Three of the original RPA pioneers (left to right): Some grinning idiot, Pat Geary (Chief Market Maker, Blue Prism) and Jason Kingdon (returning as Executive Chairman of Blue Prism)

So almost exactly seven years to the day that RPA was invented, Blue Prism’s major shareholder Jason Kingdon has scratched a huge robotic itch to make a return to active duty leading Blue Prism to drive its AI roadmap as RPA prepares for its rebirth in the industry. Current CEO Alastair Bathgate (interviewed here), who has overseen the IPO and evolution of the firm in recent years, stays on as CEO, but Jason will be driving much of the technology roadmap and vision with Alastair more focused on the business side.

Jason has a PhD in AI from University College London (UCL) and has been commercializing AI for over 25 years. He was co-founder of the Intelligent System Lab at UCL and Searchspace where he was CEO between 1993 and until its highly successful exit in 2005, when he sold the business to US private equity.

Blue Prism must now grasp these three critical challenges and opportunities

1) Carefully position itself in the industry as the heritage RPA inventor now taking the industry into a new AI-driven phase. While AA and UiPath have been publicly biting chunks out of each other, Blue Prism has soldiered on with its business with minimal noise and hype. In fact, the reverberations from Las Vegas and New York only help drive more attention to the industry and Blue Prism hopes to capitalize… not dissimilar to the amazing work IBM Watson did creating an AI industry for everyone.

2) Roll out a technology roadmap that takes RPA into the AI era. While both its competitors have focused on what Blue Prism calls an “RPA butler service”, proving bots for everyone’s’ desktops, Blue Prism wants to focus on its years of heritage RPA experience managing robots and aligning them with AI capabilities to make them self-remediating and aligned with transformative process roadmaps for its clients.

3) Recreate market energy around itself and its technology roadmap. In typically British fashion, Blue Prism has ignored the noise generated for its high-impact competitors, but now needs to come back aggressively into the market with a laser-focused technology roadmap that is unique to clients and aligned with their deep-set needs.

Bottom-line: This is a marathon, not a sprint and Blue Prism has every chance to reaffirm its former leadership position

Blue Prism did UiPath and AA a huge favor by going public when it did a few years ago, as it exposed the challenges of having its activities open to public scrutiny. However, Blue Prism, under Bathgate’s stewardship, has survived it well to be in a position to make critical investments in its platform that many of its large client base will be delighted to embrace. While its competitors will continue to toy with IPOs and increased private investment, Kingdon and Bathgate now have the luxury of greater certainty with clients and their respect as the original pioneer of low-code technology for business operations professionals. Having Kingdon’s impressive technology passion and prowess at the helm will significantly benefit Blue Prism’s standing in the market and help propel the firm’s offering into the AI era…

Did you hear the one about the GE finance captive spinoff which ended up as a Top 6 AI Services firm before making a bold move into the front office with the acquisition of the respected Right Point Group? And did you hear it broke into the world of digital service capability without ever succumbing to the delights of acquiring an IT services shop? Welcome to Genpact, folks, the former BPO firm which has been breaking the mold of business services for the past two decades.

This is a serious digital acquisition that brings Genpact right into the customer paradigm

Genpact has been slowly but steadily building thought leadership and capabilities around “experience innovation” over the last few years. Genpact’s 2017 acquisition of Design Thinking consulting firm TandemSeven was its first demonstration of the firm’s appetite to develop a OneOffice capability, aiming to move beyond its back office roots and help its clients develop more holistic experiences. It has now announced an agreement to acquire digital consultancy Rightpoint, with a focus on digital transformation, with capabilities for CX, commerce, and mobile application development.

A highlight of the acquisition and one of Rightpoint’s most distinctive features is its expertise for designing and implementing digital workplaces – its work with Aon, for example, demonstrates Rightpoint’s capability to reimagine the workplace. This is such an important element that many companies need help with, as they struggle to connect experiences across the organization and align to the customer.

While TandemSeven gave the firm a flavoring of customer experience design, the sheer size and scale and depth digital tech implementation across North America puts Genpact right on the digital map, with a unique value proposition of leading with process transformation, enabled by AI and digital capability where we can expect a significant jump from its current position, which we assessed earlier this year in our 2019 Design, Sales and Marketing Services Top Ten report. Genpact landed at #14 in the rankings, largely as it just begun developing thought leadership for front office focused offerings and mindshare has been relatively low on our Voice of the Customer rankings. The Rightpoint acquisition is a step in the right direction to move up the value chain – particularly as it can bring in its strong capabilities around data and analytics to fuel the digital transformation roadmaps for its clients.

Genpact will not force its culture onto Right Point as it learns from the Accenture play-book

We view this as the most exciting acquisition yet by Genpact, as it signifies the direction the firm is taking as a process designer, executor and engineer enabled by supporting digital and AI technology. We also see this as one of the most genuine OneOffice investments made by a (predominantly) middle/back office service firm to unify and front-to-back “OneOffice” offering. While we have seen contact center firms such a Concentrix acquire Tigerspike, and Sutherland partner with Google, there have been few moves from traditional BPOs to bring together front and back office delivery with real technology enablement.Other front-to-back moves in the business process space have also been WNS quietly beefing up its call center capabilities in South Africa, Teleperformance’s acquisition of Intelenet and InfosysBPM’s recent pick up of Irish call center Eishtec.

The challenge will be integrating Right Point into Genpact mothership, and keeping it as a separate entity reporting to Ahmed Mazhari (Chief Growth Officer) as opposed to attempting to force a quicker integration into Sanjay Srivastava’s Digital organization tells us that Genpact is keen to retain the culture of Right Point in the initial phases and not force Genpact’s culture onto Right Point’s people. This is more from the Accenture playbook of 36 digital acquisitions to-date, where they learned quickly not to Accenturize these creative firms too quickly.

The Bottom-line: business process service providers failing to invest in digitizing their capabilities across front-to-back offices are in a race to the bottom

The message to today’s business process services firms is simple – you’re dealing with the institutional processes of the world’s biggest businesses. Help align them with the needs of their customers and you will win. Stay doing the same old legacy processing and you’re probably toast in a couple more years.

Believe it or not, if you’re helping clients manage their processes and data, you’re right where you need to be… but you need to develop or acquire the expertise to help them get where they want to go. That means you need to help them design, digitize, automate and self-remediate their processes to stay ahead of their customer needs, as they simply cannot survive treading water in today’s environment. As we recently pointed out, 75% of enterprises will demand significant changes to their services partnerships when they next evaluate their contracts. So providers thinking most of their clients will tolerate them not making significant investments in delivering digital services are going to be in serious trouble (and some are and are fast realizing it).

Well what a week that was in the world that is automation software… while 11 automation leaders at the HFS New York Summit pretty much all agreed that the world that was called RPA is stuck in the mire of making legacy tasks work better, we then were treated to Automation Anywhere’s launch of its new platform upgrade A2019 right afterward at the Nasdaq center, where CEO Mihir Shukla declared he wanted a “Digital Assistant for Every Worker”. A2019 claims its ease-of-use in the cloud, its new plug-ins into Microsoft Word and Excel, and its ability to be run from a mobile device make it the best task support tool in the business. Oh, the timing! Will UiPath stay safe with its status as the “developers favorite”, will Blue Prism stay true to its “friend of the business pro”, or will AA’s focus on bridging a solution for both business and IT with the day?

So all eyes now turn to UiPath’s flagship Forward III event in Vegas next week, where CEO Daniel Dines and his team are under intense pressure to drive an even more powerful narrative for the industry to keep itself at the forefront of robotic software. The onus is on the UiPath leadership, more than ever, to seize the initiative, especially as their noisy competitors are unlikely to keep the brakes off the PR Newswire next week… (Oh and HFS mega analyst Elena Christopher is there speaking, who co-authored the now-infamous “RPA is Dead, Long Live Intelligent Automation” blog. And Kudos to the UiPath folks for having the courage to bring in an untethered analyst viewpoint after some of the recent utter mush we’ve been subjected to at these things. Oh and a woman too, thank God!

Here are the 25 key tenets where UiPath, AA and Blue Prism must draw battle as they look to cross that chasm from RPA to a true digital workforce

Consultants, fellow analysts, here’s everything you need to advise your clients… steal away as HFS is just giving it allll away….

1. Stop counting customers. Start counting and showcasing growth with accounts/scale… 40% of engagements are still in pilot mode, so these cannot be considered long term clients until they get into some form of live usage.

2. Stop hiring armies of salespeople who have no idea what they are selling. Sorry, but we really needed to say that one…

3. Stop amassing as many partners as possible. Prioritize quality not quantity (which would require well thought out partner programs).

4. Stop referring to SaaS as cloud. Seriously just stop. Now.

5. Make the gap between unattended and attended seamless because customers don’t actually want to decide what flavor of automation they need, they just want automation.

6. Start addressing governance and meaningful management of bots in the context of broader workflow. Don’t let massive attended automation and freedom to automate shift from democratization to chaos. address how attended is managed in a way that does not make the IT shops in all of their clients want to abort mission

7. Bring IT and business visions together as one integrated approach. Education must focus for technical and non-technical resources – into communities and educational institutions globally.

8. Shift focus to an integrated automation roadmap – expansion of functionality beyond RPA/RDA to AI and smart analytics. Badging everything as RPA is definitionally incorrect and fails to give clients a roadmap to follow to advance beyond (legacy) repetitive task automation, desktop and document automation.

9. Provide proven scale and depth of professional service to support the SI/advisor channel. This is the battleground where the winners and losers will be decided… if you have the support available to train the channel and your major direct clients, you will get your clients into double-bot figures.

10. You must drive digital change management to help enterprises grapple with transformation with its services investments. Relying purely on Big 4 advisors and service providers for change management will cost clients a fortune and drive many away. This is a key area UiPath needs to take the lead on.

11. Prove it has the lowest-code capabilities of all the bot players. The shift from low-code to no-code is on… proving real no-code abilities is becoming increasingly critical as frustration build with the ease-of development of some of these solutions. This is the real key to proving “one bot for every employee” is truly possible.

12. Really demonstrate you can win in the cloud. This is the impressive push from AA that UiPath and Blue Prism needs to counter… the ability to create public, private and containerized solutions for large automation is one of the main avenues to moving out of pilot mode into a fully industrialized approach.

13. Have the most mobile-enabled bot solution. Moving bot development into the hands of code-hating business professionals is key and having really cool mobile interfaces is becoming increasingly important.

14. The developer ecosystem must be expanded to extend functionality, libraries etc. Commit to specific goals for how much of their codebase will be available on Github et al to build an industry solution skewed against technology-vendor lock-in. Much of this RPA functionality is not rocket science or any trade secret.

15. Commit specific sums to meaningful partner relationships with leading service providers and consultants, including opensource partner technical support systems, events, education resources, and people to help the industry grow

16. Commit to funding local academies (building on their online academies) especially in blighted neighborhoods near its biggest offices to bring young coders and potential customers together with employees for on the job real-world training

17. Must get focused on core business processes by industry, such as supply chain in manufacturing, core banking in BFS, underwriting in insurance, billing in telecom etc

18. Revisit its client engagement model to ensure it is best serving its customer base – its rapid growth in salespeople may expand capacity, but if sales lacks vision, then clients may not be well served (as per comments in our recent survey above)

19. Commits to drawing down technical debt (Every SW company has it, some more than others). As illustrated above, our customer surveys point out which elements of their platforms and solution are known to need immediate re-engineering and investment

20. Identify and subsidize hands-on automation industry experts and influencers whose independent thinking deserves funding and not just focus on checking boxes with legacy analysts. The automation industry is being impacted by many unique stakeholders.

21. Kick off an enduring and sustainable initiative modeled after Salesforce’s 1-1-1 program

22. Invest in cross-technology customer events that will expand overall value creation, for example partnering more aggressively with the likes of Salesforce, Microsoft, Amazon, Google etc.

23. Spearhead an Automation Industry Technology/Business Roadmap that shows a clear path for enterprise clients to progress from basic robotic task automation through to integrated automation and then to achieving genuine AI value

24. Provide sensible RPA pricing options. A “bot” is not a standard unit of measure. It is an abstract measure and a UiPath bot is different than AA and not the same as Blue prism. Yet most continue to price RPA as some of the function of “bots”

25. Focus on actual business transformation. We are using RPA to run ineffective processes cheaper and faster. That is not transformation and is a short term game.

True leadership will come from those who make the most advancements in these versus fancy rhetorical statements and press events. If you want to be a leader…. then bloody act like one!

If I have to listen to another technologist promoting “AI as a key component of the CIO’s agenda”, I am going to start getting a little irked… AI is not another app that can be installed and rolled out like a Workday, SAP or a ServiceNow. I even had to listen to an IT executive asking me whether he should “leave AI in the hands of SAP as part of their S4 upgrade”. Not only that, I noticed a well-known analyst firm promoting a webcast last week advising “CIOs how to rollout RPA”. Really?

One of the biggest issues in our industry today is the abject failure of the business teams who design and own the processes, to partner effectively with their IT teams to deliver automation and AI that supports the business vision of where the business leaders want to take it. IT people are not clairvoyant – they can only aspire to deliver what their business colleagues clearly instruct them to do. Otherwise, they’ll just buy all these fancy software suites and say they did their bit for AI… So enterprise leaders have to knock the heads of their business and IT teams together and get them partnering effectively to design a roadmap that takes them and their data where they need to go to stay competitive. There’s no time to keep pointing fingers, we just need to sit down and figure out how to work together in much more effective ways than we have over the past few decades.

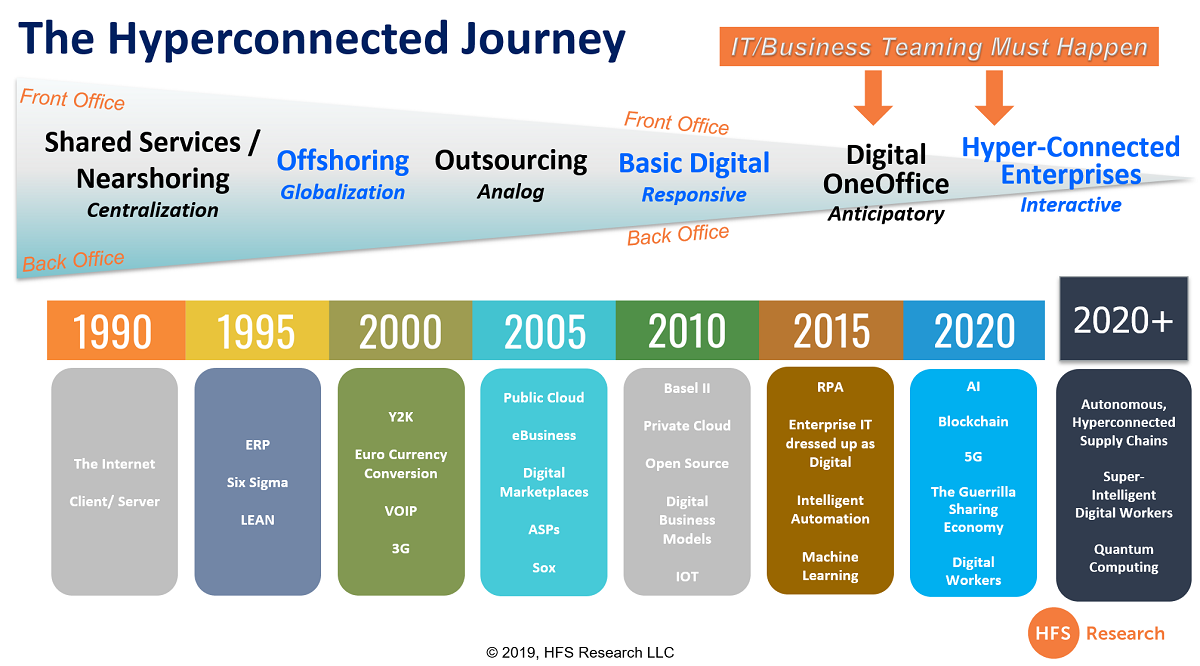

Embracing AI is all about crafting the anticipatory organization, one that is hyperconnected across its ecosystem, its customers, employees and partners

The whole purpose of AI in the enterprise is to have business operations running as autonomously and intelligently as possible, which means we need to build enabling IT infrastructure that supports the business process logic and design. People are talking about “re-platforming the enterprise”… this is really about redesigning IT to support the business needs, to help the business respond to customer needs as soon they occur, and have the intelligence to anticipate the needs of their customers before its competitors can.

Enterprises need to be as hyperconnected and as autonomous as possible within their business environments if they want to pinpoint where disruption is coming from, where to disrupt and how to keep reinventing themselves in an unforgiving world when we no longer have time to rest on our laurels:

The problem for IT is that AI doesn’t come packaged in a nice box with an instruction guide

I’m sorry to be mildly offensive here, but AI and automation are only effective when they are designed to solve process and business problems, not check another box on the CIO’s resume. While it is important to keep the IT team in the communication loop so that it is ready to provide the right infrastructure and technology stacks required for operationalizing AI solutions, the steering wheel of any business application of AI must be in the hands of the businesses. Smart businesses know their key pain areas and can identify the most relevant and feasible business cases. They own the data, they know the context, and how a process should run when it is augmented with appropriate AI techniques.

For many firms, the day they implemented their first ERP was akin to pouring cement into their enterprise

The reality is the ERP system of the last 3 decades is no longer the system of record for ambitious, hyperconnected enterprises. It is a rigid suite of standard processes that keep when wheels on a legacy operation. The emerging system of record is the data lake itself, when the business leaders have the ability to extract the data they need to make the right decisions, or have systems that can start to help make intelligent decisions for them.

So let’s examine at the interplay between business and IT with these emerging AI-driven environments with 10 prescriptive activities business leaders and IT leaders need to put into effect, if they want genuinely want to develop AI capability that takes them into this hyperconnected state:

10 AI activities the business teams must lead to ensure AI success

Prioritize use cases from AI technology availability. The business team must prioritize AI business use cases from the initially identified list of potential AI application opportunities. The team must demonstrate its process knowledge and desired end-state scenario to help the IT team to ensure effective project coordination and outcome-setting. Using external consultants at this phase can be very effective to ensure the best business/technology fit.

Develop the AI Business case: The most critical step, where the business team must set initial benchmarks, define pre- and post-process improvement metrics, and estimate target benchmarks.

AI feasibility analysis and specification development: Business teams must solicit help from IT teams for their expertise with items such as technical feasibility analysis, infrastructure requirement specifications, and technology stack selection. Other areas are technology cost estimation, deployment, and production release,

AI Technology cost estimation: Developing estimates for the cost of technology stacks and solution deployment efforts must be the purview of business teams, but it requires significant and detailed input from the IT team.

AI Data preparation and identification: Business teams must ensures success by identifying and preparing the data for training algorithms and building models. The team must solicit assistance from analytics and data warehousing teams.

Coordinate with partners: During design phase of the target process model, the business team should must provide input to implementation partners (both internally and with their consultant/services partner) regarding ontology of the problem domain, the existing process models and rules. Teaming here with IT is essential, but the business team must define and communicate the business and process needs effectively.

AI Testing: The business team must lead testing the models against the project goals during the early POC and pilot phases

Manage effective AI feedback loops: To make use cases fir for production release, the business team must provide detailed, regular feedback on the accuracy and performance. Again, they need to work with implementation partners, which may be internal teams from an AI CoE or external partners.

AI Training: The business team must be responsible for budgeting, planning and executing the training for large AI user teams, encompassing all of the staffing resources, external consultant costs, processes and task owners that are involved in the implemented use case.

AI Deployment: Deployment doesn’t end once the use case is in production. The business team must continuously monitor the model’s outcomes, maintenance, and updates during the inferencing phase, and if the problem context changes with new rules or data, the team needs to add new dimensions and models and create new clusters. Users may also require retraining, especially as processes may change over time. There will also be the need to monitor change management issues, potential legal issues with data privacy / staffing impacts etc.

The Bottom-line: AI is a business issue that must be directed and managed by business executives, supported by technology experts. CIOs who ignore this will fail

The business team should seek help from IT in terms of infrastructure and tech stack needs, but it needs to own and run the AI projects because it owns the data, context, processes, and rules and understands the pain points.

CIOs will face an existential fight if they don’t start genuinely enabling the business. The world where IT was all about mitigating outages and avoiding risk is being replaced by one that demands speed, agility, and a genuine understanding of the business.

Being tech-savvy isn’t enough anymore… just knowing where to build a data center is pointless if you don’t know what the rest of the business has planned. And this IT obsession of continually trying to upgrade ERP solutions, when most business units these days can handle it. That’s the pitfall of the old traditional IT approach – we have to make sure we never get cemented in like that again.

Just as the industry was running out of steam, just as we’re writing the obituary of the outsourcing model… suddenly we have sal-vation. We’re an industry desperate for leadership, for new ideas, for personalities we want to work with, for a new culture that inspires us to get out of bed in the morning.

So how about one provider many of us were giving up on recruiting one of the most charismatic, energetic and determined leaders who grew Accenture Operations from $1.5bn to more than $7bn. How about the guy who jump-started one of the most impressive machine learning businesses in the industry? How about the guy who pioneered whole new approaches to service delivery with the Six Generations of BPO and the As-a-Service Economy? How about the guy who drove an acquisition so smart it locked up an entire market vertical?

Just as we thought DXC was caught in a perennial treadmill of mere survival, they have made one of the most ambitious, creative – and smart – CEO appointments the services business has witnessed in Mike “Sal” Salvino – someone I have known as a friend and industry peer for two decades. Sal is proven to take legacy business, mine the gold, bring in the talent and make strategic moves, which is exactly what DXC needs at a time this industry is in transition. We’ll have Mike at our HFS Summit on 2nd October to have a more candid discussion with industry leaders if you want to try and grab a last-minute spot.

So what are Mike’s challenges and opportunities according to the HFS analyst team?

Developing market position and messaging. The new combined entity still trying to find its unique market positioning. DXC needs to hit the ground quickly to consolidate and clarify its combined offerings and transform internally to cater to the changing market needs.

Double-down on tech where it can win. DXC has oodles of capability and talent in automation, digital enablement and AI, in addition, to a $2bn business process services business. There is gold here if it can bring it to the surface and take it to market in the right way.

Expanding its base. DXC has a significant existing client base of nearly 6,000 customers especially in healthcare, public sector, and CPG. Large deal heritage from CSC and HP. they have capabilities across OneOffice but have been reduced to a me-too player. No one knows what they stand for… Mike needs to change that, and fast.

Find a way to highlight some of the hidden gems in their incredibly complex patchwork of assets and capabilities from past acquisitions. The “blanket DXC” is drowning out some of their areas of differentiation because they’re not talking about them anymore.

Verticalizing their offerings effectively. DXC spent a bunch of time slinging what HP + CSC can do and came up with 8 master offering buckets. But it was all horizontal. They are struggling to build relevance by industry. If they could fill the white space with their gigantic customer base alone would ensure success.

Finding a thumb for the dyke. Stemming the flow of long term infrastructure customers getting poached by aggressive ITO competitors and AWS.

Build a true brand association and a mission. DXC doesn’t have a clear story for anyone outside of very specific groups, and that’s really dependent on who you speak to. It’s the same for clients – as part of a major branding project where we interviewed some industry luminaries who all struggled to understand what DXC is up to, what differentiates them, or why they should even think of working with them.

Target (and execute) on acquisitions that provide true differentiation. As Mike looks at strengthening vertical offerings and service delivery areas, there will me boundless firms on the block to evaluate. Time is not on DXC’s side and the right targets need to be integrated effectively, alongside the current firms in the organization.

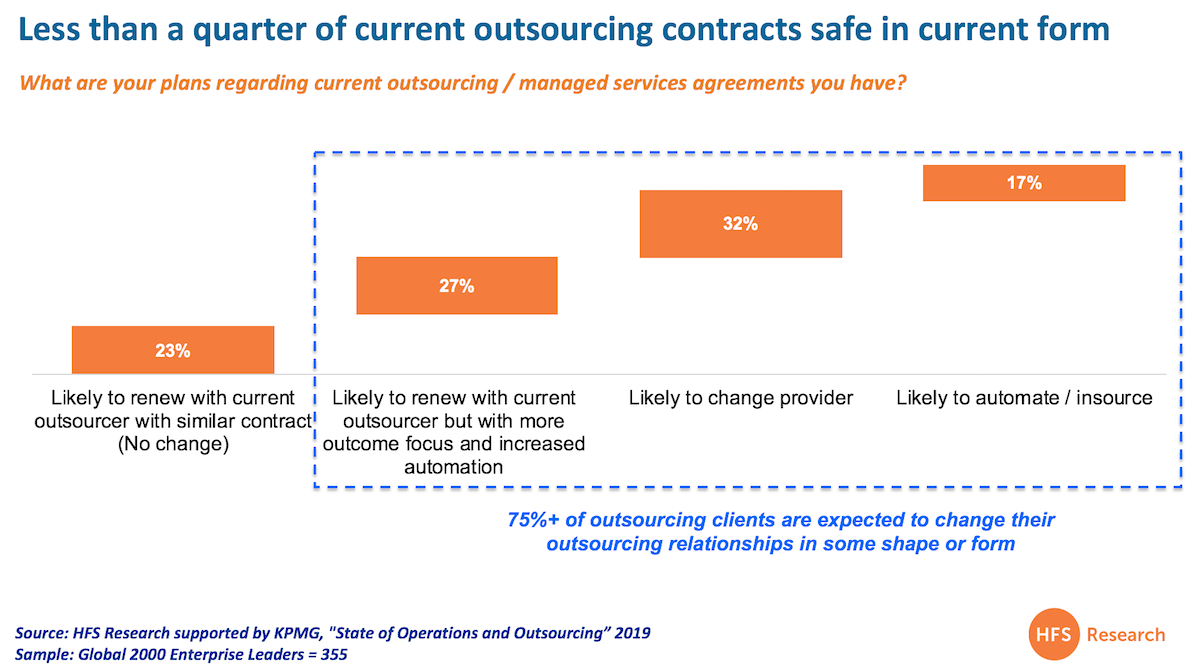

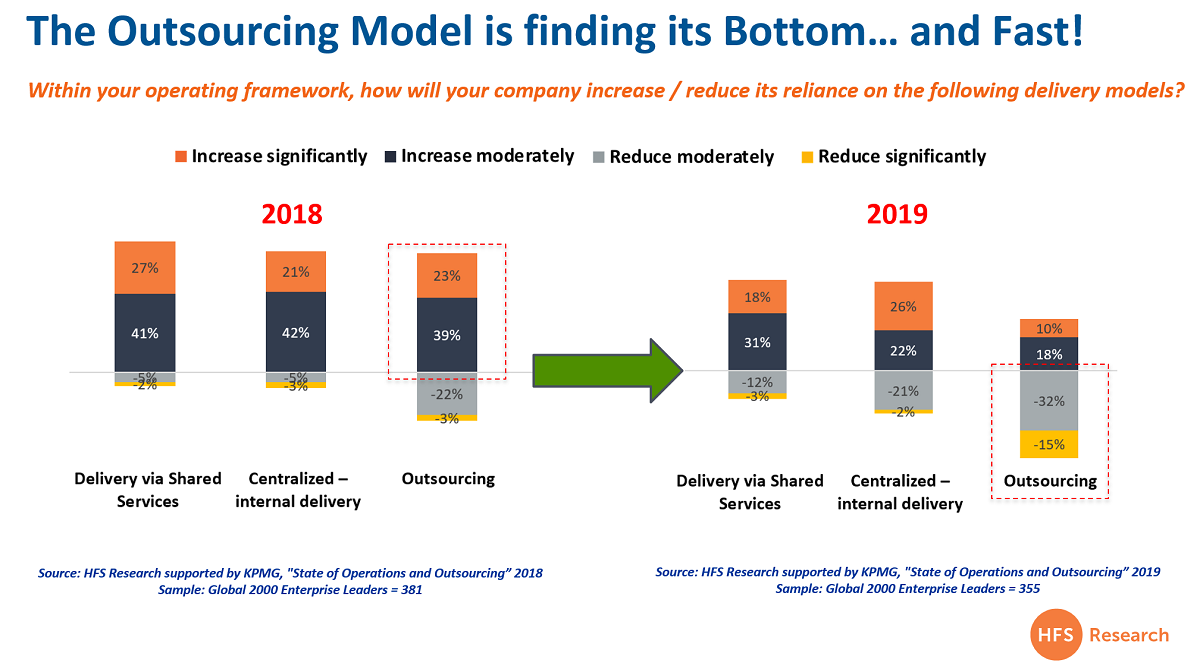

As we discussed last week, the 2019 State of Operations data shows a strong appetite from enterprises to dump legacy outsourcing practices and reinvest in operating models that can take them straight to digital.

While the desire to invest in an outsourcing model nose-dived from 62% in 2018 to 28% this year, it’s also worth looking at the definitive actions enterprises plan to take when their current outsourcing engagement come up for renewal:

There is a clear appetite for change and complacent service providers are in serious trouble

Several service providers have already commented that they “just don’t see their clients wanting to change this aggressively” since our recent roundtable in London and the recent blog post which amassed huge attention across the industry. However, many are clearly in denial that we’re deep in a critical transition from the traditional labor-driven model to one that is much more touchless and less physical in nature. In my view, the issue here isn’t that these peoples’ observations are wrong, they’re just not having the right conversations. Most of the BPO executives admit they are “feeling their way” to address their clients’ needs for more RPA and digitization of their processes, but simply do not have the scale of people on hand with the necessary training and skills to help them. Instead, they are simply waiting for a burning platform that forces them into some sort of action. Worryingly, when we look at this data, when this burning platform finally appears under their posteriors, it’s already going to be far too late for them to save themselves.

Why going straight to digital with your outsourcing engagement is like buying a Tesla – it’s a big change, can be expensive and requires a very different type of service partner to make it viable

Most enterprise operations leaders are unlikely to tell their provider’s client partner “we’re fed up with spending the same dollars each year for the same tired old processes and small army of staff to deliver them”. That is like going to your car dealer and saying you’re sick of paying extortionate sums for gas to fuel your car, and you’re also sick of polluting the environment. Unless your car dealer is fully up on electric cars and has a great financing model to switch you up, you’re more likely to find a dealer who specializes in what you need. The only way your existing car dealer is going to have a chance of retaining your business is if his firm has invested in mechanics who are trained in electric car maintenance, sales people who know enough to sell you one, and a financing partner to get you “fully electric” with a financially affordable package.

So what can we expect today’s enterprises to do when their current outsourcing engagements expire?

Barely a quarter of enterprises content to stick with their gas-guzzlers. As the data clearly tells us here, not even a quarter of clients intend to stay true to their tried, trusted, stable (and stale) relationship. Perhaps they just don’t care that much and can quietly drift along to retirement by merely “keeping the lights on” with their legacy business practices that just about get the job done.

Another quarter wants to move the needle, but may opt for a hybrid model. Meanwhile, 27% are getting itchy to kick their service provider up the rear end and get them embedding some real automation into their delivery if they are to renew with them. This means they want to see real commitment to reduce the dependence on the staff army and see real investments in process automation to digitize their delivery. This could perhaps be the car dealer selling you a hybrid vehicle as you look to move to an electric model, but need a defined transition period to get there. It is also less extreme for a car dealer to invest in hybrid cars as they require less specialization than fully electric vehicles, so this is often a great compromise for both parties.

A third is more decisive and likely to make the switch. 32% have clearly got to know their current outsourcing provider only too well over the years and have zero hope they can get any real co-investment out of them. As we have discovered over the last couple of years, some providers have made real investments in competencies like automation and AI, while others have merely added a little sugar-frosting and persist with selling the same old model with some cost shaved off the package, and some added incentives for performance (i.e “outcomes”). Moreover, ambitious outsourcers are heavily targeting their competitors’ disaffected clients and are willing to offer eye-catching deals to win their custom. This can include attractive pricing tied to aggressive delivery staff reduction over a 3-5 year amortization plan that is offset by efficiency savings due to automation and digitization.

In some cases, it may also prove more attractive for the legacy provider to shed the business than fight to keep a client that will quickly become unprofitable (and the industry is littered with those engagements). In many of these cases, this is more like a car customer moving towards a brand they haven’t driven before, most likely a hybrid, and having an acrimonious split from their current model because their dealer tried to sell them a car that just didn’t check the boxes. However, in several services markets, we are seeing emerging offerings from providers where they are offering fully digital offerings (with vastly cheaper support), such as TaskUs in the customer call center market, or nDivision in managed IT operations, which can undercut traditional outsourcers so aggressively, there is no feasible way the traditional providers can compete. In addition, we are seeing several India-centric service providers offer $-per-chat support models for some transactional services that are essentially chatbots offering basic-level support services at costs as cheap as 15 cents a chat… we are finally seeing “digital disruption” attack the traditional outsourcing market that has somehow staved it off for years thanks to lethargic clients and lock-in contracts.

The 17% who have given up and will just look at something very different. Maybe the cost of changing the model is just so abhorrent it’s time to pull the work back and fix it yourself. Maybe you’re so fed up with the lack of innovation in changing anything you’ve realized you have smarter people on staff who are better deployed to take the work back, staff up to execute it while you explore all your digital and automation options. Maybe you want to invest in an integrated automation platform, and you want to use the funds saved by backsourcing the work to invest in an automation backbone that enables you to perform work in a touchless, smarter manner? Maybe you’ve seen that shiny new Tesla in the showroom window and decided to take the plunge and to hell with the upfront cost…

The Bottom Line – after years of providers complaining about their clients being unwilling to invest, the outsourcing chickens are coming home to roost

The problem with outsourcing is that it has always been underpinned by financial models that give the buyer or provider little wiggle room to make investments to do anything differently. Most firms still run most of their processes exactly the same way as they did 20/30/40 years ago, with the only “innovation” being models like offshore outsourcing and shared service centers, cloud and digital technologies enabling those same processes to be conducted steadily faster and cheaper. However, fundamental changes have not been made to intrinsic business processes – most companies still operate with their major functions such as customer service, marketing, finance, HR and supply chain operating in individual silos, with IT operating as a non-strategic vehicle to maintain the status quo and keep the lights on.

And the poor whipping child over the past couple of decades has been the poor outsourcer, who’s taken on the putrid old processes and attempted to deliver them for their clients at lower cost, where the necessary investments needed to redesign the processes and improve the technology backbone would far outweigh the slim profits being eked out through using cheaper labor and following sensible process delivery templates. Sadly for our lovely outsourcers, they have little choice but to suck up the fact that they ventured into this business to turn a profit, and if they want to remain in it, they need to make some new investments to get into a position to turn more profits in the future.

As we can see, 59% of their clients are open to doing things differently or using a different partner altogether, so the opportunity is there if you’re willing to take some short term pain for longer-term gain. This means retraining current delivery staff; this means adding skills in areas like RPA, ML and AI; this means smarter partnering with software firms and specialist consultancies. This means you need to get out of your niche and provide solutions that your customers need, not merely force them to buy what is convenient and profitable for you to sell them. This means you may need to start selling Teslas, not gass-guzzling SUVs….

It’s taken more than 12 years – ever since the first-ever blog post written right here – but the outsourcing marketing is on the cusp of its most seismic change since the offshore revolution… the majority of enterprises are seeking to pull away from their stale outsourcing relationships and replace people with intelligent cognitive workers which learn context – or simply bots that perform transactional tasks. And the reality of outsourcing is that it’s far easier for an enterprise to eliminate workers that are contracted via a service partner than have to go through all the painful change and resistance when trying to eliminate their own staff directly with software investments. What’s more, enterprises rarely want to bring outsourced work back inhouse until it has been fully automated and the outsourcing offers little future value.

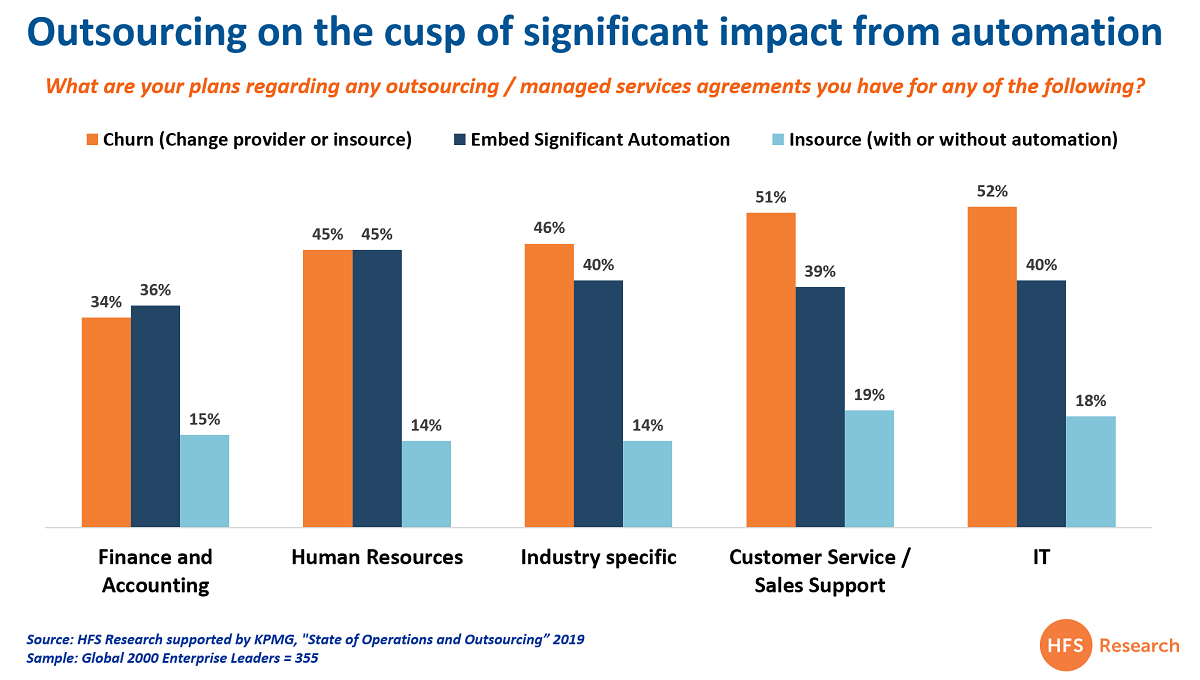

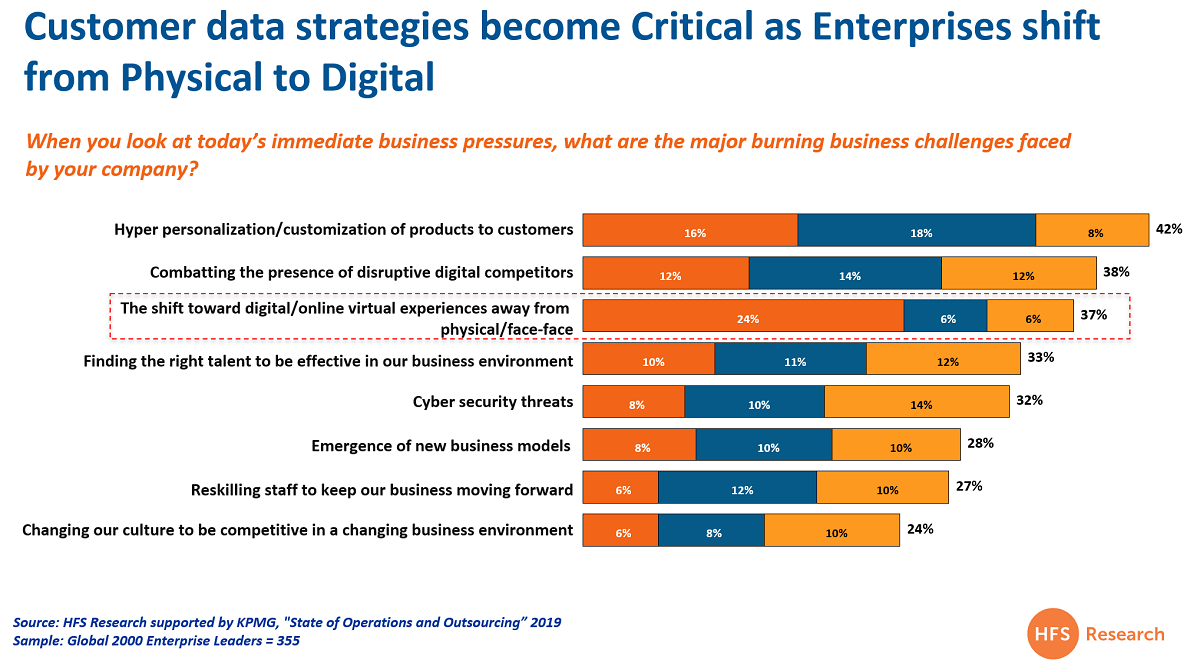

All the lovely fluff about “automation and AI creating jobs” is being proved to be utter claptrap for the services industry when we look at fresh new data from the 2019 State of Operations and Outsourcing Study across 355 operations leaders in the Global 2000, conducted with the support of KPMG:

What’s shocking here is the degree of change in mindset from operations leaders since a year ago, where 62% were still pretty gung-ho positive about investing in their outsourcing model, which has nose-dived to only 28% this year, and a startling 47% actually seeking to decrease their reliance on outsourcing. So if they’re looking at new models to deliver their business operations – and traditional outsourcing no longer fits the bill – what are they looking to do? Let’s take a deeper look:

In short, up to half of major enterprises are looking to find another provider to break their years of painful status quo, while a similar number are looking to embed significant automation into their current engagement. About one-in-six are looking to pull the whole lot back in house and have given up on the delivery model.

Why this change to outsourcing… and why now?

When we look at our reliance on staff to run our operations, we’re seen a substantial reduction over the last couple of decades, mainly due to advances in software applications that embraced process standards (and natively automation). For example, most G2000 enterprises had hundreds of people running finance processes a decade-plus ago, and likely barely have 50-100 based on advances in financial software, combined with efficient outsourcing labor arbitrage models delivered by the likes of Accenture, Genpact, Capgemini, and WNS. Procurement probably had 150 and today barely needs 30… and HR is down to its barebones across most large enterprises. The division most affected by outsourcing – IT – has shrunk from the thousands to the hundreds in most major enterprises over the past two decades. Net-net we’ve been through a very long, sustained period of labor osmosis from enterprises to outsourcers, while shared service functions have stayed largely static.

At the same time, people-driven outsourcing engagements have continued to deliver similar process work back to its enterprise clients with the same number of staff, where the outsourcers have had little incentives to make investments in automation and digital technologies, unless they can directly benefit financially, or have contractually agreed to reduce staff numbers over the course of a long term contract. We are already witnessing the likes of Automation Anywhere, UiPath and AntWorks making significant investments in their own implementation staff as they are frustrated with their lack of traction many outsourcers to incorporate automation and AI technology into the people-focused delivery models.

The new solution is to bypass staff-intensive processes and go “straight to digital”

The big change we are seeing now (and we’ll share more data to back this up shortly) is that the outsourcing models we know and love have long reached their saturation points, and the only real value enterprises can get from them (in the near future) is to remove the number of staff delivering the work and replace them with digital technology. For example, a bank we spoke to recently that is replacing hundreds of staff whose job it is to create customer appointments with a conversationally-intelligent cognitive worker solution. The savings are massive. However, if the bank had outsourced those workers, the only way to force their service provider to replace them with a digital solution would be to demand it upon contract expiry, or bring it back inhouse and do it themselves.

The key is for software and services providers to develop aggressive adoption programs to create the real “straight to digital” ROI

In recent years, we’ve seen many of these digital models evolve – from simple software apps, to chatbots, RPA tools and now more conversationally-intelligent cognitive workers (such as IPSoft’s Amelia, IBM’s Watson, Automation Anywhere’s IQ Bot, TCS’s partnership with Amazon Connect, HCL’s Lucy and Wipro’s solution of Holmes with Avaamo). However, the earlier models where enterprises were being forced to invest multi-millions upfront just to get a cognitive or RPA solution actually functioning without constant human intervention and training, have failed, with the notable inability of IBM’s Watson solution to reach anything like the heights the firm had promised because the market a) wasn’t ready and b) wasn’t convinced the massive outlay would reap massive rewards. And the high-profile struggles of many RPA solutions to replace people with technology (merely augment processes) threaten the rapid rise of those solutions as investors pile on with unrealistic expectations. So the answer is staring us in the face, and it’s pretty straight forward… the winners in this tough new transition market are those which can guide enterprises to take existing processes and move them straight to digital and remove the layer of people delivering them.

The Bottom-line: The only true ROI which created the traditional outsourcing model is now repeating itself with digital solutions

As much as we can spin wonderful stories about augmenting people and enriching jobs etc., the goal of most Global 2000 enterprises is to maximize profits and the stated goals of C-Suites and Ops leaders are to a) reduce operating costs and b) move away from physical to digital environments:

The industry has spoken and it’s clear where they will invest – in partnerships that can accelerate the move to digital without all the painful and costly steps to get there. And the areas most primed to make this happen are where the staff have already been outsourced and the logical next step is to reduce or eliminate them altogether.

The challenge for outsourcers. Defend the clients you really want to keep and attack ones from competitors to backfill the inevitable losses as the model shifts from people to digital. This means you need to develop programs that get your clients leveraging the benefits of automation and AI quickly by hiring talent to make this happen, and forging deep, mutually-be partnerships with software firms to work with you. As we recently discussed at our Robotic Business Outsourcing Roundtable in London, outsourcers face a stark choice between embracing digital models that require less labor, or fading into insignificance.

The challenge for enterprises. Forcing your service providers to cannibalize your business is not an easy task, but if you are willing to work with them to build real digital models that work and become a showcase client for them, you should find a cooperative (and hopefully) ambitious partner to work with you. If you do not, then look further afield for partners willing to invest in your business. If noone wants to transform your operations your business clearly isn’t very attractive (especially if you got a cheap deal to begin with) so you may well be better off bringing operations back inhouse and digitizing them yourself.

The challenge for advisors. Today’s environment should be gravy for you – I’ve heard from several advisor friends that deal flow is really healthy – and it’s mainly outsourcing renewals demanding digital enablement and less people-centricity. Hence deal amounts are declining and demanding more complex tech skills to enable new solutions. Your problem is going to be finding providers willing to embrace disruptive models and work with thinner margins in the short-medium term for longer-term gain. There are several providers out there willing to be aggressive to “land-grab” deals and increase market share, despite thinner margins and scarcity/cost of tech talent. However, you really need to flesh out the providers prepared to put skin in the game, versus those paying lip service.

End of the day, many of the outsourcing partnerships that got so many of us here are unlikely to be the same ones to take us to the next phase…

At HFS, we’re approaching ten years’ in existence – yes 10 bloody years’ of this stuff – and we’re still the “new analyst kid on the block”. As we approach this new phase in our journey, we’re focusing heavily on the massive impact our research has across all corners of the services and tech industry. The traditional channels of slapping stuffy reports behind a firewall and blackmailing suppliers with scatterplot grids are still the predominant way the analyst industry persists in operating (or simply regurgitating supplier press releases dressed up as “insight”), which has helped HFS expand our operations across three continents and bulldoze our way into a small elite group of analysts firms.

However, we’re not stopping there… we want to engage even more digitally and effortlessly with our global community, using video, blogs, podcasts, webcasts, summits, roundtables and various other forms of social media. So were gone and added some serious firepower to our digital prowess with our recent acquisition of Quigley Media, where the founder, Tom Quigley, joins us as Chief Marketing Officer. So let’s hear a bit more from the unassuming Scotsman and his plans for HFS, while he’s not practicing his blackbelt in karate on his three wee lads…

Tom – you’ve been a pretty active figure in the world of global sourcing for some time now – can you share a bit of background about yourself?

Sure. For this first half of my career I worked in mostly operational roles for two large insurers, Commercial Union (now Aviva) and Prudential UK & Europe. During that time I designed and delivered a 3 year programme of events for the CEO whereby he and the executive directors would travel around the country meeting hundreds of policyholders and doing impromptu Q&A sessions with them, which was pretty disruptive back then. I also delivered conferences in Mumbai and Dubai.

I joined BPO provider Capita in 2009 and headed up the marketing function in one of their nine divisions. When I left in March 2016 I was Head of Marketing, Design and Events for a consolidated number of divisions, overseeing a team of 2 Business Partners, 5 marketers and 8 graphic designers.

I joined the National Outsourcing Association as Marketing Director and we rebranded to the Global Sourcing Association (GSA), which we launched in Sofia in October 2016. It was at the time I recognised the emerging talent from central and eastern Europe, and so I set up my own marketing agency providing services to CEE businesses looking for market entry or engagement with the UK and Western European countries. During the last two years I also co-founded and was the CEO of the Alliance for Business Services, Innovation and Technology, with members including Pwc, Cushman & Wakefield, Convergys, Stefanini as well as institutions like IAOP, Nordic IT Association, Bulgarian Outsourcing Association etc. I also met with and successfully persuaded the Bulgarian President to be our honorary Chairman!

I stepped away from that role at the beginning of the year to focus purely on the agency and we’ve enjoyed working with clients from Poland, Romania, Bulgaria, the UK and US during that time.

So you recently sold your firm and its digital assets to HFS… what was behind this move and what can we expect to see from you in the next few months in your new role?

Well its quite ironic because I’d been spending the last 2 years telling anyone who would listen that I would never work inside another company again as I was having too much fun being my own boss, so it did take me by surprise at how quickly I said yes when the offer to acquire QM came about. We were just completing brand perception study for HFS Research when I got a Skype message from you late on a Friday night. We met on the Monday, signed contracts on the Wednesday and I was in the Cambridge HQ at my desk on the Thursday – it really did happen that fast!

But I’ve known HFS Research for a number of years and was very well aware of its unique stand in the market. I am a big admirer of the quality of insight and unfettered views it provides – and when the offer came I genuinely had goosebumps, that told me it was the right move to make.

As for the months ahead we will launch a new website with improved functionality and integrated multi-platform analytics that gives us a more unified view of our customers, we’ve just set up a digital studio in the Cambridge HQ giving to open up some new channels and give us more control over our digital content, and we’re currently building a number of great marketing campaigns to land some important messages in the coming months. We’re also mapping out customer journeys to see how we can improve client experiences as well as establishing a more structured, tier-based relationship with our supplier partnerships to improve speed and innovation. In addition to that we have our New York Summit in October as well as events going on in Paris and Stockholm, so there’s lots to come. Our clients will definitely notice a new, more emboldened brand overall with a clear focus on building closer, more meaningful relationships with our communities – not only through our research, thank tanks and other market activations, but also through more targeted communications.

How is the industry different these days? You’ve been very involved with emerging locations for several years now – where do you see this headed next? Is the game changing?

We’re in a market of perpetual change now. Technology has overtaken consumer needs as the main driver of innovation, and the lines between BPO and ITO are dissipating. It really is about the provision of integrated digital services and one office. Contracts are increasingly focused on partnership agreements delivering outcomes, providing access to innovation and sandbox environments that will enable businesses to deliver more personalised services to their customers at scale. Central and Eastern Europe has been producing STEM resources for years but they are becoming more even more prevalent because they are forming better and more active networks and alliances, backed by their governments and funded by the European Commission in some instances – they are becoming more adept at integrating themselves into the connected ecosystem. Going forwards location will be come completely irrelevant as technology will enable the proliferation of agile – scaleable – teams that will form virtually to work on multiple projects, before disbanding and reforming on other assignments. I believe we’ll eventually see the end of the permanent employee contracts as more millennials become a part of our economy.

And how about the research industry – you’ve been on the outside looking in for your entire career… how do you see it evolving? Is it looking any different from the inside?

Well I’ve only been on the inside for a couple of weeks now, but I’m not sure the analyst industry IS actually evolving at the same pace. Sure the analysts are reporting on technology and how businesses are thriving or otherwise in industry 4.0, and the means of capturing research and analysing data has advanced but for the most part I don’t believe the research industry has become transformative enough. Some companies appear to have become machine monoliths, churning data and reports that seem pretty vanilla and without much of a voice; if you laid out reports and magic quadrants from a number of them and then covered up the logos I doubt many people would be able to distinguish who is who. Let me be clear, the analysts themselves are highly credible, very clever people regardless of what organisation they work for, but I think the ‘corporate machine’ sterilises a lot of what they actually produce.

This is where HFS Research stands apart, and the reason I’m so excited to be here. I know how different it is observing from the outside but I can see how different it is operating from the inside. Our purpose, our culture and how we operate has completely different DNA from other analyst firms. Last week I listened to Mark Hillary’s first ever podcast talking to you about why you progressed from writing a blog to starting your own analyst firm, and I can see that the values that drove that decision are still very much alive in everyone involved with HFS today – and that podcast was recorded 10 years ago. My job is to make sure our clients and the market at large are aware of that, and recognise the value in choosing HFS Research as their partner going into the hyperconnected future-state!

And finally, there’s a rumor going around that HFS is going to be ten years old soon… any plans to celebrate?

Next March marks the 10th birthday of HFS Research, and yes we will definitely be celebrating with our people, partnerships and communities. But you’ll have to wait a little bit longer to discover exactly how..!

Welcome, Tom – and we’re hopeful that many of our clients can meet you in New York this October 1 and 2 for our next major HFS Summit!

Who remembers this classic “statistic” from a couple of years’ ago, where we caught some friends declaring RPA fantasies that are simply miles from reality:

We’ve been keen to share with the world that RPA satisfaction has been in positive territory for more than half of the adopting enterprises, which is OK for a relatively complex new type of solution that takes a while to get right, and we revealed a 58% a satisfaction rating a few weeks later.

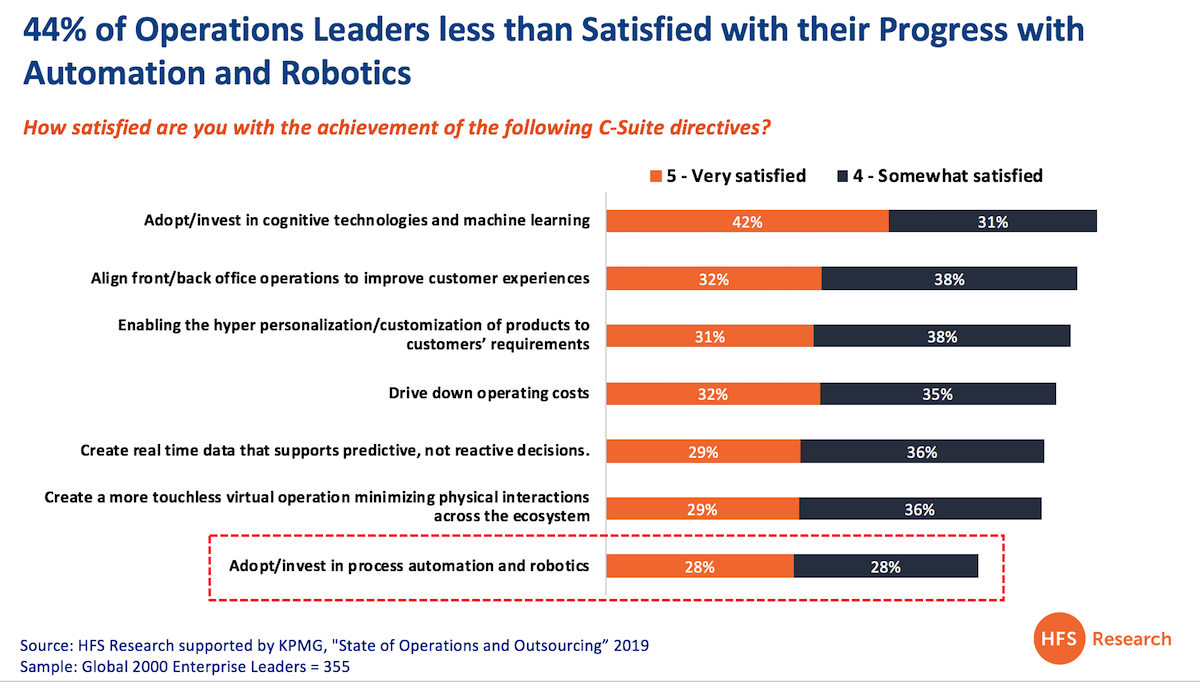

Sadly, two years on, satisfaction ratings have not improved

Our brand new study of 355 operations leaders, conducted with the support of KPMG, has revealed that only 56% of the Global 2000 express a positive experience from process automation and robotics:

What’s alarming about this is we asked operation leaders to assess the satisfaction levels of all key C-Suite directives, such as the adoption of AI/ML, enabling hyper-personalization, ever the old faithful of “driving down operating costs” …and process automation finishes dead last. I would argue this isn’t because process automation and robotics initiatives have been a disaster, but more likely, expectations from the sell-side have been vastly over-inflated. While this may sell more licenses and consulting days in the short-term, it will stunt longer-term growth for the industry. Let’s delve deeper here…

Why are process automation and robotics lagging in terms of satisfaction?

The over-hyping of how “easy” this is. The problem we have in this industry right now is an obsession with glittering outcomes and not enough real-world guidance on how to achieve them. The majority of robotic adopters have never ventured into double-figures of bots deployed, and many simply have little idea how to progress their adoption beyond a handful of pilot projects. The focus of the narrative needs to be directed to helping clients develop broader robotics strategies across organizational areas. We’re also hearing about some enterprises aborting some major RPA projects because they just didn’t expect the cost and scale of the effort to be so large. So we need to be realistic and balance the great benefits of robotic software with the challenges of training people on it, scaling the technology and gaining buy-in across business units.

Lack of real experiences being shared publicly. Enterprises RPA adopters are fed up with the constant deluge of “motherhood and apple pie” being served up by the industry when they know full well these deployments are among the biggest challenges their customers have ever faced. The RPA vendors – and several of the leading services firms – will be far more appreciated if they started sharing the real customer experiences with the world. For enterprise operations and IT executives, being successful at automation and AI is career critical – they want to learn how to be effective and how to invest their time wisely. If this stuff was easy, they’d be out of a job pretty quickly, but fortunately for them, it is not, and they can embrace these experiences to increase their value to their firms and their careers.

Huge translation issues between business and IT. Simply put, most IT folks have little understanding of RPA and think all their world problems can be solved with an API. RPA – for most operations executives – is the first time they have had to work with actual software development and get involved in some low-code activities. And they approach it with a “process first” context – how can I use these tool to integrate these apps / screen views / objects / documents etc? I can honestly say I have been to two major software developer conferences where RPA is on display and the developers are simply clueless with regards to how RPA fits into their world of platform modules and APIs. If we can’t bridge this divide, we run the risk of RPA being relegated to the scrap heap of failed technologies.

Obsession with “numbers of bots deployed” versus quality of outcomes. If I hear another executive claim he/she has deployed over 100 bots, and that is their prime measurement of success, I will start naming and shaming =) In all seriousness, there is no race the finish-line with this, and can see many enterprises still grappling with automation projects for many years to come. The ones whom I have met who have expressed the most dissatisfaction are those who have bought far more licenses than they know what do to with, and have real issues trying to explain this their over-investment to their bosses. I’ve even seen some fired because of it.

Failure of the “Big iron” ERP vendors and the digital juggernauts to embrace RPA. Let’s be honest, with the exception of SAP’s small acquisition of Contextor, which didn’t even warrant a mention at the recent Sapphire event, the IT bellwethers haven’t fallen in love with RPA. It’s just not sexy and scaleable enough for their suites, and if you read some of the guff on social media from IT “thought leaders”, they have no bloody clue what RPA really is – and does. IT people just struggle with a technology that starts with a business process headache – they prefer to work with code-intensive products that can be shoe-horned into businesses, which they can make really complicated to install and manage. Only Pega, from the world of large enterprise software, has made greater efforts to embrace process automation with its 2016 acquisition of OpenSpan, and I was quite impressed with the prominence it gave digital process automation at the recent PegaWorld event, but, even at Pega, it’s clearly a challenge to communicate the true benefits of RPA to the Pega traditionalists, whose entire world revolves around its shiny CRM orchestration platform. While we can point to all the lovely partner announcements we hear from the big three RPAs about their Google, Microsoft, Oracle, Workday, IBM etc partnerships, the truth of the matter is excitement and investment levels from the IT glitterati have been nothing close to what we were hoping/expecting just a couple of years ago.

Bottom-line: Over-setting expectations is putting the automation industry at risk of failure, not setting it up for the success it should be

The lesson here is that the sell-side is pushing too hard to sell too much too quickly and is setting up too many clients for disappointment. We just need to set expectations better and get the balance right…. Rome wasn’t built in a day. We need to hear the RPA big daddies talking about how enterprises are grappling with real issues of internal change management, training and education. We need to hear our IT leaders finally reach their “aha!” moment when they finally understand how robotic software is pulling in their frustrated business operations leaders into their world of embracing technology to help achieve real business outcomes. Because one adage has rang true for 30 years now – design your processes the way your business needs them to achieve the business outcomes you crave… then invest in the right technology to make this happen. RPA has the potential to be the first true catalyst to make this a reality, and we mustn’t waste this opportunity. Let’s create an industry that can flourish for the next 30 years, not one that we’ll break in the next couple with our greed to get rich and close that next contract…