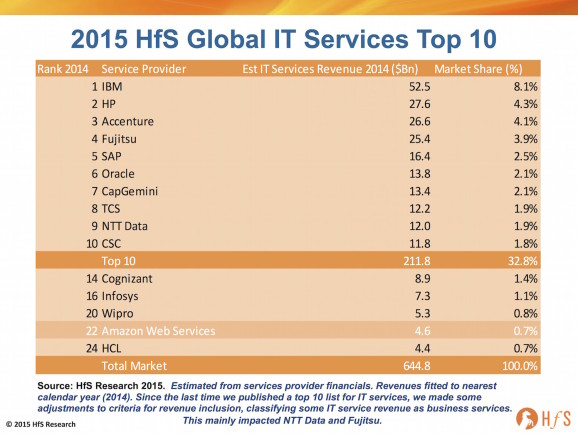

Yes, we threatened to update our annual look at who’s climbing and falling in the IT services world, after the storm we created last year when Jamie Snowdon put out the 2014 Top 10. So here it is:

Click to Enlarge

While the Indian-heritage providers continue to surge, here cometh Amazon

Last year, we observed the entrance of the first of the large India-heritage service providers into the Top 10 IT Services providers, with TCS entering the fray. Throughout the past decade, the five major India-heritage offshore-centric IT services providers have dominated growth in the marketplace, and had created a new market segment – a tier of fast growing services providers.

Over the last 5 years, we have seen another unique growth phenomenon emerge, representing another tier of the IT services market, a tier of even faster growth the cloud pure play providers. In this year’s 2015 list, we have included the Top 10 providers, the major 5 India-heritage offshore-centric providers and Amazon Web Services (AWS), as the largest as-a-service IT services provider (see above).

AWS has dominated the infrastructure cloud market with revenues as much as ten times larger than its nearest pure play public cloud providers, at over $4.6 billion. In response to this threat, the traditional providers are also staking a major claim to be in the As-a-Service business with IBM, for example, stating it now has achieved cloud revenues of $7 billion in 2014, with $3 billion of which is As-a-Service, with the rest presumably comprising more traditional consulting and integration services.

Accenture poised to overtake HP, Fujitsu wobbles

HfS’ Jamie Snowdon, Author of the HfS Global IT Services Top 10

IBM remains the lead provider thanks to its broad portfolio of technology products and services, plus its genuine global reach. IBM is one of the few providers with significant revenues in professional services, outsourcing/managed infrastructure services, application services and traditional support services. Although HP remains in the number 2 spot, consistently poor growth performances in its Enterprise Services group, over the past 3 years, creates the possibility of being overtaken by Accenture in the near-to-medium term. Fujitsu has slipped down the list, in part due to exchange rate, with ~60% of its services revenues coming from Japan and over-exposure to the recent weakness of the Yen.

Of the traditional onshore-centric service providers, Accenture has created a tier in its own right for the last 2-3 years, with a couple of exceptions, posting consistently strong growth quarter by quarter. A large part of this success has been its dual role as a strategic thought leader for its clients, in addition to its focus on delivering global services across an expanding array of global delivery centers, most notably in India and the Philippines. Accenture’s focus on balancing consulting with managed services has helped support the firm’s differentiation and revenue growth in the industry. In addition, its early wins in the digital space that brought about new investments in technology could lead to significant new business value and wealth being created for the firm.

SAP and Oracle both have large professional services teams, accounting for ~$3.7 billion in revenue, for both providers. However, HfS includes their product support revenues in its IT services definition that pushes both providers’ IT services revenues to the level above.

Capgemini and TCS move on up

The last 12 months have been good for Capgemini, has managing to remain robust with solid organic growth across its regions, particularly in North America, Asia, and the UK. Its continued focus on portfolio management, taking the best ideas from its large teams of local consultants and building global repeatable business seems, to be working and helping it to grow against the tide in the difficult continental European markets. Its acquisition of IGATE adds some much-needed capabilities and scale in Indian IT services delivery, particularly in financial services markets.

TCS stellar growth trajectory has continued at a 15% clip, rising to the number 8 position. Despite being the largest of the India-heritage providers, TCS has continued to grow its IT services business at a pace that belies its massive scale. TCS’ strategy has very effectively broadened its service portfolio, providing customers with a comprehensive set of services in all the markets it plays and has been effective at adapting its services to the idiosyncrasies of local markets, particularly in Europe. In addition, TCS’ focus on organic growth seems to have served the firm well, while most of its India-heritage competitors are more focused on acquisitions.

Traditional IT outsourcing not dead, just limping, the shift to As-a-Services is already underway

The changes in market share over the last year show that even as economic conditions improve, the IT services providers cannot expect an instant return to strong growth without major investments into their delivery organizations. Plus, in spite of solid performances of the India-heritage providers, there already appears to be another stalking horse approaching the market in the shape of the “As-a-Service” providers. While offshore labor arbitrage has been the catalyst for increased revenue growth over the last two decades, the shift to less labor-centric As-a-Service offerings that are more dependent on automated technology platforms and more specialized skill sets, is starting to alter that dynamic.

Despite these secular challenges, we don’t expect the traditional IT outsourcing market to disappear in the short term. One of the criticisms we hear most often about cloud services is the lack of end-to-end support and good quality holistic services. If anything, we expect services to both scale down to meet cloud based services and to add better servicing and scale into traditional style managed services deals. However, the shape of the prime outsourcing contractor agreement is likely to change – with an increasing emphasis on the technology partners and cloud services providers engaged to bring the infrastructure offering together and, increasingly, a more diverse set of application services companies delivering turnkey and custom applications. Moreover, capabilities around robotic automation, analytics, cognitive computing and self-learning are gradually coming to the fore, with many enterprises more willing to make investments in technology-driven As-a-Service outcomes than merely labor savings based on offshore delivery.

However, the end of 2015 and 2016 will mark another critical moment in IT services market, with questions about what will become of the traditional enterprise infrastructure outsourcing market as AWS makes huge disruptions to the legacy model, with its cloud based As-a-Service model. These changes will be particularly important for services providers that have struggled to adapt to the new market conditions – HP and CSC are two of the traditional providers we will watch with particular interest as they continue their annual ballet to survive and continue their growth path.

The Bottom-line: Expect AWS to surge into the top 10, Cognizant to continues its climb and the new breed of As-a-Service providers starting to emerge

Not long after the initial impact of the offshore providers, a new wave of disruption is beginning to have an effect on the IT services leadership. Indeed, we expect the pure-play As-a-Service providers to target positions in this top 10 list, particularly AWS. We see the most exciting developments happening with these providers. If AWS maintains its current growth rate, it could be in contention of a Top 10 space by 2016 and likely to have one in 2017. This is a big if, as it would need to maintain its 50% growth rate, but certainly not impossible in these fast-paced times.

We could see TCS joined in the top 10 by another offshore provider, Cognizant as early as the 2016 Top 10, although looking at its results so far, this seems unlikely. Particularly, given the Atos acquisition of Xerox US IT outsourcing business and the expected $2 billion boost in its revenue (currently they are $10.5 billion at number 11), and it is doubtful whether Cognizant will hit the $12 billion market in IT services to catch them or NTT Data, although this may happen in 2016. We may see this delayed or overtaken by the inclusion of AWS.

Everyone is talking about the two-tier nature of the IT services market at the moment – largely dividing the market between traditional services markets like IT outsourcing and new solution based services around the adoption of digital technologies (social, mobility, analytics and cloud). With flat or declining market growth in the traditional services businesses and double digital growth in the emerging digital space, it is no wonder why most of today’s service providers are pushing some form of Digital in their service portfolios. However, the competitive landscape is increasingly multi-tiered and you could argue it is currently divided in to three groups: traditional technology services companies, India-heritage providers and now the pure play As- a-Service providers. What is also worth noting is the renewed buying up of niche talent by the leading IT services providers in the high-growth SaaS markets such as Salesforce, Workday and SAP Successfactors.

Over time, we expect the first two categories to merge and the distinction between these groups moving away from location or offshore, but to the success of bringing digital to life – and enabling digital for enterprises (not just selling basic IT services to implement apps). By that, we mean demonstrating that they can utilize technology within their client’s business to generate business value. We expect some of the offshore providers to transition more permanently into the slower growing group – we have seen temporary examples of this already with both Wipro and Infosys flirting with lower growth over the past 2 years. We will also see higher growth emerge from some of the traditional providers as they shed more of their legacy business, but retain the higher value work and build on the thought leadership they have created around digital.

The addition of providers like AWS into the mix will further commodify the infrastructure management business, however, as mentioned above this will not mean an end to managed services. It just will change what the outsourcing providers manage – they will not be managing as much of the physical technology directly. The role will be more virtual managed service, orchestrating and managing a big catalog of services delivered, in some cases by themselves, but increasingly by an ecosystem of partners. Many of these partners will be this new tier of provider, the pure play As-a-Service companies.

HfS subscribers can download the HfS Global IT Services Top 10 report here.

The silicon valley giants are not satisfied with embedding themselves into your phones and laptops – now they are looking to connect up our cars, bank accounts, air conditioning systems, washing machines, even our hair dryers (OK, maybe not hairdryers just yet)… They want to manage data tied to your whole life, not just your computing activities. Live with it, it’s happening.

Suddenly, IT services are morphing into “Things services”. So we decided to get ahead of this and conduct exhaustive research into how the leading service providers are shaping up their capabilities and investing in this emerging space. HfS’ Charles Sutherland is a walking, talking, breathing example of the Internet of Things. He’s plugged in 24×7 into a global network of devices and companies operating said devices. Yep, he never stops, and his research into autonomics has naturally pulled him into this market.

Charles and his team have been conducting exhaustive research interviews over the past few months with many enterprises to learn more about their experiences with IoT, in addition to the performances of their service providers to provide the bread and butter service delivery and assess their innovative capabilities, vision and investments.

So Charles, why have we undertaken an HfS Blueprint on the IoT services market today?

Because we wanted to sort through the daily avalanche of IoT related press releases, presentations and conferences to understand how 18 different service providers were really designing and delivering IoT services for enterprises clients. HfS is focused on the emergence of the As-a-Service Economy and the impact that digital services are having on IT and business processes and the IoT is part of how those are coming together for clients today. It is still very early in this market but we wanted to assess how service providers compared to each other as they build their execution and innovation capabilities to deliver IoT today.

How does HfS define the IoT Services market?

IoT Blueprint author Charles Sutherland is HfS Chief Research Officer (Click for bio)

We believe that there are 5 components to the IoT Services value chain today available from service providers. There is IoT Consulting, which includes planning, technology road mapping, governance strategies and custom app development. IoT Enablement that encompasses product engineering, sensor development, software engineering, embedded technologies and security services at the device layer. We also include IoT Connectivity which brings together network engineering, implementation and security. There is also IoT Integration for databases, SI, analytics implementation and application modernization. Finally, IoT Management services, which include device management, cloud hosting, network and data management. It is a complex value chain that typically requires the coordination of many partners to deliver a complete system, which is a theme we return to again and again in assessing the state of the market in this Blueprint.

What is the state of this IoT Services market?

Overall, HfS believes that the IoT Services market is still very much in its infancy. Despite the daily flow of press announcements and articles on IoT, it’s clear that overall proofs of concept (POCs) rather than large-scale system deployments are the most prevalent cases out in the market today. 2015 has seen a figurative explosion in PoCs for IoT and we expect this to begin to transition into a greater deployment of production systems in 2016 and beyond. That said, IoT will still take some time to achieve scale, because both enterprises and service providers are approaching IoT from many different angles and with a great degree of circumspection as to what the long-term goals are of these IoT initiatives. Will IoT enable greater operating efficiency in the business as it exists today or will it facilitate the creation of new markets and disruptive behavior, that is still very much an unanswerable question in the market as it exists today.

So which service providers are shaping the IoT services market?

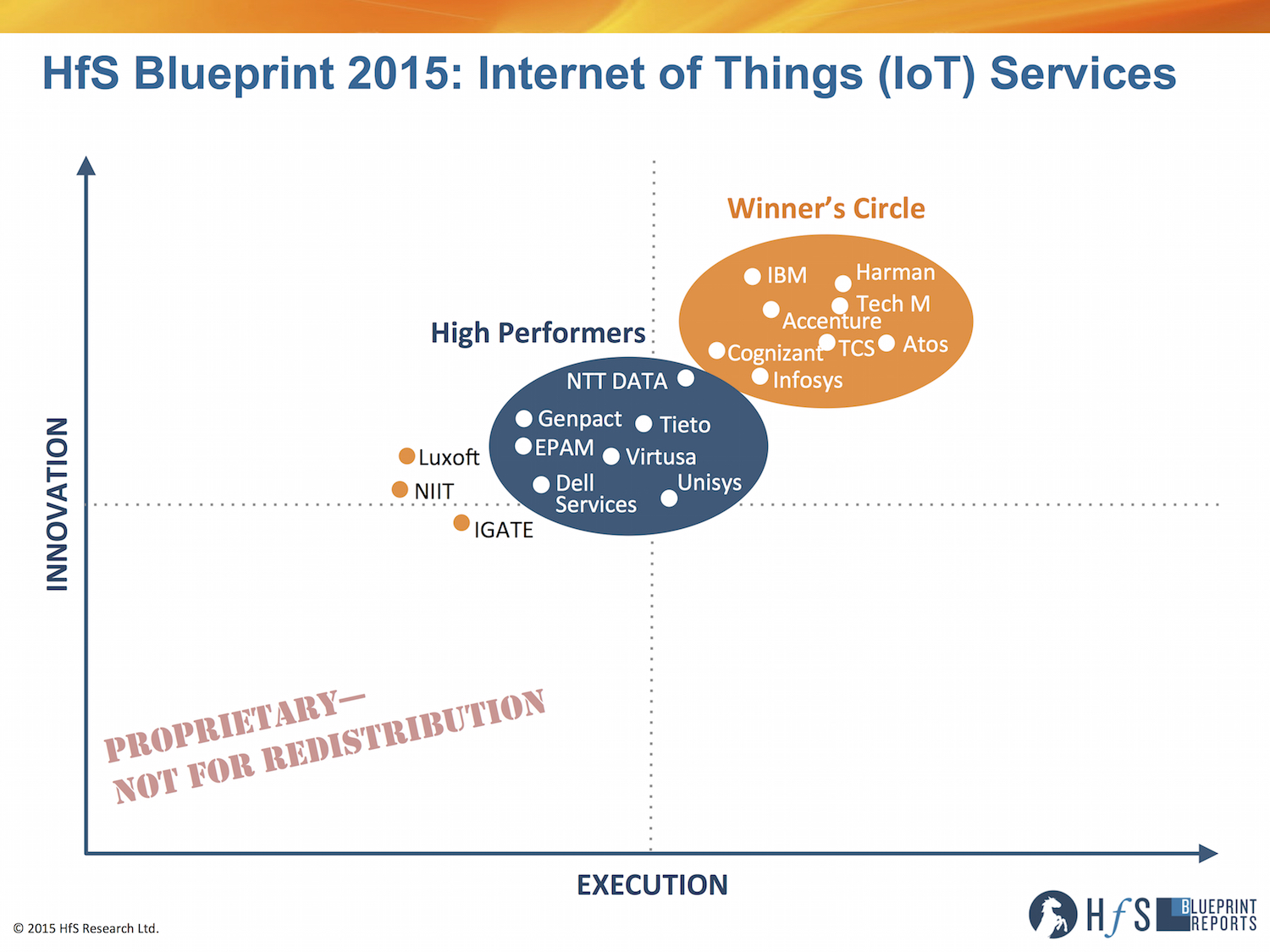

Our HfS Blueprint methodology, which incorporates crowd-sourced evaluation metrics on criteria related to both Execution and Innovation together with client references, resulted in 8 service providers being captured in our Winner’s Circle. These were Harman (including the recent acquisition of Symphony Teleca), Tech Mahindra, Atos, TCS, IBM, Accenture, Cognizant and Infosys. Each service provider has addressed this market differently but many share some common leading characteristics as well. We cited Atos, Harman and Tech Mahindra for the capabilities of their proprietary delivery models for IoT. Accenture, Atos, TCS and Tech Mahindra were noted for focusing on as-a-service pricing models for many IoT engagements. Cognizant, Infosys and TCS also scored well for their willingness to co-invest with clients in projects to develop IoT related assets, which could be brought to other clients. While Harman, IBM and Tech Mahindra have been aggressive in acquiring the capabilities they need to lead this market through integrating specialist firms and capabilities at scale. Finally, Accenture and IBM showed well in developing a wide variety of industry models and related skills for IoT deployment in the G2000.

We also identified a further cluster of 7 service providers as our HfS High Performers including: NTT DATA, Tieto, Genpact, EPAM, Virtusa, Unisys and Dell Services all of whom are making investments to grow their capabilities and become participants either directly or through partnerships across the entire IoT Services value chain.

What are the major trends we see which will impact these service providers over the next several years?

Well first of all the competition will continue to intensify. IoT is a magnet today for investor funding not just in Silicon Valley but globally and from this both many more potential partners and competitors will emerge to the service providers we see here today. That growing ecosystem will mean that definitions for the market will remain fuzzy for many as capabilities across design, mobility, cloud, analytics, supply chain and more get integrated into what are defined as IoT projects. This complexity also means that both service providers and enterprises need to deploy both Design Thinking and Systems Thinking when looking at IoT so that the projects solve real business needs and then account for all of the inter-relationships with broader processes and technologies both in the enterprise and outside. Improving partnering skills will also be a key trend for IoT service providers as so many different players are required to bring many IoT concepts to scale and traditional ways of working autonomously found in other IT fields will not work with IoT. Finally, creating data lakes and stitching together the myriad of APIs involved in IoT will be important for service providers as will enhancing analytical and process skills to account for these new capabilities.

So given all these developments in the IoT Services market, what recommendations do we have for enterprise buyers through 2015 and 2016?

HfS believes that enterprises that want to make the most out of investments in IoT going forward should:

• Select IoT initiatives with care. It can seem easy to roll out new sensors and devices but integrating the resulting data and changing business processes is often very complicated and expensive and not all PoCs will make economic and strategic sense to pursue.

• Demand service providers co-invest in innovation and are willing to be experimental in their solution designs.

• Keep the attention internally and with partners on security and risk management in IoT as PoC and evolving deployments may be creating new access points into the enterprise often with high sensitivity and a failure to manage this may cause unforeseen problems over time.

• Stay calm. Most of the IoT activity in the market including in competitors to the enterprise remains at the PoC level today. Yes, much of this may be disruptive over time but not everything that happens in this market will be successful and seeing a path through for the enterprise requires both investment and patience.

And what recommendations do we have for service providers through 2015 and 2016?

HfS believes that service providers that want to make the most out of investments in IoT going forward should:

• Build out Design Thinking and Systems Thinking skills to create new more business outcome based IoT projects and deployments.

• Learn to partner better both within the service providers, with enterprise clients and across the IoT ecosystem.

• Integrate internal silos so that IoT skills don’t become buried inside of practice areas that are isolated from broader developments in process, mobility, design, analytics, engineering and cloud capabilities in the service provider.

• Finally, recognize that not every IoT investment will meet its goals in these early days and not every client project or co-investment opportunity will create a repeatable asset for other clients. Right or wrong, the majority of the works in IoT for the next several years will in HfS’s opinion still bespoke solutions for individual enterprises rather new industry platforms for the service provider to exploit. Stay wise, stay calm and stay busy and the potential of IoT will be there.

So what are you doing on Guy Fawkes’ night? Well, rather than blowing up Parliament, why don’t we start with the legacy analyst business?

With the swirl of social media, free information and business model disruption in the technology world, everyone assumed the traditional analyst world would follow suit. We thought there would be a plethora of new generation analyst boutiques cropping up to challenge the old model. Some tried, and most have failed. A few linger on in their death throes, but the revolution we thought would happen – let’s face it – never really did. Except in one corner—right here at HfS.

I’ll be presenting on Research-as-a-Service and how HfS is changing the face of the analyst industry

As we look around the industry, we see the same old legacy analyst houses producing their useless charts and dull, turgid research just as they did a decade ago. Few subscribers actually read the stuff, but technology vendors still fund these firms because they have few other outlets to justify their existence.

Here at HfS, we’ve been fortunately enough not to be beset by legacy contracts and the dirty vendor dollar to give to industry a very different analyst model – one where we are unafraid to make our research widely accessible to the world with our freemium model and call out the real trends that are happening to our industry (as opposed to regurgitating the same old marketing fluff that turns off the smart buyers). In short, we’ve thrived because of our huge global community, our continuous demand data from our readers and a team of great people and analysts who love the freedom of Research-as-a-Service.

This is where the real fireworks will be on the 5th November…

I’m pleased that I’ll be in London on November 5th to share our story as I keynote the Analyst Relations Forum. My keynote, Thriving in a Market that Refuses to Change: Research-as-a-Service, will look at how HfS has fought to transform a conservative industry that has been slow to change.

I’ll also be having a fireside chat with Wipro’s dynamic new CMO, Naveen Rajdev, and we’ll also hear from Accenture’s popular Managing Director for Global Analyst Relations, Allen Valahu, about what it’s been like to work with a multitude of analysts over the last two decades and what they would like to see in the future (see full agenda for the menu of analytical delights).

We are providing 10 free tickets for those who hurry to register! Sorry—all gone!

We have made special arrangements for ten free tickets to the event (with promotional code JoinPhilFersht) – first come, first served! Sorry—all gone! But we also have arranged for a $124 discount (with promotional code ARForumKeynoteHfS) for those who did not manage to register in time.

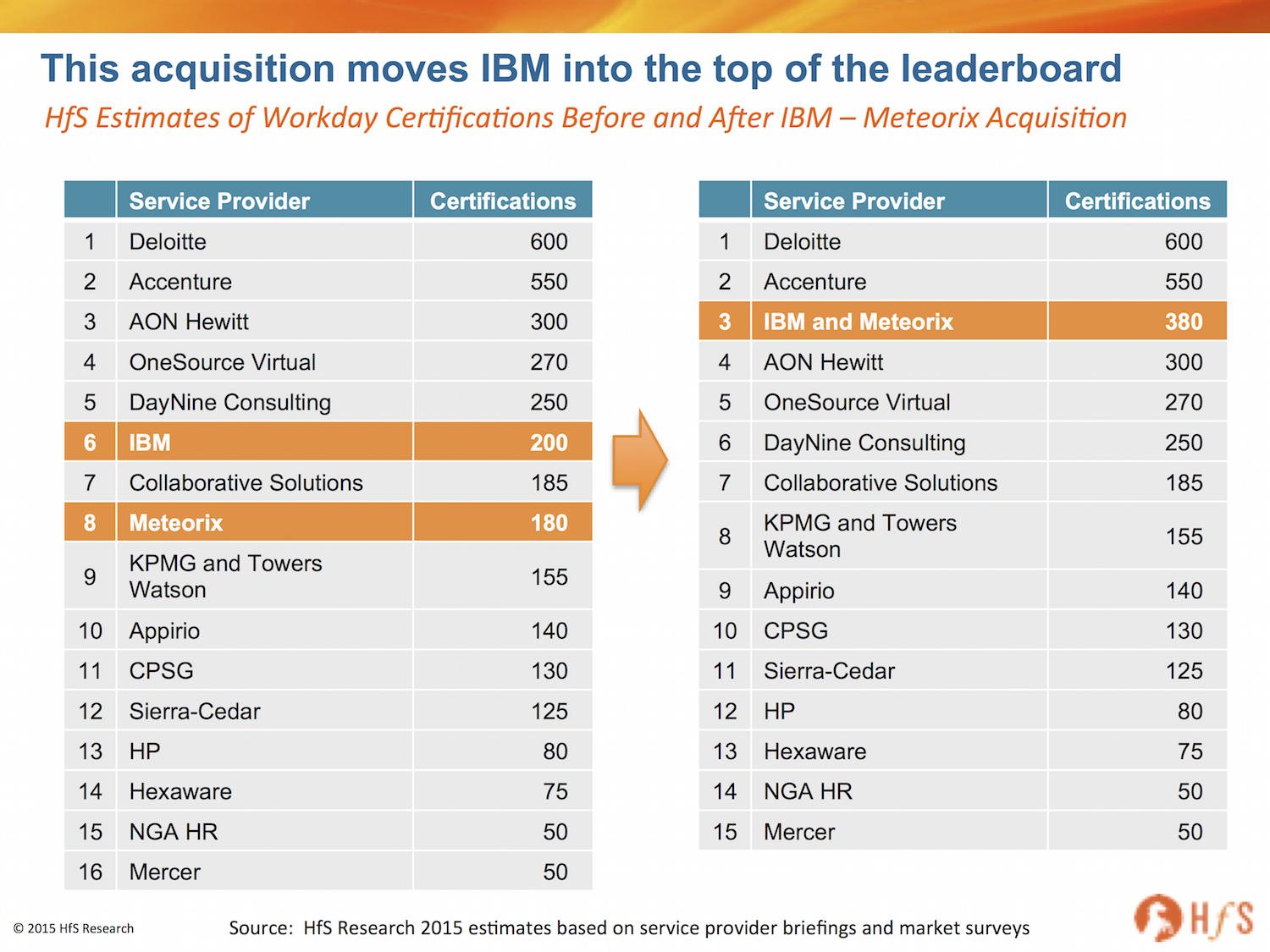

Just when you thought IBM’s Global Business Services was cratering into an As-a-Sleep state, having sold-off its call center business exactly two years’ ago, Big Blue’s next-gen services star is once again shining, with the acquisition of one of the finest up-and-coming specialist Workday services firms in the market: Meteorix.

Every HR head wants a Workday rollout… and every SI wants a SaaS services acquisition

There is a clear scramble for talent which can implement and support popular SaaS platforms, such as Workday, not completely unlike what happened with specialist consulting firms supporting the ERPs in the ’90s and 2000s, such as SAP, Oracle, Peoplesoft et al. Specialist SaaS services providers supporting SaaS products, such as Workday, Salesforce, SAP SuccessFactors, NetSuite, ServiceNow and Google apps, are now in hot demand as ambitious global service providers seek to avoid the commodity trap of legacy software maintenance, which can still generate revenues, but not at the growth rates of past years.

As HfS, we estimate this has set IBM back something between $80-$100m and adds 180 certified Workday consultants to IBM’s stable. This creates the third biggest Workday services player in the market, with a total of 380 certified Workday consultants and elevates IBM into the coveted Winner’s Circle of Workday service providers (please note this is numbers of certified Workday consultants only):

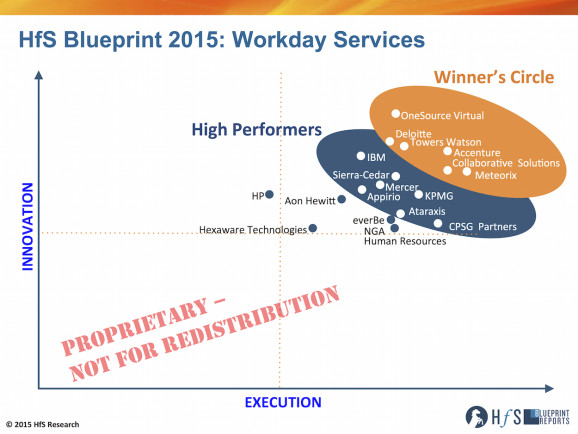

IBM has acquired one of the leading up-and-coming Workday services specialists, which leads the industry for execution capability for Workday clients:

Click to Enlarge

Positives of the acquisition:

Adds considerable scarce talent in a hot market. Not dissimilar to the recent Accenture acquisition of Cloud Sherpas, these SaaS services takeovers are all about the large providers hoarding scarce As-a-Service talent. This deal effectively doubles IBM’s share of certified billable Workday consultants and gives it greater scale and capability to compete with the likes of Deloitte, Accenture, AON Hewitt and OneSource Virtual on large Workday deals. Meteorix staff brings an excellent client culture, collaborative reputation and great array of new clients – different from the pedigree HR transformation talent KPMG recently acquired from Towers Watson, but nonetheless great practical implementers and practitioners of Workday. Our recent Blueprint report reveals that 60% of Meteorix’s customers are in on-going “post-production support” state, one of the critical ingredients behind this deal: acquiring talent that drives the business transformative needs far beyond the initial implementation and go-live activities.

Empowers IBM’s ambitions to control core enterprise data. Being the service provider which controls the creation and interpretation of critical enterprise data, especially the knowledge of the global workforce, really creates a client stickiness that could be more powerful than ever before. Integrated SaaS suites, like Workday, have this capability to enable truly integrate data repositories – hence the trusted service provider of record will be in a very powerful future position to service its clients and deepen its footprints.

Prevents other disruptive As-a-Service providers entering the market. Unlike Salesforce, which has a much more mature ecosystem of service partners, there is a feasting on the small band of worthy specialists in the Workday arena, and they could all be swallowed up by the large players in a couple of years. There are really only a small number of attractive potential acquisitions left in this space after this acquisition which boast genuine scale in numbers, most notably OneSource Virtual, DayNine and Collaborative Solutions. In many respects, not making an acquisition of this ilk could have been more damaging to IBM’s ambitions in Workday world…

Adds considerable services methodology to the IBM capability library. Meteorix has already build more than 1000 reusable integrations into Workday. If IBM can effectively leverage these into its global practices, there is some serious scope for scaling and expanding its Workday business.

Adds real North American depth and entry into the lucrative higher education market. While Meteorix was not strong with multiple vertical industry depth, it does bring capability in the hugely lucrative US higher education market, upon which IBM can capitalize. It also negates IBM’s need to partner with Sierra-Cedar in this sector and go after the space solo. What’s more, Meteorix’s North American bench is well complimented by IBM’s resources across Europe and Asia, even though most Workday demands tend to be confined to the North American market at present. There is also the opportunity for IBM’s practitioners to share their considerable years of SAP HR knowledge, that tend to span much broader global engagements across Europe and Asia/Pac, to where many Workday clients are hoping to expand their platform next beyond North America.

Mid-market focus and scale potential. Meteorix has tended to play in the upper-middle market space, which can provide a great platform to target enterprise level clients. Not dissimilar to the ADP strategy of building the competency in the mid-market before scaling the solutions to move up, IBM has a great opportunity to do this with its new Meteorix talent and IP. There is a huge amount of intellectual property to leverage – the key is to retain the talent and train it to work with higher end enterprise clients – and charge higher-end billable rates!

Potential negatives of the acquisition:

Retaining the new staff. IBM will really need to work hard to create the right culture for its new found talent. This is its first significant services acquisition for some time and it needs to make this work. Meteorix had a very distinct culture, which needs to be nurtured and not suffocated under Big Blue doctrine.

Lack of a SaaS-centric services practice. Accenture’s acquisition of Cloud Sherpas is being integrated with its Cloud First approach, where consultants are trained to implement – and then provide – ongoing support for cloud clients. IBM needs to create something similar with Meteorix to avoid merely being a glorified systems integrator for Workday. The cardinal sin with SaaS is forgetting that SaaS is about empowering the end customer, not the consultant, and this is something IBM’s GBS group needs to work hard at creating. All the major SIs, like IBM, have made billions over the years selling IT programmers to stitch together legacy ERP platforms, which is not the case with true SaaS platforms like Workday. IBM must ensure it instills and develops the business insights and skills for its clients, well beyond the go-live moment, if it truly wants to create deep analytical tentacles with its key clients. Again, As-a-Service is about empowering the client, not the consultant…

Click to Enlarge

Enterprise-enabling Meteorix’s methodologies. While this should be a major strength, this could also be a major weakness of IBM fails to nurture it’s IP and talent and grow its client base across both the mid-tier and enterprise domains. With its determined focus to develop its Watson offerings and cognitive computing capabilities, there must be considerable focus on investing in the “Born in the Cloud” clients of the future, and not just today’s resource-laden legacy enterprises.

Creating strong Workday capability across both HR and Financial Management domains. The speed at which Workday’s Financial Management modules are being evaluated and implemented is really beginning to pick up, and it’s vital for the multifunctional providers, such as Accenture, Deloitte and KPMG to develop delivery and transformation skills across both HR and finance Workday domains. While encouraging to see IBM being affiliated as a Workday FM partner, it’s important to see the firm develop comprehensive Workday delivery skills across both domains long-term.

The Bottom-line: IBM makes its As-a-Service claim, but the hard work starts now

Just when it really seemed that IBM’s services strategy was simply to tie everything, in some way, to Watson, this acquisition is a refreshing reassurance that Big Blue is still very serious about competing for today’s enterprise services with the leading global characters. Now the real hard work is adapting to the new enterprise services culture of empowering the client and building genuine repeatable, scalable methodologies for the future. It’s also about creating platformized solutions for the F500 of 3-5 years’ time and not simply catering to the needs of monolithic enterprises today. We believe IBM recognizes its challenges and is making measured strategies to get ahead of them. However, recognizing is one thing, addressing, making sacrifices and ultimately succeeding is quite another…

The BMP Masala Dosa Reality: Great product, Weak Message

My recent experience of dosas, one of Southern India’s favorite food snacks, typifies the potential and shortcomings of India’s BPM (Business Process Management/Outsourcing) industry. The product is fantastic once you experience it, but, as a Westerner, you probably haven’t got a bloody clue what you are actually buying.

“It’s a bit spicy, sir” was the response, when I asked what the Mysore Masala dosa actually was. At that stage, I just took the plunge, but a little more description of why this food product is very tasty and will meet my desired hunger-fulfillment outcome, would have really helped close that deal.

This scenario isn’t a million miles from the typical experiences of dealing with an Indian-heritage business process service provider….

Coming back from the excellently well-attended and content rich 2015 NASSCOM BPM strategy summit in Bangalore this past week, I find myself feeling conflicted between excitement and frustration for the future of Indian-centric business process management / operations services.

My excitement

Execution is better than ever. India-based process delivery is getting really good. The tiresome client whining about poor execution and failed promises is become fainter than ever, with the vast majority now proudly talking about how smoothly their offshore operations are running. At HfS, we don’t need to visit India to get this feedback, but seeing so many operations up-close is always a good refresher to reinforce the progress being made.

India has massive potential to lead the world in process delivery centered on analytics and robotic process automation. This was, personally, my biggest reinforcement. India delivery is all about passion for processes, getting them executed and doing smart things to make them run better and throw off meaningful data. Most of the analytics and automation needs of today’s BPM deals are not rocket science – it’s making sure insurance claims, invoice generation, order management, credit and collections etc remove unnecessary manual steps, produce the outcomes clients want at lower cost of delivery. Most of the competent BPMs are now deploying bots in their centers alongside their staff, leveraging many of today’s off-the shelf tools, such as Automation Anywhere, Blue Prism and UiPath. And they’re pretty damn good at it.

BPM providers have a real permission to play as As-a-Service providers. Barely 2-3 years’ ago, most industry folks assumed a service provider had to be a serious purveyor of IT services and business processes to be taken seriously as a one-stop-shop for Business-process-as-a-Service solutions. Analysts and advisors clamoured for the pureplay BPMs to merge with the IT services shops lacking business process capability, in order to get ahead of the emerging wave of solutions that have cloud-based technology platforms powering the processes. Today, that assumption is a fallacy, as the confidence in public cloud from most enterprises shifts the service provider differentiation from IT to process excellence. Noone questions the competence of a professional provider to host as-a-service platforms, such as a Netsuite, Workday, Blackline, Coupa, Salesforce (or homemade solutions) – the onus shifts to said provider’s ability to provide the bread-and-butter fulfillment, the analytics, process automation and creative services to deliver their clients outcomes and achieve attractive cost-reduction targets.

Big is no longer beautiful as the new wave of BPM deals emerge. Many of the leading BPM service providers have become endowed this year with bulging pipelines of potential new business – the only headache for them being that most of these new potential deals are coming from the next layer down (in size) of buyer, and from buyers wanting narrower scope of delivery. Moreover, buyers are getting fed so much information about cool things such as digital, analytics and robotics, they are demanding a lot more complexity from providers, than merely a simple lift-shift-transition of staff, at minimal business risk. Simply put, most of the new deals are just not as appealing from an economics perspective, and it’s much more effort to cobble together a winning solution. However, for the ambitious service providers, there’s a lot of business out there to keep them growing and drive them toward building integrated As-a-Service solutions.

My frustration

Lack of decisiveness. It always baffles me why many Indian-heritage providers can see that’s happening staring them in the face, but, instead of aggressively getting ahead of the change, they opt to play it safe and copy what everyone is doing. I was disappointed with the approach of many of the service providers refraining from hammering home their distinctiveness, instead opting for the canned messages that, quite frankly, said little of their differentiation, beyond the fact they were quite good.

Very poor positioning of analytics and automation. These capabilities must be front and center, aligned to industry and horizontal process acumen. Instead, most of the BPM providers seem to have forgotten that analytics is the most important differentiator, and plop in automation as a one-slider towards the back of the sales deck. There is an obsession with following the messages of the IT services firms (which spend loads more on marketing hype), than focusing on real process capability, which is really what they are selling. If I want to buy digital technology platforms, am I really going to call up a BPM firm? And if I want process excellence, am I really going to call my local app testing extraordinaire? C’mon people, let’s get a reality check here. Indian BPM firms range from average to very bloody good at managing data and automating basic process delivery. This is where they need to focus.

Automation paranoia must cease. While I would agree there is a genuine move toward FTE elimination in customer call center services, through smarter automation and better tech (which has been going on for about 30 years now), when you get into the rest of the back office world, most automation is about streamlining elements of the processes, not replacing entire FTE roles. These soft-savings are offset by creating more capacity for staff to focus on interpreting data, proactively addressing client needs, adding genuine value to the service delivery. Now, if there are staff who only ever do the most basic of transactional processing, there will likely be some work for that individual on a less sophisticated client engagement, or that staff member may simply need a career rethink – most people really don’t want to do boring transactional office jobs anymore. Net-net by embracing new automation technology and proactively upping the value of the service delivery, will only grow demand for India-centric delivery, not reduce it. True, the influx of new BPM staff hiring will (and already is) gradually decrease, but this is what happens when industries mature and growth slows to a more sedate pace. This is just basic economics. If the Indian-heritage service providers fail to embrace automation effectively, they will get hit hard by those as-a-service providers which are making RPA native to their delivery without even an afterthought.

Too many heads buried in the sand. Most of the Indian BPM industry seems to have talked itself in a comfort zone, that, quite frankly, doesn’t exist. We’ve seen many once-great service brands tank alarmingly quickly because they failed to get ahead of industry dynamics, opting to rest on their laurels. I hate to say it, but several of the Indian-heritage BPMs are falling worryingly into that trap. There needs to be a jolt somewhere to shift this mindset, or this industry could slip into insignificance very quickly. From my conversations, many folks just don’t seem worried about their firms’ inabilities to integrate services across P&Ls, or a clear lack of any direction. Many folks just seem to think that these disruptions will affect their successors at some distant point in the future, and do not really need to do much about addressing them today.

The Bottom-line: The Indian BPM industry is not doing itself justice and must wake up to smell the roses

I am not in the business of providing false hope – if I was, I’d probably go back to consulting. I truly believe India is very good at bringing together a wonderful story around analytics, process excellence and automation – where clients can receive great quality, low cost process solutions… delivered As-a-Service. But there really needs to be genuine focus on three things to achieve this:

Invest in smaller deals that have common process elements. Indian BPMs need to invest in effective as-a-service platforms by picking up an array of smaller client deals and building something robust that can scale and become profitable over time. As the mega deals continue to slow, this is the only way forward for most of the BPM providers. They need to pick the processes where they really want to play and make a concerted medium-term investment plan to create their As-a-Service platform for future growth. This may mean taking on 15-20 new clients on modest margins to build that platform, but that is the only way forward – build the solution first and stop customizing deals for clients that have little scalability or reliability.

Invest in proper marketing. The disease of commissioning cardboard white papers nobody reads; producing mimicked meaningless messaging than means nothing to anyone; hours spent with out-of -touch legacy analysts who impact nobody, has, let’s face it, reached news depth of affliction. We are in the process of boring ourselves out of existence, and – most worryingly – turning off clients. The whole BPM industry is crying out for a facelift and a fresh series of conversations that reflect reality, not fluff.

Move on from “BPM” as the brand, as effective BPM is now the table-stakes. While I commend the Nasscom folks for creating an alternative to the dreaded “BPO”, BPM is more of an interim term, in my opinion, to the eventual As-a-Service end-state. It just doesn’t mean a helluva lot, and in today’s market, effective business process management is par for the course – it’s the staple solution you buy. The real value today is in the services that can be delivered with the BPM to make them really effective.

We’ve been a having a great time helping the Nasscom team pull together this year’s BPM Summit agenda and speaker lineup. And how could you fail with the theme “The Emerging Digital Economy: Thrive, Survive or Die”?

So get over to Bangalore this Thursday and Friday where you can mingle with the HfS team, a whole plethora of service provider leaders, advisors and buyer executives, where we will attempt to unravel the mystery, hype, excitement and confusion surrounding the BPM industry. And you can find out just why this picture fits in with the HfS vision for the future of the workplace…

Find out what’s making Chandra, Vishal, Tiger and TK strut their stuff in Bangalore this week…

Accenture buying Cloud Sherpas unveils the value of As-a-Service talent

Accenture has added considerable strength to its already-strong position in Salesforce services with the addition of Cloud Sherpas for an undisclosed amount (press estimates have been $350-$400 Million) coming on the back of previous Salesforce services acquisitions of Tquila and ClientHouse GmbH. In addition, there are added capabilities in ServiceNow and Google, but the lion’s share of the Cloud Sherpas acquisition is in the Salesforce implementation domain, where we see the most medium-term growth opportunity for ambitious As-a-Service providers in the customer centricity solutions arena.

HfS views the success of this acquisition tied to Accenture’s capability to integrate its capabilities across operations, consulting and systems integration and to use the core training and certification methodologies of Cloud Sherpas to transform Accenture’s own ability to grow Salesforce consulting, implementation and management talent.

However, if it only focuses on the low-hanging fruit – the systems integration – Accenture will fail to reap the full benefits of the investment, hence it is critical how it integrates the Cloud Sherpas talent across the core Accenture divisions, especially Accenture Operations and consulting. Accenture also needs to follow the mantra that As-a-Service is ultimately about empowering the customer, not the consultant.

In short, we believe this move not only consolidates Accenture’s already-strong position in Salesforce services, but also keeps out competitors from muscling into the space at a critical time, namely Deloitte, Capgemini and IBM.

As-a-Service can provide tremendous growth at scale potential like legacy ERP did, but the skill requirements are different

SaaS platforms like Salesforce and Workday might not be like traditional ERP platforms, but the commonality is still one of scale and skill. The difference is simply the type of skill requirement needed. With traditional ERP, enterprises need constant teams of engineers to mold the platforms to the business needs of the enterprise, whereas, with SaaS, they need teams of process and technical professionals to mold the enterprise to the SaaS standards and processes and make them effective. This is why we’re seeing the global professional services giants eying teams of talented consultants and delivery staff who can do more than merely implement these popular platforms and respond to the customers’ demands to have a post go-live partner.

The capability onus shifts firmly from the back office to middle/front offices to unleash future value

Ultimately, the enterprise will need less IT programmers to develop out a SaaS platform, but will increasingly need process experts and transformational minds to help them make maximum benefit from the SaaS functionality. The onus is shifting from back office engineering skills to middle/front office data science, design thinking capabilitles.

The real battleground in As-a-Service is emerging within business functions where there is no ceiling for innovation. With a process like payroll, for example, most enterprises can purchase the services they need to get the job done and provide the data they need to make decisions – they know what good looks like and can get there relatively quickly with the right As-a-Service provider.

Where this ceiling for innovation is limitless, is in processes such as sales and marketing, where the technology platform is the enabler for ambitious firms constantly pivoting to keep ahead of their customer demand and market shifts. Other functions with a high innovation potential include finance, workforce management and supply chain, where enterprises have a constant need to act decisively on data, not simply collect it and store it somewhere. This is where ambitious As-a-Service providers can gain an edge in the market, by investing in talent that help clients really achieve ongoing business value from SaaS, as opposed to simply deploying armies of programmers to keep the lights on. This is why KPMG bought out Towers Watson’s Workday practice earlier this year – and Accenture has now added to its global SaaS delivery strengths with this significant investment of Cloud Sherpas.

As-a-Service has to be all about empowering the client, not the consultant

This is why leading As-a-Service providers are finding themselves in a rat-race to absorb talent that can not only deliver the bread-and-butter execution of process and technology implementation, but also help their clients post “go live” to work with them unto perpetuity to help them be effective and competitive in their industries. Simply put, the future growth in services is tied to many of the leading SaaS platforms that are being adopted aggressively by enterprises, such as Salesforce, Workday, ServiceNow, SAP Successfactors, NetSuite, and so on.

However, the critical factor the likes of Accenture, KPMG, Deloitte, IBM et al. need to understand is they have to do more than sell a COE of expensive consultants to slap in the platforms. Enterprises are investing in SaaS to free themselves up from the shackles of legacy technology and have operations that can keep pace with the needs of the front office: in other words, they need to be able to help their clients receive operations As-a-Service:

Click to Enlarge

Why Accenture/Cloud Sherpas is a strong fit in terms of talent empowerment and scale for managed Salesforce-based services

For Cloud Sherpas, we believed that having depth across the breadth of all the components of the Salesforce Customer Success Platform was a looming challenge as our recent discussions with clients have shown that they want that breadth but saw Cloud Sherpas as much more specialized in the Sales and Marketing Clouds than the other components. These clients were telling us that they were increasingly looking for support and coordination across the full Salesforce offering and that they expect their service providers to be able to bring them not just implementation, but also consulting and management skills to support their business needs.

They aren’t looking for single product implementation partners in 2015, as they may have in years past, but their needs are more comprehensive, so for Cloud Sherpas this meant that they would have to invest further in consulting depth, in addition to product implementation capabilities to meet this evolving demand as Salesforce revenue itself was up 24% in Q2 2016 YoY. The other challenge we had noted was that Cloud Sherpas was not as developed in providing ongoing managed services post implementation, both for application or business process delivery around Salesforce, than other leading service providers.

Simply put, Cloud Sherpas has grown its business to the ~$200 million level largely more through one-off implementations than in the provision of post go-live ongoing support. At HfS, we believe the firm was beginning to plateau at this level and needed access to global resources to grow the business to a broader level, both in terms of scale and geographic presence. Many Salesforce clients have indicated to us they want to shift more and more of the tasks around Salesforce management over to others to run and support the platform, and this would also have required a significant investment and shift in focus for Cloud Sherpas. In short, this is a good a time as any for Cloud Sherpas to make a strategic market move, and merging with Accenture is a very realistic and practical move for the firm.

Both of these challenges for Cloud Sherpas are also strengths for Accenture, with its breadth of Salesforce platform coverage and its extensive management services capabilities. However, the challenges for Accenture are different. Even with the largest pool of Salesforce-certified talent, Accenture was still resource constrained especially as clients (including many we spoke with) looking to broaden the depth of their Salesforce deployments and to transform their operations. Part of this challenge is simply being able to recruit and train staff with the right technical and business process skills to enable Salesforce to be not just operational, but a generally effective platform for clients seeking better access to customer data, more responsive marketing campaigns and enabling sales and marketing teams to approach business problems more creatively.

Accenture was especially short relative to its size in access to higher level certified architects and building a training environment for certifications that could keep pace with demand. Those as it turns out were both strengths of Cloud Sherpas who as a SaaS services start-up had built the specific Salesforce (as well as ServiceNow and Google environments) team development programs and processes that Accenture was lacking. Accenture had the scale and the global delivery network to support their clients but now needed the accelerants for growth to match client demand. HfS also believes that Accenture needed to also give greater internal visibility to Salesforce and other cloud platforms than had been the case because as big as these capabilities have grown they are still dwarfed internally by the team around SAP, Oracle and other solutions. Buying Cloud Sherpas therefore not only adds to the capabilities to grow the practice faster but also adds ~1,100 members to the team across Salesforce, Google and ServiceNow including roughly 600 in Salesforce services alone. Like when Accenture purchased Procurian for procurement services BPO back in 2013, HfS believes that the acquisition of Cloud Sherpas acts as an internal organization change agent within Accenture. The need to make the business case of the acquisition concentrates the organization on a shared goal and allows for the re-shaping of resource pools and organizational models that can’t be as easily undertaken just with organic growth. In the case of Salesforce Services, this organizational change is manifested in the decision to create the Cloud First Group to incorporate all of the focused SaaS design, implementation and delivery resources in one place and to further elevate its internal position to the client teams and the leadership of the Technology Growth Platform.

Therefore, when we look at two challenges that we had identified for each of Cloud Sherpas and Accenture around Salesforce services, we believe that barring any visibility into the actual financial structures of the deal, these challenges are well addressed by this coming together.

The Bottom-line: Competitor response is critical, otherwise Accenture will continue to lead the Salesforce As-a-Service market

We believe Accenture not only solidifies its position at the forefront of the market, but it also keeps out its competitors by tying up one the most attractive specialists in Salesforce delivery. Rather like its acquisition of Procurian in 2013 tied up the Procurement-as-a-Service market, Accenture is banking on Cloud Sherpas having a similar impact in Salesforce services: take a stranglehold position as the market is quickly maturing.

The big question, now, is whether Accenture’s core competitors in Salesforce services have the appetite – and depth of funds – to make a play for other specialist Salesforce providers such as Acumen, Appirio and Bluewolf. Deloitte is consistently avoiding being a managed services provider – preferring its role as consulting partner; KPMG is flirting with it, but seems more enamoured with building a service delivery world for large enterprises around Workday, while IBM sold off its CRM BPO services to Concentrix and needs to make a similar move to Accenture here, if it really wants to be more serious that an SI player in the space. HP could be a wildcard, with its strong CRM BPO business and Salesforce relationship, provided it can quickly get past its recent restructuring to make a strategic investment in this area. Capgemini is another contender here, with excellent technical implementation capability, but its BPO services are much more centered around finance and supply chain, that customer centricity.

HfS readers can click here to download a freemium copy of our new POV “Accenture buying Cloud Sherpas unveils the value of As-a-Service Talent” authored by Charles Sutherland and Phil Fersht

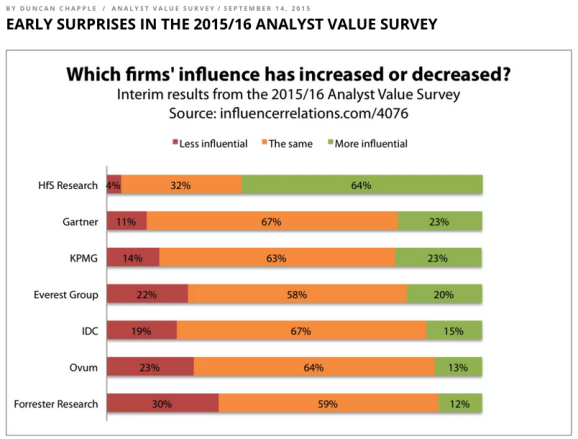

The main man who tracks the influencers, Duncan Chapple, gives us a little sneak preview into how this year’s Analyst Value Survey is chugging along, with several hundred research buyers already sharing their views:

Click to access article

If you haven’t yet had your chance to share your opinions of which analysts are doing (or not doing ) it for you, do spend a few minutes completing the 2015/16 Kea Company Analyst Value Survey by clicking here.

Duncan Chapple leads Kea Company’s Influencer Relations Practice (Click for Bio)

It seems the “freemium” model we’ve adopted at HfS over the last six years is really having an impact. It’s our view that top insights shouldn’t be stuffed behind a firewall. Clients will pay for premium data, indepth analyst strategy session and in-depth competitive landscape reports, but when it comes to insights, viewpoints, or just some plain old entertainment, why hide it?

Freemium isn’t disruptive, it’s the way forward for an analyst industry, much of which refuses to break out of its stale model. If people stop reading research and genuine insights, we might as well all pack up and go home now, so let’s promote what we do, not hide it.

Having a prolific analyst team beat the As-a-Service drum every day is the real reason for our continual impact – they keep the views fresh, varied and unvarnished, while maintaining that personal touch, which is what we’re all about at HfS.

Thanks for those who have voted for us (so far), we really appreciate your support and feedback. If you would like to share your views on what you would like to see more (or less) from us, do email us here.

India has massive potential to lead the world in process delivery centered on analytics and robotic process automation. This was, personally, my biggest reinforcement. India delivery is all about passion for processes, getting them executed and doing smart things to make them run better and throw off meaningful data. Most of the analytics and automation needs of today’s BPM deals are not rocket science – it’s making sure insurance claims, invoice generation, order management, credit and collections etc remove unnecessary manual steps, produce the outcomes clients want at lower cost of delivery. Most of the competent BPMs are now deploying bots in their centers alongside their staff, leveraging many of today’s off-the shelf tools, such as Automation Anywhere, Blue Prism and UiPath. And they’re pretty damn good at it.

India has massive potential to lead the world in process delivery centered on analytics and robotic process automation. This was, personally, my biggest reinforcement. India delivery is all about passion for processes, getting them executed and doing smart things to make them run better and throw off meaningful data. Most of the analytics and automation needs of today’s BPM deals are not rocket science – it’s making sure insurance claims, invoice generation, order management, credit and collections etc remove unnecessary manual steps, produce the outcomes clients want at lower cost of delivery. Most of the competent BPMs are now deploying bots in their centers alongside their staff, leveraging many of today’s off-the shelf tools, such as Automation Anywhere, Blue Prism and UiPath. And they’re pretty damn good at it.