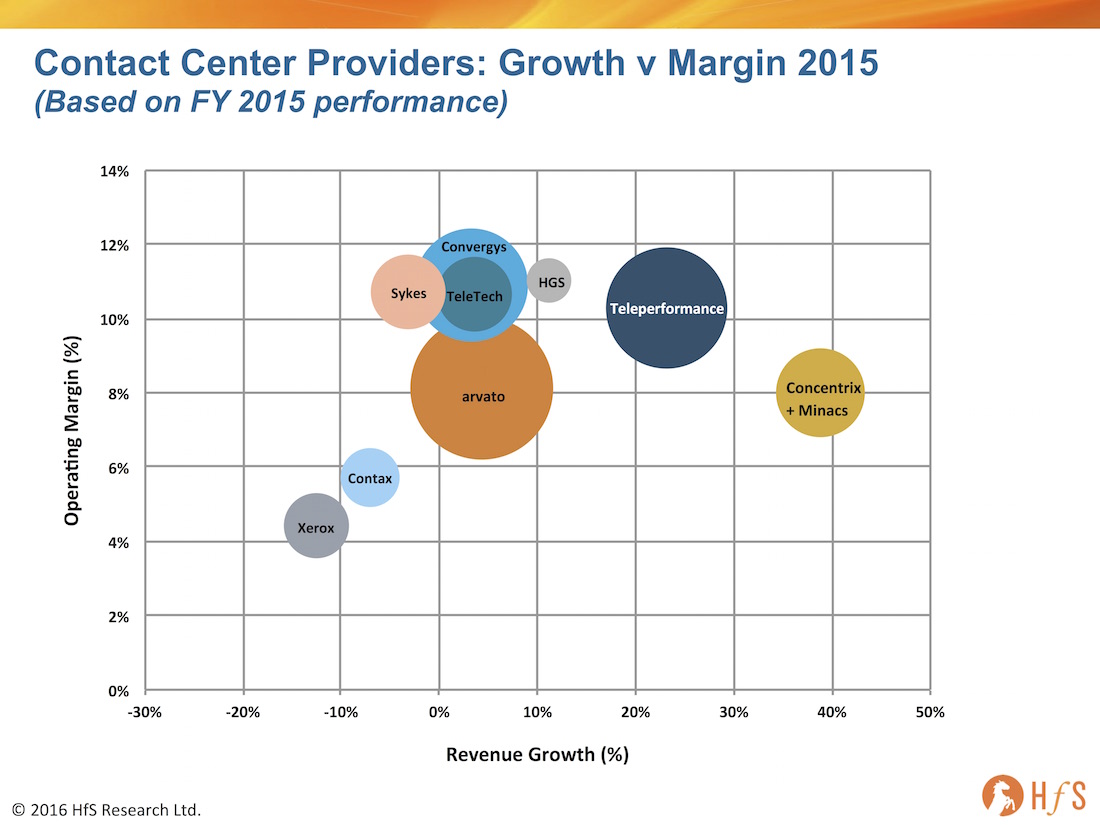

SYNNEX-owned Concentrix today announced a definitive agreement to buy Canadian born Minacs, previously owned by Indian conglomerate Aditya Birla Group and presently owned by two private equity firms. HfS estimates the combined entity will easily surpass $2bn in 2016 and is a singificantly show of force to the rest of the contact center industry.

Minacs is an approximately $500m services firm with 21,000+ employees focused on contact center BPO servicers and a strong background in automotive, with about 40% of revenues coming from that industry. Minacs has always been a solid player with a strong Apple relationship and good marketing analytics/ support capability. The service provider struggled to position itself in the US and trying to get into markets where it had small chances of success, like banking, procurement and a small F&A play. The acquisition price looks reasonable and adds considerable size and scale to Concentrix. While there are some clear signals that Concentrix is looking up the CX value chain (and there are some good upsell opportunities with existing clients), the most prominent feature of this deal will be scale—raising Concentrix to the $2bn level and positioning itself firmly against Teleperformance/ Convergys/ Arvato at the lead end of the market. Not only that, HfS revenue analysis shows the combined entity leading the market in terms of revenue growth:

(Click to Enlarge)

The addition of Minacs would bring Concentrix the following key assets:

Digital Marketing Capabilities/ Loyalty Marketing, especially in the area of automotive where Minacs helps clients navigate OEM. In addition to expertise, Minacs has proprietary marketing automation tools which have been customized for vertical alignment.

Delivery Footprint: The acquisition of Minacs would broaden delivery with sizeable nearshore operations in Mexico, the Dominican and Jamaica and offshore in India and the Philippines.

Analytics: Given that Concentrix analytics story has not been vertically focused, Minacs’ strong industry aligned analytics may help Concentrix to develop analytics expertise in key industries such as automotive, telecom, media and high tech.

Concentrix is wise to build out more digital capabilities in the marketing realm, the way that other pure play providers the way Sykes has with ClearLink, TeleTech is doing with Revana, and Indian BPOs and multi-nationals have been building for a while. This is a natural next step to explore the inherent complements of tying in contact center with the greater picture of customer experience, given the increasingly blurred lines between marketing and customer care. As with all providers attempting to address all elements of the front end, the key will be to combine capabilities on marketing automation with CRM, and bring together customer care and marketing stakeholders within client organizations to make strategic decisions for customer experience.

The challenge for Concentrix will be to stabilize leadership as Minacs has had recent C-Suite attrition issues, high staffing turnover rates and poor organization at Minacs according to glass door reviews. A recent Minacs analytics acquisition also brings the challenge of attempting to cobble together these disparate entities. And the assertion that the acquisition expands Concentrix into Internet of Things (IoT)’ is questionable; this is initially really more depth in automotive.

The Bottom-line: A solid scale play with potential – Concentrix now needs to demonstrate a commitment to enhancing the digital customer experience

The global scale play is compelling as long as the larger entity operates efficiently next year once combined, and enables more depth and a platform for more omnichannel offerings to both sellers and customers. As with all the recent M&A activity in this space, this acquisition is more about added scale than skill, but we would love to see one of the major contact center players acquire one of the design consultancies/ creative agencies to really get in the forefront of the market to address digital customer experience. The implications in the greater market are that the leading contact center operators need to get focused on designing and enabling the digital customer experience—those who don’t will be caught up in the cost focused race to the bottom.

I think I just read one of the most (brutally) honest and practical articles by a guy called Len Kendall, an LA-based marketing executive with a clear penchant for writing. His piece is based on two premises:

The market no longer allows for employing older workers who deserve higher salaries

Technology is killing jobs at a very fast pace that will only continue to accelerate

OK – we all kind of know this. But where this gets interesting is where the discussion shifts to what he constitutes “expensive” workers.

“Thanks to advancements in technology, jobs are becoming more automated. Assuming that we can eventually automate all basic jobs and allow artificial intelligence to conduct more skilled work, there will only be a need for a small group of educated, experienced, but inexpensive workers.”

So what counts as “expensive” workers?

Group A – low-skilled, but still expensive. Large populations of low-skilled workers (varying in age) who require lots of benefits. Companies will look to replace groups of ten or even hundreds of people with one computer to reduce costs. This is the premise behind the new HfS Future Workforce Impact Model, where we expect to see a reduction of a third of low-skilled positions over the next five years in the US in IT/BPO services jobs – an even greater proportion that what we anticipate in India. The cost of healthcare alone in the US can be as high $20,000 per employee per year, not even taking into about wages, payroll tax and other benefits.

Group B – medium-skilled 20- to 50-year-olds, still needed to manage people and technology. These are the mid-career people who have the expertise and experience to manage people and machines. These people command a spectrum of salaries but are willing and able to work efficiently relative to their compensation expectations. They’re still “expensive,” but the ROI remains palatable, since machines cannot run completely independently or manage people…yet. This is where we anticipate new work and job creation at HfS (7% in the US and 14% in India, for example), as many enterprises need high-energy, “affordable” creative talent that can apply technological change to business model change.

Group C – 50+ year olds who are extremely skilled and experienced workers. They can effectively manage people and machines but require very high salaries. Often, due to realities of aging, they cannot operate at same levels of efficiency as Group A or B. This makes them “expensive”. However, as the emergence of digital business models continues apace, this group is moving further and further out of touch with the evolving needs of the business. Being able to compensate very experienced people at the $250K+ salary level will fast become a fading practice, especially if (and when) we reach an economic downturn.

Group A is under serious threat as our automation impact model suggests, Group B is where we anticipate further job creation, and Group C could likely get completely eliminated – and could happen alarmingly quickly. As Len points out:

“During the Industrial Revolution, millions of jobs were eliminated because of machines or development of new products that made others obsolete. The difference between the technological advancements of the industrial revolution versus those of today is that half or more of all future product and service needs won’t be replaced by humans but by computers. Some may argue that we’ll create more jobs to replace those lost, but the last ten years are a clear indication that computation and automation are advancing faster than the invention of new products or industries that require (human) labor”.

As our HfS model has indicated for the services industry, we expect a 7% growth in mid-high skilled job needs in the US, which culminates on a 12% overall decline in IT/BPO services jobs. So in an industry which has technology and labor skills at its core, automation of low-skilled work is outpacing the growth of medium/high skilled work.

The Bottom Line: Preparing for the future if you’re too “expensive” to be employed

If you’re clinging on to that fat paycheck and can see the writing on the wall in your enterprise, then you need to be smart and get ahead of what could happen to you. There’s nothing more frustrating for me than to see highly-experienced executives coming onto the workplace whose salary demands to support their lifestyles are turning off many potential employers. What’s more challenging for the Group C-ers is the desire of forward-thinking employers to hire people who can embrace ambiguity and less structured environments in order to drive innovative business models and understand how to act on data more effectively. This means that executives who’ve been superb at doing specific things in specific ways for many years for one company are likely to be irrelevant to other employers, unless those skills are clearly transferrable, or those specific things provided a real competitive edge to the new employer. So, while you may not be employable anymore from a cost standpoint, you can certainly make yourself financially viable for future work.

Here are some ideas to add to your future financial viability:

Start developing your marketable skills now that you can sell them in the future. Smart employers love being able to hire contract talent for specific tasks – especially on an outcomes basis. However, this will mean a willingness to roll up your sleeves to do work tasks you probably have delegated for the least decade or two. For example, you might have very strong communications skills, and could be great at proofing market collateral, sales pitches, white papers, executive blogs etc. There is good money to be made renting out hour creative writing skills to senior executives, sales heads, CMOs, CEOs etc. But you need to get your hands dirty and be prepared to do real work again. You may be a very polished presenter – so many employers’ today, would love to get their Group B-ers trained to deliver better sales presentations. Moreover, I keep having enterprise clients complain to be how bad service providers are at selling to them – so why not offer up your services to help them improve their selling techniques and “listening” skills etc? And you’ve likely lived through years of change and staff mentoring, so why not offer yourself up to support change management workshops or reorientation / Design Thinking programs. Use those skills and experience to become a great student teacher!

Avoid burnout and prepare for a new financial structure in your life. Len does a very admirable job advising people post 50 how to be smarter with their money. I am not a financial advisor, but I would say that we need to be realistic about our earning potential, as our careers advance. If you want to command serious wages post 50, then you either need to be in a very safe position in your current company, or you need to be smart about how you manage your work/life balance, as you may be working well into your 70s these days. You have a great deal of experience and knowledge to offer, but most companies, today, just don’t want to pay the 300k+/year salaries to enjoy your delights. And even if you are a great survivor, the chances are your company will find ways to wind down your gargantuan salary over the next 3-5 years – and they will burn you out in the process – it’s going to be miserable. So be realistic, figure out how best to go independent as an expert contributor / consultant, or even stay with your current employer on a part-time status where you can do some extra curricular things to to up your salary if you need the extra money. Many employers increasingly love experienced folks as part-time employees – they get the expertise they really want and feel like they get real value for money from them.

So focus on your lifestyle a bit more – how can you early $150K a year for the next 20 years and enjoy your life, than giving yourself a heart attack trying to survive the next few years of disruptive hell and our legacy business attempt to drag themselves out of the Dark Ages? The business world is changing and that fat salaried job for life is really fast slipping away… so be realistic, become a student again if you have to!

I have spoken to nearly twenty client references in the current Workday Services Blueprint research project. I fully expected to talk to many ‘Human Resource’ Directors or IT experts assigned to the ‘HR’ division, as the Workday HCM product has been the most prominent deployment in this market. It has been refreshing to speak to several executives with the word ‘People’ in their title. For example I’ve spoken to a People Services Technology Leader, a Program Manager for People and Culture and a Solution Specialist for People and Culture.

Over the years I have seen some fascinating titles, including many that don’t actually give any clue as to what the person actually does all day. The funniest are the ones where the person has obviously tried to get as many hot topics into the title as possible. ‘Hi. I’m the Chief Worldwide Evangelist for Innovation and Digital Transformation, leading with Design Thinking As-a-Service.’ Huh? It is refreshing to talk to executives who do not need lengthy explanations of their job title. ‘I’m the People Person’. Fantastic! How easy would it be for employees, customers and suppliers to just be able to call the front desk and say, ‘Hi. I’d like to talk to the People person please.’

When I first started out as an analyst, mentors explained to me that IT services was about the bringing together of people, processes and technology. It seems that it has taken most of my career before anyone is actually focusing on the ‘people’ part of this equation. Finally, buyer enterprises and service providers alike are focusing on hiring, motivating and retaining the best talent as they realize that people are their most important differentiator in the market. It is no surprise that enterprises are asking to interview delivery teams in the service provider selection stage, nor that the best client satisfaction scores are attained because of the quality and collaborative nature of the people they worked with. And the best people need to also be people oriented. Technical certifications, relevant enterprise size and industry experience, functional expertise – all these things that can be ticked off on a capability list are important but increasingly taken for granted. The real skill lies in whether they can actually work well with other people. Do they have the necessary social skills and real commitment to help clients and employees? These are the valuable skills needed for enterprises and service providers to succeed in today’s market. Power to the People!

HfS has launched the 2016 Workday Services Blueprint, in which we are assessing the capabilities and vision of 16 Workday service partners. Since the first Workday Services Blueprint published in 2015, this market has exploded. Service providers have been busy investing in organizational structures, acquisitions, partnerships, service development and talent retention programs to remain competitive (see: The Speed Of Change In Workday Services). In our upcoming Blueprint we will assess these strategies in detail and determine who is currently winning the differentiation battle.

Many of the enterprise leaders we have spoken with have indicated a clear corporate strategy to move to cloud applications. Enterprises of all sizes realize that they need to have modern systems to support a more innovative outward looking strategy. Old legacy systems that are clunky and fail to meet business needs in a timely manner are rapidly falling out of favour, and enterprises of all sizes are now seriously considering Workday Human Capital Management (HCM) and/or Financial Management products to bring their processes up-to-date. While most enterprises started with the HCM product, before considering the financials application, others have started with a financials implementation. Either way, clients see the value of running both products on the same platform, aligning with Workday’s own vision for this market. Interestingly enough, enterprises are selecting Workday even if it does not match all of the functionalities of the competitive solutions, because they value Workday’s vision and focus on continual innovation.

Additionally, clients are highlighting that having strong resources is the number one selection criterion as well as the main reason for high client satisfaction rates post deployment. Buyers often request to interview the actual deployment team in the RFP stage. They want to meet the people they will be working with on a daily basis, as ultimately that relationship will determine the success of the project. For their part, service providers have been investing heavily in talent development and retention programs to offer increased career opportunities as well as develop more rounded consultants that are able to support clients at different stages of the development and management cycle.

The real differentiation in all SaaS services is all about ‘how’ a service provider engages and delivers its services. This includes collaborative engagement methodologies and the ability to communicate the ongoing business effectiveness of the Workday solution for clients.

We look forward to sharing more insights from this research over the next few months, before publication of the full Blueprint report in September 2016.

Doing business is all about making successful deals happen and negotiating them effectively. Getting deals done right says something about your own personal negotiating capabilities, but most importantly, it speaks volumes for your company’s brand.

By following the following five simple tips, you get a better sense of what to do before entering the process of making a deal.

Understand what you are selling: Make very sure you understand your core business. You can only negotiate what is there and what will ultimately be delivered. Understand what people can do within your firm, or what your software is really capable off. Only when you truly understand your capabilities, can you negotiate the best deals for your firm.

Be aligned with your internal team: Make sure that your team is aware of your progress when entering negotiations. You do not want them to walk into your line of fire because you need to be in control. If you are not aligned internally, then don’t make a deal. If you do not have the support of your team to deliver what you are selling, you are in serious trouble. No one wants to work with a sales person who sells hot air then runs for the hills once the deal is done. You sell a bad deal your firm can’t deliver; you will quickly inherit a terrible reputation that you could get stuck with for a very long time. So make sure your internal agenda is in order before starting the negotiation process. I use the parent approached here. Daddy said no, and so did Mom.

Know your competition: Make very sure you understand the competition in your core business. Know what they offer and their pricing and services that come with it. Never take someone else’s word for it – make sure you know what you’re up against. Deals are often made based on trust, but trust is earned and is never based on assumptions. And really make sure you sell your firm’s value, not just try and react to what your competition is selling (or what your client is claiming your competition is selling). It is not always possible to compare apples with apples, but you need to be able to explain your own firm’s value and approach – and do it very effectively.

Stick to your plan: Never abandon your calculations. This has nothing to do with ego, although people love to play that card. Ego should never be part of negotiations. Only inexperienced people use their egos or job titles, and they always fail in the long run. If you take your clients’ and your own business seriously, your negotiating plan will always back up the numbers.

Make sure it is all about doing business: Don’t you ever make it personal. There is no “me” in negotiations. You deal in the “we” form because it is never personal. Unfortunately, there are many people out there that like to annoy you, but if you follow steps one through four, you will frequently achieve a very positive outcome.

So always stay true to yourself and your company’s values. Keep communicating and only sell based on value. In the end, personal value and business values are the most important aspect of deal negotiations. Value is in the mind of the buyer. If it is not, why are we negotiating?

Unless your contact center clients are all blunt Bostonians like me, they may not be in your face about one thing they need that you’re not giving them – customer experience delight beyond the standard service delivery. Maybe customer service leaders get so harassed on the job, they just hate to complain themselves when their expectations fall short!

As a service provider hitting all your KPI metrics, delivering the services the contract requires, you might be completely oblivious to an undercurrent of dissatisfaction, even among your most seemingly happy service buyers. We interviewed many contact center clients for our recent Contact Center Operations Blueprint report and the one resounding piece of feedback, even from clients that achieved Winner’s Circle glory, was that service providers need to be much more proactive, in particular with improving customer experience. Omnichannel discussions have got them thirsty for ideas, and they want leadership and guidance. They are hearing “digital customer experience” everywhere and need help with how to approach it. So while business is humming along as usual, and buyers may not be telling you directly, they’re wanting a lot more from their contact center providers.

This is not to say providers don’t have the capabilities. There’s some pretty exciting stuff happening in this space, and contact center providers have been eager to rave to us analysts about things like omnichannel platforms, customer journey mapping, sophisticated analytics and the like, which could all somehow get baked into “proactive” ideas for clients. It seems like these value added services are landing on the ears of new logos, but many long term clients are unaware that their providers had these capabilities. In fact, most of the clients we spoke to were only using their service providers for basic phone and email customer service and not much else. No doubt being a trusted, reliable partner is still of prime importance; it’s the foundation of every successful contact center BPO relationship. A lot of these relationships are long term, stable, comfortable relationships. When things are going well, why rock the boat?

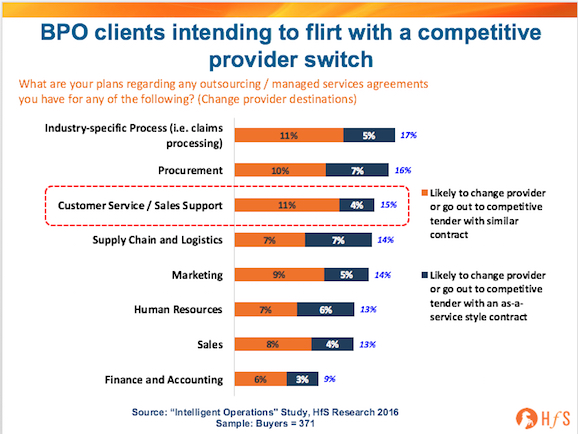

This doesn’t necessarily mean that buyers are lining up to jump ship on their current providers, but, as one buyer put it, regarding transforming for digital customer experience, “I started on this journey with them but don’t know if they can keep up the pace in the future.” Times are changing, and rapidly, for contact center dynamics. Consider that new HfS research covering 361 major enterprise buyers indicates that 15% of customer service/ sales support buyers are likely to change sourcing providers when their contract is up, combined with an increasingly competitive marketplace, and you realize that breaking up may not be that hard to do in this space:

Along with this need to showcase higher value CX services to key clients is also a recognition of legacy engagements that need to morph or face imminent danger of extinction. One buyer reference I spoke with from an office supply chain had 700 plus BPO agents, many doing data entry of B2B orders that are faxed in. He praised his service provider’s work, especially their ability to meet SLAs. This is problematic for many reasons. For one thing, in the short term view, OCR can likely do most or all of the work those agents are doing. For another, who still wants to submit an order via fax? This company needs to implement an online ordering system or will be out of business in short time. One way or another this contract is going away in the foreseeable future. So now is the time to take the opportunity to step up and to help roll out an automation strategy, assist the client with digital transformation and customer experience by designing and setting up web ordering…. or just wait a while and let it die a slow death on its own.

The Bottom Line: The comfort zone has become a deceptive place for unsuspecting providers

By not stepping up to this call for action, service providers are missing opportunities to establish better client relationships, leaving money on the table, and burying their heads in the sand about the quality of their client relationships—and the future of the contact center business. This business is fast commoditizing, with many providers chasing too few clients – if you fail to do anything more that the basics you could be in for a rude awakening come renewal time. So be proactive, go see you clients and ask them where they aren’t being delighted – and come equipped with plans to surprise them.

While we all are debating the impact of Brexit, I feel that Brexit will be advantageous to Indian engineering service providers in the long-term, both in the post-Brexit UK and EU marketplaces. And it’s not that I am biased as I cover engineering services sector – so here are some reasons for this hypothesis.

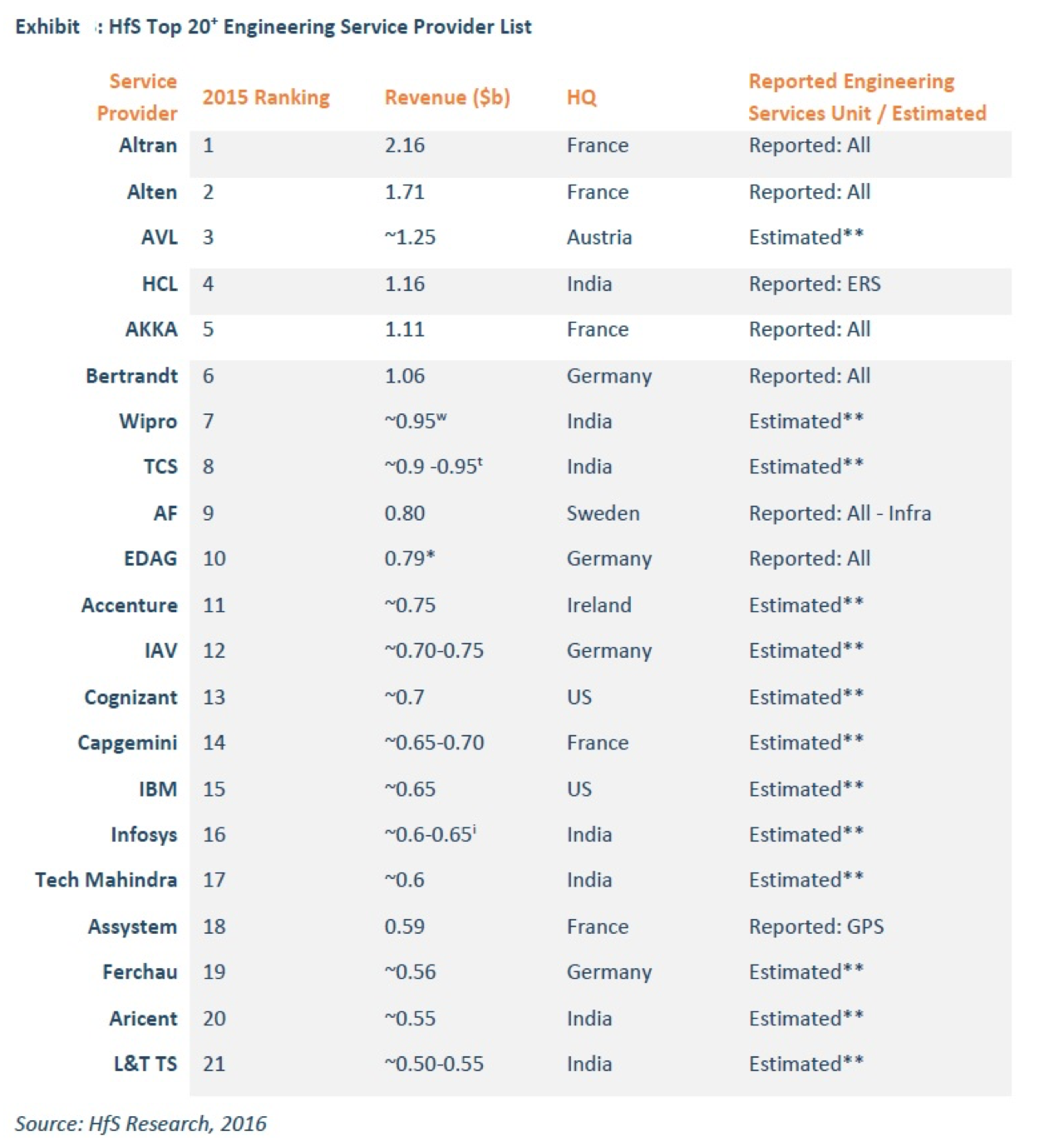

First, some context around the global engineering services outsourcing landscape. The global engineering outsourcing service sector is somewhat unique as it is dominated by European companies (mainly French, German and Austrian Firms). In the top 10 list, there are three French firms, two German firms and one Austrian firm. (Read HfS Engineering Services Top 20)

I don’t know any other services segments which are dominated by European firms to this extent. And there is a reason to this European dominance; product engineering is a core business activity for enterprises which many were unwilling to outsource in the early days of outsourcing, unlike transactional IT Services and BPO services which are not core activities and can be better managed by experts. Product manufacturers’ “secret sauce” that has kept them competitive, has traditionally been their internal design and make capability. It started with Airbus, which wanted to accelerate its product development to compete with Boeing and started leveraging local outsourcing partners to access the expertise it needed to be more competitive. This led to the scaling up of the French engineering outsourcing industry, as more enterprises saw the potential of outsourcing for engineering competency in a country with a strong engineering culture. Still, Airbus will be one of the biggest customers of all leading French engineering service providers and Aerospace being of the largest verticals. There’s a similar story with the German automotive industry. The German automotive firms started outsourcing to local outsourcing partners to accelerate product development to compete with US and Japanese automotive OEMs. In the last few years, there was a lot of M&A among the engineering providers and few French and German firms have scaled-up and surpassed a billion dollars in revenue. Still, European engineering services firms will have automotive and aerospace as their largest verticals.

In contrast, Indian engineering services providers became US-centric and followed general IT services industry footprints. Their largest verticals, for engineering services, are the telecom and software markets. In Europe, Indian engineering service providers have struggled to penetrate the French and German engineering sectors and compete effectively with the local European engineering services firms. When the overall corporate focus for the Indian IT service providers in Europe has been UK-focused, it has become difficult for engineering service providers to leverage their parent companies for to win business in Germany and France. Many engineering service providers have realized this of the late and started locating their senior management to Germany. Simply put, Germans like to buy from Germans and the French from French!

Now with Brexit, Indian IT service providers will reevaluate their European strategy and probably France or/ and Germany will become the center of the action. The language barriers will be taken care of. And this will help engineering service divisions to sell their story and capabilities better in the German and the French markets.

The other factor will be engineering demand in the UK. It is estimated that the UK is facing increased shortages of engineering graduates in the manufacturing sector. According to 2015 estimates from EngineeringUK, UK manufacturing sector needs, on average, 182,000 people annually with engineering backgrounds through 2022, and supply is only at 108,000 people annually. These numbers will be revised downwards post-Brexit, but it should be reasonable assumption that after Brexit, UK will face further supply crunches in the engineering sector as it will rely less on EU engineering talent. This will be an opportunity for Indian engineering service providers to get in and win the higher share of UK engineering services industry.

The Bottom line: It’s all upside for Indian Engineering Providers post-Brexit

There are lots of ifs and buts, but I don’t see any major potential downside to Indian engineering services business from Brexit. It can only provide further opportunities for Indian engineering service providers to increase their spread and penetration both across the EU and the post-Brexit UK. It’s the European service providers which need to worry more now!

There was a time when “learning on the job” meant you were an apprentice or a “newbie,” someone with little practical experience. However, today, “learning on the job,” is a critical activity to do all the time, as digital technologies and business models change the way we work, not a little, but quite significantly and often at a breathtaking pace. There is no defined curriculum for the pace of change in today’s businesses—it’s a capability we must all be very adept at—dealing with a constant flow of new ideas, new technologies and ambiguity that takes us outside our comfort zones.

The expectation today to drive faster time to market with new ideas, faster response to queries, and faster results from the work we do is also impacting the services and outsourcing industry. This industry grew up based on a culture of “getting the job done faster, cheaper, more efficiently”… and as those expectations are met… it’s still true. And because many companies can meet the cost reduction baseline, differentiation now depends on quality, innovation, and not meeting but beating expectations. And that means constantly evolving.

Do you need to shake up your outsourcing engagement to redefine the value and create a new way of working together? A way to bring “both sides” back to the table? To build on a trusted relationship, one that is collaborative? Nothing creates a team like solving a problem together. There needs to be some degree of trust in place—either through experience or through reputation and recommendation. Design Thinking is also gaining interest and traction as a way to identify and solve a problem as a team in a services relationship. The bottom line is that the way forward for outsourcing—service buyers and service providers—is based on willingness to learn… experiment… and start over.

On the Job: Learning by Doing is the way forward

To make it work, service providers—and many service buyers too—need to step out of the risk averse and “no fail” “yes” culture. By nature, Design Thinking requires more of a “learning by doing” approach. And it may take awhile to yield measurable results. In one example, a service provider launched a Design Thinking exercise to address a very general interest—to reduce the cost of their collections process. Reducing collections would help the client but also may hurt the service provider as that was their job. But this problem of the cost of collections is not unique to that one client or to one industry, so anything learned could likely be reused.

While the project was focused and undertaken with a specific client, the learnings, regardless of whether they led to more work for the client, would still increase the understanding of the service provider team of the consumers in that industry and the experience they were having at the time. In this way, it became a learning exercise as well. It also focused the service provider on the clients’ consumer base, increasing the understanding of the context of their work.

The interaction between the service provider and the service buyer’s customers brought to light some opportunities and challenges that would not have been noticed without a service provider employee “shadowing” someone living the process that had been in place for years. This effort was not about changing the process per se, but about changing the focal point from the process itself to “who” was in the process—to the experience and the desired outcome. That’s a pretty new way of working in the outsourcing industry.

From the observations and interviews, and studying data collected over time from its call center, the service provider came to the table with the client with an informed, but different, perspective, and with some ideas on what to do next. Some of these ideas were ones that interested the client and led to further plans and projects. Some were not, and others were simply put on hold. The point is, the service provider took the first step to say, let’s try this—with the client’s permission and participation—and invested in those first steps.

The Bottom-line: It’s about courage, budget and stories

This exercise tapped into the three partnership “Power Ups”—the courage of the service buyer to let the service provider get close enough to their customer base to interact with them personally; a budget for the shadowing and testing ideas; and stories—those of the consumers that drove the next steps toward change and business impact—and that of the project overall. Are you ready to tap into your inner “gamer,” and partner to Power Up to drive real, impactful innovation?

Superhero movies have been particularly popular over the past several years, but long before then they’ve been a staple of our culture. We love the hero coming to save the day, helping fellow citizens and making the world better. In the movies (and in real life) there are superheroes who save countless people from human trafficking, sweat shops, and other dangerous conditions. I want to be a superhero and do these things too. And guess what? I’m going to do it. How? By helping companies buy IT products and services ethically and by helping suppliers create new opportunities for themselves and their people.

Will you be a superhero with me? Here’s what we can work on together to make our world a better place:

Buyers, make it your mission to use sourcing for the good of your company and all workers/locations touched by a deal.

Source ethically. Searching for the lowest cost labor (and then negotiating even lower rates) often can lead to firms ignoring warning signs of poor ethical labor practices. Don’t be one of the companies that will choose the lowest price over a supplier that treats it workers fairly and gives them good working conditions.

Don’t rush through compliance and treat it as a “check the box” activity. Use compliance and regulatory requirements to shine a light on where your value chain can be improved. Try to exceed regulations on supplier ethics and work practices.

Monitor, test, and remediate on supplier compliance obligations. It’s expensive, annoying, and time consuming to audit whether suppliers were telling you the truth on their security, compliance, and other obligations. Do it anyway. It’s important for your legal and regulatory obligations. It’s also important for you as you try to make the world better. Hold your suppliers accountable – make them fix what’s wrong or pick different suppliers.

Suppliers, use new technology to create opportunities. Don’t just settle for doing the same thing with fewer people or for less money.

Use automation to find new ways to employ your talent and spend more on retraining before choosing staff reductions. HfS’ latest research shows automation taking away about 1.4 million jobs. Will you just take those jobs (and people!) out of your company, or will you find new things for them to do, new places to invest, new frontiers to explore? Don’t get lazy and settle for doing the same thing faster and cheaper. Find new things to do and create more opportunities for your people and your clients’ people.

Show clients your worker conditions and how you’re making the world better for your people and the communities where they live. Clients need to know you’re following legal and ethical practices. Go beyond that to proactively showcase the programs you have in place to enhance the lives of your workers. Turn corporate social responsibility into a differentiator.

Follow compliance guidelines in practice, not just on paper. Just like buyers need to make sure they’re not just “checking boxes,” suppliers need to make sure they follow the spirit of these regulations and use them to drive business and worker improvements.

Influencers (analysts, deal advisors, self-proclaimed evangelists,) Find and expose areas where the market is hurting workers and communities, and talking about ways to fix those areas.

Educate the market on opportunities coming from new technologies and service models. Many of us in this space are automatically attracted to new things and shiny objects, so this one might not seem difficult. But as you look at these new areas, get beyond the sunshine and roses to discuss downsides and how to avoid them or to balance those negatives by positives in other areas. Explain to buyers why ethical sourcing is important for their specific engagement and for the market.

Help buyers find suppliers who can collaborate on the superhero-mindset of the market instead of road-blocking it. Clients that want to find suppliers who are legitimately invested in avoiding issues like poor worker conditions need help from advisors who feel the same way. Make worker conditions, people issues, and other similar areas a more explicit part of selection criteria and educate buyers on how to validate supplier responses to those criteria.

Guide suppliers to find ways to deliver services that treat employees fairly, serve market needs, and create growth opportunities for both suppliers and clients. Just as suppliers should find ways to expand the market as new technologies emerge, influencers should work with them to discuss how suppliers can operationalize their ideals.

With no physical danger to ourselves, we can help stop poor working conditions, human trafficking, and a host of other challenges affecting the world right now. We only need to do our existing jobs well. I want to do that. I want to be a superhero. What about you?

At HfS, we’re growing fast in a very competitive and volatile market… and with growth comes change – but change is always good if you ask me! The most fun in jobs is when you have changed – you learn new things, get new ideas and you meet new people to help accommodate the change. Nine months ago, we needed to add more firepower to our sales function. To be precise, we needed top sales quality that could thrive with the HfS mentality and culture. We found that person in Samyr Jriri (see bio), and today I wanted to give you a little more background about him.

Bram Weerts, Chief Commercial Officer, HfS: Samyr, can you share a little about your background and why you have chosen sales as your career path?

Samyr Jriri, Vice President, Global Business Development, HfS: Next to having owned a small restaurant and antique furniture business, I started out working in the Telco sector here in Belgium. That was just at the time when the monopoly held by the – at that point – state-owned Telco provider, was broken up, and I joined it’s first big competitor. After spending about five years working for the two largest Telco providers in Belgium, I joined Microsoft where I focused on the upcoming Dynamics platform and later on became a generalist, managing a portfolio of top and mid-market clients. In those days I wasn’t too familiar with the research industry yet until I moved to London and joined Gartner. There I spent seven years, mainly working with startup and midsized tech providers, as well as helping set up the account management team for their Supply Chain business in Europe post the AMR acquisition during my last year there. After that, I went to Kea Company, a consulting business in the analyst relations industry, before joining the HfS team. Sales were always in my blood I guess, I always had an interest in this multi-faceted discipline, from the perspective of an individual contributor as well as from sales leadership point of view. It’s one of those arty sciences that touches upon many principals that are applicable in daily life. I also always enjoyed the meritocratic character of a pure sales role, where I think this philosophy had a motivating effect on me.

Bram: Why did you choose to join HfS?

Samyr: Being active in the research industry for quite some years, I was already familiar with HfS before joining. I guess HfS had a high likeability factor as a new upcoming brand, but my sympathy for HfS went further than that. The As-a-Service Economy really isn’t covered by any other analyst firm in the way that HfS does it, and it profoundly resonates with where the market is going. On top of that, I liked watching this ‘new kid on the block’ who came to challenge the conventional business models of the bigger analyst firms – and successfully so! Everyone talks about change, innovation, sharing and all that good stuff, but in practice, we often see the low-risk safety approach. So for a young research firm to put out 70% of their punchy and high-quality publications for free, shows a great understanding of how information and insights should be treated these days, as well as courage to do so in today’s economy. That was all before I got to meet the team here, where I discovered the pleasure of being part of the HfS family.

Bram: What are the focus areas on driving your revenue?

Samyr: The research and advisory business are all about the relevant exchange of information and insights that fuel business decision making. What we sell is not transactional, nor is it tangible, so relationship and trust are essential. In our efforts to grow the business, we focus on matching our capabilities against our clients’ priorities, as well as ensure that the ecosystem we build up is compatible with the trends we see happening in the market. Sales are the growth engine, which fuels the investments in talent and content, which in turn fuels business growth and market influence. This principal needs careful discernment.

Bram: What trends and developments are capturing your attention today?

Samyr: I think that we are living in great times, there is great insecurity of course, but great opportunity equally balances that. It’s a cliché sentence, but it seems that the fabric of our current organizational structures is being pressured so much that we will start to see real change in how people organize themselves from the bottom up. It can be observed in the business world as well as socially and politically. The automation trend is a great example; there are many doomsday predictions of disappearing jobs and the redundancy of human labor. This only used to be true for mechanical processes, today it is almost equally applicable to cognitive processes. It’s the organizations’ actual choices that will determine whether we will experience the automation continuum as positive or negative. One thing is for sure, at some point, the entire organizational premise on which automation solutions are built will need to be revisited. This will initiate the real change.

Bram: And what would you like to see different in the research / services industries?

Samyr: We already see the beginning of an important trend that I would like to see move a little bit faster: companies should refrain from taking a directive role towards their service providers by just telling them what they want from them and move towards treating them as equal partners, which allows for more dialogue leading to better solutions. Only when this dynamic is truly in place from both sides will we see real innovation. But it takes some time to learn to let go. It remains hard to let complete control slip through your fingers in exchange for projected innovation and improvement.

Bram: And, what do you do with your spare time?

Samyr: I love cooking; I am a bit of an audiophile, and I enjoy traveling as well as hiking.

Bram: If you could change one thing in Sales what would that be?

Samyr: I think a lot of sales efforts across markets have created a dynamic that is seen as normal when it comes to negotiations. If you can get a 50% discount on a deal, you might be happy with that cut. However, I see that as a total loss of credibility. Every company is trying to create customer loyalty, meaning no matter how transactional your business is, you need to build trust. A correct pricing strategy should therefore not allow for ridiculous discounts, which in the long term only creates unnecessary confusion with the buyer, as well as often cannibalizes long time opportunity for the seller anyway.

Bram: Thank you for your time Samyr, it’s a real delight to have you onboard and work with you in these exciting times!

SYNNEX-owned Concentrix today announced a definitive agreement to buy Canadian born Minacs, previously owned by Indian conglomerate Aditya Birla Group and presently owned by two private equity firms. HfS estimates the combined entity will easily surpass $2bn in 2016 and is a singificantly show of force to the rest of the contact center industry.

SYNNEX-owned Concentrix today announced a definitive agreement to buy Canadian born Minacs, previously owned by Indian conglomerate Aditya Birla Group and presently owned by two private equity firms. HfS estimates the combined entity will easily surpass $2bn in 2016 and is a singificantly show of force to the rest of the contact center industry.

I think I just read one of the most (brutally) honest and practical

I think I just read one of the most (brutally) honest and practical