Anyone who’s been in and around the tech industry for the last couple of decades, will have come across the legend that is Bruce Richardson. The first of the true blogging analysts with his famous “First Thing Monday” newsletter, having had the misfortune of bringing me back to the analyst industry with AMR (Gartner) and being my (last) boss, has today survived that experience to lead strategy for Salesforce.

We were priveleged to dust off Bruce’s old analyst hat and bring him along to our recent Buyers Working Summit at Harvard Square where he immediatetly declared, “If anyone here doesn’t have a Cloud-first strategy, I am walking out of hrre right now”… He did also start to worry he was starting to sound like the Donald Trump of cloud computing… So over to you Brucey!

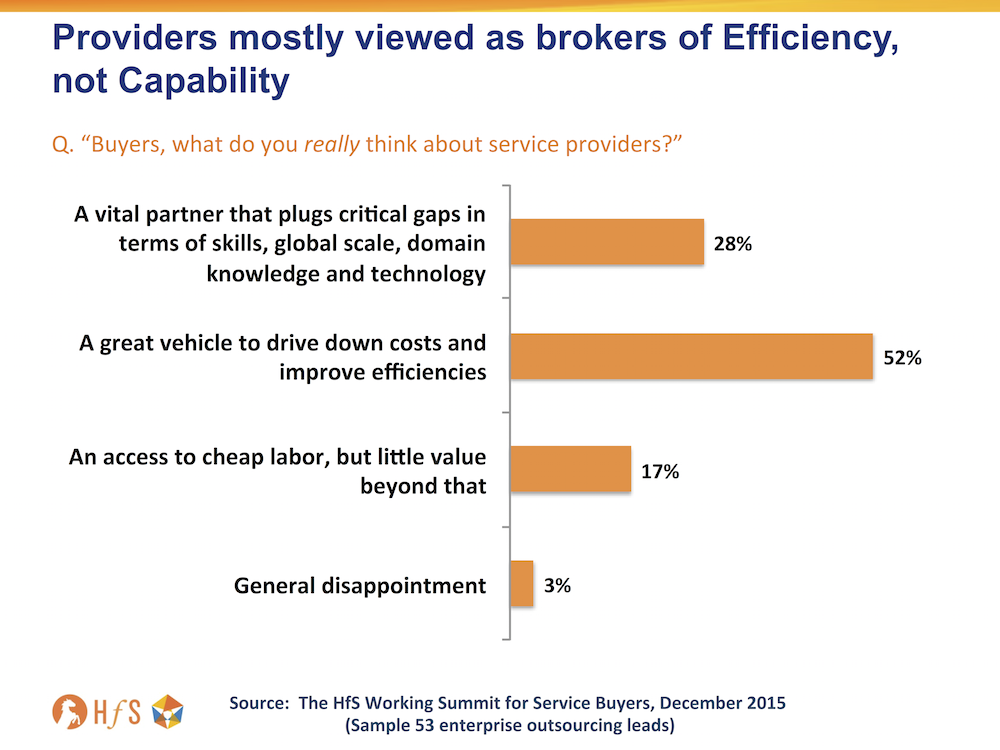

Our theme for 2016 is all about us “getting back to basics” as a services industry, and nothing exemplifies this more than what the buyers and providers privately said about each other at the recent HfS Working Summit in Harvard Square. Once we get past all the talk of disruption and change, the real issue holding back progress is the simple fact that too many of today’s services relationships are just not set up to be collaborative ventures.

What’s more, in spite of all the chest-pumping from providers on their revolutionary capabilities to turn their clients’ business models on their heads, over half their clients still perceive them as brokers of cost-efficiency… not capability:

Click to Enlarge

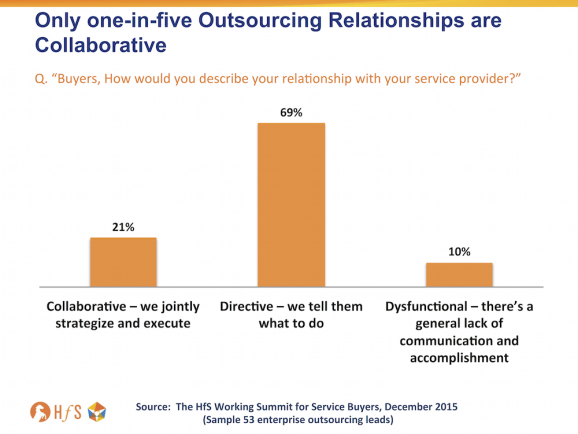

I am sure many of you are muttering to yourself, “This is very consistent with previous studies HfS has run” – and you are correct. Little is changing. However, it’s worse than just the buyers’ having negative perceptions of service providers… 80% of buyers simply aren’t engaging with their providers in a collaborative way:

Click to Enlarge

Until we can break this legacy master/slave culture, this industry will continue to stagnate

Here are three measure that could break the cycle:

1) Buyers need to entrust more higher-value work to their providers, with their leadership incentivizing their middle-managers to “let go”. Many buyers consistently admit they need to entrust their provider with higher value work to improve the quality of their engagement. But this isn’t really about trust, it’s more about the buyer letting go and having the confidence to give their service provider more responsibility, which would make them more effective at their own jobs. Sadly, most middle-managers have absolutely no motivation to entrust more to their service provider -and, frankly, why should they? What motivation would you have to make yourself less dispensable to your firm? So it’s up to their leadership to force the issue, either by demanding more work is outsourced, or by incentivizing their managers by giving them more motivating work to do… with real financial and career benefits to do so.

2) Automation is the “new offshoring”, so leverage RPA to create renewed opportunities to collaborate. The next wave of value is blending global sourcing with the mimicking of manual processes in RPA software that are predominantly high throughout, high intensity tasks. All enterprises have varying potentials for real automation value to be created by robotizing rote manual tasks. And most of the respectable service providers have invested in capabilities to develop an RPA strategy for their clients. Buyers must learn from mistakes of the past to look beyond short term cost savings and create a broader intelligent automation strategy, which also creates significant opportunities to establish more collaborative, value-added relationships with their service partners. Moreover, it is in the interests of buyside managers to put automation capabilities on their resumés as CEOs increasingly demand a cohesive plan to create a more automated operating platform to support non-linear future growth for their firms.

3) Weave Design Thinking into engagements to shift the impetus towards mutually beneficial outcomes. The less hyped, but nevertheless creeping uptake of Design Thinking is helping several relationships inject lateral thinking and renewed motivation to work together, not only in the customer-facing front office, but also in the back office operational functions. Design Thinking in services is based, primarily, on both service buyer and provider coming together to create business outcomes that are mutually beneficial – and motivational – for both parties. However, this must be established as ongoing collaboration across all key relationship stakeholders, and not simply two days of senior management putting sticky notes on each others’ foreheads. There must be senior pressure and buy in to adopt Design Thinking as a means to move away from Six Sigma-obsessed old world models, and really change the way the service buyer and provider teams work together. We’re seeing encouraging signs from several providers aggressively promoting Design Thinking techniques, such as Infosys, IBM and Cognizant, into their engagements, but this is still restricted to far too few a number of buyers at this stage. But Design Thinking, and new creations of Design Thinking-eque collaborative methods are increasingly important ways to bring together new concepts and ideas, better teamwork, and ways to design outcomes jointly that can incporporate investments from both sides.

Forget the Trump, 2015 has been one helluva year for pontification on big disruptive, and occasionally ridiculous topics.

Anything robotics, artificial intelligence, the end of work, the end of sanity… the end of pretty much anything has been bandied around. Hence, it was refreshing to bring together a host of service buyers and providers in Harvard last week, to dial back into planet earth and really get to the point of where we need to take things.

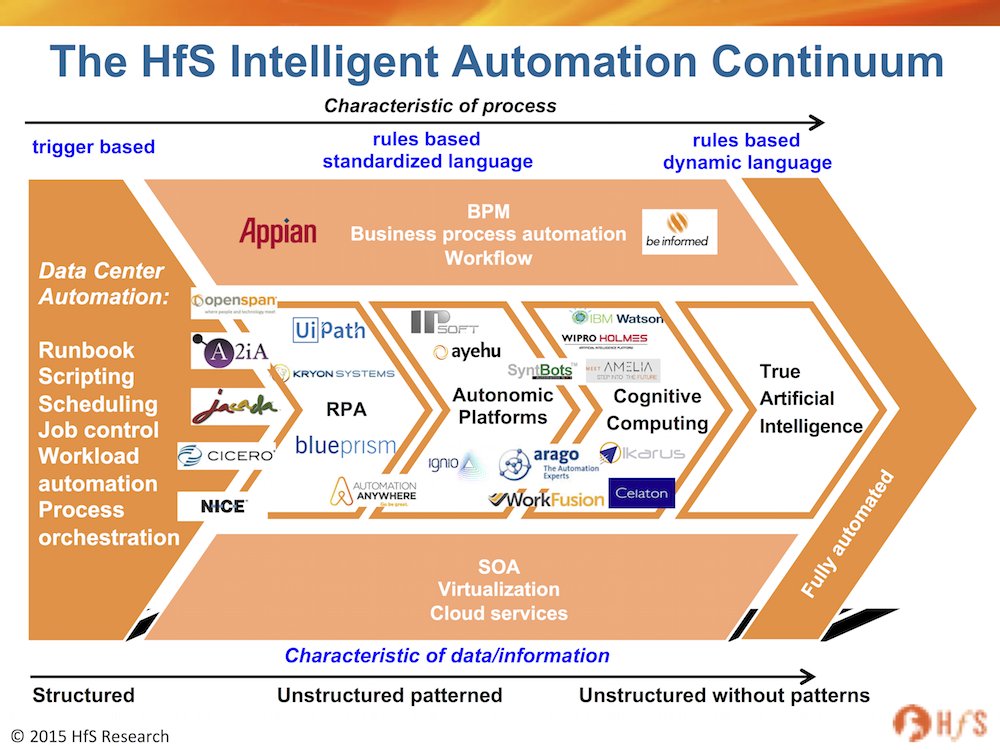

Glaring into a future, where there is no written rule book, no set curriculum to follow, can be a little daunting. So it can’t hurt to take a look at some of the mistakes of our past to create a more long-term, focused strategy to set us in better stead as we embark on this new wave of change and disruption to our cosy little world: the Continuum that begins with establishing a rudimentary, trigger-based Robotic Process Automation underbelly, that forms the building blocks for incremental investments in more predictive autonomics and – ultimately – cognitive self-learning capabilities, before reaching a haven of true artificial intelligence (which doesn’t actually exist yet, but we can all dream, right?):

Click to Enlarge

I’ve been reading some interesting arguments that discuss separating RPA out from the more intelligent developments further along the Continuum. And they’re half right, but I also argue they’re half short-sighted too. The best comparable is BPO, where we are going to see most RPA deployments, as many service buyers seek to eke out more productivity from their messy processes, which they didn’t quite get right the first time around.

And why – pray tell – did so many BPO buyers not do enough that first time around? Why is our industry literally littered with hundreds pf underperforming BPO contracts that are caught in a purgatory of status quo, where the provider has no desire to change anything and simply keep pumping home their predictable profit margins from a pre-set provision of offshore FTEs, while their buyers have long-lost the attention of their CFOs to get renewed investments to make their processes run better.

Why is it that so many BPO buyers only enjoyed some “transformation” during their brief 18-24 month transition towards a BPO steady-state, before their service provider packed up the Visio charts and redeployed their process wonks to work on that next deal coming down the pipe?

The Bottom-line: Only focusing on RPA is a fast-track to short-term disappointment. A broader Continuum focus is where the smart buyers are headed

The answer is simple – most BPO buyers only focused on getting that initial 30-40% of cost out the door. They were not thinking beyond that. They did not budget or create a real plan for achieving ongoing process improvements and innovations, once they reached that steady state of lower cost. And it’s the same with RPA and cognitive – focusing only on the short-term cost is only going to get you so far.

Do you think your CFO is really going to release significant funds to embark on a cognitive strategy once you have reached a happy state of RPA, where you have a few bots cranking through processes more effectively and more headcount freed up to do other things? Did that same CFO open up the coffers to invest in significant process transformation once BPO steady state was reached? Of course he/she didn’t…

So learn from that experience to make a broader business case for an intelligent automation journey right from the onset. RPA is only the first step on a journey of self-learning, self-healing, dynamic process creation and really smart decision making support for your business. Don’t ring-fence it… embed it in a broader program of Intelligent Automation.

After the brilliant “back to reality” conversations at our Harvard Summit last week, where we crammed 53 senior enterprise buyers into a fantastic room with the HfS team and some very “game” sponsors, we are thrilled to unveil our 2016 Summit Agenda, starting with a return to Cambridge University in March, a debut Summit in San Francisco in the Spring, and a major industry gathering in September. We’ll be rolling out themes, speakers, crazy new ideas and lots of associated buzz in the coming days and weeks… click here to learn more and apply for your places.

Next stop in the HfS quest for operational perfection… Gonville and Caius College, Cambridge

Click here to learn more and apply for your places.

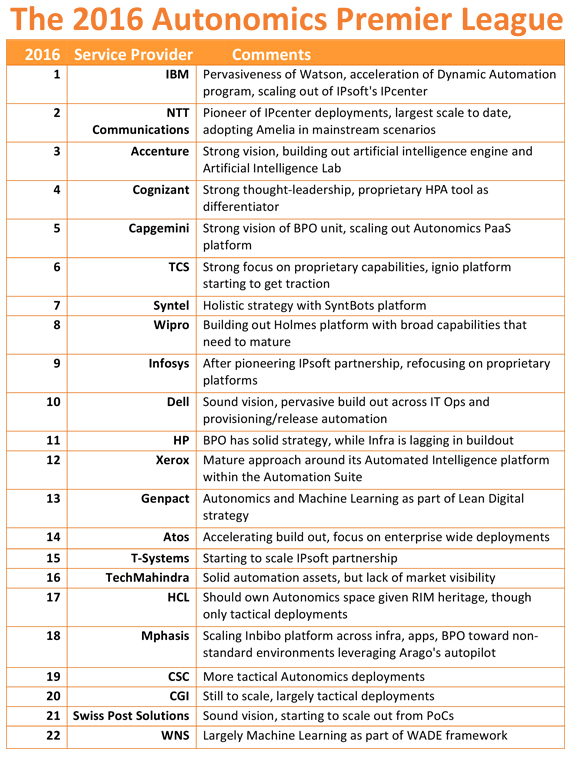

And finally… the eagerly-awaited industry bellwether 2016 HfS Autonomics Premier League table is unveiled…

Tom, firstly, what is autonomics and why is it different from RPA?

Thanks Phil, before we dive into the details, let’s level set where we believe the industry is at. We have seen the market and the discussion on Intelligent Automation change significantly, both in terms of maturity as well as in terms of scale especially in 2015. The large service providers are accelerating investments in and build out broad capabilities around the comprehensive notion of Intelligent Automation. Yet the mainstream narrative on Intelligent Automation remains largely focused on the narrow notion of RPA rather than depicting the interdependencies and implications of a diverse set of tools and approaches. In our view, the journey toward Intelligent Automation is aligned around three dimensions:

Unstructured data

Less well defined processes

Broad notions of cognitive computing and artificial intelligence

Therefore, HfS is aiming to stimulate a much broader discussion on Intelligent Automation by launching the Autonomics Premier League Table. On purpose, we have opted to use the term “Autonomics” as a broad reference term for process automation approaches beyond RPA. Thus, for the purpose of this study we refer to Autonomics as self-learning and self-remediating systems. Just to be clear, HfS is not aiming to redefine the term for RPA or even Intelligent Automation, we are aiming to stimulate a more holistic discussion!

To your question on the main differences, in short these are around the use cases and around the capabilities. RPA is largely focused on business process services with capabilities around extracting data from heterogeneous systems and around capturing, scheduling and executing process steps. Conversely, Autonomics evolved out of IT centric scenarios where comprehensive cognitive engines are not only self-learning but more importantly self-remediating. Though as suggested for this study we chose a broader definition on Autonomics to include a plethora of approaches including Machine Learning and Crowdsourcing that span across the spectrum of IT and business process services.

Tom Reuner, HfS Research (click for bio)

“Automation” has been the watchword of 2015 – has it lived up to the hype? Can we expect the noise to continue next year, or will it calm down?

If I am honest I am shying away from calling it hype. Normally in our industry no topic is small enough or largely aspirational to be hyped. But typically it is the IT juggernauts that are at the forefront (or being culpable) for hype. Within the context of Intelligent Automation the large service providers and BPOs are unusually coy on the topic, presumably because they haven’t yet fully understood the impact on revenue models as well as being anxious about the levels of transparency resulting from automation. This manifests itself in many NDAs curtailing our ability to discuss many of the issues in public. Thus, it is the comparatively small technology providers who are educating the market. Put in other words, the market is still nascent but maturity is noticeably setting in.

Having said all that, both the level of interest as well as of deployments has increased significantly. For many organizations having an automation strategy has become a strategic priority. It is about de-coupling routine service delivery from labor arbitrage. At the same time Intelligent Automation is a key building block for moving toward the As-a-Service Economy. And lastly, the large service provider are starting to educate the stakeholders around automation. All this will lead to Intelligent Automaton moving center stage in 2016. However, as I have indicated, RPA is not only dominating the discussion, but is also more mature than Autonomics, not least at is much smaller in scale and aimed at low hanging fruit. But my hunch is, that in two years’ time we won’t talk about RPA anymore as it will be a reality in the back-office. The differentiation will be around cognitive computing and artificial intelligence.

So what was your methodology behind putting together the Autonomics Premier League?

The process started by sending out a RFI to the leading service and BPO provider. This led to deep dive interviews with the participants. These insights were enhanced by HfS research stream on Intelligent Automation. At the same time input by technology providers balanced and corroborated the feedback by service providers. All this information was analyzed and we ranked the service provider by the following criteria:

Vision and credibility of Autonomics strategy

Breadth and maturity of internal tools and external partnerships for Autonomics

Scale of deployments

Institutionalization

Commercial traction

Effectiveness of marketing effort behind Autonomics strategy

However, the Premier League Table is just a catalyst for a broader discussion. Stay tuned for the Intelligent Automation Blueprint in Q3/16!!

So what did you learn throughout the research process? Why are some providers outperforming and other less so?

Beyond the issues I have called out already, two points are jumping out. First, the process has reiterated our belief that Intelligent Automation is about cost and value. Thus, the direction of travel should be around human augmentation. We have to move beyond narrow notions of cost take out. Second, higher levels of automation are the prerequisite for getting closer to the endgame which is in our view vertically infused insights and analytics.

The provider standing out are either the pioneers who took on risk and scale out deployments such as IBM and NTT Communications or organizations demonstrating strong thought-leadership including Accenture, Cognizant or Capgemini. Crucially these leaders embraced the Continuum of Intelligent Automation and don’t look at individual tools as the panacea but are building out a portfolio approach to Intelligent Automation. However, the dividing line between the leaders and laggards is drawn around two issues: The willingness to take on the risk of revenue cannibalization as well as overcoming the fear around transparency that automation invariably will create.

When you look at how this will shape up for next year, are they some providers you expect to surge up the table?

2016 will be the year when the IT juggernauts are finally taking the plunge and will start to educate the market. This will lead invariably to a significant acceleration of maturity. At the same time organizations are increasingly demanding from their service partner to help them moving to a more holistic automation strategy. As a result all the provider in the table are likely to move closer together. The India heritage provider will ramp up their comprehensive proprietary engines. Providers like Dell and Atos who have demonstrated sound visions, will aggressively ramp up deployments. And even organizations like Swiss Post Solutions who can hardly be described as the usual suspects will built on their strong understanding on Autonomics and scale out.

Crucially, the discussion on Intelligent Automation will move beyond RPA toward broad notions of cognitive computing and artificial intelligence. The HfS Continuum of Intelligent Automation will get ever more crowded as new technology players will enter the fray and will find their place in automation portfolios. Thus, the ability to manage and integrate this plethora of automation approaches will become the reference point for providers’ maturity and ultimate success. As we have stated at the outset, HfS is aiming to broaden the discussion and extend our collaboration with stakeholders. We would love to hear your views!

Great work Tom – it’s been a pleasure having you help drive our autonomics coverage this year and am excited to see how rapidly this space continues to evolve in 2016.

HfS premium subscribers can download their copy of the Autonomic Premier League table and analysis here.

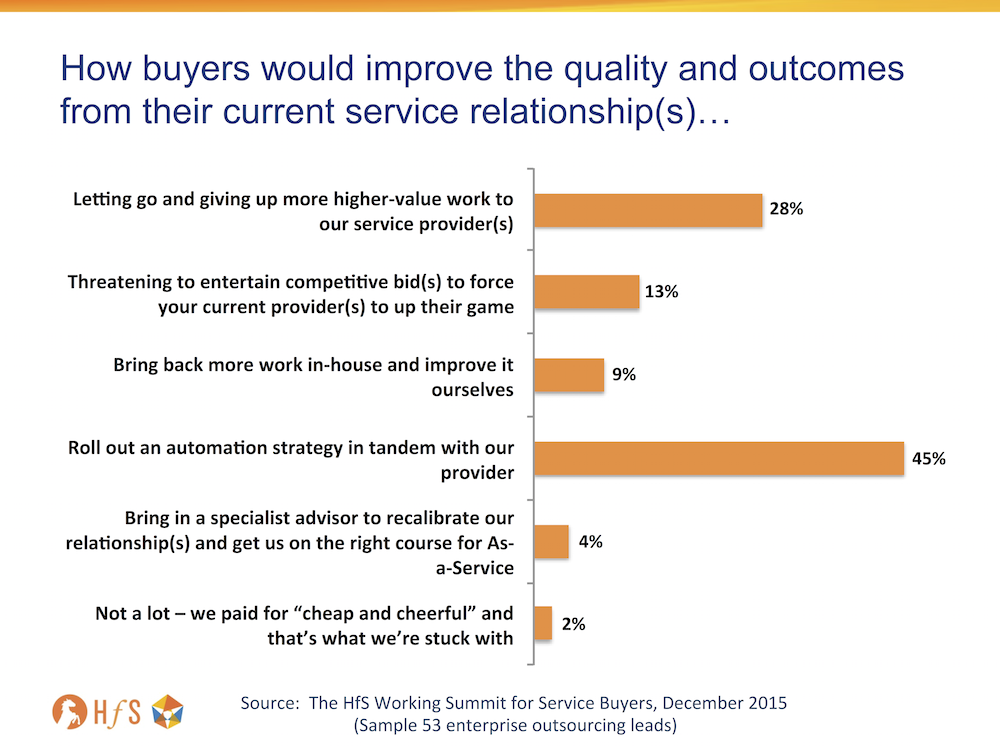

The reality of Robotic Process Automation is hitting us at the HfS Summit for services buyers at Harvard Square this week. We anonymously polled 53 senior outsourcing relationship leads with the question “what measures would improve the outcomes and quality of their outsourcing relationship”:

Click to Enlarge

Last year’s buyer’s summit saw 48% polling they needed to let go and entrust their service provider in higher value processes… now that number is dropping to 28%, with the preferred partnering focus shifting to working jointly on an automation strategy. Nearly half of today’s buyers (45%) now see that as the main area to get renewed value.

What does this tell us?

As mature outsourcing deals get stuck in holding patterns, automation is providing the new flavor to find that next increment of value. The industry hype and marketing is clearly reaching the buyer – and many want their service providers to work with them to help figure out an automation strategy.

So the real conversation now shifts to how buyers and providers can find common commercial models to make automation work for both parties. However which way we look at this, buyers will need to make some new investments in Robotic Process Automation technology and expertise, while the service providers will ultimately have to concede they may need to reduce the FTE provision on their side, as automation takes effect.

Now, the real challenge here is for the service provider to redeploy the freed-up FTEs on their clients’ higher value processes. So these two motivations should go hand-in-hand: decreasing labor effort on automatable tasks and increasing it on the higher value work the clients would like to outsource in the future. So if buyers and their providers can get this right, automation will be a long term play for both parties, where higher value work gets done and delivery staff are kept busy because of the closer collaborative relationship and greater volume of work being parsed out.

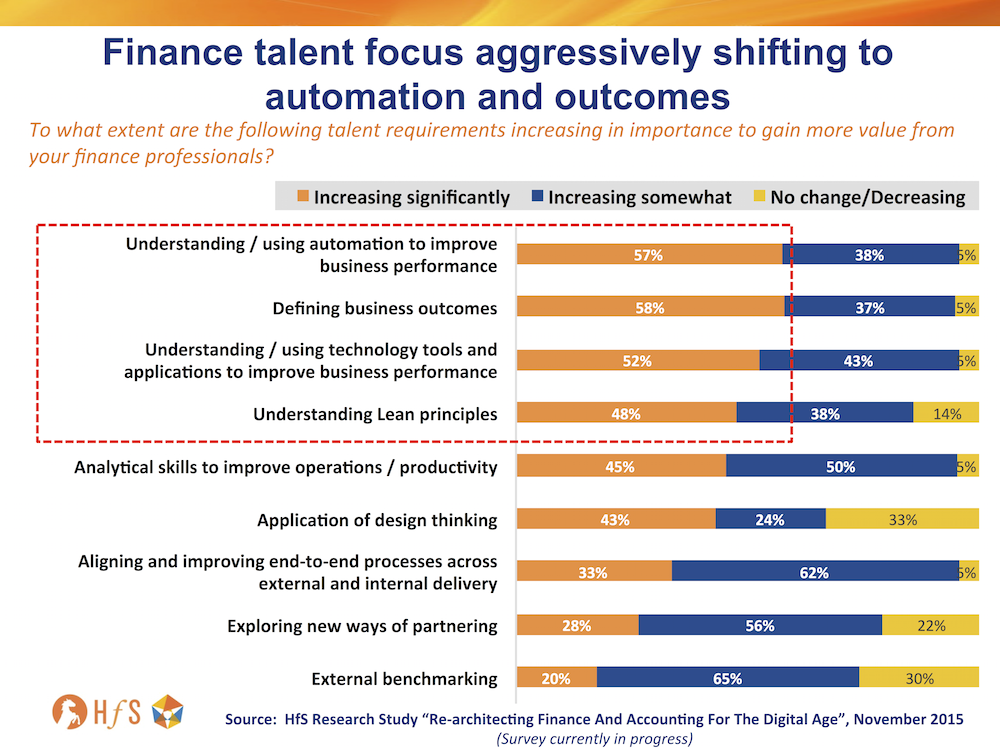

Our current in-the-field study looking at Re-architecting the Finance Function for the Digital Age (click here if you are yet to complete it) is confirming some major changes in the capabilities organizations need from their finance staff:

Click to Enlarge

What’s eye-opening, here, is the softening focus on analytics skills and the huge increase in the need to understand automation and better define business outcomes. I’ve long preached that you can’t really get the data your organization needs real-time, if you don’t have well automated processes to generate it in the first place.

Enterprises are settling for what they have, and are now focused on making it function more productively

It’s becoming clear that staff have to be less focused on creating data, overseeing operational processes and performing routine tasks, and much more adept at figuring out how to make better sense out of what they are doing to achieve more measurable, value-add results (outcomes) for their organizations.

In many cases, enterprise operations leaders are realizing they can’t create armies of world class data scientists out of their current crew, and it’s simply too expensive to hire top-notch MBAs to sit around all day trying to correlate data points. Yes, you need to have some of those people on staff, and yes, you can pay your service provider or consultant to add data talent, but the more immediate and tangible need to shifting to automating finance processes more effectively, and the influx of robotic process automation tools and platforms is changing the conversation.

The fat fluffy middle is running out of excuses

When you talk to customers today, there is a clear growing lack of tolerance and impatience to run operations more efficiently and more digitally… and you simply can’t do that when you rely on messy processes, poorly integrated systems, on-premise software and over-reliance on constant manual intervention to just to keep the lights on. The excuses around security fears of the public cloud, the offshore outsourcing horror stories have run dry and it’s time to act.

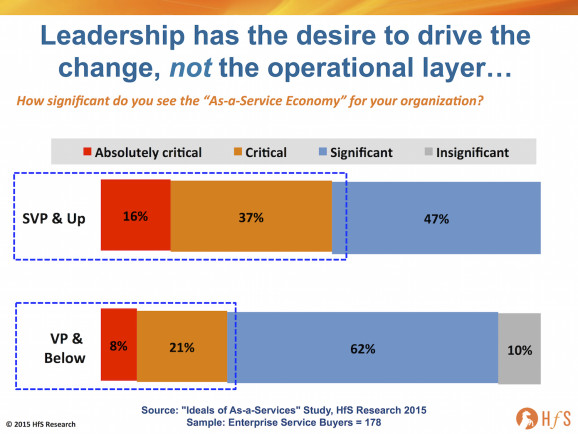

Our recent As-a-Service Study clearly outline the growing bifurcation between leadership vision and middle-management inertia:

Click to Enlarge

Let’s be honest, most people are comfortable with their daily grind – they stare at metrics on spreadsheets, ensure exceptions are handled and the corporate engine keeps running. They turn up at meetings and say all the right things, avoid challenging the status quo (while acknowledging there can always be improvement), but deep down have settled for adequacy and a steady treadmill of efficiency without too many fireworks or drama.

The Bottom-line: It’s time to get with the program, or get out of the way

Why would they want to learn how to access and interpret data more intelligently? Why would they want to find problems, as opposed to reactively solving them when they crop up? Why would they want to mimic manual processes into scripts to have them run robotically, when they can patch over these inefficiencies with cheap offshore labor? Why would they want to explore the potential of artificial intelligence and self-learning computing capability when they can just do these things themselves (or at least pretend to do them). Answer – they have no burning platform to change the way their do their jobs.

But there is one significant burning platform that will burn them, if they are not willing to adapt to the As-a-Service world: they will be irrelevent in tomorrow’s enterprise. Yes, they may be lucky and survive in legacy organizations that can get away without changing, or they may be in their late 50’s and only care about lasting a few more years until retirement, but – for most – if they cannot adapt to As-a-Service, their bosses will shift them on and either replace them with a service provider staffer, or just simply phase out their legacy job, as it was not really needed anymore.

Stay tuned as we drip this study out to market in the next few weeks. The world changed at lot in 2015, and we need to get back to basics in 2016 to understand actions customers are taking to change with it…

While we can all obsess about a future where any work requiring any sort of basic logic will be automated, where we won’t even need to think anymore, because machines will do that for us (in fact, we won’t need to do anything anymore except exist, or maybe play golf or twister or something…), the market for good old-fashioned BPO is quietly picking up very nicely as several smart providers, quite simply, are getting better at developing offerings that are much more effective, profitable and scalable.

Rohit Kapoor is Vice Chairman and CEO EXL (Click for bio)

One such service provider, which has been quietly going about its business very effectively of late is EXL, which has been enjoying a record stock price this month and very healthy improvements in profitability and revenue growth this year.

I first met a fledgling EXL before the firm went public, back in 2006, and was immediately impressed by the hands-on steely determination of its CEO, Rohit Kapoor, and his close-knit team of process-obsessive young managers. Fast-forwarding a decade, and that same firm has passed the half-billion dollar revenue threshold, developing deep process niches in verticals like insurance, banking and healthcare, while building out real global depth and competency in analytics and finance and accounting. And it’s this breed of provider which is really beginning to thrive in today’s As-a-Service Economy – small enough to be nimble to cater for needy clients, large enough to take on complexity and scale, and resourceful enough to lay the groundwork for multi-tenant As-a-Service offerings for the future.

So without further ado, let’s drag Rohit away from the golf course (where he’s probably upsetting yet another of his clients by not letting them win…) and hear his views of how the industry has evolved and how he intends his firm to evolve with it:

Phil Fersht, CEO and Industry Analyst, HfS Research: Rohit, it’s great to have you with us today. I think I’ve known you nearly 10 years – and it’s the first time we’ve had you on HfS to talk to our audience. So maybe you could give us a little bit about your own career background, what you started out doing and how you ended up running a major BPO firm like EXL?

Rohit Kapoor, Vice Chairman and CEO, EXL: Hi Phil, thanks for having me on – great to be here! I started my professional career with the Bank of America in India, ,and came to New York 25 years ago to establish a new business unit for the bank dealing with High Net Worth Individuals, helping them manage their money. As part of this, I started to make a lot of private equity investments into the Indian IT services companies, which were just growing up at that stage. These were highly under invested companies, not very well known in the public market, and there were a lot of myths around them. But as I dug deeper into these companies, I saw the leverage and power of the business models of the firms in this space, and you know ended up doing really well for some of my clients and making outsized returns for them. So that’s what led me to set up EXL with the concept that if you could do this for IT services and leverage the offshore delivery model, why can’t you do this for back-office operations. It’s now been 16 years with EXL. We continue to have fun and continue to enjoy growing this company and be successful.

Phil: So, Rohit, where do you think the industry is today? It seems like there’s an awful lot of noise circling around, in terms of shifts towards automation and new types of delivery models. Do you think the industry is really changing this rapidly or do you think it’s a lot more rhetoric than realistic business practices, right now?

Rohit: I think the industry is going through what I would call its growing pains. There are points of time in the industry’s evolution where things become a little bit hazy and there is a lot of talk and divergent viewpoints. Then ultimately a few companies break out, move through the clutter and show leadership and direction to the rest of the market. Then everything gravitates in that direction in a much more clear-headed way. Our industry is going through one of those phases where there are a lot of buzz words being thrown around and different things mean different things to people. One example is when people talk about digital, they talk about analytics, they talk about automation, they talk about outcome-based models, design thinking, platform BPO or talk about products. There are a number of different elements that get tossed around, and the fundamental underlying clarity is just beginning to emerge. It’s an exciting period. Companies that deal with these types of issues at a much more fundamental level and get it right and be really successful for their clients and for themselves, and others will struggle to change. So we are in that period of disruption in our industry right now.

Phil: I recently came back from a visit to India, where I met with a large number of service providers and their clients. I got the distinct impression, with maybe a couple of exceptions, that a lot of them have their heads in the sands a little bit. They don’t seem to think that there is a disruptive wave coming, and things are going to carry as on business as usual, for the next 3 or 4 years …and this interim panic will soon blow over. Is this something that you are seeing as well – and does that concern you?

Rohit: Yes. Absolutely, Phil. I think you know a number of companies that have been successful doing work the traditional way, and so many of them believe that staying with traditional models might be the right way to do it. Others are certainly being more adventurous and embracing changes that clients and the environment are pushing them toward. Some are proactively adopting some of these changes, and in many cases either cannibalizing their existing business or completely adopting new models. The tipping point has not yet been reached, but a few companies will actually accelerate their growth rates and end up showing the rest of the industry how you can adopt these new models and take the business forward. Just take the example of moving from traditional BPO towards BPaaS. Right now there seems to be a fair amount of confusion between the ownership of the technology assets working in what I would call a platform BPO model compared to true BPaaS. There’s a very, very important difference there – the ability to offer the service and the technology over the cloud, to have it be multi-tenanted. Those are distinctive features of BPaaS, as opposed to having the platform and offering BPO on it. There’s very little leverage with platform BPO, whereas in BPaaS there’s tremendous leverage. So some of those models are, as you know, being explored and a few courageous companies will get that right.

Phil: It’s interesting with BPaaS, Rohit. I think we’ve seen quite a lot of success in the market around platforms like Saleforce.com and Workday in the HR and CRM spaces. But it seems to be a lot more of a challenge for companies in banking, insurance and other disciplines, such as F&A, for example. Do you think that this challenge will be overcome eventually, and BPaaS will eventually take off at an industrial scale? Or do you think it’s a very slow gradual transformation, for most firms?

Rohit: I think this is a definite trend, Phil, which has very strong, fundamental drivers to it. Clients are looking to variablize the cost structure completely and want new choices to manage risk associated with technology as well as with the service. Everybody wants to have best-of-breed technology in place and the flexibility to make changes to that underlying technology platform, both in terms of functionality and cost structure. We are seeing the evolution and creation of disruptive companies with aggregator and network models, and as you move toward these models, BPaaS is going to be a critical component. The companies you referenced, Workday, NetSuite and Salesforce, all of these are what I would call software technology platforms on a SaaS model. The trick I think for us is going to be how can we leverage the same SaaS architecture to provide services in a manner that’s got operating leverage on it? It’s not just a matter of providing service alongside Workday, Salesforce or NetSuite. It’s how you take that service and scale it to get the benefits of a much lower marginal expense for every incremental piece of business added to it and then pass on that benefit to your clients to share in that reward.

Phil: Indeed, Rohit. It seems for this model to be successful, it’s going to take a provider or two to say “I am going to take on a bunch of BPaaS-based initiatives with my clients for the next couple of years, and I am going to work with them at a very low margin to build up a base that I can sell as a multi-tenant solution of people plus technology”. Is this something which you people at EXL are doing and you can see other companies being successful at it? Or do you think it’s still a long time coming?

Rohit: Phil – good question – we’ve certainly started to work on this as this is not a long time coming. Initially, we are trying to tackle non-core areas for our clients which, irrespective of their size and scale, they have been willing to adopt. Let me give you an example. We’ve built a product for an area that is increasingly standardized and a lot less customized called MedConnectionSM that, at the heart of it, summarizes medical records for insurance claims. So in the claims process when someone is hurt, we take all the medical files, a whole host of documents anywhere from one page to 400 pages, and this tool will summarize all of that information into a readily accessible digital format available over the cloud that can be accessed by the adjustor who is settling that claim. Adjusters can look at these records, get the summarized content and be able to make decisions far more nimbly, effectively and accurately than you could previously, and its priced per document, not on a per-FTE basis or the amount of time that it might take somebody to do this. So, we’re road testing and creating several of these kind of examples, predominantly in our core industry verticals of insurance and healthcare, where we have the maximum subject matter expertise, understand the pain points, see where can we create this type of functionality and deliver the maximum value – to not just one customer but several. That’s what the model is based upon.

Phil: When you look at EXL’s role in running a number of clients on this BPaaS model, Rohit, does this mean you are going to have to look to scale up in terms of the different types of skills you need and capabilities, you are going to have a look at more analytical workers, you’re going to have a look at more creative folks to support clients? Where do you see the real investments need to be made?

Rohit: Yes. I think this requires a sea change, Phil. First, we already have the domain subject matter expert. So that’s a good starting point, but it requires us to invest in the resources to architect and build these technology platforms. Right now we’ve got about 300 developers just focused on creating these types of tools and technologies to enable the commercialization of this kind of SaaS and BPaaS functionality.

We are then, layering on top of this, resources to embed analytics into product functionality. Then it also requires a retooling and retraining of our sales force because the skills and ability to take this to market, communicate and sell this are very different than selling traditional FTE-based models. So it’s actually the technology, the analytics and the frontend that needs to be retooled in order to make this successful.

Phil: I think this jives very much with the perception I came away recently from my India trip. I saw a real passion for process which we always knew existed, combined with a passionate analytics capability, which I think is still poorly marketed, in general, by most providers. But also, I did see some very good quality robotic process automation initiatives that were taking place within some of the India-based delivery centers. And these are simple things – they’re not rocket science – and are really helping improve the flow and throughput of certain processes. And I do think India has a really strong role to play in RPA analytics, as well in some of these BPaaS type delivery solutions. I just sense it will be a little bit of a while before we can see the true potential, and there is still a bit of shyness and trepidation, in terms of pushing the model heavily. Is it something which you are seeing as well, when you look at the real core strengths of a company like yours?

Rohit: Yes, absolutely. And you know we’ve invested our own which we call the Business EXLerator Framework™. What that does is it optimizes a client process end to end, leveraging a number of different skill sets — Lean Six Sigma, technology, business process automation, robotics, analytics — in an integrated, real-time fashion. The way to think about it and the way we are applying it, particularly for robotics, is we bifurcate the processes we handle for our clients into complex and simple processes.

The simple elements of our processes are where we apply a lot more of technology automation applied in two ways. Number one is to eliminate that exception altogether, or number two to roboticize it, so we can automate those processes totally without manual intervention. So whether it’s the elimination of the process itself or it’s the smarter more mechanical and automated way of dealing with it, which we call advanced automation, we are applying those types of techniques.

For complex processes, we adopt a number of tools to manage them a lot more efficiently and increase the effectiveness of the processing capability. We leverage the full skill set of analytics, work-flow solutions, benchmarking, lean sigma and we’ll make that a lot more efficient for our clients.

Phil: So I’m going to ask you one final question to share with our readers, Rohit. You’ve been around this industry, really, since the early days, so if I could anoint you as the Emperor of BPO for one whole week – and you had one wish that you could have granted – what will that be for this industry?

Rohit: Well, I think you know this industry really needs to have some real clarity in terms of the direction in which we all need to go. That clarity is in terms of providing the business outcomes to our clients and to be focused on outcomes first, understand what needs to be achieved, and then figuring out different ways of getting there. So whether it involves the Business EXLerator Framework, BPaaS, creating new products, new automation, using analytics, all of that needs to be centred around outcomes and having a very clear blueprint of what the outcome should be. So I think some of that is actually outside in-thinking rather than inside out-thinking, and if we can change the industry’s viewpoint to an outside in-thinking that will be a significant step forward.

Phil: Good answer! It’s been really good to have you share of your views, Rohit, and what we can do to move to a more evolved model. Can’t wait to share this discussion!

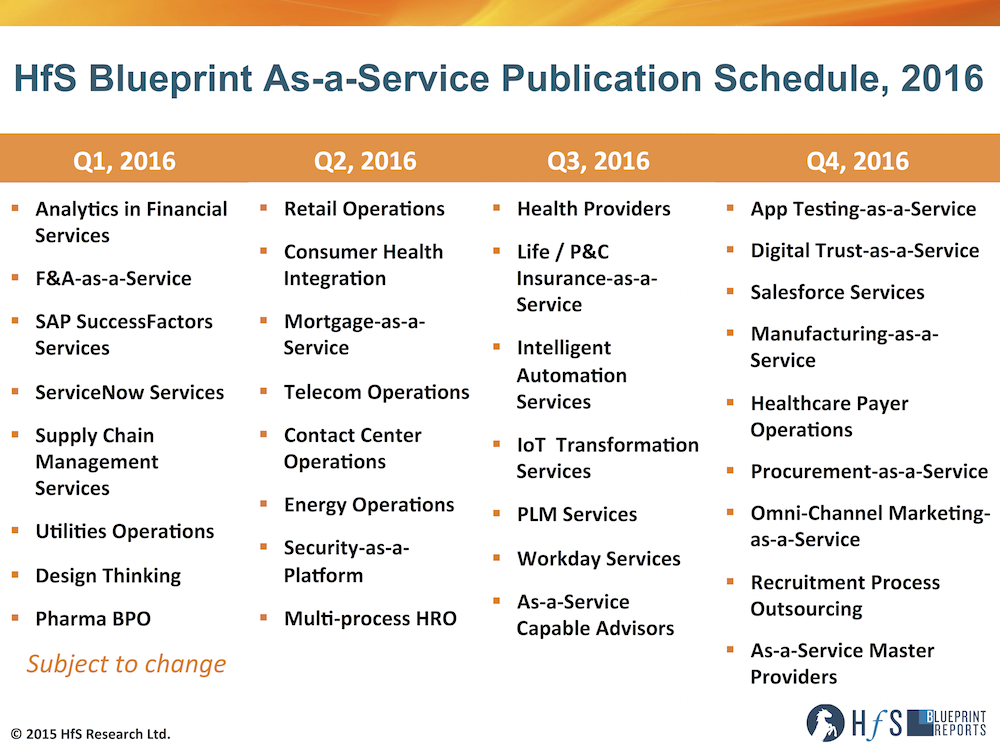

2016 will mark our seventh year as an analyst firm and will be our most expansive as we tackle many emerging areas and industries. Yes, we have come an awfully long way since the days people thought we “only covered BPO”:

Click to Enlarge

The analyst industry’s most ambitious 2016 research agenda tackles the continuum from legacy operations to the As-a-Service Enterprise across talent, technology and process

Earlier in 2014, we introduced to the world the concept of the As-a-Service Economy and how it is fundamentally impacting how business and IT services have to be fashioned, solutioned and delivered. Enterprise service buyers and providers have little choice but to evolve how they manage their services, or face extinction.

This means both parties need to make genuine investments in their underlying process architectures, reorient their talent capabilities and make some short-to-medium term sacrifices in their financial models to remain viable in the As-a-Service Economy. The same issues apply to sourcing advisors and analysts that face increasing irrelevance if they fail to adjust to the shifting demands of what it means to be an “As-a-Service Enterprise” in this new economy.

The legacy model of IT and business services sales and delivery that has dominated the industry for decades has rapidly become obsolete in our increasingly digital world, where speed, agility, flexibility and re-invention are no longer optional, but core characteristics for the success of any As-a-Service Enterprise.

For HfS, As-a-Service is about continuous progression, where enterprises do not pause at a status quo state. Instead they are continually exploring better ways to automate processes, access rapid meaningful data, and advance self-learning capabilities in a secure, trusted environment.

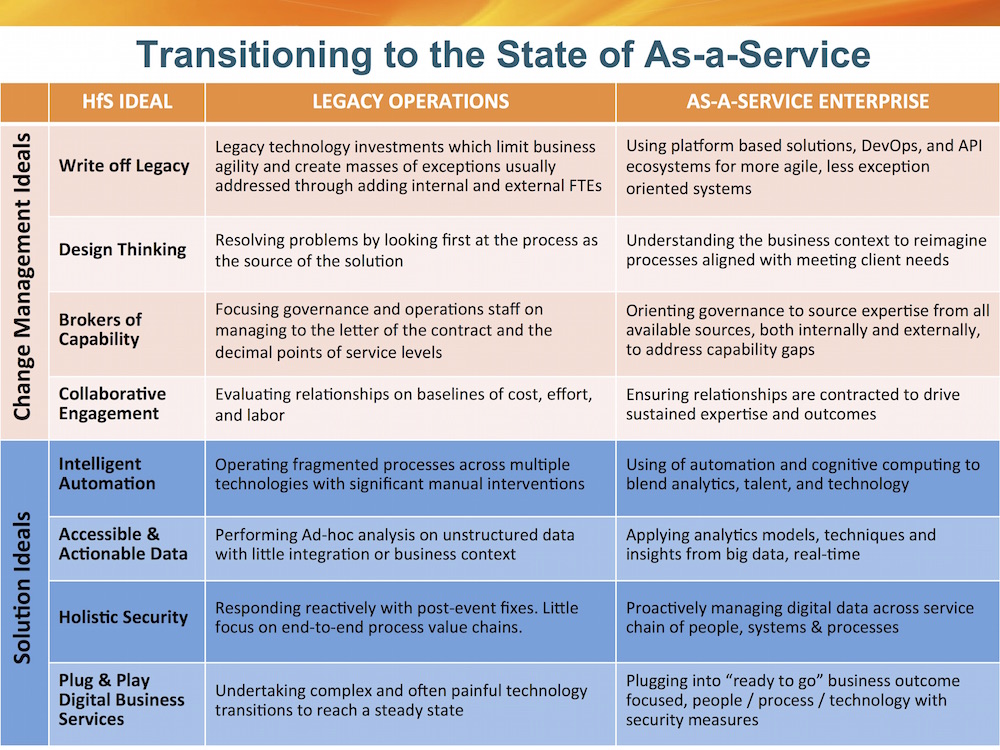

Our thinking about the Ideals of the As-a-Service Enterprise also has progressed this year. We now segment the ideals into Change Management Ideals and Solution Ideals that intermingle and build upon each other on the journey to the As-a-Service Enterprise. This journey will require significant change management, and through the course of 2015, we have seen encouraging examples of that throughout the industry, especially with efforts to simplify and automate increasingly unwieldy legacy operations and technology.

We could write and talk for hours about the unwillingness of enterprises to change the status quo to achieve better results. But ultimately it all boils down to the leadership of the enterprise having the appetite to go out and find a trusted partner that is motivated to share the risks of this transition within a financial model that works for all parties. Middle management will always resist anything that doesn’t pay them more, make them happier and more excited, or more motivated to perform. The only way forward to achieve genuine plug-and-play digital business solutions is for service providers and enterprises buyers to embrace real design thinking concepts and work together continuously in a much more collaborative and transparent fashion. This means they need to invest in talent, in training, in change fundamentals—and ultimately in solution fundamentals.

The Ideals of the As-a-Service Enterprise explained

In sharing our thinking on the Ideals of the As-a-Service Enterprise through countless client strategy sessions, industry-wide webinars and briefings this year, we have had the chance to test these Ideals with industry stakeholders to understand their relevance and practical applications.

What came out from these sessions was that the Ideals fell into two key themes: Change Management Ideals and Solution Ideals. In many cases enterprises approach these ideals sequentially.

Click to Enlarge

To move toward the As-a-Service Enterprise, it is beneficial to begin with a willingness to write off the legacy technology and operations and with that adopt Design Thinking as a way to look at business challenges and opportunities with a fresh perspective. Then an enterprise can orient governance and relationships toward building service solutions with the optimum capabilities, regardless of their source. Moreover, enterprises can build the right commercial arrangements that break from past “zero-sum” constructs to encourage sustained collaboration and shared outcomes. These are the core building block Ideals for enterprises embarking on the change management required of this journey.

Click to Enlarge

With those change management Ideals underway, it’s then possible to craft an As-a-Service solution that incorporates talent, processes and technology to achieve the Solution Ideals of Intelligent Automation, Accessible and Actionable Data, Holistic Security and Plug and Play Digital Business Services.

2015 showed us that these Ideals resonate with both enterprises and service providers, as they conceive solutions for the future of IT and business processes. Our discussions in 2015 also showed us that security that encompasses the entire solution stack was a critical Ideal that we had initially underplayed. It was this realization that encouraged our research expansion into covering new approaches to digital security and trust.

These Ideals are capturing the spirit and strategic intent of the industry through the journey to the As-a-Service Economy and form the basis of how we will look at our overall Research Agenda and our HfS Blueprints throughout 2016.

Melissa O’Brien is Research Director, Contact Center and Omni-Channel Operations, HfS (Click for Bio)

Pretty much everything we cover at HfS has a contact center at the heart of the process, whether it’s an insurance claim, a supplier inventory call, a sales inquiry, an analytics request, and so on….

So we realized it high time we actually brought on an analyst who has set up contact center operations around the world, lived and breathed the offshore experience, has intimate knowledge of the service providers, the technologies and the skills needed to make these things function effectively. We also realized we needed that analyst to be expert at kick-boxing to keep us all in order. So join me in welcoming a great talent to educate us all on the future of the contact center and omni-channel operations, Melissa O’Brien…

Welcome Melissa! Can you share a little about your background and why you have chosen research as your career path?

Thank you for the welcome, I am very excited to join the HfS team! I have been following contact center operations and customer experience as an analyst for the last four and a half years, and I previously worked within the BPO industry in various roles. I’ve been an implementation manager, designing and transitioning processes from onshore to offshore- managed client relationships, and have also developed and administered training to groups of new contact center employees and to the trainers themselves. When I got the opportunity to work in market research, I had found the perfect combination of continuing to work with clients on solving problems, but also getting the chance to do a lot of strategic thinking and writing about my domain. I really enjoy research because you’re always learning as the market is constantly changing and evolving – I love the challenge of always having to be that step ahead!

Why did you choose to join HfS… and why now?

I have been working in the contact center operations market for the past 10 years and my passion is understanding what makes great customer experiences. HfS’ focus on the As-a-Service Economy is at the heart of how the contact center is evolving today, and the way that companies are now looking at customer experience, which is a much more holistic and outside-in approach. Ambitious contact center operations providers have the potential to use technology, talent and process expertise to improve how companies interact with their customers to have a major impact on their clients’ strategic business objectives. These services influence critical metrics like Net Promoter Score (NPS), which is not only indicative of customer satisfaction levels, but can actually predict revenue performance for an organization. So, I’m looking forward to diving deep into this critical alignment between customer interaction and business outcomes, within the theme of the As-a-Service Economy.

I also think that HfS is a really socially intelligent company in leveraging digital content, the web and social networks to reach customers and promote discussions. This approach is congruent with many trends I’ve been watching in omni-channel communications, and it’s just a smart approach to business. The HfS events programs, like our intimate buyer summits, are very complementary to this model- leveraging a diverse global community and furthering that social dialogue. I’m excited to participate in these conversations and be a part of the thought leadership that HfS is driving.

What are the topics and big issues that you will focus on in your analyst role?

An important topic will be the role of intelligent automation on contact center operations and BPO. Automation has been prevalent in contact center operations for many years, but there is so much maturing that can be done to make automation in this space intelligent and more complementary to the labor components of the business. The human element is something that is transforming as well, as the impact of technology and digital channels is shifting the skills needed for BPO talent; I’ll be exploring in depth how the talent and technology are shifting and how to find the right balance.

There is tremendous opportunity in this space for analytics to drive better customer engagement, so I will be giving a lot of attention to how data and analytics tools are being used. It’s so important that enterprises act on the customer data they have more intelligently – it’s one thing to collect data, but another to use it to make real-time decisions to improve the customer experience. Given that omni-channel communication is driving convergence and synchronicity of contact center with marketing, I’ll also focus on research that examines these relationships ad synergies. I will be working across the HfS analyst team to collaborate on research where our coverage areas intersect, in particular around key themes like analytics, automation, cognitive, cloud and digital.

And what trends and developments are capturing your attention today – especially in your world of omnichannel and contact center?

What’s fundamentally changing, today, is the importance of the customer experience placing the contact center as an increasingly strategic part of part of the enterprise. The old model was about handling customer inquiries as quickly and cheaply as possible, often with not much forethought to how those interactions affect a company’s brand and the overall customer experience. The commoditization of products and services along with rapidly expanding communication channels has made the experience a customer has with a company or brand its greatest differentiator. As a result, more companies are making customer experience a strategic corporate imperative- trying to understand the customer journey and its impacts on a company’s financial performance. With this perspective, it is impossible to dismiss contact center as a transactional cost center; it’s an integral part of a greater strategy that needs to examine the experience through the entire customer lifecycle and across all communication channels. In industries such as retail, insurance and banking, the actual “products” are pretty much standard across the board, so it’s the customer experience that has become the true differentiator. The customer engagement strategy is what is making or breaking many business today.

Melissa gets inspiration from her coonhound, Bentley

A key part of this, which has shaken up this space, is the role of digital communication channels, in particular social networks, for customer engagement. Customer-facing social networks have primarily been a function of marketing departments to date, pushing out content and driving clicks, but the fact that consumers are using social as a channel for inquiries, complaints, and as a kind of back door to the call center when they aren’t getting their desired resolution, has forced companies to look at social as an engagement platform. This has had numerous impacts, including the way departments communicate internally within organizations. It has brought some broken processes into a very public light, driving companies to reevaluate and re-design customer- impacting processes, including back office functions.

The thing I am most excited about, within these developments, is the potential for using the vast amounts of customer data that are constantly being generated to better understand and ultimately improve customer experiences. This is the greatest area of opportunity for service providers to transcend the traditional call center model, not just providing omni-channel BPO, but also consulting for CX best practices and customer journeys and using analytics to drive value for their clients. This lends itself to more collaborative partnerships and outcome based engagements; I’m seeing more examples of buyers partnering with their service providers to look at customer engagement in a much more strategic way.

And what are you working on first for our clients, Melissa… any sneak previews into what we can expect?

I’ll be getting to work on a contact center operations Blueprint for the first part of next year, followed by some specific research around how companies are handling social customer engagement and service provider offerings in that space. Vertical specific BPO themes will be high on the agenda, in particular as they relate to customer engagement.

Welcome to HfS, Melissa. We’re delighted you have chosen HfS as your analytical home and can’t wait to see you first soundbites hit the presses =)