We’ve run twenty leadership summits at HfS over the last few years and am sure most of you who’ve been to some of them love the candid conversation, the zero-selling ethos and absence of plastic booths and cardboard PowerPoint presentations. However, what most people haven’t realised is we’ve never dedicated staff to running these fulltime, and all we really had to do was invite our network, put together great people to speak and provoke some terrific debates.

However, we really want to start having a series of intimate regular roundtables across New York City and London, where we can drill into the hot topics du jour that we all love so much, such as Intelligent Automation, Blockchain, the Digital OneOffice etc. But to do that, there are precious few characters in the world who have the tenacity, network and charm to make these happen… and we managed to snag one of the very best, Steve Dunkerley (see bio), to run these for us.

I have known Steve for 15 years and have always enjoyed some of his terrific CXO roundtables, where he has this uncanny knack to bring some serious hitters together in one room. So when we had the opportunity to bring in the best guy in the biz to lead our summits and roundtables, we had to convince him join the HfS family and not rekindle his karate career…

Steve – it’s just terrific to be working with you at HfS after all these years! Can you share a little about your background and why you have chosen C-Level events, research and strategy as your career path?

Hi Phil, it is a pleasure to join the HfS family.

In terms of my background, my life really began in 1999. This was the year I met my wife to be, got married and started my B2B media career having earned a degree in communication studies a while before that.

From 1999 until the end of May this year, my employer was the company that is now known as Compelo. I was initially responsible for industry specific publications in the textile, water, food and MedTech sectors. Then in 2005 my attention turned to the office of the CFO with FDE (Finance Director Europe) and its sister title Future Banking.

My role was initially commercial, whereby I positioned providers alongside appropriate commissioned content. Then I became more focused on editorial strategy across multiple media, whereby I sourced and interviewed CFOs on a particular topic and then brought them together in a briefing or roundtable setting. I have organised dozens of these types of events across Europe and have had the pleasure of introducing top CFO speakers such as Graeme Pitkethly (Unilever),Iain Mackay (HSBC), Laurence Debroux (Heineken), Natalie Knight (Arla Foods), Koos Timmermans (ING), Andy Halford (Standard Chartered), Brian Gilvary (BP), Imran Nawaz (Mondelez Europe and soon Tate & Lyle) and most recently Gilles Bogaert (Pernod Ricard).

Aside from the thrill of bringing leaders together for them to share their pain points and ideas, I also enjoy hearing about the personal and business victories that were a direct consequence of attending an event.

So why did you choose to join HfS… and why now?

Well Phil, aside from your mastery in persuasion, outsourcing, automation and digital have been a reoccurring theme at my events, so moving deeper into this space with a research firm like HfS was a logical choice for my career path.

What distinguishes HfS from the competition is its pioneering nature in addressing topics before anyone else, as well as its reputation in the market. For example, it seems that most of the press releases or magazine articles I read concerning IT or BPM services typically features HfS’ opinions before any other analyst. Also, on a number of occasions at my events, speakers have actually referenced HfS statistics in their presentations.

While I chose HfS, you of course chose me too. It’s always a two-way thing. I’d like to think that when you have spoken and moderated at my events, you have been hooked by the event experience – especially in terms of the seniority of the participants and the quality of the content.

So where is the industry right now, Steve? Do you see us in a transitional state, or is something else bubbling to wake us all up?

Looking at the service providers, it used to be all about who had the biggest headcount to serve clients from a labour arbitrage perspective. As headcounts haven’t really receded despite the potential job displacement associated with the RPA & AI movement, I definitely see the industry being in a transitional state. Enterprises seem to be still applying RPA in a tactical way for very specific tasks. That said, there is massive interest in these type of change agents judging from massive audiences you have been speaking to at the recent Automation Anywhere “Imagine” and Blue Prism World conferences

This, together with the what I have also been hearing from CFOs at my recent events and the compelling messaging from the vendors via HfS POVs, it’s only a matter of time before things take off. Many CFOs are very excited about the potential of blockchain to revolutionise operational finance, so I see this one bubbling away nicely and is one of the topics that personally interests me most at the moment.

So what can we expect to see from you at HfS… can you give us a little snippet of what you’re going to be working on as you develop our FORA Leadership Council, roundtables and summits?

One of the key objectives for me is to assemble a council that is made up of enterprise leaders that are in tune with the OneOffice framework as well as domain experts in areas such as blockchain that can move the conversation forward. For this I will work in collaboration with Karel Franchois, who is in charge of the FORA membership programme, which is an annual subscription service that has been designed to enable enterprise leaders to have access to the HfS blueprints and data as well as join the exclusive ‘invitation only’ events throughout the year for a nominal fee.

At the recent FORA Summit in Cambridge I was delighted to have invited leaders from two of the biggest companies in the area to be the keynote speakers. Tim Pullen, CFO, arm and Steve McCrystal, VP GBS at AstraZeneca both provided some great insight as to how their operations are evolving in a time of rapid growth and digitalisation. I also managed to interview them both before the event to and hear first-hand about the journey they have been on Click here to read my interview with Tim.

For the remainder of the year and in 2019 I look forward to working with you in order to help assemble another stellar line-up for the New York FORA Summit in December and the London Summit in March 2019. I am also pleased to confirm the leadership roundtables are starting to take shape with one scheduled for 17 October with you and Derk Erbé at the helm.

For those FORA members that can’t attend the events, I will interview as many of the speakers and participants as possible either before or after the event and share content that can keep FORA members abreast of what was discussed. I also want to involve HfS analysts in content creation, so one example of this is a video interview I am planning with Sandy Khanna, Managing Director, Group Business Services from BT in collaboration with Elena Christopher from HfS, who has just published an in-depth Telecom Blueprint. Sandy will be joining the roundtable on the 17th October, so I look forward to welcoming him and 14 others to this exclusive event as well as collaborating with the new HfS digital content lead, Hannah McBeth to drive useful output.

And finally, is the analyst industry as exciting as it was 10 years’ ago?

10 years ago, analysts were the gatekeepers of the most desirable enterprise information – they were the popstars of content. This is also true to some extent today, although the democratisation of information via public blogs, google and freemium access to HfS – for example – has levelled the playing field. That said, the digital paradigm is moving at a tremendous speed and is getting ever more complex, which means the analyst is always going to be in demand – breaking down the complexity and serving clients in a more sporadic ad-hoc basis. If anything, quality analysts who can simplify the big, complex and (sometimes) thorny issues are more valuable than ever – but they need to demonstrate real enterprise use cases and clearly define the market, not add to the confusion!

Welcome to the analyst community, Steve – am sure you’ll find HfS a fascinating laboratory for observing the next phase of this industry!

We’ve now seen three pretty small software firms demonstrate 20x valuations… Blue Prism went public on the London Stock Excheng, UiPath received $150m in series B funding and Automation Anywhere has now announced $250 in series A funding. So it’s pretty clear there are three established leaders at the front of the RPA market and investors are convinced that RPA is the start of something much bigger for enterprises. Not only that, it’s becoming pretty clear that the barriers to entry are high, and we’re unlikely to see new players bulldoze their way into this space in the foreseeable future. So why is this?

RPA is kick-starting the true digital journey for many enterprises by helping create a digital process baseline

People love to espouse that RPA has quickly become commodotized and we’ll barely be talking about it in another year, when we all suddenly become experts so good at building algorithms, we can actually train systems to build their own algorithms on the fly. Suddenly, RPA will be some pervasive capability that is so devoid of value, it will disappear somewhere into insignificance. Utter garbage: anyone who’s got deep into RPA and tried to incorporate it into processes knows immediately that this type of thinking is naive, and likely coming from someone with no experience of the real world outside of their ivory tower. Firstly, RPA and RDA are not apps you sell to IT people to “rollout”, they are low-code solutions, designed for business operators to replicate, fix and digitize their manual processes, or scrape “static” data from screens to integrate into a dynamic workflows. And secondly, “low-code” does not mean “no code”. Talk to anyone with RPA battle-scars and they will tell you about the amount of code customization that was needed in certain areas.

Digital today is all about an enterprise being able to respond to the needs of its clients as an when those needs happen. Today’s RPA and RDA provides integral building blocks that digitizes processes to enable businesses to process the data they need to have business operations support customer needs in real-time. Sure, they may simply be performing dumb tasks, such as running process workflows in recording loops, or scraping data from screens into automated scripts.

The commodization of RPA breeds familiarity – and familiarity breeds innovation. The market is already established

Commoditization is good for bots, but remember that most enterprise folks have had to train to use the products and we already have very loyal followings for AA, Blue Prism and UiPath. The tech needs to be simple, low-code and easy to install, scalable and manageable. Noone wants highly customized solutions these days, so please do not confuse the devaluation of commoditization with the value of familiarization. You think Workday and Salesforce are not “commodity” apps? They are successful because they have crushed their markets through effective channel relationships, the creation of cult-like followings and years of building familiarity with their customers. I’ve even heard of HR people threatening to quit their jobs if their firms refused to invest in Workday – it’s an important part of their entire career path. You think you can’t find quality alternatives to Saleforce, such as ZoHo and Hubspot that are lower cost and even better in some areas, or likewise for Workday with SAP Successfactors and Ultimate? I predict we are already settling on AA, Blue Prism and UiPath as the RPA platforms of choice, as so many business users have already been through the pain barrier of training to understand the whole RPA paradigm. We’ll actually see more “micro-solution” firms, such as Thoughtonomy, which is building a service layer over Blue Prim and reselling that solution with positive results. Another example is Antworks, which is impressing a lot of people with its data ingestion capabilities and integration with automation needs.

AA, Blue Prism and UiPath already have 700-1000 customers each (depending on what you believe) and have energized many new careers for many people – it can take a couple of years for non-IT people to really learn these products (and many experiment with at least two of them). This market is only going to get stronger and more robust over the next three years – and beyond that, it’s really all science fiction as we observe the speed of development and macro changes to our business environments. Like with all other technology-driven markets where the key stakeholder is the business executive, once they are familiar with a platform, getting them to retrain on something else is a massive effort. Remember WorkFusion’s attempts to offer “free RPA”? People don’t want something just because it’s cheap – or even free, they want some skin in the game.

The Bottom-line: Today’s “Dumb RPA” provides a baseline for the development of intelligent bots in the future

You have to start somewhere, and for enterprises fixing their manual process messes, these three tools have provided the answer, with 70% of Global 2000 clients now expressing satisfaction, according to our new 2018 State of Operations study results. However, if these firms rest on their laurels, this market dominance will be short lived. Once the digital baseline is created, enterprises need to create more intelligent bots to perform more sophisticated tasks than repetitive data and process loops. Basic digital is about responding to clients as those needs occur, while true OneOffice is where enterprises need to anticipate customer needs before they happen (see below). This means having unattended and attended interactions with data sources both inside and outside of the enterprise, such as macroeconomic data, compliance issues, competitive intel, geopolitcal issues, supply chain issues etc.

So we have some clarity for now with three dominant solutions, and enterprises can invest more in learning these tools with more certainty and peace of mind. Some stability, after so much change in the world of business operations, is more than welcome. Now let’s hope these firms will wisely invest in taking their products into the world of intelligent bots, and not splurge all the newfound capital on yet more sales and marketing.

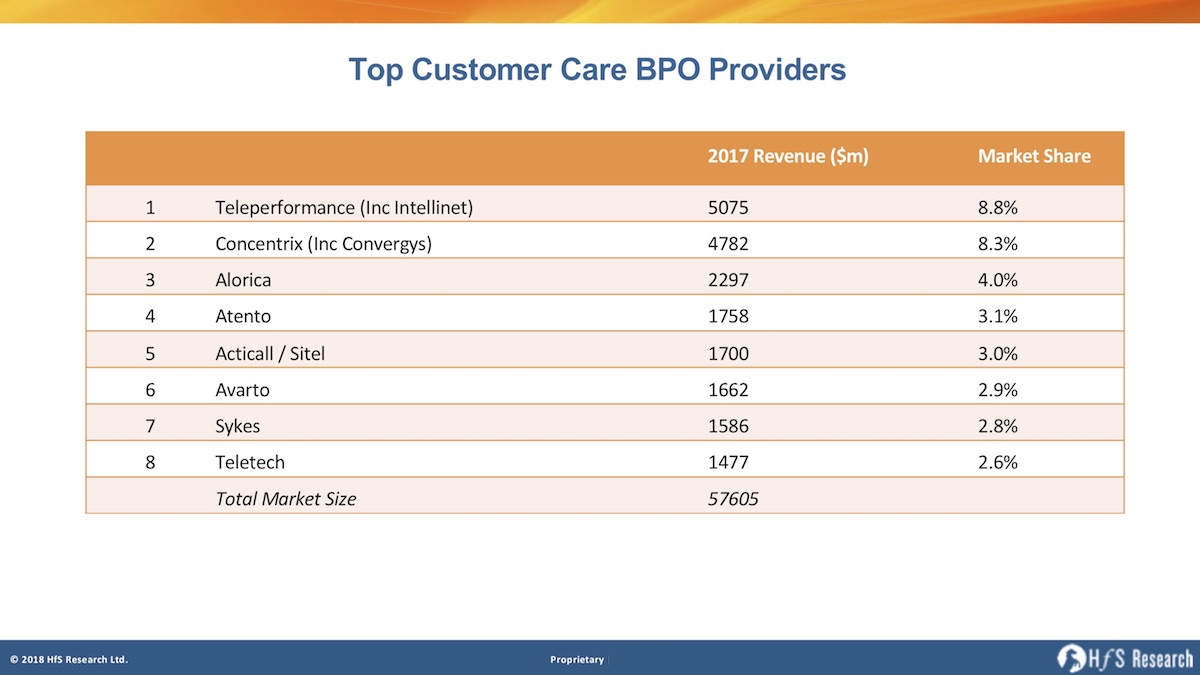

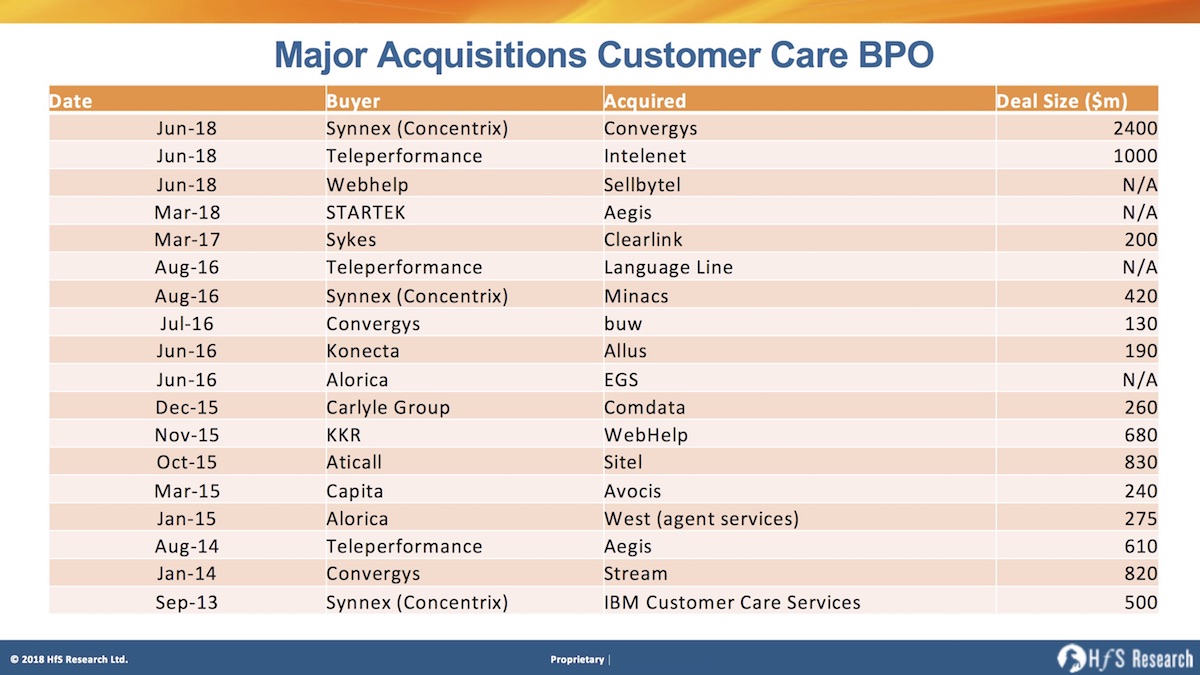

One of the worst-kept secrets in the world of call centers finally went from gossip to reality as Synnex Corp added Convergys to its acquisition portfolio to roll under Concentrix. As we covered here in 2013, IBM spun out its call center business to the Concentrix brand and – almost five years on – will merge forces with Concentrix under the leadership of Chris Caldwell (recently interviewed here).

So, from 10,000 people (just 5 years ago) to being very close behind the market leader, let’s see how the call center market is shaking out right now:

Let’s just get right to the nub here… what’s good and not-so-good about this lovely marriage?

Pros

The price tag is extremely attractive – especially when compared to $1 bn for Intelenet, which is a much less heritage firm in the market. At these investment levels, this appears like an amazing deal for Synnex, especially with its track record of making sound investments over the past couple of decades.

We now have a very strong rival to Teleperformance at the top of the market. If Teleperformance had made this move, it may have been game over for a lot of these firms.

Convergys was stuck and needed a new direction – and here is one with an exciting young firm. Convergys is a great, traditional contact ctr firm, very dedicated to its craft, but has been hurt by low-cost competition and struggled to maintain its edge in recent years.

Scale can be priceless in a commodity market. When an industry is commodotizing like call center, it’s often better to operate at a larger scale, so you can ringfence your legacy business and invest in strategic clients who want to work with a co-investment mentality. Geographical expansion and diversification will help the merged entity drive greater cost synergies and variety for clients.

Similar business ethos. As both core contact center service providers, both have a strong global operating model for consistency of services as well as a training and employee-focused culture. The challenge will be integrating the two together, but are generally aligned in terms of employee centricity and ops excellence.

Convergys has a very loyal client base that identifies with the firm, its culture, understanding of call center agents, and its understanding of their needs.

Microsoft partnership. Convergys has a very promising partnership with Microsoft and capabilities to harness Cortana and other apps. CNX will need to nurture this relationship.

Good technology assets. Convergys brings a solid IVR business and some very popular agent portal platforms.

Gives Concentrix strong market visibility and helps shed its “we used to be IBM” tag. For Concentrix, this could help them carve out the message of what they’re doing and want to be in the market. For Convergys, lends some sense of direction in the post Andrea Ayers era.

An injection of fresh thinking and new ideas. Chris Caldwell has a terrific opportunity to take his ideas to a very significant level if he can get this right, especially with acquisitions such as Tigerspike in the digital design space, and Minacs in marketing analytics and support. Chris has a bold view of where the industry needs to go – this should be a terrific challenge for him and his team.

M&A can buy time to take control in a commodity marketplace. Large mergers like this create the perfect distraction to make some discreet investments, keeps the shareholders at bay for a few quarters and can (potentially) help them focus on retooling the offerings and sharpening the whole approach. However, this depends entirely on decisive leadership and swift, focused transition and very strong communication to investors and shareholders.

Cons

Is bigger really better? This acquisition seems to be more about bolstering scale and size, with Convergys having little to show in terms of proprietary IP or differentiated offerings (Contrary to Concentrix’s investments in Tigerspike and Minacs). However, in a market that has been largely stagnant for years, any movement like this can help shake things up.

Convergys lacks a diversification in clientele with AT&T/Comcast being an enormous piece of CVG’s business. Telcos are typically the epitome of butts on seats deals—why choose a company that’s practically half telcos? Maybe this explains why the price was so attractive.

Client overlaps in large accounts will impact some revenues, i.e. Cisco.

The potential for culture clash. Concentrix comes out of IBM business and Convergys is essentially a traditional telco out of Cincinatti Bell … one has a background of tech and innovation and the other a very conservative and risk-averse culture.

Convergys’ revenues have been decreasing the last couple of years. Call volume fluctuations and trying to compete with cost-focused customers and several butts-in-seats service providers in low-cost geos, has made it very challenging to focus on value-based deals.

Desperate mid-tier providers. Many of the midtiers service providers may make the whole situation worse, by forcing price points even lower out of sheer desperation. Let’s be honest, we’re in a rat-race and the game is all about who can survive the next 18-24 months to emerge ontop.

Low-cost IT/BPO offshore providers making subtle moves into the contact center space as digital customer needs accelerate. We’re already seeing many of the Indian heritage firms chasing after call center deals they would not have looked at a couple of years ago. They can be especially effective with “chat-only” engagements and with clients wanting to buy into a strong cognitive / automation story. Large IT-centric outsourcers, such as Techmahindra, HCL and Cognizant have been seen picking off some impressive wins with clients, especially where there are very strong IT elements. BPOs such as EXL and WNS have been much more active in the customer service segment, and EXL is making an impressive repositioning of itself as a digital intelligence provider, with some impressive depth in insurance, utilities and healthcare sectors.

The Bottom-line: As long as this “traditional consolidation” is short-term, this could pave the way for a OneOffice future for the winning contact center providers

Let’s cut to the chase here – Convergys is a great call center provider, but lacked the leadership and investment to break into the digital era effectively. This merger may just provide that opportunity for a very talented employee base with a terrific customer culture. For Concentrix, they needed one big play to get up-close-and-personal with Teleperformance, and this is the move. Plus, the price was really damn good, and we’re surprised why others with huge financial backing didn’t make the move, such as Sitel or Arvato.

On the negative side, these contact center heavyweights appear to be doubling-down on size and scale, rather than pursuing a true OneOffice vision for digital customer engagement. We are more excited about some of the smaller acquisitions happening in the space, such as Webhelp’s recent Sellbytell acquisition from Omnicomm and SYKES’ pursuing digital marketing with Clearlink – connecting the pieces in the front office as marketing, service and sales continue to overlap and converge, and using the vast amounts of customer data they process to better engage with customers.

The large contact centers can’t seem to get out of their own way—they talk about providing digital, analytics and CX consulting focused services, but the reality is that the bulk of their business is still traditional contact center. Despite some real capabilities, salespeople aren’t incentivized to sell a different way, and customers aren’t ponying up to partner and buy a different way. Continuing in this paradigm is a short-sighted view… look at what is happening with eroding revenues from the telco sector now, the most mature of the contact centers will eventually happen in other sectors, such as retail and banking. In addition, the wave of “chat only” deals are increasing and threatening the life out of the traditional voice business. Providers like Teleperformance and Concentrix don’t have to disown their core business – there’s always going to be a huge market for traditional interaction management, however, adding some truly differentiated digital offerings would be a much smarter long-term strategy.

Net-net, this is a massive coup for Synnex and the Concentrix management teams – and Convergys has found a good home to focus on the future with confidence. However, we would like to see some significant investments in intelligent automation and digital technologies to drag contact center BPO into the OneOffice era. Let’s hope these guys can work it out, as there is a real war on between the legacy cost-obsessed approach and the OneOffice approach…

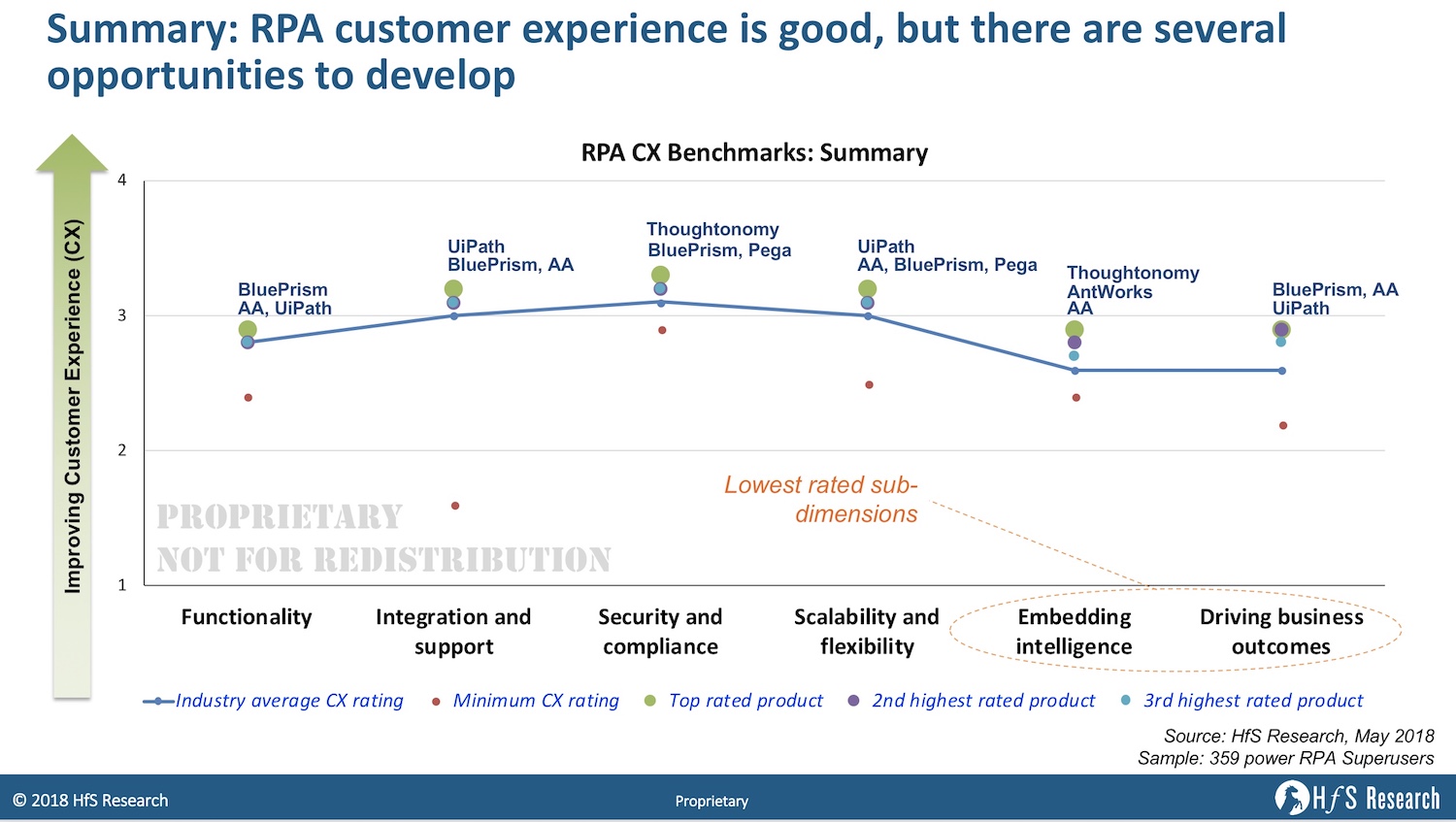

In case you’ve been asleep for the last month, we recently announced the industry’s most comprehensive analysis (by far) of RPA product functionality, covering AntWorks, Automation Anywhere, BluePrism, Kofax, Kryon, NICE, Pega, Thoughtonomy, UiPath, and Workfusion.

We interviewed 359 superusers of RPA products (172 enterprises, 87 RPA advisors and 100 service provider RPA practitioners) across 40+ customer experience dimensions across the following 6 key dimensions:

Features and functionality

Integration and support

Security and compliance

Flexibility and scalability

Embedding intelligence

Achieving business outcomes

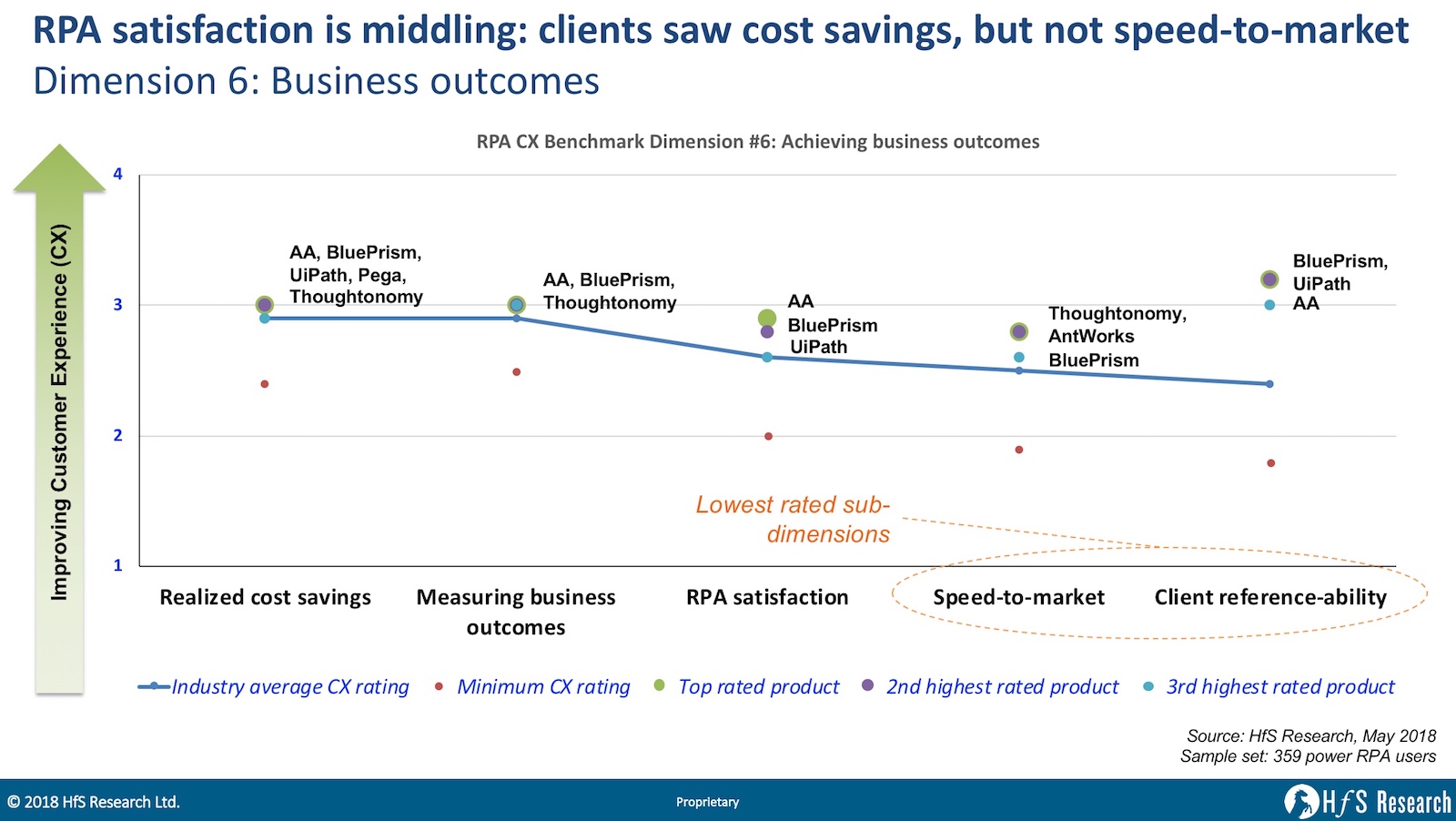

Here is how the overall satisfaction for RPA customer experience came out looking across the products

RPA’s core functionality works but deployments are not as easy as promised.

RPA products offer adequate client support and training but IT skills are required. Some RPA products have made significantly more investments than others around client support.

Most RPA products performed well on security and compliance related assessment.

RPA products have shown satisfactory flexibility but clients are still confused about pricing models.

RPA products are not as intelligent as they claim to be (at least not yet!).

RPA satisfaction is middling. Clients have largely realized cost savings, but speed-to-market has not met expectations.

Take time to delve into the realities of RPA and some of the findings may just surprise you:

There aren’t too many people you can listen to today where you feel all those sticky layers of hype just fall away from your brain, as this guy actually knows what he’s talking about and (as we English love to put it) he just doesn’t mince his words. So, after a terrific meeting with Hans-Christian (Chris) Boos, Founder, and CEO of leading AI platform vendor arago, I pinned him down to share some of his views with the HfS crowd…

Phil Fersht (Founder and CEO, HfS Research): Chris – you’ve been a terrific guy who adds so much energy and colour to the intelligent automation industry… but can you shed a little light on your story? How did you find yourself setting up the business in 1995? Was the focus on intelligent automation back then? I thought we were all going nuts about ebusiness!

Chris Boos (Founder and CEO, Arago): Phil – I originally wanted to do AI research at a university and then I saw how slow academic research is today with the way it is financed. I chose to do it inside a company instead. We could control the pace there. We setup arago to research general AI and my belief has always been that general AI is all about automation. If it is intelligence – even the quite boring artificial version – I guess you could say that smart automation was my goal, then.

Most people are surprised about the research phase. But if you look at most people who are doing significant work in AI they all plan or have done a roughly 20-year research phase. The one thing that is special about arago is that we financed it ourselves. We split the company down the middle, half was doing research and the other half was doing projects to get the money. That way we did not only get to do basic work on AI and make money to finance the work, but we also had a testbed for all our components in real businesses. A brilliant idea I cannot take credit for, it was my uncle who founded arago together with me who came up with the model. It worked out really well for us. We did pure research from 1995-2008, then used our own toolset to start automating IT operations and slowly turn it into a product and do some deployments till 2014, then scaled automating IT operations on top of more static approaches while collecting a dataset that is descriptive of all kinds of companies in all kinds of industries and 2017 we finally started applying AI generally in other industries and processes than IT.

By the way, 1995 was before the e-business boom started. I remember we did the first online banking on the web in Europe then and the page said, “your browser should support tables”. Can you still remember these days?

Did you ever expect to be where you are today?

Absolutely not. I am still being surprised every day. If you had asked me about feeding animals with an AI a year ago, I would have looked at you like you just tole me the aliens had landed. Now we are feeding animals with an AI. This is what is so absolutely fantastic about the industry, there is a new frontier to be pushed further every day.

Fortunately makes up for all the crap you have to hear because everything that has the slightest bit of math inside is called AI these days. I would like to reverse that saying: It is only called AI as long as it does not work. As soon as it works, it gets a real name like “facial recognition” ????

So you’ve been talking about some very real and honest stuff regarding machine reasoning… what’s this all about?

In the area of AI, we have made one mistake since 1954 now. Whenever we found a new algorithm or were finally able to actually apply an algorithm we found a long time ago, we declared this algorithm to be the one solution to everything. This one-size-fits-all approach is not only stupid but lead to AI winters which were periods in research and commerce when no one would touch AI with surgical gloves – except for the crazy ones of course; did I mention 1995 was during such an AI winter? We are making exactly the same mistake again, by declaring deep-learning equivalent to AI. One algorithm will not be a solution for everything, it is a solution for a defined set of problems. This means it will fail miserably at other problems and also have clear limitations in the scope it was originally built for. Let’s stick with machine learning for a bit. The clear limitation is data. At some point, there will not be enough data to describe “now”.

I believe there are three basic sets of algorithms to be considered when building a general AI:

Machine learning. The ability to learn to recognize patterns and associate positive actions with them. This is like evolution, everything that behaves favorably survives, everything else dies. Adding a temporal memory to this system was what started deep learning with long-term-short-term-memory networks. But there are many other learning algorithms. In biology, we call this “instinct” and all species have them.

Natural Language Processing. Now this is where it gets tricky, because language has so much compression. Think of how many different pictures you can imagine on the 3-byte input of “cat”. Your implicit knowledge of context and an internal argument narrows what you understand when you hear “cat” in a conversation down to a very likely correct interpretation. Machines, unfortunately, do not understand anything, and they also lack all the context. This is why NLP is still one of the hardest parts of AI. There is no way to “learn” the meaning of language through machine learning (yet), especially because the context, is so volatile. This is why the hype around chat-bots has lead to a lot of disappointed customers. They work well if you can predict the dialog with a high degree of certainty, for example, if you offer a telephone line where people can call in sick you know that there are only so many ways to say “I am not feeling well” and the only result you want out of the dialog is “when will you be back”. But all other more general cases are very difficult. This is why you have to change your language structure quite drastically if you want Alexa, Google Assistant et al to do anything for you. There are a lot of very advanced algorithms in this area which are mainly very advanced statistics to create probable context, probable synonym, probable XYZ and then math this to a pre-determined understanding structure. These are the least self-reliant algorithms in the AI family. In biology, language was the single differentiating factor that made us as a species outperformed everything else on the planet. We no longer had to go through long cycles of observation as well as trial and error to have only the ones with the right solution to a problem survive. We could simply tell each other “if you see a Tiger, run away” and no evolutionary iteration was needed. This is a huge advantage which machines are completely missing.

Machine Reasoning. The one you were actually asking about. This was how AI started. The idea was to make a logical argument to find a solution to a given problem. The first attempt was to use decision trees to “write down the one and only answer for every situation”. This does obviously not work, because the more interesting a problem is the more different ways of reaching a solution there are. The industry moved from decision trees to decision graphs. Then we found out that logic does not govern the world and that ambiguity, contradictions, overlapping information, wrong information and unexpected events have a huge influence on how to really solve a problem. The type of algorithms that create a solution by outputting a step-by-step execution instruction for a more complex task by choosing the best step to take out of an existing pool of options and then the next and so on are called machine reasoning. The limitations of these algorithms used to be in the knowledge base because the maintenance effort of such knowledge bases grew exponentially and the benefit grew polynomially. In the world of biology, this is called “imagination” of if we want to be less philosophic the ability to simulate a bit of the future in our heads to make the right choices of what to do in order to reach a defined goal.

Looking at only one algorithm set to solve all problems in the world seems dumb, yet if you read about AI, it seems that machine learning has become synonymous with AI. This literally guarantees a bursting bubble once the limits of data availability are reached. My prediction is early 2019.

We have set out to combine these algorithms to produce a single engine with a single data pool to mitigate these problems and this is why we started in IT automation and are expanding to more and more complex automation across all kind of different industries.

And you’ve been quite poignant regarding your views on AI actually substituting human intelligence and how unrealistic a “singularity” is – can you share some of your candid thoughts here with our readers?

The entire debate about singularity does not make sense, Phil. We pretend that simply by rebuilding the electrical part of the brain we get a self-conscious self-reliant entity, why should that happen? If you build the skeleton of a dinosaur you don’t get a dinosaur either.

Ok, to put this down in numbers. A large neural network used in deep learning has about a million nodes today. Is uses up the power of half a powerplant. An average human brain has 84 billion neurons and uses 20 Watts. According to Moor’s law, we can achieve rebuilding this by 2019 and I am one of the guys who believes that Moor’s law will hold. Yet, that is not all there is to the brain. The brain also has a chemical system creating a literally infinite number of configuration of the brain’s 84 billion neurons. Infinite because the chemical system is completely analogue. And then for good measure, there are a lot of well-reviewed research papers arguing that the brain also must have a quantum mechanical system injecting probabilities. So there are two entire dimensions we are missing before we can really reproduce a brain-like structure.

And even if we could… We don’t understand or know what consciousness and self-awareness are, do we. So how do we think we can build it? Is “by accident” really a good explanation? “Build the field and it will come” is definitely not the answer here. This is why all the talk about killer AIs and ethical machines is far too early. I am not saying there will never be a super-intelligent AI, but not in the new future.

That does not mean that current AI technologies cannot outperform us at tasks we have already mastered. Tasks that we as humans already have the experience for and thus tasks we can transfer to the machine. But why would we mind? A crane is outperforming my weight-lifting ability everyday and I think that is perfect, I have absolutely no desire to become a crane, do you?

What will AI truly evolve into over the next 10-15 years, based on your experience of the last two decades? Is there any real reason why change will accelerate so fast? Are just getting caught up in our own hype?

What will happen is that automation leaves the constraints of standardization and consolidation. With AI systems based on today’s tech, we can automate tasks, even if they only occur once and even if they have never been posed like this before.

I think I was a bit too abstract here. I believe that AI will make any process that we have mastered and that is not entirely based on language autonomous. Machines will most likely do 80% of what we are doing today. Which means that our established companies get a fair opportunity to catch up with the tech giants. This is why I believe that we need RPA as a transition technology, because it basically puts an API to everything that there is in the corporate world. On top of that, we can use AI to automate almost everything allowing every enterprise the wiggle-room to actually evolve

So what’s your advice to business and IT professionals today, Chris – how can we advance our career as this intelligent automation revolution takes hold?

I think in IT we are in a unique position. What click-data was for commerce, IT ops data is for the enterprise. IT ops data describe everything a company is doing and thus forms the foundation of applying the next generation of automation and autonomy.

The only thing we as IT professionals really have to do is open our minds. If we do so, we can revolutionize much of the business and not be the “laggards” who are slowing everything down as we were in the ecommerce revolution. You know I am German, so I get to be blunt: I think we have to “grow a pair” and take on the risk of automating everything from IT, otherwise business will do it for us and then who needs IT?

And finally… if you were made the Emperor of AI for one week and you could make one change to mankind, what would it be, Chris?

Mankind? That is too big for me… It would have nothing to do with AI, I would force people to think rationally for at least 50% of the day instead of 0.5, but let’s not go that far or people will think I am a cynic.

Let’s say I was made king of AI in the enterprise world for one day. I would decree to stop every POC, POV, Pilot, or whatever other terms you can find for trying to be half-pregnant and force people to start doing things in production right away. There simply will not be enough speed if we keep on “trying”. As master Yoda said, “Do or do not, there is no try”. We really need to adopt this behavior pattern.

Thanks for your time today, Chris. Am looking forward to sharing this discussion with our community.

Still enjoying life now GDPR’s cleaned up your inbox, but now realize HfS is the one you just cannot live without?

Let’s be honest, you probably do need to keep up-to-date with the finest change-agent research on RPA, blockchain, AI, and much more, right? Then you really must register here to receive HfS’ content, or update your email subscription to keep receiving us.

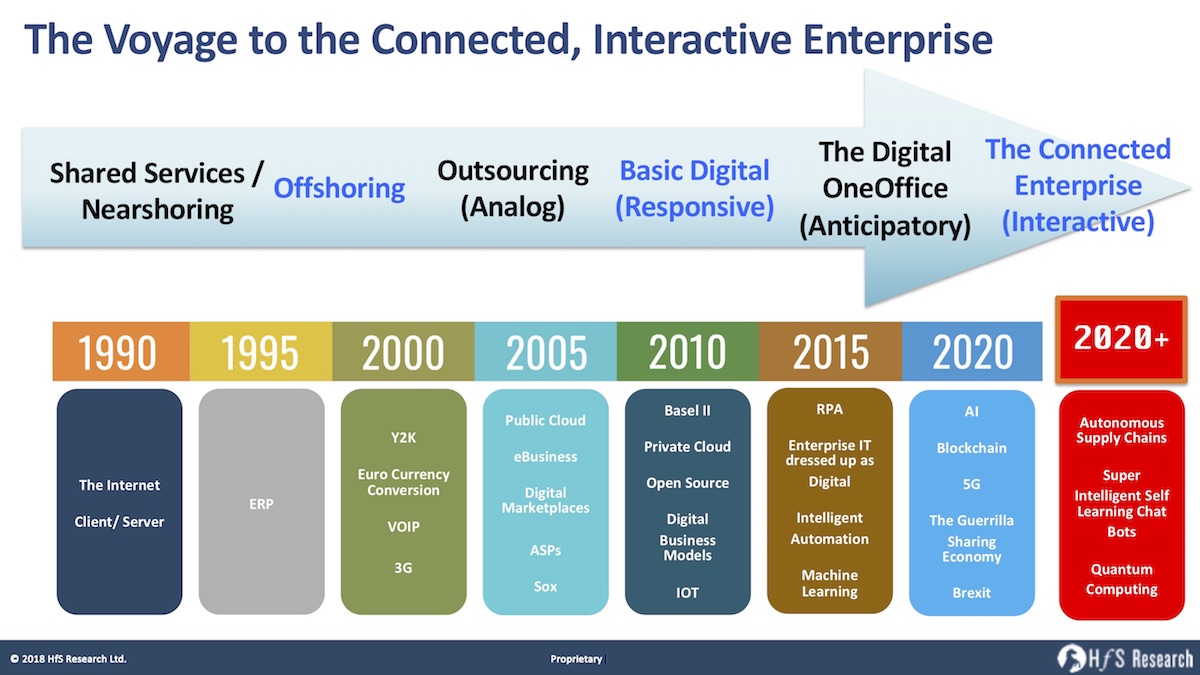

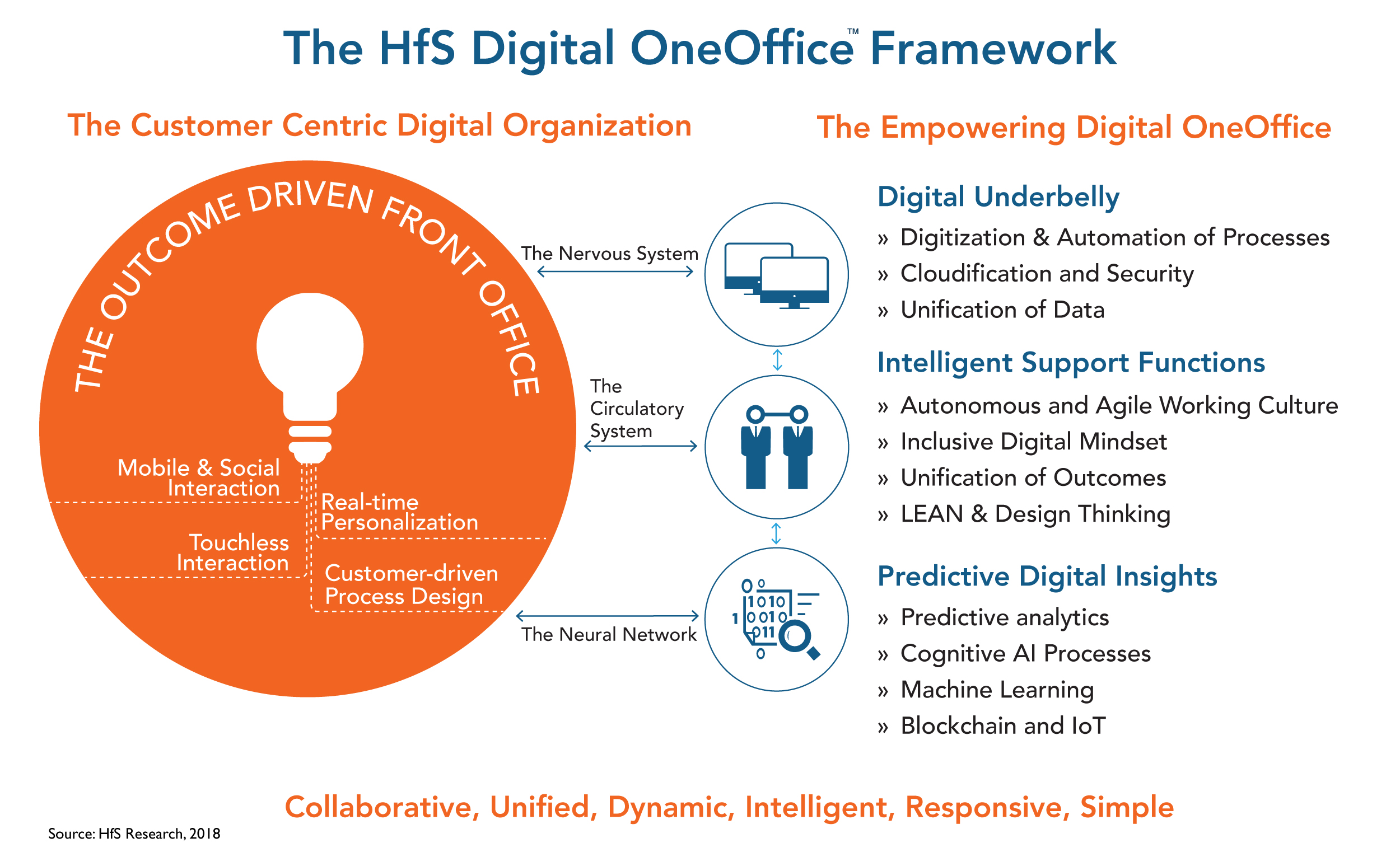

Digital is all about an organization’s ability to respond to the needs of their customers as those needs happen – or even be smart enough to anticipate those needs before they happen. This is all enabled by interactive technologies to create those touchless interfaces with the customers. Smart analytics and AI enable organizations to anticipate these needs based on the ability to recognize patterns and inferences over time, but nothing can really substitute for human intelligence to bring customers, suppliers and employees closer together, unimpeded by frustrating silos and legacy processes.

Remember, every broken process chain, or poorly converged dataset, slows down an organization’s ability to do business in real-time and stay ahead of its market. Traditional barriers between front, middle and back offices hinder the true ability of companies to operate in this real-time, responsive and anticipatory digital fashion, which is why we coined the term “OneOffice”, where the unification of digital business models, intelligent automation, analytics and creative talent is happening before our very eyes.

The HfS Digital OneOffice Framework (see below) describes how organizations must integrate their digital customer interfaces with their operations in order to fulfill and anticipate their customers’ needs. It is the organizational end-state to survive and succeed in a world where digitized processes dictate how responsive, agile, cost-effective, predictive and intelligent firms have to be to stay competitive.

To this end, we have delved deep into all the four dimensions of the Digital OneOffice, and conducted deep analyst discussion to aggregate service provider performance at delivering the sum of the Digital OneOffice parts:

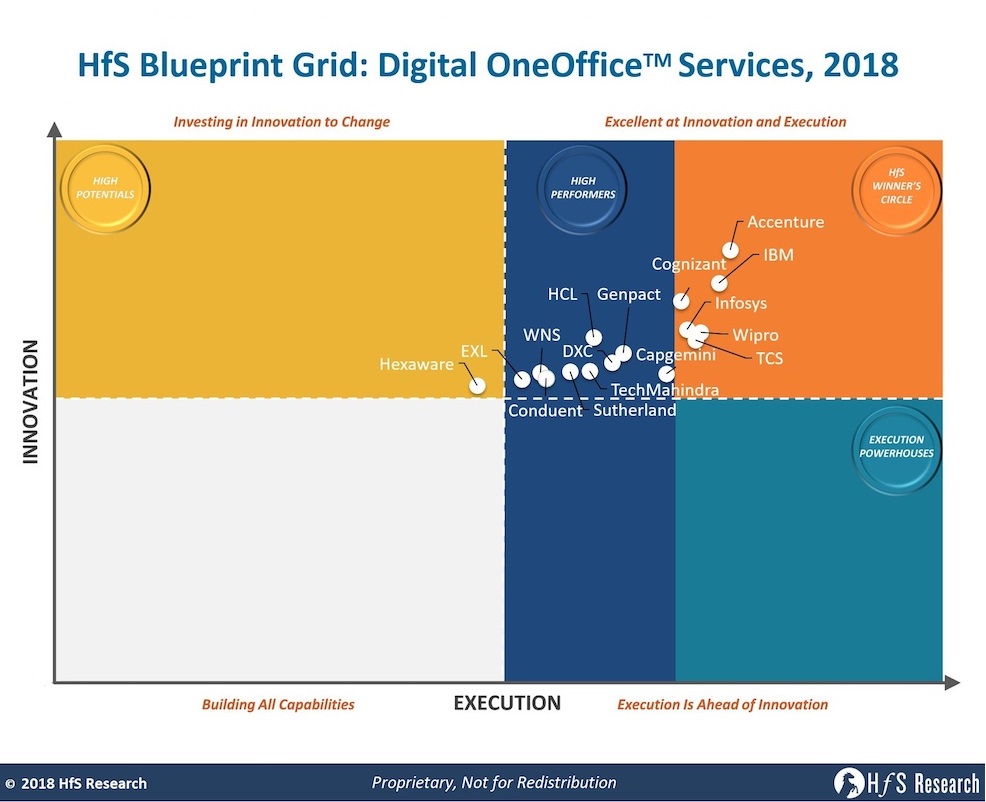

So how did the Winner’s Circle service providers fair?

Accenture

Strengths

Well-rounded portfolio across OneOffice: Accenture has the best performance overall across the OneOffice portfolio, and a breadth of industry expertise to complement it. Accenture placed in the Winners’ Circle for each of the Blueprint studies used to compile this OneOffice assessment.

Strong marketing operations capabilities to support integrated digital OneOffice offerings. Accenture has 16,000 business-focused staff dedicated to delivering digital marketing assignments – a considerable asset that goes well beyond the firm’s IT delivery.

Strong intelligent automation capabilities. Acquisition of GenFour and exciting partnerships, with significant investments, with the likes of Automation Anywhere, Blue Prism and IPSoft.

Winning with thought leadership: Accenture is well-known as a thought leader across many of the change agents as well as within individual industries.

C-Suite relationships beyond IT. Digital business and intelligent automation decisions are largely being driven by both IT and business C-Suite executives in the Global 2000. Accenture has the combination of strategic relationships outside of IT, in addition to the managed services execution.

Leveraging creative assets for CX and UX design: Accenture has developed an industry-leading focus on becoming a customer experience expert, as evidenced by its 30+ design agency assets, by the broadest portfolio of digital design assets in the services industry (click here for a full list of digital M&A in services.)

Challenges

Size can work in its disfavor: Its size and success have given Accenture a reputation as a premium, high cost, and less responsive organization. In particular, for smaller companies, just this perception in the market can steer buyers instead toward more niche specialized agencies and the attention, flexibility, and experience they receive from a smaller provider.

Finding the right culture balance: Accenture is well known for its results-driven, traditional consultancy culture, which will need to be balanced out or effectively blended with the more left-brain focused acquisitions in order to retain creative talent and remain generally effective.

Proving to the industry it can deliver the end-to-end Digital OneOffice portfolio: There is no doubt that Accenture can pick up strategic work and execute for clients, but being able to demonstrate to the industry it can deliver both the strategic design integrated with complex operational delivery – at scale – is still in its infancy. Many of its competitors will fight hard for execution work where Accenture is delivering the high-end design and consulting. It needs to demonstrate the “one-stop OneOffice shop” is where it wins.

IBM

Strengths

Strong intelligent OneOffice offering: Market leading capabilities to drive the OneOffice underbelly (automation, security, cloudification) and neural networks (AI, smart analytics, blockchain, and IoT). Impressive development of credible global automation capability and several notable early wins.

Portfolio breadth: End-to-end and scaled IT and business process services across front, middle, and back-office.

Horizon 4 investments: Very strong investments and IP in horizon 4 (and beyond) technologies that will shape the future (e.g., Quantum Computing).

Design Thinking: Has made some considerable investments in recent years, but needs to align more aggressively with OneOffice approach

Watson: The analytics/cognitive powerhouse has a significant role to play as a cognitive virtual agent, an analytics resource that has huge scalabiity and a long-term investment area for firms with deep interests in their cognitive capabilities.

Challenges

Size can be a disadvantage: IBM is a large and complex organization, which makes it hard to seamlessly deliver all that it has to offer.

Translating tech to business outcomes: IBM is often perceived as a technology powerhouse, but one lacking the business translation and context to successfully apply emerging technologies.

Agility: Lacks the nimbleness and flexibility of smaller players.

Focus on cognitive may impede its ability to compete for design-focused end-to-end deals: IBM has substantial credibility to drive analytics-driven, cognitive/automation projects, but its lesser focus (over the last couple of years) on true digital design may see it lose out to firms such as Accenture and Cognizant, where digital is firmly established at their core.

Cognizant

Strengths

Digital marketing is leading front office services: Cognizant performed well in our digital marketing services Blueprint, primarily based on its targeted acquisitions and proprietary IP and frameworks.

Solid portfolio for the digital underbelly: Cognizant landed in the Winners’ Circle for each digital underbelly-focused Blueprint.

Strong thought leadership: Cognizant has a very compelling and polished messaging around customer experience focus and automation with forward-thinking leadership, bolstered by design-oriented acquisitions.

Simple, focused strategy: Unlike several of its Indian-heritage counterparts, Cognizant has always kept its focus simple and business focused. It’s “SMAC stack” approach was the perfect prerequisite to digital.

Challenges

Integration of key acquisitions will be key to success: Cognizant has made targeted acquisitions such as Cadient, whose capabilities the service provider is still working to integrate in order to bring value to clients.

Expansion of Design Thinking across services capabilities: Cognizant needs to develop its Design Thinking capabilities to other elements of services outside the front office in order to help its clients on the journey to realize the OneOffice endgame.

Keeping the momentum going: Cognizant has grown faster than any of the major service providers over the last decade. Keeping its scale aligned with its growth is going to be a challenge to the firm, with greedy investors still expecting 10%+ annual growth in a slowing market.

Infosys

Strengths

Portfolio across OneOffice capabilities: Strong capabilities across all dimensions of the Digital OneOffice—digitally enabled front office, digital underbelly, intelligent support functions and the nervous system. Recent re-focus on digital expansion is a plus.

Focused go-to-market approach: Digital platforms, automation, and AI have emerged as key pillars of the go-to-market strategy.

Digital OneOffice transformation services: All-rounded and scaled IT-BPM capabilities required for Digital OneOffice transformation.

Data DNA: Infosys has already been very strong with its data capabilities and provided it stays focused on this new course (see the recent interview with its new CEO), the future should be bright as a OneOffice heavyweight.

Strengthening BPM capabilities: InfosysBPM has demonstrated some of the strongest growth in the industry with some impressive BPM wins over the last 18 months. With deep competencies in middle/back office, in addition to marketing and analytics, the firm can make a strong run at the likes of Accenture, IBM and Cognizant, provided it keeps investing in its digital capabilities.

US onshore investments: Infosys has targeted 10,000 new staff to locations such as Indianapolis and Dallas. This is being well received by politicians and clients alike and helping align the firm with clients needing more onsite/onshore support.

Challenges

Relatively conservative M&A outlook: Despite recent acquisitions, overall outlook to M&A continues to be conservative.

Leadership turnover: Frequent changes to top leadership impact market positioning and consistent messaging. The new regime has to keep this ship firmly focused.

Market perception as a tech player: Infosys continues to be perceived as a technology player and needs to double down on driving business context in its solutions.

Needs to spend some of its war-chest: Infosys needs more depth in front-end digital delivery than Brilliant Basics and WONGDOODY. Salil needs to go shopping and spend some of his massive war-chest.

Wipro

Strengths

Key acquisitions bolster digital transformation capabilities: Wipro’s acquisitions of Designit and Topcoder (Appirio) give Wipro some significant assets for strategic design and UX, and also strong talent in the realm of data science, design, and development.

Services delivery excellence: Wipro has a strong execution approach to BPO and RPA with its Enterprise Operations Framework and is known as a solid delivery partner across a broad portfolio of services. Strong global presence and competitive aggression to win strategic deals.

Partner ecosystem: Wipro Ventures’ investment highlights its partner-focused approach. it’s reputation for being easy to work with has helped the firm develop exciting alliances with emerging firms in the fintech, startup space.

Much improved thought leadership: In previous years this was a major weakness for the firm, but a successful rebrand and a consistent delivery of market positioning and client experiences has change the percpetion of Wipro significantly with clients and market influencers alike.

Reputation for execution: Wipro has done a lot to up its game in recent years to deliver a multitude of touch, complex global deals. Many of its clients have a strong level of trust in the firm to move further up the value chain.

Challenges

Integrating acquisitions for a more consultative capability: Clients are looking for stronger thought leadership from Wipro and could use a stronger business- outcomes approach to its messaging. Further integration of acquisitions like Designit can help Wipro be a better innovative thought leader for clients on the journey to OneOffice.

Development of marketing of HOLMES platform: Wipro should invest in messaging for its HOLMES platform, one of the first broad automation frameworks on the market, to highlight its deep capability and assets in the bot library.

Needs more front-end digital acquisitions: Not dissimilar to Infosys and TCS, Wipro needs to keep focused on further front-end acquisitions to boost its digital presence with the design areas of the market.

TCS

Strengths

Client relationships: Appreciated for its engagement with clients, proactive focus on process improvements, and flexibility. Good account management skills. Clients mention factors such as understanding their business and unique operating models and being flexible to work with.

Embedded analytics: TCS is one of the top service providers with analytics reported as embedded in contracts. Has positioned much of its talent in its data analytics areas as a front-end strategy.

Intelligent Automation: Major focus on internal capabilities, including ignio platform. Impressive record with clients and a willingness to cannibalize revenues to grow emerging areas.

Partner ecosystem: TCS has a strong partnership ecosystem for emerging technologies. Its work with academia and startups has been most impressive, with significant funds being invested to create strong talent programs and joint business ventures with innovators.

Challenges

Thought leadership needs a lot more focus: TCS needs to be more proactive and vocal about ideas around innovation and best practices. It is often challenging to pinpoint the core focus of the firm beyond being a competent technology firm.

Behind on M&A: While most of the big service providers are scaling up their portfolio through acquisitions, TCS has made a few acquisitions, but is relying primarily on organic growth. While this is clearly a desire from leadership to grow organically, it could significantly stunt TCS’s ability to evolve into more creative design areas where the firm is currently lagging. A reversal of strategy is probably likely in the future as the market shakes out.

IT services and middle office focused: Aside from a strong digital marketing offering, TCS is more back and middle office, with more of an IT services presence in the middle office. BPM was a core focus, but seems to have faded somewhat in the last couple of years.

Heavy India delivery: TCS could increase recruitment in specific geographies for more diversification.

Other notable service providers

Outside of the winner’s circle, Capgemini was one of the most notable exclusion, despite a well-rounded OneOffice portfolio across front and back office. The firm still struggles with its North American portfolio, despite its IGATE acquisition and its co-CEO structure and lack of thought leadership has held back progress. Genpact has impressed clients with its LEAN Digital approach, its depth in processes and recent acquisitions in AI, but its lack of scale in IT has kept the firm of the Winner’s Circle. HCL has performed well its strong breadth of services, strength in automation and notable flexibility with clients, but lags the leaders in terms of digital design, change management analytics and innovative messaging. DXC is still trying to find its feet since the HP/CSC merger but has very strong IT delivery capability. The firms does need a strong injection of market positioning and expansion beyond its infrastructure capabilities. Tech Mahindra has quietly emerged as a high performer, boasting a series of impressive digital front-end platforms, a real appetite for innovation and strong client partnerships. We expect the firm to keep improving its market position, providing it can diversity effectively beyond telco, make some astute analytics investments and leverage its M&A for effectively (its Pininfarina acquisition has largely been considered to be misaligned).

Bottom-line: Winning at OneOffice services is about delivering the four dimensions as a true client partner with co-defined outcomes and investments on both sides

The traditional services model was all about delivering incremental productivity and efficiency for clients. There was rarely much purpose behind the client/service provider relationship beyond attaining a series of predefined cost/delivery metrics and KPIs. And once the first set of metrics were met, the next set was normally more of the same, but with added pressure on margins, which ultimately led to a degrading of quality and talent. “They sold us the A team and we ended up with the B and C team” is probably the most worn services catchphrase of the last two decades in the services industry. However, if clients wanted the cheap and cheerful model, that’s ultimately what they ended up with: getting exactly what they were paying for. All you have to do is look at the depressing number of legacy services relationships littering the Global 2000, where most the value has been squeezed out, and both client and service provider are stuck on a depressing treadmill where both often want out, as they just don’t get much business value from the relationship.

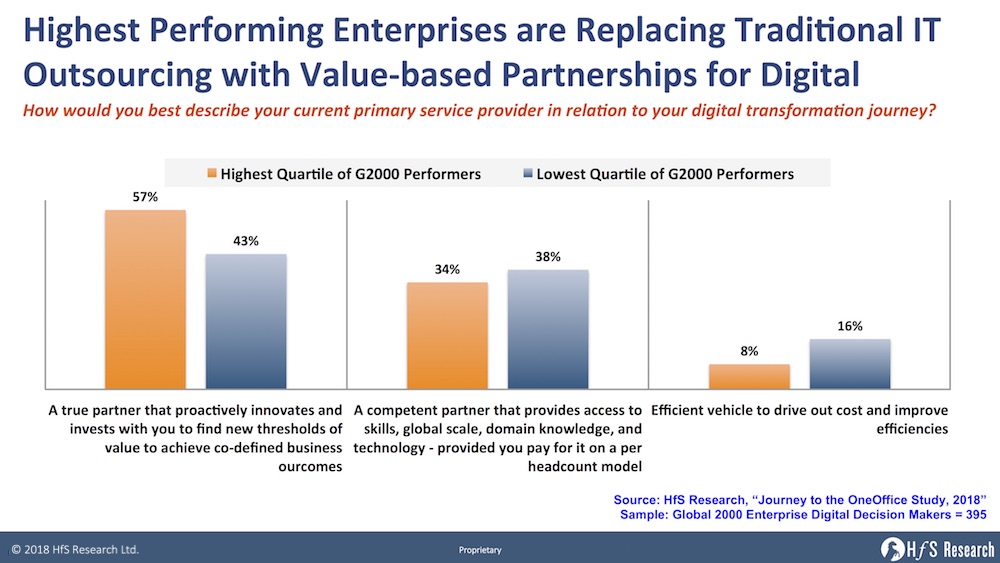

Fortunately, the business imperatives have been changed forever with the evolution of digital business models, which is having the impact of driving much smarter, value-driven partnerships for ambitious clients and service providers. Sure, there will always be the laggards who will persist on cranking out the same old business models until they fade into insignificance, but 57% of digital decision markets among the highest performers (based on revenue and profitability) in the Global 2000 now view their primary service partner as a co-creator of innovation and value, as opposed to a provider of prepaid services that merely provides efficient services as our recent study looking at digital transformation to the OneOffice reveals.

This data speaks volumes – enterprises digital leaders need providers which can work with them to achieve outcomes that are increasingly challenging, with only a third viewing their service providers solely as a resource to provision skills and scale via a headcount model.

A true digital business cannot succeed without unifying front, middle, and back offices – it’s no longer about being great at one component, it’s about weaving together the disparate parts to bring customers and employees as closely together as possible to create the best possible customer experience that wins out in cut-throat markets. Sure, there will always be niche opportunities to support certain needs for enterprises, but the ultimate winners will be those which can partner with their clients to help define and deliver their business outcomes over the long-term. This means providing the business intelligence, market understanding, and technical abilities to help their clients be as competitive as possible. The stakes are higher than ever, and the smart providers are those placing their investments in clients with whom they can thrive over the long-haul.

Salil Parekh, recently appointed CEO and Managing Director for Infosys took some time out of his busy schedule during his client partner conference to catch up with me to talk about his vision for all things Infosys and the future of services…

Phil Fersht, CEO and Chief Analyst, HFS Research: Welcome to your first HfS interview Salil! Maybe you could take us a little bit back to your early career. When did you get the appetite to lead one of the largest IT services firms in the world? You know, was this something you always wanted to do? Was this planned, or have you always been an opportunist?

Salil Parekh, CEO, Infosys: Thank you, Phil, this was quite an un-planned scenario for me. So, maybe when I finished with Engineering, a Master’s in Computer Science, and I was working with a consulting firm for years. Then we got acquired by a consulting and tech company, so I’d basically been in the same company for 25 years. And then this opportunity showed up a few months ago. It’s a tremendous privilege to have this opportunity. It’s one of those things you dream about, in your career, as you sort of think, ‘Maybe it’s possible,’ but when it happened, at least, for me, it was completely unplanned. So I’m delighted to be here, I wish I could plan such things, but I can’t [laughter].

Phil: So, how would you compare this new Infy experience with Capgemini, you know, both global services powerhouses, one with a Parisian epicentre, the other one Bangalorian, so – what haves been your observations?

Salil: Well, I think, Cap’s a fantastic company. I think I would focus much more on the strengths that I’ve found within Infosys. The first few months, I’ve spent essentially meeting with our clients and our employees. I met with just about 50 clients, and it’s been just amazing to see how much the clients trust Infosys, and our delivery capability, and the strength of the organisation. And then, with the employees, it’s been much more the pride in being with a number one company. And so to me, we have, at least in my mind, an incredible platform, from which, if we can execute right, we can become partners for our clients’ digital journey. So, that’s really the joy, of where I am at Infosys right now.

Phil: Salil, your predecessor unleashed some of the passion and culture in Infosys; it didn’t quite end up, I think, how he wanted it to, but how do you think you’re going to be different from him?

Salil: So, my thinking is, the way we’ve built our strategic direction, which I’ll spend a minute on, maybe later, is, what are our clients looking for and where are they going? So, how do we evolve with them? Then, what other new areas, new clients, can we target from our asset base, or our foundation? And those are the two ways in which I have looked at the business. From our clients, they all want to progress on their digital journey. They have the foundation tech in good shape, and my focus is going to be to see how we scale up our own digital focus to go on that journey with them.

It’s interesting, already one fourth of our revenue is in those Digital areas, so it’s not that we’re starting from zero. The new Digital areas that we want to go after, there’s new sets of clients, there’s expansion in the European markets, there’s more expansion in the Asia-Pacific. There are some sectors we are underpenetrated, healthcare, or life sciences, or manufacturing, and we have great strengths which we can leverage, I think, to go after those. And in terms of the strategic direction, it’s more in the services area, with 4 pillars – scale agile digital services, energize core services, reskilling of our people, and localising, that is a new approach where we’re starting to build delivery capacity here in the US, in the European markets, in Australia, to make sure that we are closer to our clients. So, that’s the direction that we’ve charted out, and so far, it’s something that’s resonated with our clients, with the market, (I know you had presented a set of views after our analyst day), the sales teams within the company. So, I think there’s a lot of support and traction for this approach, and now it’s more really, an execution play for us to make sure we get this organized properly.

Phil: I think you’ve excited the market, acquiring two interesting digital firms in the UK, and US: Brilliant Basics and WONGDOODY. What’s the plan to bulldoze your way to the front of this market? Do you have an M&A strategy lined up, or is this going to be more opportunistic? How do you think this is going to play out for you?

Salil: There we have a very focused approach to what we call ‘Programmatic M&A’ and we’ve defined five dimensions of digital: experience, insights, innovate, accelerate and assure. Behind that, we’ve put each of our service lines. So, our head of M&A, Deepak is now looking at, from the landscape of companies that are in the market, how do they map on to this framework? And then which are the areas we should invest in. From these, we want to create multiple $1 billion businesses. So, you can take an example, on the cloud migration journey. There’ll be large plays in Azure, AWS and Google Cloud, and we want to be in that space. There’ll be large plays in data and insights. On experience, which is where these two companies are, Brilliant Basics and Wongdoody. Traditionally, we do not have a strong position in these areas, so I want to make sure that we build up our position, so that we can engage with our clients on any aspect of this digital journey. Different clients start at different places, and then go on to the different parts. And what we have noticed is, that it’s not really a transformation with a start and a finish, it’s more a journey that people are going through different components, some going faster, some taking a longer path. My approach, through this five-pronged, Digital ‘pentagon’ that we’ve put together, is that we want to be part of any digital journey. Therefore the experience side, is where we thought we should build out some strengths. But overall, we’ve got, I think there’s a shortlist of companies that he has built, from some companies that we’ve been meeting over the last three months. With M&A, as you know, it’s more a question of availability, price, and, sort of, a lot of other factors going right at the last minute, culture, integration, fit. So, hopefully we’ll start to execute on that.

Phil: M&A’s been a key issue in our industry for a while, Salil. There’ve been far more failures than successes when we look across the board at all that’s happened over the last few years. As you look at bringing on some of these emerging companies, with a very different mindset, what’s your view on how to integrate them into your business?

Salil: So, yeah, just as an example, with Wongdoody (and with Brilliant Basics); we are recruiting, in the US, students from design schools as well and those will essentially be under the direction of the Wongdoody leadership. Plus, two individuals from Infosys that will join that team, and that will drive the scaleup. So, they know how that must be done.. So, we will leverage their knowledge and experience, and build it out, under that umbrella. Then, our service line leaders have put together a plan for how all the experience assets, user experience, or creative, come together. We are also thinking about what we should do with the branding because at this stage, we’ve not made any changes; however, over a three-year period, we want to align to a branding position that we want to develop.

Phil: Salil, we’ve seen a few other providers try and influence their culture too much on their niche acquisitions (especially with digital firms)… and I think what you’re saying is, “buy some of these special firms, and nurture them, grow them, build them, retain the culture, and then figure out the synergies”

Salil: Absolutely, yes – because, as you know, there are two basic models of acquisitions in our business. One is, buy it, make it look exactly like them, and then go ahead.

My experience has been much more than you buy something, learn the culture, and try to build the best of both, as opposed to overwhelming one or the other. And this is what we are trying to do by not changing the culture, in fact, enhancing it. We still need to have some guidelines in how the overall strategy comes together, but the culture is very difficult -if we start to impose upon these companies, as you mention, it will destroy value quickly.

Phil: There’s been a lot of talk, Salil, about investing in products .v. services. It feels like Infosys is moving down the services path. Going higher-value, looking at more consultative, digital mindsets…

Salil: My focus today is much more services. But what I would say is, first, there are things that I call platforms, and what I mean is, within Infosys, we have an insurance platform called McCamish. You may have heard of it.

Phil: I know it very well…

Salil: So, that, I will scale up. So, we just announced, three weeks ago, a large win with John Hancock, it’s in the public domain, $175 million win. That is a phenomenal approach, we think, in the insurance market of today, where we can use that platform. So, it’s not just a product play for us. Equally, we are not (and we’ve announced that we are exploring to sell Panaya), which to me, is not a product that I can scale that much. The market there, for SAP upgrades, has changed and there’s always bandwidth issues and management. So, if there are platform plays, we will actually buy and expand. We are not going to, at least at this stage, look at standalone product plays. Some of these also require multiple third parties to implement them, which is not easy, when you sit within a services company. So, given all of those dynamics, that’s the approach we’ve taken, primarily services. If you can build a platform that would be phenomenal, like this McCamish one, there could be others you could imagine, on mortgage processing, or trade settlements. There are areas which lend themselves to platform. But we have to find something, or build it ourselves, and that we will scale.

Phil: I’m sure your BPM guys’ll be thrilled to hear that =)

Salil: They’re delighted and BPM’s growing very well for us right now, so we are very happy with that.

Phil: Good. I’ve known them since the Progeon days!

Salil: Oh, brilliant! Okay. Yeah, no, I think if you saw that, we went through a bit of a dip, but the last 24-36 months, we had a good trajectory. In fact, if you look at it on a standalone basis, it’s probably the highest, fastest-growing BPO business, if I look at competitors, and it’s also the best margin BPO business. So, I think that, in that business, I will happily invest in platforms.

And there is Finacle, where we are leaders, and that is a product and a platform play for us, that we are scaling up. We have seen recently two very successful Digital banks being built on Finacle – one here in the US and one in Asia. That is a strong business for us and we will look to scale.

We also have our AI platform Nia – which will become the foundation of all our services re-invention. We will enhance and build that out.

Phil: So we’re looking at a lot of these interesting insurtech/fintech businesses. What’s the approach there? Are you going to look to acquire these, or maybe do more partnering?

Salil: So, today we are more on the partnering, but it also depends. There are some fintech players, which could become a platform. But today, as you know well, they’re very expensive, if you’re going to buy. So, you’ve got to figure it out first. And we’ve not done a lot of partnerships yet. We’ve got an investment fund, through which we invest, we haven’t tried yet to have a partnership where we do many client projects together. So, first we’ll try a bit of that with the fintechs, and then, if it looks like we can build, again, a scaled fintech play, which is more a platform, so it’s not just a product play, then we will look at it eventually.

Phil: So, one final question, Salil… You’ve been annointedthe Emperor of the Services Industry for one week, and you have one wish, to change the industry for the better. What would that wish be?

Salil:[Laughter]. Give all your business to Infosys, of course [laughter]. But, no, I think, you know, it’s a bit ironic, notwithstanding what people outside think, I feel like we are in a uniquely good position, so I’m not sure I would change many things. We are doing many things to enhance our position. The industry, itself, is in a nice phase where there is massive opportunity in the future, clients are changing. For any company that’s ready to invest and position themselves, within the next five years, you will have a new set of leaders emerge, and to me, that’s as good an opportunity as anyone can get, when you have a huge incumbent company, which still has an opportunity to win again in a different area. So, I’m delighted. There’s not too many things I would change. I think the best wish is, try not to be the Emperor beyond a week [laughter].

Phil: There you go, that’s a fantastic answer =) Good luck in the new role, Salil… you sound very geared up for it!

As am sure most of you noticed, HfS quietly released the most comprehensive customer satisfaction benchmarking of the 10 leading RPA solutions, authored by Saurabh Gupta, myself and Maria Terekhova. We covered 359 super users of RPA products (enterprises, advisors and service providers) across 40+ customer experience dimensions across the following 6 key dimensions:

Features and functionality

Integration and support

Security and compliance

Flexibility and scalability

Embedding intelligence

Achieving business outcomes

As an example, here is how dimension 6, “Business Outcomes” came out looking across the products:

So why did we undertake this research?

Our industry is plagued by many consultants with limited depth in RPA, who have no access to product level data that supports the tough decisions facing enterprises. In addition, most analysts deliver these 2 x 2 matrices which offer very limited insight or value (and all look remarkably similar). It’s time to dispel myths and provide enterprises with unbiased, credible and highly statistically significant data. The HfS RPA customer experience benchmarks are designed to help enterprises with RPA product selection as they formulate their intelligent automation roadmaps.

It’s more than a report… it’s an online RPA decision-support tool

In addition to the report, HfS is also launching an online RPA decision-support tool for enterprises to enable client-specific due diligence on RPA providers. This tool will allow HfS clients to customize the decision criteria and associated weights from the available 40+ customer experience dimensions. It will provide clients a customized report detailing the top three RPA products that the client should consider, based on the rich insights that HfS collected as a part of the RPA study. HfS analysts are also supporting RPA clients through collaborative ThinkTank sessions, half-day workshops designed to problem-solve and validate strategies. These ThinkTanks go beyond the data where HfS analysts can share HfS IP, perspectives, and experiences on RPA tool selection, best practices, and common pitfalls to avoid.

So take time to delve into the realities of RPA and some of the findings may just surprise you

The industry is still struggling to solve challenges around the process, change, talent, training, infrastructure, security, and governance. Our mission at HfS is to dispel this confusion and uncover the truth to successful RPA deployment. It’s time to separate the hype and propaganda from reality – and here is the reality!

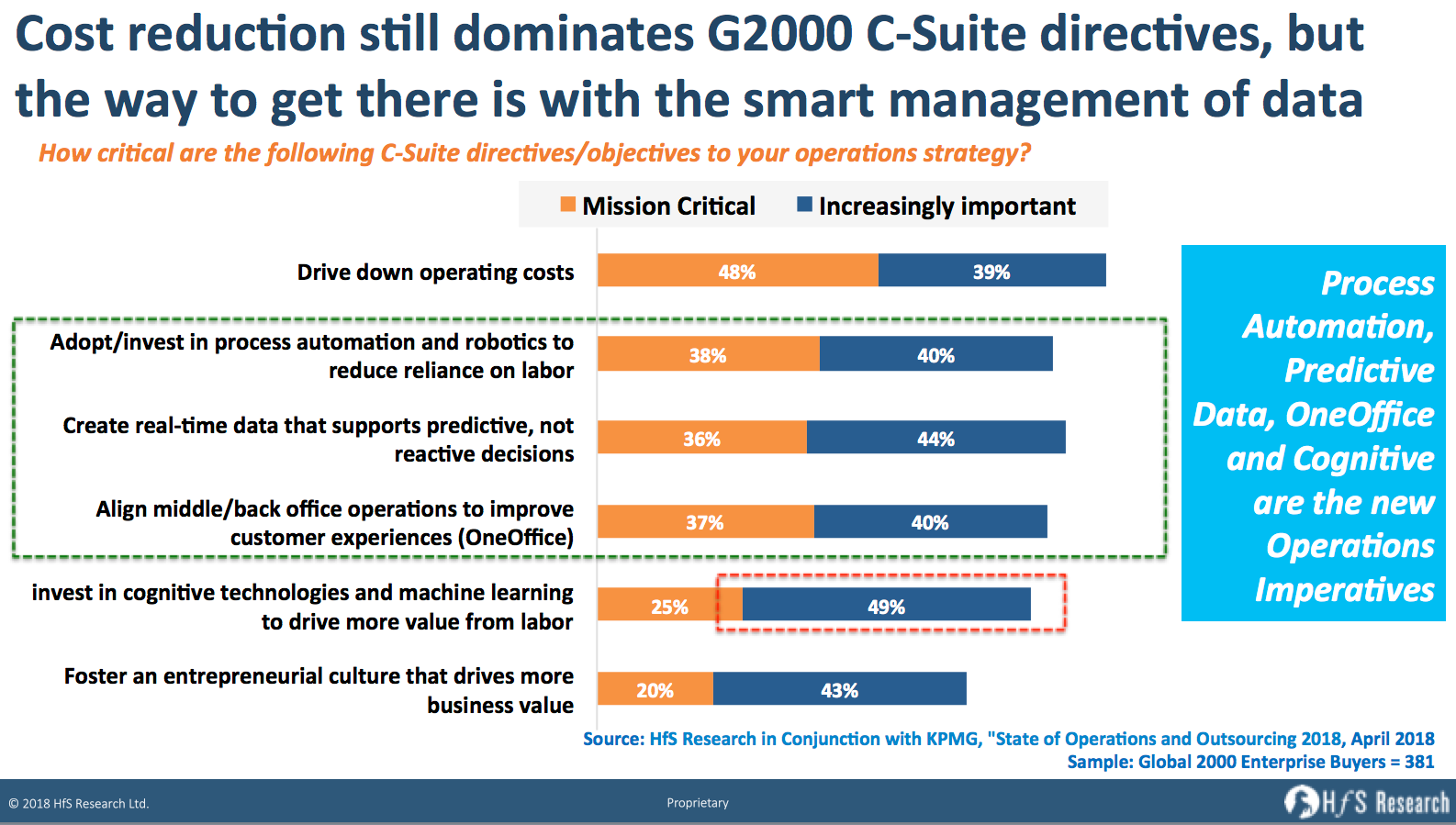

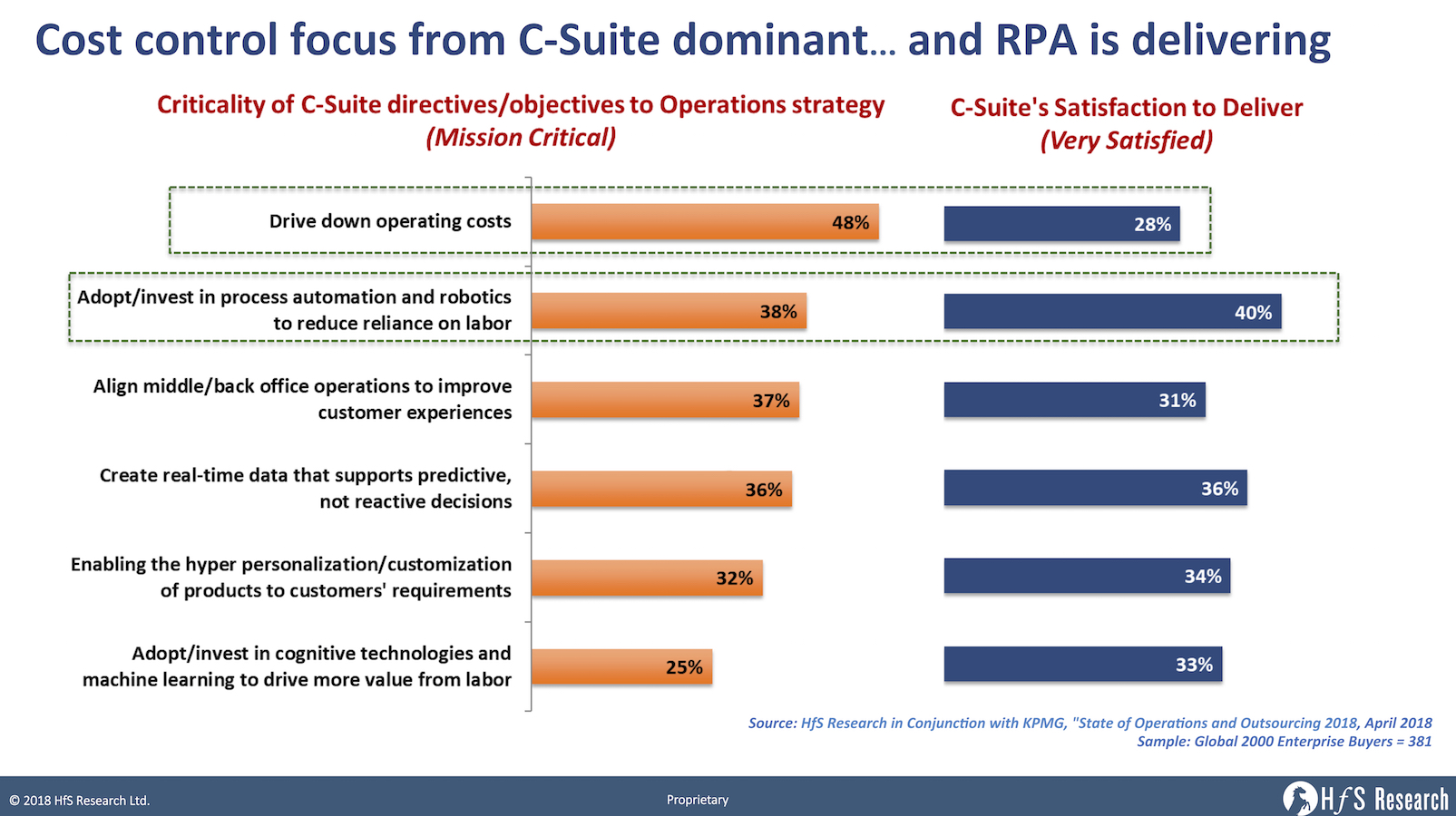

However which way we look at it, driving out costs from business operations still dominates the directives of C-Suites across the Global 2000 – just revisit our 2014 study to see how little has changed. Fast forward to today, and the only real differences, since then, are the methods to slake this thirst for cost elimination, as traditional operating models are no longer delivering much more than incremental value.

Our new State of Operations and Outsourcing Study, conducted with KPMG, covers the dynamics of 381 operations leaders from the Global 2000 and reveals these rapidly changing C-Suite directives to drive out their number one nemesis: cost.

Traditional cost savings models are running out of steam, as robotics, predictive analytics, OneOffice and cognitive become the new operating value levers

Little tweaks here and there to delivery locations and headcount allocations are becoming less and less effective, as it becomes clear only the fundamental rewiring of underpinning data repositories – and the digitization of manual processes – are going to progress operations to a place where real efficiencies can be enjoyed. In addition to fixing data and manual processes that clearly hit that old cost button, C-Suites are also recognizing the dire need have their customer needs being addressed by their employees as and when they occur (OneOffice), and also to invest more in cognitive tech and machine learning to drive more value from their current pool of talent:

Cost reduction mandates still fall well short, but expect to see them improve as data-driven initiatives bear fruit

The perennial issue here is clearly one where C-Suites rarely feel exhilarated by the cost reduction impact of their operations leaders. Of all their mission-critical directives this year (see above), none disappoints them as much as their ability to impact cost reduction (only 28% are very satisfied), while there are much larger numbers of C-Suite leaders already a lot happier with their robotic process investments (40% ‘very satisfied’ and a further 30% ‘satisfied’). However, as we continue to see this strong impact in these areas aligned to robotics, OneOffice, and predictive analytics, surely it’s merely a test of time until we see these initiatives having greater visibility, in terms of ironing out unnecessary costs and inefficiencies in the system.

The Bottom-line: It’s taken several decades, but our enterprises finally have no choice but to make fundamental changes to the very make up of their processes, data, and people if they are going to survive

Ever since my first blog 11 years ago (right here), we’ve pretty much repeated the same conversation that’s been continually refined over the years. The only game changers have been the gradual need for less people to run operations as cloud-based software platforms take-hold, offshore talent is optimized, and the more recent introduction of robotic process automation solutions to remove manual workarounds and create broader digital processes, that can be aligned with common business outcomes and metrics.

However, these changes are more fundamental than merely slimming down the number of cooks in the kitchen and making the food taste better: it’s forcing a complete rethink from ambitious firms to redesign operating frameworks where revamped business processes are enabling true digital business models, where emerging AI capabilities can be weaved in… where innovation is native to the culture of the firm and its people. Yes, it’s redesigning the entire kitchen, not merely hiring some better chefs with better recipes.

The toughest challenge is fixing many years of poorly-constructed data repositories, where the corporate IT ancestors that built them have likely long-since departed, and other IT stormtroopers from the midst of time have plastered on countless workarounds and spaghetti coding to keep the back end (somehow) functioning. These are the deep, murky areas where it’s frighteningly difficult for many firms to take the risk of investment and change to find their way out of the dark data ages. Somehow ripping out the very fabric of what got you here is what you may have to do to survive in the future… and that can be one very painful, risky and costly experience. Sure, you can keep papering over those yawning cracks, but the wallpaper just isn’t working like it used to…