There’s only one thing in our world that keeps Donald Trump off the headlines… of course… it’s good ol’ Infosys! Yes, folks, we actually seem to care more about who is attending these board meetings and squabbling about the cost of refueling the company jet, than the nuclear warheads currently pointed at Pyongyang.

Yes, people, the $10bn Bangalore-headquartered outfit is trumping Trump in the media… an exclusive on what Murthy had for breakfast is far more interesting these days than the handbag Ivanka just purchased. And the eighty-seventh article analyzing just why poor ol’ Vishal wasn’t quite leaping for joy every morning during his tenure, is clearly more impactful to our lives than the US government potentially shutting down, because Donald wants his wall built…

But there is a solution: Donald Trump can avoid impeachment, quit the Prez job and take the reigns at Infosys. Where better to make something great again, where he will hog the headlines more than anyone has… ever! Just think: Trump + Infosys… we will never need to read about anything else again. Ever.

Why this would be Donald’s dream job:

1) Build a wall around Electronic City to keep out the TCS and Wipro headhunters. Then rename it Trump City.

2) Repeal Murthycare without the need for any new ideas. Just get rid of it and think of something later.

3) Tweet incessantly about how much he hates Abid, Frank, Premji, Vishal, Meg, Ginni, Murthy…

4) Ban the Times of India and Livemint from all press briefings – only allowing in the new Trumposys Monthly magazine

5) Invest the whole $6bn warchest in Infosys Russia. Including a state-of-the-art Kremlin Lab that Putin can open personally

6) Put Sean Spicer in charge of the Artificial Intelligence strategy

7) Impose a travel ban on all robots to keep the FTE model intact

HfS’ Saurabh Gupta recently caught up with Brian Behlendorf (see bio), the Executive Director of Hyperledger at the Linux Foundation. Brian was a primary developer of the Apache Web Server – the most popular web server on the internet. He was a founding member of the Apache Software Foundation, the founding CTO of CollabNet, the CTO of the World Economic Forum, and the managing director at Mithril Capital Management LLC before heading Hyperledger. He is also a board member of the Mozilla Foundation since 2003 and the Electronic Frontier Foundation since 2013.

Two decades after developing the Apache HTTP server that played a key role in giving us the internet and the web, Brian is reimagining our world again with blockchain. We discussed a range of topics around the reality and practicality of blockchain for enterprises along with the one wish that he wants to come true.

Saurabh Gupta, Chief Strategy Officer, HfS Research: Brian, one of the stated goals for Hyperledger is to create enterprise grade frameworks and solutions. Why do you think enterprises should adopt blockchain?

Brian Behlendorf, the Executive Director of Hyperledger at the Linux Foundation: We have lots of transaction networks that, Saurabh, because of historical network choices, have resulted in many central actors who facilitate digital transactions like a hub in a hub-and-spoke network. And we have to proxy our trust to them – sometimes they do a noble job and charge a nominal rate, but there are times when these central actors charge unreasonable double-digit rates. Blockchain allows business models to become more equitable and agile by behaving more like the internet.

The cryptocurrency community has produced a lot of interesting technological advancements, and there are valid and worthy uses for them, but the majority of the enterprise market is looking for a consortium approach – one that still sees a representative organization to set the rules of a market, but where the market operates more directly peer-to-peer and distributed, rather than all transactions going through that central party. These consortia can upgrade the rules from time to time with the consent of the market, , and help define and enforce a set of legally binding agreements to cover situations that the technology does not cover.

As an example, an organization like SWIFT can reinvent their current offerings as distributed ledgers, to not only optimize the product (reduce turnaround time from 3 days to 5 mins) but also make them more accountable to their member backs. Essentially, they become referees on a football field, instead of the quarterback.

It’s not just financial markets; we can re-invent claims processing with distributed ledgers and smart contracts to make it is less bureaucratic. We can share patient records with strong audit and access control. There are use cases across healthcare, supply chain provenance, and many industries. These may sound like disparate use cases, but it’s similar to how TCP/IP transformed the world in the 1990s….who thought that an online bookstore would become the most valuable company 20 years later, but it did.

Saurabh: Why should enterprises look at Hyperledger? There are so many different permissioned and permissionless frameworks out there, so what is the elevator pitch?

Brian: As new technology develops, there is a call for standards. Participants want to focus on time and effort and investment to build solutions versus worrying about the framework. This is the rationale for open standards. There has been a linear progression from open standards to open source software. While financial firms are behind the curve, if they want to get behind this idea you need everyone else to adopt it…and that requires open source.

That is why we are pulling together the most exciting portfolio with a multi-lateral developer and vendor community. As a result, clients don’t just have to go to IBM; they can reach out to Accenture or Wipro or frankly hundreds of other startups and still get the same basic technical architecture. It’s similar to the benefits that Linux brought to the world of operating systems.

Saurabh: We recently saw the release of Hyperledger Fabric 1.0 (see blog) and even wrote our perspective on it. So what, Brian, should we expect going forward from Hyperledger?

Brian:Hyperledger Fabric version 1.0 is not the end but the beginning. We are already working on version 1.1 which is a logical progression from 1.0. We will also launch Hyperledger Sawtooth version 1.0 and possibly some others in the near future.

We are also starting to see a lot of collaboration between projects. For example, Hyperledger Sawtooth and Hyperledger Burrow are working together to run the Ethereum Virtual Machine (EVM). This kind of mixability is what we are working on all our projects. Over time they converge to tell the full story that is built under the same umbrella with the same legal framework.

Saurabh: So what’s your advice to enterprises regarding when to consider blockchain and when not to?

Brian:With every use case for distributed ledger technology, there is always a question whether it could be cheaper to do it as a centralized architecture. And the answer is yes! BUT: then you enable a central actor, and that is what markets want to get away from. The first question enterprises should ask is around how are they doing things now, and are the bottlenecks due to centralization? If you are paying a 1% fee or less, and the centralized actor is well managed and doesn’t also compete with its market members, then possibly blockchain is not the answer in the short-term. But if not, then you should go to your stakeholders and participate in a blockchain solution. I believe that every such scenario will go towards blockchain, but that is a 20-year vision. Right now we should be looking at the low hanging fruits.

Saurabh: There are lots of pilots and PoCs around blockchain, Brian, but rarely do they go live. What needs to happen for blockchain to become a reality for enterprises?

Brian: What we need to do is build confidence in technology leadership that blockchain technology can scale up to performance levels that enterprise requires. We have established a Hyperledger Performance Working Group which is a cross-project initiative to build a repository of test scripts, develop benchmarking tools, etc. to help IT leaders understand what the tune-able attributes are. A lot of Fabric 1.0 enhancements were around guaranteeing performance and improving DevOps such as assigning different roles to different nodes that are different from standard blockchain architecture but helps improve some latency factors.

There is a recognition to make it real, and we are putting a lot of effort into it. Projects like Hyperledger Cello (as-a-service deployment model) and Hyperledger Composer (collaboration tool) are also enabling adoption.

Saurabh:And finally, Brian, what’s your one wish for blockchain if you could make it come true

Brian:By an order of magnitude, more developers – a thousand more developers that are one year further down the learning curve. I talk to many companies on participation formalities, but the thing that I want them to contribute is developer resources to write code…I am not compensated by revenue targets, success for me is becoming the reference standard for distributed ledger technologies.

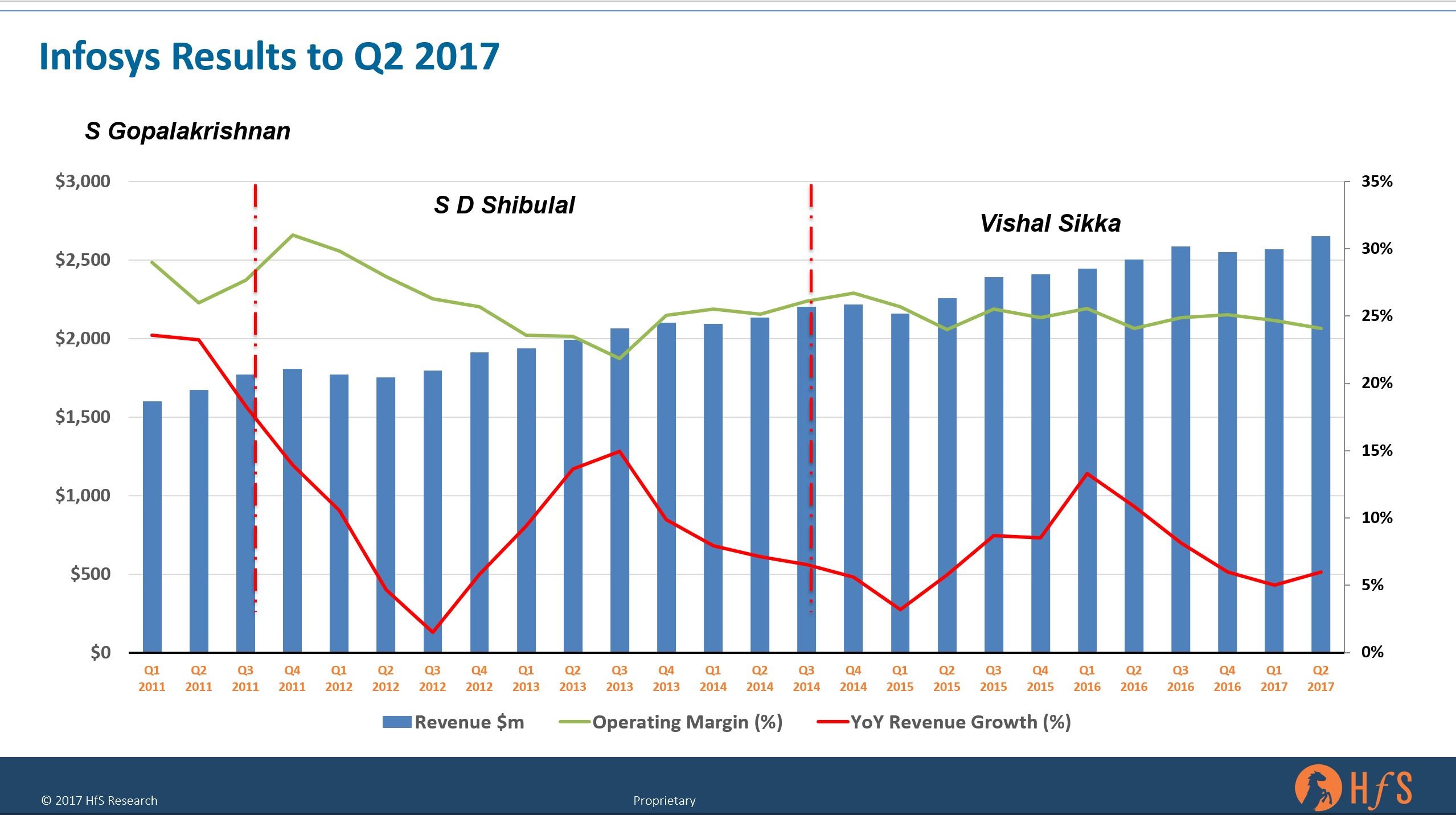

Once dubbed the “Indian Accenture”, being the Indian heritage outsourcer with the high-end reputation, the firm now finds itself enduring, perhaps, the most difficult period of its history – and it could be poised to get a hell of a lot worse.

Vishal Sikka brought energy, fresh ideas, hope… and a Silicon Valley mindset to its leadership when he came aboard amidst his Design Thinking and jeans-to-work attitude just three years ago. However, all Sikka’s energetic ideas and innovations have been largely forgotten over the past year, as the public spat with Founder Narayana Murthy gathered irritating momentum and completely slammed the brakes on the momentum Sikka had sparked. Sikka had woken Infosys up to its potential and the Founders were more obsessed with his use of the corporate jet than making the acquisitions the firm needs to be competitive.

From the poster boys for innovative offshoring, epitomized in Thomas Friedman’s seminal “The World is Flat” through to the constant public interventions in corporate affairs by Murthy, Infosys has had a bumpy ride over the last decade of its short history. And to magnify its issues, all of Murthy’s interventions have been played out in public, with the Indian press the grateful recipient of endless reams of news fodder being provided by this corporate soap opera.

Vishal Sikka’s resignation grinds to a halt this public transition from the Founders’ generation to becoming a “normal” corporate company. Without a doubt, this episode will find its way into economics textbooks for future students to learn the lessons in strategy, corporate governance and beyond. However, at least decisive action has been taken, and Murthy and his founders can try and restore a stability that ends this public drama. This is just a bad time to go through such a strategic leadership nightmare, when competition is at its most severe, with too many suppliers chasing too few contracts and margins under extreme pressure. This is especially troubling when you consider Sikka has kept the revenue and profitability ship progressing well, maintaining profit margins close to 25% and revenue growth over 5%, even at a time when the industry growth is flat and political stances towards offshoring are heated, with several US deals being awarded to “Western” suppliers:

So what are the lessons that can be learned from all this?

Murthy is the dominant father figure of Infosys and he has made that very clear with his actions. As founding CEO, he is synonymous with the early success, the culture, but more crucially, with the decision-making at Infosys. When SD Shibulal, another of the founders, took over it was difficult for him to step out of Murthy’s shadow. Shibulal’s “Infosys 3.0” strategy was designed to address the over-dependence on the US market (see interview) and rebalance the portfolio by building out IP-based platforms, namely the EdgeVerve portfolio. But he took also the bold step to sign the first Intelligent Automation partnership with IPsoft at the time. Yet, the sales engine continued to stutter which remained the dominant feature of Infosys recent history.

This provides the background to the stage on which Vishal stepped, when he was appointed CEO in June 2014 (see post). Vishal was not only the first “outsider” but more importantly not part of the Founders’ generation to take over the reins at Infosys. Being Indian, yet working in California with a strong product background from his time at SAP he ticked a lot of the boxes in order to return Infosys to its erstwhile glory as the beacon for innovation that Thomas Friedman had so eloquently and prominently described. Vishal’s strategy focused on aligning Infosys around automation and AI to re-emphasize the heritage in innovation and Design Thinking, but also to boost the balance sheet as the industry is going through the secular shift towards non-linear growth and outcome based offerings. This was underpinned by an influx of executives from SAP meant, in particular, to help drive the platform and product business.

However, the narratives around automation and AI were never succinctly explained and, more importantly, not driven consistently through the organizations. For instance, the teams at EdgeVerve were waiting for guidance from the teams at Mana and vice versa. Without consistent narratives, it was difficult for the sales teams to leverage those capabilities in client discussions. Similarly, Mana was announced with great fanfare as the answer to all automation challenges. What Mana actually is, is a compelling analytics engine. It took another Confluence (Infosys’ main customer event) this year to finally launch a holistic automation framework called Nia. But at this year’s Confluence, Vishal appeared to HfS as being despondent and at times disconnected leaving us to speculate that he might resign or be pushed to step aside. Yet, when he did at this conference an AI tutorial, he appeared to have his old sparkle back. Innovation and discussions with thought-leaders seem to be his passion. And his passion offered something different to an often guarded corporate world.

Undoubtedly, current clients will have questions about where this leaves them. Not only was the firm’s latest CEO the driving force behind the firms shift to analytics, automation, and AI, but Vishal’s appointment also saw the CEO’s office take personal responsibility for key clients in a bid to strengthen relationships and develop and solidify revenues from current client engagements. The whole corporate strategy will change dramatically, should the new incumbent come in with different ideas, and in the process likely shake and disrupt progress to solidify client relationships.

The Bottom-line: Re-igniting the sales and marketing engine is critical

Infosys has to reignite the sales and marketing engine and prove it has genuine distinctiveness when competing with the likes of Accenture, Cognizant, TCS, HCL and Wipro. Clients need to know what Infosys stands for, and why they should pay the top dollars to invest in this company, when there is so much intense competition making more impressive noises at present. While Vishal Sikka hit the ground running with a whole suite of ideas and innovations, these have largely dissipated over the past year amidst the public infighting. Without consistent financial performances, all the innovations will more or less evaporate and Infy will be left battling it out for low-margin transactional IT contracts. Infosys 4.0 (or whatever it ends up being called) needs a new dynamic CEO, it needs an aggressive sales leader, and a CMO that can articulate what the company is trying to do next and what it stands for. Merely parroting the insufferable fluff about digital and outcomes will not work – Infosys needs to lead India’s innovation, not merely to make up the numbers.

On the positive side, any incoming CEO will have a strong set of assets to build on, which have enjoyed significant investment. First and foremost, Infosys analytics and data management prowess, strong products including Finnacle as well as many automation assets integrated into the Nia framework. There has also been solid investments in its US delivery, most notably in Indianapolis and Texas. However, Vishal’s resignation is likely to complete the power shift back to Bangalore. Many of the California-based executives will either jump ship or be pushed out very quickly. The crucial question though is whether the group of Founders will continue to interfere in public or whether they finally take a back seat and demonstrate confidence in any incoming CEO and his executive team. If the latter is not being addressed, any new king will wear very old clothes.

I was recently given the lowdown on how amazing ServiceNow is becoming with the “integration of Watson and Chatbots into its core platform”. Sounds terrific, but does this added functionality really deliver huge value to customers when we examine the realities of their current business models? I would argue our industry has become so carried away with the promise of technologies we barely comprehend, we have taken our eyes off the real prize: working with customers to help them be more effective. We’ve got to stop selling the Ferrari, when their Volkswagen will comfortably get them where they need to be with the help of a routine service inspection.

I increasingly believe today’s “post-digital” market is much, much more about aligning services to customer business models than selling software with lots of bells and whistles – there are so many tools on the market that have 10-50x the functionality customers today really need with their current business models. Whether Ignio has more bells than Holmes or Nia, or whether anyone truly understands Watson’s capabilities, the key here is which suppliers can work with their customers’ business models to drive better automated processes, introduce more self-learning capabilities and smart analytics that can truly improve their businesses.

Net-net – we must look at everything through the customer lens:

1) Why should I care about ServiceNow? 2) What can I truly do with ServiceNow that can improve my speed to market, my customer engagement, my OneOffice experience? 3) Can ServiceNow really make me a smarter, more analytical operation, based on the people I have on staff and within my service partners?

Just adding software isn’t the answer, it’s about really understanding your desired business model and crafting the operations to sustain and support it. The service providers who invest in staff, that can really align business models to new tech, will win; software firms that can train those winning services firms to do that will win.

This is why Watson is failing to meet IBM’s lofty expectations – they’re selling solutions to clients that simply do not have the skills or experience to understand how to improve their current biz models with cognitive.

The Bottom-line: It’s time to invest in real consultative talent… or go home

Net-net – the biggest issue today is that these are solutions trying to find business problems, as opposed to clients having business problems who are looking to find tech solutions to get smarter. This should be about SOLVING existing problems first… Sadly, most of the problems today are too focused on people elimination that may not be feasible or financially viable.

The services industry needs to evolve to higher value consulting…. educating clients on the true business value of investing in solutions. But unless suppliers invest in themselves first to understand their clients’ real business needs, the ROI of investments like ServiceNow will never be realized. It’s time to invest in real consultative talent… or go home.

It’s time to close the chapter on the legacy analyst industry that has lost its energy, its identity, its independence and sense of purpose. HfS was founded seven years ago to shake this up, and what’s astounded us is the stubborn refusal of the rest of the industry to change, preferring to milk the remnants of a stale model. So we’ve worked very hard behind the scenes to develop a knowledge platform that impacts, with an engagement style that shakes our clients from their slumbers. Welcome to our ThinkTank…

Why is the legacy analyst industry stuck in a depressing holding pattern?

The analyst industry never made it out of 1.0. Despite all the guff about analysts using twitter and blogs, the sporadic number of boutiques and one-man/woman bands that slipped in (and out) of the analyst market over the last decade. Despite the “freemium model”, where there was a pretence of free research “disrupting” the market, but most of it being regurgitated supplier press releases. We are still trapped in the old analyst model:

Let’s face it, this current model has steadily deteriorated over the last decade, with most analysts firms selling their praise to willing vendor marketeers only too happy to fund the propaganda, adding increasingly damp fuel in vein attempts to heat up their sodden sales decks and watery marketing brochures. Even firms like NelsonHall, Everest, Zinnov and others have got in on the act of putting out endless scatterplot quadrants of supplier positions in all sorts of markets – as if customers really take this stuff seriously anymore? Is this the only way these firms can forge a living these days? How can you “influence” a market when your only impact is a few thousand quasi-human twitter followers, you don’t run customer summits, you don’t provide your clients with research labs, you don’t provide relevant data products and the only people you ever talk to are suppliers?

I would even go as far as declaring some of these “analyst” firms should be more correctly reclassified as supplier marketing support firms. How can you be an “analyst” when all you do is take money from marketing people to reinforce their products?

The current model is increasingly desperate, we now see tech suppliers buying up advance licences of Quadrants, Waves and Marketscapes at the beginning of their budget cycles, before they are even written, so they can pick and choose which scatterplots to buy licenses when they like the outcome. Yes, people, this really happens.

How did it get this bad? Simple – most analyst firms are just not very good. They are jaded, they are too stingy to invest in real talent with real experience, and just reel out the same old dinosaurs whose only value to industry is to market the wares of their paying customers.

Fortunately, we have started to see light at the end of this rather dingy tunnel. Which is about time, as there’s nothing more depressing than bemoaning a stagnant industry encircling the drain before its eventual plummet into the plug hole of irrelevance.

Don’t lose hope. Analyst 2.0 is finally here!

The industry is reaching its first major Come-to-Jesus moment, where growth is flat, there is mass confusion surrounding the real impact of “disruptive digital business models”, with the potential creative destruction of automation, the lack of clarity of the business benefits of cognitive and AI, and the blurry potential of blockchain in its nascent pre-industrial form. It’s well past time for enterprise customers, suppliers and other key stakeholders to come together and really collaborate and think about what their true options are moving forward.

But, all is not lost, folks, because HfS is kick-starting a new era in the analyst biz with the HfS Impact model. Let’s be honest, the analyst 1-800 hotline market, where you have to wait 3 weeks to talk to some clueless kid, and those strategy days when you got subjected to an endless deluge of dull slides explaining the basics of your industry that you were reading about in 2003, are fizzling out. No one cares anymore. No one bloody cares.

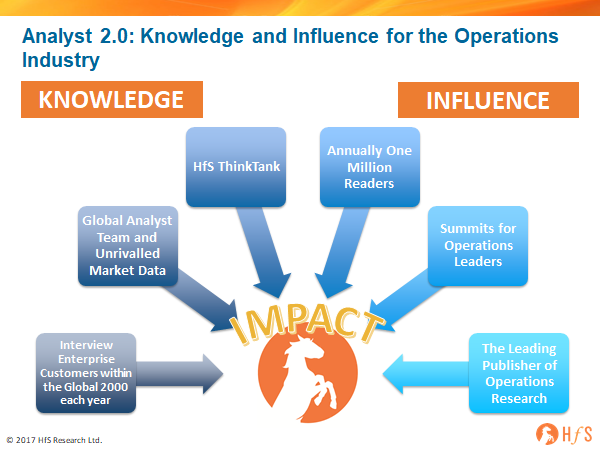

We’ve made it our mission to drag this business kicking and screaming out of these dark ages of obsolescence. So, welcome to Analyst 2.0, a model based entirely on Knowledge and Influence, centred around our revolutionary ThinkTank:

The ThinkTank approach is all about getting the industry collaborating again, where we use Design Thinking techniques to drive joint problem-solving. Our mantra is that the analyst role is shifting from passive observer to facilitator. To make this happen, we have dedicated an entire floor of our new offices in Cambridge England, in addition to facilities in Chicago and Boston, to hosting day long ThinkTank sessions with our clients. ThinkTanks are where we invite customers, suppliers and even advisors to spend entire days with us Design Thinking their desired goals, and solving the problems that are preventing their achieving these outcomes. This is where we challenge you, you challenge us, and we work together, supported by our research, to drive genuine achievement, defining where you need to go and clearing the path to get there. And yes, we lock all our phones away in a safe, while we drive this whole ThinkTank process. Learn more about the ThinkTank.

The Bottom-line: The HfS Mission is to Revolutionize the Industry and lay the Analyst 1.0 model to rest. For good

HfS’ mission is to provide visionary insight into the major innovations impacting business operations: automation, artificial intelligence, blockchain, digital business models and smart analytics. We focus on the future of operations across key industries. We influence the strategies of enterprise customers to develop operational backbones to stay competitive and partner with capable services providers, technology suppliers, and third party advisors.

HfS is the changing face of the analyst industry combining knowledge with impact:

ThinkTank model to collaborate with enterprise customers and other industry stakeholders.

3000 enterprise customer interviews annually across the Global 2000.

A highly experienced analyst team.

Unrivalled industry summits.

Comprehensive data products on the future of operations and IT services across industries.

A growing readership of over one million annually.

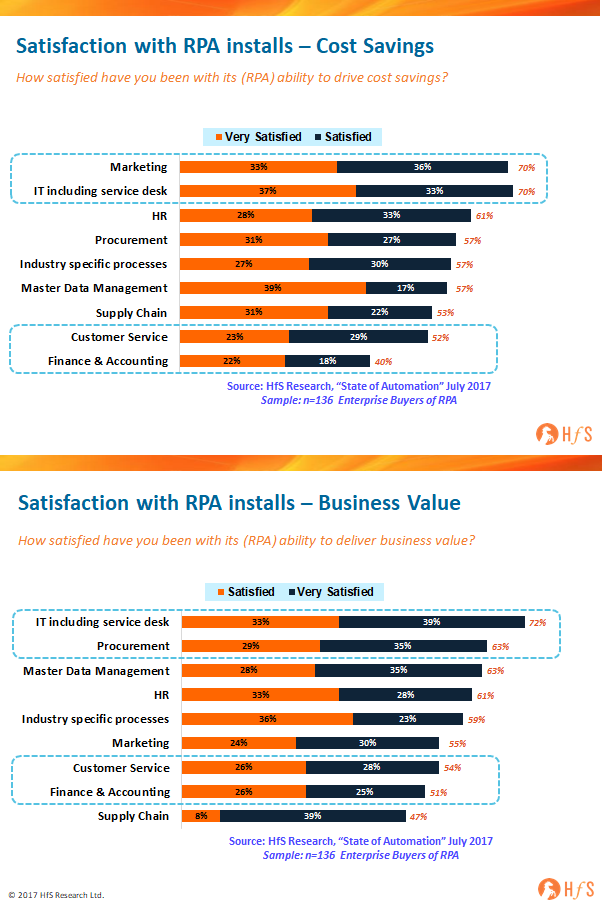

So we’ve determined that 58% of enterprises which have adopted RPA are satisfied with both cost and business impact (see recent post). But how does this differ by business processes?

Let’s consider this data:

IT processes and apps are clearly the biggest beneficiaries of RPA. There’s nothing like music to the ears of cash-strapped CIOs and CFOs than prolonging the life of those once-expensive IT systems that just don’t integrate with each other. Plus, isn’t it great to make band-aid patches over those spaghetti codes to keep those cobol monstrosities functioning for a few more years yet? Suddenly that “technical debt” doesn’t feel quite so bad. The thing about writing off legacy, means you really only write off the stuff that just doesn’t work anymore… RPA is highly effective at prolonging the life of legacy systems by recording actions and workflows to give these things a new lease of life, allowing for technology investments to be made elsewhere (read our recent example of NPower).

Marketing functions have a lot of unnecessary manual fat that can be trimmed. There is one function that perennially suffers from excessive manual work and real issues integrating systems and processes, and that is marketing. Simple tasks (or tasks that should be simple), such as linking together databases of customers, subscribers, and prospects to align with campaigns, collateral, automated emails etc., are the bane of every CMO’s existence. So… rather than spending millions on consultants to recreate new processes, CRM capabilities and training people to use them, why not get what you have working better, while you figure out where to make those really valuable marketing investments in the future?

Procurement can really benefit from process automation. One function that has been cut to the bone – and still uses the fax machine as a mission critical tool – is procurement. RPA has the most positive impact on functions beset by poorly integrated processes, where the goal is to get things functioning better, than those functions where the goal of automation is really just to drive out cost. Being able to link together procurement systems, analytics tools and cognitive applications with the manual work that still creates major breakdowns in speed of execution and quality of data, is a major benefit for those customers which map out an RPA plan and execute against it. The more you can use procurement to support the business and speed up the cash cycle, the more effective the function becomes. HR is somewhat similar to procurement, in the sense that the fat has already been long-trimmed from most companies, and RPA adds value to processes in similar ways, such as supporting better analytics and linkages between legacy systems and processes. Payroll, in particular, is emerging as a major area where RPA can have a huge value impact, where all the critical employee data is housed and can be integrated with other knowledge systems to support better decision making. Another area is recruiting, where the whole process can be massively transformed simply by linking together actions, databases, social media, OCR etc. RPA can provide a great temporary fix while companies figure out where they really need to invest in the future – and “temporary” could mean a very long time indeed…

Finance and Accounting disappoints from a cost take-out standpoint. With only 40% of enterprises satisfied with the direct cost impact of F&A, we can conclude that many of them have their expectations set too high that RPA will drive short-term headcount elimination. On a more positive note, half of them are happy with the business value impact of RPA on F&A, so clearly there are process improvements, just not enough to remove the human cost of administering them immediately. Considering F&A is the number one process being used for F&A today (it dominates 50% of installs) it’s clear that the suppliers are playing the cost take-out game too aggressively and leaving many customers disappointed. As with outsourcing, it’s one thing separating tasks and removing workload elements from staff, it’s another being able to remove headcount simply my improving or digitizing processes. Customers must take a more transformative view that if they can free up 50% of an employee’s time, they need to focus on refocusing her/him on alternative activities. That is where the value is to be found.

RPA satisfaction in Customer Service functions is mixed. For a function that can truly benefit from intelligent data and digitized processes, it’s surprising that barely 50% of customers are experiencing either cost or business value benefits from RPA. The reason for this is two-fold: firstly, customer service functions are too mired in the legacy practice of managing shifts of low cost agents, whether they are inhouse or outsourced – and have little time or funds to investigate the value of RPA, which may require upfront investment and longer term planning. Consequently, with this short-term mindset to cater for, most the call center BPO suppliers have little pressure to change how their sell their services, if their clients are not clamoring for RPA solutions. While we are seeing significant interest in chatbots and virtual agent solutions, and established automation vendors in the call center space, such as Nice, have established relationships with many customers, the whole call center space seems to be lagging behind other functions when it comes to embracing how to leverage the benefits of RPA effectively – which could be significant when you take into account the dysfunctions across customer interaction channels.

The Bottom-line: RPA satisfaction is a lot higher when the motivation and mentality is one of process improvement, not cost-elimination

The main issue with RPA, in today’s market, is this misconception that customers will make significant headcount reductions in the short-term. With outsourcing, the cost savings are staged carefully over a 5 year engagement as work is moved to cheaper locations, better technology and processes are introduced, in addition to automation, and the processes are re-mapped over time to allow for work to get done, ultimately, with less people. Simply plumbing in RPA and not having a broader plan to transform the work, pulling several other value levers, in addition to the patching of processes and digitization of manual work, will likely result in a mismatch between expectations and reality. RPA needs to form part of a broader strategy to automate and streamline work, where people, processes, analytics tools, SaaS platforms, outsourcing models and carefully developed governance procedures, are taken into account as part of the broader transformation plan.

Infosys has announced the acquisition of the UK-based design-thinking firm, Brilliant Basics, and if it plays out according to the name, it is exactly what Infosys needs to bridge design to execution and impact. The acquisition brings in a digital, strategy, and customer experience design capability, a global studio network, and brand name credentials including HSBC and INSEAD (online education experience) as well as new startups like CBI bank (business strategy and omnichannel touchpoints). These are all valuable resources to Infosys and its clients, but what the service provider has had real challenges with is addressed in this quote from the Brilliant Basics web site – a framework and resources for scale:

“Our deep experience in working with talented people in the areas of service design, user experience and technology has allowed us to create repeatable processes for building digital products and services.” – Brilliant Basics

Infosys committed to training internal resources and using design thinking but faltered in scale and consistency

Influenced by CEO Vishal Sikka’s interest in design thinking, Infosys introduced human-centered design into its digital transformation methodology called AI KI DO, which receives positive feedback from clients. And, through Zero Distance, Infosys provides a framework for account and service delivery teams to work on getting to know their customers, ask questions, and make suggestions for change. Infosys is also using design thinking to help companies identify new growth opportunities and to change its own operations as the company grew fast and got a bit stuck in the “old ways” of hierarchical, process-centric decision making. (Read further: Is Infosys Stretching Past the Growing Pains?)

However, while Infosys partnered with Stanford d.school, brought in leaders with deep design expertise, and aggressively trained its leadership team and workforce on the concepts of design, it has not been able to address three challenges that stood out in the evaluation we did earlier this year on the use of design thinking to help reorient and/or transform business operations for impact on business outcomes:

(1) project management;

(2) moving from design to execution, identifying opportunities for reusable assets to scale; and

It looks like the design approach of Brilliant Basics and the influx of design and customer experience experts could help address the gaps.

This type of acquisition is overdue by Infosys but it is not too late and shows its commitment to integrating human-centered design

Even though Infosys was one of the first to appreciate the value of design thinking for human-centered service design, other service providers moved faster to acquire and integrate design firms into their companies to bring in skilled resources and re-orient their methods and cultures (see: How design thinking plays an integral role in outsourcing, service design, and delivery). This work is still underway, though, with only early results and impact. It’s still not “par for the course” with any service provider yet. Infosys needs to focus on integrating Brilliant Basics into the organization, the culture, and the sales and delivery, quickly. This will be a challenge as Infosys has not done many acquisitions, and this one is very different from the traditional Infosys.

Bottom line: Brilliant Basics could be exactly what Infosys needs – the ability to manage and scale innovation. It appears to bring the kind of project management capability and design-to-action methodology that has been a missing link between the design expertise Infosys has hired and the solid engineering and service delivery capability it’s developed over the years. Infosys needs to put a strategic focus on bringing this one into the fold in a way that builds on and out these capabilities that can help realize its vision to partner with its clients in a more consistent innovative and meaningful way.

At HfS, we hear quite a bit about the challenges of incorporating RPA and AI into business operations, so when I spoke with a healthcare operations leader about his experience at a U.S. healthcare payer recently, I wanted to share it… but can only do so anonymously. Here’s how RPA first – and AI down the road – is being incorporated into the business operations, by defining appropriate scenarios, thinking outside the box, managing proactive communications with staff, and looking to get people excited about the positive impact on jobs, relationships between payers, providers, and patients and healthcare consumers and on health, medical, and financial outcomes.

What is the use of Intelligent Automation in your organization today?

We are building momentum from our business case into implementation with robotic process automation (RPA) and defining a conceptual “bridge” to get into artificial intelligence (AI) – what is the use case and how to use to impact financial and medical outcomes.

Where and how did you get started?

Started by looking at RPA to drive additional efficiencies from labor and financial perspective and then realized that the organization needed to be considering a broader strategy. It isn’t just about the technology but how does it change the experience of the internal employees and the health plan members directly? We have a plan that we are iterating as we go… as we learn more about the capability and the potential impact. Using RPA and AI can change our internal processes and free up talented staff. We can change the way our employees interact with members, providers, and patients in a way that changes their experience and medical and financial outcomes.

How will employee roles change when RPA is introduced?

RPA – and eventually AI too — will free up our employees to engage more directly and interactively with our stakeholders such as healthcare consumers and clinicians. For example, today, the provider office has to fax authorization and wait for response. How can we use RPA and AI to ingest the form on a front end web site, have an algorithm that runs to identify “we always provide authorization for this service” and flip it back in seconds; or if not, route it for the appropriate review. This kind of intelligent automation frees up the care management team to do something more important; and hopefully, that translates into relationship and outcome uplift for the provider, member, or both.

Employees who are processing claims and reviewing authorizations, for example, have interactions and engagement with members, providers, and patients that are reactive and responsive. We could get in front of these same people more proactively if those processes and reviews were automated and only potential denials or exceptions were flagged. These employees could be reaching out, instead, to discuss a pended claim or questions about authorization. Our hope is that “in a year or two, we can shake our heads and say, wow, we used to have hundreds of people who are now creating personal interactions instead of processing behind the scenes.”

Who in the organization do you need to work with and how does that play out?

First, we had to go through a process with the enterprise architecture team and get approval to proceed. We are working with a service provider who helped define the scenarios and evaluate the technology. We then moved forward with a proof of concept that showed what we could deploy around claims payment and pended claims, the business story for our business unit colleagues. Then we laid out what is RPA and AI and demonstrated how it works—how you could address a claim that 15 people used to work on full time just for one fall out. It resonated. Over the years, I have had to advocate for software that we were excited about – rarely have had to sell a product or idea where the senior level is buying into it before the grassroots technical effort. That was the case here. The executive team could see the opportunity and get enthused about it.

How is the move to intelligent automation and “digital labor” impacting your workforce?

From a technical perspective, our CIO team is working through the details. As the senior leaders get excited and then go into the team to talk to subject matter experts to codify RPA based solutions, the employees are concerned that their job is going to be automated and eliminated. You have to be able to tell the story to help employees understand that what is being automated is this routine action you do in the back shop today – that here is an opportunity to parlay your experience into interaction and impact with the members, providers, and patients. It’s a dialogue that is playing out pretty well.

We believe that as we move services people to working more directly with the providers and members, they will be performing work they will find more enriching. We also realize that we need to understand what skills and capabilities are needed for this. We are building out a robotic operating committee and working with business leaders to talk about – as we deploy these solutions and staff becomes available for different roles, what are those roles and what capabilities do people need for them. And we don’t want to move them into doing work that will be automated “next.” We are in early stages here. So far our efforts with intelligent automation have been grassroots with excited senior executives how have said, go into my organization and show me how it works. As we get scale, we will work through retooling.

Tell me about how the funding and business case development is coming along.

Our organization is quite rigorous around investment. When we talk about RPA and provide evidence of 4:1 and 5:1 return on investment the story becomes easier. We are always focused on continuous improvement and how that parlays into impact. Again, the story of using automation to free up skilled staff is powerful. For instance, in finance, changing manual reconciliation at the close of month with large team to be automated and the more complicated work being the focus of the human effort, the logic becomes more apparent and the investment, obvious.

From these “early stages” of about 12 months in, the momentum and excitement is gaining, and I anticipate that we will pick up speed with RPA and into AI over the next year with top down sponsorship. What excites me most is the possibilities of what we can do to free up our own employees and at provider offices to anticipate and be more proactive about issues and concerns and eliminate bottlenecks and slow downs for higher quality service and interactions.

Bottom line: While this interview is a bit like the old dating game where one person asked questions and the other sat behind a black curtain, it helps shed light on how enterprises that have been working one way for so long are making progress in moving forward with RPA and AI, considering talent and technology and how it changes the way we need to work going forward in healthcare operations.

The HfS’ Blueprint reports are our temperature check of an industry. A guide to some of the trends that are already in play, and those starting to bubble under the surface. We have just launched the first in our series of IT Services reports focused on Infrastructure Services, and it’s some the trends around this research we’d want to shine a light on today. Of course, if you’re interested in all of the market information and dynamics covered in the research, you can get your hands on a copy here.

The industry breaks with tradition

When we talk about infrastructure services, the mind immediately jumps to build and manage or “lift and shift” engagements. Indeed, for a long time, it was this type of work that was the most in demand and lucrative of providers operating in the space. However, this is no longer the case as businesses seek to secure more holistic IT Services to support their digital ambitions. As we researched the mechanics of the infrastructure and enterprise cloud industry, it became apparent that providers are breaking with the traditional services and models they used to thrive on, and are seeking to focus on higher-value transformational activities instead. For some providers, this is more of a pivot, as they grapple with providing traditional services as well as new ones. While for others it is a more decided and strategic shift, in which “lift and shift” engagements are avoided entirely in favour of juicier transformative projects.

Our expectation is that this will transform the way some vendors pitch their infrastructure services completely. Polarising some to either end of the spectrum – those focused on high-value transformation, and those solidifying their position in at the traditional end. Somewhere in the middle, we’ll see some of the larger firms, capable of spreading themselves across the spectrum to handle a broad range of engagements.

Service Brokerage enables firms to become a one-stop-shop

Another dynamic, undoubtedly linked to the commotion caused by an industry pivoting and refocusing engagement models, is the decidedly increased role service brokerage plays. Many firms are moving toward semi-impartial and fully-agnostic service brokerage models to enable clients to secure best-in-class services through them. Many firms are moving toward semi-impartial and fully-agnostic service brokerage models to enable clients to secure best-in-class services through them, allowing them to offer a one-stop-shop for sourcing services across the IT spectrum.

However, some firms will find this easier than others, particularly those who have invested considerable sums in building proprietary technologies. For these firms, balancing the incentive to protect investments and assets against the industry shift to brokerage will be tough. But potentially necessary if client expectations set the pace at the agnostic provision of best-in-class services.

As this trend develops, we can expect to see larger and more tightly woven partner ecosystems in the space. Alongside increased activity from vendors trying to prove their credentials to partners in a bid to take relationships to the next level, while articulating their brokerage credibility to clients.

Consultancy-led engagements focus on business outcomes

The two preceding trends have the potential to completely alter the dynamics of the infrastructure and enterprise cloud industry and, indeed, IT Services as a whole. In part client expectations and demand are leading these challenges as business scream out for services and solutions that meet their digital and operational ambitions. Of course, businesses vary considerably, and the suitability of one IT Service offering varies accordingly. Leading to another shift away from tradition, as providers seek to deploy higher value solutions that tackle the core of a businesses problems.

We can see this trend play out in various ways – such as evolving pricing models that focus on business outcomes – but there’s another way that paints an encouraging picture. A picture of an industry refocusing its engagement model away from core, unadaptable services and towards the design and implementation of those which tackle a particular challenge. At the forefront of this shift is the increased focus on consultancy-led engagements that seek to understand a business and its challenges and objectives.

Approaches like this will be necessary if firms are to thrive in the changing marketplace. For example, it’s only through understanding a client’s needs that a provider will be able to select and recommend the right services through its brokerage model or if the firm is to assess whether the engagement fits in with their model and approach.

As this trend develops, we can expect to see firms shoring up their consultancy brains and brawn to support engagements across IT Services from initiation to completion.

Bottom Line: Trends impacting the infrastructure and enterprise cloud industry signal a potentially turbulent future albeit one packed with opportunity for dynamic and agile providers.

{kind=link}