Remember all those juicy reasons why companies jumped into outsourcing? Like driving out cost, standardizing processes, perhaps even finding a few nuggets of innovation along the way with better access to talent and technology? Well our new 2017 State of Operations and Outsourcing Study of 454 major enterprise buyers gives a pretty gloomy picture of the current value impact of today’s outsourcing engagements:

What made us happy in the past no longer passes muster

If there was ever one home-banker benefit from outsourcing, it was always the ability to take 30%+ off the bottom line cost of running a process or set of processes.

The VPs and below are those who are managing the engagements – and not even a third of them view their engagements as being very effective at driving out significant cost or making their operations more flexible and scalable. Their bosses are slightly less cynical, but still the vast majority is underwhelmed.

“But how can they be unhappy, we saved them so much money?” I hear frustrated providers cry…

Well, the answer is quite simply that those costs have been removed from the balance sheet – they no longer exist. Managing operations in a global environment is now the new normal – money that was saved was a onetime experience in the past. It’s like trading in your Hummer for a Prius… you don’t think to yourself, everytime you fill up with gas, “Wow, I’m saving $50 per tank”, but you might even think, “Hmmm… maybe I’ll get a fully electric car next and save even more on my running costs”.

We can go on to bemoan the disappointing lack of effectiveness from analytics, automation and cognitive from over four-fifths of outsourcing engagements, but we know clients are unlikely to have invested actual funds in these areas as part of most of these engagements today – they are getting what they have paid for in the past.

All is not lost as many operations leaders want their service providers to change with them

However, the next wave of engagements have to be set up in a very different way to bring back delights to these jaded customers, which is where the brighter news appears:

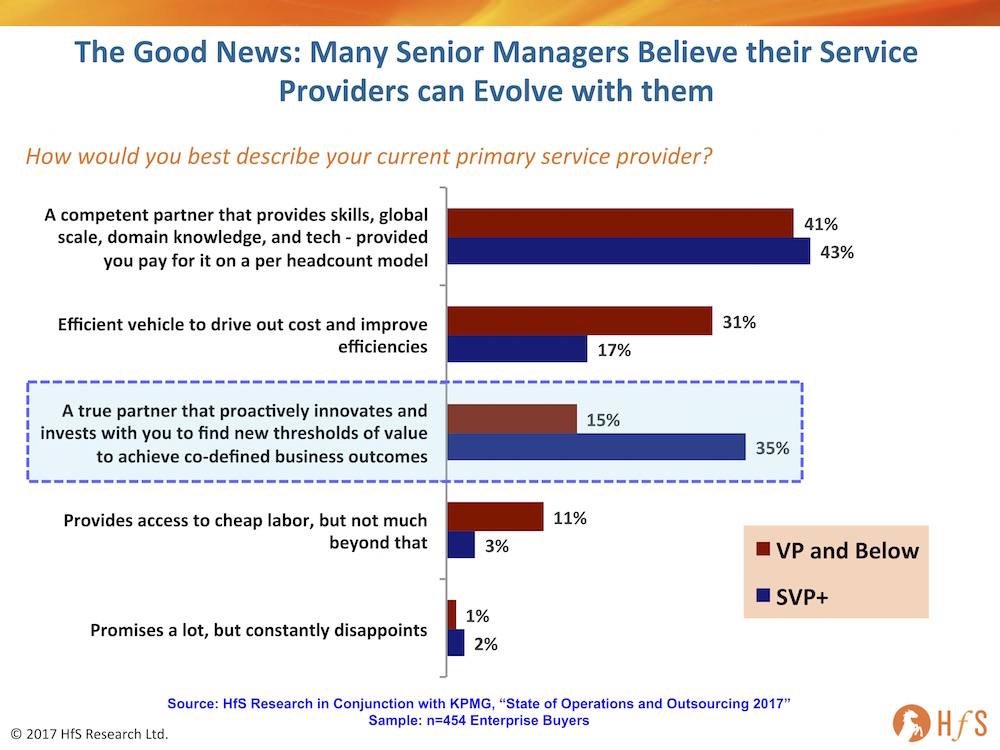

What’s encouraging here is that buyers, by and large, do not view their service providers as mere efficient cost take-out vehicles, which was how well over half viewed them a couple of years ago. While 43% of SVPs and above see service providers as competent partners who can deliver the goods, another 35% actually view them as real innovation partners who can work with them to achieve co-defined business outcomes. This is a breakthrough for the services industry.

The Bottom-line: The door is wide open for ambitious providers willing to invest in developing their talent, but closing firmly shut for those perpetuating what worked in the past

There has never been a time in the history of services where we’ve arrived at such a pivotal turning point – what used to work for clients is now commodity, and those service providers wanting to avoid this drain-circling spiral into transactional insignificance must make serious investments in their internal capabilities to partner with their clients. This means more people who can work in close proximity to their clients with real capabilities rolling out automation roadmaps, designing digital business models, working with clients to develop predictive data models and smart cognitive strategies. Sadly, there isn’t much of an available pool of eager college graduates ready to leap into these roles at low wage rates, so providers need to reinvent themselves radically as true learning establishments and universities for their emerging talent… ambitious people will want to invest their careers with firms who are prepared to invest in their talent. The future isn’t about buying packaged consulting, it’s about partnering with services firms whose stakeholders want to co-invest in themselves and their clients with a long-term vision and definitive plan. The model has changed forever… and we can only watch, learn and work with it as it unravels piece by piece.

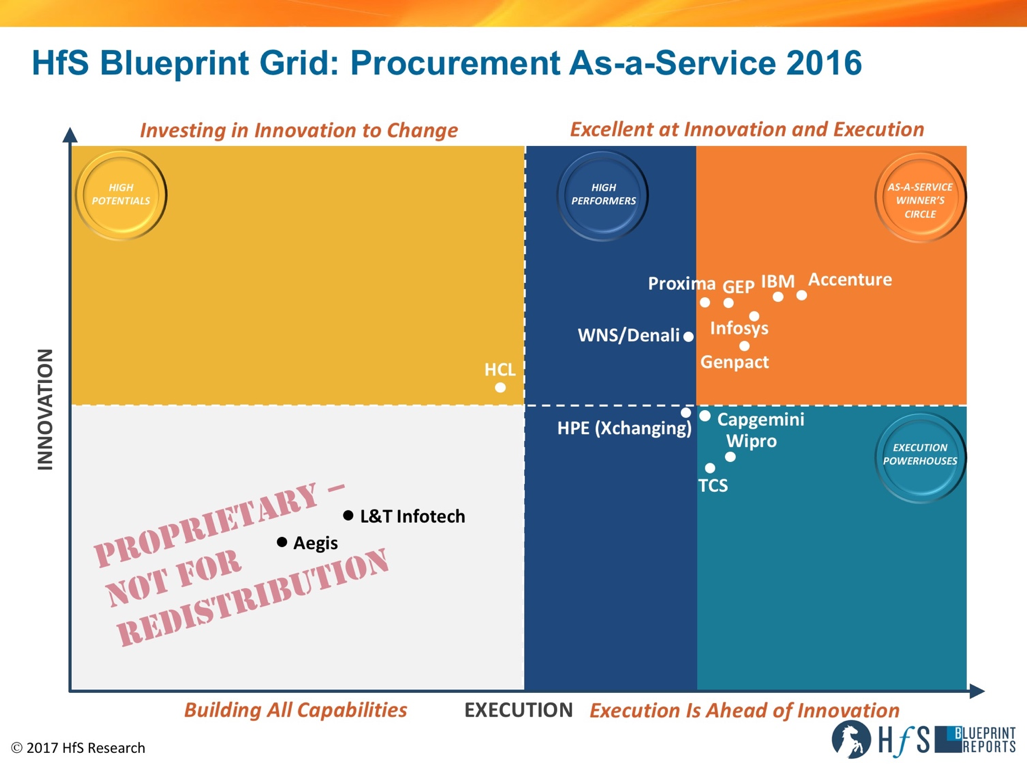

Looking further into the future, who will dominate the space in 2020? Three providers are set to remain at the helm for the foreseeable future: Accenture, IBM, and GEP.

IBM has a massive supply chain, which it smartly leverages in its procurement offerings. IBM is bullish on cognitive procurement. IBM BPS is morphing into Cognitive Business Solutions. Its own procurement provides a great playground for applying and road testing all the new cognitive procurement solutions, giving it an advantage over providers who don’t manage procurement for their own organization or have less ‘cognitive savvy’ clients.

Towards 2020 IBM will be leading in the cognitive procurement services space. Underpinned by a strong BPaaS platform, most clients will look at IBM first when it comes to new cognitive technology-driven services with vastly improved data analytics capabilities. The biggest challenge for IBM to succeed with cognitive procurement is to bring clients along this journey. The vast majority of procurement organizations perceive itself as far removed from advanced innovative procurement capabilities – they are fixing the basics, getting procurement technology to work and pondering the opportunities RPA could bring the procurement function. The gap between cognitive procurement and the (perceived) level of maturity and change readiness of procurement is the hurdle IBM needs to take to make its cognitive ambitions reality or be at risk of running too far ahead of the game.

Accenture has a significant head start to all other providers, having invested and developed capabilities through acquisitions like Procurian and putting technology into every procurement engagement, leveraging one-to-many advantages for years. Now Accenture is betting on modularity to give them sustained advantage with current clients. And opening markets with medium-sized enterprises, for whom the business case of outsourcing procurement never added up.

Accenture seems to have a more ‘wait and see’ stance when it comes to cognitive procurement, investing in capabilities and use cases, but not willing to bet the farm just yet. Be confident they’ll pounce when the time is right and gobble up any procurement related cognitive and artificial intelligence capabilities they might lack. We expect via acquisition, maybe not of the magnitude of Procurian, but an inorganic technology growth strategy makes sense.

GEP plays in an increasingly contentious market, with its procurement BPO brethren gobbling up smaller niche firms, investing heavily in technology and partnerships. As the largest pure play procurement service provider and a pioneer in procurement technology, the onus is on GEP to continue its leading position and ‘best in class’ technology. We expect technology and services to converge more and GEP may emerge as an acquirer of cognitive capabilities as cognitive and AI in procurement are on the rise.

Which are the providers emerging to challenge the leaders?

The early 2017 activity is driven by Indian heritage providers WNS and Wipro. They show their ambitions and make steps to move up the strategic value chain and incorporate more procurement technology into their service delivery and offerings.

WNS, with the Denali brand as a strategic procurement services arm, will have moved into the As-a-Service Winner’s Circle by 2020. The strong vision and upstream procurement capabilities from Denali put together with the execution prowess of WNS leads to cross-selling opportunities and investments in tech-enabled new services. The downstream procurement side of the business will have moved to procurement platforms of WNS’ partners, with WNS managing the platforms.

Wipro announced an investment and strategic partnership with Tradeshift, which is emerging as a top 3 digital procurement platform and arguably the only real “platform” in the space. This will turn out to be a smart move for Wipro, addressing a technology gap in its procurement offerings and developing on top of the proven platform that is Tradeshift, leveraging an existing and expanding network and adding Wipro Holmes capabilities. On top of this, the partnership with Tradeshift has the potential to help Wipro move up the strategic value chain, with more upstream services and shifting technology-based services to new commercial models faster.

Genpact continues to move up the strategic value chain, and between now and 2020 will have sought to bolster the technology layer in its Procurement As-a-Service offerings, something it lacks compared to other As-a-Service Winner’s Circle providers in 2016. Genpact’s conundrum is choosing between organic growth to add technology prowess to its BPO capabilities and acquisitions to get there faster. With a poor track record with acquisitions – Headstrong comes to mind – we will follow their ability to make the RAGE Frameworks acquisition work and how the newly obtained Artificial Intelligence capabilities are transferred to procurement solutions.

Infosys builds out the procurement practice on AI, analytics and platform technology. ProcureEdge and Mana will continue to converge and bring innovation in downstream and upstream procurement. The lack of enthusiasm for BPO from Infosys’ top brass is a big concern. To make a concerted move in the Procurement As-a-Service space, Infosys needs a bigger commitment to BPO in general and more focus on bringing all the pieces (Mana, ProcureEdge, category management and strategic sourcing talent and capabilities) together.

Proxima leapfrogged incumbent legacy procurement BPO providers with high value, on-demand As-a-Service services, leveraging technology and expertise. Building out technology led point solutions (beyond current offering in Commercial Management) and marketing pure subscription-based services, a fairly new area for Proxima, will be a major effort to cement a leadership position in Procurement As-a-Service.

All signs point to buyers looking for more modular services – fitting well with Proxima’s focused approach and offerings. However, if the market would shift back to demanding end-to-end procurement services, Proxima would have to quickly acquire more end-to-end capabilities.

Fading into Obscurity?

In an earlier version, I wrote: “Capgemini will have lost most of its appetite for the BPO side of procurement, while IBX remains a technology asset in the increasing tech-focused procurement services market”. Reality caught up, and Capgemini sold IBX to Tradeshift last week – essentially selling its biggest asset in procurement. Combined with the seeming lack of focus for BPO in Capgemini’s C-suite post iGate acquisition, we can conclude it exited the Procurement As-a-Service market in early 2017, well before 2020. IBX needed significant attention and investment from its parent to compete in the procurement platform market, and Capgemini decided it wouldn’t stomach this.

HPE is now the home of Xchanging, once a force to reckon with in procurement outsourcing. Xchanging dropped from the As-a-Service Winner’s Circle in the 2016 Procurement As-a-Service Blueprint and are in danger of sliding down further in this space. Neither ‘interim-owner’ CSC nor HPE are big on procurement outsourcing, a market HP neglected in the last decade, although it had the biggest supply chain in the world to service and leverage.

The Bottom Line – From Cost Obsession to Value Creation

Looking into the glass bowl, we expect the procurement As-a-Service market to continue to build value for providers and service buyers as the value of digital solutions, analytics, procurement tech platforms and cognitive automation takes hold. Albeit with a smaller number of providers, which have a full stack approach ranging from upstream strategic capabilities to platform-based execution of transactional procurement – delivering business outcomes on a subscription model.

In 2020 the market will be bifurcated into the ‘Haves’ and ‘Have-nots’, the ‘Haves’ being those providers with technology, platform based delivery and upstream procurement capabilities, offering flexibility, agility, modularity and superior digital customer experience.

With affordable, modular services making procurement services accessible to midmarket enterprises, a new hunting ground for service providers is gradually emerging. Moreover, emerging digital clients, which may be less than $50m in revenues, but have high volume transaction needs, will need to access procurement services. It’s not going to be all about size and scale, but also profitability and transaction volume.

Providers will be venturing, more and more, into direct spend delivery models, supporting clients to drive value and efficiency with cognitive, AI capabilities. As enterprises like to keep control of sourcing of direct materials and services, this will be a collaborative, partnership approach as opposed to full-blown outsourcing.

While we wait for the new Obamacare “replacement” bill to sink or swim, we can’t help but ponder the implications of whatever outcome on the healthcare industry and the services ecosystem that supports it (especially since we get asked!). Amid all this uncertainty, one thing that is sure not to change is the consumerism that has taken a strong hold within the healthcare industry, which would be the case with or without the ACA. As consumers, we are wondering, if I can order merchandise from many different suppliers on amazon and pay in one place, why can’t I see all my clinical data and lab images and send them from one doctor or clinic to another? If I can send the record of my dog’s shots to a boarding kennel electronically, why not send my children’s immunization record to schools and summer camps just as easily? Yes, we know about interoperability and security issues. However, we have come to expect the same access and convenience in our healthcare experiences as we do in all the other aspects of our lives.

Healthcare providers and payers are challenged to meet these increasing expectations—and are investing accordingly in digital enablement. HfS’ recent state of business operations survey indicated that 42% of healthcare companies are planning a significant investment in analytics to better understand what are the issues for whom, what are the opportunities to interact and impact members and patients and administrative support; and 36% are investing in social/mobile/interactive enablement to redefine, “modernize,” or create the customer experience. Despite all this planning and rhetoric, dealing with the healthcare system often feels like the dark ages rather than a modern customer experience. Our recent research found several examples of service providers and buyers working together that are hopeful of experiences to come:

Creating the digital customer experience by connecting front and back office: Due to ACA regulations, healthcare payers have needed to adjust to dealing with consumers (versus employers’ HR departments.) Many have set up retail storefronts including mobile centers where people can come in for enrollment (majority), questions and paying bills. Teleperformance uses a proprietary software, TLSContact, to manage the process and workflow of the customer retail journey. Representatives are able to access the initial app that the customer started online, and the workflow software helps identify the bottlenecks and how to better staff these centers. For example, they can look at and analyze the processes to find out why there are long wait times—enabling clients to improve the process and better staff to meet demand.

Developing customer journeys that look “outside the hospital walls” and building solutions that support the journey: Approaching healthcare in a consumer-centric economy drives healthcare organizations to look at how to initiate and keep the customer relationship over an extended period of time, not a point in time. Emergency rooms are designed to address a “point in time,” but we know that a health incident starts before a person arrives at the ER. VCU Health neurologist Dr. Sherita Chapman Smith is championing an effort to use telemedicine as a way to do assessments on stroke patients while they are in the ambulance, on their way to the hospital. (link). In pilot simulations underway, the hospital is using trained actors to simulate stroke symptoms to test out the platform during ambulance rides to the hospital. “Patients” are picked up in an ambulance and connected via teleconference to the neurologist in the hospital, who conducts a remote assessment; and when they get to the hospital, they are quickly advanced to the next stage of treatment. The approach creates faster interactions between the points of care and speeds the time to treatment.

Using digital technology to make the users life easier and more real-time interactive with support systems: A healthcare organization that has partnered with NTT DATA Services described a consulting-led project which was aimed at the total redesign of the patient’s journey in various medical use cases (i.e. bariatric surgery, knee or hip replacement) in order to personalize that patient’s journey whenever he/she logs into the mobile app or accesses the website. This means drawing together an understanding of that patient’s journey from start to finish, and knowing what stages they are in throughout their course of treatment, and what their needs might be. This hospital relied on the provider’s experience mapping expertise.

It’s clear that healthcare isn’t getting less complicated any time soon. Whatever the fate of the ACA, the current political tone is foreshadowing more complexity and anxiety. Whether people are going to be uninsured or underinsured as critics of the current bill claim, or need to switch plans or providers, we can be sure that activity in the healthcare systems will increase. We can also be sure that that emotion will be at an all-time high, with the anxiety and fear that comes with people uncertain about what the changes mean for their lives and their loved ones: all the more reason that healthcare organizations need to be more nimble, intuitive and empathetic to that customer experience. Unfortunately, examples like the ones we highlighted above are the exception rather than the norm.

Bottom line: It’s time to think of and treat patients and members as customers you want to attract and retain, whether you are a health care provider or payer or a third party service provider partnering with a healthcare organization. Now we need to roll up our sleeves and partner in the effort to create a healthcare experience that puts the customer at its center.

“We’re driving this community as we try to figure out how to make our over-150-years-old financial institution relevant to the digital age and beyond,” said an executive from John Hancock last Monday, as they opened the inaugural Boston Fintech Showcase event. With 16+ startups in attendance, the Showcase was held at John Hancock’s Seaport district location, home to its Lab of Forward Thinking (LOFT) innovation group. The Boston community has growing influence in how modern technologies are making their way to various BFSI segments including payments, capital markets, insurance, mortgage, financial reporting, and taxation. Within the diversity at the showcase, what struck me were two common threads that bound the majority of the showcase participants and their value propositions to the legacy banking, financial services and insurance industry.

Reducing customer effort using technology: Driving better customer experiences is usually outlined by most large financial institutions as one of their key focus areas – with just cause, as customer ratings continue to fluctuate for this industry. A large part of financial services experience has to do with the level of effort it takes for end customers to interact with their banks and complete any transaction. Using more straight-through processing, automating redundant interactions, reducing the legalese required, and overall easing of the customer effort was a big theme at the Boston Fintech Showcase. For example:

Quilt is trying to streamline the life insurance segment for the new generation of millennial policyholders that want 100% online transactions/interactions with lower legal ease.

Rate Gravity is simplifying the home mortgage industry by eliminating salespeople and providing a single source for potential customers to compare lenders and complete their loan process more efficiently using technology.

Circle is a social payments platform that is using the open internet to offer secure and fast payments globally all from your mobile device, without any lengthy data entry/form filling (think Venmo for cross-border payments).

Leveraging data for new ways of working: A large number of the startups showcased, including the examples mentioned above, have focused on simplified data entry and making more efficient use of external data sources through automation. While this in itself adds to reducing the customer effort, we see ways in which some fintech startups are developing new businesses on the back of big data and analytics. For example:

Prattle is a text analysis specialist that offers sentiment data that predicts the market impact of central bank and corporate communications to help traders spot macroeconomic trends and improve their predictive models.

Finomial automates aspects of investor services by providing a single platform for fund administrators to process inflows/outflows, track transactions, get compliance dashboards (FATCA) and performance reports, as well as giving investors access to data and documents.

Finmason provides independent investment analytics to help customers make better decisions on their portfolio.

Partnering on fintech will drive new results for financial services

From our research, these examples and use cases are aligned with investment intentions that large financial institutions have expressed to advance their digital journey. They are also problem areas that IT and business services providers that run operations for banking clients are trying to solve.

While these startups have a head start with building out solutions, the next step for them is critical market exposure to scale solutions and drive adoption, partnering with clients, technology and service providers to the industry.

The corporate strategy head of a large financial institution brought up during our conversation at the event, “We are trying to prioritize which of these initiatives we really want to double down on in the next two years. We might have to look outside because we cannot create incubators for everything.” It is an opportunity for partnerships/acquisitions for service providers looking for innovative solutions, and at the same time, an opportunity to bring their strengths together. Part of the Fintech Sandbox initiative is giving startups free access to financial data to help them develop their offerings. This is another area where service providers could step up, with valuable operational data and expertise.

Overall, we see a strong need for the industry to work together to solve these critical challenges – lowering customer effort to create better service experiences, and making better use of data and analyses available to financial institutions. The event was a great example; many BFSI firms had internal strategy and innovation groups exploring fintech internally and supporting startups with incubator-like capabilities. With that kind of support, the Boston fintech community is quickly becoming a hub for smart enterprises on that journey.

In business operations, global shared services, and outsourcing, the mantra has been: centralize, standardize, industrialize, globalize. Traditional shared services and outsourcing contracts have been developed to focus on “lift and shift” and how to make processes increasingly more efficient and effective, measured by service level agreements. But what happens when the SLAs are green but customer or stakeholder satisfaction is level, stale, or down? When you feel that “innovation” is lacking? That the world is shifting to become faster, more flexible, and in-touch—but your business delivery isn’t and you just don’t have the time to think about it?

The answers to those questions are more and more often to use Design Thinking as a catalyst for innovation and continuous change. And it is the reason we explored the integration of Design Thinking into business operations and outsourcing design and delivery. Insights on how Design Thinking plays a role in creating a different experience—a different way of working and new insights for operational excellence and expansion—and 11 service providers are profiled in the recently published HfS Blueprint: Design Thinking in the As-a-Service Economy.

All of the service providers in the blueprint we’ve just published, Design Thinking in the As-a-Service Economy, are increasingly incorporating the principles of Design Thinking—human-centered, collaborative, action-oriented—into the way they work. Just like the increasing attention to robotic process automation and cognitive computing, experimentation has been going on for a while now… and so it is no longer “new” to many of them.

Design Thinking is a complement to, not a replacement for, operational excellence and solutioning for service design and delivery

You can use Design Thinking to understand what’s really causing problems or issues or expenses, by better understanding what people are actually doing –or not—and feeling. What is their experience? And then working through ideas that may revise, or replace, or eliminate process; that may change what people are doing and how; and could use current technology better, or new technology. As one shared services executive told us, “we already know how to make something efficient [with Lean Six Sigma] and we required a new way of thinking in some specific areas.” Along these lines, we are not anticipating an end or replacement to Lean Six Sigma or “operational excellence” but adding a way of stepping outside the process to identify trouble spots and new solutions.

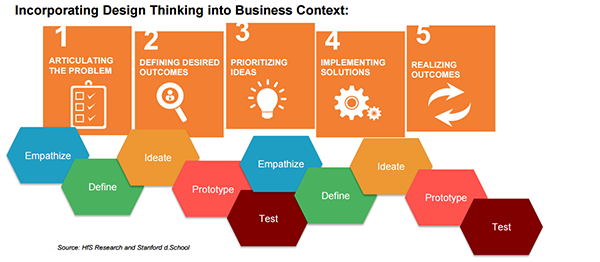

With Design Thinking you focus on understanding who is involved in whatever process or problem you are looking to address, and what are their expectations and needs (the “human” side)? And what is the industry and corporate context, the business outcomes to impact (the “business” side)? And what are the technology enablers? Then bringing it all together in a solution through a series of prototypes and tests. (See Exhibit 1: Incorporating Design Thinking Into Business Context for Shared Services and Outsourcing) Sometimes the solution is a quick fix, like changing the day of the week or where a request from a consumer is directed in a system; and sometimes it will help you identify a new way of working or a new service or solution.

Exhibit 1:

Bottom line: By using Design Thinking, we are moving a more human-centered, business-outcome oriented, and questioning approach to defining and delivering services in consulting and outsourcing, just the way the world is doing in general.

Using Design Thinking “was helpful because we make assumptions about people,” said an insurance executive interviewed in our study. Taking the time to empathize with the end user through interviews and observations “helped us to make sure we understand not just what we do for the consumer but how it makes them feel.” In other words, it’s not just about what you’re doing but the relevance of it to your end user. If you want your customers and your stakeholders to work with you to reach your business outcomes, then look for ways to make it easier for them to do it – and that means understanding them better, and that’s a role that Design Thinking can play.

Where is the outsourcing services industry on the path to integrate Design Thinking?

We want to help you, through our blueprints, to make the right match for a services engagement – short or long term. While that effort used to be about “we as a buyer post a list of requirements and look for cost reduction” and “we as a service provider will tap into our best practices, tell you about our features and functions, and hire or assign people who can process transactions” … times are changing.

Now, engaging a service provider or providing services to a business means understanding the context, the challenges, the outcomes desired, and how to broker and define a solution that can be flexible and change as the market changes. We’ve been calling this movement the “As-a-Service Economy.” Design Thinking can play a role in this movement towards a new way of working as partners. But because it is a new way of working, it does take time – trial and error and willingness to work in a new way. It impacts roles, governance, budgets, and contracts. And equally important, you need to have alignment in the expectations and cultures of the partners involved in order to feel as though this way of working can work – to deliver results.

In the Design Thinking in the As-a-Service Economy Blueprint, we look at the relevance, use and impact of Design Thinking in services engagements as it takes shape as an integral part of business operations and outsourcing solution and service design and delivery. It includes coverage of the following service providers in terms of Design Thinking integration into the way service buyers and service providers are working together: Accenture, Capgemini, Cognizant, Concentrix, EXL, Genpact, Infosys, Sutherland, Tech Mahindra/BIO Agency, Wipro

While most of the services and operations industry obsesses with Robotic Process Automation to streamline its rudimentary back office processes, one provider that’s never shied away from making bold moves to disrupt illustrious competitors is Genpact, with an imaginative move to integrate true artificial intelligence with its business process service offerings by acquiring the impressive Boston-based Rage Frameworks.

It’s almost history repeating itself from a decade ago, when the (then privately held) Genpact turned the BPO model on its head with its disruptive virtual captive proposition that significantly challenged the pricing models and ability to integrate offshore capabilities into the old BPO model. Now, the firm is breaking the mold, yet again, by making real inroads into infusing AI into business processes and introducing these concepts to its huge global community of finance leaders.

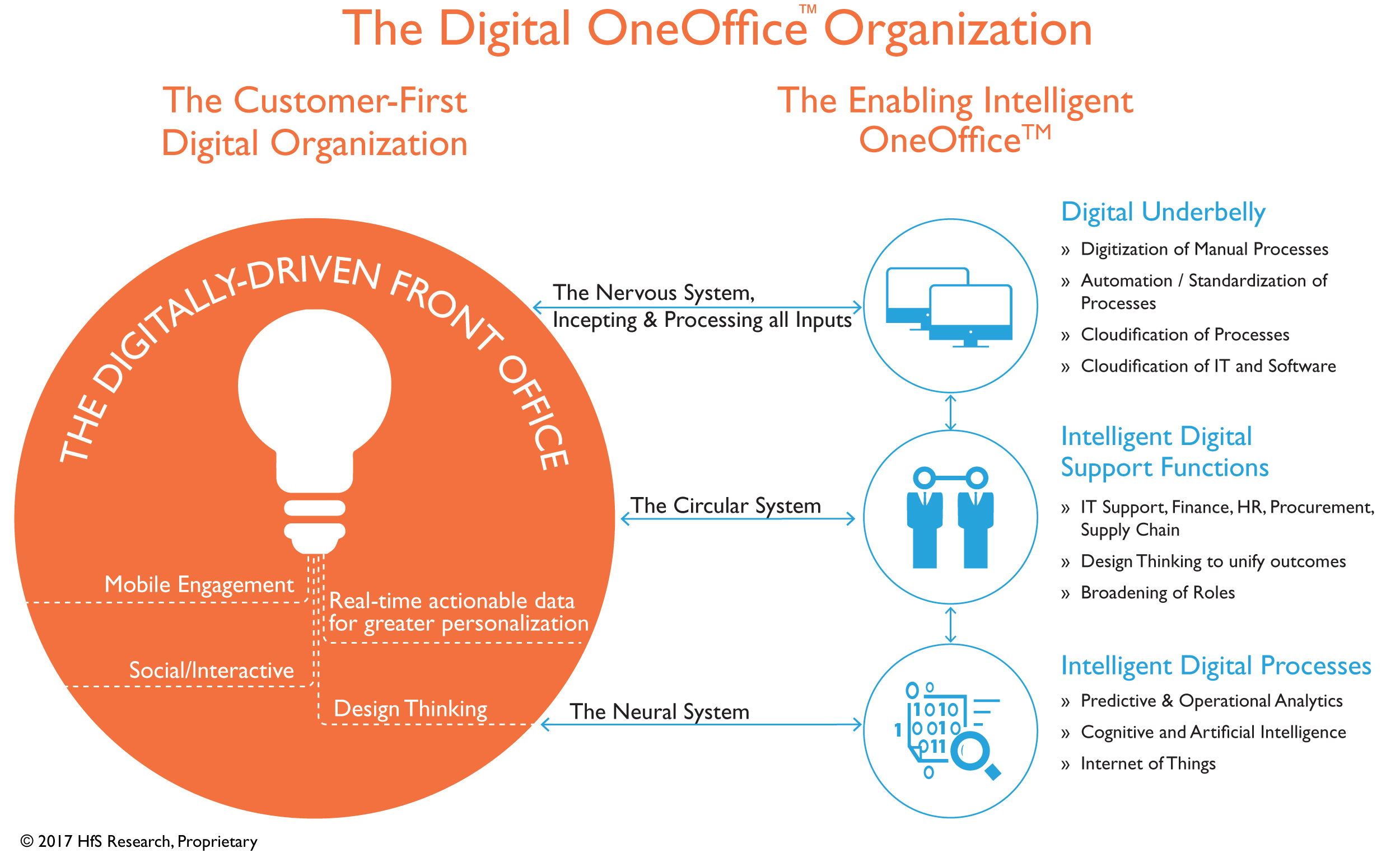

Let’s get to the rub: RPA is all about digitizing the back office, but Artificial Intelligence is where we see the true marriage of business processes with clever technology and self-developing algorithms. We’ve danced for years trying to prophesize when BPO will truly integrate with IT, but we’ve now had reality unveiled: RPA platforms streamline the back office, while AI brings the middle and front together to create that true Digital OneOffice™ experience. The Digital OneOffice is not about collecting and archiving historical data simply to discover what went wrong, it’s about being able to predict when things will go wrong and devising smart strategies to get ahead of them. The Digital OneOfficeis about embedding smart cognitive applications into process chains and workflows, it’s about learning from mistakes and new experiences along the way. This is the emerging “organization neural system”, where the needs of the customer can be intelligently supported by real-time, self-learning intelligent operations:

In a nascent market where stakeholders stumble through smoke and mirrors to make any sense of the many claims around Intelligent Automation, M&A is a clear indicator that the market is starting to mature. When in December 2016 ISG bought Alsbridge and CA acquired Automic, HfS suggested that Intelligent Automation was at an inflection point and that the focus on automation tools will shift toward the likes of Google, Amazon, and Facebook around deep learning and the integration of unstructured data. While we have not yet seen the Internet giants play their hand, Genpact’s acquisition of Rage Frameworks is underlining exactly these market dynamics. And this is the first time that a service provider is driving automation capabilities through M&A.

Rage Frameworks drives pre-built automation engines deep into unstructured territory

Whereas the broader market remains misguidedly focused on the intricacies of RPA, Rage’s focus is not on automating specific process steps, often on sub-process level, but on developing a broad ranging platform (RAGE Enterprise) for custom solutions with a deep vertical footprint. While RPA is largely focused on structured information, Rage will take Genpact deeper into integrating semi and unstructured data. Their development effort over the last two years to build enterprise applications for financial industry processes (wealth management, commercial loan processing and financial statement spreading) is shifting the focus from automation tools and capabilities to providing an end-to-end process leveraging a model driven business transformation platform.

In our view, the value proposition of Rage Frameworks is centred on leveraging Machine Learning and Natural Language Processing to build out highly vertical engines in Financial Services, Capital Markets, and Supply-Chain. The functionality of these engines ranges from managing business rules to real-time integrating content to data access and NLP all built around a process assembly engine. These engine building blocks can then be assembled for custom solutions that automate business processes or can be used as one of three pre-assembled financial services industry applications: LiveWealth, LiveCredit, and LiveSpread. In addition, broader capabilities including front desk automation, real-time intelligence, and pricing are transforming how commercial lending, policy underwriting, financial statement analysis, investment research, and multi-system reconciliation can be performed.

RAGE’s industry applications are a big part of the allure for Genpact, which has spent the last few years going deeper into its commercial banking and capital markets operations accounts with data and analytics solutions trying to solve the same client operational challenges as Rage. In our recent HfS Capital Markets Operations Blueprint, Genpact placed in the Winner’s Circle, with an HfS callout about its need to bring more technology enablement to capital markets. The service provider has examples of using emerging technologies such as machine learning, automation, dynamic data extraction, etc., in LOBs as retail banking. What Rage brings to the table for Genpact is a more strategic approach for impacting client operations through technology-led change.

Genpact continues to lead the automation discussion from the front

From Genpact’s perspective, the acquisition is reinforcing the perception of being a pioneer in Intelligent Automation. Having led the market with the first publicly announced partnerships with AutomationAnywhere, Exilant, and Automic around its Rapid Automation program, Rage Frameworks fits in well with Genpact’s holistic approach to automation. Within that context, Rage’ assets will further advance the integration of unstructured data: Genpact has invested heavily in analytics and big data with a dedicated research lab in Bangalore, India. They have developed a Data Engagement Platform using big data technologies, in order to be able to harness structured and unstructured data from multiple sources. Thus, its Lean Digital strategy is aligned with HfS OneOffice concept. But the company has to demonstrate that it is starting to link up back, middle and front-office.

The broader market will follow with accelerated M&A activity

Regulations and risk management requirements are forcing banks to rethink the way in which they capture, store, manage, and distribute the growing volumes of transactional and trade data. Structured data from multiple departments and asset classes are maintained in silos, and unstructured data present new challenges as well as opportunities for automation and analytics.

Despite the continuing noise around RPA, we believe the market will shift toward operational analytics and the broader notion of AI. Not only are the leading RPA tool providers expanding in that direction, but we expect the investment focus to progress toward Deep Learning, Neural Networks, and broad NLP capabilities. While it might sound trite, data really is becoming the new currency. But this currency needs to be integrated into delivery backbones on an industrial scale. Thus, service providers need to reinforce their efforts on service orchestration. We haven’t seen many proof points for a successful expansion into data-centric scenarios, but those deployments will be a clear demarcation between the leaders and the also-runs.

Central to this will be the articulation and delivery of business outcomes for specific industry functions through the use of operational analytics, RPA, BPO and AI. Can Genpact put together a financial spreading function by leveraging its operational expertise in BPO and RPA, the RAGE LiveSpread application and analytics interventions to deliver more efficient and effective credit risk management?

Bottom-line: Genpact is progressing toward True Digital OneOffice capabilities

Genpact’s announcement can be crystalized to its ambition of blending RPA in the back-office with AI in the middle-office, which is why the firm, still regarded by many as a “pureplay BPO” managed to break the top 10 in the recent Digital OneOffice Premier League, despite not dragging a multi-billion dollar IT services business around.

Thus, BPO is ever more changing to becoming technology-led. We expect that this strategy will be increasingly underpinned by neural networks and notions of self-remediation to enhance the Digital Underbelly and the Intelligent Digital Processes of the OneOffice concept. While Rage Frameworks is one of the superior suppliers across the Intelligent Automation Continuum, the more providers that are progressing toward the notion of AI, the more inflated the valuations for M&A will become. Against this background, valuations for RPA providers could look like peanuts very quickly. But then again, M&A is rarely rational in today’s foggy market.

At HfS Research, we’re growing fast in a very competitive and volatile market… and with growth comes change – but change is always good if you ask me! The most fun in jobs is when you have changes – you learn new things, get new ideas, and you meet new people to help accommodate the change.

HfS is always on the lookout for serious talent that can help our clients become even more successful. So happy days when I heard that some serious quality was on the lookout for some new chapter in her life. Sunayana Hazarika has joined per January, and today I wanted to give you a little more background about her.

Bram Weerts, Chief Commercial Officer, HfS:

Bram Weerts, Chief Operating Officer, HfS Research: Sunayana, can you share a little about your background and why you have chosen Marketing and Brand Reputation as your career path?

Sunayana Hazarika, Senior Brand Strategist at HfS Research: As the saying goes” Everything happens for a reason,” the economic recession in 2008 changed my career path. From an engineering graduate to a remote executive, my first job in TTK Services introduced me to the world of marketing. I was facing global clients- the who’s who of the business world from renowned bloggers to technology founders, and helping them in doing Digital marketing (web marketing is what it was called then). The varied requests from clients opened the door for understanding SEO, content marketing, social media promotions, brand messaging, to even executing fundraising events. This inspired me to pursue my MBA in marketing and soon after explored both services marketing and product marketing of software enterprise solutions.

What draws me towards Marketing is the very nature of it – dynamic, fast paced and the fact that it is centered around the relationship between People’s awareness, product/service innovations and the value generation. I am intrigued by how brands impact the market. To me, Brand Management is like nurturing a sapling to grow and proliferate into a forest. The right and proper projection of the organization is the heart of Brand Reputation. A big and serious task, but with the passion and right intention, we can see the results. All this put together has compelled me to make marketing a career and more so in brand management.

Bram: Why did you choose to join HfS?

Sunayana: HfS Research is an industry leading research and data analytics firm, renowned as a trusted voice with edgy insights and disruptive viewpoints. They do not shy away from raising real issues even if it bruises some egos. I echo the same spirit. The organization has an impressive and matured outlook focusing on fostering an optimized business function, fully empowered team and delivers maximum value for the global community of clients. This provides me an opportunity to unearth optimum potentials to scale heights of success. Moreover, the fact that it analyzes cutting-edge technology and services like Digitization of business processes and Design Thinking, Intelligent Automation and Outsourcing makes it even more viable for a marketer to be on top of latest market trends. And to top it up is the pleasure of working with some of the most intelligent and good people on earth. Trust me; I have never been more content.

Bram: What are the areas of focus for driving success in your current role?

Sunayana: The success of marketing in a Research, Data Analytics, and Strategy firm lies in enabling the “informed decision making” by providing the right information at the right time to the right set of people. For this, it is crucial for Marketing to merge into the organization’s core objective and culture. This enables outlining the appropriate value proposition to the audience. It is also equally important for marketing to connect with the audience to know their expectations and be abreast with the market. The focus on maintaining a symmetry between the two approach creates a two-way network for shared experiences and true value projection.

Bram: What trends and developments are capturing your attention today?

Sunayana: The world is moving towards digitalization and the marketing function of an organization, as a harbinger is expected to lead the way. Mobile, Social Media, Analytics, and cognitive automation are breaking the path for an individualistic approach towards interacting with the target audience. We as marketers should harness these technology enablers to increase market reach and have personalized engagement with the audience directly. These innovations can be used to evade distractions, garner relevance and bridge the gap between insights and actions.

Bram: And what would you like to see different in the research/services industries?

Sunayana: “Change is inevitable” and occurs sooner than ever. Information, opinions, trends, technology and processes have an expiry date, so it makes sense for the industry to keep ahead and have control of this transformation through continued innovation and research. Even if it requires challenging or superseding conventions, proven methodologies, tested services, recommended solutions, wealthy analysis or rich offerings.

Bram: And, what do you do with your spare time?

Sunayana: I love to explore nature and my husband partners with me, we go hiking in the forest and hills, trek to mountains, swim in natural water sources, to get out of comfort zone and appreciate the basics. I love to travel and go on backpacking trips to live life in a million different ways, with people from various regions and enjoy a variety of cuisines.

I also play racquet sports regularly and enjoy watching good movies and reading books.

Bram: If you could change one thing in Marketing what would that be?

Sunayana: Marketing has often been looked at as a function that projects the magnified and exaggerated image of the values provided by an organization. This need not be the truth anymore. Marketing is an integral part of an organization aligning to its goals and objective. Marketing enables organizations to stay in touch with their target audience, understand them and relate to their unique and different needs. Now in this new age with the availability of instant information in one’s fingertip, the audience is gravitating towards facts and authenticity of every promotion and do not get allured by the shine. Therefore, it is time marketing reflects the true image of the organization and value of the offerings to its clients.

Bram: Thank you for your time Sunayana, it’s a real delight to have you onboard and work with you in these fascinating times!

This roughly $300M deal, expected to close end of June, doesn’t only have the potential to positively impact the HCM agendas of 4,000 combined customers worldwide between the two talent management players. It also has the potential to lift the HR Tech domain overall. How can this deal possibly achieve something that the much larger HR Tech deals done by SAP and Oracle didn’t?

For one thing, SAP buying SuccessFactors and Oracle acquiring Taleo were motivated in large part by accelerating a transition to the cloud, and secondarily, by the ability to leverage best-in-class Performance Management (SuccessFactors) and Recruiting Technology (Taleo) at the time. Elsewhere, IBM acquiring Kenexa gave it a nice beachhead from which to eventually launch other HR services and solutions. In short, these deals arguably benefited vendors more than they helped customers achieve better HCM-dependent business outcomes.

The Saba – Halogen Software deal opens new routes to HCM optimization

We suspect many forward-thinking HR technology customers will want to take advantage of the combination of a world-class LMS (Saba) and a top-tier Performance Management solution (Halogen) in ways that extend beyond performance review and coaching outputs feeding employee learning and development plans. These talent management “meat and potatoes” capabilities are there. The “kicker” is the combined ability to address today’s unprecedented rate of change, the explosion of corporate social tools, and just-in-time learning.

And this leads to the often-illusory goal of “organizational agility.”

Saba + Halogen together could enable a bottom-up, employee-owned and initiated way of quickly addressing whatever performance, behavioral or skill gaps are most relevant at any point in time. Saba has robust capabilities around informal learning and social collaboration tools (even social network analysis functionality). Put it together with Halogen Software’s flexibility to support many different performance management models, and you go beyond that “meat and potatoes” passing of performance management process outputs to actionable learning plans. It’s a whole new level of execution that ties together professional development, employee engagement, individual / team performance and business results that include improved organizational agility.

Take the example of a mid-level professional being moved from an individual contributor role to one of managing a project team, add-in that the vacancy was unexpected, the project is behind schedule, and there aren’t many other resourcing options. The new project manager can immediately start marshaling peer and team member feedback, coaching and mentoring, broader community or social network support plus other internal and external resources to make this resourcing dilemma a much more manageable issue. Now multiply this unexpected, unplanned scenario by dozens company-wide.

When you can mitigate risk to sustain momentum on key initiatives this way, you have the essence of organizational agility.

Bottom Line: This new pairing of HR Tech players might be the answer for many organizations that are too often held back by their lack of organizational agility.

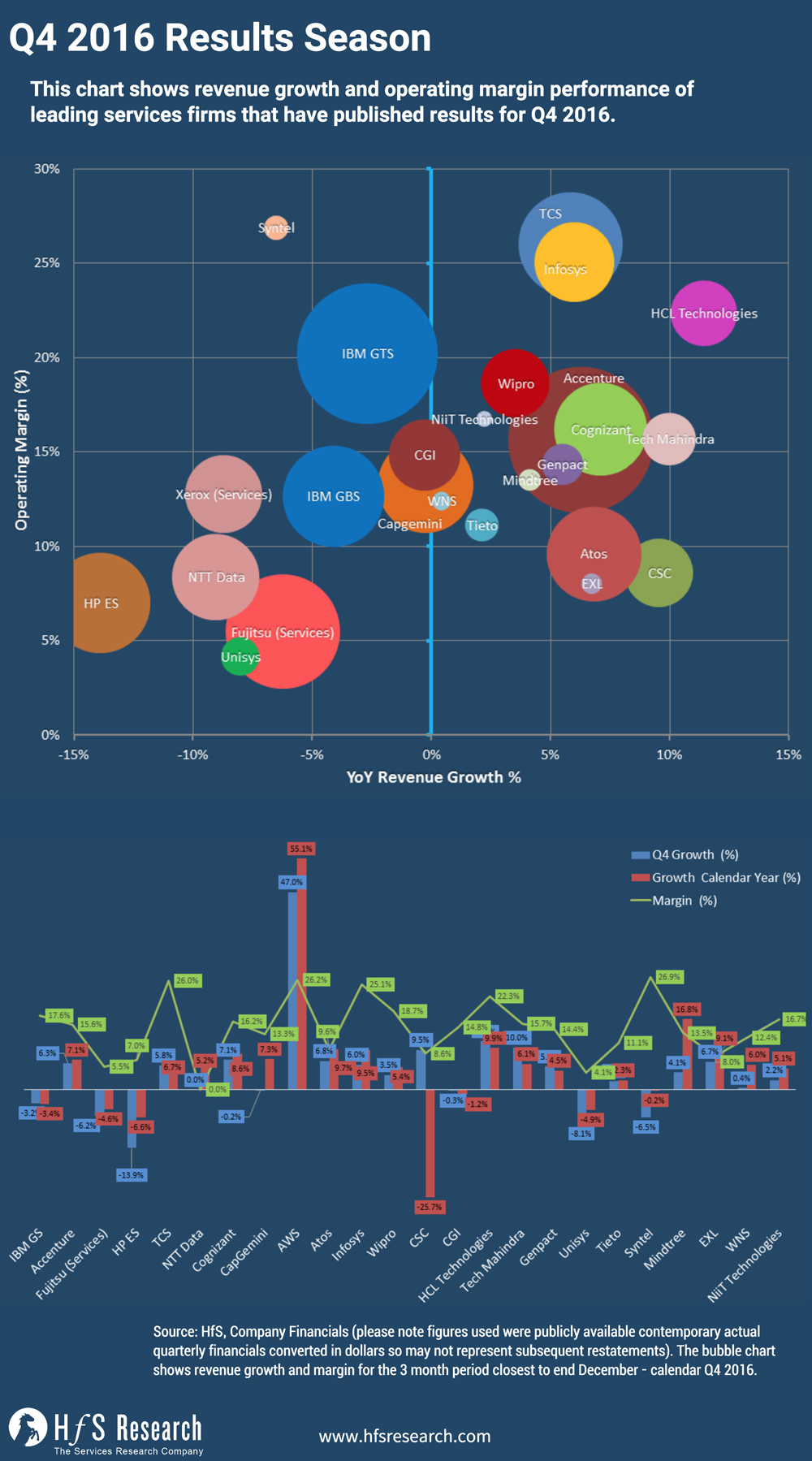

The traumatic Q4 results season has finally ended and our Chief Data Officer, Jamie Snowdon, is able to report on the final Q4 standings…

We’ve visualised the latest set of results for Q4 in the diagram, the top chart shows our usual margin v growth view (excluding AWS). With a chart showing the quarterly growth for Q4, an estimation of the annual (calendar) growth and the Q4 operating margin.

For each of the providers the results look like this:

Growth Q4 (%)

Growth 2016 Calendar Year (%)

Margin Q4 (%)

Comments

Accenture

6.3%

7.1%

15.6%

Good quarter for Accenture with plenty of success stories around digital, cloud and security. Constant currency growth around a percentage point above the actual growth for the quarter. Annual services growth is 7.1%.

Atos

6.8%

9.7%

9.6%

Coming down from the highs of its recent acquisition-fuelled growth of the last couple years – Atos remains solid with organic growth at 1.8% for the year and 1.9% for the quarter. Benefiting from strong execution and its investments in analytics, security and automation.

AWS

47.0%

55.1%

26.2%

Although AWS revenue growth has slowed in percentage terms that is due to the scale of its actual growth in Q4 2016 it added over a $1Bn in revenues over Q4 2015. AWS is adjusting its strategy to become more relevant to large enterprise clients that want more than just public cloud. Thanks to its partnership with VM Ware hybrid is no longer a dirty word at AWS.

CapGemini

-0.2%

7.3%

13.3%

Poor end to a good year – 2016 growth up 7.3% (7.9% in constant currency) -0.2% in Q4 (1.9% CC). iGate integration now done can concentrate on operations. Strong application growth for the year (10.6% CC) – portfolio shift toward digital, cloud and automation.

CGI

-0.3%

-1.2%

14.8%

Constant currency growth was higher than actual at 2.8%, giving the provider around market performance for the quarter – the firm has strong signings and order backlog so we expect to see actual growth during FY 2017.

Cognizant

7.1%

8.6%

16.2%

Cognizant continue to shift portfolio more toward digital services as its traditional markets slow. Hit by weak UK market performance in Q4 – we expect its growth profile to remain at similar levels into 2017. Overall growth for 2016 was at 8.6%

CSC

9.5%

-25.7%

8.6%

CSC saw a healthy pickup in revenue growth due to recent acquisitions, notably xChanging and UXC. However, revenues overall for the year still down thanks to earlier split. The company is still due to merge with HPE’s services business in April.

Fujitsu (Services)

-6.2%

-4.6%

5.5%

Q4 declined -6.2% in its technology solutions services busines for the quarter, with small declines for the whole year. Sales in the Japanese market picked up with growth of 4.5% during the quarter. International business impacted by strong Yen – with Europe and especially the UK hurt the most. Infrastructure services hit particularly hard – although its systems integration business showed a growth of 5.7%.

Genpact

5.5%

4.5%

14.4%

Constant currency growth was stronger for the quarter at approx. 7%. Growth for the year was at 4.5% (6% at constant currency) – this growth was largely down to its BPO business which grew at 7%, its IT Outsourcing business shrank 5%.

HCL Technologies

11.5%

9.9%

22.3%

HCL’s growth in 2016 was 9.9% US$, it expects to hit middle of its 12-14% guidance for fiscal year. HCL seen strong growth in application services and infrastructure services businesses, Infrastructure services growth due to large deals like Volvo.

HP ES

-13.9%

-6.6%

7.0%

Not a great deal to say about HP’s servies business – we expect more meaningful dialog once the merger with CSC has happened.

IBM Services

-3.2%

-3.4%

17.6%

IBMs total growth driven by strategic imperatives analytics, cloud, mobile, security and social. Q4 YoY all cloud topped $4.2B in Q4 growing at 33%, its annual AaS run rate reaching $8.6b (GTS only had 50% cloud growth with AaS RR of $5.8b) IBM GBS hit by declines in traditional services revenues like ERP – it is still struggling to grow. GBS saw declines in consulting, GPS (BPO) and apps management in Q4. Revenues shifting to digital as GBS delivers more cloud services revenues, which reached 77% growth for GBS in Q4.

Infosys

6.0%

9.5%

25.1%

Overall Infosys revenue for 2016 was up an impressive 9.5% during the calendar year. Like its contemporaries, Infosys continues to drive additional growth through refocus on digital – particularly on Automation and AI.

NTT Data

0.0%

5.2%

0.0%

Although growth in Q4 was flat, thanks to strong H1 growth in 2016 was at 5.2%, with improvement in the Japanese market. Strong growth in cloud and digital services.

TCS

5.8%

6.7%

26.0%

Growth below 10% for 8 quarters, still largest offshore-centric firm adding c$250 million in revs Yr-on-Yr in Q4, and >$1Bn in 2016. Growth driven by cloud, digital and platforms business, 30% growth in digital.

Unisys

-8.1%

-4.9%

4.1%

Unisys declined by 4.9% for the whole of 2016. Unisys still can’t seem to catch a break, it needs a good quarter to break the cycle constant internal cost-cutting and focus on becoming relevant to the market by executing changes to its services portfolio.

Wipro

3.5%

5.4%

18.7%

Wipro’s 5.4% for 2016, the weakest of the offshore firms. Wipro is pivoting from traditional services to Digital and AaS. Making digital priority with >$1Bn in acquisitions this year. Digital up c10% sequential growth in Q4. Digital 21.7% of revenues.

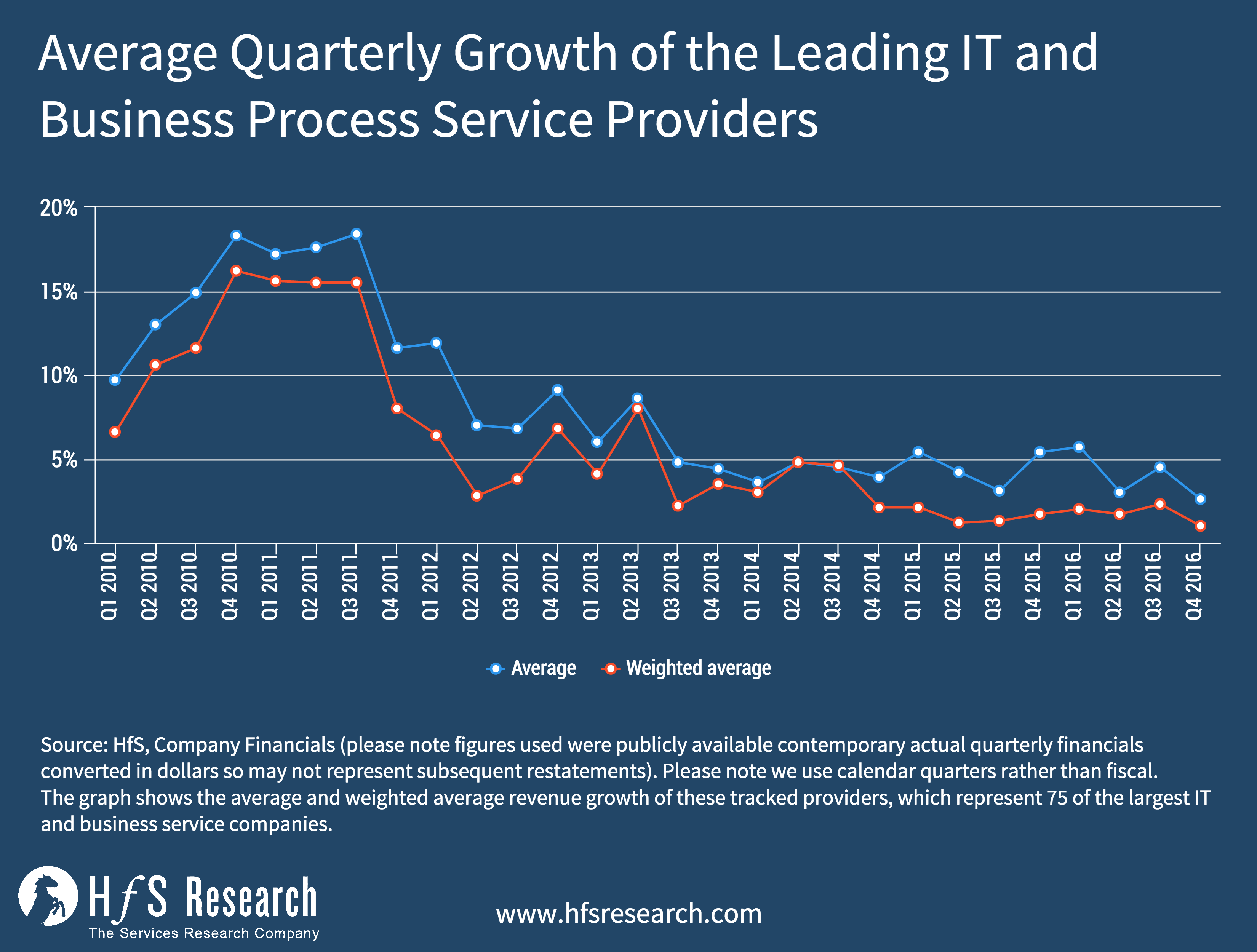

However, it is important to view Q4 in context, the following chart shows the average and weighted average revenue growth of these tracked providers, which represent 75 of the largest IT and business service companies.

After a strong Q3, Q4 dropped back – making it the worst quarter for average growth since 2010. There are a number of factors that caused this drop – partly the on-going uncertainty in the market heightened by Brexit and Trump, but also the last few quarters were boosted by revenue from smaller acquisitions which no longer impact the growth.

The Bottom Line – The traditional outsourcing model has had its day, now we need to focus on the emerging client needs in this transitional market

For the market as a whole Q4 was a disaster – with the worst average growth rates seen since we started this tracking in 2011. This really shows how much the market is shifting toward new more technology driven solutions and how much of the traditional cost is being cannibalized by these new digital platforms and automation.

The onus is on us as analysts to start looking more deeply into the underlying trends in the market as the top-line data is increasingly swamped with hangovers from last decade. There is growth out there – but it is barely offsetting the declines in existing business. We have looked under the hood of the infrastructure management services market in one of our latest reports – IT Infrastructure Management Services in the Post Digital World – which is available on hfsresearch.com.

The time for smart partnerships to drive real innovation and new thinking in Artificial Intelligence (AI) and cognitive computing is now. This means we need to see the industry’s deep-pocketed innovators become increasingly open – and eager – to working together to help the services industry make the shift to true digital, intelligent, cognitive capabilities.

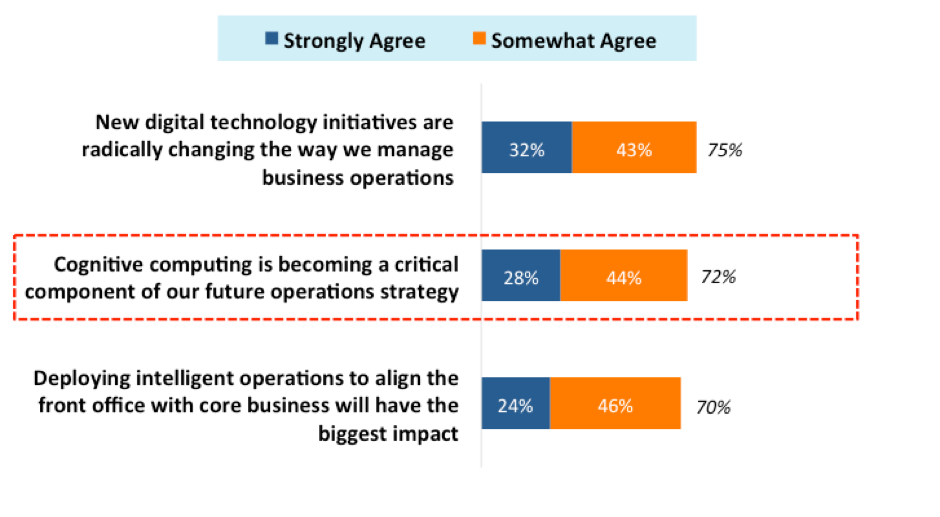

Recent HfS research shows adoption of Artificial Intelligence (AI) and cognitive computing to enhance operational analytics and Machine Learning is strongly accelerating, with 72% of senior operations executives citing cognitive as becoming a critical component of the future operations strategy:

Digital and Cognitive are Driving Enterprise Operations

While the market perception around these topics remains refreshingly blurred, AI is a critical building block as organizations increasingly look to progress from legacy labor-driven service delivery to progress toward notions the As-a-Service Economy and the Digital OneOffice (see link). While AI is capturing the imagination of many PE investors and VCs and is being used to hype up media reporting and conference circuits, the market dynamics are far from clear.

Against this background, the fundamental question being posed is “Who will be in the driving seat scaling out the deployments? Will it be the service providers, the leading industry platforms or will startups scale out?”

Salesforce Einstein and IBM Watson Partnership: A genuine step forward in AI, or another nice Press Release?

Salesforce and IBM have announced a global partnership to integrate their respective AI platforms to provide enhanced information and services to joint clients. Clients currently have access to Salesforce Einstein, which is built into the Salesforce Intelligent Customer Success platform. Einstein provides a broader set of capabilities around operational Analytics and Machine Learning. Salesforce’s ‘Spring 17 product announcement made Einstein available across Salesforce cloud products for customers. The integration of Einstein with Watson, planned for the second half of 2017, would bring significantly deeper and broader analytics insight to customers. In addition, IBM Application Integration suite for Salesforce, which enables clients to integrate on premises and cloud data for Salesforce, will become available at the end of March 2017. IBM, for its part, will deploy Salesforce Service Cloud enterprise-wide.

So, what does this mean for the respective parties?

Client and business growth: Both providers have broad opportunities to cross-sell into their respective customer bases through the partnership. The providers have an estimated joint client base of more than 5,000 enterprises.

Salesforce strengthens growth area: As market awareness, if not real demand, for AI increases, Salesforce will be able to offer clients a broader orchestration of AI enabled services. The fact that it has already made Einstein available across Salesforce cloud products demonstrates the software provider’s commitment to and investment in this space.

Potential to create leading AI offering: The partnership has the potential to drive broad AI capabilities into industry platforms. Thus, extending the reach and commoditizing of Watson capabilities. From a domain standpoint, while Einstein has focused on customer relationship management, Watson is going deeper into vertical scenarios, in particular financial services, healthcare and retail. Additionally, weather data from Weather.com will create new opportunities for both AI capabilities to test new use cases altogether. Salesforce brings its broad customer base and rich customer data to the table. IBM has had a head-start with building Watson APIs and products, which Einstein could benefit from. Clients will most likely select multiple cognitive engines in the next few years, as they embark on their journey towards increasingly intelligent operations that require less direct human interaction. These systems will need to interact with each other, built upon interoperable standards for data curation and access. A partnership like this could help that process, and possibly help clients with overall cognitive engine adoption in the long run.

IBM wins in technology and services: As well as finding an additional, lucrative channel for its Watson technology, IBM also has an advantageous position to take the associated IT services work. IBM strengthened its Salesforce services capabilities by acquiring specialist Bluewolf in 2016 (see: IBM Culls The Pack Of Salesforce Partners By Buying Bluewolf). Salesforce has always had a close relationship with Bluewolf, and it’s no surprise that it has decided to strengthen this particular partnership now. Bluewolf, an IBM company, will establish a practice to deploy the combined functionalities for clients, called Bluewolf Dedicated Consulting Services and Expertise for Cognitive Solutions. IBM will therefore strengthen its position in this market, with potential increases in technology and services revenue. Other partners in the ecosystem with the relevant capabilities have opportunities to build out similar services, but Bluewolf has a first mover advantage.

How can this partnership truly plug Salesforce’s gaps in Analytics?

While the stage could be set for AI in the long term, Salesforce needs to address the more basic analytics piece of the equation. While access to advanced AI insights delivered by a combined Watson and Einstein platform is useful, most Salesforce services clients are simply grappling with implementing basic analytics solutions. Some Salesforce services clients who require analytics capabilities have selected alternative solutions to Salesforce because of the disappointment with the slow development of the Salesforce Wave Analytics product and the service providers’ slow ramping up of Wave capabilities.

Our research from the HfS Blueprint Report: Salesforce Services 2017 highlights that most Salesforce services clients are just starting to consider analytics services, so Salesforce needs to speed up its development of the analytics module as well as market the developments made, so as to prevent any future clients looking elsewhere. Analytics services, particularly consulting services are a massive growth opportunity for Salesforce services providers. Leading service partner, like Accenture, Deloitte, Cognizant and IBM, have invested in analytics solutions and services, anticipating the upcoming demand, but the specific solution selected by clients will not necessarily be Wave Analytics.

The bottom-line: This new partnership could genuinely accelerate the commoditization of AI capabilities

This partnership is a smart move by both Salesforce and IBM to use their strengths collaboratively – potentially winning IBM and Bluewolf more business, bringing Einstein up to speed on Watson’s expanding range of cognitive capabilities and industry depth and most importantly, unite the industry heavyweights that are most heavily marketing AI capabilities. At HfS, we increasingly view smart partnerships with real teeth as the way forward for the software and services industry makers.

The ecosystem around Watson capabilities is slowly starting to emerge. IBM is working on a more structured approach to driving the broad capabilities toward partners that often are its competitors beyond the more narrow Watson context. As with all partnerships, most will come down to the investments into the collaboration and how transparent the account management will be. For IBM the partnership could accelerate the pervasiveness but also the commoditization of its Watson capabilities. The upside could lie in establishing Watson as de facto standard for broader industry platform and thus see Watson crystalizing its position in emerging ecosystems. Conversely, Salesforce could get access to much deeper analytics capabilities that would increase the stickiness of its products.

For the broader market, this could provide the blueprint for driving Watson capabilities into other industry platforms such as ServiceNow, Workday, and others. Fundamentally though this requires significant education of clients that the combined marketing power of IBM and Salesforce could provide. And these initiatives could prove tactically helpful to contain the impact of emerging competitors to Watson. If executed effectively, the Digital Underbelly of the OneOffice could mature significantly faster.

Sunayana Hazarika, Senior Brand Strategist at HfS Research: As the saying goes” Everything happens for a reason,” the economic recession in 2008 changed my career path. From an engineering graduate to a remote executive, my first job in TTK Services introduced me to the world of marketing. I was facing global clients- the who’s who of the business world from renowned bloggers to technology founders, and helping them in doing Digital marketing (web marketing is what it was called then). The varied requests from clients opened the door for understanding SEO, content marketing, social media promotions, brand messaging, to even executing fundraising events. This inspired me to pursue my MBA in marketing and soon after explored both services marketing and product marketing of software enterprise solutions.

Sunayana Hazarika, Senior Brand Strategist at HfS Research: As the saying goes” Everything happens for a reason,” the economic recession in 2008 changed my career path. From an engineering graduate to a remote executive, my first job in TTK Services introduced me to the world of marketing. I was facing global clients- the who’s who of the business world from renowned bloggers to technology founders, and helping them in doing Digital marketing (web marketing is what it was called then). The varied requests from clients opened the door for understanding SEO, content marketing, social media promotions, brand messaging, to even executing fundraising events. This inspired me to pursue my MBA in marketing and soon after explored both services marketing and product marketing of software enterprise solutions.