The future is so exciting, we need to focus on our disruptive talent to make it all happen… just like the Blue-footed Booby!

Posted in : Confusing Outsourcing Information

The future is so exciting, we need to focus on our disruptive talent to make it all happen… just like the Blue-footed Booby!

Posted in : Confusing Outsourcing Information

I just couldn’t resist the annual pilgrimage to Mumbai to experience the Indian IT elite’s gathering, in the case my concerns that the offshore-centric IT service delivery industry was getting complacent were misplaced. Sadly, they were not.

It has been two years since the NASSCOM leadership forum of sell-side IT execs was held in Mumbai (after a pretty disastrous diversion in Hyderabad last year), so it was pretty obvious that attendance was clearly down, compared to two years’ ago. Am sure numbers will be reported otherwise, but it was pretty easy to navigate the entire venue without having to resort to the traditional scrimmage position to hack through the usual sea of people.

My takeaways:

The atmosphere was “relaxed”. Seriously. The traditional urgency has somehow dissipated to this bizarre – almost chilled-out – mindset from most of the people there. “Aren’t you guys worried about Brexit or this Chinese/US trade war escalating. Surely that could really hurt Indian service delivery?”. Most people just shrugged. No-one seems to care that much anymore… everything is just fine, and, I hate to say it…. BORING.

Digital as a term is done. Yes, even in India. After the last few years of digital overdosing, the only time the word is now uttered is when an Indian provider exec explains that “half their revenues are now digital”.

“AI” is the new Digital. And absolutely no one can define it. Great. Hurry up Quantum…

Service providers fell into two camps: inspiring and downright awful. Yes, we literally hammered our way through 30 meetings and I can honestly report that about a third were truly inspired conversations… the other two-thirds were dull as dishwater. Some came to us with a precise vision and focus, others literally had nothing to say beyond “we’re doing OK”. There was nothing in between.

There is a depressing lack of service delivery disruption. All the execs wanted to pitch was their amazing new pricing models that incorporated some RPA and some type of “outcome” pricing. Few were pushing their ability to disrupt actual service delivery with a next-generation talent development strategy. Few were talking about how they were helping clients with innovative role development, with change management programs, with co-investment plans, with the re-platforming of IT for their clients. And no-one was talking about investments in cognitive assistants and blockchain… it was all about dumb RPA bots and new-fangled pricing models that helped them win deals. Who is advising these people? Don’t they – at least – talk to decent analysts anymore to tune up their messages?

Where were the CEOs? We got visits from Salil Parekh (Infosys), C.P. Gurnani (Tech Mahindra) and mid-cap CEOs Keshav Murugesh (WNS) and Nitin Rakesh (Mphasis). In addition, we were treated to Accenture’s CTO Paul Daugherty, which was welcome… and Capgemini’s Thierry Delaporte, co-COO (and potentially the next CEO) did manage to make the trip. However… Cognizant, HCL, Genpact and TCS all failed to serve up any C-Suite royalty.

Isn’t this supposed to be India’s premier IT event? And what about IBM and DXC, two of the largest IT employers in the country? I don’t think a single leadership soul from those giants made the effort. Not to mention Deloitte, EY, PwC… all huge beneficiaries of Indian IT talent. Where were they?

Where were the RPA dignitaries? Considering RPA was pretty much the most discussed topic this week, apart from AntWorks co-founder Govind Sandhu and a rumored sighting of Automation Anywhere’s Mihir Shukla, they all gave this conference a wide berth. Considering the Indian IT service provider channel probably represents the largest growth opportunity for the RPAs, this was a huge miss from them. And from NASSCOM for not inviting them along.

What happened to the analysts? Aside from single individuals from Gartner and Forrester, only a handful of lower tiers analysts were seen parked in the meeting lounge desperately trying to pitch their wares to Indian marketing folks (pretending to be excited by them). Even the HFS trends session was thrust into an obscure breakout room that ended up with wall-to-wall standing and disappointed people being turned away. When I mentioned to some NASSCOM folks that it “may have been wiser to stick us on the main stage”, the response was “We’re truly sorry, but we have to be careful not to upset the other analysts”. As if anyone would have cared… there were hardly any there in any case… and when did the feisty Indian IT monster of yesterday worry about upsetting a few people?

Thank god for Rishad! The one truly bright shining light was the effervescent Rishad Premji gracing the halls, bouncing around on stage, talking to everyone he could, even having beers with his buddies in the hotel bar. Someone with a vision, oodles of passion… saving the day for a tired old show that badly needs a facelift. I must apologize to my friends at Wipro, but can you just let this guy run for PM?

The Bottom-line: It’s time to change the Indian IT record… or this industry will be disrupted by… something else

I can recall all the way back to my first NASSCOM invitation in 2002… this was THE event of the year, back then. Anyone in IT services who meant anything just had to be there. This thing literally used to be Davos for global IT. Now it appears to be descending into a microcosm of an Indian IT industry bordered on complacency… content to make quarterly numbers and little else.

Having spent time, in recent months, at industry events in the US and emerging European locations, something is going wrong in India. Is Indian IT losing its luster? Has it settled for what is has… losing its ambition to keep disrupting the world of technology, like it did so magnificently between 1995 and 2015? Will we see IT services firms headquartered outside of India creating the next big shift, leveraging more talent from emerging locations such as Ukraine, Poland, Russia, South America and China… and lessening their reliance on India?

Posted in : IT Outsourcing / IT Services, Outsourcing Events

Posted in : policy-and-regulations

Bathgate. Alastair Bathgate… Unshaken and stirring the pot, but doing it his way

Anyone who’s known Blue Prism CEO and Co-Founder Alastair Bathgate over the years has seen a marked change in his executive presence, especially since the IPO two years ago. While he still insists on driving his Volvo SUV, while his buddies are prancing around in fancy Aston Martins and Bentleys, he is a more assured and confident individual than the chap I first met seven years ago, when we first alerted the world to RPA. Yes, he still has the same honest style and just tells you what he thinks, but there’s a certaswagger about him now – he sees the future of his firm and is hell-bent on taking it there. And yes, if only he could use his wine pricing app for RPA, all his problems would be solved =)

In short, it’s been a mildly frustrating couple of years for RPA’s early mover and market maker, Blue Prism… the firm was the first (and still only the first) pureplay RPA firm to go public, with every dollar spent being visible, all staff moves closely scrutinized, and a CEO who’s had to divide his time between board meetings and investor days instead of harassing the conference circuit as aggressively as his rivals.

Meanwhile, while some of his competitors have been in stealth mode, raising all sorts of private investment and offering licensing models that appear (on the surface) a lot cheaper, while selling the “This is easy, this is no/low code, we can train you in weeks and get you a nice certificate to share with your friends on LinkedIn”. This is what I personally detest about the software business… anyone can sell dreams, confuse executives too scared to ask critical questions like “how exactly does this work again?” especially when you have the lovely term “robotics” to excite greedy CFOs and CEOs eager to find new ways to increase margins.

‘Refusing to get carried away’ may have hurt Blue Prism in the short-term

Cutting to the chase, the Blue Prism team has stuck together for almost a couple of decades and has stayed true to its very British style of keeping the discussion realistic, refusing to get too carried away with the hype and the fantastical stories gripping many starry-eyed executives eager to slap RPA success on their CVs… not unlike the SAP and Oracle roll-outs of the 90s and Workday and Salesforce escapades of the last decade.

Now it’s all about stitching the wonderful skills of building scripts, macros, document processing and screen scrapes with the emerging excitement of Machine Learning, Natural Language Processing, Augmented Reality and Computer Vision. Yes, folks, you thought the hype-train of the past 30 years was bad, the one we’re venturing into is going to drive many of us completely nuts.

It’s been pretty hard for Alastair Bathgate not to get irritated by the challenge of his highly-visible firm taking pot-shots from other firms, playing on the excitement this market is generating, promising enterprise clients dreams that will likely turn into nightmares when they set their expectations to achieve outcomes their staff simply do not have the skills to achieve – with a hodge-podge of processes far too messed up to fix, simply by slapping new software components over the top.

However, Blue Prism’s low-hype, pragmatic approach could pay attractive dividends as the hype-phase dissipates and fresh investments are made in re-thinking the whole RPA/AI model

While his firm may not have been quite as successful as UiPath in forging lucrative partnerships with professional services firms and lacks some of the terrific messaging and vision of Automation Anywhere… while having to tackle a publicly-listed firm persona and widespread (unjustified) confusion over its pricing model, you have to credit Alastair, Dave Moss, Pat Geary and Martin Flood for sticking to their knitting and focusing on what they know best – keeping the conversational balanced and realistic and investing in the sales and technical talent they believe they need to keep developing their product.

It went unnoticed to many that Blue Prism recently landed a $130m investment round. What excites me about this investment is the firm will actually get the money over the next two years and we can see exactly where it is going… on its product-specific developers in Manchester and an exciting new group of research in London, where 25 crack AI thinkers will be working hard to take Blue Prism’s solution into the place it needs to go. The firm already has a diverse group of 250 salespeople… now it can focus on the development areas that hold the key to who will ultimately will this automation arms race.

Upping its RDA game and expanding its presence in Japan are immediate needs that it needs to deliver

In addition, the firm is working hard to fill the gaps in its current solutions… while it prides itself of the back office unattended automation, if has suffered at the hands of AA and UiPath when it comes to very RDA-centric (Robotic Desktop Automation) engagements (what we call “unattended watched RPA”).

Plans to release (in version 6.5) document processing capabilities to support end-to-end processing of document workflows which also acts as an OCR system to classify documents, extract key-value pairs and encode verification steps into the digitization process, could well propel the firms back to the front of the market as the reality of delivery exceed these dreams of great visions. In addition, Blue Prism plans to deliver full Japanese and simplified Chinese language capabilities with this new version release… essential add-ons as it plays catch-up to UiPath in this region.

The Bottom-Line: The real work starts now as RPA evolves to become a key component of the AI tool kit

The stark reality we’re currently facing is getting ahead of market confusion to forge genuine learning journeys for ourselves, our careers and our companies. At our AI-enabling Operations roundtable last week in New York, we all agreed that AI is Nascent, New, Hard … but it is, most certainly, Inevitable.

The most important clarity that most organizations have gained over the last several months is that AI is not some monolithic thing or a singular technology. Instead, we’ve come to understand AI as a toolkit, or “a bucket of stuff” that enterprises can use to make their operations more intelligent; building blocks that include various elements of foundational AI moving across a spectrum toward more packaged solutions.

The one common denominator among the executives was that they were all determinedly seeking to evolve their experiences from RPA to join the dots to the next steps of achieving enterprise-wide automation and AI capability… essentially integrating the tools and hatching a real plan to get it done. This is where the likes of Blue Prism, Automation Anywhere, UiPath, Pega, Kofax, and AntWorks need to head next; building on the RPA digitization to create real solutions that go far beyond scripts and bots… solutions that can help re-invent the underlying institutional processes that have held back firms for years.

Posted in : Cognitive Computing, intelligent-automation, Robotic Process Automation

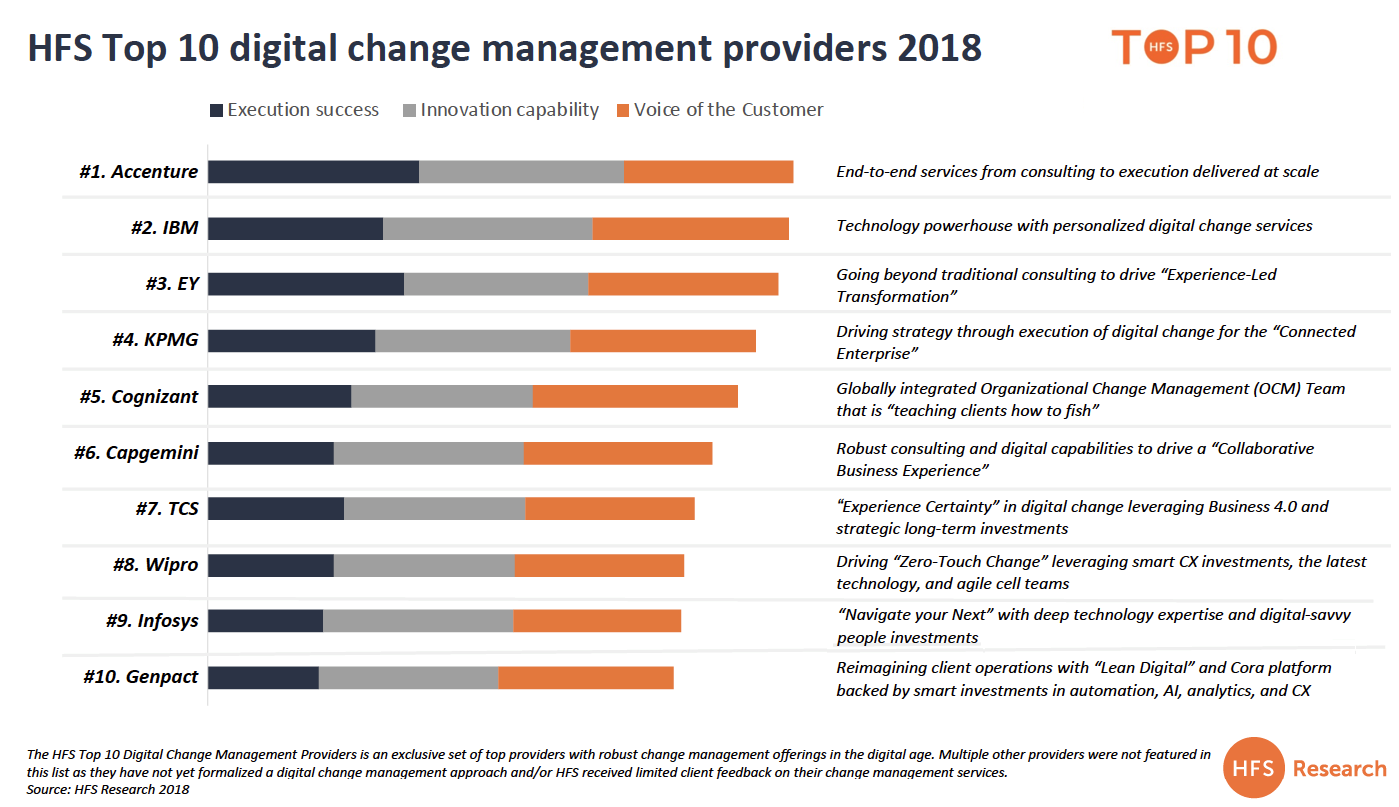

Let’s get to the point: most of the past five years have borne witness to our industry postulate on the why and what of digital (and many still do). It’s time to focus on the how.

Unlike the wild grandiose claims from most services and tech providers that everything they do, these days, is “Digital”… it is far, far more than simply investing in new technologies. Digital is about embracing interactive technologies, mobile, social and analytics to drive new revenue and customer experiences, as well as harmonizing business silos to support these digital outcomes.

However, success in digital initiatives is much less about technology adoption… and much more about people and culture, and the ability to manage that change. Code errors can always be fixed, workflows stitched together, apps integrated… but taking enterprise teams through the whole volatile experience, helping their staff learn new techniques, creating an environment where an enterprise can keep evolving on its own accord, and not rely on armies of consultants until perpetuity, is how we evaluate the performance of today’s ambitious service providers.

With this evaluation objective in mind, HFS shortlisted and assessed 10 leading providers: Accenture, Capgemini, Cognizant, EY, Genpact, IBM, Infosys, KPMG, TCS, and Wipro across the following five dimensions of digital-change prowess:

1. Embracing emerging change agents;

2. Creating true partnerships;

3. Promoting the principles of OneOffice;

4. Enabling change management for digital labor;

5. Driving real business outcomes.

Click the table to view more detail

For a limited time, we are making our new report: “The Top 10 Digital Change Management Service Providers” completely free to HFS subscribers. (Click to download)

Posted in : Digital Transformation, OneOffice, sourcing-change

There aren’t too many people who can boast to be one of the true pioneers of the emerging robotic process industry, or whatever we end up calling it, but one man who didn’t need to recreate his resume in 2017 is Francis Carden, one of the original brains behind recreating desktop automation to become Robotic Desktop Automation (RDA) which is such a key component of the broader RPA offerings attracting so much noise and attention today. And he now leads the whole robotics strategy for customer engagement and data orchestration giant Pega.

Francis – a British Floridian these days – is never one to hold back, and when one cynic mercilessly described some of today’s RPA rollouts as “lipstick on a pig” at our recent New York FORA event, he just had to take it one stage further to declare them as “lipstick on a pig’s arse”. So without further ado, let’s hear from the granddaddy of RDA himself…

Phil Fersht (CEO, HFS Research): Francis – firstly, tell us about the OpenSpan business you co-founded and how this evolved to the acquisition by Pega?

Francis Carden (VP, Digital Automation and Robotics at Pegasystems): In 2004, a group of “tech head” advanced windows operating system engineers approached me about forming a company using an automation technology vastly different from anything proceeding it. It let companies rapidly automate, through the Graphical User Interfaces (GUI) of windows applications, any task or process that a normally would be done by a human on their desktop.

On first hearing of it, I had to laugh and said to myself, “It sounds like screen scraping.” I didn’t believe what they were proposing was even possible. But I did a deeper investigation into the background of these engineers and the technology and found it both unique and incredible. So I bought in – and even invested a significant amount myself. Today, we label our RPA technology “Deep Robotics” given it is so different.

In 2005 we started OpenSpan and over the next three years, as CEO, we convinced a consortium of Atlanta technology angels and then attracted four Tier 1 VC firms that what we had was something different. The customer base grew rapidly. Our patented technology started life as being called “Surface Integration” because it was so different from screen scrapers of the past (and current RPA). But we quickly settled on “Desktop Automation” (known today as RDA), and “Automation Broker” (known singularly today as RPA). We ended up implementing most of the world’s largest RPA projects over the next 10 years.

Then Pega acquired OpenSpan in 2016. Pega recognized our RPA approach was markedly different from any other RPA vendor. After we got talking, I realized our unique technology would be even stronger if it were part of something “bigger.”

What I mean by that is organizations on the digital transformation journey shouldn’t aspire to RPA as the end game. You really need to look at RPA as a short-term plug to fill the gaps on the road to get there. When you deploy RPA, you’re just masking the poor processes behind it. And when application UI changes, the bots are prone to break. It might be weird to hear me – an RPA vendor – say that. But it’s the truth.

And that’s where Pega’s digital process automation (DPA) software comes into play. Pega enables you to digitally architect those processes the right way, from the ground up. No more organizational silos, no more inefficiencies, no more needlessly manual processes … and really, no need for RPA to always be the first option. RPA gives you a digital automation jump start, and when it’s time to deploy DPA, those bots can be put out to pasture.

And the good news, at least for us, is that everyone is on a digital transformation (One office as HFS call it Phil) journey, and it really never ends. RPA and DPA are the perfect one-two punch. So the tie up and combined value prop with Pega was, and has been, an ideal match.

You’ve been the undeclared granddaddy of RDA, so what is the key “difference” between RDA and RPA… unattended and attended… etc?

Imagine if every compiled windows application ever built allowed itself to be automated from within its own code, robustly and in real-time. You wouldn’t need any RPA, right? However, very few apps running on windows are easily automatable at the UI layer – at least, without resorting to screen scraping techniques like MSAA, UI automation and OCR.

In 2005, we patented a more sophisticated approach to UI automations – a “plug-in” like architecture that enabled any compiled windows application and all its objects to be non-invasively automatable in a single architecture. This “deep robotics” automation occurs inside the windows layer, inside the memory of the machine, and runs as if the original developer of that application had natively built it. This plug-in like approach automates at the application’s original speed (10x to 100x faster than scraping), highly robustly, and far less susceptible to application UI changes. More importantly, and hence the dual name “attended RPA,” it even allows the desktop worker to use their machine, keyboard, and mouse while the automations are running. This is something unheard for old school scrapers and other RPA products. It is this pure form of RPA that also enables it to be used as RDA, giving every worker their own personal robot or “co-bot” to automate from one percent to 90 percent of their work. Agile RPA. And only then, after you’ve rolled out RDA, should you look at those same processes ready for full automation with RPA (unattended as opposed to attended) operations.

Before the Pega acquisition and continuing since, we have 100s of 1000s of bots deployed across some of the world’s largest enterprises in all industries. By the way Phil, being a Grand-daddy makes me feel old, but I did calculate that I’ve been doing automation of the UI for 20 million minutes of my life!

So what happens next as RPA (assume RPA includes RDA here) moves from “tinkering” to broader enterprise adoption – where do you see clients finding the most value, and how can they scale their people and tech platforms to accommodate?

Good question, Phil, and the key word to the question is “tinkering’ – which is how most RPA vendors excuse themselves, after 10 years of trying, for not getting many customers to really scale or still stuck in pilot stages.

It is hard to believe, looking at the crazy RPA vendor valuations today, but yes, most RPA projects are tiny compared to scope of the company’s using them. RPA is not new, so the real question enterprises need to ask is, “What’s stopping this large-scale adoption across the globe, and why do RPA vendors keep insisting it’s because it’s new”

Attended RPA (RDA) scales — that’s a fact. It automates all the easy stuff in an agile way. But RPA unattended constantly struggles with trying to automate everything, both the easy and the hard stuff. Putting RPA band-aids on top of old and tired processes is just wrong for the long term. As Gartner says, “RPA is a tax on legacy,” but businesses are often so enamored by the hype.

But the thing is, RPA will indeed scale if it’s part of something bigger. RPA is tactical to the extreme. Digital transformation is strategic. What happens though if you combine the two? This is where software robotics shines. Using RPA and RDA to plug gaps that currently prevent digital transformation allows business and IT to align to solve the real problems. This gets you real and rapid ROI from RPA out of the gate, but equally, it encourages planning to then “fire” the robots as fast as you deploy them. Not something you’ll hear other RPA vendors promote Phil. With robotic automation capabilities embedded and fully integrated into the heart of Pega’s DPA, we are seeing enterprises really changing the way they compete in a race to become them most digital company in their market(s). Analog companies, using tactical RPA only as the glue, or those not buying into your one-office analogy, will simply not survive.

Francis, we’re seeing some tentative moves from “big iron” ERP vendors such as SAP into the process automation space, but do they really want to delve into this world, or are they merely ticking the “we have an RPA module” box?

Like I said, if all new applications were built to be truly digital and open, then there is no need for RPA at all. But we’re living in the real world here. While we wait for that to happen, the real “transformation” vendors selling the digital dream need to be able to use tactical technologies like RPA to help their customers plug the (hopefully) short term gaps. This gives customers quick relief where they are strangled by their legacy systems with no other integration capability. If a vendor doesn’t have this kind of automation, this sets the customers up for failure – they need to automate now to compete, not six or 12 months from now when your big overhaul project is finally done.

There are now 30+ RPA vendors, but I think the bubble will burst on these companies riding the hype wave. Most of them use many of the same old scraping technologies, and none of them have a unified DPA play to help companies for the long term. I’m not sure how long these RPA companies will be able stand on their own. Consider that Pega now includes bots as a standard capability of our DPA platform. We’ll give you all the bundled bots you need as part of your DPA strategy. So yes, we’ll likely see more consolidation in this market.

And how do you see the “blending” if classical RPA with some of these newer AI products on the market? It feels to me that RPA has really evolved from the process/operations side of the business, while AI is some magical vision being pushed hard by IT, but lacks in real business applications? What is real versus fantasy in your view?

This is the biggest myth of RPA. The idea that AI will help accelerate getting RPA to scale. It’s a red-herring perpetuated only by those in the RPA industry. No bias there then!! I concur with you Phil that AI is central to becoming a truly digital company. However, the idea of using AI with RPAdoesn’t fly – at least not right now. AI must live central to anything an enterprise does, everywhere. AI needs data, and LOTS of it. But very little of that will come because of RPA.

In order for AI to be really valuable, it needs data from as many systems as possible as well as data feeds from interactions with as many customers as possible, in real-time or extremely fast. Only then can you use AI start to predict what customers are going to do and/or create models that make the best decision for each individual customer. RPA would likely touch less than 1 percent of 1 percent of that data, so if anything, the RPA world is embarrassing themselves by trying to join these two tactical vs. highly strategic dots.

Don’t get me wrong, AI can create work for RPA bots, and maybe some RPA feeds some data into AI, but that doesn’t make RPA Intelligent. At the heart of AI is a digital company with data feeds from every source feeding into it. The DPA (one-office) movement is joining real transformation technologies together, acting as one, with AI at the center. The vendors that have DPA are the ones delivering IT and business on the promises of the past – a real digital company – and envy of their peers!

Thanks for the insights, Francis… we’ll be watching Pega closely in this space this year as the market finds its sea-legs… and some more attractive lipstick!

Posted in : OneOffice, Robotic Process Automation

There’s nothing more jarring than an ex-Gartner analyst desperate to continue dining off a legacy analyst industry that is actually trying to change. And lo and behold, Just before the Christmas break, a blog emerged on LinkedIn with an enviably click-baity title ‘Is Gartner research quality under threat?’.

Simon Levin, a Gartner Alum and owner of a boutique business “The Skills Connection” that helps tech vendors lobby their way through the Gartner and Forrester MQ and Wave processes, plies his trade on the fact he “knows” how to work his friends at Gartner, to help his vendor clients get their dots edged in a more positive direction for the firm. And why not? If I was a CMO, and lobbing Simon some moolah can help get some sort of leg-up in the process, I’d probably give him a shot. And however you performed, there is no doubt Simon will claim it would have been worse without him. It’s like that hair product “Rogain” that claims to slow down hair-loss… you’d never really know if it actually helped unless you went completely bald…

Simon makes the case that now most his former Gartner buddies he worked with in the 90’s are being quietly “retired” and replaced with a new breed of youthful analysts, and their research maybe less predictable:

“Quality control is hard to enforce. When a client of ours became involved in escalating a dispute over an MQ assessment recently, we saw some signs that Gartner’s controls may occasionally creak at the seams.

Our vendor noted factual errors in both the wording and the scoring of the draft assessment. We protested and took the client through the escalation process, and the company’s dot was rightly promoted from midway down Niche to the top quartile of Visionary, while the words were rewritten and became significantly more positive.”

So Simon literally cannot lose here: “In the old days I could leverage my influence with my former colleagues, now they’re going, I can help even more with the new kids they’re throwing into the mix who might make a few errors”

Predictably, the conclusion from Simon Levin was “as long as you hire my firm early enough in the MQ process to make sure their analysts don’t misrepresent you, you’ll have nothing to worry about”.

Why the content of Simon Levin’s blog should also be of real concern to the industry

In many ways, the stance taken in this blog is representative of how tech marketeers AR professionals view analysts – after all Simon’s revenues come from advising vendors on how to put pressure on analysts in the right places. But let’s break down in stages what’s wrong with this argument:

Misguided principle 1: Wining and dining analysts mean they’re in your pocket and should stay there!

The piece starts off innocently enough by confirming what we already knew and discussed in our blog covering nodding dogs – vendor marketeers and their analyst relations professionals should expect analysts to do their bidding all the time they’re being wined and dined. We know this because Levin discusses at length how irritating it is for vendors when they have invested so much time “cultivating” an analyst, to find out that said analyst isn’t handling that big competitive analysis this year. The misguided presumption here, of course, is that wining and dining analysts is just as important for getting a decent score as, say, providing relevant and timely information.

While this isn’t true for many analysts – we can infer, given the provenance of Levin and his compatriots, that Gartner analysts are perhaps more willing to boost scores if they have a good relationship with the vendor. Isn’t this knocking the value of objective assessment somewhat? I’m sorry Simon, but most analysts do this job because they actually value their ability to be objective. While one analyst firm obsesses with incentivizing its analysts with P&L responsibilities, most separate their analysts from the direct revenue impact of license reprints. Having a good relationship never hurt anyone with any business engagement, but a decent ethical analyst is never dissuaded by a decent steak (or vegan) dinner. Which moves us neatly on to our next puddle of misguidedness…

Misguided principle 2: Fresh perspectives are bad – the game is about controlling stale opinions, not embracing new insight

This is a big one, and it slithers through Simon’s blog as a core theme – the only stakeholder worth thinking about is the vendor. What’s misguided here, though, is the prospect that a fresh analyst jumping on a piece of research is always a bad thing. Sure, vendor marketeers and their analyst relations professionals may be rightly upset the steak dinner they bought has gone to waste as a new analyst’s in town, but for the enterprise executive who relies on balanced research to make decisions, a fresh perspective is almost always welcome.

The same staid analysis from a crusty ol’ analyst recycling the same themes may well be predictable and easy to influence. We all know the types who have those decade-long loyalties to the likes of SAP, Workday. Oracle, IBM et al. It’s very hard to convince a 30 year long analyst that the world is changing and and the vendor that have been lauding for their entire career may be losing its edge. Changing things up a bit is important to keep the research fresh, and analysts on their toes.

However, change is nearly always inconvenient for vendor marketeers and their analyst relations professionals – the clientele that keep Simon Levin’s coffers swelling. What’s soul-destroying here is that the quality of the research (despite being the core focus of the misleading title) is pushed to the fringes of the discussion. Simon’s blog isn’t about getting the best research and coverage into the market. It’s commiseration on the annoyance that is losing a tame analyst for a new one that may not be as willing to down the Kool Aid.

Nevertheless, quality is mentioned – but it masquerades in the narrative as a single metric – the average tenure of an analyst. Because, of course, the longer an analyst is in a firm, and covering an area, the better they get. I mean that’s just math’s…sort of. But unfortunately, even that old-world idea is being consigned to the history books. And – just like the rise of avocado ownership, and the crippling private rental market, we may as well blame the millennials for our next part.

Misguided principle 3: Experience trumps relevance

This is the bit that really goads us. Why are we perpetually locked in this bizarre world in which we believe the best perspectives come from those that have been doing it the longest? Why do we shrug off the new and refreshing insights because their origin hasn’t been dipped in decades of painful CIO workshops? We endlessly hear the need to develop new skills, to re-imagine our processes and redesign our business models, so why do the analysts get a free pass when it comes to keep up with the times? Why shouldn’t analyst firms practice what they preach?

The main assumption in Levin’s blog is that age begets wisdom. That there may be a quality issue at Gartner because the average tenure of analysts has dipped. But could it be possible, just possible, that the average tenure dropping is a good thing? Already we’re seeing hordes of younger executives and professionals flood into enterprises, no longer restrained by mandatory experience quota’s or ridiculous policies from HR insisting that employees stay put in a junior role until they’ve paid their dues. This coupled with the army of young entrepreneurs driving growth in tech start-ups and disruptors, is starkly altering the demographics of the average analyst firm’s client. So, is it reasonable to infer that the demographics of the analyst catering to this market also evolve?

Comments and blogs that imply quality research is inextricably linked to the quality and value of research are not only wildly out of touch with the changing market. But they’re just obscenely ill-informed. In a room full of 20-year-old tech innovators, does the experience of an analyst with decades of early 90s CIO experience more valuable than a young analyst who can live and breathe the unique challenges of the market?

Bottom Line: It’s not about tenure, it’s not about gaming the system, it’s not about wining and dining analysts. If this analyst is to survive to see 2020, it needs to focus on the quality, relevant research that a diverse market needs

The reality is that diversity is always beneficial and throwing in the perspectives of both analysts will undoubtedly be of benefit. But what doesn’t help is commentators like Levin churning out the same vapid and misguided tripe, in a bid to form a reactionary guard against the changing tides of the market. If anything, they’re proving themselves to be irrelevant and damaging to an industry that, much to our lament, is crashing around us.

Posted in : Uncategorized

It’s not everyday you can find a prolific industry expert, living and breathing AI and IT services, who wants to return to the analyst industry to make her mark. So when a former Gartner legend – and one of the brains behind the market development of Wipro Holmes – was eyeing a return to the analyst fold, we didn’t need too much encouragement when Tapati Bandopadhyay came calling…

Phil Fersht (CEO, HFS Research): Welcome Tapati! Can you share a little about your background and why you have chosen research and strategy as your career path?

Tapati Bandopadhyay (VP Research, HFS Research): First of all, thanks for giving me this opportunity Phil, to get back to my favorite world of analysts and research, in a firm that can make any enthusiastic 40+ feel like a 20 something again!

I have been a nerd all my life, and very proudly so. I wrote my first year PhD exams when my girls were 2 and 1-year old and I used to study for the exams from 12 to 4 at night and loved every moment of it. Even now, I cannot get sleep if I don’t read at least 20 pages of something completely new, something to anticipate and to be excited about when I wake up the next morning!

In last ten years I have probably taken the Strength-Finder 2.0 test at least three times, and each time my top two strengths remained exactly the same: Futuristic and Analytical. I think I am destined to be a research analyst and strategist! The upside of it has two key aspects: 1- analysts are future-makers, if we don’t push the real to the imaginary and back, the art of the possible is not likely to transform into the science of the real anytime soon; and 2- in addition to being future-proof and creatively bot-proof, analysts’ jobs are also recession-proof, as we can apply our analytical skills to find cheaper ways to do things with same or even better quality.

What are the areas and topics that you’re focusing on in your analyst role with us?

AI is my area of strength and there’s so much going on currently that I think we in the research and analyst world have a great responsibility right now, to clear up the clutter and let people focus on what’s real vs. what’s plain hype. Never losing sight of the Big Picture is becoming increasingly difficult in this technology-blurred world of “AI-defined everything”. While I love all the math models and algorithms and routinely devour new research papers in areas like deep belief nets, XAI, NLG, or imagination augmented AI, ultimately we have to keep it simple and human-centric. Only then all this technology hullabaloo will start making real business sense.

AI and IoT are highly connected, especially with 5G becoming mainstream in 2020 and even 6G at the works to come in by 2025-2028. Therefore I will be quite actively tracking the IoT space, chasing Nicola Tesla’s 1926 dream of creating a world-wide human-machine combined brain, which will become real when we achieve the next level of HFS OneOffice- the hyperconnected intelligent enterprise.

Talking about Things, I will cover the manufacturing and industry 4.0 research agenda too. I have always loved machines- be it those mammoth hydraulic presses at the Tata Motors truck factory, or the precision drilling machines at GEC Marine Glasgow. Manufacturing is truly the parent industry where tangible economic value gets generated with the land-labour-capital inputs. Only, the labour is now the ‘phygital’ workforce- with smart machines augmenting our quality of work and productivity, while freeing us up from loads of hazardous or boring tasks. That’s where AI, IoT and industry 4.0 connect beautifully in my mind-map, creating a simulated digital twin of the physical machine-world.

What trends and developments are capturing your attention today in technology and business operations?

I take what Andrew Ng said about data being the new oil, to data becoming the new glue, the invisible ‘ether’, the collective grey matter of the world. In sync with what you envision about the next OneOffice becoming ubiquitous in a hyperconnected world, the data oligopolies that we all know to exist today will come crashing down. We have already seen this happening just as the entry barriers to AI algorithms went down with the cloud-based pay-as-you-go models, and the entry barriers to top talent got broken in an open world of millennials comfortable in crowdsourcing. Now, with machine learning itself becoming partially autonomous, with unsupervised learning in a limited way and then with AutoML, human learning will also have to undergo transformation, where enterprises will learn from each other’s data, intelligence, experiments, experience, and thrive in a fairly co-opetitive world of frenemies where ultimately mankind and the unsuspecting individual, wins.

Is the analyst industry much different now than when you were at Gartner a few years ago? What is changing in your opinion, Tapati?

I think the analysts in this agile, new-age, ‘open research’ side of the world, are far more than mere subject matter experts. We are bolder, actionable and direct, hands-on folks, been-there-done-that type, and I love it. We are also listening better, to build our perspectives from a 360 standpoint. Not just technology, not just business, but the ability to cover all aspects, keeping the end-customers at the centre. Because, whatever be the industry or technology, if the end-customer is not impacted, nothing else matters.

So I see three key changes: 1- the idea of open research and collective intelligence, given that even IBM and Microsoft have now become proponents of open models; 2- the cognitive agility- to think fast and slow as the situation demands, and 3- to be direct, actionable and relevant with a holistic perspective – keeping the end-customers at the centre of any value universe.

So, Tapati, what are you working on first for our clients?

I am planning to cover the practical aspects of applied enterprise AI, as I have experienced this freshly and first-hand and have learned a lot. I have some very strong views and counter-views, on how these AI algorithms and their applications will pan out in the immediate and intermediate future, and the subsequent to-do’s. We will have to stay ahead of the curve. Hence I plan to share these as predictions and actions kind of PoV’s. I will also be covering the IoT and industry 4.0 with our India team along with the global team.

And given I have the locational advantage of being based out of India- the services factory of the world, and especially in Bangalore- world’s no. 2 silicon valley, I will work with a lot of tech start-up’s and service providers on their AI and automation initiatives, and IoT and manufacturing vertical practices.

And, what do you do with your spare time (if you have any…)?

Oh, I have to try very hard to play the cognitive catch-up game with my three children – my teenage girls and our 3-year old German Shepherd – named after our most fav physicist Dr. Feynman, we most humbly accept the fact that he is the smartest in the family.

I love to read physics books and fictions by the likes of Archer and Grisham, but I get constantly rebuked by my girls on not reading enough. Therefore I always try the easier way of asking them questions and then listening to every word of wisdom that they have internalized, post reading the tough non-fictions.

I also love to paint and play Indian music on the piano. And I love to cook for our friends and family. So next time any of you are in Bangalore, you have to come prepared. It’s a statutory warning- there’s no getting away from my unique cuisine while you’re here!

Welcome to HfS, Tapati. Delighted you have chosen us as your analytical home and can’t wait to see those first pieces of insight to hit the press =)

Tapati Bandopadhyay (pictured above) joins HFS research to lead our India research operations and expand coverage of AI and IT services. You can read her bio here.

Posted in : Uncategorized

In 2008 Lehman Brothers nearly took down the global banking system… in 2017 Greece’s debts were poised to destroy the European economy… today, we are staring at a stock market that gyrates up and down double-digit percentages in a single day, based on one awkward tariff tweet-up between Xi and Donald…

We’re talking about the world’s 5th largest economy going into immediate meltdown. This is more than a UK-only debacle

So… who cares about the world’s 5th largest economy potentially plummeting into a complete meltdown? Let’s just have a good giggle at those idiotic British politicians hell-bent on destroying the country over a referendum staged 2.5 years ago on a topic no-one actually understands. Yeah, let’s not worry as they’ll be screwed, and we can all make Brit-jokes at parties as those idiots run out of medical supplies and are forced to import frozen butterball turkeys pumped full of Ractopramine and several other GMOs… yum.

Here’s the bad news – Lehman and Greece are small-time when you consider the potential damage a complete Brexit failure will cause, if – as it possible – the UK government paralyzes itself and lets its economy degenerate into a warzone of regulation chaos, complete data disaster, supply chain meltdown and political purgatory. While we have boldly – and positively – predicted (see earlier post) that Brexit won’t actually happen, there is also the distinct possibility that Brexit and no-Brexit blindly meander into the nothingness of a “No-Deal” scenario.

We have predicted that – at the end of the day – politicians are surely not that selfish, and voters really aren’t that stupid to allow their country to descend into complete economic and social chaos… and madness. But that’s because we, at HFS, have assumed a modicum of intelligence does exist in the world. But, we could be sadly naïve. However, there is some hope – and that hope is the simple fact that if we Brits commit the ultimate harakiri of a No-Deal Brexit, we take the rest of the global economy down with us. You thought Lehman Bros was bad? You’ve seen nothing yet folks.

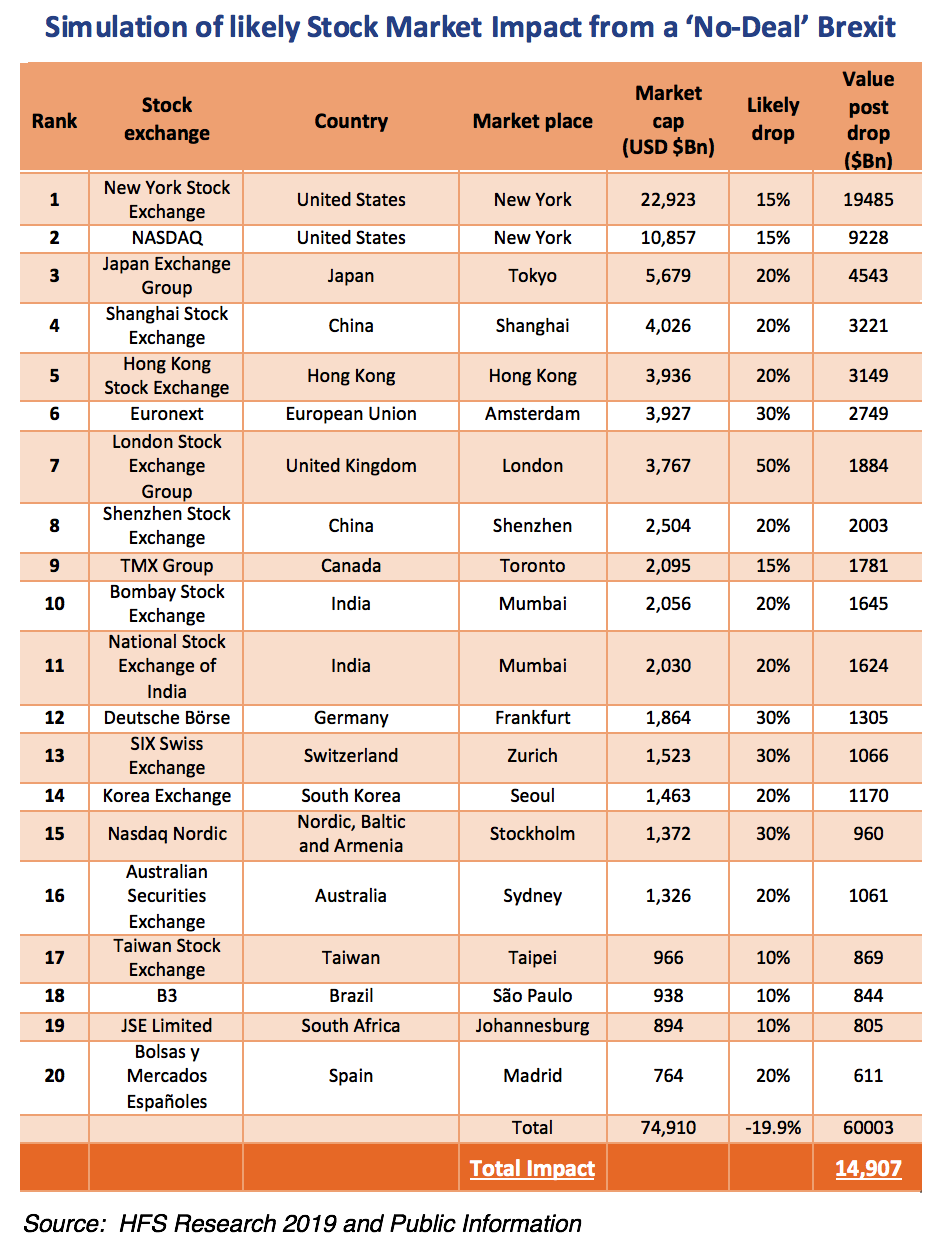

Why this could be a $15 trillion global decimation

If we look at similar shocks to the stock market over the last century, it takes relatively little to create a major downturn in global asset values. We don’t need to look too far back this decade to see how even a moderate dip on global stock markets cans seriously impact the health of the economy.

If we look at the Asian financial crisis in 1997, for example, we can see just how quickly the collapse of even a relatively small economy can wipe off a huge percentage of global stock values. If we look at the potential consequences of not only one of the world’s largest economies, but one tightly integrated with the global economy, it’s not hard to see how much of an impact this could have on the major stock exchanges. That’s not to mention the major role the UK currently plays in global finance – with some estimates advising that the City of London manages over $9 trillion in assets, three times the size of UK GDP.

In a no-deal scenario, almost overnight the UK will no longer be compliant with EU rules and regulations – of which the previously discussed GDPR is just one of. There are countless other regulations that have formed part of the business environment of the United Kingdom, Europe, and by extension, the rest of the global economy, that are likely to emerge during the real-time stress testing that a no-deal crash out will lead to.

We can simulate (with the same degree of absolutely no certainty characteristic of the Brexit process) a major tumble in global stock prices by examining how previous shocks to the market have impacted in the past. And it’s worth noting, that our estimates are generally very conservative compared to other financial crises over the past century.

In the following illustration, we can see how some significant impacts to the value of stock markets can play out – particularly in areas most likely to be impacted by Brexit. In this simulation, we can expect the value of the twenty largest stock markets to drop by $14.9 trillion as a result of the major market shock of no-deal Brexit.

Bottom Line: A no-deal Brexit has far-reaching consequences, and could knock chunks of value from global stock markets to send us crashing into a serious economic depression

The warnings about the implications of no longer being compliant with GDPR are chicken-feed compared to the true global impact of allowing Britain to hive itself off from the EU with no insulation from the multiple disastrous consequences. In the past, major financial crises have been caused simply from a much smaller and less integrated economy defaulting on debts, now we’re facing the very real prospect that one of the world’s largest economies will wake up one morning with a completely different rule book, and much more red-tape and bureaucracy between it and the rest of the world. It’s not hyperbolic to say, the consequences to the global economy could be huge.

In a sick way, maybe this No-Deal scenario is what we all deserve to open the eyes of the politicians and gullible voters of the world for losing their grip on reality. Maybe a period of poverty and hardship will knock us into shape to prepare for the next chapter of economic and political life.

Ugh – we seriously hope it doesn’t take a crisis of these immense proportions for everyone to wake up to the world we are shaping, where facts are merely tools to shape opinions and this sense of entitlement that so many people possess is threatening to destroy everything we’ve worked so hard to create.

There never was a “Brexit deal”. Brexit was all about pissed off working class people (mainly older folks) sticking it to the rich and to “foreign” people they saw ‘stealing’ jobs (they were never going to do themselves in any case). So the only “Brexit” these people wanted was to ruin the economy for the wealthy British middle class and to stop immigrants coming into the country (and kicking out the existing ones too). This is why the situation is such as mess. The real motives behind Brexit are not the ones being discussed in Parliament or in Brussels. It’s a mess and needs to be somehow reset so the real debate can take place. Otherwise this never ends.

We all agree at HFS that change can be good, and we must embrace change… but changing to what? That is the issue right now – what is wrong with the current system and what is the ideal system we need to move to… and its not only the UK grappling with this problem…

Posted in : policy-and-regulations

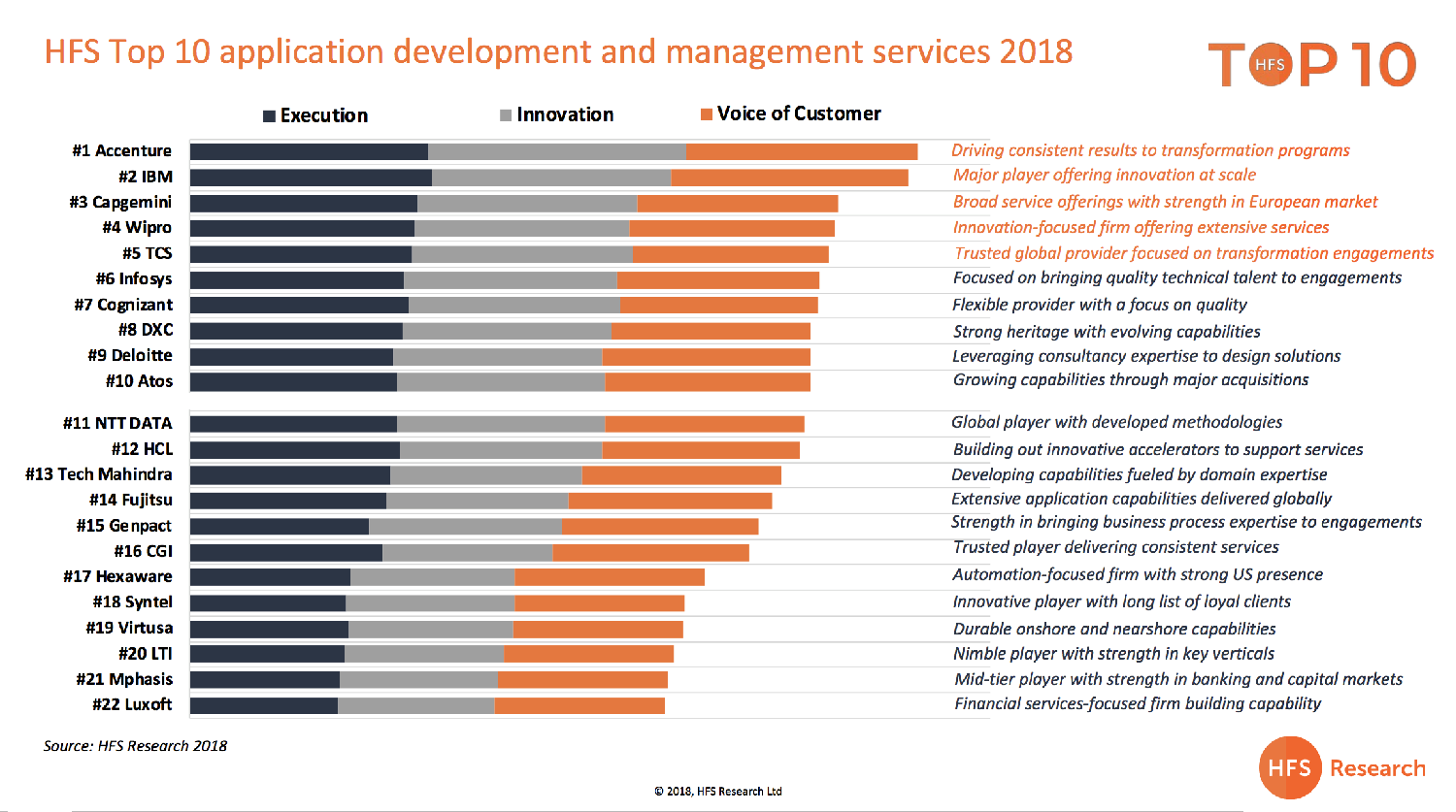

So it’s now 2019, and HFS’ Ollie O’Donoghue and Jamie Snowdon waste no time in the world of the new feisty Top 10 methodology, where they take no prisoners in ranking how the leading application development and management service providers performed…

The market continues to test and experiment with new frameworks and methodologies. The most notable are DevOps and agile, which are now widely adopted by many of the major IT service providers. Providers are implementing sweeping training and culture redevelopment programs to adopt best practices to support innovation and delivery in the application services space.

Now more than ever, enterprises are looking for providers to help them rationalize and optimize their technology stack, of which business applications is a significant component. In their drive toward the Digital OneOffice, forward-thinking enterprises are engaging with providers that can build innovative solutions that can integrate and unite business applications and in the process break down business siloes.

Given the importance of technology and business applications, enterprises are looking for collaborative partners that are invested in their success. As a result, we’re seeing an increasing reliance on existing relationships to deliver on fresh engagements.

Service providers are also working tirelessly to ensure they are making the most of their talent—driving training and retraining programs to help keep employees’ skillsets up to speed in a changing market.

So let’s see how the leading ten service provider shake out, based on interviews with 300 enterprise clients of IT services from the Global 2000 in which we asked specific questions pertaining to innovation and execution performance of service providers assessed. The research is augmented with information collected in Q1 and Q2 2018 through provider RFIs, structured briefings, client reference interviews, and from publicly available information sources:

Click to view full 22 service provider assessment

Developing talent. Providers are working hard to develop talent internally through retraining programs and bring in the right people by building out innovative talent attraction processes.

Building out partnerships. Providers are developing broader and deeper partnerships to support the increased demand from enterprises for a diverse and complex ecosystem.

Blurring service lines. Traditional service lines, particularly infrastructure and applications, are coming under more pressure as enterprises show less willingness to differentiate between siloes when designing an engagement.

Investment in capability. Many providers are building out their capability through acquisition of innovative start-ups and boutiques, as well as some major investments in the acquisition or merging of major providers and ISVs already operating in the space.

Q&A with Report Author, Ollie O’Donoghue

“Are the partners who got us here the ones to take us to the next place?”

This is always a tough question to answer, particularly in the application services space where the scope of projects is getting larger and encompassing far more technologies. To thrive in this market there is no perfect route – we see firms like IBM bolster capabilities through acquisition (RedHat being the largest), while firms such as DXC and Accenture pull in capability through partnerships, and the major IT outsourcers try to build up skills and talent organically. At its core, this is to meet the needs of an evolving buyer community that expects the best solutions from a complex array of technologies and practices.

So, what we’re seeing is a large section of the provider community fight to stay relevant in a rapidly changing market. Honestly, we can expect to see some casualties, there’s just too much to specialise in for some providers to keep pace with, and many are spread too thin to become real specialists. The future in this space belongs to those who can keep layering valuable interfaces between a growing technology stack that includes advanced automation capabilities. For some, this will be through becoming a jack-of-all-trades, and for others, it will be through unique specialisms – all who are in between are vulnerable.

Which of this bunch are going to break out of the pack, based on your recent conversations?

As we’ve mentioned, there’s a lot of movement across the leading service providers – but there are four or five that have a lot more going on than many of the others. Let’s start with IBM, which already has scale and differentiation in the space, but has jumped ahead of the pack in open source through the mammoth acquisition of RedHat. We also have Accenture which continues to be synonymous with innovation and bringing high-quality solutions to clients. The firm has also plugged in more digital design and apps agencies into its service lines in recent years, adding more brains and brawn to the rapidly growing market.

It’s also worth highlighting Wipro, which has a strengthening reputation in the application services market – strengthened by the firm’s big bets in digital. This part of the IT services market has always been the core of Wipro’s business, so the firm is able to pull in experience and skills that other firms still need time to develop. We also have Infosys which, with fresh leadership, has started to take the services game seriously again. The firm has done a lot of work to retrain talent and redevelop its strategy. Jumping on the developing push for onshore and nearshore, Infosys is also building out delivery centres, particularly in the US with plans for more work in Europe. Finally, Capgemini and TCS are gaining ground. The former through capturing more mindshare in Europe for its IT Services heft and expertise – a potential gold mine as businesses grapple with geopolitical pressures and look to local technology experts to help them. And the Latter for pushing a fresh narrative on the need for technology in the modern enterprise through its Business 4.0 thought leadership.

As a last note, HCL presents somewhat of a quandary to us since its purchase of IBM assets. It’s difficult to see the acquisition of somewhat legacy assets as a route to breaking out of the pack, but the reality is this could be a platform on to a broader customer base for HCL. All in all, though, we’re holding judgement until the firm has a clearer strategy for the assets.

Are there any niche firms popping up who can disrupt this space?

It’s a tough market for smaller firms to play in, but for specialists who can corner the market or disrupt business models, there’s plenty of room for manoeuvre. This is the first major IT Services analysis where we’ve included some of the mid-tier players where a lot of the innovation is taking place – simply because these firms have to try much harder to fend off the majors whether that’s the flexibility and agility of Mphasis or the vertical specialism of LTI.

There are even smaller players starting to challenge in the space – nClouds, an HFS Hot Vendor is an excellent example of a small firm with a compelling track-record in the market, particularly when helping enterprises shift applications and services to the cloud. There’s a vast amount of space opening up for players in the ‘small and cool’ category – the acquisition of RedHat leaves behind a massive gap in independent open source and there is a large portion of the community disillusioned by the acquisition that could be a huge boon to the right company. And with several mid-tier players hoovered up by the majors – notably Syntel and Luxoft – there are gaps in the market waiting to be filled by agile firms.

So, Ollie, which emerging apps services firms are worth keeping an eye out for?

nClouds – In many ways, nClouds is the definition of a company thriving from the increasing blend of application and infrastructure. The firm leverages practices and technologies such as DevOps, Containerization, and public cloud to help clients evolve their technology stack. We were so impressed by client feedback from this firm that they made their way into the first HFS Hot Vendors at the start of 2018.

Trianz – While not necessarily a niche player, Trianz has proven itself more than capable of taking on much larger firms to win deals. The firm has a broad range of services, but its edge seems to be the agility and flexibility it can bring to engagements. The firm has won multiple awards and seems to be benefiting from increased enterprise appetite to diversify engagements amongst many small players, rather than one giant one.

Linium – (acquired by Ness Digital Engineering) – For specialisation, we need to look no further than Linium which has worked tirelessly to carve out chunks of the enterprise service management space. The firm has dedicated practices for core business platforms such as ServiceNow, as well as capabilities in custom application development. The firm was acquired by Ness Digital Engineering in 2018 – bringing with it broader capabilities and access to talent, as well as access to a broader pool of clients.

GAVS Tech– When we covered Gavs Tech in our Q3 Hot Vendors, we concentrated on their zero-incident framework, an approach to reduce the impact of IT issues on end-users. But the firm has used the mantra across other service lines in the space, including a pay as you go DevOps models that focus on deploying reliable application code and resources. The DevOps platform provides an integrated solution for application development, testing, deployment, scaling and monitoring – not only offering improved speed and quality, but also a degree of simplicity in a complex technology environment.

Bottom-Line: Increasingly scarce talent, combined with a never-ending demand, places real pressure on service providers to keep innovating their delivery models

Simply put, the modern application services market is now so complex it’s not possible to be an expert in everything. Providers are beginning to recognize this and continue to bring in partners to support their delivery capabilities while retraining staff to move them into higher value work.

At the center of this changing market lies a huge question mark around talent. Enterprises are telling us that there are major talent crunches in key areas of the market and for some applications, which is forcing them to push more work over to providers. The challenge is that many of these providers are facing similar challenges. All of the IT services providers assessed in this research have extensive retaining and retraining programs in place to ensure they get the most out of their teams. They’re also partnering up with major sources of talent, particularly higher education institutions.

Nevertheless, the market is showing no signs of slowing down to allow providers any breathing space. Enterprise applications are now a major focus area for CIOs and technology leaders to get right. They need help writing off legacy, making sense of extensive technology estates, and finding areas of opportunity for new services and solutions.

Posted in : IT Outsourcing / IT Services, OneOffice