My colleague Mike Cook and I are in the middle of a blueprint on Managed Security Services, and as we talk to client references and review provider information, I’m reminded again about how difficult it is for clients to feel like they’ve really gotten the best possible team for their engagement, based on their investment outlay.

You might be disappointed with the quality of your team, and maybe you think it’s because it isn’t as good as you thought. Maybe they oversold their capabilities or flat-out lied about what they could do. While this is possible, in my experience, it’s more likely that clients confused the provider’s corporate image with the capabilities of the specific delivery and account team on their engagements. A provider’s capabilities are never evenly distributed across the entire company and the reality is that some delivery people are better than others. Plus, providers can often be very crafty with how they allocate their best and brightest to their clients.

A while back, I was at an event, and chatting with several vendor executives. A vendor management person from a buyer client that we all knew came over and started chatting. He looked at the company names on everyone’s badges and mentioned that his company worked with every provider represented there. Then, company-by-company, he pointed at each one and said things like “Yup, we hate you guys. We’re suing you. Your team is terrible. You never give us good people.” That broke up the circle quickly as everyone made excuses to move to other conversations!

And afterwards, two things that stuck with me: the first was that buyer getting up as a speaker at the event to talk about creating shared value and better relationships with suppliers (I kid you not!) The second was one of the providers sharing with me privately his frustration with that particular buyer, saying “he wants the “A” team, but he’s paying for the “C” team. And even still, all he talks about is cutting our rates in the next negotiation. Why would I invest in a client like that?”

This story highlights several reasons that a company many not get the “A” team from a supplier that have nothing to do with the supplier at all:

1. You aren’t mature enough. Providers can tell what your internal team is capable of – both for execution and understanding. A supplier won’t give you “A” level resources if they think you can’t appreciate the value. Now, of course, the question is “if you can’t tell the difference, how do you know it’s not the ‘A’ team?” And the answer is, you probably can’t put your finger on it but you’re vaguely unhappy and realize things aren’t progressing the way you want even if you don’t know why. Smarter clients get smarter teams.

What to do about it: This one starts with increasing your own expertise first so you can ask better questions, understand the answers better, and make your own suggestions of how to remediate so you can have productive discussions with the provider. When the provider sees that you know what you’re doing, they’ll give you better resources. In the story above, you wonder why the company was suing a provider – that’s the kind of thing that happens when you didn’t scope properly or weren’t smart enough to ask for the right things.

2. You’re cheap. I hear this one a lot. As a client, you’re complaining that you got the “B” team. But when you look at your rate card, you’re getting “C” team pricing. You may even have gotten the “C” team instead of the “B” team. This is exactly what frustrated the provider executive in the story – he was delivering better resources than the client paid for and yet the client wasn’t grateful, instead the client only complained that the resources weren’t good enough!

What to do about it: If you pay for the “C” team and got the “B” team, be happy. You’re doing better than most others in your situation. If you’re paying for the “C” team and actually have the “C” team, then you need to have a discussion internally about what your goals are. Maybe you’re actually ok with the service you’re getting and the complaints are just water cooler venting. If you’re actually having a delivery problem, then you need to look at increasing what you’re paying or changing the delivery model. You can change a delivery model by seeking to automate some part of the engagement and paying a little more for the resources you’re keeping.

3. You’re a bad client. Maybe you complain about things that aren’t actually wrong. Maybe you blame the provider for problems that really resulted from your internal team. Maybe you constantly want things that aren’t in the contract and get mad when you don’t get them. There are lots of variations on this theme. Here’s the thing: no one wants get abused as work, and top talent doesn’t have to put up with bad behavior. They’ll get switched to better clients. Or, worse, you HAD the “A” team and you beat them down until they’ve devolved into “C” quality work. While I don’t know the inner workings of the buyer’s organization, I can tell you that in this conference setting where provider normally love the chance to socialize with their buyer clients, providers avoided this person at all costs. That speaks to the poor relationships this person built.

What to do about it:Of course, if there are legitimate problems with the provider’s work, address it. But if the problem is really your team, then fix your internal situation. You can train your team to address challenges differently, swap your internal provider liaison or even fire staff that are creating a bad environment. You definitely need to get realistic about your expectations of the engagement. Then let these internal changes get demonstrated to the provider staff to show them you’re no longer the client from hell.

4. You’re not important. Sometimes you can be a great client from all sides – you pay well, you’re a pleasure to work with, and you have interesting work. But maybe you aren’t a big client, or you’re not a brand name, or you in fact have a weak brand (the “loser in your industry?) The provider is likely putting top talent onto clients that spend a lot of money or that have brands that with star power or they use as client references. In the story above, the client was important in its industry but had a reputation as a bad place to work, so there wasn’t the “star power” that often comes from a well-known brand.

What to do about it: This one’s trickier than the rest, because the only way to really fix it with your existing provider is to spend more money until you’re a bigger and more important client. Sometimes you can fix it by being willing to be a reference client, tell your account team if they fix the talent situation, you’ll agree to be a reference for future prospect or analyst calls. However, if you’re willing to go through a transition, you can solve this one by switching providers. You can look for a smaller provider so you can become a “bigger fish in a smaller pond” or a player who specializes in your industry so your brand becomes more important to that provider.

The Bottom Line: You’ll only be satisfied with your service providers when you deal with your own responsibilities to the engagement.

Get more realistic with your expectations based on the factors above and decide what’s good enough for your needs. Hold the supplier’s feet to the fire, but do the same to your own team. Addressing these internal issues will give you more value from your existing deals and also position you better for future work with your key suppliers.

There’s no two ways about it. I’m excited to be on the cutting edge of a Design Thinking-led services engagement in healthcare to address patient experience. Thank you to Lawrence General Hospital (LGH) and Sutherland Global Services for inviting me through the door and into this initiative…. and especially for agreeing to let me blog about it! We are constantly looking for where companies are “taking a detour with design thinking” and finding results to share. This time, we’re bringing you along on the journey.

We’ll start with a workshop led by Sutherland Labs, and follow their version of this human-centered, iterative innovation methodology over the next few months. The goal is to re-think the patient experience at LGH, and I’ll be sharing the progress here in my blog as we go. After months of researching, interviewing, and writing about Design Thinking and the value it can bring to a services engagement, I will be able to give you an inside look as well. If you have done this before, you can compare it to your own experience and perhaps find some new ideas; and if you haven’t, here’s a way to get some further exposure to a work in progress

Design Thinking can play a strategic role in helping healthcare organizations to better service the consumer as the patient, member, caregiver, clinician, etc… and rethink operating (and business!) models.

We believe design thinking can help bring about a more healthcare consumer focused type of engagement, which is so needed in health care today. With the latest news burning the wires that in the U.S., premiums are going up yet again, healthcare consumers are just going to get more discerning about how and what services they are receiving for their money. Value – always defined by the beholder – is changing for healthcare consumers. Being aware of that, and aligning the organization –front, middle, and back office – is simply becoming an imperative to the future health and success of healthcare providers, period. And service providers can play a role in doing so.

Despite the potential, and early success stories in and outside of the industry to date, the use of Design Thinking in healthcare for impacting business outcomes through operations is fairly nascent, as seen in Exhibit 1 from our recent Intelligent Operations Study, which included 45 Healthcare Operations Services Buyers. Only 23% of the respondents say they are using Design Thinking today, so we see LGH and Sutherland as pioneers here. For those of you who have not yet jumped into the waters, you can also find some ideas on how to get started in my recent interview with Charlotte Bui, Global Lead of Design Thinking at SAP… and stay with us here as this story with Lawrence General Hospital and Sutherland Global Services develops.

The LGH and Sutherland partnership to put patient experience at the center of reimagining the hospital business operations – the use of Design Thinking – exemplifies one of the 8 Ideals that HfS Research considers critical in the move to more “intelligent business operations.” As it is also one of the least mature of the Ideals in this services industry, they are breaking some new ground here.

Exhibit 1: The Maturity of Design Thinking in Helping Achieve “Intelligent Operations” in Healthcare Organizations

At the same time, fellow HfS analyst Hema Santosh, and I will be launching an update to the Design Thinking for the As-a-Service Economy Blueprint we published with Phil Fersht in early 2016. We expect to hear more about how service providers are using Design Thinking and incorporating innovation into their engagements, to be more forward thinking and investing in the long-term value of outsourcing services partnerships.

If you have a story to share, questions to ask, or challenges to pose, please fee free to post them here, or contact me at [email protected]. And, stay tuned…

Cognitive computing generally refers to having a system mimic the way people think, learn, solve problems or perform certain tasks. In HCM systems specifically, the system leverages what it knows about us — including our job, social network, and interests – to yield solid benefits in areas such as social recruiting and social learning.

We are also seeing take-up of some newer entrants into using NLP (natural language processing) in the form of chatbots and intelligent agents. Examples highlighted in my recent POV “Intelligent Automation in HR Services and Solutions” included an employee having a conversation with the system about an error on their timesheet that the system had the wherewithal to resolve … or the HR technology platform proactively pre-filling a timesheet based on items in the person’s calendar and previous timesheets.

So far, generally no controversy surrounding these type of cognitive capabilities … efficiency gains and better customer service without any apparent downside. But what if a near-future incremental step in the cognitive HR tech journey goes something like this:

Employee: Hi there, kindly initiate a PTO time off request for me for this Thursday and Friday after confirming that I still have the 2 PTO days to use.

HR System: I can certainly do that sir, but are you sure you want to take 2 days off this week given you have a major project deadline next Monday, the project seems behind schedule, and as you know, you were late on your last major project deliverable?

Can we say C-R-E-E-P-Y?

The norms regarding leveraging these capabilities in the HR/HCM realm will likely not be established anytime soon. We probably need a few high-profile lawsuits to be the catalyst, followed by consultants developing practices as quickly as they did for Y2K. In the absence of this, it’s reasonable to assume companies will start to get feedback from employees and job candidates that they were put off by the intrusive nature of their HR system interaction.

Until such time, here are four cognitive capabilities in HCM that go beyond (or way beyond) intelligent HR agents and chatbots. Some may still become standard HR systems capabilities and practices in the months or years ahead. For the time being, this is arguably a matter of weighing business benefits (ranging from efficiency gains to improving employee satisfaction/engagement) against potential liabilities that could include a total distrust of using the HR system — for anything!

Upon “clocking out” late one evening, the system notices that excessive hours have been worked by that employee in the last 2 weeks, and auto-emails the person’s supervisor a suggested communication advising the employee that … “the company values work-life balance, and they may want to consider getting back to a more normal schedule.”

The system recommends internal or external training courses to look into, or even a personal development coach, based on formal or informal feedback received (the latter from corporate social collaboration tools).

The system alerts a business unit head that a certain employee has initiated the processing of a leave of absence or early retirement, and identifies key “institutional knowledge” they possess (again based on formal or informal feedback) that should be transferred to other colleagues at the earliest.

A personalized, auto-generated on-boarding communication from soon-to-be team members who let the new employee know they have some things in common … e.g., school attended or outside interests or reside in same part of the city or birthday … and also expresses how excited they are to have them as a team member. (Of course, in this example, the “sender” would receive it first and have a chance to modify.)

Bottom Line: Cognitive capabilities within HCM systems will keep pushing the envelope, perhaps until lawsuits, governance issues or perceived creepiness get in the way.

My good pal, Steve Rudderham, formerly of Genpact, Capgemini and Accenture fame… and recently anointed the great GBS leader at Kelloggs, posed the irresistible question to me on our Robotic Premier League blog:

Phil, One thing we’ve struggled with is really where the rubber hits the road in terms of credentials. There are a lot of good innovation “stories” around RPA but several of the players on your list have really struggled to articulate savings and examples outside of their own in-house improvements using macros in excel. When do we expect more maturity in this space in terms of client stories that the rest of the industry can get behind?

Fair enough, Steve, great question… so here’s my answer:

@Steve Rudders –

It’s early in the morning, the filters are off so I’ll just answer your question as bluntly as possible: We live in ignorant times – people are blindly groping for that next vehicle to drive out cost, and RPA currently fits the bill.

I, personally, thought the hype would die down this quarter as companies struggled to figure out what not to automate. Don’t get me wrong, the RPA value proposition is tremendous – taking high throughput, high-intensity processes that require large amounts of unnecessary manual intervention and digitizing them to free up thousands of man/woman hours, is a terrific way to add value to a business.

But RPA is a murky, weird, and very complex, technical world – you need people with good process knowledge (not too hard to find), you need people to help evaluate what to automate in the software that makes business sense (you can’t automate everything or you’ll forever be automating and forever be spending money on automation) and you need technical folks who can help integrate the software behind the Citrix firewall in enterprises, who understand complex APIs and security issues. You also need a skilled change management plan as the “robo” paranoia can make the old offshore paranoia seem like chicken feed. Then you need some serious robo-governance competency… and these people are really hard to find. You can’t train your 28 year old MBAs to be robo-governators – these need to be your battle-weary operations leaders who know how to balance politics, panic, understand enough about tech to be dngerous, and can communicate the bloody stuff to leadership and middle management.

So to conclude, we will need some time before the true excel-proven results really materialize – and many firms will forever struggle to metricize the true ROI of RPA down on paper. It’s a bit like ERP 20 years ago – did anyone ever truly prove the ROI from huge investments in SAP or Oracle? It just became “assumed” that you couldn’t run a business effectively without and ERP system. In a couple more years, we’ll just assume you can’t run a business properly if you haven’t retro-fitted RPA into your down and dirty business processes to make some of them run better.

So most people associated with outsourcing and shared services are now aligning themselves in some way with RPA – the advisors are shaping up to make their clients look like they have a plan, the providers are working hard to make it look like they have RPA firmly embedded in their capabilities, and many savvy buyers are slapping RPA somewhere in their job title / job description.

But the true answer to your question – “when will we see more client stories the industry can get behind”? Simple – when the hype finally fades and those firms that made the smart investments finally put their experiences to print, unafraid to talk about how they improved their business with smart automation software. And this can take years – moving processes into software is a significantly more challenging exercise than moving them to lower cost people half way across the world.

One other issue, Steve, is the paranoia and reluctance of buyers to talk openly about their automation initiatives. Automation is being treated with a much more heightened degree of sensitivity than we ever saw with “outsourcing”.

Having said all of that, I do expect us to see many better communicated RPA cases next year simply because, for the first time, we have software marketing people in our services industry. Experienced software marketeers are simply better at getting their success stories across than services marketeers – because technology is at the core, not people. Enterprises are buying magical products to provide them with magical silver bullets… my concern is we could lose the very essence of operations… that they will always really be about people managing technology… not the other way around,

For outsourcing to continue to grow contracts need to move beyond simply removing cost and in addition add true value to the client. In HfS’s PoV, Defining the Seismic Shift from Legacy BPO to BPaaS we uncovered what BPaaS really entails. In this study, we identified that BPaaS is not simply platform-enabled BPO as some would have you believe. BPaaS contracts are fundamentally defined to deliver business outcomes such as revenue growth, with KPIs and SLAs like average handling time being more about tracking and reporting on progress as opposed to being the only reason for payment. This approach requires a significant level of trust between the service buyer and the service provider – trust that is based on experience, credibility, or the combination.

The focus and purpose of BPaaS are not on how results are achieved, but the fact of achieving them (or not). In some cases, the service provider is paid based on the outcome, such as incremental revenue that is recovered in a collections operation. In other cases, while there is a specific business outcome in the contract, such as increasing medical adherence, the payment is based on a transaction, such as number of patients managed, or number of payrolls processed. For example, Webhelp’s contact center contract with UK retailer ShopDirect, whereby Webhelp is paid through a combination of FTE pricing and an outcome based model that varies according to service line, examples of outcomes include revenue gained, first call resolution rates etc.

With the amount of control placed in the service provider’s hands, trust is the key building block in BPaaS contracts.

BPaaS contracts are very seldom undertaken by first generation outsourcers. The level of trust involved in handing over complete control of processes is not something buyers are willing to undertake lightly. More often than not these BPaaS contracts evolve from well-established and successful BPO deals.

Another aspect to consider and something I have recently witnessed firsthand as I’ve visited a few South African BPO service providers (jealous much?), is the location of account management teams. Almost without exception, traditional BPO contracts I have witnessed have a top-down directive account management team based onshore with the client. This creates a further barrier to communication between service delivery and service destination, which can potentially hinder the development of trust needed to move to a BPaaS contract. Conversely, all BPaaS contracts I’ve covered during my time here have a dual account management function with one onsite at the delivery location and the other onshore near the client’s head office.

Is this dual account management function a symptom of a BPaaS or is it a key enabler of making these BPaaS contracts happen? The answer, more than likely, lies somewhere in the middle. This dual account management function creates a more fluid communication channel between the delivery center and the client. This communication helps to dispel the fear of complete loss of control from the client side and lead to a greater degree of trust.

Bottom Line: The key takeaway, however, is that this dual account management function could be a key factor in facilitating the transition from traditional BPO contracts to BPaaS partnerships by increasing communication, trust, and onsite presence.

Security’s a hotbed of complexity – many different kinds of threats, technology that’s evolving all the time, and businesses can’t keep up. Changing standards and incredibly complicated threats make most non-technical buyers either throw the problem over the wall to their technology team (and miss out on the value of a business-led security approach) or their eyes glaze over at the mere mention of security and never really give it the attention it requires.

And what’s worse is that this complexity isn’t getting better, it’s getting worse. That’s why we all need to get over our apprehension, fear, boredom, and whatever else is keeping us from really understanding what we need to do in security. The best way to do that is to keep a business-value focus on it, making sure we learn what we need without digging too deep into the weeds and getting frustrated?

Bridge the divide between the highly complex and the need-to-know by focusing on three core, interrelated areas:

Digital trust: Your ability to succeed in the digital environment requires that your trading partners (customers, suppliers, external stakeholders) trust you to be ethical, legally operating, and practicing up to date security procedures to protect their data and IP. If others start to doubt your ability to secure your own data or theirs, you are dead as a business. It’s pretty simple as a concept and amazingly complex when executing.

OneOffice: Digitization and the renewed rise of customer-centricity mean that the wall between back office and front office has collapsed – everyone in a company is customer facing in this age where customers have significant visibility into our internal operations. That means your security policies, procedures, and risk approaches need to be brought up from the basement and shared across your entire organization.

Shared responsibility: Security isn’t just something you worry about within your four walls anymore. As data and IP get shared across trading partners, the need for a shared view on securing digital assets becomes critical. Everyone in a trading network owes the other members a secure environment, so sharing accountability for security will become the new normal.

We started our security resolution early by publishing new research that defines the eight prerequisites of digital trust, including data integrity, business alignment, and device security, among others. And then we’ll be building on that by publishing our findings on how well service providers can help clients with managed security services for digital trust in February 2017.

Don’t be intimidated by security challenges, put them in the context of your business and make progress toward digital trust. Here’s to a secure, business-focused 2017!

The range of information managed in HCM Systems is quite impressive, and in most leading platforms, encompasses data relating to the 3 legs of the proverbial (HR data) bar stool: Administrative, Transactional and Strategic data. Administrative covers what’s needed for policy and regulatory compliance and core HR process support (on-boarding, payroll and benefits admin, etc.). Transactional covers the events in an employee life cycle (changes to job, organization, supervisor, compensation, etc.) or personal life event updates that impact employee benefits for example.

Strategic data covers … hmmm … maybe just see Administrative and Transactional.

Is this HR heresy? Is it a yearning for the simpler days of Personnel Management when key business strategy decisions often excluded HR executives, HR/HCM systems largely weren’t used outside HR Departments, and Talent Management was a term reserved for Hollywood? No, it’s only a lead-in to a question I’ve asked myself over the years, namely: Are we missing something when we point to data tracked on HCM systems like performance ratings, compensation and job progressions, training courses taken or competencies displayed and say this allows us to be very strategic in managing human capital?

Yes we are probably missing something. It seems the data we track in these technology assets, while broadly useful, might sometimes be obscuring the real mission at-hand: The need to manage and provide ready access to WHATEVER people data enables a highly engaged and productive workforce, and the proactive management of business risks and opportunities … thereby creating and enhancing sources of business value and competitive advantage.

So What Needs to Change?

For one thing, let’s not forget the aforementioned mission at-hand. Let’s also not forget that employee engagement, retention, productivity – and business innovation and agility – are all HCM-related themes but they are NOT HR processes with routinely defined steps that can be system-tracked or enabled. Perhaps just as important, these themes rarely have a single process owner with a budget (for enterprise software) that solution vendors can sell to. The main implication of this is that while HR Tech circles continue to espouse moving away from being too process-centric, and being more ‘desired business outcomes’ centric in our systems design and usage, the HR/HR Tech disciplines can perhaps be faster on the actual uptake of this.

3 Examples of (Non Process-Centric) HR Data Worth Tracking

Employee Value Indicators … present a broader picture of the employee’s value to the organization, far beyond performance ratings or competencies. These dimensions or data points might relate to referring candidates who became top employees, serving as a mentor to new employees, suggesting ideas that led to new revenue sources or operating efficiencies, or forwarding personal contacts that were great sales leads and became customers.

And speaking of competencies, how about Latent Competencies … those that employees possess that might be invisible to the organization, and therefore not leveraged, because they are not relevant to an employee’s current job function. These would be pretty handy when a major shift in business strategy is considered which has implications in terms of re-tooling the workforce. Also Competency Value Trajectory (or “CVT”) would be a simple way to note on the system which competencies are becoming more important to the organization due to impending business undertakings.

And finally, one that arguably qualifies as not seeing the forest through the trees, all the valuable data that could be tracked around Career Goals … including how an employee’s goals change over time, progress toward achieving them, and what the organization has done to support them. This way of driving employee engagement could fly by the positive impact of employee surveys or various (non-sustaining) forms of employee recognition for 2 reasons: Employees perceive their needs/interests as being important to their employer; and management decisions about leveraging their people better align with those needs/interests.

Bottom Line: HR Tech’ers should not forget about the virtually limitless potential of these platforms to house strategic, and often non-process centric data

A focus group I conducted a few years ago with a dozen CHRO’s addressed where HR Technology was — or wasn’t — making a difference in their organizations. The consensus was that managing the potential fallout from downsizings, or the people aspects of M+A’s were areas where HR Technology was not playing a major role … both obviously more about potentially game-changing events than defined HR processes.

As HCM system configurability and extensibility capabilities have achieved new heights in recent years, addressing these perceived (historical) system shortcomings have perhaps become a matter of customers doing a better job of defining decision support needs and related data capture processes, and simply leveraging their HR Technology assets better in general.

We did in once, we did it twice… and I bet you never thought we’d do it a third time. Yes, amigos, it’s the 2016 airing of how effective the leading service transformation providers are in that beloved RPA space that just refuses to go away…

Ever since HfS bought the topic to the attention of stakeholders back in 2012, the robotic thrum of RPA throbs louder and louder. With the conference circuit over-flooded with more and more RPA conferences, robotically repeating the same rhetoric, the actual RPA deployments are significantly scaling up and M&A in the space is gaining momentum. Yet, true meaning and definition of what truly constitutes “RPA” are as blurred as ever, as more people jump on the bandwagon who couldn’t define cognitive vs digital vs autonomics, if their job really depended on it. Enough reasons to take stock where this industry is at, and add some definition and clarity to this fuzzy world into which we’re stumbllng. With that in mind, we asked our analytical Automation Overlord, Tom Reuner, to talk to the industry’s stakeholders who buy, sell, implement and generally go nuts over this stuff… and take a fresh look at the market dynamics.

So, Tom, amidst all this noise what is really going on in RPA these days?

Noise is a good way of describing it, Phil. Yet, underneath the surface, we are seeing clear signs of maturation. This maturity manifests itself in different ways. The pace of change in which the suppliers are building out automation capabilities is nothing short of astounding. Most providers are embracing a holistic notion of Intelligent Automation ranging from RPA to Cognitive Computing to AI all the way to self-learning and self-remediating engines. However, we must be careful not to confuse building out capabilities with traction in the market. At the same time the leading tool providers such as Blue Prism, UiPath and AutomationAnywhere are expanding their capabilities mostly toward operational analytics and the broad notion of cognitive. Lastly, buyers demonstrate a much more solid grasp of the implications of RPA, both on the technical side as well as around the business implications. Mature sourcing organizations are starting to build out automation centers of excellence cutting across business units and automation technologies. Thus, the tool-centric discussions (often a pure tick box exercise) of the early RPA days are getting less and less.

However, despite all those positive developments there continue to be constraints. The key one jumping out is the scarcity of talent. Putting a bot into a process is not too difficult. Scaling them up to an industrial level and having both the technical know-how and process knowledge is quite another thing. It is here where the differentiation between the various providers is starting to crystallize.

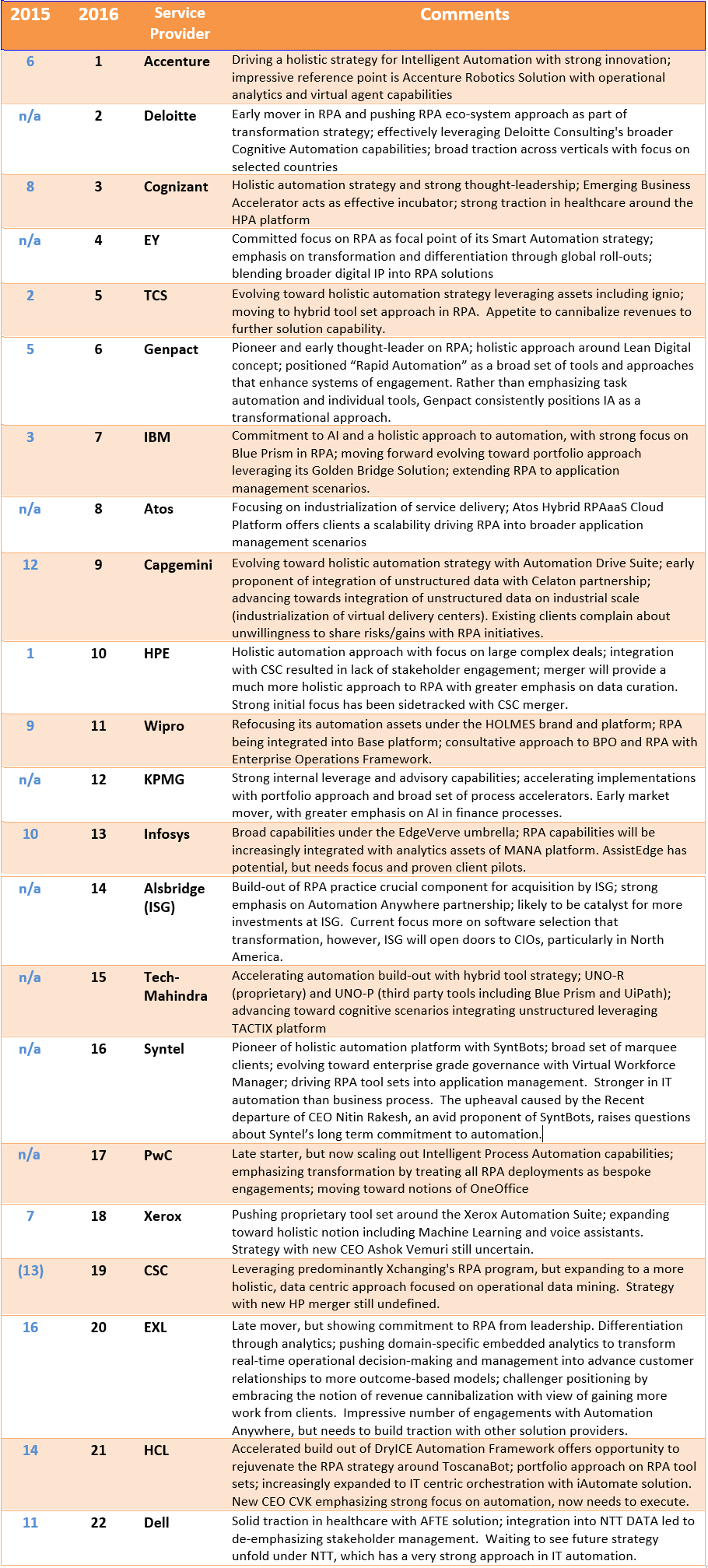

What has really changed since the last HfS RPA Premier League Table?

Really all change, Phil. The 2015 RPA Premier League Table was a reflection of a still nascent market. At the time, Charles did a great job of benchmarking providers against the HfS Maturity Model, but invariably the emphasis was still strongly around the strategic vision and the effectiveness of the market communication. In 2016 the market has strongly progressed toward understanding and applying RPA as transformation projects. We are finally starting to overcome the early misconceptions that RPA is a turn-key solution, non-invasive, low risk and largely focused on replacing FTEs. Not least from many failed projects the market has learned that, unsurprisingly, life is much more complex. Underlining this point, RPA tool providers have progressed to push notions of virtual and/or digital workforces. Equally, RPA increasingly is seen as part of an automation eco-system rather than a silver bullet.

As a direct consequence, the market is becoming increasingly bifurcated. The leading providers that are heading the 2017 iteration, are positioning RPA as transformational projects. The process owners have been put back center stage and discussions focus on the whole continuum of Intelligent Automation rather than just RPA. Aligned with that data curation is becoming increasingly a focal point as organizations are advancing toward the As-a-Service Economy. With that, we are seeing the rise of the Big 4 but also organizations like Alsbridge who is expanding from broader sourcing advisory. However, the other half of the market remains stuck in understanding RPA as a placeholder for short term cost take out, task automation, often on a sub-process level and often without the knowledge of the process owner.

Lastly, M&A is accelerating with Pega having acquired OpenSpan and just this month ISG acquired Alsbridge. And the market is rife with rumors about more transactions. In our view, M&A is a strong benchmark for increasing maturity as money talks louder than PowerPoint.

So Tom, what was your methodology behind putting together the 2017 RPA Premier League Table?

The RPA Premier League Table is building on and following up on the discussions for the HfS Intelligent Automation Blueprint. Thus, RPA should be seen as a subset of the broader service delivery capabilities of the service providers. The input for the Blueprint was enhanced by additional material and discussions with the respective service providers. Additionally, we had discussions with Blue Prism, UiPath, and AutomationAnywhere to get a steer on their partner eco-systems. Based on these inputs we have evaluated the services providers against the following criteria:

Vision and credibility of RPA strategy

Driving value through end-to-end process view as opposed to short term cost cutting

Breadth and maturity of internal tools and external partnerships for RPA

Scale of deployments

Integration of RPA in delivery strategy

Commercial traction

Effectiveness of marketing effort behind RPA strategy

Not beating around the bush, who is standing out as RPA performer?

Phil, the leading providers are blending a holistic approach to automation with broad transformational capabilities. Top of the tree is Accenture who is complementing its consulting capabilities and a plethora of third party tools with its new proprietary Accenture Robotics Solution. The solution is modular and able to integrate optional technologies for each client, for example, by using Google or Facebook APIs when needed. Deloitte is the strongest riser in the RPA Premier League Table by pushing a holistic transformation agenda. Cognizant’s automation team within the Emerging Business Accelerator (EBA) is at the vanguard of educating the market place on the implications of automation. Close behind the leaders is EY and TCS. EY has embedded its RPA approach into the broader Smart Automation Framework with a strong focus on transformational projects helping clients to move toward self-service and CoEs. Conceptually, EY is moving toward the notion of the OneOffice. TCS’ RPA approach has significantly matured, in particular by embracing a hybrid tool strategy and by focusing its go-to-market around nuanced use cases. However, the context is by no means just BPO centric scenarios. Atos and Capgemini are examples for driving RPA tool sets into application management scenarios. Alsbridge stands out as one of the few sourcing advisors, and the only one with a global presence to expand its capabilities into RPA implementations. These capabilities were a key consideration for the acquisition by ISG.

Gazing into a crystal ball, what can we expect for 2017?

If I would have all the answer, Phil, I could make a lot of money. But on a serious side, two issues are standing out for me. First, M&A will accelerate and disrupt the market. Following on from the acquisitions of Alsbridge and Automic, leading tool providers as well as the leading pure-plays are likely to be absorbed by acquisitions of the next 18 months. This might lead to more proprietary tools being developed, both to mitigate those risks but also to allow for broader functionalities. At the same time, go-to-market strategies have to be adapted as the large management consultancies will play an increasingly dominant role as RPA deployments will pivot around transformational projects. Second, the rise of Virtual Agents. We will see increasing traction of virtual agents that will fundamentally change the notion of service agents. These deployments will push more holistic automation approaches while disrupting workforces. Thus, these agents will increasingly offer broad management capabilities such analytics and integration capabilities for code and files. Therefore, the focus will shift toward enabling a seamless customer journey underpinned by broad knowledge libraries, dynamic case management and above everything else NLP. Thus, RPA will have to be part of ever more holistic automation approaches.

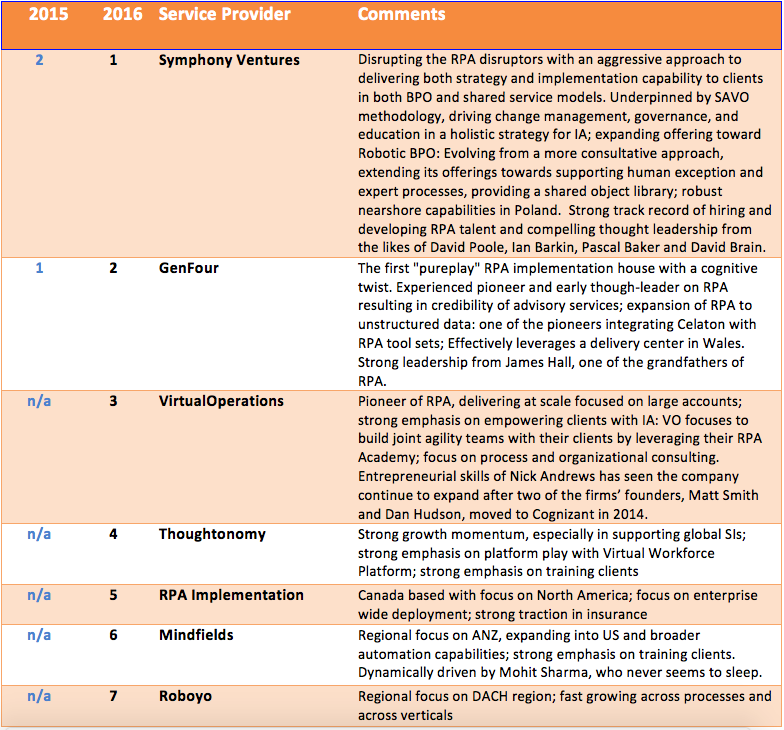

So who do you call when you want a robot? When we embarked on the 2016 RPL, we had to evaluate all the professional services firms operating in the space – both to help clients develop an RPA roadmap, evaluate the RPA software options and alignment with their processing requirements, and ultimately get some help implementing the solutions, developing out the RPA team and creating a workable robo/human governance structure. In addition, many clients find themselves in conflict with their BPO providers and need third party help to bring them together to find workable risk-sharing compromises.

What has transpired is several smart people, mostly working for BPO firms, eyed the RPA value proposition emerging, shortly after time we introduced RPA to the services industry in 2012, and they hatched plans to jump ship, club together and do lots of consulting work to build up their organizations.

Due to the murky, complex – and often very technical – needs of RPA, the demand for skilled expertise from real specialists is unprecedented – which is why we’ve seen the Big 4 leap into this space – but also why we’re seeing some of these small, highly-focused, players in real demand. And they’re not only making money working with clients seeing to RPA-ify BPO and shared services environment, they are also training many of the service juggernaut services to implement RPA for their clients. In short, there’s a lot of business to go round and you will often see these curious RPA pureplay folk huddled in the corners of conferences, sharing war stories and even passing business over to each other because they ae simply too overwhelmed with client demands to take it all on.

So, without further ado, let’s take a look at the seven candidates out there in all their naked glory….

Wipro has recently been firing on all cylinders to get going on its ‘drive the future’ strategy for growth. We wrote about their smart move on acquiring Appirio with the opportunity to bring together consulting, IT integration, BPO, and global delivery scale. From my recent conversations with its analytics leaders, I’ve seen a similar “combination” strategy resonate around Wipro’s analytics stack.

The new Data Discovery Platform, or DDP, is becoming its flagship solution for exploratory analytics projects in the big data realm. It features industry apps and is built using open source technologies, including a Big Data Ready Enterprise (BDRE) data product from Wipro as its data ingestion layer. This platform works across the lifecycle of managing data in an enterprise data lake that makes it possible to ingest, organize, enrich, process, analyze, govern and extract data quickly, significantly accelerating a big data implementation in a cost-effective manner. The DDP is beginning to find meaningful examples with enterprise clients, with upwards of 50 engagements in some stage of piloting.

Apart from DDP, we heard other examples where Wipro is trying to evolve its role to deliver more business value in analytics engagements. What is interesting among all these is Wipro’s approach:

Placing a greater focus on partnerships: DDP, for example, relies on a partnership driven ecosystem, along with open source technologies driving the core. For a life sciences client that has not yet invested in a data lake and gone down the path of setting up its big data infrastructure, Wipro has sought out and partnered with companies in areas such as data cataloging, to stitch together a joint value proposition. It is also actively evaluating how its portfolio can be enhanced by leveraging:

partners such as Tableau and Trifacta

internal capabilities such as Wipro Holmes, which is under the CTO’s umbrella but is being leveraged by the analytics practice for NLP, ingesting unstructured data and automation

companies in which it has made investments such as Talena and Opera

Taking more risk to deliver value: The value of bringing new thought – and more importantly – new actions, cannot be underestimated for a service provider like Wipro that has over a decade of delivering standardized data and analytics services under its belt. A financial services client expressed interest in bringing more integration in its BPO processes and the reporting, BI and data services that Wipro delivers. The service provider collocated the teams and is exploring collaborative opportunities to improve the overall business outcomes for the client from both service areas. In another example, Wipro is making joint pitches to consumer-facing enterprise clients in collaboration with a leading direct mailing company. The combination of the company’s vast amounts of valuable consumer data with Wipro’s big data capabilities is enabling them to have a more meaningful impact on multichannel marketing through targeted consumer insights.

Investing in new kinds of talent: Wipro has recognized the need for more consultative, business-led conversations and expertise as it tries to make its way from the CIO’s office to analytics decision makers in other parts of the client organization. It is steadily building a team of consultants in the U.S. that have functional/vertical experience from working in the industries, working knowledge of analytics and data sciences and can drive early conversations with clients to evaluate their needs, frame the right use cases and work with analytics teams to deliver results against them. Data platform engineering is another area where Wipro is starting to hire new talent locally to help build out the layers of technology required to run analytics in the future, including data architecture, data mining, search indexing and machine learning. To create a business-focused culture, Wipro’s analytics business runs its own competitions like Datathon, and participates in the TopCoder community for data science and advanced analytics competitions.

Bottom-line: The potential is there, but Wipro’s real challenge is aligning analytics beyond the IT function

We believe that these leading indicators of change are promising, and could help Wipro with its goal of more ‘drive the future’ digital engagements, using analytics as a key lever. What is yet lacking is a cohesive and simplified messaging around all the new and ongoing activities. Wipro’s analytics leadership is out there with its technology vision and roadmap (e.g. what information architectures will look like in the future and what partners to work with). We’d like to see how Wipro builds on this approach to champion and enable non-IT (or non-techie) analytics decision makers with an industry and functional lens.

Cognitive computing generally refers to having a system mimic the way people think, learn, solve problems or perform certain tasks. In HCM systems specifically, the system leverages what it knows about us — including our job, social network, and interests – to yield solid benefits in areas such as social recruiting and social learning.

Cognitive computing generally refers to having a system mimic the way people think, learn, solve problems or perform certain tasks. In HCM systems specifically, the system leverages what it knows about us — including our job, social network, and interests – to yield solid benefits in areas such as social recruiting and social learning.