Yesterday, you may recall we discussed the comments made by Nigel Barron, who spend 13+ years at CSC before the merger with HP (when DXC was formed). After nine months at DXC, Nigel was sacked. I was sad to see him go because he was one of the few folks in CSC who pushed hard to persuade its executives to spend time with HFS analysts (as opposed to Gartner, IDC etc). I remember Nigel would frequently share our work with his team and would put out some pretty cool insights.

Firstly, I would like to thank Nigel for excusing the behaviour of many people for acting like “nodding dogs” to keep their jobs. Secondly, I would personally like to apologize to Nigel for inadvertently portraying him as one of the nodding canine family, when, in fact, he is anything but. Nigel asked me to publish his explanation that he was actually sacked by DXC because he was fired for refusing to conform to the nodding brigade, daring to challenge a firm that (let’s face it) is in danger of drifting into insignificance.

“Hi Phil, thanks for the mention. I was the antithesis of the nodding dog at CSC/DXC, so much so that it probably contributed to my being laid off last December. I was a top five company internal blogger on the company’s collaboration platform writing blogs such as ‘The end of management’ and ‘Nowhere to hide’. My bosses kept the faith until the second round of layoffs occurred after the merger. My then boss had an easy choice to make when told to find someone to cut, although there were other circumstances that I won’t go into here (Mike Lawrie refers to ‘Pyramid corrections’ in earnings calls). I do sympathise with analysts who have become nodding dogs for the reasons I mentioned in my comment, but that doesn’t mean its the right thing to do. I’ll be 54 in a couple of weeks, I’ll never, ever be a nodding dog but I’ll always be a supporter of HfS, you and your team. Nigel”

If anyone from DXC is reading this, you need a few characters like Nigel who can shed some light on what your firm is trying to accomplish, as we – at HFS – are flummoxed with the whole premise behind this merger. Why remove the only people who can challenge you, just because you can? Good luck Nigel – feel free to share any of your views with us in the future, you are developing quite a sympathetic following. DXC is poorer for your absence and you deserve better, my friend. PF

After yesterday’s slightly risqué rant, I received an interesting comment from Nigel Barron (pictured) this morning, an avid follower of HFS over the years, who spent much of his career with CSC and subsequently DXC before recently going independent (and clearly off the leash and wagging his tail!):

“Since 2008 every job has become a hustle and analysts are no different. Authenticity is not a winning attribute. To survive, being the nodding dog is the difference between having a paycheck and not having a paycheck and when they’ve got mortgages to pay and kids to put through college truthful, honest and clear research might not be the best bet. That’s not to say its the right thing to do, just an observation. I speak from experience also.”

I refused to become a nodding dog. It’s simple if you keep at it…

Nigel Barron: Nodding Dog Sympathizer

Well, Nigel, I also speak from experience here. I used to work for Deloitte Consulting back in the day, and my lead Partner demanded I take my blog offline (having initially been fine with me continuing with it, during the interview process). The firm literally could not tolerate one of its consultants having freedom of thought and bypassing its painful thought police (aka “risk”) process. I eventually left the firm after that… I just couldn’t stomach an employer putting the muzzle on thought leadership. Especially mine!

A couple of years later, I was working for AMR Research (now part of Gartner) and a huge debate ensued among management whether “Phil should keep his blog up”. Many of the clients insisted one of the reasons they stuck with the firm was because of my blog, so money eventually spoke – they felt they got some real views of the industry and wanted to call me to discuss as part of their research contract. In fact, our Chief Research Officer, Bruce Richardson, at the time candidly said, “Let’s just let all the analysts blog, I can guarantee only 2 or 3 will bother”. Bruce was right. In fact, I think it only me who actually bothered. And then another boss decided to try and ban analysts using LinkedIn. My god… where do they find these people?

Amusingly, around that time, I went for a job interview with SAP (yeah OK, I wanted a Merc)… and the first thing the hiring SVP asked me was “Phil, you will keep your blog going, won’t you?”. I nearly fell off my chair – you’d have thought the Germans would be the first to censor free thought =)

Find an employer who lets you express your ideas and views. Otherwise just work for yourself. Or just be a nodding dog…

If you are a nodding dog who’s happy nodding away and taking home your paycheck each month, then I am very happy for you. Life is good. However, if you are bored out of your mind and are desperate to craft a living that utilizes your creativity, please get out of your predicament… for your own sake. The digital world is all about people with creative relationship skills and entrepreneurial capabilities. Nodding dogs can (and will) be replaced by automated ones… please don’t nod your way into unemployment.

Let’s face facts, the world is a digitally-scary place, and the only way to deal with it is to keep trying to learn more and keep talking to colleagues and peers in other firms about how to get ahead of this. Suddenly, we have become disposable assets and we need to keep reinventing ourselves to keep sounding like we’re up on all the new stuff. Suddenly, we live in a world where everything is about to be transported to the scrapheap of legacy professionals who can’t be retrained to do anything meaningful anymore. So keep nodding at your peril…

However which way we look at this, the real answer is that we simply don’t actually know what the future has in store for our careers, our companies, our economies, politics and our children, but what we can do is keep understanding the facts and keep sharing knowledge with other like-minded people… and the future will unravel before our eyes as we keep trying to make sense of it all.

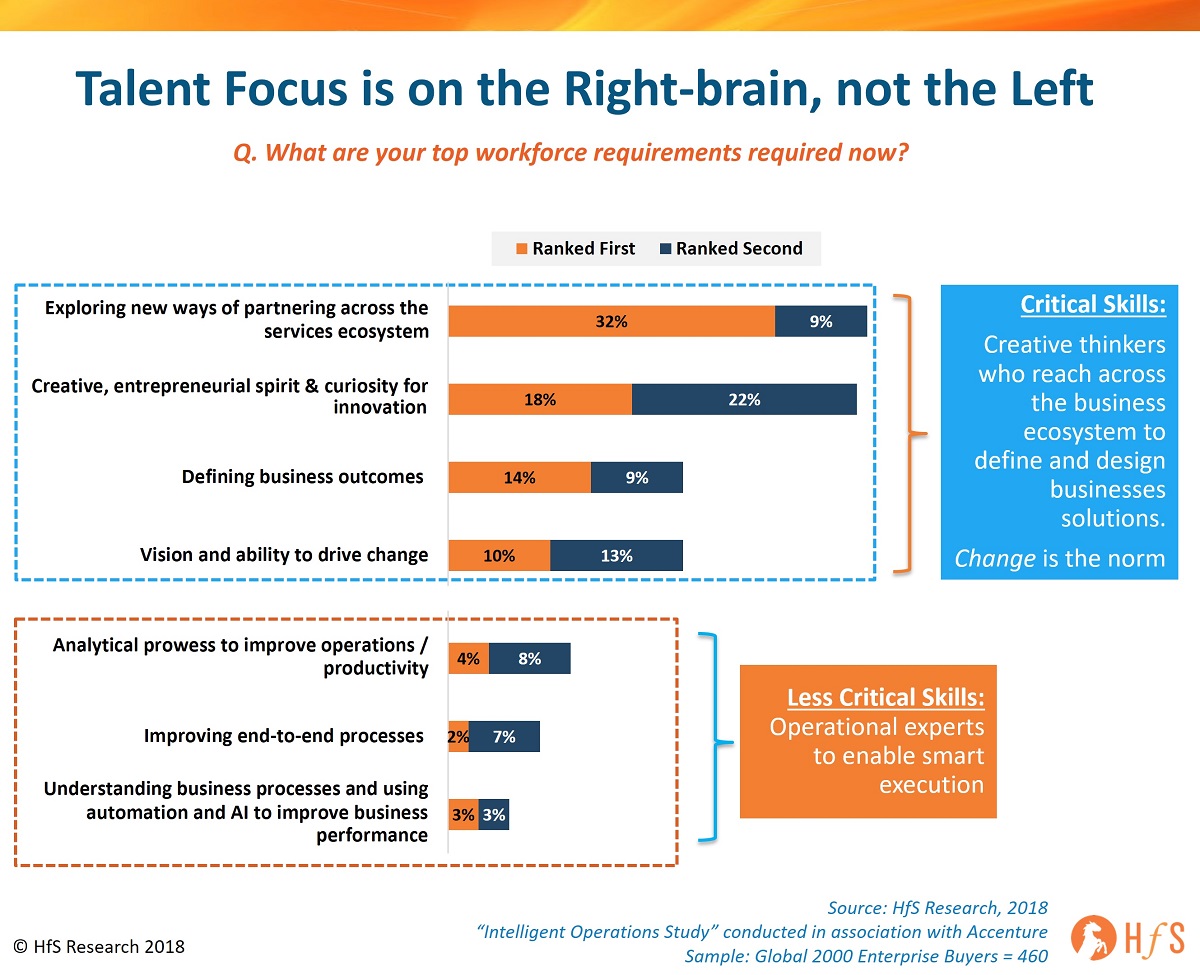

Our recent study on Intelligent Operations, conducted with the support of Accenture, which covers the views and dynamics of 460 global 2000 operations leaders, gives us some real insight into this shift towards the creative, curious types, with a thirst to learn and an obsession with networking and partnering:

The focus is heavily shifting to dynamic, entrepreneurial individuals who understand how to define outcomes

So if we’re one of these obsessively socially curious animals with a penchant for constantly knowledging-up on all the cool new stuff – and we love to talk partnerships with other companies in our network, the near future is actually pretty encouraging for us: our skillset now tops the list for what global 2000 leaders are looking. Leadership is under intense pressure to change the norm, to align their operations with the direction their customers are taking them. The wonks who spend all day staring at spreadsheets, focused on execution “left-brained” activities are less in demand – they need to learn how to wrap the needs of the business into broader processes that can cater to customers and support management decisions in real-time. Essentially, if your operations are not in sync with the customer-driven front office, you will likely fail. Yes, you need opinions, you need to speak up, yes you need to stop the nodding and find your inner digital mojo.

The Bottom-line: This is the new normal – leaving our comfort zones and getting out there to make stuff happen. End the nodding now!

It really is as simple as that – we’re all leaving that big comfortable world where all you had to do was turn up for work, do the same routine activities each day, go to the same mundane meetings and keep the lights on. We all know those days are leaving us behind, and if you’re under the age of 55, it’s unlikely you can plot that sneaky escape to early retirement… we’re living in a world where we need to learn about new technologies (you don’t need to code anymore), we need to share experiences and use cases with peers across the industry, and we need to reach outside of our cosy internal networks to talk through smart partnerships with tech firms, supply chain partners, customers etc.

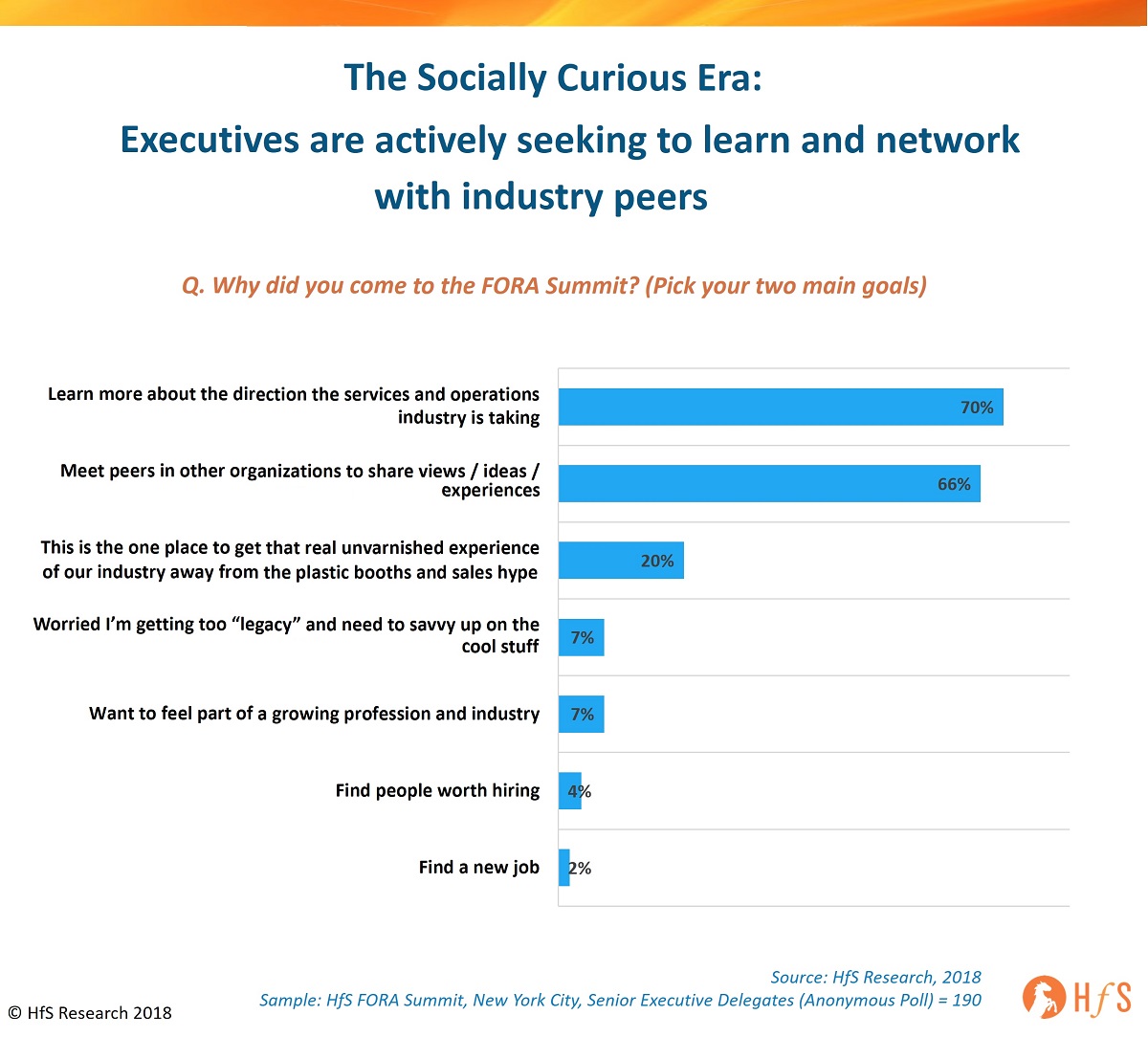

You only have to look at the reason 200 executives showed up at the HfS FORA Summit in New York to understand motivations have changed in an anonymous poll: they are going out to get educated and share experiences with peers. The days where conferences were all about job hopping are over – it’s more about how to stay relevant and ahead of the game.:

In essence, there is no written rulebook where this all leads – the world has become an uncertain place politically and we have yet to experience an economic downturn for many years. However, what is clear is sitting in a quiet office all day staring at your emails and nodding in a canine-like fashion is unlikely going to get you where you need to go next in your career. This is the age of getting networked, getting smart and learning from collective experiences. The only comfort zone is the one you make for yourself – being comfortable with the impact of change agent technologies and the experiences you can have working with them.

So let’s wage a war on the turgid dog nodding motherhood and apple pie, people… Ugh, it makes me want to curl up into the foetal position and reemerge in the 1960s… when thought was valued, and democracy was everything.

As an analyst, you spend your time with a lot of other analysts – for better or for worse. And, recently, worse is taking up more than its fair share. It just seems like, as an industry, we’ve lost our collective teeth, our ability to question, challenge and find out the truth. We’d even go as far as questioning whether we’ve lost out soul.

When HFS launched ourselves onto the market over eight years ago, the cornerstone of the firm was a blog that was revered as one place you could get the real truth about the industry, where people were safe to make a (gasp) controversial comment where we could all call a “spade a spade”. One industry leader (from IBM of all places) even went as far as describing this blog as the “Wall St Journal editorial section of the industry”. More recently, we’ve been called “Blue Collar” research, which I guess we’ll take as a compliment. Anything is better than being seen as fully paid and played by the dirty vendor dollar… which is sadly how so many recent pieces of “research” have been described.

Today, most analysts and advisors use hype as their comfort blanket – even if they don’t understand it, they just circulate it because it makes them feel relevant

Sadly, at HFS, we doubt we’d have succeeded with our honesty and bluntness if we launched today. The industry is too controlled by vendor marketeers who shower their lovely budgets at analysts and advisors alike to keep them all in line… where most just regurgitate the same hype as each other because they just don’t care anymore. Most barely understand the hype, but regurgitate it because it gives them a sense of security, a sense of belonging. It really is fucking sad, isn’t it?

Today, when you go into a vendor briefing packed with analysts, you’ll be confronted with row after row of nodding dogs, passively absorbing the hype, marketing drivel, and outlandish ‘thought leadership’ that has no bearing on reality today, let alone the future.

Yes folks, let’s face reality: vendor executives deliver lovely fluffy cotton candy the analysts and advisors gratefully inhale. No one seems to want to give anyone a hard time these days… it’s all PowerPoint bullshit being delivered to plastic smiles and nods of universal agreement, even though no one really has a fucking clue what reality is versus bullshit anymore. In fact, no one seems to care… they just keep nodding… like dogs. I mean how can you really be an expert in RPA when you’re spinning your wheels at conferences 13 months a year? When are you actually talking to real clients about real issues? Does it matter in this age of #fakenews?

Vendors just insist on nurturing the nodding dogs

Let’s give you an example. At a recent event on the “future of work” (yep… that old chestnut), a room jam-packed with senior analysts listened and nodded intently to a vendor expert proselytizing on the business benefits of pushing 70% of enterprise employees onto the modern equivalent of zero hour contracts. It’s scalable; enterprises can tap into talent whenever they want, reduce costs, all of the good stuff businesses have been desperate to do. Eventually, a couple of HFS analysts broke ranks and said ‘what on earth makes you think the labor market will accept that deal?’

I mean, honestly, it’s weighted so heavily in favor of the enterprise that if government regulators and unions don’t kick it in to touch, a massive disenfranchised labor force almost certainly will. But the simple act of challenging this line of thought was almost enough to cause the immediate ejection of the analysts. The look on the faces of the professionals from the vendor told the whole story – they hadn’t been challenged in such a long time they didn’t know what to do with it. The other analysts in the room stopped their nodding briefly with dazed confusion across their faces. I can imagine it was the same reaction a courtier would get if in the middle of a banquet they told Henry the Eighth he should stop eating so much and think about his cholesterol… or his gout For once, the nodding dogs stopped nodding and looked up in amazement…

We’re in a world where rocking the boat gets you quickly hurled overboard

There have been other occasions when plucky analysts have challenged the core narrative – at its worst, they’re ejected from the room. At its best, they have been picked on as a ‘negative person’ or someone who ‘hasn’t read around the topic enough’. The world we are building for ourselves is one in which analysts are just a collection of dullards with a single purpose – to toe the party line of whatever a vendor is telling them. Either that or be ostracised and ridiculed. You can see why keeping in the pack is a much more attractive prospect to some. Why rock the boat when you can nod like a dog and everyone leaves you alone?

In many ways, vendors are as much to blame as the analyst firms. A short while ago it became vogue to cram analysts into large lecture theatres and run presentation after presentation – “Thanks for listening to two hours of us running through our financial performance, now you’re suitably sedated we’ll tell you about cloud, automation, blockchain, AI, GDPR, et al. quick succession over the next five hours. Unfortunately, there will be no time for questions. Try and ask a question and you won’t be invited back. Thanks, have a great day and remember your earplugs and eye masks are stored under your chairs.”

This bred a particular type of analyst – the nodding dog – that silently sits at the back of the room, nodding reassuringly when anyone makes eye contact, and briefly types out a mirror image of what the vendor has splurged out on their slide deck. “Doing lots more digital huh? great, I’ll write that down and get it off to editing.”

Just take your money and nod like a dog, please

Now, this may seem like a vitriolic attack on the analyst industry as a whole – which is partially correct – but this is really a look at the series of factors that have slowly eroded the value that analysts can provide to clients. The days of clear, impartial insight that fuel business decision making on their way out unless we start fixing this industry now.

The biggest issue is that the analyst firms swimming against the current are the first to be snubbed by vendors looking for the immediate gratification the industry now offers them. Publishing something even lukewarm will see your inbox filled with demands for ‘rebuttal’. You can’t imagine the response to something which is openly critical. Ultimately vendors know this works, they hire pushy and aggressive AR people to drive their narratives into the skulls of analysts. The big firms, chasing the money, know not to fight back – drilling their analysts to nod politely and, crucially, not to write or say anything that could lose them the account. Take your money and nod like a dog.. and we’re all cool, right?

This short-termism is pillaging the credibility of our industry.

‘Pay to play’ has become an insult so frequently used that’s it’s lost all meaning. Like that family member we all have whose frequent profanity was shocking at first, but eventually became an endearing characteristic. Corruption, subjectivity and personal agendas have become the knowns that clients expect and budget for. Frankly, it’s a constant surprise that 2×2 grid hasn’t disappeared as quickly as positive interest rates did after the financial crisis. There’s no value in them anymore – and if enterprise decision makers know that, by and large, they’re sketchy and not worth consulting, why do them at all?

Our worst fears were confirmed in a recent dispute on LinkedIn, in which industry grandee’s defended research that contained none of the major players in a market as a better way of supporting buying decisions (although they went on to argue that these reports, paradoxically, have no role to play in informing sourcing professionals!). As a sign that the industry is doomed – as with a failing company where all assets are for sale in a desperate bid to eek out a few more months – professional credibility and the reputation of a firm are up for sale for a relatively small price tag

What business are most ”analysts” in these days? Not “research”, that’s for sure…

This is the question at the center of an existential crisis for the analyst industry. In recent years, business models have eroded from research and analysis to vendor PR and marketing. The proliferation of nodding dog analysts which serve only as a mouthpiece for vendor marketeers, and the production of research which only has market value as far as vendors are willing to sponsor it has pushed analyst firms further and further away from the core mission of the industry – to inform clients. For some, the journey back is too long and arduous – they may as well throw in the towel now, or just honestly label their output as marketing fluff. At least they’ll be able to claw back some credibility for owning up to the true nature of the business.

For others that have drifted less, they must ask themselves ‘what business am I in’. If the answer is anything other than to provide clients with truth and clarity, sorry – you may as well phone it in as well.

The tragedy is that the current analyst market incentivizes the nonsense. For guaranteed business revenue and analyst bonuses, it adds up to pump out the same hype that we are supposed to be cutting through. Blockchain and AI hype trains are mandatory for most analysts if they want to get paid. And the easiest way to join in the conversation without needing to do any actual research is to circulate what vendors are saying. Even I’ll admit that it’s easier to find free time as a researcher if you don’t need to do any research.

But this dynamic simply can’t continue. The type of people that consume analyst research are, save some exceptions, exceptionally intelligent people. As soon as they start seeing the same crap from analysts as they get from vendors – the type of drivel that doesn’t tie up with how their business works – then they’ll stop reading and listening. It’s a simple as that. Even the most remote watering hole in the desert will stop being visited by local wildlife if it gets filled up with sewage and shit.

Bottom Line: If things don’t change soon we may as well close up shop and join a circus. Assuming we’re not in one already.

So as an industry we need to keep asking us what business we’re in, who we’re serving, and why we’re doing the things we do. Luckily, at HFS we’ve built a community of candid, and often ruthlessly honest analyst, buyers, enterprise leaders, and advisors. While other vendors and analyst firms are stifling the voice of dissension, we’re giving it a loudspeaker. Because if we’re not producing truthfully honest and clear research – then we may as well jack it in as well and join a circus (or move to the part of the industry that’s already become one.)

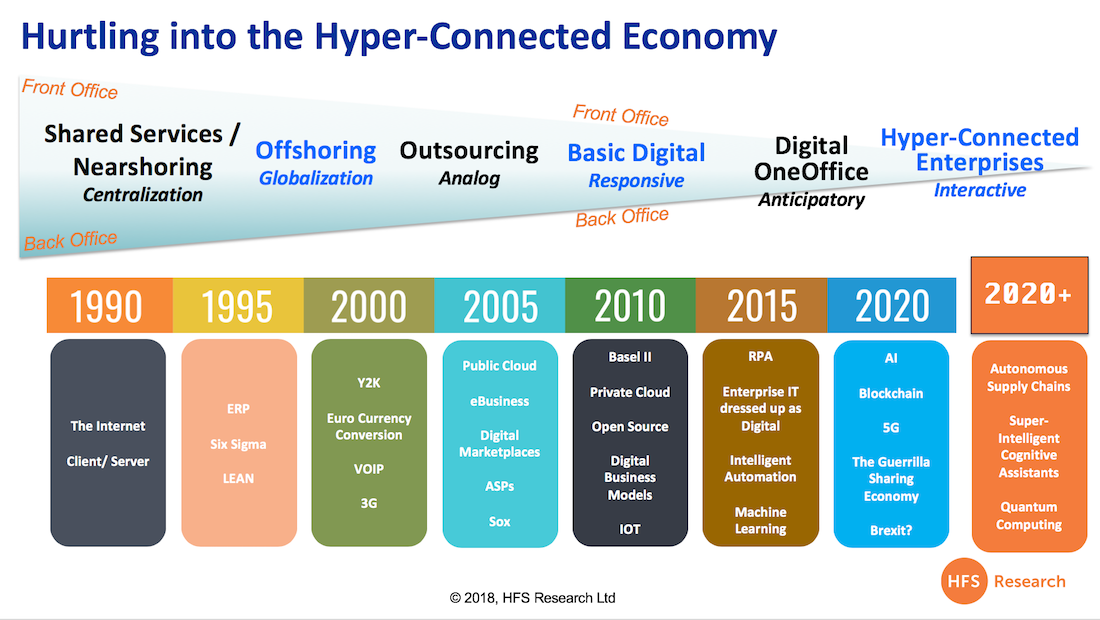

As business operations have advanced through several inflections points over the last three decades, the core component at the heart of these changes has been the emergence of digital interactivity driving the hyper-connected global business – only made possible by intelligent automation.

Digital connectivity has transformed both front and back offices over the last three decades. The key now is to integrate and automate these activities to place the customer at the core of business operations

As you can see in our (below) “voyage to hyper-connected, interactive enterprise” we have leveraged digital connectivity to drive productivity and innovation across both the back and front offices of our organizations. Offshoring and outsourcing became a huge bi-product of digital connectivity to run business processes and apps remotely to save Western businesses huge costs through global labor and centralization of resources.

However, until recently, most of these activities have been restricted to improving efficiencies and reducing costs. At the front end of the business, the advent of ecommerce hit its stride in the late ’90s, where customers could communicate digitally with organizations to make purchases, make genuine inquiries and get connected with others with like-minded business interests. Where automation comes into play is being able to pull together these disparate front and back office activities into one single office (aka the HFS Digital OneOffice), where customer needs are placed front and center across all business processes, where staff performance can be measured on delivering customer driven outcomes, where the entire business operations are in-tune with their customer needs… and superior to those of their competitors to stay ahead of the game.

The urgency to be Hyper-Connected dictates why we have to drive Automation with real Intelligence

“Basic digital” capabilities (where most companies are today) make it possible for business operations to respond to their customers as those needs happen. Emerging capabilities in data analytics tools, machine learning and cognitive computing are making it possible to anticipate changing customer needs before they happen, where shifts in global supply chains, market and competitive dynamics, economic or political changes, compliance or regularity issues, all combine to change customer behavior.

The more intelligent your business operations, the more you can stay ahead of the game, but none of this is possible if your processes are not automated effectively to create this knowledge for your business operators:

Once the digital baseline is created, enterprises need to create more intelligent bots to perform more sophisticated tasks than repetitive data and process loops. This means having unattended and attended interactions with data sources both inside and outside of the enterprise.

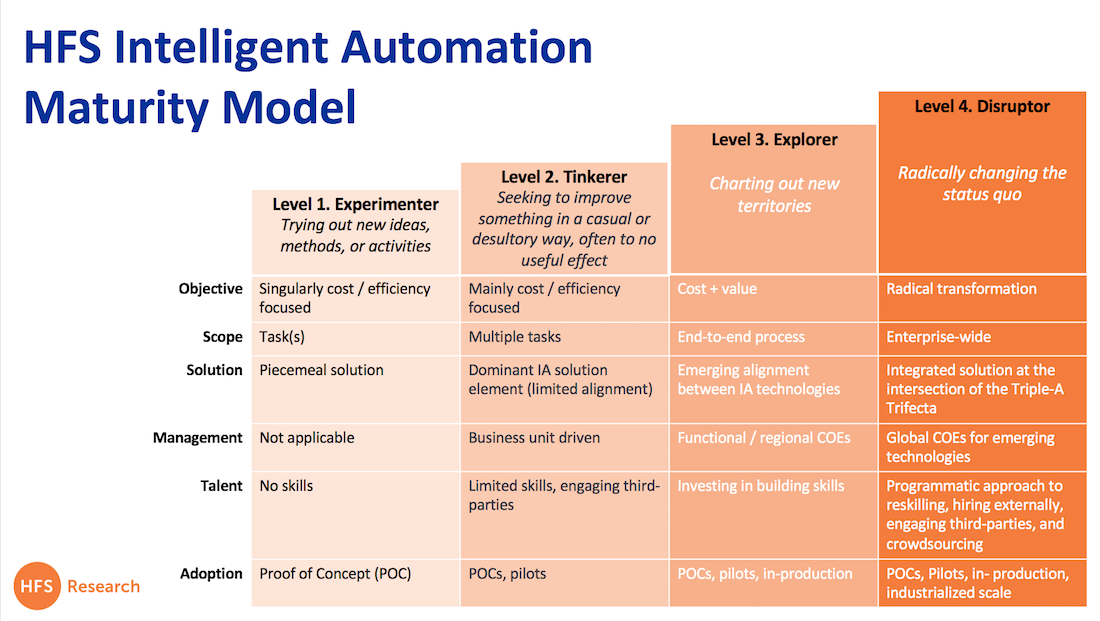

From Experimenting to Disrupting: Cracking the Intelligent Automation code in Four Stages

The industry is struggling to solve challenges around the process, change, talent, training, infrastructure, security, and governance. There is deafening noise and hype around Intelligent Automation, but there are very few enterprises that have cracked the code of driving transformative impact by leveraging Intelligent Automation at an industrial scale. Why?

Our research and ongoing conversations over the last six years (remember our ‘Greetings from Robotistan’ in 2012?) in the automation space has allowed us to interact, help, and follow automation initiatives at several global 2000 enterprises. And we leveraged this extensive experience to develop HFS’ Intelligent Automation Maturity Model (see exhibit below). Our experience suggests that the organizational maturity and the resultant impact from intelligent automation typically follow four stages of evolution:

The experimenter – trying out new ideas, methods, or activities. The intelligent automation journey often starts with some maverick individuals in some corner of the organization playing with different technologies. There is no real strategy at this stage, just passion. The objective is simply driven by automating a particular task that is innately boring or transactional but still time-consuming and inefficient. Different experimenters start at different places across the Trifecta. It is not necessary to start with basic automation and then advance to AI-based automation, but experimenter’s automation solutions are typically piecemeal.

The tinkerer – trying to improve something in a casual or desultory way, often to no useful effect. The early successes from experimentation often result in the most frustrating stages of the intelligent automation maturity model. The tinkerers start to copy and paste what worked in experimentation for everything else. But if all you have is a hammer, everything looks like a nail. Failures are widespread at this stage, but tinkerers who don’t give up are the ones who eventually succeed to move to the next step. This is the stage where enterprises are trying to find some method to the madness but often with limited success. The tinkering stage is exemplified by rhetoric winning over reality!

The explorer – charting out new territories. As reality dawns after extensive tinkering, enterprises start to realize the different pieces of the puzzle. They start investing in organizational management (often through COEs and a hub-spoke model), recognize that they need to invest in multiple technologies across the trifecta to solve problems and start tackling end-to-end processes versus individual tasks.

The disruptor – radically changing the status quo. Intelligent Automation transcends from a program and becomes an enterprise-wide movement at this stage. Disruptors can bring to bear integrated solutions that combine the power of automation, analytics, and AI. Several automations at this stage are scaled up, and there is a high degree of confidence in scaling up others. It is only at this disruptor level when the promise of intelligent automation starts to become a reality.

The Bottom-Line: The more hyper-connected we get, the more this is about people, purpose, and planning – and less about whichever shiny new gadget is the flavor of the month

While the industry is busily adding fancy new words to their résumés and job titles, we have to remember that our technological journey is gradual. Change comes slowly and incrementally and you can’t just rip off the proverbial BandAid, hire a bunch of Millennials and Gen-Z kids… and it’s mission accomplished. As the Hyper-Connected journey illustrates, it took 30 years to get where we are today – and that’s because both front and back offices needed to go through major, secular changes to become efficient and digitized.

But the next phase is not a trade-secret – this “Future of Work” is merely a phased transformation of the present. Dumb robots evolving into intelligent assistants… ineffective supply chains plagued with manual breakpoints becoming fluid, autonomous and intelligent – with the ability to interact with other supply chains. Quantum computing and blockchain emerging to challenge the very logic of TCP/IP and computing architectures. But to get there, we need to be experimenting, tinkering, exploring and disrupting with the kit that available today to get our organizations in a place where all these far-flung innovations can have some real possibilities.

So let’s have less talk about the future of work and focus on the present… we know where we are and what we need to do. So let’s do it!

What is wrong with us old timers these days? We go to conferences where we make sure no one under age of 40 comes near the place, and we spend half our time bemoaning the lack of a “digital mindset” from our colleagues because we all have these world-class digital mindsets ourselves. And can someone please explain what the f*** a digital mindset actually is? And can someone explain why everyone blathers on about their company’s inability to change with the times, but never admit they don’t really want to change anything either…

But let’s be honest, we treat our beloved Millennials like some sort of obscure species whose members only communicate digitally with each other, like to wear these really big expensive headphones, drink far less than we did at their age, and no longer go to bad discos to find romance. Not to mention an unhealthy love of avocado toast that helps their quest for a purpose in life because of failed parenting strategies leaving them permanently depressed because of low self-esteem.

In addition, we’re now accusing them of lacking ambition and only caring about their next vacation. But how can we blame these poor folks from feeling like we stitched up the world before they came along… as most cannot come close to affording the cheapest shoebox in any half respectable neighborhood, the poor folks in the UK are going to get cut off from working in Europe soon, and the lost Millennial souls in the USA had to choose between two septuagenarians as their president, who hardly represent the emerging mindset of the digital youth (even though you do have to be impressed with the President’s twitter skills…).

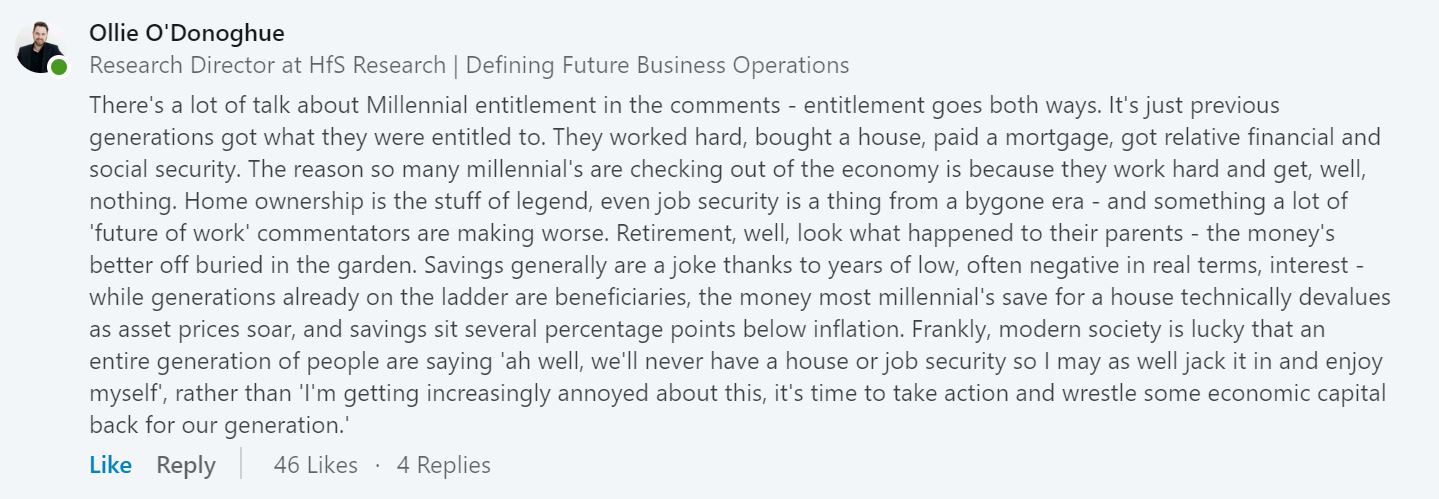

So imagine the refreshing impact when HfS analyst Ollie O’Donoghue, a proud representative of the Millennial race when he’s not trying to annoy Amazon, piped up on LinkedIn with the following staunch defense of his species:

The Bottom-Line: Love them or loathe them, Millennials are the Future

So to quote Ollie directly: “Entitlement goes both ways. It’s just previous generations got what they were entitled to. They worked hard, bought a house, paid a mortgage, got relative financial and social security. The reason so many Millennials are checking out of the economy is because they work hard and get, well, nothing. Home ownership is the stuff of legend, even job security is a thing from a bygone era – and something a lot of ‘future of work’ commentators are making worse.” So let’s use this opportunity to bring Millennials into our inane conversations about a future of work with less need for people, about our businesses being persistently disrupted by imaginary digital competitors, about blockchain’s emergence to destroy whatever we have left… because if we don’t, we’ll have a big hole left in our corporate legacies that we’ll struggle to fill, as all the talent will be checked out on the beach dreaming of their next avocado latte.

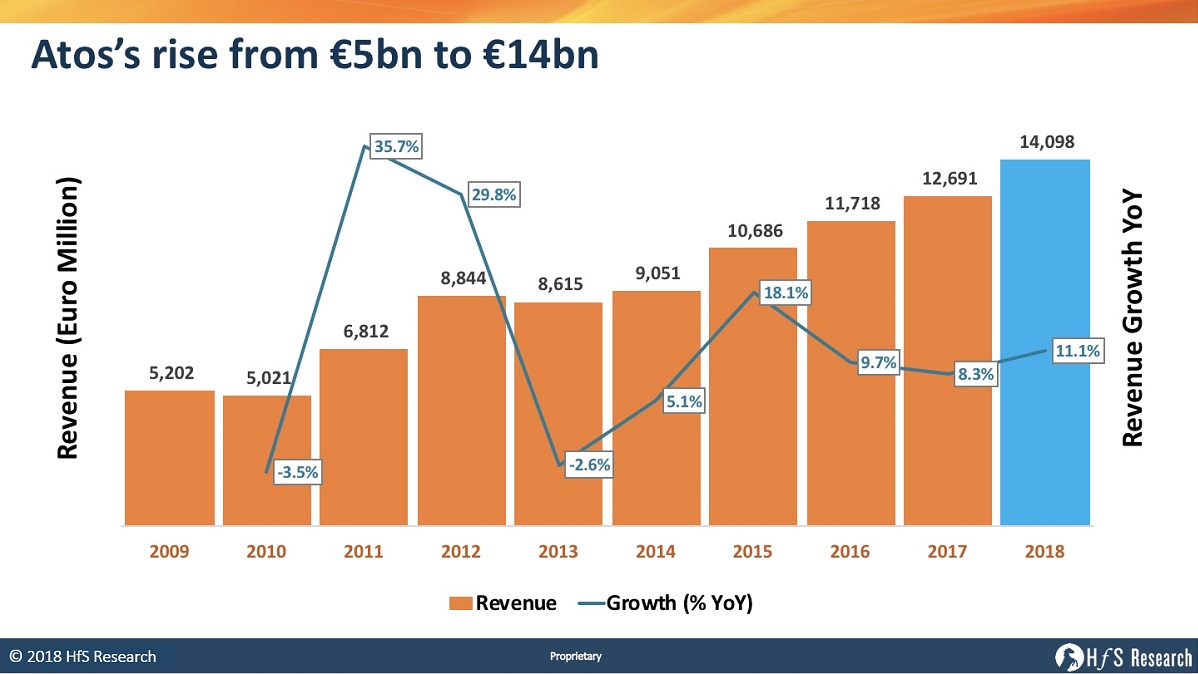

Syntel brings to Atos a larger platform into the North American market, stronger IT automation capabilities to augment its data management and analytics heritage and, above all, access to quality long-term engagements. And not to mention a mighty Indian offshore IT depth that fills a lot of delivery holes for the firm. And don’t forget, this firm tends to know what it’s doing when it comes to acquisitions and making them work:

However, even with all this combined, $3.4bn seems like a hefty price to pay, albeit a price that will likely set both industry valuations, and other acquirable mid-tier service provider hearts’ racing. Not only that, competitors with banking pedigree, such as Capgemini, Cognizant, DXC and IBM will not welcome a stronger Atos being welcomed to the dance at a time when competition is already reaching a cut-throat breaking point.

We haven’t seen any meaty M&A in IT Services for over two years… So why now?

We’ve been predicting an increase in merger and acquisition activity across the business process and IT outsourcing space for some time, but these IT services monster marriages are like London buses – you wait ages for yours to arrive, and suddenly several appear right behind it.

Let’s be realistic, there really aren’t too many “heritage” mid-sized offshore-centric IT services providers left in existence which can get you an immediate seat at the adults’ services table, which explains Syntel’s fantastically lucrative exit, and the disappointment of several other suitors which had been eying picking the firm up on the cheap for several years. Moreover, providers like Atos are feeling the pressure like never before to force their way forward in terms of growth and breadth of offerings and believe the pressure point has been reached and it’s time to act.

A drought in traditional client wins for some firms is literally pushing them to acquire as a way to drive market share. The IT services industry is no stranger to firms buying out rivals to gain short-term respite from the market in the face of poor market performance – buying time to regroup/transformation, an injection of new clients and scale.

Atos’ recent announcement of its intentions to acquire Syntel has already set tongues wagging in the industry, but before we get caught up in the inescapable hype, let’s dig into the facts!

At $3.4bn this could be the start of the M&A silly season where “Everyone’s up for Sale”

It’s hard not to get lost in the number of zeroes in this deal and, frankly, the price tag has left us all scratching our heads a little. At a recent press conference, an investment analyst asked whether Syntel was happy with the deal…why wouldn’t they be? And it’s this sort of seller’s market that’s getting a lot of the mid-tier firm’s excited about a potential takeover from a major firm in the space. “Everyone’s up for sale” proclaimed the CEO of the of the leading service providers recently in a private conversation.

With some of the world’s biggest IT services firms looking to shore up revenues, capabilities, and access to clients, a lot of firm’s are adjusting pricing expectations, setting the bar far higher than they would have a few years.

And the market is undeniably tough right now, and many firms are struggling to find their way. Recently, brighter horizons have been on the cards for some firms as the HFS Digital tipping point theory started to yield results, with enterprises investing in technology to drive their transformation ambitions. But the same theory argued that many firms would struggle to pivot their business models and offerings to meet the changing demands of the market. In this winner takes all market, it stands to reason that firms will shore up their capabilities through acquisition, at the same time that smaller firms that struggle to gain market traction become more attracted to the idea of a buyout.

Is chasing a “$250m a year synergy target” realistic, or just merger charm?

But, according to Atos, the hefty price tag is supported by some strong arithmetic. The firm stands to gain access to a lot in the deal, including strong long-term banking and financial services engagements and a decent launchpad into North America – a geography the firm has struggled to position itself in from its European stronghold – in spite of its 2014 acquisition from Xerox. But let’s start with what the firm has championed as the main selling point to investors, a $250m boost to annual revenues by 2021 from the synergy of the two firms.

On the face of it, this seems a challenging target to hit. Revenues in Europe have been hit just as hard as everywhere else in the IT Services space, more so in Atos’ strongest line – infrastructure and enterprise cloud. And Syntel’s revenue growth has disappointed financial analysts for years – even if its operating margin is aspirational to many. If the firm can export Syntel’s processes and embed them across Atos, it may stand to drive greater operating margins. Moreover, if it can leverage Atos’ Syntbots RPA technology in new and existing engagements, it could drive out some serious costs. But an increase of $250m a year is perhaps a little more ambitious than the numbers can accommodate. Even with Atos assuring investors that if its current bookings stay put, it should be more than capable of reaching its objectives.

The real motivation behind the price tag is likely to be tapping into Syntel’s existing client base and cross-selling between the two firms. In the current market, where new deals are few and far between, the adage of ‘if you can’t beat them, join them’ has never been truer. For the princely sum of a few billion dollars, Atos has gained access to some major financial institutions and enterprises that Syntel has managed to keep on its books for years (over 30 years in some cases). And many of these are big spenders, Syntel is always pleased to mentions that it has grown a handful of its clients to build out up to half of its overall revenues.

However, the challenge for Atos is to keep these clients happy. We’ve chewed over the pitfalls of some of the major M&A activities in recent research. And in many cases, these clients may be even tougher to please. Syntel’s ‘customer for life’ no questions asked approach has built a fervent loyalty among its client base – while its too early to say now, the sentiment from this client base may prove to be less than enamored with the recent announcement than either Syntel or Atos are willing to admit.

It is also worth pointing out that the oft-stated criticism of Syntel has been its overexposure to a small handful of large clients, should one get acquired or kick them out. However, with a massive new owner in Atos, surely there is now some air cover from this long-discussed risk.

A nice deal for Syntel’s shareholders, but what’s in it for the clients?

As usual, the bit that’s often missed from the narrative when a big deal like this rears its head is ‘what’s in it for clients of both firms?’ At an early stage like this, we can only be speculative, but there are a few things that enterprise clients of both firms should be cautious and excited about. First of all, for Atos clients, there is the opportunity to get your hands on some real RPA capabilities. Atos has struggled over the past few years to find its place in the market, but Syntel has positioned itself nicely with Syntbots – an intelligent automation platform that while lacking some of the bells and whistles of the others has proven itself time and time again to be a solid cost-reducer. Existing financial services clients can also look forward to more verticalized expertise, and a stronger proof-point around delivery as Syntel brings in its considerable experience to engagements. Finally, Atos’ multinational clients can consider leveraging some of Syntel’s North American and Indian delivery capabilities to expand engagements or move work closer to home or further offshore dependent on the circumstances.

For Syntel clients, it’s a different kettle of fish. Foremost on their mind must be the protection of the partnership culture they have become accustomed to. That’s not to say Atos is miles from the culture of Syntel, but long-term partnerships have been the building block of the mid-tier firm since its inception and may be a tough hurdle to overcome after the firm’s combine. But they can expect some of the benefits that the firm will bring, such as strong credentials in the enterprise cloud space, and the scalable heft that a larger provider can offer over mid-tier players.

Bottom Line: Market conditions and appetite for acquisition mean we’re sure to see more activity like this in the future

Ultimately, there’s a lot of areas where the two firms can create synergy, and cross-sell offerings into each others client bases. But there’s also a huge amount of risk that this engagement is akin to the appetite of the day, which is to stop trying to outbid rivals for engagements and simply buy up rivals. In some of these engagements, clients may come out on top, with access to more experienced and capable delivery partners – but equally, they could lose out on the cultural alignment, and agility that they looked for in a smaller partner.

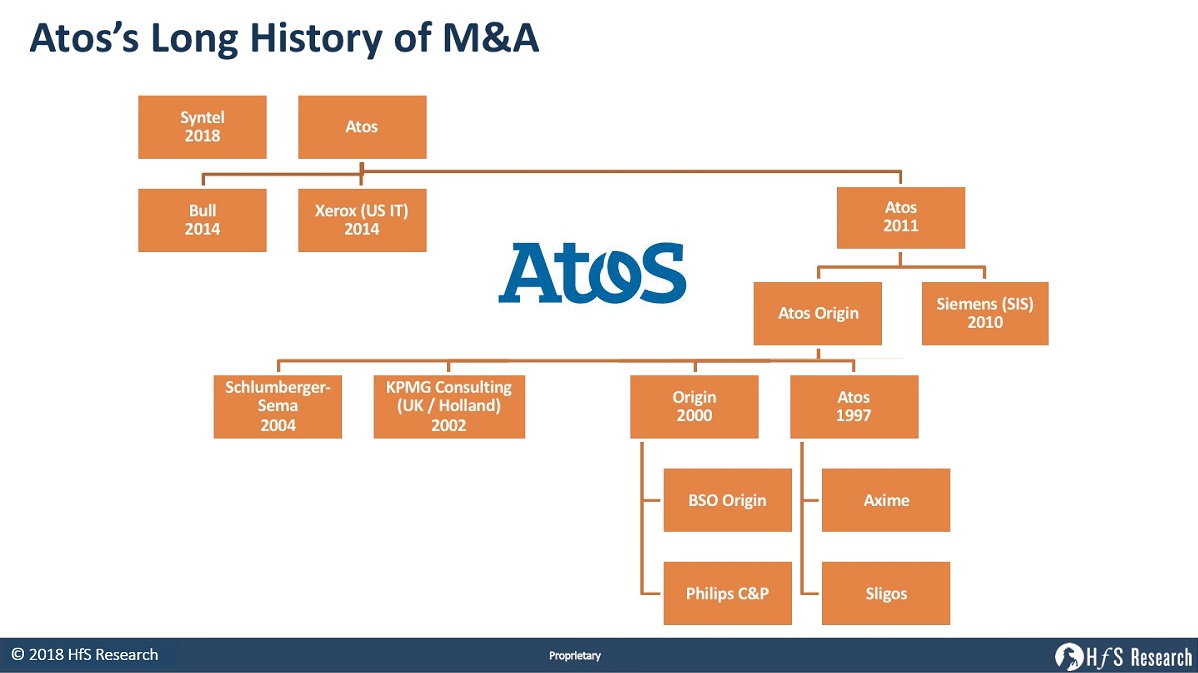

However, Atos management has a historically strong track record for acquiring and integrating business in both the long and medium term. The firms have a long history of large acquisitions across borders and huge integration challenges, starting with Origin in 2000. Plus we see relatively successful integrations of Siemens Business Services back in 2010, Bull and Xerox IT Services in 2014. Indeed you can trace it’s acquiring prowess back to decent purchases of SchlumbergerSema in 2004 and UK and Dutch KPMG Consulting business in 2002.

The issue as ever for successful acquisition is making the most of synergy – so that the whole organization is greater than the sum of its parts. This is always a hard trick to bring off measured financially, by the value it can deliver clients and increasingly important, culturally. If the financial boost is only $250m on a $3.4B investment let’s hope gains in the last two are worth it.

What does this say about future mid-tier IT services acquisitions?

The fact remains that in spite of the turbulent market we’re now in, Syntel has attracted a big price tag. This can only mean many of the larger firms are on the acquisition trail. Which means this is unlikely to be the only major M&A activity we’ll be seeing in the coming months. Possible mid-tier targets we can expect to come under the spotlight of some of the big players (if they’re not already) include:

Hexaware – possible price tag $1.50 / $1.25bn: Hexaware is gaining ground quickly and building a narrative that seems to resonate well with clients – however the firm remains small enough for some of the bigger players to see it as a valuable route to inorganic growth. Has good hybrid BPO and IT capabilities, a strong specialization in HR Tech and promising potential in RPA services.

Mindtree – possible price tag $1.75 / $2.25bn: Mindtree has had a scratchy few quarters at the start of 2017, but since then have posted rapidly improving revenue growth – over 20% in Q2 2018. The firm’s strong digital offerings make the firm a good prospect for bigger firms looking to shore up capabilities as well as build out market share. Has managed to make a strong shift from BI and analytics to adding digital prowess and has a capable suite of offerings and loyal clients to boot.

Mphasis – possible price tag $2.25 / $2.75bn: Has made a strong market impact since freeing itself from a decade-long HP hell… plus CEO Nitin Rakesh is credited a lot for his fine work at Syntel, getting the place in better shape financially. Strong financial services presences could make this firm the next IGATE/Syntel-esque pick up.

Virtusa Corporation – possible price tag $2.00 / $2.50bn: Virtusa’s strong consulting background – gained from the acquisition of Polaris – puts this firm as a valid target for large providers looking to build up talent and onshore delivery capabilities in North America. Very strong offshore business built from the ground up by the irrepressible Kris Canakeratne, with deep presence in insurance IT.

Yesterday, you may recall we discussed the comments made by Nigel Barron, who spend 13+ years at CSC before the merger with HP (when DXC was formed). After nine months at DXC, Nigel was sacked. I was sad to see him go because he was one of the few folks in CSC who pushed hard to persuade its executives to spend time with HFS analysts (as opposed to Gartner, IDC etc). I remember Nigel would frequently share our work with his team and would put out some pretty cool insights.

Yesterday, you may recall we discussed the comments made by Nigel Barron, who spend 13+ years at CSC before the merger with HP (when DXC was formed). After nine months at DXC, Nigel was sacked. I was sad to see him go because he was one of the few folks in CSC who pushed hard to persuade its executives to spend time with HFS analysts (as opposed to Gartner, IDC etc). I remember Nigel would frequently share our work with his team and would put out some pretty cool insights.