As we dived deep into procurement for the Procurement As-a-Service 2016 Blueprint, we had a lot of almost philosophical conversations about the future of procurement. About the fun stuff, not the procurement grunt work like invoice processing, PO matching, accounts payable. No, about cognitive procurement, predictive analytics, procurement being completely automated and invisible.

Amara’s Law concluded about the future and our estimations thereof: We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run. Bill Gates famously paraphrased: “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.”

So, here are our overestimations and underestimations for procurement in two and ten years’ time:

Overestimations … within two years: * Service providers successfully scale the knowledge of their scarce category experts with brilliant cognitive solutions. * P2P platforms completely automate away manual transactional procurement. * Suppliers are completely digitized on what we used to call Supplier Networks or Business Networks and now know as collaboration platforms. * Service providers have adopted on-demand As-a-Service to the extreme – they don’t talk about multi-year contracts or total contract value anymore – just about number of subscribers, active users, churn, annual and monthly recurring revenue (ARR / MRR) growth. * Amazon takes over the B2B Marketplace (if in Asia – Alibaba). Amazon Business is the de facto marketplace in B2B. * If you’re looking for the Procurement department, follow the signs: Brokers of Capability. * Competition from outside outsourcing or procurement disrupts outsourcing of specific categories – like DHL in logistics. * With Blockchain cemented into the core processes, we also pay in Bitcoin.

Underestimations, or what we’ll see (!) in 10 years: * Algorithms will decide the preferred supplier du jour. * Algorithms will determine what, how, where and when to buy, show you options and recommendations. * No one touches an invoice or a purchase order. Blockchain and smart contracts take care of transactions. * Some categories disappear (probably office supplies – as we go paperless, you can bring your own pen or pencil (BYOP). * Connected assets (IoT) in value chains will tell algorithms what to buy and when. * No need for approvals, the algorithm got it. * Predictive analytics decide what you need – the system knows our needs better than we do. * When I want to buy something algorithms, and analytics didn’t figure out already, I just tell Alexa to get it for me. * Stuff will unexpectedly appear on your desk or doorstep. * Fedex and UPS will help return stuff you, after all, didn’t need….by a drone or an Uber.

Bottom Line: The future is already here – it’s just not evenly distributed yet To end with the famous quote from William Gibson. All the forces impacting procurement and driving our overestimations and underestimations are here today. Some very nascent and aspirational – cognitive procurement, IoT, Blockchain, true predictive analytics. Others have been embraced by the market and broadly implemented into procurement and Procurement As-a-Service offerings – procurement platforms, supplier networks, intelligent automation. Ask yourself; will you be on the overestimated or the underestimated side of this transformation? Figure out what the future looks like for your procurement function and start preparing now or risk becoming obsolete.

How do you change a workforce and shift performance management from status reporting and check-ins to an outcome-based approach?

With Pokemon Go! hot news in the press and, frankly, in my house, this summer, I was reminded of an example of gamification used effectively for performance improvement, financial impact, and employee development and engagement at a US healthcare system.

The director of revenue management and patient financial services brought in gamification, along with training and outcome-based performance management, as part of a change and quality management program. Along with an increase in AR staff productivity and engagement, the impact on the business included an increase in payments, a decrease in net days in accounts receivable, and a decrease in denial turnaround time.

Mission: Quality Control

This healthcare provider has a centralized business office that manages the revenue cycle for a group of medical facilities. Within this office, the director launched a mission to certify every one of the over 80 staff coders, having learned that the ability to resolve a claim on the phone with payer is 40% more efficient than if the staffer is not certified. While he hired a coding instructor, he also realized that to really have an impact, the team of coders needed to take ownership and be engaged, to want to learn—so why not inject some competition and a little fun? To make the program less of an “attack,” and more of an incentive, the director worked with HR and marketing to build a program around it—with logo, t-shirts…and a game, one that has helped to drive higher quality and revenue impact among all ages of staff.

This is a great example of up-skilling to generate higher quality results…and also add an element of “competitive and spirited but team oriented fun” into the work environment.

“You can’t learn if there is no proper feedback on a consistent basis,” shared the director. “Accountability through transparency into progress and issues as well as communications is key.” So he found a tool that would generate progress reports on a recurring basis, without being overwhelming: UpdateZen. is a mobile-based program management app that allows team members to share relevant and timely updates in 240 characters or less. This way, the management team can stay on top of a project based on the targeted milestones and deliverables, and not on “what did I do today” updates.

In addition, they set up a scoreboard so that every Monday, employees see which of their assignments are on track, what’s outstanding or delayed, etc. There are online rewards and visible “stars” for exceeding expectations, a leaderboard to show rankings, and call outs for “Top Producer,” for example. The scoreboard also reflects measures for productivity and quality, with flags for where there are suggestions for corrective actions or training.

In the scoreboard, the performance measurements are grouped by outcome. That’s because another element of the program for this operations team is to tie performance to revenue-generating outcomes. As such, there is a revenue indicator associated with each group of assignments. Employees and the management team can see how the work they are doing impacts business results. Of course, there was work “behind the scenes” to tie the work to the business outcomes, and that’s where an analytics professional played a key role.

Powered by performance analytics

The team that defined and implemented the outcome-based performance management with gamification engagement scorecards included an analytics expert from the patient financial services department, and HR and marketing professionals. The effort included identifying performance metrics mapped to business outcomes, defining workflow, performance management and HR coaching. During this time, the staff was also kept up to speed and involved in the effort so that by the time the program went live, there were no big surprises. Along the way, there were people who realized that the new way of working was not for them, and some moved to new roles or left—and those who did shared that they at least appreciated the feedback and interaction the approach created.

Quality and employee engagement results…with more to come

The program has resulted so far in a reduction in denial turnaround time, with higher quality work. The team continues to add to the usability of the system—increasing the use of automation for work that does not need to be done by people on the team, and continuing to add and change the metrics to ensure a continued focus on quality improvement. While the shift to outcomes-based performance management is still a work in progress, this effort does show how bringing together a team—revenue management, patient services, HR, and marketing – can work together to define and roll-out cultural and process changes to move towards an outcome-based and outcome-driven environment.

Pokemon Go! served a role in getting people of all ages engaged in a fun and spirited competition, but also drove change. It unintentionally became the means by which some people learned new skills (using GPS to get home after biking into “new territory” to catch Pokemon), interact in new ways (in the real and virtual worlds), and inspire new marketing and sales opportunities. It also breaks down something big—change in culture, process, and technology—into something smaller and engaging. Infusing a gamification approach into the business can motivate, inspire, and also align people around a shared or similar goals.

There’s been an awful lot of focus on the emerging Robotic Process Automation (RPA) solutions since we unveiled the concept to the services industry in 2012. While early movers, like Blue Prism, have stolen most of the early headlines in the space, we’ve seen other very effective tools and platforms emerge, such as Kryon Systems, UIPath, WorkFusion and Nice.

However, one solution has been especially rampant in the BPO space (especially in finance and accounting) – Automation Anywhere – whose team has been working tirelessly with leading providers such as Genpact, Accenture and EXL to streamline processes and drive all the associated benefits of automating high volume, high throughput tasks that were previously plagued by unnecessary and costly manual interventions.

So we felt it time to sit down with Automation Anywhere’s brainchild and co-founder Mihir Shukla, to learn a little more about what is driving this unprecedented demand for RPA, and where this is all leading as we venture into curious times…

Phil Fersht, Chief Analyst and CEO, HfS Research: Good afternoon, Mihir Shukla. You’ve been at the forefront of so much of the new thinking and ideas in RPA and Intelligent Automation in the last couple of years. Automation Anywhere almost came out of nowhere. So I’d love to hear a bit more about your background and how you really ended up leading this firm. What was the journey?

Mihir Shukla, CEO, Automation Anywhere: Good to talk with you again, Phil. It’s interesting when you look back, how you end up with something. I came to the US to do my PhD around the time when the Internet was just coming around. So I got the disruption bug, and it was a lot more fun disrupting different industries than doing a PhD. 22 years later, I look back and I’m fortunate enough to have led five or six large disruptions in various capacities. First, I started at Netscape, where I had a chance to shape the era of the Internet. Then I worked at Infoseek, which was one of the early search engines, where I got to help define how to access the Internet, how you discover things, and we built an early eCommerce platform. Then I had a chance to be an advisor to OmniSky, creating the first Internet-enabled smartphones. I still remember the time when I was one of the 14 guys in Silicon Valley who could go anywhere in the world and find the nearest restaurant. Today, there are a billion of us who can do that.

There was lots of learning along the way. The genesis of Automation Anywhere came from one of my last disruptions, which was at E2Open, where I had the opportunity to integrate the supply chain of the top 10 high-tech companies. At that time I had a chance to use various BPM tools, enterprise application integration tools, and ETL tools. It was during that experience that I saw the challenges faced in trying to integrate a global supply chain that includes hundreds of applications and thousands of people.

I thinking at that time was there must be a better way to do this.

So in 2003, we started Automation Anywhere—and that was a genesis of RPA. Of course, it wasn’t called RPA back then. But the idea was to simulate human behavior on a computer and be able to automate everything we do on a computer screen. And 13 years later, we’re the largest provider of RPA solutions. So that’s how it all started, and that’s where we are today.

Phil: So what can you share with us about Automation Anywhere secret sauce? What is it that makes you guys tick? What is it that you feel has been the catalyst to this hyper-growth that you’ve been experiencing?

Mihir: There are quite a few things that we do very differently, that are unique to us. First of all, we’re the largest and most fluent platform on RPA today. We have over 500 enterprise customers, the highest number of bots, many large deployments on our platform, and the highest ROI. What that means for a customer is, as I said, the most fluent platform. So the product is a lot more mature, our practices are a lot more refined and we’re a lot more humble as a result of all of that.

Anyone looking at RPA today will see a company that arguably owns 60% or more of the market share—which is us. So that’s the first one.

The second secret sauce ingredient is that, in addition to being the largest RPA vendor, we’re also the only one who has a digital workforce platform. It is a combination of RPA, cognitive and analytics together. What does the combination of these three things mean? One is that if a typical RPA vendor can automate 10% of the processes, our platform can automate 60% or more of the processes, with the combination of the three capabilities together. So what you can automate is significantly broader.

The second part is in terms of returns. You have reported that RPA gives returns anywhere from 30% to 70% and there are some examples of a few hundred percent returns as well. With digital workforce, you could get two to four times more return than just the RPA platform. For one of the large telecom customer, there is an 18,000% return. Yes—18,000%. Almost unbelievable, right? Digital workforce can deliver significantly higher results. So that’s the second big differentiator.

The 3rd differentiator is that often in the industry for RPA implementation you either get scale or you get speed. But how do you get scale and speed? To our knowledge, ours is the only platform that can get 50 people worth of productivity in six weeks, and 500 to a 1,000 people worth of productivity in one year. I have not heard of a single installation outside of ours that can deliver this level of digital transformation.

We also have the largest partner channels—17 of the top 20 companies are our partners. And there are more than 10,000 people trained on our platform in the industry today.

Let me mention one last differentiator. Maybe you’re familiar with it. BotFarm is one of our latest innovations. It’s a bot platform that can deliver anything from 50 bots to 5,000 bots—with a click of a button. Where you need it, when you need it, for however long you need it. That level of scale and speed is just one example of how we deliver. So those are a few things.

Phil: Mihir, you talk a lot about the digital workforce and digitally shared services. What does this really look like, Mihir?

Mihir: A few years back we were looking at what was next. How do we take this beyond what we deliver today? That, for us, is the digital workforce—it’s the next generation of RPA.

Think about it, Phil, what do all of us do at work? About four things.

We think about things, then we do it, then we analyze it, and we drink coffee. Now, think how do I augment these capabilities with technology, of course except the coffee? So cognitive thinks with you. RPA allows you to do things better, faster, at digital speed.

Our real-time analytics allow you to analyze. So now technology has given us a way to augment thinking, doing and analyzing. When you combine them, you get a digital worker with all the three capabilities that we require at work. Each one by themselves is a huge wave, as we know. Combine them, and you get a tsunami. It is the true digital workforce that will lead the next wave in the industry.

Phil: That’s good to hear. You’ve moved so fast as a business. So as you look out where you go next, where does Automation Anywhere develop its capabilities beyond automation? What does the long-term product roadmap look like as you peer into the future, Mihir?

Mihir: Okay. So I think we have come really far, but there is a long way to go. There are two areas where we focus significantly. One is, as I already mentioned, scale and speed.

So, today we can do 50 people worth of productivity in six weeks and 500 to 1,000 in a year. We’re now looking at how to do 200 people worth of productivity in six weeks. How do we get to 5,000 people worth of productivity in a year? How do we push this digital transformation speed even higher?

In the next year, you will see series of innovations from us in various areas, all pushing the boundaries. We’re heavily into R&D investments, Phil. We have about 150 people in our R&D team alone. So one thing for sure is you can expect some amazing things in the next year.

One area we focus on is integrating cognitive RPA and real-time analytics—looking to make it more and more seamless, and more and more powerful. So, take an example of our cognitive solutions today. After many years of effort, we have reached a point where you could get up to 80% return in two months. One of the challenges in the cognitive world has been how to train your system that fast.

It typically takes a long time. I’m very proud of our R&D team here. To achieve that level of sophistication, where you could train a system in just two months, where 80% of the straight-through processing is possible. It is an achievement, I humbly believe.

We’re going to push those boundaries even further and combine these three capabilities to take it to new levels.

Phil: Good to hear. So finally, then, I’m going to give you the keys to the kingdom of automation for one whole week. If you can do one thing to change this industry for the better, what would that one thing be?

Mihir: I like the question already. What would I like to do? Am I dreaming here, or do I have to look at all the constraints?

Phil: One thing you can do with full empowerment.

Mihir: I think I’m going to take the license to One A and One B. There is so much domain expertise and knowledge with service providers. But digital transformation is coming through and they need to re-invent. So I would take service providers private, automate 40% to 70% of everything they do, go back to the public market with three times the valuation and three times the profit.

Easy to say, but there would be a lot of challenges.

The second one is in the shared services space. If I am doing 10 functions, 10 areas where I am doing shared services, I would take three of those functions and make digital workforce the first strategy—and this is not me dreaming, we should start doing it in my opinion.

What it means is that I don’t need a reason to automate. I need a reason to do it manually. It should be digital workforce first.

It should be all digital unless it is required not to be. I would start pushing that way in my shared services and take it from there. In five years every business will be a digital business, operating like Google, Facebook, and Uber. That’s how the world will be in five to seven years. You start there, by taking three departments and say goodbye to manual.

Phil: I think that’s a really good answer!

Mihir: Are you going to grant my wishes?

Phil: I definitely like the one about taking the service providers private. That would get them out of this quarterly mindset and they might actually do something to prepare for the future and not just the present. Being able to help their clients get ahead of digital disruption is very smart, because the biggest threat to the industry right now isn’t automation, it’s digital disruption.

When you look at the Fortune 500 in three to five years time, it will be made up of all these digitally run businesses. Like for example, an insurance company can come along with an Uberized-type delivery model to compete with an Allstate or State Farm, which has 10,000 people onshore processing insurance claims on green screen technology. They’re out of business overnight! You can look at digital banks, for example, targeting millennials with pure app-driven bank account capabilities.

The disruption can put these guys out of business so fast. And they need to pivot a strategy. They need to understand what is happening, so they can react to it – staying ahead of the curve and not reacting to it.

We’re even seeing some clients investing in startups so they can almost move into a startup type model, to get out of the model they are in. So I think helping clients understand, combat and pivot against disruption are really the keys here. Thinking with a digital-first mindset, which you’ve laid out very intelligently, is exactly the way to go.

Mihir: You know, I recently had a chance to travel around the US, Europe, India, and other some Asian countries. I met about 50 of the Fortune 100 leaders, one-on-one. I asked them when digital-first will really take hold. I was talking to people from all industries—banking, financial service, insurance, manufacturing, retail, oil and gas, healthcare and others. Each one of the leaders had a model on when they must fully go digital.

Very surprisingly, almost everybody had the number at around seven years. It was shocking to me, that almost regardless of industry everybody says that in seven years, if they didn’t have full digital scale, they would face an existential threat.

But I would say the countdown is five years. Because no employer or investor is going to wait for rock bottom. What do you think?

Phil: I think it could even be sooner than that…

Mihir: Is five years a good countdown or would you say other industries have more time, before they have to push all-digital button?

Phil: It depends on how we define digital. But I think in some industries we’re seeing the all-digital button being pressed now. So, in retail and travel, I think it’s being pressed now and it’s probably more like two to three years for them. In something like maybe banking, probably more like five to seven. Insurance, maybe three to five. Media, it’s already here. So, I think it depends on the industry. But seven years is probably the slowest. Some of them are already getting in now.

Mihir: Good answer, Phil!

Phil: Mihir, this has been a great, enlightening discussion. Thanks for joining me. I know our readers will enjoy this.

Mihir Shukla (pictured above) is CEO and Co-Founder of leading robotic automation solution provider, Automation Anywhere. You can view his biohere.

It’s quite the humbling experience when your fellow professionals recognize your achievements. The HfS Research team should be very proud of being awarded both Independent Analyst Firm of Year and Analyst of the Year for 2016 by the Institute of Industry Analyst Relations (IIAR), which covered 170 analysts and all the global and boutique analyst firms.

Nothing better to do next Thursday? Fancy spending an hour with the award-winning HfS analyst team, hearing about our research plans for 2017 – and why we are focusing so intensely on the reality of technology-inspired business operations versus the hype? Have nothing better to do than sip on a festive mimosa and hear our happy band of analysts get all excited about their research? Pray tell… what more could you want…

Digital disruption is no longer new – some industries have already been shaken up by evolving digital business models, while others are in the throes of being impacted. This is the new normal for enterprises, and we need to develop actionable strategies to survive and compete in this post-digital world. In 2017, it’s all about enterprises being digitally capable of engaging their customers in real time using immersive communication channels, supported by intelligent unified operations that can enable their business to pivot to remain competitive.

The HfS 2017 research theme is all about “making it real”. We will explore the experiences, dynamics, intentions, challenges and opportunities of thousands of enterprises in their quest to align their operations to meet the rapidly changing needs of their clients.

In this webinar, the HfS analyst team will share our 2017 vision for the industry and our plans for the 2017 HfS research agenda.

Hear about our plans for 2017 research across the following areas:

The Intelligent OneOffice: Taking an “outside-in” approach to Intelligent Operations, breaking down the barriers between the front and back offices.

The Post-Digital world for IT Services and Strategy, Business Operations and BPO and Cognitive Automation

Industry-specific dynamics for banking, insurance, energy, utilities, manufacturing, healthcare, life sciences, travel and retail industries

The market dynamics in the world of Intelligent Automation are hotting up. Two acquisitions within a single week and the market is awash with fresh rumors about more M&A. We already know about two other ones imminent – one a done deal and the other closing in.

First, ISG acquired Alsbridge, not just for their rapidly expanding RPA advisory and implementation capabilities, but RPA is likely to have been a key consideration as ISG was lagging both in terms of traction, as well as skill sets. Second, CA announced its intention to acquire Automic. This is a strong indication that the juggernauts appear to be not only willing to overcome innovator’s dilemma, but are expecting that offerings around Intelligent Automation will ringfence their leadership position rather than erode their bottom line. Moreover, the risk of not investing in Intelligent Automation is clearly outweighing doing nothing and hoping this feverish wave of interest dies down (which is not doing).

Sourcing advisors are currently not bringing automation deals to the supply side the way they used to with the people-scale centric legacy deals. As part of our research for the Intelligent Automation Blueprint, we tested this assumption with all the participants. Yet, at the same time, we are seeing the Big 4 play an increasingly important role in implementing transformational RPA deals. Thus, they have significantly moved on from largely doing top level advisory and tool selection. This is shifting the market from a narrow focus on task automation with short-term cost considerations. However, this shift and acceleration are being curtailed by an acute scarcity. In the broader market talent that understands the impact of innovations around the notions of Intelligent Automation on broader process efficiency remains a rare breed. Therefore, we expect more M&A predominantly by the Big 4 with pure plays like Symphony Ventures, VirtualOperations, GenFour and thoughtonomy likely to be high on their shopping list.

CA’s offer for Automic is strategically even more illuminating. First, the price of 600 million Euros is underlining that Intelligent Automation is becoming serious business. Given the slightly misguided focus on RPA by many stakeholders, Automic might not be a household name. But orchestration engines like Automic and Cortex become increasingly central tools for service delivery where organizations are starting to standardize on ServiceNow and integrating the plethora of Intelligent Automation tools with those orchestration engines. Second, we are nearing an inflection point where the innovations around the notion of Intelligent Automation are deemed critical for improving both top as well as bottom-line. Thus, we wouldn’t be surprised if the likes of BMC are casting a serious eye on the likes of Arago and Cortex. We have been gazing into the Automation Crystal Ball not too long ago and outlined 4 scenarios. Therefore, in this context, we will close by looking at how these acquisitions apply to those scenarios and how we are seeing the next 18 months panning out.

Bottom Line: Intelligent Automation is at an inflection point

The HfS Intelligent Automation Blueprint provided a broad set of reference points as to how the market is maturing and how the deployments are starting to scale. The discussed acquisitions are adding even more poignant points to a rapidly maturing market. Thus, we put out the following stalking horses for crucial dynamics over the next 18 months:

In 18 months, we won’t talk about RPA anymore. Most of the leading technology providers will have been acquired and RPA is a reality in the back-office.

The 4 leading pure plays (Symphony, VirtualOperations, GenFour, thoughtonomy) will have been absorbed by the leading managing consultancies.

ServiceNow is entering the Intelligent Automation fray either organically or through acquisitions. The likely focus could be on operational analytics and process execution.

The focus around automation tools will shift toward the likes of Google, Amazon, and Facebook around deep learning and the integration of unstructured data. As part of an eco-system approach, the leading service provider will increasingly integrate their OpenSource algorithms and libraries. Data literally will become the currency.

An organization will go into administration due to a badly implemented or governed automation project.

These are stalking horses. We love to hear your views, so if you are interested in discussing these issues, drop me a line at [email protected].

The Work At Home Agent (WAHA) model of contact center outsourcing is increasing in adoption. My colleague Melissa O’Brien is set to release some interesting findings of the growth of the WAHA model in the coming weeks. The growth that WAHA is set to enjoy, however, has been hard fought as there are key inhibitors (often perceived as opposed to actual) to the model. These include lack of control, service consistency, and most notably security.

For regulated industries, the idea of having a completely virtual workforce dealing with customer payment and other sensitive data fills them with dread. But what is the real story? Well, according to numerous service providers I’ve spoken to there is a lower average instance of security incidents from the WAHA environment as opposed to the traditional brick and mortar equivalent. We recently spoke to home based agent pure play BPO Granada’s new CEO Felix Serano and CTO AJ Flores. When asked about on the issue of security it turns out that Granada has not had a single security breach from its WAHA population over the last 12 months. Given the frequency of cyber threats we see in the news at present, this is encouraging.

So, what are service providers doing to address the security needs of clients in the WAHA environment?

Hiring the right people: Ultimately security needs to start with the right people. Due to the nature of the working model, at home programs are typically able to recruit a more seasoned and experienced type of candidate (the majority of WAHA hires are 35 years and up in age), enabling the potential for more sophisticated and more importantly trustworthy contact center support. Also, service providers generally tailor hiring approaches to target individuals with a university qualification.

Train: Next is to train agents on security protocols. Clean desk policies, not repeating information out loud when speaking to a customer– all these measures need to be reinforced to the agent, even in the work at home environment. Training is just as important in a brick and mortar facility, but from a cultural perspective is critical to ensure the concepts are digested with the absence of physical “team huddles” and the like.

Physical security measures: There are two overarching categories to look at from a WAHA physical security perspective. One is the Bring Your Own Device (BYOD) model and the other is using a service provider supplied thin client device. For the sake of this discussion we will look at the BYOD model as this has been gaining traction in recent years and is, by and large, the most cost effective WAHA model. In 2013 I did a report on the WAHA market, at that time we were seeing some extreme physical security measures rolled out by service providers. These included keyboards with integrated keyboard entry analysis, multi-layer biometric analysis, etc. These measures were all extremely costly and often not that effective due to limitations in the technology. Now what we are more commonly seeing is simple fish-eye cameras, installed at an agent’s home workstation, through which service providers can perform randomized audits. Another interesting side note is that brick and mortar service providers are seeing cyber thieves targeting call center agents outside of physical centers and extorting them to steal credit card information; in this sense, the physical security risk is heightened in a home agent model.

Software: This is where we have seen the biggest advances in security measures and hence why many of the more extreme physical security measures are no longer needed. A desktop layer, such as Citrix ZenDesktop, is used to replicate in-center desktops. This is then locked down to prevent cut and paste, print screen, etc. Payments and sensitive information are handled by an IVR system to exclude the agent. VOIP is often embedded into the desktop to provide continuity when transferring to IVR systems. Interestingly, Granada tracks the internet latency of agents and can automatically remove them from the workflow if internet speed drops below predefined parameters.

As I’ve mentioned, many of the security measures used in WAHA today seem much less extreme compared to what we saw a few years ago, however they are considerably more effective. With WAHA expected to grow rapidly over the next five years, it seems service providers have finally cracked the code for security and can now provide extended track records of fraudulent free delivery from this model. Service providers offering the WAHA delivery model seem to get it now that the key to security is as much about intelligent and foolproof software as it is finding and developing the right people.

Remember eMarketplaces (also called Supplier Networks)? They were networks of suppliers and buyers where the goal was to make information sharing easier by standardizing and consolidating platforms, products, prices and policies. In many cases, clients got in “free,” but they still had to pay for some integration cost. Suppliers had to pay to be part of each network, and most clients each used different ones, making it expensive and complicated to decide which networks to join.

As a buyer, you could try to insist suppliers join your preferred network, as long as you were a big enough client, or if you were willing to pay the supplier’s connection costs. As a supplier, you had to decide which networks were important to belong to, either because a lot of clients used them, they catered to specific industries, or offered some other unique benefit.

These supplier networks were a great idea, but the practicalities of connecting everyone was a big headache, and very few of these eMarketplaces survived. Many of those that did survive were bolted on to procurement apps. Without a way to make the networks talk to each other and give trading partners, on different networks, a way to work together, eMarketplaces achieved some limited value for customers, but ultimately failed to deliver the game-changing impact they envisioned with these “super networks” that never quite materialized.

In the example above, go back and replace the word “eMarketplace” with “blockchain.” Minus some of details, it’s pretty much the same problem we’re all about to face today, as companies struggle to understand where, why, and how they can get the most value from blockchain implementations.

When we researched blockchain this past summer, we found that almost all POCs and client examples were focused on internal operations – transferring funds across business units in a bank, for example. Yet, the foundation of blockchain is creating exponential value from a collaborative and engaged peer-to-peer network.

Everyone’s experimenting, and there are a lot of technologies and validation/authentication options being used and explored. There are also no standards at the moment, so everything’s getting siloed into one-off projects. Are you starting to see where the eMarketplace experience gets echoed?

Let’s say you’ve chosen the blockchain technology, as well as an authentication approach with which you are happy, that work for your needs. Now you want to expand your execution of blockchain to connect with partners.

Your partners likely made different choices They may have stricter authentication approaches than you use. And each trading partner’s blockchain implementation is different than everyone else’s, so you need to connect to each one using a separate connector, or you choose to get onto their blockchain. And then you have the initial cost of integration, plus compute costs. And blockchain often isn’t efficient with compute power, so connecting to multiple systems is more expensive that way than you might initially think.

And, of course, the market’s so new that we also don’t know how much cement we’re pouring when we build blockchains. We do know, for example, that no transaction or other data in the blockchain can get erased. Once it’s there, it’s there forever. But, what if we decide to switch to another network or technology? We don’t know the costs of switching from one network to another if we have a lot of data sitting in the blockchain.

In our blockchain guide for BFSI, we recommended that you start talking to trading partners, because the real value comes from using blockchains outside the walls of your company. And this issue of linking networks makes that recommendation all the more important.

Bottom-line: Make sure you fully understand the broader network of partners impacted by your blockchain options

Here are some questions to start asking trading partners (and yourself, if you haven’t already):

What validation/authentication approaches are you considering?

Which blockchain technologies do you like and why?

What criteria do you want to use to approve new members to join a network?

Who pays, if someone wants to join the network? What if we want them to join? Will we pay only for integration costs or other longer-term costs like the compute power needed to process blocks?

If you have thoughts on this, or know of companies who are already working on the interoperability problem, tell us. We’re always looking to talk to more people about what’s going on in the space.

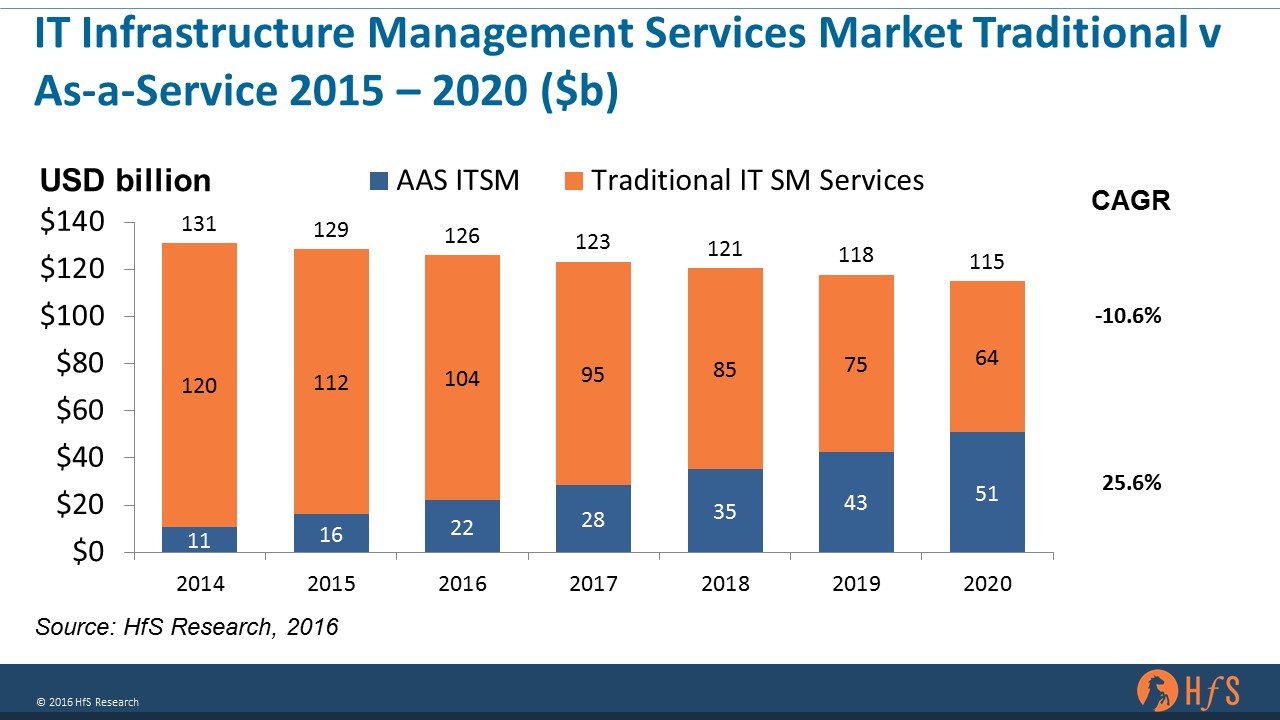

It’s no secret that the traditional infrastructure outsourcing market has taken a beating over the last few years, with our predictions of growth for the overall IT infrastructure management market hovering around 2% the last couple of years. We are forecasting a calculated annual growth rate of 2.2% from 2015 to 2020 for this market globally.

The chart below shows our estimation of the size and forecast for the IT infrastructure management market – a market set to reach $129 billion in 2016. The chart illustrates this showing the split between the traditional IT infrastructure management market and the new “As-a-Service” model for IT infrastructure.

In our view, As-a-Service IT Services includes infrastructure managed services delivered in either a pay-per-use or a managed cloud platform. When we include the whole IT services market, it includes professional services revenues related to transformation to cloud/SaaS, digital engagements and the move to IT-as-Service delivery models.

The disruption we expect in the market over the next few years is dramatic, with almost half (44%) of spending from infrastructure management anticipated to come from As-a-Service models by 2020. We believe that this forecast is a touch conservative and there is a possibility that the As-a-Service component could even grow more aggressively. This won’t necessarily reduce the traditional infra spend, as the biggest uncertainty in our market model surrounds companies that don’t currently use any traditional IT service management, particularly small and medium enterprises and companies in Asia. If growth in that sector shifts more toward the top end of our scenario, we could see the As-a-Service component even reach as high as $70billion in this timeframe.

One of the big impacts to the competitive landscape will be Amazon Web Services (AWS). The company recorded revenues of $7.9b in 2015, with estimates of $12b in revenues in 2016, meaning if it tracks with the market at the current rate it will reach around $25+b in revenue by 2020. Please note not all of AWS would be counted in this category and given their propensity for disruption it’s unlikely its revenue profile will be the same in 2020. To put this in perspective, these estimates mean it would be competing with Accenture for the number 2 position in the IT services market by 2020.

Bottom Line: The infra market has already made the shift, now we need a plan to take advantage of the benefits of AaS

It’s worth pointing out that the reduction in spending isn’t all about a transition to the As-a-Service model – but the increasing efficiency of traditional IT infrastructure management. Causing deal values to plummet over the past five years as the offshore firms aggressively target this space and buyers opt for asset light solutions with more automation and remote managed “traditional” options.

Increasingly, it will become hard to differentiate between the two models, particularly as they meet in the middle, with large enterprise customers wanting cloud and As-a-Service packaged in a managed service-like wrapper, with professional services bundled into the mix.

For buyers this broadly means more choice, increasing flexibility and scope while making informed choices about risk. Public cloud will be an increasingly viable option for more types of workload – which means more organizations will need to consider it as an option for both new and existing compute. The rise of richer public cloud options and managed hybrid cloud platforms to help manage more complex infrastructures should help this transition process. Cloud was seen as a limiting choice for infrastructure in terms of workloads – now there are very few cases where security and compliance requirements cannot be met.

For the traditional IT infrastructure providers it is increasingly about partnering and making your hybrid offerings as rich as possible. On the SaaS side, it is about partnerships with the likes of Salesforce, Infor, Pega, and Workday – as well as Microsoft, Oracle and SAP. On the infrastructure and hybrid cloud side it is about having a managed service layer that helps shield clients from the complexities of cloud. One that allows them to bridge legacy applications and legacy infrastructure pools, bringing cloud flex to existing environments – and helping clients build devops platform for future development work that encompasses great architecture and great creativity. This means partnering with AWS, Google as well as Microsoft – helping increase clients choice without reducing scope and risk.

Can these two newly-weds weather the storm of a stagnant outsourcing industry?

Yes – that happened. We just had the biggest shakeup in the outsourcing advisory market since KPMG’s acquisition of EquaTerra in 2011.

The last two large independent outsourcing advisors (outside of the management consulting firms) realized they needed to stop killing each other and would be far better off becoming one. So now we’re left with an even bigger ISG and a few really small shops, like Avasant, Aecus and Everest, to scrap around for the remnants of demand for former EDS executives to negotiate a nice contract for them.

This is a really smart deal for both ISG and Alsbridge. ISG takes out its prime competitor to monopolize its space, while Alsbridge’s prime investor, LLR, makes out nicely on its 2013 investment within the typical 5-year window private equity firms give themselves.

This is a great deal for most the Alsbridge consultants. Many are welcomed back into the loving arms of their former employer and they have a bigger brand, global scale and presence to hone their craft.

This is a great deal for most the ISG partners. Now many of them will not have to suffer their fees eroded by a very aggressive competitor (or losing deals to it). They can still easily undercut the Management Consultants’ fees, and have access to more talent to win deals, especially in areas like telecom and Robotic Process Automation (RPA), where ISG was previously struggling.

This is not a great deal for all the employees. Large mergers of like companies always present rationalization opportunities. The new ISG will surely look to retain the cream of the Alsbridge talent and hive off its lower performers. The outsourcing market is flat and advisory firms are struggling to make the numbers of past years, with the $500m ITO mega deals becoming confined to history.

This is not a great deal for the management consultants. ISG’s principle competitors, KPMG, Deloitte, EY and PwC, now have a bigger badder ISG to contend with, that can no longer only undercut them on fees, but also can boast competencies in the emerging area of RPA, where the Big 4 are currently winning out. While the market is one player lighter, it is also one player stronger.

This will have mixed results for clients of advisory services. For those ITO buyers who loved to trade off ISG and Alsbridge to get their fees lowered, they will have to resort to really small firms like Avasant and Aecus as alternatives, who are good at some things, but will often struggle to scale up to meet client needs. For loyal clients of both ISG and Alsbridge, most will have a larger pool of talent to help them.

This might be good for the emerging RPA boutiques. While Alsbridge has been developing quite impressive capabilities in RPA, we’ve also seen a rapid emergence of RPA boutique advisors, such as Symphony, GenFour, Virtual Operations. They could be able to take advantage of the merger to scale up further and may be able to pick off some talent that comes available. On the flip side, I wouldn’t be surprised if ISG starts to look at swallowing up a couple of these shops as the RPA demand continues apace.

My personal view: This won’t be “Veritage 2.0”

I know both companies well, their leadership teams, and have many good friends in both. I was expecting one of the management consulting firms to buy up Alsbridge (especially EY, where the original Alsbridge founder, Ben Trowbridge, is a partner). So it’s always a surprise when two very fierce competitors bury the hatchet and see the business sense in becoming one. We’ve been so used to seeing both firms trying to take each other out on deals, it’s going to take a little while to get used to seeing them whispering sweet nothings to each other.

But cutting to the chase, these firms have some seriously experienced fellows who know this business inside and out. They know what they are doing and I would be highly surprised if we see a repeat of the now infamous “Veritage”, when EquaTerra and TPI failed to tie the knot after some very expensive offsites (and had chosen the lovely name “Veritage”).

Alsbridge CEO Chip Wagner (pictured left) thinking about his impending windfall…

Digital disruption is no longer new – some industries have already been shaken up by evolving digital business models, while others are in the throes of being impacted. This is the new normal for enterprises, and we need to develop actionable strategies to survive and compete in this post-digital world. In 2017, it’s all about enterprises being digitally capable of engaging their customers in real time using immersive communication channels, supported by intelligent unified operations that can enable their business to pivot to remain competitive.

Digital disruption is no longer new – some industries have already been shaken up by evolving digital business models, while others are in the throes of being impacted. This is the new normal for enterprises, and we need to develop actionable strategies to survive and compete in this post-digital world. In 2017, it’s all about enterprises being digitally capable of engaging their customers in real time using immersive communication channels, supported by intelligent unified operations that can enable their business to pivot to remain competitive.