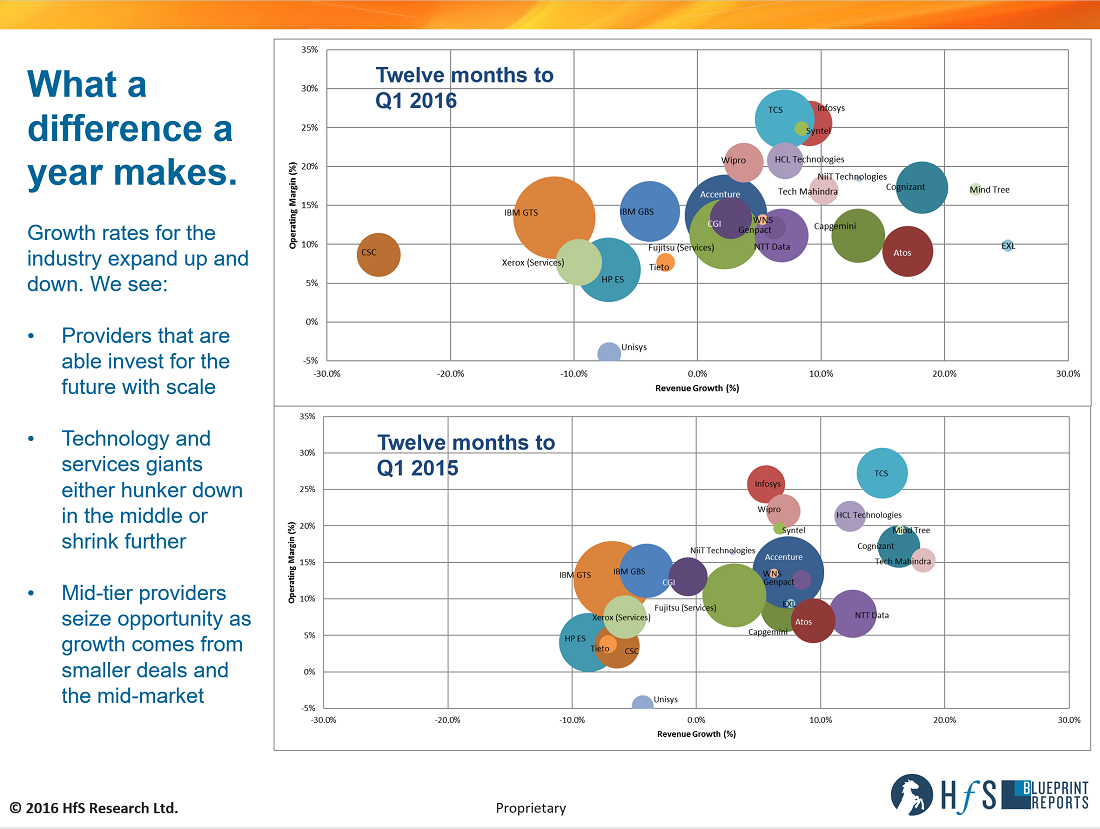

The shake up (and potential shake out) of the services market is continuing with 2016 starting to show the unravelling of the winners and the losers more clearly. The following chart shows revenue growth and margin performance of the leading IT and multi-process BPO services providers – these providers are publicly traded, provide quarterly financial results for the services business. Each chart shows the data for the twelve months leading to the end of March (or closest prior month, in the case of providers whose fiscal periods are not aligned with regular calendar quarters).

Incidentally, neither chart shows the position of AWS because we’d have to zoom out too much and you’d see a cluster plus AWS way out to the right! But it would be at 24% margin and over 70% growth for the 2016 chart. So above Cognizant, with a bubble about 10% smaller, two charts over to the right.

To make the charts easy to compare – they are deliberately on the same scale. So you can see the change in the performance from one year to the next.

The most interesting phenomenon is the stretch in market growth between the two years. With the top chart, the latest twelve-month period, showing a broader range of growth rates. With the bottom chart showing a cluster of providers in the middle.

CSC mostly drives the stretch to the left. However, the impending merger of HPE services and CSC will hopefully remove the need for much of the left side of the chart. CSC’s position due in part to poor market performance but mainly because of the split of its Federal business. However, unless they do something drastic to change the perception of them and start to win more business, the position of HP/CSC entity may not shift much from HP’s current position, it’ll just make the bubble bigger.

We see IBM, particularly the old GTS business, struggle to gain momentum, although we anticipate some better traction as changes to its organization and portfolio made over the last 12 months start to have an impact. The repositioning of IBM toward data and cognitive are market winning moves in our view, particularly with the power and potential of Watson. The issue is how the services business positions itself, during the change and afterward. Given the spin-off of services by other hardware heritage services players like HP, Xerox, and Dell – one starts to wonder what parts of the services business will be remaining this time next year!

Accenture took a step to the left during this period. Demonstrating that the shake-up in the traditional services business has hit everyone. However, they still grew in every quarter and performance is picking up – with double-digit growth in its latest financial results. So we anticipate a move right over the next quarter.

The stretch to the right has been driven by robust growth from some of the smaller players and the pure-play BPO firms like EXL, who are small enough to pick up mid-market business, but also large enough to compete for enterprise deals. Plus some of the cloud providers like AWS are still riding the public cloud wave, with that market having significant growth expectations as enterprises slowly move away from legacy hosting models. However, some of the traditional providers are starting to react to changes in the market. These firms are starting to reposition themselves and are willing to invest in their futures. We can see this from the two major European services firms, Atos and Capgemini. With both providers taking a more aggressive stance in the market, bolstering their positions with acquisitions and shifting portfolios to address market coverage issues. The recent transformation and acquisitions are ultimately making them more global in outlook but also focusing more on digital and cloud markets.

The offshore-centric firms hokey pokey has been mixed for the last 18-24 months with the relative performance of all the firms changing, with individual providers performance being up and down. Even the uber-consistent Cognizant and TCS have had a few up and down quarters. Given both firms scale and mixed market conditions, this is not surprising but is worrying when Accenture, Cognizant, and TCS run into growth issues.

As Phil pointed out in his blog about the HP+CSC merger – “we’re operating in a services world obsessed with preserving the past and ignoring the new. The past was all about predictable revenue and highly-visible cost reduction opportunity – there was a method to the madness. But this was because the true value was about doing things slightly better, but at much cheaper costs. The future is not so predictable – it is about being smarter, more business aware, and technically superior to piece it all together for clients. Oh, and without increased investments. It’s hard, and requires a very different focus, which is one of developing talent to learn on the job, one of evaluating experiences professionals to assess their ability to change, of being able to learn new tools and platforms, which require a mixture of process and business understanding to align with real business outcomes.”

Bottom-line: Those providers breaking away from inertia will define the unravelling marketplace

We observed at the start of 2014 that the competitive landscape was increasingly two-tier and that the main differentiator between the two categories is inertia – it is the companies that react quickly to the changing market conditions that are growing, not necessarily the cheap, low-cost providers. This statement still holds true. You can segment into a traditional or new wave, low and high cost, digital / non-digital, operating or transformational – but fundamentally the real x-factor is agility.

Posted in : Business Process Outsourcing (BPO), IT Outsourcing / IT Services

Jamie. Spot on. Especially your x factor claim about agility. Operating in a digital world is all about agility and many legacy companies that I talk with (and their partners) simply must increase the metabolism at which they iterate, experiment and innovate both inside and outside their corporate boundaries with a tight operational core. And its happening. Be interesting to see what your charts look like in 2 years…

@Euan. Thanks.

I sense that the providers that will thrive are those driving the change – the Amazons/Googles and those hungry for the challenge. It’s time for the best vendors to show their quality…