A big challenge for sourcing specialists is needing to rely on security domain experts internally to judge provider quality. The internal team, already working on their day jobs, often doesn’t have as much time to devote to the selection and negotiation process as sourcing leaders want. It’s important for sourcing teams to get smarter about security themselves to lessen their dependence on domain experts for preliminary RFP screening and downselecting.

In our upcoming security services Blueprint, we asked the client references (themselves security experts) what advice they’d give non-technical teams on buying security services. Some of them are general sourcing best practices, and some are very specific to security. But they’re all important to ensuring the success of your security services engagement. Here are some of their key recommendations:

Make a map of your security landscape. You need to cover your bases regarding what kinds of security technology you’re using – end point, antivirus, etc. — so you can ask the provider about its expertise in each one. Ask in-depth questions about what kind of expertise it has with those tools, and look for specific clients and places where it can demonstrate the details of its experience. Have the provider pull it all together into a diagram and one vision so you can see it and make sure it matches your expectations.

Communicate. A lot. How you interact with the provider will have as much bearing on the engagement’s success as the technical security. Make sure you’re not so focused on technical questions that you ignore challenges in communication. Remember the provider’s on its best behavior during the RFP process and it’s unlikely that communication problems get better after signing the contract. As one client reference said, “if the communication is good, you’ll get it right 90% of the time.”

Ask references about mundane details. Beyond the technology expertise, talk to references about what their daily experiences are like. Ask about little things like how quickly the provider answers emails and responds to questions that aren’t part of a service issue. Talk to people who have direct experience with the processes and skills you’re buying to make sure what the provider wrote in the RFP response is actually borne out in client engagements. For example, one client we spoke with mentioned a situation where its incumbent provider proposed expanding scope based on its process for innovation – yet the process described in the proposal looked nothing like the process the client experienced every day with the provider. So even tactical steps within a proposed process need to be explored.

Weight flexibility and potential highly when grading. One client reference expressed sympathy for his sourcing counterparts: “It’s hard to know what questions to ask and know how to evaluate the answers,” he said. But he then explained that evaluating a provider’s flexibility is critical to engagement success. He points out that flexibility matters because even if you ask the right question, your questions will change over the course of the work. So flexibility and potential capability are better than specific current capability that may not be relevant in another year.

Pick a supplier that can meet you in the middle. It’s been a truism of outsourcing to hire for areas where you’re weak. But this often leads to provider teams that can’t effectively work with client teams because they have no common skill sets. One client pointed out that she relies on her provider’s ability to speak “business language” when discussing security. Can the provider talk about security from a business perspective or are they expecting you to translate their technical discussions for your stakeholders? What you really want is a provider that can go deep in the technology but still have a business discussion, while you’ll match those skills with your internal security experts and stakeholders.

Bottom line: Don’t be intimidated by the lack of deep technical security knowledge. It’s important to bring in domain experts as much as possible, but sourcing teams can dramatically improve their own efforts by making sure they focus on the business side of security.

On a recent visit back home to India, I had the opportunity to spend some time with EXL’s EXLerator team that is working on how to improve insurance operations and deliver more business value for its clients with a “version 2.0” of EXLerator. From what I saw, this team’s efforts couldn’t be more timely and are in line with what we have outlined in our research as its areas of improvement.

Like the HfS Buyers Guide on EXL suggests, the service provider pursues an industry-led approach to providing business processes, with strong vertical practices in insurance, healthcare, travel and logistics, banking and utilities. The 2015 Insurance As-a-Service Blueprint highlighted EXL’s domain expertise and scale and execution on BPaaS strategies. However, both the Buyers Guide and the Blueprint also pointed out that EXL needed to bring more technology enablement. It has struggled to find footing with technology-enabled BPO that will fundamentally change the way day-to-day operations are run, moving away from the legacy BPO model. In addition, we have heard from clients the message, “great story but give us examples of how it all comes together.” So EXL also needs to convince its clients to come on this journey.

The work-in-progress V2 of the ‘Business EXLerator Framework’ is EXL’s approach to delivering a change in customer and business outcomes for its clients. What stands out to HfS from the visit, is alignment on the HfS Eight ideals of As-a-Service delivery, which we see as the building blocks for more collaborative and business oriented engagements, including:

Design thinking principles: The EXLerator team highlighted “effortless experience” for insurance customers as one of its key goals. The point, therefore, of EXLerator v2.0 is to give the EXL team a framework for helping clients create “effortless experience” for their stakeholders and clients. Instead of focusing on only traditional process views to make improvements, EXL is starting with comprehensive customer journey maps, taking an insurance customer/agent lens on, for example, lead-to-sale, and then working through the appropriate processes and where and when to use what technology to create that targeted experience.

Collaborative engagements working towards outcomes: EXL stressed its commitment to improving business outcomes, which are impacted by achieving process outcomes. In this way, EXL is making a distinction between efficiency (and KPIs) and business impact. Confusion between the two is what usually results in the “watermelon effect,” an industry challenge where the service provider delivers on its KPIs, but the services buyer is unhappy with the results of the engagement. Defining and delivering business outcomes comes with its own challenges, but we like the linkages that EXL is making with process outcomes as building blocks to overall business goals. For example, its client, a US personal lines insurer, outlined “cost per quote” as an outcome, which was reduced by 20% by EXL, through a 10% improvement in process accuracy using the EXLerator framework.

Actionable and accessible data and analytics in core processes: EXL is investing in machine learning and operational analytics as one of the key technologies that will improve core insurance operations with EXLerator v2. The journey maps we saw had clear points of decision making where analytics interventions could make a difference, such as the insights that agents and underwriters need in commercial underwriting. Its EXLerator analytics team sits on the operations floor and receives direct mentorship and guidance from EXL’s analytics practice.

The vision is gradually coming together for EXL as it evaluates how to change its traditional business and drive progressive services engagements that will survive the next 5-10 years of this industry. EXL has invested in developing or acquiring a lot of ‘pieces’ and is known for delivering on analytics, etc. but the EXLerator 2.0 framework looks like it is designed to bring it together to enable a journey with the clients.

Even with this progress, the hard work for EXL – like many of its competitors – starts now. The future is all about driving more intelligent operations that will help enterprises become digital customer-facing organizations. Technology enablement is a big piece of that puzzle and EXL has challenges to overcome in executing on its 2.0 vision. The EXLerator team is still fairly small and will be unable to hit EXL’s entire client base consistently, making those valuable “2.0” experiments slower to roll out. Additionally, its robotic process automation approach is currently hinged squarely on its partnership with Automation Anywhere, with which not all clients are willing to get on board. In its journey to create “effortless experiences” for end customers, EXL must keep working on how to make it easy for clients to join along for the ride.

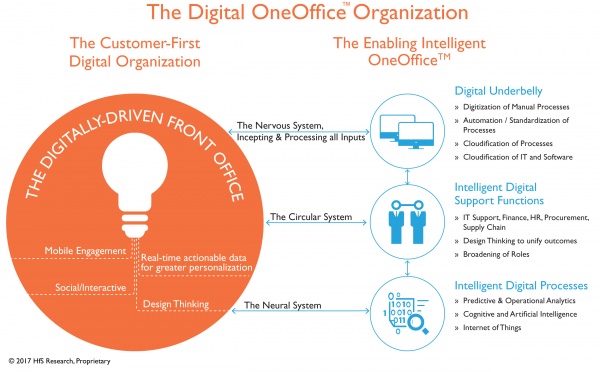

A digital organization has the ability to take all the cool social, mobile and interactive tech we use in our personal lives and create that experience for all the people in its environment: its employees, customers, and partners.

The Digital OneOfficeTM Framework is all about creating the digital customer experience and an intelligent, single office to enable and support it. In a few months, we won’t be talking nearly as much about intelligent automation and digital technology as the critical “value levers” for operations, as they become an embedded part of the fabric of the future operations platform for new generation organizations. Instead, we will be talking about an integrated support operation having the digital prowess to enable its organization to meet customer demand – as and when that demand happens.

Everything about the digital organization is about engaging people by responding to their needs instantaneously, giving people their choice of medium to interact with it, be it voice, chat box, text, Facebook messenger, email, virtual agent, etc.

The OneOfficeTM Framework is wrapped around the needs of the people in its environment, where automation is completely native and decisions can be made on predicting events, not merely reacting to historical data archives.

Myself and HfS analyst Melissa O’Brien, discuss the following during the webinar:

Why the Digital OneOfficeTM Framework is the Future of Outsourcing

How the new generation of enterprises are leveraging digital technologies to link the customer experience with the supporting operations

New dynamics we’re seeing in the market that point to a Digital OneOfficeTM future, based on 450 enterprise interviews

Our methodology for evaluating professional services firms to enable the Digital OneOfficeTM experience for enterprises – and how they stack in in 2017

You can read more about our vision for the future outsourcing framework, the Digital OneOffice, by downloading our complimentary POV here.

I recently caught up with Wendy Shlensky of HGS to talk about customer service trends on her blog. Here’s what we talked about:

Today’s companies are challenged to meet everyday customer service pressures while also building for the future. They must provide optimized customer service across various digital channels while also using new tools to better understand customer demographics and preferences, to deliver more personalized service. The ability to simultaneously achieve these goals is really a differentiator in a world where many products and services are commoditized.

Wendy: Can you share the trends you’ve seen in customer service?

Melissa: Today’s customer service trends are being driven by customer expectations for really simple and straightforward communication. In many cases, this means self-service tools, although customers also sometimes need to pick up the phone and speak with a person. Depending on objectives and available channels, customers will use various ways to communicate with companies to ask a question or give feedback.

Balancing self-service and digital—including human assistance, when needed—is a significant customer service focus area. Customer service solutions that pre-empt and solve customer inquiries—before requiring agent assistance—are driving self-service as a solution to decrease customer effort. Improving self-service is frequently put forward as a cost savings mechanism, but often has the most immediate impact on service quality and consistency. Most importantly, weaving all of the potential touchpoints to support an omnichannel customer experience is a design challenge for most organizations to undertake.

Wendy: How essential are digital CX tools in today’s marketplace?

Melissa: These digital tools are critical. At HfS, we have been working on the concept of a digitally enabled contact center. We have produced a competitive assessment of service providers in this space. Essentially, this means that a contact center is equipped to service today’s digital customer, who, as we all know, has increasing expectations in terms of communication channels. At the most basic level, the start of the digitally enabled contact center means embracing “digital” channels: social media; web self-service, including mobile apps and visual IVR; video kiosks; and chat. Also important is seeking to use automation to create efficiencies and the really smart contact center operators are trying to figure out how to involve increasingly intelligent automation into the mix.

However, it’s more than just implementing these channels, it’s the design of how each channel fits into the overall customer journey, and the understanding of how talent fits into the equation. This talent should not only be able to handle communication on varied channels that demand different styles (yet be consistent), but can also take contextual information from multiple sources and use that in a way that benefits the customer. From an analytics perspective, it’s all about using the data to better understand customers, enable personalization, and be more predictive.

Wendy: How is this changing BPO services engagements?

Melissa: Digital channels and the underlying technology will fundamentally change the way that service providers and buyers of BPO services engage. We have learned from our recent Intelligent Operations study that almost half of senior leadership buyers are using a “customer first” strategy to drive their sourcing models. This means embracing the change and solution ideals of “As-a-Service,” including design thinking. We see opportunity for service providers to use design thinking to help their clients develop better processes, especially around “customer journey maps.” Rethinking customer journey design is absolutely essential to the digital customer experience.

For example, HfS recently spoke with a retailer that was struggling with efficient scheduling processes for an in-store service. The service provider took the approach of interviewing the staff members fulfilling the services to understand the areas where they saw inefficiencies and problems. The results included a scheduling process redesign that blended the digital self-service channels and those that were human assisted. Often, design thinking projects will involve an employee-centric approach—recognizing that employees are customers, too, who often hold the key to improving customer experience.

The service provider-buyer relationship is also affected by buyers’ expectations of greater flexibility and value. Some service providers are looking to their BPOs to be really nimble, and scale, as needed. Additionally, they want their service providers to be thought leaders and help them figure out this puzzle of digital customer interactions.

Wendy: What do you see as the future of digital BPO?

Melissa: In a customer-first digital economy, BPOs will strive to find the right balance of technology and talent, and deliver that as effortlessly as possible to clients. Contact center service providers’ strategies must be multi-fold—they must provide something more valuable in conjunction with traditional operations that addresses automation and self-service, built in with exceptional support (with a great talent strategy) to address the changing contact center model to derive more value out of clients’ investments.

What’s one of the biggest wild cards, with the biggest impact? It’s artificial Intelligence, or the development of “intelligent” virtual assistants. While right now most contact center automation is augmenting agent talent, we are seeing virtual agent pilots and POCs that can replace some contact center talent. Regardless of how quickly this evolves, eventually artificial intelligence will have a material impact on contact centers. Service providers, together with their clients, will need to figure out how to blend the best of human and artificial intelligence, and most importantly have a greater sense of urgency to understand how this will impact the customer experience.

We’ve seen a number of consulting and outsourcing firms making investments in design thinking over the last couple years. The most visible approach recently has been the roll of acquisitions of design-thinking boutiques. A few representative ones that are being covered in our current research for the Design Thinking in the As-a-Service Economy Blueprint include:

Capgemini – Fahrehenit 212 (2016)

Cognizant – Idea Couture (2016)

Tech Mahindra –BIO Agency (2016)

Wipro – Designit (2015)

Accenture – Chaotic Moon (2015), Fjord (2013)

And while other outsourcing companies are not making acquisitions, they are partnering with design thinking firms (e.g., Sutherland with UXAlliance, Genpact with Elixir Design) and academic institutions that offer design-thinking curriculum (e.g., Infosys with Stanford d.school). Do their clients feel like it really makes a difference? From what I’m hearing in my interviews with operations executives, product managers, and finance transformation leaders to name a few… Yes, it does.

Here’s how:

From designing to doing: Design thinking offers an approach for a diverse group of people to work together to identify and articulate a common problem, brainstorm ideas for addressing it, quickly prototype/wireframe/storyboard and test it, and continue to iterate on the idea as it takes shape into a proposed solution. While designers often operate within a “non-constrained world,” Consultants bring a healthy dose of a reality check into the process, shared one interviewee. For example, a market-based and analytical approach adds context to the process of testing the ideas and prototypes for how well they could work in the business and how relevant they are to the market. Another executive described it as an “innovation agency” partnering with a “solution provider.”

Industrialization of methods and tools: Consulting and outsourcing firms have a rich history of standardizing what they have seen work in multiple instances. Many of them have been known to go to the extreme of “this way or the highway.” Most design thinking firms take a more creative, empathetic, and flexible approach, but are typically not as strong in analyzing, identifying, and setting standards. There are design-thinking agencies that are known for strictly adhering to standardized approaches and toolsets – IDEO comes to mind – but it is not the norm in the industry. Likewise, there are pockets of creativity in consulting and outsourcing, but, again, not typical. These two groups are starting to find complements in one another. Clients are appreciating this emerging combination of creative, engaging, and simple (thanks, designers) and standardized, contextualized (thanks, consultants) approach.

Research depth: Design thinking can be a richer experience through thoughtful diversity – bringing together people at different levels (hierarchy) in a company, from different business units and functions, and from different professional backgrounds (e.g., ethnographers, CPAs, and programmers). Design thinking firms are rich in creative professionals; and consulting and outsourcing firms can tap into industry subject matter experts, technology gurus, and change management leaders, as well, because of the breadth and depth of their organizations. They can help address needs from market sizing to industry experts to rapid prototype development with new, emerging technologies because of internal experts or their own ecosystems.

Recalibration underway

A key theme we hear over and over in the outsourcing industry is the drive toward “recalibration.” Outsourcing firms that have been in business for years were built on the premise of providing lower cost, higher efficient processes using best practices: Lean six sigma, and ERP or now, increasingly, cloud-based/SaaS platforms. But to keep doing something basically the same way and expecting different results is insanity (a refrain often accredited to Einstein) – design thinking offers an approach to finding those new results.

Bottom line: A design thinking led approach moves the focus of the operations executive and service provider partner off the process itself, off the internal, “what’s wrong inside of what we do” to “what do we actually want to achieve” (the business outcome), and what do we want people to feel and do naturally that will lead to further engagement and new—and different—results.

After seeing the impact of the human-centered, flexible, creative, fast approach within “innovation centers,” “labs,” or “digital” business units, consulting and outsourcing firms are realizing that design thinking can help a company and its clients reimagine something that desperately needs a new way of working. Outsourcing and service delivery is an industry suffering from hitting thresholds on cost reduction, failing to meet expectations of innovation, and wondering how to use digital technology and overcome barriers in communication set up within and between clients and service providers. At the same time, though, there are key aspects of rigor, process orientation, and service inherent in the services industry that fit well into enabling design thinking to move into solutions and results such as increased customer and employee loyalty and new revenue streams.

About 18 months ago, we thought – wow, what an interesting idea, using design thinking in the services industry. And we launched the first Design Thinking in the As-a-Service Economy Blueprint to explore whether it not it was feasible – if there were any examples of how design thinking was changing the way consulting and outsourcing firms work, internally with or for their clients. There were a few. As we go through the current refresh, we are finding that design thinking is actually changing the way many clients and service providers work, that there is a real complement between designers, consultants, engineers, and service delivery; and we will continue to share examples over the next few months.

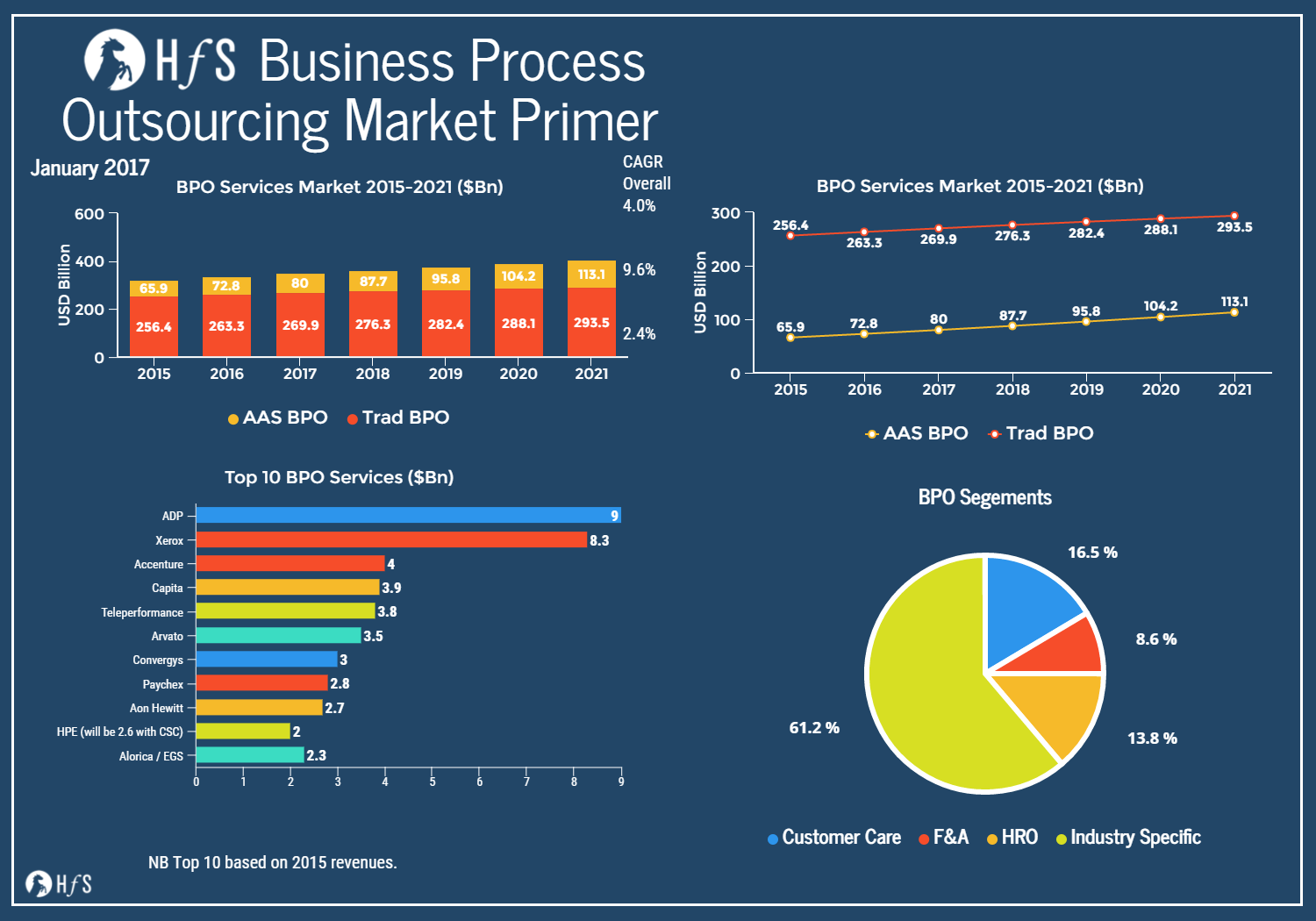

As we mentioned in our recent blog on the IT Services Market we are looking to make our content more visually appealing. So we have below the companion primer cover the BPO market for 2015 to 2021. We will be doing a full update of the forecast at the end of Q1. When we have a chance to analyze all the vendor results for 2016.

This chart gives our top level view of the BPO market in numbers – this provides a top level look at the market as a whole. We will be looking at producing a number of cuts of this data over the next few months, especially as we roll out our BPO Top 50 report and our updates to our market forecast.

The Bottom Line – Watch this Space

We are publishing a point of view on market conditions over the next few days, which presents these charts again with some additional commentary. Please find the piece at www.hfsresearch.com.

HfS has been spending the past several months talking about the Digital OneOffice – a business model focused on placing the customer at the center of every internal operation, even those not normally considered customer-facing. Whether you consider your firm a “traditional” business or a digital native, you need better customer centricity.

Recently I saw evidence of how this new focus on customer centricity is affecting the retail industry. Retail is rife with brick and mortar giants struggling to pivot their operations to support omnichannel shopping, and online upstarts vying to make their voices heard amid the e-commerce din. After hearing yesterday’s news that Target’s Goldfish project — its mysterious Silicon valley digital startup — now swims with the fishes, I started thinking about the tales I heard at the recent NRF conference. From both retail giants and small retail innovators, moving to OneOffice is about enabling the ability to support heightened customer expectations and often strengthening business fundamentals in order to do so.

Stepping into the Customer’s Shoes

Target’s stated reasoning behind abandoning the potential e-commerce spinoff was to renew a focus on the brick and mortar business, strengthening the personalization of the in-store shopping experience with greater personalization and payment options on its shopping app. In doing so, Target is putting a stake in the ground about where it wants — and doesn’t want — to compete. In the case of this retail giant, leaders see greater value in digitizing and optimizing the experience of its in-store customers than in creating something new that doesn’t necessarily jive with what customers want from Target. It seems counter-intuitive that focusing on brick-and-mortar stores helps in Target’s Digital OneOffice transformation, but this move shows that the retailer is honing in on its customers’ experiences where the customers want it.

This strategy had plenty of examples at NRF. I saw providers demonstrating solutions which have the potential for retailers to take their traditional businesses to the next level. These solutions ranged from getting real-time information from the store to engaging the shopper around product education to promoting promotions or specials while they’re making the product decision were top of the list for this kind of optimization. Specifically, here are some exhibitor examples:

Wipro Intelligent Displays: Wipro had a retail in-store demo which featured the use of sensors to allow the shopper to get more information about the product on a display screen in the store. For example, the shopper could pick up two items and compare them side by side as they would online or in a mobile app. This could also be reconfigured with near field communication (NFC) to connect to the app for greater personalization. I think this would be even more effective.

Infosys Home-to-Store Journeys: Infosys took a real customer-journey-centric approach with its immersive demo of a full home-to-store shopping experience. The journey demonstration begins in the customer’s living room, with the customer shopping on a mobile app and noting preferences and upcoming events (birthdays, vacations). The journey then moves to the store, and demo participants were greeted by name by the store employee who knew what items the customer shopped for at home. The comprehensive booth also featured a demo of the possibilities for augmented reality in store. Infosys is using a combination of technology and services to customize these journeys for its retail clients and showing what’s possible for the future of retail.

Sutherland’s Predictive Chat: A demo at the Sutherland booth highlighted a chat solution which originated with a design thinking approach to bridging store and online experience. The platform enabled more proactive engagement with customers by drawing customer data from various external and internal retailer sources, feeding insights into the chat which could pre-empt customer questions and concerns.

Honeywell Employee Tools: There were also interesting products at NRF. I popped by the Honeywell booth where I saw demos of plenty of tools aimed at making the customer experience better through improving the employee experience. This ranged from a software infused headset enabling pick and pack staff to more efficiently sort items in the warehouse (and move away from manual tracking!) to light, durable wearable scanners that employees can wear on the wrist or finger to enable more swift customer check out; all pointing toward creating better efficiencies in the entire process behind a shopping experience.

The bottom line: being customer-focused means improving the customer’s experiencein store as well as online. Remember that in store sales still represent the bulk of revenues in the retail sector.Optimizing legacy systems to make them complement new business initiatives in a way that supports customer experience is how retailers will successfully move to DigitalOne Office.

HfS has published its second analysis of the Salesforce services market. In the HfS Blueprint Report: Salesforce Services 2017, we analysed and positioned twelve Salesforce services providers according to their execution and innovation capabilities.

CSC and Hewlett Packard Enterprise (HPE) merged in 2016

NTT DATA acquired Dell Services in 2016

Acquisitions continue to be an important way to gain consultants and certifications. They can also bring valuable approaches and mind-sets that understand the cultural aspects of enterprises adopting cloud applications, which is essential to succeed in this market.

Service providers in general have continued to invest in developing service capabilities and investing in tools to support clients’ Salesforce deployments. Salesforce’s recent products, including Marketing Cloud, Community Cloud, and Commerce Cloud, change the value proposition from being simply a set of CRM tools to a complete customer engagement platform. As we highlighted in the 2015 note, Salesforce.Com Service Provision Must Have Real Investment To Succeed, Salesforce service providers need to adopt a holistic, business-led approach, and bring all relevant skills to the table, including mobile, security and social capabilities to differentiate in this market. While most of the current market is for Sales Cloud implementations, enterprises often expect the delivery of a complete solution, for example including mobile access to applications.

Growth areas identified in the report include:

Consulting services: including cloud readiness services and organizational change management services.

Ongoing management services: including advice on new releases and functionalities.

Analytics services: whether it is the Salesforce Analytics Cloud or an alternative solution

International deployments: more than 60% of current Salesforce deployments are in NA.

Leading service providers are investing in developing these capabilities, ahead of the market demand.

So, which service providers stood out?

In general, service providers in the Winner’s Circle have made impressive investments to achieve certifications for technical architects, Fullforce Master, and Fullforce Industry solutions. Salesforce itself views these as differentiating strengths in the Salesforce services market. These service providers also typically adopt a business outcome approach, supported by a strong vision for Salesforce effectiveness for clients. They have developed differentiating tools and services, and received among the highest client reference scores in the research. Accenture, in particular stands out as Salesforce’s biggest partner. As well as having impressive scale and bench strength, it continues to invest in services to further differentiate in the market. All the service providers in the Blueprint Report demonstrated a good understanding of the Salesforce service market and a desire to invest in innovation. Deloitte remains a strong contender for the leadership position, while Appirio, Bluewolf, PwC, Capgemini, Cognizant and NTT Data all impressed with their execution capabilities. All of the Blueprint participants had an impressive investment in innovation, including the relatively smaller practices. For example, Infosys, Tech Mahindra, Persistent Systems and VirtusaPolaris have developed proprietary solutions to support specific industry sectors. Moreover, Infosys and Tech Mahindra demonstrate good use of partners to develop solutions. Persistent Systems positions as a Healthcare specialist, and VirtusaPolaris is developing its analytics services.

What are we expecting next year?

The number of certified technical architect, Fullforce Master and Fullforce Industry solutions remains low in the market as a whole. Although they require a lot of time and effort, they represent an opportunity for all Salesforce services providers to differentiate in this crowded market. So, we expect all the players to drive certification programmes in these areas over the next year.

All of the service providers in the Blueprint Report have enhanced their service capability and proprietary solution development in the past year. Those who have made acquisitions, will solidify acquired entities and work on integrating offerings, and marketing new value propositions to clients. Others will continue to make prospective clients aware of their developing capabilities.

Bottom Line – Providers need to build market awareness to make a success of the Salesforce services market

Buyers need to prioritise technical skills as a selection criteria if they don’t already. As this combined with clear business outcomes are the main ingredients for a successful relationship. The path to success in Salesforce services market is clear: strong technical credentials, outcome based services and market awareness.

Indeed, lack of market awareness of capabilities was the most noted challenge in the service providers we profiled. Salesforce has thousands of service partners. In order to stand out, the service providers must make a considerable effort to increase awareness of their skills with prospective clients and with Salesforce, which often called upon to recommend partners to clients. Choice for buyers is increasing so building awareness and capabilities through certification is the best way not to be left behind. For more detailed recommendations for Salesforce buyers and service providers, see the HfS Research site.