Moving at Warp Speed into the As-a-Service Economy?

Thanks to all of you who spent a fabulous day with us in Dallas for our first HfS Working Summit, dedicated purely to a joint unravelling of how we can find a way to the As-a-Service Economy.

What struck me was how quickly our industry has genuinely become focused on achieving business outcomes over the past few months – and this is being weaved into many of today’s new contracts and governance performance metrics. The conversation has moved along quite markedly and I view this is a major leap forward for many industry stakeholders to change the way we manage service delivery that isn’t purely based on valueless metrics and squeezing out those last remnants of bloated labor cost.

However, it’s also clear that ambitious enterprise leadership teams are growing increasingly frustrated with their teams’ struggles to progress their capabilities, which will be the ultimate burning platform for many enterprises to make the shift and write off their legacy back office. Here cometh the As-a-Service Economy, where stagnation and legacy will no longer be tolerated…

So what are we learning, at HfS, about the current readiness of enterprises to outsource and leverage As-a-Service delivery?

In short, we’re on a train hurtling towards something resembling “As-a-Service” and we need to make sure we stay on it:

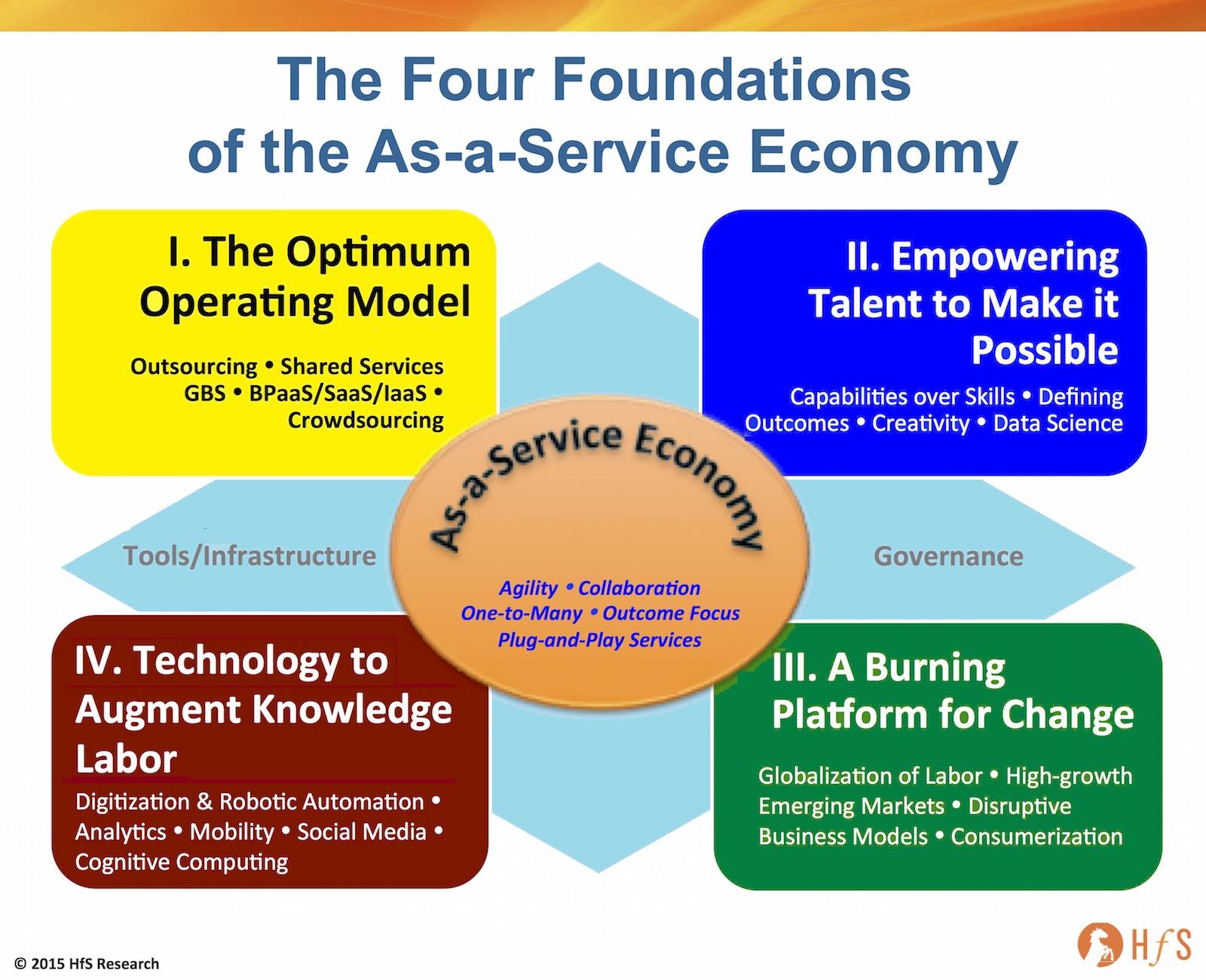

At HfS, we are baking this unraveling of As-a-Service delivery into four distinct foundations:

Foundation I. The Optimum Operating Model: Outsourcing not exploited nearly enough by ambitious enterprises

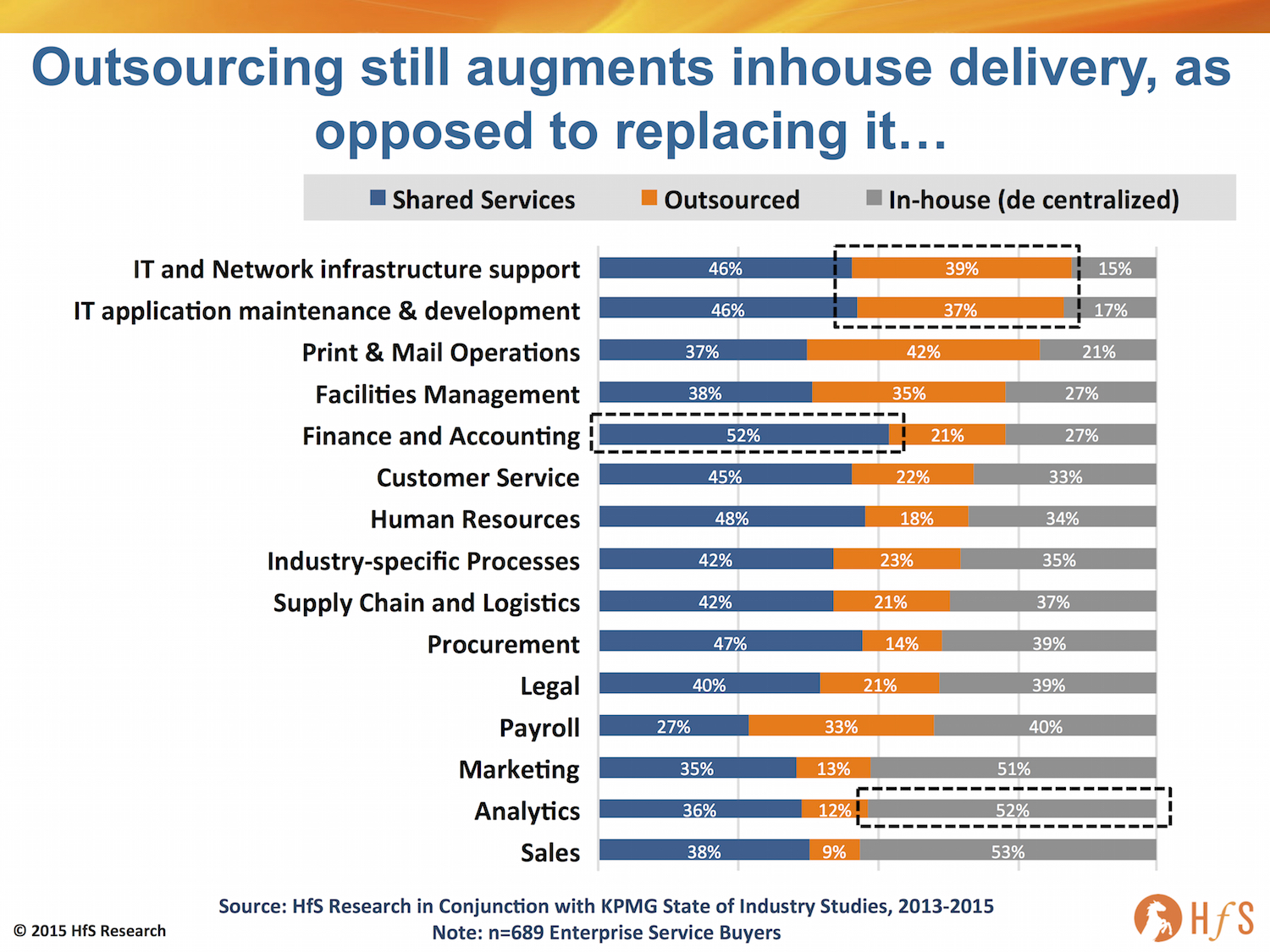

Today, most buyers are still using outsourcing as an augmentation vehicle for most of their processes – filling occasional delivery gaps, but more as a vehicle to drive scale and cost efficiency:

Click to Enlarge

Our new research shows only a third of buyers today view outsourcing providers as a real strategic partner, while half see them as efficiency vehicles for themselves. However, it’s becoming abundantly clear that the desire to shift towards As-a-Service delivery is much stronger at the senior levels, and we believe many enterprises will turn to their service providers more aggressively over time as they simply lack the skills and capabilities inhouse to get them past the traditional service delivery model.

What’s clear in the chart above, which illustrates a view from our recent industry studies with KPMG on how enterprises run their business operations models, is that outsourcing is still predominantly an augmentation vehicle to support business processes, as opposed to the end-to-end delivery of business functions themselves. For instance, less than 40% if enterprise IT s outsourced, 20% of finance and accounting – and only (amazingly) a third of payroll.

When we look at real value-add areas, such as analytics, where As-a-Service focused providers can really help clients, we can see that over half of analytics work is still conducted in decentralized models, with only 12% currently being serviced externally.

Foundation II. Empowering Talent: The Focus shifts from Skills to Capabilities, from solving business problems to finding them

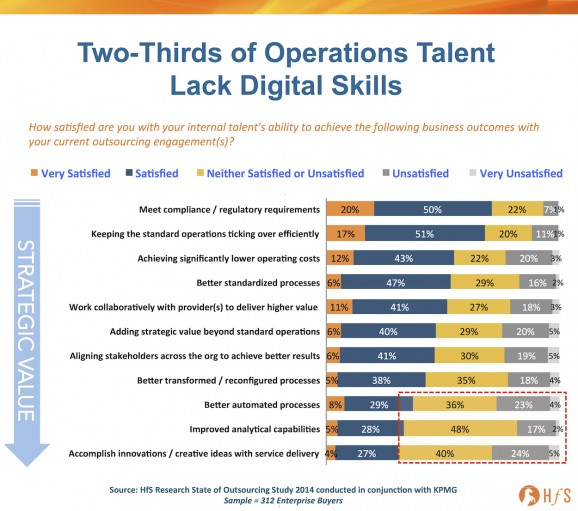

The biggest issue impacting buyers, service providers and advisors in the industry today is the challenge of broadening, not only skillsets of delivery staff and leadership, but changing their mindsets and capabilities.

Our State of Outsourcing study clearly reveals two-thirds of operations jobs are now under threat if staff fail to reorient their capabilities. Simply put, barely a third of enterprises, today, are actually happy with their internal talent’s ability to drive positive outcomes from their analytical and creative capabilities, with their current outsourcing engagements:

Click to Enlarge

This is nothing new; organizations have been trying to reduce their labor costs for centuries, but something feels very different about the emerging digital reality in which we operate. Many of us believed the onset of web technologies would be the big game changer with how we utilized labor, but it actually increased our reliance of humans – many business processes became web-enabled, which necessitated training on new applications and helped us work more effectively – but they didn’t fundamentally change how we operated. The web really just enabled us to run things the same way as previously, except with more global capabilities and much more effective communication and collaboration.

It was this earlier wave of digital evolution which really enabled the great outsourcing boom of the last 15 years, as communication costs plummeted and web applications made it possible to work with people anywhere/anytime. The initial web evolution helped globalize the workforce, but didn’t have as much impact on how we could automate processes, mine vast lakes of data and embrace mobile applications to drive interactions across our employees, partners and customers.

We have entered an era, today, where there is real capability – and need – to change how we run our businesses – from back office transactional processing through to the front office customer interaction: we have tools and apps to target and interpret meaningful data, we have developing software solutions to automate and even robotize processes to mimic human tasks like we never could in the past, and we have all submerged ourselves in a mobile culture where all forms of business are conducted on all types of devices and interfaces.

Perhaps, even more importantly, cloud-based platforms are being developed which allow us to share these capabilities, re-invent the way we run services and process transactions that require such a lesser amount of human intervention and oversight.

Hence, the onus shifts to the capabilities of our talent to add value to their organizations that are insightful to help base decisions; that are creative, which help try new ways of doing things, or targeting new markets; that are innovative, where their organizations can find entirely new ways of competing, or developing unique products or services. Whether they work in finance, HR, marketing, procurement, IT, supply chain, their job is to leverage digital technologies and platforms effectively so they can refocus their time adding value, because the need for people to sit around and fill in spreadsheets all day is being gradually eliminated. People need to do a lot more thinking, and less executing.

It’s less about having specific skills wrapped up in a nice box that can be marketing, such as “ABAP programmer”, or “Vendor Contract Manager”. It’s now about being brokers of capability – people who can multitask across multiple disciplines and find business problems, in addition to solving them.

The Bottom-line: The As-a-Service business world is moving the talent goalposts, and many workers will struggle if they can’t adapt

I truly believe the oncoming wave of As-a-Service is going to be driven by the inability of enterprises to reorient their existing talent to move beyond the traditional transactional outsourcing model.

This talent crunch is already coming. The old safety nets of years gone by have bigger and bigger holes in them – you only need to look at the job ads and the types of skills smart companies are now looking for to understand quickly how irrelevant you could become if you don’t embrace the digitally transforming world we are now living it. It really is time to get with the program, people, or start preparing for an early retirement.

Stay tuned for Foundations III and IV coming As-a-Service style to a screen near you very soon…

Posted in : Business Process Outsourcing (BPO), Cloud Computing, Digital Transformation, Finance and Accounting, Global Business Services, HfSResearch.com Homepage, IT Outsourcing / IT Services, kpo-analytics, Mobility, Outsourcing Advisors, Procurement and Supply Chain, Robotic Process Automation, SaaS, PaaS, IaaS and BPaaS, smac-and-big-data, Social Networking, Sourcing Best Practises, sourcing-change, Talent in Sourcing, The As-a-Service Economy, The Internet of Things, the-industry-speaks

Excellent article. Agree the skills to capabilities issue is becoming critical. Do you see providers really being able to plug these gaps, Phil?

@James – those service providers investing in top talent will always be able to service their clients who are willing to pay for it. The bigger issue in my view, is enterprise clients openly recognizing their shortcomings and developing a coherent plan to define where they want to go. Once they have that roadmap, then they can figure out what types of skills they need – and at which investment levels – to get them there.

So, in short, it’s a chicken-and-egg situation, as most enterprises today struggle from ill-defined business outcomes. They still focus more on the old model of driving out cost through labor models, and while leadership would love to find new avenues for productivity improvements, they simply do not have the talent to help them figure that out. Smart service providers can plug the gaps, but only when those gaps have been identified and the client has the burning platform to invest to fill them…

PF

Phil,

This blog is like a splash of ice cold water on our faces! Not that we don’t recognize the urgency. But, the quicker we understand, address and adopt niche skills, the faster our ability to keep our customers in their businesses.

We are in a game changing era now. It’s going to be hay-day for those who can brim up their skills for various requirements, and will open a huge, distinctive industry of professionals.

We can’t just wait and watch and continue with the legacy work!

Suyog

@Suyog – The fundamental issue is becoming the delta between the desire of enterprise leadership to change, and their middle-management’s ability to make it happen at an acceptable pace. It’s happening in IT, with so much of the routine maintenance, support and development being outsourced and automated. The next wave is that layer of services that require a greater understanding and context of the business, which is where Design Thinking has such relevance. Whether providers can truly step in to help their clients find new ways to operate and think laterally about opportunities / problem-finding is open to debate – some will, while many will talk a big game a fail spectacularly. BPO is still a long way behind IT in this regard – most buyers are still just trying to get the basics right so they can think beyond labor arbitrage, but progress is being made as technology tools and platforms mature and the focus on outcomes versus effort-based inputs is clearly underway for many mature adopters.

PF

Organizations need to control each and every aspect of their business. Outsourcing a capability could mean a lack of internal understanding of that capability and thus loosing the ability to integrate it meaningfully into the operations / strategy of the company. Outsourcing is nothing new. Companies have been outsourcing manufacture of parts all the time. The design (and thus R&D) capability however is still sacred and maintained internally. The question is what is the equivalent to this in services? If you are outsourcing customer service calls for example, organizations tend to maintain the service capability for its high end customers while outsource the low value calls. This way they maintain the top end talent who can help define and design the customer service experiences. Just like design and R&D in old time manufacturing operations.

[…] Part 1 of our Four Foundations, we discussed the challenges and opportunities facing enterprises which are […]

Sounds like an impasse for a while now and the challenge has in a manner of speaking, become even bigger than the previous year.

The more the focus on the various considerations (of talent, process, technology, culture, legacy, alliances, vendors etc.), the bigger it all gets for both enterprises and the service providers. And there are two deltas here; although on the point about enterprise inertia, some would say stating intent and actually charting a course of action are two very different things.

No one disagrees with the HfS/KPMG data and what buyers are saying, as it is indeed so direct from them and evidently these issues are very real, but can enterprises really afford to wait for a vast majority of their peers to reach that point where the answers are visible, matured GICs/SSCs/total outsourced models (IT + functions) are the norm across industry sectors, the new HR/people models have emerged etc.? Perhaps that data focuses on the state of the late majority that will not really the be drivers of change at this point in time?

How are early enterprises scripting the shift from their current stage (imperfect) ops model to the plug n play (future) services model, are they chipping away at obvious significant parts of the transition on this journey first (rather than attempting every aspect of it), whiz. 1. Shifting function by function (simplify, standardize, automate) to a hybrid cloud approach, BPaaS/SaaS model in a manner that business and IT are aligned 2. Re-architecting their internal IT from a common integrated horizontal to a distributed strategic layer + partner enabled consumerized layer? The sub steps along the way, perhaps boosted by some (not all) elements in your boxes II and III?

Sorry….read last sentence as…The sub steps along the way, perhaps boosted by some of the elements in your boxes II and IV?

Phil,

I am curious abut your thoughts on the use of crowdsourcing platform models like Lionsbridge or MechanicalTurk (at a stretch) in the as a service economy. What impact could they have on the traditional outsourcing models?

Anshul