To paraphrase Freddie Mercury, “Another bank bites the dust.” This time it’s First Republic Bank – the latest financial institution that was unable to sufficiently rebound from the liquidity crisis borne out of rising interest rates. J.P. Morgan scooped them up on May 1, with its Chairman and CEO Jamie Dimon widely quoted in the press insisting that this is not a global financial crisis repeat.

HFS tends to agree with him. Central banks and the financial services community have too much at stake to let that happen. It was a long road back from 2008. Trust in banks is still dicey at best. We expect we’ll see continued regulatory oversight, financial support and rescue buy-outs if needed to keep the global banking system functional.

While there is an undeniable crisis of confidence at play fueled by various macroeconomic factors and exacerbated by the spate of bank failures, crisis begets opportunity for the bold. Here are three recommended actions that growth-minded banks should take immediately to ensure survival at a minimum and potential leadership if done well.

- Continue investment in critical modernization initiatives.

- Digitize your commercial banking offerings

- Create actual offerings for small and medium enterprise clients, inclusive of start-ups and scale-ups

Let’s break these down…

1. Continue investment in critical modernization initiatives

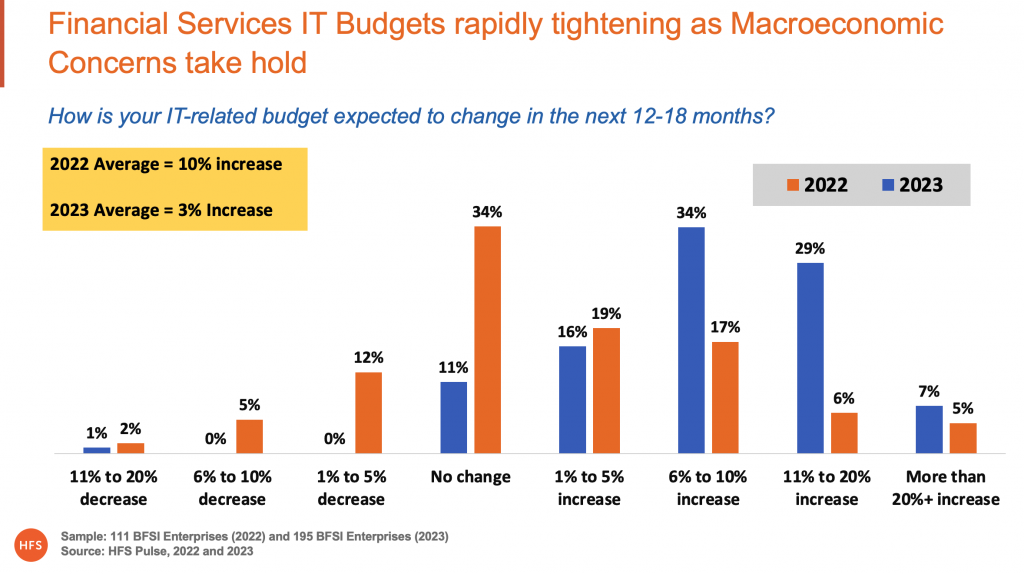

Before Silicon Valley Bank went belly up, global IT spending was already in a death spiral from the strain of ongoing macroeconomic conditions. With the pandemic largely at bay, everyone was forced to now pay attention to all the other contributors to macroeconomic malaise – global conflict, inflation, recession, talent challenges, and heightening cybersecurity risk. HFS saw this crisis of confidence reveal itself through a massive year-on-year slowdown in projected IT spending. As the below chart showcases, BFSI spending went from 10% projected growth in 2022 to just 3% in 2023, with the greatest portion of spending now sitting in the “no change” bucket.

This will further slow enterprise spending and related deal closures for services firms. This will persist for at least a quarter with the potential for stabilization and turnaround when banks fail and interest rate hikes quiet down, possibly in Q3 or Q4 2023.

As banks navigate the current mess, we beseech you – do not fall prey to the cost reduction path to perpetual mediocrity. While digital native competitors may be loads smaller than established banks, their technology nimbleness is real, enabling their ability to swiftly spin up new personalized offerings, use data to not just have a 360 views of customers but also to do something useful with the data immediately, and they can and are driving interesting new business models built on open banking and embedded finance. Smart banks need to have a firm understanding of which modernization initiatives are essential to enable growth. Core banking modernization and data migration to the cloud are two likely candidates that are well worth staying the investment course.

2. Digitize your commercial banking offerings

The four fallen banks of 2023 thus far – Silicon Valley Bank (SVB), Signature Bank, Credit Suisse, and First Republic Bank all had varied portfolios and customers. Still, they all offered a significant commercial banking proposition. These failures have already sounded the alarm for updated regulatory standards pertaining to interest rate risk. But they should also serve to raise awareness about the shoddy state of commercial banking – built for large enterprises and starved of digital investment. Smart banks should turn this so-called crisis into an opportunity to finally modernize their aging commercial banking capabilities. The impact will be better quality of service for existing clients and realization of the growth potential in SMEs.

A recent HFS survey of 150 commercial banking leaders revealed investment in offering expansion is heavily focused on enhancing existing capabilities not spinning up sexy new offerings:

- The same but better. The top three areas for commercial banking offering expansion are lending and lines of credit, deposit accounts, and commercial cards. Treasury services rolled in at number four. The emphasis is less on new offerings and more on better versions of existing offerings.

- Customer onboarding time takes too long. Respondents indicated the average time to onboard a commercial customer is 32 days. The leading factor slowing onboarding is implementation or integration requirements.

- Host-to-host connectivity still rules customer access. 65% of respondents indicated that host-to-host connectivity is still the primary standard for accessing products and services. Commercial banking leaders expect strong growth in API connectivity in the next two years.

- Current investments favor operations automation. Commercial banks indicated their current top area of investment is in intelligent automation of transaction and operations management. The top areas of investment in two years’ time shift from process optimization to international enablement with trade finance and embedded finance opportunities.

As banks consider their paths forward in the low-confidence economy, there is a clear need and growth potential in commercial banking that can be unlocked with appropriate investment.

3. Create actual offerings for small and medium enterprise clients, inclusive of start-ups and scale-ups

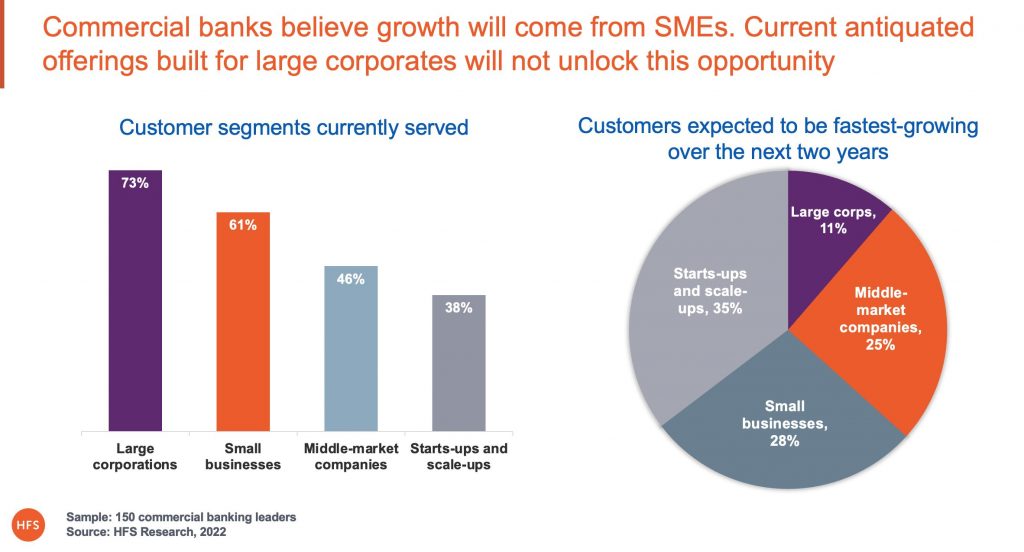

Commercial banking has largely been built for large corporates. The definitions of “large” tend to change based on the size of bank, but the customer baseline is very consistent – with large corporations making up the lion’s share of commercial customers served (see below). SMEs, start-ups, and scale-ups are represented, but often these segments are clubbed with and supported by retail banking businesses rather than being treated as commercial clients – or as their own unique customer segments. This is a missed opportunity to support and enable the growth of SMEs.

As Exhibit 2 also shows, commercial banks realize future growth will come from SMEs. The conundrum, though, is how to truly cater to these segments. The gaps left in the market by SVB, Signature, and now First Republic – all firms that were notable backers and supporters of SMEs – raise issues of bank choice, who is willing to support SMEs and innovative start-ups, and how to do so. As we suggested earlier in this piece, banks supporting commercial customers must invest in digitizing their offerings to deliver better services to existing clients. But it is also a critical ingredient to customer expansion. SMEs want the digital capabilities they’ve been enjoying on the retail side of the house with the benefit of traditional commercial services like various treasury services, lending and lines of credit, and merchant services – but done digitally. SMEs and start-ups, and scale-ups need to be treated as a distinct business segment.

The Bottom Line. Despite the crisis of confidence, there is a glaring opportunity in the face of the banking mess – better commercial banking

Banks should clearly shore up their balance sheets in the face of the liquidity crisis. Those not on Moody’s or other watchlists should consider seizing smart opportunities The need for better commercial banking is not new. But the recent bank failures have put a spotlight on banking choices and the options available to SMEs and innovative start-ups and scale-ups. There is a clear need and opportunity for digitization in commercial banking. As part of this investment, banks need to consider the needs of the SME community – typically representing over 99% of business in most country markets. These are your future growth customers, and they want offerings designed for them.