The lifeblood of the IT outsourcing industry has always been application testing – it’s not sexy, but it’s a huge portion of ITO spending – and massively important to the revenues of the major ITOs.

And while much of the traditional app testing market is commoditizing, with advances in remote management and automation, the proliferation of digital apps (social, mobile, analytics) and related technologies are creating renewed growth and market demand for testing. Here at HfS, we have watched this development closely. And, with Tom Reuner on board as Managing Director for IT Outsourcing Research, we thought it high time to take our Blueprint microscope and have a close look at application testing services. Tom worked feverishly over the past couple of months to prepare the Blueprint, along with HfS Executive Vice President, Research Charles Sutherland. The result is a groundbreaking Blueprint report:

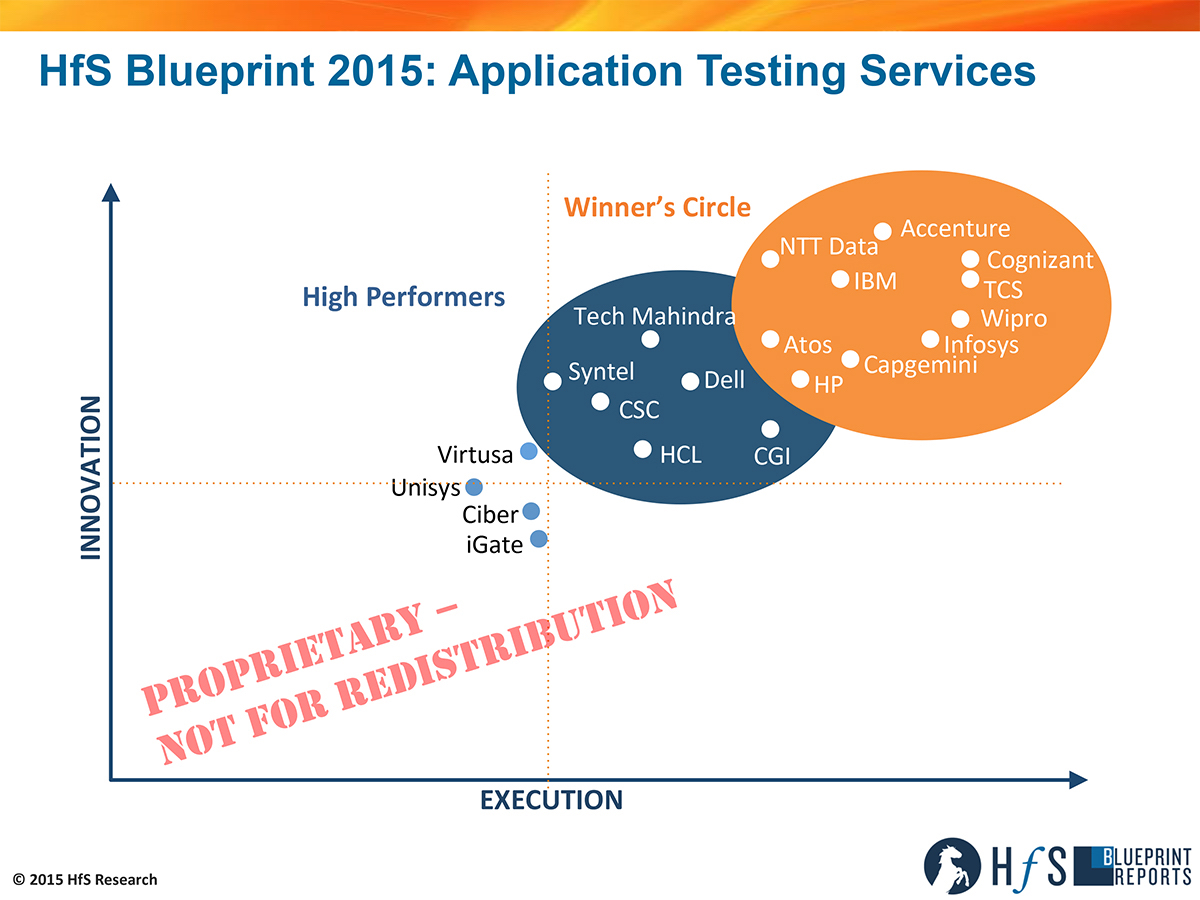

Click to Enlarge

So let’s get an up-close view of the report from the man himself, Tom Reuner:

So what’s new in App testing these days, Tom?

Thanks Phil, in order to answer your question, I have to start by going one step back and outline where the industry is, as there is little reference material from analysts and third-party advisors. The notion of independent testing is evolving where services are not just bundled as part of an IT outsourcing contract but are delivered as a stand-alone offering. But, broadly speaking, testing services lag most IT service lines in terms of mindshare and broader visibility. A lack of investment, immaturity of organizational models, a highly fragmented supply-side, and inadequate marketing top the list of reasons behind this. Or, to put it in simpler terms, it is rare to see testing as part of broader sourcing discussions or conversations on how testing is helping organizations on their journey into the As-a-Service Economy.

But things are starting to change and the maturation is tangible. Increasingly, we see standalone testing outsourcing deals in the hundreds of millions of dollars. Organizational models are evolving with mature approaches, often blending centralized and decentralized concepts. Furthermore, the leading providers are progressively embedding testing into the delivery of business processes, in the process moving up the value chain beyond a narrow focus on tools and technology. And lastly, capabilities around cognitive computing and artificial intelligence are being built out and are increasingly underpinning mature approaches to test automation However, what is still woefully inadequate is the marketing around testing services. In order to get a seat at the table for the big IT decisions, the testing community has to move beyond an emphasis on tools and technologies by building out narratives that resonate with process owners, namely around business case, transfer of assets and people as well as mitigating risks.

You’re considered a real guru in automation these days. Surely, automation is having a huge impact on the app testing space? Or is this simply driving up the quality of the labor component? What’s your view and experience here?

As I tried to explain in my introductory remarks, testing is at a different maturity level than most IT disciplines. So automation is largely discussed as a means to get to higher levels of industrialization by augmenting labor. But it’s not included as much as a means to replace FTEs – as we have seen for instance in the discussions around RPA. Fundamentally, we haven’t had a discussion on disruption in the testing community as yet – and it would be a difficult one because most professionals chose testing as a career and it wouldn’t be easy to retrain or rebadge them.

However, it is striking that there are some strong innovations in test automation that haven’t been leveraged in the broader market. The testing community should be more vociferous about its achievements. Furthermore, leading providers should demonstrate the increasing maturity with capabilities around cognitive computing and artificial intelligence – all with a view to move toward more predictive models. However, the flip side of this argument is that you can’t confine automation to testing. It needs to be part of a holistic approach to delivering services. And the acceleration of the journey into the As-a-Service Economy will exacerbate these issues significantly.

How are the winning service providers approaching app testing services today? What are they doing beyond the bread-and-butter basic operational services?

To differentiate your offerings is, by no means, easy. Much of the technology is based on standardized third-party tools. But the providers we have positioned in the Winners Circle stood out in a crowded marketplace for different reasons. Starting with some highlights in the context of execution: For TCS, testing is a standalone business unit and testing is a door opener for new logos. At the same time, Cognizant is the leading provider for comprehensive outsourcing with strong traction in the banking sector. IBM demonstrated solid traction in complex global deals, including its strong capabilities in the Japanese market. Finally, Capgemini deserves credit for educating the market on comprehensive outsourcing. Looking more closely at innovations, Accenture added a strong narrative on evolving toward predictive testing, underpinned by expansive analytics capabilities, plus the provider has built out strong industrialized vertical capabilities. NTT Data stood out through its innovations around mobile testing. In addition, Wipro embedded testing automation within its overall approach to automation, leveraging tools such as Fixomatic to provide predictive analytics and cognitive systems. These are just some examples and I could have added more providers with similar approaches. But the common denominator of the companies in the Winners Circle is that they stand out due to their vision to increasingly embed testing into business processes and encourage its evolution into a much more strategic proposition.

Tom Reuner, HfS Research (click for bio)

Many of the Indian-heritage service providers built their businesses over the years from app testing support for major Western enterprises. Is this still the case for many? Isn’t it still a major component of their revenue base?

There are various ways of looking at it, Phil. Fundamentally, testing services are high-margin business. As such, they have a high strategic importance for every provider. Suffice it to say the leading Indian-heritage providers are constantly evolving and building out capabilities across the board, including consulting, infrastructure, BPO – you name it. This way they have much more balanced portfolios and can move up the value chain to become strategic providers for their clients. On the other hand, the market for testing services is highly fragmented. There are still many pure plays with a focus on specialist services or specific verticals. So consolidation is unavoidable, as IT services are all about global reach and scale.

With the maturity of global labor delivery at scale, and with these advances in intelligent automation and cognitive computing, how to you see the app testing market unfolding in the next 2-3 years? Is the advent of digital, mobile, RPA, and so forth, driving the need for more testing?

Good question – but not easy to answer briefly. My gut feel tells me that the leading providers will accelerate building out more business-centric approaches. As a result, they’ll provide a much stronger demarcation to the many pure plays. The reference points here are embedding testing into business processes, embracing comprehensive outsourcing and supporting clients in their journey into the As-a-Service Economy.

While the direction of travel is easy to depict, the road ahead will be a bumpy one. For instance, how can providers ring-fence their high margins in view of the rise of Intelligent Automation? Flipping it to the more positive side, the testing community should provide a much more proactive approach in guiding clients on how to test innovative products and offerings that can be As-a-Service propositions. Take RPA and Autonomics as an example: Testing these highly industrialized offerings is paramount, but I have yet to hear how the testing community will rise to this challenge or grab the opportunity. Similarly, in the context of “digital transformation,” the community should switch from reactively stating that it supports mobility, cloud, social and analytics to outlining how it will support business transformation. Much of this is about cultural change. And we are looking forward to engage with the community around exactly these challenges.

HfS readers can click here to view highlights of all our 22 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report: Application Testing Services 2015

Yes, I have been trying hard – and failing miserably – to avoid using the term “Uberization”, but it’s everywhere! Even in the analyst business, where the sharing platform is the Internet and any old whackjob can get in on the act. All you need is a computer and an ability to write remedial English.

The technology and services industry today is awash with individuals whose only professional activity is flitting from vendor conference to vendor conference, with the sole purpose of writing completely non-objective puff pieces praising their vendor hosts in exchange for money (or in the hope said vendors will pony up some dough in gratitude). Vendors are only too willing to pay these people’s travel expenses, in return for such a willing and compliant audience.

Now, there is nothing wrong with this, in today’s free-for-all economy, as long as these individuals stop masquerading as analysts. I can’t proclaim I am a professional accountant, lawyer or hip-replacement specialist, without proving to the world I am trained and can deliver those services adequately, so why should we allow these people to call themselves analysts, when they are not. Do these vendors hire these fake analysts to do real strategic work for them? Of course they don’t – they use them as marketing advocates, and pay them as such. So let’s call them what they are: Vendor advocates.

We need to settle on this correct term for these fake analysts

Once we can all settle on that term, then we can all stop complaining about their tactics, crying foul when we see their blatant pay-for-play. Once they are officially branded as vendor advocates, then they can rent themselves out as much as they like to marketeers willing to buy their services, without having to masquerade as something they are not.

I know several of these individuals (and I am sure most of you do too). They never produce any real research (most simply do not bother doing any and hope noone notices), they usually have limited knowledge (because they do no research) and love the sound of their own voice. Some even plagiarize, make up data and fake surveys (but let’s not go there right now…). However, there is a role for these individuals in the world, but let’s just stop pretending they are analysts.

These vendor advocates play an important role supporting the industry – as long as they are correctly branded as such

But it’s not all bad – these vendor advocates really do have a purpose – they are helping marketing execs in technology and services vendors validate their offerings. They are helping out those frustrated marketeers who do not want to pay the exorbitant prices of the traditional research shops, and simply want to pay someone posing as an industry “expert” to express how wonderful they are.

And there is nothing wrong with this – companies have to pay to advertise to sell product – it’s been going on for centuries. If you are selling technology, you need to hire people with writing skills to communicate to the world that your products and services matter. So why not outsource to someone outside your firm who is at least pretending to have an objective viewpoint?

Bottom-line: You can be a great Vendor Advocate and be loved by industry. So be proud of it, but don’t expect analyst credibility

Anyone who appears in a TV commercial, or writes an advertorial column in a magazine, is an advocate for the brand paying them. It’s credible – for example, you see pro golfers advertising all sorts of products and services on their shirts and visors, but we aren’t offended. Noone cares whether Phil Mickelson uses KPMG to audit his accounts, or whether Shaq O’Neill really does use Gold Bond, or whether Roger from Madmen drives a Lincoln MDX… we love these personalities and our attention is drawn to the products and services they are marketing. It’s the same for marketing advocates – many of these individuals are great people with lovely personalities… there’s nothing wrong with marketing someone’s products or services, just don’t pretend you’re an analyst when you do it!

Sangita Singh is Chief Executive, Healthcare & Life Sciences, Wipro (Click for Bio)

I recall when I founded HfS Research nearly six years’ ago, one of the first people to visit our offices was the calm, but tenacious Sangita Singh – one of the most recognizable and popular faces of Wipro over the last decade.

Since then, Sangita has made a regular habit of visiting us at HfS during her analyst rounds in the Massachusetts area – a location right at the heart of many of her life sciences and healthcare clients. And what amazes me about Sangita is the fact she manages to (somehow) live simultaneously in both Manhattan and Bangalore at the same time, in the midst of all this merger-mania in healthcare.

While Wipro has built a reputation for helping to drive cost savings and provide IT and business process support and capability, Sangita is on a mission to take her firm’s healthcare solutions to the next level, by working with clients and partners to build connections between the many silos in today’s US healthcare system. At the heart of it is how to better serve the patients with the right combination of services and technologies in a more simplified and accessible way. It requires a different way of working both within Wipro, and with clients. It’s a big, bold dream, but that’s what gets her excited.

So when we convinced Barbra McGann to join us to lead our analyst coverage of healthcare and life sciences, I couldn’t resist introducing her to Sangita… and lo and behold the two of them cooked up a little interview for our reading pleasure…

Barbra McGann (Managing Director, Research at HfS): Sangita, your career has lately been a smorgasbord of specialized leadership roles, from an education in engineering, to most recently at Wipro as Chief Marketing Officer, then Head of Enterprise Application Services (EAS), and now, Chief Executive of Healthcare and Life Sciences. What is your approach to tackling each of these very different areas of expertise as a leader?

Sangita Singh (Chief Executive, Healthcare Life Sciences & Services at Wipro): Hi Barbra – it is to be open to listening and learning—from the team, from peers, from management, from the external environment, and to be inclusive. One thing that defines me is my curiosity—my willingness to not take myself too seriously and be willing to learn from anybody and everybody. That provides the input. Then I do three things: First, I carve out a really audacious big bold dream that can be called strategic vision, that I remain consumed by. Then I try to spend hours and hours getting my entire team inspired and on the same page with respect to that dream. Therefore, the second aspect is gathering, garnering and building a team that lives that dream and I think is better than me to be able to execute on that dream. Thirdly, I focus on execution or whatever we have committed to make it happen for my customers, and for my people as well, within Wipro.

Barbra: It sounds like you’ve created an ideal triangle—vision, team, and energy for execution—to apply to healthcare, where there is such an opportunity for change. In general, people have a poor view of healthcare, often describing it with terms like “confusing,” “red tape,” and “expensive.” What’s your vision for the future of healthcare?

Sangita: Fundamentally, Barbra, healthcare is about enriching people’s lives. Clearly, the industry is going through a huge disruption and a lot of transformation in the way healthcare will be delivered, the way it is accessed and how affordable it can be. There are three mega trends that we think are shaping the direction. One is clearly patient empowerment, which includes how patients access and use information through digital technologies. The second is the pay for performance revolution that we are seeing in accountable care organizations, and with population health management to drive the accessibility, affordability, and quality of care. Finally, the third important piece is digitalization, the rapid adoption of which will allow a patient-centric platform to give new access to customers through mobile, cloud, and 3D printing.

Barbra: Technology can be a great enabler, as you know, Sangita. How do you seeing it playing a more effective role in changing the way healthcare is perceived to be more about enriching people’s lives?

Sangita: 32 million new people are coming under the coverage driven by Obamacare. A lot of that is Medicare. In Medicare we have a Software as a Service platform that allows access to people, that allows eligibility, enrollment, and revenue reconciliation to be done through that one platform. Secondly, we are able to build analytics to drive population health management through patient engagement. Finally, in the Medicaid space, we are working with modern platforms that can drive all the business objectives that are relevant for the new Medicaid priorities such as dual eligible. Therefore, we are helping our customers in two ways. One is around changing their business models—how do I digitalize them better? And the other one is as far as the run is concerned—how do I drive automation and application and infrastructure support to run organizations more efficiently?

Barbra: How would you sum up your vision for the role of Wipro as a business process outsourcing services provider in the emerging As-a-Service Economy?

Sangita: Our vision is to build a patient-centric interconnected health ecosystem through solutions and platforms at the intersection of payers, providers, life sciences, and medical devices. I think the big role that we can play is to be able to create the interconnections in the healthcare ecosystem. This used to be fairly siloed. So medical devices would operate in isolation with the patients or largely with the providers. But today with the patient at the center of everything there is a need for the data to get connected, there is a need for interactions to get connected, there is a need for engagements to get connected. We can provide systems, services, and IT that can enable this. To build a very patient-centric interconnected health ecosystem is really our big dream.

Barbra McGann is MD Research, Healthcare and Life Sciences, HfS

Barbra: Sangita, this is some significant change we are talking about with interconnections and digitalization. It’s going to take another many-syllable word: re-imagination—stepping outside of what is it that we are doing day to day, reminding ourselves that this is really all about the patient and considering how create the right process to get them to the health and care they need at the time they need it in way that they can afford to pay for it, or get help to pay for it.

Sangita: And the word that you used, the reimagining, is the most powerful part. Across every process thanks to digital technology at the front and automation at the backend, really every process that touches the patient can be reimagined. And that’s really in essence the huge opportunity that lies before us.

If you see the number of startups that are there that are leveraging cloud in the form of digital technologies and disruptive traditional business models, it’s just astounding. I was just reading about a startup (Theranos) started by Elizabeth Holmes, which could disrupt the diagnostics business, using a drop instead of a vial of blood for tests and taking lab reports on line. So cloud and digital is reality.

I think is very exciting for new age providers like ourselves because of the opportunities it provides and therefore levels the playing field for all. Because it’s new it would be the same for IBM, it would be the same for Accenture and the same for us. So that’s what’s exciting. I think cloud is the best disruption to have happened for any new age service provider.

Barbra: Earlier, you mentioned analytics. Will you tell us a little bit about how Opera plays a role in analytics for Wipro and its clients? It was a big announcement and a very strategic move for Wipro to invest in Opera. How this is playing out in the healthcare industry? What role do they take in helping to realize the vision?

Sangita: Opera has been an interesting partnership. What Opera was known for was building algorithms used in the payer and provider space: in the provider space for revenue leakage, utilization of hospitals, and in the payer space for fraud and abuse detection. They had a number of use cases for payer and provider. Now we are working with them to build use cases for life sciences, largely in the R&D and clinical trial space.

We have also used Opera on the backend for all the service desks supporting business process outsourcing. We leveraged Opera to drive analytics that can help us drive better user experience and a quantum jump in productivity.

Barbra: It sounds like there’s quite a bit going on with clients directly, as well as internally, on Wipro’s own processes and activities around outsourcing services.

Sangita: They have data scientists who can build algorithms that can detect patterns, remove false positives, so on and so forth… really almost any business problem. The constraint that we have if any, Barbra, is Wipro having access to customers where they call us in assuming that we can help them with their business problem. Our brand is more synonymous with cost takeout. And so that’s a big constraint. But once we have worked with a customer and have gained their trust and confidence, then we move forward and proactively propose value added propositions like what we can do with Opera – this is how we define success.

Barbra: Certainly a key change we have seen as the sourcing industry has matured, Sangita, is that partnerships between service buyers and providers bring more long term value to both parties where trust has been established. You have said that personal interaction and networking is incredibly critical. What would you recommend being effective this way in networking?

Sangita: It’s important to learn from anybody and everybody, Barbra. Thanks to the digital world we are no longer as siloed as we were before when you could network only by meeting people physically. Now all of that has been disrupted and you can meet anyone, anytime virtually. In addition, you know there is so much access and information that you can have about who to connect with and how to connect through social media.

Each one of us is unique and we hear and have read this a dozen times but yet we do so little about it. Each one of us is passionate about something, and we have the opportunity to be a thought leader in that area. And I think one should always go out there and network and be known for something. I am still not there 100 percent but it is definitely in one my strategic to dos. And I am learning hard from the millennials on how to get really active and relevant and sort of cool in the digital world as well.

Barbra: You have inspired me to do that, too, Sangita! Thank you so much for sharing your passion for patient centricity and Wipro’s role in helping healthcare and life sciences companies achieve it. We will be watching for more of it online @sangitasingh101 and @wiprohealthcare.

The As-a-Service Economy is all about achieving the outcomes we most want with a great service experience. So let’s look at how to avoid that not happening and becoming legacy businesses that failed to stay ahead of the demand curve.

The perfect anti-example is Subway. Back in 2001, the release of Fast Food nation shocked much of the Western world into realizing we were slowly killing ourselves on pink-slime infused fast food. It was great for Subway as it sold sandwiches that – for all intents and purposed at the time – we thought were a far healthier option than Burger King. And it seemed to taste OK too…

Fast forward to today – people are increasingly aware that chemically-preserved fake colored bread, cheap antibiotic-induced meats and pesticide-flavored vegetables aren’t much worse for you than a greasy concoction of pink slime, protein and french fries.

Coupled with this is the service experience – I accidentally ventured into a Subway the other day (one of those once-in-every-five yearly visits, where you are just so damn hungry and want to avoid the golden arches). The only desired outcome is to subdue hunger – in the vain hope it may be a somewhat enjoyable experience in the process. To cut the the chase, the restaurant was filthy – every single table was covered in food remnants, the toilet stank, the staff were curious life forms from some distant planet… and the sandwich was just lame. Net-net, I had just about achieved the outcome I was looking for, but the service experience was horrible. I will not venture back for at least another five years. Hopefully never.

On the flip side, if my desired outcome was to have a tasty fast-food burger – and to hell with the consequences – I would just have had one. I know exactly what to expect and the experience and outcome is clear – unhealthy tasty food that is enjoyable and fills the hunger hole. So contrast the two outcomes – a nasty sandwich versus and tasty enjoyable burger, that is probably only 10% more unhealthy (source HfS, 2015).

The Bottom-line: Once you lose touch with your customers’ desired outcomes, do something fast to find them again, or resign yourself to a slow extinction

Yum

I don’t want to spend hours reviewing Subway’s income and profitability, as I am sure they have their quarterly accounting revenue model down-pat – they sell cheap(ish) food to people who probably don’t care that much about food, and don’t have much understanding of what bad food chemicals can do to your insides.

But I am sure that even many of their loyal customers are slowly wisening up to the experience, and the brand will eventually need to do something radically different to continue its existence – their stuff just doesn’t taste as good at their nemesis alternatives and it’s not even good for you.

The answer is quite simple – how can they produce a healthier, better tasting product with a less crappy service experience. Oh wait – Starbucks has already figured that out and you can even get a better meal in a Dunkin Donuts or Tim Hortons these days (and that’s saying something). Sorry Subway – you’re legacy and probably confined to the once-great corporate successes that failed to evolve its services experience to meet changing customer desired outcomes.

A raft of luminaries ranging from Stephen Hawking and Steve Wozniak to the figureheads of Artificial Intelligence (AI) at Facebook and Google, Yann LeCun and Demis Hassabis, have signed a petition warning of a “military artificial intelligence arms race” and calling for a ban on “offensive autonomous weapons.”

Meanwhile, among the developer community, the discussion on the ethics and ramifications of AI has been as intense as it has been far reaching. Yet in the discussions around the notions of RPA and process automation, the issue of ethics and the impact on the future of work are (still) largely absent.

A dichotomy of ethics is in play: Outsourcing is viewed as somewhat evil, while labor elimination via technology is barely an afterthought

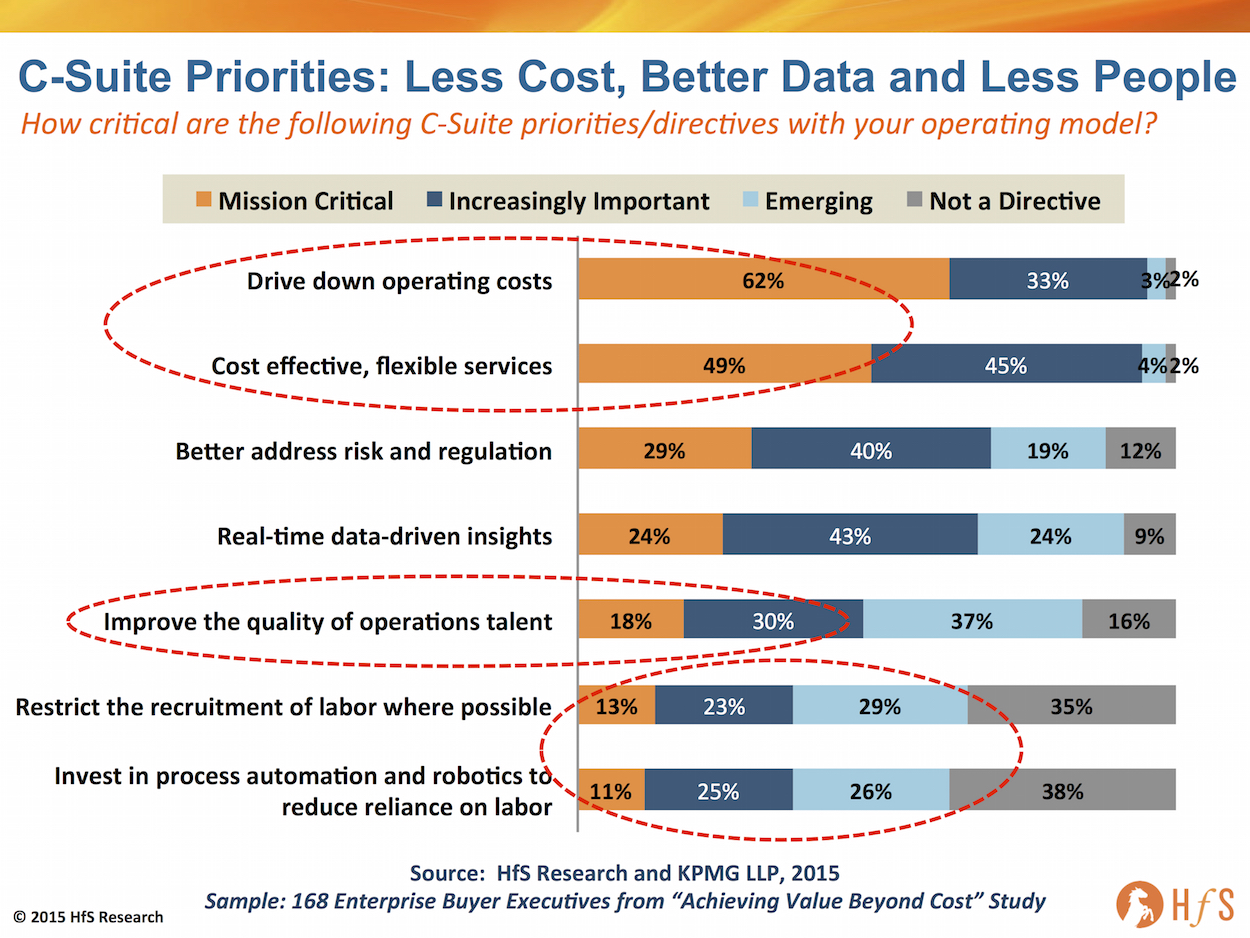

One main observation we, at HfS, are beginning to notice is that many enterprise clients are showing an increasing willingness to invest in technology-based (rather than people-based) solutions. You only have to revisit our Value Beyond Cost study, which we ran with KPMG earlier this year, where we asked 168 senior executives about the priorities of their C-Suites with their operations:

Click to Enlarge

What is startlingly apparent here, beyond the fact that well over 90% of C-Suite directives are obsessed with cost and flexible services as operational priorities, is that less than half (48%) view improving their operational talent as important, 65% are exploring efforts to restrict the recruitment of labor where possible, and 62% are looking, with varying levels of interest, at automation and robotics with the specific purpose of reducing their reliance on labor. The bottom line here is very clear—C-Suites are caring less and less about their people, and more and more about their services.

The big question many enterprises are facing now is not whether to invest heavily in their people. Rather, it is whether to invest in technology to replace staff or use outsourcing partners to reduce the burden of inhouse staffing cost, while improving their access to flexible services. Many enterprises are exploring a combination of the two, or merely leveraging an outsourcer which is using robotics on itself and is willing to pass on the benefits to its clients desperate to move from a legacy labor-centric operational infrastructure.

Suffice it to say, within the context of process automation, the arguments are contingent on the points of view as to the validity of the various approaches and on the assessment on timelines for reaching maturity. Ananth Krishnan, CTO of TCS, offered food for thought at a recent conference where he outlined that in 5 to 10 years’ time we need HR policies for (software) robots. Despite the mainstream narrative that—through the implementation of RPA robots will replace FTEs—Krishnan’s argument was decidedly more thoughtful. In the medium term, future software robots will be a blended reality in the back-office. Therefore, HR policies among other issues need to proactively deal with this development. And crucially, he has started to engage with this stakeholders around these challenges.

While in the context of RPA and Autonomics, the narrative is maturing and we appear to be moving toward emphasizing transformation over simplistic arguments of replacing FTEs, we urgently need to follow the broader developer community and discuss the implications of these approaches. Whether we call it “ethics” or something else is largely semantics. What is completely lacking is how these approaches will impact the future of work.

The Bottom-line: We need to talk more openly about the future governance of artificially intelligent environments

Robotics vendors and service providers need to engage with clients around how all these disruptive approaches will affect talent management as well as organizational structures. Even without apocalyptic scenarios, many job functions are likely to either disappear or be significantly diminished. Equally, we need to talk about governance of these new environments, touching upon ethical but also practical issues. This is not only a necessity for the broader adoption, but also offers high value opportunities.

You can download the POV on this topic, authored by HfS analysts Tom Reuner and Phil Fersht, here.

John Haworth is Chairman of the HfS Sourcing Executive Council (Click for bio)

So what do you do after a rollercoaster career working in ERP software, HR services, sourcing advisory and finally the BPO lead for one of the largest healthcare insurers?

Where do you next take a career, which was centered on traditional services and outsourcing, when all you want to do is challenge the old model and bludgeon a path towards the new?

Of course, you already knew the answer… come to HfS and make some serious trouble.

John has been intimately involved with the HfS community for several year as a service buyer and has long talked to me about his desire to “saw off the legacy”. So when we reached the size and need to have a dedicated leader of the buyer rebels, armed and ready to hive off the turgid, valueless detritus of yesteryear’s transaction-dom, there was noone better to ask to fill the spot. And he loves it so much he’s already written more research pieces than the analyst team in his first month on the job.

So let’s find out a bit more about John’s plans for the HfS buyers council and a little about himself too…

Phil Fersht (CEO, HfS): Good afternoon John! You took the decision recently to join us at HfS Research and we’ll talk about that in a minute, but first could you could give us a bit of your own background?

John Haworth,Chairman of the HfS Sourcing Executive Council: Like a lot of people I think I’m in this industry somewhat by accident. The reason it wasn’t by design is because to some degree the industry as we know it didn’t exist, so there wasn’t anything for anyone to aspire to become part of. I think if you go back twenty years you’ll find strong BPO examples starting to show up. But the seeds had been planted in this industry before that, largely by ITO players and “service bureaus” like ADP or the Sabre reservation system, for example. There has been time sharing in the IT world for a long time, but moving business processes outside of the walls of companies became a rather noble ideal; and I happened to be around when I think some of the very first examples of that were playing out. When I was the co-founder of the HR outsourcing business at Fidelity, there was not a lot of company in the market, and we were essentially inventing a category, including broad HRO—payroll, benefits, HRMS, talent, etc. There was not a lot of company in the market at that time in the other BPO categories, Accenture being the most developed.

We actually co-branded an offering that we put in the market that was one part business process from Accenture and one part Fidelity’s capabilities in HR systems for defined benefit and defined contribution plans. We were ahead of the market in that, but I think we both took away from each other what could be learned at that phase of the industry’s development. As I said, this was about 20 years ago by now, so, by now, we all have lots of experience. We could not have imagined how broad and deep this model has become.

I’ve had the good fortune of being in a position where all of the aspects of the business become a career for me, because I’ve kept it interesting by moving from the sell-side to the buy-side and then as an advisor in-between. I’ll tell you, this is one way to continually learn and also develop a much deeper appreciation for what the realities are on the other side of the table, which I think is incredibly important to the industry in order to advance its overall success. It is, after all, a model of trust and faith in the other party to live up to commitments. Until you have sat in the other seat I don’t think you truly appreciate what can and cannot be moved in any given deal, or in any given business model.

Phil: So what made you decide to join a company like HfS at this point in your career?

John: I’d say two things. One, it’s the right time in my career to take a step back and reflect about not only where the industry has been, and two, to participate in a positive way with where this blossoming industry is going.

I think it’s an exciting time right now, as we’re seeing the rise of truly global markets in labor, in intellectual property and in the supply chain of services, sort of broadly defined. If you combine that trend toward the ubiquity of connectivity and computing power, with the ability to add value at the individual and small organization level, you see that we may be on the verge of something quite big. This could be a very great opportunity area for companies around the globe to be born and prosper in a very short time. So it’s a very interesting time to step back and be more of an advisor, to address this latest and largest wave with the insights born of the experiences that I gained over time.

To help anticipate where the challenges might arise and what we can do about them is a service that those of us that serve as researchers and advisors can continue to do in favor of this industry. It’s always fun to be involved on the leading edge things, and that’s why HfS was attractive to me. Because I’ve identified with the mission of HfS since it was born on the web and as blog, and I’ve seen the impact of community on both understanding the market more completely, and now even helping to shape its next phases. Why? Because 100,000 people thinking generally around the same subjects are a lot smarter than any one person or any group of people usually are. No one has a monopoly on this kind of knowledge—but to be able to participate and guide this explosion at the source, where a lot of people are thinking original thoughts and having similar insights, is something that HfS is accomplishing. And I believe this is the way that we are really going to propel knowledge forward, in the world of the future. Crowd-sourced genius, if you will.

Phil: John, you’ve taken on the role of Chairman of the Sourcing Executive Council at HfS, representing the service buyers in our global community. With the big event coming up in Harvard Square at the end of the year, can you give us some flavor about the theme and what we can expect?

John: I’d say that one of the biggest things we’d like to do right now is establish the buy-side of the HFS community, as a more far-sighted, collaborative, and motivated group. We want to bring out and respond to buy-side leaders who have largely kept to themselves, lacking a forum and the trust factor that our community has been able to develop. I think a lot of corporate people have had private thoughts about this industry, but if HfS can convene these people and help to draw out what’s really on their minds, what’s working, what isn’t, what’s troubling, what the future needs to look like—this would be of great value to service providers and industry innovators.

In our events, we usually succeed in focusing our buy- and sell-side leaders—also advisors—on a very important topic area that really hasn’t been developed very deeply elsewhere. So the December event (Defining and Realizing Business Outcomes: HfS Working Summit for Service Buyers) is meant to crystallize our current concern (as-a-service and its broad implications) before a room filled with some of the smartest people that we can assemble—and the nicest people as well, I would add—who are community-minded and would really like to take this industry to the next step. We will all be focused on this question: How do we deliver business outcomes to the corporate buyers, in a way that keeps the industry healthy and evolving? In this time of rapid change—and even radical change—how do we fairly balance out the views that we get from sell-side, buy-side, and the concerned intermediaries? HfS events have proven to be a unique and valuable forum for sincere participants who are full of ideas and full of valuable experience. We intend to build on that tradition with more events, and more challenging topics. Harvard Square from December 1 -2, 2015 is the kick-off for this new emphasis.

We will be about outcomes. This will come from coupling the real world experience on the buy-side, with what it’s like to actually operationalize some of the available leading edge technologies and innovations. We will explore how to fairly price some of these things. It is all part of creating workable outcomes—I think that buy-side people really need to have a rallying point to come up with a kind of jointly articulated set of agreed upon norms, and agreed-upon beliefs, at least for the near term, about what’s really needed versus what might be on offer from the sell-side. It’s all about market efficiency at the end of the day, and that’s to the degree this market becomes efficient it will continue to prosper. These are the outcomes that we aspire to and that can only occur in the atmosphere of trust and collaboration that characterize HfS events.

Phil: How would you, John, compare the dialogue that we’re having today to when we started doing these buyer summits four years’ ago?

John: Phil, I think outwardly some of the questions look the same, and perhaps they always will. How do we deliver value? How do we develop trust? What are the mechanisms that we use to advance the aspirations of both sides? Those are, let’s say, contracting norms, contracting approaches. Some of that looks the same and some of the ideas look the same. What’s changed, what’s new and different I think is this technology explosion we are living through, and the continual rise of social, mobile, and cloud-based apps and services. The sophistication of the technical environment that everybody lives in, is just sweeping through everything and it’s changing everything. It’s turned the outsourcing model into something that is forced to change, but in ways that I think that HfS has characterized as the emerging As-a-Service economy. We have been leading the way in understanding implications of the merger of new technology with the old-line outsourcing service ethos.

Today, what was formerly called outsourcing is largely migrating to the As-a-Service model, which combines social, mobile, cloud, intelligent applications with processing and support workforces that enable the new outsourcing model. That’s where outsourcing has gone and that’s where outsourcing is going to continue to go. This is a shift that I think we all recognize, and while some of topics we address outwardly look the similar to those in prior years, the context in which these things are happening has changed drastically. Our expectations of outsourcing have to change as well. So I think this is very exciting time to be convening the buy and sell-side in a way that, to my knowledge, nobody else is doing in the market.

Phil: Tell us a bit about some of the exciting presentations we got to look forward too, particularly the Keynote that you’ve arranged for us, John.

John: Because we’re having an event in Harvard Square, where HfS is headquartered, and a lot of us have been associated with the Harvard and MIT environments over the years, we thought it would be a good idea to try to ground some of what we’re doing at least with a smattering of an orientation coming from the Harvard Business School! We’re delighted to have Dr. Francesca Gino as our Keynote speaker. Dr. Gino is of special interest to us because her specialty is negotiation, especially in the psychology of negotiation. If you break down what I said earlier about where we are as an industry, and how we need to collaborate in order to create satisfactory business outcomes in an environment that is radically changing on both sides, it is clear that progress will demand evolved negotiations between buyers and sellers. These will probably look different than the relationships that existed in the past and the negotiations that existed in the past.

So bringing our conference attendees into the presence of someone who’s thought deeply about the psychology on both sides of the table, and what it takes to really understand each other and make progress, something that seems very apt to us. We’re delighted to have Dr. Gino open our event and establish the tone for what we hope will be the new era and the sort of crowning glory of the HfS “insight machine.”

Phil: The crowning glory! Absolutely love it! Good. So, any final thoughts from you, John, as we hurtle towards the end of the year, and some of the things we can expect to from some of the thought leadership that you’re going to be providing?

John: I think, Phil, one of the things that I’d really like to do is, as I was suggesting earlier, give voice to the buy-side in a way that isn’t my voice, but it is a collective voice that starts to be actionable and useful to the sell-side. So that we’re not wasting cycles, wasting each other’s time. I think what emerges as the sine qua non of the world of the future, if you will, is that change happens and it happens very quickly. So there is an opportunity for us to make the market more efficient. We can make sure that that the sell-side isn’t making errors with their offerings and that the buy-side isn’t buying things that aren’t real, or that don’t matter or that will lead them down the wrong path.

We’re doing a real service to the industry to the degree that we can inform the industry and help them make smarter decisions faster in this dynamic environment. The entire industry—both buy- and sell-side—has to deal with the doubling time, if you will, of change in the environment. We will deliver the real service to the market, which has always been the goal of HfS, if we can help the industry as a whole make better choices, faster. I think we really want to rise to the occasion here and be the one research and analysis firm that is aspiring to do this and it is actually able to do this because of the methodology that we perfected, our strong community, and our collaborative events. I think that is going to be where the better answers are coming from.

Phil: Good stuff. We’re excited to have you on board John, and I think as the excitement grows towards the event at the end of the year and the ones beyond that. Will be hearing a lot more from you. So thanks very much for your time today.

Infosys CEO Vishal Sikka talks to HfS on his first year in charge

So… one year into the new job and Infosys’ Vishal Sikka has managed to perform a task noone thought possible. He’s dragged a once-famous Indian-heritage IT services firm – kicking and screaming – out of a maddening tailspin into that dark sinkhole of legacy-ness that is scaring the life out of today’s services industry.

The reason for this is quite simple – he never brought with him a baggage of legacy services culture, where the common practice is to:

1) Copy what all your competitors are saying and try to out-bullsh*t them;

2) Hire cheaper, younger staff and gut the middle layer;

3) Sugar-coat every ADM, Infra and BPO renewal with terms like “digital”, “transformation”, “automation” and “outcomes” etc., when none of these things were really included in the actual contract, but made nice additions to the press release.

Vishal just gets to the point with a refreshing and honest perspective about what his firm needs to do – and is already making shrewd investments in critical areas, such as Panaya (automation) and Skava (digital). He’s also been growing the traditional business, with Infosys just reporting its best quarterly revenue growth for 15 months (4.5% year-on-year), and overseeing several new $2Bn+ sized engagement wins in the last 12 months, with the likes of Allied Irish Bank, Deutsche Bank, NSW State Government and ICA Gruppen in the last 12 months).

The business is stable, growing well again in an industry where many competitors are scrambling all

over the place trying to find renewed direction and focus. What’s more, the management bleeding has stopped and there is a distinct new energy and passion around the place from everyone you meet.

However, where Vishal is really impacting the culture of Infosys is by driving a renewed culture, based on his Design Thinking principles, that is exciting his staff. Design Thinking is real – it’s something delivery staff, account managers and senior executives can all relate to, understand and embrace. Rather than confuse the living daylights out of people, he talks about real business challenges and how they need to be addressed. And this coming from a guy who has a Phd in Artificial Intelligence… talking real business issues to real people is quite the achievement. So we caught up with Vishal is his Silicon Valley start up-esque collaboration offices in Palo Also to hear first-hand his year one Infosys experience, and where he wants to take things next…

Phil Fersht (CEO, HfS): Vishal, it’s good to be with you here at Infosys. You’ve been CEO now for about a year, so I thought it would be a good time to check in. HfS has done a considerable amount of research into Design Thinking and how it aligns with services outcomes. Can you bring me up to speed on how Infosys is faring, with your own brand of Design Thinking?

Vishal Sikka, CEO and MD, Infosys: Thanks, Phil. It’s great having you here. We started teaching Design Thinking at Infosys back in October of last year. We brought some of our trainers here to the Institute of Design at Stanford—the d.school. Then members of the d.school faculty went to our corporate university in Mysore and started training our people.

When I say training—this is not like some guy watching a video on Design Thinking. These are one or two-day immersive sessions, where people are hands-on and actually build things. As much as possible we try to get the d.school faculty directly involved. This class has now been taken by 36,000 employees. I’m told this is by far the largest rollout of Design Thinking education in history. The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane.

So it is not a center of excellence, where you have three, four people who understand Design Thinking. This is 36,000 employees of the company who understand what it is and practice it.

We are now creating customized training for project managers in our delivery organization. 22,000 of our 36,000 people are in delivery, and 3,000 are project managers in delivery. So we’re creating a special program for project managers to be able to bring Design Thinking into the ongoing work that they do. So in my view we are by far the biggest adopter.

Design Thinking is happening with clients, too. This morning before you came in here, we were doing some Design Thinking work with the German utility. We’ve had about 36 or 37 customers for workshops here in our Palo Alto office in the last nine months, and of course others around the world. In fact, I would have liked for you to meet Sanjay Rajagopalan who heads up our Design and Research team, but he is doing Design Thinking workshops with clients in Australia this week. We have a pipeline of 100 clients interested to do this.

These workshops are not focused on best practices. When we think about “best practices,” hidden behind that phrase is the reality that this stuff is already known. Known problems are really yesterday’s.

But then there are things in life that are unknown. So how do you go after the unknown?

We had a very, very large consumer products company here, which among other things is very famous for chocolate, and we talked about how to deal with the demonization of sugar. There isn’t a demonization of sugar package available for SAP or from Salesforce.com. There isn’t a best practice sitting there somewhere. You have to think about this.

All our lives our education system teaches to do problem solving. Nobody teaches us problem finding.

And Design Thinking is a methodology for problem finding. So that is how we see it.

Phil: So you’ve done this all in a year?

Vishal: Nine months, actually!

This space (pointing to the colorful Palo Alto office which sports writable walls and modular works spaces) and all the new spaces that we are building, they are all designed like this. These are design spaces. These are flexible. In the Bay Area, we have 3,000 people working at various clients. And we had a long conference call about Zero Distance on Monday night. This whole area was opened up and all those tables were moved here, people were working from this corner and there were a 100 people in that area. We had a giant video conference in there.

Phil: Can you talk a little about “Zero Distance”, Vishal?

Vishal: Zero Distance is about innovation. Innovators aim to maximize their relevance by reducing the distance to the user, to code, to value. I have asked everyone at Infosys to focus on getting to Zero Distance, and bring innovation to every ongoing project.

For example, Abdul Razack has a team that is doing IIP, the Infosys Information platform, which is based on Hadoop. Abdul shared with me yesterday some incredible things that they have achieved on open source technology, solving some extreme analytical problems. We have the Infosys Edge team doing new product development. And we have many teams that are doing innovative things. And they will continue to do their thing and bring breakthroughs to life.

But if innovation is done in these small pockets—like in Abdul’s team, Sanjay’s team or Sudip’s team—we’ve missed the point of innovation. Innovation has to come from everybody. It has to come everywhere. And this is why I say, “The Innovation Department in Infosys is Infosys.”

Right now we have 8,500 master projects that are going on in the company. This is the lifeblood of the company. Infosys at the end is a project company. So these 8,500 projects represent the work that we do. And we started this program to basically bring innovation to all 8,500 projects. The 8,500 projects break down into 35,000 sub-projects.

I made a straightforward five-point template about how to bring innovation to every project. And it has just taken off virally. And we do these sessions with teams where we share some amazing thing that our team did. And customers are already starting to see that.

Phil: So when you look at everything you’ve achieved in Design Thinking so far, what would you say is the critical ingredient to finding what’s not there?

Vishal: First of all, you have to have the desire—the instinct—to look for it.

I did a survey when we crossed 25,000 Design Thinking-trained members of the Infosys team. I knew at that point that this was a big moment. When we hit 25,000, roughly 12,500 were freshers—young minds just out of college. And 12,500 were the senior folks.

It was astonishing to see the spreadsheet. I was reading this thing and I was just moved. Of course one thing that was shocking was they had put this in two tabs, the freshers and non-freshers. And the older folks, their responses were always three or four lines long. And the one’s from the freshers were terse—less than one line long. Like text messages.

But the sentiment is exactly the same. There were only three questions. How do you bring Design Thinking to your work now? What has it changed, etc.? The answers from the senior folks, said it had opened up their creativity: “It is like I have seen the light, it is like I can think again. I forgot that I had a brain,” stuff like that. Amazing responses.

One fresher wrote that he went and fixed his mother’s sofa because he had done Design Thinking and because the sofa was broken. And he said, “Let me think about how can I fix the sofa.” I was reading that thing and I said, My God! It was astonishing: this is actually changing not just how people work, but how they live.

Of course it is too early to know what all this means. In the last two months, we met a few clients who tell me that there is something going on. One of the huge banks on the East Coast told me that suddenly because of the Zero Distance thing, innovation is inserted into every project. They said that it appears that the quality of work has just gone up.

We are also by the way bringing Design Thinking to our RFP process. Every response that goes to an RFP of more than $50 million now goes through this team.

Our HR team works like this. They redesigned our performance process. We just finished our promotions and they went through this thing. So it is everywhere.

It is very early, but the result of all this will be quite fundamental I believe.

Phil: So clearly, Vishal, this is having an impact on Infosys. Do you think this will have a ripple effect on a lot of the other Indian-heritage service providers?

Vishal: It will have to, it will have to. I think it is inevitable, because this thing about problem finding and problem solving, I personally went through this when I first came to Stanford.

Even though I had gone to Syracuse for my Bachelor’s degree, I still had grown up in India and was trained to do what I was told. So when I came to Stanford and I went to my advisor, and I asked him, “What do you want me to work on?” And he said, “I have no idea.” And it was a shock to me, so I said, “What do you mean? What will my PhD be on?” He said, “You figure it out.” And I told him, “No, you are supposed to tell me what problem I work on and I am supposed to work on that.” He said, “No, if this is what you thought then this is not the right place for you. You are supposed to find your own problem, we are supposed to tell if the problem is good enough or not. Then you solve that problem and then we tell you if the solution is good enough or not. This is how it works and if this is not what you thought, then you are in the wrong place.” He said this to me bluntly within one month of coming to Stanford.

And I thought they had a catalog of open problems and I would work on one of these. So that really put me into a tailspin.

Narinder Singh was a research associate there and he told me, “Yeah, people spend years looking for a problem.” He said, “Remember that guy Andrew?” Andrew was in the seventh year at the time. He said, “He still doesn’t know what his topic is going to be.” I said, “What the hell has he done for seven years?” Turns out this happens all the time. Either you luck into it and you find one right way or sometimes you spend years finding it.

So then I saw a talk by John McCarthy, the father of AI. And in that talk he made a very interesting statement. He said, “Articulating problem is half the solution.” So I talked to him after his lecture. I said, “What did you mean by that?”

He explained. He said, “Look, you know, most of the time we don’t articulate the problem right. And he was talking about it in the context of AI search. He said that when you frame the problem right, you have basically an idea of how the solution is going to work. I though this was very interesting.

And I talked to Bob Floyd who was another professor in Computer Science, also an A.M. Turing Award winner. He wrote the Floyd algorithm for graph traversal. So Bob Floyd told me that, “Oh, that is not enough.” I said, “This is what McCarthy just said—that articulating a problem is not the solution.” He said, “Of course, he’s absolutely right but it is not enough. I articulate the problem, I solve it, then I go back to see if I can rephrase the problem now that I have solved it. Then I re-solve it. And then I go back and rephrase it until I can no longer improve the solution. That is when I know that I have found a beautiful solution.”

I realized that there is so much to this problem finding, problem solving thing that I never thought about. In those days I read the books by George Polya, called How To Solve It. And actually Floyd’s algorithm that Bob Floyd wrote, was his seventh attempt of solving the same problem.

As an Indian kid, who grew up dutifully doing what I was told, this was my introduction to opening up your mind to see.

And here’s how I found my problem. I found it within a year.

Somebody told me to look at what interests you, what excites you. And I was reading many PhD theses that I found interesting. I quickly realized that at the end of the PhD thesis, people will write about the things that they left unfinished. I was reading Karen Myers’ PhD thesis and she wrote three things that her approach could not do. And I thought that this was something interesting. I was very excited by her area anyway, which is why I had read her whole thesis. When I saw those three problems, I went and I talked to my advisor and I said, “I want to solve these, I want to find an approach that doesn’t have this three problems.” He thought it was a good idea. That is how I came to my PhD thesis, based on the weakness of Karen’s approach. And one of the projects that was a part of my PhD work was Center For Design Research in Stanford.—the precursor to the d.school.

It was a part of the mechanical engineering program, and Mark Cutkosky was the professor there. He used to collaborate with my PhD advisor, and we did a bunch of projects. One of the projects we worked on in 1992 was called Design World, which was about how do you design things. So that is how I got into this whole thing. And I brought into wherever I could.

So you see I had been through this experience of problem finding and its importance myself. As important as it is to see what is there, it is as much or more important to see what is not there. This is why we’re doing what we are doing.

Phil: Vishal, thanks for sharing your current views with our readers – am sure many will appreciate them!

If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life…

However, iet’s be honest here – who really cares about these taxi drivers being forced to improve their services, clean their cabs, clean themselves, start using credit card machines and even (on occasion) help you with your bags? The fact is, unless you are a legacy taxi driver, or related to one, you’re most likely delighted they are being forced to get competitive and improve their services.

It’s the same with Spotify / Google music – unless you are in the business of selling music, most people are ecstatic they can now get all the music they desire for $10 a month or less, without having to spend a fortune on CDs, with the hope that there’s the odd good tune. And there’s Amazon versus Best Buy, there’s Airbnb versus Marriott, there’s Netflix versus Comcast, and so on. Moving to our industry, there’s Onesource Virtual versus NGA, there’s ZenPayroll versus ADP, Workday versus SAP, there’s software versus people, there’s offshore people versus onshore people, there are robotically automated solutions versus people, there are self-learning machines versus people, in fact, every advancement in services we look at today is all centered on less people… and delivered As-a-Service.

And like the happy world of taxi customers now getting a better and cheaper service for their money, there are many business leaders who are only too happy to get cheaper and better business operations, because they can reduce their reliance on people. If you’re not an employee who is being replaced by a piece of software (although it’s widely assumed we will be someday), the chances are you’re happy your firm is becoming more profitable and doesn’t need to rely on so many bodies to keep the lights on. Just revisit our Value Beyond Cost study we ran with KPMG earlier this year, where we asked 168 senior executives about the priorities of their C-Suites with their operations:

Click to Enlarge

What is startlingly apparent here, beyond the fact that well over 90% of C-Suite directives are obsessed with cost and flexible services as operational priorities, is that less than half (48%) view improving their operational talent as important, 65% are exploring efforts to restrict the recruitment of labor where possible, and 62% are looking, with varying levels of interest, at automation and robotics with the specific purpose of reducing their reliance on labor. The bottom line here is very clear – C-Suites are caring less and less about their people, and more and more about their services.

The big question many are facing now isn’t whether to invest heavily in their people – it’s whether to invest in technology to replace staff, or use outsourcing partners to reduce the burden of inhouse staffing cost, while improving their access to flexible services. Or use a combination of the two… or use an outsourcer which is using robotics on itself and is willing to pass on the benefits to its clients desperate to move from a legacy labor-centric operational infrastructure.

The Bottom-line: In the The As-a-Service Economy, we only care about achieving our desired outcomes

Here’s the nub of the argument, while people like Hillary Clinton want to turn back the clock and protect the legacy job-for-life, the vast majority of people really do not care that labor forces are being disrupted, along with legacy business models and obsolete practices. Today’s world is all about faster, cheaper, more accessible services – and to hell with any obsolete process, system or person which gets in the way of convenient and affordable As-a-Service models.

People care most about enjoying the outcomes of what they pay for, not the efforts made to achieve those outcomes. Expenditure on services is increasingly related directly to outcomes, not a fixed tax we have to pay for a standard service. Personally, I always pay a limo driver $10 over the norm to drive me to the airport. He picks me up in a Cadillac, hangs up my suit, gives me a bottle of water and a newspaper – and only makes conversation if I want to. My desired outcome is a relaxing journey and the extra cost is worth it – and he wins my business everytime and I refer him to all my friends and colleagues. Now that’s one way to win over the Ubers of this world – people will pay when the outcome is what they want. Welcome to the uncaring economy where is all about the outcome…

And this isn’t some traditional HRO play, it’s KPMG making a serious investment in Workday delivery across both HR and Finance & Accounting. KPMG already claims to be the transformative partner for 45% of the world’s Workday financials rollouts… now it is playing with the leaders in Workday based HR delivery, namely OneSource Virtual, Deloitte, Accenture, Collaborative Solutions and Meteorix.

Does this mean KPMG is now an HR-as-a-Service Provider?

Yes it does. The firm has realized it has to be in the managed services business to support the emerging SaaS offerings across technology implementation, post go-live support, transaction business processing and higher value services, such as organizational change management, workforce analytics and ad hoc strategy needs… in an on-demand model. It also knows it needs to be in the position to provide these on-demand capabilities around several core HR SaaS product suites, notably Workday, Oracle HCM and, ultimately, SAP Successfactors.

So can KPMG lead the HR-as-a-Service market?

KPMG can certainly compete against the consultative global leaders in HR, most notably Deloitte, Accenture, IBM and Mercer, while also having serious capabilities to spar with the emerging niche service providers, especially where clients have global requirements at scale. With this Towers Watson deal, HfS estimates an additional 150 Workday specialists are being added across United States, United Kingdom, China/Hong Kong, Canada, Singapore, and the Philippines to add to KPMG’s current HR practice of ~600 practitioners across 18 major global countries. This is now a serious global player, which can pivot impressively across both finance and HR domains around the leading SaaS platforms. With this deal, KPMG also assumes ownership of both the famous Towers Watson HR Service Delivery and Technology Survey and Forum, which it can quickly absorb to enhance its own brand credentials and domain leadership in HR-as-a-Service.

The Bottom-line: The ambitious consultants are moving into As-a-Service, so what are the next moves we can expect?

Accenture never veered from being a service provider, in addition to a consultant, and now reaps the rewards for dovetailing the best of both worlds – managed services, global scale and scalable skill. Deloitte, KPMG and PwC have claimed, for the last two decades, to be consultants and audit firms – and not managed services providers (even though Deloitte has always had a few discrete offerings that smell a lot like managed services).

Now, KPMG is moving into As-a-Service delivery, with a particular Workday flavor that is clearly the best starting place with the level of global demand for this offering. The next move will surely be it continuing to build a Finance-as-a-Service capability around the emerging Workday financials management suite that is attracting major interest from CIOs and CFOs.

Accenture and Deloitte will be nervously watching this move, not to mention several traditional HR service providers, such as AONHewitt and NGA, which are trying to figure out where (or whether) they truly belong in this As-a-Service business. Accenture has done an impressive job honing its HR-as-a-Service delivery around Workday and SAP Successfactors (among other SaaS offerings), while Deloitte is still clearly stalling on whether or not it is in the As-a-Service HR business, versus merely being a consultant – and may now be thinking that KPMG is stealing its thunder in the space. Meanwhile, we have a whole host of feisty new-generation As-a-Service providers, such as Aason, OneSource Virtual, Meteorix and Appirio, which are unraveling their gameplans to stay ahead of this evolving space.

Consolidation is going to be the next step for many of these service providers – the brave will stave it off, some will take the exit money while they can, while there will be some legacy players who panic and make a move to stay in the race (remember those awful acquisitions during the HRO 1.0 era?). As-a-Service has arrived, and HR provides the early battleground… so sit back and enjoy the show, as this one could get messy 😉

Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton openly attack the Sharing Economy in a speech outlining her economic theory.

Clearly taking a swipe at the likes of Uber and Airbnb Mrs Clinton states, “This on-demand or so-called gig economy is creating exciting opportunities and unleashing innovation. But it’s also raising hard questions about workplace protections and what a good job will look like in the future”. Clinton “Vows to crack down on employers who misclassify workers as independent contractors”, which she says is “wage theft”. Along with globalization and automation, Clinton describes the “Sharing Economy” as “conspiring against sustainable wage growth”. The report says “she will argue that policy choices have contributed to the problem, and that she can fix it.”

So why does added protectionism of US workers help offshore and nearshore outsourcing?

While the open attack on innovative business models is in itself mind-boggling, the less obvious impact of her focus here is to discourage service providers and enterprises from hiring US talent to provide business support services. As service delivery becomes increasingly focused on higher value needs, such as organizational design, analytics modeling and supporting complex apps development across multiple environments, the opportunity for local US talent to be leveraged is huge.

In addition, the way in which new generation As-a-Service providers want to engage with talent needs to be more “As-a-Service” to be competitive. Virtual support models are becoming critical for BPaaS support functions where clients need quick, on-tap support, and – in many cases – the new generation of service provider isn’t simply looking to stock up hoards of full time employees in a call center somewhere in the Midwest – they are also seeking to engage talent which prefer a flexi-model and do not demand entitlements such as healthcare, 401K etc. Isn’t that what things like ObamaCare are for? Just look at how the new class of Workday service providers, such as Collaborative Solutions, Meterorix, and OneSource Virtual, all of whom are upending the old guard of “Was-a-Service” providers, clinging to costly legacy models that have already been disrupted. These firms are all employers of local US talent in support of innovative As-a-Service delivery. Does Hillary really want to discourage these firms from flexing up with more staff locally as they grow, or would she prefer them to invest more in India, South America etc where talent is more fungible and flexible to manage? Because that is what will happen if more protectionist employment laws are put through.

Why not make it easy and fluid to hire local talent to scale up – as and when needed? Why not support our service-driven businesses to be more agile and cost-effective with their delivery? Because if services firms and enterprises are being strong-armed into hiring fulltime employees (many of whom don’t even want to be fulltime employees), they are going to evaluate alternative talent models to deliver their services, such as hiring more local people part-time, or outsourcing to service providers which can provide talent from across the globe.

Bottom-line: The US is an increasingly unattractive place to do business. Let’s not make it even worse

For starters, the US has stayed at the lead of the global economy ever since Winston Churchill stuck two fingers in the air because their leadership has embraced innovation in technology and life sciences – and supported their leading firms and academia in the process. Now, rather than staying ahead of the curve and realizing the future of work doesn’t look anything like the past, we are seeing the leading Presidential candidate come down heavily in support of protectionism in order to win a few cheap votes from taxi drivers who overcharge us. Aren’t our wage costs, payroll taxes, healthcare contributions etc already off the scale? Why not give our innovative employers a chance to be successful so they can create new jobs for the future, as opposed to discouraging them from hiring in this country at all? It’s not as if there is a huge unemployment problem in the US these days…

Uber is an easy target for Hillary as it has to rely on local contract workers to be effective and the government can step in to interfere. However, what about all the tech start-ups, As-a-Service providers, major enterprises which can leverage fungible labor from anywhere across the globe to fulfil their needs? Don’t bite off your nose to spite your face Mrs Clinton – protecting a few taxi drivers who overcharge us would have much broader impacts on the attractiveness of US talent at large. Let’s just hope this is a minor aberration as she realizes the consequences of this bewildering campaigning and quickly corrects course to avoid being seen as a dated, legacy politician.

The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane.

The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane. If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life…

If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life… Right on cue, after we

Right on cue, after we  Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton

Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton