This is era of the emerging BPO provider, as IT services stagnate and clients demand greater personalization and attention from business services firms that have the scale, resources, hunger and technology enablement skills to take on increasing complexity and make sense out of the dataswamps plaguing so many of today’s businesses.

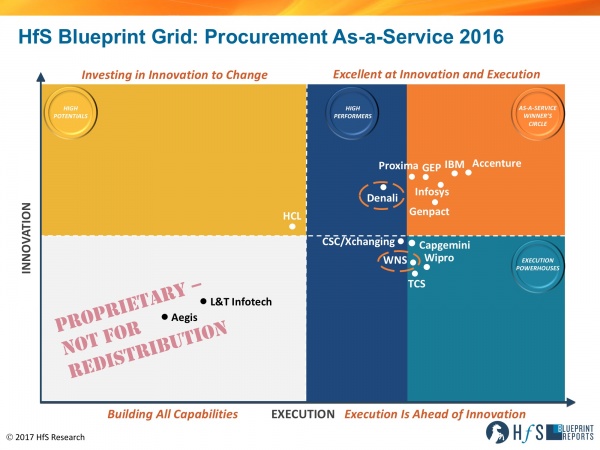

One such stalwart of BPO, quietly going about its business over the years with steady growth and increasing reputation for solid delivery, is WNS (yes, the one that was spawned out of the British Airways captive back in the day). WNS has performed well over the years, growing business streams in knowledge process domains, finance and accounting, insurance, travel, mid-size banks, contact center and some other areas. It has oft-threatened to make a grander procurement BPO play, but mostly opted to partner with the likes of Denali when the need arised.

In my view, having solid procurement delivery capabilities goes hand in hand with F&A, so it’s refreshing to see WNS snap up one of the best pureplay strategic sourcing providers left in the market, which should make the merged entity a Winner’s Circle contender later this year when we rerun the Procurement-as-a-Service blueprint:

So let’s hear from our Procurement and Supply Chain analyst, Derk Erbé, who’s recently emerged from a major analysis of the procurement services market:

WNS + Denali – The Details

To start the New Year with a bang, WNS announced the $40 million acquisition of Denali Sourcing Services. We have covered both WNS and Denali in our December 2016 Procurement As-a-Service Blueprint. WNS is ranked as an Execution Powerhouse, while Denali is a High Performer in the Procurement As-a-Service market.

The acquisition of Denali Sourcing Services is a good move from WNS, and effectively bolsters both organizations’ capabilities. Building on a partnership that has developed over the last couple of years, in which WNS and Denali together offered end-to-end procurement solutions, these two organizations know each other well and have extensively explored their complementary capabilities. Integrating and move forward as one is a logical next step.

Denali is an agile and dynamic strategic sourcing and category management pure play provider of procurement managed services, known for strong relationships with clients and quality of their personalized account management and service delivery. WNS’ strengths lie in procure to pay (P2P), transactional and tactical procurement services, often part of a multi-tower BPO engagement stemming from its F&A process heritage.

Delivering large end-to-end Procurement-as-a-Service was a partnership effort for WNS end Denali, with Denali providing the upstream Source-to-Contract (S2C) scope and WNS providing the large scale downstream Procure-to-Pay (P2P) scope or as part of multi-tower engagements.

What immediately fits well

WNS procurement clients have commented positively on the level of access and commitment shown by WNS senior management. The expertise and empowerment of their project management teams and their hands-on management style fits well with Denali’s personal account management style.

Denali was one of the pioneers of on-demand, managed services in the procurement market. It has build out on-demand As-a-Service offerings and commercial models over the last several years. Its plug and play “Category strategy on demand” platform is a fitting example. WNS is known for being flexible in delivery and commercial models, going the extra mile to meet client needs, earning a reputation of being easy to work with.

Exploring key complementarities

Besides the common ground Denali and WNS share, there are a number of challenges either organization had in the Procurement As-a-Service market which are addressed by this acquisition.

WNS lacked in innovation in Procurement As-a-Service. Clients express a desire for innovative ideas and proposals from WNS. Briefings HfS had with WNS show us their willingness and ambitions to become a more innovative partner for clients. Denali has been an innovator in the space for years and adds a valuable piece to WNS in terms of innovation.

WNS needed to move up the strategic value chain. In order to position itself as a more strategic partner to clients, we encouraged WNS to focus on immersing at more strategic levels in the client organization. A more pronounced vision and thought leadership for change in procurement is a vehicle to engage more senior leadership at client organizations and the addition of Denali’s strategic procurement acumen and thought leadership fills this gap.

Vision for the future of procurement. In our Blueprint, we challenged WNS to develop and articulate their vision for Procurement As-a-Service; “WNS procurement deals are generally just a component of multi-process BPO engagements. HfS would like to see a greater vision from WNS as to how they will transition in the future to offering more modular procurement solutions which is where we believe the PO market is heading over the next several years”. Denali has a strong vision and strategy for Procurement As-a-Service, for instance around Category Enablement, offering on-demand academy, templates and coaching to category strategies and category plans, adding capability that sustains the client organization. This vision resonates with more mature procurement organizations and younger hi-tech organizations looking for different ways to organize procurement.

North America: Denali gives WNS a much needed foothold in North America, where most of Denali’s revenue comes from (~95%). Denali needed to expand its geographic footprint further to continue to compete with the larger global delivery capabilities of competitors.

Implementation and program management. One of the challenges we noted from client in the Procurement As-a-Service Blueprint is the need for Denali to give additional attention for the planning of implementations and the project- and program management capability

End-to-end services. Although Denali served about a fifth of its clients with end-to-end procurement services, the focus and strength has always been upstream, strategic procurement. WNS’s strength in downstream, transactional procurement needed to be complemented by upstream capabilities to compete for more valuable and interesting deals in a market looking for help in strategic sourcing, category management, analytics while automating big chunks of transactional procurement processes. The successful partnership between both parties addressed this need to a certain extent, but with buyers consolidating in procurement, having ‘one throat to choke’ can be a plus in the current market.

Remaining challenges

WNS and Denali have a great fit and several high value complementarities that will strengthen their capabilities. There are however a number of challenges that this acquisition doesn’t solve. WNS needs to keep its focus on these areas to become an even bigger challenger in the Procurement As-a-Service market.

Procurement Technology. Although Denali brings a number of proprietary technologies into WNS, it still lacks the core procurement technology platform many of the As-a-Service Winner’s Circle providers have. Expanding partnerships with procurement technology platform providers like Ariba, Coupa, Tradeshift is part of solution to this challenge.

Invest in methodical process improvement. Clients love Denali’s flexibility and willingness to engage in a consultative manner, but would be willing to trade some of that for a more process improvement oriented and best practice sharing culture in delivery. WNS can also do more to provide proactive and methodical process improvement into engagements according to clients we interviewed for the Procurement As-a-Service Blueprint.

Knowledge sharing and client communities. Clients love to be more involved in client communities, learning from experiences and developments in other client organizations. We mentioned this can contribute to Denali’s role of innovation partner, even more in the new constellation.

What this means to the market

This acquisition is not going to shift the market dramatically nor is it putting leading providers on notice. The direction of the market is clear and the move to smaller, shorter, on-demand, modular, As-a-Service delivery and commercial models focused on value adding strategic procurement will continue. The talent shortage in upstream procurement is growing and WNS has managed to secure one of the sources of sought after strategic sourcing and category talent in Denali. The WNS/Denali combination is a stronger competitor for end-to-end procurement, providing the market with a stronger alternative for clients looking for a flexible, collaborative approach.

Bottom Line: Finally some long awaited action in the evolving Procurement As-a-Service market

Analysts and market experts expected a lot of M&A activity following Accenture’s acquisition of Procurian in 2014. Denali was one of the pure play procurement specialists on the M&A radar. In the years following the Procurian acquisition, not a lot of movement materialized. This acquisition by WNS not only expands on an already successful partnership, a fact that can help the post-acquisition integration efforts and increase time to value for this acquisition, it also makes a lot of sense from the market direction and capabilities that are needed for Procurement As-a-Service.

It brings together two organizations that showed a willingness to invest in flexibility, meeting the varying needs of clients with delivery models, pricing options and commercial constructs.

One of the keys to success is the positioning of the new WNS/Denali procurement practice in the market.

Derk Erbé is Research Vice President, Supply Chain, Procurement and Energy at HfS Research (full bio here). Derk is responsible for a compelling, leading-edge research agenda covering the core topics of interest for buyer and vendor communities in the areas of digital business transformation services and business operations, with a specific emphasis on key vertical markets, namely Energy, Utilities and Resource Industries.

With the continued rise in cyber security threats, highlighted by the recent Tesco banking breach in the UK and the ongoing Russian hacking debacle in the US, organizations across industries are scrambling to get their cyber security measures in order. The General Data Protection Regulation (GDPR) and the Network Information and Security (NIS) directives in the EU have only increased the urgency for organizations in this region to bolster their cyber defenses.

This urgent need to address cyber security, coupled with challenging hurdles to overcome in building internal security practices, is driving more firms to partner and outsource this critical business function.

One of the key internal hurdles we have identified in this market is that clients are challenged to source the required talent to keep abreast of their security requirements. This is a well-documented problem within the cyber security community and is one of the top three drivers that is shaping and driving the outsourced cyber security market at present.

So, the solution seems simple enough, if you can’t find the talent, hand over the responsibility on to someone who already has it.

But this begs the question: if there is a lack of security talent in the market how are service providers finding it?

Well, not easily is the answer. The more successful service providers have branched out and are tackling this problem from several angles. These can be largely categorized under external sourcing and internal sourcing:

External Sourcing

Hire young: For most of the leading providers in the market, partnering with universities to hire graduates straight out of the gate has been a go-to method. EY, for example, has partnered with 12 of the leading universities that provide courses on cyber security and analytics in the US. EY has not stopped there however and is now building partnerships with six smaller regional universities to further plumb the graduate talent pool. Often within these university/service provider partnerships, the service provider is fundamental in helping to shape course work and the curriculum, this is a positive dynamic as it gives students the skills needed to hit the ground running in the workplace.

Increase diversity: For example, reach out at the grass roots level to mentor female students taking analytics, mathematics, and related courses into the cyber security field. Capgemini has made a huge push in this regard with 20% of its UK and 25% of its Indian security operations now female. Next is looking outside of the professional sphere and into the military, many operations specialists in the army possess the necessary skillset to thrive in the cyber security field. Finally, is an apprenticeship scheme whereby hiring is conducted on behavioral and cognitive characteristics rather than qualification.

Poach: Or in corporate terms “hire laterally”. With the cyber security talent market lacking the volume it currently requires, attracting talent from competitors, or in some cases startups, is typically going to be on the cards.

Internal Sourcing

Upskill: This is basically what it says on the box, taking junior staff and putting them through internal and external training qualifications such as the Certified Ethical Hacker (CEH) or GIAC Certified Penetration Tester (GPEN) certificates.

Creatively use the people you have: The service providers covered in the (upcoming) 2017 Trust as a Service Blueprint all have overall staff counts in the thousands (some in the hundreds of thousands). With such a wide and deep IT talent pool, it makes sense to laterally pull in staff from other divisions in the organization. The most common positions targeted for internal transfer to security teams include application developers, risk and compliance, people assessment and digital transaction professionals. These staff will then be trained in security courses complimentary to their previous experience and skillset.

Sourcing security talent, even for service providers, is a challenge. The one ace these service providers have up their sleeves is the large and diversified IT workforces they have to hand. Some service providers are sourcing up to 60% of their security personnel from inside. With this in mind, organizations need to carefully consider the cost and time involved in building an in-house security team over partnering with and integrating capability from ones that have already fought the battle.

My preoccupation with change management can be traced back to when I realized that success on HR Technology initiatives was perhaps more a function of the organization being “ready, willing and able” to change (in the form of leveraging new technology) than anything else, including the virtues of any particular system. Now before some folks in the vendor community or others fascinated by shiny objects yell “blasphemy”, let’s remember that:

Any HCM system (aka HRMS) that‘s been successfully deployed in hundreds of similar organizations likely provides at least 80% of the major process-enablement capabilities a typical customer needs, plus many innovative people management features as well.

It’s unlikely that any HCM system will 100% match a buying organization’s business requirements, let alone their future vision around managing talent for competitive advantage.

Much of the gap between 80% and 100% can often be addressed through a combination of configuration tools, influencing the vendor to address in an upcoming release or product update (more frequent updates with cloud delivery) or inconsequential process workarounds.

Successful HRMS implementations are more linked to factors outside the chosen technology, and the #1 factor is (internal) customer-centric change management.

It took me some time to have the above epiphany partially because senior management and project sponsors at my first few employers generally assessed project success based on the system being delivered on-time, on-budget and stable. End-user adoption and business case realization were rarely on the project charter in those years. You could say this was fairly helpful to my HR Tech career at the time, but not so helpful to those particular organizations as a whole.

As a result of inadequate attention to change management in the first few rollouts, very few folks outside the HR Department used the system at these companies, and worse, most line managers maintained their own spreadsheet with HR data and related update processes. They simply trusted their own, personally crafted low-tech data repositories more. These dynamics can cost companies millions annually. (Post a comment below if you’d like to see the math!) What was missing? All future end-users needed to be “ready, willing, and able” – a framework used by many change management experts.

“Ready” suggests the impacts of the change are understood, and sources of resistance and associated mitigation steps identified. “Willing” relates to the case for change being widely syndicated, tailored to stakeholders as needed, and reinforced through communications programs and executive support. Finally, “able” suggests that relevant skills, competencies, performance measures and even corporate culture aspects are being put in place to execute and sustain the change.

Ready-Willing-Able: A Success Story

In one of my later HR Tech involvements, we went beyond understanding process automation requirements and spent considerable time with line managers discussing people management (not process management) issues that kept them up at night, how real-time access to high-value data would help them, etc. This time, we put “empathy for the customer experience” first. We also worked to overcome (beginning with acknowledging!) some long-standing disappointments with HR on the part of many consumers of HR solutions, services and programs. This was Design Thinking before the term was widely used, although empathy had been around for eons.

The team also figured out creative ways to give end-users (mostly line managers in this instance) a sense of control and ownership over the system and its data. One example involved hitting a “challenge button” about any data that line managers suspected of being incorrect. That opened a dialogue box for comments and auto-generated an email to an appropriate HR administrator requesting research and resolution. Quick turnaround was ensured through an associated SLA (service level agreement) process.

The “black hole” of trying to resolve data issues with HR disappeared!

That prestigious bank’s Chairman came into my office for the first time ever to congratulate our team on the crowning achievement for the HR Department, not just that year, but any year in his memory. He heard that people outside HR were using the system, and regularly.

Combating Employee Disengagement from all the Change

Multiple generations at work with different personal drivers, automation changing the nature of work, achieving more with less, and the frequency with which businesses tweak their operating models or totally re-invent themselves are dynamics that won’t be changing anytime soon. These dynamics can lead to employee disengagement even without adding new “HR / People Systems” to have to learn and use. And disengagement can bring down even the best run companies. Investing in employees in ways that resonate certainly helps with the employee disengagement challenge; but empathetic change management is absolutely essential when the change is represented by something very tangible, like a new system.

Bottom Line: When end-users genuinely feel their work lives and perspectives are taken into full account, due to proactive change management, the prospects of broad HCM system adoption and even a stellar ROI are significantly higher.

Much as I’d like to, I can’t foresee the actual future of the U.S. Affordable Care Act (ACA) or healthcare policies under President-elect Donald Trump… anymore than anyone could predict the true outcome of the recent U.S. presidential election. What I do foresee, however, is the increased need for partnerships to focus on what the ACA is designed to accomplish (regardless of its existence) – affordable, accessible, quality health care.

Getting to the heart of the problem –the cost.

There are many people who are upset at having to pay for “other people’s” healthcare costs – which they believe is because of the ACA. And there are many people who are receiving care who didn’t before and wouldn’t otherwise, because of pre-existing conditions or age, for example. And these are often people who when they did get sick, would go straight to an emergency room – an expensive treatment which by the way somehow had its cost passed in some way at some time to, likely, people who today do “not want to pay for other people’s healthcare.” Any way you look at it, costs get spread around.

So let’s look at this issue – cost – from a different angle… how about the angle of reducing or eliminating some of these costs? Reducing the cost of ER visits or readmissions because we can identify and intervene in someone’s pattern of such use or events before they happen because of triggers? Or, increasing the possibilities of people being healthy because of proactive education around nutrition, exercise, and lifestyle?

Partnerships are critical to truly changing the nature and outcome of health care

Just as it “takes a village to raise a child,” it takes a community of partners to create a high quality, lower cost environment for healthy consumers. Those partners include people on the front lines of care everyday—the obvious, like doctors, nurses, pharmacists, social workers – and also professionals who work behind the scenes but have an impact on care and cost – such as billing coordinators, claims processors, and coders. If everyone is thinking about their work, and how changes to the way they work, can impact the healthcare consumer, we have a giant brain trust and energy force working for change.

A significant part of this “back office” for many years in healthcare operations has been the service provider. Business process outsourcing service providers (BPO/BPS) have been engaged mostly in stages – for claims processing, enrollment, billing, utilization review, collections—but few have been involved, truly integrated into the health care operations so that they have insight and impact on the healthcare consumer experience.

It’s time to change the nature of engagement in healthcare business operations, using design thinking, digital technology, and relationships

Now that we are more than 30 years into experience in BPO/BPS, and many healthcare providers and payers have such partnerships, it’s time to step back and look at how to partner more effectively and use digital technology such as robotic process automation, mobility, and analytics tools, along with human centered, creative problem solving like design thinking, to define and address problems with services and solutions that fit – that broker across organizational silos and internal and external partners.

A number of service providers are stepping in to help change the game in this way, and partner to make healthcare business operations more effective, with an eye toward impacting health, medical, and financial outcomes. We hear from service buyers that they are partnering increasingly for resources—to allow local clinicians more time and energy for interactions with healthcare consumers by rethinking what activity can be done remotely, through partners, or even automated.

What are service providers doing to help healthcare providers and payers?

In our recent Population Health and Care Management Blueprint, we take a look at the role of service providers in bringing together talent and technology to broker solutions through BPO and BPaaS engagements. The scope is:

Population Data Management and Analytics: identifying whom to target with what intervention

Consumer Engagement and Interaction: reaching out, engaging healthcare consumers

Utilization Management: processing authorizations, reviews, appeals and grievances

Care Coordination: coordinating care activity

Performance Management and Operational Analytics: program evaluation and assessment, quality and compliance reporting

Here’s a quick look at the service providers that participated actively in this research – each one brings value to a business process services engagement, depending on how you want to partner and what you want to accomplish.

We go into more detail on trends and service provider analysis in the blueprint report, which you will find described here, and you can go so far as to download here.

The bottom line is that regardless of the good, bad, and ugly of the ACA, what it did was drive forward a change towards value-based and consumer-oriented care that was and is needed, not just in the U.S. but globally.

And this kind of value-based health and care system is one that requires effective operations, and effective partnerships—and that’s what gets my vote.

Barbra Sheridan McGann is Chief Research Officer at HfS (see bio). This role encapsulates her passion for research, analysis, and strategy, which has been 20 years in the making. Barbra’s scope of work covers the business process outsourcing and emerging “as a service” market broadly, as well diving into industry and functional areas of Healthcare & Life Sciences, Public Service, and Marketing.

I remember vividly reading an article back in 2012 that a new set of software termed “robotic automation” could be a serious threat to offshoring if not outsourcing at large. Suffice it to say I sat up straight in my chair and wanted to find out more. And I am very glad that I not only read that article but started to research those topics. This research not only got me immersed in the small yet highly innovative Intelligent Automation community, but it led to HfS suggesting that we should join forces to push the envelope on how these tools might disrupt our industry. At the time, Phil titled the blog in his inimitable fashion: “Greetings from Robotistan, outsourcing’s cheapest destination.” And the key strategic questions the HfS team was asking included: If you were a buyer, how fast would you jump at the option to hire FTEs at rates that undercut the Indian body shops by 50% — without sending jobs offshore? (“Hire” isn’t the right word, of course: it’s “create”.) If you were a BPO services provider, how would you like to build a software robot to automate a business process for one client, and then resell copies of that robot to a dozen other clients in the same vertical?”

So, fast-forward 4 years, is the offshoring industry any closer to the abyss? Those questions raised by HfS can be condensed to the suggestion that RPA will lead to a surge in insourcing which in turn will cannibalize large parts of the offshoring industry. This was underpinned by the assumption that scaling those robots is a piece of cake. Suffice it to say those suggestions need to be understood in the context of time, but equally that it were tool providers like Blue Prism and UiPath pushing that narrative in order to get the concept of RPA on the radar screens of the industry’s stakeholders. So where is the industry really at and what are the likely scenarios moving forward? Two recent industry events might help to shed more light at this. First, early in December Capita announced restructuring program. Crucially, the expected job losses are meant to be buffered by both moving services offshore as well as investing into a proprietary RPA solution. Capita is an important reference point as it has been used by the likes of Blue Prism and UiPath as a case study for the suggested trend of increased insourcing through RPA. What this tells us is that we have to stop ask binary questions, namely is one concept supplanting another. This is also demonstrated by the second event. HfS did spend a couple of intriguing days in Vietnam visiting Swiss Post Solutions (SPS) delivery centers in Ho Chi Minh City and Can Tho. SPS is a compelling example for scaling out RPA as part of its Global Sourcing strategy. The company is blending proprietary IP, RPA (UiPath) and Artificial Intelligence (Celaton) to accelerate toward higher value services. Thus, SPS is aiming to expand from its core in document management outsourcing toward BPO services. This journey is incremental, building on its historical strengths around document management and invoice processing but progressing to broader capabilities in F&A BPO and Insurance Claims processing. Unlike many other RPA deployments which tend to focus on client specific activities, often on a sub-process level, SPS is focusing on industrializing the core of its delivery capabilities through RPA and AI.

Before you raise your eyebrows, the point here is not to suggest that the market will necessarily follow SPS, but that we need a much more nuanced understanding of the implications of RPA and Intelligent Automation at large. HfS has been vocal, to put it mildly, on the impact of automation. First and foremost, this impact plays out differently in different scenarios. We see the most pronounced impact on service providers internally. It is here where RPA is being deployed aggressively and as financial earnings calls show, thousands of jobs are being “freed up”. Service providers are much coyer in deploying RPA in Managed Services contracts as top line revenues will be impacted. More recently we see a surge in transformational projects building out captive automation capabilities for clients. However, the boundaries between the last two scenarios are blurted. As part of the sourcing mix both might exist within one organization. But equally, we are seeing failed in-house projects that end up as BPO contracts and vice-versa.

However, to get a better sense for potential disruption, we have to continuously enhance our understanding of what automation really means. The more I think about automation, the more discussions I have with stakeholders, I keep increasingly coming back to one issue that helps me crystallizing my thoughts on the impact: How much of automation conceptually is actually a managed service and how much conceivably could be run as unsupervised learning. Take the example of SPS, business agents are being supported by elements of RPA and AI but their activities continue to require significant manual intervention. You can apply the same logic to the various tool providers and you get a sense when you visit their offices. Do you see hordes of developers doing manual tweaks and coding or do you see largely just R&D capabilities? Unsurprisingly the latter technologies offer higher value moving forward, even though at times it might require more effort to get the deployments up and running. Now combine the emerging notion of Virtual Agents underpinned by those forward-looking technologies and we really are staring at highly disruptive scenarios. On the danger of sounding like a broken record, we urgently need an honest and transparent debate on the various implications of Intelligent Automation.

Bottom-line: Intelligent Automation projects will only be successful with constructive change management

The White House released a report on the implications of automation and AI on the economy, the UK Government undertook an inquiry into robotics and artificial intelligence, yet our industry appears largely to remain in denial about those issues. Almost all service providers we try to engage with around this topic continue to suggest there will be no disruption. People “freed up” from projects will re-trained, re-badged – and you will have guessed it – all be happy. But I keep scratching my as we work in the sourcing industry. I am the last one proposing restructuring and job losses, but we finally have to get to a more honest and transparent debate on all of this. The implications will not only be felt in global sourcing locations but much closer to home in equal measure.

When somebody offers me something that is allegedly free, I tend to get skeptical, if not outright cynical, about possible motives or hidden catches. This is especially the case in the emerging intelligent automation market, where the focus needs to be centered on making automation work effectively and driving value from digitizing legacy processes, not saving some money on software licenses.

I had the same reaction when I first heard about WorkFusion’s plan to offer core RPA capabilities for free. In a nascent market that is clouded by the reluctance of many stakeholders to share their views and more importantly playback experiences, leading to extremely blurred perceptions, the move to commoditize core RPA, before it even has become mainstream could open a Pandora’s Box. In mythology, Pandora’s Box contained all the evils of the world. So what is really in WorkFusion’s box? Is it rather an altruistic box helping clients to climb to the stairway not to heaven but to digital operations as the company did put it? Before I let my cynical inner-self rip, I listened to WorkFusion’s webinar to find out more details. So, let’s first look at what WorkFusion is actually planning to launch. Dubbed RPA Express and planned to be launched in Q1 2017, the new product is said to offer the core RPA capabilities including:

Bot Recorder

Developer Studio

UI Automation Drivers

Bot Libraries

Scheduling

Control Tower

User/Role Management

While RPA is not defined across the industry, those suggested capabilities capture the value propositions of the leading RPA tool providers such as Blue Prism, UiPath, and AutomationAnywhere. Thus, WorkFusion’s strategic move to offer these for free could have profound implications for a market that has not yet reached maturity.

The two fundamental questions we have with WorkFusion’s aggressive move:

Will it lead to commoditization before we have even reached market maturity and

How this move could impact the leading RPA tool providers – and how will the respond (if at all)

WorkFusion’s move will accelerate the move toward transformation

WorkFusion suggests the motivation for offering RPA Express for free is to accelerate customer’s journey toward cognitive automation including crowdsourcing, chatbots and a broad integration of machine learning. As WorkFusion is not a shy organization, it reminded the audience in a recent webinar that it had launched several industry firsts including:

Train Machine Learning with Crowdsourcing

Virtualize data science

Combine RPA with broader cognitive capabilities

Build-in Tableau analytics

Automate conversations through chatbots and other means

Fundamentally, free RPA tool sets will lower the barrier to entry. Organizations can trial capabilities without having to worry about licensing costs. WorkFusion was at pains to stress that RPA Express is not a community version, requires costly upgrades to delivery enterprise-wide results or containing padlocks on higher value features. Provided these claims will get corroborated, the move could accelerate the move toward understanding RPA as part of transformation projects rather than a short-term focus on cost elimination, often on task rather than process level. Suffice it to say, at the same time it WorkFusion will strike at the heart of the RPA tool providers. On the service provider side, many will be chuffed by the elimination of licensing costs, but at the same time, many have established practices for Blue Prism, AutomationAnywhere or UiPath and will not easily jeopardize these relationships at least in the short term. However, the missing piece in the jigsaw is the talent that can integrate RPA capabilities – regardless whether they are free or not – into broader service delivery strategies. Therefore, partners will charge for training around RPA Express as well as helping to advance the journey toward higher value, cognitive automation capabilities. Nothing in life is really free.

Move could impact valuations of RPA tool providers

RPA Express is all about free tools for structured data. Yet, as we have stated repeatedly the industry needs to embrace the broad Continuum of Intelligent Automation (IA), with a strong focus on integrating unstructured data and building out cognitive automation capabilities. It is here where WorkFusion’s Smart Process Automation (SPA) is providing the value add and will thus provide the revenue streams. WorkFusion’s starting point in IA was Crowdsourcing and Machine Learning. Initially, it had used the RPA moniker to get a seat at the table for the decision-making on automation projects before building out broader RPA capabilities. The core RPA discussions continue to center on Blue Prism, AutomationAnywhere, and UiPath. It is these providers that could lose most from this move. Their licensing models will come invariably under scrutiny. The key question here is, how quickly can those providers accelerate their roadmaps in building out operational analytics and cognitive capabilities to buffer against potential losses in licensing revenues? Suffice it to say, I expect Harvey Ball graphics depicting the differences between RPA Express and the leading tool sets any time after the expected launch. And I can hear already voices claiming that WorkFusion has only limited capabilities in RPA to start with and can therefore easily suggest free offerings. However, in a market where very few understand the technical details of RPA tools and their impact on broader process flows, perceptions are likely to remain as blurred as they are now.

But there is possibly another subplot here. I believe that the leading RPA tool providers will be absorbed over the next 18 months by M&A. Thus, free RPA tools could weigh on valuations while management of RPA tool providers will be forced to focus on accelerating their roadmaps as the key value proposition is being forcibly commoditized. RPA Express could easily be seen as a spammer thrown into those M&A scenarios. Having said that, Blue Prism’s share price has not yet suffered, but then again, the broader market does not yet have seemed to digest the news of WorkFusion’s move.

Bottom-line: Disruption, but at what price?

We are seeing the move as a strong positive for WorkFusion as it will accelerate its customer acquisition but equally the progress toward higher value services. For the broader industry, however, the jury is still out. While WorkFusion might succeed in squeezing competitors boosted by a strong balance sheet, the market might lose important educators on the broader notion of IA. Obituaries on the demise of RPA might be premature, but the stakes have been raised significantly. It could hasten M&A in either direction. However, it could be a case of forced commoditization that carries significant risks for the broader market. A “self-medication” with free RPA tools might throw the hard-fought progress in understanding RPA as part of transformation projects off track. Put in a nutshell, it could be a highly disruptive move. It will take more clarity from WorkFusion’s partners to understand how they are planning to balance their ecosystems and what the detailed strategies are. Therefore, be braced for disruptive counter moves.

Thank the Lord 2016 is over. It’s easy for any old big head to claim they “were not surprised with Brexit and Trump,” but they would be lying – this surprised even the most brilliant minds and political experts.

Noone saw this coming – but it’s opened the eyes of many business and political leaders that we are living in transitional times and we desperately need to focus on ensuring we transition our economies, businesses, health and educational establishments to a more stable, secure place, where we can all plan for the future, with a clearer vision of where the world is going. Many people voted for change, without much idea what that change was, besides turning back the clock and ejecting politicians they didn’t trust and didn’t talk their language. It is my belief the global economy is inexorably moving in one direction and there’s little politicians can do about it, beyond starting World War 3 (heaven forbid).

Moving into 2017, the future is foggy for so many people. However, what is clear is those who keep trying to paper over the cracks will slip further behind in this secular shift to a global digital economy. But there is one constant we can rely on: focusing where new wealth and fiscal growth is being created and aligning our investments and education around it. This is exactly what we need to do in our world of business operations and technology; it’s time to rip off that legacy BandAid and embrace the future.

I believe the fog will start to lift as the new world emerges and people see where the opportunities lie. Small-thinking politicians will try to hold back innovation with anti-immigration measures and restrictive trade policies, but the building blocks for the global digital economy are already in place.

The inexorable journey to the global digital economy has started and this train won’t be stopping

We’re in a transition economy clouded by confused politics and too many people looking backward, not forward. Many legacy businesses are already being replaced by emerging digital businesses. This is inevitable, and legacy politicians will only speed up this process. It’s happening in our own industry, with traditional offshoring being gradually morphed into (global) digital operating delivery models that include intelligent automation and cognitive capabilities.

“Offshore” will cease to exist as a word – it’ll just be about companies staffing themselves with whatever talent they need to deliver their services and satisfy their customers. Whether China has the best availability of Hadoop programmers or India analytics skills for a particular business function, or the UK the best RPA expertise, it really doesn’t matter anymore – there won’t be this obvious “replacement” of onshore staff with offshore / whatever-shore, it will simply be organizations tapping into whatever services they need in an on-demand model.

So, while dinosaur protectionism rears its head in 2017, the likes of which Messrs Trump and Schumer are threatening, it will only speed up the death of legacy outsourcing. All they are really doing is helping accelerate the global economy to its natural destination – larger numbers of agile, lean, intelligent digital businesses, operated by talent which is in tune with the needs of its customers. There will no longer be a front and back office… only OneOffice that truly matters in the modern business that has survived this transition from the old world to the new world. Yes, you can penalize firms which import overseas staff to support themselves, and even stifle the obvious “lift and shift” of closing down onshore facilities to move the work to cheaper overseas ones, but you can’t stop smart digital business tapping into globally dispersed resources as they grow. Hence, you can only punish the legacy businesses for ripping out cost, but not the emerging business for building their global digital support infrastructure.

We’re currently experiencing what I am calling a “BandAid Economy”. While we’ll see our legacy traditional service providers, consultants, and IT suppliers struggle for growth, we all need to start looking deeper at the emerging businesses – and focus on the creation of new wealth around the digital economy. The Fortune 500 in 2020 will be dominated by businesses that are very different from today’s characters – they will be all about the ability to scale up and down to meet business demands, without massive incremental infrastructure investments, about having immediate access to people to service their customers, and native digital business models that cater for their needs, as and when they arise. Moreover, they will drive new spend from customers, because of their ability to predict intelligently their behaviors and their needs.

I bet all of us here are spending a lot more of our income as a result of digital business channels, than we would have done in the past (the likes of Amazon, AirBnb, InstaCart, Ocardo, NetFlix, SocietyOne, UAccount, targeted Facebook ads etc) this is the emerging present and future – smart digital businesses running on intelligent technology… all enabled by people. These businesses are generating increasing wealth without making the linear capital investments of yesteryear – but they do need talent to scale, just less office space, legacy IT system perseverance and expensive shop fronts. In fact, they won’t really need RPA as automation is native to their systems and processes. But one thing is clear, money is flowing into talent and tech like never before…

The Hi-tech sector is leading the way into the new economy

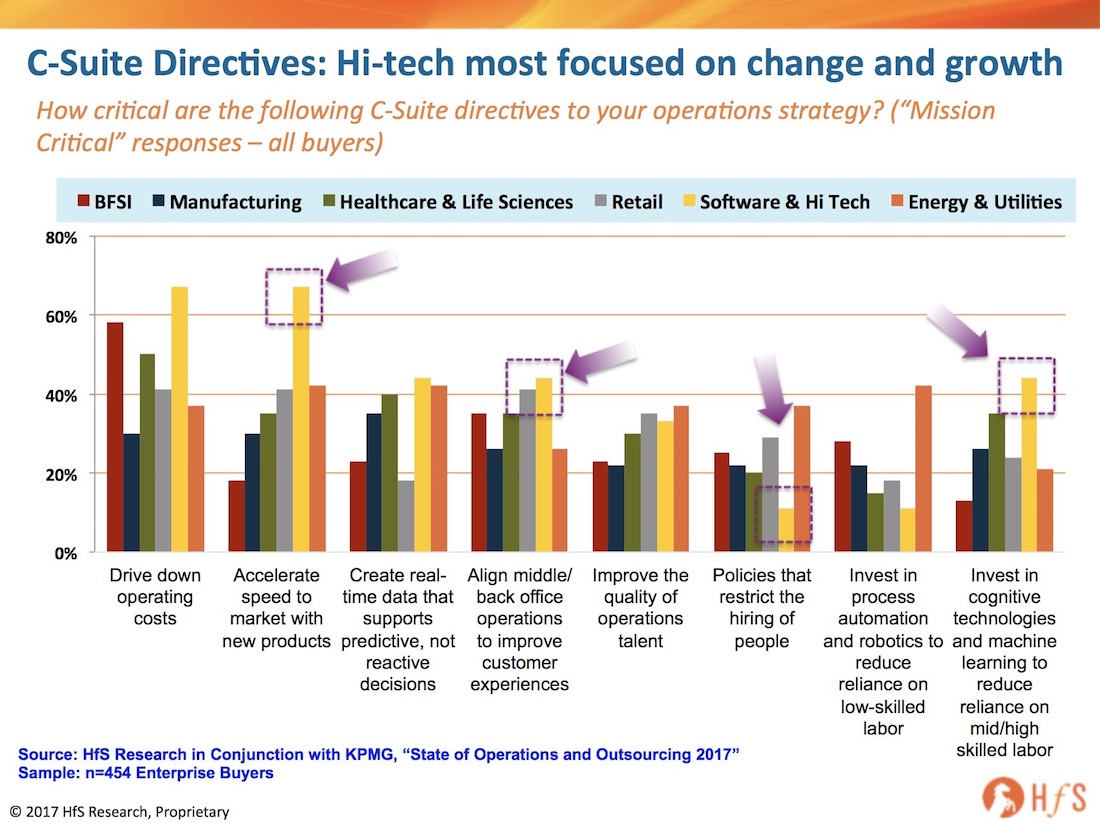

Cutting to the chase, I believe our salvation will be in the digital economy, where the hi-tech firms make up one huge growth sector that still cares about talent, ideas and new business models. Our new State of Operations and Outsourcing study with KPMG clearly dictates which industry sectors are gearing up for growth versus those merely playing a survival game. In the software and hi-tech sector, the C-suites are as keen as anyone to cut costs, but they also are the least focused on restricting talent investments (only 11% view restricting people investments as mission critical), close to half (44%) are very concerned about aligning the back office with the customer (OneOffice), while two-thirds are hell-bent on getting new products to market as quickly as possible (compared with only 18% of financial services firms):

The Bottom-line: Money is flowing into talent and technology like never before, not into the legacy juggernauts stuck in the old world

We’re moving to a very different tech-dominated economy – so many emerging startups and consulting firms are emerging and many have not even yet been formed. While some of today’s current crop of service providers are trying to build the parallel model by making ongoing tuck-in acquisitions of digital consultancies, their bread is still very much buttered by their legacy clients, many of whom are really struggling to keep up with the current pace of change.

Digital business models are what drives growth from the vast majority of today’s customers who want to buy from digital businesses. This is where so much creative talent is heading / developing – people who are figuring out how to develop business models designed for digital environments, where purchases are made over apps, customers are targeted using intelligent cognitive tools and serviced by people who can understand their needs on a much more individualized basis. The new world is getting smarter, while the old one just continues to get dumber.

I, for one, won’t be too sad to see the back of 2016… it just felt like the world kept becoming an increasingly ignorant place to exist. The Internet became the medium to block out information, not share facts and data points to foster intelligent discussion. It (almost) became acceptable to be racist; it (almost) became acceptable to talk about women as sex-objects, as long as it was playful “locker room talk”.

2016 became a time people complained about immigrants taking away their jobs – even though they’d never work those jobs in a million years. It became a time when we all finally realized so many of our politicians had lost touch with so many of the population that they got booted out… sadly only in favor of alternatives that didn’t make any sense, but it must have felt good for the disenfranchised to stick the middle finger up at the establishment.

It became a time when many of us decided we could no longer tolerate people as our Facebook friends, because they just refused to listen to rational arguments and get beyond their prejudices. Let’s be honest, it was a pretty ignorant year.

Hello to a year of, er, maybe a little common sense

So if we could have some good things happen next year….

Trump becomes a pragmatist. Like so many of you here, I am secretly wishing most the guff old Donald was spouting was just, well, guff. As Bernie Sanders told a private meeting of scientists recently, Trump is a very intelligent man. Plus, I believe the guy is not an idealist, he’s a businessman and a pragmatist. It’s my personal hope that he realizes globalization of business is an inevitable occurrence, but I do like his stance on China, and the fact we’ve allowed them set their own economic rules for long enough. This is one economic power where we need to fight back, review our trade deals and our tolerance of their unfair currency fixing and economic policies. If Donald wants to get into a fight, then I hope he goes after these guys and drops a lot of the anti-Mexican rubbish and electoral bravado. At the end of the day, DT will be judged on economic growth and job creation… all the other stuff is noise.

People stop being so lazy and start educating themselves again. How did we get to a point where so many people just spout off about the latest buzz terms, with no ability to define them or apply them to real business situations. How many “Digital” presentations have you sat through, where the presenter literally had replaced “IT” with “Digital” and reeled off some unintelligible random nonsense that just left you more confused than when he/she has started? Did we all just become stupid overnight? Please can we just get back to educating ourselves again, as opposed to making each other even more ignorant than we already are?

Automation becomes a business strategy… not the next “outsourcing”. Fortunately, anyone with half a brain who’s kicked the tires with RPA software has realized this is a lot harder than the masses realize. While there is considerable benefit to the fact that most RPA implementations are fast and do not involve any changes to the underlying applications, the ROI of there RPA implementations can be very attractive. But the core issue is the transition to an RPA environment is a multi-year process for most enterprises that requires a strategic focus on process value in the early phases, not cost take-out. Basing decisions primarily on the license fees of RPA software is just about the dumbest thing some companies were doing in 2016…

Service providers stop thinking that bribing analysts wins them business. My god, I went to one service provider’s website recently and all it had on its home page was “Marketscape this” and “Wave that” and “Magic Quadrant whatever”. Does anyone possessing half a brain care? Does the fact that some faceless analyst, who probably has never observed a real business process, or a real line of code, got suckered by a dose of clever marketing and a couple of client references (and was probably busy on Facebook during the telebriefings in any case)? Do clients really sit in board meetings, torturing themselves over whether to select Provider A or Provider B, and then decide to base their razor-thin selection decision on each one’s average performance across all these scatterplot charts? C’mon folks… who are we kidding?

The Bottom-line: Can we at least try and be a little less stupid next year?

I don’t think I can take another year like the one we just had. I miss intelligent debate and conversation, I miss being able to disagree with someone, but share our viewpoints, even if we ultimately agree to disagree. I miss people who would actually read articles, not simply tweet them or “like” them. I miss people who didn’t view Facebook as some place to be politically correct and pretend to “like” things they really don’t care about. I miss Twitter as something that was fun and social, not a place for robots to spam the masses… I miss a world where it was definitely not cool to complain about immigrants and generalize nations and religions… I miss a world where people would actually say, “Can you explain to me what you actually mean”, instead of nodding blindly with a blank grin on their face?

Well, that just about finishes my holiday rant… did I miss insulting anyone, or have I pretty much covered it here?

One of my biggest gripes with some analysts is that they clearly develop preconceptions about service providers and struggle to deliver a balanced view in their research – they have their favourites and struggle to recognize when others are improving their capabilities. And what’s bothersome here, is that they don’t realize they are doing it.

So I’ve decided to do something different to make sure I don’t fall into that preconception trap and force myself to give everyone a blank sheet of paper before we embark on our groundbreaking 2017 Blueprint, which will be bolstered by 300 references from Global2000 clients… I’m just going to get all my preconceived opinions out there now, so providers know where they need to prove me wrong, or validate where I am right.

You may have already seen that HfS Research is expanding our focus on the IT services market in 2017 (see press release). An initiative lead by Phil Fersht, myself and Tom Reuner. I will be leading the infrastructure and cloud part of the story. As part of the preparation for the infrastructure management services blueprint, I wanted to write down my own personal bias – those traits that immediately jump into my cynical old brain, when I think of the various infra services providers. So I am clear where I stand and what I need to get past to do a good independent assessment.

So for those that are interested this is where I currently stand. My message to those that want to question any negative opinion is confound me. You know where I stand.

Provider

My Starting Point

IBM

The daddy of infrastructure services. Technically very solid, services still seem unevolved – even with the acquisitions of the likes of Softlayer and Gravitant seem not to have a coherent/consistent message around infrastructure services. The whole cloud story within IBM is disjointed – bluemix, cloud brokerage, hybrid – as a firm it has all the pieces but seems to have trouble bringing it all together – or at least explaining to me how it fits together. Great consulting and transformation capabilities particularly suited for the very largest of enterprises.

HPE

Ignoring the limbo state HP (or whatever it ends up being called) are going through thanks to the spin-off and merger with CSC. HPE had a good hybrid cloud story, I particularly liked the ambition for its cloud ecosystem. Like IBM it has a history of being very capable, particularly with the very largest of deals. Probably one of the few providers to be able to manage the very largest multi-billon dollar infrastructure deals with mass transformation. In some ways HP had the business messaging and cloud story that IBM lack, but a lack of cohesion and financial problems hindered progress.

CSC

CSC embodies what is wrong with traditional outsourcing, which is slightly unfair as the last pure outsourcer left standing. I can’t help myself I associate CSC with change orders, lift and shift, and first generation outsourcing. I think largely unevolved, in spite of some progress toward As-a-Service with the acquisition of ServiceMesh – but tired and now in limbo thanks to HPE deal.

Accenture

Apart from the uninspiring name, I like the Accenture Cloud Platform, I like the agreements with AWS, Microsoft and Google. Accenture is playing to its strengths in infrastructure by looking to be the consultant and advisor leveraging best in class infrastructure provision to deliver customers a managed service experience. It has great long term experience with Microsoft through Avanade. But I’m left feeling that infrastructure is a means to an end with Accenture rather than a passion. Although for a provider like Accenture that is probably right.

Fujitsu

Traditionally a strong infrastructure player, perhaps stronger on the desktop, solid investment in cloud, but not much penetration/mindshare outside of Asia. I suspect Fujitsu have something interesting to say, but I’m not sure if it is able to communicate coherently to customers.

Capgemini

I get the impression that infrastructure is not what Capgemini wants to sell. But infrastructure was a large part of its heritage and it ran some very big traditional outsourcing deals in the past – particularly in the UK. Not sure it has managed to find the right balance in hybrid world, some interesting stories around cloud, but I believe their destiny is elsewhere.

T-Systems

T-Systems has a great deal of technical no-how in development of high end hybrid cloud environments, however, it struggles to get the message to market outside of Germany. In some ways I think technically it is the best at genuine hybrid cloud infrastructure, particularly in situations where real performance or complexity is required, even if it is not the best it is at least in the top 2-3 in terms of the quality of the service delivered.

Atos

Atos have some great partnerships in this space around high end infrastructure management. They have a good roadmap for hybrid and software defined datacenters thanks to VMWare and investments in automation. Atos are in a position to take some big deals based on the quality of the infrastructure they are able to deliver. The issue is a lack of momentum, and ability to articulate a game changing proposition to the market.

TCS

I lazily lump TCS and HCL into the same group in terms of infrastructure. Great at taking on horrible legacy infrastructure and managing it more efficiently. TCS seem increasingly conservative in approach so I’m not sure how cutting-edge the infrastructure will be, but there is no doubting the technical strength and it has plenty of resources to throw at any issues. I always this TCS, with Cognizant, are the hungriest of the offshore players.

Microsoft

Second biggest, second best IaaS (certainly in terms of feature/function). Much more enterprise focused and enterprise ready than AWS, big in-house services team, ability to transform and add value in large partner led propositions. It lost much of it’s arrogance in the late nineties.

AWS

OK AWS is the biggest and probably the best public cloud, certainly in terms of scale, and feature/function. Very customer centric, always innovating and adding to the platform. Small internal service team, so reliant on partners. Great customer stories and case studies. Although it seems to be run for nerds by nerds. Seems to have inherited the arrogance of a late nineties Microsoft, but if you grew a >$10Bn revenue company in 10 years, you might be arrogant too.

Cognizant

A bit like Wipro (below), I was never 100% sure that Cognizant’s heart was in infrastructure. A growing part of the business, but not as much success as HCL and TCS at grabbing its share of the first generation outsourcing business from the old school incumbents. Yet to really communicate a strong message around future of infrastructure – which may reveal the firms loftier ambitions. Not an organization I would ever count out given its traditional hunger, but its infrastructure message got lost in translation. At least with me.

Infosys

Impressed by Infosys cloud ecosystem hub, particularly in terms of ambition around infrastructure and roadmap, perhaps the best of the offshore providers. At least from what I have heard and absorbed. Although I question the success of this initiative to date.

Wipro

I tend to think of Wipro as an also ran for Infrastructure services amongst the big offshore providers. Like Cognizant, haven’t been as successful at winning business as HCL and TCS in this space – hasn’t been as big a push to innovate as Infosys.

HCL

Similar to what I said for TCS. Strong at lift and shift. Strong at modernizing. Very capable at untying the Gordian Knot of old deals. Although I suspect they are all tactical strength and little strategic direction in infrastructure.

Unisys

OK – this is where it gets hard. Unisys were traditionally a strong IT Outsourcing shop. But, much like CSC there is a whiff of decay about it as a business. Traditionally strong on the desktop – but who cares?

CGI

I am not as familiar with CGI, at least its global proposition as some of the other providers here. Very much an old school service provider. Strong business until the acquisition of Logica just seems to have had its energy sapped by this painful merger and lost its way.

So prove me wrong, or assure me I’m right… drop me a line when you get a chance at Jamie dot Snowdon at hfsresearch.com

In 2017, HfS is focusing heavily on IT services as a research topic and, thanks to my stint as a cloud and data center services analyst and hands-on experience in infrastructure services over the past 20 years, – I am looking after the cloud and infrastructure part of the market.

Given my recent blog on the infrastructure as a service market. HfS believes that making the right choice of infrastructure services partner is becoming increasingly critical for end-user clients, particularly given the amount of disruptive change the market is going through.

In preparation for this renewed focus, I’ve been looking more in-depth at the market for the main cloud and infrastructure service providers. This has inevitably led me to look through briefing information HfS has collected on the suppliers, talk to end user clients, look at many of the suppliers’ websites, and at the various quadrants that are in circulation around this space. One of the most recent ones, which is on Amazon Web Services (AWS) website is Gartner’s Infrastructure as a Service quadrant – which has placed AWS as a leader for six years.

By the way, this is not a critique of this quadrant or an attack on AWS – far from it – the positioning is dictated by the information provided and the customer references, and, given its laser focus on IaaS, I can buy the positioning. It’s hard to argue with AWS’ huge strength in this space, and that it’s a leader… by some margin. It acknowledges, by Microsoft’s position, that it’s closing the gap. As a slight side, note I do like the euphemistic “niche” player category particularly its use in this quadrant. What niche are these players filling? Do they provide services to organizations that want a crappy cloud? Is that a niche? Not that I want to start a semantic discussion, but I’m not sure IBM is a “niche” infrastructure services player even in IaaS, regardless of your view of the market. Particularly if you buy the IaaS as part of a larger infrastructure engagement, with any perceived shortcoming of the IaaS layer provided by another part of the service delivery.

This is what is missing, for me, the relevance of this research to an enterprise buyer. I see how the quadrant, as it stands, would be useful to a developer looking for the “best” IaaS to use, but for an enterprise looking to plan its cloud infrastructure strategy, I’m not so sure. Although IaaS can -and is – bought on its own, it is rarely bought without a context, at least in an enterprise organization. This means the services that wrap around the delivery of the IaaS are probably as important, if not more important than the actual IaaS – particularly in a hybrid environment. Of course, there are some 100% pure public cloud situations, but these are still fairly rare – most enterprise organizations, even in 2017, have a degree of complexity and require a mix of computing types.

My argument is that, in a complex environment, comparing one element is not enough and the excellence of that one component may be lost, as the whole infrastructure is built from interconnecting pieces, and some of the additional services that make the compute component great, are provided by another layer. The fact that there are a lot of additional services on top of the compute layer from AWS, for example, may not be useful to an enterprise looking for commodity compute delivered through a service provider that adds the additional functionality.

The Bottom Line – Who is this Quadrant benefitting?

So is the quadrant suitable only for companies that are looking to buy an IaaS engagement and don’t need to integrate it into any other environment? This would be the one way to make sense of the positioning. There are some uses that are 100% public cloud, and I can see situations where consideration of the overall enterprise architecture is not relevant, but this is quite a limited picture. Again for enterprise organizations.

So is this quadrant for a services firm suitable for an IaaS firm to choose a partner? It does help if the service provider is looking to pick the richest IaaS environment and leverage the brand of the IaaS provider. Which would work if infrastructure were more like a software eco-system, but in many cases, the service provider will want to add value on top of the IaaS. So this doesn’t help select a good basic IaaS service offering.

So what are we going to do about it? Next year we are going to look at the whole infrastructure management space with our own quadrant – an HfS Blueprint. One that takes advantage of our buy side contacts and uses over 200 interviews as the basis for our positioning and a guide to what is critical in the marketplace. The IT Infrastructure Management & Cloud Services Blueprint will take a more holistic view of the market and provide guidance on selecting the best provider for an enterprise organization. Focusing on end to end management of a client’s infrastructure services rather than just one aspect.

Derk Erbé is Research Vice President, Supply Chain, Procurement and Energy at HfS Research (full bio here). Derk is responsible for a compelling, leading-edge research agenda covering the core topics of interest for buyer and vendor communities in the areas of digital business transformation services and business operations, with a specific emphasis on key vertical markets, namely Energy, Utilities and Resource Industries.

Derk Erbé is Research Vice President, Supply Chain, Procurement and Energy at HfS Research (full bio here). Derk is responsible for a compelling, leading-edge research agenda covering the core topics of interest for buyer and vendor communities in the areas of digital business transformation services and business operations, with a specific emphasis on key vertical markets, namely Energy, Utilities and Resource Industries.

I remember vividly reading an

I remember vividly reading an

In preparation for this renewed focus, I’ve been looking more in-depth at the market for the main cloud and infrastructure service providers. This has inevitably led me to look through briefing information HfS has collected on the suppliers, talk to end user clients, look at many of the suppliers’ websites, and at the various quadrants that are in circulation around this space. One of the most recent ones, which is on Amazon Web Services (AWS) website is Gartner’s Infrastructure as a Service quadrant – which has placed AWS as a leader for six years.

In preparation for this renewed focus, I’ve been looking more in-depth at the market for the main cloud and infrastructure service providers. This has inevitably led me to look through briefing information HfS has collected on the suppliers, talk to end user clients, look at many of the suppliers’ websites, and at the various quadrants that are in circulation around this space. One of the most recent ones, which is on Amazon Web Services (AWS) website is Gartner’s Infrastructure as a Service quadrant – which has placed AWS as a leader for six years.