The world of enterprise innovation has changed dramatically since pre-pandemic days, and we – at HFS – have redefined how we evaluate service providers and tech suppliers to reflect the value ambitious enterprises are demanding in today’s business environment.

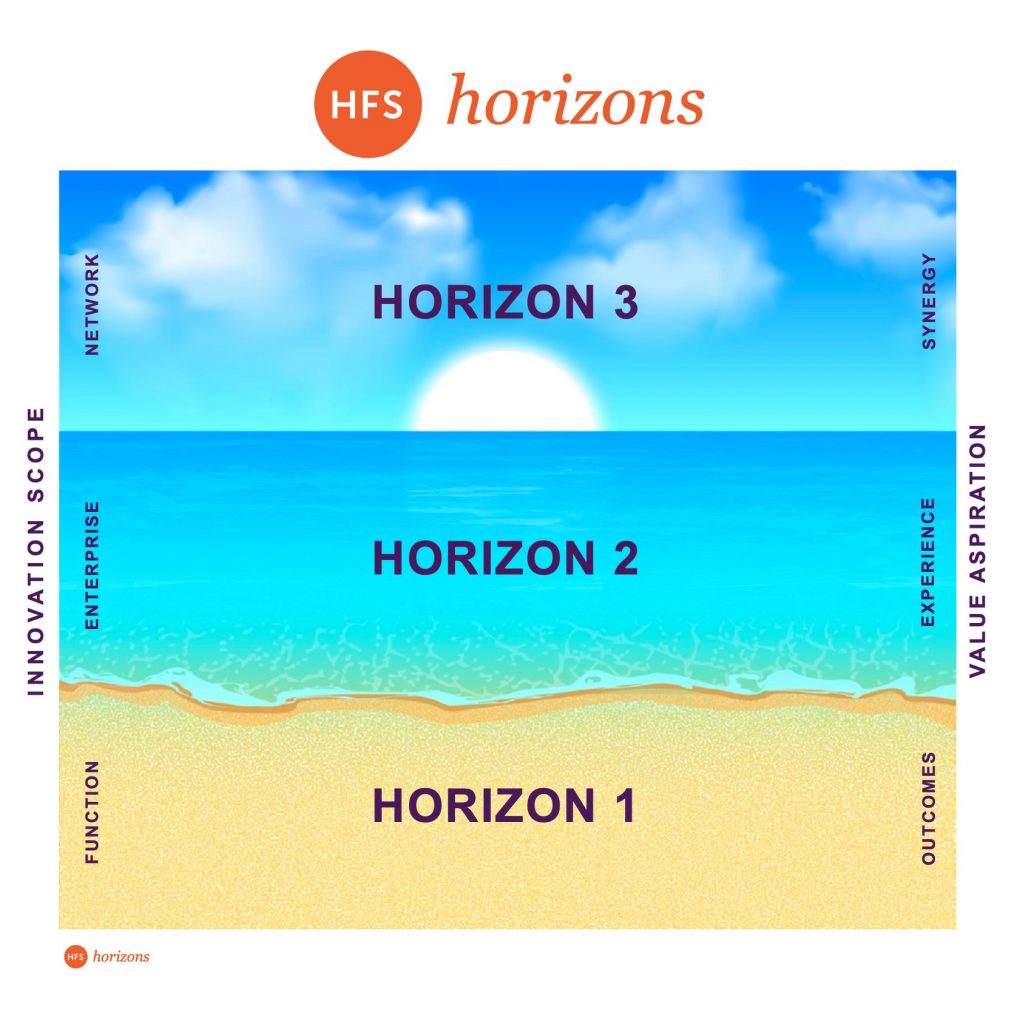

Today, we’re officially launching “HFS Horizons’ to align the performance of today’s service providers and tech suppliers with the outcomes they help their clients define, the great experiences their clients enjoy, and the synergies their clients are developing across their ecosystem partners to create new sources of value:

So why is it time to phase out the HFS Top 10?

When we introduced the famous HFS Top 10 over four years ago, the whole purpose was for our analysts to put a stake in the ground and produce something relevant to support enterprise decision-making. We wanted to differentiate HFS from our competitors by producing a relevant decision-making support tool for enterprise leaders, not marketing fodder for vendor press releases.

Fast-forward four years, and the analyst industry hasn’t changed a bit – we are still subjected to Magic Quadrants, Waves, and Peaks developed solely for the paid inclusion in supplier sales decks and press releases. While some are pretty decent, there are so many that miss key suppliers, lack the integrity of customer references (if they do any at all), and are scored largely on how well the vendor wows them in a briefing and at their fancy conferences.

Moreover, by lumping so many suppliers into the top right of their charts, the analyst has essentially made many of them “winners” to make it easier to sell more licenses to eager marketers. As a result, the HFS Top Ten has become hugely popular as the one decision tool that enterprise buyers really trust to access deep profiles of suppliers across many dimensions of innovation, execution, voice of the customer, and OneOffice alignment.

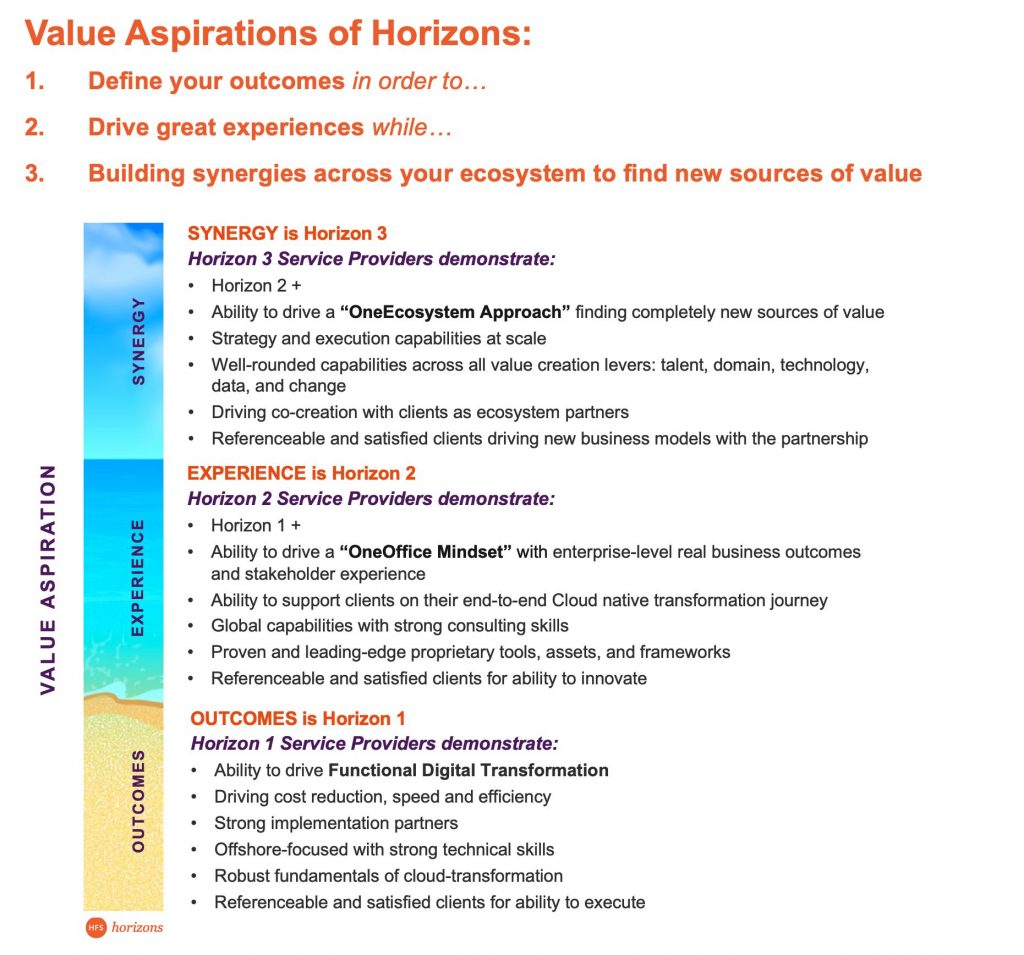

However, like all good things, we need to evolve with the times, and while we want to build on the integrity and depth of the Top Ten research, we strongly feel it is time to align supplier performance across the three horizons of innovation: Outcomes, Experiences and Synergy:

While the rest of the analyst industry persists in looking in the rearview mirror at the world, we’re determined to keep looking forward

We need to stay true to our reputation of being unafraid to challenge and disrupt ourselves and keep looking forward. The best time to retire a product is when it is successful!

So how will Horizons reports work?

HFS Horizons reports will be completely aligned with our vision for enterprise innovation and will paint the supplier landscape across:

Horizon 1: Outcomes (based on functional digital transformation)

Horizon 2: Experiences (based on a OneOffice mindset)

Horizon 3: Synergy (based on a OneEcosystem approach)

Instead of ranking based on execution, innovation, and customer satisfaction; we will be evaluating suppliers based on the “Why, What, How, and So What” of enterprise innovation:

Why? – The value proposition

What? – The solutions and capabilities

How? – The Go-to-Market strategy and investments

So What? – The market impact in terms of mindshare and wallet share

While customer feedback will continue to be a critical ingredient for Horizonsassessment, we will also expand our data sources to understand employee experience and partner experience. HFS will invest and rely on its own proprietary data sources more heavily versus supplier-provided information

Beyond supplier-provided client references, we will survey relevant clients in our own network leveraging HFS Pulse

We will also reach out to employees directly (and anonymously) to understand their perceptions on their employers

In addition to client references, we will also ask for partner references

The HFS Horizons reports will be governed by an agile research process:

No laborious RFI responses. The value is in conversations. Essential data requirements will be shared as an appendix to the briefings

Customer references are recommended but not mandatory. We have in-depth network of clients who are willing to talk to us to provide unvarnished feedback

There is no opt-out. Sharing information and briefings with analysts is helpful and recommended, but we will leverage our network to assess suppliers.

HFS Horizons report will also allow us to be more inclusive where there are 20+ suppliers in a market

If you have questions on the new HFS Horizons reports and how you can get included, please email [email protected]

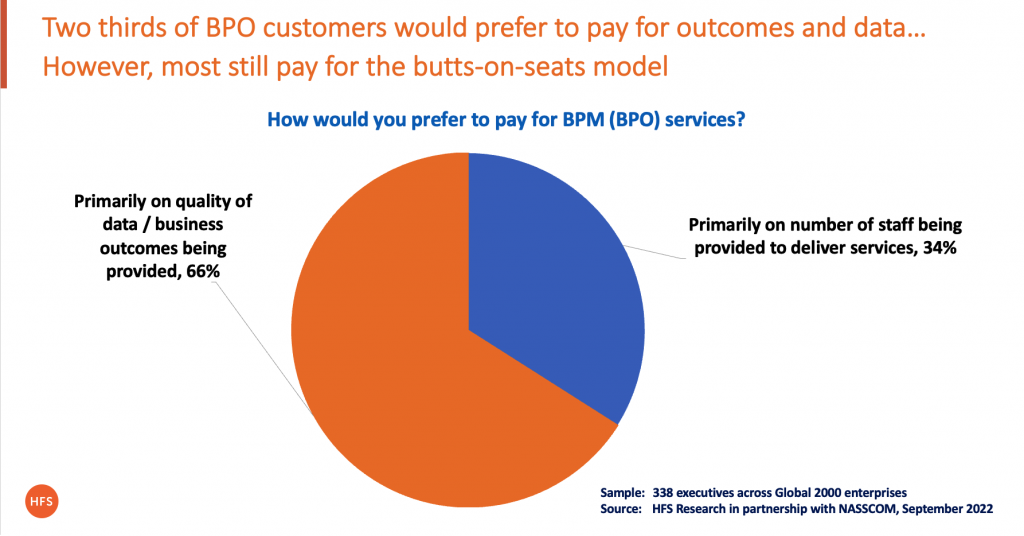

Today’s current “effort-based” BPO (BPM) services model is failing, but there is hope that this industry can course-correct its outmoded ways of behaving, with two-thirds of enterprise leaders preferring an outcome-based approach. Here’s why:

The economics of the current services model are capitulating

About 90% of business process outsourcing engagements are still largely priced and valued on low-cost labor. Moreover, that labor is becoming increasingly costly as inflation deeply kicks in and the talent supply drains away – especially at the lower-income levels. Service providers will walk away from many of their clients as they simply can’t make the numbers work to deliver their contracted services effectively and profitably. It’s becoming a painful race to the bottom… a zero-sum game that could see the BPO industry rapidly consolidate – and even shrink – if enterprises and their service partners cannot change how they engage with each other.

Our new research, which we will be presenting at the NASSCOM’s Business Process Innovation Showcase next month (see details), is revealing an industry primed for some fundamental changes as the current “effort-based” model becomes more and more misaligned for clients seeking better data, better performance, and much more dynamic partnerships to help them operate effectively in the current climate:

The purposes of client and provider must be aligned, or the relationship ultimately fails

When engagements are priced on the number of people, there is very little incentive to explore new methods of creating value, such as automation, AI, quality data, etc. The service provider is incentivized to maintain/increase the staffing levels, not invest in programs to reduce manual dependencies. Enterprises need to pay for performance, not effort if they ultimately want to benefit from sharing a common purpose with their provider. Net-net enterprises and their service partners must be motivated to achieve the same goals if they want to enjoy a long-term, mutually beneficial relationship.

Why legacy many services engagements become bad business deals

So what incentive does the provider have to become more effort-efficient if they will be penalized financially? The short answer is that there is no incentive, which is why many services engagements move to different service providers when contracts end. In most cases, it’s preferable for the incumbent provider to lose the business rather than cannibalize its own revenues with that client.

The sad reality is that the enterprise client just lost a service partner which has years of experience running their institutional processes – which could probably have automated the crap out of them and delivered a game-changing scenario. But they just had no financial incentive to do so. So the cycle continues, and that same client has to go through the same dog-and-pony show with another provider for the next 5-10 years. They still have the same crappy operations that will remain crappy with another partner, which also has little incentive but to deliver the same crap to maintain the effort levels as bloated as possible, to keep the business as profitable for themselves.

So what needs to change to get the focus on value versus effort?

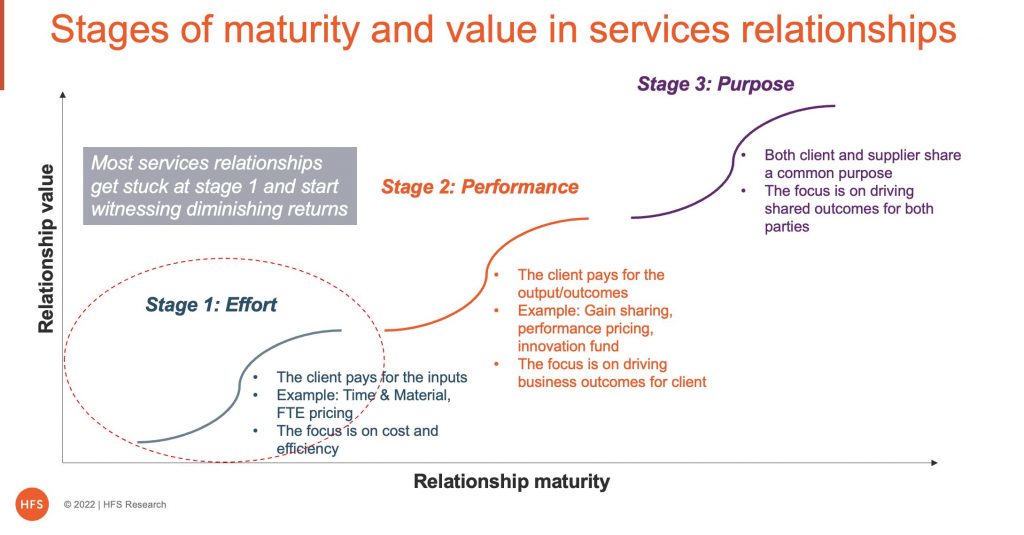

Clients and suppliers need to jump to a new S-curve of value creation where the client pays for the performance, not just the effort (See Exhibit below). Performance should be measured based on some attribute of business value, not just cost and efficiency. Business value can be defined in terms of working capital optimization, speed-to-market, improvement in business metrics (e.g., DSO or DPO), customer/employee satisfaction (e.g., NPS score), or procurement spend reduction.

Most services relationships get stuck at stage 1 and start witnessing diminishing returns because you just cannot keep squeezing the lemon for more juice. In a performance-driven relationship, the supplier and client share the risk and reward while providing services at the lowest cost possible starts to become a given.

Most sourcing advisory consultants describe a gain-sharing approach at this stage, but be careful as gain-sharing can drive opposite behavior than initially envisaged. A “pay-for-performance” pricing is often more practical. This is how it works:

Identify the desired outcome for a potential relationship by milestone

Supplier proposes fixed service fees to implement milestone

X% of Supplier fixed fees “at risk” for non-performance

Supplier earns a “performance bonus” (up to Y% of fixed fees) if it exceeds project Savings Target

This pay-for-performance pricing is simple, transparent, and mutually beneficial as the service provider is incentivized to create value, it is relatively straightforward to track and measure, and the buyer payouts cannot be so huge that they can cause budgetary issues.

A gain share model backed with an “innovation fund” is also a better idea than pure gain sharing. Here the supplier (and buyer) commits to a pool of money to drive innovation. A joint innovation council identifies potential projects and uses the innovation fund. The supplier recovers its investment using a gain-share approach with a potential upside if the project is a huge success and a downside if it fails.

Finding a common purpose in a relationship can convert it into a growth engine for both parties

The most mature relationships are not based on math on some complex savings calculations but on a shared drive or goal (see stage 3 above). This is where co-creation happens. When combined with the supplier’s experience and technology, the buyer’s data and real-life business context create a unique solution that can be taken to the market jointly, with both parties sharing the potential windfall. Suppliers struggle to develop innovative solutions in a vacuum, and co-creation allows buyers to drive the partnership toward revenue creation. Purpose-driven associations rely on each other’s strengths to build a strategic, mutually beneficial relationship. A recent example is where bp and Microsoft formed a strategic partnership to drive digital energy innovation and advance net zero goals. Microsoft would further bp’s digital transformation with Azure, while bp would supply Microsoft with renewable energy to help meet the company’s 2025 renewable energy goals.

Bottomline: There is no pricing nirvana in IT and business services. But pricing structures should evolve as the relationship matures from effort to performance to purpose

Each pricing structure – input or effort based (e.g., FTE-based), output-based (e.g., price per transaction processed), or outcome-based (e.g., gain sharing, pay-for-performance, innovation fund) has its pros and cons. It generally makes sense to start a new relationship with some effort-based pricing to establish the baselines and build trust, but then it is time to move on to pay for value.

Where we are seeing most progress toward performance-based relationships is when the CEO gets involved to learn the nuances and value of moving towards areas of common purpose that can also involve other entities in that industry ecosystem. The challenge for service providers is to have leaders capable of developing C-suite relationships and changing that age-old master-servant conversation to one of common purpose to create mutual value.

In the past, spending our weekdays in the workplace entailed sacrificing our time in exchange for food and shelter. Now, many people want to “work” and not sacrifice anything.

We’ve talked about this virtual work environment thing to death for the past couple of years. Literally to the point where I can’t take another person sounding off about “empathy” and “flexibility”… oh god, put another record on, puh-lease.

There has to be a balance in the workplace

Yes, we need to create environments where managers invest time with their people to understand them, motivate them, and show they care about them. And staff reciprocate by appreciating more flexibility on the job to focus on family needs/lifestyle etc. (see earlier blog). But at some point, there is a line to cross between giving staff flexibility and essentially allowing them to “work” when they want. The problem many organizations are now facing is teams of disengaged and “burned out” employees who struggle to identify with their jobs and think it’s OK to work when they can be bothered.

Motivation is on the wane, and burnout is to blame.

We’ve been talking about “burnout” on the job for years before the pandemic, and the cure was normally to delegate more, take a break, even go to the gym / find an outlet for stress, etc. Today, most people are claiming they are burned out; however, the reasons are more than being stuck at home staring into a screen all day while enduring soul-crushing video meetings where they’re trying to multitask and appear engaged. Yes, that is burnout behavior, and we need to get smarter about the incredible time wastage having half these meetings, but the real reason is the shear multitude of worrying events happening to us that are destabilizing our lives… inflation, recession, job security, energy crises, the climate crisis, extreme, irrational politics, ongoing war, etc. Yes, we are living in a world where we’re all burning out by the sheer instability and misery emanating all around us.

What is essentially happening in many organizations right now is a breakdown of the very fabric of a company… what it means to belong and spend most of your working week with your colleagues and customers. Many people I am engaging with these days are simply disengaging from their companies. They are literally having a handful of in-person meetings with a select bunch of colleagues over the course of many, many months. They are trying to keep the threads of connectedness going, but the reality is they are drifting further and further apart.

The Bottom-line: With all the instability in the world, the workplace must become a place where we can focus on positive things and engage with each other like we used to

In pre-pandemic days, your job was an important part of your life, and the people around you mattered. Work mattered, and performing well really meant something. Today, many people are withdrawing from engaging with their colleagues. Many are producing the bare minimum to stay relevant in the workplace.

With such a global assault on the stability of our lives, shouldn’t this be a time when we find some solace with our colleagues? Isn’t this a time when our bosses and colleagues are people with whom we can share our concerns and find some comfort in working together? Because the more we distance ourselves from our workplace, the more we are cutting off a valuable place that can help us through these challenging times.

Employers have no choice but to re-engage their workforce by any means possible. This means managers set the example, going into the office at least two days a week and demanding their staff follow suit. This means companies getting tougher with employees who are simply underperforming… especially when other staff sees their colleagues getting away with coasting, as many will follow suit. Sure, we all got a free pass during the pandemic, but those days are long in the past, and organizations must refocus on being meritocracies.

While it’s easy to point the finger at this coasting culture, the major reason behind this hybrid work failure is poor management. Far too many mediocre managers out there haven’t adapted to the remote environment and are simply failing to approach the job differently to be effective. Good managers are driving better collaboration across colleagues, encouraging more in-person sessions, investing in technologies like whiteboarding and smart meetings that really help collaboration, investing time in social activities that promote staff bonding etc. It is no surprise to me that so many staff are disengaged because they do not have mature, motivated leadership to give them direction and motivation.

There has never been a time like this where the very nature of doing a good job is under threat. Companies settling for mediocrity are going to face a huge struggle trying to get their mojo back in the future. It’s not OK to be meh… it really isn’t.

One IT services provider delivering superlative performance in recent years is Capgemini, recording over 20% revenue growth in the first half of this year while also enjoying growth in operating margins, despite all the inflationary pressures and high attrition across the industry.

As it approaches its $20bn revenue milestone, it’s high time we caught up with Group CEO Aiman Ezzat to understand what’s driving this growth since he took the helm over two years ago…

Phil Fersht, CEO HFS Research: So I’ll dive straight into this, Aiman. Did you always want to be a CEO of a €20 billion services giant? Was this what you always wanted to do when you started out?

Aiman Ezzat, CEO Capgemini Group: I’ve been with Capgemini almost 27 years now, Phil. I am a chemical engineer, but I started my career with IBM in the mid-80s, IBM Europe, actually. I stayed there for a few years and then went to do an MBA at UCLA. After that, I was curious about consulting, so I joined what was called the Mac Group, at the time, which was a strategy consulting boutique which was created by Harvard professors, and as I joined, this company got acquired by Capgemini to create what was, at the time, called Gemini Consulting, which was a transformation consulting arm of Capgemini. I stayed there for nine years, half of the time in Europe, and half of the time in the US, I was based on the West Coast. I left in 2000 to join a smaller firm that was supposed to go public, it never happened. I stayed there for four years. At the end I was running the non-US business; I was based in D.C., but running Europe and Asia. I left in 2004 to come back to Capgemini.

My career restarted in Capgemini, after that four years’ divergence, I was first in group strategy, I was Deputy Director of Strategy, I did a lot of the transformation programmes, I did a lot of the acquisitions. And I moved to help one of the acquisitions, which was Kanbay, to help create our global financial services P&L. I joined as COO, and after one year, I became the CEO of that business, to make it a global business for Capgemini. That was 2007, and I became CEO of our financial services entity on the 1st of January 2009, perfect timing to see the financial market crash. This was an interesting experience, of course. At the end of 2012, I became the CFO of the group, I stayed CFO until mid-2018. In the meantime, I was chosen as being one of the two people to potentially become the successor for Paul Hermelin, so I also became COO. And then you know the rest. In September 2019, I was confirmed as being the next CEO, and I became CEO on 20th of May 2020. So that’s kind of my career, very, very Capgemini, but very diverse in Capgemini, as well, because I touch a lot of things, strategy, operations, finance.

Have I always dreamed of becoming a CEO? No. There are some people who, when they are 18, they want to become a CEO. Me, I wanted to do interesting things in life. So I followed my career, from one thing to the other, always trying to find a way to be able to add value and learn something. I was quite successful in the CFO role, I was chosen to be one of the two potential people to succeed Paul, and it was only then that I realized that I could potentially become the CEO of Capgemini. That’s kind of how my career went. So I’m not a big power guy; I was interested in taking the CEO job because I had ideas about what I could bring to the group. This is it. When you take the CEO job, it’s for that. It’s not for power; it’s because you have a vision, and you see that you can add value, and see what you can bring.

Phil:So who have been your influences along the way that you can share, maybe some personal and professional ones, Aiman?

Aiman: There are a few things that marked (ph 05.28) me through my career. When I was younger, I was interested in strategy and did a lot of reading, one the persons that influenced me was C.K. Prahalad with Strategic Intent and Core Competencies, that was early 90’s. In the late 90s, one guy that influenced in terms of thinking was Chan Kim, who is a professor at INSEAD, who with Renée Mauborgne wrote a piece called Value Innovation and Fair Process, and then went on later to write Blue Ocean Strategy. That influenced me in terms of how you need to focus on the client, and how to create value for the client; moving away a bit from the notion of competitive advantage, and much more around value creation being focused on the client. This influenced me, in terms of thinking.

In terms of people, you look at a lot of people, you learn from a lot of people, I cannot say I have one role model. But someone that impressed me, in terms of what he did, is Steve Jobs. He was passionate, he had a vision, and people could tell him whatever they want, they didn’t necessarily agree with him, but he was convinced about what he wanted to achieve. He created a lot of value. That’s someone I like, in terms of personality, in terms of his commitment to achieving something, his vision., He drove it all the way to the end.

Phil:Yeah. I love watching some of his old videos, including when he launched the iPhone, he could accurately see 15 years into the future. It’s incredible if you watch that 2007 launch.

Aiman: Exactly.

Phil:But when he relaunched the Apple brand, he was all about experiences, not products. It’s like when you watch Nike commercials, you don’t see products being sold, do you? You see athletes, you see health, you see what this brand stands for. And I think he brought that into the consumerization of IT, which is fascinating… he really did change the industry.

So Capgemini has grown a lot over the years, and with a lot of M&A… you’ve done a lot of acquisitions as a business. But I feel that one of the defining acquisitions you’ve made is Altran. You’ve built this unique OT/IT focus, it gets you really heavily into supply chain, and engineering, and sustainability. One, do you agree with this? And two, how do you see Capgemini’s DNA today, as you hit this €20 billion milestone?

Aiman: Yes, it definitely was defining, Phil! I think some others in the history of Capgemini were defining in different ways. There were many geographic expansions in Europe: Hoskyns got us in the UK, Volmac got us in the Netherlands, and Programator in Sweden. So a lot of the expansion was geographic, a lot of the expansion was around getting us into new territories. We changed a little bit, after that. The Kanbay one was really around India, and how to learn the India model, and the one-team model, etc., so we had to move from a western model, to a much more Indian integrated model. IGATE was about scaling in the US. But yes, the Altran one was defining in terms of it was probably one of the more strategic ones, because this one was really around a vision we had around the concept of intelligent industry, and how the convergence between the digital and physical worlds is going to happen, and the need to be able to have people really understand the physical world, to be able to create that value around intelligent industry.

So I fully agree that this is definitely something defining, in terms of Capgemini’s evolution, in terms of strategy, as well. It’s about a space that was being created in the market. People bring it to Industry 4.0, and the concept of intelligent industry goes beyond that. Because it’s not just about digital manufacturing and intelligent supply chain, but it’s also about the creation of the new products and services of the future, and their platforms. A car now becomes an intelligent product, full of software, and it needs to run on a cloud platform. So it’s not just how we manufacture the car, and the supply chain that goes with it; it’s how we create, how we conceive the car.

And this is where the understanding of the physical world becomes important. If you think about it… look at the financial services industry. What was specific in financial services, compared to other industries, from an IT perspective, is that it was already in the product and the service. A credit card is made out of IT. A bond, an equity, a payment system is made out of IT. In most other industries, IT was not in the product or in the service. IT was not in the car. And suddenly, IT comes into the car. And what was specific in financial services is that you moved out of the horizontal needs. You were not in finance, in HR, etc. Of course, you could do that. But when you talk to the business, when you talk about credit card, you need to understand the credit card business. You cannot develop products or functionalities for a credit card if you don’t understand the credit card business. And when it comes to a car, it’s exactly the same thing. You cannot develop the software architecture of a car if you don’t understand how a car operates, or what a car is made of.

And that’s really what we got through Altran. We had people who knew how to build cars, how to build planes, understand how a factory operates, understand the pharma companies, in terms of 3D manufacturing, and engineering, and R&D. And when you bring that with digital, that’s really when you are able to give birth to the intelligent industry concept, which, as I said, goes beyond the digital manufacturing and intelligent supply chain.

Phil:As we get into manufacturing and supply chain, the role of providers with sustainability becomes much more relevant, doesn’t it?

Aiman:Sure, Phil. When we look at sustainability –we are pretty big on sustainability – there is, of course, the internal part. We are doing the job, but we are a service firm, we are not a big emitter. A lot of it is linked to business travel; you reduce business travel, your footprint goes down quite a bit. realizedTechnology, digital and data have a big role to play, in terms of helping to drive sustainability solutions. So we made a commitment to help our clients reduce their carbon footprint by 10 million tonnes of CO2 by 2030. Following that commitment, we started developing an offering architecture around focused on “How can we make this happen? What value-add can we bring to our clients?” So, of course, there is the strategy. How do you get to net zero? What are the levers, depending on your industry, that you can act on, to be able to get to net zero? (? 13.17) That’s the business consulting, the strategy consulting part, you need an industry understanding, understand the levers that people can use, energy efficiency, or others depending on their industry. And from there, you can say, “Okay, these are the levers, this is how you can get there, this is how you can do the saving, this is what you need to change, these are the technologies that are available to you to do it.”

At the other end, you have one of the most complex parts, which is measurement and monitoring. On one side, you have to be able to measure the carbon footprint, and I think that’s an area where we evolved, we’re working with a number of technology partners around developing calculators, and other tools, and measurement, including on the procurement side. On the other side, you have the monitoring; how do you monitor the evolution of your carbon footprint? And in the middle, I call it the doing part. The doing part has three legs, for us. It’s green IT, or sustainable IT. We are definitely in that business, we help our clients reduce their technology footprint. The second part is sustainable operations, that’s really by industry. We’ll not cover all industries, because it’s very industry specific. There are things that are common, like energy efficiency, and energy transition that you can work on, but there are things that are very industry specific, and there you really have to go to the heart of the industry to understand what levers you can use. And here again, the engineering capabilities are important. And the third leg is sustainable products and services. We work on helping clients redesign a gearbox to reduce its size, and also the materials to make it lighter in order to reduce the carbon footprint. We worked with a forklift manufacturer for a completely redesigned forklift in order to reduce the carbon footprint over the lifecycle. This is the doing part. It’s the sustainable IT, it’s sustainable operations, and it’s helping clients to redesign their products and services to make them more sustainable, with the monitoring and measurement and, of course, the strategy part. We are starting to do a lot of projects, it’s really taking off, and I do believe that it’s going to become a big business.

And one other positive thing about this, besides being good for the planet, is that it’s a talent magnet. Young people love to work on these projects.

Phil:And in that vein, I know you’ve mentioned this is a long-term change in the way that we’re approaching talent and work. Can you share a bit more about your thinking here, Aiman?

Aiman:There are two different things happening at the same time, Phil. On one side, a big shortage of technology talent, because we are moving to a digital economy. Companies are impacted across the value chain, and they all need technology talent. Whether you are talking about your customer relationship, how you manage your company, how you design your products, how you manufacture them, or how you move them through the supply chain, so the whole value chain now requires technology, not just the management of the business. This has significantly expanded the demand for technology capability in most companies… in the economy overall., Technology spend is becoming a bigger part of the economy, , and to be able to fuel that, you need more talent. That talent does not exist. The growth of demand is far too fast. We have a big imbalance between supply and demand of talent. That’s one side.

The second side is the evolution of the new generation, Gen Z, which is coming with different expectations, and the whole evolution of the workforce, and the model of working, coming from hybrid. You have to combine the two, the two are happening at the same time, and you need to deal with the two. First, there is definitely the reskilling of talent, and we have done a huge reskilling of talent internally and we are also helping our clients reskill talent. Going beyond reskilling, we take people with no technology background and train them. We work with universities to develop new curriculums. We even tried to influence a bit some of the governments, saying “We need to think differently. The technology talent is not just engineers.” Otherwise we’ll never have enough talent. You need people who can do coding. They don’t need to do five years of engineering to write code. We can train people, if they have the right math background or logic to write code, we can train them in 12 to 18 months, or 24 months. We need to find a way to diversify the education model, to be able to bring more people up to speed to fuel that digital economy.

So upskillingbut also the creation of new talent is important. That’s why we hire a lot more young people, train them, sometimes people with no technology background.In our industry, we are big employers in terms of tech; with all our large competitors, we are the ones who can really train massive amounts of people, and fuel these people into the economy, going to startups, to other tech firms, to our clients. This creates attrition, because of the imbalance between supply and demand, you cannot do anything about it. That attrition is coming because the demand for talent is so high. You have to learn to live with it, for the time being, until we come to a more balanced environment in terms of supply and demand. Attrition will probably remain high for a while. It will probably come down a little bit, quarter after quarter, as this imbalance gets reduced.

The second part is the whole evolution of the interaction between employees and the firm, but even going beyond that, it’s people who you want to associate to what you do, who are not necessarily going to be your employees. That’s why I talk more and more about the talent ecosystem. First, there is, of course, your employees, and here people join because of your purpose, because of what you are trying to do, because of the interest of work, because you care for them, the whole people experience becomes important, the whole trusted work culture becomes important. The leadership model has to evolve. You have a generation that doesn’t want to be told what to do, but wants to be given a direction, be motivated, be cared for, and have some freedom in how they get things done. Which is quite different. . So it’s much more an alignment, and a leadership model, than it is a management model. I’m going a bit from one extreme to the other, it’s somewhere in the middle, but there is an evolution in the way you have to lead, with all this generation, if you want people to stay with you.

And the realisation, as well, that the workforce is going to become more fluid, people move easily from one company to another, you have to learn to live with that. The fluidity of the workforce will increase, and it’s a fact. We will not go back to where we were pre COVID, where people will stay for a long time in companies. You definitely need your core of employees, of people who stay longer, but you’re also going to have people moving faster. Which means that you need to start to learn to live with what I call a talent ecosystem, which is not only your employees, but also people that go beyond your employees, gig workers, potentially people who have retired, potentially students, people who only want to work three or six months a year. All this is an ecosystem of talent. They are not employees. But I put a very important concept in that; that you need to identify them. It’s a bit like personalised marketing. I can work with them, if I know who they are, because I know when to call on them, and they might or might not be available. In a certain way, I need to identify them, I need to get to know them. And maybe I get to know them because I am certifying them. I give them a Capgemini certification, they have been trained by me, and they can go and valorise that certification somewhere else. By doing that, I also get to know them, and I can ping them when I need. It’s at will. But having identified a much larger pool of talent, which goes beyond my own employees, I can be in touch with them, and associate them with my work.

So it’s really an evolution, the foundation is going to be your employees, but you enlarge it with an ecosystem of talent that you know, and to whom you are connected.We can really make it happen.

Phil:My final question, just a quick one, is how are your feelings about the future, when we look at the chaotic times we’re in with geopolitics, and inflation, and things like that? Are you feeling slightly positive? Are you feeling negative?

Aiman: Of course, like everybody, Phil, we are closely monitoring the situation. There are a lot of complexities today between geopolitics, inflation, and the big evolution in terms of what’s happening in the economy: we cannot be ignoring it. On the other side, I am optimistic, because the fundamental trends, the structural trends are positive. In the past it was the Industrial Revolution, now this is the Digital Revolution. Everything is moving on a technology platform, on a cloud platform, we’re going to have a lot of new digital services, we’re going to be able to use quantum computing to discover new drugs. So there’s plenty of positive trends. As an industry, we are in the middle of that, we are in the middle of the transformation of business and society. I can only be positive about the structural trends, being part of digital transformation, being part of inventing new products and services, being part of inventing new public services, being part of enhancing people’s lives, being part of finding solutions to sustainability. I am very positive about the fact that we are creating a digital economy. Structurally, the long-term trends are good. In the short term, we have to monitor closely what is happening, and learn to be agile and adapt to what’s going on in the market.

Phil:Well, thanks for your time, this has been really insightful, I look forward to sharing this with everybody… it was great getting some time with you today, Aiman.

We’ve been covering IT and business services for over 20 years, and it’s still sold and bought the same way: enterprises pay for effort, and providers sell effort. However, the current “effort-based” model has become unsustainable in today’s climate for two reasons:

1. The economics of the current services model is failing

It is based on low-cost labor, and that labor is not so cheap anymore… or available. Service providers will walk away from this business as they simply can’t make the numbers work to deliver it effectively and profitably. It’s becoming a painful race to the bottom.

2. When the purposes of client and provider are not aligned, the relationship ultimately fails

When engagements are priced on the number of people, there is very little incentive to explore new methods of creating value, such as automation, AI, quality data etc. The service provider is incentivized to maintain/increase the staffing levels, not invest in programs to reduce manual dependencies. Enterprises need to pay for performance, not effort, if they ultimately want to benefit from sharing a common purpose with their provider. Net-net, enterprises and their service partners must be motivated to achieve the same goals if they want to enjoy a long-term, mutually beneficial relationship.

Why so many services engagements become bad business deals

So what incentive does the provider have to become more effort-efficient if they will be penalized financially? The short answer is that there is no incentive, which is why many services engagements move to different service providers when contracts end. In most cases, it’s preferable for the incumbent provider to lose the business rather than cannibalize its own revenues with that client.

The sad reality is that the enterprise client just lost a service partner which has years of experience running their institutional processes – which could probably have automated the crap out of them and delivered a game-changing scenario. But they just had no financial incentive to do so. So the cycle continues, and that same client has to go through the same dog-and-pony show with another provider for the next 5-10 years. They still have the same crappy operations that will remain crappy with another partner, which also has little incentive but to deliver the same crap to maintain the effort levels as bloated as possible, to keep the business as profitable for themselves.

The legacy services industry perpetuates mediocrity and is playing a zero-sum game

The even sadder reality is that the whole services industry has become a vehicle to run the same crappy processes for the same tired old clients – with as many staff as they can get away with – to eke as much profit as they can.

And the despairing, even sadder reality is that this industry has become a vehicle to move this litany of terrible antiquate processes – many of which originated after the second world war – into the cloud, where enterprises can spend a fortune operating with as much mediocrity as they did before.

The problems start when enterprise clients become increasingly uncompetitive because they drive Teslas with knackered old gas engines. Simply moving your mess for less to the next services provider willing to spin its 20% margin over the top is a zero-sum game. The clients will struggle to get the data they need to compete effectively with companies with much more digitally native front-to-back processes. And when the clients start to fail, so will their services partners feeding off the inefficiency.

So what needs to change to get the focus on value versus effort?

Clients and suppliers need to jump to a new S-curve of value creation where the client pays for the performance, not just the effort (See Exhibit below). Performance should be measured based on some attribute of business value, not just cost and efficiency. Business value can be defined in terms of working capital optimization, speed-to-market, improvement in business metrics (e.g., DSO or DPO), customer/employee satisfaction (e.g., NPS score), or procurement spend reduction.

Most services relationships get stuck at stage 1 and start witnessing diminishing returns because you just cannot keep squeezing the lemon for more juice. In a performance-driven relationship, the supplier and client share the risk and reward while providing services at the lowest cost possible starts to become a given.

Most sourcing advisory consultants describe a gain-sharing approach at this stage, but be careful as gain-sharing can drive opposite behavior than initially envisaged. A “pay-for-performance” pricing is often more practical. This is how it works:

Identify the desired outcome for a potential relationship by milestone

Supplier proposes fixed service fees to implement milestone

X% of Supplier fixed fees “at risk” for non-performance

Supplier earns a “performance bonus” (up to Y% of fixed fees) if it exceeds project Savings Target

This pay-for-performance pricing is simple, transparent, and mutually beneficial as the service provider is incentivized to create value, it is relatively straightforward to track and measure, and the buyer payouts cannot be so huge that they can cause budgetary issues.

A gain share model backed with an “innovation fund” is also a better idea than pure gain sharing. Here the supplier (and buyer) commits to a pool of money to drive innovation. A joint innovation council identifies potential projects and uses the innovation fund. The supplier recovers its investment using a gain-share approach with a potential upside if the project is a huge success and a downside if it fails.

Finding a common purpose in a relationship can convert it into a growth engine for both parties

The most mature relationships are not based on math on some complex savings calculations but on a shared drive or goal (see stage 3 above). This is where co-creation happens. When combined with the supplier’s experience and technology, the buyer’s data and real-life business context create a unique solution that can be taken to the market jointly, with both parties sharing the potential windfall. Suppliers struggle to develop innovative solutions in a vacuum, and co-creation allows buyers to drive the partnership toward revenue creation. Purpose-driven associations rely on each other’s strengths to build a strategic, mutually beneficial relationship. A recent example is where bp and Microsoft formed a strategic partnership to drive digital energy innovation and advance net zero goals. Microsoft would further bp’s digital transformation with Azure, while bp would supply Microsoft with renewable energy to help meet the company’s 2025 renewable energy goals.

Bottomline: There is no pricing nirvana in IT and business services. But pricing structures should evolve as the relationship matures from effort to performance to purpose

Each pricing structure – input or effort based (e.g., FTE-based), output-based (e.g., price per transaction processed), or outcome-based (e.g., gain sharing, pay-for-performance, innovation fund) has its pros and cons. It generally makes sense to start a new relationship with some effort-based pricing to establish the baselines and build trust, but then it is time to move on to pay for value.

Where we are seeing most progress towards performance-based relationships is when the CEO gets involved to learn the nuances and value of moving towards areas of common purpose that can also involve other entities in that industry ecosystem. The challenge for service providers is to have leaders capable of developing C-suite relationships and changing that age-old master-servant conversation to one of common purpose to create mutual value.

Sustainability is a massive problem involving multiple interconnected factors – literally, everything happening everywhere links to it in major or minor ways. Those systems need to align rapidly to the global context.

Consulting, technology, and services firms sit at the center of these vast systems. The leaders have realized the scale of impact they can have from that center. They are addressing their own organizations’ sustainability—but more importantly, they are doing so with their clients and partners. They use their networks to drive the level of collaboration and alignment we need. They can scale best practices and solutions.

The leading providers of sustainability consulting, technology, and services in this report influence and help to transform organizations, industries, systems, and governments, which must all build and execute transition plans that align towards decarbonization and every other environmental, social, and governance factor underpinning the UN Sustainable Development Goals.

I sat down with Josh Matthews (you can see him above speaking at COP26 in Glasgow last November), our Practice Leader for sustainability, to dig into the results of this new research.

To download a copy of the report, please click here.

Phil Fersht, CEO and Chief Analyst, HFS Research: Firstly, Josh, how does HFS define “sustainability” these days… has your attitude / focus towards the whole sustainability topic shifted since you started writing about it for us in pre-pandemic times?

Sustainability Practice Leader Josh Matthews (click for bio)

Josh Matthews, Practice Leader, HFS Research: Sustainability has to include all environmental, social, and governance (ESG) elements. Companies, governments, industries, and entire ecosystems need to build and align roadmaps under the global sustainability context: that means reducing emissions to zero (or at worst) net-zero by 2050 (or ideally as soon as possible) and addressing all the other ESG factors underpinning the 17 UN Sustainable Development Goals (SDGs). These roadmaps have to start at the systems level and break down to day-to-day operations in organizations. The most ambitious and influential organizations in their ecosystems will be the ones to drive collaboration and alignment to this context. I guess we’ll talk about them later on…

But the fact we have goals for sustainability is a massive advantage. Yes, the goals that make up the global context need refinement and detail the transition planning underpinning them (the SDGs are based on this in some detail), but contrast this to the last 10 to 15 years where we all saw organizations chase the vague specter of digital transformation without an endpoint in sight.

Our systems are not good enough to address sustainability. But too many of the most influential firms use this as an excuse for not moving first and bringing their ecosystems with them. There is a glaring opportunity in all industries and ecosystems for organizations and coalitions to set the standard by reinventing business models and loudly disclosing their transition plans. These leaders must show their ecosystems—including competitors and regulators—that addressing the entire global sustainability context is not only competitive but also by far the best environmental, social, and financial option now and in the coming decades. This applies in spades to sustainability consulting, technology, and services firms.

Phil: What has stood out to you most with the service providers, both in terms of where they are delivering value and facing challenges?

Josh: Growth is soaring across sustainability services revenues, headcounts, and clients—we expect approximately 240%, 190%, and 210% growth, respectively, over the next two years. Together, the 18 leading firms in this study account for more than $13 billion, 68,000 employees, and 22,000 clients dedicated to sustainability services. Seventy-five percent (75%) of their clients are located in North America or Europe. Clients are more impressed with execution capabilities versus innovation. Case studies and references proving technical and domain expertise are more vital in winning business for sustainability than in most areas. Maturity is high across the value chain, with net-zero roadmapping, platforms, and ESG reporting as standouts.

More than 80% of organizations don’t have the plans they need to address sustainability internally, let alone influence systems. Employees want to work for firms that act on sustainability and have it embedded throughout the organization. There’s a talent shortage for deep sustainability expertise. The energy, utilities, manufacturing, financial services, and consumer goods industries show the most demand for sustainability services. Given their impacts on sustainability beyond their industry walls, they are critical in addressing the global context. Analytics is the most widely used digital technology for sustainability efforts, followed by cloud and automation. Demand is increasing across the sustainability services value chain from consulting to technology and managed services; supply chain and procurement strategy, net-zero roadmapping, platforms, and ESG reporting stand out. The roadmapping approach must also be applied to social sustainability.

Phil: And who impressed you out of the Top 5 we selected? What sets them apart from the rest, Josh?

Josh: ERM, EY, IBM, Accenture, and Capgemini make up our top 5 overall. The firms that lead the leaders in this study are set to make the most significant impact across the global sustainability context. However, it is not just a token nicety to say we have been beyond impressed with all 18 firms profiled. Most have developed scaled revenues and headcounts, growing at pace with the market. They have broad capabilities across the value chain and beyond. They have large clients and case study pools with examples of deep strategic engagements with the most influential firms poised to change their systems. Their strategies are clear, ambitious, and aligned with the global context. They use a broad range of technologies and IP and have impressive R&D initiatives. Their ecosystems are powerful across partnerships, acquisitions, co-innovation, and global networks. Customer references speak highly.

But specifically on the top 5:

ERM’s 50+ years of sustainability experience and engagements have set the standards others follow—including writing the TCFD scenario analysis playbook and JP Morgan’s critical Climate Compass methodology to, in their words, “replumb the financial system”. Lord knows we need it. Its “Boots to Boardroom” approach to operationalize full sustainability from strategy through to physical implementation is what many of the other 18 providers are aspiring to.

EY is setting the strategic direction for sustainability at the C-suite and United Nations levels—including around COP27 this November in Egypt. It has a scaled global practice of 25+ years and a powerful ecosystem stemming from its historic strategy and auditing base.

IBM’s ambition for just what is achievable as a provider in the center of so many systems stands out. It’s partnership ecosystem is powerful and has potential beyond most; combined with its longstanding technology and innovation really has brought IBM to the global sustainability forefront.

Accenture has established its sustainability services scale, and its practice is on a steep trajectory from an early-mover position. It also has outspoken ambition throughout global networks. Its ecosystem of partnerships, acquisitions, co-innovation, and these global networks leads the pack.

Capgemini has a breadth of capability few can match, from business models to physical engineering. Its global leadership spans ecosystems and also international governments. Sustainability is a top-line company priority. Expect Capgemini to challenge for the number one spot in years to come.

Phil: What do you expect to see in this space over the next two years? How are the enterprise needs /concerns shifting and what do service providers need to do to stay ahead of the game?

Josh: The glaring opportunity in sustainability applies to everyone: organizations, policymakers, and the consulting, technology, and services sector. We need them all to meticulously detail how they can and will address the entire global sustainability context on the three key fronts. First is addressing internal sustainability by reducing emissions to zero and tackling all other ESG factors underpinning the SDGs. The second is helping clients address their sustainability by positioning products and services under the global sustainability context. Third, organizations and coalitions with the greatest influence over their ecosystems must move first, prove the commercial models work, and publicly disclose their transition plans. This influence must also drive adaptation-–given the desperate state of climate and ecological breakdown currently being experienced. It is set to get worse. The final element is a call to all at the forefront to be unashamedly ambitious and transparent. Too many are playing not to lose in sustainability. Leaders can help everyone win.

Phil: Finally, Josh, what can we all do as individuals to learn more and make a difference – even baby steps?

Josh: I think this glaring opportunity applies to individuals too. Think about what impact you can have from whatever position you find yourself in—whether that’s daily life or your job. Think about how decisions and work fit under the global sustainability context. (But also, don’t beat yourself up for, say, taking a flight to see a relative or ordering a meal that’s flown from afar… while we can, of course, all play our part… the scale of the systems change we need means that the weight falls on the most powerful).

If your job, say, is a barrier to the impact you want to make, there’s a phenomenal number of opportunities out there. As I said, companies are not only hiring sustainability talent like there’s no tomorrow… a fitting phrase for sustainability and climate change… but are looking to embed sustainability and broader purpose into everything they do… at least the leaders are.

In terms of learning more, I’d suggest How to avoid climate disaster and Net positive as two books that frame the global context and solutions we need well. Also, a shameless plug for our coverage at HFS, both over the past years, the new Top 10, and the upcoming works, talks, and events that will include a refresh of the sustainability services ecosystem map and more market analysis.

Phil: Thanks for your dedication and passion for this critical topic, Josh.

HFS premium subscribers can click here to download our new Top 10 Report: Sustainability Services, 2022

My new reality is entirely digital, unless it’s meaningful to me. I mean, actual conversations used to be cool, but who really needs them anymore? If the pandemic taught us anything, it’s that we can hide away in our homes and never talk to anyone again. Except maybe that Verizon voice-remote… but that’s just some misplaced technology that started to work about 20 years too late.

I don’t want to go into a bank anymore. I used to have a dedicated bank manager who knew me and provided personalized service. Now it’s just people staring into a terminal and repeating what I can see myself. I don’t need to engage with these people – they can’t help me. Why do I need meaningless transactional dialog with someone who seems pissed off with the world?

I don’t need to talk to airline customer service anymore. They just repeat what I can see myself online. I don’t need to engage with these people – they can’t help me. And I don’t need to spend half my life on hold… just automate this nightmare for me, please.

I don’t need to go to the Apple Store anymore. I know what I want and can buy it myself. I don’t need some cool kid making me feel like some aging techno-moron. Just ship me my purchase, please.

I don’t need to call Amazon customer service anymore. It takes forever to find a number to call and they’ll just tell me they’ll get back to me… and never do. Or just accuse me of lying and hang up (yes, that actually happened).

I don’t need to talk to my cellphone provider anymore. They just sell me upgrades I don’t want and put me through to other departments for the help I need, which never pick up or send me back to the original department that tries to sell me those upgrades again. Why persist with this painful waste of time?

I called google enterprise support once (yes, there actually is one) and was emailed a manual to read to solve my issue. But the person was friendly and had a nice Irish accent.

I don’t need to talk to my colleagues anymore – I hardly ever see them these days. I can get what I need over Zoom or Teams chat. In fact, I don’t really need to talk to my boss unless I need to resign, but I guess I can do that over Zoom too… And am sure if I get sacked, it won’t be via an actual conversation.

My mom and dad do sometimes call me, but never with any forewarning… and I am always busy when they do. But they can (just about) use texts now, so we have something to work with…

The Bottom-line: Our new reality is entirely digital unless it’s meaningful to us. So the Metaverse it is… let’s go!

Let’s face facts, we only want to talk to people who are worthy of our attention, who give us their attention too. We only really want to invest in personable relationships that are meaningful. Everything else is really just a transaction that can be automated or AI-ed. So buy that VR headset and give up on transactional humanity… the future is in the Metaverse folks!

One CIO I spoke with recently declared, “I’ll keep finding automations ’til I die”… the guy is eagerly looking at the many break points and dysfunctions across his company, generally excited at the impact of speeding up repetitive tasks and delighting teams that can focus on higher value work. He’s literally hopping from one project to the next, intent on driving significant improvements to his business. He is a fairly typical example of what happens when you insert smart technically-minded leaders into these automation programs in a market where the rush to modernize systems and processes has never been more determined.

The pandemic has acted as a catalyst for many business models and their enabling technologies

Covid either accelerated the demise of business models that were dying in any case, or it created opportunities that would have eventually opened up but would have taken several years to materialize. One of those enabling technologies that have sprung into life, due to the pandemic-induced secular changes, is the array of automation tools… from RPA and task-mining to intelligent chatbots, to API-driven workflow platforms, to process mining and digital twinning, to computer vision and machine learning solutions. We’re even seeing the emergence of geospatial technologies to analyze spatial data and create visual representations that are critical for the metaverse.

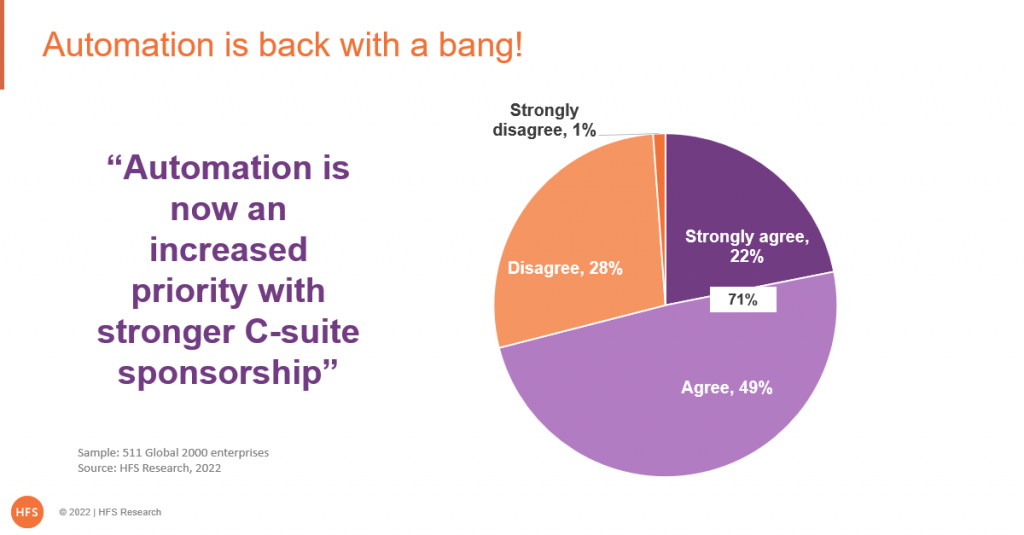

Our new study of 511 automation decision-makers (stay tuned for imminent release) reveals that the pandemic held back two-thirds of enterprise automation efforts, but over 70% are now experiencing a strong bounce-back with C-Suite sponsorship. In short, debilitating labor shortages and wage inflation, combined with desperate moves to modernize digital infrastructures has firmly propelled a refreshed approach to automation back into the corporate spotlight:

The implications of the pandemic on automation have been two-fold:

1. Non-essential automation has been put on the backburner

For many organizations, the pandemic halted every nonessential activity while crisis management went into full swing to ensure the survival of the company. And our research pre-pandemic showed very clearly that the vast majority of automations were being trialed on low-risk back office tasks. The onus for automation back then was to drive out cost from the business, and most organizations were only beginning to figure out that solutions such as RPA rarely resulted in headcount reduction – it, most often, simply freed up time for people to spend on less routine, soul-crushing activities. You rarely can automate someone’s entire job, usually, just some cycles that could be taken over by attended automation scripts.

2. Automation has become a key discipline where it has immediate business impact

For example, for banks that had to “pause” millions of student loan payments, automation became a lifeline to get them moving again. For other entities, such as healthcare organizations that had to implement track and trace metrics in days or weeks, the automation teams were at the ready and immediately went to work. Or pet-care facilities that became overwhelmed with customer demand during the pandemic and rolled out intelligent chatbots to keep their customer service wheels on. In addition, how does a consumer products firm take data from legacy supply chain systems into an Amazon environment that is essential to keep it in business? It’s not the sort of thing you can solve overnight, but smart RPA connectors, combined with relevant APIs, have been commercially transformational for many organizations making the rapid shift to fully digital business ecosystems.

The Bottom-line: The changing business environment has completely flipped the business needs and mindsets toward automation

You literally can’t operate seamlessly in the virtual economy if you don’t have the tools to link the old with the new, and automation tools must be part of the toolbox to make immediate impact with the suppliers and customers which provide the lifeblood for survival in a world where supply chains are falling apart at the seams, customer needs are right-now, and stitching together processes from the front to the back office is the only way to function in these increasingly hyperconnected ecosystems. These things would just not have been possible just a few years ago.

Welcome to a whole new era of automation, folks… where immediate purpose is driving everything forward.

I don’t think I’ve ever lived through a period in my life where there’s been so much doom and gloom around the economy… and while I tend to be a naturally negative human being, I am also an obsessive analyst, and I must declare that I am not convinced we’re entering a 70’s style recession. If anything, we might be finally on a weird and rocky road to a much more normal future, compared to our highly abnormal recent past.

In 2008, when we thought the whole capitalist system would fail (and it was close) – and in 2020 when the world locked down practically overnight, we thought seismic business failure would engulf us. But we’ve recovered from both calamities and now face a new set of unknowns… that cancer of capitalism itself, inflation, a shortage of commodities that keep the economic wheels on, and a rebellious workforce that was locked down for the best part of two years.

Why this resembles more of a cooling-off than a recession

We’ve had 14 years of negligible interest rates which have driven businesses and consumers to pump up house prices and stock markets… as there really haven’t been many other places to deposit our excess cash. On top of the amount of practically free money on offer, we’ve printed trillions of dollars of money to prime economies during the two crises, US corporate tax has been slashed, unemployment has reached record lows while major stock markets have just kept going up and up. There’s too much of a good thing, and then there are 14 years of continuous good things…

So, let’s examine the current economic situation for businesses:

Those businesses that were based on hot air and analog business models are failing fast

Where we’re seeing recent business failure is in areas that are almost purely speculative and have very little basis for their value, such as cryptocurrencies and various flavors of AI and automation that just don’t make a lot of sense. I won’t even get into biotech and other markets where reality misalignments disappointed many naive investors. Simply put, there have been many spectacular startup failures where both business and consumer investors gambled on business propositions that were based largely on pure fantasy, where they listened to analysts posing as experts – and believed them. In addition to businesses run on vapor, we’ve seen businesses unable to adapt to digital commerce fall by the wayside – restaurants that couldn’t pivot to home delivery, taxi firms that couldn’t develop apps as easy to use as Uber or Lyft, manufacturers which failed to adapt to making products and equipment that customers still needed. One can argue that many of these businesses were set to fail in any case, and Covid merely accelerated the failure process.

Businesses addressing real market needs will thrive

Conversely, while stock prices have suffered in recent times, those businesses that address a clear market need and have a path to profitability and growth are surviving and will eventually become safe bets for investors eager to escape the madness of these recent speculative times. Core tech suppliers and IT services firms have enjoyed record growth over the past 12-18 months as enterprises rely more than ever on technology to run and automate their operations. Airlines are bouncing back as people are eager to leap out of lockdown purgatory and go on vacation and get their business lives normalizing again. Many consumer product and manufacturing firms are rebounding as two years of pent-up consumer spending is unleashed, while many banks have digitized their business more than their wildest dreams during the pandemic and are eager to reap the record profits of transitioning their painfully unprofitable analogous businesses. We can go on and on, but the customer needs to engage have never been as eager as now… and the fundamentals are all there to project a healthy future for many industries rebounding after the pandemic, or growing more than ever because of the pandemic.

I believe we’re entering a “realistic economy” where companies are expected to be profitable, offer substantive value to their markets, and have a sensible fiscal plan to ride out the current inflationary pressures, especially in terms of keeping their core staff onboard. The cranks and the fakers are slipping away and the real businesses are taking over. And our investor speculators are desperate to dump their dwindling funds into businesses that actually have a realistic business plan.

Two key issues have contributed to today’s economic peculiarities

1. The Ukraine war

The war has resulted in wheat and fertilizer shortages driving the cost of many food products higher. Even commodities like neon gas have been hard hit, which is essential for the manufacture of computer chips, as half the world’s supply comes from two Ukrainian companies, Ingas and Cryoin. Suddenly it’s harder to purchase tech hardware and these prices are steadily escalating. And let’s not mention the massive impact on oil prices which has driven up the costs of every product and service needing gasoline. On top of that, the oil companies are exploiting the situation and raising their profits… because they can.

2. Rampant consumer demand post-pandemic

Many families hoarded cash for two years, some bring topped up by government support, others simply earning good money and saving on no work commute, moving to the countryside getting great mileage out of their old pajamas. On top of that many people have enjoyed wage increases or taken more lucrative jobs due to the labor shortage – without leaving the house. Times are good for many, and they are indulging in buying overpriced vacations, cars, BBQs, household furniture, etc. You can’t even find many Rolex watches on the market these days… we’re in a world where demand is just trumping supply in so many areas.

In addition, rents and house prices are climbing as people move back to the cities and there is a shortage of properties, while restaurant bills spiral because of rising food and labor costs. There is now a shortage of taxi drivers emerging in many major cities as it becomes too expensive to make the job worthwhile anymore. There is a shortage of workers right across the service industries… but as things cool off and the economy corrects, so will these stresses on the cost of living and working. We are all (just about) adapting… even during unprecedented times where you can’t find good willing workers for love or money. We should take solace in the fact that things are at their inflationary peak, and we are still moving forward as an economy. The fundamentals underneath it all are strong…

The Bottom-line: We’re experiencing unprecedented economic and societal challenges, but the fundamentals to get to the other side of this are strong

While we can deplore this shortage of workers who underpin our economies and the impact of this awful war in Europe, which hurts our supply chains and drives the cost of living to unbearable levels for many, we have to look at the bigger picture to realize we’re just in the process of cooling off, and not necessarily plunging into a terrible recession. Businesses based on real substance are – by and large – doing fine, there is a desperate need for workers of all types to support our industries, and there is a lot of excess money sloshing around the place (Deutsche Bank estimates US households have $2.3 trillion excess cash stashed away to weather inflation and higher interest rates).

We also have a sensible Fed which is looking to fix inflation before making other key economic injections, and we are already seeing early signs that inflation is beginning to cool off with these interest rate hikes. If we can somehow fix these supply chain issues and find a resolution to the Ukraine situation, we will get past this current period without too much damage. Yes, there are some big IFs here, but we may just be just going through a readjustment of a rather distorted 14-year-old bubble. And we may be moving into a work of two diverging superpowers

There are surely more normal and rational times ahead, as the past couple of years have been anything but!

I don’t think I’ve ever lived through a period in my life where there’s been so much doom and gloom around the economy… and while I tend to be a naturally negative human being, I am also an obsessive analyst, and I must declare that I am not convinced we’re entering a 70’s style recession. If anything, we might be finally on a weird and rocky road to a much more normal future, compared to our highly abnormal recent past.

I don’t think I’ve ever lived through a period in my life where there’s been so much doom and gloom around the economy… and while I tend to be a naturally negative human being, I am also an obsessive analyst, and I must declare that I am not convinced we’re entering a 70’s style recession. If anything, we might be finally on a weird and rocky road to a much more normal future, compared to our highly abnormal recent past.