Technology is useless without the H Factor to drive it and apply it to business scenarios

I woke up to an interesting piece by Everest’s Peter Bendor Samuel yesterday, where he describes how IT service providers have developed their delivery staff into, essentially, “human robots”. He goes onto say that, while providers have delivered real value serving up these “human robots” to their clients, their staff no longer wish to work in such a robotic fashion.

“With automation, we no longer need human robots. But then what do we do with these people?”… which is where Peter leaves the question hanging. And that was the biggest takeaway for me – not that operational jobs are gradually being automated away, but what are people going to do next, who didn’t actually want to be human robots in the first place? So let’s cut to the chase… technology is useless without smart humans (the “H Factor”) to apply its potential to real business scenarios

Tackling the H Factor: Today’s human workforce’s challenges in the face of automation

Today, we essentially fall into three categories of worker, with each one roughly a third of today’s workforce:

Millennials. Yes, that strange, fascinating species we all need to be extremely careful not to upset. Remember, we weren’t born with Snapchat and Instagram embedded into our DNA, and we have to be very cognizant of the fact they need Youtube playing on their machine at all times, while they try to reimagine our procure-to-pay processes. Remember, these kids weren’t introduced into the workplace needing to work for their money. They need to be wrapped in cotton wool and nurtured in an environment with plenty of open spaces, coffee bars, collaboration rooms, movable white boards, a 24×7 gym and a tattoo parlour. The challenge here, is that while Millennials are, on average, more loyal to their employers than their previous generation, how can they all be aligned with adding real business value in the real world? Do we really need as many Design Thinkers as we used to need coders and process managers?

Baby Boomers. Yes, that motley crew of crusty old farts just hanging on until they get pensioned off. Most want to call it a day, but have expensive lifestyle tastes and can’t afford to – I mean, have you gone to Whole Foods recently? For the Boomers, there is no point changing anything now, as retirement is only a few short years away and they’ve convinced their bosses of the imminent security meltdown, should they tinker with their career defining masterpieces getting their firm’s operations to this fine state of operational performance. I mean, who else can boast a gold watch, simply for showing up to work everyday for the last 30 years? The challenge here is how to retire this lot, so we can create career progression for the younger generations…

Moomers. The weird bunch stuck between Millennials and Boomers. They’re half-terrified they need to be effective using social media, and half-terrified they are going to get automated out of existence, as they aren’t “Digital” enough to break out of their humanesque-robotic existence. They’re trying hard to get to 100 Twitter followers and have got quite adept at posting little essays on LinkedIn, which they think hundreds of people read, when, in fact, noone really got past the headline, with a few sympathetic souls clicking the “like” icon. They really want to be seen as “Digital Transformers” and made sure they added “Digital” into their job titles (as if “being Digital” was what they aspired to be when they graduated from college). Little do we suspect they were also previously experts in eBusiness, Web Services, SOA, Cloud, Big Data, and so on… The challenge here, is most these lovely people don’t really have a lot of skills beyond marketing themselves as valuable people, as most the stuff they really do is tactical and highly automatable.

The Bottom-line: Without Social Intelligence, we’re entering an employment apocalypse, unprecedented in history

It’s been seven years since the last economic crash, many businesses are awash with cash, and the desire to make radical changes to drive out costs and automate work is pretty low. However, while the current motivation is low, the capability to outsource, automate and digitize is massive. One nasty economic nosedive and we’re facing a potential employment armageddon that has no precedence: millions of jobs will be eliminated, which never again need to be recreated.

And with China struggling to manage its own economy, all hell breaking loose in the Middle East, and this creeping, worrying risk of deflation, we need to be smart about how to prosper in this potentially dark new world, once our enterprises are forced to get much more active about negating their reliance on these increasingly-devaluing, increasingly automatable and digitizable jobs.

People, increasingly, want to work with people they like and people who spark positive energy, first and foremost, as technology continually makes jobs more sophisticated and intelligent. I don’t need an accountant who can tell me my revenues this month, as I have software that can do this for me easily… I need an accountant who can talk me through the nuances of sunsetting a legacy product and its impact on my profit line. I don’t need a lawyer who can create employment contracts – I can pull these off Legal Zoom… I need one who can talk through the nuances of creating incentive plans to motivate my staff. I don’t need a web developper who can integrate a few databases – most of these new websites come with them already native to the package… I need a developper who can help design the sexiest website ever to embarrass my competitors. I don’t need content people who just check the boxes to fill content space – you can get content produced anywhere these days (and even automated)… I need content people who want to exchange ideas on creating content that gets noticed and read by our clients. I don’t need marketing people just to send out email-push campaigns… I need ones who can help me figure out which conferences to go to, how to associate my brand with the right partners, how to use social media more intelligently, how to create communities among my clients etc. I don’t need someone to manage my insurance claims… I need someone who understands my business and can help me evaluate the ROI of new policies to protect me from unforeseen future scenarios.

I can go on through each profession and business function in turn, but the underlying premise is the same – I need intelligent people I can work with, whether in my company, or in a partner organization. And they don’t need to be rocket-scientist intelligent, just smart enough to understand by business and engage with me to figure out how to do things better. But the value is in the ongoing interaction and team-work, not a wooden worker/manager reporting line model.

So… while I don’t have the definitive answer to all these looming employment catastrophes, what I can do is challenge each of us to figure out the H Factor in all of this: technology is useless without smart humans to apply its potential to real business scenarios. We need to be those smart humans who can intelligently apply the tech, not the ones being replaced by it.

Yes, I know I promised to savage anyone who used the term “uberize” to describe a disruptive business model, but having spent a fascinating day at the ARForum in London last week, it really struck me that uberization is pretty much what HfS has done to the traditional IT analyst industry, when you look at the results of what ~1000 consumers of IT research are saying:

Click to read the full article over at Influencer Relations

While you can’t really do a direct apples-t0-apples comparison between the Uber and HfS business models, what we have in common is the fact we’ve both leveraged digital platforms to disrupt traditional, slow-moving industries – and with limited infrastructure and resources.

So why is HfS the “Uber” of the analyst industry?

1. We use digital technology, the web and social as our customer platform. At HfS, we do not need to hire armies of expensive, aggressive sales people to grow our customer base. We use our webplatform, a host of digital content and marketing apps, our blog and our social communities to bring the customers to us – at a fraction of the cost.

2. We don’t view “customers” as entities that have to give us money. Do Facebook, Twitter and LI fail to influence people because they are free? It’s the same with research – why does everyone have to pay money to be considered “influenced”. We get over a million visits to our stuff every year, well over 100,000 subscribers to our blogs and research and 15-20k pieces of research being downloaded each month. These are our customers. We just don’t believe in making everyone pay-to-play – we are of a size where we are proud to share what we do without slapping a huge paywall in front of the world. That’s why we are already the #3 firm in the industry in terms of reach and influence, after only 6 years in existence.

3. Freemium research, that is compelling and easy to access, is what gets read today. Most people tend to read only research when it’s slapped in front of them, that is digestible and compelling. Trying to navigate your way behind an expensively assembled firewall and search engine pretty much loses most people before they even think about trying to reset their password. I recall when I was last working for a “legacy” analyst firm that we were lucky to get more than 15 people downloading a report. Today we have in excess of 20,000 reading them. The difference is, simply, off the scale.

4. The revenue model is different from the incumbents. We don’t believe most people really want to pay for libraries of reports any more. They will, however, pay for benchmark and pricing data, competitive analyses and access to awesome analysts, who are fun to talk with and easy to get hold of. We also mix access to our massive global community (both physical and electronic) with the research access. Our buyer clients can come to our industry-leading quarterly summits, while vendor clients can have sponsorship privileges. We believe peer networking and sharing the dynamics of thousands of the global community as a critical part of the Research 2.0 process.

Talking about analyst disruption last week, at the 2015 ARForum

5. The customer experience is just so much better. I love the fact that, with Uber, both the drivers and customers get to rate each other. It’s a bit like that with HfS – we love our clients and we want them to love us. We do not put in 1-800 numbers to set up faceless analyst discussions, and we certainly do not stick analysts on competing postage-stamp P&Ls where they cover extremely narrow areas. In fact, talk to HfS and you’ll likely get a meeting with 4-5 of our analysts within a few days as so many areas are overlapping, if you really need to talk to us urgently. We also make time to hang out with our clients, at our office or theirs. We do this because we enjoy it, not because we just want to get through the ol’ 9-5 treadmill. It’s like getting into an Uber, where the driver is genuinely grateful to be of service, as opposed to some self-entitled miserable worker who’s just going through the motions.

6. The incumbents can’t/won’t cannibalize their revenues. No-one likes having to drop their prices, while improving their services and customer experience at the same time. It costs money and upsets investors with short-term mindsets. There is also an arrogance when your firm has been printing money for years, and suddenly you have to work for it again. Entitled people just do not want to work harder/smarter and with a better attitude. It’s the same for many of these overpriced creaking old taxis that smell like a dog died in the trunk – they simply have lost the ability and appetite to up their game.

The Bottom-line: It’s all about being non-traditional, using digital tech and creating a workable revenue model

Hopefully, after reading this, people will start to use the term “HfS-ize” instead of uberize =)

But, seriously, surviving in a market that refuses to change, such as the traditional IT analyst industry, is all about leveraging digital tech and the web to have a much, much more competitive model in terms of cost, reach and customer accessibility. However, you can use all the cool tech in the world, but it’s useless without the human factor to drive it and make the magic work. That’s where having a team of motivated, passionate – and genuinely nice people, makes this business successful.

While technology and a great business model is what makes the thing function, it’s really the people, the socially intelligent attitude and culture which make up our secret sauce.

Mike Small is the Global Sales Officer, BPO at Capgemini

People in the BPO world have noticed that Capgemini has really started to win business in the US over the last couple of years – no longer is the firm seen as largely a European/International player, but a global player with a strong US footprint.

One of the key reasons for this has been the introduction of Mike Small, initially to lead US BPO development efforts, before his elevation to global BPO sales leader after his success helping bring in major new clients such as NBC, Office Depot, UBM and Ferro.

Despite being very tall, very charming and very articulate (come see Mike at our Harvard event this December), Mike is also a complex-deal addict – he loves grinding out the really large, intricate engagements, when he’s not out playing golf or running off his business dinners. So it’s high time we made a major introduction to the HfS community to Mike Small…

Phil Fersht, CEO, HfS Research: Good morning Mike, it’s great to have you join us today… please give us some of your background and how you got to the role you’re in today.

Mike Small, Global Sales Officer, BPO at Capgemini: Great Phil, and good morning to you. I’ve been with Capgemini now for over a year and a half. As far as my current role and responsibilities, I head up global sales and marketing including go to market operations for Capgemini’s Business Process Outsourcing business. The best part of my job is working with clients in multiple industries and helping them address their business challenges mostly around finance and accounting as well as supply chain. Capgemini BPO is a leader in both of these disciplines from a marketplace standpoint. So that is my current job. Prior to that I was working at a major technology firm, again focused on business process outsourcing mainly in the North American market. Specifically with a domain focus in both healthcare and financial services, and again running sales and marketing.

When I first started in the industry about 18 plus years ago; I was focused on finance from a controllership and audit perspective and then quickly moved into another multi-national outsourcing firm. Since then, I’ve pretty much been with outsourcing firms, both ITO and BPO as well as applications with experience in solutions and service delivery. Over the past five years I’ve taken what was an IT/ application outsourcing background and really focus on end-to-end business processes. So that’s my passion. Helping clients with shared services strategies, global business services adoption, integration of hybrid models, and full outsourcing of business processes

Phil: What attracted you to join Capgemini? Surely the world was your oyster =)

Mike: Capgemini is a leader in the BPO space and well recognized by analysts like yourself as well as others globally. So that was one initial draw. As I started to explore the corporation, I looked at the cultural fit. Like any career decision a lot of it comes down to feel. So did I feel that I could bring my talent to this organization? Did I feel that this is the right fit? Both of these dimensions for me, personally, were an overwhelming yes. Plus, this is an organization which is extremely entrepreneurial.

When I speak to many of my colleagues that have been around the firm longer than I have, Phil, what keeps them focused and happy is that desire to be entrepreneurial and express our values of freedom in the marketplace, and that’s quite unique to our culture.

Phil: You spend an awful lot of time talking to clients, Mike, and one of the hot topics that we’ve been talking about is the level of hype in the industry today. Do you think there is too much hype in general right now?

Mike: Our market, Phil, is becoming more mature and when you have crowding at a supplier level, what tends to happen is a fierce competitive focus around trying to differentiate. What I have seen to your point is a little bit of hype around robotics process automation as the next wave of business process outsourcing. We’ve obviously embraced the technologies that have emerged and adopted them both for helping our clients and improving our own global operations. We have been delivering robotic process automation for many years and we currently have over three thousand software robots currently in operation.

We use our Global Enterprise Model in the adoption of all technology like robotic process automation and see it as another lever to be pulled in a framework that provides a holistic view of addressing global business processes.

Do I see some hype in the marketplace? The answer is yes. I attribute that to a very crowded field, where many suppliers are trying to push a differentiated value proposition. I think it’s on all of the various members of the ecosystem to continue to test those propositions, so that they are based in reality. We’re not putting any operations at risk. I’d like the adviser and the analyst communities to really dig deep and come back with a re-setting of the market on what’s attainable and what the focus should be strategically. I also think the service providers should really take a step back, and ensure that as we look at going to market and differentiating, that we really are focused on delivering the outcomes. That we commit to it commercially and keep it routed in fact.

Phil: So let’s talk a bit about BPO and where that’s going, Mike. Where do you see real growth coming from as we look maybe three or five years out? Is it in the traditional businesses like F&A and Procurement? Or do you think there are new areas beginning to open up in the market as things mature?

Mike: One area, which coincidentally we have just launched a new offering, is around digital supply chain. Obviously we’re seeing solid growth in our traditional F&A and Procurement business, but supply chain is where we see market demand, specifically in the consumer products, retail and manufacturing industries. For us, when we look at that as a capability and a market opportunity, it’s driven by a couple of drivers that are traditional challenges with clients associated with looking at their supply chain. There is tremendous amount of volatility and customer demands are changing. And there’s also a lack of visibility and companies need a better way to aggregate time sensitive information so they can actually make decisions properly and at a timely manner. We need to get this right to help our clients drive customer loyalty and profitability.

We’ve spoken in past around the proposition around speed to value, and the need for supply chain management and operations to create value with speed. This is where we’re seeing a tremendous opportunity with some of the assets that come to bear within our portfolio. With BPO as well as Capgemini’s consulting, application, and infrastructure capabilities, we can enable a digital supply chain with a lens to in-depth knowledge for consumer product and retail, as well as manufacturing organizations. So that’s an opportunity that’s emerging where we’re seeing tremendous growth. We absolutely take that as the next big opportunity for growth, as we look at the next two to three years. As well as obviously the continuing focus around our traditional business that continues to grow.

Phil: So to finish up, Mike, I’d love to ask you one question about doing something to change this industry. So if you are anointed Emperor of BPO for one week, what’s the one thing you’d do to impact the industry?

Mike: If there is one thing, I would say accelerating the rate at which BPO as a stack services are integrated. If you look at some of the challenges that we see within our client set it’s; how do we integrate? How do we from a value standpoint gain greater insights? How can we be more flexible to adapt to multiple challenges within the environment? How do we overcome barriers to success such as silo-based organizations? How do we extract value rapidly? Because it is very much a changing dynamic.

It’s about extracting and integrating that thinking into strategies to implement into the operations and then delivering it seamlessly across processes and technologies. That’s the one area that is often the biggest barrier for clients – that thinking of the end-to-end integrated view, and how to approach that to address their challenges. So if I were BPO Emperor I would drive that thinking around seamless integration of process and technology in both the client domain as well as the supplier community as I really believe it would deliver an enormous amount of value for the market and for BPO.

Phil: Great answer; did a good job there, Mike! Thanks again for your time with us today.

Why aren’t you prepared to share more risks with your clients, Mr Provider?

If I have to hear another advisor, lawyer or provider sales executive whining about their lack of business, I am just going to tell them straight – “You’re a dinosaur, you are selling a capability from a bygone era. The reason clients don’t call you anymore is because you are not offering them what they really need – or at least educating them on what they need to haul their legacy back ends out of the dark ages.”

The narrative simply has to change. Today’s enterprise world is littered with literally hundreds of legacy outsourcing relationships where the service providers are unwilling (and many just plain incapable) of making any genuine productivity improvements.

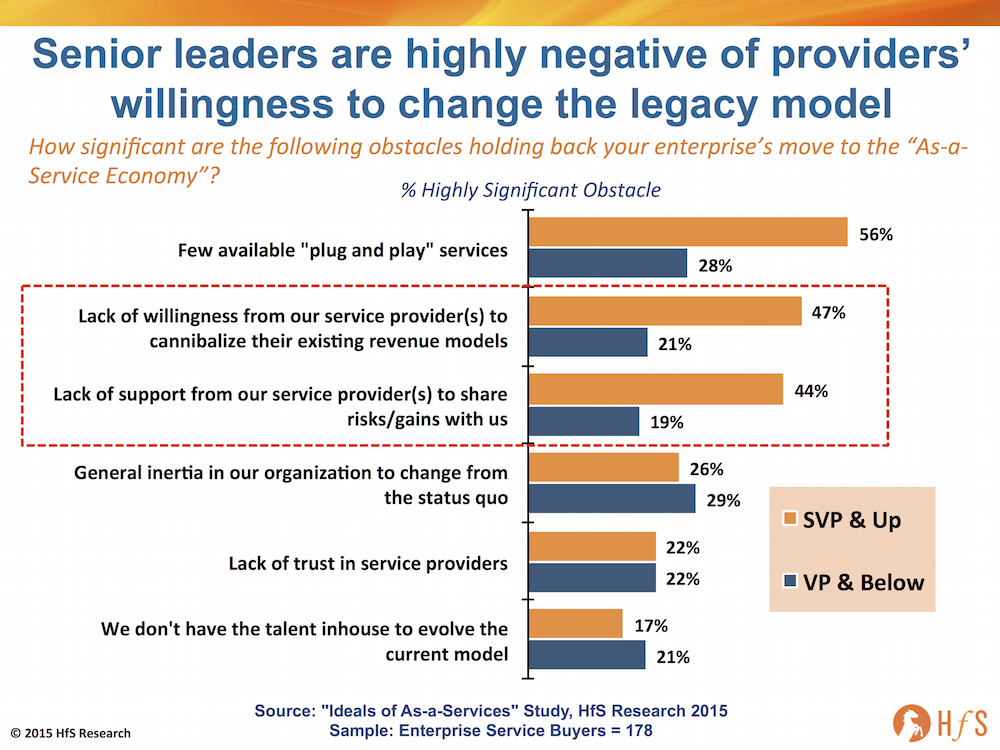

What’s more, the leadership in their clients is quickly wisening up to what’s going on and simply does not trust them to invest in their delivery capability, or share risks with them to find new thresholds of value. Close to half (47%) the enterprise leadership we spoke to in our recent As-a-Service study view their service provider’s unwillingness to cannibalize their existing revenue model as a highly significant obstacle to make the As-a-Service shift, and a similar number (44%) view their provider’s lack of support to share any risk as a key issue:

Click to Enlarge

The outsourcing industry is stuck in a legacy holding pattern and is in real danger of decline

The problem we have, today, is that the leadership within many enterprise “buyer” clients is under huge pressure to take their operations to the next level, but most of their middle and lower management clearly only care about keeping the current status quo. In a nutshell, our industry is suffering from hundreds of stagnating outsourcing relationships, where the service provider has zero incentive to do anything much beyond keeping the margins consistent, while the middle management on the buy side has a similarly lethargic ambition not to do anything much… bar keeping the lights on.

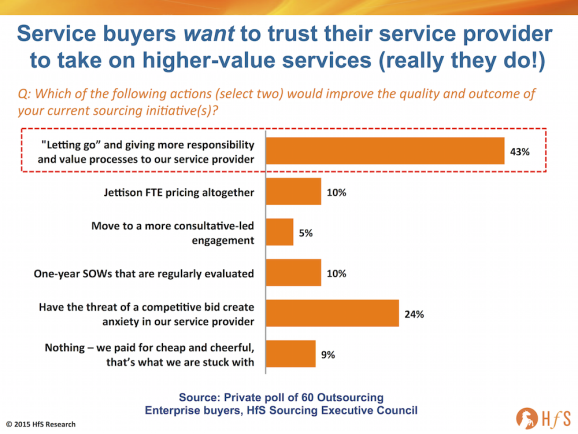

However, when we anonymously polled 60 outsourcing services buyers in a private focus group last year, 43% said that giving more responsibility to their service provider would be the most important factor to improve the quality and outcomes of their outsourcing initiatives. Clearly we have reached a paradoxical situation:

Click to Enlarge

The Bottom-line: Here’s the great modern-day outsourcing paradox – many enterprises want to give up more to their service providers, but many of the providers are just not interested in investing in As-a-Service capabilities

The reality today is that senior buyer executives want to progress the operating model towards As-a-Service, while their counterpart service provider leaders are talking a big game about delivering Digital and As-a-Service capabilities to their clients, which can spread the wealth generated by better automation, actionable analytics and a multi-tenant model. Hmmm… reminds me a bit of outsourcing 1.0, where the leaderships in many enterprises dove into outsourcing fuelled primarily by lower cost labor, forcing the situation on their underlings. Now a similar pattern in emerging, with the difference being the “tangible” productivity factor is automation, while access to better, more actionable data to make business decisions the ultimate desired outcome.

The challenge today, quite simply, is less of an appetite from the sell side to absorb the risk. Making savings through automation is a lot more “risky” for many providers than the ease of swapping out bodies. However, taking these risks, and investing in the talent and technology to de-risk these situations, is what is key to survival.

Most service providers, while talking a big game, are not convincing their clients they are really prepared to share risk and make genuine investments to build out a true multi-tenant As-a-Service delivery capability. That’s probably because they only really care about making their quarterly numbers, not having a sustainable, well-planned long-term strategy.

This situation spells a near-certain recipe for failure for the outsourcing industry, where the decision-making layers claim they want to shift the gears, but the existing relationships are clearly stuck in a depressing holding pattern. In fact, from many client discussions we are having today, execution from certain providers (you know who you are) is deteriorating further, as they simply cannot say no to the increasingly complex needs of their clients, but are too stingy (or should I say cannibalistic) to invest in better talent and capabilities to up their game. It’s a situation that is going to end in outsourcing failure for many, if steps are not taken to arrest this decline in delivery quality, and investments made in future capability – most notably robotic process automation, real time analytics solutions and a roadmap for self-learning and artificial intelligence.

Those providers with these capabilities can break this cycle by building multi-tenant solutions for the future – and will be the winners. I believe this could happen in barely a couple of years, when you look at the current pace of change and mood in the market. The key is to pick off the next 15-20 deals they can win at lower margins in order to invest in common automation, common analytics, common SaaS underpinnings and common service skills – hence a more competitive, more scalable multi-tenant As-a-Service delivery model.

It’s easy to point fingers at certain service providers for preserving the legacy FTE labor model, but the stark reality is that many of them simply don’t have leadership prepared to invest in the depth of talent, or technology capability to drive genuine advancements. So – let’s face facts here – we’re at an impasse. There are tremendous opportunities to create genuine productivity advancements through robotic process automation, smarter analytics and the onset of cognitive computing, but much of the present service provider bunch are not going to be the ones to take true advantage of them. I predict a few will break out, but the next winners will be from a new breed of As-a-Service provider, many of whom many not even have been formed yet.

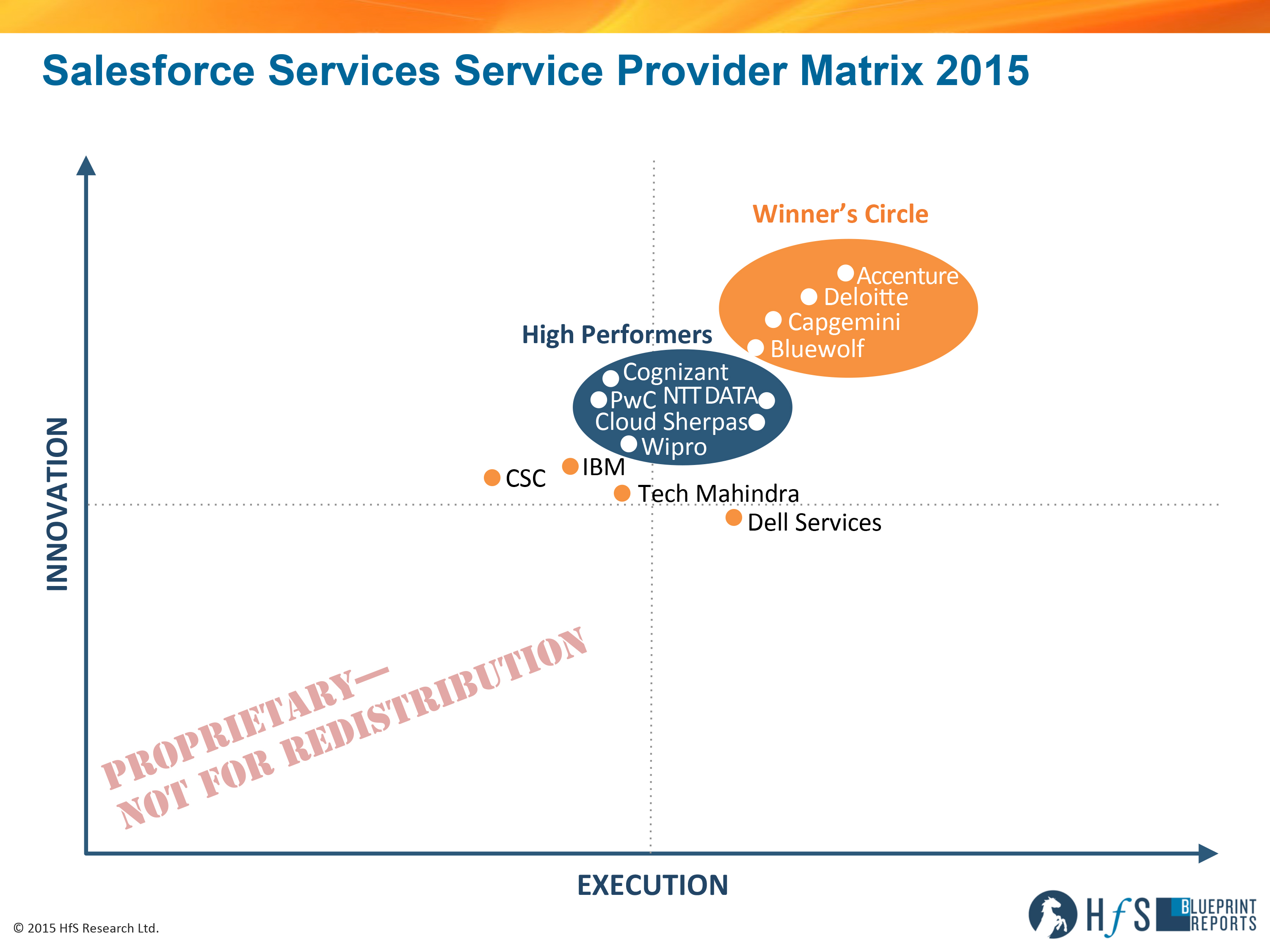

Salesforce dot com. Remember that upstart little CRM online platform that created affordable, intelligent customer management capabilities that defied the evil on-premise model?

Well, it’s now a multi-billion dollar service market that commands ERP-level rates, demands expertise that are in very scarce supply… and has driven a whole ecosystem of services upstarts and established providers all seeking to master the art of delivering salesforce-as-a-service. So without further ado, let’s hear from Blueprint report authors Khalda de Souza and Charles Sutherland on this escalating As-a-Service market:

Click to enlarge.

Khalda.. why have we undertaken an HfS Blueprint on the Salesforce Services market at this juncture?

Well, we saw the Salesforce services market as being analogous to a “petri dish” where many of the innovations of the “As-a-Service Economy” are visible. As a result, we wanted to use our Blueprint methodology to assess how service providers were responding to all of these innovations up close and in a structured manner. Every enterprise and service provider is making the commitment to Write Off Legacy in some way by moving to Salesforce to begin with and with that they are looking for Plug and Play Digital Business Services that deliver Actionable & Predictive Data on their operations. Responding to these Ideals alone is leading service providers to innovate and invest in better execution of as-a-service capabilities yet these service providers are also experimenting wit how to bring Design Thinking into solution delivery, creating a regime of Collaborative Engagement and working together with clients to become Brokers of Capability. It’s a fascinating market today that is helping to shape the new way of delivering IT and business processes especially given the enthusiasm of all parties in this market that is on display not just at Dreamforce each year but in the way that all parties talk about what they are doing with Salesforce on an on-going basis. As a result, there was no way HfS wasn’t going to be covering this market with a Blueprint in 2015 and beyond.

How does HfS define the Salesforce Services market?

We believe that there are 5 components to the Salesforce Services Value Chain today as delivered by service providers to create value for enterprises: Plan, Implement, Manage, Operate and Optimize. Plan includes consulting services such as: Salesforce business case development, compliance, security and governance services, as well as CRM strategy and Salesforce specific process and design services. Implement covers all the services and skills required for effective deployment, including but not limited to: project management, testing, training and data migration services. Manage includes: all ongoing integration and support services. Operate includes: business processing outsourcing (BPO) services where they are delivered by the service provider around the enterprise’s Salesforce environment from sales and service to marketing and more. Finally, Optimize services are intended to improve the impact of Salesforce solutions and may include: the assessment of new Salesforce platforms, on-going CRM strategy alignment, best practice content curation.

So, which service providers seem to be thriving best in the “petri dish” of Salesforce Services today?

Using our HfS Blueprint methodology with its crowd-sourced metrics for Execution and Innovation assessment criteria we found 4 Service Providers who belong in our Winner’s Circle for Salesforce Services today. The Winner’s Circle providers were: Accenture, Bluewolf, Capgemini and Deloitte. Some of the reasons these service providers came out on top included the way that account management teams guided clients into the “As-a-Service” world, the breadth of reach in capabilities in Planning, Implementation, Management and Optimization, the vision each provided around maximizing Salesforce effectiveness, the management of solution partners and the investments in tools, accelerators and industry solutions.

We further identified 5 additional service provides that are HfS High Performers including: NTT DATA, Cloud Sherpas, PwC, Cognizant and Wipro.

What are the major trends we see which will impact these service providers over the next several years?

Khalda de Souza, Principal Analyst and report co-author (click for bio)

The biggest trend we see impacting service providers going forward is the ever-increasing reach across processes of the Salesforce offering. Enterprise clients are expecting service providers to be able to support across Sales, Service, Marketing, Analytics and now the world of IoT as well through Salesforce solutions. This means that service providers need to be investing in the recruiting (and retention) of Salesforce certified staff and then their on-going training across the offering set. The leading service providers will continue to invest in differentiating skills and solutions to meet the growing client demand for business focused Salesforce deployment and support services.

The next major trend we see is the increasing opportunities to offer value added services across the Salesforce service value chain, with the most obvious being in the Implement phase. Here service providers have opportunities to create differentiators by developing proprietary tools and technologies that facilitate faster and more effective implementations. Notably these would include automation technologies, and the leading offerings would have industry specific focus to deliver relevant business benefits to clients. The ultimate aim should be to achieve the coveted Salesforce Fullforce industry solution certification, a stamp that is clearly presented on the service provider’s profile on the Salesforce Appexchange web site for potential clients to see.

The third major trend of note is the continued push towards the realization of the 8 Ideals of the As-a-Service Economy in this Salesforce environment. In particular, HfS expects to see service providers invest in Design Thinking skills to maximize the benefits of new Salesforce environments and for investments by Salesforce themselves, third parties and the service providers in capabilities to drive through greater levels of Intelligent Automation in Salesforce solutions as well.

What recommendations do you have for enterprise buyers who want to get the best out of their Salesforce service providers today?

HfS believes that enterprises that want to make the most out of investments in Salesforce services going forward should:

Use the Salesforce Success Community for information and to collaborate with experts.

Use the Salesforce Appexchange web site to browse the latest solutions and consultant partners. There are top level profiles of the latter to facilitate provider selection short lists but beware that the statistics presented are not always up-to-date.

Use the HfS Salesforce services value chain to identify which skills you have in-house and for which you require assistance from an external service provider.

Push the service providers to go beyond the RFI and prove real differentiation, and demand access to other clients before selecting the service provider and during the engagement to compare best practice and experience.

And finally, what recommendations do we have for service providers through 2015 and 2016?

HfS believes that service providers that want to have the greatest impact on enterprise clients and lead the Salesforce services market should:

Invest in functional understanding and adopt a holistic approach to CRM. Leading service providers position CRM and Salesforce in particular at the heart of clients’ digital transformation journeys, rather than view it as discrete, tactical technology implementation projects.

Invest in industry sector solution development. Visionary service providers that continue to invest in industry specific solutions and strive for Fullforce industry certifications have opportunities to establish a leadership position in selected markets.

Identify valuable partnerships. Leading service providers are able to identify valuable partnerships, including equity investments that will enhance and tailor Salesforce solutions.

Be bold and stand out. Service providers should think out of the box, present innovative approaches and ideas to stand out from the crowded partner ecosystem.

Tell the market what you’re doing! Too many of the service providers in this Blueprint are coy about their Salesforce services capabilities. This market is going to get more complex and demanding going forward especially as small service providers with unique skills will continue to be prime acquisition candidates for the major service providers. Therefore, Salesforce service providers need to market their strengths to Salesforce so that it can recommend the relevant providers to enterprises, as well as to potential clients themselves. Moreover service providers need to ensure that their profile on the Appexchange web site is up-to-date and reflects the latest statistics and capabilities.

Who else can put on an event and oversubscribe it before even releasing the bloody agenda? Didn’t people realize the central theme this year is invoice processing transformation in Kazakhstan?

Well, the long wait is over and we’re proud to present a slightly eccentric and highly knowledgeable line up of industry luminaries for our upcoming HfS Working Summit for Service Buyers, in Harvard Square, Cambridge, MA, December 1 – 2:

Here’s a mere sprinkling of the luminaries joining us for the December summit:

Sitting on the panel: Ian Maher, Hanover Insurance Group; Bill Pappas, State Street Global Services; Jason Barkham, Warner Brothers Entertainment.

10:45 am Break

11:00 am Breakout Working Sessions: Applying Design Thinking to Achieving Service Outcomes

Buyers and providers break out into the Aggasiz, Comstock, Compton and Kennedy rooms, hosted by Phil Fersht; Charles Sutherland; John Haworth, Chairman of the HfS Sourcing Executive Council; and Barbra McGann, HfS EVP, Business Operations Research.

Panelists: Gajen Kandiah, Executive Vice-President Business Process Services and Digital Works, Cognizant; Rohit Kapoor, Vice Chairman and CEO, EXL; TK Kurien, CEO & Member of the Board, Wipro; Debbie Polishook, Group Operating Officer, Accenture Operations; Mihir Shukla, CEO and Co-founder, Automation Anywhere; Tiger Tyagarajan, President and CEO, Genpact.

3:00 pm Break

3:15 pm Panel: The Future of Work

Hosted by Gary Cormier, Head of HR Consultancy, Harvard Faculty of Arts and Sciences.

4:15 pm Fireside Chat: Concluding Thoughts on the Summit

Phil Fersht and John Haworth talk with Mark Hodges, Founder and CEO, Acresis, LLC, about his observations and reflections on the HfS Working Summit discussions.

4:45 pm Closing Remarks

5:00 pm Summit Adjourns

6:30 pm Farewell Reception and Dinner Reception at the nearby HfS offices, followed by dinner at the neighboring Gran Gusto Restaurant. Transportation will be provided.

Anyone who knows me well has seen how hard we’ve been pressing the importance of security and trust in a global services delivery environment, since we founded HfS.

In short, we’re moving into a world where reactive fixes to security breaches is a sure-fire recipe for disaster. Savvy enterprises simply have to deploy proactive, holistic management practices of their data flows across systems, people and processes. What’s more, with all these new investments going into digital technology, SaaS platforms, global outsourcing initiatives and automation bots, the risks out there with our data flying all around the place – and the trust in people needed to manage these risks – is second to none.

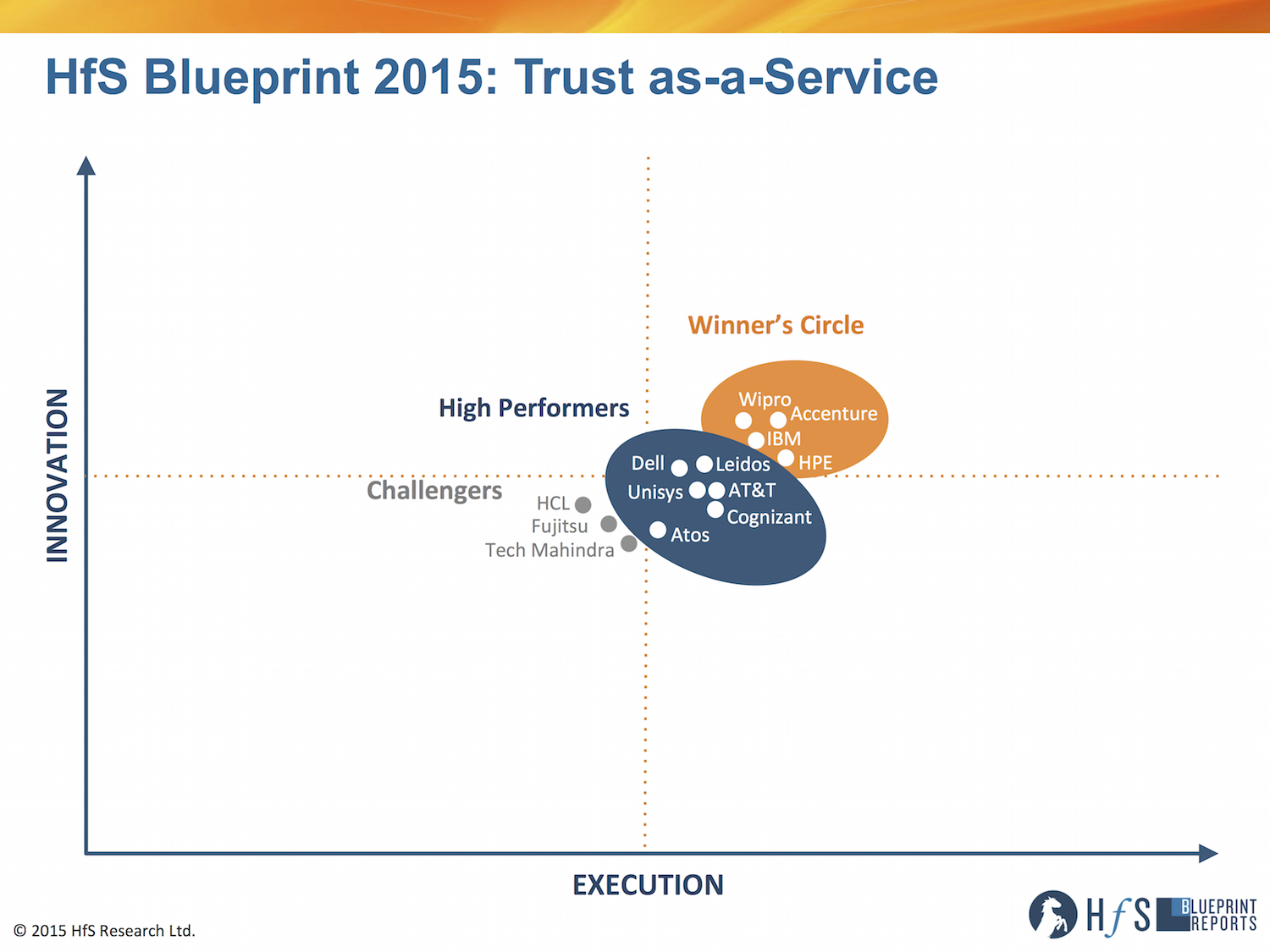

So who better than an analyst legend of the networking and computing boom era, the founder of analyst firm Current Analysis himself, and now a year-long member of the HfS team, Fred McClimans, to have a serious deep dive into what we are calling… Trust-as-a-Service:

Click to Enlarge

So Fred, why a Blueprint on security, or perhaps the better question, why trust as a Blueprint topic?

The transformation from an analog to a digital economy has been profound, giving rise to a whole new wave of business and economic models that place the consumer first and corporate assets online. This is a huge shift from the legacy models where brands controlled the message, consumers ate what was available, and managing risk meant not much more than a solid business plan, a line of credit, and Master locks on the front and back doors. That game ended a long time ago.

With most, if not all, corporate data now available online, and a massive consumer-driven omnichannel engagement model, we’ve literally given competitors and “evil-doers” a map of where to find corporate treasure, while replacing those locked doors with free keys that we hand out to every customer. While the legacy threat had to get close to inflict damage, the threat today can manifest itself from anywhere.

We’ve also seen a huge shift in the value that brands deliver to their consumers. It used to be all about the product, but now it’s increasingly about the experience – an experience that is inherently digital, less personal, and perhaps a bit more fragile. No matter how you look at it, enterprises today face risk both to their internal assets as well as to their greatest asset, their customers. Hacks and data theft – especially personal consumer data – ruin that customer experience, and decrease the level of trust. If your online or digital brand isn’t trusted by the consumer, they’ll easily go elsewhere. So, as we looked at the market for managed security services, it became clear pretty early on that it wasn’t just security, or cybersecurity, that mattered, but the trust it enabled between a brand and its customers, partners, and even employees. That realization shifted how we approached the security market. Security isn’t about securing assets, it’s about creating trusted assets that can be leveraged in the market, hence Trust-as-a-Service for our Blueprint theme.

That’s quite a shift from the traditional approach of measuring security in terms of firewalls, identity and access management, and malware detection. What was the approach you took to measure the ability to provide trust as a service? And can you share some of the key takeaways from your research?

Fred McClimans is Managing Director for Security Research, HfS (Click for Bio)

Well, first off, this Blueprint definitely takes all the traditional security elements into account – what we refer to as the technology side of security. Security Event and Information Management (SIEM), Data Loss Prevention (DLP), Identity Access Management (IAM), app and device security are just as important today as they were a year ago, perhaps even more important as the sophistication of cyberthreats has increased. But the real area where we are seeing new value in security is in behavior, and not just user behavior, but enterprise behavior.

An increasing number of security breaches can be directly tied to enterprise behavior and processes that haven’t kept up with the growing threat. We see insider threats all the time, even though most security is directed outward. And increasingly, data isn’t just being stolen from within the enterprise, but from enterprise partners and consumers. So there’s real need to start looking at some of the business structures and processes, the deals we make, and the types of information and access we’re willing to share, that often lead to increased risk that even the best technology is unable to protect from the right prying eyes.

T-mobile had a significant (hack recently that came through one of their partners, Experian. And Sony’s infamous hack last year, that was linked to North Korea and the film “The Interview”, revealed that over 100 internal Sony system were simply unmonitored. Both of these hacks can be tied to behavior and process.

So what did we do? We started with the main technical criteria and then layered on top the ability of providers to take their customers to the next level of blended physical/digital and process/behavior maturity, which you’ll see referenced in the Blueprint as the HfS Digital Trust Framework (see Can Today’s Providers Deliver the Elements of Digital Trust?) and the Digital Security Maturity Model (see Transforming the Security Maturity Model).

What separates the winners in security apart from the others? Is there a particular technology or focus that gives them the edge in helping enterprises counter the cybersecurity threat?

Now you’re really getting into it. I think the best way to put it is to start with the technology. Every provider we looked at had solid technical chops. In fact, there’s a pretty good overlap with some of the partnerships that operate behind the scenes. And while each provider has a bit of their own special sauce in the mix, technically they all show very well.

Moving up the maturity stack, what tended to set the providers apart was vision, and execution, for how enterprise security and trust enablement would materialize moving forward. Accenture and Wipro, two examples from our Winner’s Circle (along with HPE and IBM), had existing services and processes that really closely aligned with our models for Trust. Leidos and Unisys, two of our High Performers (along with Cognizant, Dell, AT&T and Atos), similarly showed a good understanding of the need to move beyond security as technology and start thinking of it as a larger enabler of corporate risk management. At the end of the day, vision, innovation, and the ability to help their clients mature digitally were all key elements of success.

You mentioned a shift from security as a way to protect assets towards security as a way to build and leverage trusted assets. Does that have a bearing on the way enterprises approach outcomes? And what recommendations do you have for them on this journey?

Phil, that mindset shift is going to play a huge part in the success, or failure, of enterprises moving forward. Security can’t afford to be an afterthought; it really needs to be thought of as a transformational enabler of a better, more trusted, business. The key recommendations? Let’s start with the basics. If enterprises aren’t aligning themselves with the Digital Trust Framework and the Security Maturity Model, they’re already behind the game. By doing this, they’ll be a bit more prepared for taking the steps needed to elevate their game.

Some specific recommendations would include elevating the responsibility for overall corporate risk and security management as close to the CEO and Board as possible; expanding their security architecture to include coordination, if not oversight, of their ecosystem partners; and a shift from a “prevent all breaches” to a “minimize breaches and control risk” approach. We’re also recommending some actions in the areas of provider relationships, in particular related to contractual flexibility, a greater level of actionable innovation, and a closer review of international privacy policies, something that delves into the role of security with regard to personal privacy and data rights.

And of course technology – automation is going to play an increasingly significant role in identifying and countering security breaches.

How about the providers? What recommendations do you have for them, and how will they need to transform themselves moving forward, or even can they?

I think transformation is going to be a challenge for some of the providers out there today. Those that are leading with tech may find themselves defining their own outcomes, and miss the opportunity to shift from service providers to service, and value, enablers. I can easily see a bifurcation of the market into two groups: one that is focused on delivering value by leveraging security as a way to create trust (as their clients go through their own digital transformation), and one that remains very tech-focused and becomes more of a modular, or on-demand, type of provider. There’s room for both, by the way.

But more directly, providers definitely need to think about security maturity in a fundamentally different fashion, which means they’ve got a lot of education to do with their clients who, based on our research, are still often thinking of security from a tech-only perspective. They also need to target the C-suite aggressively, as many of the security-related improvements and initiatives that need to be discussed go beyond the scope of a CISO.

There’s also an emerging physical/digital approach to security that winning providers will, and are starting to, adopt. Biometrics, access control systems, these are all physical systems that help provide a trusted environment, but today they’re separate from the digital security grid, unless they’ve been included as IoT devices. But the future of security services will require providers to start to leverage these devices to provide both contextual awareness of threats and help seal off threat venues.

We’re also recommending providers take a much more aggressive stance regarding corporate processes and behavior, especially from a larger risk mitigation perspective, that more emphasis be placed on aligning security services with specific business unit objectives, and that user education be significantly strengthened, to the point of bringing users in as collaborate security partners to help build a more trusted digital ecosystem.

And again, on the tech side, we’re pushing for a greater level of modularity and adaptability to keep pace with the rapid evolution of malware, spear-phishing, and embedded code hacks. This is not an easy market to be in, and they’ve got their work cut out for them.

What can we expect out of the industry in the coming year or so – it sounds like the threats show no sign of abating any time soon?

Let’s face it, the security market may never achieve a stable, or inherently safe, status. One of the constants throughout the past decade – really since the inception of digital technology – is that the level of threat always seems to meet or beat the level of protection.

Enterprises are constrained by time, technology, and budget. Hackers, especially those that are organized or sponsored, live by a different set of rules. There’s somewhat of an asymmetrical challenge at play. If you want to keep an asset 100% safe, you have to win every battle 100% of the time. But if you want to steal something, you only have to win once.

This imbalance is likely to become more pronounced as hackers find, and exploit, an increasing number of zero day vulnerabilities, especially in older, legacy systems, or as they start to leverage more of the accumulated personal data, that’s available in the dark corners of the web, to put together sophisticated personalized hacks that continue to blur the lines between the physical and digital worlds.

We’re also expecting an increase in the number of “mass risk” attacks – hacks that have the ability to cause fairly significant damage to a very large number of people, as well as an increase in smart hacks that find value in the accumulation of smaller pieces of less valued, or protected, information.

Gary Nowak (pictured right) is Partner for KPMG’s Shared Services and Outsourcing Practice in China

How many consultants do you know who just give up their life of first class travel, champagne lunches, and arrival by helicopter to luxury golf courses to slum it in the back streets of Shanghai?

Yes folks, KPMG’s Gary Nowak had it all . . . but his love of Yoga, meditation, and people-watching just got the better of him and off he went. So, without further ado, let’s learn more about KPMG’s Gary Nowak and what he’s learned having lived in China the last few years . . .

Phil Fersht, CEO, HfS Research: So good evening, Gary Nowak. Thank you for spending some time today with HfS. I know we’ve met in the past, but I’d like for you to give a little introduction to our audience. Tell us a bit about yourself, your history in the industry, and how you’ve ended up leading a practice for KPMG in China.

Gary Nowak, Partner, KPMG China:

Sure. Thanks, Phil. I appreciate the invitation. I’ve been in China since January 2013. In the summer of 2012, I took a trip to China in connection with a client I had taken globally—to Eastern Europe, India, and eventually China. I was very impressed with China, specifically Dalian China, a city with a high concentration of outsourcing, located in Northern China. After that visit, I requested, through KPMG, to be sent to China, specifically Shanghai, because shared services was—and still is—a very hot topic. During the preceding five years, there had been a lot of government attention and support for outsourcing, where the government specifically identified over 28 cities that could support shared services. So, my client visit in 2012 and the impressive infrastructure in China is what brought me here. Prior to my time in China, I worked in shared services in the United States, Europe, and Singapore with Arthur Andersen and, EquaTerra. And now, KPMG. These companies have filled out my over 17 years of experience in the industry. The move to China has provided me with a perspective of a dynamic, fast paced, and quickly growing country. Overall, China has been a tremendous experience both personally and professionally.

Ironically, back in 2004, I was in Singapore for about 10 months to set up a shared service center for the Asia-Pacific region, something that I just did in Europe. While in Singapore, I remember going to China and recognizing how complex business was in this country. More than 10 years later, business is still complex. In addition to business complexity, language and culture are also significant considerations when working in China. Mandarin is the main language, with only the higher-level executives comfortable doing business in English. A majority, if not all, of my clients prefer to do business in Mandarin. Once a project is sold, the day-to-day delivery is conducted in Mandarin, and I will debrief and receive consistent updates in English from my team.

So, that’s a brief history of my involvement in the shared service industry during the last 17 years—setting up shared services in different regions.

My time with EquaTerra and KPMG have given me valuable experience with outsourcing relationships. I’ve been involved in 13 different deals across the world with Fortune 500 multinational companies, where our clients wanted to outsource specific functions to various service providers. Eight of those deals were successful, and I was involved in every step of the process from identification of the service providers to the RFP creation and finally, the contracting process. Two of those thirteen deals took place since my arrival in China, and I’m in the process of supporting a third deal. There is a trend in China for companies to focus on internal captive centers rather than outsourcing; however, in the upcoming years I see the trending moving toward outsourcing since captives are extremely hard to maintain, and the employment costs continue to go higher and higher.

So globally, outsourcing is much more prevalent. And within China, the discussions are centered around internal shared services and captives. Notably, 90 percent of my client discussions have something to do with setting up China-for-China captive centers. As I talk to multinational clients, I get these kinds of questions: “What are my options for China? How do you handle the Asia-Pacific region? Do I need a center in China and also outside of China?” My perspectives have been shaped through speaking to probably more than 45 different companies that conduct business in China. My overall opinion is that if you have a China presence, you need a China shared service center. A China shared service center can service the rest of Asia-Pacific countries. However, handling China outside of China is extremely difficult. There are very few companies that do it, but it does happen on the rarest of occasions. As an example, I’ve spoken with Indian service providers about delivering work from their centers in India, and basically due to the things that I’ve mentioned—complexity and language—this isn’t possible.

Phil: Interesting! So when we look at China’s role in IT business operations sourcing, it’s clearly very, very different from the role it played in the growth of manufacturing over the years. Where do you think it is today in terms of capability and its role in the global sourcing marketplace?

Gary:

Prior to my arrival in China, KPMG conducted a study on outsourcing in China. The study identified over 22,000 service providers in China; 22,000—that’s a big number. These service providers were predominantly focused on IT outsourcing. I do think there is a need for this in China. I think that business is growing. I don’t see China as a major competitor for other regions like, say India, based solely on the competency of the resources here and the rising salaries in China. India has always been a lower-cost location for outsourcing, and I don’t see that trend changing anytime soon. There are companies I’ve spoken with that deliver IT services for the globe, from China; but, this is rare.

China has 6,000,000 to 7,000,000 graduates per year. My perspective is that the government is looking to support an industry where these graduates can gain employment. Shared services has been one of those industries where the government has provided incentives. Now, whether IT outsourcing can support a significant number of these graduates remains to be seen. Regarding the IT outsourcing industry specifically, I’ve had conversations with many Indian service providers—Infosys, Tech Mahindra, WNS, Wipro, Cognizant—and they all had expected to make a greater impact in the IT outsourcing market. They viewed China not as a competitor, but as a country where they could support the growth of their business. Several years later, the Indian service providers have been disappointed with the lack of China growth. NASSCOM hired KPMG to conduct a study as to why the Indian providers haven’t gained more traction in this market. The fundamental conclusion was the Chinese companies aren’t ready to outsource functions.

Phil: I think we’ve got to hand it to India for really taking hold of their traditional IT maintenance services business: app testing, app development for broad-scale enterprise, bread and butter apps. They’ve done a fantastic job. But we’re now going into a new era of more complex technology needs, such as testing around digital technology, mobile device platforms, BPaaS platforms—more niche applications and things like that. Do you think this is the opportunity for Chinese capabilities to step out and focus on some specialized areas that will involve new apps—new needs and capabilities? Or do you think this is still India’s game to play as they evolve in this disruptive economy we’re looking at?

Gary:

I think that question centers around one thing and it’s the leadership capabilities within shared services in China. If you had strong leaders in China who recognized there is a niche for these specialized areas. The struggle I see with Chinese companies is the lack of shared services leadership—those that have experience in this area and understand the fundamental value. The concept of taking higher value or specialized work is not easy to instill in Chinese executives. For example: I visited a Fortune 100 company at their Guangzhou shared service center. The center leader was a gentleman brought in from Germany; he and I spoke at a recent conference about the China Shared Services. So, I went to visit his center and they had 200 people, and I asked him, “Why aren’t you moving things in from other parts of the world, like Manila or your other locations?” He said, “Two reasons. One, it’s been done very well in the current locations. So all I can do is mess it up. Secondly, the costs are getting higher and higher here in China.”

So, he has 200 people responding to social media information. Rather than trying to take over work from their existing centers, he basically took on a new scope of work. So what he did was—he hired people to do that. And the other interesting thing about the leadership is—I think I met him on a Thursday, and during that week he took 25 members of his team to an off-site location to discuss strategic thinking on how to think more outside the box. To get back to your original question, for China to think outside the box is a bit outside the normal comfort zone of traditional leadership here.

I think that specialized IT outsourcing clearly sits with India to go up the value chain. If anything, India has pushed some of the lower value work into China. However, the problem with that is India in the foreseeable future is likely to be the cheapest delivery location. So moving from India to China isn’t going to create a positive business case. It’s going to be very difficult. Some Indian providers are thinking about using China as a disaster recovery/business continuity planning location. However, that is still a perspective to be fully recognized.

Phil: For multinational Fortune 500 enterprises setting up Pan-Asian headquarters, we’ve traditionally seen Hong Kong and then Singapore becoming popular. Are more companies shifting to Shanghai and some of the Chinese areas to run Pan-Asia operations, or is China becoming its own area?

Gary:

I absolutely think it’s in the conversation these days. Multinationals are setting up in and around Shanghai. If you start talking to centers of excellence (CoEs) and where they should set up, then you start having conversations about Hong Kong. Maybe you start having conversations about Singapore. But the real value and what I see in China that I don’t see in other parts of the world is coupling your corporate headquarters with your shared service center in the same location. This concept seems to make a lot more sense in China. So, basically your CoE and your shared service center coexist in the same location. Why? As I’ve learned through conducting several shared service roundtable events, Chinese employees want to feel integrated with the companies rather than isolated in a smaller Tier 2 or Tier 3 city performing shared services functions. It’s difficult to make those employees feel like they’re part of something while they are in a remote location. I think companies have had a lot more success here with combining their shared services and corporate headquarters.

You can immediately start reading the downside to this model: it’s a higher cost location, and it’s more expensive resources. But the upside is your attrition is more manageable the skill set to work between a CoE and shared services is something that, when combined, is more likely to help the CoE, like a tax and the treasury function with resources who have supported the company through your shared service center.

I run roundtable discussions here in Shanghai with multinational leaders and shared service center management team members. As we start talking about shared services in Shanghai, talent management is always a topic that generates significant attention. I can’t run a roundtable without talking about how to get good talent, how to retain talent, how to develop talent, how to manage attrition, how to keep the good people . . . so, I think a viable option for a lot of companies is to leverage their shared service center to be close to the corporate headquarters. So as you hire people, hire them through your shared service center. Work them for two or three years and then push them out to your organization, whether it’s a position locally, or as a business partner, or in the CoE. The concept is to leverage your shared service center as a training ground for future employees throughout your organization. In fact, KPMG is currently doing this with our shared service center in Foshan, and we believe it creates loyalty.

We have our own captive shared service center in Foshan, which is in the southern part of China about an hour outside of Guangzhou. We established the center about two years ago. For the employees who have been working there for two years now, they have the option to apply for positions within China in our Tax, Advisory, or Audit practices. We feel it’s a great incentive for people who start out in a support function and learn about KPMG and its culture. Essentially, when we want to hire resources, we can tap into this pool. It’s basically a two-year interview session. I feel that is a great way to address issues in China, which are around managing, developing, and retaining good talent.

Phil: So there is a bit of nervousness regarding the potential over?inflation of Chinese stock valuations and whether this could lead to a correction. What’s the mood in China right now in terms of the health of the economy and a potential cyclical downturn?

Gary:

I don’t see it on a day-to-day basis. As you could imagine, in China people don’t talk politics or the stock market all that much. There are discussions with other US partners, but I don’t know that by and large the majority of the people are playing in the stock market. Regarding the cyclical downturn, the younger generation is not afraid of losing their jobs. They’re not afraid to quit their position without having something else lined up. They don’t have a fear in them about the poor economy, high unemployment, or any type of downturn that would cause them to lose their jobs.

At a recent roundtable discussion for the financial services industry the participants agreed that they’ll get a candidate, extend an offer to them, and two days before their proposed start date the candidate will turn down the offer they just accepted. There was an example of a resource coming in, working for a week and then quitting because they got a better offer. So when you look at the economy it becomes apparent that the younger generation has never been affected negatively by the economy. They haven’t known unemployment. They have only known, “I can get a job anytime I want.”

Phil: Yeah. I remember that during hypergrowth times. That’s not necessarily a good thing now, is it? It makes it hard to keep things under control and build long-term business plans. What’s your take?

Gary: Unless there is a crisis in the market, which isn’t good for anyone, this younger generation won’t comprehend the impact of unemployment or a bad economy. They haven’t experienced anything different. What’s happening in the United States with the downturn, people have a different perspective about the value of a job and the idea of working. In China, they’ve just seen very high growth in many areas. You go around Shanghai or any Chinese city and you see buildings go up all over the place. China is sponsoring some 30 different cities for shared services. Where they’ve built buildings, they’ve built infrastructure—very good, solid infrastructure. They’re just really encouraging companies to go set up shared services in these cities. Shared services is very much a top-down-driven strategy, and China is trying to pull companies into their cities. Pulling a company toward shared services is difficult even with incentives. Under the best circumstances, implementing shared services is challenging let alone when leadership was brought into the opportunity for the sole purpose of saving money.

Phil: From my time in Asia, I remember it was “in vogue” for ambitious younger Chinese workers to learn English. Is this still the case, or is that fading a little bit these days?

Gary: I think so. People I work with definitely started learning English at a lower level. My view is that learning English will significantly enhance individual careers. I attend a lot of KPMG events with interns, graduates, and students, and I really enjoy talking to them about their careers. They are speaking more English now than they did when I first arrived in China. Also, as I previously mentioned, they have no fear about finding a job upon graduation. They just try to determine their best option. Some KPMG managers may not be as comfortable in English, but I don’t see any fresh graduates or any of our junior levels not feeling pretty comfortable speaking English. Many of our recent hires have been educated in Europe or the United States. Recently, we hired two great candidates who were born in Shanghai, educated in the United States and who worked in the United States and now want to return home to continue their career. One thing I’ve learned about working in China is that eventually people want to make their way back to their homeland.

Phil: Do you have the same kind of feverish discussion around disruptive technology, automation, and things like that in China—like we are having over in the States?

Gary:

It’s not getting a lot of traction here with clients because China is fundamentally on the low end of the shared service maturity spectrum. My view is that if China waits so long to implement shared services, so that when robotics and technology are more prevalent, companies can “leap frog” over the better, faster, cheaper lean six sigma model straight to leveraging technology to capture savings. In this case lagging has its advantages. The caveat there is companies still need to do the hard work of standardizing their policies and processes and move toward standardization.

Getting everybody on the same page from a process and policy perspective can in itself be a challenging task. Robotics and technology won’t eliminate or magically solve these types of complexities. In trying to formulate my strategic thinking about China, I think that companies should standardize as much of their operations as possible and look to leverage technology either internally or externally through outsourcing. Service providers are already starting to build in technology as part of their solution to be more competitive moving forward. Once service providers offer a strongly competitive price that’s less expensive than what companies are incurring today, outsourcing will begin to take off.

Phil: Thanks. So one final question, Gary. If you were to look out five years—what do you think it’s going to be like in China?

Gary Nowak, Partner, KPMG China (click for bio)

Gary: So I would say, just based on that last topic, I think technology is huge and if service providers can leverage technology to create a more compelling price for Chinese companies, they’re going to jump to outsourcing. Two things are going to happen: One is what I just mentioned—with outsource providers coming through with a technology solution that reduces costs. The second is if overall costs— specifically, salary costs—continue to rise, then alternatives need to be considered. If these two things happen, outsourcing will be very viable here, and of course if there is a crisis with control, compliance, regulatory or general business pressure, the executives need to address these issues and shared services offers a highly viable solution.

Phil: Gary, this has been great. I appreciate you taking the time from across the world to join us here on the blog!

Gary: My pleasure, Phil.

Gary Nowak is Partner, KPMG China. You can view his profile here.

Let’s get together in New York next week to reminisce about that wonderful phenomenon that was BPO, which – of course – is now a thing of the past, with everyone digitizing and automating their business operations, while adding layers of artificial intelligence to help make groundbreaking business decisions. Who needs BPO anymore, right?

In fact, us humans are probably not even needed at this conference, so why don’t we just meet at the bar instead and leave the discourse to our future employees:

Come to NYC next week and get your future BPO employees motivated…

But wait! It’s not over for us humans yet – honest!

The problem with all this much-hyped digital tech and automation is that it’s completely useless without the right talent to operate it. Don’t tell the software firms, but better technology underpinnings actually empower humans to do their jobs better – and spend more time on higher value activities.

“BPO” is now going through its biggest-ever facelift, with the advent of intelligent automation, analytics and digital, and I am personally excited to get some quality time in the Apple next week, at the 2015 BPO Innovations Conference, where we can cut through the hype and get to the real conversation, starting with my opening keynote address: Welcome to the As-a-Service Economy.

Come along and I will be hanging around all day to spend time with you all, with some of the HfS team, including Bram Weerts and Tom Reuner. We would love to spend time locking heads on where our industry is heading.

So!

Don’t miss Keynote sessions from HfS Research, Xerox’s Chief Innovation & Chief Process Officers, and HBO executives

Join leading buyer execs from Astra Zeneca, Bloomberg, HBO, McKesson, Pricewaterhouse Coopers, SunTrust Bank, Thomson Reuters

Hear from industry expert thought leaders at Avasant, Capgemini, Tata Consultancy Services, Xerox, Loeb & Loeb & Neo Group

Register today to build your rolodex during 5 designated networking sessions, including complimentary breakfast, lunch, and evening cocktail reception, where you will have the opportunity to win a test drive with a Tesla.

Registration is complimentary to buyers and practitioners. Influencers and Suppliers can use code HFS15 when registering to receive a 15% discount.

Conference Details October 22, 2015 8:00 am – 6:30 pm

Bohemian National Hall

321 East 73rd Street, NY, NY 10021

“Ten years ago, my CEO asked me to drive efficiencies through offshore outsourcing, now he’s asking me to make them through automation”, declared the CFO of a major corporation at the recent NASSCOM event in India.

This pretty much sums up where we are as a global services industry. We’re embarking on the next phase of productivity, and that means we have to incorporate it into our contracts and prepare to invest in the future model, not merely perpetuate the old one.

Service Providers invested in the old FTE model and it worked, now they need to make new investments in As-a-Service delivery

It’s not completely dissimilar to the old “lift and shift” FTE-centric deals of 5+ years ago, where providers would invest in the short term costs of client transitions, and spread the investments out over a 5-7 year contract to make the deal offer immediate attractive cost-saving gains for clients. Yes, they were making their first steps to becoming insurance firms for their clients, which is even more the case today, where the risks are higher and the savings more challenging to generate. However, if today’s service providers fail to develop scalable As-a-Service delivery platforms they can replicate across clients for the future, they will likely get replaced by other service providers in the future, which have made the investments necessary to provide more automated delivery, better data – and consequently more intelligent operating talent.

OK – the legacy FTE deals were less risky, so long as you could deliver up the lower cost people and shift the work to them without any major blow-ups. The modern deals require providers to find additional margin by automating processes effectively, converting freed-up effort into lower operating costs and also redeploying available talent on higher value collaborative activities. In other words, the old model was all about hard savings from direct labor swapping, the As-a-Service model is about a combination of smarter labor provision and genuine process transformation through better technology (i.e. soft savings).

It’s higher risk to avoid making the necessary investments – extinction could beckon for many

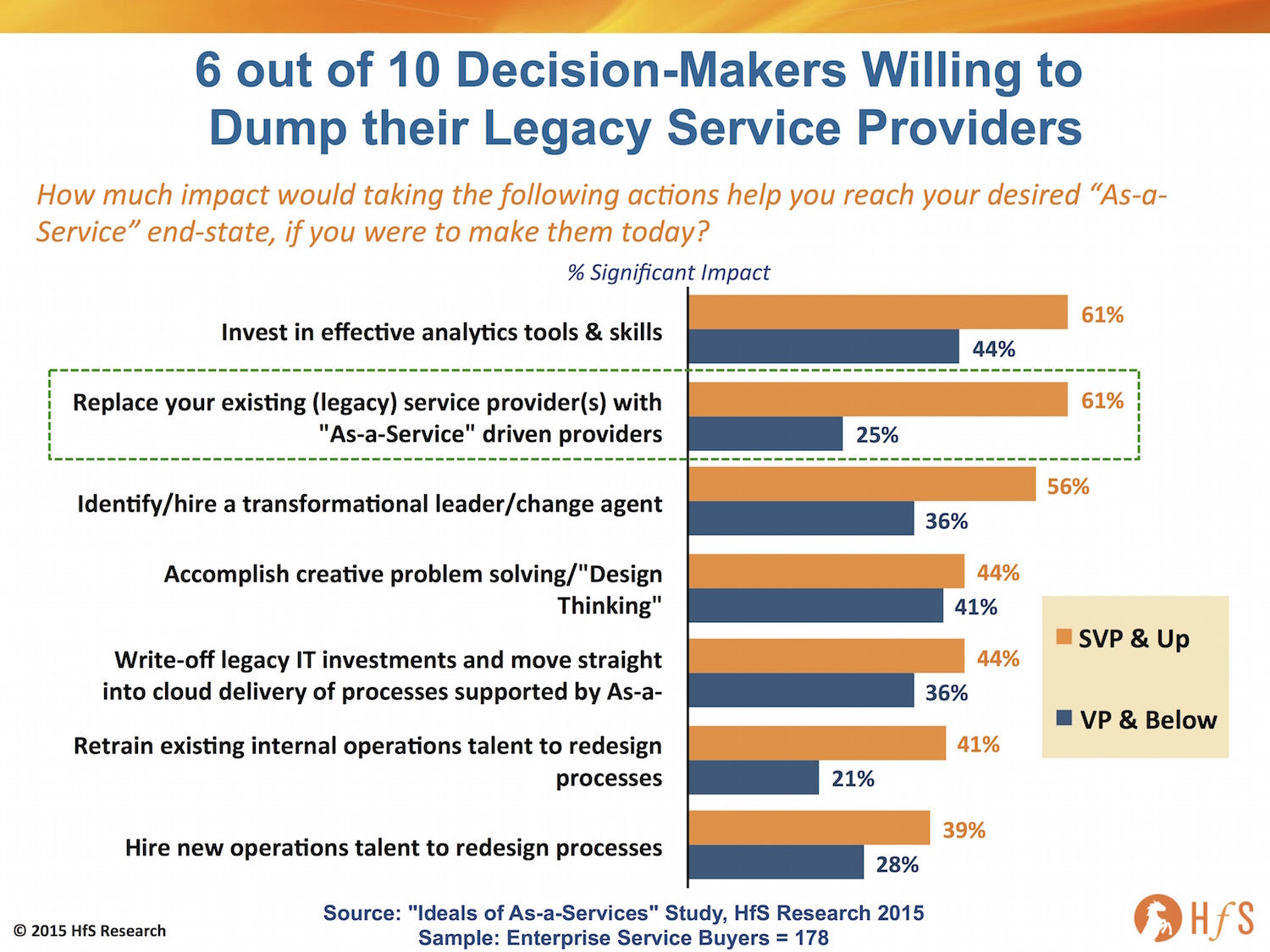

As the following graphic clearly illustrates, from our recent As-a-Service study covering 178 major buyers of services, if the major decision makers (SVPs and above) fail to see real As-a-Service progress made by their existing service providers, six-out-of-ten believe replacing their services providers would have a significant impact smoothing their progress towards their desired As-a-Service end-state.

While their more junior subordinates clearly do not view replacing their service providers as having such a drastic impact (25%), the frustration at the senior levels from providers’ failed promises and lack of progress to invest beyond the legacy model is abundantly clear:

This isn’t about like-for-like body-swapping, this is about removing menial transactional work and redeploying people resources into areas of higher value-add to clients. This is what real “transformation” (sorry, I said it) is about – spreading workloads across talent pools effectively, by leveraging smarter automation, SaaS-based process standards and training talent to work more collaboratively and intelligently.

The Bottom-line: Most service providers are not structured for success…. and the problem lies at the top

There are a lot of client RFIs on the market that are increasingly complex, but aren’t as attractive to providers as the juicy scale deals of the past, requiring a determined effort from the provider to cobble together the right resources and expertise to take them on effectively. Sadly, many of today’s service providers are simply not structured in the right way to take on more integrated / As-a-Service-type deals. At HfS, we are seeing some of the legacy service providers turn up their noses at these deals because they simply cannot break down the barriers internally to bid effectively for them. They are geared up for the dwindling legacy deals, not the new ones that are emerging from the next layer of buyers ready to move into outsourced As-a-Service business models.

In most cases, service providers are too vertically set up, for example, most still have an infrastructure service line, an application service line and a BPO service line – and most have product service lines too (not to mention some legacy vertical industry groups that do not even talk to each other). Each service line still tends to use its own unique contracting, pricing and risk tolerances. In short, client expectations are increasingly becoming much more mature around integrated services, taking the form of As-a-Service models, comprising elements of infrastructure, storage, comms, apps functionality and BPO, optimized around that integration as opposed to discrete components.