Two CEOs clearly up to no good… Genpact’s Tiger Tyagarajan (left) and Infosys’ Vishal Sikka (right)

One of the great things about HfS is the fact we never partake in gossip or idle speculation. So let’s change “never” to “rarely”…

I was happening to be Uber-ing myself aimlessly around the streets of San Francisco last week when I happened to drop in on Infosys’ sexy new Design Thinking center (I think that’s what they call it) in Palo Alto, where I caught two of the industry’s finest minds having a sneaky cup of coffee.

Now, before you all jump to conclusions that Vishal Sikka and Tiger Tyagarajan are about to join forces, they are actually old friends and neighbors, and this was purely a social call… but it did get me thinking about what if Infosys and Genpact got a little more intimate with each other…

Pros:

Challenging the old way of thinking. Infosys’ fresh Design Thinking approach and Genpact’s re-imagination of business processes are very well aligned. Both firms have jumped on the importance of challenging current thinking and instilling that across their organizations (and not a CoE approach).

IT services meet BPO… on steroids. A great IT services firm meets a great BPO/operations process management firm. This would be a real powerhouse. What’s more, Genpact is the largest “process pureplay” breaking new ground in terms of its sheer scale and size – where it takes the business next, there is no written rule book available.

BPaaS at a global scale? Infosys EdgeVerve + Genpact’s emerging process consulting capability would be very interesting. Scalable BPaaS solutions that could be industrialized at a global level… the mind boggles at the possibilities to realize a long-held industry vision.

Cross-client synergies. Great upsell opportunities across major clients, especially in horizontal process areas where Genpact is market leading, such as finance and accounting solutions or procurement where this combination would create an even stronger challenger to Accenture than they are individually today.

IT autonomics + RPA + AI potential. Interesting combination of automation capability across IT autonomics (Infosys) and robotic process automation (Genpact). Would also be a nice playground for Vishal to put his Ph.D. in artificial intelligence into practice. These two could certainly build a cognitive+autonomics+analytics computing platform that differentiates itself in the market alongside the likes of Watson, Holmes, ignio, Amelia etc.

Digital meets Process. Digital strategies need to bring together real process acumen and technology enablement skills – at scale – in areas such as mobility, analytics and social media/collaboration. The ability to design “digitally-native” end-to-end business processes is core to the future of services and these guys may just be able to pull off something quite special together.

Adds real vertical strength and depth. They would nail insurance and banking in spades, have really strong presence across manufacturing/consumer/retail and Genpact’s life science’s presence would be a fantastic opening for Infosys.

Geographically and culturally. Very interesting spread across India, UK, Central Europe, ANZ and the US. However, still trying to visualize (or is that Vishal-ize) the whole Palo Alto/New York/Gurgaon/Bangalore cultural thing they’d have going on.

Timing. This market is ripe for some aggressive moves to change old habits and shake up the apple cart. This one would certainly set the big cat out loose among the pigeons, when investors are hungry for new ideas, bold moves and aggressive plans. With Vishal enjoying a healthy dose of momentum as he reaches his first anniversary at the helm of Infy, there are worse moves he could make… surely? And this would likely be at a similar size to Capgemini / IGATE…

Fashion. Tiger could clearly show Vishal a thing or two about designer New York business attire, while Vishal could certainly help Tiger get with the West coast tech-nerdy thing.

Cons:

Who would run the show? These are two fiercely proud firms with very strong cultures and very dynamic leaders. Could you really fuse these together?

What methodology would they follow? Would Smart Enterprise Operations win out or would the Process Progression Model lead the way? Come to think of it does that even matter.

Limited time to integrate. In this market, no-one can afford to take their eye off the ball. Prices are at an all-time competitive low, several ambitious providers are eager to “buy” their way into strategic deals to develop out their offerings and maintain market share and there are emerging As-a-Service contenders willing to disrupt the old model with new disruptive approaches.

Doesn’t wholly address the consulting gap. While there is some excellent talent across both firms, this is nothing near the scale of an Accenture, Deloitte, PwC or KPMG on the strategy/consulting side. We would like to see both firms up their consulting talent pools – at scale – as the As-a-Service Economy continues to unravel. While the expertise-as-a-service model emerges, there does need to be the right blend of managed services and consulting acumen to really get ahead in this market.

Big isn’t as beautiful these days. Just looking at the efforts the likes of IBM, HP and CSC have made to make their business more manageable with more clearly defined business units, getting to monster size for the sake of being just bloody huge (and this one would become one of the largest services firms on the planet) is not a reason to do this.

The old IT+BPO thing isn’t washing as well as it used to. Up until recently, the whole talk in the services business was always about IT services firms offering BPO as there were so many great synergies between developing and maintain apps and being able to deliver process solutions. Hey – you not only could you support a legacy ERP platform, but why not milk the dollars processing invoices and paychecks off the back of it? With As-a-Service, that isn’t so appealing. When you can get much of the IT you need in the cloud, the ambitious BPO these days is pushing “Finance-as-Service” or “Revenue-Cycle-as-a-Service, or “Insurance-operations-as-a-Service” as so on… The future isn’t about buying IT services, but more buying a business outcome delivered As-a-Service. If a credible BPO can enable and deliver business services in the cloud, who cares who is developing and supporting the underlying apps… especially when they are standardized?

The Bottom-line: This could be a match-made in Heaven, Palo Alto, Gurgaon or Hell…

It’s fun to speculate, and this one is especially interesting. When we looked at IBM+TCS, there were clear service line synergies, but the cultural gap between those firms is huge – and the sheer sizes involved make this too unappealing for so many stakeholders. However, in this case, Infy (we think) has just about enough cash if it really wanted to take a serious look at G, and there is clearly a closer set of synergies in terms of cultures and less overlap. These are also two ambitious firms who are clearly not ready to rest on their laurels and want to break new ground if they can. They are also led by two popular and visionary guys who are in tune with their people and the market. However, at the end of the day the bankers do the real talking and these may just be too many complexities to make something of these sheer scale and size pay off.

If there’s one market people have been raving about for the past decade – and still are – but has never quite taken off as quickly as many have predicted, it’s the world of engineering services outsourcing.

This market is all about using third parties in the design, analysis, manufacture and augmentation of products. And in today’s world of global labor, the global marketplace, emerging technologies, smarter global sourcing models and the Internet of Things, the potential to embrace outsourcing expertise to bring products to market smarter, faster and cheaper has never been so exciting.

Engineering services has a huge market potential, but – somehow – engineering service providers have had limited success in transforming this potential into the actual outsourcing engagements. Now things are changing, and we believe that engineering services is evolving from a niche offering to the mainstream. So without further ado, let’s hear from HfS Research Director, Pareekh Jain, on the excellent research he’s completed that delved deep this this market:

Click to Enlarge

Pareekh, how do you see this market evolving and what are the key drivers for engineering services?

Engineering services outsourcing, over the last decade, has evolved from simple drawing and drafting to complex end-to-end product design. Now an enterprise which wants to enter a new market segment can partner with some leading engineering service providers, that can not only deliver complete new product design but that can even collaborate with manufacturing partners for additional benefits. Some engineering service providers are also collaborating on high-end R&D projects with the world’s leading research institutions and filing patents both on behalf of their customers and the service provider.

We have observed six key demand-side drivers transforming the engineering services outsourcing market. First, product life cycles are getting shorter which means more product design work and faster time-to-market requirements for enterprises. Second, enterprises are looking to adjacent markets for growth but rather than do it all themselves they are partnering with engineering service providers. Third, enterprises are entering emerging markets and leveraging engineering service providers to do value engineering and to develop frugal versions of the enterprises’ products that can compete at the different price points in these markets. Fourth, the long tail of products created when technology companies merge (and they wish to maintain all existing revenue streams) is increasing the demand for the external help to manage the lifecycle management requirements of legacy or low growth products. Fifth, demand for smart products with the combination of software and hardware is driving enterprises to leverage engineering service providers which have developed expertise over the years across software, hardware and embedded solutions. Sixth, availability of composites and lightweight material is enabling enterprises to rethink the design of their products with the help of engineering service providers.

What was the scope of this Blueprint?

This Blueprint is focused on the product engineering segment of engineering services. The other two segments of engineering services i.e. software engineering and product lifecycle management (PLM) package implementation were excluded, and we will look to cover them in future Blueprints.

How did the Blueprint turn out?

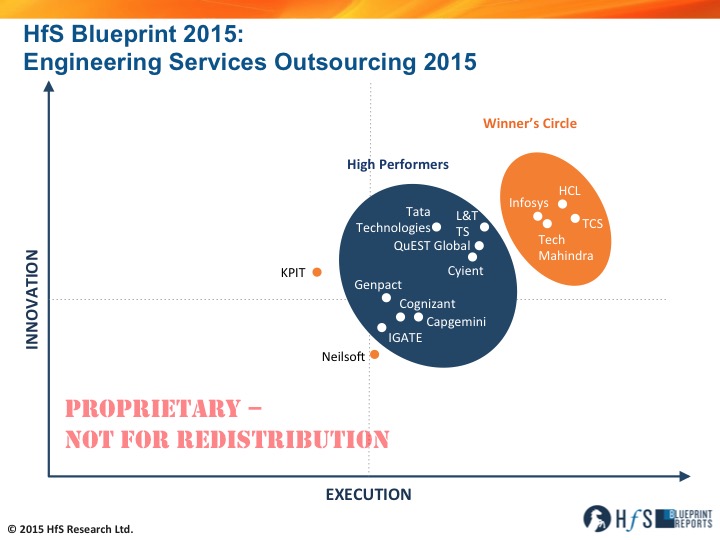

Engineering services is a diverse market spanning across many different verticals and industries. While the value chain element of product development is common across this diversity the skills for designing a car are very different than the skills for designing medical equipment. We analyzed key engineering services outsourcing market dynamics and evaluated the capabilities of 14 service providers at the organizational level, the vertical level, and the service level. We evaluated both specialist service providers as well as broad-based service providers which also offer engineering services. All 14 service providers are leaders in at least one of the verticals.

Our analysis shows four clusters. The first cluster includes leading broad-based IT service providers which also have scale in engineering services. The second cluster consists of leading specialist service providers with strong expertise in few verticals. The third cluster includes broad-based IT services firms that are relatively late entrants in engineering services and building their scale and capabilities. The final cluster consists of specialist firms which have strong expertise in one or two verticals.

There are four service providers in our Winner’s Circle – HCL, Infosys, TCS and Tech Mahindra that have four things in common: scale, scope, investment in future capabilities and strong customer references.

The eight High Performers in our study are Capgemini, Cognizant, Cyient, Genpact, IGATE, L&T Technology Services, QuEST Global, and Tata Technologies. They are on the right path and building their capabilities.

In this Blueprint, we also focused on benchmarking and operations improvement. This is first of its kind of engineering services study where we tried to collect important operating data from engineering service providers and arrived at the aggregate or the average engineering services industry metrics. This should help each engineering service provider and captive to benchmark their operations and identify their strengths as well as areas or levers of improvement.

Pareekh Jain is Research Director, HfS (Click for Bio)

So what are your key takeaways from this study and what should we be watching for in the next few years?

There are three key takeaways.

First, engineering services is a huge untapped market. Currently, it is dominated by captives but we believe that is rapidly changing as outsourcing to service providers becomes more significant.

Second, scale is becoming very important in this market as it enables service providers to make investments in labs, capability development, additional services and market access which are critical to developing this market further. Finally, the scope and complexity of work being outsourced is continuously expanding.

This year the revenues from engineering services for Indian services providers has grown faster than the IT services according to NASSCOM data, and it is fast becoming a growth driver for the global outsourcing market.

We will be watching three key trends in coming month and years.

First, we believe engineering service providers will witness high growth and eventually service provider outsourcing will overtake the captive outsourcing. Second, we will be watching for mergers and acquisitions among engineering service providers. Finally, we will keep track of how service providers augment their capabilities and service offerings. We believe IoT/M2M and engineering analytics will become mature service offerings in next few years.

HfS readers can click here to view highlights of all our 21 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report: Engineering Services Outsourcing 2015“

Most of the outsourcing industry is still trying to figure out what’s possible beyond doing labor arbitrage really well – because that’s what we do. Sorry, but there I said it – we officially have an identity crisis.

We’re trying to forge a new identity for ourselves and re-imagine what our careers, our services and our platforms could be like if we only figured out how we can define, prioritize and realize business outcomes that are valuable, as opposed to merely keeping the same old factory ticking over at the lowest possible cost.

Sexy robotics software, analytics tools, BPaaS platforms and artificial intelligence can only be effective and impactful once enterprises have re-designed their processes in a way that drives them towards their desired business outcomes. This has always been the case with (now legacy) ERP implementations, where thousands of clients have blown billions of dollars on enterprise software they simply never could mold effectively to their businesses. They weren’t finding problems to solve, they were creating new ones they didn’t need in the first place.

It’s the same with the next wave of As-a-Service solutions – they will fail without the right approach to designing processes that produce the desired results. Without Design Thinking, enterprises are really just retrofitting expensive solutions into legacy processes and likely wasting a whole load of time, resources and money. It all starts with Design Thinking.

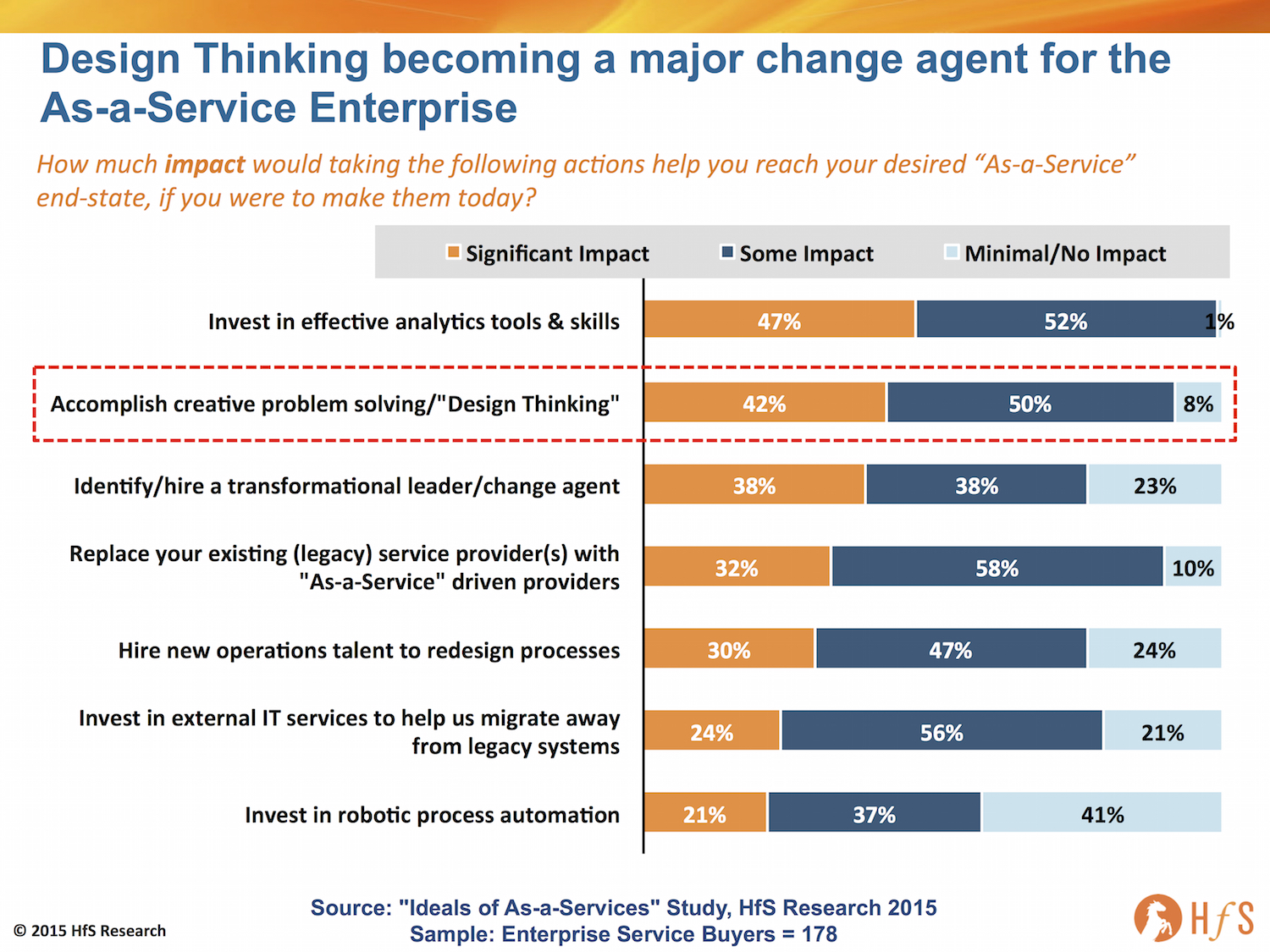

New HfS research into the Ideals of As-a-Service, which canvassed the viewpoints of 178 major enterprise operations executives, points to the rise of Design Thinking and the cultivation of creative ideas, as critical to more than four-out-of- ten enterprises today, in terms of having immediate impact in their quest to reach an As-a-Service end-state, second only the investments in analytics tools and skills:

Click to Enlarge

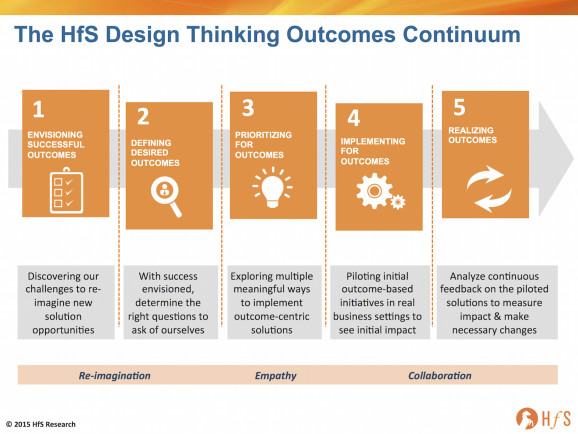

HfS’ Design Thinking Outcomes Continuum aligns traditional concepts with the realities of today’s services industry

In today’s whirl of constant information and social media, it is much easier to visualize how effective enterprises will be running their operations in another five-to-ten years. However, developing a realistic strategy to get there is an immense challenge – and threat – for most enterprises mired in decades of legacy processes and systems.

We all know we need to get smarter with digitizing and automating legacy processes in order to access meaningful data to grow the business and be less reliant on inefficient labor. Plus, an increasing majority of us know we need to explore the possibilities capabilities of self-learning and artificial intelligence, to augment our existing knowledge labor. Today’s challenge isn’t only identifying what the future of operations should look like, it’s developing and adhering to a collaborative and entirely new way of re-imagining processes in order to explore what’s possible and execute against that.

Being successful in the As-a-Service Economy requires ambitious service providers to make fundamental changes to their whole approach to service design and delivery. At the heart of this evolution is a shift to service solutions being designed with real business context, as opposed to simply “looking at a process”. This involves a genuine focus on approaching and interpreting a client’s challenges, identifying and experimenting with opportunities, and ultimately evolving these approaches into the service delivery.

HfS believes that traditional capabilities, such as Six Sigma-based process design and execution, while essential to delivering the efficiency benefits of the traditional sourcing, are today standard, commodity-based capabilities embedded into any standard service model move to an As-a-Service delivery environment.

We believe that a new methodology must be front and center that imbues the full spectrum of human-centric design ethos. This methodology, commonly dubbed “Design Thinking” by several industry stakeholders, is based upon a more responsive relationship between the service buyer and the provider, one that is open, empathetic, experimental and yet efficient. We have seen Design Thinking come to organizational prominence in recent months at IBM, Infosys and Wipro, to name a few service providers, and at the offering or project level in many others. This makes sense to us, because without this more open and innovative approach, it will be difficult to build solutions to meet the challenges and opportunities of the “As-a-Service Economy” such as increasing consumerization of technology and a more virtualized workforce.

As our new survey data illustrates above, we firmly believe 2015 to be the year in which Design Thinking comes to the forefront of the sourcing and services market. It will be the time during which service provider leadership teams are sent to design camps, and a whole new set of conferences and workshops feature Design Thinking as their theme of the moment. Some of that may be hype or even unnecessary, but at the root of it, the arrival of Design Thinking into the mainstream of IT and BPO services makes sense to us as a way to re-imagine more effective process-based solutions for this increasingly digitized As-a-Service world.

There is no one best way to apply Design Thinking, but there are useful starting points, and we believe the HfS Design Thinking for Outcomes Continuum to be a valuable and meaningful way to think about how to solve problems in designing services for the As-a-Service Economy.

Click to Enlarge

The Bottom-line: Design Thinking for outcomes is a real methodology that enterprises can understand and embrace today, not in five years’ time

While we believe Design Thinking will take root in IT and business services in 2015 as a methodology to enable further innovation, at the end of the day it is still just another tool. What you make of it depends on the intent and practices of its users, whether individuals or organizations.

This approach will not be easy for some legacy service providers who cannot yet see how the world is changing. For those service providers and their enterprise clients who can see that thriving in the As-a-Service Economy requires new approaches and capabilities, we see a real potential to use Design Thinking in the move from the present into the future.

Getting new digital processes and services right from the perspective of their end users is critical. Design Thinking, which is about context and empathy for the user, can facilitate this focus. It will be an integral part of the emerging As-a-Service provider offerings, many of whom are already rapidly emerging to redefine the market.

You can read the full POV on HfS’ approach to Design Thinking by Phil Fersht, Hema Santosh and Charles Sutherland by clicking here.

When we look back at this current era of IT services, we’re going to remember this as the time when many of the leading providers launched their platforms to help orchestrate, analyze, automate and artificially intellectualize the delivery of technology to enterprises.

We’ve already had IBM’s Watson™ and Wipro’s sidekick Holmes™, in addition to the several specialist IT autonomics platforms such as IPSoft’s IPCenter™ and Arago’s Autopilot™, so surely, it’s just a matter of time until we get the full gamut of branded autonomics-driven IT management platforms from all the major service providers. The most recent launch comes from TCS, which has been putting a significant amount of investment and attention into its new IT autonomics “neural” platform ignio™.

So we recently got some time with ignio’s mastermind, Dr. Harrick M. Vin, who’s the Chief Scientist and Global Head of Innovation and Transformation, and IT Infrastructure Services at TCS. Maybe he should just call himself the Platform Professor…

Phil Fersht (CEO, HfS): Good afternoon Professor Harrick Vin! It’s great having you on the blog. Maybe you can start by giving us some color into your background, and earlier career–and how you ended up working for a major service provider like TCS.

TCS’ Dr. Harrick Vin launches ignio this June in New York City (click for bio)

Dr. Harrick Vin: First of all it’s a pleasure to be here, and I appreciate the opportunity to talk to you, Phil. Let me first introduce myself. My name is Harrick Vin and I’m vice president for R&D and Chief Scientist at the Tata Consultancy Services (TCS). I look after our largest R&D center in Pune, India. For the past several years, I have also been driving the overall strategy and innovation for the infrastructure services business unit of TCS. Most recently, my team and I have been involved in developing a product called ignio, which we are launching in the market. I have been with TCS for about 10 years. Prior to joining TCS I was a Professor of Computer Science at the University of Texas at Austin for almost 15 years. At TCS, I have had an opportunity to closely work with and analyze some of the most complex systems, ranging from human systems, technological systems, to large engineering systems. We have used a lot of the learnings about how to manage complex systems, to design ignio.

Phil: So talk to us a bit, Harrick, about why automation is suddenly the flavor of the month in the industry. Why is it suddenly such a talked about topic as we look at the future of services and where things are going?

Harrick: Automation is not at all new, Phil. In fact, the whole IT industry is about automation, because that’s what IT does to the business. In fact, in my mind, the words IT and automation are synonymous. But what is interesting is that while IT has been used to automate business, the way we have been running IT and operations behind the scenes involves a significant amount of manual work. We are still very dependent on a lot of tacit knowledge, experience and intuition that people gather over a period of time while running these systems. Most organizations have exercised several people and process optimization levers to reduce cost, make technology and operations more efficient and consistent. And this has served us well to date.

However, I think the next decade is really going to be all about speed or agility. While the digital revolution has created many opportunities for businesses to transform themselves, it has also created some very tough challenges for the enterprise technology and operations teams. For instance, in most enterprises, technology complexity is on the rise; on one hand, most enterprises are struggling to reduce legacy, while on the other hand, new technology, new applications, new businesses processes are being introduced at an unprecedented rate. Data volumes are on the rise, and decisions are becoming difficult to make. Rising complexity is also leading to increased operational risks resulting from failures, technology misconfigurations and human errors.

Because of these, conventional methods for running technology and operations in most enterprises are starting to fall a bit short. In fact, to deal with complexity, most enterprises IT teams have organized themselves into lots of layers and silos, and deployed many workflows. This essentially ensures that everybody who needs to know or who needs to have a voice gives an approval before something gets done. Unfortunately, this slows things down. Work essentially flows and doesn’t get done very quickly. The lack of an end-to-end view resulting from layers and silos also increases operational risks from human errors.

Thus, the combination of rising complexity, lack of agility or sluggishness caused by complex workflows, and significant increase in operational risks are some of the key drivers that are really making automation of technology and operations essential for the future.

Phil: As you look at the value that a service provider can bring in this space, obviously it’s bringing a lot of capabilities around system integration, bringing together platforms and processes. What do you see new evolving from a technology perspective, that is really changing the game here? Is it that new things are coming on to the market that are creating better types of platforms that are more effective, or do you think it’s just increased skill sets on the services side?

Dr. Harrick Vin talks to us about neural automation…

Harrick: Most enterprises have failed to use conventional automation products or practices to create scalable or sustainable automation. We have seen automation applied in pockets, leading to islands of automation. However, we have not seen most enterprises being able to scale the benefits of automation. This can be attributed to two primary reasons.

First, today’s best practices and tools often require enterprises to embrace a standardize-first model: standardize technology and processes first before you spend the time and effort to automate and thereby derive efficiency and other values. This has often failed because standardize-first requires a fairly large lead-time and there is also no clarity on what is the necessary diversify that one has to actually support. So when you say standardize-first, the question is standardize to what? This is difficult to answer for most enterprises.

Second, perhaps, what has really resulted in lack of scalability and sustainability of automation, is the very fact that most of the current tools or products for automating operations, implement run-book automation, in which a standard operating procedure for doing something manually is converted into a workflow, a script, a program, or a set of rules. This run-book automation model has its roots in manufacturing, where once you configure an environment for automation, the environment doesn’t change much. For example, if you consider a BMW factory that produces a 3 Series car, it produces exactly the same car design for the next several years. But in the case of enterprise IT, everything changes all the time: the workload keeps changing, the underlying technology and their versions keep changing, application functionality keeps changing, new applications keep getting introduced, among others. And all of these changes make automation obsolete, and often leads to automation maintenance nightmare. In fact, because of the challenges in accommodating changes, many enterprises automate only things that are not changing very frequently or things that are at lower layers of technology stack. The higher up you move in the technology stack, the greater the rate of change hence the greater rate of obsolescence.

Thus, to be effective, we need new technologies and products that will enable enterprises to build automation that is inherently designed to accommodate change, designed to accommodate diversity and designed for high degree of reuse, such that automation benefits can be obtained quickly. So, in effect, we need highly intelligent automation with the head-on, rather than dumb automation.

Phil: So let’s look at the next generation solutions to help clients. We talked just recently about an exciting offering that TCS is coming out with called “ignio.” What is different about what you are bringing to market with ignio?

Harrick: Phil, ignio is the world’s first Neural Automation System for the digital enterprise. Let me explain what neural automation means to us. To us, neural automation means four things.

First, it means connected. Ignio has ability to collect data and assimilate data from a large number of enterprise data sources, to create context awareness about what the enterprise environment looks like. In a typical enterprise today, there is no one data source that gives you everything you want. There are hundreds of thousands of data sources that actually contain relevant information. ignio taps into all of these data sources to build context awareness.

Second it is adaptive, in the sense that it does not require an enterprise to make changes to its tools or systems; it does not require standardize-first. It simply connects to what an enterprise has and adapts to the enterprise environment.

Third, it is intelligent in that just like how our brain works, it breaks any complex activity into a large number of smaller simpler tasks, performs each of these tasks and then composes these tasks together on the fly in order to carry out a complex activity. Because it has the ability to create the context awareness, it also has the ability to predict an emergent condition and take proactive actions. So that’s why it is intelligent.

Last but not the least, it is resilient. It is able to accommodate changes or failure gracefully, and reconfigure itself to accommodate change. Which as I said a little while ago, is a fundamental requirement for automation to be scalable and sustainable.

So, in a nutshell, it’s connected, adaptive, intelligent and resilient. These are exactly the characteristics that you would actually associate with a human brain, and how our neural system works. This is exactly what ignio does.

Phil: Why “ignio”? What was the thinking behind the brand?

Harrick: Interesting question. Let me explain. ignio converts every service into a piece of software. By doing so, it is essentially allowing us to create a technology-first service model, whereby ignio has the right of first refusal to do any work, and ask for help when it does not know how to perform the work. So, ignio in our mind is this invisible, evolving intelligence that will ignite and drive change for a large enterprise. That’s what led us to the name ignio.

Phil: So last question, Harrick. When you look at the world today, if you were crowned the emperor of IT services for one week, what’s the one thing you would do to change this industry?

Harrick: That’s an interesting question; let me think a little bit, Phil!

To answer this question, let me draw an analogy between IT services and manufacturing. In manufacturing, because of the industrial revolution, we’ve gone from manual engineering or craft, to mechanized, to now precision engineering. That happened because of the sophistication of automation. If you look at IT services today, we are still very much a manual engineering type of industry. We rely very heavily upon intuition, experience and tacit knowledge to perform different types of complex operational tasks. I believe that the IT services industry is ripe for undertaking this industrialization journey, and this is what I would try to promote and drive.

I also think that converting services to software, like what ignio is designed to do, to enable a technology-first service model for enterprise technology and operations is a critical step towards realizing this industrialization vision. If you look at the last decade or two, we have witnessed disruptions in many other industries, whether it is retail, whether it is taxi rental, whether it is video rental, and so on, where a people-centric model of service has been converted to a technology-first model of service.

Phil: That was very well answered! It’s been a pleasure having you talk to our readership today, Harrick; we look forward to sharing your views with everybody. And good luck with ignio!

Dr. Harrick M. Vin (see bio), is Vice President and Chief Scientist, Global Head of Innovation and Transformation, and IT Infrastructure Services at TCS. He holds a PhD in Computer Science and Engineering, University of California, San Diego, an MS in Computer Science from Colorado State University, and a BTech in Computer Science and Engineering from the Indian Institute of Technology.

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.

The whole premise behind As-a-Service is one of a fundamental cultural change with how enterprises approach their operations and partner more collaboratively with capable service providers to re-imagine their processes, based on defined business outcomes. Simply put, it’s a huge, huge challenge for most current services relationships to morph into anything closely resembling an As-a-Service model, with the current mindsets of most buyside and sellside delivery staff. Buyers need deep expertise to help them reorient their skills and capabilities – and their service providers need to make serious investments and sacrifices to help them, which give their accountants and shareholders hives.

Coupled with the troubles facing buyers and their service providers, is the abject failure of most of today’s sourcing consultants to do anything difference to reform their old way of doing things. Yes, it’s a Catch-22 of many service industry stakeholders not wanting to change their ways, but being forced to address these issues to remain relevant and – let’s face it, employed. In short, the pace at which the services economy is evolving will render many people unemployable in a few short years who fail to get ahead of this.

Just remember how foreign the concept of cloud computing was just five years’ ago… you think it’s going to take that long again for RPA to take hold, and significant advancements in artificial intelligence to reshape how enterprises run their operations? Think again, people; things simply have to change – and these market forces will make sure there will be winners, survivors and losers who will fizzle away into insignificance.

But the answers are staring us in the face – the future of services is a combination of the ability to create business value based on processes that are run efficiently, simplistically, and to common standards we find acceptable.

Consultants make a living demonstrating value in order to create demand to sell their capabilities. This is where too many service providers will terminally struggle

Clever consultants find problems, not just solve them. The only way to get buyers to do anything different is to convince them that hiring you will inspire them to make these changes. This is what able consultants do – they want to be billing themselves out 2,000 hours a year to their clients, so they are constantly looking to find problems, not merely make incremental improvements to existing processes that add minimal value.

BPOs need consulting skills – at scale – to succeed. I hate to say this, but you can’t achieve real success with the next wave of labor-lite solutions with a couple of smart visionary guys living on planes with their PPT mosaics. That may have worked for BPO rounds one and two, but this is round three and there needs to be lots more feet on the ground to be effective. Most of today’s BPOs are operating with very thin layers of consultants to front their client relationships. Simply put, they do not have enough to genuinely scale this beyond a few discreet engagements.

Clients will pay when they see the value in front of their faces. BPO grew up on the sale of immediate cost reduction – a unique value sale that created the industry we are in today. However, as the labor savings run out of room, the sale has to shift to one of future ROI and value – something, let’s face it, which is very challenging for our legacy service providers and advisors to succeed at and manage. However, clients frequently pay for skillful consultants who can come in and make a difference, who will find problems and sell their capabilities to solve them to their clients. The As-a-Service value proposition is really a combo of this consultative prowess and the efficiency and simplicity of effective BPO. So, the two need to be better conjoined to grant clients what they really need. (I stress the term need, as opposed to want, as many enterprises do not know what they need, so there isn’t too much to want until they have it spelled out in front of them…)

BPO delivery staff are simply not very “right-brained”. It’s just how the industry has evolved – lots of people who have a transactional mindset. They do what they are told, they follow a process… that’s nigh-on impossible to change. However, put BPO staff under the management of skilled consultants and this impossible mindset may just start to be molded.

Consultants will struggle without an As-a-Service delivery model behind them. While BPOs clearly need consultants, the same applies vice versa. Clients increasingly do not want to spend millions on custom engagements – the cash just isn’t there, like it used to be, to reconfigure their operations. However, they will buy managed services that are predictable and have a sustainable value proposition. I have used the term Expertise-as-a-Service for a while now, and it’s making increasing sense as the realities of the As-a-Service Economy continue to unravel.

There is no written curriculum for this industry to follow. Yup – we can rewrite the rule book, folks. We’re really venturing into unchartered waters, so what’s preventing this marriage of business models?

New market entities can chase after As-a-Service projects without the risk of self-cannibalization. This is significant. Let’s just assume, for example, Deloitte purchases an F&A BPO business and launches a spin-off As-a-Service provider business that doesn’t conflict with its audit business. This new entity can bid for brand new As-a-Service deals that incorporate the benefits of RPA, AI etc without any legacy revenue that will get eroded – it can pick off re-bids from legacy deals that have become stagnant, in addition to bidding for “virgin” As-a-Service deals from clients venturing into the model for the first time. Bottom-line – all new business is gravy.

As-a-Service demands the whole gamut of people-process-technology change. The pilgrimage to As-a-Service is all about simplification – people willing to offload the transactional work to focus on higher value talks; IT willing to write-off legacy applications and systems that may have absorbed millions of dollars to keep them functioning over the years; and processes that have become obsolete and need re-imagining to align with providing genuine value.

Clients need to trust providers to give up more… consultants are successful because they build trust. This is what consultants do – they invest in clients to trust them, as trust is all they really have. Service providers struggle to build trust because it’s all about the deal to them – once they have a contract, it’s about meeting the obligations, as opposed to really building that trust. It’s just the nature of the relationship.

The Bottom-line: Change is coming with the advent of As-a-Service, and it might not be quite what you expect

You only need to have a few conversations with key industry stakeholders to realize something isn’t quite right with the industry these days. Many buyers are in denial that they need to do anything different, despite all the disruptive technology emerging; most service providers recognize the disruption, but are more concerned with sounding impressive than actually delivering. Can we really progress in this era of denial and bullshit? Of course not…. we will see a few bold moves to get ahead of this market, and some may well come from this potential marriage of big consulting and big BPO.

It’s high time we brought the HfS show back to our hometown of Cambridge MA this December, where we’ll give everyone a big reality slap around the face with a wet kipper:

Yes, people, it’s time to dial back the rhetoric, stop talking about fantastical things that will probably never happen, and get to the heart of the matter: how can we actually define and realize business outcomes from outsourcing?

This will be a service buyer event, where we have 45 exclusive enterprise buyer seats reserved for the chosen few, and we will wheel in some unsuspecting service provider leaders for our famous face/off debate, where we are going to challenge them on why they aren’t self-cannibalizing, why they all insist on using the same lingo we can barely comprehend, and how they plan to be different from each other when the fog lifts.

We’ll be holding the HfS Working Summit in Harvard Square just down the road from our headquarters. So mark your calendars now:

Defining and Realizing Business Outcomes

HfS Working Summit for Service Buyers

December 1-2 2015, Harvard Square, Cambridge, MA

More details–including the agenda, accommodations, how to apply for registration and sponsors–to follow very soon.

Bookmark our event site to stay up to date! Drop us a note to apply for a seat (Service Buyers Only)

We hope you can make it to Harvard Square this December. It will be a great way to end the year and get ready for 2016. And, of course, we’ll have a little fun, great food and booze while we’re at it.

This will be an invitation only event, but we do encourage you to drop us a note if you are interested in applying for a seat. It’ll be great to have you there to celebrate the year we’ve had and get stuck into some unvarnished debate!

The beauty of procurement is that is was never really geared up for cheap and cheerful labor-arbitrage based BPO. In short, most procurement functions have been cut to the bone in most organizations, and many still rely on fax machines, photocopiers and copious filing cabinets of yellowing contracts to get the job done.

Shipping this stuff off to far flung offshore destinations for a few FTE savings has rarely proved to work very well. However, creating a capability where clients can plug in to a whole new experience of procurement capabilities, category expertise, spend management analytics and gain-share opportunities As-a-Service is now happening for many ambitious buyers and service providers.

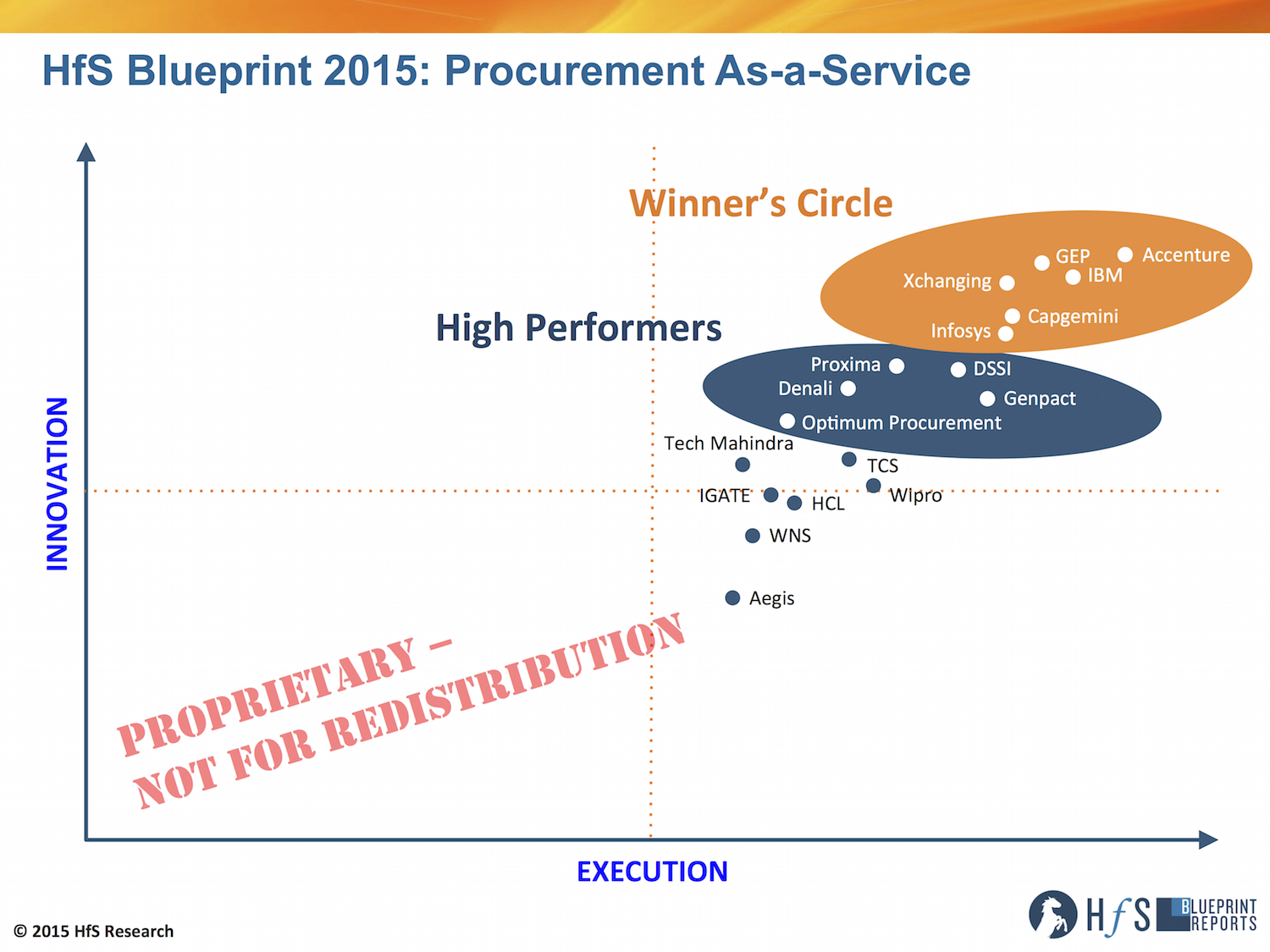

The procurement outsourcing market has evolved significantly since 2013 since HfS launched its first Blueprint, covering 14 service providers, to this new report that covers 18, co-authored by analysts Charles Sutherland and Hema Santosh. This new report is looking very closely at the evolution of procurement services from its legacy outsourcing roots in lift and shift mega-deals, coupled with strategic sourcing consulting, to the increasingly available As-a-Service solution models offered today.

The latest HfS Procurement-as-a-Service Blueprint captures the transition of service providers into the As-a-Service Economy:

Click to Enlarge

What has changed since 2013 in procurement outsourcing services?

If we look at where we are today, or starters, we’re living in a post Procurian world, as its acquisition by Accenture in late 2013 shifted the competitive landscape. Both were in our 2013 Winner’s Circle and when combined they created a market leader by share and by innovation. When we first commented on the acquisition we expected several more would quickly follow especially for Genpact and Capgemini who needed to replace the partnerships they had been developing with Procurian. It turns out that rather than buy at least for now, those service providers who had gaps in capabilities or technologies turned to partnerships instead.

Indeed, partnerships between service providers born out of the transactional procurement market (e.g. TCS, Genpact, WNS) and those out of the technology (e.g. GEP) or strategic sourcing (e.g. Proxima, AT Kearney) are more prevalent in 2015 than they were back in 2013 as service providers construct end-to-end offerings to better compete with Accenture and IBM in particular.

But acquisitions didn’t end with Procurian. Xchanging has followed suite with two more that have revitalized their presence in North America and brought them a new proprietary technology base. While Infosys has accelerated the value of the 2011 acquisition of The Portland Group by utilizing their procurement consulting skills

Internal investments have also mattered over the last several years with service providers increasing their development budgets significantly while also spending on adapting solutions models. In fact over the last two years we have seen previous solution models of end-to-end procurement lift and shift and sourcing consultancy become impacted by the arrival of more modular technology supported service delivery models. While still not the broad norm, this “As-a-Service” approach is setting roots in many service providers and we expect this to increasingly be the norm in the years to come.

So in many ways the last several years have been less revolutionary than they have been evolutionary with a slow and steady acceleration for all end-to-end service providers in the breadth of their offerings and only modest movement in their Blueprint positioning as a result. It should be noted though that the specialist service providers have markedly picked p their game in the last few years and now have a much more prominent place in our evaluation than before.

What matters today in procurement outsourcing

We are seeing slowing growth. Procurement outsourcing while still much smaller than F&A or HR is becoming a substantial multi-billion market and with that we have seen a slowdown in overall market growth from 10%+ a few years ago to something more in the 6% range and so the competition for new clients and renewing deals is greater than ever.

The nature of transactional procurement is changing. Transactional Procurement for the last decade has often looked like a “lift and shift” model supplemented by post transition process excellence projects by service providers. In the last 18 months, we have seen a rapid evaluation of the potential first for robotic process automation and of late cognitive computing as well to this process in order to move away from the labor arbitrage heavy model of the past and to improve overall delivery speed and quality

Sourcing and category management still in demand. Client value creation and service provider differentiation often depend on the breadth and depth of the available sourcing staff in the service provider. The battle to hire and retain sourcing expertise is significant especially as clients in both North America and Europe are looking for the on-site availability of consultants from their outsourcing service providers. Many of the strategic actions undertaken over the last several years by the service providers including acquisitions and partnerships have been made in order to address gaps in organic indirect sourcing category coverage.

Procurement technology and technology management has never been more important. Service provider technology has always played a role in procurement delivery but in the present market with the increased availability of SaaS solutions it has increased again in importance. We have increased the attention and weighting given to technology in this iteration of the Blueprint and spent even more time reviewing service provider capabilities and strategies for technology as well as what it feels like to be an enterprise client today that is increasingly reliant on technology they no longer control to deliver procurement results.

Moving to As-a-Service. We are certainly not there yet, but procurement outsourcing service providers have made extensive efforts over the last several years to further transform their offerings from “lift and shift” transactional procurement together with consulting led sourcing to more modular, integrated, technology based as-a-Service solutions.

Which service providers are taking advantage of this market?

Our 2015 Blueprint Winner’s Circle members who led in our evaluation of the criteria on Service Provider Execution and Innovation are: Accenture, Capgemini, (promotion) GEP, IBM, Infosys and Xchanging (promotion).

Our 2015 High Performers include: Denali (new entrant), DSSI (new entrant), Genpact, Optimum Procurement (new entrant) and Proxima.

So what does HfS expect will happen next as this market unravels?

HfS’ Charles Sutherland, report co-author, having a bit too much of a good time in Kraków last week

Crystal ball gazing in procurement has proven to be challenging over the last few years but let’s throw caution to the wind and make at least three bold predictions about where we will be by the next Procurement As-a-Service Blueprint.

There will be a much greater commercial adoption of As-a-Service in procurement as current trends towards modular processes and hosted software make further inroads.

There will be much more extensive adoption of robotic process automation and cognitive technologies in procurement than we have seen so far. For most service providers these are still at the PoC or limited deployment stage in procurement but we don’t see that being the case for much longer.

Some of the recent partnerships especially for sourcing and category management not lasting the test of time and leading to increased efforts to grow organic capabilities

Attracting and retaining leaders in strategic sourcing and category management will continue to be a struggle for many service providers as that is part of the solution we don’t see diminishing in value or importance anytime soon.

So that’s our take on Procurement As-a-Service in 2015. Please do share your thoughts with us as this important segment of the business process market continues thrive, and…

For you HfS subscribers, please click here to download your full copy of the report

We’re participating in two sessions at the NOA Symposium held at etc. venues, St Paul’s on Wednesday 24th June. We’re also sponsoring the pens (which will surely create an avalanche of new delegates)

Click the logo to get more details on the 2015 NOA Symposium

I’ll be part of a panel with a motley assortment of legacy analysts from Gartner, Everest and NelsonHall as part of “The Outsourcing Debate”, moderated by the Professor of Process himself, Leslie Willcocks. This meeting will surely produce some fireworks as we vehemently debate the most overhyped and underhyped ITO and BPO trends in the UK.

Then, I’ll be chairing a workshop session on “Transitioning to the As-a-Service-Economy.” This is a subject sure to be close to the hearts of many of our readers and we’ve lined up a couple of HfS community friends to co-host with me, John Ashworth, VP Finance Transformation and Systems at Pearson, and Steve Turpie, Deputy Chairman of West Suffolk NHS Trust.

NOA Symposium… all the outsourcing royalty will be there

We’ll weigh the importance of the ideals of the As-a-Service industry vision, discuss how to get the right mix of technology and talent, and evaluate how the painful shift to As-a-Service is/will impact traditional buyer/supplier relationships.

The Symposium will be followed by the NOA Summer Party (we guarantee it will not rain), where booze and entertainment (whatever that is) will be provided for the rest of the evening. I’ll hopefully see you there!

You can book your tickets for the NOA Symposium online via the NOA website.

If you have any questions, you can email NOA Events Manager Stephanie Hamilton at [email protected] or call her on 0207 292 8692.

We’re excited to be heading to Krakow next week to participate in the two-day 6th ABSL Conference from June 16-17.

The great agenda features 80 speakers who will engage the 800 delegates in attendance in discussions about strengthening talent management and supporting regional business leaders for their next global roles in (and beyond) the industry, achieving sustainable and accelerated growth of the sector for the next decades, stimulating innovation and improvement culture, and taking advantage of the technology and client expectations revolution.

With any luck, I’ll get a selfie with Tony. Show up yourself and see what happens.

I’ll be standing on the same stage as Tony Blair (he actually shows up right after our panel discussion where I will attempt a selfie… stay tuned) when I deliver the Keynote Presentation, titled “The Four Foundations of the As-a-Service Economy: The Industry Has Spoken” at Auditorium Hall from 12:40 – 13:00 on Day 1. My talk will look at how the emergence of As-a-Service represents the most disruptive series of impacts to the traditional global services industry that we have ever seen. I’ll share some of our new research, covering more than 2,000 enterprise service buyers in the HfS global community, which paints the picture of what our industry needs to do to get ahead of this impending disruption.

HfS Executive Vice President Charles Sutherland will facilitate a Day 2 Panel, titled “Looking for more fuel! – how to build on current success?” The discussion will focus on the experience of world class GBS organizations, as well as the next SSC trends and opportunities.

Charles will be joined by a group of industry luminaries, including Tom Bangemann, Senior Vice President Business Transformation, Hackett Group; Adnan Behmen, Associate Director GBS, Procter & Gamble; Wojciech Karpinski, Services Head, Global Operations Manager, Infosys BPO Ltd.; Agnieszka Kubera, Managing Director, Accenture Poland; and Magdalena Wlodek, Director Finance Service Center Europe, PMI.

This will be a terrific two days. I hope to see you there!

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.