At the HFS Summit this week, we asked 200 enterprises if they cared about automation software vendors bragging about self-inflated valuations. Not a single person did.

The robotic transformation software industry has three problems right now:

i) Defining itself;

ii) Scaling Bots and being Transformational;

iii) Obsessing with this “Funding Arms-Race”… so let’s dig in

1) Defining itself correctly… “RPA” is not correct. Most of “RPA” in its current form is incorrectly defined, and this market is dying if it doesn’t have a radical overhaul. Only a small portion of “RPA” it is actually “process automation” – most of it is desktop apps, screen scrapes and doc management. RPA in current form is incorrectly labeled and the way forward is to integrate these tools. When we introduced the term RPA in 2012 (with Blue Prism) the focus was on unassisted automation, it was self-triggered (bots pass tasks to humans) and centered on increased process efficiency. Only a small portion of “RPA” today is actually “process automation”. Most “RPA” engagements today are not for unattended processes – they are attended desktop automation deployments, a loop of human and bot interplay to complete tasks (not processes). These engagements are not the pure form of RPA that we envisioned back in 2012 – they are a motley crew of scripts and macros applying band-aids to messy desktop applications and processes to maintain the same old way of doing things. We need to refer to these “RPA” products as Robotic Transformation Software products which is a far more appropriate description. Now if these firms cannot partner with their clients and the services ecosystem to support transformative automation as part of an integrated automation platform, this market balloon will burst as dramatically as it got inflated…

2) Scaling bots and finding a transformation story versus a “fixing legacy” one. The more these robo tools can be used by clients – not only to do things better and more automatically – but also to help re-wire their operations, then we have lift-off to something fr more strategic than merely getting crappy tasks working better and moving data round the company better. If you just work on steady-state fixes without focusing on the real changes needed, we will see many firms stuck in legacy purgatory, unable to switch out bots in the future. Sure, there is usually a reduction in labor needs – but in fractional increments – which is rarely enough to justify entire headcount elimination. Crucially, the current plethora of “RPA” engagements has not resulted in any actual “transformation”.

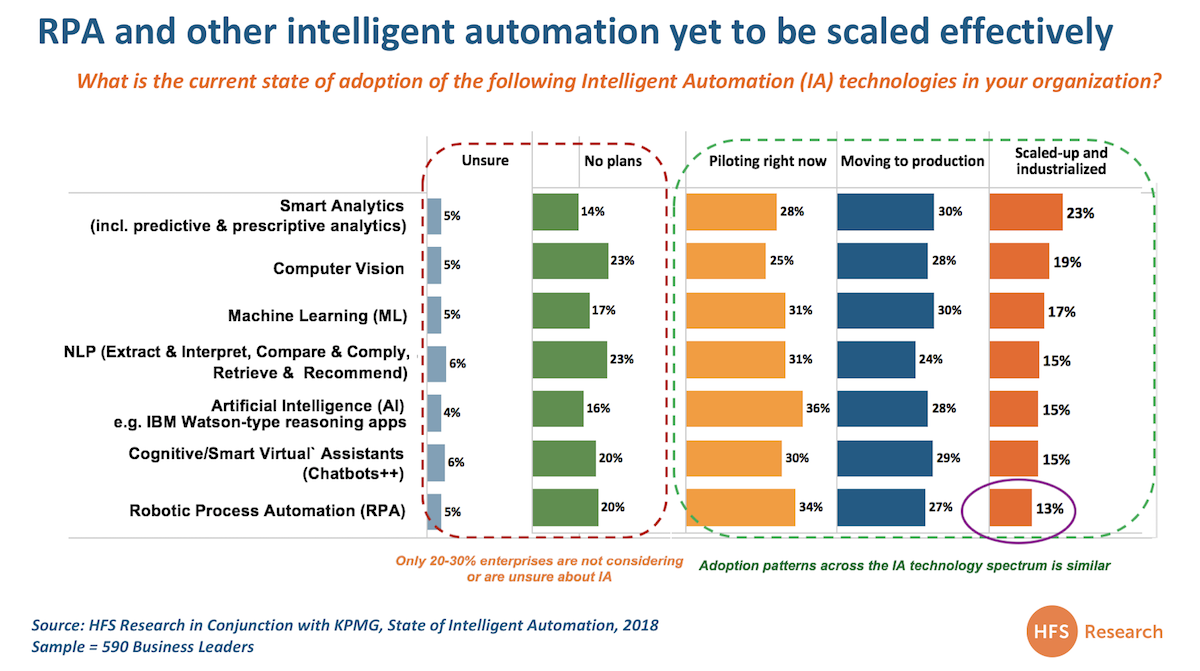

As our global study of 590 leaders of Intelligent Automation initiatives, supported by KPMG reveals, barely more than one-in-ten enterprises has reached a place of industrialized scale with RPA – and the word from so many clients is loud and clear that they need help:

This struggle to get to a point beyond pilot exercises and project-based experimentation could prove to be a serious point of failure for the whole industry. There needs to be a much stronger melding of enterprises with implementation and consulting capability to fix these issues. Just like we realized that throwing bodies at a problem does not solve the problem, we need to recognize that merely hurling software at business process will not drive transformation. The real genius lies in understanding what to use when and how. The software also needs to come with support and services. Otherwise, we’re just selling more snake oil and magic.

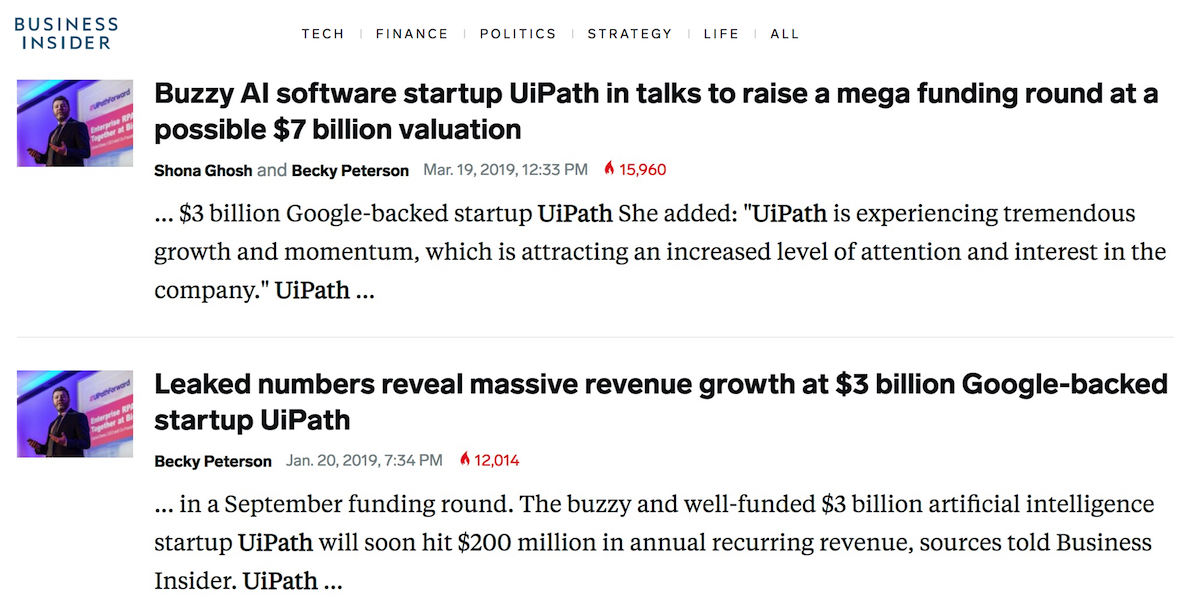

3. End this “Funding Arms-Race” obsession nonsense. Now. While Automation Anywhere was busy with its Imagine conference in London, on 20th March, “news” about UiPath’s self-proclaimed valuation, based on its much-discussed future Series D funding round, was conveniently released the day before, claiming the $3 billion touted last year was now a whopping $7 billion. It was also widely rumored that UiPath was pushing to announce their Series D during Automation Anywhere’s New York event last week. Here are some snippets from the Business Insider news publication, which was also picked up by Tech Crunch:

So what, pray tell, is the point in all this?

UiPath is putting the whole automation industry under unnecessary pressure. If the UiPath Series D round has yet to be signed, these antics could be placing the negotiating power into the hands of the investors, who can clearly see UiPath’s management is obsessed with embarrassing its hated rivals as opposed to focusing on the first 2 items discussed above. Fortunately for UiPath, they have officially secured Series D this week, but these antics and obsession with fictitious valuations do the industry no favors and put incredible pressures on the automation software companies and enterprise to deliver genuine scale and results on months when the reality is this integrated automation journey will take years.

UiPath is creating the perception that this whole industry is after a short-term cash bonanza. Our automation industry cares about making these solutions work, and this ridiculous noise about inflated funding isn’t adding any value anywhere – this valuation noise only makes most people think these software firms are obsessed with a quick IPO or a quick sale, as opposed to a true long-term journey that will help enterprises enter the hyper-connected age. I can guarantee you all – right now – that none of today’s enterprise operations leaders are basing their robotic software selections off these crazy media-fuelled “valuations”. It is also an entirely separate debate about why robotic software firms with revenues under $200m can claim 35x valuations… stay tuned for that.

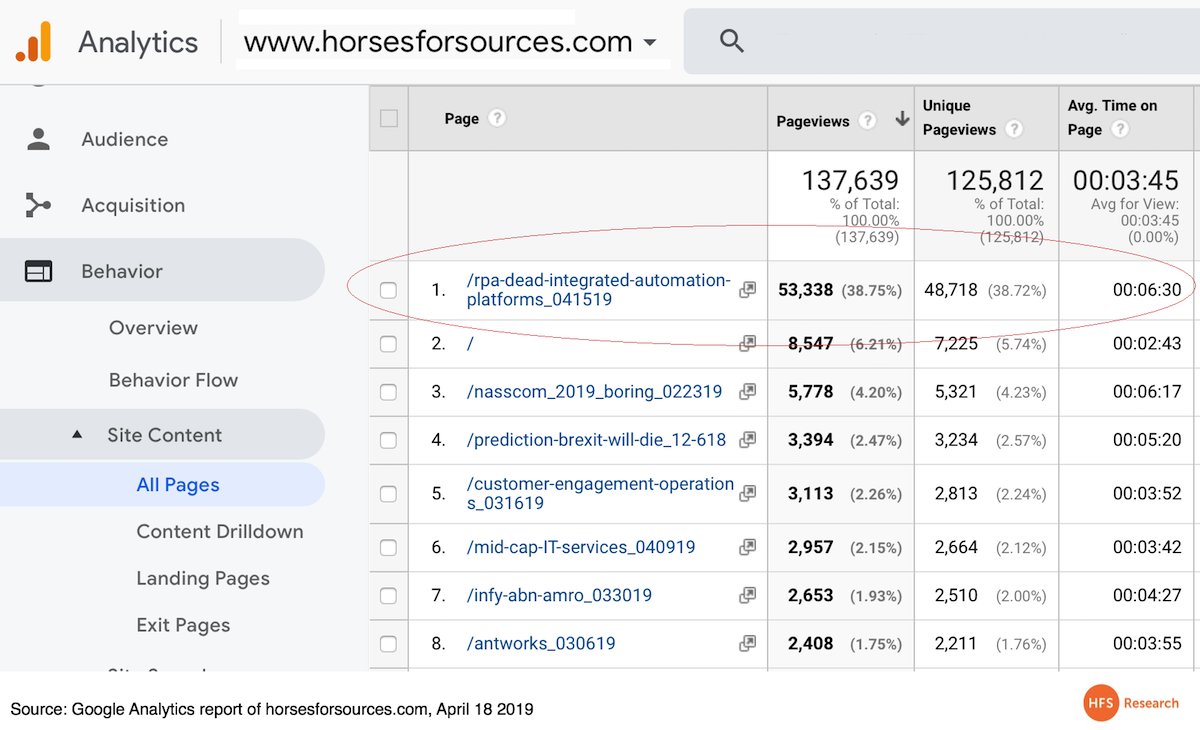

Well, you can’t beat a good headline, and you really can’t beat it when 50,000 people read the “RPA is dead. Long live Integrated Automation Platforms” blog article in just 48 hours, spending a whopping average of 6.5 minutes actually reading it. Yes, most of you made it further than the headline!

For those of you familiar with google analytics, I thought I would take the unique step of actually sharing some readership stats from our blog this week, just to show you how the extent of impact our plea to the industry is having to “wake up to enterprise integration and stop festering in obscure RPA”:

RPA as a term just doesn’t make sense anymore, but these terrific brands will thrive as Robotic Transformation Software. We re-badge RPA as Robotic Transformation Software (RTS) because that’s what it is (or what aspires to be). Only a small portion of “RPA” is actually “process automation”… most of it is desktop apps, screen scrapes and document management fixes. Most “RPA” engagements that have been signed are not for unattended processes, instead, most are attended robotic desktop automation (RDA) deployments. Attended RDA requires a loop of human and bot interplay to complete tasks. These engagements are not the pure form of RPA that we invented back in 2012 – they are a motley crew of scripts and macros applying band-aids to messy desktop applications and processes to maintain the same old way of doing things.

Integrated Automation Platforms are the Holy Automation Grail (HAG*) if we can make it there. Automation ultimately needs to support transformation, not legacy. The more these RTS tools can be leveraged by clients – not only to do things better and more automatically – but also to help them re-wire their operations to achieve their outcomes, then we have lift-off. These tools also need to make enterprises more agile – if you just work on steady-state fixes without focusing on how to make real changes down the road, we will see many enterprises stuck in legacy purgatory, unable to switch out bots in the future.

*HAG is not an official acronym, I just made it up. Peace out robo-warriors ✌

The biggest problem with enterprise operations today is the simple fact that most firms still run most of their processes exactly the same way as they did 20/30/40 years ago, with the only “innovation” being models like offshore outsourcing and shared service centers, cloud and digital technologies enabling those same processes to be conducted steadily faster and cheaper. However, fundamental changes have not been made to intrinsic business processes – most companies still operate with their major functions such as customer service, marketing, finance, HR and supply chain operating in individual silos, with IT operating as a non-strategic vehicle to maintain the status quo and keep the lights on.

Enter the concept of Robotic Process Automation (RPA), introduced to market in 2012 via a case study written by HFS and supported by Blue Prism, which promised to remove manual workarounds and headcount overload from inefficient business processes and BPO services. However, despite offering clear technical capability and the real advantage of breathing life into legacy systems and processes, RPA hasn’t inspired enterprises to rewire their business processes – it’s really just helped them move data around the company faster and require less manual intervention. In addition, most “RPA” engagements that have been signed are not for unattended processes, instead, most are attended robotic desktop automation (RDA) deployments. Attended RDA requires a loop of human and bot interplay to complete tasks. These engagements are not the pure form of RPA that we invented – they are a motley crew of scripts and macros applying add band-aids to messy desktop applications and processes to maintain the same old way of doing things. Sure, there is usually a reduction in labor needs – but in fractional increments – which is rarely enough to justify entire headcount elimination. Crucially, the current plethora of “RPA” engagements have not resulted in any actual “transformation”.

The major issue with RPA today is that it is automating piecemeal tasks. It needs to be part of an integrated strategy

Real research data of close to 600 major global enterprises show just how not-ready we are to declare any sort of robo-victory. In our recent survey of 590 G2000 leaders, only 13% of RPA adopters are currently scaled up and industrialized. Forget about leveraging RPA to curate end-to-end processes, most RPA adopters are still tinkering with small-scale projects and piecemeal tasks that comprise elements of broken processes. Most firms are not even close to finding any sort enterprise-scale automation adoption.

RPA provides a terrific band-aid to fix current solutions; it helps to extend the life of legacy. But does not provide long-term answers. The handful of enterprises that have successfully scaled RPA across their organizations have three things in common:

A unifying purpose for adopting automation,

A broad and ongoing change management program to enable the shift to a hybrid workforce, and

A Triple-A Trifecta toolkit that leverages RPA, various permutations of AI, and smart analytics in an integrated fashion.

So HFS is calling it as we see it. RPA is dead! Long live Integrated Automation. And by integrated we mean integrated technology, but also, and all importantly, we mean integration across people, process and technology supported by focused objectives and change management. Integrated Automation is how you transform your business and achieve an end-to-end Digital OneOffice.

Integrated Automation is not about RPA or AI or Analytics. It is RPA and AI and Analytics.

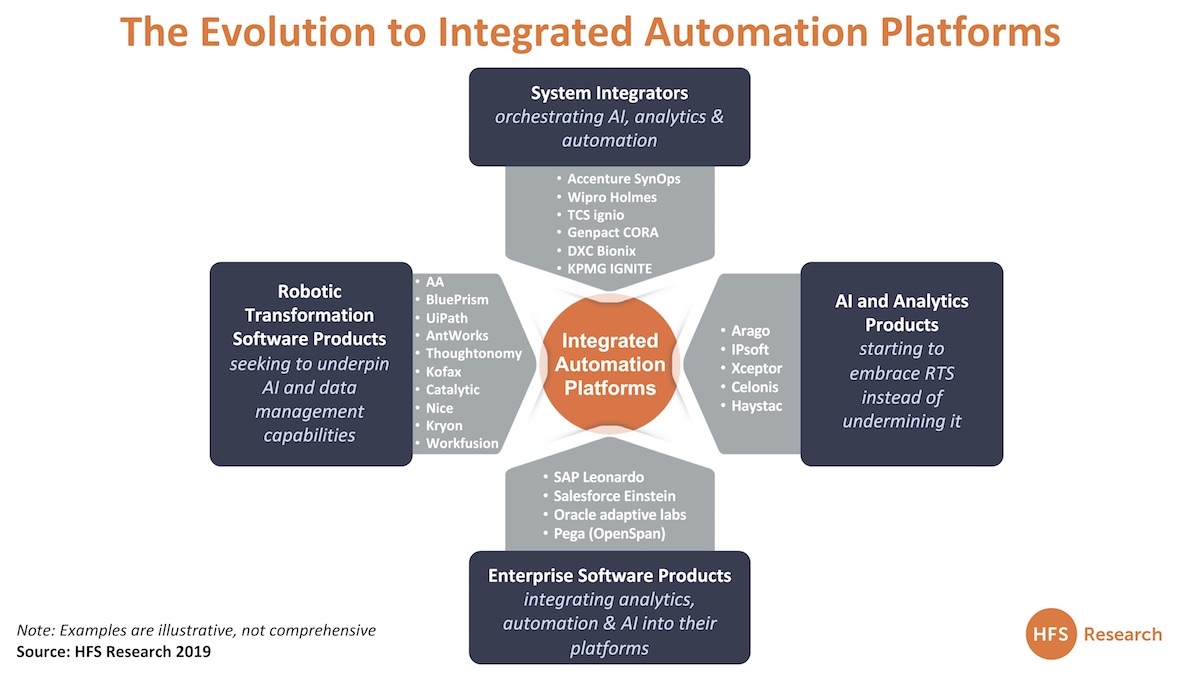

Business problems are not entirely solved by one stand-alone technology but by a combination of technologies. While only 11% of the enterprises are currently integrating solutions across the Triple-A Trifecta, there is emerging alignment. The supplier landscape is also starting to realize that clients will buy integrated solutions (see Exhibit 1) and examples below:

RPA products are seeking to underpin AI and data management capabilities. WorkFusion was arguably the first to combine RPA and AI with its “smart process automation” capability. Other subsequent examples include Automation Anywhere with its ML-infused IQBot, Blue Prism announced its AI Lab to develop proprietary RPA-ready AI elements, and AntWorks embeds computer vision and fractal science in its stack to enable the use of unstructured data. What these products having in common is their use of robotics to transform tasks, desktop apps and pieces of processes. Hence, we need to refer to these “RPA” products as Robotic Transformation Software products which is a far more appropriate description.

AI and analytics focused products are starting to embrace Robotic Transformation Software, instead of undermining it. IPsoft launched 1RPA with a cognitive user interface. Xceptor’s data-led business rules and AI-based approach to automation leverage RPA to help extend its functionality. Arago is starting to go to the market where it can help orchestrate RPA capabilities within its platform.

Enterprise software products are integrating the triple-A trifecta capabilities in their products. SAP Leonardo aspires to harness the emerging technologies across ML, analytics, Big Data, IoT, and blockchain in combination. It also acquired RPA software company Contextor (late 2018) similar to Pega when it acquired OpenSpan in 2016 adding RPA functionality to its customer engagement capabilities.

System Integrators are orchestrating the Triple-A Trifecta across multiple curated products. This typically combines some of their IP and service capabilities. Accenture launched SynOps in early 2019, offering a “human-machine operating engine.” Genpact’s Cora, a modular platform of digital technologies, similar to HFS’ Triple-A Trifecta, is designed to help enterprises scale digital transformation. IBM’s Automation Platform includes composable automation capabilities that orchestrate responses and alerts between Watson and Robotic Transformation Software solutions. KPMG’s IGNITE brings RPA, AI and analytics tools together with KPMG IP and services.

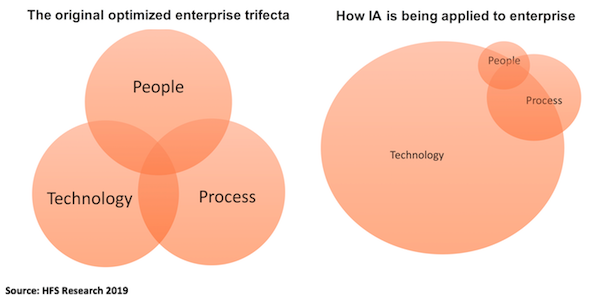

Integrated Automation is not just about Technology. It is Technology + People + Process.

The real point of Integrated Automation is actually to move beyond the tools. Yes, the Triple-A Trifecta offers more functionality, but it still does not work unless you change your business, your people, your processes. Integrated automation is the effective melding of technology, talent, organizational change, and leadership to get to the promise land. It requires the integration of the Triple-A Trifecta change agents in your toolbox and their application across the original trifecta of people, process, and technology. If you keep throwing technology at a business problem, you will have more technology rather than a solution.

Technology has overpowered the discussion today without adequate focus on people and process:

Source: HFS Research 2019

Integrated Automation is not a Product or a Service. It is a Product and a Service.

Just like we realized that throwing bodies at a problem does not solve the problem, we need to recognize that merely hurling software at business process will not drive transformation. The real genius lies in understanding what to use when and how. The software also needs to come with support and services. Otherwise, we’re just selling more snake oil and magic. Strategic and collaborative relationships of the future will be formed by providers that can consult as a trustworthy advisor and execute as an “extension” of clients’ operations. Enterprises need partners to drive innovation, contribute investment, apply automation and new ideas, and focus on delivering business outcomes – and that requires a combination of services and software. An ecosystem approach with symbiotic relationships between service and product companies is a must-have ingredient for automation to succeed and truly be transformative. It is imminently clear that no one can be everything to everyone.

Adoption is not the measure of success for Integrated Automation. It is about Change Management.

Fifty-one percent of the highest performing enterprises see their cultures as holding them back in the digital transformation journey, while only 36% of the lowest performing enterprises identify culture as a problem to progress. Providers need to offer change management approaches that are agile, measurable, and iterative to be impactful. Scaling up digital initiatives and enabling the right governance models are also critical points. The ability to codify “business outcomes” in contractual agreements, pricing structures, and performance measures is also a vital element to drive change. While there is no nirvana around pricing, it needs to be implemented based on every client’s unique requirements and context. The flexibility to put skin in the game with innovative and non-linear commercial models is essential to drive real change.

Integrated Automation will not be effective with a functional approach. It requires an end-to-end “OneOffice” strategy.

Less than 12% of the enterprises we surveyed have an enterprise-wide approach to automation. This strong focus on task-level and process-level automation remind us that automation often takes place in functional silos, with parallel but unconnected initiatives. The ability to balance task-specific and process-specific pilots and production instances with broader enterprise mission and vision is certainly daunting, but it is precisely what needs to occur to enable scaled and successful automation programs.

The collaboration between business and IT is another crucial issue. While automation initiatives require IT involvement, the programs are generally impacting and enhancing business processes—which requires participation from business constituents who understand the functions in question. The ideal leadership mix, then, is a combination of IT and business. However, our data shows that just one-fifth of respondents have created integrated IT and business leadership teams to grapple with automation strategy and deployment.

Bottom Line: Integrated Automation utilizes the power of AND, not OR!

We are lucky to live at a time where we have a multitude of established and emerging change agents at our disposal: global sourcing, design thinking, Robotic Transformation Software, AI, Analytics, IoT, and blockchain, among others. But, unfortunately, most of the discussions in the market end up becoming a comparative discussion versus integrative discussion – man versus machine, offshore versus automation, RPA versus AI, consulting versus execution, and so on. These change agents must work together rather than operate in silos to solve real business problems. The power of AND is much greater than OR and Integrated Automation is all about the power of AND. Thus, RPA is dead. Long live integrated automation!

Brian Whipple, CEO Accenture Interactive, describes the evolution of the world’s premier experience agency

The term “digital” has become overused, diluted and – in many ways – rendered useless. After all in 2019, what ISN’T digital, and what’s the point in distinguishing? We have instead moved to a world that’s comprised of integrated and immersive experiences – as consumers, or as patients, as employees, etc – experiences that shape our buying habits and our quality of life. The recent announcement of Accenture’s acquisition Droga5 has raised the stakes of creating immersive customer experiences to a whole new level (read our POV here).

Companies that are really seeking to align themselves to experiences need to break down their silos and better understand what their customers want… and really execute on that. We caught up with Brian Whipple, Accenture Interactive’s CEO (and recent winner of an HFS Disruptive Award), to learn how his firm’s massive acquisition appetite has helped build a company embracing an entirely new philosophy, helping its clients align to customer needs in the post-digital world. Accenture is integrating technology, design, commerce and content to help clients develop “living” experiences that meet customer needs today and are ready to evolve in the future – requiring a wide breadth of talent, expertise and even cultures within cultures to deliver on those experiences. The bits and pieces that have come together at Accenture Interactive over the last several years, most recently with Droga5, are all adding up to Accenture’s mission to “create the greatest customer experiences on the planet for our clients.”

Phil Fersht, CEO and Chief Analyst, HFS Research: Can you talk to us a little bit about how digital came to be, and how Accenture Interactive came in to the space? Because you were really the first of the service providers to coin the “Digital” phrase, and really put it together, industrialize it, etc. Could you give us a brief history about how it came to be, how it got started, and what the original philosophy was, and how that may have changed in the last five or six years?

Brian: Sure. There are three distinct phases to date, for Accenture Interactive. The original philosophy was that the world needed digital diagnostic tools that work in the arena of digital marketing; things like online campaign optimizers, A/B testing it, “I’m going to present offer A, with this creative treatment online, and I’ll test it against offer B,” or, “I’ll move it on a placement in a banner,” or, “I’ll have the banner come up in a different media vehicle,” and you learn from that, then redirect investment. Typical relationship marketing/direct marketing concept, but for digital, so you’re optimizing how you serve up creative advertising, digitally. And that was the one tool.

A second tool would be around things like digital diagnostics, like scanning through webpages, looking at traffic, looking at problems, and broken links, and where people get stuck on a page, and when people abandon a commerce transaction, and diagnostics around digital commerce. And those were looked at from a software tool perspective, and so at Accenture, we made a couple of small software acquisitions, and the genesis of Accenture Interactive was largely around these software licensing tools, around digital optimization and digital diagnostics.

When I came on board, we’d started that, but there was what we perceived to be a much greater opportunity– and that was a particularly crowded space, at the time – and the opportunity was really around doing what Accenture does best, which is stick to a services company, but apply that best-in-class services company mentality to the marketing space, instead of to the CIO space. So there was this notion of developing capabilities for the CMO, instead of the CIO, but keeping the concepts of being their business advisor, trusted relationship, multi-year contracts, and bigger, not smaller.

Phase two of Accenture Interactive was developing large capabilities, really in three or four areas, those areas being strategy and design, marketing, but commerce and content. So, you know, design, marketing, commerce and content, those four practice areas, and so we built up global large scale practices in those four areas, and that was the main, huge growth engine for Interactive that you saw, and you saw us go in to the billions in the Ad Age reporting, and things like that.

Then, about two years ago, we slightly pivoted again, through leveraging those capabilities much more into reinventing experiences for clients, and it’s really not about advertising per se, and not about augmented reality per se, or email marketing, or any particular capability. It’s about stitching them all together, to reinvent how people receive patient care, from a hospital group, or how people fill up their car with gas, or how people try and close at a department store, or any of these normal, like, consumer experiences you and I have, that need all of those things, and that is where we are now, as an experience agency. That’s the evolution. That’s phase three.

Phil: You very eloquently expressed a lot about bringing the technology to the user, in our personal lives, into our commerce lives. Some of these basic digital capabilities, how can companies respond to the needs of their clients as those needs arise, are working towards this emerging phase, getting more about how can companies anticipate their client needs better, before they even arise, and how intelligent can they become, as they start to evolve. Is that where you guys are going? Do you feel that’s what you’re already doing? Or do you think that’s the phase that we’re moving in to?

Brian: I think that’s, to some extent, table stakes now, but I don’t think it’s executed all that well. The notion of, essentially, in layman’s terms, giving people what they want, and in technical, or consulting jargon, it would be “personalization experiences”, and “expectation management”, and all those types of buzzwords. But what it really comes down to is, the technology is there to have micro personalized experiences today, but what people want may not be that, so it is about finding out the degree of personalization that individual consumers want, and then tailoring your experiences to those wants and needs. That orientation is what any consumer-facing experience should be aspiring to have today.

Now, the execution of that, how many companies do that particularly well, and are really reinventing things for efficiency and for human good, a la something like an Uber, or like Amazon, Spotify, etc., but there’s tremendous growth ahead of us, in the broader experience industry, to do that. The capability is there, it’s the execution of that, to give people exactly what they want, is spotty, in the industry. It’s hit and miss, today.

Phil: Right. And as things have evolved, a lot of CMOs have started calling themselves CDOs, and obviously, the use of the term “digital” has become a little bit too convoluted. Accenture’s the master of coming up with new terminologies and phrases. How do you see this happening? Are you going to stay true to this digital value proposition? Or do you think is actually now morphing into something different?

Brian: I would say, at this point, at 2019, what isn’t digital? And the notion of things being digital, that digital equals new, or digital equals better, I think is a notion that should probably be about to sunset. Because anything new is inherently digital, so it’s sort of redundant in its vocabulary, as a general descriptor. Now, I think leveraging the many technologies that are out there, that are all, scientifically, digital, to create, reinvent, establish, meaningful, efficient experiences for our clients, and our clients’ customers, we’re just only at the infancy of that. It’s just that I don’t think we need to refer to it as digital because everything’s going to be digital. It’s table stakes. So I doubt that five years from now, we’re going to see new firms sprout up that’s going to be, you know, “ABC Digital”, or something like that. I doubt that.

Phil: Right, remember “e-business” 20 years ago? As you look at the type of business Accenture’s becoming, in a digital, interactive scenario, you’ve acquired 30-odd of these design agencies around the world, so you have a lot of local talent, and we’re familiar with how you’ve bedded some of those in. And then you’ve obviously got a lot of competitors in the space, who may be much, much less focused on design, and they like to focus on the enablement of these digital capabilities. How important is it to have one company to do the design and the implementation, and the execution, and the management? Or do you think some clients have a good experience breaking it up. so, they may use Accenture for design, and go with a different business to maybe execute? What’s been your experience of that?

Brian: Yes. So, I definitely have a defined point of view on this, right or wrong, and that is that, as experiences are redesigned, all of them have built-in feedback loops and mechanisms, and are constantly… well, the word we would use to describe them is “living”. It’s not something you build it, implement it, and then go away for five years. They’re constantly evolving and changing, based upon new expectations and elements of the experience, and new technologies that come out available. So, within Accenture Interactive, and we are Accenture Interactive, these aren’t separate companies now, because we integrate them, as those companies come in, they’re not all design. Some are design, some are commerce, some are digital content, some are digital twin technology companies. They’re all pieces of a capability that are part of rendering compelling experiences.

So if you are a client who is reinventing how you try on clothes at a high-end department store in Japan, and rolling that out at your flagship stores in London, and New York City, and San Francisco, etc., then the design elements of that, along with the actual commerce technologies, and mobile technologies, connected device technologies on your app, as you walk in to the store, all with the customer service agents, and purchase histories, all of those things are all linked. So if your design of your experience is in a completely different partner than your technology experience, that becomes cumbersome, at best. So that is why we are not a design agency, and we are not a commerce agency, and we’re not a digital content agency, and we’re not an advertising firm. That is why we are an experience agency. Because you have to stitch all those things together, with people actually, physically, butts in seats, sitting together, so that all those things are naturally integrated.

There used to be this notion that a new process was designed, and then you’d hand that through to some “delivery organization.” And that delivery organization would then build it, and then it would go in to what’s called “production”, and it would run. That’s not the case anymore. All of these technologists, and the designers, and the creators, they all sit together. These are all integrated, very quick, agile technologies that people use, and, you know, artists and scientists are not all that different today.

It’s not so much that I think having them separate is a disaster, but I can tell you authoritatively that we see tremendous market value by integrating all those capabilities together, because it’s constantly evolving, and they’re not separate things anymore.

Phil: Interesting, I think that’s a very pertinent point. And as you’ve evolved the business and brought on lots of agencies, and these kids with nose rings, and all that type of stuff, how have you found integrating it into Accenture, over the last few years? What’s worked, what hasn’t, and where do you see this going next?

Brian: Yes, of the companies that we have folded into Accenture Interactive, there’s a couple of salient points there. One is that Accenture Interactive, and our leadership, Pierre Nanterme, and many other top executives, my colleagues in Accenture, have been very supportive of us having our own culture. So, Accenture Interactive is expected to push boundaries within Accenture, culturally, in terms of the types of studio office space we have, and things that are perhaps less strategic, like dress code, and things like you mentioned. So that’s point one.

Point two is that not all of the companies that are now part of Accenture Interactive are typical creative agency types. Some of them are technologists. We have some of the leading, for example, ecommerce technology, around Hybris or Websphere, or people that are deeply skilled in Adobe Engagement Manager, or other tools like that. These are technologists and integrators, and many of them have cultures that are similar to the recent cultures of Accenture around technology integration. It’s just that we’re doing it in a marketing space, instead of, say, in financial management, or business, or supply chain, something like that. And all the marketing stuff is in Accenture Interactive.

So, although we have what we call a culture of cultures, in Accenture Interactive, and we embrace that, as long as you are united, around the P&L incentives, and around the mission of being laser-focused on creating the greatest customer experiences on the planet for our clients. So I think, if you were to go in to our studio in Hong Kong, or in São Paulo, or in New York, you would find, you know, high-end, you know, virtual reality studios, next to designers, next to commerce architects, and the like, and many account service people, who are really the experience architects for clients, all working together. And yes, at Accenture, they have embraced that. But the key to it is, you have to have innovation, not far away from the core, but you have to have it at arm’s length from the core, or else the innovation will stifle, and our management has been great about giving us that arm’s length.

So, of them are called agencies, but they’re more like commerce integrators; some of them are true agencies, like Karmarama in London, or Rothco in Dublin, but culturally they have to buy in to the notion of being aligned around customer experience. So, for example, Karmarama in London; if they want to just be a really strong brand creative ad agency, then we’re not the right home for them. If they want to do that in the context of helping clients reinvent broader experiences and leveraging technology, and all that, and work on much larger transformational assignments, we are the right home for them.

So, there’s a certain weeding out of cultural affinity that happens naturally, in our process, when we look at possible acquisitions, and that is aided by the fact that we don’t ever, and I’m adamant about this, ever do a deal for the sake of just getting bigger, or growing revenue. Never, ever, ever. We would do a deal to add a new capability, which we feel is part of rendering future experiences, such as Mackevision, with its digital twin augmented reality technology, and such as Karmarama. Or we are trying to scale a new capability –scale this experience agency thing, in a geography where we are subscale, such as what we did in Tokyo, a few years ago, with IMJ. And that becomes the seed for Accenture Interactive in that space.

So, in summary, Accenture is very supportive of us having a different, but yet complementary culture, and it’s very much our role to help push the broader technology firm, and we’ve been given that leeway. But in terms of within Accenture Interactive itself, there are different cultures. A commerce architect is not the same thing as a service designer, and we don’t force them to be the same, but you have to be aligned around the desire to reinvent experiences, rather than working only in your silo. If they don’t, then they don’t become part of the Interactive family in the first place.

Phil: Right. That was very well put, and I think that’s given us some food for where this shifts. I’ve got one final question for you, Brian. If you were anointed the Emperor of Digital, which we kind of did, but if we did that for one week…

Brian:[Laughs].

Phil: What’s the one thing you would empower, to change the industry for the better? What would you enforce, on making digital better for everyone?

Brian: Without a doubt, I would take a couple of these experiences that have direct impact on human benefit, and change them. Not all, but many of them are in healthcare, and I would unite resources, really of the world, to kind of tackle them. I’ll give you two examples. If you have a loved one receiving chronic care for some kind of cancer … you know, every three weeks receiving a chemo infusion, and the like. The coordination of care between different hospitals, the flow of data between the anesthesiologist for procedures, and the oncologist, and the general practitioner, and the specialist, say it’s a throat cancer, so the ENT. All the different disciplines, the coordination between them is abysmal, and it’s abysmal globally, in the Tier 1 medical centers of the world. And that is an experience we can solve with data, with technology, and with user requirements, and changing that experience through a better design. We just have to align and do it, and create the economic incentive.

So I am very passionate about some of these experiences that have not changed in 20 years. Maybe you have a child that broke her ankle on the basketball court or the soccer field. That child goes in to the emergency room, or trauma centre of the hospital, where you don’t know how long it will be until he or she is seen, you don’t know what doctor’s on call, they don’t have any of your medical insurance information, it takes forever, you don’t know what the options are, you don’t know which hospital… but all the technology is there to solve all of that. Aligning some of these experiences to create human good is something that is an increasing priority for us in 2019.

The problem is not technology. The technology is there. The problem is – and this is sort of the headline of this answer – that we have to help clients break through what we call the “permission barrier”. The permission barrier is the census of consensus management, and risk aversion, and lack of innovation, because I don’t want to screw up, and I just want to do what my competition is doing. There’s some of that going on right now, and I actually think technology, right now, is being underutilized. And we’re seeing it in healthcare, being one of several places. I hope that helps.

Phil: I think your wish is something that is very commendable, and I’ve seen it, myself, with how much impact it can have on the healthcare systems, and interacting, giving people more information, and everything, so I think it is truly revolutionary, and it’s great to hear.

Brian: You know, so much money is put in to solving healthcare issues, and it should, I’m not trying to subtract any of that money, but if we could also pay attention to what the actual patient experience is, in terms of the quality of life, not the quantity of life, I think that would be a very good thing.

Phil: Yes. Good. Well, that was a great wish to have, and I look forward to sharing this discussion with our network.

Brian: Thanks for the reach out. I’d like that, and have a great weekend. I appreciate your time.

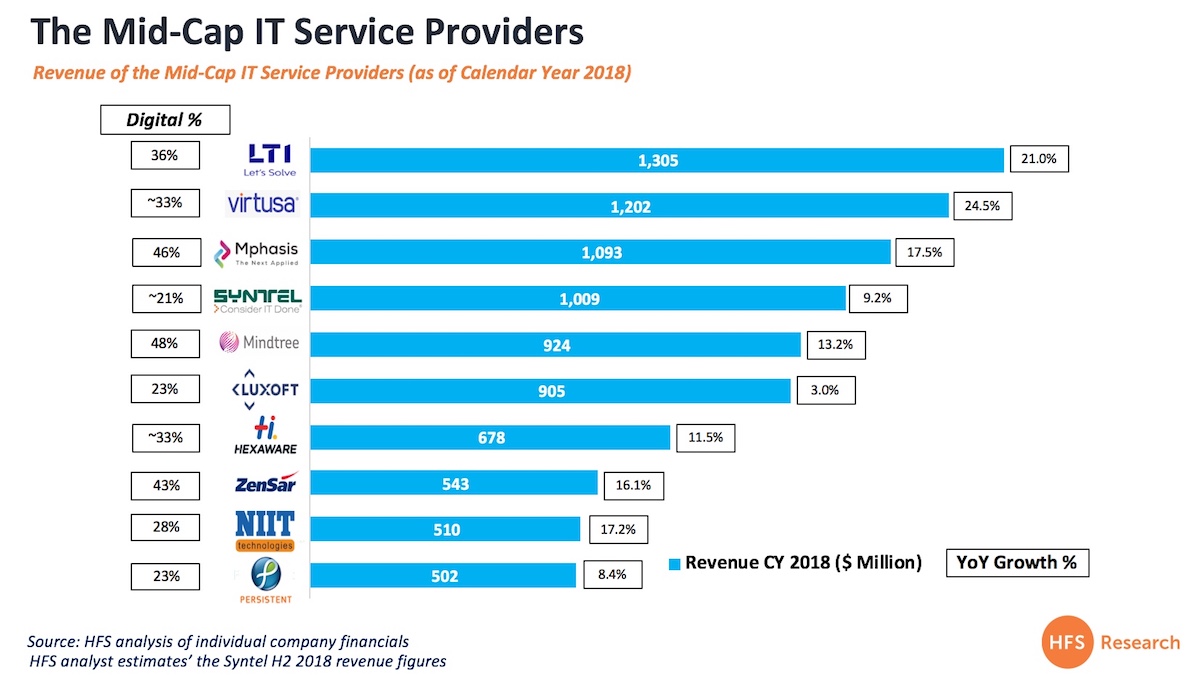

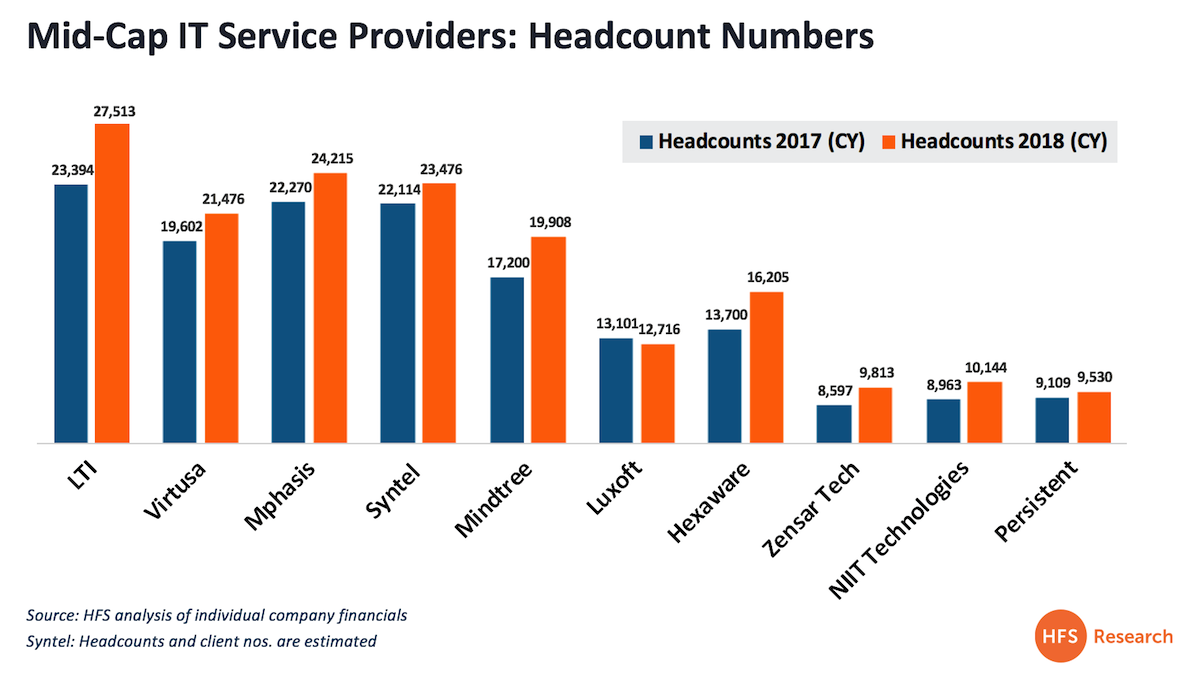

These are unique times for IT services – at the big-ticket end of the spectrum you have the mega-scale and competitive-cost propositions of the tier 1s vying for greater wallet share within their enterprise clients, while at the other, we have specific technical needs that warrant a lot of close attention that grabs the focus of the “mid-caps”, which are much more flexible and can operate at smaller scale, while turning an attractive profit.

The mid-caps are catering to the “build” needs of enterprises where the Tier 1s often struggle to deliver top talent

I recall just a couple of years ago how many of the big boys arrogantly called time on the smaller providers, but the exact opposite is transpiring; many clients are less brand obsessed as they once were and are more focused on accessing the skills they need with the attention they deserve. Why settle for a B- team, when you can get a B+ team that’s going to go the extra mile and work with you to figure out how to deliver complex requirements? And the numbers, simply, do not lie:

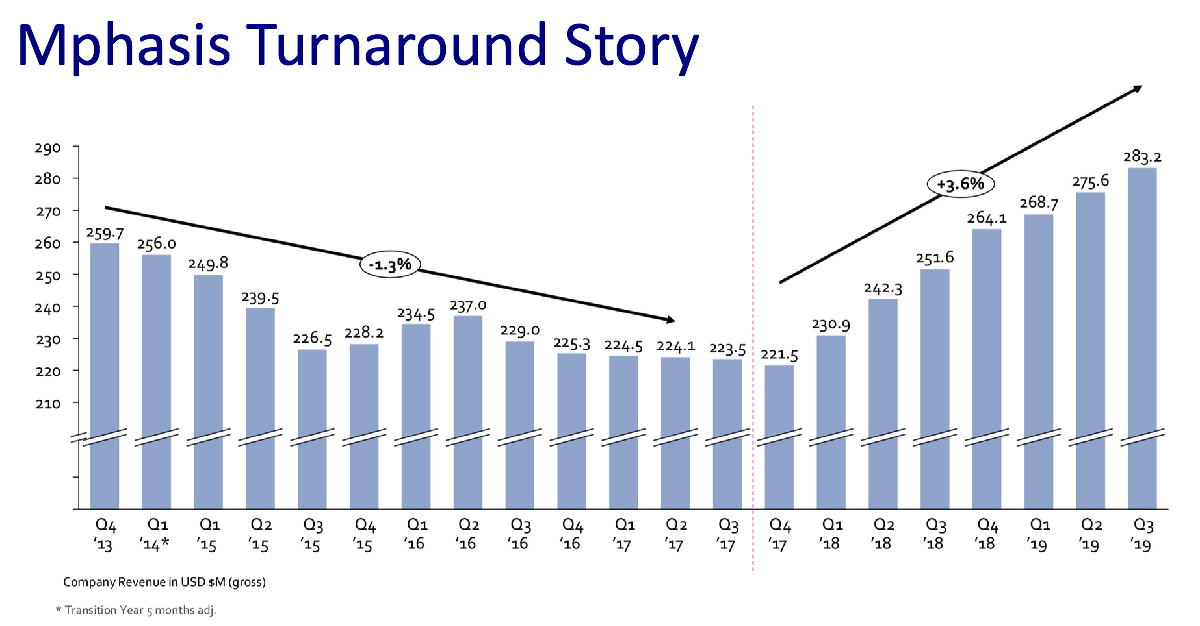

The mid-caps can rely on dynamic personalities to win deals

Remember the good ol’ hyper-growth days of IT services where the likes of Chandra (TCS), Frank (Cognizant), Nandan (Infosys) and Shiv (HCL) would fly around the world to close deals? Well, those days are long-gone as the top tier providers are simply too large and clients know they can’t just pick up the phone to scream at the CEO anymore.

However, they can still do that with most of these mid-caps. We conveniently forget that services is still largely about people and that personal touch from the top is still what most clients really want. One such eye-catching success story has been that of Mphasis, where the impact of CEO Nitin Rakesh (read the interview here) has been nothing short of remarkable:

Bottom-Line: The success of the mid-caps was not in the script… new rules of services are being written

In the last few years, Capgemini acquired IGATE and Atos acquired Syntel. In both cases, the company being acquired was the leading mid-cap on the market, and both provided some crucial resources for European-centric service providers lacking strong Indian delivery capability. However, what transpired since has been the door opening for the next tranche to step up up – notably LTI, Virtusa and Mphasis – all of whom have blown past $1billion. While LTI and Mindtree are embroiled in a less-than-friendly merger and Luxoft has already been bolted into the DXC empire, it would be of little surprise if any of the successful ones in this list are snapped up in the coming months as enterprises grapple with their needs for close attention to their creaking IT infrastructures and the dire need to develop agile capabilities, take better advantage of automation and AI tools… and find more sophisticated help to sort out their cloud messes. And as the latest ones are picked off, it’s simply the time for the next wave to step into the void… firms like Zensar, NIIT and Hexaware are routinely discussed these days as strong providers in their own right, and are also potentially attractive acquisition targets, provided the fit is right(despite decades of heritage).

These are the new rules of the services game… because the simple fact is that there are no rules and we’re all writing new ones as the need for rapid, personalized IT salvation becomes more and more a critical part of the C-Suite agenda.

For all you blockchain aficionados, you’d better get quantum-savvy asap, or you’ll find yourself having to re-skill yourself to do something relevant

This article will discuss some aspects of quantum computing, but – don’t worry – we’re not going to detail out all of the different uses in one initial education. It’s not going to describe the workings of quantum and we shall avoid using words like qubits as much as possible, we won’t mention quantum supremacy or the theory of quantum entanglement. If you want to know about these things, buy an undergraduate quantum physics textbook and then explore a decent quantum computing book like “Quantum Computing: A Gentle Introduction” by Eleanor Rieffel and Wolfgang Polak. Which we are lead to believe is only gentle to those with a good undergraduate understanding of maths and physics. Although in a review, Physics Today described it as a masterpiece. But for you blockchain followers, we’re sure you can quickly redefine your talktrack to wax lyrical about Quantum for your next Ted Talk.

The difference between quantum and traditional computing is at an eye-wateringly fundamental level. And this requires the knowledge we mention above to have a fighting chance to understand what it is. But is something every business leader needs to at least know about, even if it is just to be able to ignore with confidence. This is because quantum computing is potentially a disruptor with as big an impact as digital computing. And it is not an exaggeration that it can be used to simulate the very fabric of the universe.

The development of a practical quantum computer could have dire consequences for traditional encryption

However, the question still remains: Is practical quantum computing still just a theory, or an impractical experiment with any stable use decades away? Or is it potentially just around the corner poised to disrupt the very core of encryption technologies? Particularly given the (not passing) resemblance to other over-hyped transformative technologies like nuclear fusion and room temperature superconductors. All dreamt up in the golden age after the second world war and without a tangible end-point, with the seemingly constant promise of a miraculous breakthrough in spite of massive investment. Which seems particularly relevant given that current quantum computers need superconductors, and the insane supercooling that currently goes with them, to operate. Making them, to many, expensive, impractical flights of fancy; fuelled by journalist research hyperbole.

So, with that said, is that all you need to know? Your job is just to laugh in the face of any minion that utters the phrase “maybe we should invest in some quantum?” Unfortunately, it is not that simple. The trouble is no one really knows the actual timeframe, even John Preskill, the Richard P. Feynman Professor of Theoretical Physics at CalTech, can’t give you a firm time-frame. With predictions ranging from single to multiple decades and the current wave of “noisy” quantum experiments unlikely to have much practical use. However, this uncertainty needs to be weighed against the serious risk. The development of a practical or at least partially practical quantum computer could have dire consequences for traditional encryption.

The first algorithm set to run using a quantum computer could have seismic, rapid implications

Part of the excitement around the prospect of Quantum computing is the first real application – the first algorithm set to run using a quantum computer could solve the mathematical factoring equation very quickly. This can be used to break existing methods of encryption like RSA and ECC rapidly. So any organizations that use encryption technology need to understand that there is a potential weakness in current systems, which will need to be replaced or strengthened when practical quantum is available.

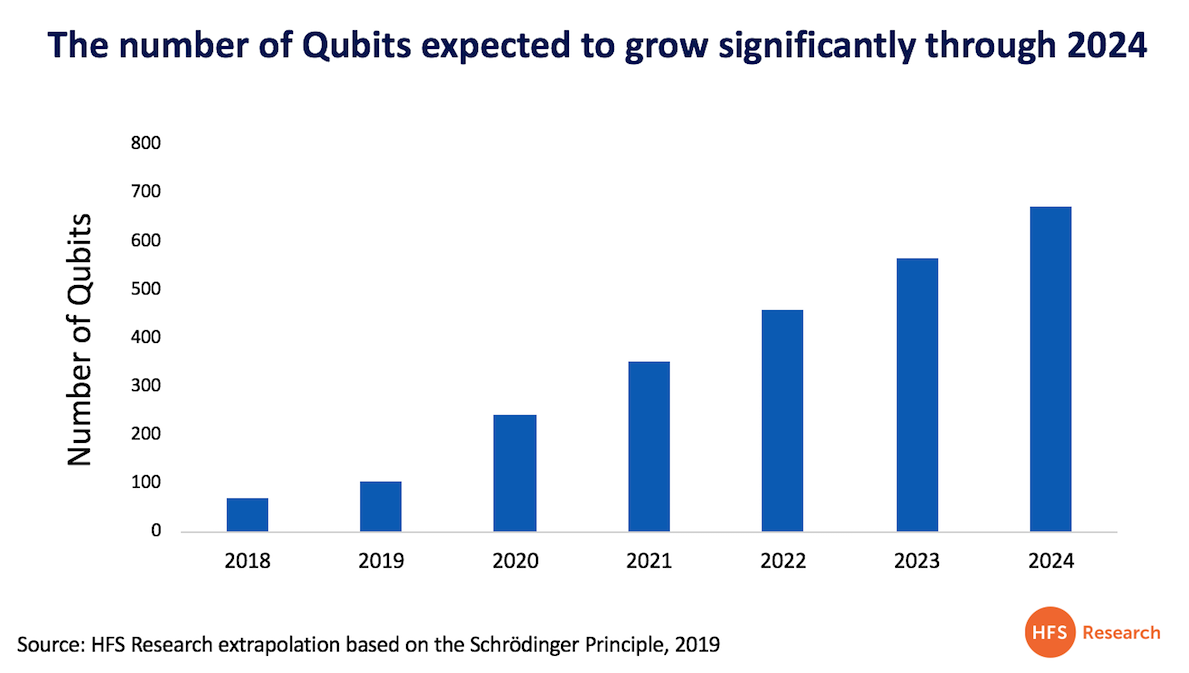

And recent experiments from Google and IBM have started to erode confidence in the long term predictions and have started to bring forward the prediction from decades to years. With both these firms recent experiments showing that quantum is starting to conform to Moores law. Which, if true, means we will have Crypto breaking quantum in 2 years rather than 20.

As quickly as 2021, HFS researchers believe we could see a quantum computer capable of breaking RSA encryption of 256 Bits – which would have serious implications for blockchain, given this is the level of encryption currently used. According to HFS academy analyst Duncan Matthews-Moore, “If we don’t get a handle on the potential speed of quantum soon, we could see the billions of dollars that have gone into blockchain become as quickly wasted as the vast sums Brexit is costing the UK economy.”

Bottom Line – Quantum is the one to watch, particularly if you have any ambitions around blockchain.

Forget RPA, forget AI, forget cloud, forget disruptive mortgage processing – and especially forget blockchain. Because if quantum can delivery real algos, everything tech that happened before is going to be disrupted like Betamax, like CB radio, like Sonic the Hedgehog.

And of course… this was an:

Please, please don’t tell me you fell for this again for the TENTH year in a row! …And I know some of you did =)

And while we’re reminiscing about falling for April Fools’ gags, here is 2018’s classic:

Infosys has just announced a joint venture with ABN Amro for mortgage administration services, where it will acquire a 75% stake in Stater N.V., a wholly owned subsidiary of ABN AMRO Bank N.V., that offers mortgage services across the value chain including origination, servicing and collections. The transaction is valued at $143.53 million and is Salil Parekh’s second acquisitive move in Europe since his appointment as CEO a year ago. Clearly, bolstering its European presence is a big deal for INFY in 2019, gaining more “zero distance” impact with European clients, adding more innovation centers, and strengthening its local footprint and brand across Europe.

Has Infosys finally gone all “sensible” on us?

Mortgage processing is one of the most commodotized 3rd party banking offerings, where services are heavily outsourced to offshore locations, the technology platforms are mature and robust, with a lot of focus on eliminating manual processes over the last 5-10 years. In addition, all the major banks have been signed up. So is this the new Infosys? Making moves into dependable industries in areas it knows it excels, such as BPM services. Has the firm become (dare we say it) a bit boring after several years of perpetuating an Indian soap-opera of jet-setting CEOs, highly-public power struggles and grand-standing new strategies?

As with most services that are reaching maturity, incremental productivity improvements can be achieved with investments in automation, analytics and AI – and training staff to manage these enhancements. However, mortgage processing to-date has proven little more than a linear, lengthy, margin-thin business, where the winners will be those who can shuffle the market shares into their bailiwicks. So while it clearly makes sense for ABN Amro to divest of a commodity asset, what’s really in it for Infosys?

The Stater acquisition expands Infosys’ European market share and provides an opportunity to transform a commoditized process

Infosys has traditionally performed well in banking and financial services in the US, but has tended to lag behind the likes of Cognizant and TCS in recent years, hence this deal really helps level the global playing field among the leading India-heritage providers focus on the space. In addition, Infosys leveraged its long-standing existing footprints in ABN to beat Cognizant to a marquee European client. With CEO Salil Parekh personally involved – especially with his personal history in the banking sector – this is a particularly satisfying deal for the firm, and marks a much more ideal addition than the recent problem technology assets Pannaya and Skava, which have proven a real bane to the firm.

Stater provides services to an array of mortgage lenders in the Benelux region, with its greatest depth of customers and capability in the Netherlands. Stater also brings intellectual property into the mix with its digital Stater Mortgage Platform. This deal brings a notable European expansion of Infosys’ mortgage administration services capabilities. The existing bulk of its mortgage capabilities are decidedly North America-focused. Stater’s leadership role in The Netherlands, its solid client base, and its existing digital platform are all strong assets for INFY to build on.

Stater celebrated its 20th anniversary in 2017 and begun focusing on the development of its digital platform. So there is a digital baseline, but clearly the INFY play here is to drive substantial digital optimization using levers such as dynamic workflow, API layers, RPA and analytics to reinvent manual processes, improve the borrower experience and, overall, create digital operations. As INFY acquired the majority stake in the asset, it can quickly make these changes happen. ABN prefers to be the lender not the mortgage servicer, so it offloaded this non-core business to INFY.

Although note ABN’s bet hedge of retaining a 25% stake in case this all goes swimmingly – and also increases the desire to co-innovate with the new partnership. There is no doubt that INFY can drive some “standard” efficiencies in this business, such as some improvements to the offshore people management, platform development and further process improvements, but mortgage servicing is a commoditized, low margin business that has been incrementally optimized, but lacks true change and innovation. It is still fundamentally laborious and slow. Hence, if INFY truly wants to meet impressive KPIs with this deal it really needs to invest in improved automation, especially with its learnings and experiences from its US clients.

Large banks consider offshoring as hygiene and no longer seek control of non-core assets

The latest mega deals in the IT and business process services market are all about buying a big book of business and using an arsenal of digital tricks to run it leaner and more efficiently. Recent business services examples include HCL’s $1.3 billion shared “services deal” with Xerox and Wipro’s $1.5 billion deal with Alight for health, wealth, HR and finance solutions. While INFY’s ABN deal looks more like a traditional acquisition than an outsourcing mega-deal, it is still premised on the unifying theme that human-only labor arbitrage-based business models are now hygiene. The new gig is driving enhanced value through better process automation, analytics, better staff development and hybrid workforces.

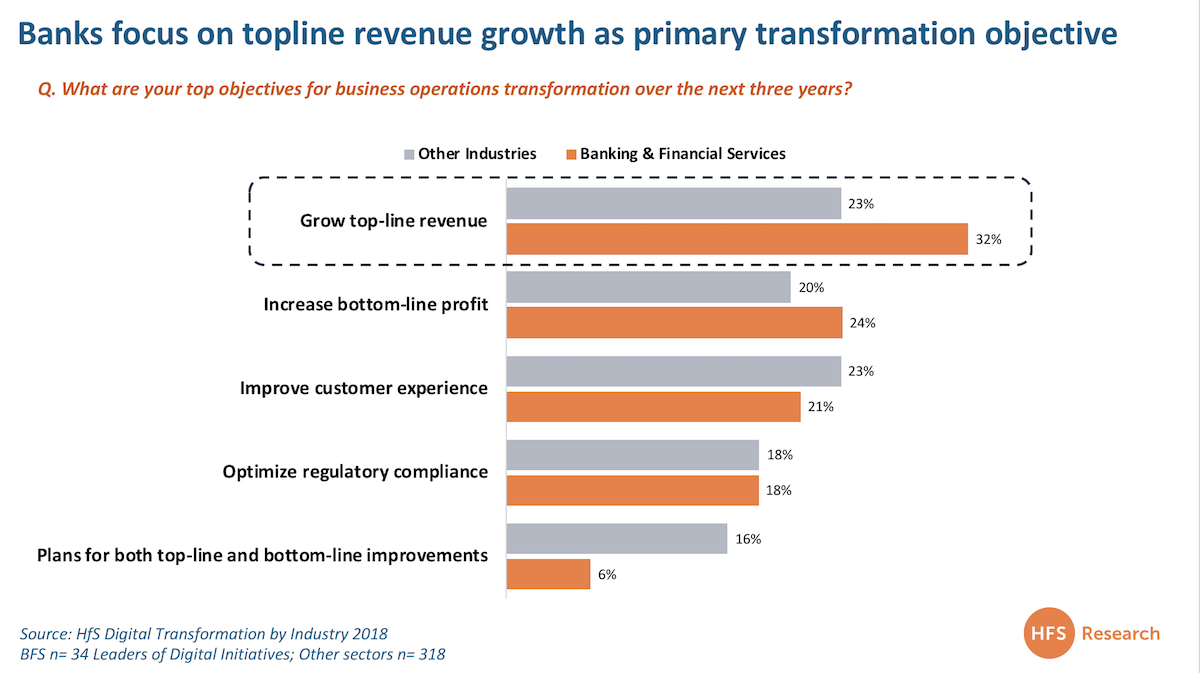

Driving growth is the leading transformation objective for large banks (see Exhibit 1). They are shedding non-core assets to enable pivot to digital growth. More than a decade after the global financial crisis, profit and revenue performance of global banks is anemic. Firms are divesting-non-core assets to better enable focus and generate funds to support investments in digital business transformation – often using divestments to streamline operating models so they can pivot more quickly toward growth opportunities. Recent examples include Thomson Reuters sale of a 55% interest in its Financial and Risk company to Blackstone for $17B, now rebranded the unit as Refinitiv, Barclay’s disposal of certain AP-based wealth management businesses, and UBS’ sales of its Dutch wealth management business.

Bottom line: Infosys gets scale and market share but needs to re-invent the tired mortgage servicing market to make the Stater acquisition truly notable.

If Infosys really wants to make this mortgage play differentiating, it will need to refocus seriously its efforts around borrower experiences across the lifecycle of originations, servicing, and collections. In a commoditized mortgage market, change has been slow to come in the form of “e-mortgage”. Infosys must use this opportunity to go beyond driving cost efficiencies across Stater’s operations and platform with its automation toolbox.

It must use its design capabilities to rethink engagement strategies for borrowers, and ultimately configuring the digital components that link these activities back to its platform and clients’ core systems. The more Infosys can simplify the complex and often harrowing mortgage process for borrowers, the better its chances for seeing ROI on this deal.

Ever since IBM sold off its Daksh business to Concentrix in 2013, “call center” has been something of a dirty word to traditional service providers and software aficionados alike.

Since then, traditional IT services have flatlined as the focus has shifted to digital solutions, where the customer is front and center to emerging interactive (“digital”) technologies. Having that ability to lead the customer front line and support those customer needs with real-time speed and intelligence is core to business operations…. and service partners which can deliver this has never been so crucial. So are call center providers back in vogue, or is this merely a blip as we transition to a world where we don’t need many human beings anymore?

The contact center operations (BPO) services industry is growing at 4% globally, despite razor-thin margins and intense competition. So, why do pundits declare the call center on the brink of implosion into a piece of software, while the stagnant IT services market escapes criticism for perpetuating a “people-centric” model? While contact center BPO growth is hardly setting the world on fire, it’s been steady over the last several years, even though the majority of contact centers worldwide are still in-house. The fact that there’s still a $65 billion market for outsourcing this work begs the question why these investments are simply going away. Contact center leaders like Teleperformance and Concentrix have recently made sizeable investments in bolstering service delivery (acquiring Intelenet and Convergys, respectively), reflecting the relative importance of this market segment. The recent development in which SYKES acquired Symphony demonstrates the optimism that automation can grow, not cannibalize, the contact center business. The latter, in particular, signals a promise that contact centers can use RPA expertise to scale and complement traditional contact center services business as they pivot to become more strategic providers.

Other large business services firms are gravitating into the customer engagement market, sensing an opportunity to disrupt deals with a hybrid intelligent automation/global talent approach. Most of the Indian-heritage IT services firms with strong BPO delivery arms are gravitating back to contact centers, as they see the potential for aligning intelligent automation and cognitive assistant solutions with their global base of talent for supporting their enterprise customers. Some examples of this are with the likes of Tech Mahindra in telecoms and Infosys with order management. Cognizant, Wipro, and HCL – for example – are also competing for call center work. BPO firms that have been more focused on non-customer centric areas are gravitating aggressively back into the market, such as WNS, EXL, Hexaware, and Genpact. Even IBM has recently flirted with a few opportunities, despite selling its call center business, and we even cam close to featuring Accenture in our new Top Ten, but the firm was very adamant that is did everything but the contact center piece.

Contact centers are ripe for a renaissance, and automation is a big piece of this transformation. The common retort that a contact center with automation is an oxymoron is false. Perhaps it’s our legacy view of contact centers and automation that is oxymoronic—and it’s time to let go of that legacy. When “digital” is ultimately about new ways of doing things, the contact center is in a more precarious and important position than ever. The contact center for companies that want to stay competitive in a hyper-connected economy must learn how to embrace intelligent engagement, using the key change agent of automation to become a strategic hub that empowers both customer service professionals and the customers they support.

Enterprises must navigate the changing of the guard for intelligent customer experience services

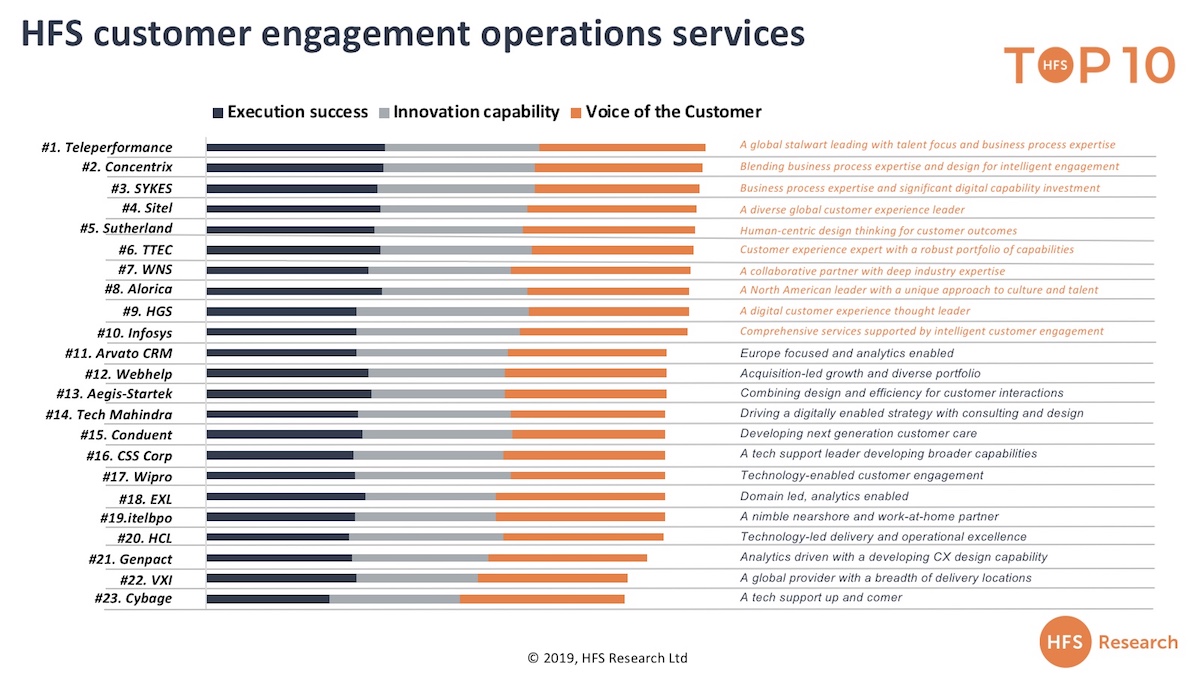

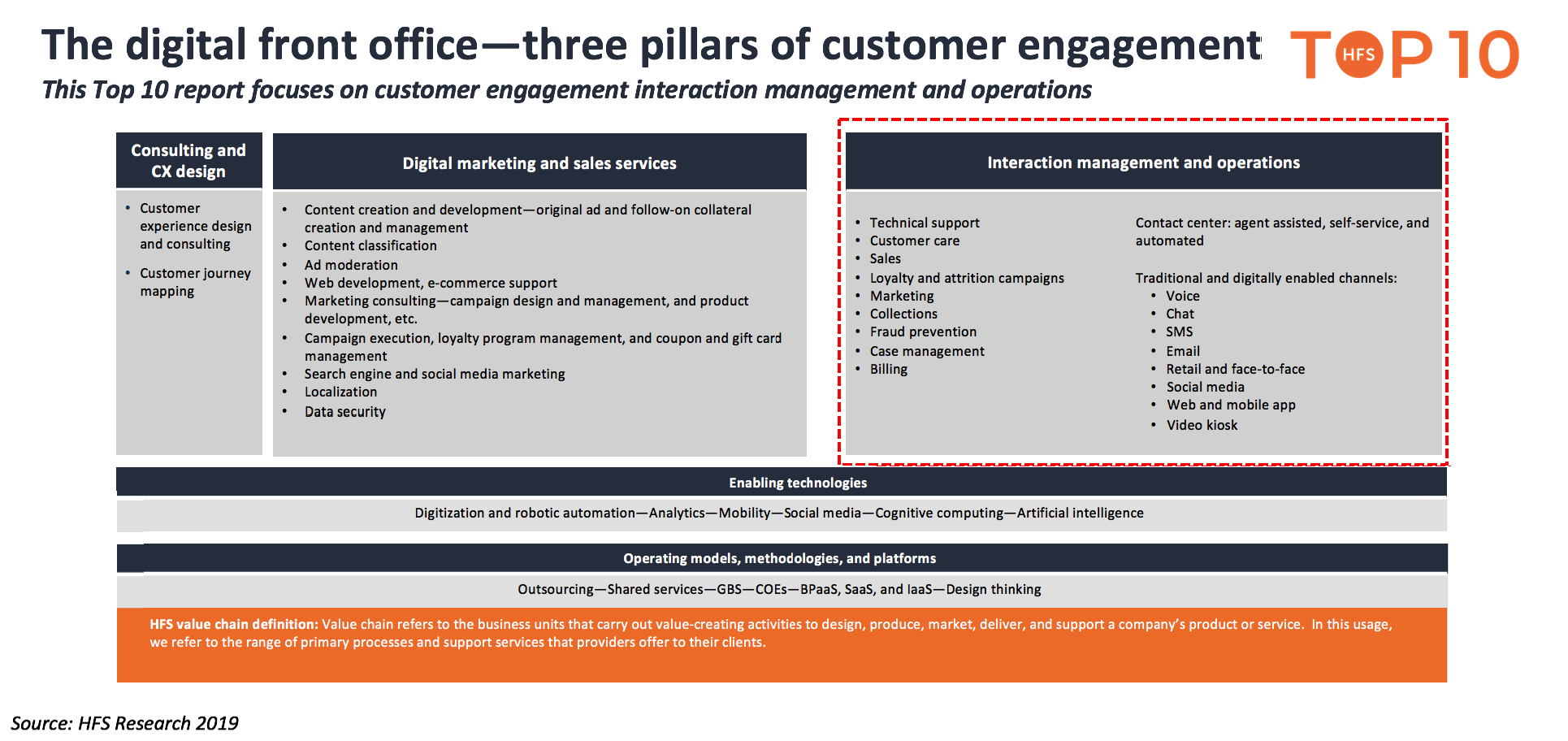

As the dust settles on our latest Top Ten, an assessment of the Customer Engagement Operations market, we’ve been fielding lots of questions about what this ranking means from a competitive standpoint. Our final top ten chart was chock full of what you might consider to be the usual contact center suspects, but also sprinkled with some interesting up-and-comers, as well as familiar names that aren’t necessarily known for competing in this space — the intelligent customer engagement services that are evolving out of the contact center. The promise of digital customer engagement and the vast amount of data in contact centers has brought back a resurgence of excitement for services that have evolved out of the legacy call center, and traditional labor focused legacy services are slowly but surely shifting to embrace automation, analytics, and digital interactions to provide a balanced, more intelligent customer experience.

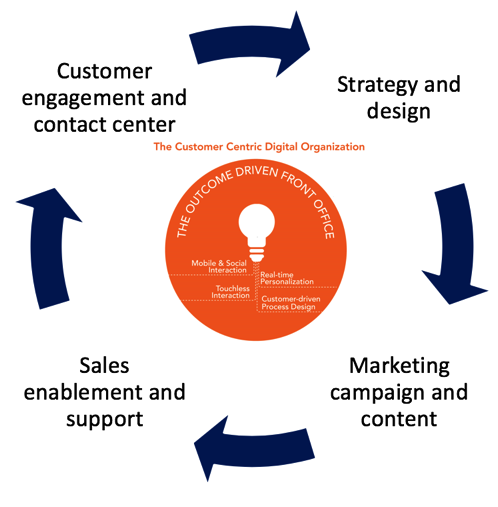

It’s clear that this isn’t your dad’s customer care BPO market. While suddenly every service provider we talk to wants to carve out a name in this space, there are different roles each will play and fit into within the ecosystem. This report focused on the interactions management and operations piece of the puzzle, but actually, the three pillars of the value chain are intrinsically linked, with front office convergence creating demand for operations to leverage strategy, and vice versa.

Pivoting to the digitally enabled front office means that customers are demanding more strategic input from partners at all points of the customer lifecycle. The recent investments we’ve seen from service providers for digital and design assets are complementary or integrated services to customer engagement operations. Thus, the services market is looking a lot less like a linear value chain and more like a cyclical system (ee below), where the contact center feeds strategy and design with customer data and analysis, where marketing, sales and support blur as one “experience,” and RPA, smart analytics and AI fuel the whole digital front office with greater efficiency, intelligence, and intuitiveness to customer needs. Our next HFS Top Ten reports will take a deeper look into the market for CX strategy and design, and marketing and sales services.

It’s a seismic shift particularly for organizations that are aligning to OneOffice and thus why we see such a different competitive set than we have in the past. Fundamentally different capabilities are coming into play in the realm of intelligent customer engagement, with bold moves like SYKES acquisition of Symphony Ventures shaking up the space with some real RPA capabilities. Firms like Infosys, Tech Mahindra, HCL, Wipro and CSS Corp are actually embedding automation into engagements, often in the form of cognitive assistants. We even see some action in this space from the likes of Accenture, which have come in with a CX consulting slant and then operationalize to support the design, or have an industry-specific capability that they’re supporting with customer interaction operations.

It’s worth noting that while the traditional contact center players tended to score well in the execution categories, there was a difference in the ranking for the innovation investment and capabilities, which was largely led by more IT focused firms. Thus, while now we still see the traditional service providers winning overall and in the voice of the customer in this market, in the future it may not be the usual suspects, but the providers that leverage niche and complementary capabilities, digital marketing, and CX design assets for their operations to be winning in the future. The demand from customers has fundamentally changed to shift away from low-cost, low-value services to seeking a partner that can help to deliver on a holistic digital customer engagement strategy, and many service providers are stepping up to the challenge.

The Bottom Line: In order to develop a truly customer-centric digital organization, you need the right partners in the right places of the digital front office

We expect the waters to muddy further as the impact of digital self-service, RPA and intelligent automation and AI accelerate. While on the one hand an existential threat, it is also the opportunity to breathe new life into a services market that for too long had been a race to the bottom for FTE based pricing. The convergence of services in the front office space means that enterprises need to choose their partners wisely. As an enterprise buyer, you will need to evaluate your partners and decide whether the partners you have today are the ones to help on your journey to deliver on intelligence customer experience. You will also need to open up to emerging business models and shed legacy contracts in order to really embrace an outcomes-focused front office that caters to its customers.

RPA has passed its peaky hype and we’re now staring into reality for the first time in 6 years. And it’s a messy picture…. the market has largely bought into three software tools and tens of thousands of people have invested a significant amount of their time training themselves on them.

However, beyond scripts and bots and dreams of digital workers scaling up rapidly to provide reams of value, most enterprises are fast coming to the realization that they need an actual process automation platform capability that ingests their data, visualizes it, machine learns it, contextualizes it and finally automates it. Essentially, the whole lifecycle of data components needs to be integrated into a single platform in order to take maximum advantage out of automating processes through scripts, bots and APIs.

AntWorks comes out of the closet to make its integrated automation play, taking the fight to the Big 3

Fresh off a series A round of funding with SBI Investment Co in July 2018, AntWorks has come out of the 2019 gate ready to up their profile and expand their enterprise footprint for their brand of intelligent automation. And why not choose the lovely island of the Maldives to press home its vision for its Process Automation Platform that integrates data ingestion, visualization, machine vision and RPA…

Having tracked the product for several years, and also researching the lions share of early adopters of automation products, AntWorks’ machine vision is an outstanding product, and Fractal math has significant advantages over Bayesian. Visiting with the core team just last week, having them show how it can extract text from images within images is something that can provide a huge edge in the market as users wise up to what they really need to integrate data. One of their use cases involves taking a picture of a coupon flyer to find out intel on what products are being promoted, special packaging, size, flavors, dates of promo etc.. They can tell you, for example, how many ounces are on a Pringles can in an image on an image on an image (label on a can in coupon on a page of coupons).

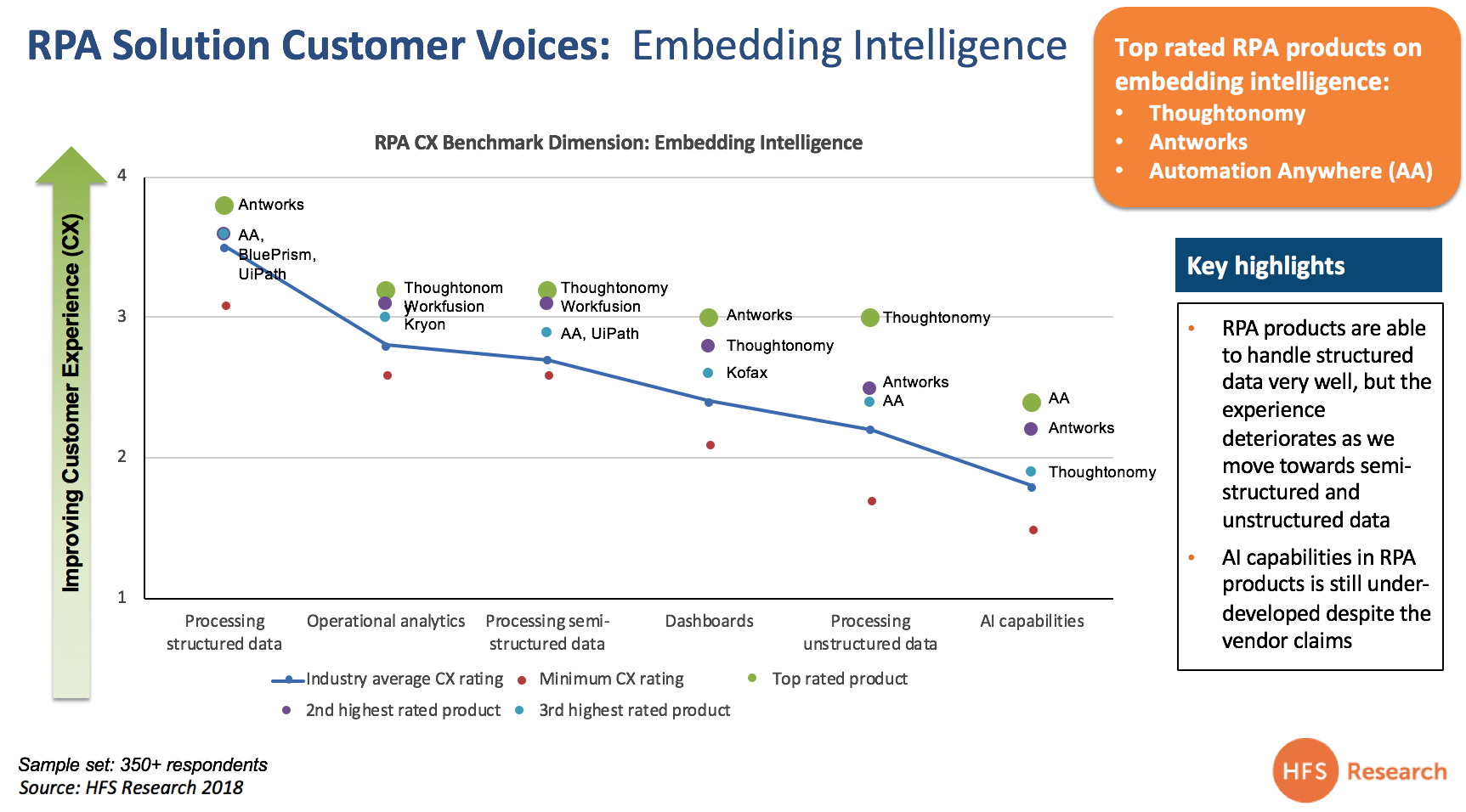

Yes, this really is slick stuff, and last year 350 users of automation products show how AntWorks is stacking up when it comes to embedded intelligence:

Five things enterprises evaluating intelligent integrated automation platforms should know about AntWorks

While HFS has been tracking AntWorks since early 2017, this was its first “official” analyst briefing. We took away a variety of facts as well as future direction and strategy points. Here are the five things we learned that we consider relevant to enterprises evaluating intelligent automation tech and partners:

1) Its platform offers up integrated intelligent automation – AntWork’s ANTstein platform consists of modular components including “cognitive machine reading (CMR)” sort of a computer vision meets machine learning-based smart OCR, RPA , and a smart analytics components. While these are available piecemeal, they are designed to work together. The primary client entry point today is with its CMR module. So rather than adding AI to RPA, AntWorks adds RPA to AI. HFS created our Triple-A Trifecta framework (eg: RPA, AI, and smart analytics) to make the point that you can start anywhere with intelligent automation, but our research shows most firms start with RPA and then can struggle with scale. Clients that start with CMR are tackling unstructured data which can then help unlock greater functionality with RPA downstream. ANTstein offers a path to integration which can enable end-to-end work flows and the potential for the coveted scaling of IA. AntWorks is launching its new version of ANTstein, Square, imminently.

2) Its machine learning engine leverages fractal data science rather than neural – While the sciences are different, why it matters to enterprises is that you can train some business process algorithms faster as there are finite sets of patterns and outcomes in many business processes. Fractal science tends to work best with a finite set of outcomes, rather than infinite, where neural would be more appropriate.

3) Innate process and verticalization depth – AntWorks’ leadership team came from the BPO industry (eg: Infosys BPO, WNS, Capita, Mphasis BPO), where deep understanding of business processes is essential. This deep process knowledge in the areas being automated by enterprises today is largely lacking from most AI and RPA software companies. AntWorks is applying this process focus to develop domain-specific use cases for horizontals like finance and accounting and HR and more notably industry-specific use cases like title search in mortgage or claims processing in insurance. The service provider community has really been bridging the gap between intelligent automation software and domain knowledge to create end-to-end workflows. AntWorks’ domain use cases bridge its full stack and demonstrate the potential of integrated IA.

4) RPA innovation – While AntWorks missed the first wave of RPA, it is working to offer RPA product improvements in areas clients are grappling with such as bot productivity to ensure its relevancy. Its forthcoming Square release of ANTstein is purported to enable dynamic reallocation of idle bots and multi-tenancy of multiple bots on one machine. One of their clients in attendance at the event indicated this would be a major resource saver.

5) Bot cloning – As many enterprises have already invested in one or more of the leading RPA software players, AntWorks needs a value proposition beyond follow the leader RPA. An interesting concept they are working on is “bot cloning” – essentially replicating existing bots and porting them over to their platform. Given its current focus on unlocking unstructured data for enterprises as their lead selling point, this may create a logical bridge to RPA as long as it works. As enterprises increasingly focus on outcomes rather than the enabling technology, this may create some conversion opportunities as enterprises look for ease of integration to enable end-to-end workflows.

Bottom line: AntWorks offers a path to integrated intelligent automation, provided enterprises embrace its full stack. One more large round of funding and it will be a real force

Go global with its platform play. AntWorks, fuelled by funding and early client success, is making a major push to take its product to market globally. While its full stack platform offers enterprises a tangible path to integrated intelligent automation, the reality is that today they are best known for their cognitive machine reading capabilities. AntWorks needs to continue to focus on its domain expertise which has the greatest potential to showcase end-to-end workflows that work across its stack – essentially showing intelligent automation in action (the Triple-A Trifecta). Currently, there are a lot of piecemeal IA tools in the market that requires custom integration to tie them together to enable straight-through processing of automated workflows. As enterprises grow weary of having to continually piece together the components that enable intelligent automation, the focus on tools will become more about what delivers the best results and can scale. AntWorks’ investment in people and expanded geographic footprint will help take the message to a broader range of prospects outside its core client case in Asia Pacific. Additionally, the firm needs work on its global channel strategy. A solid network of partners, particularly strong service partners who understand the tech and value proposition, can help AntWorks reach a broader range of prospects.

Secure more investment funds to fight for a limited supply of talent. What’s needed next is a significant second round of funding, not dissimilar to those being ingested by UiPath, Automation Anywhere and more recently Blue Prism. The sales team, under the experienced leadership of Bill Schrank, need added firepower, and AntWorks needs to prove its RPA story aggressively… how can they truly bring it all together and negate the need for enterprises to purchase expensive RPA licenses when ANTstein provides it all for them in a one-stop solution? And finding the talent is tough as the Big 3 currently soak up any semi-decent professional with a pulse capable of understanding and communicating the value of integrated automation.

Combat “RPA fatigue” to re-energize a weary and frustrated market. Too many enterprises have been oversold the same old story of no-code and the fact this is supposed to be “easy”. So Ash and his crew need to make the case that clients of AA, BP and Ui can jump ship without losing face. In addition, weary service providers and advisors need to be convinced to put similar resources into AntWorks that they already have into the others.