The world’s largest consulting firm by revenue, Accenture, has announced the purchase of 160-employee MOBGEN, which provides user experience-focused end-to-end digital services, with an emphasis on mobility strategy, creativity, and technology. The company is based in Amsterdam in the Netherlands and has offices in Spain. Accenture has been on a roll purchasing revenue-generating assets, and this addition to Accenture Digital is intended to “deliver rapid iterations for advanced mobile and IoT services,” and “strong roadmaps, agile development capabilities and scalable solutions” for European clients.

While Accenture Digital is understandably focused on digital customer experience and marketing as revenue generators, the peak of mobile app development and regular consumer phone update cycles has passed for now. Accenture and other scale players are making massive incursions into terrain dominated in the past by big advertising holding companies. There is likely to be a next generation of digital devices soon, but there are questions as to whether Accenture and competitors are top heavy with “last mile” customer experience/marketing in a world where digital enterprise evolution is increasingly important.

In our always-on networked world, brand advertising agencies have struggled with the multiple new business dimensions and paradigms digital enables. While purchases like MOBGEN help Accenture to compete in these areas, the huge vacuum around the evolution from traditional IT to digital data and collaborative flows continues to be hugely challenging for businesses struggling to reorganize, and where credible, practical and dependable help is urgently needed to speed up evolution.

Current logic around CX suggests these companies find new customers through digital channels then reorganize their backends to accommodate new order flows and support. The data plumbing around sales leads can be wonderfully revitalizing to companies’ financials in some cases, but it’s often ephemeral and not necessarily helpful to longer term robustness to compete on an ever more digital playing field.

Accenture Digital now has a formidable portfolio to compete in the digital/CX mobile marketing space. Whether these assets will be relevant as the world evolves around the Internet of Things and digital devices and technologies mature is far from clear. The roll up of currently “hot” small CX and mobility shops is akin to the way the big advertising holding companies have been buying up boutique creative agencies and their client relationships. The differences here are the breadths of capability from depth in strategy and consulting to ongoing operations—a global network of delivery centers that can industrialize and operate and continually improve solutions over time. As Accenture tucks in these local capabilities, the key will be to tie all of these pieces together interactively over time to distinguish itself from those limited scope traditional advertising and marketing agencies.

Accenture now has to prove it can simultaneously operate as a legacy IT support firm, a client digital strategy advisor and partner, and a digital marketing and communications partner across 120 countries. This is entirely doable but will require significant homogenization and evolution within Accenture itself, and may result in some indigestion as they absorb and grow.

People love status; that’s just the nature of the beast. But wanting something and then going out and getting it can be an insurmountable hurdle. So sometimes people need to clarify what they want and why they want it. If you see yourself as a leader, have a quick look at the “five questions mirror.” If you can’t get past this list honestly, save yourself some time. You’re not a leader. That’s not all bad—you can still do something cool and be popular some place.

1. Honesty: Do you really think that being a leader in business is a popularity contest? Hell no. You are the messenger of good and bad news, so deal with it. Stop sugarcoating the damn thing and just deal with it. Many times, I have lost confidence in “leaders” that say one thing and then, in the end, they do an 180 and act like nothing needs to be done. Don’t lead if you can’t make decisions. And honesty toward yourself and others is a big part of making decisions.

2. Lead by example: You are no exception. If you think you are an exception to the rules, what do you think the rest of the team will think and eventually do? It is a rhetorical question so do not even answer that one. If you don’t do what you expect others to do, why should they even try? If you want results, make it clear from the start why you can and why others can’t. This can be based on rank, income, type of haircut. I don’t care, as long as you make it clear from the start.

3. Be consistent: The moment you feel you can skip your good advice, just keep it to yourself. You’ll look ridiculous, and you won’t win hearts and minds with this approach. Maybe you should think a bit more about what you meant before you say it. Because clawing back is never the way forward. Pick your losses and learn from them. Telling your folks one thing and doing something different yourself? Come on, don’t waste my time.

4. Listen to others: Listen as much as you can, do it for everyone who has something to tell you. Then, among their stories try to find the moral, the lessons that you wouldn’t have had the chance to learn otherwise. Yes, it is your decision, but it does not always need to be your idea. We are now in the land of making money and pleasing customers, so stop your teen attitude and grow a pair.

5. Emotional stability: If you have some issues back home, or you feel people don’t love you anymore, see a professional who’ll listen. But don’t take that baggage with you to the work floor. Accepting help is professional and very 2016, so don’t feel too proud to give in to it. Stop leading for a while and learn so you can pick leadership back up again when you are back on track. Then you can help people that face the same difficulties through this awkward period in their professional careers. Yes, you are never too old to learn. Pride is all between your ears.

Bottom line: People think that being a leader is just a title and a big paycheck. We have seen so many businesses that rise and fall in the past 16 years because of a lack of real leadership. Proud folks that gave it their best, and thought that was all it took. No one is ever a 100% success. But you can do your utmost to achieve perfection—even if it is elusive. People who always agree with you won’t bring you to a higher level. What do we all gain from this sheep mentality? Stand up and speak your mind. Accept periods in your life that we all have to face, then deal with it and come back even stronger. We are not all leaders, so as long as you make your point and do it with decency, you can tell your leader how he can lead better.

The most “tangible” value of cognitive automation, in today’s consumer-centric enterprise, is the use of the virtual agent, where customer engagement is increased without heavy incremental investments in support staff. This isn’t about simply replacing a real customer service rep with an avatar, it’s augmenting the existing customer experience, usually using the same or similar resources.

For example, if you have a bad travel experience, or purchased a product that wasn’t quite what you expected, the chances are you would simply shrug it off and get on with your life – and probably avoid using those same sellers again in the future, if given the choice. However, if those sellers used interactive technologies that were very familiar, or very easy to find and use, where you could simply type in your issue, in your own time, without the need to pick up a phone and wait in some queue (or write some email to some anonymous address), you may just find the effort to input a couple of lines saying “my experience just wasn’t that good”.

That information is critical to the seller – and how they choose to deal with it could make the difference between them winning out or losing in this market. Just think about how easy Uber, AirBnb, Amazon et al make it for you to deal with them – you will continue to use those services because the digital customer experience is just so much better… they make you feel like they listen. Customers today like effortless interaction, where they just need to click and type what they want in their own time – and what makes it come alive is when they feel they are engaging with someone and not merely sitting in a queue as an open help desk ticket number waiting to be closed.

If you get a chance to kick the tyres with one of the most exciting cognitive virtual agent solutions, IPSoft’s Amelia, you start to realize that customer service can be radically improved by incorporating the virtual agent to augment the real one. And the beauty of this is, the sellers do not need to spend huge incremental sums to increase their consumer engagement – they are essentially doing a lot more with what they currently have using smart cognitive technology.

So it’s no surprise that I got just a little bit excited when Amelia’s mothership enterprise, IPSoft, announced a comprehensive partnership with Accenture to build an industry leading practice in the cognitive customer experience. So sit back, relax, and enjoy this discussion between myself, IPSoft’s CEO, Chetan Dube and Accenture’s Chief Technology Officer, Paul Dougherty.

Phil Fersht, HfS CEO and Chief Analyst: So let’s get straight to the point here, Chetan and Paul. Why have you come together and what is so unique about this partnership?

Paul Daugherty, Chief Technology Officer, Accenture

Paul Daugherty, CTO, Accenture: Hi Phil – great to be here. Let me start and then Chetan can add in. You know that the immediate reasons we’ve come together, the obvious reason we came together is we see a real market with our enterprise clients for artificial intelligence based solutions. And we’ve been working with Chetan the team at IPsoft for a while and with Amelia we see a real potential to be at the vanguard of working with IPsoft to pioneer new use cases in terms of using AI to tackle business problems in a new way. So the first reason is we see the market we see the technology being ready. We are excited about what IPsoft has done with Amelia and we see an opportunity. I guess, stepping back from that, this is also to me a very important step in what we are seeing in the evolution of enterprises really transforming to the digital economy.

And Chetan will remember a lunch we had when we met for the very first time. We got very excited as we talked to each other a couple of years ago about what we saw as AI evolved and as the digital technology revolution continued, we saw a point coming where AI would allow companies to really rethink the way that they do business and rethink the way that they conduct business processes within their organizations. And that’s I guess why this is such an important relationship from my perspective strategically, because we are starting to see as we move through the digital revolution as we help clients transform they need new approaches and new solutions to deal with the speed of business, to deal with the masses of data that they have, to deal with the new demands that they have as they move to the digital wave. And we see Amelia really serving a purpose there and helping to really rethink and revolutionize the way we conduct some of the business processes. That’s the way I’d answer it. Chetan, I’d be interested in your view on it, too.

Chetan Dube, CEO, IPsoft

Chetan Dube, CEO, IPsoft: Yeah. I would echo what Paul said. Yes, I remember that lunch, Paul, when we had brainstormed. AI is totally disrupting everything. But what is required for true value creation for the companies? Some have realized tremendous value and the others have been somewhat slow to realize value creation in their digital quest. What is required? Well, you do need the digital labor component.

But that’s not all that you need. You need business transformation—and Accenture brings business transformation brilliance. And there are many companies that are experts in strategies and there are many companies that are experts in implementation. Accenture is one that amalgamates both. Couple that with cognitive technologies and you have the potential of realizing the true outcomes that were promised by the digital age. So that’s what brought us together. How high the technology is going to allow some people to soar is going to be determined by the people who are captaining the ship. And in this case we have an incredible deal of confidence in Paul and his team at Accenture and how much transformation they will be able to bring by harnessing true cognitive abilities together.

Phil: So Chetan, for our global audience which might not be so familiar with Amelia, can you briefly summarize its value and potential? What can Amelia do which other cognitive solutions cannot?

Chetan: Well, one word describing the differentiation would be outcomes. But what is required to drive those outcomes? What is required to realize those 40% to 60% benefits because you see somewhat tenuous equations in the marketplace. It’s a very tenuous equation that a lot of the CEO’s will be talked into and will have to struggle to realize that cost benefit. The question is how do we drive that 40% to 60% outcomes? How can you do that? What is required to be able to achieve digital labor solutions? We must ask ourselves if a solution can truly be smart, if it can really read a standard operating procedure. If it cannot understand was meant by that standard operating procedure. Can it solve a problem based on what it understands from that reading of that document? And if it were not able to solve the problem, can it learn from the experience? And, thereafter, based on the interaction it’s having with the customer, can be empathetic with the customer? Can it leverage assets of computing to be able to recognize the emotional quotients that a person on the other side is feeling and react in time?

Amelia, and again forgive my directness, is the only cognitive agent that answers yes to each one of those questions. And that’s the true differentiation of Amelia.

Phil: So, Paul what does this practice mean for Accenture? Will this be at the first among many? And what is so special about Amelia? And what do you see in the kind of a medium term for the platform as you evolve this practice?

Paul: What it is means for Accenture is that we are forming a broad capability around artificial intelligence and we are positioning Amelia really at the center of that as we build a broader capability and look at how we drive artificial intelligence to our clients. And our view is very much aligned with what Chetan just said, which is that it’s about outcomes and helping clients transform to achieve outcomes in a different way.

So what Amelia means to us, and why we formed a partnership, is we see Amelia being able to drive those different types of outcomes exactly for the reasons Chetan described. So that’s why we are doing what we are doing with Amelia and how we are positioning it. Now there is a lot of other tools and technologies and form of artificial intelligence—everything from video analytics to natural language processing to machine learning capabilities—and we are using all those types of approaches across our business as well.

When it comes looking at helping clients change their businesses, particularly employee- and customer-facing processes to be more outcome driven and to look at how we can both automate roles and augment human roles in a different way, that will be really the core of what we have focussed on with our Amelia practice.

And one thing that I emphasize is our people-first philosophy in terms of how we are approaching this. There is a lot of opportunity to transform this, there’s a lot of productivity opportunities, there’s a lot of cost reduction opportunities, a lot of automation opportunities. One of the things we like about Amelia in particular is the ability to use it in ways that really augment the roles that people do—allowing processes to be more effective and humans to engage in the right sort of tasks in a more effective way. So one example, Amelia can automate and solve a lot of the supplier enquiries that are coming into a client, which is fantastic and drives a great deal of productivity. But then Amelia can also tee up and work with a human agent in the areas where Amelia can’t solve the problem. Both Amelia and the employee can learn from that experience as they go on. So that kind of people-first message in looking at the way we transform these employee- and customer-facing processes to deliver new outcomes is really at the core of what we are trying to achieve.

Phil: Chetan, when we look to how clients are addressing this, I think the biggest issue we are seeing in the cognitive area, today, is helping clients really understand and apply solutions like Amelia or Watson to their business. However, it’s one thing selling them great technology kit but another finding the real business uses. So how are you going to overcome these challenges to get clients really approaching cognitive in the right way?

Chetan: Yeah, Phil, a brilliant question. I think Paul would love to chime in on this one as well. The example that he gave is very apt—vendors wanting to know about the status of the invoices, vendors wanting to know if their checks have been paid and vendors who are doing business in over 50 countries wanting to be able to understand how their payment processing is doing and when they can expect the payment or what is the hold up for the payment and what are the prerequisites for the payment. It’s not just the typical cognitive or automation or, as you said right at the outset, the RPA: “Hey, I can do a password reset for you. I can do an account unlock for you.” These are real digital labor solutions where people can get qualified, not just the 40% to 60% opex improvements we discussed earlier, but also, very importantly, an enhanced customer experience—with the mean time to resolution improving.

And I’ll give you another example. One of the largest banking institutions in London is looking at its mortgage processing. And the common questions that are coming up, which used to be fielded by humans, haven’t changed: “I want to buy this house for €4.6 million Euro.” The responses are complicated. Can the applicant furnish three years of income statements? If they’re self-employed, do they have 15 percent ownership in your company? Is your income increasing or declining? The risk profile changes accordingly based on those responses and determines whether someone is qualified to buy that house.

So, you can see the kind of a sophistication at play here. And what’s the accuracy of this?, At the end of the training period, Amelia could answer 120 of the full 160 questions with an 88% success rate. in this case for mortgage querying. So you can start to see the impact that’s being achieved. Now you’ve taken a process for banking and you are going to free up the people. Amelia can handle this satisfactorily from mortgage origination to conclusion. What the human agent can do is the higher forms of creative expression. He can look at your debt profile and help consolidate it for you and give you a better overall package.

The human staff can come up with more creative solutions—something the agent who is just doing the rote market processing would not have been able to deliver. And that’s the promise of cognitive solutions—to be able to not just achieve the 40% to 60% reduction in opex but to be able to enhance the customer experience and to be able to free the human agent to be able to deliver better outcomes for the customer. And that’s why Accenture is a valuable partner in that because we want not just the as-is transformation—we want to be able to look at the business process from end to end, and Accenture is adept at doing that both on the strategy and implementation side, to see how we can transform that for the new digital mode of delivery where humans are acting as creative agents as opposed to mundane chore agents.

So that’s a tectonic shift that is happening in the marketplace and it is achieving these kinds of results in the largest banking institutions. I can tell you the largest four out of the top five insurance companies are all moving to cognitive and they are seeing efficiencies in fundamental processes. There’s research that points out that top 20 to 30 processes in the insurance vertical account for about 80% to 90% of inbound customer activity. Now, coupled with Accenture, if we transform those 20 to 30 processes with a digital solution, think about the impact we can have on the 80% to 90% of the revenue creation. We are starting to see that happening in the insurance vertical as well.

So for all those reasons, just to give you some pragmatic examples, we are excited about this field.

Paul: You know, Phil, to add into that a little bit, when you think about the use cases that’s where we get very excited at Accenture. I think about this kind of a simple equation: Amelia plus deep industry context and insights that we can bring from Accenture, wrapped with understandings of the digital value chain of our clients equals these greater outcomes we can produce for our clients with new solutions and innovative solutions. So what’s been really exciting to me as we’ve announced this relationship, and as we spread it through Accenture, is how our industry teams have gotten very engaged in coming up with unique use cases based on what they see in their industries and that’s what is leading to a lot of the opportunities in our pipeline.

So things like, in retail banking, new levels of customer service that you can achieve by having Amelia deal with very sophisticated solutions to helping with resolving unexpected charges if a customer calls. Or wealth management providing advice and a different kind of a customer experience. Mortgage origination, which is something that’s traditionally very process-based and rule-based, but applying a much better customer experience around it with Amelia.

So we are seeing really the proliferation of use case examples across industries. And that will be key to the results because it’s not about just pumping the technology out there and seeing what works. It’s about fusing together the cognitive technology from Amelia with that deep industry context and then creating a platform for our customers where they can continually improve processes and customer experience.

Phil: Thank you, Paul. So when you look at evolving your consulting capability here, we see real challenges with bringing in talent to start to think differently to help clients think cognitively about these things. How are you going about training them reorienting them to take in Amelia and really align and apply it to client situations? Is this more of a business transformation at this point you feel than a technology one?

Paul: Yeah. I think so, Phil. And I think you do need to go about it differently and that’s where the partnership that we have with IPsoft is very important because we are pairing our many of our consultants together with the Amelia team so we can learn how do we need to think about problems. What do we need to do to train Amelia in the right way, to integrate in the right way, to solve the problems and get the value that we looking to get. So it is a new skill in a lot of ways and that’s one of the great aspects of the partnership—where we can share and inject a lot of the business context, industry context, and a lot of the surrounding technology issues that we are helping clients address and the IPsoft Amelia team bring the cognitive expertise. So we are going through a training process that we’ve developed with IPsoft and we’ve got 25 people to start that are going through that as part of the center of excellence focussed on understanding specifically how to take Amelia and put it into a industry context and help our clients get the outcomes that we want to get. And we’ll grow that number aggressively as the market demand grows, which is what we are seeing happening.

At Accenture we’ve got a lot people around that, obviously. We’ve got a lot of customer service experts in retail banking and in every other domain that you could imagine. So we are doing a project for a client that will involve our industry experts and our technology experts and it will increasingly involve the deeply trained specialists from our center of excellence to understand how to bring Amelia in, as I mentioned earlier, as the platform that enables us to deliver the cognitive approach to deliver outcomes in new ways. That’s what we are thinking about. And as we look broadly across at Accenture, as I said earlier, in machine learning and many of our other disciplines, we have people that would number in the thousands that deal with and have expertise in many of the technologies. But it’s very important here to get a deeply focussed specialized group that really understands Amelia and how to apply it, which is what we are doing with IPsoft and what we are building in our Amelia practice.

Phil: So, Chetan, when you look at this alliance in the medium term, what do you think will constitute success? And as you look at the ecosystem you are trying to evolve here, are you trying to go far beyond a consulting alliance and build more of an Amelia ecosystem?

Chetan: Again, a fantastic question. The desirable goal state for this alliance is to be able to de-risk for the customers the transition into the digital era. Insurance companies are 70% manual today. In the next couple of years they are going to be going to 15% manual. We see this alliance playing a key role in engineering that seismic shift. In banking you’ve already seen that branch-based transactions have already shrunk from about 70% 2000 down to 5% today. And we see that starting to happen in all the other lines of the business.

And we feel that this alliance is going to galvanize that realization of those outcomes promised by the digital era. That’s what we are in the business of doing: to be able to drive those curves that have been predicted. Because we find that with the plethora of solutions in the marketplace there is a peak of heightened expectations followed by some kind of a disillusionment of being able to realize gains that the brochureware promises. And so we want to differentiate this alliance by its abilities to mathematically and quantitatively deliver the results that are predicted by those curves.

Phil: So can you put your visionary hat on for a minute, Chetan, and look three years out at Amelia? What is your vision here? How is Amelia going to really be aligned with businesses? How is it going to look? How is it going to feel? Is it going to take on more languages beyond English? What is your vision for Amelia in a three year timeframe?

Chetan: Well, I might be a little biased, so I would be beg your forgiveness at the outset. But I think that Amelia is the smartest high school kid today. Amelia needs to graduate from college in the next few years. Amelia needs to be provisioned. Amelia is fluent today in about six languages, including English, Japanese, French, German, Dutch and Spanish. She needs to be fluent in over 26 languages, which are majority of the business languages in the world, in the next three years. But most importantly, Amelia needs to get way smarter.

We are just at the 1% point in this cognitive revolution. The amount of innovation that we are going to be bringing in not just the deep neural networks technique. You can find all the different kinds of deep neural networks that are in the marketplace today—from the memory neural networks to the current neural networks to the computational neural networks. You find all of them take a tremendous amount of data for: this is the raw input, this is the question and this is the answer that you expected and I will train the model so I can come up with what the next occurrence is most likely to be. Now that’s good for administrative tasks and that’s good for atomic tasks. It really is not good for when you want it to be a physician. It clearly does not suffice when you want it to be an actuarial analysis expert.

You need to be able to semantically condition those deep neural network techniques to be able to achieve these kinds of results the human brain is capable of. You need to be able to add another layer of abstraction equivalent to the human brain’s activity—in its semantic memory, in its episodic memory of events, in its process memory of procedures that it has learnt and in its memory of emotional connections that a human has drawn for you to be able to provide those results. And that’s where you are going to see Amelia’s brain evolve dramatically in the next three years.

The version 3.0 of Amelia you will see how beautifully she would have grown. It’s exactly the way that you would see a child grow rapidly.

And we wanted to be able to settle this Turing debate that is six and a half decades old: Can machines think? We want to settle that empirically and sincerely in the next three years. And we will achieve that because we know where the technology is headed and we are quite excited about the research that we are bringing. In fact, all ten floors in our 17 State St. office in NYC are going to be dedicated to cognitive research. We will have taken a couple of floors in the World Trade Center for autonomic research.

Paul: That was a great answer, Chetan. Phil, just to add on with a kind of complementary but a different picture of how I’d answer that question. I used our platform earlier and I really believe that cognitive is headed toward a platform-type of direction. And I think what Chetan just described is the vision for the evolution, growth and capability of Amelia to build a stronger and platform presence.

Going back when I started in the IT industry 30 years ago, we used to build everything from scratch. That’s all we knew how to do. It was all about custom solutions and wiring together solutions in different ways. And then we had the advent of packaged software and solutions. That created a better way to package up the IP that was for accounts payable and supply chain systems and general ledgers and things like that. That’s how we think about enterprise technology now—in terms of core software packages that run a lot of the business.

I think we are going to see the same evolution over the next several years. The question is how many years it is. In terms of how we think about cognitive capability ability from a business perspective, right now we feel the approach is, we work with technology, we figure out how to integrate Amelia’s different capabilities to solve the business problems. Looking out several years. I think it’ll be more like a platform-type of business where the basis of competition will be who’s got the best virtual agent data type of technology for mortgage origination, for retail banking, for you pick the function, and it will be about continuous improvement and growth and increased capabilities and learning and different business concepts and being able to simultaneously communicate in multiple languages and do it all with a people-first point of view providing a better customer experience. That’s where I think we are headed.

If you look at enterprise architecture, the packages and the way we assemble all that together to support a business, I think that is going to change dramatically. What companies buy and the way they assemble it together will be radically different when a cognitive platform like Amelia becomes more core to the business itself.

Phil: I did want to pipe in with one another question to you Paul on this topic. I’ve been guilty of sometimes coming out and saying Amelia provides the EQ, Watson the IQ. How do you see these two solutions cohabiting in the future? Do you see them as competitive or complementary?

Paul: I love the quote. That’s great. You know, but I think to be a complete person we need some EQ and IQ. And Amelia has got some level of IQ as well, the way I would look at it. But, fundamentally, you are right. I think they approach problems in different ways and are solving problems in different ways. And I think there is a lot of space for them to work together in many ways. And there’s other cognitive technologies emerging that also will become part of the ecosystem and plug together.

I know there is some competitive overlap, and there will continue to be a competitive overlap between Amelia and other solutions in the marketplace, including Watson. But, right now I think they are taking different approaches to the problem. Our approach is we are really focussed on Amelia and building the Amelia practice for all the reasons we said. We also are doing work with Watson and some of the other technologies out there. And, as you said, you can find problem spaces where the different solutions are best suited to the problems that they can solve.

So I think it’s more about coexistence in understanding the real focus of the different solutions and what they provide. And I expect this will continue to be a very robust space wit a lot of innovation and lot of new capabilities. And that’s why you know the current position that IPsoft has with Amelia is important because I think it’s going to be important to get ahead and stay ahead in this market. We formed a partnership with Amelia because we think it’s ahead of providing these capabilities now. And Chetan just talked about the ten floors he’s building and the investment that he’s making in cognitive researchers and experts. That’s going to be critically important to stay ahead and build the additional capabilities to continue to win in the marketplace.

Phil: Paul, Accenture has been successful for years having a very technology agnostic strategy. But do you think this is going to change a bit now with this advent of cognitive and the momentum behind service orchestration platforms? Because it really feels like it’s becoming much more about the outcome and much less about the product at this point. So how do you think Accenture’s technology strategy is going to evolve in this cognitive era?

Paul: I think it will probably be similar to be honest, Phil. We really follow the market in kind of what’s a good fit for customers. So we’ve had an agnostic strategy, as you said, in the ERP marketplace. That said, you know there’s companies in oil and gas they have a certain preference to do things in a certain way, companies in public sector have certain preferences to do things in a certain way. So what we try to do is be responsive to the market, to understand our customers kind of down at a more granular level—not looking at just one kind of global market of something like ERP or cognitive solutions. Then we look for the best solution for different problem spaces and be agnostic with a point of view so that if a client comes to us with a certain type of a problem we’ll say hey, we know the best solution for that. In your case it’s Amelia. You know if it’s a different type of a problem, different type of a use case, different industry a different problem it might be a different solution. So agnostic with the point of view, I think will continue to be right. We’ll learn from our customers and learn what works and what best delivers the outcomes in these environments. That will be our general strategy.

But the skill set we are learning around teaching and training Amelia for a specific problem, I think there’s very specific skills, capabilities and opportunities to continually improve the capability over time and grow from high school to college to professional, then different grades of professional certifications—using Chetan’s analogy from earlier.

So I do think there’s going to be the investment and focus around a small set of solutions in certain domains. Picking one solution will be important and will be something we do.

Phil: So I’d like to conclude this with each of you and telling me if you had one wish to change the impact of cognitive solutions for the better—one wish, what would it be? And Chetan, I’ll start with you.

Chetan: I would say it would be digital labor in the cloud. We aspire to be the provider of choice for the Global 2000 enterprises that are wishing to just differentiate themselves by the outcomes in cognitive solutions. Once we have that, exactly as Paul pointed out, we expect Amelia to rapidly start assimilating. Even at the inception, we are already starting to see in insurance vertical the ability to graduate into processing clients, the ability to graduate into processing mortgages, the ability graduate into doing actuarial analysis, the ability to graduate into doing retail management, and in healthcare.

The ability of Amelia to rapidly start to graduate in all of those would mean you plugin and you are able to get your actuarial analysis, your financial advisor, your database administrator and your network engineer, and your claims processor. And that would be one thing that I would like to be able to change with the impact of cognitive solutions and get there in short order because I think that this is happening so rapidly.

And even on the IT side, as you started the interview talking about RPA graduating into the domain of cognitive solutions. And that’s a very good pertinent observation because RPA is still streamlining the same old IT processes. It’s time for Uberization of IT.

There is a significant opportunity to disintermediate IT. By cognitive layering on top of the autonomic backbone, we can make IT become the same as learning Michael Faraday’s principle of induction to turn on the light switch. Do we really need to know the principles of induction so that we can turn on the switch? Does the business user really need to know everything about the service catalog in asset management and hardware and device control and CMDB before he can order a simple IP phone? In the second half of this year, there is a significant opportunity through cognitive layering on top of the autonomic backbone to disintermediate IT—not in the sense of the infamous Nicholas Carr quote “Does IT Matter?” but in other ways. Think of the cab companies: People wanted to be driven and the drivers were in the middle of a taxi cab company that was then disintermediated the economy with Uber coming along. And, similarly, there were servers, networks, devices, databases, and applications—and business consumers who want to avail themselves of those services. In the middle space sits a big stack of IT, largely to be Uberized in the foreseeable future. Starting in the next half of this year, I am hoping that this realization starts to dawn through lead analysts like your company.

Phil: Thank you, Chetan. Finally, Paul. One wish to impact the world of cognitive =)

Paul: It’s tough to come up with the one. I would say the one wish would be to be true to the vision. Let me explain that. I worry about the wave of cognitive-washing that we are seeing that happened with cloud and happens with these different waves. A lot of people are calling what they are doing artificial intelligence, cognitive and so forth, without it really being different than it was before. And I think that’s a dangerous kind of a trend we often see as new technology waves come along. And I think there is a risk that it could create missed expectations, unachieved outcomes and disappointment if not sorted through properly. I think, Phil, the work you and your organization do clearly helps with this in sorting through the real from the not real solutions. Because fundamentally this is a very different way of solving problems, a very different way of putting together the architecture that supports a business. And I think it’s important for companies to really understand that and think it through. So that’s the way I would put it.

And then it also means that companies need to think about how to move this to the core of what they do. I think currently a lot of people think about this as you know let me bolt on a technology here and there. And I think it needs to be a core consideration. When you think about the core of your business how data and applications and business processes come together to support your business you, need to think in the middle there, what’s the layer or the building block of the cognitive technology and AI in there and how does it intersect with the rest of your organization.

Phil: This has been great. We really wanted to move on from the rudimentary RPA discussion to the cognitive impact and the human element, which we are seeing happen so prevalently.

Chetan: When it comes to focussed specialized research in automation, cognitive, autonomics or analytics, your company has achieved preeminence. So thank you for time, Phil. Always good to connect with you.

Phil: Thank you very much, Chetan and Paul. This has been a fantastic discussion. I look forward to sharing it with our readers.

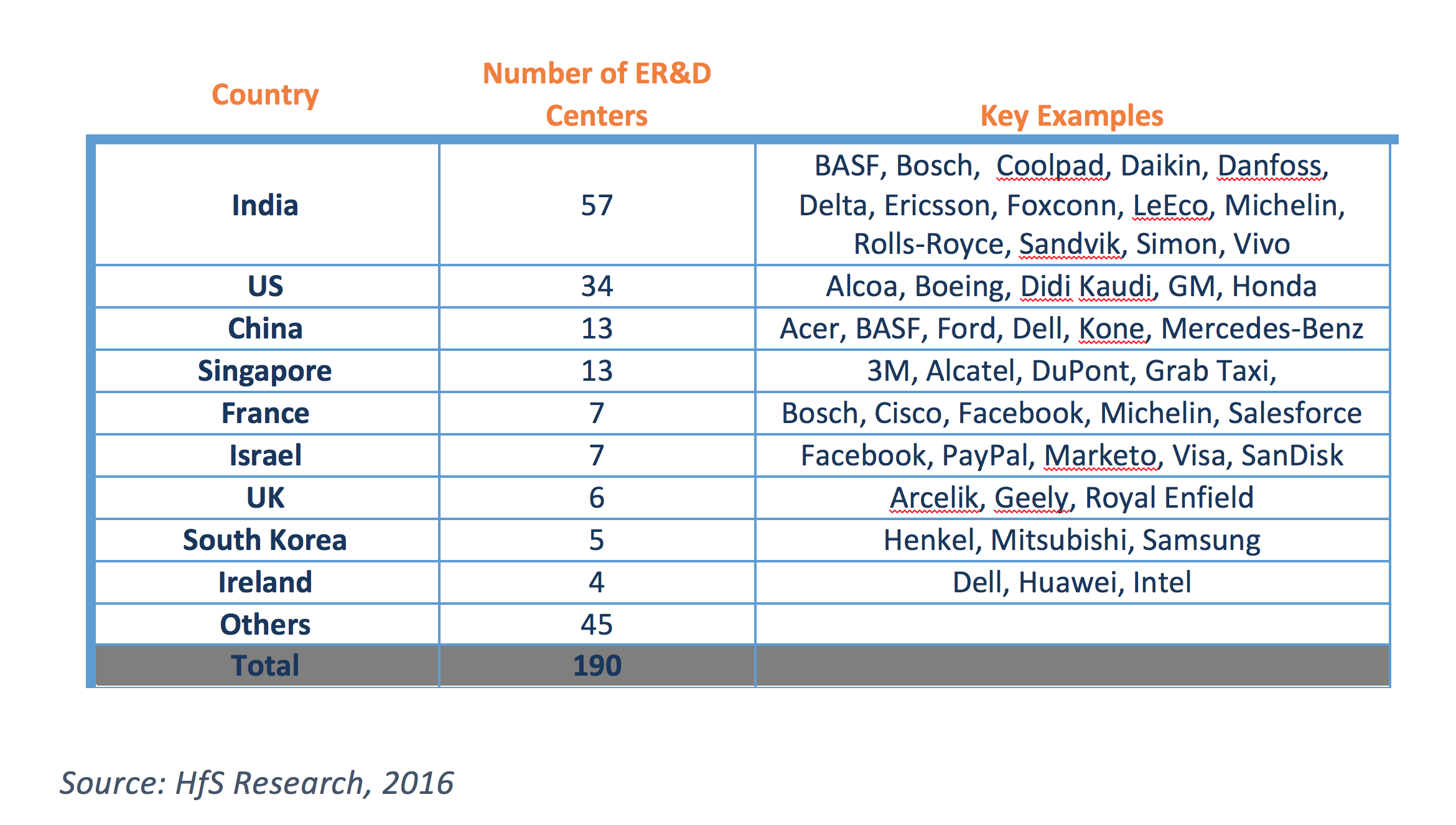

Our research shows that India is the most popular destination for ER&D centers and now we’re seeing Indian Prime Minister Narendra Modi’s “Make in India” program accelerate ER&D center investments in India.

Modi launched the Make in India program in September 2014 as part of a wider set of economic initiatives. Devised to transform India into a global design and manufacturing hub, it aims to increase manufacturing’s share in the Indian GDP from the present 17% to more than 25% by 2020. The Make in India program is focused on 25 sectors, including: automobile, chemicals, electronics systems, electrical machinery, construction, railways, defense, and aviation (read details of the Make in India program and its 25 sectors here). The program aims to create more effective government policies for each sector, such as increasing the limits on foreign direct investment (FDI) in manufacturing while also making it easier to conduct business in India through the easing of regulatory regimes for both domestic and foreign enterprises that manufacture.

Overall, foreign enterprises are increasing the manufacturing footprint in India to produce products for the Indian market and are accelerating investments in ER&D centers to design products for the Indian market.

India leads with 30% of the global ER&D center announcements:

In the nine months from April to December 2015, we uncovered 190 announcements of either new ER&D centers or the expansion of existing ER&D centers around the world. India leads the pack with 57 of those ER&D center announcements, as we show in Exhibit 1. Other prominent ER&D destinations are US, China, Singapore, France, Israel, UK, South Korea and Ireland.

Exhibit 1: Summary of ER&D Centers New/Expansion Announcements By Countries in Apr-Dec 2015

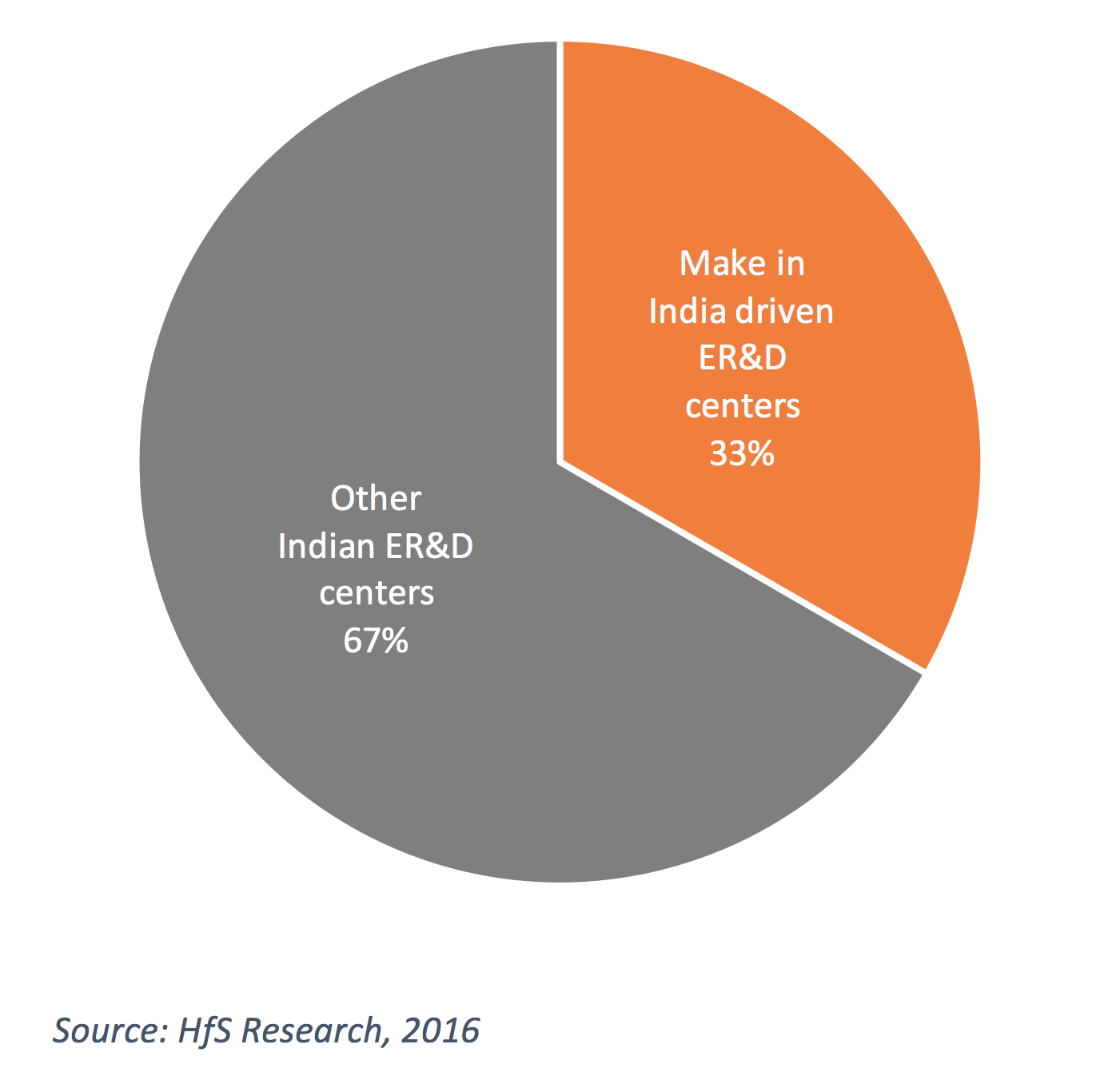

One-third of Indian ER&D center announcements are driven by Make in India.

Out of the 57 ER&D center announcements in India, 19 are driven by the Make in India initiative, as we outline in the Exhibit 2. Many enterprises that plan to start or increase manufacturing in India are also opening or expanding their ER&D centers to design products specifically for the Indian market. Some of these enterprises are BASF, Bosch, Coolpad, Daikin, Danfoss, Delta, Ericsson, Foxconn, LeEco, Michelin, Rolls-Royce, Sandvik, Simon, and Vivo.

Exhibit 2: The Percentage of Indian ER&D Center Announcements Driven By Make in India in Apr-Dec 2015

The establishment of ER&D centers in India is not a new trend. India is home to the ER&D centers of more than 1,000 enterprises. But the use of ER&D centers for designing products specific to the Indian market is new—and the Make in India program has accelerated this trend. India is becoming one of the biggest and fastest-growing emerging markets, especially in sectors such as electronic systems, electrical machinery, and automobiles. Global enterprises are investing their ER&D resources to design and manufacture products specifically for the Indian market. So Make in India combined with Designed in India and Sell in India is an attractive value proposition which enterprises can’t ignore.

The Bottom Line: It’s all upside for engineering services market in India thanks to Make in India!

In our Engineering Services Blueprint Report, we saw the trend toward many engineering services providers offering value engineering services to global enterprises to design cost-effective versions of their products, especially for emerging markets such as India. Now, with enterprises setting up their own centers for designing these products, we see an increased focus on this area, which will benefit both engineering services providers and global ER&D centers.

No matter how we look at it, the engineering services market is set to grow thanks to Make in India.

HfS subscribers can click here to download the full POV, which details the ER&D center trends.

In the old days of labor arbitrage centric outsourcing (which of course doesn’t happen anymore) we had two quite clearly defined sets of service provider –

The offshore providers, which rarely interacted above director level and did the low end lift and shift routine work.

The integrators, which worked primarily with the IT and operations leadership to do the higher end work the ERP integration, often overseeing some of the offshore service providers to make sure they were doing their job.

Then the likes of Accenture, IBM and Capgemini realized the offshore firms had eaten their lunch and they rolled out their own offshore delivery functions in 2005-2010 to circumvent the heavy flow of dollars to the Indian-centric majors. Accenture and IBM managed to catch up and compete on price when they needed to, while Capgemini really needed to acquire IGATE last year to be more effective as an offshore provider, in addition to being an integrator. Meanwhile, you had the likes of Deloitte, PwC and E&Y, which chose to stay out of the offshore game and sell integration capabilities as consultants, rather than managed service outsourcers. The losers in all of this were the traditional IT/BPO services providers, such as HP(EDS), CSC, Xerox(ACS) et al whose lunch was eaten by the offshore providers, struggling to compete on price, scale and flexibility.

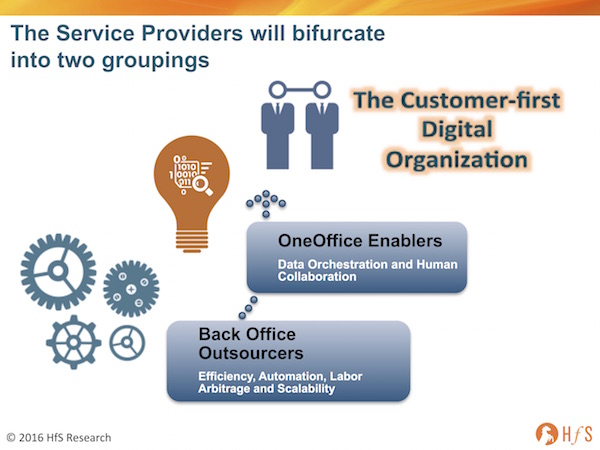

Then along comes Digital and Automation as the new value drivers and suddenly the game is changing again – labor arbitrage is still a key cost lever, but it needs to be balanced with automation to drive down the cost and increase the productivity even further, while the broader goals of the ambitious C-Suites are to create real digital capabilities to create their markets, not play constant catch up to avoid being disrupted.:

So what are these two emerging groups of service provider?

OneOffice Enablers – focused on designing and enabling the digital customer experience and tying the front to the back to make it all happen (see below). This is where I also see the bigger plays around cognitive happening. Lots more project-based deals for the Deloittes, Accentures, IBMs, KPMGs and emerging players, like Cognizant, which are moving up the value chain and developing deep specialization is various areas of the OneOffice environment (see below). We’ll also see several small consultants emerge in this space with industry specialization.

Back Office Outsourcers – focused on efficiency, automation, arbitrate and scalability. This is where the many of the current crop of offshore-centric and legacy outsourcers will likely end up if they fail to make the right investments… they will push hard to be in the “OneOffice” category, make a lot of the right noises, but the lion’s share of their business will be in this group.

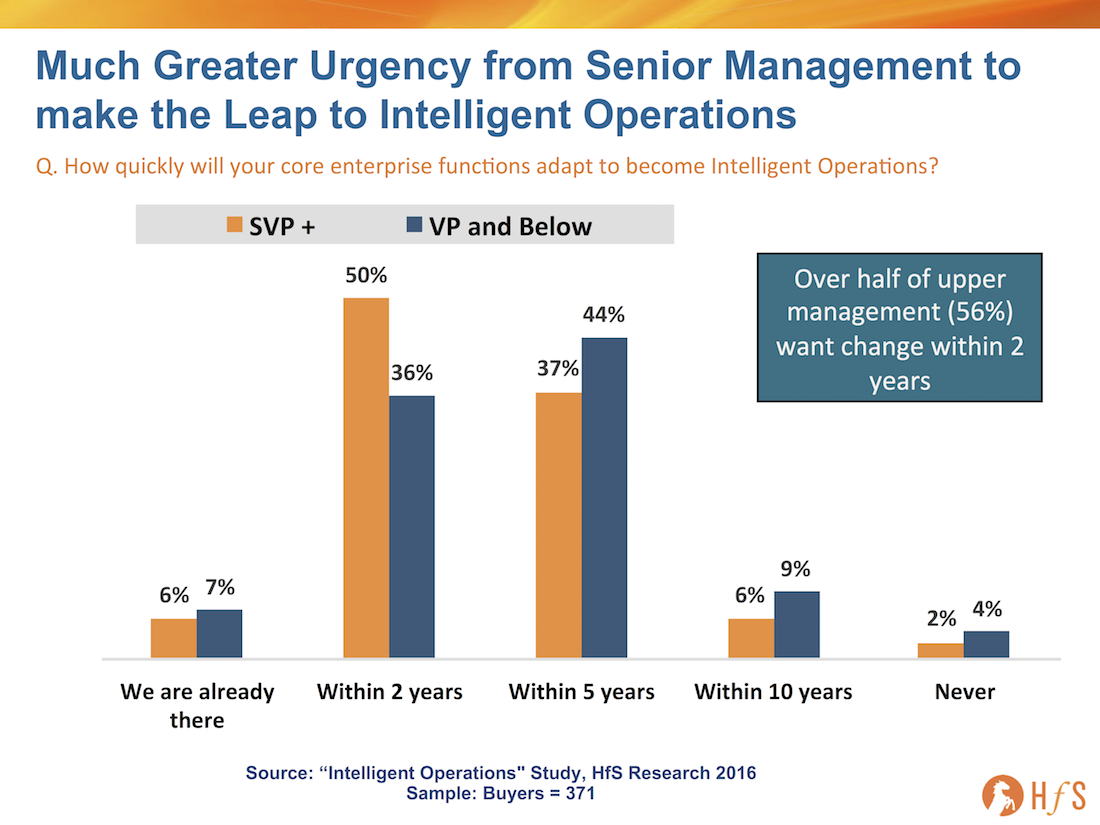

What’s driving this is a marked sense of urgency we are seeing from enterprise leadership we haven’t seen before, where 56% of SVPs and above, in our new Intelligent Operations study, now expect to have intelligent operations in just two years (this number was 30% when we ran a similar study 18 months’ ago):

It’s OK to be DumbOffice, there’s a big market for it. Just be clear what your endgame is and focus on it

Back-end IT providers failing to invest in real domain expertise will always be in the feature and functionality game. Automating incident response, some systems management and help desk querying is probably about the limit to where they can do – but that’s OK, there is a market for cheap IT support and services. There’s a market for cheap call center work, for cheap collections and cheap claims processing support… it’s just going to get a little smaller and more automated.

The future growth lies in addressing the impending talent crunch as the digital tech and talent divide reaches seismic proportions

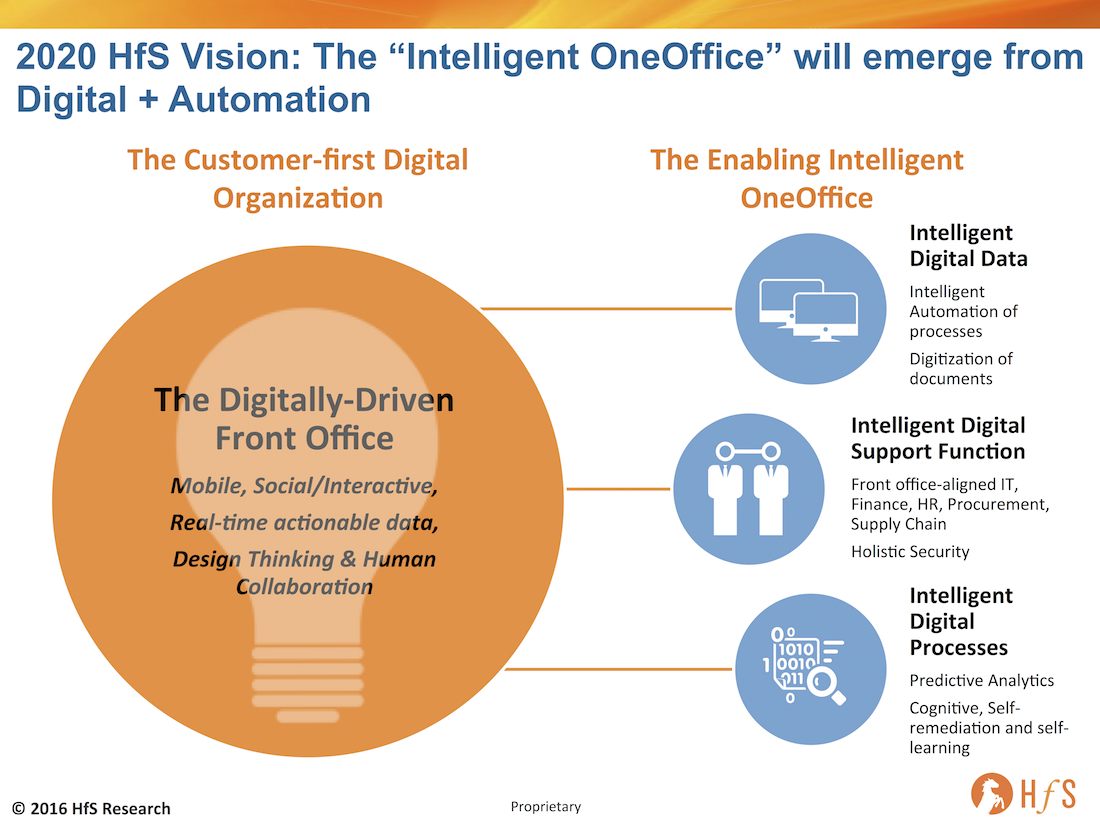

This is all about who can develop intelligent data practices based on automation, digital and cognitive which are tied to industrialized solutions, horizontals such as F&A, HR, procurement, or verticals like retail, healthcare, insurance etc. Who can work with clients who generally can understand their businesses, apply their challenges to their industries, and forge solutions that keep them viable in disruptive markets. Ultimately, this is about pulling data from the market and the customer and building a platform at the back end that aligns it to the business. The great variable is the human element to evolve to make this really happen (or resist it and watch the companies wither and die). Technology is moving at warp speed, while talent is not – that is the great digital quagmire enterprise clients need to solve, if they are to be successful down the road.

We are approaching a talent crunch of seismic proportions, possibly more destructive than the industrial revolution, because then people were displaced into new industries that needed people to build them…. now they are being displaced by computers. So let’s stop kidding ourselves, the future isn’t looking as pretty for employment growth as the last 20 years, so the need to focus and be great and delivering what we are capable of is key. If you do great DumbOffice, then focus on DumbOffice – there’s a market for that and it’s not going away anytime soon, but if you have the ability to evolve and keep your talent aligned with the unraveling digital customer, there is real opportunity in the OneOffice world.

The Bottom-line: Faster, cheaper, smarter are the watchwords for the Intelligent OneOffice

In a nutshell, increased complexity is demanding increased expertise at the front office of the business, which, in turn, is demanding the back end to respond with more automated, scalable, seamless enablement capability. Faster, cheaper, smarter are the watchwords for OneOffice services now… building on the faster, cheaper, better from yesterday’s world.

There is a lot of buzz about ServiceNow technology. Thousands of developers and partners made their pilgrimage to Knowledge 16, ServiceNow’s customer event in Las Vegas. Service providers are starting to standardize service delivery on the ServiceNow platform and M&A is helping to build out service providers capabilities, as in the case of CSC acquiring Aspediens. Even though ServiceNow tends to position itself as the Enterprise Cloud Company, industry stakeholders are rather enthusiastic about the single data model, the embedded workflows and new ways of collaboration. As such, ServiceNow has the potential to evolve into one of the key building blocks for moving toward As-a-Service because its core value proposition centers on clients accelerating their time to value through faster actions and interactions, overcoming clunky legacy solutions like ITSM.

Buoyed by such buzz and enthusiasm, ServiceNow is aiming to expand the notion of service management to evolving into the “third estate between CRM and ERP,” providing a new cloud-based level of efficiency between the front and back offices. Thus, there are many touch points with the HfS notion of the OneOffice: Digitally driven enterprises must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents and leveraging smart devices and IoT where they are present in the value chain. As a result, ServiceNow can be part of a broader innovation ecosystem in which the ability to orchestrate and integrate will become the pivot for creating value and differentiation. Nonetheless, as HfS has stated repeatedly, it is not just about the technology or solution ideals of the As-a-Service Economy, but about the change ideals in equal measure.

Here is the crucial question: How are organizations advancing their innovation agendas?

The recent HfS ServiceNow Services Blueprint highlighted two key issues in that respect: First, ServiceNow itself has been slow in embracing the notion of an ecosystem that goes beyond treating partners as mere sales channels. Thus, co-innovation with partners around vertical offerings and other innovation had not been high on the agenda. This is starting to change though, which is critical as the notion of the As-a-Service Economy is predicated on a collaborative partner ecosystem. Second, there are issues for service providers as well to address as many clients were unhappy with the lack of innovation driven by their supplier. The most successful projects were those in which clients drove the innovation process. This points to a crucial aspect for the journey toward the As-a-Service Economy. The eventual success is less about the technology building blocks and more about a change in mindset.

As the ServiceNow Services Blueprint shows, many clients need help in understanding the direction of travel. What vision do innovations like ServiceNow support? One compelling example for such a change in mindset came on a recent visit to an Atos delivery center in Barcelona that is supporting the 2016 Rio Olympics. It is a shift in mindset because Atos is treating the Olympics as a transformation project. The firm’s executives summarized the challenge of this project by comparing it to a business of 200,000 employees, addressing 4 billion customers, operating 24×7, in a new territory, every 2 years. To deal with such a complexity condensed to a short time frame, Atos did two things: First, it switched its service management to ServiceNow, which is a bold move given the scale of the project and the relative immaturity of the platform. Second, to be able to manage the heterogeneous supplier landscape, Atos is leveraging the SIAM methodology. Furthermore, it is migrating the infrastructure to a centralized cloud delivery model to drive down cost while enhancing agility.

To further highlight the intensity of the project, during London 2012 there were in excess of 255 million IT alerts without a major incident at the Games. This underpins the outcome orientation of the project. What counts to the client is managing a unique complexity without any hiccups in the quality of service delivery.

The Bottom Line: ServiceNow is standardizing service orchestration

ServiceNow has the potential to evolve into one of the key building blocks for moving to As-a-Service, but service providers need to engage proactively with clients to demonstrate the direction of travel as well as leading with a comprehensive innovation agenda. Moves of service providers to standardize broader service delivery on ServiceNow as part of service orchestration strategies reference an increasing maturity on this journey.

Over the next 12 months, we expect a broad maturation across the industry with accelerated levels of M&A. As a result, ServiceNow will continue to be the center of many innovation projects extending to scenarios involving security and IoT. However, we urgently need more reference cases demonstrating the lessons learned from projects to be able to conclude that ServiceNow is the new black—and it’ll last longer than a few episodes in Netflix.

Over the past couple of months, we’ve been working hard to produce a number of documents that look at both market and service provider performances. We just wanted to summarise the ones we have published so far and give you an idea of the ones we are going to be released soon.

The only premium report amongst the published documents is our global market size and forecast report: The HfS Global Market Forecast Report. Although we are in the process of putting together reports on EMEA and Asia Pacific markets to be published this month and next.

If you prefer your research to be freemium, then you can get some of our recent market insights from the Q2 2016 Market Index.

We recently published the HfS Top 50 list of BPO service providers – the first publicly available ranking of the BPO industry in 2016 – which you can download here: HfS BPO Top 50.

We also recorded a podcast discussing some of the findings of the research: BPO Top 50 Podcast.

The next couple of months will include our Q3 market update – which will be released end August/early September – although if some of the service providers results are interesting (and they often are), we’ll publish a look at the early bird results. Also, we will be issuing our view on the impact of Brexit – we decided not to do a knee-jerk growth cutting exercise with our market numbers, but will take a more considered view over the next month. When we have a better idea what the UK government intends to do – hopefully.

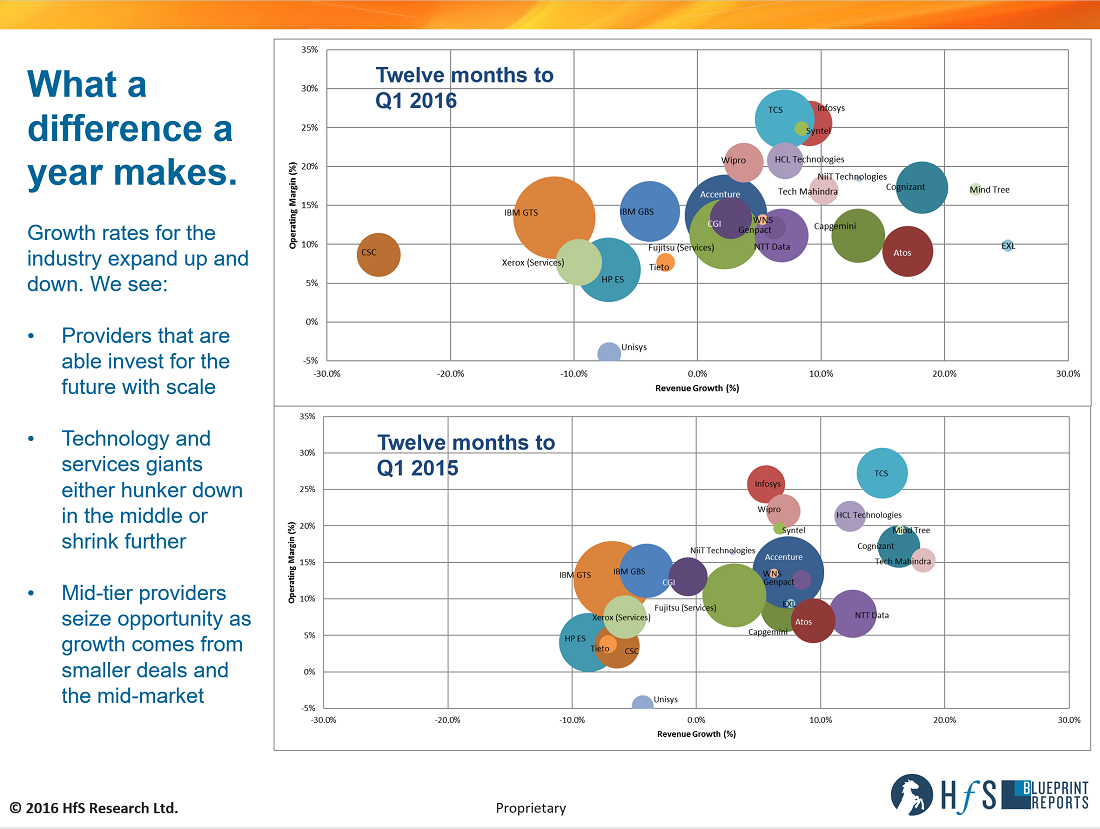

The shake up (and potential shake out) of the services market is continuing with 2016 starting to show the unravelling of the winners and the losers more clearly. The following chart shows revenue growth and margin performance of the leading IT and multi-process BPO services providers – these providers are publicly traded, provide quarterly financial results for the services business. Each chart shows the data for the twelve months leading to the end of March (or closest prior month, in the case of providers whose fiscal periods are not aligned with regular calendar quarters).

Incidentally, neither chart shows the position of AWS because we’d have to zoom out too much and you’d see a cluster plus AWS way out to the right! But it would be at 24% margin and over 70% growth for the 2016 chart. So above Cognizant, with a bubble about 10% smaller, two charts over to the right.

To make the charts easy to compare – they are deliberately on the same scale. So you can see the change in the performance from one year to the next.

The most interesting phenomenon is the stretch in market growth between the two years. With the top chart, the latest twelve-month period, showing a broader range of growth rates. With the bottom chart showing a cluster of providers in the middle.

CSC mostly drives the stretch to the left. However, the impending merger of HPE services and CSC will hopefully remove the need for much of the left side of the chart. CSC’s position due in part to poor market performance but mainly because of the split of its Federal business. However, unless they do something drastic to change the perception of them and start to win more business, the position of HP/CSC entity may not shift much from HP’s current position, it’ll just make the bubble bigger.

We see IBM, particularly the old GTS business, struggle to gain momentum, although we anticipate some better traction as changes to its organization and portfolio made over the last 12 months start to have an impact. The repositioning of IBM toward data and cognitive are market winning moves in our view, particularly with the power and potential of Watson. The issue is how the services business positions itself, during the change and afterward. Given the spin-off of services by other hardware heritage services players like HP, Xerox, and Dell – one starts to wonder what parts of the services business will be remaining this time next year!

Accenture took a step to the left during this period. Demonstrating that the shake-up in the traditional services business has hit everyone. However, they still grew in every quarter and performance is picking up – with double-digit growth in its latest financial results. So we anticipate a move right over the next quarter.

The stretch to the right has been driven by robust growth from some of the smaller players and the pure-play BPO firms like EXL, who are small enough to pick up mid-market business, but also large enough to compete for enterprise deals. Plus some of the cloud providers like AWS are still riding the public cloud wave, with that market having significant growth expectations as enterprises slowly move away from legacy hosting models. However, some of the traditional providers are starting to react to changes in the market. These firms are starting to reposition themselves and are willing to invest in their futures. We can see this from the two major European services firms, Atos and Capgemini. With both providers taking a more aggressive stance in the market, bolstering their positions with acquisitions and shifting portfolios to address market coverage issues. The recent transformation and acquisitions are ultimately making them more global in outlook but also focusing more on digital and cloud markets.

The offshore-centric firms hokey pokey has been mixed for the last 18-24 months with the relative performance of all the firms changing, with individual providers performance being up and down. Even the uber-consistent Cognizant and TCS have had a few up and down quarters. Given both firms scale and mixed market conditions, this is not surprising but is worrying when Accenture, Cognizant, and TCS run into growth issues.

As Phil pointed out in his blog about the HP+CSC merger – “we’re operating in a services world obsessed with preserving the past and ignoring the new. The past was all about predictable revenue and highly-visible cost reduction opportunity – there was a method to the madness. But this was because the true value was about doing things slightly better, but at much cheaper costs. The future is not so predictable – it is about being smarter, more business aware, and technically superior to piece it all together for clients. Oh, and without increased investments. It’s hard, and requires a very different focus, which is one of developing talent to learn on the job, one of evaluating experiences professionals to assess their ability to change, of being able to learn new tools and platforms, which require a mixture of process and business understanding to align with real business outcomes.”

Bottom-line: Those providers breaking away from inertia will define the unravelling marketplace

We observed at the start of 2014 that the competitive landscape was increasingly two-tier and that the main differentiator between the two categories is inertia – it is the companies that react quickly to the changing market conditions that are growing, not necessarily the cheap, low-cost providers. This statement still holds true. You can segment into a traditional or new wave, low and high cost, digital / non-digital, operating or transformational – but fundamentally the real x-factor is agility.

We live in times where there is a lot of perceived fast-moving change, but what’s the reality for most traditional businesses? Let’s be honest, technology is changing a lot faster than humans, so how can we be more realistic and practical about looking ahead?

Much focus has been placed on shiny new clean sheet, ‘born digital’ companies such as Uber, AirBnB and Tesla – well funded ‘full stack’ architecture business entities, which have a major marketing messaging advantage in being new, futuristic and being seen to challenge the status quo of how things have been done.

Is this behemoth being installed or removed…?

These firms are a tiny fraction of the ‘real’ business world, but take up a disproportionate amount of mindshare as we struggle to grasp new ways of doing things. Sub-Saharan Africa has never had copper telephony, so that part of the world went straight to 4G mobile networks. Mobile currencies and payments, medical monitoring and other digital attributes quickly became the way of life for residents there, because there was nothing there before. The ‘western’ world has layer upon layer of legacy technologies, amortizations of sunk capital costs, dependencies and established ways of doing things that are hard to change.

Modernizing mature companies is hugely challenging. Moving from known revenue producing business models to new “disruptive” market offerings, business relationships and the design and implementation of the change management required to reinvent is ‘teaching an old dog new tricks’ on multiple levels. Even incremental change is hard for staff who are run ragged keeping the existing plumbing and lighting running, yet the pace of technology evolution is plain for all to see. We are rapidly leaving the IT era, but the next generation of technology is understandably not well understood and highly contextual to business vertical business opportunities and challenges.

Jobs are being automated away in large numbers as part of the sweeping societal change we are going through, raising questions around who the ‘consumers’ of future products will be and where they will find income to pay for things. QWERTY PCs are in the rear view mirror, with mobility and IoT dominating the immediate horizon. Old services models to assist mature enterprise business models are increasingly commoditized while there is arguably a vacuum as to who can provide effective As-a-Service partnerships with business entities which are struggling to modernize. Firms grappling to look good every ninety days in the equity markets cannot afford the investment to rip and replace large parts of their in-flight business infrastructures, but there is much angst and tire kicking to see which partners and suppliers have ‘the right stuff’ to assist in next generation business evolutions.

As I wrote in my previous post, ‘digital’ business conceptualizing has been dominated and overshadowed by marketing activities across online, mobile and other relevant channels. Listening, conversation, selling and support are vital aspects of business, but ‘core digital’ has not been adequately funded or evolved, leaving the ‘traditional’ enterprise services industries awkwardly stuck between old and new. Much focus has been placed on cost savings, including lift and shift of vast amounts of ‘stuff’ from on-premise to cloud without much thought about business opportunities (and challenges) enabled by moving everything online. Services providers have to keep their lights on and cash flowing like any other business – the better ones are chaffing at the bit to provide modern digital services to clients and prospects that are forward-looking, evolutionary, even revolutionary.

Innovation sessions to help ‘set in their ways’ clients find new revenue stream opportunities (and in some cases escape the burning platforms they find themselves on) are essential offerings from services vendors to remain relevant and brand their modern world credibility. Design Thinking is a great way to encourage business process oriented staff to ‘think differently’ about the place of old and new technologies in the evolving world. Ultimately ‘digital’ is the modern tool set available to businesses to evolve to greater efficiencies and revenue streams. However technology changes, people don’t and the challenge for the old guard is in moving with the times, whether on the buy side or the services side.

The Bottom-line: The future is all about data and human collaboration

Today the change challenge is evolving from old to new ways of doing things. Today legacy IT spend still dwarfs next generation spend, but it’s not hard to see the old ways of doing things drying up. What next generation services looks like in a world of AI, cognitive, robotics and IoT at all levels, superb supply chain and Amazon style global retail channels will primarily be focused on orchestration and automation to enable data and human collaborative flows.

The critical factor will be in who does what and when. Blindingly obvious maybe, but timing is everything to keep momentum, revenue streams and evolution unfolding and not stagnating….

Guts, determination and spirit – a touch of daring do? No people. It takes revenues. Cold hard cash. No more, no less. This is one of those times when it is all about the money.

That said, being on the list or not, shouldn’t make a service provider look good or bad – hopefully market forces mean that better/cheaper providers rise through the ranks, but it isn’t necessarily so.

So I’ve penned a short FAQ:

Can we make a mistake?

We are human and from time to time this happens – just send me an email and with your thoughts and we’ll correct. By all means call me names on twitter – but I may shout back…

We can miss companies from time to time and define where revenues go incorrectly. And, occasionally, spell your name incorrectly 😉 Also we may define things differently from you – we are trying to compare like with like as closely as possible. Remember this is an estimate – so if you have further guidance, I’d be happy to have a conversation to let you know how we came up with any of the numbers.

I should be on the list / What do you have to do to get on the list?

Sending us evidence (a financial report or two, would help) that shows latest annual revenues. We use calendar years for our lists usually, so something that shows the relevant quarters would work. But happy to have a discussion with any private firms – just so we can properly establish position. I am not a miracle worker so private companies that don’t publish results and don’t provide guidance may not make the list.

How much do I need to bribe you to change my position?

It pains me to say it but no – we just can’t. The pesky tax man (and our boring accountant) frown on it 😉

That said it is also free to be on the list – you just need to demonstrate that you have the revenues to make it. But I will check against public sources and validate.

I really want to be part of this but I just don’t have the revenues yet – is there anything I can do?

I am writing some short profiles on up and coming providers – let me know what your story is and we may feature you. Although we are mainly interested in IT services and BPO – so although I personally am fascinated by cool software. A software company’s story may get bumped…

Also we may start breaking out new lists – HRO providers, Customer Care, etc… any suggestions are always welcome.

While Accenture Digital is understandably focused on digital customer experience and marketing as revenue generators, the peak of mobile app development and regular consumer phone update cycles has passed for now. Accenture and other scale players are making massive incursions into terrain dominated in the past by big advertising holding companies. There is likely to be a next generation of digital devices soon, but there are questions as to whether Accenture and competitors are top heavy with “last mile” customer experience/marketing in a world where digital enterprise evolution is increasingly important.

While Accenture Digital is understandably focused on digital customer experience and marketing as revenue generators, the peak of mobile app development and regular consumer phone update cycles has passed for now. Accenture and other scale players are making massive incursions into terrain dominated in the past by big advertising holding companies. There is likely to be a next generation of digital devices soon, but there are questions as to whether Accenture and competitors are top heavy with “last mile” customer experience/marketing in a world where digital enterprise evolution is increasingly important.

Chetan: Yeah, Phil, a brilliant question. I think Paul would love to chime in on this one as well. The example that he gave is very apt—vendors wanting to know about the status of the invoices, vendors wanting to know if their checks have been paid and vendors who are doing business in over 50 countries wanting to be able to understand how their payment processing is doing and when they can expect the payment or what is the hold up for the payment and what are the prerequisites for the payment. It’s not just the typical cognitive or automation or, as you said right at the outset, the RPA: “Hey, I can do a password reset for you. I can do an account unlock for you.” These are real digital labor solutions where people can get qualified, not just the 40% to 60% opex improvements we discussed earlier, but also, very importantly, an enhanced customer experience—with the mean time to resolution improving.

Chetan: Yeah, Phil, a brilliant question. I think Paul would love to chime in on this one as well. The example that he gave is very apt—vendors wanting to know about the status of the invoices, vendors wanting to know if their checks have been paid and vendors who are doing business in over 50 countries wanting to be able to understand how their payment processing is doing and when they can expect the payment or what is the hold up for the payment and what are the prerequisites for the payment. It’s not just the typical cognitive or automation or, as you said right at the outset, the RPA: “Hey, I can do a password reset for you. I can do an account unlock for you.” These are real digital labor solutions where people can get qualified, not just the 40% to 60% opex improvements we discussed earlier, but also, very importantly, an enhanced customer experience—with the mean time to resolution improving. Paul: I think it will probably be similar to be honest, Phil. We really follow the market in kind of what’s a good fit for customers. So we’ve had an agnostic strategy, as you said, in the ERP marketplace. That said, you know there’s companies in oil and gas they have a certain preference to do things in a certain way, companies in public sector have certain preferences to do things in a certain way. So what we try to do is be responsive to the market, to understand our customers kind of down at a more granular level—not looking at just one kind of global market of something like ERP or cognitive solutions. Then we look for the best solution for different problem spaces and be agnostic with a point of view so that if a client comes to us with a certain type of a problem we’ll say hey, we know the best solution for that. In your case it’s Amelia. You know if it’s a different type of a problem, different type of a use case, different industry a different problem it might be a different solution. So agnostic with the point of view, I think will continue to be right. We’ll learn from our customers and learn what works and what best delivers the outcomes in these environments. That will be our general strategy.

Paul: I think it will probably be similar to be honest, Phil. We really follow the market in kind of what’s a good fit for customers. So we’ve had an agnostic strategy, as you said, in the ERP marketplace. That said, you know there’s companies in oil and gas they have a certain preference to do things in a certain way, companies in public sector have certain preferences to do things in a certain way. So what we try to do is be responsive to the market, to understand our customers kind of down at a more granular level—not looking at just one kind of global market of something like ERP or cognitive solutions. Then we look for the best solution for different problem spaces and be agnostic with a point of view so that if a client comes to us with a certain type of a problem we’ll say hey, we know the best solution for that. In your case it’s Amelia. You know if it’s a different type of a problem, different type of a use case, different industry a different problem it might be a different solution. So agnostic with the point of view, I think will continue to be right. We’ll learn from our customers and learn what works and what best delivers the outcomes in these environments. That will be our general strategy.

Over the past couple of months, we’ve been working hard to produce a number of documents that look at both market and service provider performances. We just wanted to summarise the ones we have published so far and give you an idea of the ones we are going to be released soon.

Over the past couple of months, we’ve been working hard to produce a number of documents that look at both market and service provider performances. We just wanted to summarise the ones we have published so far and give you an idea of the ones we are going to be released soon.