We’ve talked a lot about the shift to the full-on digital workplace, and now we’re in this “phygital” purgatory where we’re trying to find the right balance between the delights and convenience of digital with the real-world excitement and empathy of engaging with real people in real physical settings again.

Publicis Sapient is driving this new era of physical/digital experiences for major enterprises

This is driving a dire need for partners who can really address this balance right across our customer lifecycles. And when we look at the changing needs of enterprises to engage their customers with experiences that will create new business opportunities for them, create new data assets, or disrupt stagnating business models from the pre-Covid era, we are seeing some digital consulting firms taking this head-on with innovative skillsets to help them.

One firm that is putting customer experience (CX) at the heart of transforming businesses is Publicis Sapient, the digital transformation hub of communication giant Publicis Groupe. The company really is unique in this world of designing and executing blended digital/physical experiences, so let’s dig into this some more…

Enter the new CXO… the Chief Experience Officer

HFS Research Leader, Melissa O’Brien (pictured top right) got time with Publicis Sapient’s new Chief Experience Officer, Abby Godee (pictured top left), who joined recently from Deloitte Digital where she led the firm’s Customer Strategy, Design and Innovation team… Over to you, Melissa:

As we hurtle toward our new OneEcosystem reality, experience is king. As such, many companies are taking a call to put one person in charge of all things experience. Enter the CXO. I met my first CXO at a Genesys event in 2011 and was thrilled to hear about how these custodians of experience were cultivating experiences across enterprise stakeholders. But back then the world was a lot different and more …. well, physical. Now as we grapple with this new “phygital” reality, creating experiences that blend remote and bricks and mortar seamlessly, where people are eager for real connection yet weary of endless Zoom calls are so important. Now we need real leadership that understands human needs and wants and aims to develop experiences, digital and physical ones, on a very human level.

There’s no time like the present to create and invest in roles like this, now when we are more in need of genuine engagement and strong leadership, and we have found that diversity of all kinds is critical to success. Abby Godee (see profile), 3 months in at Publicis Sapient and bringing a tremendous background of experience design, shed some real light on what it means to be a CXO in 2022, and her vision for enabling experiences for Publicis Sapient’s employees, customers, and the greater community.

Melissa O’Brien, Research Leader, HFS: Abby, the CXO role is still relatively a new one but is rapidly maturing. What is a CXO? Can you tell us what it entails, and the vision Publicis Sapient has for you?

Abbye Godee, Chief Experience Officer, Publicis Sapient: It depends on the maturity of the organization, Melissa. Publicis Sapient has been in the experience business for many years, it gives me the opportunity for my role to be more expansive. At Publicis Sapient my role is about strengthening and scaling the impact of experience. There are traditional design capabilities like UX, product design, and other core capabilities, but we also have strong design strategy and CX strategy. So it dovetails into transformation strategy on one end of the spectrum and on tech execution and platform execution on the other end. My role is to guide the impact experience can have. We are ensuring our approach to technology is not just best in class but informed by human needs. I see my role as being the custodian of the human in experiences. I don’t think we design experiences; we design the opportunity for people to have great experiences. It’s up to us to deeply understand our employees, our partners, the patients, the citizens and so forth, so we can design ways for them to have the right experiences. You have to embrace skills way beyond core design skills to enable that.

Melissa: Can you share some of your background with us, Abby, and what do you consider to be your greatest influence?

Abby: My educational background is in cultural anthropology and that has always informed my approach. I studied design and was art minor, and can design my share of products, but what’s always driven me is “why do people do what we do?” So there’s a lot of overlap with behavioral design. I worked at Smart Design where we were busyRead More

Barely more than two years ago we did audio calls. Yeah, audio calls – remember those awkward things, where people not only left their mute buttons on, but often just went missing from the discussion altogether? Now we’re all so well organized in our visual virtual worlds that it’s a huge challenge trying to balance the ridiculous notion of wasting time getting dressed, going to an office, and – heaven forbid – actually having voluntary discussions with our colleagues.

We are all human beings and we’re super comfortable in our own isolation. The days when all our colleagues were on Facebook, and our companies had become extensions of our families are long gone. I wonder how many people reading this met their spouses over a water cooler (or company Xmas party)? So how does our relationship with our company change?

Unstructured flexibility is the new “nine-to-five”

I remember once being chastised for sending out emails to my staff over the weekend. Gosh, how dare I ruin that wonderful work-free time, when I can wait until Monday to bark orders? Seriously, I don’t have bloody time on a Monday morning, so I will send out what I need when I have time to ask! If people demand flexibility to cater to their busy lifestyles/family commitments, then this whole nine-to-five bullsh*t died with audio calls.

Now I am the first to laud judging performance on outcomes, but if you’re spending half your day taking mom shopping, kids to soccer practice, taking in a quick 9-hole round, then you’re gonna have to find some time somewhere to meet your work outcomes. If you want to decompress and escape work interactions, then you need to manage that yourself – turn off all work apps, get a personal cellphone… you need to manage your own clock on/clock off these days. If you want nine-to-five structure then go back to the office. Am sure you can be amazingly productive with nothing much else to do than work 40 hours a week imprisoned in a work setting.

Managers need empathy skills… emotional intelligence is the route to the top

I have spent my entire career screaming that people management capability belongs outside of the HR department. Suddenly all ambitious managers are being judged on their ability to retain and develop their teams, keeping their staff focused and motivated. An unstructured work environment demands a lot more cohesion, honesty, and teamwork – and the only way to achieve that is through emotionally-intelligent leaders. That means management is more than dolling out tasks and conducting awkward performance reviews… it’s about getting to know what makes your people tick. When people are happy, they feel trusted, and they value the people around them, they perform. And it today’s work environment you will lose your best people if you can’t bond with them – not only will you likely fail to meet your goals, but your leadership will also notice that you’re struggling to drive your team.

The Bottom-line: An unstructured environment is based on trust and closer emotional relationships between managers and colleagues

We all have bad weeks when we are off our games – so don’t hide, let your manager or team know and they may help you get back in the groove. Good people are sympathetic and empathetic, and so are good colleagues. And if you’re having a period of great productivity, success and inspiration, let people know too… good vibes and passion are infectious and make people want to bond with you. Bare your soul a bit, whether you are an experienced leader or a junior team member, and you’ll find your work environment can be a bit more than a laptop screen and soul-crushing interactions with people who you barely know. There is no defined curriculum anymore when it comes to the workplace… when it comes to trust and passion, that comes from people and their ability to motivate and empathize with each other.

With its proposed contentious Kyndryl-style split and rapid CEO departure, Atos is teetering on the brink. As if its decline in stock price, recent accounting scandals, and lackluster financial performance were not enough, the firm now is more primed than ever for being acquired with these latest developments. In addition, Atos is shackled by the intense involvement of the French government as it manages sensitive tech and data for both the French military and tax collections, with former PM Edouard Philippe being on the Atos Board. HFS believes competitors should move to acquire Atos’ crown jewels now and not wait for the bleeding to start.

We believed buying Kydryl last year made a lot of sense, however, it has lost a lot of talent and could take too long to absorb to make the acquisition worthwhile, even as its stock price is likely to fall below $2bn. Our recommendation would be to make the move now to acquire the crown jewels of Atos – notably big data and cybersecurity – before the business sheds more talent and loses market position.

So what are the lessons learned from IBM’s Kyndryl spin-off and what is HFS’s take on the current predicament in which Atos finds itself?

Staring down the strategic barrel

Having had a full in-tray from the word go (see earlier post), recently appointed CEO Rudoplhe Belmer presented the findings and conclusions from his strategic review as well as his new management team. The pillar of his turnaround plan is a spin-off of its infrastructure business similar to IBM’s move to spin-out Kyndryl. If that was not enough, just an hour before the announcement was made, news broke that Belmer has since resigned after the Atos board rejected his suggestion to sell off its BDS division (Big Data and Security). Simply put, Atos is teetering on the brink of disaster, not helped by a tanking stock market and IT services firms desperately clinging onto their delivery staff in this cut-throat market.

We were starting to write this analysis looking at the announcement of a Kyndryl-style spin-off. This was more than enough to get our heads around. Before the second coffee news broke that Atos CEO Rodolphe Belmer despite presenting the strategy to investors, had just resigned before the meeting. According to press reports he is said to have lost a power battle after he allegedly wanted to sell off the new business unit comprising security and high-performance computing. Let’s take a deep breath and rewind…

Atos’s Kyndryl is called Evidian, kind of…

The original announcement comprised the following. After a strategic review by the new CEO, Atos is planning to follow IBM by separating its business into two, publicly-traded entities. One focused on a higher-margin business dubbed “SpinCo” but with the brand of Evidian. It consists of two business units Digital (digital transformation, cloud, and applications) and BDS (digital security and high-performance computing). In 2021 its revenues would have been €4.9bn with an operating margin of 7.8%. The entity that is meant to be spun off is dubbed TFCo (for “technology foundation”) and is meant to retain the Atos brand. It comprises the low-margin units of core infrastructure, digital workplace, professional services, unified communications, private cloud, and platforms, as well as BPO. In 2021 its revenues would have been €5.4bn with an operating margin of minus 1.1%. Despite the intended spin-off Atos is continuing to look for a buyer of its unified communications business. And while BPO might have a low margin, it doesn’t really fit into the infrastructure-centricity of TFCo. Probably it is telling that the infrastructure business is retaining the Atos brand, flipping IBM’s logic with Kyndryl.

Separation is the right action, but it will be a long and painful process

Atos’ intent is to deliver the carve-out in 12 to 18 months. As the challenges of Kyndryl have demonstrated, it is tough to deliver on such a spin-off. Kyndryl’s market cap is down to $2.1bn. But that is a pitiful fraction from the $19bn in revenues it started out from. In Atos’s case, its management acknowledged that its talent pyramid needs serious surgery as 40% sit in high-wage economies. Put another way the acquisition of Syntel has at best marginally changed the talent pool. The other headwind is a stuttering sales engine as Atos has to re-engineer a sleuth of unprofitable deals.

The security business is the jewel in the crown. Selling it off might have filled Atos’ war chest but the interdependencies on digital operations are immense. Take Siemens as one of their key customers, re-evaluating and potentially re-engineering operational processes would be immense.

Competitors should give a toss about Atos’ cybersecurity business

The security business is the jewel in the crown. From 2020 to 2021 Atos acquired very promising and innovative companies (Paladion, Digital. Security, SEC Consult, or Motiv) in the cybersecurity arena, and its initial strategy was to go on with further targeted acquisitions combined with organic growth. Atos cybersecurity services revenue has grown by two digits year-on-year over the past 3 years and the total number of dedicated headcounts has substantially increased in the same period. AIsaac (a Managed Extended Detection and Response platform) and Evidian (a Managed Identity and Access Management platform) are the two flagship proprietary platforms that seriously distinguish Atos from its competitors by leveraging the power of automation, AI, and analytics for way more intelligent and resilient cyber defense capabilities.

With one out of two clients belonging to public, defense, or manufacturing sectors, Atos has developed a very compelling end-to-end cybersecurity offering with a distinguished industry vertical expertise and a rich partner ecosystem. Atos works with many defense organizations worldwide on mission-critical programs, where it combines cybersecurity services with a wider range of proprietary products.

Atos’ digital security vision has always been quite ambitious: be a “global trusted orchestrator between the virtual and real-world, assuring digital innovation, defending critical assets and allowing operational resilience between people and systems everywhere”. And Atos has clearly not lost its “Raison d’être”.

Atos needs a cultural makeover

Atos is still very French. Almost all senior executive positions and the new management talent are French. Yet, the necessity for wholesome cultural change goes much deeper. IBM made a bold move for RedHat to drive strategic and cultural change. Suffice it to say even that cultural change didn’t prevent the spin-off of the commoditized infrastructure business. Atos doesn’t have a change agent like RedHat. What Atos needs is more wholesale cultural change akin to Microsoft, which under Satya Nadella went from a toxic brand to an innovation powerhouse and magnet for talent. The separation might have helped in parts but with the CEO’s resignation, any change will be on hold till a new leader has found his feet under the new office desk.

As with Kyndryl, predators might hover but none has taken the bait as yet

Our assessment of possible suitors for Kyndryl holds true for Atos as well. Its unified communication business remains up for sale and the UK-centric BPO accounts look out of place in the new infrastructure-centric TFCo. But where it gets more complicated is Atos’ entrenchment in European and French public sector and defense deals. With GAIA-X the European cloud initiative being top of mind. Political involvement and backroom maneuvers are highly likely.

However, with the stock market in peril, especially with the looming interest rate hikes to combat inflation, the timing for acquisitions is a lot more attractive today than last year

Lasy tear, many of the major service providers were avoiding big painful acquisitions while they were killing it with double-digit growth – but are all now desperate for delivery resources. You have to think acquisitions like Atos / Kyndyll are starting to make more sense just for added scale. Especially at these cheap prices (Kyndryl’s market cap is close to $2bn, despite colossal revenues of over $18bn. For example, Accenture will likely be over a million staff soon to deliver on its growth promises… the firm has to find the scale somewhere. M&A motives have to be shifting from “fuelling pure growth to delivering on what they have taken on”. This is the same for all the other leaders who’ve bitten off more than they can chew. You can easily see the likes of Cognizant, HCL, Infosys, and others intensely considering the possibilities of added scale to dominate the market.

HFS believes competitors should move to acquire Atos’ jewels now and not wait for the bleeding to start

The issue is also that most CEOs don’t want to risk large mergers when they are in strong growth periods, but when things start to look dicey they are much more open to making strategic bets. HFS believes competitors should move to acquire Atos’ jewels now and not wait for the bleeding to start. HFS believes buying Kydryl last year made a lot of sense. Now it’s lost a lot of talent and could take too long to absorb to make the acquisition worthwhile. Our recommendation would be to make the move now to acquire the crown jewels of Atos – notably big data and cybersecurity – before the business sheds more talent and loses market position.

Bottom-line: With another vacuum in leadership Atos is likely to be carved up rather than carving its infrastructure business out

Rodolphe Belmer is said to stay on till September to help with the transition. Yet, Atos can ill afford another transition period. Even if suitors don’t take the bait, it will be challenging to sign up for new strategic deals. Also, we shouldn’t forget that the macro environment is worsening with recessions a likely scenario. Thus, as HFS said in its most recent analysis is that Atos needs a new strategic playbook more than it needs a new CEO. Today this has increased humongously in poignancy.

Finally, you’re free from the house-slavery! You escaped and are now back in conference land. While it barely feels like the last 2.5 years of your life just happened and you’re right back in the swing of physical interaction, there is something weird lurking around your inner consciousness:

1. Those Zoom and Teams calls have become a plague on your life

For chrissakes, I am back in the world of humans, people. Just f***ing leave me alone with the soul-crushing Zoom calls. I am at a REAL CONFERENCE talking to REAL PEOPLE. No, I do not have hours and hours to stare into that video-call abyss… I am back in the real world and that’s really IMPORTANT!

2. Everyone’s lacking stamina

What happened – we used to be such a youthful bunch, hanging around the hotel bar, sneaking off to a nightclub/cigar club etc. Now people can barely make it through three boring panels without having to take a sneaky nap. “Just going to say goodnight to the kids ” is the last thing you’re hearing from loads of people these days as they discretely slip into the elevator…

3. You just don’t hate people like you used to

Oh those people you avoided eye contact with are now chatting to you like long-lost friends… omg am I enjoying human contact? Did I just press the flesh with people?

4. Content takes a backseat as Covid may have actually killed PowerPoint (gasp)

Seriously, this could be one pandemic benefit we hadn’t noticed, but no one likes staring at cardboard PPT anymore – we actually like talking and engaging with each other. We’ve had enough watching people reading off scripts. Let’s cut loose and TALK!

5. Noone’s talking about bloody Covid

Yeah, the topic-du-jour is now taboo… it’s just mind-numbing to engage in yet another conversation about everyone getting sick… yet again.

6. The end of the world is nigh, so let’s just enjoy what we have left

After that apocalypse that was posing as some faded version of Davos, where nuclear war and hyper-stagflation were combining with the fact no-one’s doing squat with this net-zero stuff to destroy the last remnants of humanity… most of us are trying to focus on more positive dynamics in the world. Like the fact that recessions can breed more focused behaviour and investments from enterprises. Plus the fact that enterprises are starting to use technology more effectively and not simply buying up licenses of software with no idea how to deploy it. And let’s not forget the fact that our employers have to pretend to be nice to us and actually want us these days. And we can always talk about the Metaverse…

7. Oh… and we can always talk about the Metaverse

Yeah – from blockchain to VR goggles, that thing the Metaverse, where we’ve already been spun several definitions, is going to save us. Yes, folks, it will because everyone says so. Service providers will start reporting “metaverse revenues” soon… Gartner will surely come out with “Meta-automation” next and HFS will be handing out mandatory VR goggles at its September Super Summit… surely?

According to the 33rd President Harry S, Truman, “It’s a recession when your neighbor loses his job; it’s a depression when you lose yours.”

In the case of the IT services and outsourcing industry, it’s the neighbors who are in trouble, and service providers are in pole position to take full advantage. There will be no services depression… and recessions only last a few quarters.

A recession may just be a blessing in disguise for IT and business services

It pains me to say this, but a recession could drive a healthier long-term outcome, not only for the IT and services industry but for economies in general. We’ve been living on printed money for 14 years, venture capitalists have bankrolled billions in business plans that make no sense (and will leave a trail of destruction), and many people can’t even motivate themselves to leave their houses to go to the office. Let’s be honest folks, the global economy is unsustainable on its current trajectory and we need a big reality check.

Moreover, the IT and business services industry is likely to benefit considerably from a global recession as cost-control takes center stage, in addition to the urgent need from enterprises to migrate securely to the cloud, automate processes and get cleaner, quicker access to data. Let’s examine why this is a likely scenario…

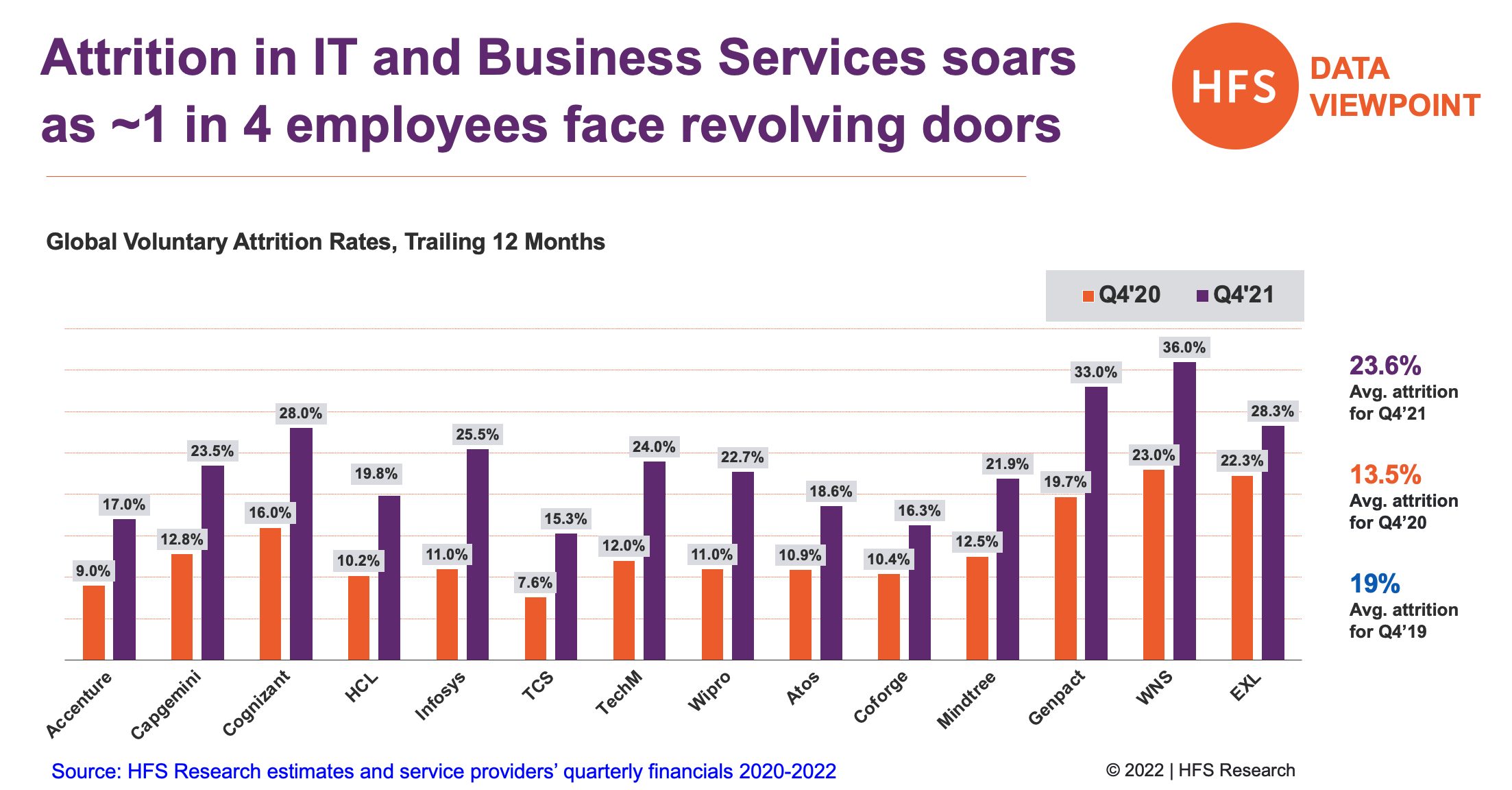

Slowing attrition will repair fractious client relationships and stem the bleeding

Staff turnover in IT and Business Process services deals has reached levels where many customers are screaming at their service providers to stem the bleeding, and we’re seeing some contentious situations developing, including some supplier switching. While some providers claim to have their attrition more “under control” than others, the problem is massive and widespread, and having (almost) entire project management teams take flight midway through complex cloud migrations has become all too common over the past few months. In short, if this situation persists, many clients will just bite the bullet and bring more IT back in-house.

Economic recessions have historically driven growth in services and outsourcing and this time should be even more aggressive as cost reduction becomes hugely significant

As attrition slows, there will be enough scale in India to respond to the needs of enterprises in dire need of reducing costs and accessing capabilities. While wages have increased in services (likely 10-15% on average), there is easily enough profit margin from all the TWILTCH providers to compensate and be able to offer clients 30%+ cost savings, on top of whatever innovations they provide. After the 2008 crash, we saw a significant spike in offshore IT services, in particular application development, which has pretty much carried us through to this 2022 recession. Since pandemic times, focus has shifted more to the frantic rush to the cloud and the focus on cost savings has been overshadowed by this great “hurry” to move enterprises into these critical virtual environments. However, we see a swing back to cost as the major impetus to outsource as industries like hi-tech, financial services, and healthcare have no choice but to improve their profitability to survive.

The Bottom-line: Cost reduction has traditionally been the conversation starter for outsourcing… and it’s back again in spades.

However, deep customer scrutiny on attrition and execution capability will dictate which providers come out on top. We know service providers can keep pushing the cost reduction capabilities, but they have to get ahead of these critical attrition issues fast – and they have that opportunity with the global economy tightening.

The turmoil in global supply chains and challenges of remote workers should work in favor of using smart outsourcing models, especially for enterprises that are struggling to retain their own key talent in areas such as cybersecurity, hybrid cloud migration, app dev etc. The leading outsourcers are those which have a depth of resources in critical areas (and at less expense) which make themselves such critical partners for their clients. I would add a huge caveat here that service providers have to get their own attrition under control, but a recession will slow down the great resignation and should stabilize this work environment.

Cost is king when recessions bite, and outsourcers that can deliver 30%+ cost savings via access to lower-cost labor at scale, combined with strong cloud delivery and automation, will be sitting pretty.

We’ve talked a lot about the shift to the full-on digital workplace, and now we’re in this “phygital” purgatory where we’re trying to find the right balance between the delights and convenience of digital with the real-world excitement and empathy of engaging with real people in real physical settings again.

Publicis Sapient is driving this new era of physical/digital experiences for major enterprises

This is driving a dire need for partners who can really address this balance right across our customer lifecycles. And when we look at the changing needs of enterprises to engage their customers with experiences that will create new business opportunities for them, create new data assets, or disrupt stagnating business models from the pre-Covid era, we are seeing some digital experience firms taking this head-on with innovative skillsets to help them.

One firm that is now past the $10bn mark and really making its name for enmeshing advertising with digital tech design and execution is Publicis Sapient, which represents the is the digital transformation hub of advertising giant Publicis Groupe. The company really is unique in this world of designing and executing blended digital/physical experiences, so let’s dig into this some more…

Enter the new CXO… the Chief Experience Officer

HFS Research Leader, Melissa O’Brien (pictured top right) got time with Publicis Sapient’s new Chief Experience Officer, Abby Godee (pictured top left), who joined recently from Deloitte Digital where she led the firm’s Customer Strategy, Design and Innovation team… Over to you, Melissa:

As we hurtle toward our new OneEcosystem reality, experience is king. As such, many companies are taking a call to put one person in charge of all things experience. Enter the CXO. I met my first CXO at a Genesys event in 2011 and was thrilled to hear about how these custodians of experience were cultivating experiences across enterprise stakeholders. But back then the world was a lot different and more …. well, physical. Now as we grapple with this new “phygital” reality, creating experiences that blend remote and bricks and mortar seamlessly, where people are eager for real connection yet weary of endless Zoom calls are so important. Now we need real leadership that understands human needs and wants and aims to develop experiences, digital and physical ones, on a very human level.

There’s no time like the present to create and invest in roles like this, now when we are more in need of genuine engagement and strong leadership, and we have found that diversity of all kinds is critical to success. Abby Godee (see profile), 3 months in at Publicis Sapient and bringing a tremendous background of experience design, shed some real light on what it means to be a CXO in 2022, and her vision for enabling experiences for Publicis Sapient’s employees, customers, and the greater community.

Melissa O’Brien, Research Leader, HFS: Abby, the CXO role is still relatively a new one but is rapidly maturing. What is a CXO? Can you tell us what it entails, and the vision Publicis Sapient has for you?

Abbye Godee, Chief Experience Officer, Publicis Sapient: It depends on the maturity of the organization, Melissa. Publicis Sapient has been in the experience business for many years, it gives me the opportunity for my role to be more expansive. At Sapient my role is about strengthening and scaling the impact of experience. There are traditional design capabilities like UX, product design and other core capabilities, but we also have strong design strategy and CX strategy. So it dovetails into transformation strategy on one end of the spectrum and on tech execution and platform execution on the other end. My role is to guide the impact experience can have. We are ensuring our approach to technology is not just best in class but informed by human needs. I see my role as being the custodian of the human in experiences. I don’t think we design experiences; we design the opportunity for people to have great experiences. It’s up to us to deeply understand our employees, our partners, the patients, the citizens and so forth, so we can design ways for them to have the right experiences. You have to embrace skills way beyond core design skills to enable that.

Melissa: Can you share some of your background with us, Abby, and what do you consider to be your greatest influence?

Abby: My educational background is in cultural anthropology and that has always informed my approach. I studied design and was art minor, and can design my share of products, but what’s always driven me is “why do people do what we do?” So there’s a lot of overlap with behavioral design. I worked at Smart Design where we were busyRead More

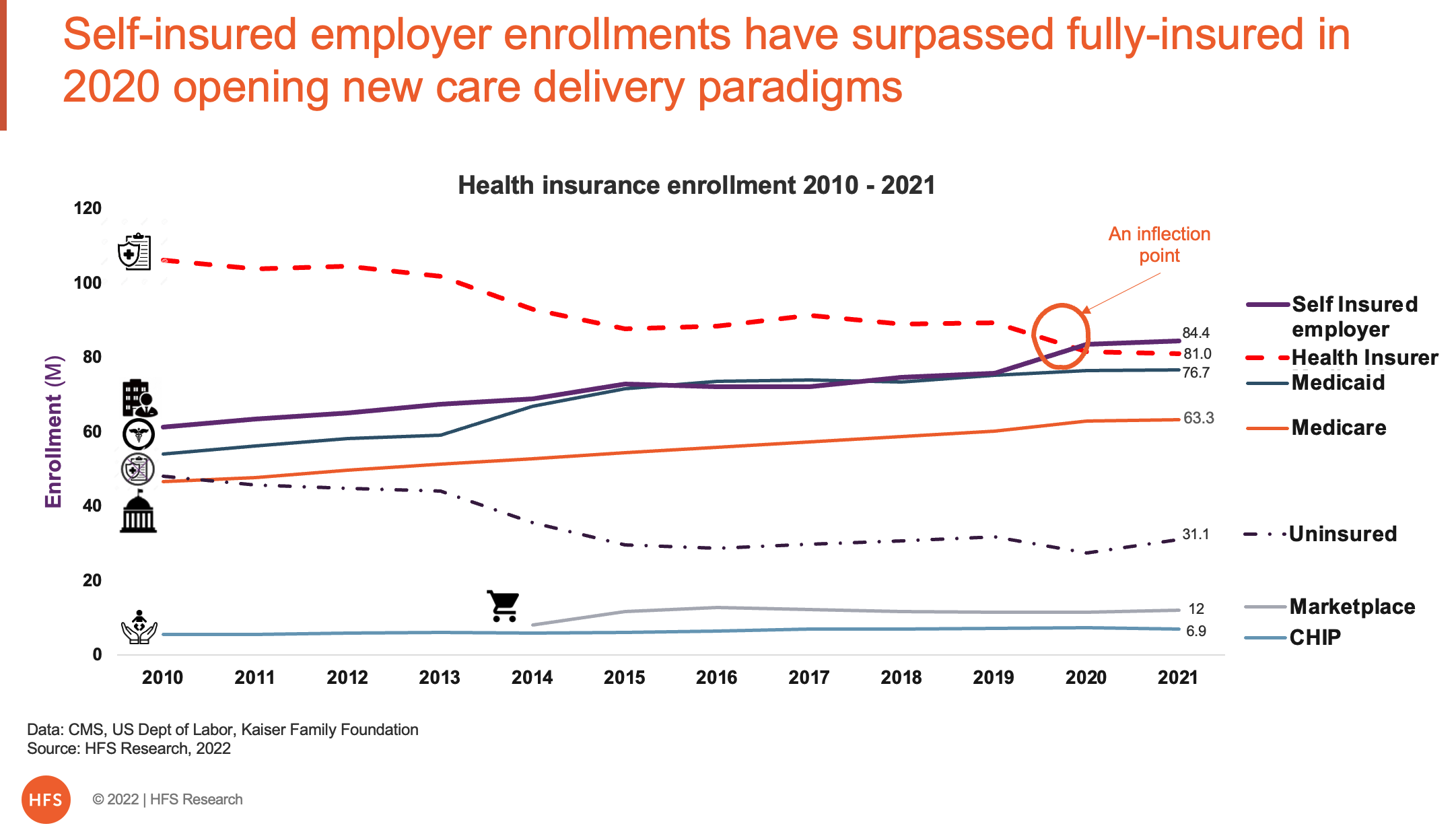

Self-insured or self-funded employers underwrite the medical risk of over 84 million of their employees and their families in the US. In 2020, self-insured enrollment by employers themselves surpassed the enrollment in health plans underwritten by health insurers, becoming the single largest market segment for healthcare. I caught up with our healthcare practice leader, Rohan Kulkarni, to learn more…

The 2020 inflection point at the start of the pandemic is a seismic event that passed off with little attention given our combined attention was on COVID-19, the economy, and yes, the 2020 US elections. Still, the growth of enrollment in self-insured employer plans holds tremendous promise of systemic change in US healthcare without the drama of national politics. It opens new opportunities for service providers, technology enablers, and consumers. It will unleash new business models, better health outcomes, and potentially address the runaway train of healthcare costs.

Health insured enrollment decline is offset by self-insured employer enrollment growth

If there’s one industry that has struggled with its identity over the past two decades, there’s no bigger culprit than Business Process Outsourcing (BPO). Ten years ago India’s IT body NASSCOM* voted among its BPO council leaders to rename itself “Business Process Management” (BPM) to amplify the nature of services being undertaken as “managed” by service providers as valued business partners, and not merely low-cost providers of outsourcing via cheap labor. However, most of the tech industry associates BPM with Business Process Management software and it’s arguable that the nomenclature only served to confuse enterprises further.

The value is in the Data. Processes provide the underlying execution to get at it

Data and processes are inextricably linked. The focus on value has shifted firmly to the strategic value of data and how designing processes can help you achieve the data outcomes that create the value. Enterprises must re-think what should be added, eliminated, and simplified across their process workflows to source this critical data. In short, enterprises want to buy continuous access to data outcomes and experience great service partnerships to achieve them. That is what BPO is all about why HFS has termed the phrase “Business Data Services”.

Despite the obvious brand identity challenge, BPM did represent the emerging era of BPO beyond cost savings (see 2010-2020 below), but after a decade, surely it’s time to revisit the very identity of business services to address the most critical need 600 of the G2000 enterprises really want… data:

Smart enterprises want to buy services that provide them with specific types of data. They care less about buying “effort”

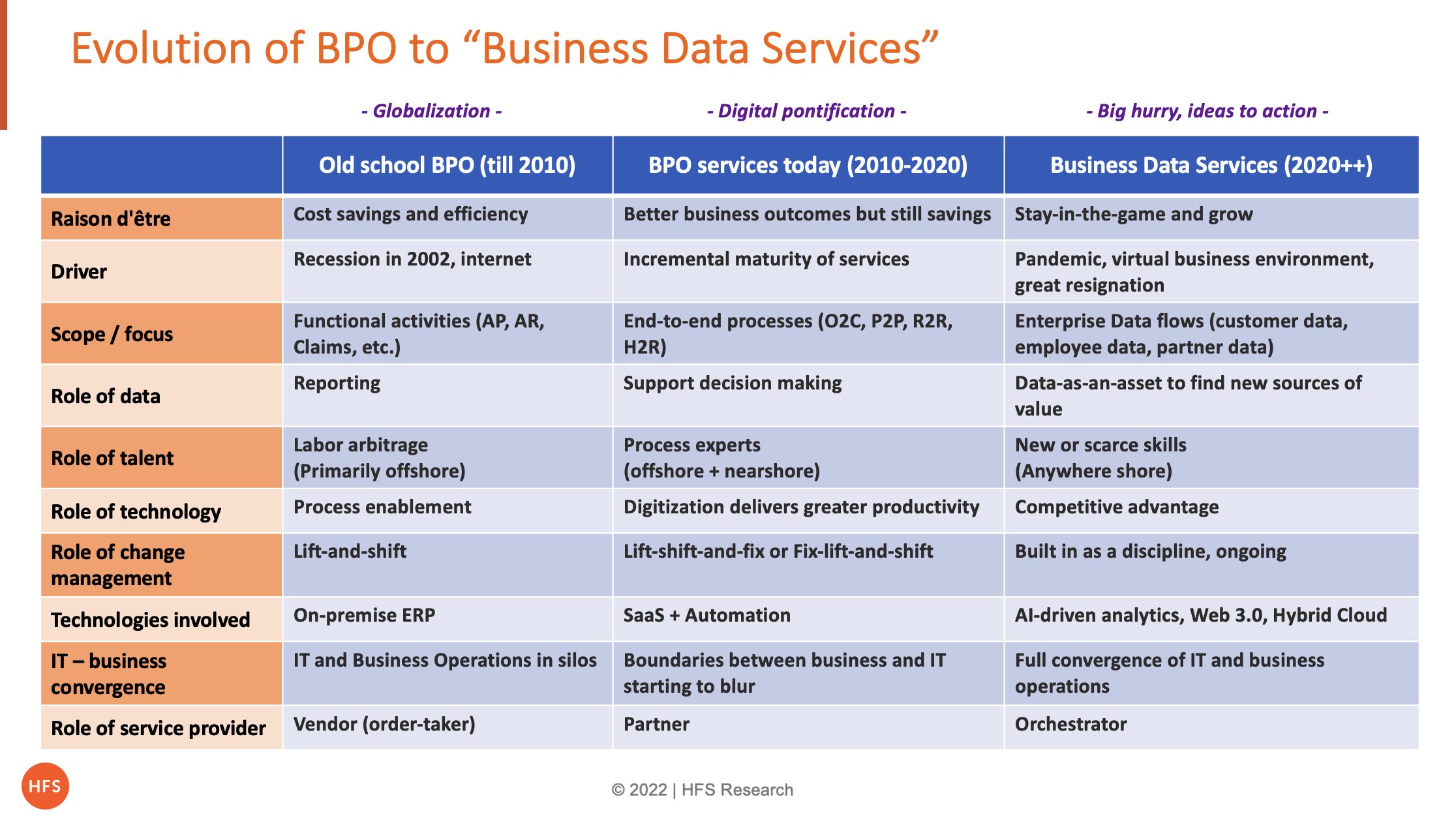

When we reflect on the phases through which BPO has evolved we can clearly identify three different eras: (1) Globalization, (2) Digital Pontification, and (3) Business Data Services:

A brief history of BPO… from ‘people and process’ to ‘data outcomes and experiences’

We can date BPO back to Adam Smith’s Wealth of Nations in 1776 where he discussed the “gains from the trade that exists in dynamic, free markets. Companies and countries that overcame the barriers to trade would reap the rewards. Those that did not overcome the barriers would forever be beholden to those that did.” He also declared that “Wealth is created through productive labor, and that self-interest motivates people to put their resources to the best use”. Was he thinking about core/non-core? Had he planted the very kernel of partnerships to drive customer impact and competitive advantage?

However, we have to fast-forward to the 1940s when ADP started handling payroll for companies outside of their own operations, and the ’60s when EDS developed an integrated system to process health insurance claims. In the ’70s and ’80s, we saw the rise of call centers first in UK and US before work was shifted to Ireland and Canada in the 1990s because of cheaper salaries and lower employment benefits. We also saw American Express, British Airways, and GE open ‘captive’ units in India to take full advantage of moving non-core work out of the main enterprise to have the work executed at a much lower cost over the medium-long term. Basically, any processes that couldn’t be tied to an ERP rollout – and executed as such – became a target for outsourcing. The advent of the Internet and real-time access to data had made many news things possible to run a virtual business that could access talent and technology anywhere in the world.

Old school BPO (pre-2010). Once the ambitious Indian entrepreneurs saw how effectively these major globals could run operations out of India, upsprung hundreds of BPO delivery firms over the next decade, with India at the heart of functional data-centric work, the Philippines becoming the epicenter of voicework. From customer services, to finance and accounting, to HR, to procurement to insurance claims processing and payment processing… the half-trillion-dollar a year BPO business was born with offshore labor at the core, and getting the work shifted as expediently as possible the hook to the eager enterprise clients.

Digital ponitification (2010-2020). This was the era where we cogitated and really saw the art of the possible. We saw the value and potential of end-to-end processes bringing employees closer to their customers aligned by common goals (OneOffice), and the blurring of the boundaries between business and technology as business executives invested in the value of SaaS and automation, helped by advancements in low-code technologies. In short, these BPO providers were making the shift from order-takers to partners. However, there needed to be a catalyst to drive the rhetoric to reality – we knew what was possible, but there wasn’t much of a burning platform for change during these years of economic growth.

Business Data Services (2020++). The collision of disruptive forces has provided the catalyst to take BPO from its pontification decade to enacting these ideas into reality: the rush to operate in a global business environment, the pandemic-induced talent crunch upping the ante to invest in an automation backbone, and providing a more challenging and rewarding work environment. Throw in spiraling inflation, a military conflict in Europe, and a desperate need from enterprises to hurry into functioning virtual models and hyperconnected supply chain ecosystems, and enterprises need more help than ever from third-party outsourcers and their armies of millions of staff to keep their businesses moving forward.

The Bottom-line: Today the onus for enterprises to buy services is to get the data they need to be effective operationally and make decisions to be competitive.

When enterprise leaders look at their operations, they need data on their people and performance, their accounts and cash flow, their spend management, their customer engagement and satisfaction, their inventory levels, their sales effectiveness, their marketing impact etc. Do ambitious business leaders really care about the effort levels being made to get this data anymore? Whether it was 150 FTEs, 50 RPA licenses, some smart AI feedback loops, and a few chatbots? Of course not. What they care about is getting the data they need to stay in the game and be successful. Having the best possible partnerships to achieve that data on an ongoing journey provides them with the ecosystem they need to be competitive.

*HFS is partnering with NASSCOM to study these dynamics of business services in-depth to shape the future of this industry

All the excesses of the past 14 years are colliding into a maelstrom of converging dynamics – the likes of which we have never experienced in such a worrying combination. The US economy is contracting and we’ll soon learn about many major economies following suit. The post-pandemic growth bubble has burst and we must open our eyes to the new reality of our business environment. Anyone who claims they can clearly visualize what the world will look like in a year simply isn’t human. Or isn’t a robot either…

Moreover, 43% of today’s US workforce is Gen-Z and Millennial and only the older Millennials may have some recollection of what it’s like to work in a contracting economy. A good tranche of today’s w0rkforce simply has no idea what’s likely to hit them in the coming months as corporate belts tighten.

My only words of comfort are that recessions rarely last more than a few quarters and we will re-emerge from this – and (hopefully) learn from this.

So how best can we prepare ourselves in the meantime?

Think twice before hopping your job

We are entering a recession and we don’t know how deep/long it will last. 8% inflation doesn’t equate to a 50% payrise, so be wary that you could find yourself in a precarious position with your new employer. The current wage-hike situation is not sustainable, and businesses struggling in a recessionary economy will have no choice but to downside/shed costly staff, and “last-in/first-out” could well apply. We are already seeing many staff seeking to return to their former employers as they quickly discover the shiny new laptop and paycheck didn’t really equate to stability and happiness. There might be a talent shortage, but when businesses struggle, they’ll look to lower their headcounts in any case. Loyalty still means something and many of those who kept the faith will be glad they did so.

Be very careful – many early-stage start-ups will fail

The champagne days of the post-pandemic start-up bubble are over. Savvy start-ups are looking to conserve cash to ride this out and come out the other side. Most mature start-ups have delayed IPO plans. Sure, they all let you work from home, but will they keep you employed in-between Netflix binges? In my view, everyone should experience the start-up thing at some point in their career, but you gotta question the wisdom of doing it right now.

Leaders must get laser-focused in the short-medium term

Spare a thought for the business leaders having to keep the wheels on their businesses with this collision of disruptive forces threatening to derail them. Employees demanding to work from home; salary demands to retain key staff; mental health of staff; cost and scarcity of people with specific skills; fractured supply chains; unscalable automation models; massive challenges to mine and manage data; broken process flows; corporate politics and executing reral change in a remote environment; customers needing immediate help; the impact of war on the European mainland… I can go on and on, but leading people in this quagmire of disruption is a huge challenge. The key is to stay focused, develop short-medium plans to keep the wheels on. Long-term planning is almost impossible amidst such business and economic uncertainty. But you can see ahead a few months to tackle these issues head-on until the fog clears.

Adjust your lifestyle for inflation

This is a huge worry for economies and our living costs, and something not experienced for decades. Inflation is one of the world economic diseases: once it kicks in it’s almost impossible to keep a lid on it, especially with broken supply chains, rising energy costs, rising food costs etc. We have to refocus on how we manage our finances and look at making real changes to our lives to compensate, such as where we live, being astute with our energy consumption, cutting back on overpriced food (learn to cook?), and saving more money for the future as this could get worse – or investing our money in things that hold their value in line with economic fluctuations.

Bottom-line: We must recognize these are highly abnormal times and grind through them.

We’ve got pretty used to tackling uncertainty since March 2020, and one thing is clear today – the only certainty is that these times are uncertain. It’s a shame that we have to face up to a global recession just as we are enjoying seeing colleagues and clients again, but things need to cool off and economies need to return to normal. My hope is that we – as people and workers – become a little bit less selfish, and a little bit more appreciative of working in the technology industry which is essential for the very continuity of business. If everyone’s simply out for themselves, this isn’t going to end well for many people and many organizations. We need to be better collaborators, better empathizers, and better communicators if we are to pull through the next few months and come out the other side on top.