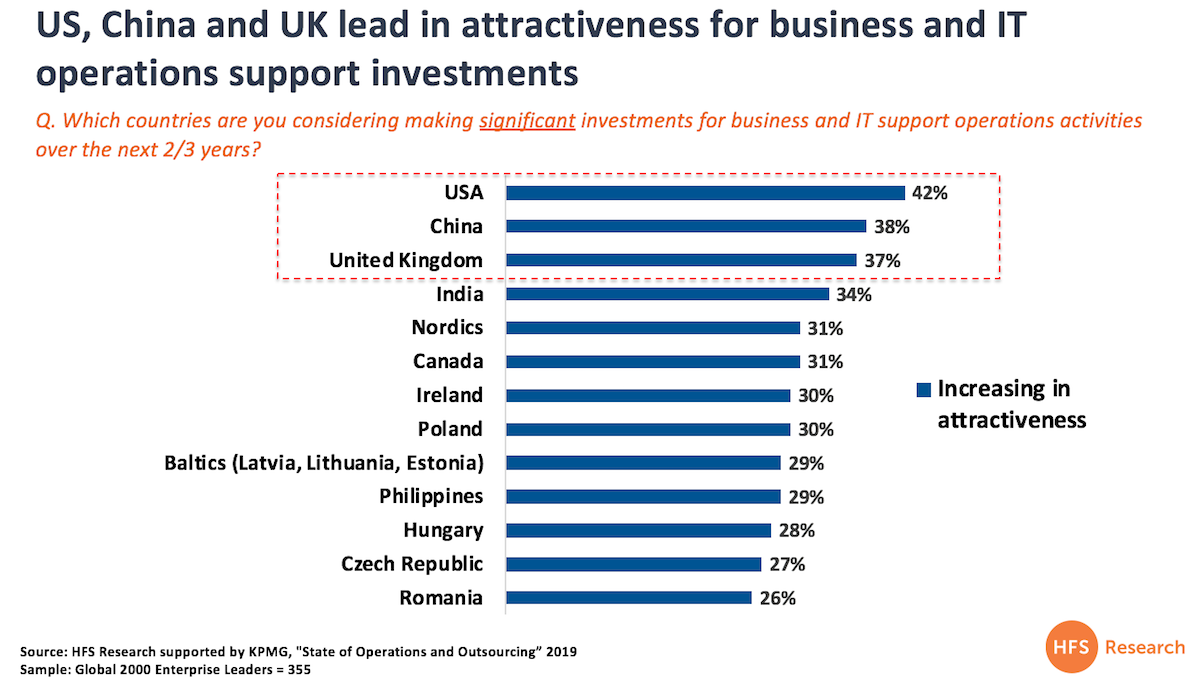

While the UK government is busily doing a tremendous job destroying the country’s position as one of the world’s great financial centers and multi-cultured commercial environments, one unlikely scenario is unraveling: the steadily devaluing currency, availability of labor (especially in its former manufacturing cities), and adequate education system is placing the country up the league as, now, the third-most attractive location to source business operations and IT support. This is according to the brand new data from the HFS 2019 State of Operations and Outsourcing study, conducted with the support of KPMG, where we interviewed 355 operations leaders from 355 of the Global 2000:

Bottom-line: As value from low-cost labor levels out, the focus shifts to increased complexity and talent closer to the business

As we reveal more of the new survey data, you’ll see a prominent shift away from enterprise intentions to invest in traditional outsourcing pivot towards a strong desire to find partners which can support technical complexity in AI, hyper-personalization, and automation. Net-net, enterprises need support staff close to the business with the ability to understand process and technical complexity that they have never before needed. This doesn’t mean that popular locations like India and Philippines will see their service industries plummet, it just means outsourcers and GBS leaders need a healthier balance of onshore/nearshore/offshore to bring it all together. It also signifies a shift from “outsourcing” to “expertise partnering” that changes the location playing field significantly. While the USA and China are no surprise as their host the world’s largest economies and businesses, the UK is the surprise mover, as political conditions have created a more competitive market to invest in support services.

Watch this space for more as we drip-feed you this incredible data over the next few weeks…

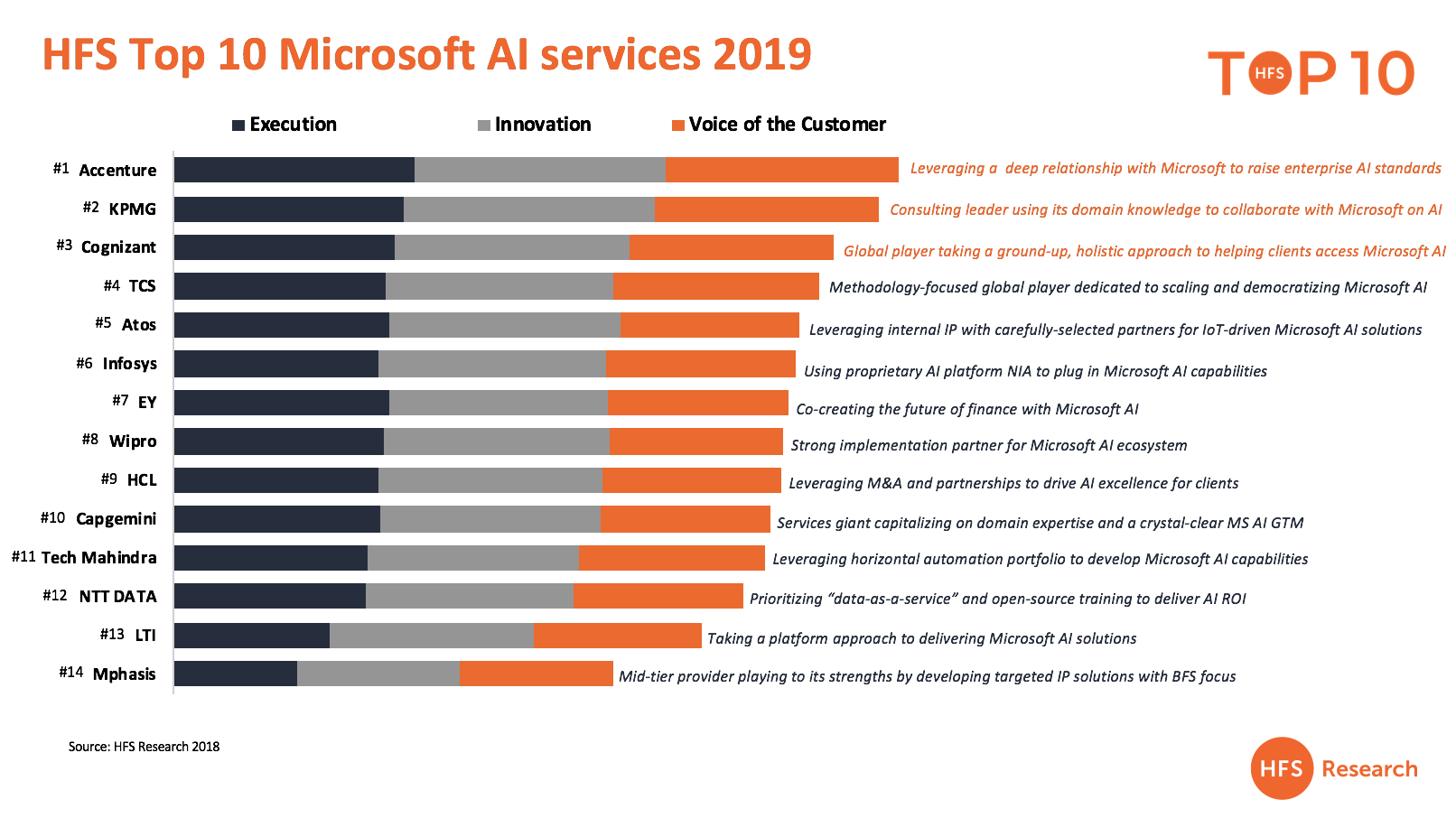

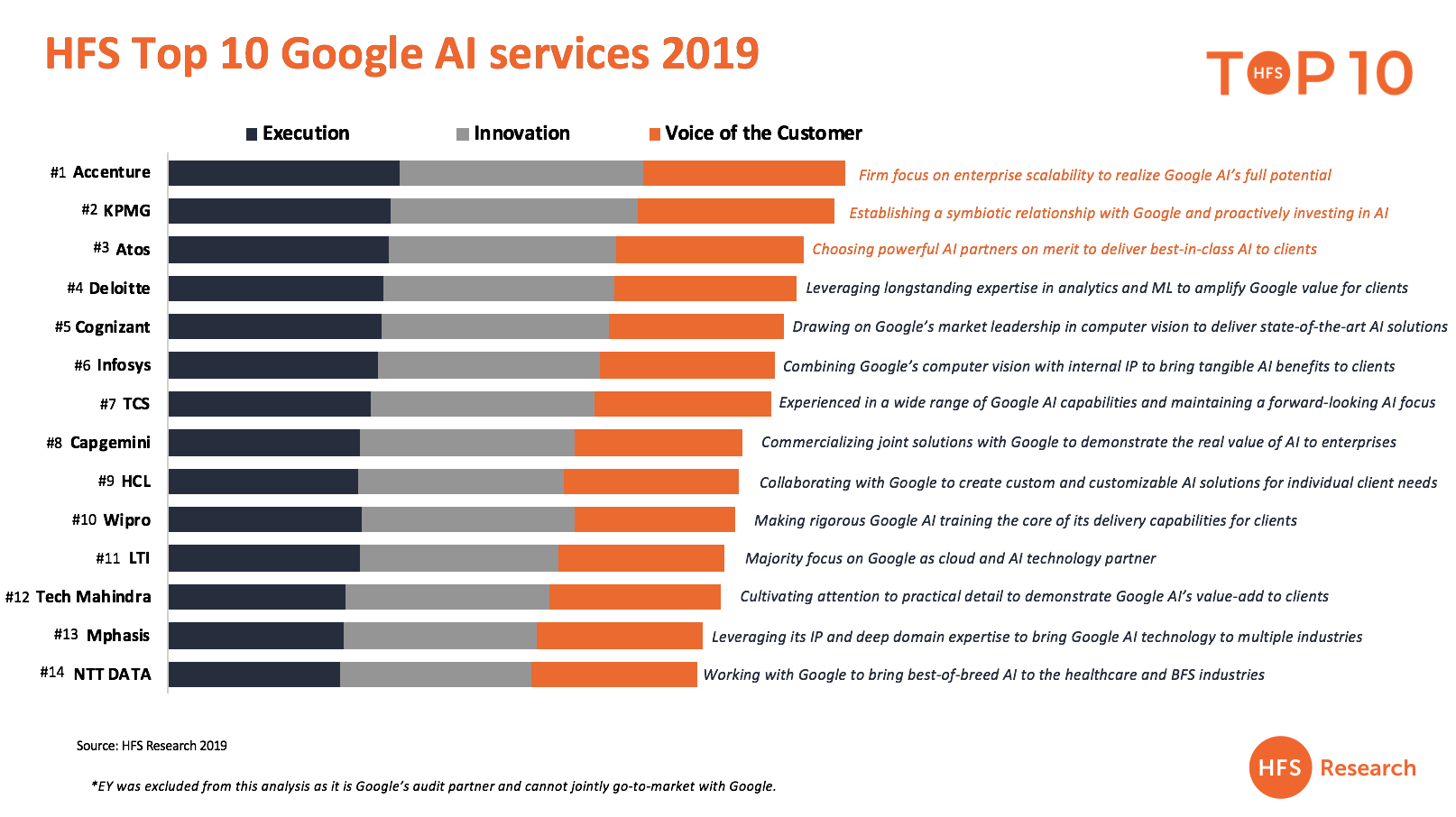

We’ve reached a stage where we can start to assess the capability of leading service providers to deliver comprehensive services across key AI platforms, especially Microsoft’s Azure AI platform and Google’s emerging AI platform suite. So without further ado, let’s ask HFS’ Research Vice President, Reetika Fleming, how she fared leading the two major Top 10 efforts this year…

Reetika – how are services around AI platforms progressing? And specifically, what have you learned with regards to Google and Microsoft platforms?

We’re continuing to see AI ecosystems evolve around the big cloud vendors – Microsoft, IBM, AWS, and Google. From our recent deep-dives into the AI services alliances developing around Microsoft and Google, I can tell you that there are different strategies at play here. Google and Microsoft themselves have their own strengths and priorities, and the SI and consulting alliance partners are collaborating with them in different ways.

Google’s portfolio of AI components, such as text-to-speech and computer vision, is a great starting point for a fundamental development layer. Google’s AI R&D leadership is well respected among clients and service providers alike. What has been missing are combined applications of these technologies to solve specific business challenges for major business functions and industry verticals. This is where service providers have a critical role to play, and they are filling the gaps by building solutions either in collaboration with Google developers or with clients in selected industries that are ready for AI.

Microsoft is emerging as the most ‘enterprise friendly’ AI ecosystem. As enterprise clients grow more comfortable with AI initiatives using the Azure technology stack, the services market is quickly developing around client demand. We expect this market to pick up significantly in the coming year as AI services and technology as a whole see greater adoption and as Microsoft and its services partners make more concerted efforts to bring more relevant and timely AI solutions to large enterprises.

Large service providers, including IT services firms, boutiques, and consulting houses, have established or expanded their ecosystem alliances to work with MS and Google on AI. Joint go-to-market activities are taking the form of:

capability development (POC and pilot funding, talent development);

market awareness creation and sales planning (joint account planning, campaign work such as Microsoft’s “Make AI Real” workshop series); and

technical collaboration (joint research, IP creation).

What is driving firms to invest in AI – is it a real desire to meet newly designed outcomes, or more a compelling need to keep on top of emerging tech?

Most of the clients we’ve spoken to in the last year have gone through the learning curve of viewing AI simply as the shiniest new toy the need to be seen to have a strategy around. This is finally starting to become about plugging real business problems and tapping into new opportunities using the evolving range of AI technologies.

Here’s an anecdotal indicator of how things are skewing towards business – at least half the number of AI leaders and sponsors we’re speaking to are business stakeholders, whereas this was squarely an IT/Digital/CoE skewing peer group in years past. Enterprises in our research are certainly looking at business outcomes from their AI investments, including driving up customer experience with AI-enabled apps with virtual assistant support, improving the quality of anomaly detection in manufacturing equipment, and reducing turnaround time on invoice processing. This is good validation for our thinking earlier in the year that AI needs to be driven by the business, with IT as a key partner.

What type of services are you seeing drive the AI industry right now? Is it more service providers delivering “support” work for clients who’ve already figured out what they need, or are you seeing real “co-innovation partnerships” where provider and enterprise work together to design new process flows to achieve pre-defined business outcomes?

The last few years has seen many services firms go from completely opportunistic AI exploration to the formal development of AI practices. This is no small feat considering:

the technologies are still evolving, at a point where new academic papers are leading to breakthroughs all the time

the talent is “thin on the ground” for both technical skillsets in data science, applied ML engineering, and distributed computing, and non-technical understanding of the application of AI into business

the range of capabilities needed to make enterprise AI a reality require massive amounts of collaboration within a service provider’s organization (and their clients) going from data, analytics, cloud, infra support, business domain expertise, consulting, design thinking, product development…

Pure support work is still a norm today, as many clients will test the waters with service providers at the execution level on a project or two. But doing pilots and POCs on repeat can only take a service provider so far. They have learned over time that they need to bring a multi-disciplined team together with industry-specific solutions to actually “collaborate” with their clients.

A few market-leading service providers have certainly developed these types of co-innovation partnerships with their strategic clients. They jointly ideate and vet AI opportunities, and are able to connect across business and IT stakeholders within these firms because of their reach. Here’s how you know these engagements are really partnership-driven – the service provider will be as invested as the client organization in helping the client develop their own AI capabilities, whether that’s through training talent, setting up CoEs, advising on governance and control, or investing to solve unique client problems.

How are you seeing AI impact enterprise “experiences” in terms of customers and employees? How do you see this advancing as AI evolves?

We’re seeing tremendous interest in using AI to drive better experiences, particularly to improve customer relationships. Phil, you talk about the hyperconnected future state where enterprises need to not just respond to but anticipate customer needs. AI technologies are perhaps the biggest catalysts for hyperconnectivity, because of their ability to “hyper-personalize” customer experiences.

I love the concept of AI ultimately becoming invisible or just natively being built into the process. You don’t know you’re using it, don’t need specialized skills or training, you just get the benefits, whether you’re a customer, partner, or employee. The best experience in these terms is either delight (e.g. this company knows exactly what I want) or effortless engagement (e.g. it doesn’t take me what feels like a million years to serve this customer!) We’re going to start to see new standards emerge for major enterprise platforms and systems in the next few years for AI-driven user experiences based on this concept. It’s no coincidence that the SAPs and Salesforces’ of the world are pouring millions into AI.

Casting your eye ahead 2-3 years, who do you see winning in the services space – will it be one of these early leaders, or can you see new players emerging with a different approach?

As we see the further formalization of the AI services market, we’ll need to watch for:

Who can find the most successful talent models for AI? Whether that’s crowdsourcing a la Wipro-Topcoder, EY’s “Badges” program to recognize employees’ new skills, or TCS’ investment with Cornell Tech through their new innovation hub in NYC… there’s different strategies on AI talent development for the future, and not all will pay off.

Who is able to develop and successfully sell digital change management to clients – we see this all the time right? Change management is set to the side because clients believe they can do it all internally, but change management for AI is fundamentally different than other initiatives – you have to alter job roles, the workings of entire processes and decision-making points, establish and continually monitor governance and transparency of new models, and so on. Not everyone can firstly sell digital change management along with AI implementations, and then deliver successfully, and it can be what makes or breaks AI engagements.

Who is able to make AI easy to develop and scale – internally and for clients. Centralizing and creating libraries of reusable assets, investing in “autoML” type of capabilities that can compress the data prep and training time, containerization of capabilities and existing platforms…these are all indicators of prioritizing scalability for AI.

Who is able to bring an integrated approach to automation technologies like AI? It’s an easy tell when a service provider’s RPA team has no idea what their AI practice is doing. As we always say, clients want to buy outcomes, so the more service providers can bring a holistic set of capabilities to the table, the more their AI pitch will actually land.

Who is able to partner with technology vendors most effectively? This includes joint account planning, joint go-to-market and product engineering AI specialists like kore.ai and of course the cloud vendors.

I see the market leaders in these early days pulling ahead, but there will also be a few new logos on the board in the next 2-3 years because of these factors. The service providers in the middle might be left doing some of that support work you referenced earlier.

Lastly, we’re in the final phase of analysis for our comprehensive Enterprise AI Services Top 10 report, so check back with me in a few weeks for more on this.

HFS Premium Subscribers can click here to access the 2019 Microsoft AI Services Report and here for the 2019 Google AI Services Report

When it comes to staying relevant in today’s workforce, let’s get to the heart of the matter – YOU have a simple choice to make:

Do nothing and be part of the “Frozen Middle”. Decide you can’t be bothered to learn anything new, so make sure your firm has the same attitude (or has a thin veneer of innovation masking a cesspool of lethargy and love of perpetuating legacy processes and business practices). And ride this next wave of hype out for a few years before you can quietly ride off into a comfortable sunset, or…

Become a change-driver. Decide you have to get ahead of emerging technologies and their massive impact on business ecosystems and make sure your firm has what it takes to sponsor your burning ambition to drive cultural changes, new learning and ability to rethink how business processes and practices are wired.

Once you decide which of these two categories which you wish to belong, then make sure you’re in the right company to execute your survival plan… otherwise, leave and find one that is.

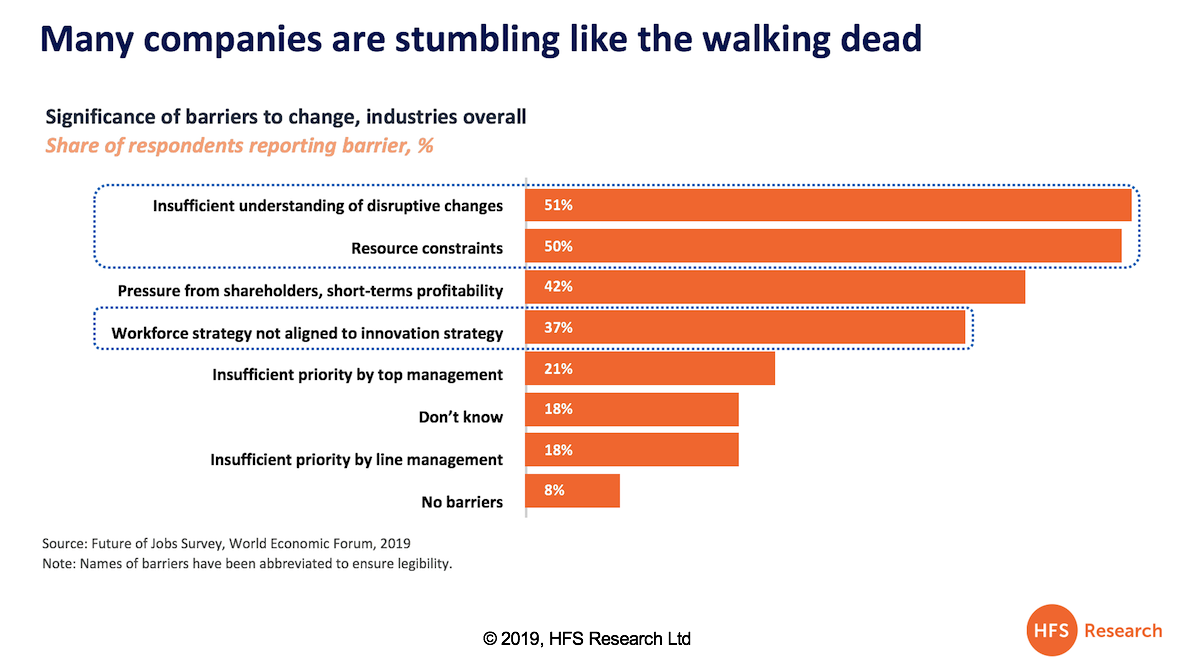

Because the data from the recent World Economic Forum jobs study shows half of enterprises are being held back because their staff fails to understand the disruptive changes in their industry, and an alarming 37% of enterprise leaders do not feel their current workforce is aligned to their innovation strategy:

There are no half-measures here, folks – you can’t dip in and out when it comes to driving automation and AI solutions – people are quickly getting found out for having a veneer of understanding. Either you decide to focus on really understanding how to apply these solutions to your business, or decide you can’t be bothered and focus on maintaining the old way of keeping your business’s operations lights on.

Assuming more people who visit this lovely blog are in category (2), then let’s review what we can do to actually become an AI change-driver….

Saving our jobs when they become “AI-able”

So the automation/AI marketing spiel is firmly espousing that our jobs will be so much richer when we offload as many of our “operational” activities to RPA loops and self-learning algorithms. Isn’t it so cool that all these new un-computerizable activities will just magically appear to fill our job voids to make our lives so much more enriched and fulfilling?

The truth is that people will only truly buy-in to AI and automation when they are secure enough to hand off a lot of the tasks they currently do, with the transition to the new work already in place to maintain their relevance and value to their employer.

Let’s identify how to learn the new stuff so we can offload the AI-able activities

Let’s be direct – in today’s swirl of constant shiny new things, it’s becoming overwhelming for many of us who got by on a traditional education and an ability to deliver routine tasks, handle the usual game of corporate politics and command an ability to “know enough to be dangerous” to stay relevant to our colleagues and management.

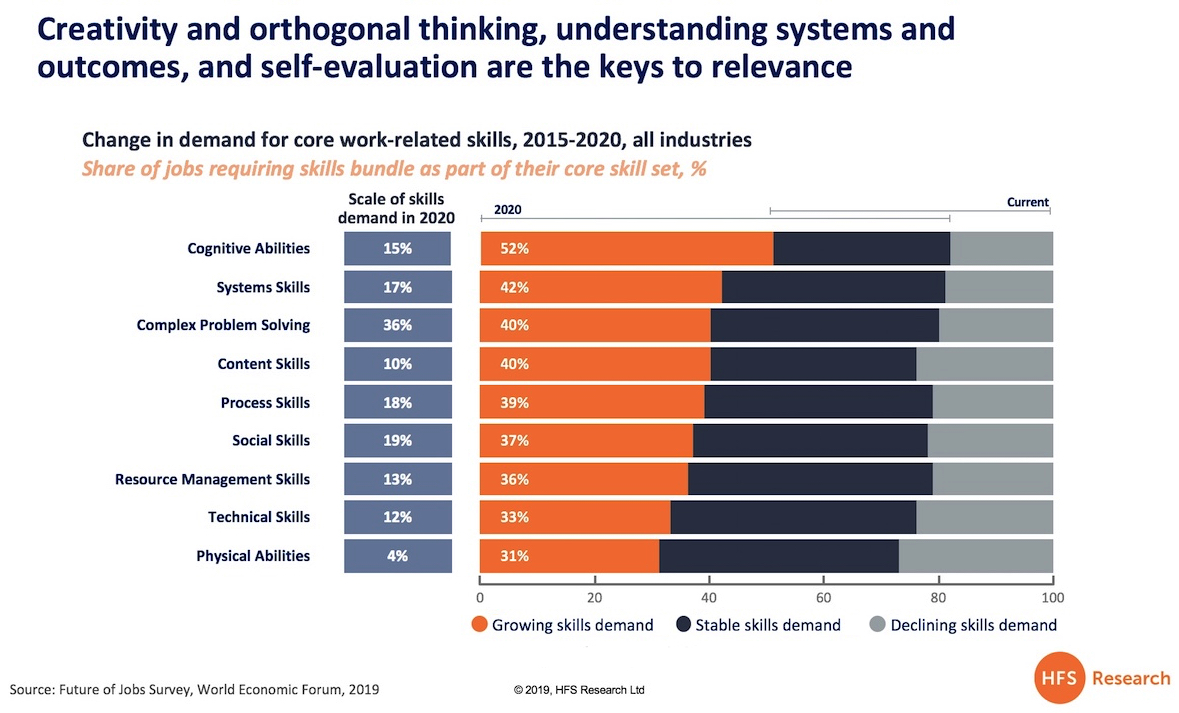

Sadly, everyone is now being scrutinized whether they have certain “skills” that will make them worthy of employment as more and more of their job can be replaced by algorithms and automation loops. So let’s take a look at these skills that came top in the recent World Economic Forum Future of Jobs report, where 100 of the leading firms within each industry were interviewed:

Cognitive Flexibility. The ability to generate or use different sets of rules for combining or grouping things in different ways.

So this means you need to know your audience and adapt your ideas to suit their needs. You can’t just repeat the same things to everyone – you need to be great at listening and communicating, so you can pull together common threads and continually adapt. Plus, people need to know you listen to them – there’s nothing worse than being that old windbag who just spouts off the same old guff because they love the sound of their voice. For example, if you are convincing your HR head about your firm investing in an AI platform, they are likely to focus on the ethics and regulatory/data privacy issues. Your CFO, on the other hand, will probably want to focus more on the cost/benefit and ease of use. Your CIO will want to understand why your firm can’t use existing tools they already have invested in. There are three sets of conversations you need to find common threads across if you are going to get a consensus to invest.

Creativity. The ability to come up with unusual or clever ideas about a given topic or situation, or to develop creative ways to solve a problem.

Creativity is so important, especially in markets where differentiation points are wafer-thin. Take our beloved IT services providers, for example. Most of them today are offering an identical solution and their pricing is usually similar, and each of them can churn our analyst reports which portray them as the best. Big fancy business terms, cardboard stories of transformation won’t cut it anymore… So the differentiation is increasingly shifting to “who do you want to work with” at a people level, so the onus must shift to really listening and understanding your client needs and proving to them you really get them. Hence, creativity and emotional intelligence are so closely aligned here.

Problem Sensitivity. The ability to tell when something is wrong or is likely to go wrong. It does not involve solving the problem, only recognizing there is a problem.

My least favorite phrase these days is “fail fast”, as this is usually a term people use in hindsight after they screwed up. But in fast-moving industries such as consumer goods or online travel, it is often not critical is you launched a poorly thought-out product or service. In slow-moving industries, such as process manufacturing, a poor decision could affect a single process that takes years to get right, and could be fatal (hence “fail fast” only works in pilot phases, not in real business). For example, your firm could be launching a recruiting campaign that you realize could be accused of discriminating candidates by age or gender, which would have been par for the course a couple of years ago. You realize this could have serious implications for your firm in today’s hyper-sensitive data privacy environment, and alert you management asap to change course. You may not have the solution, but you were sensitive to the problem. Here, your ability to think laterally and other variables is so important.

Monitoring Self and Others. Monitoring/assessing performance of yourself, other individuals or organizations to make improvements or take corrective action.

The ability to assess performance for your firm – and pinpoint improvements – is incredibly valuable to your management. As the WEF data emphasizes, two-thirds of financial services firms (for example) see an insufficient understanding of disruptive changes as a significant barrier to change. At the same time, half of them see a poor alignment between their workforce strategies and their firms’ innovation strategies. This indicates that staff who can pinpoint how to test their own understanding of the changes within their industries, and also the awareness of their colleagues, and then suggest ways to work together as teams to train themselves how to close these knowledge gaps, will be highly appreciated.

So if you work in a traditional bank, for example, and you recognize several digital startup banks that could really hurt your business as they target millennials who are prepared to switch banks because they have a better app experience, you need to make sure you are ahead of the game and your team is also. Being able to bring in experts to educate you and your team, or forge enlightening discussions with disruptive startups willing to share their business model ideas are great examples of how you can be a great performance evaluator. This is where we see a lot of cognitive flexibility and creativity aligned with emotional intelligence – and a willingness to put your ego to one side.

The Bottom-Line: When times are good is the time to hone your skills and get ready for when times get tough. You have an amazing opportunity to rise to the change, so please don’t waste it

Remember all the discussion about the carnage automation and AI were going to bring to the market place? Forrester claimed 1 million US B2B sales jobs will go away by 2020; Gartner predicted one in three jobs will be converted to software, robots and smart machines by 2025; an Oxford University Study claimed about 47 percent of total US employment is at risk; Stephen Hawking (may he rest in peace) warned us that AI would be the biggest – and possibly the last – event in human history. At HFS, we have bleak predictions too about the future of job as most modern ambitious companies are simply stopping creating the jobs we’re doing today, and refocuses on the additive needs they have in the future, that technology cannot deliver them.

The simple truth is that change that necessitates the fundamental retraining and learning of new ways of working, new attitudes and collaborative cultures is much slower moving that analysts, academics and pundits can predict. Merely slamming in new tech kit and expecting change to happen is the ultimate recipe for failure in today’s market. Remember it took enterprises two decades to adapt to ERP solutions (many still are)… it even took accountants a decade to adapt from Lotus 1-2-3 to Excel. Why would we expect today’s business and IT professionals to adapt much faster to new tools and solutions that actually require real training – and all that coupled with making real changes to processes that have been operating exactly the same way as they did 20/30/40 years ago, with the only “innovation” being models like offshore outsourcing and shared service centers, cloud and digital technologies enabling those same processes to be conducted steadily faster and cheaper? Let’s be honest, most companies still operate with their major functions such as customer service, marketing, finance, HR and supply chain operating in individual silos, with IT operating as a non-strategic vehicle to maintain the status quo and keep the lights on.

Coupled with the pain and pace of change and the lethargy of enterprises to do anything fundamentally different, is the fact that it’s been over a decade since we experience a real economic downturn. We’re operating at a time where it’s challenging for firms even to populate the call centers and find junior staff willing to perform mundane routine activities. And talk to any C-Suite executive and they will tell you finding leadership talent and managers with “transformational” skills is nigh-on impossible – and incredibly expensive.

We are lucky to live at a time where we have a multitude of established and emerging change agents at our disposal: global sourcing, Design Thinking, Robotic Transformation Software, AI, Analytics, IoT, blockchain among others. So use this time to learn-up and take advantage of the demand for talent, as one day the climate isn’t going to be so rosy for talent, and jobs that can be automated / AI-ed will never resurface. The time to challenge yourself and make this crucial choice is now, please don’t sit on the fence and wait until it’s too late.

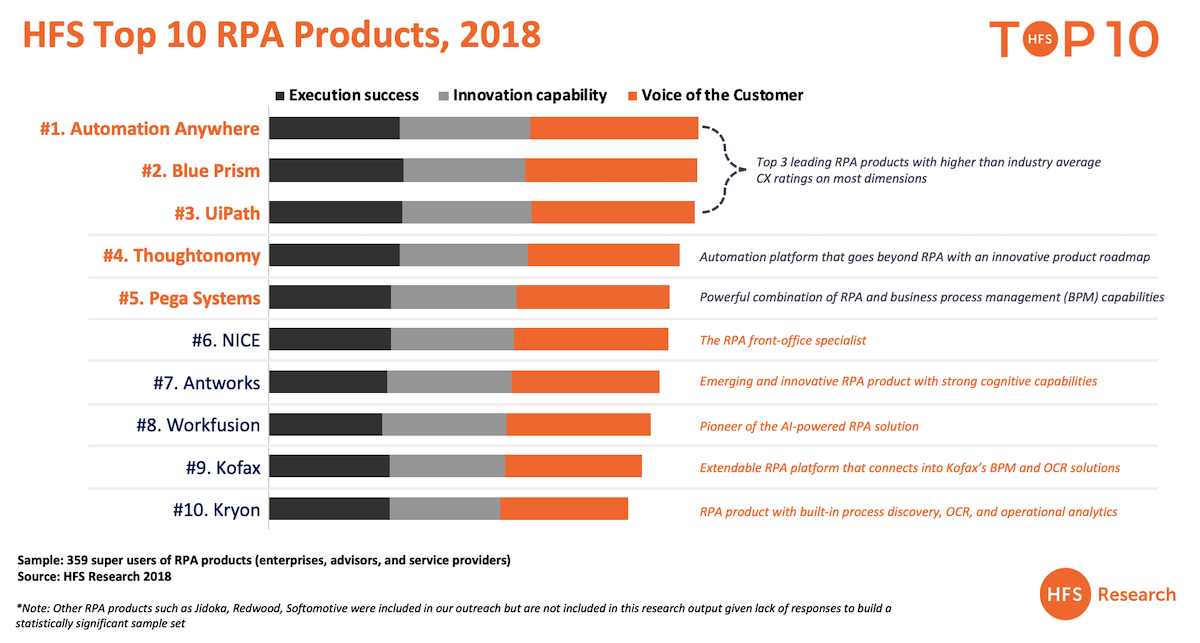

Are you as confused are we are with some of the recent analyst matrices floating around the industry this year? Some products are performing completely differently depending on the analyst and how they “define” the market and whatever methodology they used to score each product.

However, one thing is clear: at HFS we ensure we rely on a lot more than a briefing and a handful of rose-tinted clients served up by the suppliers themselves. We reach out across our global network of power users (enterprise clients, advisors, and service providers) to get the true unvarnished experiences of robotic software.

This is why we scrapped the 2×2 matrix last year and went for a direct ranking of suppliers, based across three critical variables: execution, innovation and the voice of the customer. HFS subscribers can click here to access the full 2018 RPA Top Ten report.

On 2018, we introduced the “Voice of the Customer” to rank the leading RPA products across the experiences of 352 power users

In short, there are growing questions about whether “RPA” can deliver transformation on the promised ROI and outcomes, especially as most RPA initiatives continue to be small and piecemeal, with truly scaled RPA deployments are rare (only 13% of client boast any true scale to date). The industry is still struggling to solve challenges around the process, change, talent, training, infrastructure, security, and governance – hence our shift to re-categorizing and evaluating these RPA products by their ability to support clients’ desired business transformations.

With the mission to demystify this confusion and uncover the truth to successful RPA deployment, last year we conducted a first of its kind RPA CX research to develop the list of “HFS Top 10 RPA Products”. The research was based on interviews with over 350 clients and product partners across the ten leading RPA products across:

Ability to execute based on product functionality (Ease of integration with legacy IT, Unassisted automation functionality, OCR functionality, Scheduling functionality, Development tools, Exception handling, Required set-up coding, Ease of product configuration); integration and support (Service extensions and connectors, Documentation, Certification program, Training and customer support, Experience in serving multiple geographies, Adoption across multiple industries, Required IT skill-sets), and security and governance (Uptime and SLA commitments, Version control and upgrade management, Centralized controls, Regulatory compliance, Enterprise security, Disaster Recovery (DR) and Business Continuity Planning (BCP))

Innovation capability based on flexibility and scalability (Accommodating process / environment changes, Licensing model flexibility, Ability to handle multiple processes, Workflow templates and library of processes, Handling multiple inputs) and embedding intelligence (Processing structured, semi-structured, and unstructured data, Operational Analytics, Dashboards, and Artificial Intelligence (AI) capabilities)

Voice of the customer based on the RPA products ability to drive business outcomes (Realizing cost savings, Speed-to-market, Overall satisfaction, and Client reference ability)

In 2019, we’re refocusing the market on the ability of robotic software to support clients’ desired business transformations

HFS Research has redefined Robotic Process Automation (RPA) software as Robotic Transformation Software (RTS) in order to put the emphasis on transformation and track how well automation software firms are enabling enterprise change.

The 2019 HFS Robotic Transformation Experience Survey will paint the truest picture yet of the software companies that are really enabling change and embracing integrated automation capabilities. This research will benchmark the collective customer experiences of the leading RTS products across multiple dimensions including:

· Functionality and ease of use · Implementation, service, and support · Security, governance, and controls · Scalability and flexibility · Innovation and embedded intelligence · Ability to transform business processes and deliver business outcomes

The research will provide a credible, unbiased, collective voice of the customer that assesses business results and transformation potential, based on actual customer experience rather than market hype and rose-tinted client references bragging about their number of bot implementations.

Note: This survey is designed exclusively for users/clients of RTS and partners (consultants and service providers).

All responses will be kept strictly confidential and it will take approximately 15-20 minutes of your time.

We will award two lucky participants with a years’ free access to HFS premium research where you can access the industry’s leading data on automation and AI solutions – and have priority time with our leading analysts:

BPO (Business Process Outsourcing) grew up because of all the exceptions enterprises have to process that were not able to be absorbed into the standard ERP software. Yes, we found people equipped to do this work at lower wages housed by efficiently run service providers. And that work we couldn’t initially send to the BPO providers we just found manual workarounds to get it done until we eventually found an outsourcer who would find a model to take on that work for you.

However, just as many enterprises were running out of places to find (yet) more and more hidden costs they could quickly remedy through (yet) more outsourcing, along came their perfect new toy to unearth costs they had never thought possible to eliminate: RPA.

Yes, folks, this stuff is just the thing to keep you occupied for the next few years to keep your greedy CFOs at bay – and even includes the word “robot” to conjure up images of human work displacement, creating hours upon hours of repetitive (robotic) debate at conferences from people who literally sprung from seemingly nowhere to become lifelong experts in this new dark art.

And, oddly, most of these new RPA maestros seem to be exactly the same people who were hawking the delights of business process outsourcing just a couple of years ago. So maybe the connection between BPO and RPA is a lot closer than we think?

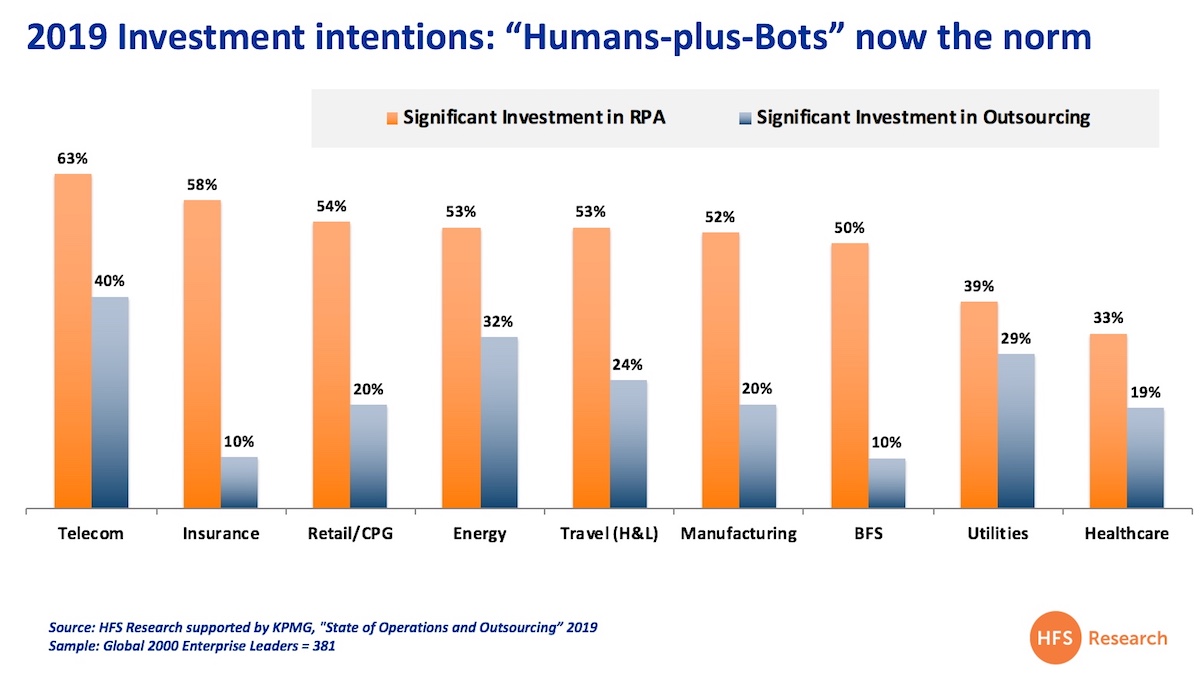

Let’s examine the findings from the recent State of Operations and Outsourcing study, conducted with the support of KPMG across 381 Global 2000 organizations, where we questioned operations leaders about their intentions to keep investing in both RPA and outsourcing. This data shows the tranche of operations leaders making significant investments in RPA and outsourcing, sliced by industry sector:

Financial services firms, where outsourcing is most mature, are showing voracious appetites to go down the RPA path

While banks and insurers are showing the smallest appetite (10%) to keep pursuing aggressive outsourcing strategies, they are right at the front of the queue (50%) when it comes to RPA. Insurers were one of the first industries to explore BPO and offshoring twenty years ago, so it’s little surprise that RPA is so appealing to these firms, where they can find completely new ways to mimic highly repetitive, intensive processes, plagued by manual workarounds, using smart software solutions. In addition, many of these firms have been outsourcing back-end processes that have become very stale over the years, and RPA provides the perfect shakeup to rethink how to rework these.

Sometimes RPA provides the perfect catalyst to force an outsourcer to get back to the table to reinvest in their client or risk losing them to a hungrier competitor. Banks have always been a bit weird when it comes to outsourcing – they have tended to move massive amounts of IT development and maintenance work to service providers over the years, in addition to infrastructure, but have been very shy when it comes to BPO, often preferring to move process work into their offshore shared service centers, citing issues around privacy and compliance as their reason to keep it inhouse. It’s surprising that the appetite to explore RPA is so strong (58% making significant investments this year) when you consider that most banks have to comply with various regulations which necessitate a human to oversee pretty much every process that is conducted within their organization.

However, with the sheer quantity of legacy detritus plaguing banking IT systems, such as spaghetti code that began its life several generations of programming languages ago, where some of the original COBOL guys who started it have since deceased (no joke), and mainframes that really should be moved to one of Kim Jong’s testing sites, RPA can actually help breathe new life into fixing some of these processes in a way that can have a massive transformative effect on their operations. (Read our POVs on Banking and Financial Services RPA uptake here to learn what 80 of them are doing, and read here to deep dive into the insurance sector and its attitudes towards automation.

Industries that need to shed costs as fast as they can to remain viable are aggressively jumping in

Telecom was always a bit late to the game when it came to heavy outsourcing, partially because its systems are so complex and they are so dependent on microtransactions which are very difficult to outsource. However, the high throughput, high-intensive nature of telecom processes places the industry right at the forefront of RPA appetite. With such a strong impetus also on outsourcing, expect to see more of these automation-led outsourcing deals transpire. Utilities firms, on the other hand, still tend to be very slow adopters of new models, and most are still very focused on getting their outsourcing models operational, after many painful years of dealing with labor unions and archaic IT systems. Surely RPA beckons soon, but expect this sector to be behind the others.

Retailers have always struggled from decentralization (often growing through many years of painful M&A) and horrific ERP experiences. With the pressure to adopt digital customer channels more intense than ever, RPA does provide some significant benefits to fixing legacy processes that were simply not cost-effective to outsource in the past. It’s a similar story for travel firms, especially those making major efforts to up their customer digital experience. RPA can be a huge help linking customer portals with back-end systems that have suffered from manual workarounds and poor integration for decades.

Manufacturers have been one of the pioneers of outsourcing, especially as many focused on core supply chain areas first, before moving onto IT and BPO in more recent years. Most manufacturers ran out of room to optimize their outsourcing engagements many years ago, and stagnated when it came to improving poorly-integrated supply chain and accounting systems. These firms are all about driving out every ounce of cost, and if they can do it, while making process fixes they have neglected since the days of MRP and JIT, then RPA is something they really want to get moving on.

Energy firms have always been massive outsourcing customers with a strong SAP underpinning – both for IT and BPO work. With the massive cost pressures impacting energy firms, and a major impetus to transform their operating structures away from legacy labor-intensive models, it’s no surprise that energy firms are among the early adopters of RPA (click here to read more about the transformation issues facing oil and gas firms, and here for a decent case study of NPower and its RPA experiences).

Healthcare has always been the “odd duck” when it comes to operating models and transformation. Starved of funding, held hostage by unions, and a culture of never changing anything, healthcare is typically at the back of the line when it comes to being bold and exploring radical new opportunities like RPA. However, with the tumult being created by the impact of Obamacare and whatever is going on with its unraveling, there are pockets of healthcare organizations now exploring more innovative ways of saving themselves, and RPA can be very effective for many (read here for some greats example of how some healthcare orgs have adopted RPA).

Bottom-line: Robotic Business Outsourcing is looking like the new BPO. People and bots delivering activities interchangeably

However which way we were looking at it, the outsourcing space was slowing down, and it’s hard to get too excited about a market growing at 1-4% each year. We have been brought up in a world promising 50% savings and achieving 30%. We’ve needed to find the next thing to grab onto that was back-office focused, a bit messy, quirky, and loaded with hype. We could bore you to tears with a lots of caveats of how to avoid screwing up your RPA, how to focus on “value” and not “cost” (who are we kidding), how you need to align business and IT, how you need to get right on top of change management and cultural impact. But read the RPA Bible if you want all the caveats, the best practices, the pitfalls… and how to avoid RPA hell.

However, if you contract with your BPO service provider to deliver you your preferred mix of bots plus humans to execute your work, they will absorb much of the RPA hell for you and work with your teams to get everything in some sort of functioning order as quickly as possible.

Today is the “new outsourcing”, where deals are spiked with RPA to deliver the numbers. So, it’s time to love with what we have created and see if we can somehow make it all work. In a couple of years, RPA will be a hygiene commodity tool in the big box of efficiency tools (or most likely as part of a broader automation platform that integrates these tools together). The future is all about managing data and partnering with smart firms to help you do that effectively so you can keep your business ahead of the curve… this RPA phenomenon (or whatever we end up calling it) is simply one additional lever to pull to knit together broken activities and move data around the company faster and cheaper.

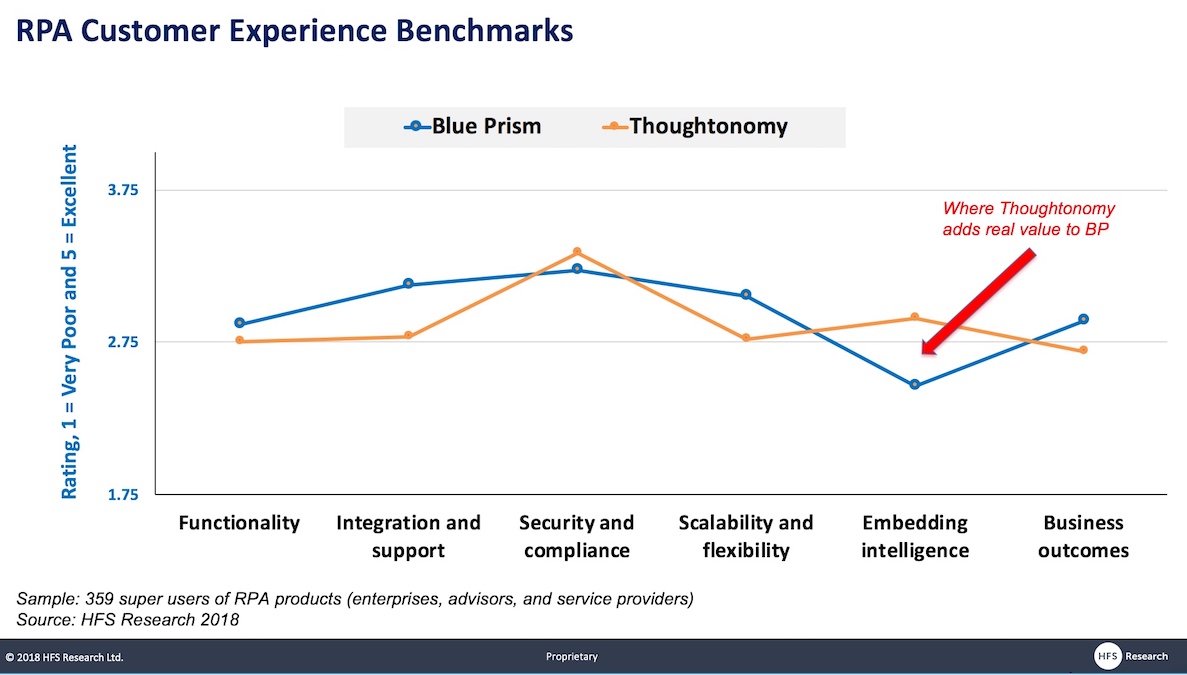

Blue Prism yesterday announced the acquisition of Thoughtonomy, a SaaS-based integrated automation platform with Blue Prism RPA baked into its core. After six years and much flirting with potential suitors, Terry Walby’s Thoughtonomy successfully exits into the welcoming arms of Blue Prism. This was always the logical end-game for Terry’s business, which he bootstrapped from day 1 and tirelessly pushed at the automation world. HFS was particularly inspired with the firm’s work at the UK’s National Health Service (NHS) (which you can read here).

Essentially Thoughtonomy is RPA + cognitive capabilities + cloud. Net-net, Blue Prism is buying a cloud (SaaS) wrapper for its own product; arguably, it could have (and should have) built that itself, but decided instead to pay a tidy sum. However, this cloud wrapper puts Blue Prism in the ring with Automation Anywhere’s V12 cloud product, which is drawing a lot of plaudits from enterprise users (our forthcoming Robotic Transformation Software Top Ten will reveal its performance across several hundred enterprises). More importantly, it increases Blue Prism’s attractiveness as an acquisition target itself by upgrading its cloud-readiness from “available cloud reference architecture” to a legitimate SaaS-based offering. We touted Blue Prism as a potential target for IBM three years ago, and with a scalable cloud story and IBM/s major pivot around Cloud with its RedHat acquisition, surely this Cloud-ifying of Blue Prism makes the firm even more attractive to them.

Finding the synergies to justify the price tag – cloud with a potential side of cognitive capabilities, but the focus is too UK centric

Now, Blue Prism can contend with Automation Anywhere’s claim that “BotFarm is the first and only enterprise-grade platform for scaling bots on demand”. The midmarket can benefit from Blue Prism’s RPA technology, with very little setup cost or initial investment. Mid size companies that considered automation out of their reach can enjoy the democratizing effects of cloud, avoiding the hassle of on prem infrastructure.

The shopping basket also contains Thoughtonomy’s gross assets, reported at 31 May 2018 as £5.6m and established relationships with Thoughtonomy’s big-name clients including NHS, AEGON, and Sony. Partner implementation and reseller arrangements are in place across many of the usual suspects in SI and consultancy such as Computacenter (from where Terry Walby moved to IPsoft before setting up Thoughtonomy).

Like Blue Prism, Thoughtonomy is UK based so there’s not much by way of additional footprint synergies to be realized. Blue Prism, therefore, will only be adding a limited new channel and will have to rely on its existing sales and delivery channel to make this acquisition pay off. The US market is where the bulk of new demand for automation solutions is surfacing, and Thoughtonomy isn’t adding to Blue Prism’s US team, which is under huge pressure from US-centric competitors with much larger pools of funding.

In HFS’ 2018 study of customer satisfaction with RPA, client ratings of Blue Prism and Thoughtonomy reveal some additional areas of complement – notably Thoughtonomy’s embedded intelligence (see Below). Blue Prism used some of the $130M it raised in January of 2019 to establish an AI lab to further the addition of cognitive capabilities to its product stack. Thoughtonomy now helps shorten R&D cycle time.

However, Thoughtonomy is small and not (yet) profitable and has never benefited from funding. For the twelve months to 30 April 2019, it reported revenues of £9.8m and an adjusted operating loss of £3.6m. It has suffered from the difficultly of being ahead of its time, offering a general purpose integrated automation tool as a service when most enterprises are still experimenting with RPA and other piecemeal automation solutions. Enterprises that have made the leap to integrated automation tend to be those that have both a clear digital transformation execution strategy and an informed perspective on which tools they need in their toolkit to achieve their objectives. Thoughtonomy offers a great integrated bundle, but, unless enterprises know what to do with it and what it helps them solve, it’s value will not be recognized. But, as we recently articulated in “RPA is Dead. Long Live Integrated Automation Platforms”, this is where the market is headed, so the potential is there.

Businesses and organizations ought to look beyond desktop automation to deeper integrated automation

It’s time for businesses of all sizes to begin their automation journey and going deeper is possible. As it’s cloud-based there’s no infrastructure capex, just the ongoing cloud opex. Furthermore, Thoughtonomy has, since its inception in 2013, had a strong view and vision on scaling its virtual workforce. Never intended as an attended or desktop solution, the plan was always to effect automation using Blue Prism’s RPA platform at a deeper level. Single automations can replace up to thousands of workers as opposed to the desktop automation route where automation is applied at the individual worker level and usually to tasks rather than processes or workflows.

Off-prem accessibility unquestionably matters, especially to the smaller business, what’s odd is that it’s not that difficult, time-consuming or expensive to build. However, with this acquisition, Blue Prism can now strike that off the list of things to do. Thoughtonomy currently has 54 employees, of which half are “dedicated to product-related activities”. Assuming the bulk of those are product development and not other ancillary product management or product marketing functions there is a team that has worked with Blue Prism’s platform in two ways that are of value:

Putting a cloud wrapper together around the RPA platform

Integrating it with AI services: Computer Vision, Natural Language Processing and Machine Learning

This technical knowledge is an important part of the value here, and it’s really hard in an acquisition to guarantee that talent below the C-suite stays in place post-acquisition, many leave and there’s not very much the acquiring company can do about it. With UiPath, Automation Anywhere and other key service providers all hunting aggressively for automation talent across both sales and technical areas, the merging entity will be vulnerable as they integrate the teams.

Consideration for the acquisition is mainly in shares – is this a brave gamble on both sides?

The payment terms of this deal comprise cash and ordinary shares. The initial cash payment of £12.5m on completion of the deal will be followed by a payment of £4.5m 18 months after completion. The remaining £63m is scheduled to be paid out at regular intervals up to two years post deal completion. The payment schedule for the deferred consideration for the acquisition includes a condition that Terry Walby and “relevant recipients” remain with Blue Prism.

With this purchase, Blue Prism is opening itself up to the scrutiny that goes with the process of acquisition at a point in time when it too is still loss-making, and its losses are deepening, increasing from £5.5m to £37.6m (IAS) in HY2019, despite revenues rising by a staggering 82% yoy. Presumably, Blue Prism must be confident of one of two things:

Delighting the stock markets sufficiently to raise more capital – and hypergrowth is in its favor here or

Being snapped up by a larger player that will ultimately pick up the tab

It would be more reassuring if Blue Prism had a clearer message and roadmap plotting out how this acquisition will help them grow and move into profit. But the share price drop suggests that the stock market is not yet impressed by this news.

The Bottom Line: Blue Prism’s end game is that it’s priming itself as an acquisition target; its market capitalization, currently in excess of £1b, is prohibitive for many would-be acquirers

The RPA landscape is at a peculiar point right now with three dominant players – Blue Prism Automation Anywhere, and UiPath – each with skyrocketing valuations which presents a stark contrast to enterprise confusion and difficulties in scaling. More worryingly, interspersed among the success stories, many stories of abject disappointment are quietly told.

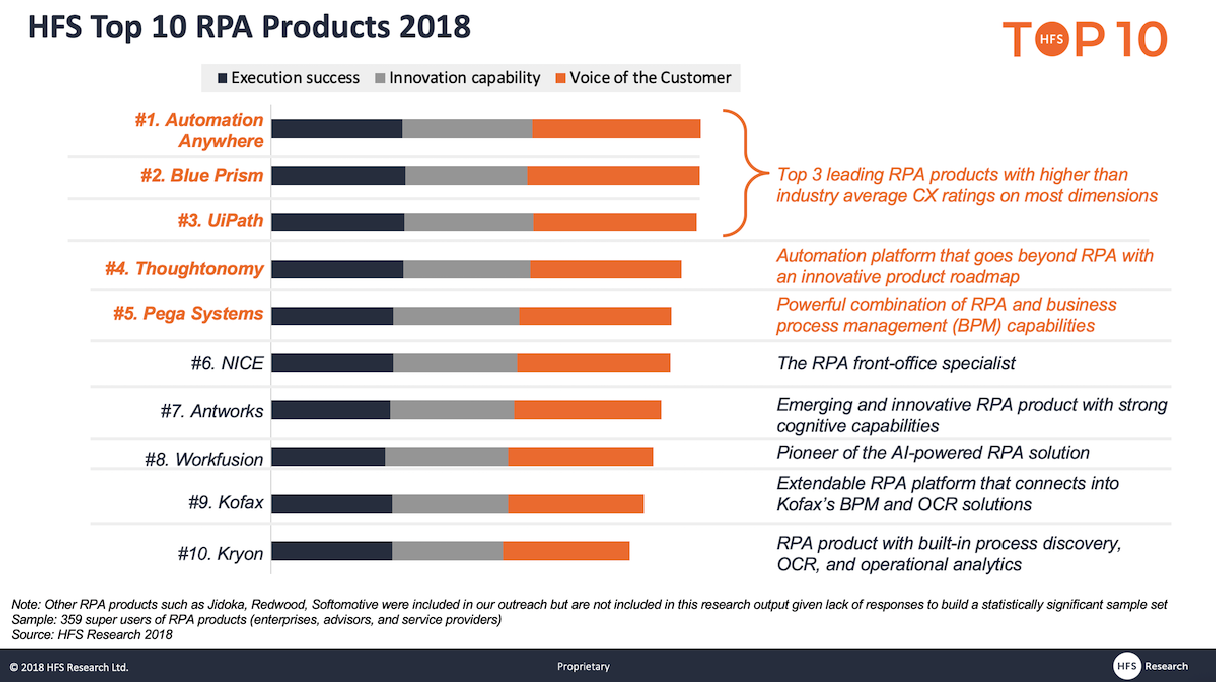

It sometimes looks as if the real product here is not necessarily RPA platforms, rather high growth companies striving to become unicorns, or to launch on the stock exchange or be bought for a tidy sum – and to be fair, if that’s what success looks like then Thoughtonomy has definitely made it. When the long tail of others outside the Big 3 in the RPA market is battling to get a strong foothold it’s difficult to compete for mindshare and revenues. Thoughtonomy was number four in HFS’s Top 10 RPA products 2018:

One strategy is worth pursuing; whether it was intentional from the outset or not, Thoughtonomy made use of Blue Prism’s platform in a way that is now so useful to Blue Prism, it’s finally making this purchase.

And as for Blue Prism in the longer term, some of its founders have already cashed in portions of their holdings, revenues are rising, it’s still in hypergrowth, but loss-making. But the stock market has high expectations and the requirements of publishing results mean the current deepening of losses is highly visible. The same could well be happening elsewhere, but we can’t see published numbers and the market is dominated more by private equity financing, as opposed to rocketing enterprise spending on the software and services. The current land-grab is taking place with an apparent absence of profit considerations – are we really just seeing growth at any cost?

HFS has previously speculated as far back as 2016 that IBM would or should buy Blue Prism. IBM is in the habit of buying competitors that appear to pose a threat and/or can significantly enhance its go-to-market strategy. While a price tag in the billions, as opposed to millions, would deter many, the $34b Red Hat acquisition last year demonstrates that IBM has no fear of big numbers. Right now, Watson isn’t being talked about as much as in the past and IBM uses Blue Prism extensively in intelligent automation solutions – is IBM happy to use, resell and create solutions from Blue Prism eggs or would it rather own the whole Blue Prism chicken?

We all remember when Jack Nicklaus played his last Masters, and when Sir Alex Ferguson managed his last game for Manchester United. These guys were godfathers of their trades, not unlike Azim Premji has been for IT services, the man who oversaw a firm which diversified from diapers and vegetable oil into one of the largest IT services firms in the world. However, when they retired, they left a legacy that enabled many to follow in their footsteps (albeit noone has come close yet). Premji’s legacy, which forever is written into the annals of IT services folklore, is still unfinished, which may be a good thing for his successors… there is still a lot of work to do to get Wipro to the place Premji always envisaged.

The current market situation facing Wipro’s leadership

To recap, Wipro’s Executive Chairman, Managing Director and philanthropic champion Azim Premji is retiring by end July. His son and Wipro’s Chief Strategy Officer, Rishad Premji will take over as the new executive chairman and its current CEO Abid Neemuchwala will become the new MD.

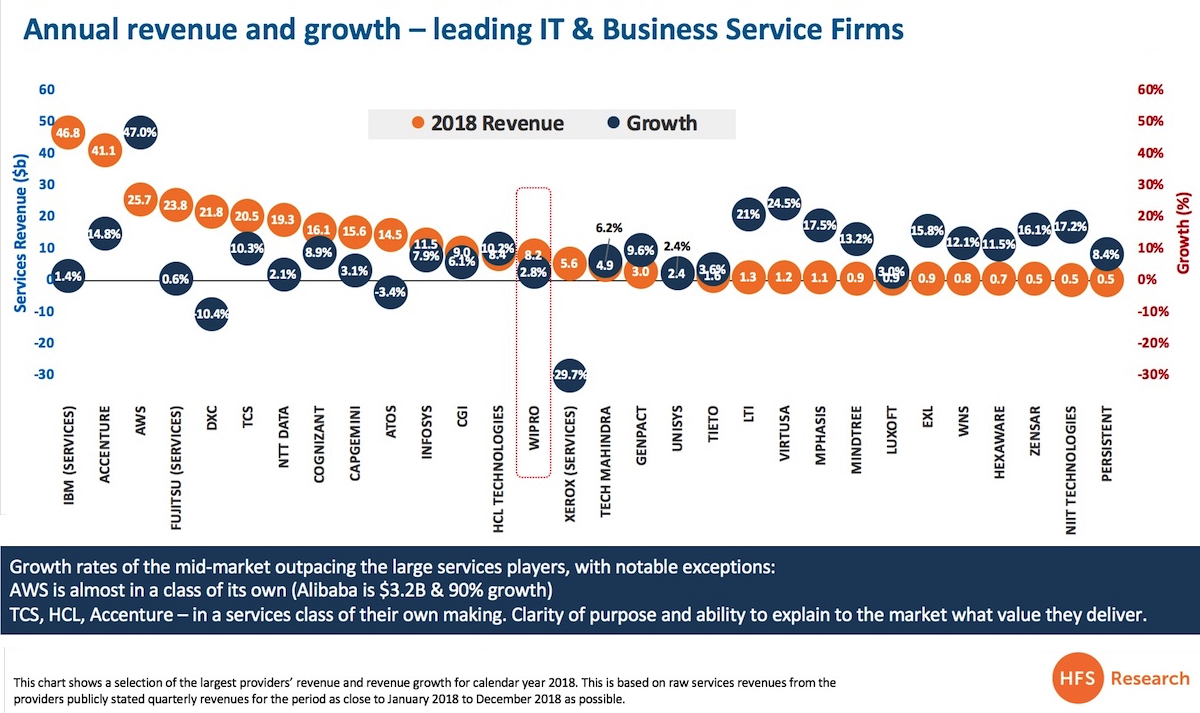

Azim Premji’s father founded Wipro in 1945, with Azim taking over in 1966 on his death. Azim led Wipro’s diversification into information technology in 1980. Today it has become one of the leading service providers in the industry and a big force within the India heritage IT service providers (lovingly called the TWITCH – TCS, Wipro, Infosys, Tech Mahindra, Cognizant, and HCL). However, Wipro has lost a bit of its cutting edge in the market. While its operating margins improved to 19.8% given the focus on the quality of revenues but overall revenue growth dropped to 2.8% YoY – the lowest growth rate of all the TWITCH service providers in 2018. It even lost its standing as the third biggest TWITCH supplier (albeit not permanently) last year to HCL.

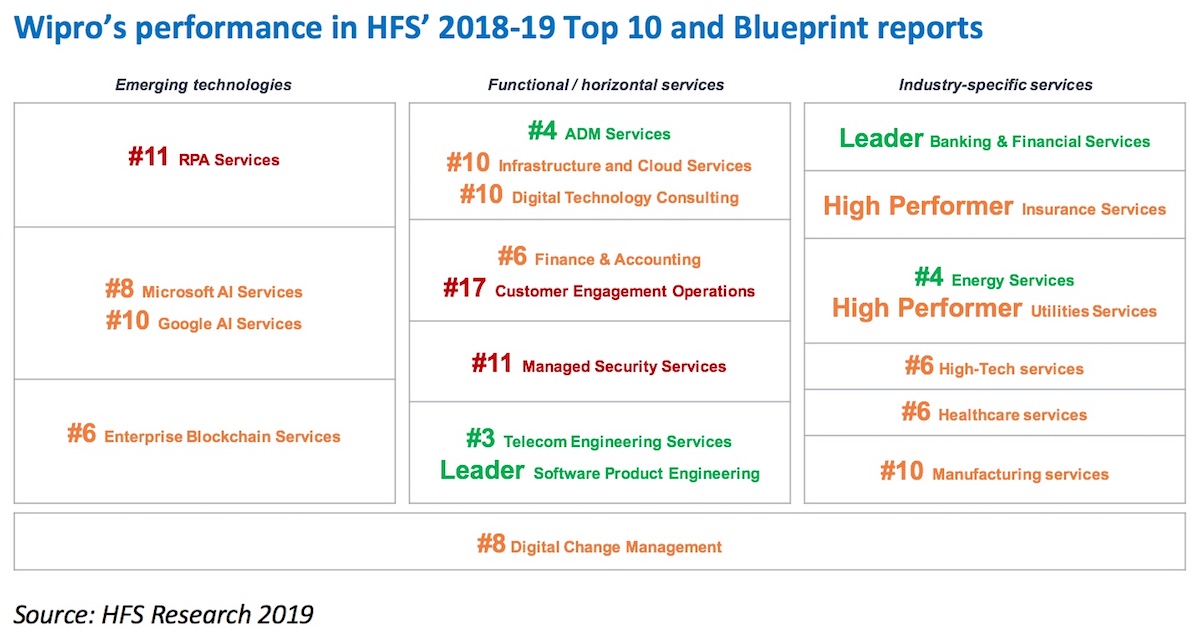

We’ve assessed Wipro’s competitive positioning across execution, innovation, and customer experience across major markets (see summary below) and while it mostly performs commendably (ranked #5-#10 in most of our evaluations), it misses out on the Top 5 positioning in most areas of our assessment.

Only 3 of the large IT Services firms with revenues higher than US$5B grew at over 10% in calendar 2018: Accenture (14.8%), TCS (10.3%) and HCL (10.2%), this excludes Amazon Web Services. All of these have an excellent service delivery, but the stand out factor is the ability to differentiate and know themselves and their strengths – which means they market services effectively and to the right customers:

We believe that the increased authority to the young and dynamic duo of Rishad and Abid to shape the overall business will be a boon to Wipro. Rishad has shown tremendous energy and passion for the business, especially with his recent development of Wipro Ventures, which is the most strategic innovation initiative for the firm. And Abid is a proven and seasoned leader. HFS continues to be impressed by his astuteness since his TCS days where he built a stellar BPO capability for the firm till just last year, where Abid was instrumental in getting Wipro’s largest ever engagement $1.6 billion multi-year TCV from Alight.

The Bottom-Line: The “What” is clear, now Wipro need to focus on “why” and “how.” HFS recommends five focus areas for the newly appointed executive chairman Rishad and CEO and MD Abid

Rishad and Abid already have a strong base to drive an aggressive growth and differentiation strategy. Wipro is a respected brand, offers large scale services with 160,000 employees across the globe, and brings capabilities across emerging technologies to its clients. The “What” in terms of its 4 stated big bets (digital, cloud, cybersecurity, and engineering) makes sense but the “Why Wipro” and “How it will help clients” needs better articulation of value and Wipro’s unique point of view. Here are the five areas that Rishad and Abid should focus on:

Competitive differentiation. Wipro needs to stand for something. Its recent financial results say that customers don’t understand what makes it different from all the other IT services firms – this lack of differentiation is not unique to Wipro and applies to several of its Indian-heritage competitors. If it is to thrive rather than survive, this needs to change.

Digital capabilities. Wipro has seemed two-speed since the acquisition of DesignIT. It needs to integrate the whole firm around its digital message – this means building out its offer and making a splash with some strategic M&A and client acquisitions. Success in the digital long term means helping customers change their DNA – not just providing new IT. Wipro’s digital message needs to demonstrate it can help customers find new revenue streams, new business model and drive customer experience as well as harmonizing business silos (or the One Office).

Change management. Digital is about enabling change – so to differentiate itself in the noisy and overcrowded digital space Wipro needs to focus on change management. It needs to demonstrate that it can manage complex change process that penetrates its clients the businesses and drives value beyond just digital adoption. Wipro’s narrative around “zero touch change” and agile cell teams is a good starting point, but it needs to embed change management in all its engagements. Rishad and Abid also have to change the internal culture and bring together all the business units and service lines to reduce internal frictions and improve internal collaboration.

Fresh talent. Injecting fresh blood and energy into the firm’s leadership, under the guidance of Abid will be important. Wipro has a credible track record of retraining ground staff as well leveraging the gig economy (courtesy of Topcoder) but needs to aggressively look at revitalizing its talent base, especially near to its clients. Service providers need to be able to draw on a broader range of skills – which means a richer mix of partnerships, on and offshore talent.

Integrated go-to-market. Wipro has a broad suite of capabilities across emerging technologies (Wipro Holmes AI platform, Wipro cloud services, an end-to-end IoT portfolio, and robust blockchain offering) but to differentiate itself it needs to create an integrated go-to-market across all these capabilities that solve real business problems. The strategic focus has to be on what clients want to buy versus the capabilities that it is selling. Co-innovation with its strategic clients, partnership ecosystem, and aggressively leveraging start-ups (through Wipro Ventures) will need to be core components of how it approaches the market. As one of the best application service providers, it is in a good position to help modernize these clients application portfolio as part of an integrated suite of digital capabilities focused on delivering business value.

Rishad and Abid have very large shoes to fill in with Azim Premji’s retirement, but it also represents a golden opportunity for Wipro to scale new heights. Rishad and Abid together bring the energy and a pulse on the changing market dynamics to transform the IT-services behemoth. We wish them and Wipro all the very best!

When you have to listen to literally hundreds of people a day spouting advice about reskilling, unlearning, change management, relearning etc., I am going to respond with “great, so what are you doing yourself to stay ahead of today’s digital environment and increase your value as a superstar worker?” You may love to pontificate constantly weird definitions of digital transformation on twitter and harp on about today’s digital talent needs, but do you truly practice what you preach?

Is it just me, or have we entered an environment where everyone loves to talk about change, but most aren’t actually doing anything (themselves) about it?

I mean, if your accountant hadn’t bothered to brush up on the latest tax changes, or your personal trainer didn’t know how to use a Fitbit, you probably would seek to replace those relationships in your life. So what gives IT professionals the right not to learn Python, or learn how to deploy data management / automation tools? And what gives business executives the right not to learn how to use non-code analytics tools to help their decision-making, or social media products to help them communicate in the market? And operations executives the right not to learn low-code automation and AI apps that can help them free up people-hours on work that adds no strategic value to the business? And who told sales and marketing executives it was fine to ignore really learning the products / services they were selling because all they had to do was to follow a set of pre-defined processes to do their job effectively?

Why have so many of us become so complacent?

It just seems that the majority of workers today just think they need to learn to follow a few processes and that’s all they need to do to command a tasty salary and remain employed for years and years…. so few people actually realize that the whole nature of people value is changing for enterprises – they just love to do things the same old way they have always done them, and simply cannot be expected to learning anything new. “We just don’t have the talent in-house to do that” is the constant whine we hear from enterprises; and “our IT managers are project managers, not consultants” is what we hear from service providers. Then why don’t you train them? Is our agonized response. Why does everything have to stay paralyzed in this constant vacuum of sameness?

Much depends on the approach our enterprises take to driving change

The biggest problem with enterprise operations today is the simple fact that most firms still run most of their processes exactly the same way as they did decades years ago, with the only “innovation” being models like offshore outsourcing and shared service centers, cloud and digital technologies enabling those same processes to be conducted steadily faster and cheaper. However, fundamental changes have not been made to intrinsic business processes – most companies still operate with their major functions such as procurement, customer service, marketing, finance, HR and supply chain operating in individual silos, with IT operating as a non-strategic vehicle to maintain the status quo and keep the lights on.

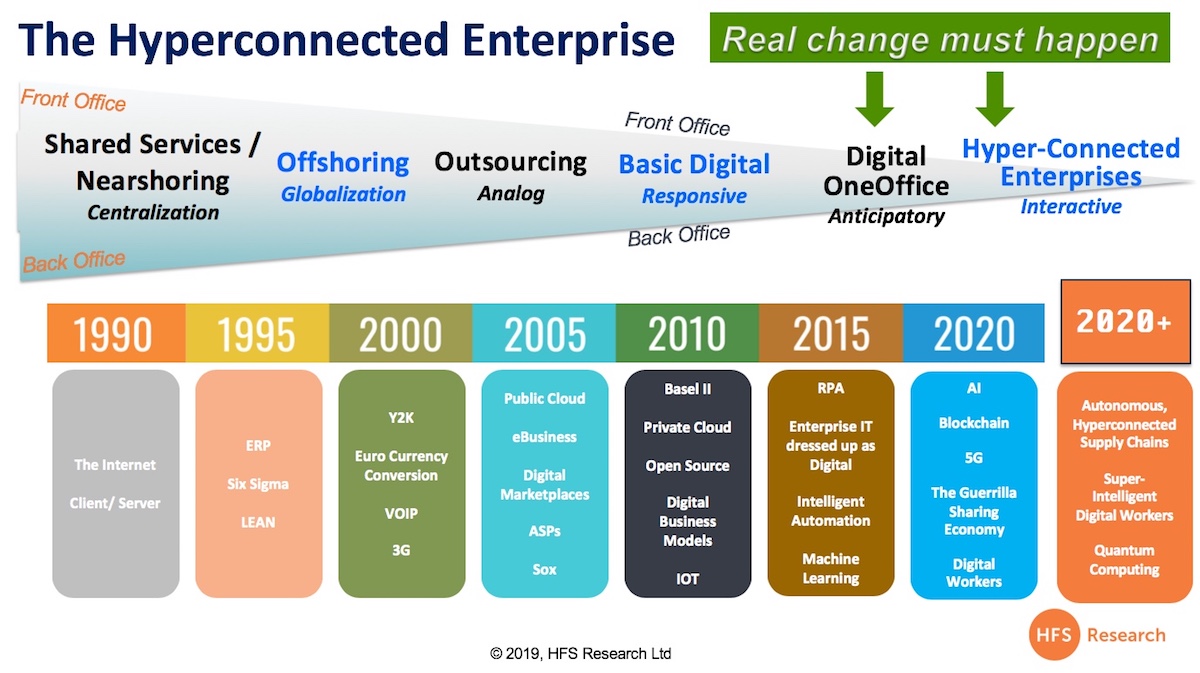

As our Hyperconnected journey illustrates, many industries have now reached a place where they have maximized all their delivery methods for getting processes executed as efficiently and cheaply as possible. They have tackled the early phases of digital impact by embracing interactive technologies to help them respond to their customer needs as those needs occur, whether electronic or voice.

In short, most enterprises have been able to keep pace with each other without actually changing the underlying logic of processes. Simply doing things the same old way has been enough for many, until a competitor comes along with an entirely unique way of servicing your customers to shrink your market share or take you out of the game completely. We are already in the OneOffice phase where wrapping the needs of our customers around our front-to-back office business processes is critical. And you can’t do that simply by adding more software and bot lisences to stitch together wonky systems and processes – you actually have to redesign how processes work so you can outthink your competitors. Simply reacting to customer demand won’t work these days, you have to be able to anticipate and think ahead, try to predict how their needs will change even before they do. This means you need systems in place to mine information up and down your supply chains, B2B networks and understand today’s geo-political environments – and you need smart people who can think creatively to drive these systems for you.

So why can’t you get away with avoiding learning new ways of doing your job? Can’t you just find another legacy firm who’s desperate enough to hire you?

In many cases, the answer is still “yes”, especially while the economy is good. You can still serve up some BS in interview and convince another firm that you are still special, that a few utterances of “digital” and “AI” may be enough to convince them you are of the “new age”. Yes, you can spin your 2 hour online Blue Prism course learnings to convince them you can take your new firm on a special journey.

But if you are looking closely at your LI network these days, you will notice that many people who are taking on these “new” jobs aren’t lasting very long in them. We are living in an age where you can’t just get away with faking your skills and relying on a wafer-thin knowledge level… you need to really learn how to rewire business processes to compete with the best in your industry, and do that you have to drive change initiatives. This means you need to make yourself emotionally intelligent and understand how emerging low-code/no-code technology tools can help you make these underlying changes to age-old processes.

Time to influence strategy: A Lack of resources we can handle, but a lack of vision and being tied down with short-termist strategies are much harder to push passed

It’s not much of a consolation to know it’s not all your fault that your professional value is in decline. A recent study conducted by the World Economic Forum, presented an unconvincing picture of barriers to change. The research is sound – with over 100 major firms providing insights within each major industry sector – but the excuses provided by executives for hitting roadblocks comes across as a little suspect. In the first graph, we can see that old chestnut of resource constraints rears its head as usual. Let’s be honest, we can’t keep whimpering about funds and resources when it comes to change efforts – executives always manage to find money when something new and shiny crops up (lock at the clamour for blockchain POCs a few years ago, and the more recent rabid adoption of AI without really knowing what it is). And if executives honestly think their biggest barrier to change is that they can’t buy their way through it, that tells us everything about their relative maturity in a rapidly changing business environment.

In reality, it’s this lack of maturity and understanding in senior management teams that’s the real barrier – and it’s one highlighted by 51% of leaders. Leaders simply don’t know where the change is coming from, and what direction they need to shepherd their teams. Package that with the likelihood that at root of their enterprise’s strategy is sits cultural short-termism – driven by short-tenured C-level and increasingly active shareholders looking to force returns in a low-interest economy. In a business environment like this, you simply can’t reply on your leadership team to have the answers – and provide you with the direction you need to keep adding value and collecting that pay cheque. So, you must take on that responsibility yourself – the future of the digital employee is one of perpetual learning and evolution.

All we can tell you, is in certain professions and industries, you’ll need to rouse yourselves from your professional slumber much sooner than others. In the graph below, we can see major crunch points in ICT and Financial services, for example, where a combination of resource constraints and an all-round pitiful understanding of disruption from executives mean your only professional direction can come from within.

The Bottom-Line: We have to get out of these silos and learn how to drive change initiatives and develop cross-functional skills

Let’s face it, change is coming, and it will keep coming. And we can’t rely on anyone but ourselves to find the right balance of skills and experience to keep adding value. We are lucky to live at a time where we have a multitude of established and emerging change agents at our disposal: global sourcing, Design Thinking, Robotic Transformation Software, AI, Analytics, IoT, blockchain among others. But, unfortunately, most of the discussions in the market end up becoming a comparative discussion versus an integrative discussion – man versus machine, offshore versus automation, RPA versus AI, consulting versus execution, and so on. These change agents must work together rather than operate in silos to solve real business problems.

In Part II of this talent discussion, we will drill into the WEF skills data to align this with actionable steps we can all take to get us back on a cycle of ongoing learning and development:

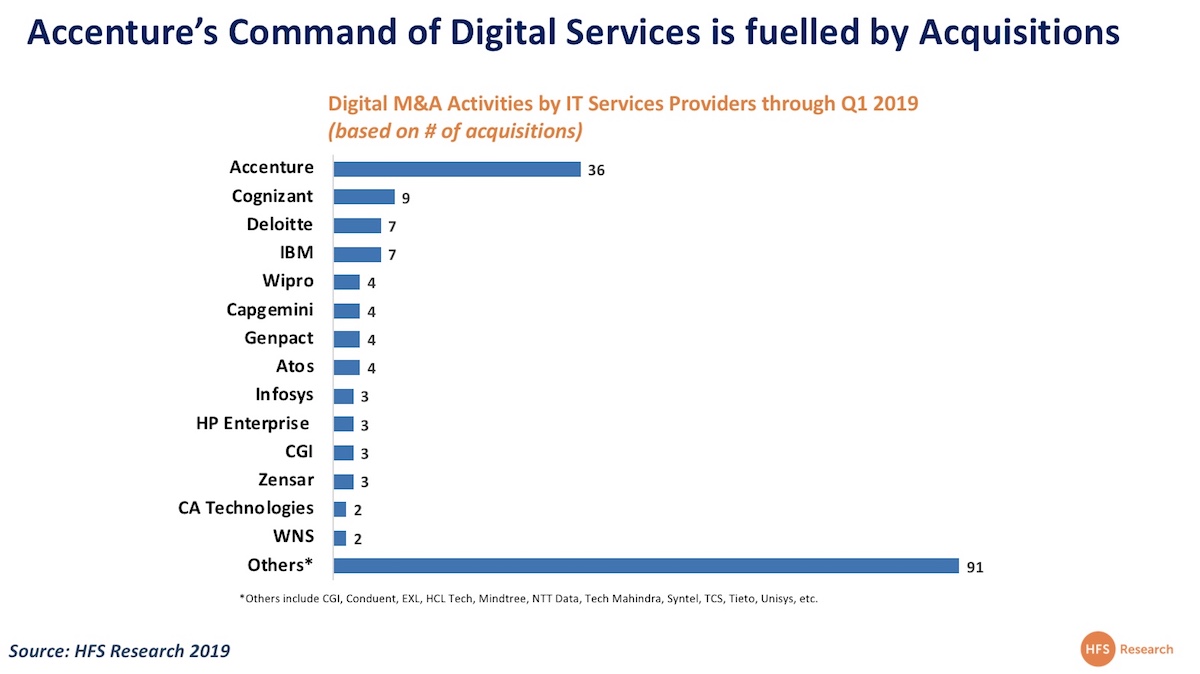

What has happened to the Indian-heritage IT service provider that stoked fear into every Accenture client partner? “They think like we do” was the declaration one of Accenture’s leaders made at an analyst briefing in 2016. Well, the slide from grace has been alarming, leading to the appointment of a new leader to stem the bleeding.

However, when the problems cut this deep, you can’t just apply lipstick to the pig, you need to reconstruct the whole farm, or you can quickly find yourself in the zombie services category alongside the likes of Conduent and DXC, where finding any sort of direction and impetus would be a major accomplishment.

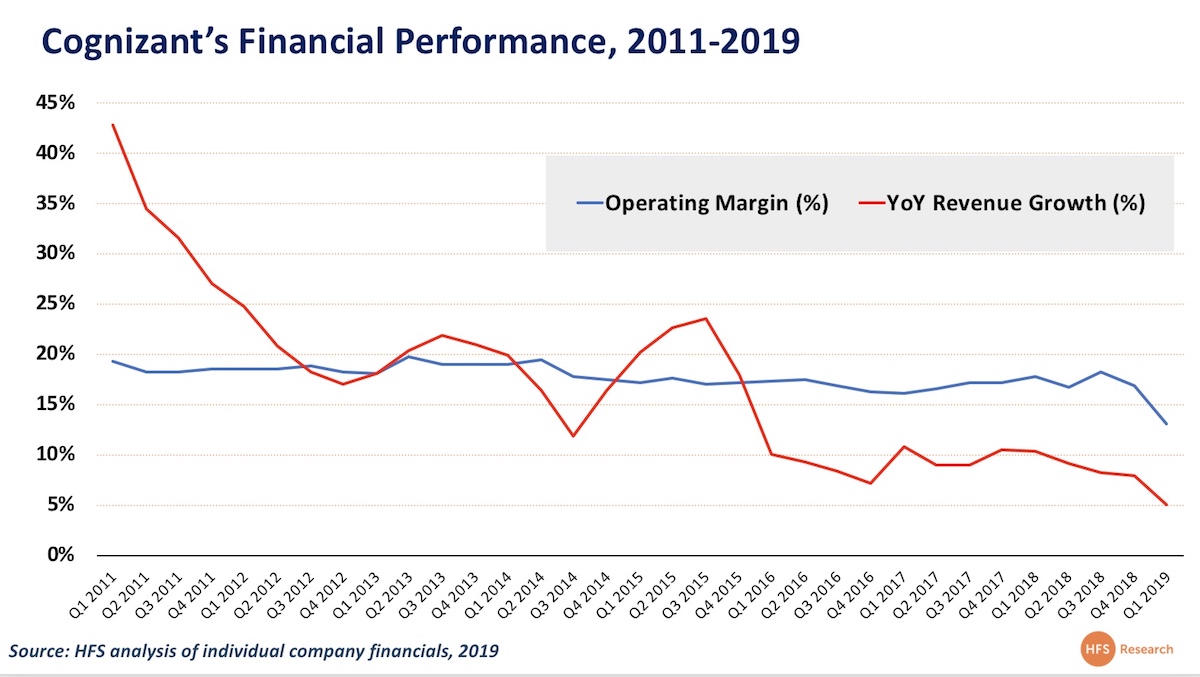

Yes, it could really get this bad, as Cognizant has posted its slowest revenue growth and worst dip in profit margins. Ever. A mere 5% annual revenue growth, when in its heyday it was posting well over 40% (and slipping below double digits was unthinkable until last year). Yes, declining revenue growth is one thing, but declining profit margins is when the panic button gets pressed.

Frank should have left when Elliott came along to poison the well

It’s clear to see why Francisco “Frank” De Souza, the poster boy CEO of the emerging power of the Indian IT Services industry, jumped ship (or more accurately was made to walk the plank a burnt out husk due to the unenviable pressure Elliott Management placed him under to keep the gravy train on the tracks and kick back billions to shareholders.) If anything, Frank should have considered making a move in 2017 as Elliott started squeezing Cognizant’s margins at a time is needed to keep pace with Accenture’s aggressive digital investments. He’d grown the firm to over $15bn by then and could have exited with a legacy no one could rival in the tech business.

And in his place comes IT Services newbie Brian Humphries – well we’re sorry to say this Brian, but the baby you just adopted has got a bit ugly, and is screaming for attention. Let’s just look at the numbers– now we’re going to be generous and forgive Cognizant’s dip in margin, a likely result of a reclassifying activity to meet fresh regulations. But the sinking revenue growth is much harder to look past:

In 2012, Cognizant invented the Digital concept before everyone else jumped on it. They were that cool…

In a punishingly competitive market, it looks like Cognizant has started to lose traction. Back in the good old days, the firm could do little wrong by challenging Accenture’s strategy – driving a hard-digital bargain and bringing in design consultancies along with their pony-tailed nose-ringed jean wearing creatives. In fact, Cognizant can genuinely lay claim to “inventing” digital with its 2012 “SMAC” stack philosophy, which was swiftly followed by Accenture’s 2013 re-branding the SMAC stack as “digital”.

But the market has moved on – away from automation point solutions and funky apps to fend off uberized rivals. It’s now about integrating capabilities and meeting clients with legitimate flexibility, a real willingness to find out what they want to buy, rather than keep pestering them with siloed offerings and poorly verticalized capabilities.

Somewhere in all this noise, India’s rising star lost its way. And, honestly, the hassle of a new leadership team is unlikely to make matters any easier to drag this tired giant back from the ropes to get them punching again.

Is now the right time for Brian to go on a cull? Crush a culture, or fix what isn’t that broken?

Changing a culture overnight is a gargantuan task in a firm that has been steeped in it for two decades – just look at Vishal Sikka’s attempts at Infosys, where the guy couldn’t charter a jet without all hell breaking loose. However, you can instill a new urgency (and a little healthy fear) which is more likely where Brian is heading with all this.

Realistically, we can’t be too tough on Cog’s new CEO – let’s face it the guy is barely in the door and the actions and initiatives behind these disappointing results were already in place before he took over the reins. But the stories we’re getting from insiders familiar with recent goings on paints a harrowing picture. We’re already seeing cuts being made and senior, albeit expensive, executives shown the door (and self-selected to take a package and quit), as the fresh CEO starts pushing for costs savings – but is this the right strategy? Maybe this is more about fixing a machine that just needs a significant tune-up – it’s working well with Salil Parekh at Infosys, where the firm needed renewed urgency, as opposed to open-heart surgery, to find a better direction for itself.

Anyone who plays in this space knows it’s not for the faint-hearted, but with major talent wars popping out across the industry, it doesn’t seem like axing staff and business units is the most prudent course of action – even with revenues in decline. And pushing for lower costs will do little to differentiate the firm from an already cluttered space packed with purveyors of low-cost offshoring.

The keys to victory are to be found moving up the value chain, not down it

Anyone who things they can “out-Walmart TCS” or “out-price HCL” needs a lobotomy. The reality is that Cognizant has little option but to loosen the purse strings – rather than tighten them – and bring in some real consulting and digital capability. It’s been a long time since the acquisition of cool kids Idea Couture, and even then this group was hardly big enough to make waves across the organization. To make a difference and reverse its decline, Cog needs to make some major investments – bringing in a BCG or Bain-sized consulting group wouldn’t see them too far wrong. They’ve actually shown more focus in digital than it’s India-heritage rivals, so it’s not too late to reboot this strategy, especially if it hands some war-chest to Malcolm Frank:

And perhaps that’s the plan all along, make savings now to open up opportunities for investments later. This may keep the accountants happy, but it does little to help the perception of a firm in decline – which in a market where the financial stability of partners is moving further up the priority list is a major concern.

What do we think of the new CEO?

But all of this isn’t to say we’ve taken an immediate disliking to poor Brian – far from it. He’s barely through the door, what we’re conscious of is there’s now a huge to-do list for an executive relatively new to the space to pull off.

When we’re asked what we think of the new CEO, our honest answer is we don’t know. He has, for all intents and purposes, kept a low profile externally, instead focusing his energies on extensive liposuction internally. But there are some concerns. First off, try to follow Brian on twitter – tried it? That’s right his account is locked down as “private”. Now this may seem innocuous enough but for the CEO of a major IT Services player it’s a big no-no.

We’ve been talking for a long time about the power of the CEO as a front-person for the firm. Take a look at Tiger at Genpact, CVK at HCL, Caldwell at Concentrix or even Ginni at IBM – they are their own firms’ evangelists – and in an over-hyped complex space, clients are desperate for that clarity.

If Brian’s not even confident that he can tweet without upsetting clients, employees and analysts to the extent he keeps his account locked down, there may be little hope of him taking to the stage to push the virtues of services. But we guess we’ll have to wait and see.

Bottom-line: Let’s give Brian a hand with a to-do list if he wants to right the direction of the Cognizant ship

Investments: Cognizant has been starved of major investments for years, ever since activist investor Elliot Management came in and held a gun to Frank’s head demanding billions in shareholder kickbacks. Elliot’s gone now and Brian should be using his fresh perspective and enthusiasm to home in on acquisition targets in the market to bring in the capabilities the firm really needs to differentiate itself. It’s 2014 $2.7bn splash on healthcare platform TriZetto is long in the distant past (and sadly healthcare probably wasn’t the best bet for the firm when we look at the sorry state of that industry today). Brian needs to look at key industries, such as banking, and key capability areas, such as further expansion of digital marketing, so get Cognizant back on track.

Talent: By the sounds of it Brian is moving through the organization with a scythe at the ready whenever a potential cut can be made. In some instances, this may be right, but we’re already hearing of talented professionals and executives getting ready to jump before the blade comes swinging round to them. We’re in a people business – and if all the best professionals jump ship, and they will, then Brian may find himself sitting alone in the boardroom desperately trying to figure out his AIs from his RPAs.

Perception: With the departure of Frank, and a crushing first quarter under Brian, there will be myriad perception battles to fight. Brian might want to start by stepping in to reassure the crew – and then it’s time to let current and future clients what the plan is – because right now, none of us have a clue.

Marketing: Finally, all the time Cognizant’s future is up in the air, its rivals are busily chomping into the limited mindshare bandwidth. Brian needs to push out a clear marketing message that lays out their differentiators and roadmap, if he’s to reverse the decline of one of the sectors most promising companies.

Mojo: Find it – and fast. Today’s market is harder than ever to build momentum, and bludgeoning people over the head with a blunt instrument is really the only way to get out in front. So find the right message, stick to it, and batter it home. There is no room for dithering anymore – and many may already think it is too late to rebound, but Cognizant’s position is way, way healthier than a Conduent or a DXC, and can quickly find its way back to the top if it stays laser-focused, makes some significant eye-opening investments and brings a fresh message to the market that defines what it stands for.

We’ve been pretty vocal regarding the unfocused direction the industry which has called itself “RPA” has taken, and the obsession some of the firms are having with their self-declared valuations. So let’s change the story from how much these firms actually believe they are worth to where they need to invest their funding to show they are serious about being part of a transformative industry.

Don’t get us wrong, in software world, it’s common practice to get attention that your company is valuable and investors are falling over themselves to hurl money at it – this is common practice in markets that are very focused on selling to IT executives. And we’ve seen far more ludicrous “valuations” than the 35x earnings ones the robotic software firms are claiming (just look at Blockchain and AI).

So why aren’t we seeing firms like UiPath shift the focus to the investments and changes they intend to make to propel a truly transformational value proposition with their products? Especially where the prime target for growth is the business executive who is far less accustomed to a world where his/her suppliers are obsessed with how much they’re worth, as opposed to how they can help you take your business through painful change.

It’s critical now to shift the vision to reality of making these bot dreams come true

UiPath, more than its competitors, has always pushed the vision of democratized IT. Literally, RPA or a “bot for every worker” and not just a sanctioned crew of IT professionals (or even a sanctioned crew of enterprises) is a brilliant marketing gimmick. However, with UiPath’s hypergrowth and rapid-fire funding, the time has come to connect the dots between a folksy vision and how UiPath can truly enable the transformation of work.

As HFS recently articulated in our blog “RPA is dead. Long live integrated automation platforms”, RPA is being used to automate tasks and prop up legacy processes. Broad business transformation is decidedly lacking and arguably cannot be achieved without supporting tools like artificial intelligence and analytics as well as digital change management to address how change is driven, managed and perpetuated. The one perhaps notable shift in the change winds is the on the democratization front – RPA is being bought and consumed primarily by business units not central IT. However, as enterprises push towards integrated automation, with a higher order of technical complexity of tools and data challenges, IT once again becomes essential. Integrated automation may drive the ultimate democratization – the balance between IT and business operations.

Despite its growth and funding, UiPath is a very long way from achieving this vision

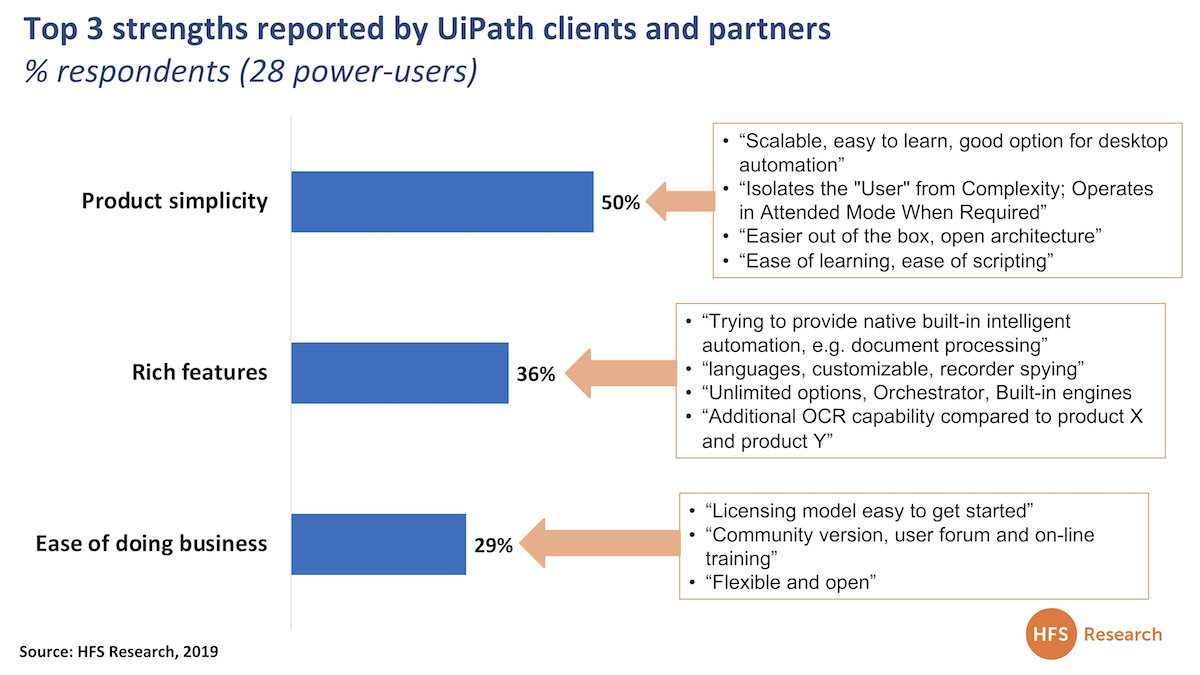

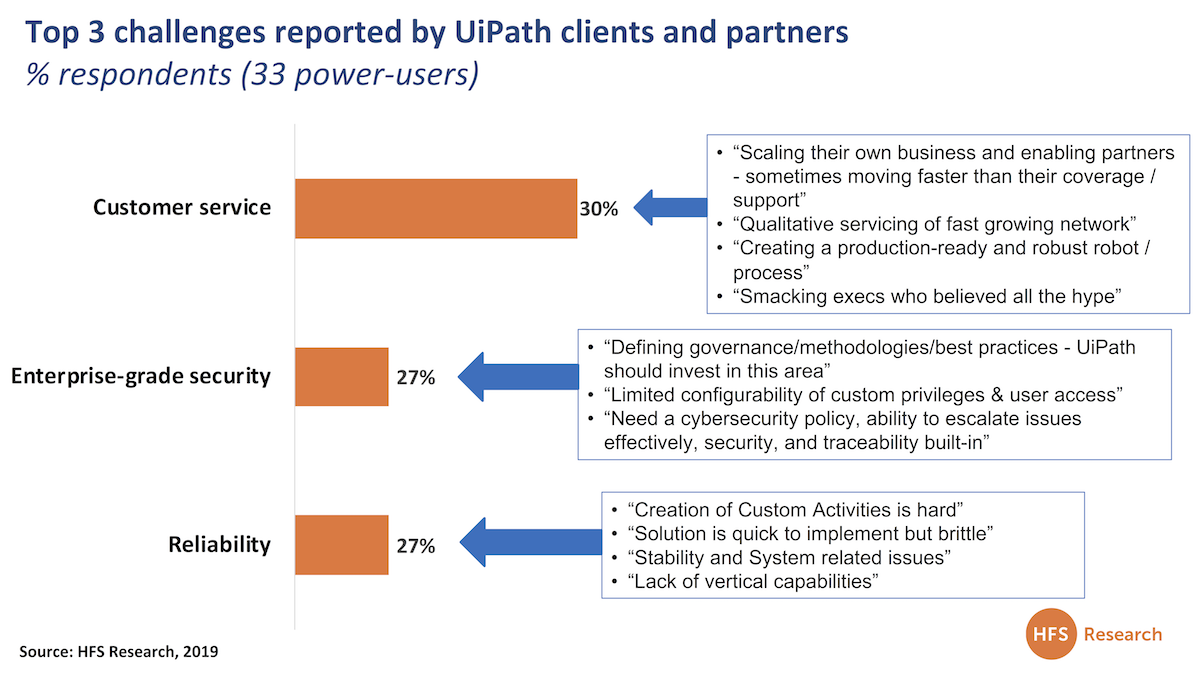

Our recent survey work with “power-users” of robotic software products (what we were calling RPA and RDA) clearly highlights the top three strengths and challenges of the UiPath solution (with sampled comments):

The Bottom-line: To democratize technology and drive business transformation beyond task-oriented robotics activities, here are 15 key initiatives UiPath (or its competitors) must take on:

1. Must bring IT and business visions together as one integrated approach. Education must focus for technical and non-technical resources – into communities and educational institutions globally

2. Must shift focus to integrated automation – expansion of functionality beyond RPA/RDA to AI and smart analytics. Badging everything as RPA is definitionally incorrect and gives clients no roadmap to follow to advance beyond basic repetitive task, desktop and document automation

3. Must drive digital change management – help enterprises grapple with transformation with its services investments. Relying purely on Big 4 advisors and service providers for change management will cost clients a fortune and drive many away. This is a key area UiPath needs to take the lead on.

4. Must include unattended and attended processes (not just focus on attended)

5. The developer ecosystem must be expanded to extend functionality, libraries etc. Commit to specific goals for how much of the UiPath codebase will be available on Github to build an industry solution skewed against technology-vendor lock-in

6. Demonstrate commitment to building a stronger QA team, and fully transparent local customer support and customer success teams to drive customers (as per the number 1 challenge outlined above)

7. Commit specific sums to meaningful partner relationships with leading service providers and consultants, including opensource partner technical support systems, events, education resources and people to help the industry grow

8. Commit to funding UiPath local academies (building on their online academies) especially in blighted neighborhoods near its biggest offices to bring young coders and potential customers together with UiPath employees for on the job real-world training