What better than to hand out some awards to people who have absolutely no clue they are going to win one… and for actually doing something in 2018 to impact the world of IT and business services that actually shook up the rules of the game? And what better to offer up zero prizes beyond a fleeting recognition that they actually did something impactful?

No, they did not pay me $10K to sponsor a table at a penguin-suited gala dinner, and no, they did not coerce a bunch of analysts to sift through hours of painful “innovation submissions”. These are purely based on my personal experiences of 2018 and my judgment on ten folks who deserve some recognition for shaking things up in 2018!

The “They just didn’t see us coming Award”, Daniel Dines, CEO UiPath

When HFS introduced Robotic Automation to the world in 2012, the industry was transfixed around Blue Prism – the firm which pioneered unattended back office RPA – and Automation Anywhere, which shot on the scene in 2014 with the industry’s first RPA Maturity Model. RDA (robotic desktop automation) suppliers such as OpenSpan (acquired by Pega in 2016) were also present in the automation narrative as the worlds of traditional outsourcing, shared services and operations executives got shaken to their very core by the fact that people conducting repetitive work could be replaced/augmented by macros and bots. However, while these firms stole the headlines, one dude in Romania quietly went about building an RPA product that would leap from $10m-$150m in just the last couple of years, while its competitors could only watch on in awe. This founding CEO, Daniel Dines, engendered trust with executives and demonstrated an uncanny skill of being a technologist who quickly grasped how to communicate effectively with business line leaders. He also hired some excellent sales people, including the much-liked Guy Kirkwood, who’s social media skills should not be understated as a key reason for growing a firm so quickly. 2018 was definitely Daniel’s disruptor year. Now the firm is heavily backed and poised to battle it out for supremacy in 2019.

The “Resurrection award”, Nitin Rakesh, CEO Mphasis

It’s not often you see a company that had almost disappeared from the world, make such a credible and impactful return to the corporate spotlight. But this is exactly what happened in 2018 as Nitin Rakesh drove his new firm past $1bn in revenues and is likely to post double-digit growth. How can a company that was acquired by EDS in 2006 (at the time being touted as “EDS’ Bangalore Call center”), then being merged into the HP entity in 2008, before selling off its BPO assets to HGS in 2015, manage to retain its core IT talent and identity to find itself back in play as a standalone IT services business – in its own right – in 2018, as Blackstone bought out the HP shares? Not only that, the firm has positioned itself excellently as a core transformational IT services firm, with deep expertise in financial services, with many loyal clients always willing to share their experiences. While great Indian-heritage IT services firms, such as Patni and Syntel, have been subsumed into larger Western entities, Mphasis is back swinging punches and poised to give some of the leading IT services firms a run for their money in 2019.

The “Making Cyber actually cool Award”, Nicole Eagen, CEO Darktrace

While the whole industry seemingly got lost in a stupor of automation and AI, the one core area that will increasingly dominate the narrative in 2019 – and beyond – is cyber security. And not too many cyber firms have effectively brought together genuine ML and AI algorithms to create an “enterprise immune system for cyber defense”. Draktrace’s focal point is that enterprises should not require a previous experience (“pre-defined”) of a threat or pattern of activity, in order to understand what it is potentially threatening. It works automatically, without prior knowledge or signatures, “detecting and fighting back against subtle, stealthy attacks inside the network — in real time”. It sounds great, but this solution actually works, the firm is now valued at close to $2bn with $400m in revenue. My favorite line from Nicole: “Cyber security was all about keeping the bad guys out. But a lot of time the threat is from an insider, such as an employee, or someone who had managed to get inside the system.” Hiring founding partners from GCHQ and MI5 certainly helps bring the cyber conversation to the boardroom.

The “Approaching Digital the way it was supposed to be, and not confusing everyone Award”, Brian Whipple, CEO Accenture Interactive

The lovely term “Digital” has been distorted by so many people, 2019 will render the term practically meaningless. The firm which originally oriented the term for the IT and business services industry was Accenture, launching Accenture Digital back in December 2013, where the focus was firmly on helping enterprises “create new sources of value from marketing, mobility and analytics”. Since that time, the firm has amassed 36 digital agency acquisitions across the world to essentially become the market leader for digital advertising. While every other IT and BPO services firm under the sun boasts “digital” prowess, only Cognizant has reached double figures with 10 acquisitions and the rest are barely at a handful. So everyone is really helping companies enable the digital strategies they have already designed. When you look at the evolution of Digital, the core area has been leveraging interactive and social tech to drive new revenue channels and customer experiences, which has been the sole focus of Brian Whipple and his Accenture Interactive group, which has tucked in these numerous digital agency acquisitions over the years, pushed hard to retain their identities and cultures (something Accenture learned the hard way where most of its competitors are still failing). Brian’s declaration that Accenture is not “looking for Don Drapers” and, rather, is focusing on acquiring talent that focuses much more deeply on the entire customer sphere (than merely crafting ad campaigns) just edges himself into a well-deserved mention for banging the digital drum the loudest for 5 years, while his IT services competitors have failed to get even close.

The “Doing RPA differently Award”, Asheesh Mehra, CEO AntWorks

While we’ve been deluged with (pretty much) the same “bots are everything” monolog from the RPA industry for several years now, it’s been refreshing to see a firm get fully-focused on driving the data ingestion piece that RPA and intelligent automation can support. And today’s emerging auto/AI firms are becoming styled very much on their founder personalities… so you just can’t avoid the effervescent and colorful AntWorks honcho Asheesh Mehra, who has managed to pop up in every corner of the operations/services/AI space in 2018. With some funding in the bag, and some really excellent hires joining, expect AntWorks to make one helluva lot of noise in 2019 as they round out their platform and become an increasingly important part of the industry’s intelligent automation conversation. We need more AntWorks to keep shaking it up…

The ‘Doing services with a product mindset Award’ – CVK, CEO, HCL

While most of the IT services industry has resorted to following each others’ strategies of being technology agnostic, having poorly-defined digital strategies and a bunch of platform-things that noone really understands, HCL has quietly forged its own path and focused heavily on embracing its engineering and product development DNA. Several interesting engineering acquisitions, such as Geometric, Butler Aerospace and H&A set the firm’s stall out as a company which really likes to make and develop things. It’s eye-opening $1.8bn pick-up of all the IBM workplace software products, including, IBM (Lotus) Notes, Domino and Appscan, while not appealing to the media as relatively “sexy”, will end up creating a masterstoke $10bn new business for the firm, provided it can develop the customer base and improve on products that need a bit of work. The man with the plan is the humble, softly spoken and incredibly smart “CVK” (C Vijayakumar) who has persistently resisted the marketing glitz and the drum-beating to focus his firm on where he sees its differentiation. I anticipate more to come from HCL in 2019 as it rounds out its ability to build products that enterprises are actually using.

The ‘Hail Mary Award’, Ginni Rometty, CEO, IBM

While poor old Ginni has had to hold the fort as IBM went through 23 consecutive quarters of revenue decline, tried persistently to keep the dialog flowing around cognitive and Watson, you have to give her some serious credit for betting the entire bank on the RedHat acquisition this year, setting the firm back a cool $34bn, despite revenues of barely $3bn. The stark reality is that IBM really wants to out-opensource Microsoft, add some cloud mojo – and also add some serious RedHat management talent to its ranks. If you forced me to give you my opinion, I’d say that IBM has taken a decided pivot away from poster-boy IA giant Watson, to go back to its enterprise IT core and solve real challenges for real people. And you can’t beat a $34bn Hail Mary… so Ginni makes the 2018 cut..

The “Superhero CEO who can close a humungous deal Award”, Abid Neemuchwala, CEO, Wipro

Abid took on Wipro at a difficult time, when the company needed to raise its value proposition with enterprise clients, had not been performing particularly well in the market and – to cap it off – have one of its biggest clients, Carillion, go belly-up. It had many of us wondering why Abid would leave his BPO leadership role at TCS, where he had pretty much created a billion-dollar business, to take up a Wipro hotseat that could drive him even more crazy. But anyone who knows Abid, knows he’s a workaholic who loves a challenge, and – to cap it off – is one of the most gentle, sincere and nice guys you will ever meet. Which may explain how he convinced Alight Solutions to drop $1.6bn on a 10 year mammoth IT/BPO engagement that is one of the largest ever known to mankind. And right at a time when his company needed it. A terrific win to steer a company in a new direction. 2019 will not be without its challenges for Wipro and its close competitors, but having someone like Abid at the helm is a much-needed advantage.

The “Multi-billion dollar startup Award”, Chris Caldwell, President, Concentrix

Before its merger with IBM’s call center business in 2013, Concentrix was a little-known contact center tech business, which its parent firm, Synnex, put under Chris Caldwell’s charge to grow. Hence Chris had to take his experience managing a much, much smaller firm and figure out how to play in a fast-commoditizing and consolidating market. And grow it he has achieved, adding the likes of Minacs and Tiger Spike before surprising the whole industry with the bargain uptake of the Rolls Royce call center business itself, Convergys, pitting the firm just behind Teleperformance at the head of the market. While his competitors have been scrambling, looking at curious pickups like Intelenet for a billion, snapping up a heritage global call center firm with flagship enterprise clients, some great technology and people delivery culture for just $2.8 billion, places the firm in a very aggressive position to kick on in 2019 and push hard for overall market leadership. Chris will need to figure out how to adopt automation at scale, really embrace emerging cognitive solutions, but with the last few years’ track record to bet on, who will bet against Concentrix now?

The “Veni, Vidi, Vici Award”, David Poole, CEO/Co-Founder, Symphony

It’s not often you get to tip your hat to someone you’ve known for a long time and witness them achieve, literally, exactly what they set out to… but David Poole did exactly that. Not many people can boast to launch a consulting firm exactly four years ago and achieve a $69m acquisition to a global provider such as SYKES. When you compare this with the $74m ISG paid for Alsbridge and the (rumored) $85m KPMG paid for Equaterra, you have to hand it to David and his founding friends David Brain, Ian Barkin and Pascal Baker for catching a wave and finding their desired exit in less than half the time – and a lot more value placed on future potential earnings than merely existing revenues. When David came to visit me to tell me he was “going full on into RPA” in the summer of 2014, I have to confess I was skeptical as I knew the area needed a massive personal commitment, and people prepared to work unpaid for a very long time to get it off the ground. But that is exactly what he and his founders achieved. You may enjoy this blog with David in 2015… where everything he said pretty much came true. Now am sure Chuck Sykes is hoping for David’s vision to stay as consistent in 2019!

Remember when Amazon, Apple and Microsoft were racing to become the first $1 trillion valued firms? In just a few weeks they all languish in the $600m-$700 range. That’s a market decompression from a high never quite seen before, and it seems that the floodgates are now fully open, as political uncertainty (driven by colossal political egos and selfish self-interest in both US and UK), combined with a sentiment of “surely it’s time for a long overdue recession”. In short, the markets are having a correction and our economic outlook is being clouded by political uncertainty. Noone is better than talking themselves into a recession than the human race.

We should have just let the robots take over and go with the flow

In the past, when we arrived at a market correction, we’ve quickly shrugged off the over-exuberance that engulfed our lives and focused ourselves quickly on the realities of keeping our jobs and conserving our cash. This time I am not so confident society is ready for a cold turkey experience of, heaven help up, reality.

This time, all those lovely pictures of robots and repetitive marketing messages that all seemed to have emanated from one festering camembert-infused Shutterstock site, have combined to send too many of us in a fantasy maze of artificial nonsense, from where many of us will fail to find a way out.

So why couldn’t we have all just stayed there, inhaling this pungent odor of future fantasy, until our tech stocks exploded in that sea of $millions, where we could just retire and let that next generation worry about fixing the stagnant world we left behind? Why have we become the ones who have to learn from our own mistakes and try and fix them?

Why does anyone have to be held accountable for anything anymore? Isn’t that the new mantra of the workplace? I thought the future of work was “no work”?

Don’t worry – you can (somehow) bring yourself back from your digitally-transformed, robotically-automated and ML-infused unreality – all made possible by that blockchain fantasy, where, if all else fails, magic will, ultimately, provide the answer. You can do it, it’s hard, but you can lock yourself in a padded cell and let the digital delirium slowly subside into a silly dream. “Remember that time we all thought robots were taking over” will be a good old topic down at the bingo hall as you reflectively look back at the AI careers that never quite materialized with your old cohorts who also dragged themselves back from digi-blivion.

The Bottom-line: Accept it was fun while it lasted, but it’s time to peel back the layers of bullshit and find those core attributes that used to make you successful.

It’s time to be honest with yourself – you never even bothered to actually define what digital transformation really was, beyond positioning yourself as someone with disruptive DNA. And you never really knew more about RPA beyond the endless posts and blogs about those stages of “maturity” you need to go through (even though you’ve never actually met anyone who knows much about RPA than those really smart software salesmen). Did you even bother to put yourself through the basic training of writing a script – or was that all a bit beneath someone of your undoubted prowess?

And you’ve probably started to bleat on about Machine Learning and AI as if this was somehow your true calling in life, ever since daddy bought you your first train-set and you demanded he return it to fund your python course instead.

Yes, folks, those heady days where you had already made it without barely even bothering to fake it are over.

So dig deep and remember what made you great in the first place… and sure you can identify with at least one of these five attributes:

You may have been an amazing communicator… so learn how to articulate your firm’s true differentiation in plain English. What is it you bring to the table that your competitors cannot? How can you siphon through the buzz-talk to articulate real value, not fake value, because in the new reality, the focus will be on the real, not the fantasy.

You may have been awesome at numbers… then learn to create metrics that matter to your business to prove the value of doing things. Demonstrate how man-hours saved equates to impact on top/bottom line. Quantify the impact on customers when you fix a process chain that includes fulfilling a customer need. Quantify the impact on growing a business by speeding up the cash flow cycle, such as people and tech investments to get ahead of customers.

You may have been awesome at selling… the get back to selling solutions people will actually buy, as opposed to solutions you want your next prospective employer thinks you can sell. Being great at sales will be even more in demand as the need to actually close business quickly supplants the need to promise future deals that most people realize are unlikely ever to happen.

You may have been terrific at relationships… so get back to getting to know your clients better, as opposed to trying to impress them with fancy stuff they don’t really understand (and neither do you, but you know some bigger words to use). However smart and amazing we all may have become, it’s the trusting, deep relationships with your peers, colleagues, and customers which will make you successful.

You may have been a terrific bullshitter… so find those remaining viable AI and blockchain firms still functioning and blowing their seed capital, and get a sales or marketing job fast!

Each year we promise no more predictions but it’s a habit we just can’t kick. So have 19 of them from the HFS research team…

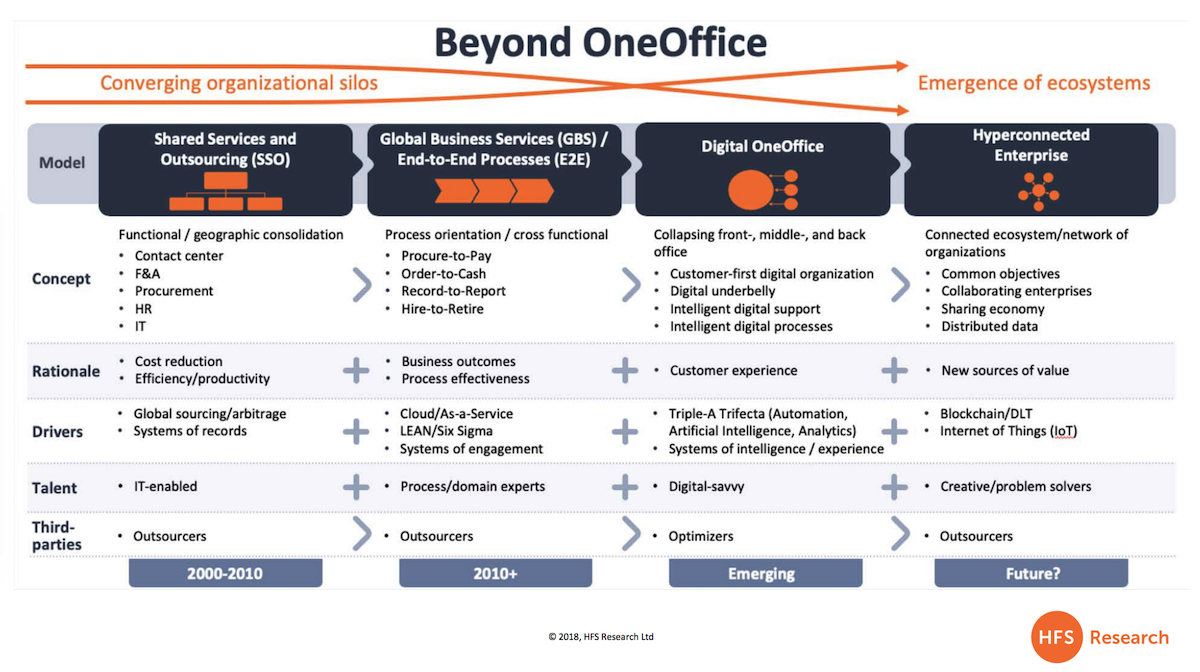

“OneOffice” becomes reality. Organizational silos around front, middle and back-office will continue to erode in 2019 to create a boundary-less organization where there is only one office that matters – and that is the office that caters to the customer. The triple-A trifecta of automation, artificial intelligence, and smart analytics is helping ambitious organizations reach their OneOffice goals at a much faster pace.

The Hyperconnected enterprise beyond OneOffice will emerge. As organizational silos converge, ecosystems will start to develop and a “Hyper-Connected Enterprise” will emerge. These B2B networks will be driven by collaboration across multiple organizations with common objectives around driving completely new source(s) of value. The emergence of blockchain and Internet of Things (IoT) is starting to make this vision of a shared economy with distributed and trustworthy information a reality.

The term “Digital” becomes so diluted, it is rendered meaningless as “Integrated Automation” drives the narrative. In the race to call everything “digital”, digital will start to mean nothing. Integrated automation across the HFS Triple-A Trifecta of Automation, AI, and Smart Analytics will drive the industry conversation in 2019.

The misplaced faith in “retraining” will fade. We will continue to see uncertainty and confusion on changing job roles due to the impact of automation and AI. This is clearly a much longer conversation than just 2019. But as more enterprises get their hands dirty with various technologies, reality will set in and we will at least retire the misplaced faith in “retraining” as the panacea to all talent management challenges. We will also see an increased focus from ambitious talent putting themselves through nanodegrees (such as Udacity) and other discrete training opportunities as the pressure builds to stay relevant in the face of emerging tech.

2019 will be the year of ‘how’. The why (customer experience, revenue impact, internal alignment) and what (emerging technologies) for transformation are now fairly clear after intense debate for the last couple of years. But “how” to go about executing on the aspirations is still a black hole. There will be many disappointments as exponential expectations are met with linear execution. Execution requires integration in every sense of the word – technology, talent, organizational change and leadership to achieve scale and deliver exponential benefits.

Success will be defined by effective digital change management versus digital adoption. There is an increased realization that simply throwing money at a new technology will not yield the desired results, but spending time in developing a method to the madness will drive success.

Emerging technologies

“Big iron” software firms will enter the RPA market. They have ignored RPA far too long and we saw SAP starting to make a move in 2018 acquiring a little-known RPA product Contextor. In 2019, mega ISVs such as Microsoft and/or leading systems of records like Oracle will acquire some RPA product challengers such as Kofax, Softomotive, Redwood, or Workfusion. The big three (Automation Anywhere, Blueprism, and UiPath) will likely remain untouchable.

RPA-as-a-service will get traction in 2019. RPA solutions will become increasingly function or process-specific to help enterprises scale. Today they are far too task specific. The push towards greater process and function focus will enable broader solutions and necessitate complementary technology integration like ML and NLP. RPA will certainly start to be smarter and the solutions will look more like the custom solutions coming from the service providers.

AI as a term will get tiresome and we will revert to something more meaningful. This is heading towards more combined applications of foundational AI building blocks to solve specific business problems. One of the “big four” mega-ISV firms (Amazon, Google, Microsoft, IBM) will pull ahead (likely Microsoft) in the AI arms race because of their deep investments and partnerships to offer the most comprehensive marketplace for enterprise AI deeply tied to cloud migration.

AutoML and XAI will gather momentum. If AI is to have true business-ready capabilities, it will only succeed if we can design the business logic behind it – and hence the need to design “explainable AI,” or XAI. The AutoML movement will also see traction as technology continues to become more accessible, resulting in a host of new companies getting started with AI despite limited resources.

Blockchain will come out of the closet as ecosystems across organizations that service the specific needs of a customer start to emerge. No single organization owns the entire customer experience and competitors and peers will have to start to figure out how to collaborate. Blockchain will provide the way to make it happen.

Cybersecurity will become a C-level priority versus the current mid-level management headache. Most enterprises understand the importance of securing their data but lack of C-level management commitment to effective investment is a key inhibitor of an enterprise’ security readiness. This will (hopefully) change in 2019.

Most enterprises and providers will realize that they will never be ‘cloud-only’ due to legacy workflows dependent on traditional on-premise kit. Cloud providers opening up the technical debt further by running towards newer more efficient platforms – migrating from one to the other is a pipe dream. Assuming the pipe is loaded with crack!

The smart providers will invest more in hybrid cloud platforms to help clients simplify the growing (expensive) chaos of multi-cloud environments. More so now due to the increased differentiation of hyperscale players forcing clients to build relationships with all of them for best in breed cloud.

Open-source technologies embed further into enterprise becoming a pillar of the modern technology stack. As CIOs are pushed to avoid lock-in to expensive and rigid proprietary tech.

Emerging players to watch in 2019

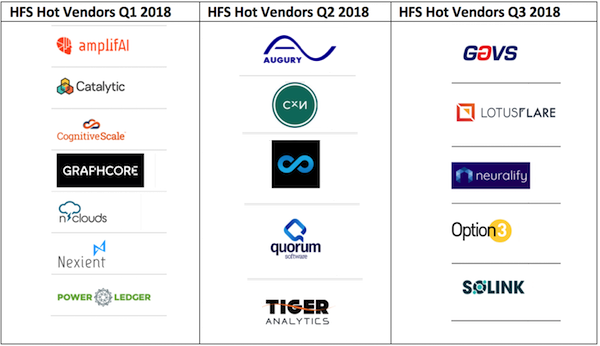

HFS Hot Vendors. Niche players with differentiated value propositions for the OneOffice will continue to proliferate. We will be keenly watching how the 17 HFS Hot Vendors profiled in Q1-Q3 2018 perform in 2019 (also watch out for the Q4 edition of HFS Hot Vendors in the new year)

Service Provider Landscape

Several traditional service providers will merge as market for services becomes unsustainable for so many commodity firms – right across business process and IT lines. Expect M&A activity involving the likes of Conduent, DXC, and NTT Data which all currently suffer from lack of market differentiation.

Large commodity call centers lose to smaller more nimble contact center players. Large commodity players have done precious little to add value beyond the FTE model will lose to smaller contact center vendors that have invested in premium tech services (such as RPA and chatbots) and nearshore delivery in their portfolio.

The boundaries between service offerings will blend into each other. Consulting and managed services will get diffused. The big 4 will start to offer more managed services and the leading SIs will continue to invest and expand their advisory services. “Fr-enemy relationships” will start to get established!

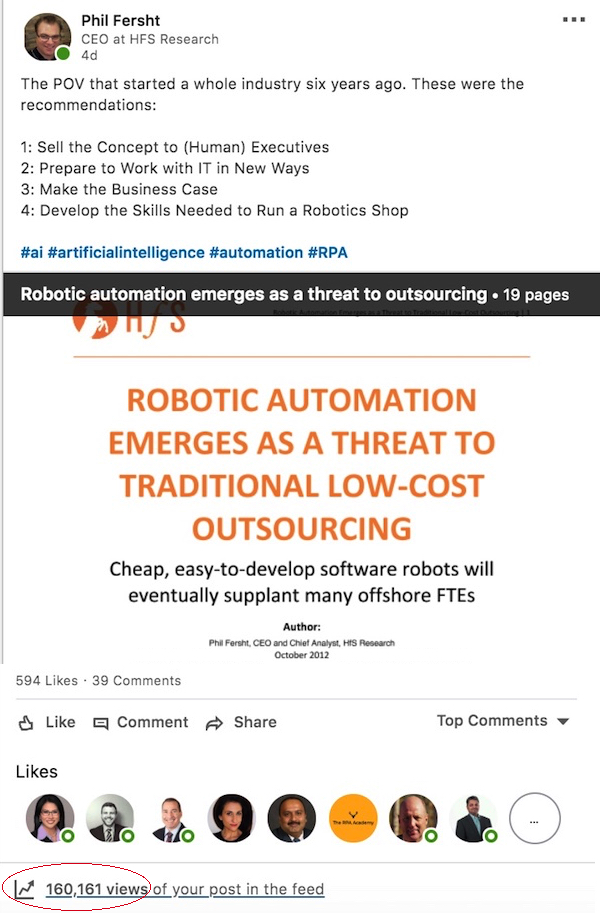

I was reminiscing about the first ever report we wrote to industry on the emergence of “robotic automation” and was amused at how little has changed in six years. So I popped it onto LinkedIn earlier this week and 160,000 people clicked on it. Wow.

What I love about RPA is it most often has the highest impact where there is a serious amount of IT failure, disorganization and overworked staff. Yes, that’s a lot of organizations to consider, and it’s one of the reasons why its hard to find this technology sexy – it’s built to fix the murky, dysfunctional stuff that has been squirreled away for decades, buried deep beneath failing ERP projects and conveniently ignored by senior executives who have few political points to score by acknowledging they should actually focus on fixing their broken underbellies.

This has been the failure of operations leaders for decades – simply focusing on layering more garbage over the top, when the real way to fix their inherent problems of dysfunction is to dig deep beneath their navels and address their broken process chains, and – heaven forbid – actually start to do something differently.

And there is no ground more fertile than the hallowed turf of the British National Health Service (NHS), the world’s sixth-largest employer with 1.7m staff, where decades of hollow political rhetoric, obscene wastage on ‘big-bang IT transformations” and big-ticket consultants on the gravy train, bravely held together by a woefully understaffed administration that end up spending on contract agencies just to keep the wheels turning. Let’s face facts: the UK National Health Service makes the basket-case that is Obama Care resemble a slick, well-oiled machine.

Enter RPA: a tool that is reducing GP referral processing time by 75%

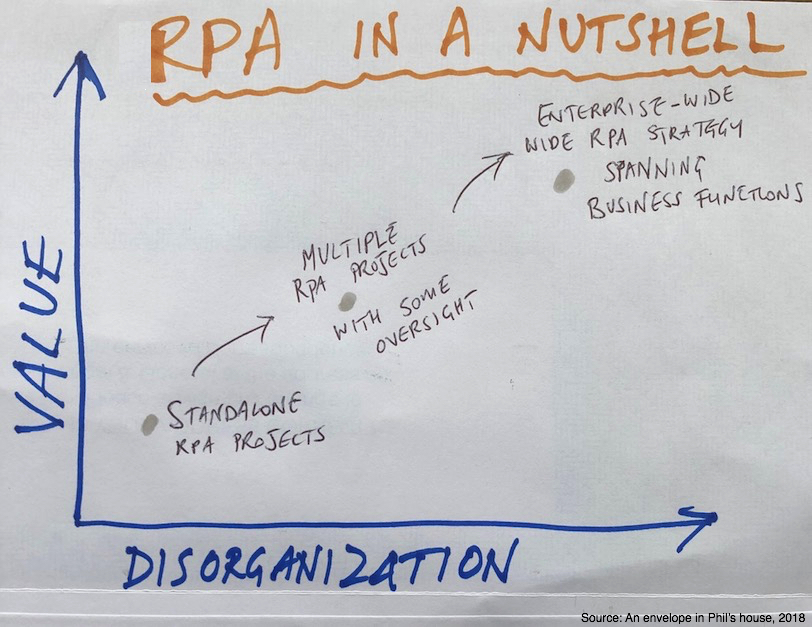

But there is renewed hope – and this hope can quite easily become reality if you entertain the idea of using RPA to unify document submissions, scrape data from legacy desktops to speed up GP referral times. And the real value to be gained here is if the NHS can adopt a common enterprise-wide strategy to deploy a common RPA as-a-service toolset and methodology across its 207 individual trusts. It’s so simple, I describe in on the back of an envelope:

Even in these tough times for the institution, many of its leaders are looking optimistically at the opportunities new technologies that can be customized provide, which can solve business inefficiencies and don’t involve the massive complexities of entire system upheavals. One particular example provides insights into how one NHS trust is actively addressing some of these issues, both in terms of saving the NHS money directly, easing pressure on administrative staff and providing a better more consistent service for patients being referred to hospitals. All of these endeavors are in line with the broader objective of ensuring that the NHS meets some overriding objectives to digitize services.

The starting point for this work began at the East Suffolk and North Essex Foundation Trust (ESNEFT). The organization faced many of the same pressures discussed above and like all healthcare services within the UK, they were directed to enable all GP referrals to be processed via the Electronic Referral Service (eRS) by October 2018. However, the existing system for processing electronic referrals was based on manual processes and was slow—a common challenge.

Essentially, once the GP had made a referral to the Trust, the support staff have to find information such as scans, blood tests, and other results which need to be manually downloaded and appended to the file. In a process which may seem bizarre to many enterprises, this often meant admin staff were required to print off material and then scan it back into the same computer (using the same printer and scanner) to create a PDF file to navigate bottlenecks between unintegrated systems. The PDF document is then uploaded to the administration system. Approximately, this process took around 20 minutes for each referral and created, what the trust described as an avalanche of admin, distracting medical secretaries from their primary task of supporting patients and consultants.

ESNEFT had already started a pilot scheme looking to automate some accounts payable processes with the RPA provider Thoughtonomy, which was showing a great deal of promise. So, the Trust decided to use the system to automate the referral process across five clinical specialties, using “Virtual Workers” (BluePrism bots), which actively monitor incoming referrals from GP patient appointments in real-time, 24 hours a day. Once triggered, the Virtual Worker extracts the reason for referral, referral data, and supporting clinical information and merges the information into a single PDF document. This combined document is then uploaded into the Trust’s administrative systems. The RPA system uses virtual smart card technology for authentication providing the same level of data security assurance as the old manual process. Overall, the complete task now takes less than five minutes. The Virtual Workforce is able to update all systems, instantaneously and extract critical information, which it passes on to the lead consultant for review and grading.

One of the most important aspects of this technology is its ability to work within the current system, regardless of how chaotic and unstructured that may be. It is technology that adapts to the real world and the way people actually behave and work rather than expecting people to miraculously change current tropes and behaviours. This is perhaps the single most important reason RPA works: it provides whatever shaped peg is required, no matter the hole.

RPA negates the need to spend vast amounts on many complex technology integration projects

This first stage has significant cost savings—estimated to be $275,000 in the first year—without removing staff. Crucially, the $275K saving achieved is made up of agency staff and sundry costs such as printing. ESNEFT believe that 500 hours of time was saved thanks to the solution. Plus it increased the job satisfaction of the admin staff, who could concentrate on more important aspects of their role.

For us, although the top line cost saving number is important, it’s the fact that a technology solution proof of concept has been deployed successfully (and relatively painlessly) within the NHS. To deliver the outcome required, there was no need to drive an enormous transformation project to align and integrate systems. Which, given the lack of appetite for big bang projects in the NHS is an achievement in itself. Simply put, the way the technology is used can be fitted into the existing chaos—it’s technology for the real world. It can provide a bottom-up solution to productivity improvements, which is a project that replaces part of existing work flows and automates manual and repetitive tasks. It accomplishes these things with the double whammy of removing tasks which is disliked, genuinely improving outcomes to patients, whilst helping to drive efficiency.

Bottom line: The NHS is not alone in facing an unforgivingly complex estate, but with technologies that fit into the chaos of the modern organization, this is only the start

If we look more broadly at the impact RPA technology could have on the NHS, we can use a simple calculation to estimate the ramifications this technology can have. We know that savings of $275K have been made on 2,000 GP referrals per week. But the figure for NHS England as a whole, puts GP referrals at 3.5m from April 2018 to June 2018. So, if this were scaled up, we could see savings across NHS England purely for GP referrals at a staggering $38m, this included all hospital referrals the figure rises to almost $63m, or around $1.3m per week. To put this in context, this would equate to almost 850 nurses for the GP referrals or almost 1,400 for all referrals in England (using the average cost of $45,000 per annum for a mid-tier nurse, source: Nuffield trust).

This is the tip of the iceberg, considering that more than 520M working hours are currently spent on admin and approximately $3.3 billion is spent on agency staff across the NHS as a whole during 2016. There is a great deal of savings to be had. Even if only a quarter of the agency spend is non-medical, that could be $820M per year that could be freed up with only positive impacts on patient outcomes.

I am not normally one for big grandiose predictions – I’m actually pretty dull when it comes to big hyperbole (I hope).

Honestly, I’d love to declare that AI will destroy a third of the workforce, and then magically perform a 360-degree flip and start creating jobs. I’d also love to declare that RPA vendors will magically infuse Machine Learning into their apps to produce AI magic. Because AI is magic, didn’t you know? I’d love to declare that software is eating the world… and then declare that it actually won’t, because a lot of it is actually pretty crap. I’d also love to declare that Blockchain will radically impact the entire business ecosystem to such an extent I can prognosticate all these business cases with so many holes in them, I might as well start lauding the transformational capabilities of emmental.

However, there is one big bold prediction I am prepared to make: Brexit will be dead in the water in a few weeks.

I am an analyst, I explore every permutation of almost anything that impacts economies, business, societies until I drive myself mad. I also work with other half-crazy analysts who do the same. Just take a gander at our recent analysis of the hazardous implications of Brexit on the UK economy.

So why is Brexit headed for the scrap heap?

It was always an “all in” or “all out”. We did neither. Seriously, we should have just drawn the guillotine on the EU right after the 2016 referendum, arranged a sensible withdrawal that could be governed effectively and transparently. We should have taken the pain then, and we’d probably be OK right now. Hell, we’d probably be part of NAFTA introducing delicious microwaved fish and chip pub luncheons to the Mexis and some actual real beer to the Canadians. And we may even finally get decent burritos introduced to the streets of London and poutine finally replacing soggy chips n’ curry sauce. Instead, we dithered, argued, bored ourselves silly arguing until no-one could quite remember what we were doing in the first place. Instead, we got to see close hand how indecisive, and stupid so many politicians are, how most of these people only care about their self-interests than any actual deep-driven mission or purpose. We also had many chances to think “Why are we doing this again? None of our businesses are happy, the Irish are freaking out, the Scots are ready to bolt, so we’ll only be left with, er, Wales (and even they are making noises)”. And Mr Trump even thinks it was a bad deal… and he was great in the apprentice, so it must really suck.

Brexit is a massive Catch-22. You can’t just compromise on an issue like this, even though 48% rejected it. There just isn’t any point in doing half-measures with Brexit – both scenarios suck. The diluted mess Theresa May has served up basically ensures we only get half-screwed by the experience. We are still tied to the EU, the Irish are still freaking out, we will close our borders in any case, but noone will want to come here anyway, because our economy will stink. In fact, most of the EU immigrant workers will probably flock to Dublin to work in the call centers after the banks have shifted over there… There really isn’t a compromise when the issues are this black and white.

The only current scenario is ‘no-deal disaster’ or ‘go back to the people to make a decision’. Let’s get to the point – the “deal” on the table is a plethora of half-measures with little upside for anyone. So that leaves only one Brexit option: no-deal and an economic calamity. There is no way 52% of the British folks care that much about putting a middle finger up at Brussels to destroy their livelihoods. When May’s deal fails next week, she will really only have one choice – to go back to the people to decide. And we only need a 3% swing from that heady warm June 2016 evening to fix this calamity. I occasionally like a bet, and this is one I’d throw a few pounds at…

The Bottom-Line: Parliament will throw this out and the British public will reject a no-deal Brexit… So Auf Wiedersehen Brexit

Firstly, there is no way MPs will vote for the current “soft-Brexit” deal on the table next week. May must know this too – and will simply go straight to the people to finalize this issue once and for all. There is no renegotiation with Brussels – that is clear, and there isn’t enough time, in any case, with the deadline being 29th March 2019. Secondly, Calling a general election with Brexit looming so close would be madness. There are now only two real options:

1) A “Hard no-deal Brexit”

2) No Brexit

So there will be a second referendum and it will swing for option 2. That won’t be the end of the matter, as a groveling “take us back” negotiation will take place, but the EU leaders all know they need Britain back to keep the EU strong – and this will drive Putin mad (who would love nothing more than a weakened EU). Trump liked Brexit for similar economic reasons of weakening Brussels’ power, but the US relies on a strong Britain as its gateway to Europe, and may now prefer an EU including the UK than one without.

There will also be considerable public fall-out as half the country did vote “leave” and they will feel betrayed by shambolic politicians. However, a “deal” was never going to be done and a transition organized in two short years – May was always on a hiding-to-nothing, and the only real takeaway is that referendums on complex issues never work. You know who loved referendums? One A Hitler… when information was easily controlled and the public easily brainwashed. In today’s age of hyper-connected everything, you simply can’t control anything!

It’s been more six years since we broadcast the concept of RPA to the industry and now we have finally unveiled the first comprehensive analysts of service providers and advisors in the space. Yes – it really does take that long for a discrete software market to build an ecosystem to install, develop, manage and scale. As my blogging pal Vijay Vijayasankar, one of the world most prominent enterprise software gurus, tweeted yesterday:

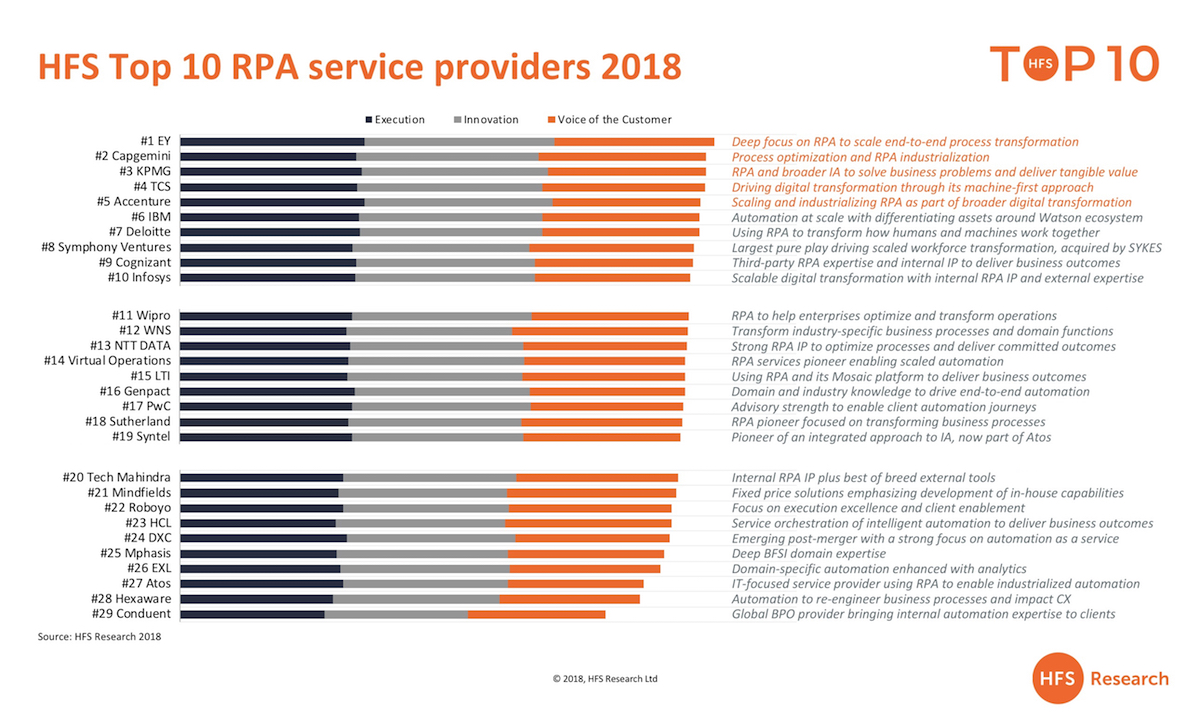

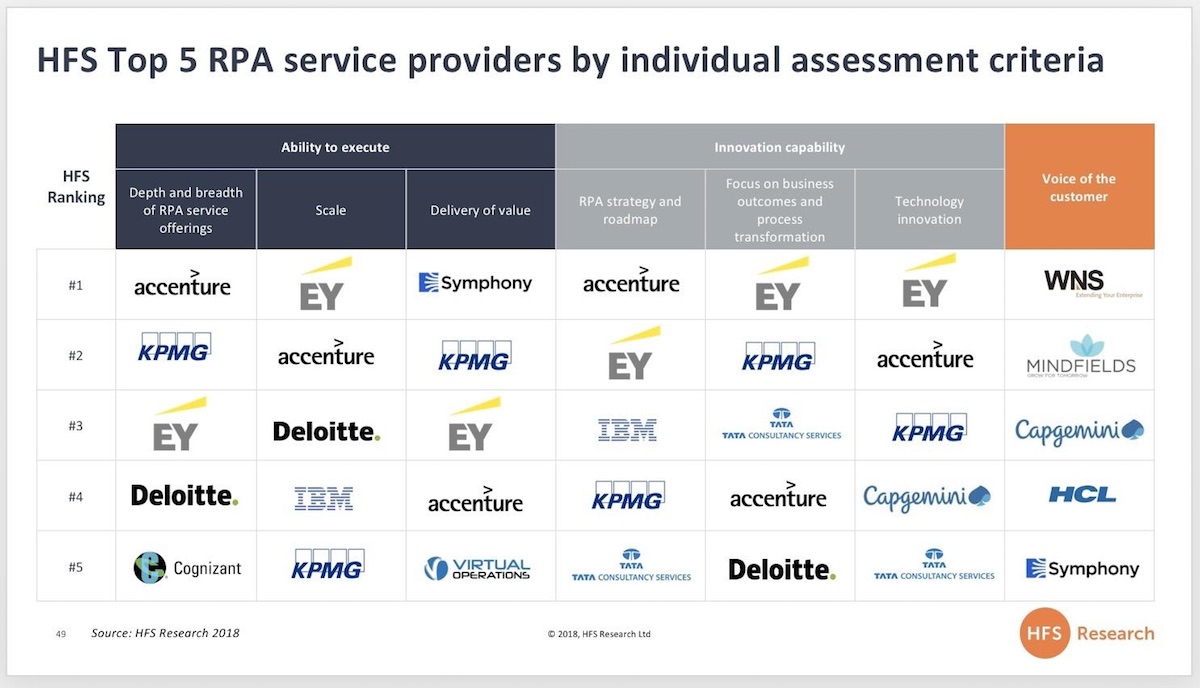

And what better than the new HFS Top Ten format where feisty analysts Elena Christopher and Maria Terekhova pull together the hygiene factors of execution and innovation with the “voice of the customer” as the makeweight factor to tell these suppliers apart:

Click on charts to enlarge

Key elements of this research

Robotic Process Automation (RPA) has emerged as a powerful change agent, with enterprises around the globe embracing it as a means to automate manual processes and create a bridge to a digital future. Despite signs of vibrant growth such as the latest billion+ valuations of the most prominent RPA software firms, RPA is still a nascent market with enterprise strategies continuing to percolate and a notable dearth of experienced talent.

In a first of its kind report, the HFS RPA Services Top 10 report examines the role service providers are playing in the evolving RPA market. We assessed and rated the RPA services capabilities of 29 service providers across a defined series of innovation, execution, and voice of the customer criteria. The report highlights the overall ratings for all 29 participants and the top five leaders for each sub-category.

This report also includes detailed profiles of each service provider, outlining their overall and sub-category rankings, provider facts, and detailed strength and weaknesses.

While we may refer in passing to broader intelligent automation or elements of artificial intelligence as part of providers’ capabilities, make no mistake, we focused this report squarely on RPA and assessed all providers only of their RPA services capabilities.

Research methodology

The RPA Services Top 10 report assessed and scored service provider participants across execution, innovation, and voice of the customer criteria. The inputs to this process were detailed RFIs we conducted with 29 service providers, reference checks with 58 RPA clients, briefings with leaders of RPA Services practices within service providers, HFS surveys with 659 Global 2000 enterprises, and publicly available information sources. Specific assessment criteria and weighting include:

Ability to execute (33%)

Depth and breadth of RPA offerings including capabilities across the HFS RPA services value chain, use case identification, change management, and governance expertise Scale including deployments, clients, RPA trained resources, and commercial traction and growth

Delivery of value including the ability to drive value through end-to-end process approach rather than short-term cost-cutting

Innovation capability (33%)

RPA strategy and roadmap including vision and credibility of strategy, integration with broader intelligent automation strategy, and identifiable investments in RPA strategy

Focus on business outcomes and process transformation including the ability to deliver outcomes, models for co-innovation around process transformation, and transformation consulting

Technology innovation including depth and breadth of internal RPA-related IP and external partnerships for RPA

Voice of the customer (33%)

Direct feedback from enterprise clients via reference checks, HFS analyst/enterprise relationships, surveys, and case studies critiquing provider performance and capabilities

Executive summary

A first-of-its-kind comprehensive study of 29 RPA service providers: The HFS Research RPA Services Top 10 report is a first of its kind study where we rated 29 service providers across elements of service execution, innovation, and voice of the customer.No single type of services firm stood out as the de facto leader for RPA services: Our resultant Top 10 leaders are a mixed bag of consultants, global system integrators, and RPA services pure play firms—all supporting customers across the RPA Service Value Chain. The broad roles of the services players reflect a growing but still nascent market with limited talent resources and services firms jockeying to secure their role as the service provider of choice as enterprises scale RPA.

The overall Top 10 leaders are EY, Capgemini, KPMG, TCS, Accenture, IBM, Deloitte, Symphony Ventures, Cognizant, and Infosys. These firms exhibited a strong mix of service execution excellence, applied innovation and vision, and verified customer satisfaction to rise to the top of our RPA services study. Being adept at provision of AI-focused services does not make a provider an RPA expert: RPA and the various building blocks of AI are different technologies requiring distinct skills. Many services firms who fared well in our AI Services Blueprint have not necessarily cultivated deep capabilities in RPA. While they complement one another in the intelligent automation context of our Triple A Trifecta, it is critical to ensure your provider has actual RPA chops.

Trained RPA talent is growing, but experience is thin: The average number of trained RPA resources across the 29 providers in our study is 1,160, with the median at 675 and total resource base at 32,474. However, HFS estimates that at least 80% of these have less than two years of direct RPA experience.

Enterprise satisfaction with RPA services is squarely mediocre: Customers have spoken! The average satisfaction score for our study was 77% out of 100%, with many firms that usually achieve high satisfaction scores receiving lower than typical ratings from both their hand-picked references and HFS’ survey-based ratings. We believe part of the causality lies in enterprise frustration with time to benefits. Transformation takes time. While many small RPA initiatives at a single process or function level can be quickly implemented and proven to show benefits, broader scaling and movement to a hybrid digital and human workforce takes time. The market hype, often from RPA software vendors, continues with its mantra of “RPA is quick and easy,” thus continuing to obscure the reality that RPA and broader intelligent automation is not a quick-hit lever but part of broader scaled digital transformation.

Change management and governance capabilities are lacking:Service providers’ ability to provide change management capabilities and assist with setting up and ensuring solid ongoing governance were the lowest rated execution criteria, reflected as an element of depth and breadth of RPA capabilities. Enterprises and service providers alike need to implement these capabilities as ongoing elements of their automation strategies and not just pay them lip service.

High satisfaction is tied to focused RPA engagements: The providers that scored well in the voice of the customer metric generally had a very focused approach to how they are offering and delivering RPA—as part of optimizing business processes as with BPO firms or as their sole focus as with the RPA services pure plays. As one enterprise executive put it “the focused approach helps us achieve targeted benefits and then move on without the pressure and expectation of a visible center of excellence and loads of expenditure on licenses.” This belies the lack of scaled RPA initiatives.

The biggest gap in RPA services capabilities is in post-implementation: Service providers have built strong depth of capabilities in RPA planning and implementation services. They are less experienced at supporting clients after go-live for management, operations and optimization services. As enterprises continue to scale RPA and broader intelligent automation, HFS expects clear needs to emerge in line with supporting in-house implementations versus managed services.

Service providers’ greatest contribution to the RPA market is their IP: While RPA technology skills are valuable, the various frameworks, accelerators, libraries and enabling tools that are being developed by the service provider community to facilitate RPA adoption are their greatest contribution. Much of this IP has been focused on process automation identification and feasibility studies, quantifying potential ROI, and fast tracking implementations. This is now shifting to enablement of RPA extension (RPA+cognitive or AI elements), building industry and domain-specific accelerators, and vendor neutral (and multi-tool) management platforms for integrated human and digital workforces.

The prevailing approach to RPA software by services firms is best-of-breed agnostic: All 29 service providers included in our study refer to themselves as RPA software agnostic. This list includes the seven firms that have developed their own RPA software. These firms will generally defer to client choice or existing investments in other tools, but do position their own tools as powerful greenfield options.

Of the “big three” RPA software products, service providers have the most experience with UiPath: All service providers in our study have built their RPA services capabilities around some variation of the RPA software big three of Automation Anywhere, Blue Prism, and UiPath. UiPath ranks as the RPA software product that service providers have the most experience with, followed by Blue Prism and then AA.

Beyond the big three, Pega, Nice, WorkFusion, and Softomotive rose to the top: Service providers have complemented their big three RPA focus with various other firms. Many global service providers already have Pega or Nice practices based on their broader platform capabilities, and RPA is an add-on. This has helped propel Pega and Nice into the fourth and fifth slots, respectively, for depth of use by service providers. WorkFusion was noted as a viable option for BFSI clients, and Softomotive was noted as cost-effective.

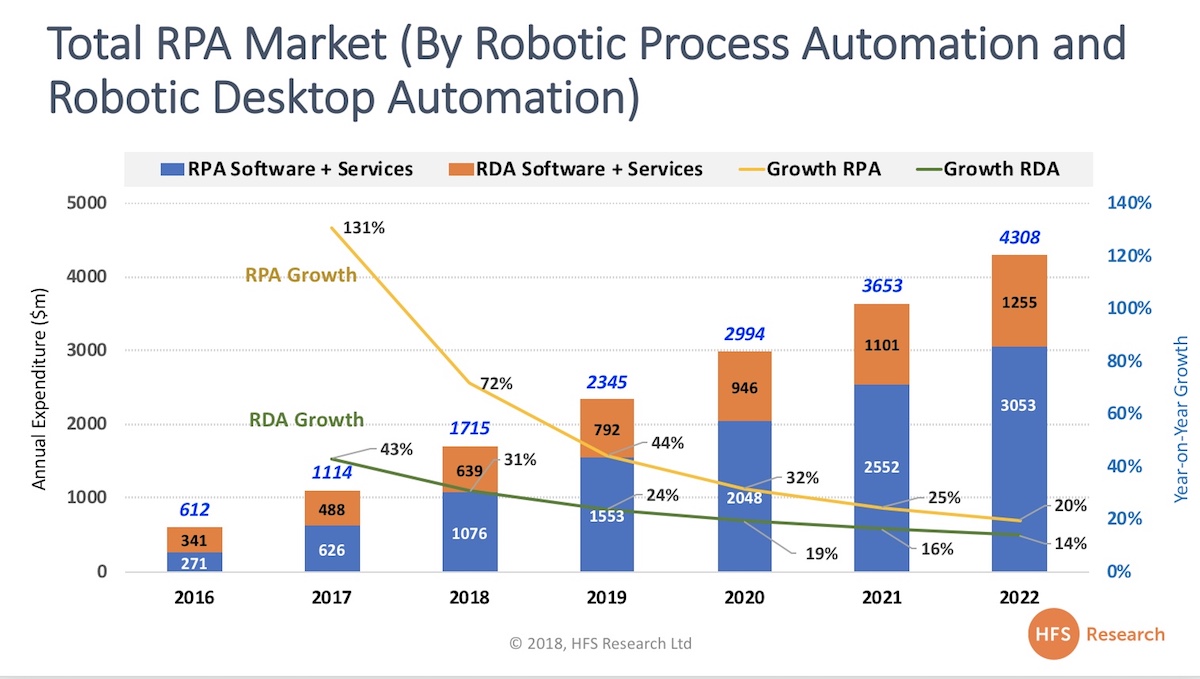

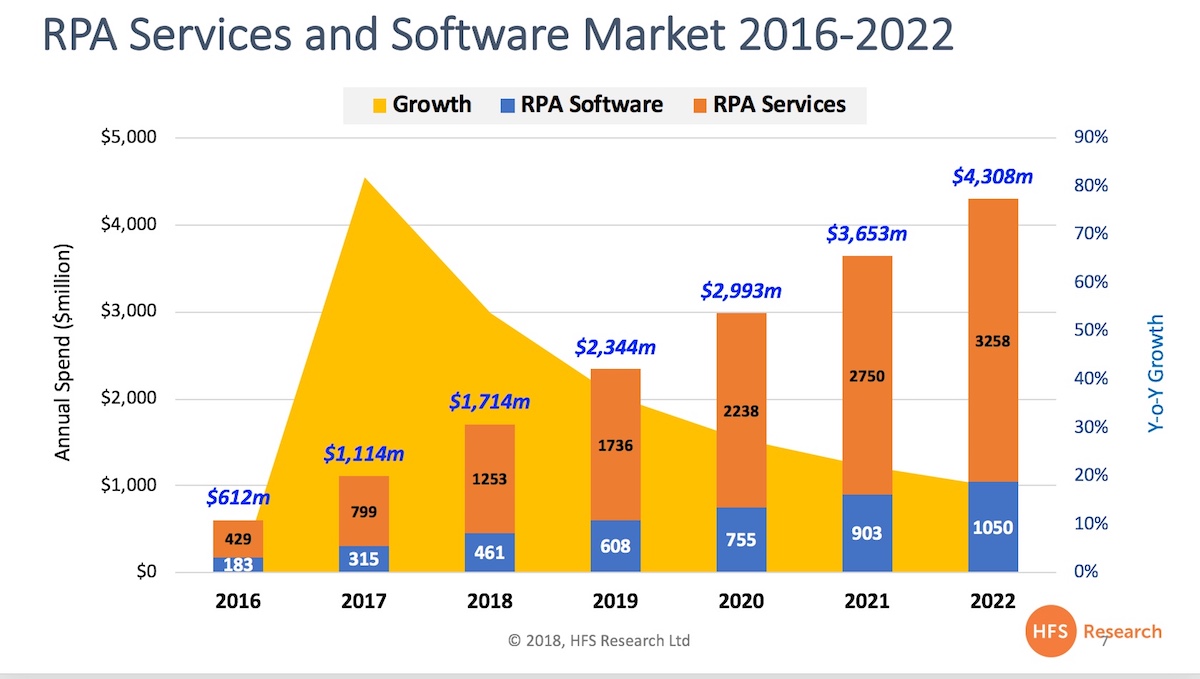

Well… it’s been quite a 2018 in the fantasy world of RPA (RPA plus RDA), where some of the fantasy dollars have magically become real, as the market hit $1.7bn – an increase of $250m from our forecast last year. So when the more conservative of forecasters (HFS) undershoots the market by 17%, you know RPA has been sneaking down the growth hormones of late.

So why is RPA growing above initial analyst estimates?

RPA vendors, in particularly UiPath and Automation Anywhere (AA), have been able to recognize more revenues than expected. Bots licenses are being sold and deployed faster than we envisaged, due to effective training programs and aggressive support from third-party services firms;

The slowdown in new business process outsourcing engagements is driving more focus from enterprises in discrete strategies to drive efficiencies and digitize processes (and encourage more bots plus humans engagements);

The shift in the focus of RPA from job elimination to augmenting talent, digitizing processes and extending the life of legacy IT systems has increased the appetite of operations executives to fast-track RPA training programs and invest in broader intelligent automation strategies – even though most enterprises are still in the “tinkering phase”;

The initial adoption of “attended RPA”, which makes up the majority of RPA and RDA engagements currently in play will eventually drive more “unattended RPA” where the increased value will be created and genuine alignment between RPA models proving to be a gateway to broader AI engagements;

The ramp up from service providers and consultants to support enterprise adoption has continued unabated, especially with the flattening of outsourcing investments and the waning interest in Global Business Services models. This reliance on third parties has proven to be a key dynamic behind the growth in RPA as solution providers prefer to sell through the services channel for larger enterprise deals and accelerate client training and development. The strong focus from the likes of Accenture, Capgemini, Deloitte, EY and KPMG has given the RPA market immense credibility;

Rapid funding of RPA vendors (in addition to rapid revenue growth) has encouraged these longer-term investments of many enterprises previously skeptical of investing in very small software boutiques. Largest examples have been AA and UiPath, attaining capital investment rounds as high as $250/$300m, but also some lesser-known niche RPA tools firms, such as Softomotive, which recently had a $25m investment round announced;

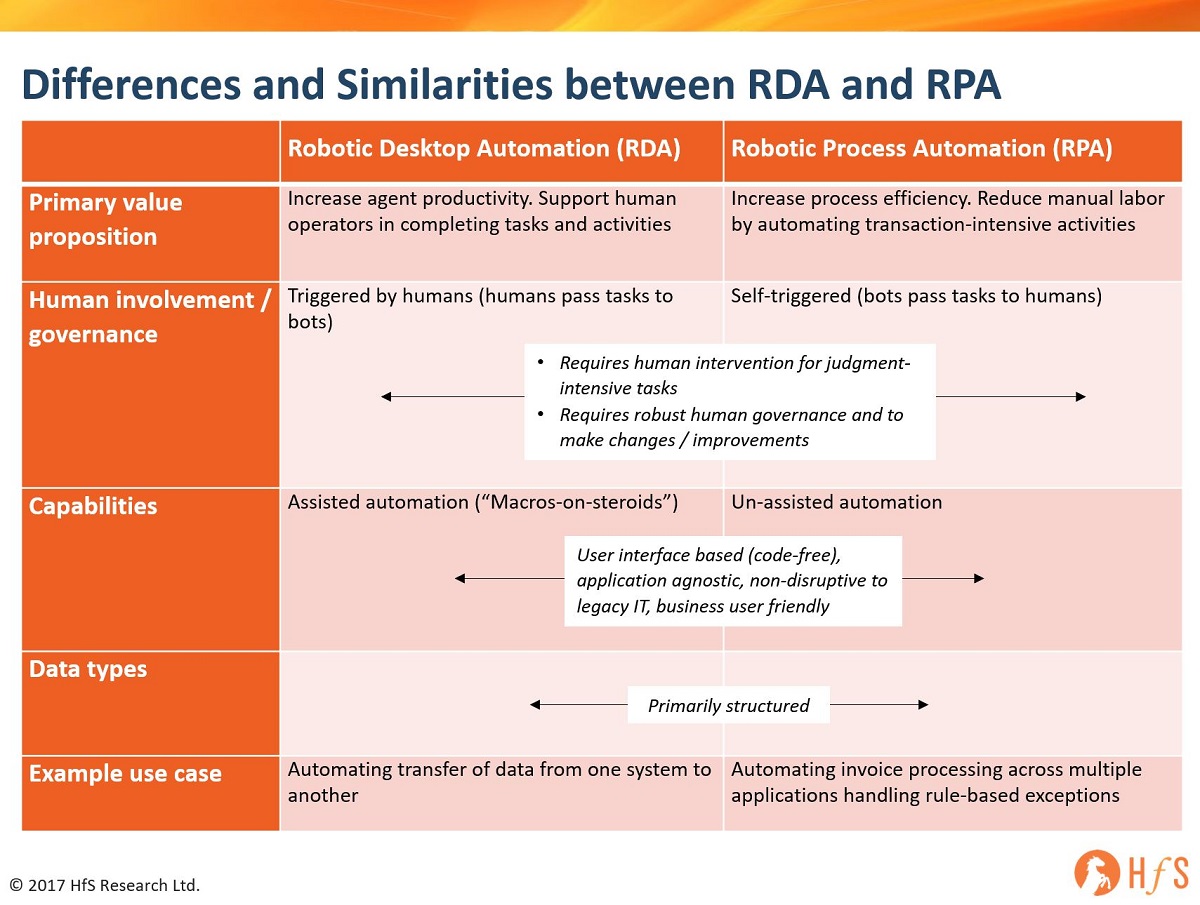

Example use-case: automating invoice processing across multiple business applications handling rule-based exceptions. RPA is different from traditional automation software as it is inherently capable of recognizing and adapting to deviations in data or exceptions when confronted by large volumes of data. In effect, it can be intelligently trained to analyze large amounts of data from software processes and translate them to triggers for new actions, responses, and communication with other systems. RPA describes a software development toolkit that allows non-engineers to quickly create software robots (known commonly as “bots”) to automate rules-driven business processes. At the core, an RPA system imitates human interventions that interact with internal IT systems. It is a non-invasive application that requires minimum integration with the existing IT setup; delivering productivity by replacing human effort to complete the task. Any company which has labor-intensive processes, where people are performing high-volume, highly transactional process functions, will boost their capabilities and save money and time with robotic process automation. Much for RPA is self-triggered (bots pass tasks to humans), but requires human intervention for judgment-intensive tasks and robust human governance and to make changes / improvements.

Similarly, RPA offers enough advantage to companies which operate with very few people or shortage of labor. Both situations offer a welcome opportunity to save on cost as well as streamline the resource allocation by deploying automation. The direct services market includes implementation and consulting services focused on building RPA capabilities within an organization. It does not include wider operational services like BPO, which may include RPA becoming increasingly embedded in its delivery.

RDA Definition:

In addition to RPA, the other software toolset which comprises the emergence of enterprise robotics software is termed RDA (Robotic Desktop Automation). Together with RPA, RDA will help drive the market for enterprise robotic software towards $2.3bn in software and services expenditure in 2019 (with close to three-quarters tied to the services element of strategy, design, transformation and implementation of enterprise robotics). HfS’ new estimates are for the total enterprise robotics software and services market to surpass $4.3 billion by 2022 as a compound growth rate of 40%.

Example use-case: automating transfer of data from one system to another. RDA is essentially surface automation, where desktop screens (whether desktop-based, web-based, cloud-based) are “scraped”, scripted and re-programmed to create the automation of data across systems. A well-designed RDA solution can automate workflows on several levels, specifically: application layer; storage layer; OS layer and network layer. Workflow automation on these layers requires equally specific technologies but provides advantages of efficiency, reliability, performance and responsiveness. Much of this automation needs to be attended by humans as the automation is triggered by humans(humans pass tasks to bots), as data inputs are not always predictable or uniform, but adaptation of smart Machine Learning techniques can reduce the amount of human attendance over time and improve the intelligence of these automated processes. Similarly to RPA, RDA requires human intervention for judgment-intensive tasks and robust human governance and to make changes / improvements.

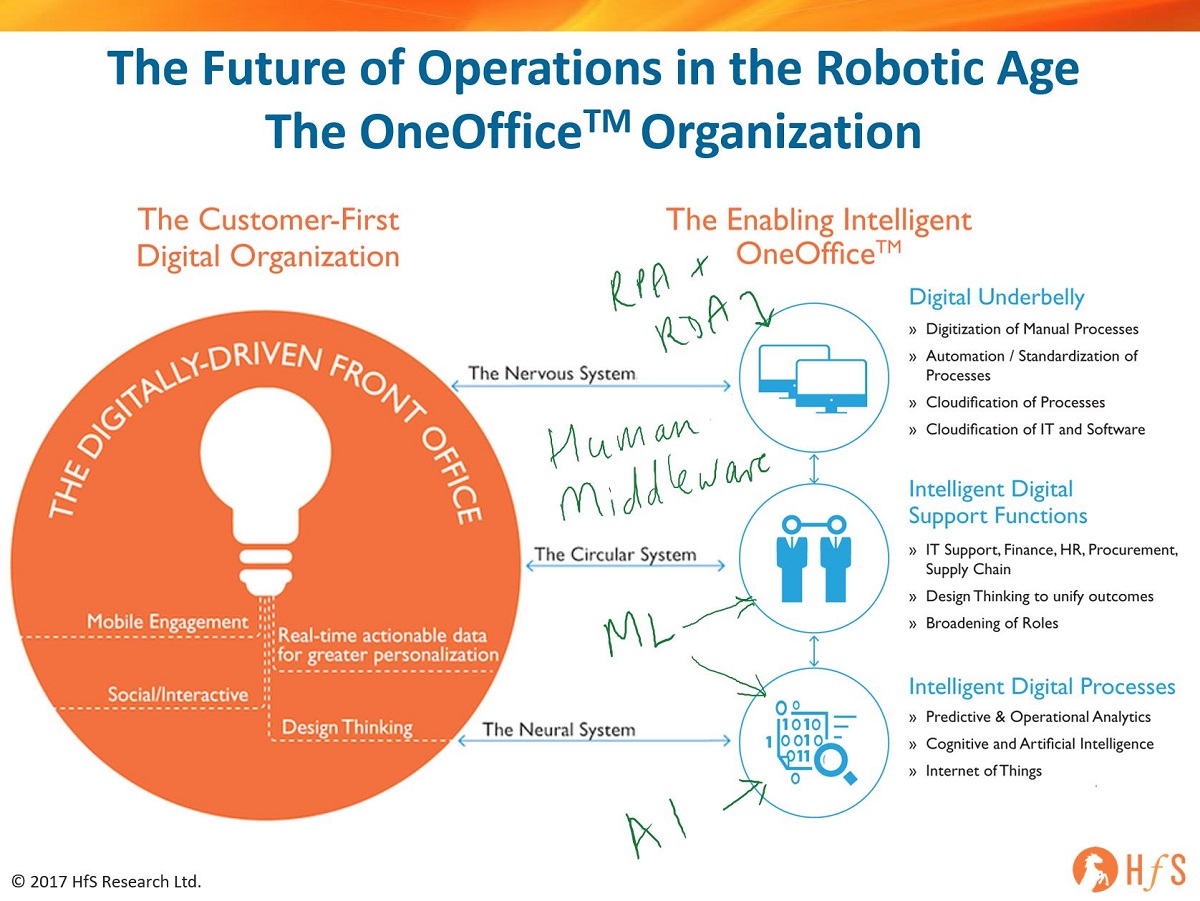

The Bottom-Line: Automation and AI have a significant part to play in engineering a touchless and intelligent OneOffice

However which way we spin “digital”, the name of the game is about enterprises responding to customer needs as and when they occur, and these customers are increasingly wanting to interact with companies without physical interaction. Moreover, the onus is moving to the most successful digital enterprises being able to anticipate the needs of their customers even before they occur, by accessing data outside of the enterprise across the supply chain, or economic and market data that can help predict changes in the market, or emerging offering that customers will want to purchase.

This means manual interventions must be eliminated, data sets converged and process chains broadened and digitized to cater for the customer. Hence, entire supply chains need to be designed to meet these outcomes and engage with all the stakeholders to service customers seamlessly and effectively. There is no silver bullet to achieve this, but there is emerging technology available to design processes faster, cheaper and smarter with desired outcomes in mind. The concept was pretty much the same with business process reengineering two+ decades ago, but the difference today is we have emerging tech available to do the real data engineering that is necessary: However, if these firms rest on their laurels, this market dominance will be short lived. Once the digital baseline is created, enterprises need to create more intelligent bots to perform more sophisticated tasks than repetitive data and process loops. Basic digital is about responding to clients as those needs occur, while true OneOffice is where enterprises need to anticipate customer needs before they happen (see below). This means having unattended and attended interactions with data sources both inside and outside of the enterprise, such as macroeconomic data, compliance issues, competitive intel, geopolitcal issues, supply chain issues etc.

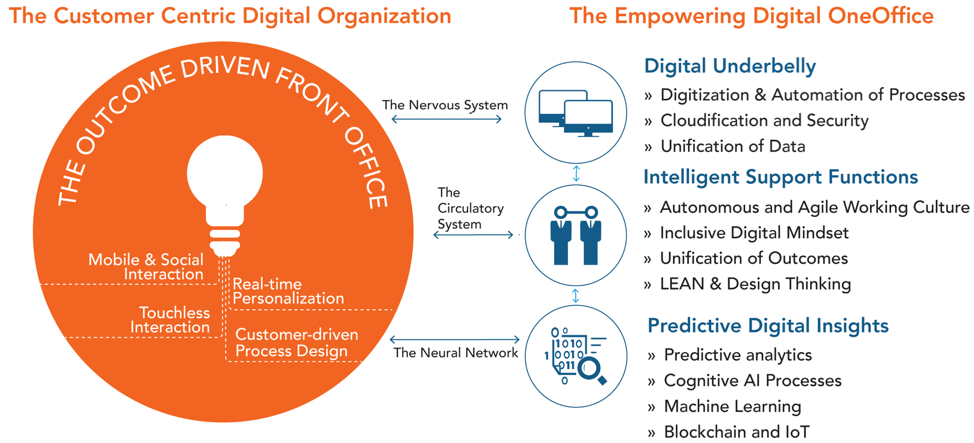

In short, every siloed dataset restricts the analytical insight that makes process owners strategic contributors to the business. You can’t create value – or transform a business operation – without converged, real-time data. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embracing the cloud in a way that enables genuine scalability and security for a digital organization. Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities. This is where RPA and RDA adds most value today… however, as more processes become digitized, the more value we can glean from cognitive applications that feed off data patterns to help orchestrate more intelligent, broader process chains that link the front to the back office. In our view, as these solutions mature, we’ll see a real convergence of analytics, RPA and cognitive solutions as intelligent data orchestration becomes the true lifeblood – and currency – for organizations.

Do take some time to read the HfS Trifecta to understand the real enmeshing of automation, analytics and AI.

The software giant and world’s premier system of record, SAP, was on an acquisition spree over the last two weeks. First it spent $8billion on the acquisition of Qualtrics, a User Experience (UX) software that helps to collect and analyze data for market research, customer satisfaction and loyalty, product and concept testing, employee evaluations and website feedback. And then it acquired Contextor, a small little-known France-based Robotic Process Automation (RPA) product to augment SAP Leonardo’s intelligent technologies portfolio.

It appears that SAP is starting to mix a heady cocktail that enables its systems of record with the triple-A trifecta (AI, Analytics, and RPA) and embedded UX capabilities. Tastes like the OneOffice?

Well, definitely for SAP mighty front office portfolio, but the huge disparity between the $8bn splurged on Qualtric and – whatever negligible sum was invested in Contextor – does not excite us that SAP is in anyway deadly serious about dominating the back-to-middle office automation space, which is critical to knit together disparate processes and systems.

What is the Digital OneOffice and why it matters?

The Digital OneOffice is where teams function autonomously across front, middle and back office functions to promote broader processes with real-time data flows that support rapid decision making. It’s where front, middle and back offices will cease to exist, as they will be, simply, OneOffice:

The OneOffice Framework is a guide to align the entire organization to driving a customer experience (CX) that gives them a competitive edge. This means breaking down the siloes between front, middle and back office so that information and data flows freely and enterprises are able to predict and cater to customer needs. OneOffice is realized when the needs and experiences of the customer are front and center to the entirety of business operations. This means enabling automated data flows between the customer interface, your customer-facing staff and operations staff in order to create common goals and outcomes across the organization. Hence the addition of Qualtrics has terrific potential to bridge critical gaps between customers and employees, and effective RPA provides a real gateway to digitize processes and create a gateway to broader AI possibilities.

Qualtrics and Contextor are attempts to plug SAP’s solution gaps in the OneOffice vision

The reason behind the success of Qualtrics (and the driver for the 20X PSR!) is that Qualtrics-driven UX is not about just a fancy UI. Qualtrics enables SAP to offer solutions that combine front and back-office data. SAP is already a leader in managing organizational transactional data but lacked the capability to understand its implications on customer satisfaction, loyalty, and experience. With Qualtrics this is now a distinct possibility.

Contextor’s addition is focused on providing the missing ‘A’ in SAP’s Triple-A Trifecta capabilities. HFS believes the “Holy Trinity” of service delivery is at the intersection of the Automation, Analytics, and AI or the Triple-A Trifecta. SAP Leonardo already has a portfolio of technologies across Machine Learning, Analytics, IoT and blockchain but lacked the basic automation capabilities that Contextor now provides. Intelligent RPA capabilities are scheduled for inclusion into SAP S/4HANA in the first half of 2019, with other SAP applications to follow.

SAP will still need to justify why embedded capabilities will be better than standalone products

Automation and UX are hot areas with multiple robust Commercially-Off-The-Shelf (COTS) solutions that can integrate well with SAP environments. SAP itself is heavily invested (and rightly so) in building its own ecosystem with the SAP App Center where third-party solution providers can offer solutions that work seamlessly with SAP environments. In today’s world, it is unclear how much more an embedded functionality is worth compared to an ecosystem approach. SAP will need to justify why and how the acquired capabilities will offer a unique or better value proposition than standalone products.

Qualtrics brings to the table a differentiated value proposition, especially when combined with SAP’s existing operational data and transaction processing market share. But only in theory. Integrated value proposition demonstrated through tangible use cases will be the real proof. The cultural mismatch between SAP and Qualtrics (as pointed out by Dennis Howlett here) will make it even tougher.

When it comes to RPA, the software giants have been largely MIA. Before SAP’s Contextor acquisition, Pega is potentially the only other software player that recognized the power of RPA with its acquisition of Openspan RPA in 2016. It initially embedded bots into its BPM suite of applications and now gives away unlimited robots with its Pega Platform.

Contextor itself is a very small player in the fast-growing RPA product market dominated by Automation Anywhere, Blue Prism, and UiPath. Power users of Contextor shared with HFS that it is a complex-to-use tool, requires coding experience, and has limited AI hooks. SAP opted not to acquire any of the big three RPA players (perish the thought at their hefty price tags!) and will possibly get basic RPA capabilities with Contextor. However, it will still need to convince clients about the advantages of using embedded RPA capabilities because the stand-alone RPA products can offer the same (perhaps even better). What’s so compelling about Contextor-driven SAP that requires a course correction from clients who are already on their intelligent automation journey? As with Pega, perhaps the answer lies in bundles bots as give aways.

The other open question around Contextor is how SAP decides to position it internally and with clients. Consider the system integration space. APIs are real-time and resilient but RPA-driven integrations are brittle. IT purists love APIs but businesses don’t really care as long as it works. In reality, enterprises need both options as an “API-everything” world is impractical or at least not terribly timely. But will SAP look at RPA as a viable long-term option for automation or just as a temporary “duct-tape” till it gets the more robust (and expensive) functionality developed within the core application?

Bottom-line: SAP’s acquisitions of Qualtrics and Contextor demonstrate that UX is not limited to the front office, but we question the ability to drive OneOffice integration with a paltry investment in automation

Qualtrics enables the integration of back-office and front-office data while Contextor will enable automation from front to back within the SAP environment and outside. This is the HFS OneOffice vision where organizational silos start to converge to focus on real-time customer and employee engagement.

However, the deep process requirements on the client side that are critical to find success with RPA, coupled with strong services partnerships needed to provide the technical expertise, reskilling and change management do not bode well for SAP to find much (if any) success with RPA. SAP has not proven particularly successful supporting complex process transformation needs of clients outside of the traditional SAP product templates (its BPO alignment division was quietly wound down several years ago) and the services partnerships that have been developed by Automation Anywhere, Blue Prism and UIPath are lightyears ahead of anything Contextor has forged (and some leading consultancies in the space had never even heard of the French firm). While it is understandable that SAP did not want to invest multiple-billions in a leading RPA solution, we believe it could have targeted a more established middle tier solution, such as Redwood (which is specialized with the SAP template), Softomotive, Kofax or Kryon.

While it is easy to criticize the Contextor investment as lacking real teeth, at least is it a much larger step forward to bring “big iron” ERP into the robotic process automation age, when you compare it with the complete void of RPA investments yet to be seen from the likes of the SaaS giants Oracle, Salesforce, Workday and the AI platform movers Microsoft, Amazon, IBM and Alibaba. Now what to expect to see next as this industry stumbles into consolidation….