The final countdown is on for the end-of-year reality check leadership extravaganza, with HFS’ New York FORA Summit where we measure the genuine pace at which we’re Hurtling into the Hyper-Connected Economy.

We’ve been living through a journey of change agents promising to shake the very foundations of how we do business, how we engage with our customers, our partners and our employees; how we structure our business operations; how we build and source our IT backbones; how we balance our portfolios of legacy systems with super-connected platforms; how we explore the potpourri of analytics, automation and AI solutions to make us smart enough to keep our businesses ahead of the competition, where the front office can anticipate the needs of our customers, with operations geared and finely-tuned to deliver on those needs.

So time to meet one of our keynote speakers, Kate O’Neill, who will be unveiling her new book, “Tech Humanist” during her speech “How to Be Successful with Human-Centric Data and Technology”…

Phil Fersht, CEO and Chief Analyst, HFS Research: Kate, really happy to have you speak at FORA New York this December. So, can you tell us about what you will cover in your keynote, and maybe a little bit about the new book? What is really driving your thinking these days, in terms of where we’re going, and what’s changed in the last couple of years?

Kate O’Neill: Phil, thanks for having me, I am really excited about speaking at the Summit so I can share some insights from my new book, Tech Humanist, and when I last spoke last time I had just published my earlier work, Pixels in Place. Then it was all about integrated, connected, smart experiences, and the data that’s shared between the physical layer and the digital layer. I talked about how humans are the connective tissue between those layers of the world, and how that implies that we need to be respectful of that data, and protective of it, and mindful about the kinds of experiences that we’re creating when we use human data to make our businesses more successful, which we certainly can do, and there’s a lot of opportunity for that.

Having spoken on the topic for a couple of years and evolving the work and research that I was doing around that, it became clearer that this was part of a bigger story and that there’s more to say about the work of creating meaningful experiences around all kinds of emerging technologies, automation, artificial intelligence, wearables, and the Internet of Things for example. This whole, broad spectrum of the full complement of emerging technologies, that are mostly driven by data, and that data is human data. So, it becomes really important to just look at that whole ecosystem, in a holistic way, and try to understand what to do with that data, to make our businesses as successful as they can be, within the construct of creating more meaningful experiences for humans, and being respectful about the data that we’re using, in that case.

Phil: And in terms of this new wave of noise, Kate, it seems that we have been on a four-year cycle of hype, which initially was around digital disruption. Then people realized how and why they were going to be disrupted, so they got a handle on that. Now there’s been a lot of fairly advanced thinking around AI, and how that’s shifting the paradigm further and it almost feels like we’re almost coming back to reality and really figuring out what this truly means for our businesses, our careers and our personal lives. Do you think 2019 will be the year where we’ll get into some real conversations? Or do you think we’ll keep seeing this proliferation of noise, hype, and fairly outlandish theory? What do you think’s going to happen?

Kate:[Laughter] I think it’s probably a little bit of both, Phil. But I think you’re right, that there is this cycle, where some of the people, who were having some of the earlier conversations in years past, are now starting to see fruits of proofs of concept and early experimentation, that’s leading to much more coherent insights, about what these things look like in practice.

Our knowledge of RPA and machine learning, for example, has matured and I think there still will be plenty of theory and speculation, but I think it’s going to be important to have that kind of theoretical conversation because it will advance the way we’re positioning ideas. I think it’s going to be interesting to see that come head to head with the realities of practice, and the way that things have been experimented with.

When I talk to people casually about how a lot of my work is around robots and automation, they seem to be thinking about some sort of far-off future, when in reality, millions of homes have Roomba and Alexa already in them. We’re already looking at the reality of types of robotics and automation in our homes, and certainly in workplaces, too. We’re used to the idea of self-serve kiosks, and self-checkout type of automation, so I think we need to have a much more nuanced conversation about what that looks like, and what it means for the future types of work that are available for humans, and how we coexist in to the next stages of automation and robots in the workplace.

Phil: One of the things, Kate, which I find really exciting is developments in things like explainable AI, where we’re working much harder with business users to design the AI, so it’s something that is driven by people, to develop business context, to really be something that we control, and we design, versus this, kind of, out-there theory, that AI’s just going to take everything over, everything’s going to be self-remediating. So, as you look at how more business-focused people are being pulled in to technology, for example, RPA being like a gateway drug to AI, how do you see this evolving? Do you see more business-centric people being pulled in to the design of technology equation here? Or do you think it’s going to be a fairly different scenario?

Kate: I don’t see one pattern playing out. In the work I’ve been doing over the last year or two, speaking and advising with companies around this, and kind of how I see that playing out as a trajectory, there seem to be a few different ways that companies are embracing how to have this conversation. Some of it is in the boardrooms and it’s about getting behind strategy first and having a purpose-centric discussion before an organization can really meaningfully model itself in data, and deploy accelerating technologies. But I think there’s an equally valid approach, in some organizations, due to culture, and due to constraints, and whatever else, that’s more tech-driven, that comes from within the IT or operations departments. These departments look at what the capabilities and capacities are, and then accelerate around those to gain some momentum, and be able to talk about some wins before engaging the rest of the executive team, or the rest of the leadership.

Within results-driven companies, however, when there is no immediate ROI from experimenting with RPA or AI are people going to walk away from it? If so, then it might be easiest to have it be just an experimentation house within the IT department. But if it’s something that the overall company leadership sees as a clear direction for the company, and knows that it needs to be embraced, no matter what, “We need to figure this out long-term,” then I think it can easily be driven at that central executive level.

Phil: So, one of the things which we’ll be talking a bit about next month, in New York, is the fact that we’ve really come through three decades of companies pretty much doing things the same way for 30 years, but just faster, cheaper, better, moving data around the organization more aggressively, and digitizing processes. But the fundamental problem has been, companies, particularly in the Global 2000, not changing how they run processes and run departments. So, HR has always done things one way, procurement one way, finance one way, for example. Do you feel we’re going to get to a point where companies are going to fundamentally redesign roles and responsibilities, and how they operate? Or do you think that’s happening more at the small to medium business level, where these businesses have native automation, have native AI, and it’s a different rule, almost, for the kind of dinosaur, traditional organizations? How do you see that evolving?

Kate: I think, Phil, there’s a sort of a compliment there, as well. You can certainly see where small to mid-sized companies have sort of an agility advantage, in being able to adapt their organization easily around emerging technologies, but obviously, on the larger enterprise side, you have scale, and you have, if you can get the alignment, organizationally, and operationally, to deploy kind of a roadmap approach, then I think you can really use those assets, and use your scale, to make that work. So, I think the key does seem to be, I come back to this idea of strategic purpose, and the advantage of purpose, I feel, in this context, is that purpose is what really helps people be motivated, and helps keep humans on the right track, and it’s also this way of distilling an idea, to concrete operational logistics that’s really suitable for machines.

So, if you can get to a point where you’re articulating well what it is your business exists to do and is trying to do at scale, in that sense of a strategic purpose, I believe that that is one of the ways in which we actually get to aligning the culture, aligning the organization, aligning even things like operational facets, like meeting structures, and hierarchy, and operational roles, and things like that. So there’s just so many nuances to the reality of that, that I think it will play out in different ways, for the different sizes of organizations, but also the different “techcentricities” of the organization, how digital the organization was in its DNA to begin with, but I think it’s going to take not, maybe, a one-size-fits-all approach, to make that work.

Phil: Finally, Kate, can you tell our readers where they can purchase your book, and give a taste of what they can expect to learn?

Kate: Yes, sure. So, you can find Tech Humanist, on Amazon, and Barnes and Noble. The subtitle of Tech Humanist is How You Can Make Technology Better for Business and Better for Humans and the idea there is about alignment, as we were just been talking about. It’s about the idea that, if technology is fundamentally built around improving on human experience, if it is using human data, if it is about constructing this environment that humans operate within, then it’s an opportunity for a business too. Businesses can utilise those hooks if you will, to create more meaningful, memorable experiences, that help scale the business in a successful way, and also create the most opportunity for humans to thrive, in an environment where it’s going to be increasingly machine-driven. So, I think we’re looking at a reality where a lot of our world is increasingly driven by machines and automation, and I think we just need to think about how that’s going to play out, what we want it to look and feel like, and how to make business successful within that context, while also helping humanity thrive.

Phil: Excellent Kate! We can’t wait to see you again next month and host you in front of a fantastic audience of people, in a truly unvarnished conversation

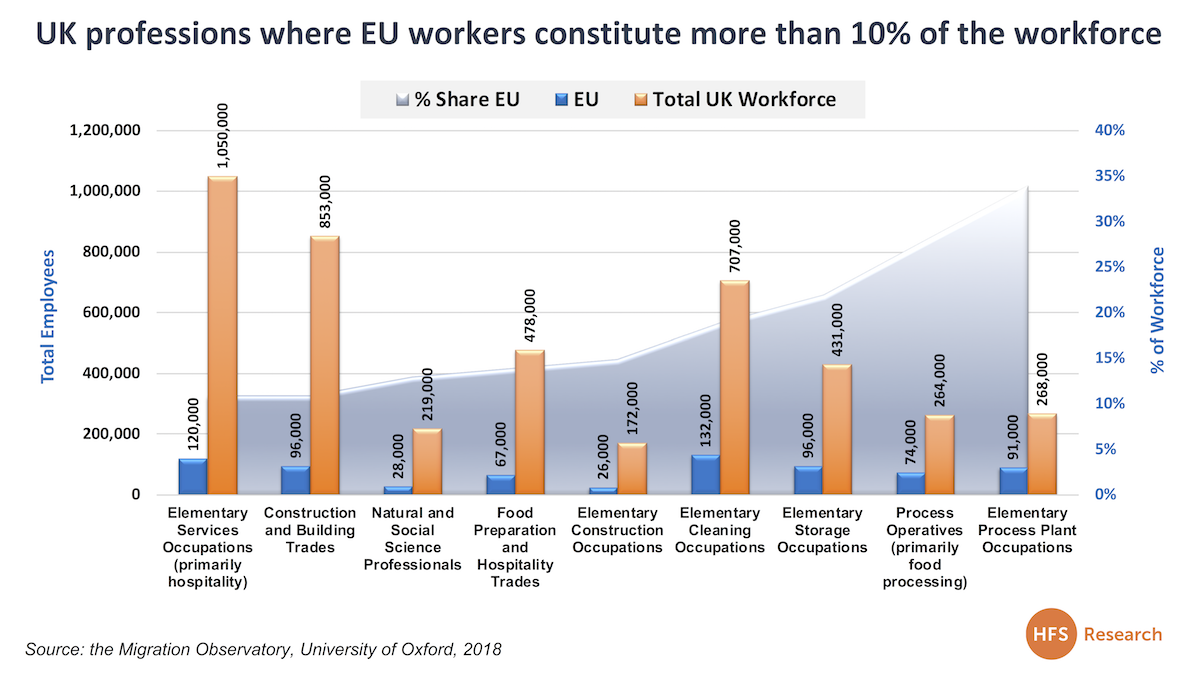

However which way you analyze all the economic indicators, and whatever your opinion may be regarding Britain’s relationship with the European Union (EU), removing the movement of EU labour into the UK will create a perilous shortage of labour, particularly for low-to-mid skilled professions. If anything, removing the worker base at the lower end of the skills spectrum is worse than at the high-end for the simple reason it’s much harder to entice people into jobs that may be low-paid, unattractive, and – in many cases – require hard graft for low wages. How are our hotels and restaurants going to find 120,000 staff willing to work for the minimum wage, our food factories to renew a third of their workforces to prepare our food, and our cleaning firms going to backfill 132,000 people willing to mop and scrub for a living? The answer is sadly obvious – many of our industries will be under real threat of implosion because they simply cannot access the people they need to keep them functioning.

And without a thriving working class, the economy will suffer due to less money being spent; our businesses will suffer because of rising hotel costs; our entire society will suffer because of rising food costs; and our commercial and domestic real estate markets will struggle to complete projects. While professions like education and hi-tech can source talent from elsewhere (and are less reliant on EU people imports), it’s those industries that form the underbelly of the economy which will really suffer. Forget “trickle down economics” Brexit will cause a “trickle up” effect that will be hazardous for the British economy and its mid-long term sustainability. In the short-term, many EU workers in the UK should be able to stay on, but the reliable conveyor belt of workers prepared to roll their sleeves up and support our entire economic underbelly will be permanently halted, and the availability of workers will get progressively worse – and much more expensive with this shrinking supply of people.

So, without further ado, let’s dive into the fuller implications of this seemingly masochistic self-flagellation known as “Brexit”…

Nice try, Theresa, but even your dancing can’t make us forget about the increasingly no-win Brexit scenario

For our fellow Britons, these past few weeks have been a refreshing break from the normal Brexit debates as we became distracted instead by our premier literally dancing for trade agreements. Trade agreements that, even for the most dismally poor mathematicians, don’t stack up when compared to the one we’ll soon be leaving.

Brexit has been a topic of heated debate for years now – and I’m sure we all have that friend or relative you daren’t mention Brexit in front of or risk a lecture based on unfounded inferences and sketchy sources. In many ways, it’s these long-winded and often inebriated debates that are the problem – we’re close to the day we sever ties with Europe and reclaim some sort of democratic freedom that only a nation with several unelected heads of state can find any ironic sense in. And yet we’re no closer to understanding what Brexit means – even if we had a clear picture of how awful it will be at least that’s something we can prepare for. Instead of this mind-numbingly irritating narrative from British politicians of ‘Don’t worry, it’ll all work out in the end.’ Well, unfortunately, we’re not an eight-year-old child looking for reassurance from our grandmother that the mean kids at school will be our friends eventually. We need proper answers. Or we’re screwed. Even more screwed than if we voted to, say, leave one of the biggest trade deals in the world.

The lack of decisiveness and the longer this goes on, the more of a no-win scenario this becomes. The fact of the matter is that regardless of your pollical leaning the longer this is drawn out, the less likely we are to see any benefits or have adequate protection from the risks – with neither side of the debate getting what they want. Much like Starfleet academy trainees in the Kobayashi Maru simulation (or a classic Catch-22 for the more cultural amongst us,) Ms. May is in a no-win situation and, as time presses on, will be far less likely to pull off a Captain Kirk-like miracle. Let’s break down the Hobson’s choice of our leadership face.

Britain is the destination for 32% of Europe’s Science, Technology, Engineering and Mathematics (STEM) graduates – but for how long?

Imagine this, you’re a business executive desperate to bring in some decent talent to help make your business successful and competitive. You offer a decent salary, good job prospects and you’re in a great location. But then your boss’s boss puts a cap on the number of talented people you can bring in, and as a cherry on top, talks loudly about creating a ‘hostile atmosphere’ for talented people. As if by magic, the applications to work for your team just dry up.

Now let’s zoom out to the national picture and that’s basically what happened. The National Health Service (NHS) is reporting one of the biggest staffing crisis in its history, and businesses all over the country are struggling to get the right people in to help them move forward.

The key point is that Britain has grown as a technology titan not through the efforts of its native population alone. It’s access to an enormous pool of talented professionals and bright academics that help drive national economic growth. A report from the European Commission (we even rely on Europe for decent data) highlights a shortfall in domestic British STEM graduates based on the demands of the labour market which, coupled with the insight that the destination of 32% of EU foreign STEM students makes us wonder what the future holds.

We’re not economic experts but we get IT and Digital – in both of these areas there continues to be a giant war for talent. And that was before we went all Brexity and Hostile. Now, why should the bright young developers and consultants from across the globe come to the UK to work? It was part of a giant labour market which made it attractive to the ambitious and talented, but may not be as attractive after brexit. Honestly, almost everyone we’re speaking to now can see this car crash a mile off. Business leaders are looking to move operations to EU nations to soften the blow, and even UK professionals are pouring over their family tree to find a potential route to European citizenship (That’s if Farage and his fellow Brexiteers don’t beat them to it…it’s so annoying when these foreigners put caps on citizenship…).

The pound devaluation versus high labour demand paradox

But it’s not all bad news – the crash of ol’ reliable British Sterling could make the UK a cheap enough nearshore location that some enterprises could be convinced to stay or even broaden their operations. At least in the short-term. You see, a weak pound is one thing, but if the talent crisis gets any worse, paradoxically, the cost of labour will increase. As businesses battle for talent, one of the only weapons in their arsenal is to up salaries – while real-term wage increases may not be on the cards across the board, for good digital talent, it could send salaries rocketing, negating any benefit of currency exchange. So, even when Brexit delivers the goods…on closer inspection, they’re not the goods we want.

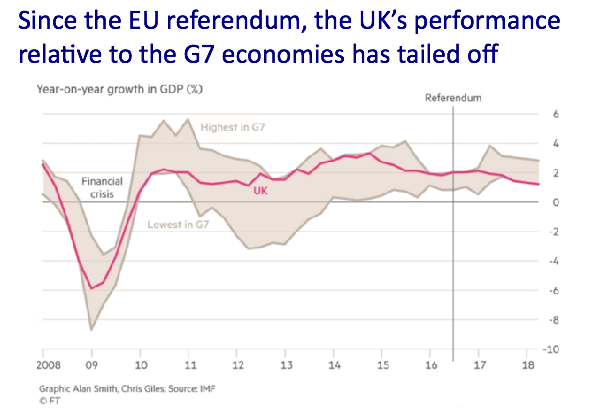

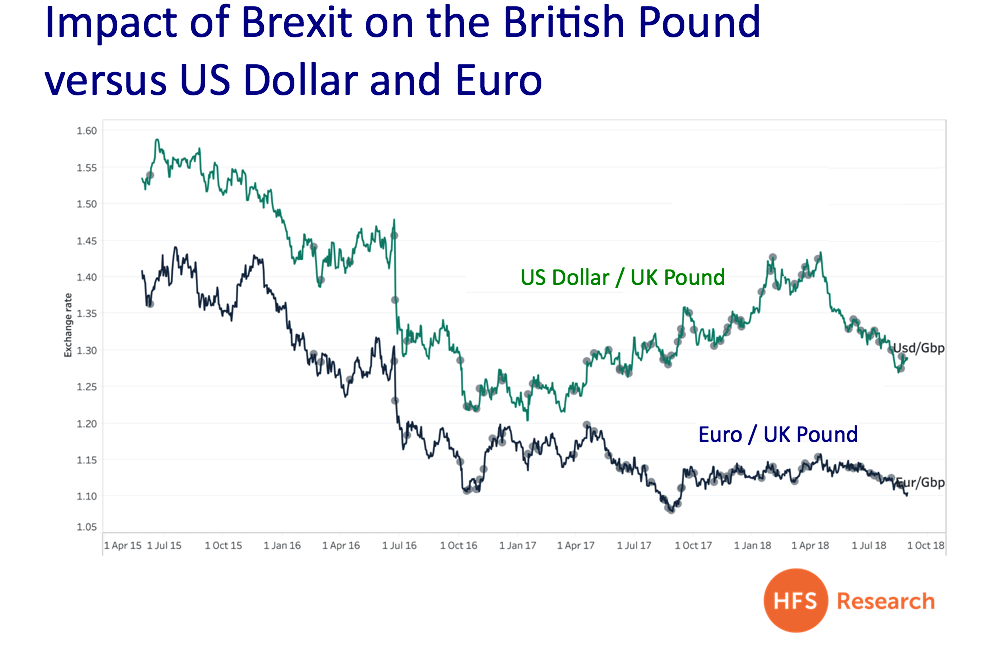

But now we need to hang a shadow of doubt over this whole business. In exhibit 1, we can see the major impact of the 2008 financial crisis and the rebound of the UK and the G7 – with the UK topping out the highest growth for several years. But unsurprisingly, this growth is lacking enthusiasm since the Brexit referendum. At the same time, the value of the pound nose-dived – we can see the effects in exhibit 2. So even with the international able to get a relative bargain from UK goods and services, the benefits to the economy are still unclear several years on.

What does this mean for the services outsourcing industry? Well, the dip in the exchange rates could bite deep in some major outsourcing destinations. The drop in the value of the pound has, effectively increased the costs of outsourcing engagements in India, for example. So, enterprises may now be keener to insource or hold out on major outsourcing deals until the pound rallies – if it ever does.

It’s not clear what the net impact will be on nearshore engagements from within the EU. On the one hand, it will potentially be harder to contract and provide services across these new borders. But on the other, the skills shortages may make it a more attractive option. It will be interesting to see if the government in charge discourages this with taxation or regulation. Particularly given a large part of the reason behind Brexit was free movement and its impact on jobs/services.

Now this may seem like good news for the British economy, more domestic investment, right? But actually, the opposite may be the case. British businesses – avoiding buying in talent and tech will struggle to find the same scale domestically. And holding out on an outsourcing deal means just that, the engagement is paused – so no investment or productivity gains. Ultimately, this dynamic is less likely to make UK goods and services more competitive as exchange rates favour exports, but paradoxically could make enterprises less competitive.

The sensible multinationals will be hedging by stocking up on foreign currencies, and major exchange fluctuations can come ago relatively quickly. But several years of stayed business investment could be disastrous.

Uncertainty leaves business leaders, well, uncertain – and that could cripple business investment

Enterprises are already grappling with tough market conditions compounded by the moving feast that is digital transformation. British enterprises and their international partners, suppliers, and customers now have a whole fresh pile of uncertainty dolloped on them. National enterprises, while no doubt concerned, have to invest in their operations to some extent. But international businesses are holding back, and with good reasons; why invest in an area riven with uncertainty when there are much safer bets to divert resources to.

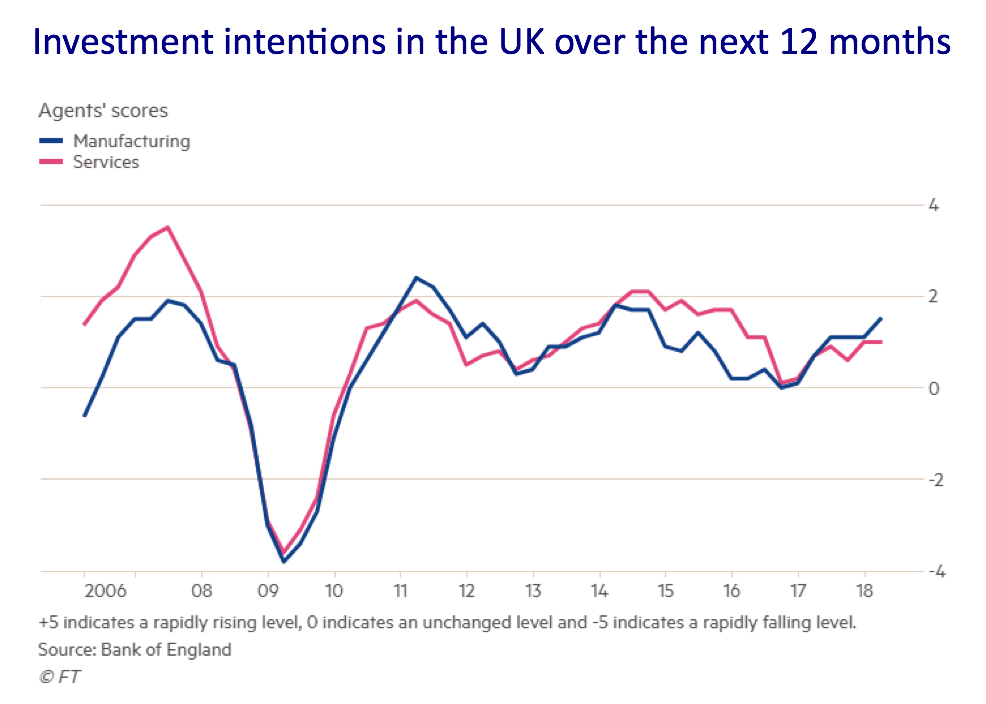

But even a recent Financial Times article charts the disparity between anecdotes from enterprise leaders advising they are holding back on investment and the data. While there have been some dips, overall investment intentions have remained relatively stable (see exhibit below). But this seems to be more down to enterprises splurging on spending after a period of adopting a ‘wait and see’ policy between the financial crisis and the referendum. The next big question is, when considering the points made earlier in this blog, is this trend likely to continue – particularly when a no-deal Brexit is now on the cards? The odds don’t look great.

Contract lawyers and consultants could be the only winners as partnerships and contracts will need to be withdrawn

The dependencies of shifts in regulation, jurisdiction, and legislation are far from clear. But if there’s one thing we can be sure of, there will be a huge need to redraw the terms of existing contracts and agreements – the trouble is we don’t know and probably won’t know for some time. A no-deal Brexit could see enterprises and providers forced to go through the small print on almost every document they have. And while bureaucracy may sound like the least of our worries, the time and resource drain of activity of this scale will bite hard. Trust us. Whether that’s sucking resources from value-add projects or the cost of hiring experts who can actually understand what’s going on.

Multiple Choice Brexit Fallacy

The biggest fallacy put about by all sides of the debate in the UK about Brexit is there were lots of options for how the UK could leave the EU. Without anyone asking the other side of the negotiation the red lines. The hard Brexit side maintains that there is some beautiful nirvana that will suit their needs and be accepted by Europe – the “they need us more than we need them” argument. This is dangerous and is one of the things that probably confused the British people the most. The EU can (and always were going to) play hardball given what they have to lose. They were never going to allow even the appearance that the UK got all the benefits of the EU without paying and being subject to some of its rules. The equivalent of being a guest at a Gym expecting to pay less per diem and not getting kicked out for pissing in the pool.

The choice was always remain, deal, or no-deal. With the deal Brexit largely dictated by the other 27 EU countries,

It would be convenient to believe that control shifted to European negotiators over the past 6 months with May’s weaknesses revealed etc. but the truth is more that the European position has been fairly static, and the EU was always going to dictate the deal that is right for the rest of the EU.

With our prediction hat on we can only assume now that the EU will set out its position on the remaining elements of the deal. There may be a little wiggle room, but the deal position will be dictated by Europe and will most probably be like being in the EU but without any say. Which will annoy both sides of the debate.

So, we really have a no-win situation and little hope of a Kirk-like figure able to reprogram the scenario so that either side of the Brexit debate will be happy. Unless of course, remain voters will be happy with the likely removal of influence in the EU and some additional bureaucracy and Brexiteers with the superficial victory of being out of the EU in name only. But hey it will mean we won’t have MEPs, so Farage et al. will lose some of his platform and influence. Which is, at the very least, a minor victory for all of us who have lived through this sordid ordeal.

Bottom-Line: Unless we get our act together soon, anything that made Britain a competitive business location will be long gone

Ultimately, in a global economy, the only way a nation can thrive is by becoming a competitive destination for enterprises. Somewhere where they can find the regulatory environment and talent pool that will help their business thrive. All of this is what made Britain a great place to do business – a nation of talented business professionals conveniently situated between Europe and the U.S. In many ways, Brexit needn’t have been Britain’s undoing, but now as we stumble around in the dark with the rest of the world watching, we have little hope of reclaiming our legacy as the centre of global commerce.

The issue we now face is the no-win scenario – the “Brexit in name only” situation proposed by the government can only be weakened further by the negotiations in play. As we saw the other week the EU are prepared to play hardball. The other choice being no deal – which is as equally

But it’s not all bad news, here are some of the many (fictional) benefits we could see from Brexit

Decline in national obesity: The government has been worried about an obesity health crisis for some time. So, it’s probably good news that Britain’s food security is at major risk due to what we can only imagine is an intentional mismanagement of logistics, supply, and haulage agreements with the EU. Which happens to be where we get most of the things we need to sustain our soon-to-be thinner selves.

British cars will be nice and cheap: Well, cost is relative, and foreign cars will be extortionately pricey if all of these wonderful default tariffs set in. Maybe it’s time to bring back some of the good old-fashioned manufacturers. DeLorean anyone?

Apothecaries will liven up the high street: With an expected staffing crisis and pharmaceuticals struggling to make their way into the UK, we might see a return of Apothecaries to the high street. I know what you’re thinking, modern medicine just doesn’t compare to stinging nettle soup and a course of leeches, but it’s probably all we’ll have.

We’ll have plenty of leisure time: With several major employers heading to the greener European mainland, the average leisure time of the British citizen could go through the roof. Unfortunately, we may be stuck sitting around a fire listening to elderly relatives tell us stories of the time when there was electricity.

We can all feel better about ourselves next time we are coaxed onto a dance floor at some boozy corporate gala dinner:

Am excited to have HFS’ Saurabh Gupta lead our session on de-mystifying Blockchain at our December NY Summit… but let’s put this all into context and learn about the Hyper-Connected economy and the need to manage these merging technologies in a business context, where integrating them at scale is really the same of the game.

At HFS, we have been increasingly concerned about the plethora of business models and articles bombarding us on social media, media websites, research and consulting firms’ websites, many of which are seemingly replicating similar terminologies and concepts. And this trend seems to be worsening. For example, we highlighted the recent direct usage of an HFS headline to drive traffic to a well-known media website. Just blatant!

We also have been observing the dizzying array of ‘intelligent automation maturity models’, especially being the first analyst to develop them, starting in 2014, refining in 2016, 2017 and this year. We recently had our attention drawn to the “Four Stages of Intelligent Automation Maturity” by Avasant, that initially gave us cause for concern, but when we communicated with them this week, they shared a presentation recording from earlier this year describing their model in much more detail, assuring us their “phases to maturity” are actually quite different from the HFS viewpoint. While there are always many shared common best practices when investing in a solution such as RPA, Avasant convinced us they had developed their own methodology and approach to automation maturity. We apologize to Avasant for making this assertion that it closely resembles the 2018 HFS Intelligent Automation Maturity Model. You can read a really decent interview with CEO Kevin Parikh here, espousing his views on the future of the consulting business.

The Bottom-line: We have to focus on our own concepts and ideas and avoid the regurgitation game

In general it is getting harder and harder to differentiate experts across the industry as many are very adept at hiring marketing resources to create whatever spin they feel they need to win business, while others simply extract another firm’s creations as their own. With the daily deluge of terminology being thrown at us, we just need to try harder than ever to provide our own original thought leadership and insight, as any smart enterprise today sees straight through the glossy veneer.

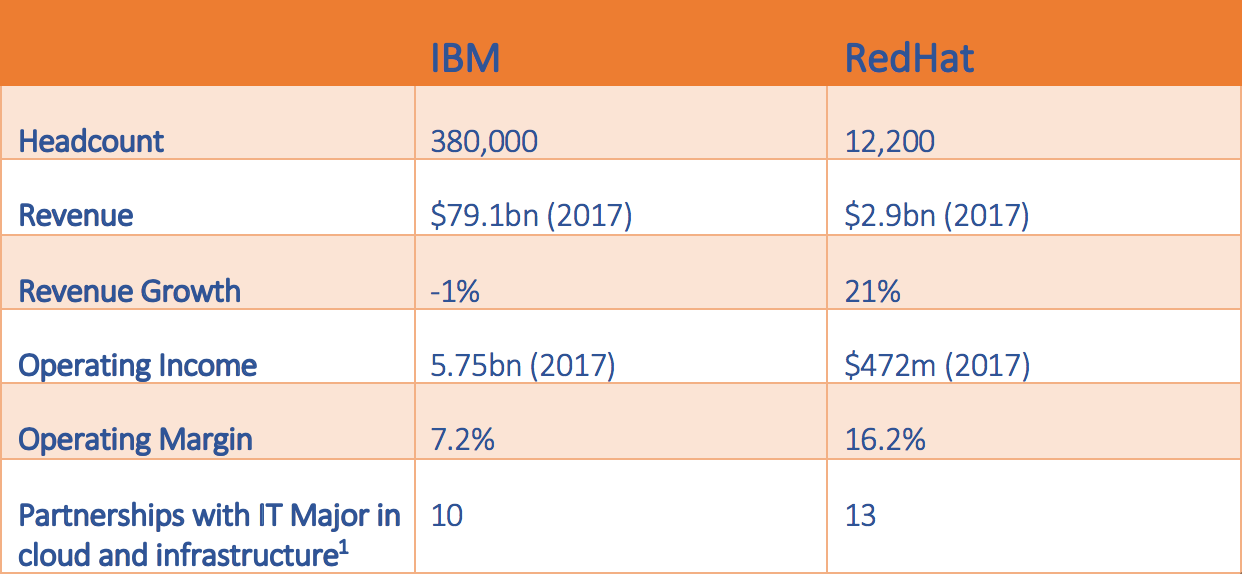

IBM’s ingestion of RedHat, the third largest IT purchase in history, is all about Open Source and dominating cloud transformations.

Commentators are already pitching this deal as long-awaited reinforcements to the trench-warfare of the cloud wars. But in reality, we need to look much deeper to understand what persuaded IBM to part with such an exorbitant sum of money for Open Source giant RedHat.

Did we read that right? $34bn? – And what will happen to renegade RedHat?

Even for budding venture capitalists, the princely sum of $34bn is more than enough to make your eyes water – especially when it’s hurled at a firm with annual revenues of just $2.9bn and headcount that will be just a drop in the Big Blue Ocean. So there must be more to IBM’s thinking than a quick financial return – it’s either a play to kick the other hyperscale players out of play, or a push to get the upper hand in the increasingly valuable Open Source sharing economy.

If we dig into the financials, it’s clear that RedHat is a profitable firm with a strong track-record in the space – describing itself as the leader of Open Source capability. In many ways RedHat has been a champion firm in the growing enterprise adoption of Open Source – a service line that has moved a long way since its one-man-band and hobbyist background. Open Source is now big money, and all of the major providers want a piece of the action. In exhibit 1, we can see, alongside the financial information, a look at the number of partnerships both IBM and RedHat have among the major IT Services providers.

It should come as no major surprise that RedHat has a larger pool of big providers in its partnership ecosystem – IBM, while having a relationship with many has always struggled to balance its role as a major competitor and a partner. This challenge is likely to impact RedHat now, which has been able to play neutrality to build a strong partner network – some of which are likely to be sheepish now they’re an arm of rival IBM. However, this risk has been addressed by a clause in the agreement which pushes for RedHat to continue enjoying relative independence.

James M. Whitehurst, CEO of RedHat advised after the announcement that “Importantly, Red Hat is still Red Hat. When the transaction closes…we will be a distinct unit within IBM, and I will report directly to IBM CEO GinniRometty. Our unwavering commitment to open source innovation remains unchanged,” and went on to argue that “the independence IBM has committed to will allow Red Hat to continue building the broad ecosystem that enables customer choice and has been integral to open source’s success in the enterprise.” However, partners and clients may question how much of this lies in a carefully orchestrated marketing narrative, and how long IBM will hold true to its word given experiences with previous acquisitions. And the open source community can be quite unforgiving of commercial entities moving from benefactor to owner of IP – unless they tread carefully, IBM and RedHat may find themselves alone on the playground while all of the other open source kids play football, all because they held on to the ball for too long while they were in goal.

Even so, the formal press announcement from IBM and RedHat should settle some nerves – it advises that “upon closing of the acquisition, Red Hat will join IBM’s Hybrid Cloud team as a distinct unit, preserving the independence and neutrality of Red Hat’s open source development heritage and commitment, current product portfolio and go-to-market strategy, and unique development culture.”

So that’s all we know at this stage about how IBM plans to slot in $34bn worth of company in its leviathan and, frankly, unforgivingly complex structure. Let’s just hope RedHat’s reputation in the open source community isn’t tarnished by selling out to a major player. Which brings us to our next point…

Forget about the cloud, this is all about open source

One thing should be made clear, the narrative a lot of pundits are pushing is that this is all about forging fresh weapons to take on the big cloud players – AWS, Azure, and Google. If it is, that’s a woefully misguided objective. All of the major hyperscale firms have consistently built up assets and developed innovative cloud layers to meet the insatiable demands of the modern enterprise. RedHat – despite its credentials in Linux and Virtualization – isn’t going to give any of the big three much pause for thought. If IBM was genuinely eyeing up targets to give them a leg-up in the cloud wars, RedHat wouldn’t be at the top of the list. And although the marketing collateral from both firms is already championing the value of the tie-up to put a fresh spin on multi-cloud – this is far from fresh thinking in a market already packed with services and solutions.

So what it’s really about, is cornering the growing appetite for Open Source in the enterprise IT services market. As Paul Cormier, President of Product and Technologies at RedHat recently announced “Today is a banner day for open source. The largest software transaction in history and it’s an open source company. Let that sink in for a minute. We just made history.”

IBM and many of its rivals have been scrambling around to win plaudits for the most engaged or best contributor to a raft of open source projects, and with them the attraction of key talent in a competitive labor pool. IBM is no stranger to open source, it’s one of the original Linux Foundation contributors – but many of its rivals are also heavily engaged – Google, for example, is rated as one of the most generous contributors to GitHub. What this acquisition is really about is cornering off a large pool of talent, capability, and IP in the Open Source space – and with it core cloud capabilities across containerization, viurtualisation and a raft of other capabilities that are soon to be the essential building blocks of the new enterprise IT.

Bottom Line: $34bn is a steep price tag, but as enterprises look to replatform to make sense of digital, this could be a stroke of genius from IBM

One thing we’ve been tracking a lot here at HFS is the enterprise push to replatform to build the utopian ideal of a touchless IT environment. In many respects, RedHat brings with it many of the core components to achieve this business goal – the firm has innovated for countless years in the space to be at the forefront of changes in technology that standardizes operating environments across enterprises. The firm, along with traditional IT providers like IBM have worked to help enterprises bridge the gap between their on premise assets, old IT capabilities, and the newer technologies coming to the market. Increasingly we are moving away from a world which dictates businesses need to overhaul their environments overnight, and instead into the more realistic thinking that the modern platform will be a hybrid of the old and the new. The providers that can help enterprises link these systems and technologies together, and build a layer over the top to support the stresses and strains of the modern business will capture mindshare, and marketshare in equal measure.

So in many ways, although RedHat comes with a steep price that will leave most financial analysts puzzled – to analysts in the Digital and IT Services space, once you get passed the price tag and the old cloud wars narrative, this deal starts to make a lot of sense. There’s also the interesting inference to make that IBM has taken a decided pivot away from poster-boy IA giant Watson, to go back to its enterprise IT core and solve real challenges for real people – and in the modern world, that will always involve cloud.

Disruption is more ripe in the call center space than any other corner of the services industry, and $1.6bn provider SYKES just upped the ante to feverish levels by becoming only the second-ever service provider to acquire deep RPA and intelligent automation expertise, since Accenture picked up Genfour 18 months ago. And $70m cash is a not insignificant sum to invest in consultative talent in this fast-emerging space in desperate need of experience and scale.

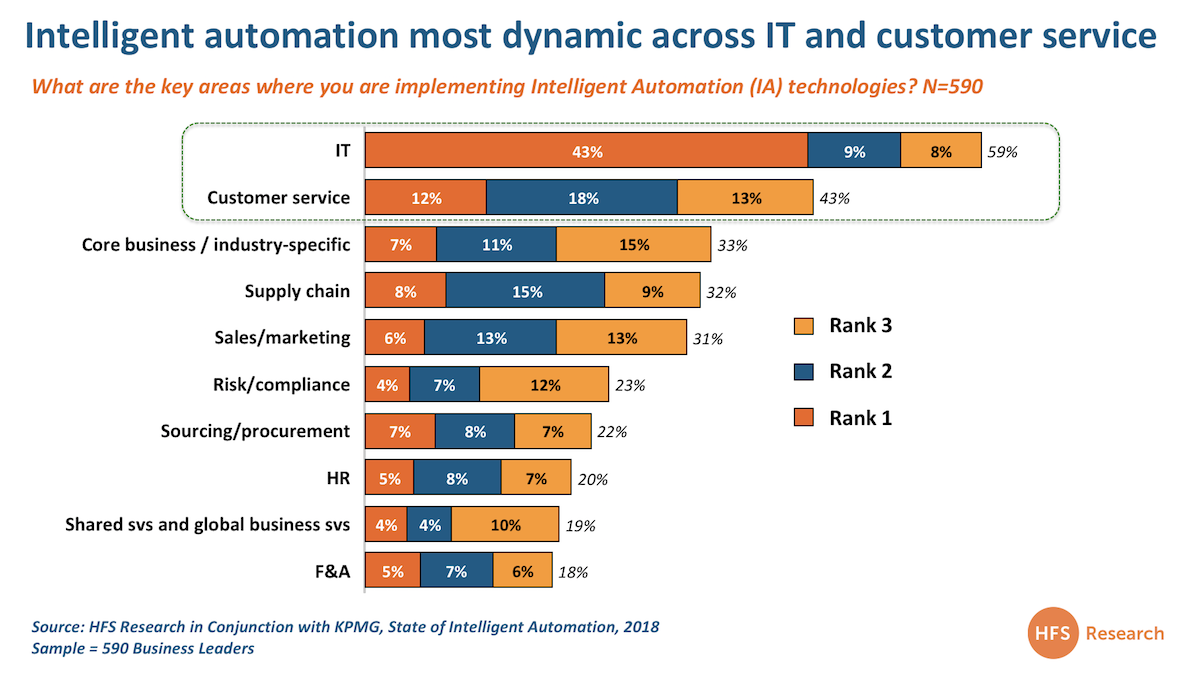

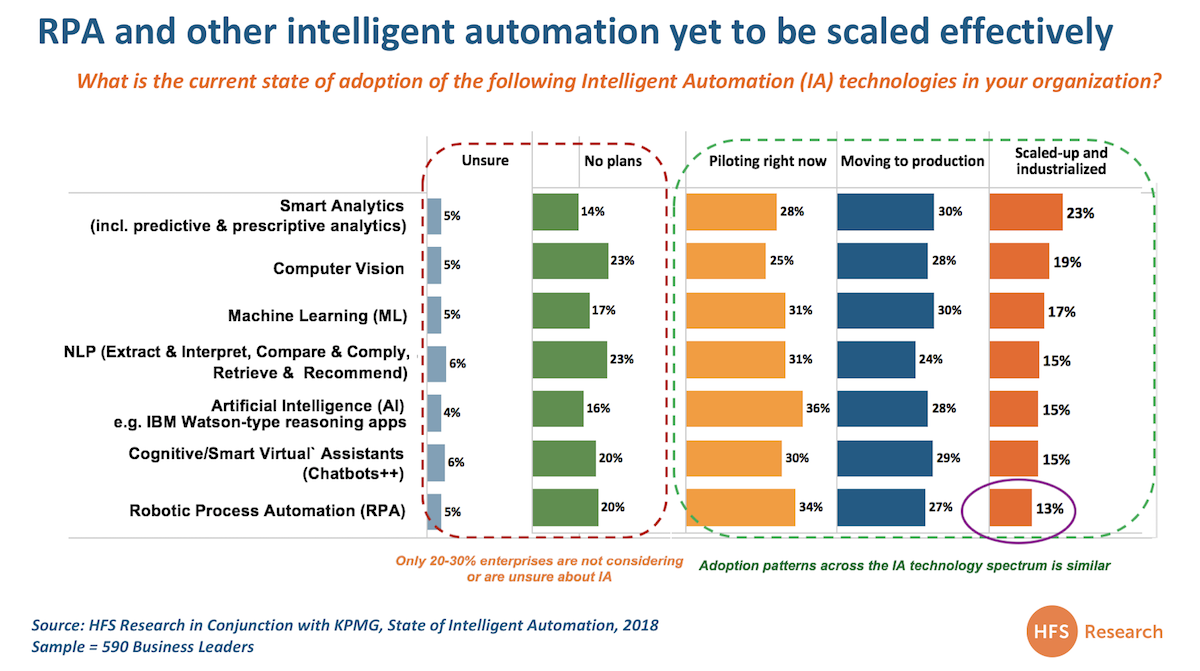

More significantly, Accenture is not a call center provider, SYKES actually is one – and now has the unique capability of attacking the market with automation-led customer experience engagements. While the market recently cogitated on the impacts of Concentrix/Convergys and Teleperformance/Intelenet, neither of these mergers had a genuine focus on intelligent automation (IA). And our new global study on AI covering 590 Global 2000 firms worldwide (conducted with KPMG), clearly shows intelligent automation is in unique demand across IT and customer service areas more than any organizational function:

None of the “traditional” call center providers have upped the ante with automation. Until now. We have found this bizarre, as there are so many opportunities to improve broken processes, speed up customer response capabilities with both Robotic Process Automation (RPA) and Robotic Desktop Automation (RDA). There’s no surprise many of the Indian-heritage providers are jumping back into call center, sensing an easy opportunity to take business from vulnerable traditional call center providers with a disruptive automation-centric approach.

SYKES is not beset by legacy enterprise deals choking the life out of it. Call center providers that got too beholden to legacy clients with dinosaur FTE pricing models are really struggling. This was one of the prime reasons Convergys (despite being one of the industry’s finest purveyors of customer care) struggled to maintain market growth and ended up being acquired for an extremely attractive price by Concentrix earlier this year. SYKES is currently the 7th largest player in the contact center space (3% market share) with revenues of $1.7bn – enough to compete at the high-end, but still nimble enough to build a base of automation-led clients, chase strategic deals and be a disruptive nuisance in a market with razor-thin profit margins.

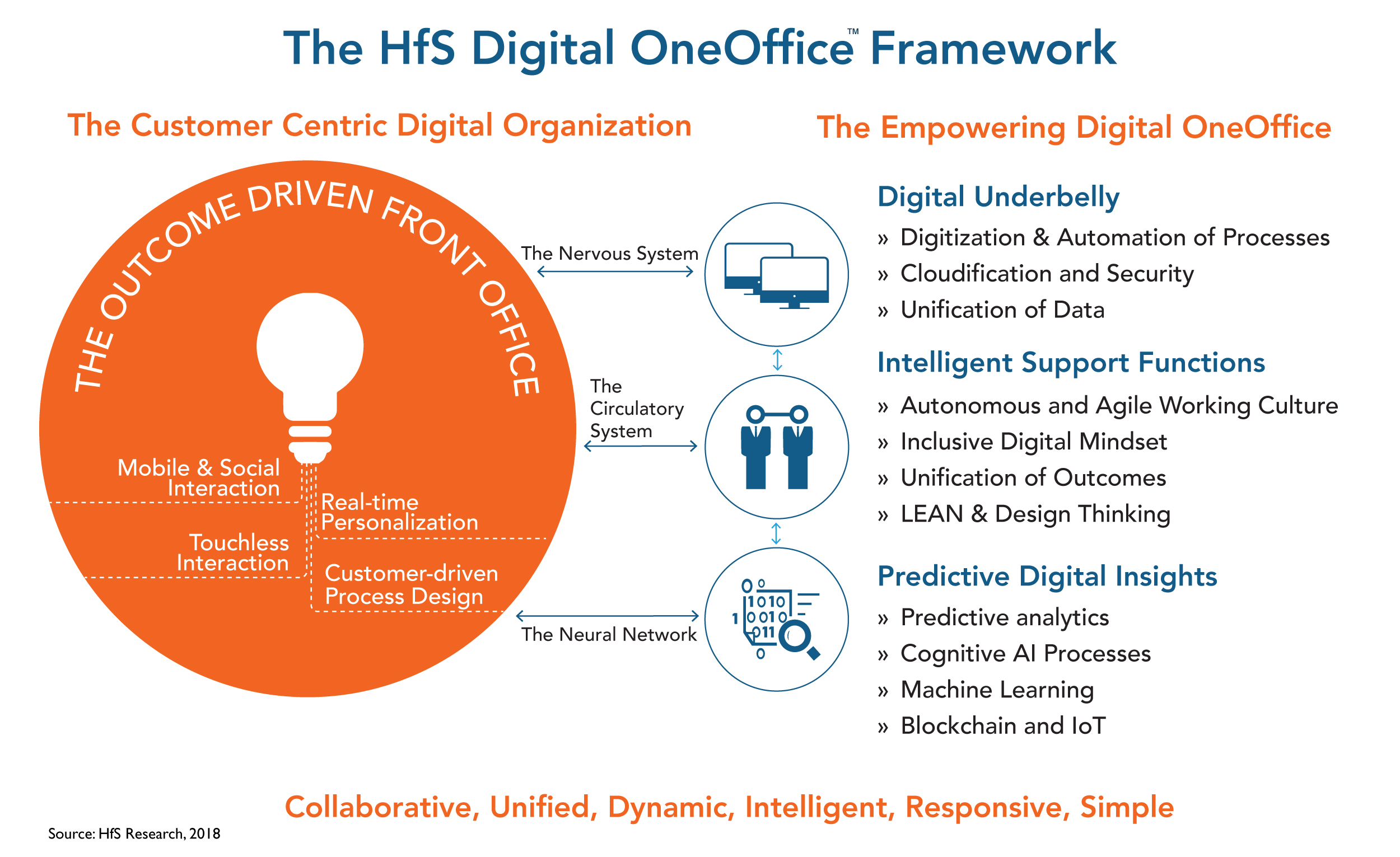

The OneOffice is here and Symphony can link the front to back office with its approach to digital operations. Digital organizations must have an operating framework that maps out how they have to operate in the future. Traditional operating models, while creating some incremental productivity value, if managed effectively, struggle to drive the unification of digital business models with emerging technologies across a business’s operations. The only true way to create a OneOffice experience is to be able to integrate the front office processes and interactive technologies (most of which are embedded in the call center) with the operations of the organization:

The Digital OneOffice is where teams function autonomously across front, middle and back office functions to promote broader processes with real-time data flows that support rapid decision making. It’s where front, middle and back offices will cease to exist, as they will be, simply, OneOffice. SYKES has a unique opportunity to consult to enterprises to make these front to back connections and weaves these capabilities into their managed services offerings. The merged entity can offer real expertise to provide automated processes as-a-service and help their clients through the journey. The only missing pieces, in the short-medium term, may be to diversify further into the middle office areas and analytics to add some real end-to-end process value, but much of this can also be accomplished through some smart partnerships.

SYKES has already been making serious investments in digital capability. The Clearlink acquisition gave SYKES capabilities in the digital marketing space, which is complementary to its core business and also a differentiator from its peers in the contact center world. SYKES’ strategy here is to connect across the customer lifecycle for an “omnichannel” solution— really digital CX. Qelp is another acquisition that expanded SYKES’ value proposition outside of core contact center services — a call center software firm specializing in self service on mobile phones, a real boon for its telecom clients.

SYKES has a sizeable WAHA delivery workforce (acquired through Alpine Access in 2012) which is a particular strength for its retail clients. The scalability and virtual training of this program is particularly effective. OneSYKES, its cloud delivery and WFM platform enable this capability. The platform also enables customer interaction analytics.

SYKES’ strength in the retail and telecom businesses. These are two of the most prime industries for automation-centric offerings, and where demand is very high (see earlier post on vertical focus in RPA). Added focus in the financial services sector would also be beneficial post-merger.

What does a SYKES/Symphony really bring to the table?

One of the last remaining automation services independents with credible global scale. With Genfour long out of the picture (and submerged somewhere inside Accenture) there are very few independent automation consultancies left worth evaluating that can impact a business the size of SYKES. Sure, there are some boutiques, such as Virtual Operations, Mindfields and Roboyo, that add some domain expertise, but nothing close to the scale of Symphony, which has 200 FTEs across Europe, North America, India and Mexico. It will be hard for any of SYKES’ competitors to respond in kind, and we are quite amazed that only one of them had made a serious move to acquire Symphony prior to SYKES’ interest.

Skill+Scale. Enterprise clients want the skill of the small guys (but not the risk), the scale of the big guys (but not the baggage). This sends out a shot across the bow to the likes of Accenture, Capgemini, Cognizant, Deloitte, EY, Genpact, KPMG etc., all competing in the quasi-consultative / managed service market… that is automation-led capability.

Appeals to the RPA software firms. The likes of Automation Anywhere, Blue Prism and UiPath will welcome any deal like that that takes them more into the front office of enterprises. This will also attract the attention of Nice, which has a strong call center automation focus. Other aspirational RPA firms, such as Pega, WorkFusion and Kofax, will also take notice and want to engage with this new entity.

Streetwise expertise. The four founders all bring a “hands-on” credibility to the table, which most organizations like to deal with: David Poole, Ian Barkin, David Brain and Pascal Baker. Many enterprises are already frustrated dealing with some of the usual suspects and may be tempted to switch to this new entity to take its OneOffice play to a new level. Obviously, much depends on SYKES leadership’s ability to retain the Symphony talent and engage them with a compelling global story.

Hands the Symphony team significant enterprise access. This will catalyze growth and disruption by giving Symphony access to a unique portfolio of 200+ enterprise clients including more than 50% of the world’s top 100 brands. While the Big 4 RPA experts struggle to convince their global partner colleagues to let them near their deep-pocketed clients, SYKES should have no problem opening the kimono to its finest differentiator that none of its competitors can (currently) boast.

Can start to heal the ‘scale disease’ threatening to derail the RPA and Intelligent Automation industry. As our (soon-to-be-unveiled) global study of 590 leaders of Intelligent Automation initiatives reveals, barely more than one-in-ten enterprises has reached a place of industrialized scale with RPA – and the word from so many clients is loud and clear that they need help:

This struggle to get to a point beyond pilot exercises and project-based experimentation could prove to be a serious point of failure for the whole industry drivthese solutions. There needs to be a much stronger melding of enterprises with implementation and consulting capability to fix these issues. This has to be an area where a SYKES/Symphony can profit.

The Bottom-line: Kudos to SYKES for making a bold bet, which has real potential. But it needs to move fast and aggressively post-acquisition to make this bear fruit

If I had to count the number of truly successful services / consulting mergers over the past decade, it wouldn’t take me very long, or require too many fingers. In so many cases, the acquiring firm is checking a box before moving onto the next shiny new object. What excites me about this move is the size of SYKES to make this really significant for the firm, the fact Symphony gives it a capability truly differentiating and hard for its competitors to replicate, and the fact it becomes the first customer-centric service provider to tackle the unquenched thirst for automation across customer processes to drive genuine OneOffice endstates.

But this is a market that simply refuses to stand still… this has to be a merger that both parties fully embrace with the verve and energy that took Symphony from a great idea in 2013 to one of the most disruptive and exciting consulting businesses in the business operations industry. That means SYKES needs to do a much better job of articulating to the world what it brings to the table, especially in the cut-throat world of customer experience BPO. SYKES leadership needs to make Symphony front and center and refuse to blunt its edge in driving narrative – staying ahead of the curve and forging great industry relationships.

In addition, SYKES needs to add to the OneOffice capability, search the globe for expertise in regions such as China, Philippines, Japan,South America and Canada. This can be with further tuck-in acquisitions and smart organic talent acquisition. It will also need to work extremely hard defining its brand and articulating the new generation of OneOffice solutions to industry. This is an exciting merger, but the hard work really starts now…

After all the fun and games we sparked with our recent blog “Seven deadly misnomers why these billion dollar RPA valuations are insane” we thought we’d give the CEOs of the leading two RPA firms (see the new HFS TOP 10 RPA report), Automation Anywhere (Mihir Shukla) and Blue Prism (Alastair Bathgate) a chance to face/off on stage to thrash out why their firms’ valuations are on such an exciting trajectory – and engage with the HFS FORA crowd to debate where the hell this space is really going and how we need to prepare for an intelligently automated future.

Yes, people, this year’s HFS FORA Summit in New York from December 11-12 is shaping up to be at our boldest, most brazen and brash best. Ever!

If you’re looking to up your RPA game and see who comes out on top, sign up to reserve your seat now, or forever hold your peace.

has been a champion firm in the growing enterprise adoption of Open Source – a service line that has moved a long way since its one-man-band and hobbyist background. Open Source is now big money, and all of the major providers want a piece of the action. In exhibit 1, we can see, alongside the financial information, a look at the number of partnerships both IBM and

has been a champion firm in the growing enterprise adoption of Open Source – a service line that has moved a long way since its one-man-band and hobbyist background. Open Source is now big money, and all of the major providers want a piece of the action. In exhibit 1, we can see, alongside the financial information, a look at the number of partnerships both IBM and