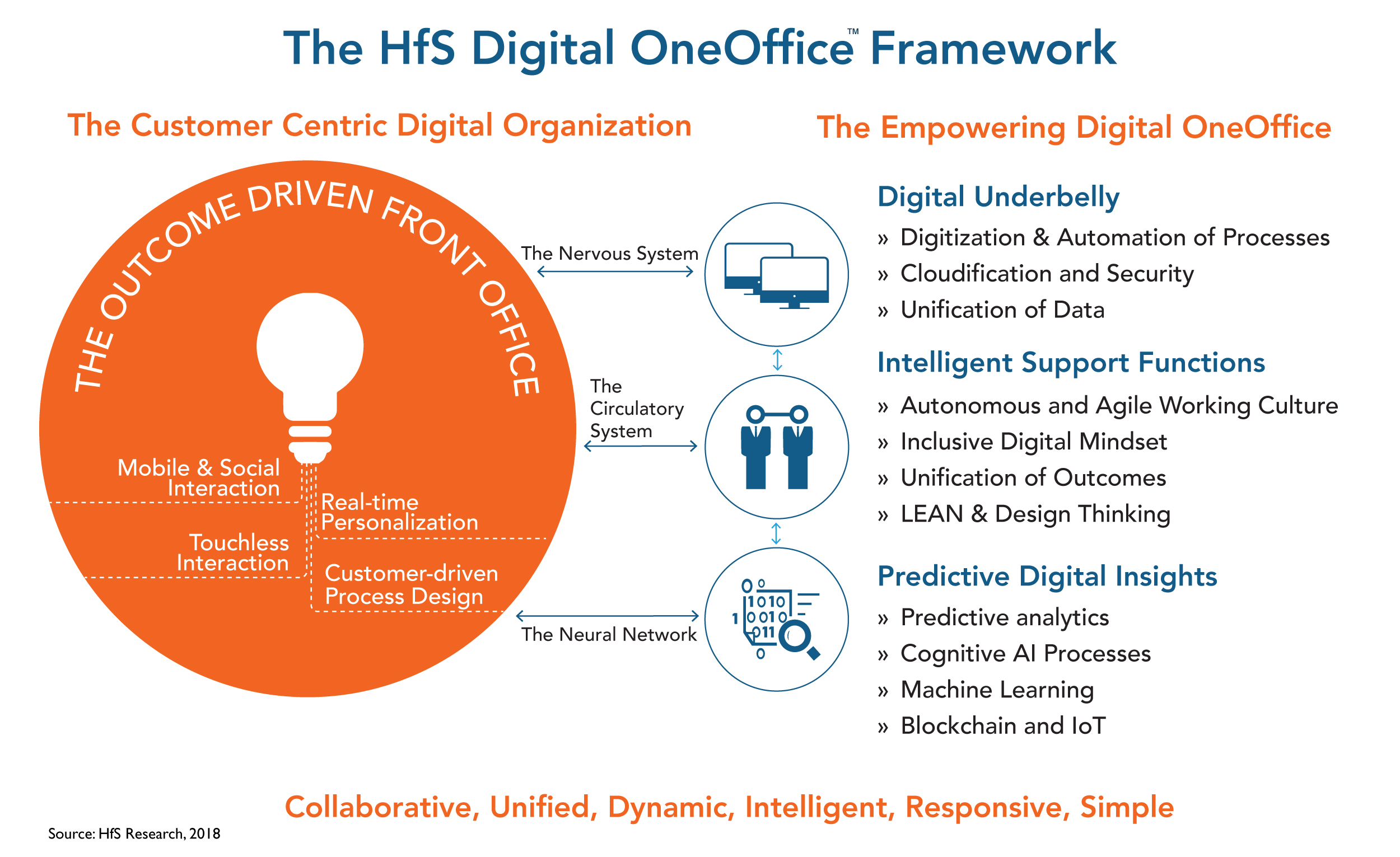

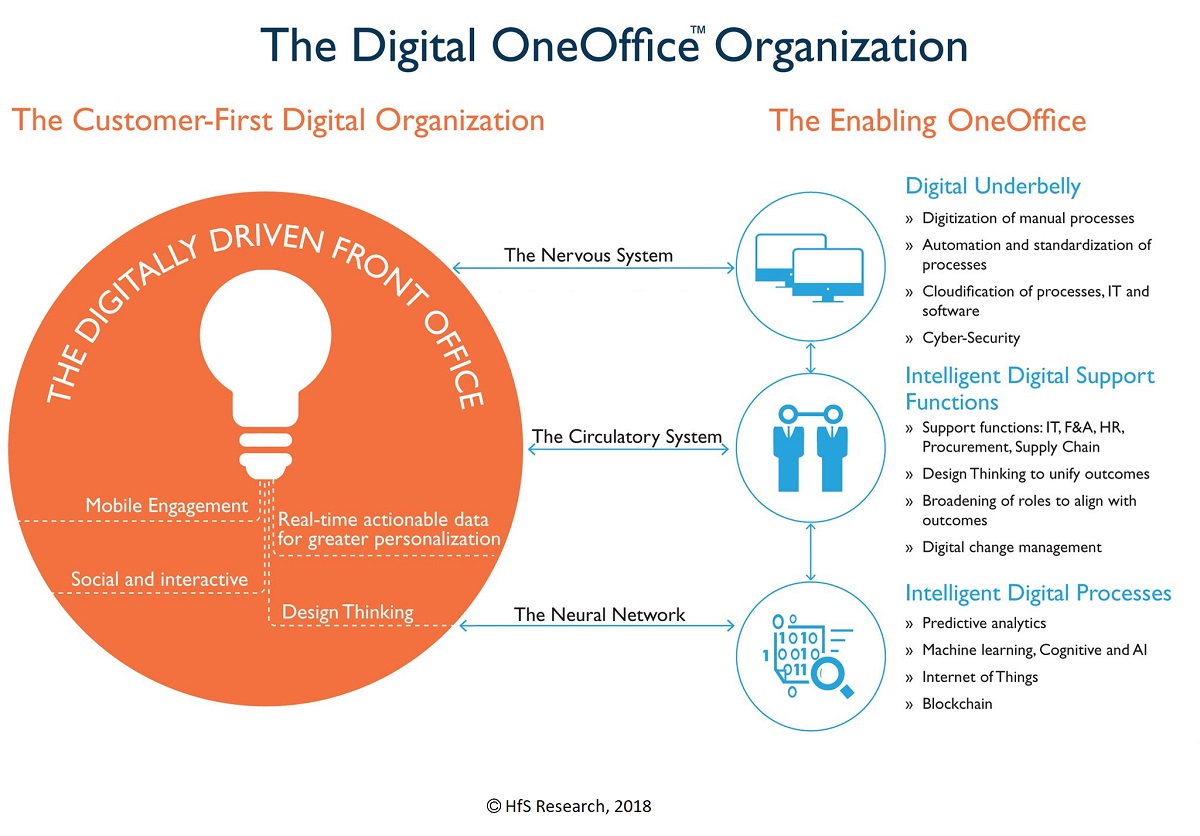

We’ve talked a lot about the HfS Digital OneOffice operating framework – it’s the HfS vision for the business operations endstate for digital organizations:

The Digital OneOffice is where teams function autonomously across front, middle and back office functions to promote broader processes with real-time data flows that support rapid decision making. It’s where front, middle and back offices will cease to exist, as they will be, simply, OneOffice.

Why Digital OneOffice?

Digital organizations must have an operating framework that maps out how they have to operate in the future. Traditional operating models, while creating some incremental productivity value if managed effectively, struggle to drive the unification of digital business models with emerging technologies across a business’s operations:

A true digital business cannot succeed without unifying front, middle, and back office

Traditional approaches (organizational restructuring) have failed to have a purpose beyond incremental efficiency / productivity

The Digital OneOffice is the organizational end-state to survive and succeed

What is the Digital OneOffice?

The Digital OneOffice focuses on real-time customer and employee engagement. OneOffice is:

Collaborative (Collective outcomes)

Unified (Without silos and hierarchies)

Dynamic (Agile and scalable)

Intelligent (Predictive, not reactive)

Responsive (Real-time)

Simple (Touchless and autonomous)

How to achieve Digital OneOffice?

The Digital OneOffice is the framework for achieving a true digital organization:

CX is not just fancy UI. Make CX the core of all your business operations from front to back. Cost reduction is not a strategy. Drive organizational alignment and metrics that measure value creation, not only cost reduction. Weed out the people unprepared to change. Invest in an inclusive talent strategy, based people who want to learn and share. Your tech infrastructure is everything. Automate, digitize, cloudify, and secure your organizational underbelly. Build co-innovation relationships and shed legacy relationships. The partners who got you’re here may not be the ones to take you where you want to go. Stop kicking the intelligent technology can down the road. It’s all here and now you need to make decisions on where you go with it Stop thinking about the Future of Work. It’s already here…act now!

The Bottom-line: Traditional operating models have been focused on incremental improvements, not creating genuine frameworks for digital organizations

While traditional models such as outsourcing, shared services and global business services promote incremental efficiencies based on centralization of support functions and use of offshore to lower operating costs, none of these models have provided an ideal endstate for ambitious digital organizations. Without having a true picture of how you want to operate in the future, you will be perennially be searching for short-term fixes to drive out further costs, and never be able to map out a strategic journey that will bring together your two most critical assets: your customers and employees.

Let’s be honest, the services business needs dynamic leaders, if we’re ever going to step up to being these innovators and true partners we keep claiming we are.

One such character I have enjoyed getting to know over recent years is Nitin Rakesh, who spent a good part of his earlier career at Syntel, eventually taking the CEO mantle for three years, until moving over to Mphasis just over a year ago, to revitalize the $1bn financial services focused IT services firm, which spent many years are part of HP, before being divested.

Nitin is also very active in the thought leadership sphere as chairman of the IT services council for NASSCOM, and serves on the advisory broad for Knowledge@Wharton (among other activities). But one of the things you’ll get to know about Nitin is his brain typically works faster than most mortals, especially when it comes to his favorite topic about aligning technology to the needs of the customer, and working those desired outcomes right through to the back office, which is a philosophy very close what we believe in at HfS, with our Digital OneOffice conceptual framework.

So let’s hear a bit more from Nitin about how to get ahead in today’s IT services industry, and what we need to do to be effective in the wake of intense competition and the leveling off of traditional IT services…

Phil Fersht, CEO and Chief Analyst, HFS Research: Good morning, Nitin. It’s great to have you on here. To start with, I’d love to hear a bit more about you personally – you’re a technical guy, you’re an engineer at heart. So how did you wind up running a billion-dollar IT services firm? Tell us where this all started and why you’ve been so successful at it.

Nitin Rakesh, CEO Mphasis: Thank you for that, Phil. I think I am an engineer at heart, I love building stuff. Early on I started experimenting with newer areas – as I came out of college, back in the days in the early ’90s looking at how do you apply technology to things like image processing, character recognition. Those were very early days of artificial intelligence because you are teaching the software how to actually recognize handwriting.

So I think early on I got really excited about the impacts technology can have on our daily lives, and how we can change the world surely but certainly. I think from then I’ve never really looked back even though I’ve done a few stints in financial services. How do you apply technology and innovation? Back in the day, in the mid ’90’s, there was a field which is now also pretty prevalent called ‘Technical Analysis of the Markets’. And that was nothing but pattern recognition to see how do you analyze human behavior looking at the patterns in stock markets or their price behaviours.

So I think the theme started to get clearer to me over the years, but I’ve been lucky that I was at the right place at the right time as well. More importantly, I am really passionate about applying technology to everyday problems and ended up running a technology services company.

Phil: We got to know each other when you were at Syntel, but you’ve since taken over Mphasis, and now it’s free of the HP empire (or former empire). So how is that business refocusing itself… and where are you taking it?

Nitin: I think this company has got some unique capabilities despite having gone through both shareholders in the last 12 years. I think we have retained and maintained our focus on applied technology. The company was founded by two ex-Citi bankers, so the focus was always applying tech to financial services and banking.

One of them was a business leader and the other one was a technical leader, a CTO. I think they built a techno-functional mindset into the business more than just a functional approach to applying problem-solving. I think it was always about embedded technology. And I think under EDS and HP, some them flourished, but some of them were impacted due to the overall global empire of HP, and the fact that we were a small piece of their overall business.

But as I came onboard about a year ago, we do have a fairly progressive shareholder who encouraged us to find our footing based on our areas of strength. What we’ve really been doing over the last 12 to 18 months is, essentially, differentiating ourselves by being an applied-tech firm that focuses on looking at how to apply new technologies to everything that banks, insurance companies and financial services firms do.

This is really about looking at, in the current age, how we make every enterprise customer-centric for their end customers and consumers, and how do you apply technologies to help them get closer to their customer in order to improve customer experience, reduce downtimes, offer targeted products and services with hyper-personalization? And all of this at a lower cost, with a fast time to market. So that’s kind of the mantra that we’ve set for ourselves.

Phil: A billion dollars in revenue: Surely, Nitin, that should be the ideal size to be big enough to be dangerous, but small enough to be sort of nimble and disruptive. What does this mean though, in reality? Can you share an example or two of how you can disrupt with your clients, while also delivering the bread-and-butter work that keeps the machine going?

Nitin: Absolutely Phil. That’s a great positioning statement! We actually use a variation of that quite often. But I think our positioning almost always is that of a ‘champion challenger”. And from that, one, we obviously have the agility and the customer-centric focus on our side. We aim to give clients a personalized white glove service experience and we continue to invest significantly in our capabilities to stay ahead of the curve. In fact, there are multiple examples where we’ve been fairly nimble – but also aggressive – about going back to our clients and proposing to them things that challenge how they run their current operations, whether technology or business.

I’ll give you a small example: Why should we not apply something like predictive analytics to an offering as standard as infrastructure application management? Why should we not turn AMS or an IMF into a big data analytics problem, and why should we wait for something to fail or break, so that we can go and fix it, which is (let’s face it) the traditional IT outsourcing model?

So, I think, from that perspective, it means that we end up shrinking the overall footprint of the ITO team, but that’s okay with us because I think that’s the right thing to do for the customer. So, I think from our perspective, we’ve been fairly aggressive in moving clients along this journey of applying technology to traditional services as well.

And given that our scale is normally a fraction of some of the very large players, we are able to go back in and propose something very creative, even if it means that it actually shrinks the core and has an adverse impact on us as well. I just think that’s the right thing to do. So that’s how we are able to challenge the status quo, and in the process, carve out a position for ourselves.

Phil: One of the big discussion topics we talked about at our recent New York FORA summit centered on emerging technologies like automation, machine learning not being an end – they are just a means to get from one place to another. So, what are these places? What – in your view – is the real end-game for clients these days?

Nitin: Great question, Phil. I think I’m a big believer in the fact that every next technology isn’t anything more than a tool, and what you do with it depends on how you are able to align it with one or two objectives. I talked about the fact that one of the biggest reasons why we are seeing fairly high degrees of disruption, especially in consumer-facing industries, is because, over the years, enterprises became so complex in the way they ran their back office systems and operations, that almost every business that’s been around for 25-30 years is essentially run back-to-front what that means that the back office determines when you can launch the next product, the back office determines what’s the next recycle for you to be able to make changes to your system, so you can have the new functionality.

The back office determines how much flexibility do you have, and so on and so forth. Whereas if you look at the new age, truly digital companies, they actually put the end customer in the middle of everything, and work backward from that. So how do you really pivot the focus of large enterprises from being functionally operationally back-office driven, to being customer-driven. And that’s how you should think of applying all new technologies, whether it happens to be analytics, which should give you the ability to understand every customer, or whether it is some form of AI, machine learning or robotics, which should really be able to reduce the time and cost it takes for you to service customers.

I think applying this customer-centric transformation, starting at the front of the customer and moving towards the back office, is really what we think that today’s technology should be applied for. Beyond that, IT has always been about automation of an existing workflow or a business process, so I think automation is really nothing but the next generation of that.

So I’m a big believer that if you keep customers at the center of everything and if you apply this transformation, essentially to provide a hyper-personalized and a great experience to the end customer, I think every large enterprise will find the digital pivot that they are looking for to avoid disruption.

Phil: As you look at expanding your own company’s footprints, Nitin, does this have a big impact on the profile of people you are looking to bring in, the backgrounds, the talent base, the business mindset? How is that changing your whole growth and talent strategy?

Nitin: I think It’s very much central to the transformation, Phil, that we need to drive as service providers in our business. I think a little bit of everything you just said absolutely, first and foremost we need our people to be aware that this business is not about just throwing resources at a problem but it’s about applying technology to the problem. So I think that’s the first realization that we’ve driven through our org.

Secondly, it’s not just about understanding one aspect of the functionality. You can’t just be a tester or a developer anymore – you have to be able to understand the entire stack of what goes on and, from that perspective, I think what becomes really front and central is what we are calling the architecture or the design layer. i.e. How do you combine an architectural solution mindset with a developer (with a software engineering mindset) to create that sweet spot of what we call a T-shaped developer or a T-shaped employee . On the one hand, you want them to understand a certain particular functional domain and, on the other hand, you also want them to be steeped into the technology horizontal domain. So, I think driving this T-shaped approach has really been our core focus.

Again, we’ve had, as I mentioned, a long track record of a techno-functional approach. We’ve got an architectural mindset and are, in fact, one of the first companies, more than 12-13 years ago who set-up an architectural community, and we’ve got to double-down on that, which is why we are driving it top-down from that perspective.

Phil: Nitin, try and think ahead three years, beyond the current horizon. What do you think our world of technology is really going to look like? When you look at the pace of change, how fast we are moving today when you consider the speed at which we’ve developed in the last decade? What do you think we’ll be talking about in three years time?

Nitin: I can give you some guideposts and some megatrends that I think will continue to evolve. Which technology will be front and central is hard to call. A good example is, who knew 18 months ago that everything in the world would be powered by Alexa. So similarly, I think it’s hard to call these technologies, but I see no reason why we shouldn’t see the continued focus on applying all forms of new tech to the customer experience. If that means that we end up evolving to a contact-less UI, whether it’s voice or AR, VR, some combination. I think that will definitely be a good example of how all things customer-centric will probably drive a lot of the technology implementations.

Secondly, I think most the enterprises will continue to focus on shrinking their core technical debt legacy footprint, applying technologies like cloud, and some form of cognitive as well.

I think, directionally, how do you improve customer experience, how do you continue to drive personalization, how do you reduce time to market, how do you drive a higher ability to monetize and understand the customer to cross-sell? And, finally, all of it must be done at a fraction of the cost, because that’s essentially what the problems of new tech are. So I think those four or five business priorities don’t look like they’ll change in the short to medium term and I think that’s the reason why almost all large enterprises will have to learn to adapt everything to the customer.

Phil:Do you think that the IT services industry is genuinely poised for a massive change, or do you think it’s going to be slow, gradual and uncomfortable? What’s your prediction there?

Nitin: I think what’s definitely happening is that as the growth rates in the core services, (the traditional ABM/IMS/BPS/Service manager), those growth rates mature to the flat lining of the S curve – as they have been on a steady cliff for the last twenty years or so and now, as they settle into mid to high single digits, I think there are a whole lot of questions being asked by investors as to whether this is still a growth industry or are we genuinely starting to look at a value mindset. I think that’s what you are starting to see with some of these large activist investors.

I think there’s still growth in the industry, but the growth doesn’t seem to be just in traditional services, which is why I think it’s important to point new items of growth, new pockets of investment that the client is looking to put money behind. Whether it happens to be tangible consumer-facing tech, it happens to be large data initiatives, maybe triggered by platforms and all things AI. I think how you really add those engines of growth to your core business, and still continue to drive the business in a way that you are seeing in growth companies, is really the challenge that a lot of our peers will have to face, especially if they are public.

I believe we are in an interesting position because we have a large activist shareholder, and we are partly private equity as well, so we definitely think of how we can apply all things active to the way we run the business. I do personally believe that it’s possible to still be viewed as a growth business, however, it will require a slightly different bent of mind. It will have to be more than a functional pyramid driven people business, to essentially be something that blends in our core technology expertise, some form of IP and platforms, at a pace and scale that can complement our growth and move the needle.

I also think that whoever can find a way to blend new engines of growth – and stay above industry growth will succeed long term. This is an over simplistic view, but I think that’s the way I think about our business, I mean we’ve defined our top-most priority: growth, growth, growth and growth. And we talk about consistent growth, differentiated growth, profitable growth and responsible growth.

I think if we can continue to have that 4G’s of growth mantra, we’ll probably continue to look for above market growth, so we keep taking market share.

Phil: So, I’ll ask you one final question, Nitin. What can we do as both business leaders, but also as educational and government leaders, to help with some of these re-skilling issues we are seeing. At the NY Summit, for example, there was lots of talk about machine learning, and we had a session where 70 percent of service providers claim they are going to re-skill huge amounts of their delivery staff on machine learning, without any real clue on how hard and technical this is.

Is there a crunch coming here? What can we do to get a stronger alignment between these changing needs of the customer, and what we are delivering as digital business becomes so core to our clients?

Nitin: Absolutely, Phil. I think I’ll answer the question in two parts. One is what can we do to make this condition from the way our staff is currently to where we think we need to take them. Fortunately, or unfortunately, some of them probably won’t be able to make this shift because, keep in mind, the business model that they were hired under over the last few years was much more functional. You’re either a business analyst, or a programmer, or a tester or a production engineer. You really were focused to go deep into one of those functional areas, because that’s the way the business was defined. What this means is that since they were hired out of college, and I am talking about these large offshore labor pools, specifically focused on building skill and driving efficiency, since they have been hired out of colleges, they really have this very deep functional view of one activity.

In many cases (and I am not saying all), the students coming out of colleges today have the ability to apply new tech. I think there are two things we need to do there as well. Firstly, we need to be able to drive the most important skillset they need to be successful, which is to have is run-ability, because the applications for change (of all things new tech) mean you can’t be an expert in anything… so you have to be able to learn new things on-the-fly. Obviously, you need foundational elements of software engineering. So I think if you can drive this software engineering mindset, if you can drive the ability to learn new things, then I think we can definitely impact the next few years of generations coming out.

And secondly, I think we also have to – as an industry – go back, shift left, work with these institutions, work with the governments and create technology-driven platforms that can actually give the ability to drive some of this learning even while they are in college.

So I think there are multiple initiatives that have been underway. The Government of India has actually got a Skills Ministry who are focussed on this issue. I know that the Chinese government is doing a lot as well, and I know in the US it’s much more driven by the private sector and the universities. However, I believe we are going through a generational transition, and the realization of how we continue to apply tech to the new generations will effectively differentiate which demographic and which country with the right labor pool, comes out the winner over the next 15 years.

Phil: Thanks Nitin for these great insights. I really appreciate your time today and look forward to sharing this discussion with our readership.

Nitin: Phil, thanks a lot – looking forward to it.

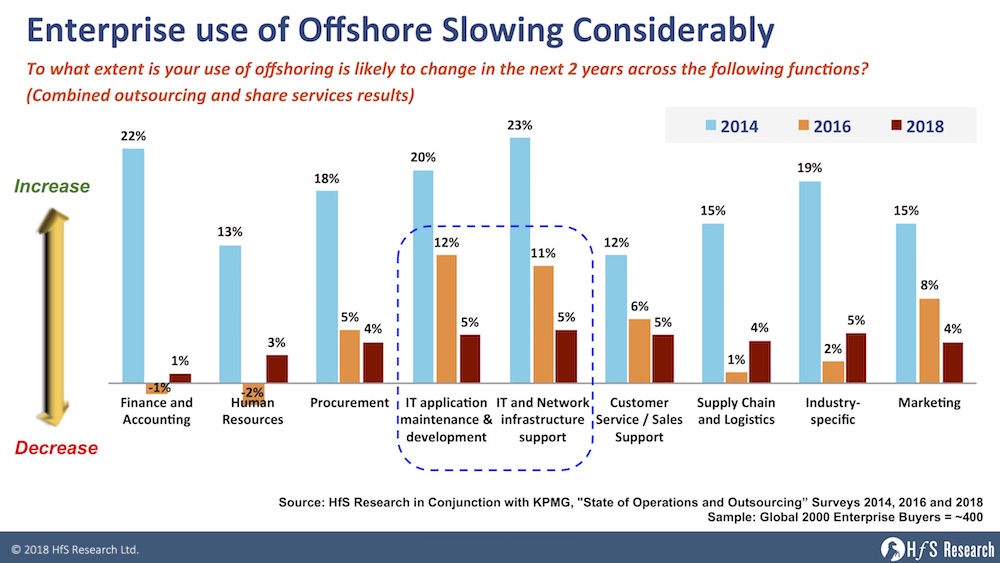

What a difference an election makes. When we ran our State of Operations and Outsourcing study in 2014 (mid-way through President Obama’s final term), Global 2000 enterprises were still planning to increase their short-term investments in offshoring their IT by more than 20%. When we re-ran the study in 2016, offshoring intent was clearly dropping to a 12% intended increase (which is a realistic number for a saturating market), but this year it has nose-dived to a mere 5% increase, which is a clear result of the anti-offshoring sentiment that has hurt offshore-centric deals:

I discussed this trend with one of the lead partners at ISG, the offshore outsourcing industry’s largest deal advisor, and he shared that Trump’s stance against offshoring was considerably slowing down the deal cycle for his firm, and he was even seeing some outsourcing deals going to the likes of Accenture and IBM because it created the façade that work was not being offshored (even though it was). Yes, this is the kind of stuff that happens when a president likes to get fast and loose with his twitter account!

However, while Trump’s open attacks on American firms using offshoring stoked panic into many paranoid C-Suites, what really transpired was a rapid shift in how US firms are viewing their partnerships with global service providers. Today’s reality is technology has become core to business competitiveness by creating new revenue channels made possible by interactive communications technologies with customers, by simplifying business operations to support the business with real-time data, and by supporting broader processes that respond to the needs of customers, as they occur.

Offshoring may be slowing, but the services business is in its best shape for four years

The healthy trend here, for the future of IT and business services, is the fact that the industry finds itself on the healthiest growth footing since 2013 – so clearly offshoring is no longer the primary driver behind IT services investments:

President Trump merely speeded up the development of global services from a cost-reduction to a business-value proposition

Many enterprise leaders are clearly no longer thinking, “How can we shave some more cost off our annual IT budget by moving more work to India?”. Instead, they are thinking, “How can I get quality services delivered at competitive prices that take advantage of the cloud, automation,and global talent.” The subtle shift here is clearly one from an obsessive focus on low cost, to one of getting quality services as the industry matures, where there are many leverage points to find productivity gains, beyond merely relying on FTE rates. The more pricing shifts towards outcomes, volumes and KPIs, the less visible offshoring becomes as a cost-lever.

When you buy electricity, do you care where the supplier houses its generators? When you use public cloud services, do you bother to question Google, Amazon or Spotify where they house their massive data farms? It’s the same when engaging with IT services firms to get work done: business operations leaders are barely thinking about where they are located anymore – and all President Trump has done is shifted the optics, compelled the leading India-heritage firms to make substantially more onshore staff investments – which they needed to do in any case – as the nature of IT work is driving the need for greater client intimacy and physical proximity between service delivery staff and client staff.

Traditional outsourcing is being replaced by partnering, and “offshoring” is not even part of that conversation

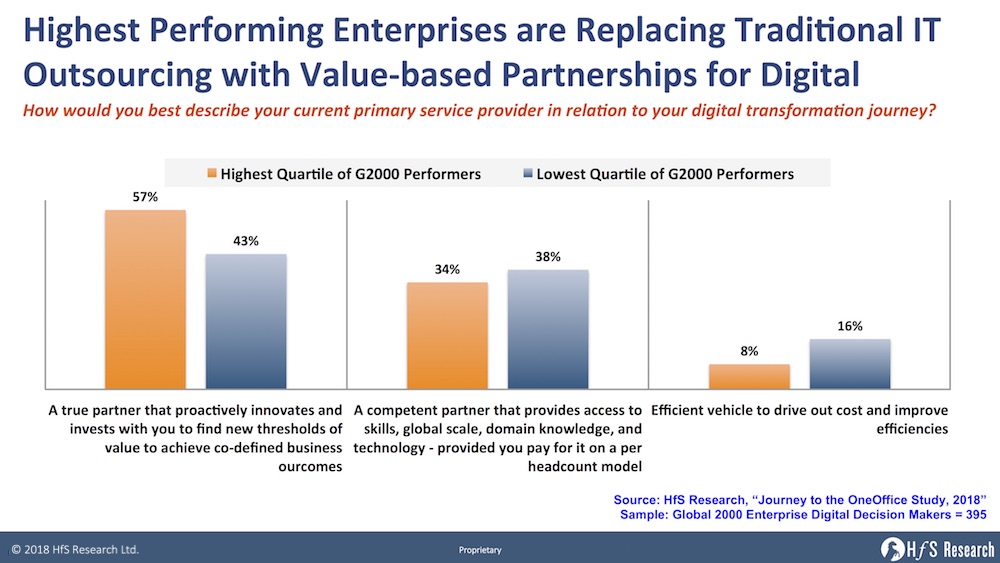

Our recent study looking at digital transformation to the OneOffice reveals that the majority (57%) of the highest quartile of performers in the Global 2000 (based on revenue and profitability) view their primary service providers as supporting their digital transformation roadmaps, as co-innovation partners helping them achieve co-defined business outcomes. Only a third viewed their service providers solely as a resource to provision skills and scale via a headcount model:

This data speaks volumes – enterprises digital leaders need providers which can work with them to achieve outcomes that are increasingly challenging – most no longer requisition 500 developers per year to code in ABAP for strategic initiatives – that is a commodity practice today, usually delegated to lower level manager to lead. Nearly all G2000 firms, today, have a Chief Digital Officer tasked with taking their companies through significant business model change, enabled by smart technology provided by partners which understand what is required. Whether the talent for these strategic projects resides in Bangalore, Basingstoke, Bucharest or Baton Rouge is moot – this is about getting results where top talent is hard to source, and the location is just not very relevant anymore.

The Bottom-line: Trump did us a favor and ripped off the legacy Band-Aid for the services industry

Trump’s stance on offshore outsourcing sparked two behaviors which have set up the future of services to be far more value-driven and business oriented: All the major Indian-heritage service providers have been aggressive adding 10,000+ staff right across North America and Europe. Several are also embarking on ambitious acquisitions of niche onshore digital firms (both creative and tech-driven) to engage themselves higher up the foodchain within their clients and be considered for more lucrative digital engagements where there are deeply engaged with their clients redesigning business models that need sophisticated technical support. So while the industry suffered from a couple of flat years trying to squeeze the last vestiges of life out of a dying body-shopping model, the new reality is a global delivery model that is now embedded in engagements where the focus is much more on business value and outcomes than prehistoric effort-based inputs. We are also entering an era where the likes of Cognizant, Infosys, TCS and Wipro will cease to be called “Indian providers” and merely be referred to as global IT services firms. Location is irrelevant… expertise most definitively is not.

Japan’s ageing and shrinking population creates real skills shortages and very high labor costs

Japan is currently the only major developed country that is experiencing a population decline. Unlike other developed economies, it is not offsetting population decline with immigration. In addition, Japan has the largest proportion of elderly citizens of any country in the world. In 2014, 33% of the population was over the age of 60 and this percentage is increasing.

Given its shrinking productive population, combined with its wealth, the cost of labor is high. Consequently, its companies are often the first to adopt new technologies, including artificial intelligence and robotics. Companies use these technologies to increase productivity in a market with severe skills shortages.

Japanese firms increasingly struggle to acquire necessary skills to optimize their technology investments which, in turn, raises the cost of these skills. This is leading to increases in spending with third party service providers that help to fill these skills gaps.

Keiretsu stifle innovation and decision-making

Japan has a unique business culture based around keiretsu. Keiretsu are a set of companies with interdependent business activities and ownership arrangements. Toyota is the largest keiretsu. It dominates its keiretsu and has several tiers of subcontractors, most of which only serve Toyota. The activities of contractors and subcontractors tend to be shaped by the dominant company within their ecosystems. This can inhibit innovation from smaller companies in a keiretsu and make it inflexible. Deals tend to be done at the top of the keiretsu. Japanese business remains hierarchical and labor mobility is low compared to other rich countries. Hence, there are typically fewer stakeholders involved in decision making.

The convergence of Information Technology and Operational Technology is driving major transformation

One of the key things to understand about the Japanese market is that operational technology is converging with information technology at an extremely fast rate. It has to, if Japanese industry is going to remain competitive. Its leading manufacturing and automotive firms are using cloud, machine learning, mobile, and Internet of Things (IoT) technologies to transform their operations.

Until recently, industrial firms used proprietary technology for very specific processes. They were often dependent on suppliers within their keiretsu, for components, management, and maintenance of these proprietary machines. Today, Japanese firms are integrating their machinery with information technology, often supplied by firms from outside their own keiretsu. For example, Hitachi and Mitsubishi are integrating third party mobile, cloud and AI technology into their industrial machinery as a way of lowering planned and unplanned outages, enhancing customer experience and lowering the total cost of ownership.

Similarly, Toyota, and other leading Japanese automotive firms, have been embedding IT into their vehicles, enabling more automation. Third party cloud, mobile, IoT and AI technology are all being integrated into Japanese motor vehicles.

The Japanese business environment poses huge challenges and opportunities for ambitious IT Services buyers and providers

What does this mean for the IT services environment? Industrial firms are looking for IT services firms that understand how information technology is converging with their operational technology. These firms must understand how their customers’ businesses operate, at a more granular level than ever before. The integration of the IoT, cloud, machine learning and mobility with operational technology is transforming industrial businesses and enabling firms in Japan to differentiate themselves. Large Japanese IT services firms, NEC, Fujitsu and particularly Hitachi are well placed in their domestic market. In addition to being leading IT services suppliers, they are also operational technology firms. This gives them a huge advantage in the Japanese market and makes it difficult, although not impossible, for foreign firms to compete with them locally. These firms continue to dominate the Japanese IT services market together with the NTT Group. To be successful, foreign IT services firms must be able to demonstrate an understanding of the convergence of operational technology and information technology in specific industries.

The financial services, retail, healthcare and government markets offer enormous opportunities. Japan’s financial services and retail sectors are mature, sophisticated and highly automated. There remains a lot of older, legacy technology, so there is an opportunity for IT services companies, both Japanese and foreign to create systems integration, maintenance and management opportunities in these sectors. Financial services firms and retail firms tend to look globally for ‘best of breed’ technology implementations. Foreign firms such as IBM and Accenture, are well placed to bring expertise created from projects outside Japan, to Japanese clients. This is more challenging in industrial sectors where Japanese firms consider themselves to be ahead of the curve. Nevertheless, in recent years, Japanese firms have shown more interest in what has been happening in Germany and its ‘Industrie 4.0’ initiatives.

The highly regulated Japanese healthcare sector offers some interesting opportunities. The world’s oldest population has focused on innovative new technologies to offer cost-effective care to the elderly. Huge investments in elder care robots have been made by the Japanese government and Japan leads the way with this technology, some of which is being used in Japan. The use of sensors and other devices that can allow remote care is also very advanced in Japan. Again, IT services firms are needed to implement and manage this technology.

The Bottom Line: Japan’s skills crisis is driving automation at a breakneck pace

If IT services firms are serious about growing in Asia, they need to develop a strategy for Japan. This is the biggest market. It is hard to say that you have an Asian presence if you are not visible in Japan.

Japan’s demographic characteristics, combined with its rigid keiretsu-based business culture are forcing companies to automate processes rapidly. Indeed, Japanese firms are blending information technology, often supplied from outside the relevant keiretsu, with operational technology, to drive out costs, engender innovation, and address skills shortages.

It took a while, but we’ve finally seen the cards being played from Infosys’ new CEO Salil Parekh – and it’s a concerted digital play to offer clients an alternative to Accenture. Make no bones about it, the intentions are crystal clear to reverse the course Vishal Sikka set with a software-centric “product” approach, and follow the Accenture model of creative digital services supported by technology-agnostic execution. The firm, once affectionately dubbed the “Indian Accenture”, has gone full circle to reclaim its mantle and revitalize itself as one of the key services alternatives to enterprise clients seeking high-value digital capabilities enabled by industrial-scale technology execution. Infosys has never been one to go about its business quietly – the firm likes to make big bold statements and attack the industry with a swagger – and, after a full year of navel-gazing as Sikka’s reign fizzled out, amid a very public media obsessed with scrutinizing every private jet excursion and every former SAP executive’s departure package, Salil has made his play in typical Infosys style.

With the chest-beating battle cries coming out of the firm’s Q1 results, Salil and his new founder friends believe they have the credibility, brand and global presence to slip in front of its rivals, notably Cognizant, TCS and Wipro, and to make up for lost ground and quickly assert their presence in this digital race for client supremacy. The (surprisingly open) stated effort to sell off their product acquisitions Panaya and Skava (and likely more), the recent acquisition of creative agency WONGDOODY, famous for its Superbowl ads, and its 2017 addition of London-based product design agency, Brilliant Basics, gives Infosys a creative digital footing in both US and Europe.

So can Infosys break out of the pack to challenge? Let’s take a look at the Digital Services market…

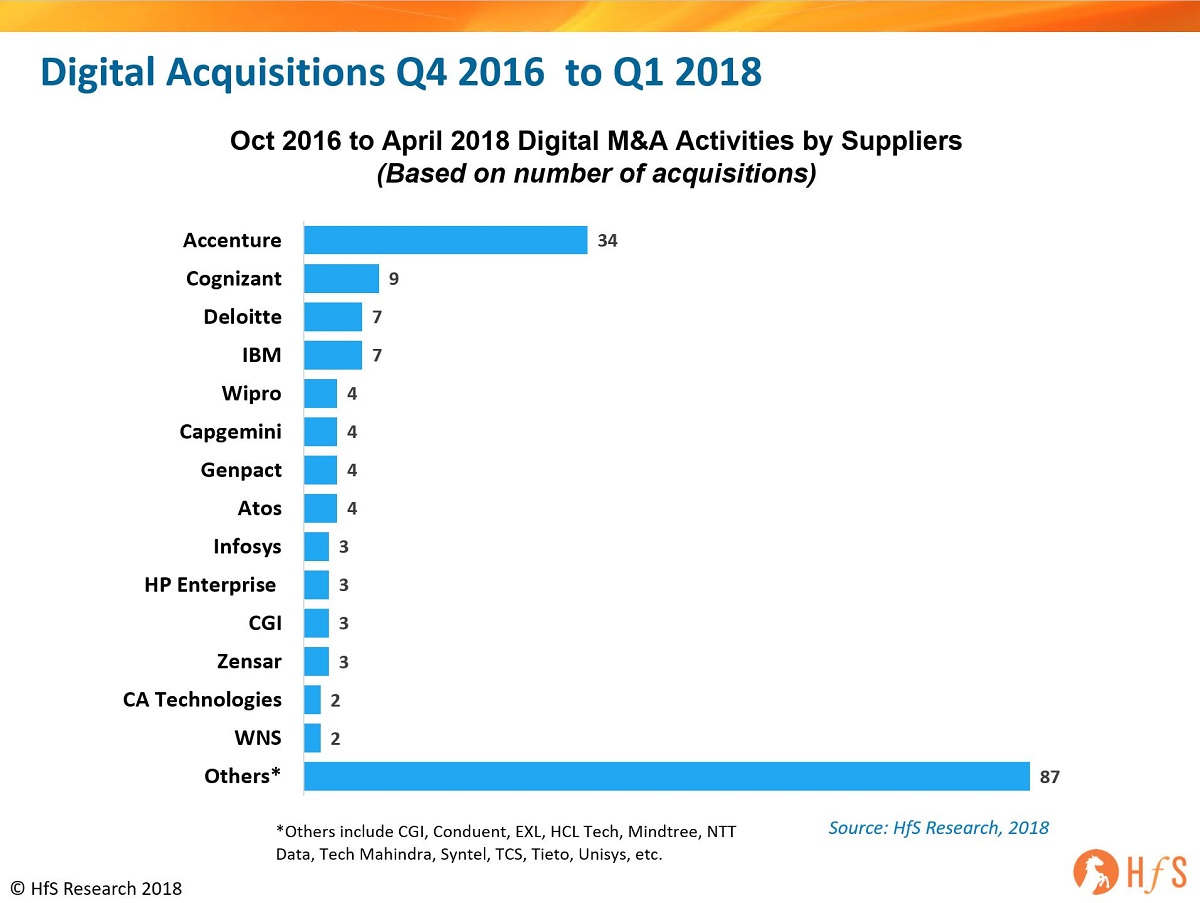

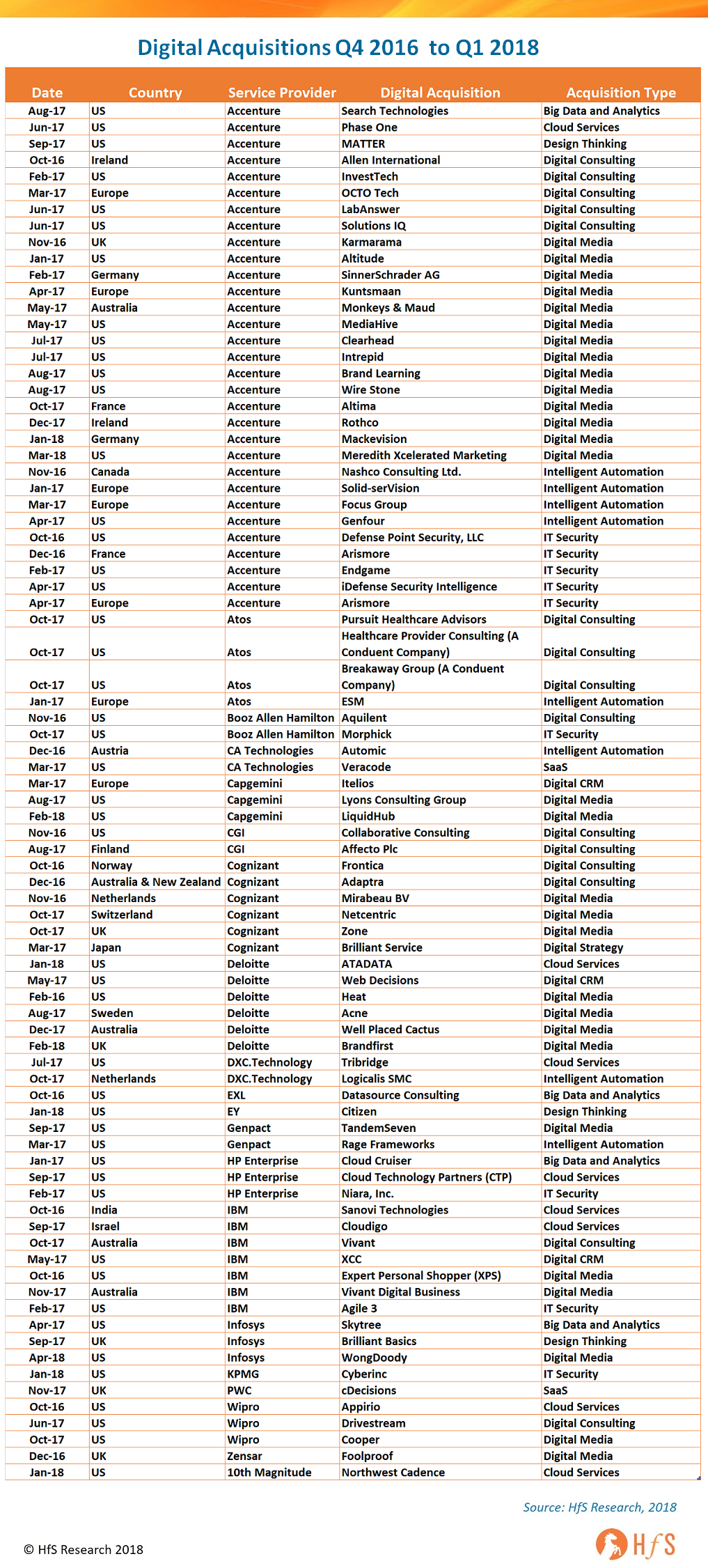

There’s been enough noise and confusion regarding what constitutes digital and which providers are truly breaking ground here, but the stark reality is that Accenture has made a relentless concerted acquisition strategy to dominate this market from the onset, and the current race is on from the rest of the service provider community to challenge them:

Digital services provide the natural evolution of traditional IT and business services firms, while products-plus-services is a struggle

For all Vishal’s intelligence and vision, the reality became very clear towards the later stages of his tenure as Infosys CEO: traditional IT services firms will always struggle to become products-plus-services firms as they simply do not have the channel to market, the sales structure or the culture to sell these offering at a one-to-many scale. “SAP has 45,000 clients while we only have 1,200” was his realization. Services juggernauts like Infosys are never going to scale effectively down to the lower middle market, hence need to deepen their footprints with large clients which are profitable to manage in their global delivery model. And remember Accenture’s aborted attempts to make a mid-market play?

A one-to-few model may work in very specific areas such as procurement (Accenture and Procurian) or healthcare (Cognizant and TriZetto), but these investments are substantial and require a significant amount of time, focus, and investment to make viable. This is why Salil made the aggressive decision to abort Panaya and Skava – these require a massive effort to deepen sales and delivery capability to make these investments truly worthwhile and pivot Infosys into a much more specialized direction. The realistic growth for a firm like Infosys is in winning big-ticket enterprise services accounts on long-term deals that require significant scale and transformation. There is a reason TCS is leading the services industry in valuation – it has its tentacles firmly wrapped around large, multi-year client relationships and is not bogged down in discreet product acquisitions.

Digital services represent the high-value end of the services business where firms like Infosys can embed themselves for many years if they get this right – the ability to design, manage and deliver the customer engaging front office, supported by a digital underbelly, support organization and predictive analytics (as we at HfS term the “Digital OneOffice“). It is that ability to enable clients to respond to the needs of their customers in real-time: Digital is the wow factor that is setting apart today’s services firms. The reality is most of these providers are competent at delivering IT services at scale to meet whatever KPIs were agreed at the onset of a contract. So the differentiation is that ability to help enterprise clients delivery the digital experience for their own clients – and you can only really do this if you have absorbed sufficient design and consulting talent at scale. Digital is much more about a services experience than a specific product experience – there are many apps and tools clients can use, but it’s how they are aligned with the business strategy that really matters. This is why Accenture’s technology agnostic strategy of the last two decades is the one so many services firms are now following.

The Bottom-line: Accenture created the digital services market and there is no clear contender to take them on from an end-to-end services standpoint. Infy has as good a shot as any of its key rivals

Three small-scale acquisitions are merely a statement of intent, but the hard work starts now – and it is a serious about of hard work! While WONGDOODY and Brilliant Basics are very credible firms and get Infy on the map for digital design and media services, Salil and his cohorts need to savage the market with some further significant investments if it wants a place firmly at the big boys’ table. Cognizant has done an excellent job taking its SMAC stack into a very meaningful effective digital offering, and currently is pushing Accenture the most aggressively, with focused offerings and marketing. Wipro has made some admirable efforts with Designit and Appirio to win some notable deals and has been very focused on this space, vastly improving its communication and positioning with clients. The reality is, no one has come anywhere close to rivaling Accenture’s scale with digital and we need to see a lot more than some small agency investments if any of these firms want to make a realistic play at Accenture’s dominance. Firms like Infosys now have to bet big if they want to do more than pay lip service to the new wave of technology-focused offerings. A major consulting acquisition, such as a Booz or AT Kearney, could make the difference, but will likely be a one-shot deal to make or break their strategy, and we all know how messy these services-plus-consultant acquisitions can get.

The bolder play is to go after one of the large creative media/advertising agencies that offers clients and scale that get Infosys immediately to the table. Firms like AKQA, BBH, M&C Saatchi, Ogilvy & Mather, Sid Lee and the Miller Group (to name a few) would deliver immediate credibility and digital design capability to a firm as ambitious as Infosys. Infosys has the swagger to pull something like this off, but has never faced such a test of focus as it does right now – it has picked its path, now the firm needs to pace some serious, eye-catching investments to stay true to its word. Most importantly, the Founders needs to stay true to Saili and not have him experience the wheels come off like they did for Vishal – that is not a road Infosys can afford to go down again, as next time there won’t be a forgiveness factor from its clients or the industry at large.

Remember that 70’s movie “Logan’s Run” when, in the 23rd century, the population and the consumption of resources are maintained in equilibrium by killing everyone who reaches the age of 30? They found a simple fix to solve their problems. Today, we seem to be entering a similar situation with employment and intelligent automation: why not just retire everyone at 40 to protect those valuable employment resources? It sounds far easier than building a ridiculously long wall or pretending all these magical new jobs will appear from nowhere in a couple of years…

Everyone, seemingly, is obsessing with the current swirl of anxiety infecting our whole career outlook, with relentless discussions raising our stress levels as we figure out how to “adapt” ourselves to a world where bots are going to do so much of our work at some indefinable moment in the future.

It’s just not cool to be normal anymore…

Whether we’re mindlessly getting our hourly endorphin rush from those lovely social media sites that keep pulling us in, or dozing through yet another mind-numbing panel on the “impact of intelligent automation” at some horrendous conference we just had to go to (listening to people who previously had nothing to do with “automation” and have since become overnight luminaries), or simply chatting with colleagues in the office… there is now a constant angst that the world is becoming a digitally-scary place, and the only way to deal with it is to keep trying to learn more and keep talking to colleagues and peers in other firms about how to get ahead of this. Suddenly, we have become disposable assets and we need to keep reinventing ourselves to keep sounding like we’re up on all the new stuff. Suddenly, we live in a world where everyone else is about to be transported to the scrapheap of legacy professionals who can’t be retrained to do anything meaningful anymore.

The current swirl of hype is driving a new behavior and energy: more partnering, knowledge sharing… and an obsessive curiosity about the future

We are subjected to a constant barrage of articles, some lamenting our woes and talking about desperate measures like a universal basic wage (Karl Marx would be impressed), and we are increasingly being subjected to declarations of unbridled optimism, where jobs will be miraculously created as a result of these incredible advances in artificial intelligence (which rarely have any sensible facts to prove the philosophies, they just spout some big theory and then the talk track fizzles out somewhere… you know them well by now I hope!). However which way we look at this, the real answer is that we simply don’t actually know what the future has in store for our careers, our companies, our economies, politics and our children, but what we can do is keep understanding the facts and keep sharing knowledge with other like-minded people… and the future will unravel before our eyes as we keep trying to make sense of it all.

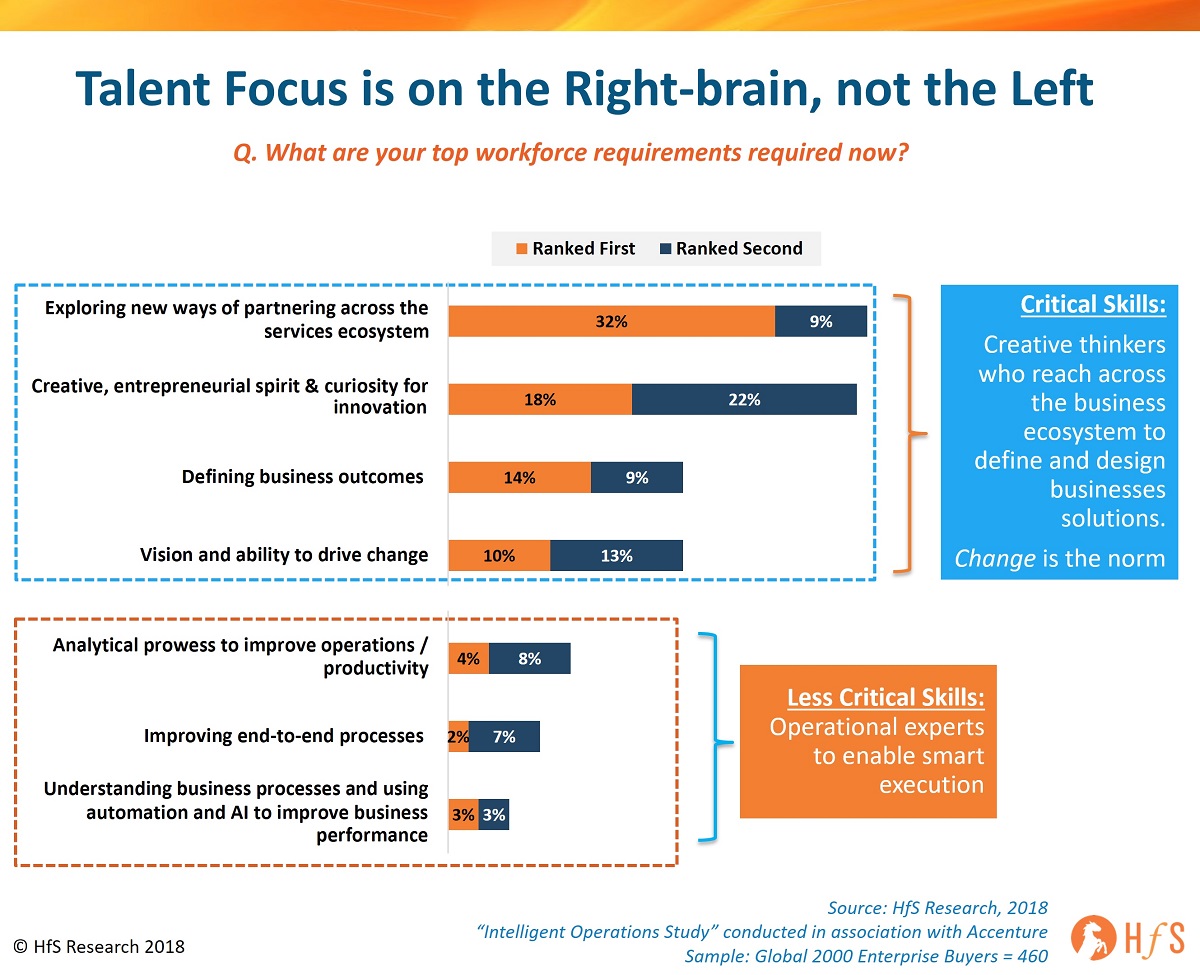

OK that’s enough of a philosophical discussion for a Monday. Let’s look at some actual new data to understand what skills our enterprise leaders are looking for today – our new study on Intelligent Operations, conducted with the support of Accenture, which covers the views and dynamics of 460 global 2000 operations leaders, gives us some real insight into this shift towards the creative, curious types, with a thirst to learn and an obsession with networking and partnering:

The focus heavily shifting to dynamic individuals who understand how to define outcomes and work to align their business operations with them

So if we’re one of these obsessively socially curious animals with a penchant for constantly knowledging-up on all the cool new stuff – and we love to talk partnerships with other companies in our network, the near future is actually pretty encouraging for us: our skillset now tops the list for what global 2000 leaders are looking. Leadership is under intense pressure to change the norm, to align their operations with the direction their customers are taking them. The wonks who spend all day staring at spreadsheets, focused on execution “left-brained” activities are less in demand – they need to learn how to wrap the needs of the business into broader processes that can cater to customers and support management decisions in real-time. Essentially, if your operations are not in sync with the customer-driven front office, you will likely fail.

Yes, it’s the people who connect the front office to the back are the ones emerging from this maelstrom of noise, angst and uncertainty. This is why we have developed the Digital OneOffice Framework, where teams function autonomously across front, middle and back office functions to promote broader processes with real-time data flows that support rapid decision making, based on meeting these defined outcomes. Hence, emerging technologies like automation and AI are significant enablers in helping enterprises meet their ultimate goals, where front, middle and back offices will cease to exist: they will be, simply, OneOffice:

The Bottom-line: This is the new normal – leaving our comfort zones and getting out there to make stuff happen

It really is as simple as that – we’re all leaving that big comfortable world where all you had to do was turn up for work, do the same routine activities each day, go to the same mundane meetings and keep the lights on. We all know those days are leaving us behind, and if you’re under the age of 55, it’s unlikely you can plot that sneaky escape to early retirement… we’re living in a world where we need to learn about new technologies (you don’t need to code anymore), we need to share experiences and use cases with peers across the industry, and we need to reach outside of our cosy internal networks to talk through smart partnerships with tech firms, supply chain partners, customers etc.

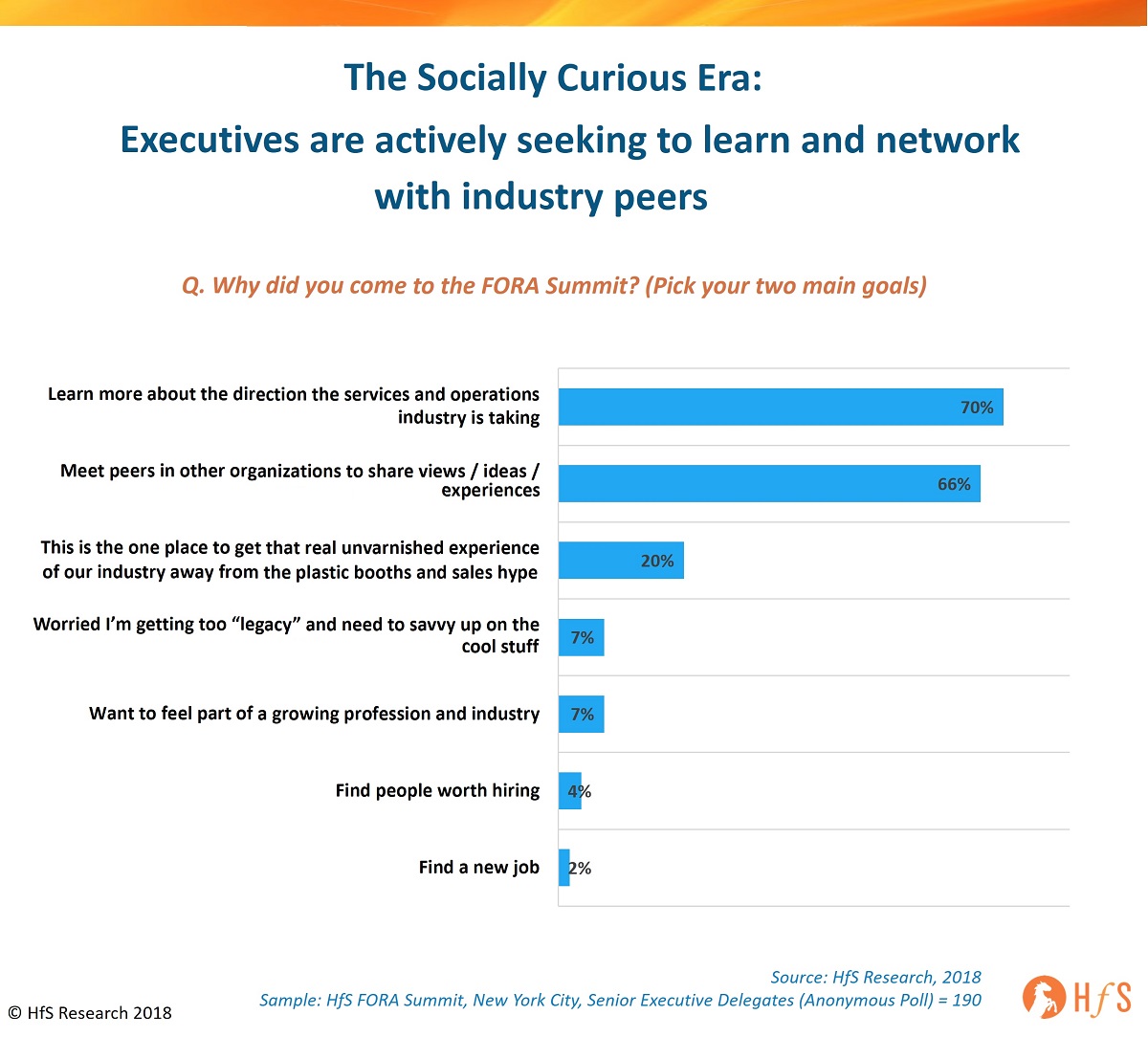

You only have to look at the reason 200 executives showed up at the HfS FORA Summit in New York last month to understand motivations have changed in an anonymous poll: they are going out to get educated and share experiences with peers. The days where conferences were all about job hopping are over – it’s more about how to stay relevant and ahead of the game.:

In essence, there is no written rulebook where this all leads – the world has become an uncertain place politically and we have yet to experience an economic downturn for many years. However, what is clear is sitting in a quiet office all day staring at your email is unlikely going to get you where you need to go next in your career. This is the age of getting networked, getting smart and learning from collective experiences. The only comfort zone is the one you make for yourself – being comfortable with the impact of change agent technologies and the experiences you can have working with them.

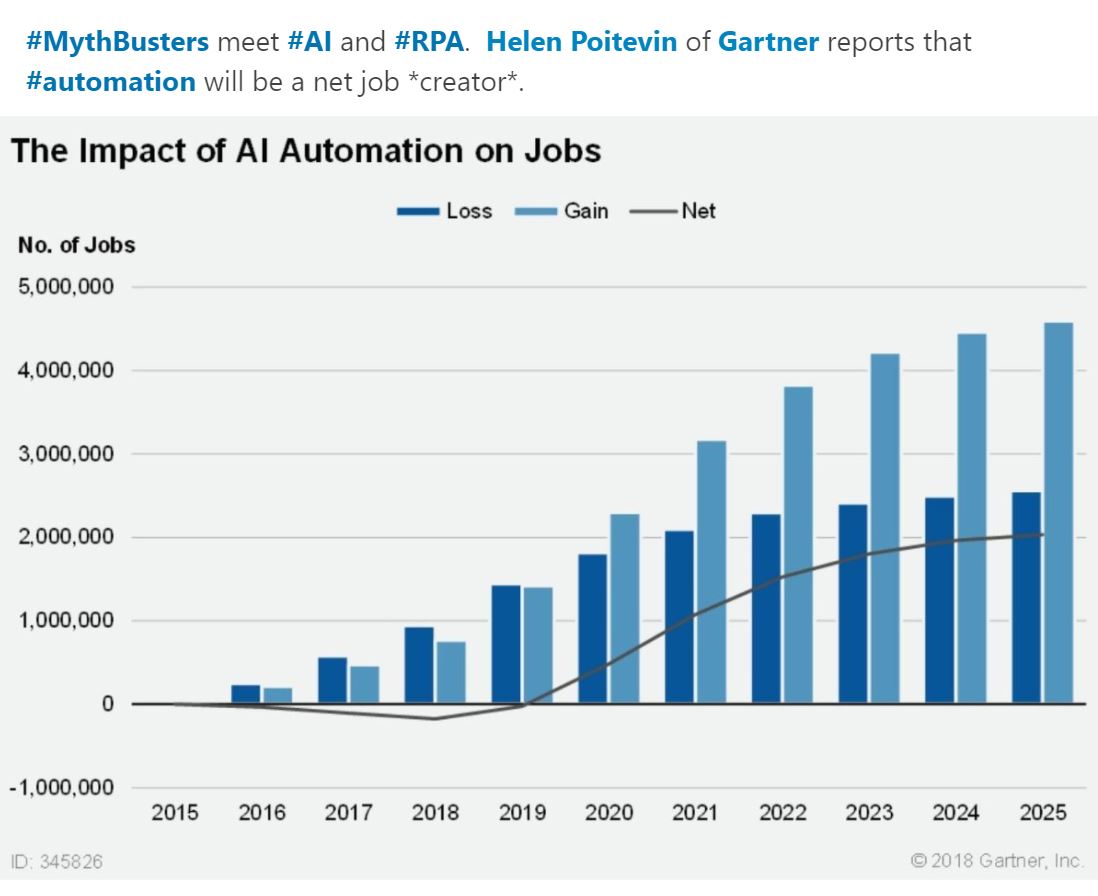

Whiplash alert: You may have noticed how Gartner recently flipped its core messaging from automation/AI being a seismic job destroyer to being now a job-creator. And both times, they just can’t seem to back up the rhetoric with actual facts. Plus, they don’t even seem to be able to define consistently what they actually mean by “AI Automation”.

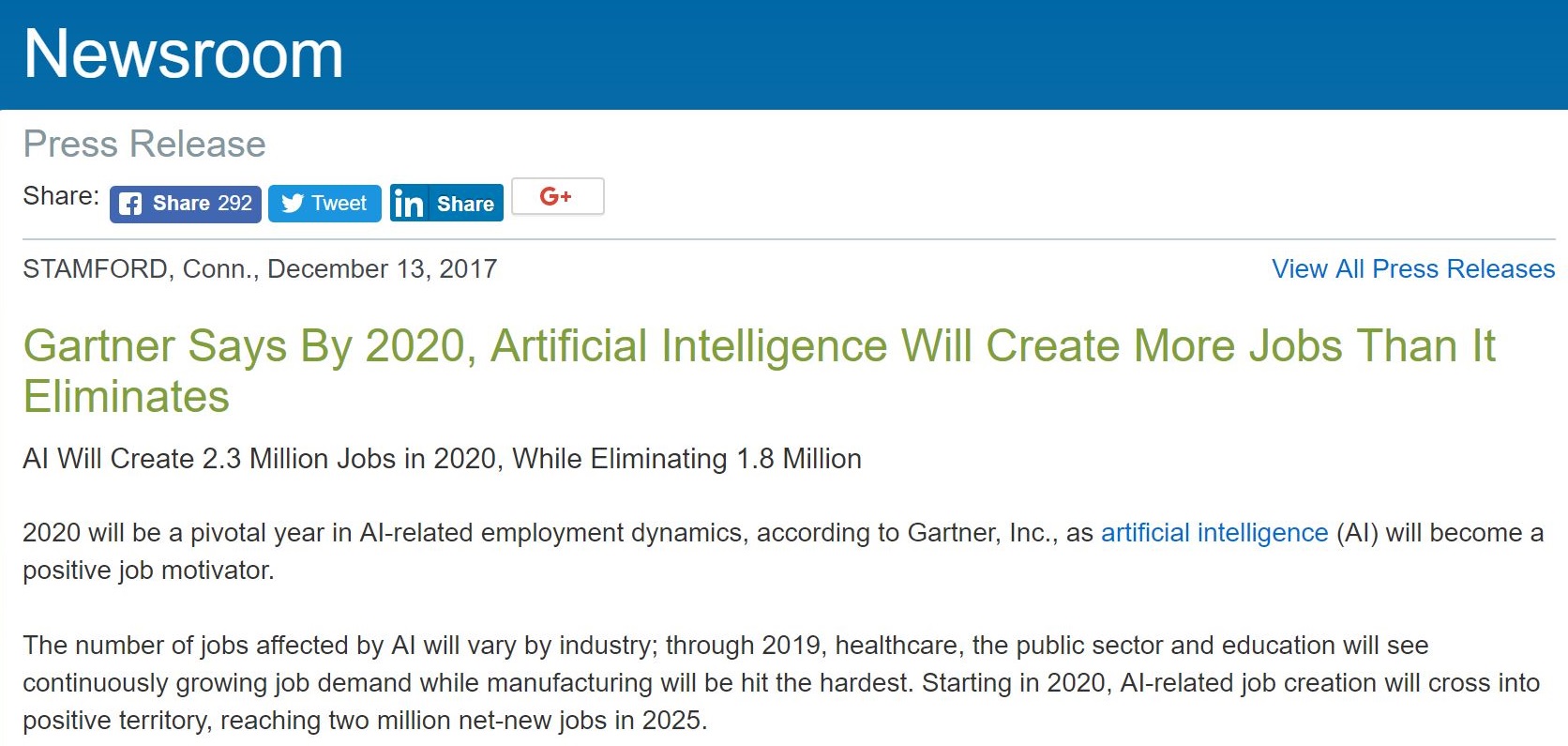

Remember when Gartner claimed that automation and AI were not only going to replace a third of jobs by 2025, but many of us would be reporting to a robo-boss at some stage this year? Well, guess what folks, they’ve now performed a complete 180-degree flip, claiming that millions of new jobs will be created after 2020, far outweighing their previously predicted gargantuan job losses (courtesy of LinkedIn). Wow:

Let’s dare to look back in time to hold Gartner to account

Peter Sondergaard, Gartner’s Head of Research, predicted one in three jobs will be converted to software, robots and smart machines by 2025. Yes he actually said that at his own Symposium, and even added, “New digital businesses require less labor; machines will make sense of data faster than humans can.” However, unlike the good old days when analysts could get away with all flavors of outlandish grandstanding soundbites to spice up a conference, these predictions tend to hang around the internet these days. While many people love to keep spinning new headlines everyday, in the hope #fakenews is now the #realnews, some of us still have memory banks that last longer than one week, especially when CIOs spend billions of dollars for this type of council.

And then who can forget this almighty whopper from Fran Karamouzis, a vice president and distinguished analyst at Gartner:

By 2018, more than three million workers globally will be supervised by “robo-bosses”. Excellent, so Fran’s surely keeping her fingers crossed that the robo-boss takeover is even more imminent than Donald Trump’s interview with Robert Mueller…

Gartner’s new claim why AI and Automation will create this massive net gain in jobs

When Gartner put out this far more positive news, I was so excited, and couldn’t wait to hear their new rationale:

“Many significant innovations in the past have been associated with a transition period of temporary job loss, followed by recovery, then business transformation and AI will likely follow this route,” said Svetlana Sicular, research vice president at Gartner. AI will improve the productivity of many jobs, eliminating millions of middle- and low-level positions, but also creating millions more new positions of highly skilled, management and even the entry-level and low-skilled variety.

Great! So there it is. Svetlana goes on:

“Unfortunately, most calamitous warnings of job losses confuse AI with automation — that overshadows the greatest AI benefit — AI augmentation — a combination of human and artificial intelligence, where both complement each other.”

Right, so all the stuff you colleagues were declaring is now calamitous and confusing? Oh, they are talking about “automation” and you are talking about “AI”. So why, Svetlana, do you call your new data forecast “The Impact of AI Automation on Jobs”. Surely you mean “AI Augmentation“. I’m sorry, but I am even more confused that I was before…

When we get into the reasons why automation and AI suddenly have become job creators, I give Gartner some credit for actually trying to give this claim some credence, but then they fail to provide a single real example of how this “new work” is being created:

Craig Roth: research vice president at Gartner: “Companies are just beginning to seize the opportunity to improve nonroutine work through AI by applying it to general-purpose tools. Once knowledge workers incorporate AI into their work processes as a virtual secretary or intern, robo-employees will become a competitive necessity.”

OK – so how will new jobs get created? Sounds like AI is helping knowledge staff cut back on interns here! Gartner continues…

Leveraging technologies such as AI and robotics, retailers will use intelligent process automation to identify, optimize and automate labor-intensive and repetitive activities that are currently performed by humans, reducing labor costs through efficiency from headquarters to distribution centers and stores. Many retailers are already expanding technology use to improve the in-store check-out process.

Great – so retailers are able to use intelligent process automation (whatever that is, I thought we were talking about AI augmentation) to fire humans. They just laid that our pretty plain and simple. No jobs created there then…

“Retailers will be able to make labor savings by eliminating highly repetitive and transactional jobs, but will need to reinvest some of those savings into training associates who can enhance the customer experience,” said Robert Hetu, research director at Gartner.

So some of the savings from sacking transaction staff will be reinvested in more customer aligned people. But that tells me less people will be reemployed, not more. Where is the net gain here?

And Robert goes even further: “While many industries will receive growing business value from AI, manufacturing is one that will receive a massive share of the business value opportunity. Automation will lead to cost savings, while the removal of friction in value chains will increase revenue further, for example, in the optimization of supply chains and go-to-market activities.”

So automation will save them money and make them richer because they will function better. But why will this cause them to hire more people? Where is this assumption coming from that those companies who make higher profits through automation will reinvest in people? Again, there is zero evidence here of a net gain in hiring… c’mon!

And to cap off this wonderful analysis, here’s the pièce de résistance:

“AI can take on repetitive and mundane tasks, freeing up humans for other activities, but the symbiosis of humans with AI will be more nuanced and will require reinvestment and reinvention instead of simply automating existing practices,” said Mike Rollings, (another research vice president at Gartner).

Great, so Mike finally mentions that money will be spent on the reinvention of new processes, as we see these wonderful new nuances of humans and machines come together. Cool… tell me more:

“Rather than have a machine replicating the steps that a human performs to reach a particular judgment, the entire decision process can be refactored to use the relative strengths and weaknesses of both machine and human to maximize value generation and redistribute decision making to increase agility.”

Awesome, Mike. So we’re talking about optimizing the best qualities of both human and machine. I love it, and completely agree with Mike. So maybe we can have an example of this in reality… and maybe even a decent explanation of what really inspired Svetlana to forecast these millions of new jobs that are going to be created? Just one example? Please… pretty please?

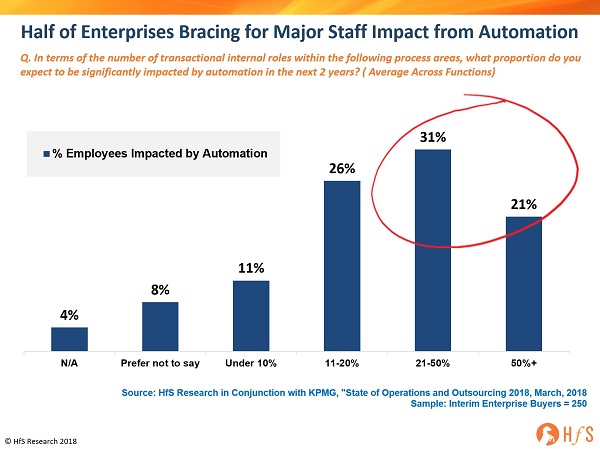

The reality: half of firms’ staff will be impacted by automation and 40% of them have no idea what to do with them

So here’s the biggest issue facing enterprise operations in the next couple of years: what to do with staff impacted by automation. Our brand new 2018 State of Operations study, conducted with KPMG, over half the Global 2000 firms surveyed believe transactional roles will be significantly impacted by automation within just a two-year timeframe:

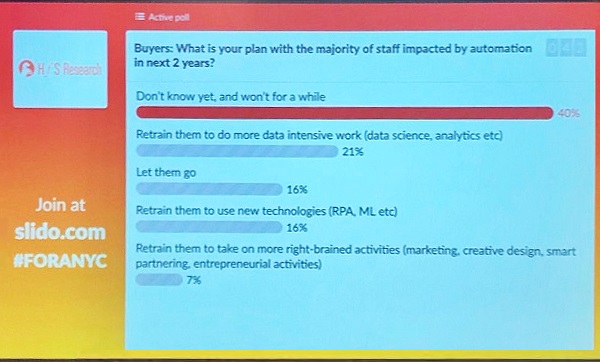

So we thought we’d poll the 120 enterprise buyers at the HfS New York FORA summit last month, and we asked them what they intended to do with their impacted staff:

While a good portion are already thinking about “retraining” their impacted staff to take on analytics work (21%) and help manage new tech such as RPA and ML (16%), the vast majority (40%) are just honest and reveal they just don’t know.

Bottom-line: Please let’s stop trying to confuse everyone. As analysts, we have a responsibility to speak from real facts and real evidence

The technology industry has thrived on the hype for decades, but in the past, it was usually based on established technologies and their real impact on business, proven through many client experiences and tested through time to help us all understand the ultimate impact on business models. Suddenly, many leading experts are making judgments based on possibilities, not realities. The tech suppliers love the hype because it convinces clients to invest, but the more confusing this all becomes, the more dangerous this hype becomes in turning off smart C-Suite executives who need to see real results before making real investments.

Careers are on the line with automation and AI, and the more embedded these technologies become in organizations, the more clients need real data and real evidence to create their roadmap for them. Outlandish claims like this are getting shot down faster than ever, and we need, as an industry, to stop pandering to the marketeers and panic-mongers and start having a realistic conversation.

Fed up with even the hype being so overhyped, that even The MIT Media Lab is severing ties with a brain-embalming company that promoted euthanasia to people hoping for digital immortality through “brain uploads”? Yes really.

Then waste no time as we plan to steer you back to some version of reality next week with an unvarnished, unsponsored, unpuffed view of the world, where any spin if countered with a powerful forehand down the line:

If I had a dollar every time an executive bemoaned their firm’s inability to “change their mindset”, to do anything differently to escape their habitual ways of running operations. And if I had a further greenback for every advisor who bemoaned how idiotic their customers are, because they “just don’t have the deep expertise to fix their underlying data structure”, I would have long retired to the Trappist Order to brew very strong beer for connoisseurs with beards (that doesn’t actually taste very nice, but it’s just so beardy).

Surely the perfect desired outcome, even if it tastes like crap

It’s all about bringing the operations closer to the customer, and lacking IT talent is a major impediment to achieving it

Getting to the point here, it’s one thing demanding your employees change how they approach their jobs to benefit your firm from deploying advanced automation and cognitive tools, but entirely another if you don’t have the technical expertise to put them to work. It’s one thing to design a leading-edge digital interface with your customers, but it’s rendered pretty useless if you don’t have the capability to integrate it with your operations to provide customer support, get your products and services to them and harvest their data to keep making smart marketing decisions to stay ahead of demand. It’s one effort to redesign processes around your customers, entirely another to redesign your operational infrastructure to make it actually happen.

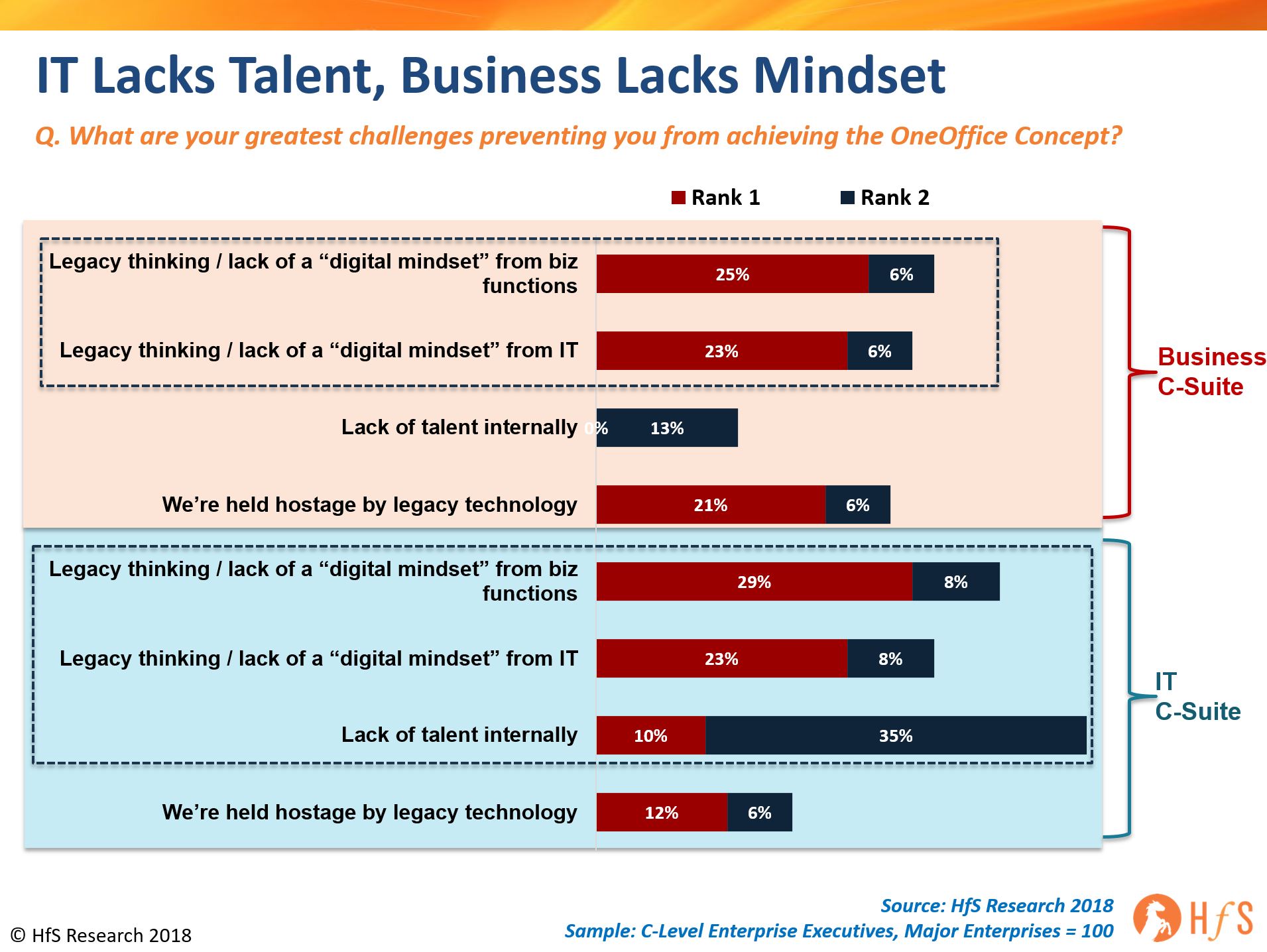

We recently interviewed 100 C-Suite executives from major enterprises and split the discussion across both business and IT leaders. While the industry obsesses about whether C-Suites know where to where to invest, what are their desired outcomes etc., we don’t focus nearly enough on the impediments preventing them from achieving these goals. We focus far too much on firms’ short-term spending on tools, and not enough on defining the ultimate outcomes and drawing up real investment and change management plans to get there. As we recently discussed, if we only focus on the means, we will never arrive at the end. To address this, we presented the OneOffice Concept to understand what is holding back both business and IT leaders from reaching the promised land of perfect real-time symmetry of their business operations staying ahead of their customers’ needs:

The Bottom-line: The Right Brain only functions when it’s in sync with the Left Brain

As we have widely discussed, four-out-of-ten customers (see earlier blog) going through initial deployments of RPA software are struggling to meet the business cases and cost savings goals. And when we bring hundreds of enterprise leaders together at our HfS Summits, the story is consistent: business struggling with change, but they struggle even more with aligning the right technical expertise to work alongside their business talent. Simply put, today’s firms are struggling with having IT depth to take their ambitious C-Suites where they want to go. So where do we go from here?

IT is at the heart of C-Suite strategy – it’s a business discussion that only works with the right IT capability. You only needed to eavesdrop on the many C-level discussions at Davos to know the IT discussion is firmly at the core of the business. Being able to satisfy your customer’s digital business needs is where it’s all heading. I was recently talking their the Group Finance Head at HSBC and his whole focus is on two elements – having the best digital app delivery and providing the best customer experience, which is incredibly challenging for any business environment grappling with differing compliance needs across borders, and ever-demanding customers wanting to do all their banking on an iPad. However, while this is a challenge, it is also a massive opportunity for the ambitious who get their business design and IT skillset equation right.

Finding the right partners is more crucial than ever. There is a massive opportunity to lead in the world of IT services, provided you can plug these skills gaps. The challenge is breaking out of the traditional sourcing model to access niche talent across the globe in areas such as crypto-technology, Python development, Lisp, Prolog, Go and C++. While most traditional firms still rely heavily on bread and butter IT services delivered at scale from regions such as India, the emergence of talent in Central and Eastern Europe, China and parts of South America also need to be brought into play. The IT services world will be a very different place in a couple of years as boutique firms offering niche skills come into the fore. Not to mention the emergence of crowdsourcing for IT talent. Having really savvy IT leaders who can cobble together crack teams on-tap to solve their IT headaches is already becoming a huge differentiator for many firms. The will also be a role for the super services integrator, who can pull together teams for clients to work with them on complex projects.

Simplification of business operations is the real key to future success. In short, there is no silver bullet to solve these endemic issues companies are facing to break out of legacy ways of working, but being able to align a determined mindset shift on the business side with smart IT skills to bring it to reality, is the only true way forward for firms who know their days are numbered, if they cannot change their inner workings to get somewhere near a OneOffice end-state. The future is really all about simplifying operations to bring them completely in line with the world of the customer. Hence, successful businesses need IT folks who can think logically to simplify business operations through the use of automation, cognitive, AI and digital. It’s not just about software packages and APIs, it’s about both business and IT staff learning to understand each other’s strengths and challenges better. It’s really not rocket science, it’s about learning to simplify business models to stay ahead of your customers’ needs and not giving your competitors a window to take you out of your market…because that may already be happening to you.