A couple of months ago we wrote about meaningless data – the seemingly endless spew of pointless information that just starts to grate. Recently, we’ve started to see another related category of pointless crap – which is probably going to become more prevalent as organizations seek to increase the ease with which information is conveyed to a public that cannot be bothered to read anything anymore.

The category that is pointless crap visualization (PCV). Where an attempt is made to visualize something, often a relatively complex concept and it fails utterly to get the point across. But looks nice and gets attention because they drop some names of big vendors in there.

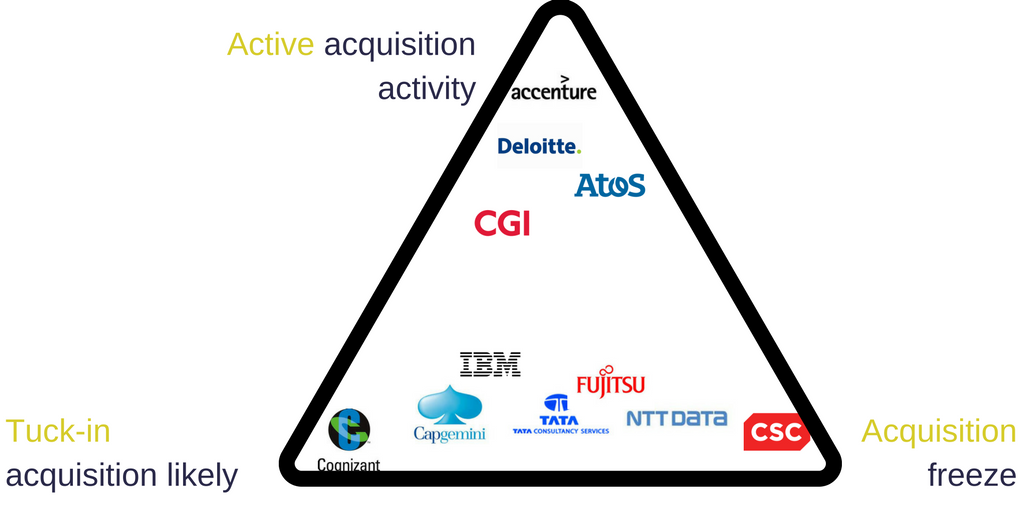

We recently noticed a thoroughly confusing diagram from one of our analyst colleagues, NelsonHall, that caused us scratch our heads in utter bewilderment:

PCV From NelsonHall

The diagram is supposed to tell you something about the acquisition strategy of the companies in the triangle. We wrote down a couple of questions about what the chart meant, having not read the associated blog post.

It looks like Cognizant is more likely to make acquisitions than IBM? Really? Which seems highly unlikely given the huge difference between the two companies in the past – and the fact that Cognizant has a much smaller war chest for M&As, especially after its massive $2.7bn investment in Trizetto. We suppose you could limit to purely IT services – but a tuck-in acquisition is just as likely to be IP based as it is additional niche skills. Although even then we’d expect IBM to spend a great deal more – its Software group having notorious deep pockets for acquisition. Cognizant have made some significant acquisitions like Trizetto, but like all the offshore firms have been pretty gun shy when it comes to inorganic expansion compared to the big traditional technology firms.

Cognizant/TCS are more likely to acquire than NTT or Fujitsu? Mmmm… Fujitsu has been fairly quiet on the acquisition front for a few years, but you cannot count them out of the acquisition game – they made a few acquisitions in 2016 and made some very large purchases in the past. Given their cloud capabilities in Asia, it seems likely it would want to build on consulting capabilities particularly in Europe and the US. And NTT – certainly we may see a lull in activity as Dell Services gets absorbed, but NTT has been one of the most acquisitive of the services firms over the years, so this again seems slightly at odds. This seems much more likely than TCS, the least acquisitive of the already reluctant offshore providers.

The inclusion of CSC using the CSC logo… er seems a bit unnecessary. In fairness it may just be the choice of CSC as the logo – but CSC is part of HPE and no longer exists – so we do wonder how useful it is to know they won’t acquire…

Also, what is the difference between a “tuck-in acquisition” and active acquisitions? To say that IBM is not an active acquirer seems odd – again it may be a narrow view of just the IT services business, but we’re not sure that view really helps anyone considering IBM as a partner given that any software acquisitions bring IP which add to the richness of the services offerings.

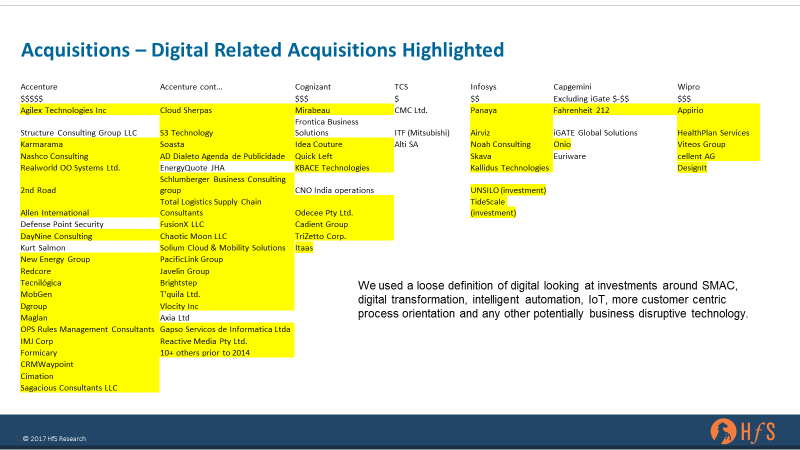

Again the distinction between active and tuck-in is not clear for Accenture – which is certainly the most acquisitive and has a very active strategy with an acquisition made seemingly every week, but some of these will be tuck-in, maybe half of them? You can judge for yourself and look at the list of Accenture acquisitions we tracked in the table below. We did some work on which providers are making digital acquisitions – not with the same list of providers, but it illustrates the scale of Accenture’s acquisition activity, compared with some of the providers on the NH diagram. So we’re not sure the visualization really captures the huge difference in acquisition trails between Accenture and the other pure services companies on the list.

HfS – Just The Deals

It is a challenge to come up with good visualizations – that support data and summarize points being made. We have some way to go converting our list of contracts above into a statement about the different players – but I think if we do something around our acquisitions data we’ll probably convert into an index and visualize as a quadrant (oh no) or a simple bar chart. So in a way you have to applaud NH for trying something new.

To be fair the associated blog made a lot more sense – but the chart fails to reflect what is said or adds much to the understanding – it just throws names at you without any clear reasoning. What the diagram needs to do is illustrate a point or, ideally, provide a short cut to understanding. This doesn’t seem to do either. Frankly, it just obscured any of the valid points being made.

The Bottom Line – in this era of fake news and poor information, analysts have more responsibility than ever to reflect reality

This year HfS is making a clear commitment to visualizing our information better and trying to make our perspective in as clear and concise a way as possible. Like the above chart we may not always get it right – but hopefully, that is where our community comes into play and you will let us know what we get right and what we get wrong.

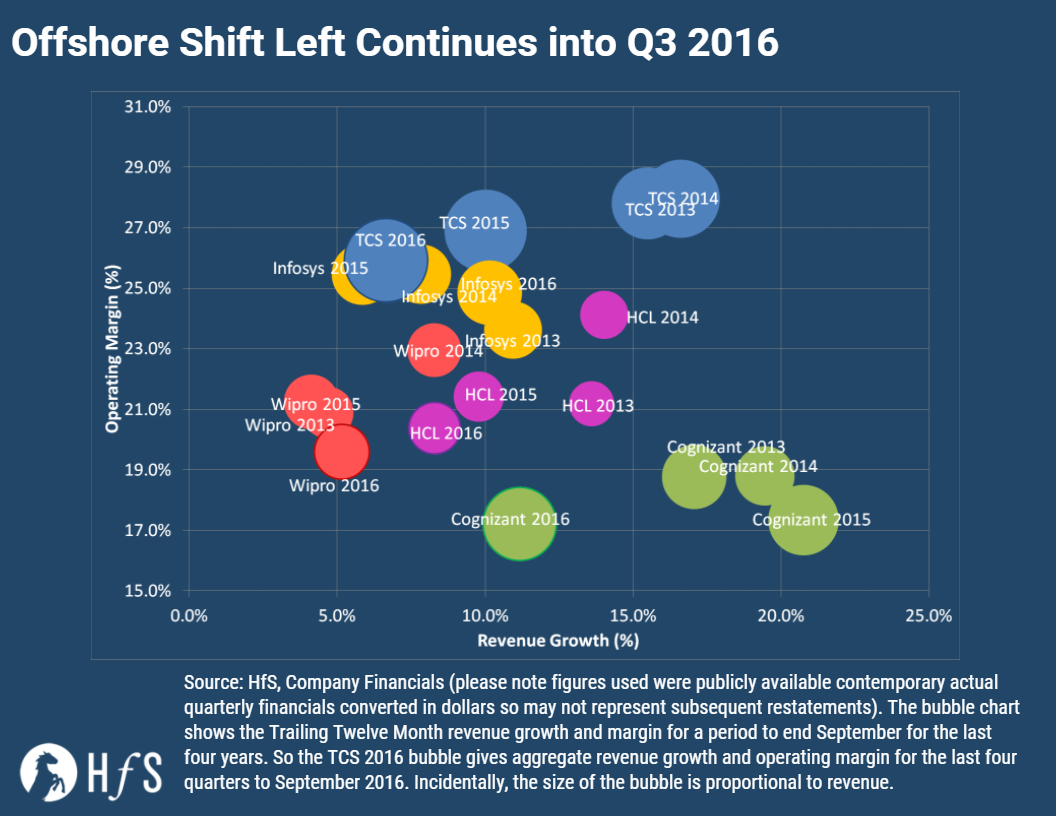

Back in August 2016 we wrote about the shift left with offshore providers – we were recently reminded of this piece and asked to update the chart. Which we have done in the chart below. It’s interesting to see if things have progressed, and as a prelude to the new results season approaching rapidly…

These results add fuel to Phil’s thought in his Bandaid economy blog. With more traditional services markets slowing, largely because they support older business models. At the same time we see a rapid increase in wealth being generated by enterprises that are tapping directly into digital business models – with the digital pure plays like Amazon, Airbnb, NetFlix, etc. and the rapid adopters like Tesco’s, CapitalOne, Staples, The Gap, John Lewis… Service providers need to find a way to tap into the money that is flowing into the technology and talent to fuel these increasingly ubiquitous digital business models.

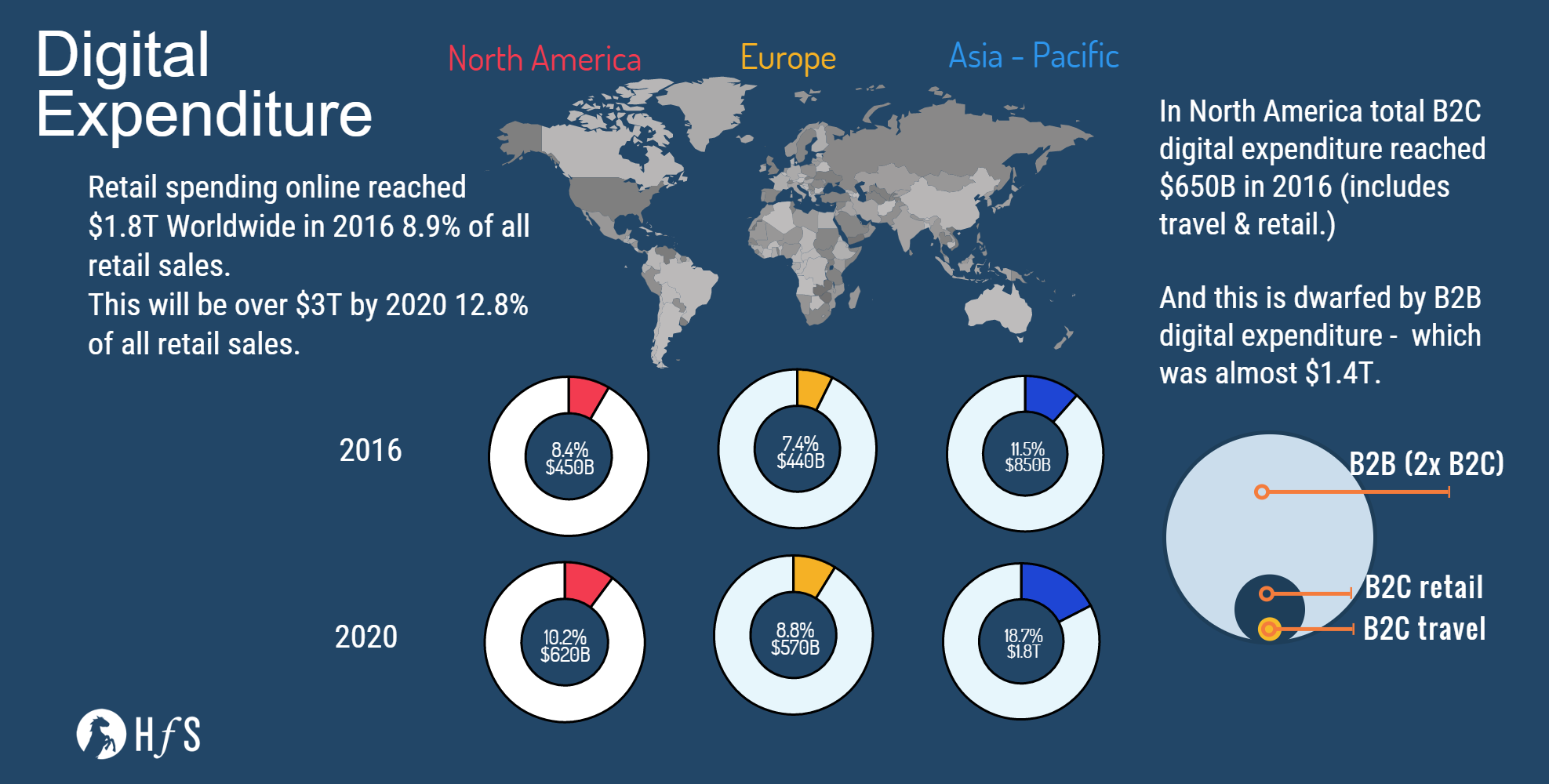

We have been looking to quantify the total opportunity for the digital expenditure or the “flow of revenues over digital channels between business and consumers”. We have started by quantifying the digital retails sales, but will expand to include business to business digital sales, travel and financial services expenditure. But below is a taste of this exciting work – with digital retail center stage and some estimates of the other components for North America to the right.

The Bottom Line – let’s just say it again…

As we have said before long term success in the services market is dependent on inertia or the lack of it. Providers that are reacting quickly to the changing market conditions are still finding growth, and this growth is shifting from purely low-cost or offshore providers. This is starting to show up in the financial results more and more as services firms customers ambitions drop, revenue growth fades. The “cut until it bleeds” continuous cost-saving model for operations is creaking badly, especially in light of new technology solutions and an increasingly competitive environment for many traditional businesses.

We will be taking note of the full calendar year results that are coming up this month and next. But we expect the current shift left to continue as providers adjust to the market realities.

Maximizing team performance and improving employee engagement are both winners in their own right as HCM themes to focus on. Solutions that focus on either are correlated with better business results. ADP and its clients can now play in this arena with the strategic acquisition of The Marcus Buckingham Company.

By many accounts, including mine, ADP’s past acquisitions of companies like Workscape, Virtual Edge and The Right Thing, while accretive to revenue (not necessarily a game-changer on a base of over $10 billion) and enabling a more diversified solution and customer portfolio, didn’t fully detach the company from its long-time transactional HR / Payroll branding. Yes, Workscape did bring cool technology around total rewards and portals, but ADP also talked a lot about their new benefits admin outsourcing capability after that acquisition.

The bold move of adding The Marcus Buckingham Company could pay off nicely for ADP, and in “multiplier effect” ways that, by definition, are much more consequential than incremental revenue or adding some new strategic customers.

Just as SuccessFactors was a clear catalyst in SAP’s embracing of the cloud, TMBC could do the same for ADP; not in terms of the cloud as ADP operates there already. The story here is adding a disruptive HCM solution, one that weaves together technology and services elements to help customers solve issues many HR tech products will never tackle.

Among other things, TMBC’s flagship technology StandOut distils the complexity of a team leader’s job into two fundamental questions: “what are my team members’ priorities, and how can I help them?”. As this will entail a new way of approaching the job for many team leaders, the transition is helped along by targeted and expert coaching, TMBC’s other strength that ADP plans to tap into.

TMBC’s technology and complementary coaching bring self-awareness to the performance management and career development process

Self-awareness/self-discovery is often the missing link in feedback and performance management models and systems. You could say that one exception is when an employee is told their self-ratings are very different than how others see/rate them; however that is “being told” rather than learning it through a guided process. Coaching is also advocated by more and more companies, but most aren’t consistently adept at it enterprise-wide. ADP customers can now benefit from Marcus Buckingham’s proven approach, one centered around individuals fully leveraging their strengths (motivating and energizing) vs. addressing their performance gaps (often de-motivating). The model also clearly fits organizations wanting to pursue a “learning organization” strategy and corporate culture.

While a talent management solution offering the type of capabilities TMBC brings can be ahead of many smaller company’s adoption or strategic interests for some time, this acquisition should allow ADP to finally break free of its transactional HR/ Payroll branding constraints.

The Bottom Line:

The Marcus Buckingham Company found its mother ship to reach the next stage in its journey to greater revenue and broader marketinfluence/impact; and ADP likely jumped on an acquisition that will put it on the broader HCM brand trajectory it’s been longing for. The pairing should bring even more value to ADP and TMBC customers, and broaden ADP’s strategic HCM footprint in those customers, over 600,000 strong worldwide.

As we discussed in Part 1 of the digital marketing operations Blueprint blog, marketers are upping their spend and re-thinking the way they spend on services as a result of digital consumer needs. The market landscape for these services includes BPO/ITO providers, marketing technology companies, traditional agencies as well as a vast array of digital and niche agencies. This is a fast-evolving space that requires multiple players to come together and create an ecosystem for business changing solutions. Many buyer organizations (e.g., PepsiCo) have been very vocal about their dissatisfaction with the traditional agency model and are taking marketing work back in-house, or instead of consolidating providers they’re distributing work to several specialty providers. The opportunity for BPO providers to disrupt in this space is increasing; while it is critical for BPO service providers to partner with agencies, which still have and will continue to have a prominent place in the ecosystem, there is much more opportunity for BPOs to provide strategic level work than in the past. In addition, technology has disrupted the way companies go to market. “Martech” has grown exponentially in the last few years, and managing an increasingly complex stack is the norm while companies struggle with the pace of change to manage these varied systems.

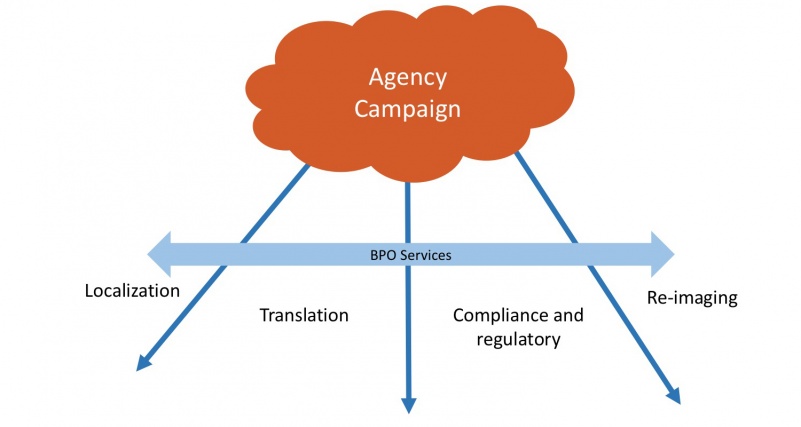

So traditional ad agencies have not kept pace with market changes and thus have opened up opportunities for consultancies and BPO organizations to enter the market in some unexpected ways. The part where BPO service providers play in this ecosystem is often in a paradigm referred to as a “de-coupling” strategy: separating the creative from the production. In this model, agencies set the big picture tone for the campaign but can’t meet the needs for reduced cost and speed that BPO service providers can for services such as localization, translation, regulatory/compliance and re-imaging. The service provider takes the agency campaign assets and reworks them for specific markets, devices, etc.

Sample Content Production Engagement Model

However, many of these services involve elements of creative design and require a blend of talent and automation to execute well. And services buyers are increasingly looking to providers to have more strategic capabilities, especially where the convergence of marketing, sales and customer service happens in customer experience design. Almost every services buyer we spoke to expressed an interest in more strategic, higher value services from their providers.

As in almost every market, buyers are increasingly looking to BPO service providers to get more innovative and hungry for their business. Most buyer references said their providers “do what I ask them to do well,” but these same references admitted there is much potential in the future for handling more strategic services: and many service providers have the capability. Even larger enterprise buyers see potential in moving away from the arrogant and set-in-its-ways agency model and embracing services with a fresher-thinking provider. As one client reference commented: “When you go with a big agency, you’re going to get their B team.”

So how are service providers coming to the table?

Players with smaller practices, such as EXL and Tech Mahindra, have some interesting vertically focused offerings and have the advantage of being able to give clients lots of attention and thought leadership. Customer experience management-focused companies (i.e., HGS, Concentrix, Aegis, Revana Digital) have the advantage of knowing their end customer’s requirements best through the connection of their contact center businesses. While these providers aren’t known as a marketing brand for new logos, with the convergence of service and marketing can often sell bespoke or smaller campaigns with an interesting value proposition to customer experience focused stakeholders. The same goes for ITO focused providers (i.e., HCL, NTT DATA Services), where these providers have solid operations engagements elsewhere in the organization, can leverage the strength of those relationships in the growing digital marketing space.

Companies like Genpact, Infosys and TCS have approached digital marketing operations with a strong stance around automation and analytics. And clients seeking alternatives to the traditional agency model have enabled providers like Cognizant, Wipro and Accenture to excel at an overall vision for digital marketing operations– these providers are acquiring and integrating digital expertise– unlike the traditional agencies who buy up digital agencies and run them as separate entities without as much thought to leveraging the assets of each piece across the organization.

The Bottom-Line: In the rapidly changing marketing services landscape driven by the digital consumer, there is tremendous opportunity for service providers bringing their A team … and it’s anyone’s game

The HfS 2016 Digital Marketing Operations Blueprint covers market trends and direction as well as the analysis of 14 service providers: Accenture, Aegis, Cognizant, Concentrix, EXL, Genpact, HCL, HGS, Infosys, NTT DATA Services, Revana Digital, TCS, Tech Mahindra, Wipro. For more detail—including analyses and individual profiles of the service providers—click here to access and download the Blueprint.

“It is a truth universally acknowledged” that the healthcare experience needs to change – for consumers and clinicians. Part of this change is to make access to data, services, and transactions easier – more “at the fingertips,” if you will—and more relevant to their healthcare experience. In a word, mobility. Mobile is about the platform; mobility is about the journey, the movement of the person, and the experience while in motion. There are a number of mobile platforms on the market today, but who is using them to bring mobility to healthcare?

“…mobility is about understanding where I am, where I am going and what I want to accomplish, and helping to make that journey exponentially better,” said David Sable, CEO of communications firm Y&R in a Huffington Post blog.

Well said. There are a number of mobile platforms on the market today to help make this happen, from well-established technology providers like IBM, PegaSystems, and SAP as well as up-and-comers like Kinvey, Kony, and MobileSmith. And I recently had an opportunity to get to know one offering suite a little better – Skava, which was acquired by Infosys in 2015.

How can mobile platform technology providers bring mobility to healthcare?

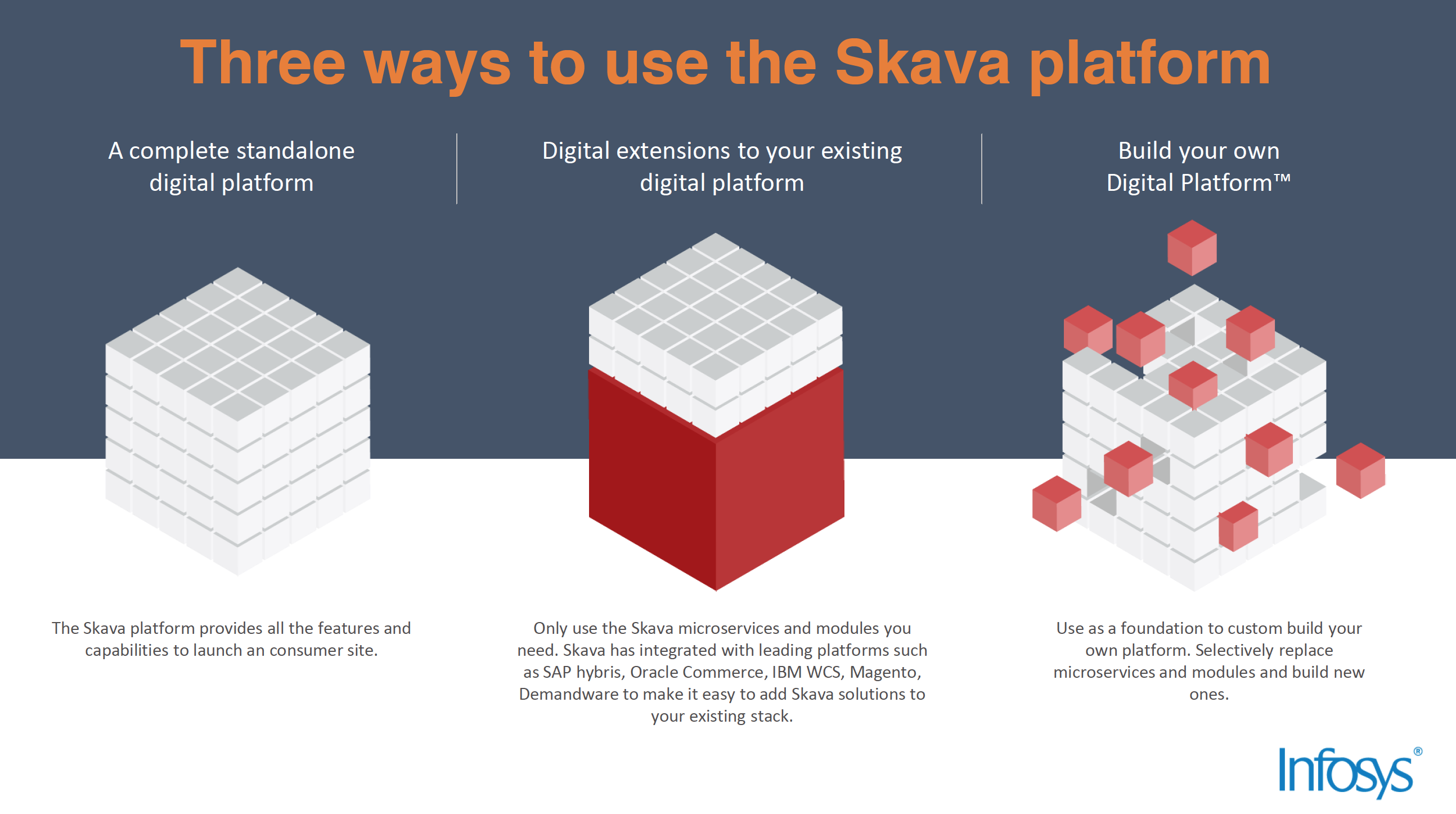

Skava is well established as a mobile development platform in retail, powering mobile apps, kiosks, and mobile devices for Gap, Staples, ToyRUs, and others. Now Infosys is bringing this consumer engagement and e-commerce enablement platform to healthcare. It is developing a set of independent, modular, discrete functional units packaged as “Build Your Own Digital Platform” for healthcare providers and payers. (see Exhibit 1) Imagine consumers, patients, caregivers, pharmacists, and clinicians – among others in the healthcare community – being able to enroll, complete transactions like paying bills, scheduling, care management plans and alerts, etc. Then imagine having it integrated into the core healthcare management systems already in place.

Exhibit 1: The “Build Your Own Digital Platform” Play for Mobility in Healthcare

Infosys isn’t the only one with this capability, so if you are looking at walking down this path, take a look around for what best fits your needs. What I found with Infosys is that even though this solution set is not well established in healthcare, it does have a strong client base and proof points from retail, an industry that is heavily dependent on engaging consumers in transaction oriented interactions. The platform supported $1.5 billion in e-commerce revenues in 2015. Infosys also has depth in IT services across industries, including healthcare, so it has the capability to work with clients to integrated and customize apps and services as needed. The Skava platform does plug into current IT infrastructure. And, the service provider is also better integrating its business services and IT capability so that if you want on-going support that includes data management and analysis, you can tap into extended services and have a single provider.

One “miss” in the story line so far, though, is my earlier point about mobility and creating an experience versus offering a mobile platform. Infosys as a company is investing heavily in design thinking capability – an innovative approach to identifying and solving problems. Yet, when we engage in briefings and look at the materials associated with this solution set, there is no mention of starting first with – what problem are you trying to solve? What opportunity are you looking to address? How are you defining and testing out the proposed solution prototypes with the stakeholders – consumers and business? And that’s a critical first step to ensure that the use of the IT-based solution is truly to address the consumer experience and how that impacts the business outcomes.

Bottom line: If you want people to do something, make it as easy as possible for them to do it. Healthcare providers and payers need to make healthcare services easier for consumers to access, use, and pay for, and mobility plays an inevitable role.

Infosys can tap into its design thinking approach and IT services, and leverage the Skava platform in a flexible way to help clients get there. There are already a number of healthcare management apps and mobile capabilities on the market, so it isn’t new. It is something that if you want to truly be a healthcare consumer oriented organization, you’ll have to incorporate into your business, and partnering with a service provider with IT, business process, and analytics skills is a viable option.

Arvato just announced its acquisition of Bangalore-based Ramyam Innovation Lab, whose stated mantra is to make customers “raving fans” by enabling contact center staff to have valuable customer information at their fingertips. Ramyam’s key asset is its omnichannel platform, Enliven CEM. The platform integrates various communication channels such as email, chat, voice and social media, and uses interaction information to generate individual customer profiles. This is layered with analytics and dashboards; the analytics model aspires to manage customer journeys with “context-based decisioning” in real time, helping agents more proactively solve customer problems.

Our research shows that in this race toward providing digital customer experience, most of the leading customer experience management companies are taking a stab at providing omnichannel customer services. Major CEM providers are starting to/have figured out their strategies for developing 360 customer views that would provide insights to improve contact center effectiveness. To provide progressive omnichannel service support, a CEM service provider needs a strong framework for the underlying data and technology, and that’s what this acquisition is about. Most are taking a third-party approach to enabling the technology, but Arvato’s move provides it an opportunity to have better integration and perhaps move towards providing CEM As-a-Service in the future.

Arvato’s approach is admirable, especially where it affords the company an inroad to one of its key growth markets in India. Ramyam’s highlighted consumer-facing verticals of telecom, retail, banking and travel are key industries for omnichannel customer communication. This also is some much-needed publicity for Arvato, which has fallen behind its customer experience management competitors in thought leadership and demonstrated investment in innovation.

However, all of these buzzwords around omnichannel are used so often and heavily (i.e. “next generation analytics-driven actionability, enabling service providers to deliver superior experience and engagement to their customers”) that they are becoming diluted, making it harder for service providers to carve out a real differentiator with these platforms. Arvato’s assertion that this capability creates “a distinct competitive advantage” is disillusioned. To create differentiation, it will need to use this acquisition to craft and articulate an As-a-Service on-demand, flexible strategy for providing customer experience management—one that provides a single contract with well-defined business outcomes by leveraging technology platforms, data and insights and omnichannel customer support functions.

The bottom line: Kudos to Arvato for making an investment in a young, emerging tech startup with some solid customer experience thinking. But the messaging needs some maturing to really highlight the differentiation that Ramyam can bring to the table.

Whether the combination can help turn Arvato’s end customers into raving fans, we’ll wait and see.

This week the Internet blew up based on news that Intel officials briefed President Obama and Donald Trump on the possibility that Russia had information on Donald Trump that was damaging to him personally and might even have implications for the entire US government. (And while one never expects a hashtag like #goldenshowers to trend on twitter, the feed was hilarious.)

Politics aside, this story is a textbook case of problems with being proactive with threats. Notice: I wrote “threats” not “events” or “incidents” because the incident hasn’t happened yet, there’s just a high potential for it to be true and for it to happen.

You get lots of finger pointing in hindsight. The common question is “what did you know, and when did you know it?” Because, after something bad happens, anyone who knew of the potential for the event comes under fire for not saying something sooner, not being more forceful if in fact they HAD said something, and for not doing something to stop it from happening. The fact is something happened and someone has to somehow get blamed.

And in the Trump intel story, you see the opposite of that, with everyone retreating to respective political corners, defending or dismissing the intel reports based on emotion and personal perspective. And since now that everyone’s already picking sides, it will be that much harder to make the right decision on how to treat the threat risk. So, how do you ask the right questions and take action in time to avoid the impending threat?

Here are the questions predictive security and risk management brings:

When do you flag a threat to executives? It’s important to have a policy in advance so there isn’t confusion later. It could be something like “a risk has been increasing steadily for the past 3 months” to “a risk increased very quickly in a short period” or similar idea. When you raise the flag may have a drastic impact on which actions you take to address the treat, since risks are often time sensitive.

How much do you tell them? Even if you’ve decided to tell executives, you must decide how much information to give. Too much detail and you may panic them unnecessarily, too little and they may not appreciate the implications of the threat. This question is usually harder to answer than the first one.

What do executives need to DO because of the rising risk? Another tricky area, what do you propose be done about the threat? Wait it out and seek more confirmation? Deal with it proactively, even if there’s potential for the threat to not happen? Take interim steps? This is the most important question to be answered when talking about predictive security management.

Focus Predictive Security On Remediation Not Reporting

We don’t know what advice the intel team gave to the government leaders, but we do know there are a few general ways you can deal with a threat or risk:

Accept the risk and go on with what you were doing. Sometimes there’s not much that can be done – or worth doing. For example, there could be a heightened risk of a terrorist attack, but you don’t want to be seen to be weak and encourage them further and choose to ignore it, safe in the knowledge airport security is already prepared for such a threat.

Try to remove or reduce the risk. In a political context, it might involve finding the people who are informants and stopping their ability to keep helping the other government. In a corporate setting, it might involve cutting a contract with a supplier you think has illegal dealings, for example.

Make a strategic bet to increase the risk. In a political context like yesterday’s story, increasing a risk strategically could involve cutting diplomatic ties, mobilizing troops or invoking sanctions, among others (these increase risk because they may cause the original threat actor to escalate further or move more quickly with the original threat.) In a corporate context, an example would be to work with a startup vendor even though you know it’s a highly risky supplier because that vendor has some amazing new technology that you want to use.

Unfortunately, if you didn’t have a remediation plan in place BEFORE the risk became likely, you’re facing much more confusion about what to do and even whether to do anything at all. This puts your company at risk and in fact, negates the value of having predictive security capabilities.

Bottom Line: Security professionals need predictive security management and prescriptive treatment plans to protect their firms from looming threats.

Security teams need clear treatment plans that address potential risks and how to mitigate them. As a simple example, if there is a threat of insiders giving information to third parties, then the remediation plan would involve something like “when someone downloads more than one file they don’t normally access, that person’s manager must ask why the person needed those files within 4 hours of the download.” Without this proactive treatment planning, companies likely do nothing and then get harmed even by risks they could have addressed.

Let’s cut to the chase – there have never been times as uncertain as these in the world of business. There is no written rule-book to follow when it comes to career survival. The “Future of Work” is about making ourselves employable in a workforce where the priority of business leaders is to invest in automation and digital technology, more than training and developing their own workforces.

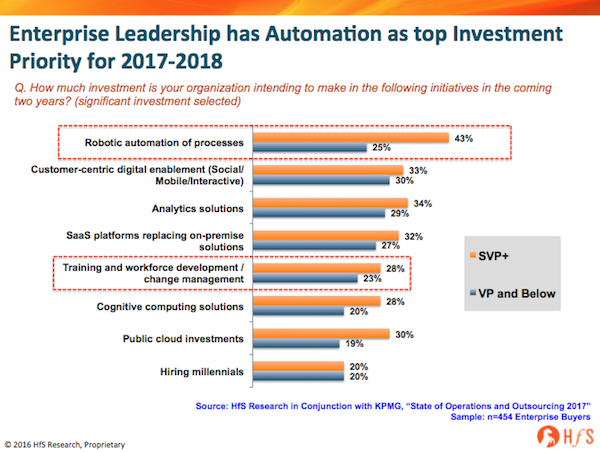

As our soon-to-be-released State of Operations and Outsourcing 2017 study, conducted in conjunction with KPMG across 454 major enterprise buyers globally, shows a dramatic shift in priorities from senior managers (SVPs and above), where 43% are earmarking significant investment in robotic automation of processes, compared with only 28% placing a similar emphasis on training and change management. In fact, the same number of senior managers are as focused on cognitive computing as their own people… yes, folks, this is the singularity of enterprise operations, where cognitive computing now equals employees’ brains when it comes to investment!

My deep-seated fear for today’s workforce is that we’re in danger of becoming this “Lost Generation” of workers if we persist in relying on what we already know, versus avoiding learning new skills that business leaders now need. We have to become students again, put our egos aside, and broaden our capabilities to avoid the quicksand of legacy executives no longer worth employing. We need to become hybrid corporate animals.

So let’s give some examples of these “new skills” we need to develop for ourselves:

Sales people: it’s no longer just about selling and relationship development, it’s about understanding evolving business models, understanding the impact of technology and the importance of smart marketing. You need to be a trusted consultant, not simply good with a 9-iron. Clients needs are increasingly complexifying and you need to be the arbiter of helping them simplify their requirements. Understanding business models is what will make you successful in the digital world.

Software people: it’s no longer about data management, security and making apps function, it’s also about understanding the desired business outcomes associated with these investments and helping your enterprise stakeholders articulate them better, so you can work with them to fashion and build the right solutions. Design Thinkwith your business colleagues, to make sure you are truly working in tandem to achieve the goals that you are setting for yourselves…. envisaging the desired outcomes and working backwards from there, is the smart way to do things with technology investments.

Marketing people: forget spending all your time dredging up useless metrics to justify your existence, and focus more on learning new methods to drive awareness and new revenue, using all the evolving channels at your disposal. Really learn about the desired outcomes of your customers, prospects and your internal sales team to make sure you can be a true business partner to them and not a one-stop shop for them to check boxes. Marketing has to evolve into both a strategic and a tactical function that intelligently ties all the channels to market together.

Finance people: this is less about churning out reports and data, but working with the key business stakeholders to understand the desired business outcomes of the organization and the evolving business models to produce relevant data and analysis. Simplification of data, as opposed to the production of it, is the watchword.

Procurement people: this isn’t only about policing expenditure, but much more about understanding your enterprise stakeholders’ needs and desired outcomes to make sure you can help them access what they need to achieve them. You are a business-savvy relationship builder, not the guardian of the corporate coffers. You need to understand the whole sales, production, and marketing cycles of your organization if you really want to be a valuable asset.

HR people: you need to make a significant shift away from being the guardians of your firm’s legal counsel, to a function that develops a genuine understanding of the business needs and the desired outcomes… as you will be tasked with finding the talent described above. Learn to identify talent with can learn on the job with an open mind, not simply finding “silver bullet” candidates who come locked and loaded with all the relevant experience. In the digital business world, the latter no longer exists. You need to be the football coach who unearths the rough diamonds with the potential your enterprise needs to achieve its outcomes.

The Bottom-line: It’s one thing to describe the skills you need, but how do you go about developing them?

If you can figure out how to demonstrate answers to these six questions, you’re probably on the right track:

1. Which customers have you delighted recently? 2. What new relationships have you made that add value to our business? 3. What work have you done that excited people inside and outside of the business? 4. How are you helping energize your colleagues and exciting them with new ideas? 5. How have you helped add value to new business wins? 6. How have you contributed to new initiatives that improve productivity and effectiveness?

Net-net, think of your firm as Walmart morphing into Amazon. Just a few short years ago, Walmart would judge its growth and success on how many new stores and how many new employees it created in a given year. Today, Amazon has completely disrupted Walmart’s business by focusing on how many new customers it acquired, without making any investments to its existing human or physical infrastructure. You need to be thinking like Amazon does… how can you be more valuable to your firm – without having to add heaps of staff to support you – by managing your time better; by reading (a lot) more; by making the effort to forge relationships with people who can make you smarter; by looking after your health better.

So turn off that Facebook – and stop checking your bloody email every 5 minutes and focus on investing your time in making yourself a smarter, more hybrid, versatile, employee. Don’t become part of this Lost Generation…

Industry 4.0 has become a buzzword in the manufacturing industry today. There is a reason for it. There has not been a full-scale change in the way we manufacture goods since the days of Henry Ford. The PLC (programmable logic controller), MES (manufacturing execution system), first generation robots have all made incremental improvements to efficiency but not to the same extent. Now with Industry 4.0 the change is beginning to happen.

But what is Industry 4.0? The danger of the buzzwords is that many service providers are trying to label their legacy services and solutions as Industry 4.0 and confusing clients. We at HfS Research believe that Industry 4.0—or the fourth industrial revolution—is the confluence of many technologies coming together in manufacturing for the creation of smart factories with significantly high efficiency, productivity, quality and flexibility than the current state. It will enable mass customization in manufacturing. While it will take few decades to enable promises of mass customization at scale, the journey has started.

While most engineering, consulting, technology, and business process services in manufacturing industry offered today (even legacy services!) can help enterprises in their Industry 4.0 journey in some way, we have identified 13 enabling technologies that we believe are critical for any enterprise to accelerate its Industry 4.0 journey.

To make Industry 4.0 real for our enterprise clients, we are launching our Industry 4.0 study, which will focus exclusively on R&D, plan, implement and operate services around the 13 enabling technologies shown in the chart. Most of these technologies are in the early stages of adoption, as we will discuss in the forthcoming Blueprint Guide.

Bottom Line: HfS Research Blueprint Guide: Industry 4.0 Service 2017 will cut the chase and make Industry 4.0 real for our enterprise clients.

This study will help enterprise clients understand the real case applications of different Industry 4.0 offerings along with capabilities and offerings of the service providers in the market today. We will work to understand the different ways that this functionality is delivered and how it may evolve. We will evaluate about 15 service providers on their innovation and execution capabilities in this emerging and exciting space. If you have any interesting Industry 4.0 services story to share, please contact [email protected].

Just before the holiday break we released our first HfS Blueprint focused solely on the Digital Marketing Operations market. In the past, we have covered customer experience management along with marketing in the same report, and this year decided to break out the front office processes and look at them in a narrower scope, including our Contact Center and Digitally Enabled Contact Center blueprints, and this most recent endeavor in digital marketing services. It quickly became obvious that while service providers have varied strengths and value propositions across each of these areas, the blurring lines between front office functions is creating confusion- and opportunity- in this quickly changing market.

Digital is all about realigning to the customer

Changing customer demands are driving companies to up their investment in digital marketing. The way customers prefer to communicate and consume information is forcing marketers to rethink their strategies, as well as collaborate with other business units for a greater holistic customer view. Whether it’s advertising on social platforms, understanding customer segments on the web or mobile apps, or putting out relevant content for greater personalization and sales conversion, the need for speed and efficiency is top-of-mind for marketers. Because these expectations and preferences are constantly changing, marketers are tasked with becoming nimbler and more efficient organizations in order to be increasingly competitive. Some of the buyer-service provider dynamics include:

Maturing digital marketing operations are driving investment: The maturity of digital marketing services buyers falls across a broad spectrum. We spoke with some buyers at the very beginning of their journeys, converting paper-based materials to digital formats. Others already have a solid digital marketing strategy in place, and are looking to further optimize and create efficiencies in their operations. As buyers mature, the burgeoning volume of digital assets becomes a greater challenge to manage—which often falls upon their service providers.

“Better, faster, cheaper” is table stakes: Not surprisingly, cost reduction still ranks as a top driver for digital marketing operations services. Buyers have ever-increasing expectations for speed and efficiency with reduced budgets. The need to reduce turnaround time and time-to-market for campaigns is common. Many clients view their service providers as an extension of their teams that they can often use in off hours when timelines are tight. On top of these increasing pressures, most buyers are also looking to their service providers to deliver market insight, thought leadership and innovation.

Customer experience is impacting governance models: While the front office traditionally operated in siloes, digital is driving a convergence of traditionally disparate departments. Often under the purview of an “engagement or experience officer,” leaders are learning to reach across functional siloes, between IT and lines of business, to deliver on a more holistic experience for their end customer. This, in turn, increases the complexity that service providers deal with when setting expectations and delivering on services to their client stakeholders.

What’s next?

It became very apparent while doing this research exercise that it’s getting harder and harder to draw a line between “marketing” and other front office functions like customer service and sales as we move to a more holistic customer experience viewpoint. As the edges of front office services continue to blur, the services that providers offer overlap and the competitive landscape will get more complex, with more niche/specialty service providers entering the mix. Many providers not included in this report were on the periphery of digital marketing operations because of their approach to customer experience; the coming year will see greater development of their value propositions and emergence into this competitive landscape in the coming year.

Also, a shift in the way that buyers and providers work together: the need for higher value services from buyers is often easily expressed but not as easily adopted by various stakeholders within client organizations. The combination of embracing the ideals of design thinking and brokers of capability within client organizations will help to enable a better reception of new ideas and strategic thinking with digital marketing operations service providers. Buyers need to be willing to work with service providers on this type of end-to-end CX initiatives. This often involves using service providers as change agents to bring together multiple internal stakeholders across the front office in their siloed organizations.

The bottom line: service providers have a big opportunity to continue moving into the realm of strategic and cause disruption in this market.

This is not only an opportunity for new entrants, but also really an opportunity for service providers which have a greater breadth of services to grow their existing relationships, evolving beyond isolated engagement to more comprehensive marketing operations services. Right now services in this market are often consumed in a more piecemeal fashion, but buyers are interested in adopting services from providers where they have trusted relationships. The majority of buyers interviewed for this report were interested in expanding the scope of the relationships with their current service providers and experiment on new platforms (i.e. social media platforms as they arise). Service providers which are focused on thought leadership will win these expansions. For some, digital marketing operations will mature into another commoditized, race-to-the bottom BPO service for cost takeout. But the smart service providers with a well-planned talent strategy and plans for intelligent automation have a real opportunity to disrupt the agency model and gain a greater chunk of marketing spend.

The bold move of adding The Marcus Buckingham Company could pay off nicely for ADP, and in “multiplier effect” ways that, by definition, are much more consequential than incremental revenue or adding some new strategic customers.

The bold move of adding The Marcus Buckingham Company could pay off nicely for ADP, and in “multiplier effect” ways that, by definition, are much more consequential than incremental revenue or adding some new strategic customers.