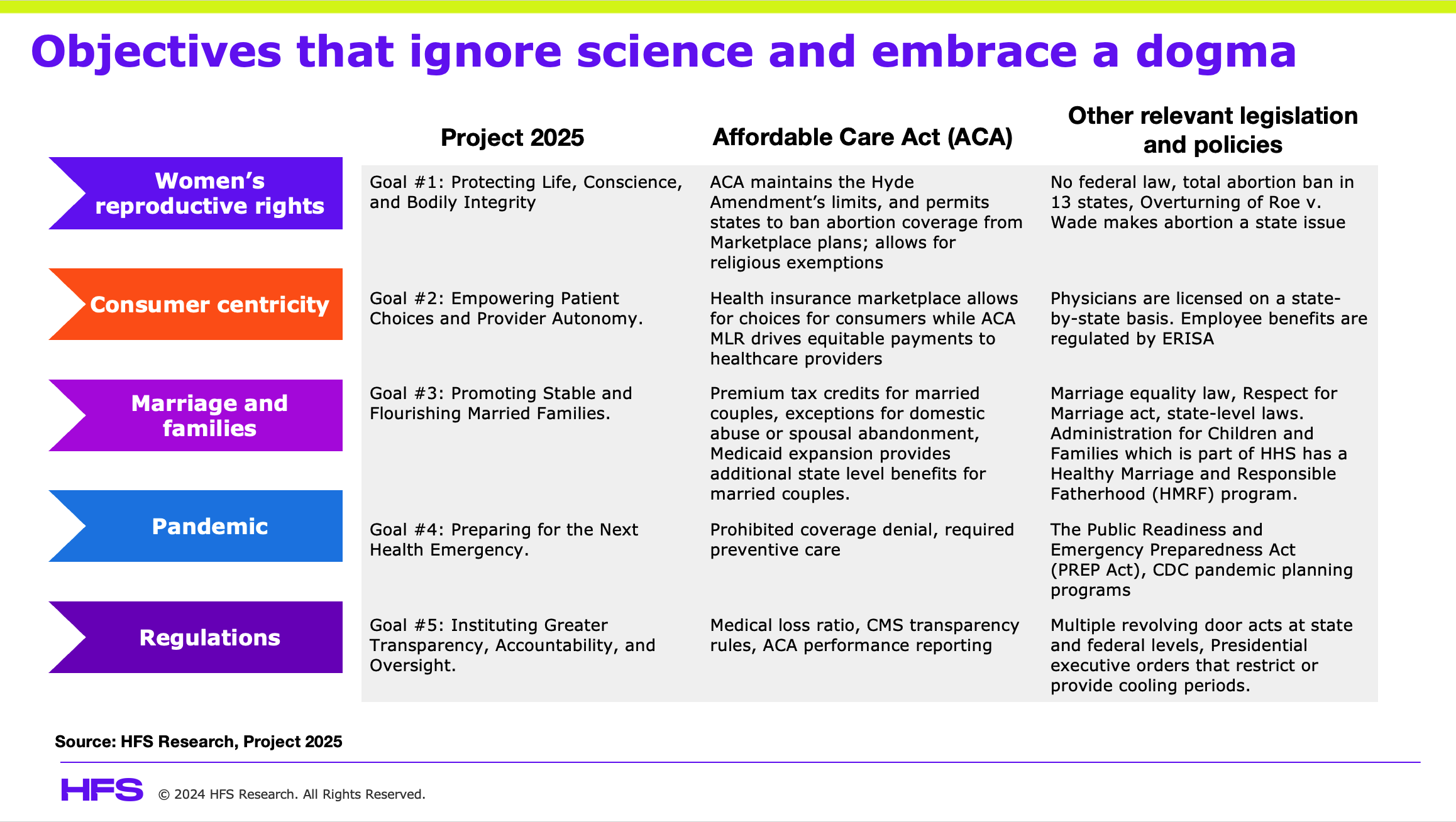

The healthcare-related goals of Project 2025 are intrinsically regressive

Project 2025 lists five goals for the US Department of Health and Human Services (HHS), as shown in Exhibit 2, that form the foundation of a new healthcare paradigm. These goals are a mix of non-healthcare aspirations, such as marriage, and non-scientific assertions like “abortion” and “euthanasia” are not healthcare. The goals are framed to transform US healthcare without the need for Congressional action, rather through the executive actions of the Secretary of HHS.

The first goal aims to ban abortion federally and ignores transgender realities, diminishing equity in healthcare. In meeting the first goal, project 2025 will drive poor health outcomes by ignoring underserved communities that often need the most help. In particular, a federal abortion ban that leaks into other women’s health affairs will curtail access to care as obstetrics and gynecologists quit the field, as we see in many states that have banned abortion.

The second goal is to empower patient choices and provider autonomy, which are already part of the healthcare system. The ACA marketplaces allow consumers to shop and buy health insurance based on their needs, from bronze plans with high deductibles to silver with moderate deductibles to gold and platinum with low deductibles, plans for everyone’s affordability and health needs. ACA provides government subsidies to buy the plans based on income levels. Project 2025 seeks a paradigm that existed prior to ACA, where health insurers could decline to cover consumers and use pre-existing to deny care. As part of the ACA plan selection, consumers, based on their location, can choose from a significant number of providers across specializations. A central tenet of good care delivery is the patient-provider interaction without outside interference, which is generally true in the current context.

The third goal warrants HHS to minimize and possibly ignore same-sex marriages and the needs of LGBTQ+ by emphasizing traditional marriages between a man and woman. While those go against existing laws that the Supreme Court has upheld, there is no empirical evidence to show same-sex marriages yield in families that are any less productive, happy, or have a negative bearing on our society. Project 2025 not only designs a path to return to times of expensive healthcare with poorer health outcomes but attempts to transform society by biasing its plans towards certain demographics.

Goal number four seeks to abandon public health strategies to mitigate pandemics, such as forced lockdowns, isolations, and vaccine mandates. Project 2025 asserts that these techniques with COVID-19 led to distrust in the health agencies and more unnecessary deaths. However, there is significant evidence that those techniques worked, here in the US and overseas, to prevent the spread of disease and reduce deaths. A state-by-state review of COVID-19 deaths shows an increase in per capita deaths in states that refused to follow locked-down and isolation protocols, delayed the delivery of vaccines, and mismanaged communications.

The last published goal intends to reduce the influence of pharmaceutical and healthcare enterprises over the functioning of agencies. It seeks to eliminate the revolving door between government and the private sector. While that is laudable, Project 2025 does not address where expertise will come from to help progress the government’s understanding of science to inform policy. It further goes on to indicate the need for a new set of metrics to determine the extent to which HHS policies and programs achieve desired health and welfare outcomes, something that is already in place with significant checks and balances.

The Bottom Line: Project 2025 seeks to kill the ACA and remake US healthcare through HHS and without legislative action.

Political noise leading up to any election can make the future fuzzier than it is. However, Project 2025 provides a blueprint of how healthcare will be remodeled. Project 2025 proposals suggest a regressive impact on the quadruple aim of care, setting America back to a healthcare paradigm before the enactment of the ACA in 2010 when selective coverage or denial of care for pre-existing conditions was the standard. It is essential that employers remain true to the health and care needs of their employees, adjusting their strategies under a drastically different regulatory framework.

I’m delighted to announce that the analyst who made sustainably great… is back to MAKE SUSTAINABILITY GREAT AGAIN! Yes, folks, Josh Matthews has returned to the HFS analyst family! And in time to meet many of you at the HFS AI Symposium at Cambridge University.

Josh, it’s great to have you rejoin the HFS family. It seems like you’ve had an eventful time in the outside world the past couple of years. What were the highlights? What did you learn about the world?