HfS is about to publish our quarterly analysis of the service provider and shared service center location announcements by Hema Santosh. As a taster, we would like to post the highlights and the infographic from this work.

Highlights for the quarter:

We see expansion of jobs in both the US and India – of the estimated 9,000 jobs that these new locations will house, 4,350 will be in the US and 4,300 will be in India.

Industry specific BPO drives expansion with 3 new BPO sites in the US in Q4 2016.

Downsizing – we saw some down sizing of in-house centers with eBay, Standard Chartered and Verizon all shrinking some centers.

There are already more mobile connections (over eight billion in 2016, according to GSMA) than people on this earth and some forecasters are already predicting we’ll have 20 billion devices or things connected in a couple more years. Yes indeed, people, the internet of things (IoT) has truly come to life in recent months, and this is only going to escalate on a massive scale.

However, is simply having this obscene level of connectivity really going to have a transformational impact on us? Won’t we reach a point of connectivity saturation where the net benefits almost become negatives in our lives, or will IoT be extended to true commerce and the banking of things?

Up until very recently, these discussions have been more science fiction than reality, however, a news item this week raises our hope that IoT will evolve in this direction and we can start talking about a world beyond mere prolific device connectivity.

IBM is partnering with Visa to offering Visa’s tokenization services to its IoT clients. Every IoT device or thing can be made a point of sales (PoS) terminal and be able to enable transactions itself, such as a car ordering spare parts and a refrigerator ordering groceries. (Read here.)

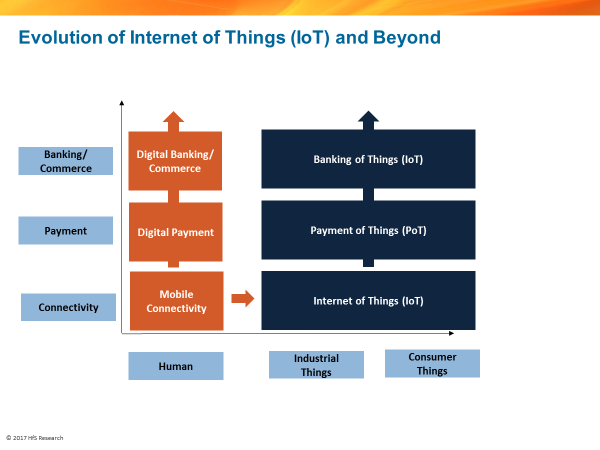

Aside from the operational complexities, analysts have liberty to think about future scenarios. We can visualize this evolution of things in two dimensions. In the horizontal dimension it is human, and different categories of things (industrial things and consumer things). In the vertical dimension, it is digital activities. It starts with connectivity and then extends to payment, commerce, and banking.

The mobile revolution has been providing connectivity to humans from late 90s. Now the era of connectivity of things has started. On the digital activity dimension, humans are using digital payments, digital commerce, and digital banking.

Getting connectivity to things is the start. It will become interesting when connectivity of things is extended to the payment of things and ultimately to the commerce and banking of things.

Internet of Things (IoT): Things have a unique identity by SIM, RFID or similar identification technologies and can be connected to each other by different communication technologies. Things produce data with sensors attached to them, which can be used for generating information and insights.

Payment of Things (PoT): Things have the capability of paying themselves. Things can do commercial transactions and pay automatically, without human intervention.

Banking of Things (BoT): Things have a legal and a commercial identity of their own and can bank on their own. They have their own existence and bank accounts. They can take a loan, generate revenue, make deposits and can do all commercial activities which humans do with banks.

The use case of banking of things could be a machine or a car, which is not owned by anyone, and it can have its own identity. Banks can give a loan to a machine and the machine can use it to pay its initial cost to the manufacturer. The user can use this machine and pay usage charges for the machine in its bank account. A single machine can be used by multiple users. The machine can pay interest back to the bank, pay for its own maintenance, pay for insurance, upgrades and can decide what to do with its profit.

Similarly, an autonomous car can benefit from the banking of things. A car can have its own identity. It can operate like a taxi and available on demand like Uber. But unlike an Uber cab of today, it will not have any owner or driver. Users can use them and pay charges to car’s bank account. The car can pay interest to the bank, pay for insurance, taxes, gas (or electric charge), maintenance, upgrades and can decide what to do with its profit. Combine this with artificial intelligence, the car can decide how to optimize its activities for maximizing profits. Combine this with robo advisors, the car can invest its profit for maximum returns. Combine this with blockchain, the car can enable smart contracts between passengers and cars.

Why is this important?

As noted in our earlier IoT research, IoT is real but not yet transformational. For transformational impact, IoT needs to be combined with other technologies and commercial activities. The IoT combined with PoT and BoT can have transformational impact as discussed in earlier use cases. Earlier waves of mobile connectivity and its evolution have produced Uber, AirBnB, WhatsApp which decimated the business models of many industries. Even internet businesses of Google, Amazon, Facebook leveraged this evolution to consolidate and expanded their positions by dis-intermediating so many traditional business models. Now IoT and its evolution to PoT and BoT will have potential to disrupt many more business models and industries.

Bottom Line: IoT provides the initial building blocks and it will evolve to Payment of Things and Banking of Things to disrupt many more business models.

The service provider ecosystem can play an active role enabling enterprises in their journey towards IoT and beyond. Enterprises now need to embrace the Digital OneOffice more than ever to thrive in this era. There is a lot of advice enterprises can still use to prepare themselves for the future. So this leaves us with the next trillion dollar question: Can enterprises really bank on service providers to take them to the world of Banking of Things?

When HfS Research community members check back here later this week they will have access to my first major research effort for HfS since joining late last year: “Predictive Capabilities in HCM Systems”. This Blueprint Market Guide includes trends, themes and related implications for both buyers and solution vendors, an evaluation of these capabilities within 9 HRMS or HR System of Record vendors, what to watch as this emerging area continues to evolve, and – of course – our recommendations for driving business value and ROI from these capabilities.

The aforementioned 3 reasons are:

Surprising trailblazers … such as some of the HRMS players blazing the trail for other vendors to follow (aka our High Performers group) are probably not who you’d expect; e.g., none of the top 3 rated vendors on these specific capabilities are in the top 3 from a market share perspective.

Insights … as well as market intelligence that will likely make you say to yourself “Hmmm, I haven’t thought of that.” As just one example, there are very logical reasons why a number of the 9 HRMS vendors covered selected ‘predicting flight or retention risk’ for their initial foray into this product investment area, but also some not-so-obvious reasons. Among the latter ilk, the “consequences of being wrong” are probably not as severe as with a number of other examples of predictive HCM use cases (actual and hypothetical) highlighted in the Report.

Recommendations … including why investments from both vendors and customers in this exciting product innovation area should arguably be ratcheted up, and ways that both parties can do that and start reaping corresponding benefits while proactively managing risks and costs.

Bottom Line:This first-of-its-kind industry research from HfS will shine a bright light on one of the most promising advances to hit HR Tech since on-premise, client-server deployments went the way of the dinosaur.

Yes, the costs to hop onboard are not insignificant, but you can perhaps start with an economy ticket (modest investment) and then go further into this realm when business impacts are obvious. In time, HfS believes they will be, and early adopters often hold onto competitive advantage once they have it.

At a time where alternative facts and fake news open doors to a parallel universe, where global labor markets are being disrupted by various flavors of travel bans to the United States, the specter of a wall being built at the US-Mexico border that costs more than the entire Space-X program, a reform of H1B visas that could likely dismantle the traditional outsourcing model, and a curious thing called Brexit that could change the global trade landscape forever, one might be forgiven for feeling slightly disoriented. Yes, people, we’ve arrived at a time where the very foundations for service delivery models across the industry are being put at risk, where there is no written rule book for how to get ahead of this. So what better time than to add a sprinkle RPA into this global potpourri of disruption? Maybe a food dose of process automation will give us all something to cling onto during these heady days?

Against this slightly perturbing background, what is the state of the RPA market, the emergence of the virtual workforce – and how will it affect the broader markets? Is RPA the silver bullet to overcome many of these issues and obstacles? Back in December, we already chartered the service provider capabilities around RPA. As a result, we not only got a strong endorsement for our findings, but stakeholders were asking us to provide a similar assessment for the RPA tool providers themselves. To get more clarity on these pressing issues, we have sent our automation overlord Dr Tom Reuner back into the RPA community to separate the wheat from the chaff… the bots from the clots.

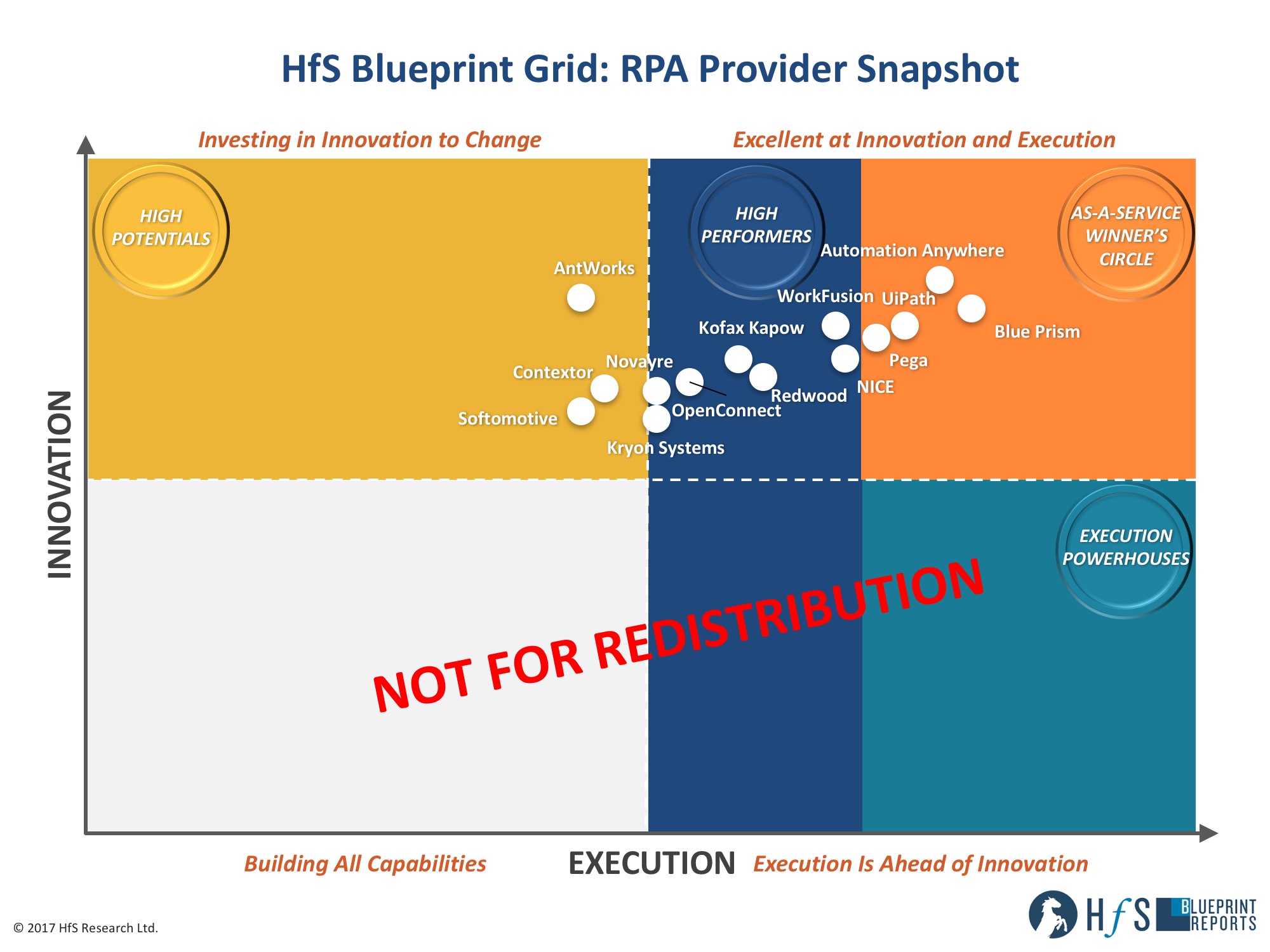

Based on his findings, Tom and I went into conclave, compared notes and war stories, as well as cranking the numbers for the evaluation. And finally, we have white smoke. Thus, we are pleased to share the new 2017 RPA Blueprint grid and the key findings with you.

Phil Fersht, CEO and Chief Analyst: Despite all the noise, many stakeholders still struggle to comprehend what RPA is all about. Tom, can you help these lost souls to get up to speed before we dive into the details?

Tom Reuner, SVP Intelligent Automation: I wish that would be so easy, Phil. Despite all the noise RPA is still an undefined market. To make matters worse, the IT juggernauts, the service providers, and management consultancies are only very gingerly educating the market. Two key reasons for that. On the one hand, it is still a nascent, albeit fast maturing market. On the other hand, it is a classic case of Innovators Dilemma: The large service providers still make more money with system integration and labor arbitrage. A cross-industry working group under the leadership of Lee Coulter and AJ Hanna from Ascension Health under the umbrella of the IEEE standards body, with the participation of the leading RPA tool providers and consultancies, is doing sterling work to drive a taxonomy and common understanding of the different building blocks of Intelligent Automation and thus also RPA. Yet, it will take considerable time until these suggested definitions will be adopted by the broader industry. The IEEE definitions of RPA are a useful reference point to describe the scope of this Blueprint evaluation: “Robotic Process Automation (autonomous)”: Preconfigured software instance that uses business rules and predefined activity choreography to complete the execution of a combination of processes, activities, transactions, and tasks in one or more unrelated software systems to deliver a result or service with human exception management.”

While nothing is defined in the context of automation, the common denominator of all the approaches to automation is decoupling routine service delivery from labor arbitrage. This is not only the common denominator but also the cause for the widespread disruption that we are expecting, largely on the supply side. But the providers are not always helping either. The biggest misconception and confusion is caused by the related proposition of desktop or Robotic Desktop Automation (RDA). It is here where there is so much smoke and mirrors in the industry. In simplistic terms, RDA has evolved from screen scraping in the front office where disparate sets of information were integrated to support call center agents. Thus, RDA is focused on quick deployments on desktop level, typically customer contact agents. In RDA, activities are being automated, while in RPA (back-office) processes are automated. On the danger of over-simplifying, in RDA the agents are passing on tasks to robots, while in RPA the robot passes on tasks to agents. And as we are on the topic of subterfuge, it is difficult to ascertain how much scripting and coding is actually needed to get solutions off the ground? Many contracts are largely a Managed Services agreement. This is confounding what automation and RPA should be all about, namely the decoupling of routine service delivery from labor arbitrage.

Phil: So, clear as mud. Against this background, what really is going on in the RPA community?

Tom: Well, yes. But I think the reason for so much smoke and mirror is that there is so much at stake. The large service providers fear an erosion of their profits, while the RPA providers have often banked their pension pots on the success of their companies. Looking at it from a more positive angle, most providers are evolving their offerings toward the notion of operational analytics and the broad bucket of cognitive. In particular, the integration of semi-structured content through Machine Learning or through partnerships with providers like Celaton or Loop AI who help to create patterns in unstructured environments.

Aligned with this maturation in the market, we see more funding coming through. The latest example is WorkFusion who raised $35m in January. However, the biggest shift in the market, underlining the increasing maturity, is the shift of mindset from RPA as a non-invasive turn-key solution that marked the early phase of market development to the notion of RPA as a conduit for transformational projects, looking at end-to-end processes rather as a short guarantor for cost takeout. And RPA as an enabler for transformational projects is the cornerstone for our evaluation of RPA providers.

Phil: So Tom, what was your methodology behind putting together the 2017 RPA Blueprint Snapshot?

Tom: Rather than taking a function and features centric evaluation that is more appropriate for software products, we are taking a market-led approach which we feel is more aligned with the need of buyers in the sourcing industry. The RPA Blueprint Snapshot is building on and expanding the discussions with stakeholders as well the research of HfS’ Intelligent Automation practice. Our Blueprints are based on multiple client interviews, interviews with advisors, service providers and internal analysts who have experience working with the RPA platforms. Our scoring system only allows for 10% of analyst judgment, where we made the case for your strong innovation. Our weightings are partially based on importance criteria we glean from our State of Industry survey with KPMG which covers over 450 major enterprises. As RPA is not yet commonly defined, we are taking a strong steer from the evolving RPA strategic partnerships of the leading system integrators and BPOs.

Against this background, and in addition to the above inputs, we have reached out to the RPA providers with an RFI set out to help us evaluate them against a set of criteria across both execution and innovation. As we have outlined above it is not an easy undertaking as there is so much smoke and mirror in the market. But given the strong endorsement for both our Intelligent Automation Blueprint and our RPA Premier League Table, we are confident that our approach is providing stakeholders with relevant information and guidance.

Phil: Not beating around the bush, who is standing out as RPA performer?

Tom: There are many ways to look at the RPA market given the caveats that we have called out. But painting with a broad brush, the companies in the Winner’s Circle – AutomationAnywhere, Blue Prism, UiPath, and Pega – are the providers of choice for the channel partners focusing on transforming back-office processes. Behind this leading group, the positioning is becoming decidedly more blurred. The best way to think about it is to be clear about the use cases and requirements to add more specific providers for tender or RFI. Be it WorkFusion for broad cognitive capabilities, NICE for front-office activities, Redwood for ERP-centric automation or OpenConnect for a focus on operational analytics. Almost below the radar, there are providers like Jidoka with core RPA capabilities who carved out a niche in the Spanish-speaking world. Similarly, Contextor who are evolving from an RDA position to broader RPA capabilities, have a strong position in the French market. Beyond a geographical focus providers like Kryon Systems or Softomotive have made significant progress evolving from attended to unattended scenarios, while KofaxKapow through acquisitions offers a broad portfolio from OCR capabilities to process analytics.

Drilling down into the specifics, the market is dominated by the “duopoly” of AutomationAnywhere and Blue Prism. AutomationAnywhere is strongest in F&A, offshore delivery centers, and the US market. Conversely, Blue Prism is leveraging the first mover advantage with strong partner relationships, having the strongest impact on industry specific services, headquartered CoEs and the UK market. Behind the two market leaders, UiPath is growing strongly as clients cite the effective partnership culture and attractive commercial terms. Thus, for mature clients, UiPath is increasingly seen as the third strategic option in multi- vendor environments next to AutomationAnywhere and Blue Prism. Adding to this mix, iPega is being credited for its the quick deployments as well as the integration of both RDA and RPA in attended or un-attended scenarios. At the same time, Pega offers broader functionality by extending bots to it BPM suite.

However, the biggest surprise in our evaluation was AntWorks that thus far have been below the radar of industry’s stakeholders. Their value proposition is about linking core RPA capabilities with machine reading including semi-structured content such as handwriting in forms as well as broader cognitive capabilities including pattern recognition, even in images. Furthermore, similar to providers like RAVN, AntWorks has Enterprise Search and Machine Learning functions to support extraction of data from legal documents. The combination of Computer Vision and pattern recognition allows AntWorks to provide one solution where many service providers have painstakingly integrated different tool sets. Even though around the broader cognitive capabilities, AntWorks is competing with IBM Watson, it goes without saying that AntWorks is still early on their journey and therefore needs to demonstrate client references to the broader market.

Phil: Despite the market being nascent, albeit maturing market, WorkFusion has announced a free RPA product. What do you think will be the impact?

Tom: When WorkFusion announced a free RPA product dubbed “RPA Express” back in December, many executives in the automation community went pale. In defiance, and sometimes confusion, executives were quick to suggest that WorkFusion does not have a “proper” enterprise grade RPA product. There are many different ways of looking at this announcement. First of all, credit where credit is due: WorkFusion has one of the best, if not the best, marketing programs in the Intelligent Automation community. And sometimes there is a hint of jealousy creeping in when we discuss WorkFusion with their peers. More pertinently to the RPA discussion, while WorkFusion might lack the enterprise-grade capabilities in core RPA that the providers in the Winners’ Circle have demonstrated, they have strong credentials in adjacent capabilities such as crowdsourcing, the integration of Machine Learning or enhancements to the RPA Object Library such as the capability to drag and drop entire processes (e.g., “KYC,” “corporate actions,” “OCR”). What is boils down to in the end is to get access to the table where the sourcing discussions and decisions on automation are being taken. WorkFusion has successfully demonstrated exactly that. Not having enterprise grade core RPA capabilities has thus far not harmed their revenue stream. Thus, the announcement might not disrupt the market, but it still might end up negatively impacting valuations of RPA providers as many look for an exit strategy.

Phil: Gazing into a crystal ball, what can we expect for 2017?

Tom: Phil, if I would have all the answers, I should probably change my job and could make a lot of money. But here are three scenarios that I am seeing for 2017:

RPA will remain undefined. Over the next 12 months, the perception of RPA will remain blurred. RPA capabilities will fold into broad propositions such as Digital Workforces or Cognitive Automation. This is adding to the continuing confusion around RDA. Extending on that, in 18 months we won’t talk about RPA anymore. Most of the leading technology providers will have been acquired and RPA is a reality in the back-office.

M&A through ISVs. Buyers will have to do scenario planning for acquisitions. While this might bring broader capabilities, licensing costs are likely to increase as well. Pega’s acquisition of OpenSpan is the template for such developments. Beyond the tool providers, the automation pure plays such as Symphony and GenFour are likely to be equally absorbed by larger consultancies.

The emergence of an Automation Ecosystem: We already have seen the impact of Watson, as it is starting to evolve into an ecosystem. Suffice it to say, IBM could be the driving force to extend those capabilities, as we have argued some time ago. But it could equally be one of the tool providers significantly expanding its reach. As stated, we are seeing the providers in the Winner’s Circle moving toward the notion of orchestrating much broader automation capabilities. At the same time, we are seeing providers like Blue Prism and UiPath being deployed in IT-centric scenarios such as IT Help Desk and Application Management, pointing to a convergence of scenarios and tool sets.

HfS premium subscribers can access the RPA Blueprint Snapshot here.

Industry adoption is the biggest obstacle to blockchain becoming important in banking, according to 78% of participants in a study. Wait, what? It’s an odd data point to me, because adoption happens (or doesn’t) because of obstacles like cost and complexity. Slow or late adoption is a symptom of a challenge, not the challenge itself. So let’s take a quick look at what might slow or stall adoption, and what to do about it.

Blockchain is an element of “the platform revolution” that’s based on user economies of scale

Recently I had the chance to speak with Marshall Van Alstyne, co-author of The Platform Revolution and a professor at Boston University. He discussed the network and platform model of many new digital businesses like Airbnb. Airbnb is successful because it can exist and profit from user economies of scale instead of company-based economies of scale, according to Professor Van Alstyne. Essentially, this type of platform business allows users to create and share value themselves instead of relying on a company to create the value. The role of the business is to provide the infrastructure and support. While Airbnb doesn’t use blockchain as its base technology, the concept applies because firms can use blockchain as the basis of new platform-based business models.

Blockchain, with its design point of peer-based approvals for transactions and distributed ledger data storage, is a great example of a platform technology. It’s the enabler of a business that needs users to help define how it will scale.

What to consider in using blockchain as a platform for business

If blockchain can help companies build a platform business, what might slow or stall adoption? Professor Van Alstyne mentions a few:

Network ownership – who manages the network and gets to decide the rules? Is that owner in a position to run the network effectively?

Cost/transaction friction – how much does it cost to join or participate? And do you have to pay before you get value out? Can you design the network so participants pay only after they’ve gotten value to reduce the transaction friction?

Monetary policy (for financial transactions) – who or what agency is going to ensure the network isn’t too volatile? Who will ensure that there are guardrails to give users comfort that the system will have some inherent stability?

Standards – can players on different blockchain implementations work together rather having to agree on the same implementation? Who creates and manages those standards to ensure adoption isn’t hindered by interoperability problems? A good example of how standards can help is to solve issues like block sizes and reducing network consensus time, both of which significantly hinder the speed with which transactions can be completed.

The end user is at the center of the platform-based business

Customer-focused businesses need to exist in an environment where user economies of scale have become the norm. That means the business needs to understand the user and the users’ needs—doing so, will help identify and drive scale. And understanding the users and what they value, and how that then fits into a business model (addressing compliance, for example) can help drive the answers to the questions above. Rather than trying to scale internal operations like manufacturing, firms that adopt this customer-centric “Digital OneOffice” need to focus on user value and associated data. As Professor Van Alstyne points out, platform businesses can scale indefinitely because they don’t require internal company investment (beyond some compute power.) Instead, platform businesses that use technology like blockchain can scale as quickly as user adoption grows because there are no marginal costs of that growth.

Going back to that study I saw – blockchain may not get adopted, but if it doesn’t, it’s because companies didn’t take advantage of user economies of scale and learn lessons from older network-based businesses like eMarketplaces.

Bottom line: Focus on solving the obstacles to adoption, not adoption itself – especially transaction friction and interoperability standards – if you want your blockchain implementation to succeed and move you forward in your digital transformation.

There’s never been a better time than this for the specialized midtier services partner which isn’t dragging around billions of dollars of legacy contracts and isn’t reliant on massive people-scale deals to sustain its growth and profit margins. Clients are increasingly looking for shorter, sharper engagements – with immediate impact – that drive executives and their staff back to the classroom… the type of engagements which may simply not be attractive enough for a Tier 1 service provider which isn’t built for smaller, focused engagements that require higher level talent to lead real change management programs. In addition, most clients today do not want to drop millions of dollars on consultants to change things for them… they would rather have someone come in who can teach them to change themselves. Moreover, with the relentless appetite for RPA, clients want service providers unencumbered by cannibalizing their own revenue models, and many are turning to the specialists who can parachute in and get the job done quickly and effectively.

In this vein, meet NIIT, India’s original IT training company, once famously dubbed the “MacDonald’s of the software business” by Far Eastern Economic Review in 2001, as it built a unique franchise business in IT education globally. Today, the business has ventured into sectors such as banking, finance and insurance, executive management education, professional life skills, BPO, and IT education for schools – and now it is going full throttle into supporting RPA and digital needs for enterprises. Never has there been a more critical time to help clients with learning new ways of thinking, understanding the true impact of emerging automation models and separating the hype from reality when it comes to digital business models.

So, without further ado, let’s talk to Arvind Thakur (see bio) who is the CEO and Joint Managing Director of NIIT Technologies Ltd, for a discussion on the impact of Digitalization on IT growth and how the Indian IT sector is adapting to the shift from traditional IT services.

Phil Fersht, Chief Analyst and CEO, HfS Research:Good evening Arvind. It’s good to have you on HfS for the first time. Maybe you could start by giving us some background on yourself and tell us a bit about how you wound up at NIIT Technologies, leading the charge?

Arvind Thakur, Chief Executive Officer, and Joint Managing Director: Phil, I have been with NIIT since 1985 when I joined the founders who pioneered IT education in India. Essentially the company had embraced a model inspired by a teaching hospital. As you know, a good hospital typically would have a research institute attached to it. Experienced medical practitioners teach at the research institute and the students who are trained get valuable experience as apprentices in the hospital. This creates a synergy between the learning and execution.

Over the years NIIT evolved naturally into offering software and system integration solutions driven by this model. It pioneered the software factory concept because the people that were being training were not necessarily experienced to face customers. To gain global customers we needed to follow good, strong processes, to deliver quality software and this was achieved by embracing quality models.

We embraced the models of those times, in the ‘90s. We began with the ISO 9000 framework and then the Capability Maturity Model (CMM). In 1999 we were the 12th company in the world to be assessed at CMM level 5, the highest level of maturity for software development. Backed by this capability we rode the internet wave and grew our software business rapidly through the nineties.

By the turn of the century, the dot-com meltdown resulted in eCommerce and Internet investments to become discretionary spends by clients. This, in turn led to a change in our software business profile which began to focus on legacy and our education business too started focusing on aspects of education other than IT. The strong synergy that existed earlier as teaching hospital became less relevant, so the company demerged its software and learning divisions into two independent companies, both listed on the India Stock Exchange; NIIT Limited, continued to focus on education and is now, in fact, a global leader in learning, and NIIT Technologies Limited was spun off to focus on services, and I came to lead the charge of the company as its CEO.

Phil: So, Arvind, what do you think today makes NIIT Technologies unique in the market? Why do your clients really hire you?

Arvind: When we de-merged in 2004, we were yet another IT services organization competing in an environment which was dominated by large-scale players. We put together a simple strategy which was to be very focused on a few industry segments and compete on the strength of our specialization. What differentiates us is essentially this strategy. People hire us for our understanding of the select industry segments that we serve: Banking, Financial Services, Insurance and Travel. We understand the platforms which are relevant to these industries. The understanding of the industry and the understanding of the technology relevant to the industry is what truly differentiates us, and that’s why people hire us. This sharp focus has resulted in the creation of our own intellectual property, which are now leading platforms in some of these industry segments.

Our training heritage enables us to rapidly build strong capabilities as new technologies emerge and our customers evolve. We’ve been able to put together a very unique culture which focuses on delivering a great experience. Our vision is to be the first choice in the select segments and accounts that we focus on. Everything that we do is guided by this vision and that is what makes us unique.

Meet the IT educator himself… Arvind Thakur, CEO of NIIT Technologies

Phil: You talk a lot about being a “digital organization” at NIIT Technologies. How would you define digital as it impacts IT growth in the medium to short-term? Do you think India can become a digital juggernaut and evolve from much of the traditional IT markets that have served you so well? How do you see the whole impact happening and do you think NIIT Technologies can be successful?

Arvind: I think our industry is at a crossroad, Phil, and actively addressing this new Digital paradigm. The industry is rapidly shifting gears to embrace this new paradigm. As with a vehicle which slows down while shifting gears, the industry too is experiencing a slow down as it shifting gears to embrace new business models required to take advantage of the Digital opportunity. The good news is that India’s IT services industry has plenty of cash and is using the cash to rapidly build new capabilities both organically or inorganically and indeed has the ability to become a digital juggernaut.

NIIT Technologies itself is seeing rapid growth in its Digital business. We are approaching this opportunity by focusing on three things:

1. Smart IT – adopting automation in a big way so we deliver value to our clients. Anything that can be automated will be automated. In this context, we’ve put together an automation framework, a platform which we call ‘Excelerate’. The platform embraces the tools required to do traditional activities associated with the development and test automation, and also other elements like smart maintenance, infrastructure automation, all the way to advanced robotic process automation.

2. Superior Experience – The focus here is on the culture, and change required to the mindset of the entire workforce to address the new Digital paradigm. The industry so far has grown on the value proposition around cost arbitrage where customers would normally tell us what they wanted and we would build it faster, cheaper and better than anybody else. In the digital world however, clients are looking at how you, as a technology partner, can deliver business value. We need to change the mindset of the entire workforce from doing what you’re told to do, to identifying opportunities of value add. I believe we have taken the lead in the industry to invest in making this culture change.

3. Scale Digital – As mentioned earlier, we are using the cash generated from the business to build capabilities around Digital offerings both organically as well as inorganically and doing it fairly successfully. Digital revenues in the company which was negligible a few years ago, is now about 18% of the revenue mix.

Phil: One final question for you Arvind. You’ve got Prime Minister Modi’s attention for one whole hour, his full attention. What if anything do you urge him to do differently with regards to growing India’s IT sector over the next three years?

Arvind: One hour’s a lot of time with the Prime Minister! There would be many interesting things to talk to him about. He would appreciate that the IT-BPM industry, in India, contributes in a very significant manner to the GDP of the country – 9.3%. What’s more important, is that the industry plays a significant role in the balance of payments for the country, with over 45% of the foreign money earned through services exports on the current account coming into the country through engagements by the IT-BPM sector. That’s very significant and I’m sure he does appreciate that.

The first part of my conversation with him would be around negotiating trade agreements specifically around, “How do we leverage our purchasing abilities as a fast growing large economy, to negotiate policies associated with free movement of people with trade partners?” Restricting movement of people particularly if it discriminatory is akin to imposing non-tariff barriers. I would urge him to get an understanding going between heads of government, that mobility of people is not the same thing as immigration. That would be one interesting conversation to have with him, which would obviously be very useful for the growth of the IT sector.

My second conversation would be around ease of doing business. You might have heard that the country is adopting a single tax regime for the goods and services which is now being made law. The focus has been to eliminate multiple levels of taxes to drive efficiency which is certainly good for the manufacturing sector, but we have to ensure is that it does not impact the ease of doing business for services sector. The services sector currently operates with a central single tax regime. The new GST (Goods & Services Tax) law creates the possibility of multiple registrations in different states for the services industry creating a lot more additional administrative work and difficulties in conduct of business. This would seriously impact the global competitiveness of the industry and so with the Prime Minister a good conversation would be “In terms of the single tax regime for goods and services – when the laws are promulgated, how do we ensure they do not impact the ease of doing business for the IT Sector”.

These would be the two important things to discuss with him.

Phil: I think that would be very relevant, Arvind! This has been a most interesting discussion – I look forward to sharing this with our readership… the NIIT model is certainly becoming increasingly relevant in today’s uncertain market.

When, in history, has there existed a market that keeps relentlessly growing at 5-10% each year, with profit margins consistently at a 15-20% level; and for well over a decade? Yet you attend the annual flagship Indian IT conference only to experience an atmosphere of acute paranoia and paralysis. Is change really that frightening?

Even most clients are openly declaring they haven’t had their budgets reduced – many simply aren’t ready to make investments while there is such uncertainty surrounding the market because of an unpredictable US President. Even NASSCOM itself adds to the uncertainty by deferring its usual business outlook…

However, acting like a deer in the headlights is not an option. The smart strategy is to expect the worst and make measures now to get in front of it…. don’t let the juggernaut, that is a protectionist US administration, squash you flat in your tracks.

Breaking out of this paralysis cycle

However negatively this could turn out for some of the Indian IT services industry – here are six simple ways to break out of this paralysis and reinvest some of these bloated warchests, before greedy investors who got rich off your spoils demand to cash in their chips…

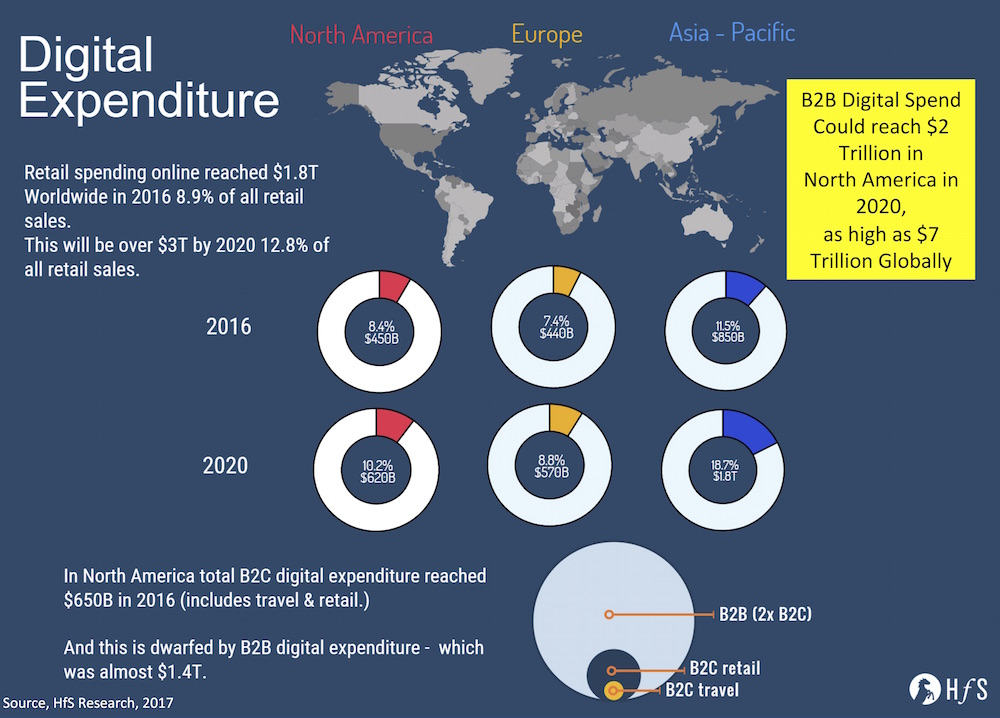

1) Invest internationally beyond the US. Those Indian IT majors in the strongest position are those that are least reliant on their US clientele for future growth. In fact, HfS estimates $7 Trillion in B2B digital expenditure by 2020 – with only $2bn being in the US (traditionally 50% of worldwide IT spend came from the US, but digital spending – both B2B and B2C – is changing that picture dramatically). For example, the British PM is already deep in discussions with Modi about closening UK/Indo ties even further in the wake of Brexit. The UK has the potential to become a major digital hub, fuelled by Indian talent. While Brexit appears like a terrible idea on paper, change forces action and these actions will be all about increasing the flow of trade and talent with emerging nations and creating new wealth. We also see a real appetite for digital business model investments and automation by Australian businesses – and many of the Asian nations are only too happy to move from zero to hero to take advantage of the humongous digital B2B expenditure in Asia/Pacific and the rest of the world.

In addition, many of the European regions, such as Nordics and Germany, are now rapidly exploring more global resources to support their digital growth. If America – as it appears – is on the path of becoming a protectionist anti-globalization country for the next four years, perhaps its time to broaden your horizons?

2) Invest in a smarteronsite/offshore model that gets you closer to your customer’s customer. Yesterday’s IT services model was all about helping legacy traditional enterprises keep their lights on by maintaining clunky old ERP implementations keep operating, adding extra sauce to spaghetti code and keeping an eye on server outages from afar. Tomorrow’s winners have moved all this stuff into the cloud and automated much of their infrastructure management. The future growth is working much closer to your customers to help them design and implement digital business models by building mobile applications, testing customer sentiment, forging partnerships and developing APIs with new digital business partners and communities. Technology skills such as DevOps, Agile, Hadoop, Blue Prism and AutomationAnywhere are the watchword, and a global race is on to access these skills. Moreover, the developers need to be closer to the business designers and customer strategies of the clients to make this effective. So Indian IT majors need to focus on developing these skilled resources where all their clients are situated, in addition to India itself. This will require re-investing some of that lovely cash sitting around – and, heaven forbid – take a small margin sacrifice for a few quarters.

3) Partner with digital agencies to get it done. Be realistic for once and accept the fact that most customers are not going to come to you to design highly creative digital business solutions. You have an IT services brand, not a creative digital brand. Most clients will go to the advertising firms, the Design Thinking consultancies and the digital specialists for that work. However, all those firms are pretty clueless when it comes to actually communicating their business designs to technology firms and having themjust get it done. This is where you can really do well – by working with these agencies and consultancies as their IT partner – bring them into your clients and they will being you into theirs! Believe me, most the digital firms worth acquiring have already been hoovered up by the Accentures and Deloittes… most the stuff left on the market is overpriced, too small, and most their nose-ringed designers will jump ship the moment you buy them.

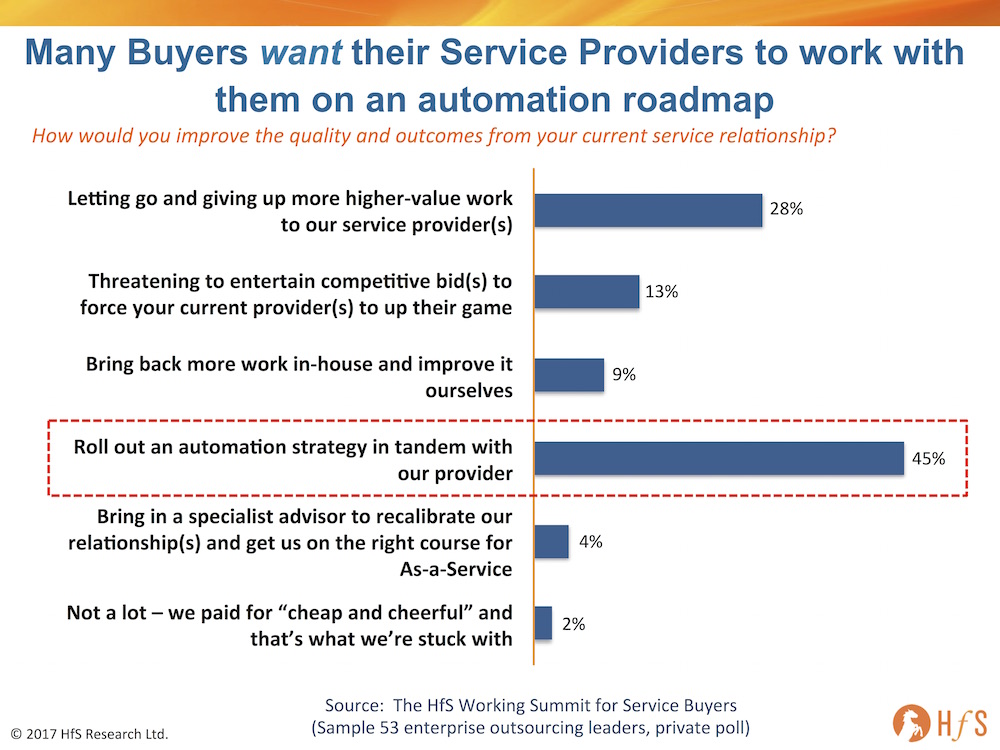

4) Become great intelligent automation intermediaries to manage broad automation and analytics environments for enterprises. Clients are crying out for providers to partner with them on their automation journeys – in fact, 45% of buyside operations leaders, when polled privately, view rolling out automation in tandem with their service provider as adding the most quality to their service relationship (see below). Several of the leading Indian heritage IT services firms are making impressive strides with their enterprise analytics and automation solutions – such as Infosys with MANA, TCS with ignio and Wipro’s Holmes – the key now is their ability to twin their solutions with the cream of the third party intelligent automation apps, such as AutomationAnywhere, Blue Prism, Pega, UiPath, Workfusion, Redwood, Antworks etc to become their clients’ intermediary for automation and analytics value. While some proprietary tools and bots can add great value, especially when aligned to specific industry processes, clients want to have the choice of adding their own independents tools to enjoy the biggest impact on their process value. The Indian IT leaders need to become great partners and facilitators in these emerging environments – they have the development talent in spades and the passion to bulldoze their way to the front of this market.

5) Keep investing in start-ups. One of the best cultural shifts in the Indian IT industry in recent times has been the emergence of the start-up scene in Delhi, Mumbai, Bangalore and other areas. Ambitious Indian IT talent is no longer desperate to walk that slippery steep treadmill of the IT juggernauts – many of whom are already too big, clunky and corporate for their own good. Moreover, tech investors are fed up having to invest $20-100m in US start-ups to develop one product or technology, when you can get the same value from the likes of India, China or Eastern Europe for a fraction of the cost. Having heard about the 400+ emerging startup firms who are already members of Saurabh Srivastata’s network (the original founder of NASSCOM), it gives me real hope for India’s future that the next generation of IT talent is already being healthily incubated.

6) Just make a plan and stick to it. The one big element of NASSCOM which I found most infuriating was the lack of a plan from most of the service providers. Most are simply playing a game of denial and react. This is a recipe for failure. Accept the fact there will likely be some uncertainty for six months before some new draconian measures are forced on businesses seeking to do business with the US. Net-net, it’ll be more expensive to deliver services to US clients and also harder to send your own talent over there to train US staff and manage projects. So set aside funds to hire more people in the US and budget for a margin squeeze on future US contracts. And forecast a 10-25% hit on deal flow due to longer decision cycles and US clients veering away from using highly visible offshore services suppliers.

Bottom-line: Take the tough blows now to roar to the front of the global IT industry when sanity returns

While the global IT world waits with baited breath, paralyzed by the ramblings of an unstable and determined US President, our beloved IT services firms can either remain numbed by fear, or actually use this opportunity to make some key strategic investments and initiatives. Those mountains of cash need to be used sensibly before those greedy investors demand their piece back, so act now, swiftly and decisively to organize an IT business that isn’t so reliant on lifting and shifting labor to and from the US, and puts you in the driving seat to lead in the $7 trillion dollar digital world, where automation is native and access to skills absolutely critical. India has a great shot at emerging as the world’s great IT pioneer, and so much more than a low cost labor provider for greedy legacy US corporates. Trump won’t be around forever, and he might actually be doing India a massive favor without ever realizing it…

A smart business operation uses the right combination of talent and technology to drive desired business outcomes. Third party suppliers are crucial for that combination, and our new research shows an increasing focus on the relationships with suppliers to standardize contract management and governance, centralize management of strategic suppliers, recruit and engage talent that has relationship building and critical thinking skills, and better leverage self-service platforms and automation in procurement and supplier management.

The big emerging trends in SRM:

Based on our new research, including discussions at the HfS Summit, our annual Shared Services and Outsourcing survey with KPMG, and interviews with executives from financial services, healthcare, logistics, high tech and other industries, we’ve put together this picture of the “state of supplier and partner management” in the IT and business process services industry:

Ambitious procurement / sourcing leaders are positioning themselves as advisors to plug capability gaps – partnering with the business units to define strategy; coordinating across business units, IT, and legal; defining standards for governance (reinforced through templates and automation); using training to ensure the more distributed relationship management is active and following a framework.

Organizations are increasingly standardizing and centralizing business operations functions – often incorporating outsourcing in hybrid / global business services models.IT has been the first mover here, with business functions following – F&A, Procurement, and HR as well as industry specific support. We expect centralization and shared services to continue, with selective and targeted use of outsourcing (on and offshore) and RPA in a model many are calling “no-shore.”

There is a similar move to centralize supplier/partner governance and contract management, often separate from the relationship management. Relationship management is more difficult to centralize, and typically happens when the suppliers are providing IT or BPO through a shared services unit. Once centralized, governance and contract management is increasingly automated; and relationship management gets more focus.

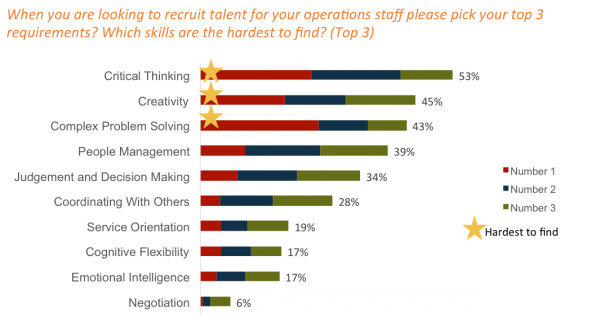

Exhibit 1: Top 3 Desired – and Hardest to Find – Capabilties for Business Operations

Source: HfS Research in Conjunction with KPMG, State of Business Operations 2017 N=454 Enterprise Buyers

Supplier management talent is increasingly oriented toward relationship building, decision-making, and analytical skills. Subject matter knowledge of the function is a basic capability that’s needed; negotiation and contract management “can be taught.” Executives are also increasingly interested in candidates with technical skills (or interest) in determining the right mix of talent and technology for managing optimal business results.

Procurement is setting the pace for evaluating and implementing robotic process automation and cloud-enabled platforms for more self-service. In our state of industry study, 57% of enterprises are in the process of evaluating/implementing RPA for procurement processes.

Across the board, we have found a move to consolidate and prioritize/tier suppliers for better negotiation capability, more effective and compliant oversight, and a more collaborative and engaged approach to partnering versus managing “off the side of the desk.”

It doesn’t matter what your operating model is if you don’t have the right talent. The right talent will make the relationship with the supplier effective for the business.

The bottom line: There are three critical components to effective supplier management that stand out in our research

Alignment and tiering of suppliers with business objectives

Standardized and coordinated supplier relationship management and contract management and governance

The “right” talent to broker and manage relationships and results

In general, companies are on a journey to have a more strategic approach to supplier management and believe it will take a matter of years to get there because of the cultural shifts required. We explore these themes further in our recently published POV, “The Rise of Supplier Relationship Management,” available for download (free with site registration).

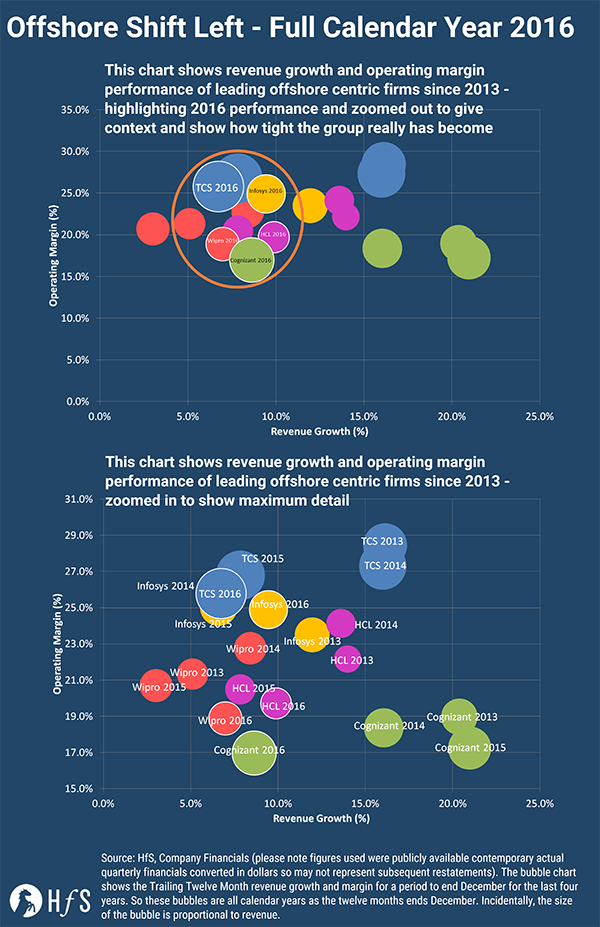

Back in August 2016, we wrote about theshift left with offshore providers– we were recentlyupdated in January. Below is the new chart that updates to include Q4 revenues – we always include a full year of data it is the trailing twelve months – now it represents the full calendar year view for all of the years.

Hopefully, the new charts show the shift even more clearly. With the top chart zooming out to show the whole of the y-axis – giving the full margin picture and demonstrates quite how close together the firms really are and highlights the convergence even more. As you can see Q4 hasn’t halted the shift and we see these companies cluster around the high single digit growth mark.

The Bottom Line – we’ll have the full roundup at the end of the month

This is just a taster of the results, once all of the quarterly results have been published we will collate them and produce our full quarterly roundup. We can then see the offshore shift left in the context of the other providers.

Am looking forward to seeing many of you in the warmer climes of Mumbai this week… so having some “Beef Wellington” to protect myself against what threatens to be a mudslide of confusion this week! I hope many of you can attend our opening session ““The Digital OneOffice – Getting Ahead of Today’s Disruption”… cheers PF

When, in history, has there existed a market that keeps relentlessly growing at 5-10% each year, with profit margins consistently at a 15-20% level; and for well over a decade? Yet you attend the annual flagship Indian IT conference only to experience an atmosphere of acute paranoia and paralysis. Is change really that frightening?

When, in history, has there existed a market that keeps relentlessly growing at 5-10% each year, with profit margins consistently at a 15-20% level; and for well over a decade? Yet you attend the annual flagship Indian IT conference only to experience an atmosphere of acute paranoia and paralysis. Is change really that frightening?