Charles Sutherland is Chief Research Officer for HfS. (click for bio)

Amidst all the feverish talk of acquisitions and divestitures in the services industry of late, spare a thought for one dynamic service provider focusing its growth the organic way: Genpact. The business process service giant has been stealthily hiring talent left right and center in recent times – mainly from its competitors – as it sharpens its focus on operations services in the finance, procurement and supply chain business services markets.

And we’re impressed with its latest deal – the absorption of respected procurement consulting firm Strategic Sourcing Excellence (SSE), which propels Genpact’s procurement-as-a-service capability to the forefront of the market – at a time when procurement BPO decisions are increasingly being made by the CFO, which is where Genpact rules the roost. Hence a timely move and a smart play to really get to grips on this market. So who better than our own procurement guru, Charles Sutherland, to take a closer look at this integrative move and its impact on the global procurement-as-a-service market space…

Movin’ On Up In Procurement Outsourcing

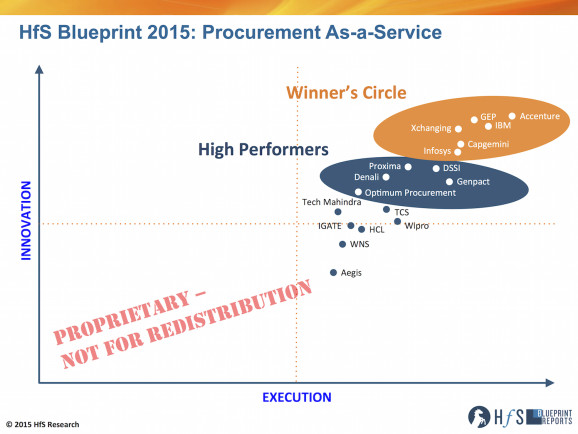

In June of 2015, we published our HfS Blueprint on Procurement As-a-Service which the continued evolution of this market around end to end and modular solutions enabled by cloud technologies and supported by ever deeper category management expertise. At that time, we placed Genpact as one of our “High Performers” with strengths in transactional procurement, process automation, geographic reach and a focus on continuous improvement. But we also felt that by comparison to the market leader Accenture, Genpact still had to further develop capabilities in category management, market intelligence and transformational procurement consulting to challenge for a leading position across the entire market.

We thought that Genpact would likely combine an inorganic acquisition strategy with organic activities such as the aggressive recruitment of category managers and rolling out new technology investment to make a push to move into our Procurement “Winner’s Circle” in 2016. And while we saw signs of the organic activities from Genpact in the 2H of 2015 as some of the other service providers stayed put, we kept waiting to see a coordinated inorganic play as well as 2015 came to a close.

So, now it’s here, the announcement that Genpact has pulled off a combined inorganic and organic play with the announcement of the integration of the transformational procurement consultancy of Strategic Sourcing Excellence (SSE) led by former Astra Zeneca CPO, Jon Kirby. Jon will be joining as the new lead for source to pay services within the CFO Services and Consulting Groups led by Shantanu Ghosh.

The Bottom Line: This may not be a “bet the farm” deal monetarily, but it does show Genpact’s determination to deliver transformational procurement and compete in the HfS “Winner’s Circle” in a market, where access to experienced talent is critical

As we have noted for the last several years, it’s a continuing struggle for all of the major procurement service providers to attract and retain sourcing and category management experts. It’s a “seller’s market for procurement buyers” if you will. Since consulting skills and category management talent are what is key to driving benefits for enterprise clients in procurement outsourcing, they have to be sourced. Hiring individual talent is a time consuming and risk strategy but it’s also easy to over-pay for talent in an acquisition who might not be properly incented to stick around after the deal is done. So there’s an inherent logic to buying just enough talent and leadership to then accelerate the effectiveness of the organic investments as well, which is what we believe Genpact has decided to do.

Genpact can make it into the HfS Winner’s Circle for Procurement As-a-Service in 2016 if Shantanu and Jon use this investment to enhance Genpact’s existing procurement capabilities in the following ways:

Drive the further adoption of As-a-Service solutions and commercial models and to move Genpact away from its historic focus in transactional procurement deals that were build around FTE or transaction based pricing alone.

Respond to the demand from clients for greater depth in category management (on-shore and off-shore) both in broad indirect categories of spend and in niche areas where the long tail of spend in a client creates cost and operating challenges today.

Retain the recent category talent and create momentum for new talent to pick Genpact (rather than other service providers) as a first choice for procurement career development

Reinforce the existing investments in spend analytics and operating insights with a greater business results orientation rather than performance management analytics alone.

Expand the investment in process automation and cognitive tools to replace human agent involvement in procurement processing as well as in sourcing and category management tasks.

Maintain the incumbent relationships for transformational consulting skills with third parties such as AT Kearney to supplement the still growing reach of the source to pay team inside Genpact.

Develop both end to end transformational consulting based solutions for enterprise clients in key verticals while also allowing clients to source more modular, technology and expertise based offerings as required.

The procurement outsourcing market is already one of the most “as-a-service” of markets today but it continues to evolve rapidly and in that time of change there is a real opportunity for change in the structure of the market leaders. The time is now in the adapted words of ‘70s TV character George Jefferson to be “…movin’ on up … to a deluxe position in the Winner’s Circle.. we finally got a piece of the pie”,

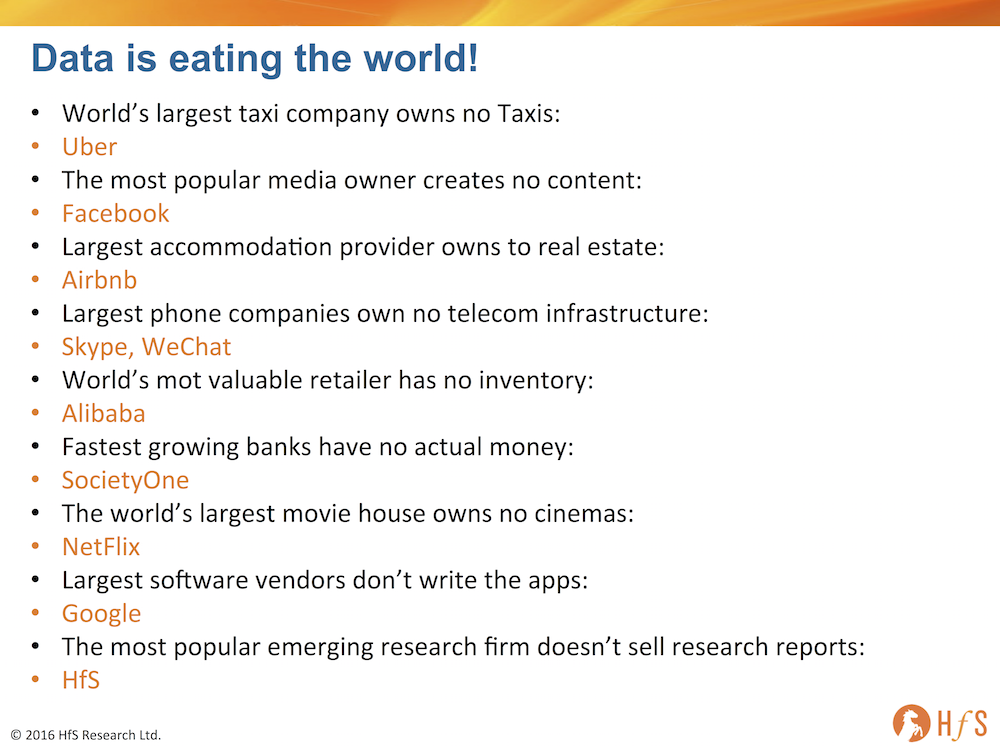

I was intrigued by Drupal’s creator (the open source content platform upon which HfS is built), Dries Buytaert’s, claim that “Data is Eating the World”, a contrarian viewpoint to Marc Andreessen’s famous 2011 quote that “Software is Eating the World”.

In short, Dries is correct in his view that the value is no longer really in owning the software, it’s in owning and orchestrating data powered by huge internet-enabled communities. And it’s also very appropriate to take this viewpoint when we look at the future of operations and service delivery, which I’ll get to soon. But first, let’s peruse several real-world examples where data is king and the orchestrators are not from the world of traditional businesses, including one that is very close to home:

Yes, HfS makes the list because we extract data from thousands of enterprises and create a service to empower them to make decisions and stay informed – in real-time. We do not need to invest fortunes in collecting that data. We merely are the orchestrator of the world’s largest community of service buyers and use digital tools and smart analysts to empower and inform our clients. We do not need physical offices in every major country, or armies of sales people to drive business. We let the community come to us and we facilitate the research data collection to reach our global participants.

And it’s the same in all of these other markets – the legacy (former) incumbents can see exactly what is going on. But sadly – for many – it is already too late to disrupt their revenues and survive. The sad truth here is that if you already know you’ve been disrupted, it’s probably too late.

The Bottom-line: The services winners are shifting the model from proprietary software and people scale to qualitydata creation and capability… as they make the true leap to true As-a-Service

A similar disruptive trend is occurring with regards to service delivery. Gone are the days when owning proprietary technology – and global capacity – was king. Yes, there are certain discrete segments in which owning software tools provides real competitive advantage (such as procurement and supply chain), so some providers can still steal a march on their competitors. But as more and more software apps become increasingly accessible and industry-standard, the value shifts to the quality of data and business services providers can offer to optimize the software platform, as opposed to providing the software itself.

Today, software is the commodity – any service provider can slam in a Salesforce, a Workday, a Sage, a Blackline, a SmartStream, etc. The value the service provider needs to build is in the data model templates that can be standardized across multiple clients, tweaked when needed and delivered by service talent that understands the data to really empower their clients.

Owning vast software and infrastructure resources is becoming secondary to being the orchestrator of core enterprise systems-of-record data. Today, we are seeing several exciting niche as-a-service providers spring up where automation is already native to their environment, where they do not need the massive people scale of yesteryear to deliver processes which should be standardized and much better automated today. The more ambitious clients focus on outcomes with their partners, the more the onus will turn to the quality of data being managed and analyzed, and the winning providers will be those who can do this using much smarter technology and people capability – at much lower cost to the customer.

And being able to orchestrate the delivery across multiple clients creates powerful process data templates that are much more “plug and play” for clients than in the past. This isn’t new, but it’s really evolving, and the availability of better tools and robotic automation, coupled with the advent of cognitive computing and advanced analytics, are the accelerants for providers to become true orchestrators of their clients’ collective experiences and best practices, as opposed to owners of proprietary applications and legacy lock-in systems.

I’m personally excited by the advent of these As-a-Service providers. Facilitating and empowering the core data of the enterprise is where the real value is. This is the “lock-in” of the future: not holding clients hostage to software licenses, but instead holding them ransom to the value of the data you are enriching for them.

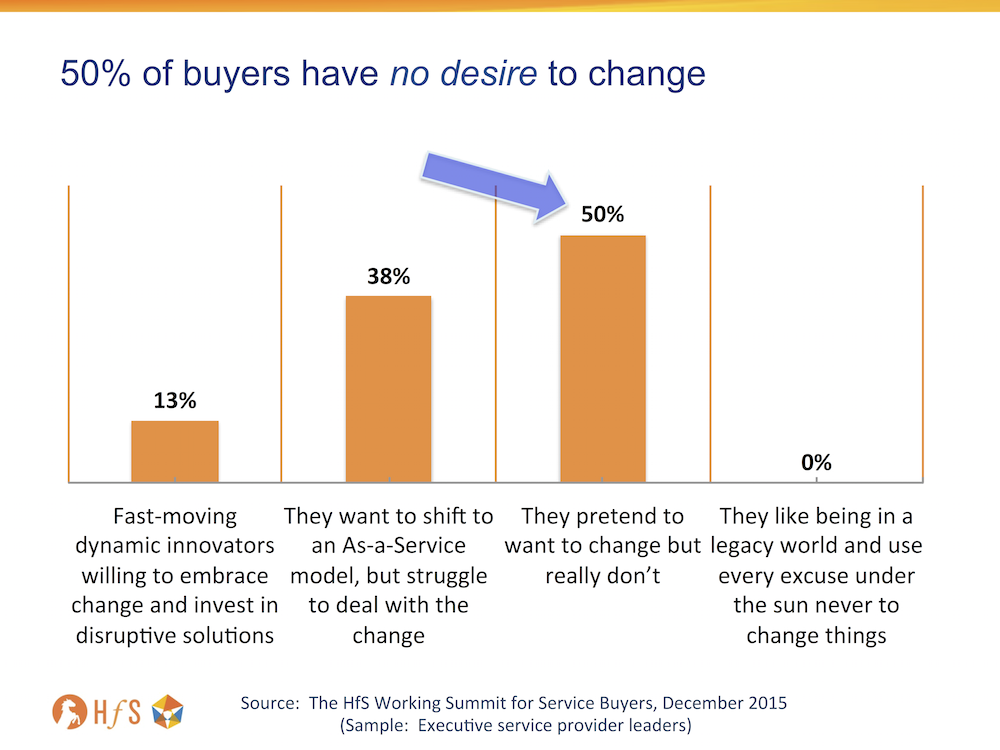

If you haven’t been bored silly listening to all the rampant change we are about to endure from literally every information outlet (and we are also complicit), then this data point from our recent Harvard Buyers Summit will open your eyes. Simply put, when we anonymously polled the service provider leaders in the room on what they really thought about buyers, half of them view them as only pretending they welcome change, and don’t really want to:

Click to Enlarge

On the positive side, 50% do want to change, but most struggle, but the fact that so many are only paying lip service to their peers, colleagues and service partners is a real issue. How can you effectively target clients you can grow with as a provider, if you can’t really trust the intentions of half your clients? And how can you drive initiatives as a buyer, when most your colleagues really do not have any interest?

The Bottom-line: You must weed out the change imposters if you don’t want to go down with them, or find another employer who promotes change

Smart consultants and practitioners are those who can quickly read their colleagues to find out if they genuinely are prepared to do things differently – and make real efforts to learn new methods and create new ideas. And this is really done through the legacy old school techniques of developing close relationships. You’ll learn more about someone’s attitude and approach over a few drinks or a nice dinner than sharing big words and corporate pleasantries in a boardroom.

Your skills to collaborate and engage with people is critical in identifying where people need to change, and how we can all improve as a team. This is where methods like Design Thinking are so important – there is little hiding from initiatives where the outcomes are clearly defined, prioritized and an execution plan is put in place. If people really do not want to embrace change, then they can’t hide forever, and clearly many are in this camp. However, if you surround yourself with unambitious people, they will eventually throw you off their sinking ship to save themselves…

Alternatively, if your company is fully laden with change-imposters and there’s no simple way to avoid them, despite your best efforts, then get out of there now. You owe nothing to an employer unwilling to foster change and encourage innovation, and there is such a talent shortage in industry these days, you’ll find plenty of firms willing to take you on with your attitude…

Utilities organizations are under real pressure on many fronts to improve their operational performances, with many are facing competition for the first time as a result of deregulation and feisty competitors offering genuinely disruptive solutions.

We asked HfS Research Director, Reetika Joshi, to take a deep look at the marketplace, with the resulting HfS Blueprint Report: Utilities BPO 2015 looking at traditional BPO services, in addition to emerging As-a-Service platforms and evolving commercial models. Plus, Reetika uncovers robotic process automation (RPA) and analytics in service delivery.

So let’s get an up-close view from Reetika:

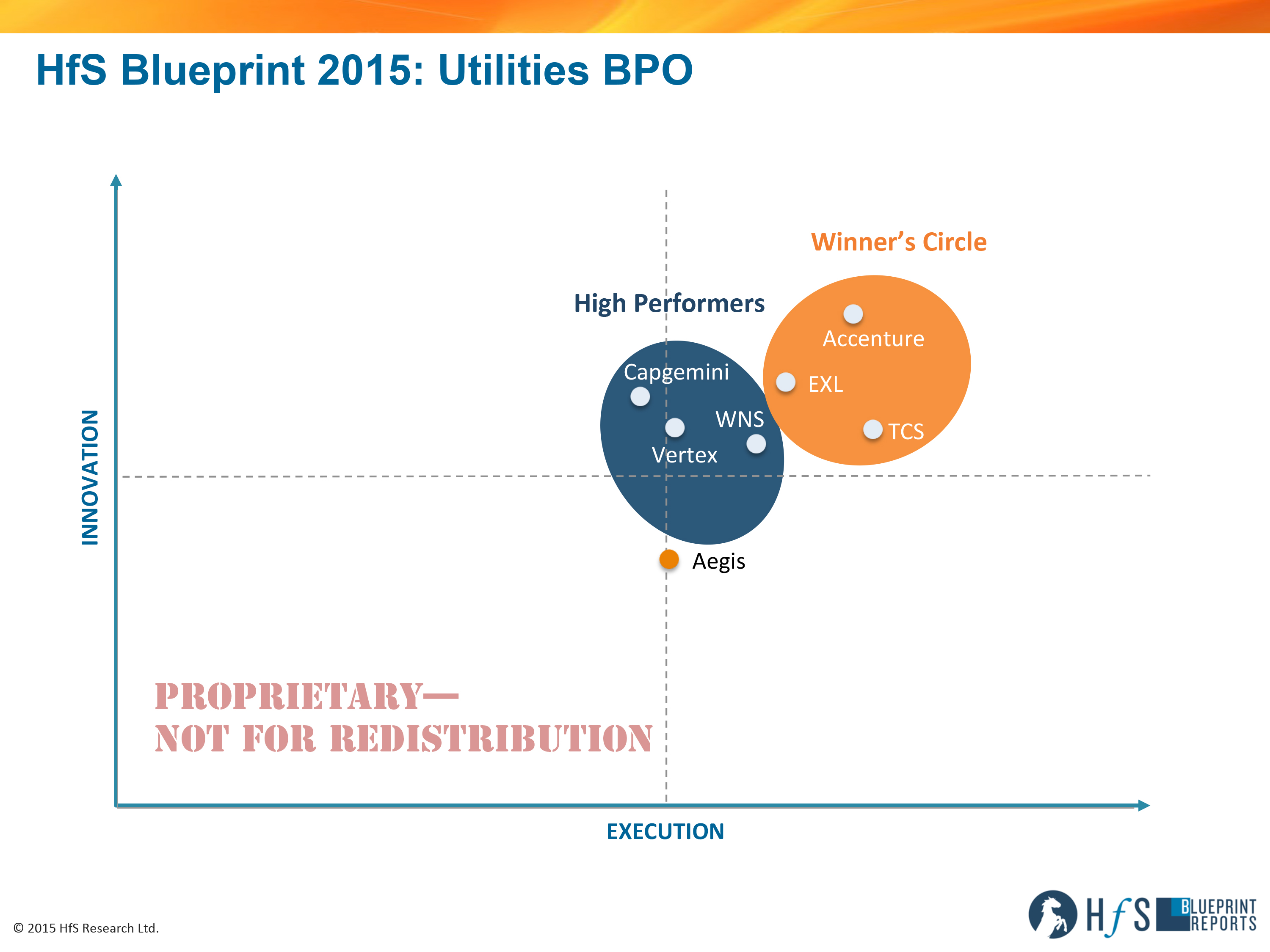

Click to enlarge.

What’s on the minds of utilities services buyers, Reetika?

Our Blueprint research shows that utilities face a harsh reality in dealing with a burning platform for change today. They need to address three sets of sweeping industry forces:

Rapid innovation to grow top lines, with new energy sources, distributed power systems, changing business models, more smart grid and meter rollouts, more deregulation and a new breed of competitors ranging from internet companies to cable providers.

Customer centricity to differentiate, with consumerization that has driven customer interactions onto digital channels, changing preferences with rising environmentalism and technology advances and customers’ need for more control in energy types, sources and efficiencies.

Operational efficiency to manage bottom lines, with the global decline in power demand due to greater energy efficiency, constant debate in regulations over environmental and market policy measures, aging assets that need to be maintained and retired while acquiring new ones, and the resulting outdated legacy systems, internal structures and operational environments.

Report author Reetika Joshi, HfS Research Director (click for bio).

How does this impact BPO…what is the state of the utilities BPO market today?

Utilities BPO engagements have fulfilled very traditional needs in the last 15 years. Buyers have leveraged third party service providers predominantly to administrate their meter-to-cash operations. These volume-based activities require processing power for growing customer bases, and service providers filled the gaps well, from customer acquisition, contract processing, account maintenance to billing and cash collection. A large part of the work involves intensive call handling for support services such as debt collections, onboarding, complaints, inquiries, outage reports, etc. Cost pressures led utilities to further outsource ITO, supply chain and procurement, payroll management and accounting services. We are still hearing about interest in such traditional BPO service delivery built on labor arbitrage and process consolidation, as a section of the utilities market is still new to outsourcing and risk-averse. However, we expect this model to change in the medium to long term as As-a-Service components make their way into the mainstream.

Service providers have been instrumental in writing off legacy from a technology and consulting perspective. They have seized the opportunity to help utilities gain agility and speed to market on new product development and deriving value from smart meter and advanced metering infrastructure deployments. BPO operations are now a derivative opportunity for modernization after system upgrades. In some cases, service providers that have a long history of working with utilities have taken big leaps in bringing in automation and analytics in meter-to-cash, asset management and horizontal processes to realize new value. Others that are domain experts in customer experience are taking utilities along the journey to customer centricity similar to other retail-facing verticals.

So who’s winning in utilities by adopting an As-a-Service approach?

The HfS Winner’s Circle For Utilities BPO features service providers that have invested heavily in vertical-specific innovation in the last couple years. In the last two years, we see a heightened focus from leading service providers on enabling service delivery for true value creation — away from labor arbitrage, where large deals primarily constituted re-badging of FTEs, selecting basic SLAs and lift-and-shift of processes to the service provider.

The Winner’s Circle includes Accenture, EXL and TCS:

Accenture — demonstrating an advanced capability for utilities As-a-Service spanning platforms, automation and analytics

EXL — a partner willing to invest and evolve with utilities clients towards Smart operations

TCS — one of the largest meter-to-cash service providers pushing RPA to the forefront of utilities operations

EXL and Accenture are playing a greater role in core utilities operations such as field force management and support using predictive modeling and forecasting to optimize labor effort. Both are also developing offerings to support new operational areas such as new energy solutions and smart services. TCS has been instrumental in building collaborative engagements by committing to outcomes, gainsharing and using RPA and analytics to improve utilities operations.

The High Performers in this Blueprint include Capgemini, WNS and Vertex. These service providers all have over a decade of experience in running BPO operations for utilities clients. They have varying concentrations of geographical experience, across continental Europe, UK and the US respectively. We see the potential for differentiation with all three, with Capgemini’s thought leadership on smart grid and AMI technology that needs to be better integrated with BPO, WNS’ customer journey frameworks that utilities are finding to be extremely relevant, and Vertex’s evolution from a customer care BPO brand to an As-a-Service provider with its new customer interaction platform, VertexOne. It will take these service providers some time to bring scale to these advances in their utilities BPO portfolios, and we expect significant competition exerted by them to the Winner’s Circle providers in the near future, depending on the client geographies being targeted.

What’s next for this market?

The industry challenges for utilities service buyers that we outlined earlier resonate well with leading service providers. They are increasingly aligning themselves to deliver on such outcomes through a range of offerings and partnerships to bring the best-of-breed technologies and services together for utilities clients.

To continue to add value, service providers will have to develop and demonstrate the following capabilities in the next few years:

Significant expertise in various intelligent automation technologies to automate back-office processes and release FTEs in legacy contracts in meter-to-cash, F&A, and HR.

Flexible commercial models, especially for new energy products and services where utilities require more variability to test market demand.

Developing multi-channel customer interaction services in multiple geographies, particularly 24/7 support for critical interactions such as fault and emergencies.

Continued evolution of smart service offerings as service providers get more hands-on experience with new deployments.

Consultative support and collaboration tools such as design thinking methodology to orient utilities operations around the customer journey.

Overall, we see a growing appetite for change with utilities services buyers, but execution will be entrusted gradually to domain/geographic experts. HfS sees utilities services buyers starting to realize that they need to fundamentally rethink their business models and operations, spurred by industry disruption. Being asset-laden and capex-intensive commodity providers traditionally makes it an extremely challenging environment for driving internal change. It will thus take this vertical longer to write off legacy and execute on strategic priorities that are being set now. However, the ones that can engage a broader ecosystem of partners to play catch-up on consumerization and new technology investments will see greater differentiation, even with the pace of regulatory and industry change underway today.

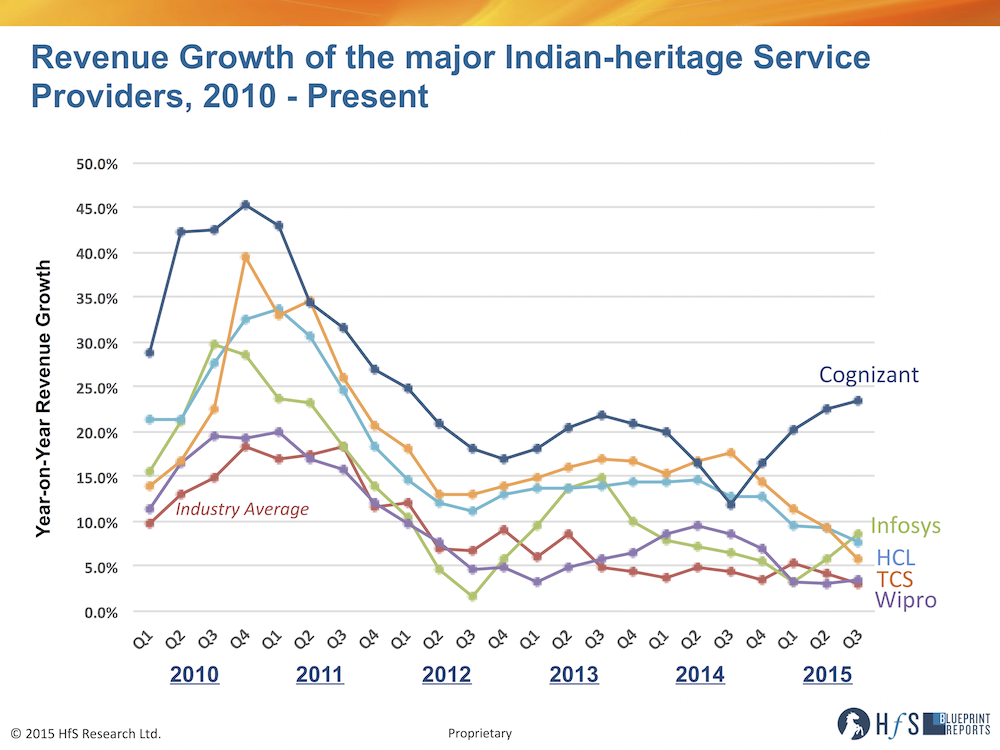

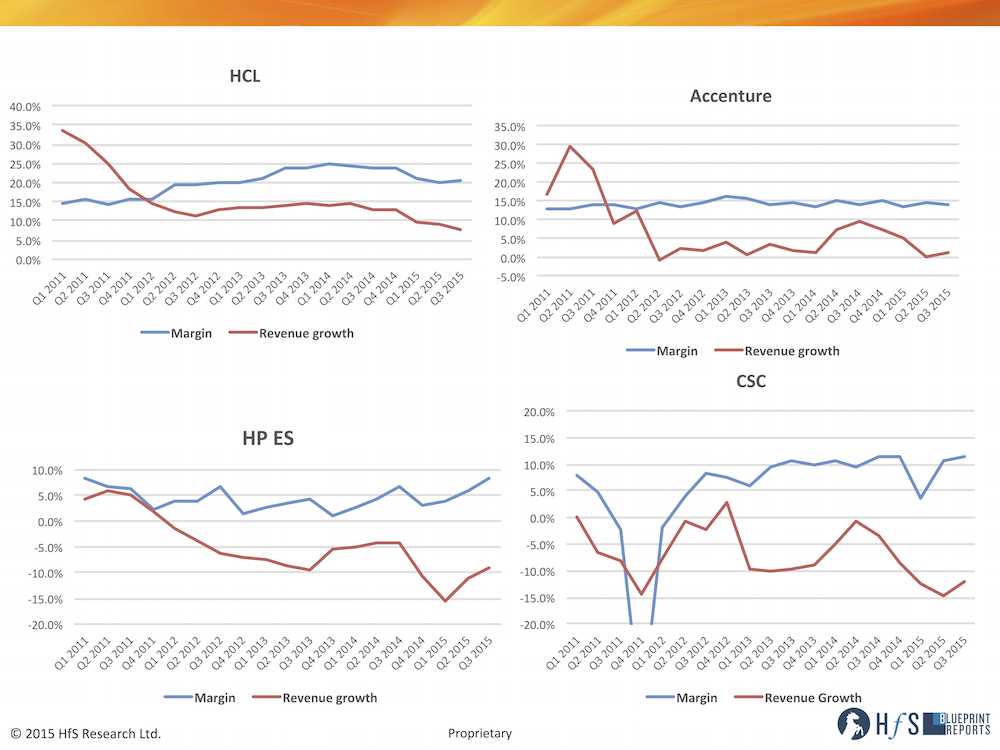

It’s on… 2016 is the year that will separate the service dinosaurs from the savvy cannibalizers, as revenue growth slides towards negative territory and the onus shifts from selling more buttocks on seats to maintaining sexy profit margins.

Cutting to the chase, the technology and business services industry is becoming a very different place, and those of us failing to adapt, should start considering alternative career plans. I hear massage therapy is in high demand these days…

Click to Enlarge

So what will really happen as we embark on our negative revenue growth journey? Here are five scenarios detailing how this will play out…

1) Big sucks – especially for providers… so get smaller and smarter. You’re still huge, clunky, siloed and political, constantly looking at “new” ways to reduce the workforce, while only being allowed to bid on big legacy deals, where the advisor is (still) squeezing everyone for price and your marketing team is still pretending you’re delivering nextgen solutions to clients (which you really aren’t). Under all the swirl of nonsense, you’re strategy is still really all about carting in even cheaper, younger kids from even cheaper, more remote places, and quietly ushering your burned out middle-management the exit. Meanwhile, as the allure of big provider life fades, many of the stars you want to keep are getting enticed by the thriving start up scene. Yes, people, being big and clunky is an increasingly crappy place to be, and many people reading this will be nodding violently that this is where they, quite frankly, are.

2) The mid-tier BPOs and up-and-coming As-a-Service providers have a great opportunity to steal the show. You either need to find sole source clients prepared to co-invest with you in their futures, or start to cater for new-gen deals that force you to build out your multitenant delivery

infrastructure to entice future clients. Believe it or not, these are interesting times for the mid-tier BPOs which can scale down for smaller deals and build out BPaaS capability for the future. Watch out for the likes of EXL, WNS and Sutherland which have all been active with the smaller stuff this year (while growing their business at a healthy clip). Other mid-size providers worth keeping an As-a-Service eye on are OneSource Virtual, which recently expanded its Workday-based HRO offering to accommodate FAO, Aassonn’s focused play around SAP Successfactors and Equiniti, a UK-based services firms very focus on BPO services tied to finance and banking technology. Also keep tabs on the ambitious contact center providers, such as Concentrix and HGS, which are verticalizing their offerings and leveraging new technologies and talent strategies to take on higher value work with much more scalable models. We are truly witnessing the convergence of BPO across the horizontal and vertical domains.

3) Disrupt your competitors’ business upon rebid. This is where things are going to get really interesting. It’s hard enough making revenue sacrifices (a.k.a. cannibalization) to keep ambitious clients happy, but – surely – it’s more rewarding (and P&L additive) to go after your competitors legacy clients with a much more robotically-automated offering with nice savings incentives? It’s not really cannibalizing when it’s acquiring new business, is it? Expect to see a lot of nastiness where providers just go and rape their competitors with all their new fancy robotic stuff and promises of cost impact taken straight from the Gartner scare-manual…

4) Sell your legacy stuff while you can get a good price for it and “re-emerge” in the future. There are several providers out there who simply cannot figure out how to compete in the “new” market while maintaining a legacy portfolio of clients, which are increasingly less profitable and almost impossible to do anything with beyond beg them to renew and cheaper rates. So why not get the hell out while you can? Sell that legacy stuff while you can still get a half-decent price for it… reinvest that money in building true BPaaS offerings with native RPA and real cognitive capabilities… invest in the F500 of 2020, not the F500 of 2016….

5) Just milk the legacy model and play the old game. Yes, there is enough legacy business out there so that you can still survive, if you pick the right deals and go after them in the right way. There are several service providers successfully operating in this fashion, and they are very happy to keep picking off the detritus of the labor arbitrage model, as that is what many legacy enterprises want – “just do it cheaper with minimum fuss, let us dictate what we want and we’re happy with the short-term savings”. And there is a lot of legacy business on offer in the upper-middle market which has yet to be infiltrated by the Tier 1s. There is a room for the unsexy body shops to play, and I see many of them sticking around for some time to come…

However which way we look at this, 2016 is the year many providers will be hitting negative revenue growth, and sustaining those nice profit margins will be nigh-on impossible, without driving major changes to the way they operate, hiring capable talent, making smart acquisitions and rethinking their own cultures. The numbers, quite simply, tell a stark, frightening story of where this is all going:

Click to Enlarge

Click to Enlarge

The Bottom-line: The major service providers need to be laser-focused on a three-pronged strategy to survive

i) Target core existing clients to develop co-investment strategies for future survival. Buyers will need to make new investments in automation technology (both robotic and IT) and people expertise to make it work, while their service providers will ultimately have to concede they may need to reduce the FTE provision on their side, as automation takes effect. The real challenge here is for the service provider to encourage their clients to have them redeploy the freed-up FTEs on their clients’ higher value processes. So these two motivations should go hand-in-hand: decreasing labor effort on automatable tasks and increasing it on the higher-value work the clients would like to outsource in the future. So… if buyers and their providers can get this right, intelligent robotic process and IT automation will be a long term play for both parties, where higher value work gets done and delivery staff are kept busy because of the closer collaborative relationship and greater volume of work being parsed out.

ii) Target your legacy competitors clients with solutions that drive that next wave of value. The likes of HCL, TCS and Cognizant have feasted off HP, CSC and IBM clients for two decades now as they could offer real cost-impact through smart global delivery capability. Now we’re in a rat-race to develop the right blend of robotic automation platforms, cognitive capability, combined with global delivery talent, to offer clients those next waves of delights. And this isn’t going to all be the same cast of characters as before – and will require a lot more risk-taking than before, as driving savings and value through other means, and not just cheaper labor, is challenging. Those providers with these capabilities can break this cycle by building multi-tenant solutions for the future – and will be the winners. I believe this could happen in barely a couple of years, when you look at the current pace of change and mood in the market. The key is to pick off the next 15-20 deals they can win at lower margins in order to invest in common automation, robotic processing platforms, common analytics, common SaaS underpinnings and common service skills – hence a more competitive, more scalable multi-tenant As-a-Service delivery model.

iii) Bring in new leadership blood which truly understands the As-a-Service Economy and what it takes to get there.It’s easy to point fingers at certain service providers for preserving the legacy FTE labor model, but the stark reality is that many of them simply don’t have leadership prepared to invest in the depth of talent, or technology capability to drive genuine advancements. So – let’s face facts here – 2016 is presenting an impasse of seismic proportions out industry had yet to experience. There are tremendous opportunities to create genuine productivity advancements through robotic process automation, smarter analytics and the onset of cognitive computing, but much of the present service provider bunch are not going to be the ones to take true advantage of them. I predict a few will break out, but the next winners will be from a new breed of As-a-Service provider, many of whom many not even have been formed yet.

We’ve pooled all the big discussion topics from our recent service buyers summit in Harvard and let our analysts loose to demand 10 big things the industry needs to address if we are going to drag ourselves away from legacy land and avoid becoming massage therapists… and venture into the promised land of the As-a-Service Economy:

Click to Enlarge

1. Outsourcing is now part of a broader management capability; it is not a standalone profession. Outsourcing is a competency that is learned on the job and through real experience as opposed to a qualification or certification. It is an ongoing, amorphous capability that has no end-state or stamp of perfection, it is the ability to partner to improve constantly processes, outcomes and performance. Outsourcing is a means to improvement, access to resources and better capability, usually not the means to a specific end.

2. Intelligent Automation has emerged as a core competency for operations staff. Like outsourcing,Robotic Process Automation (RPA) is a means to improve processes and applications, but rarely the ideal end-state – it typically is retrofitted to make legacy applications and processes function more automatically and efficiently. Legacy operations delivery and BPO can only achieve a certain level of efficiency, without a well-planned Intelligent Automation roadmap. RPA is one of the leading technologies to provide efficiency improvement in rules based tasks and processes, but Intelligent Automation (see link) is also now including the adoption of real time self-learning techniques, predictive analytics and cognitive computing.

3. Ambitious providers will cannibalize their revenues when their buyers give them more to work with. Moving forward, buyers will need to make some new investments in Intelligent Automation (especially RPA) technology and expertise, while the service providers will ultimately have to concede they may need to reduce the FTE provision on their side, as automation takes effect. A service provider must prove it can redeploy “freed-up FTEs” on their clients’ higher value processes. So these two motivations should go hand-in-hand: decreasing labor effort on automatable tasks and increasing it on the higher value work the clients would like to outsource in the future. So, if buyers and their providers can get this right, automation will be a long term play for both parties, where higher value work gets done and delivery staff are kept busy because of the closer collaborative relationship and greater volume of work being parsed out.

4. The race to the bottom is killing innovation. This is tied in part to Insight #3, large outsourcing deals have been driven by desire to drive out costs continuously and make the processes increasingly more efficient. This constant race to the bottom is not sustainable and is impacting service provider’s ability to add value to deals in a tangible way. Although, service providers need to take notice of Insight #3 and work with buyers on automation to help plug this innovation spending gap.

5. Design Thinking is a real, tangible practice that can bring together common outcomes and support co-innovation activities across buyers and providers: The core issue holding back the services industry are relationships being too “Directional” and there needs to be a pre-agreed willingness and desire on both sides to get to the table, on an ongoing basis, preferably in close physical proximity, but also using visual media collaboration tools:

Effective Design Thinking can work, provided both buyer and provider can use the method to agree, prioritize and ultimately execute on common outcomes that constitute success for both parties. One buyer said we must learn to “think big, start small, and adapt fast”, which is the heart of the design thinking ethos. With many making the point that design thinking is not about turning all your staff into product designers, it’s a technique to empower staff to become change agents. Used in conjunction with rapid development techniques like DevOps, it allows staff to make changes with a great deal less investment and resultant risk. One buyer at Harvard put it like this “empowering process owners and overcoming fears of accountability is a crucial step moving toward the as a service economy.” Although there was a note of caution, the edge given by design thinking may be short lived as its second nature to Millennials, they don’t need design thinking, they just call this thinking!

6. The critical skills to be effective with As-a-Service are adaptability, creativity, and interpersonal communication. Service buyers and service providers need to provide an environment for “fast fail,” and allow for risk in order to more decisively shift sourcing engagements from “directive” to a “vital partner”:

We are in a world of constant change and fast moving developments. To capture the value, we need to have effective ecosystems brokered by Global Process Owners. These people can define business problems, identify opportunities and broker relationships to bring the best solutions together across internal and external resources. These skills are developed through experience, not by training, and challenges HR to rethink its approach to hiring. Creating a more “fluid workforce” by shifting selection from an inventory of skills to a candidates “coach-ability.” HR needs to be more effective in defining and building these ecosystems in order to effectively recruit and manage the people who will make it happen. The generations entering the workforce and growing up in it today, may not have a career “path” so much as a career “journey”—a general direction that is taken in steps that follow their interests and capabilities matched to opportunities.

7. The strategy behind the deployment of Digital Plug & Play Services remains bifurcated. Enterprises are rapidly increasing their investments in digital platform based services that deliver processes around a system of engagement (e.g. CRM, Marketing, HCM, Procurement) but remain as reluctant as ever to take on re-platforming core systems of record (e.g. Finance, Accounting and Claims Systems). As a result, Intelligent Automation will be focused around systems of record, to prolong the life and extract greater value for enterprises out of these legacy platforms for the next several years.

8. Automation is impacting entry-level roles—and the industry is not prepared. The roles that used to drive entry into business process and IT careers (e.g. data entry, level 1 help desk, systems admin, exception processing) are changing as many of the core tasks for these roles are being addressed by deployments of Intelligent Automation. As an industry, there is a need to recognize this change and determine what will constitute new entry-level roles and career paths for the future. This means changing many elements including: educational programs, models for recruiting and training new employees, promotion and evaluation criteria, supervisory role definitions and more. It also means that middle management baby boomers and Gen Xer’s will have to accept that their reports will build their careers on criteria that are new and sometimes hard for the older employees to recognize and accept.

9. Organizational design will become a key differentiator. Workforce demographics, rapidly changing employment contracts, business process automation, and cognitive computing will collectively stretch traditional employment and organizational models to the breaking point. Enterprises that are able creatively to leverage these disruptions will not merely succeed, but will replace once-respected slow-to-move competitors.

10. True shared risk/reward contract structures that buyers and service providers actually buy into will emerge. New shared-risk, shared-investment deal structures at the transaction level, and relationships akin to alliances will be the models that produce the most rapid and satisfactory results in the maturing as-a-service economy. The rapid wins made possible by large-scale adoption of robotics, cognitive computing, and the altered workforce relationship will create an imbalance in contracts that are not structured with those successes in mind. While the high end has the volume and the opportunity, look for upstart providers with novel deal structures to take share early in the next wave of innovation. One of the delegates put it “to advance towards the As-a-Service Economy we have to move beyond case studies and facilitate connections of stakeholders.”

The Bottom-line: 2016 will be the year where the fog lifts and we figure out how to adapt

When we look back at 2015, I think we’ll reflect on a year of confusion and too much over-thinking of what’s happening down the road. What we learned at Harvard is that many enterprise buyers are much more aware of what is possible, but struggle to engage effectively with their provider to risk more and share more to find new thresholds of value.

However, there is a strong realization that if you fail to tie your career to Intelligent Automation, understanding how to leverage digital technology more effectively, noone’s going to wait for you to catch up. None of this stuff is rocket science, it’s simply resetting the goals and revisiting stagnant relationships to figure out a realistic way forward. Sadly, I do think money and cost is the ultimate arbiter of change, and it’s not until the providers really start to feel the squeeze on their profit margins, and the clients get tempted by disruptive rebids, will we really see much of the change described above become reality. Those service providers and buyers which have not yet begun to address (with genuine investment) the reorientation of capabilities and enablement of technologies to support business model disruption, are already circling the drain of yesterday’s legacy.

To Apply for a Seat / lead a session (buyers only): Email us here

This promises to be another UK style “throw the kitchen sink at everything crappy about our service industry”

We’re back at Gonville & Caius College, Cambridge this Spring (Click to learn more)

Join these core discussions where we’ll finally address these issues:

The Race to Irrelevance: Are we on a race to the bottom, or are we genuinely in the midst of change: Are service providers really selling what service buyers actually need? Europeans v Americans: Who’s outsourcing smarter and where can we improve to get to the As-a-Service Enterprise?

Demystifying all that Robo Hype: What is the realistic place for a Robotic Process Automation strategy inside the enterprise – and what should Service providers be doing to support it? Digital Transformation: It’s really all about the business, stupid! Beyond the Transition: How can service buyers and providers really share their risks to achieve longer-term gains? Ending the Master/Slave Model: Can service buyers and providers leverage “Design Thinking” to fashion a collaborative relationship with a common purpose, common values and jointly desired outcomes? Getting beyond the Paperwork: What does it really take, in today’s environment, to execute and manage a meaningful, effective and lasting contract? Getting past that “outsourcing career track” discussion: Is the outsourcing “profession” now part of a broader management capability? The Message we have to Send Back to the Industry: How can we fix this industry to deliver the As-a-Service Enterprise?

Service buyers email us here to apply for your seat…

While the benefits of the cloud and the pervasiveness of new digital technology impact our professional and personal lives – more than at any point in history – the need for the tech skills to make this all work has never been under so much intense pressure.

Not every firm can drop $200K a year on whizkid programmers who can actually handle this stuff, so the focus moves to those firms which can do this effectively and affordably. The industry’s only dedicated engineering services analyst, Pareekh Jain, has been micro-focused on the emerging engineering service industry over the past couple of years and today unveils the industry’s first unvarnished view of software product engineering capability of the leading service providers.

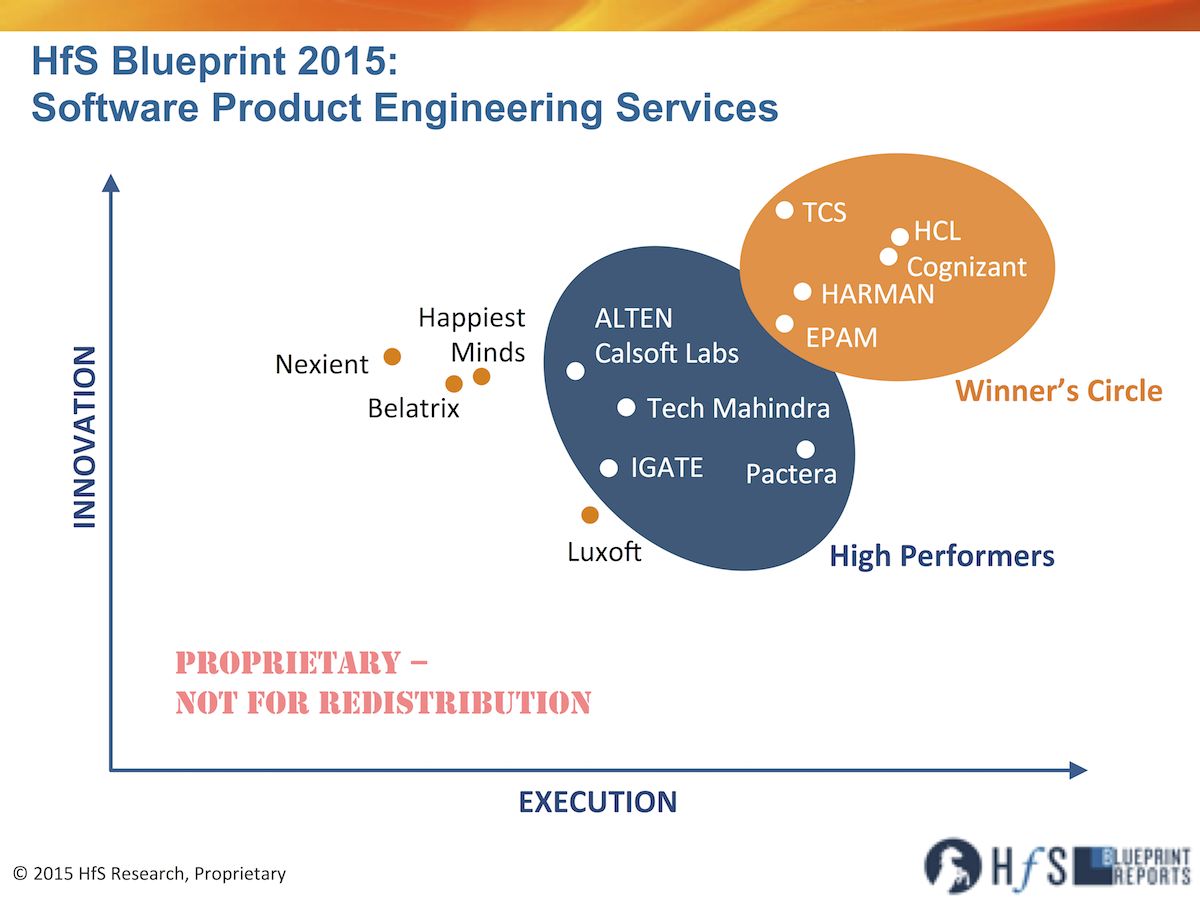

This is our second engineering services Blueprint. In the first one, we focused on the provision of engineering services for physical products. In this Blueprint, we look at Software Product Engineering (SPE) services in detail. So let’s turn to Pareekh to learn more about his Blueprint experience in this emerging space:

Click to Enlarge

Pareekh, how do you see this market evolving and what are the key drivers for software product engineering services?

This market is very dynamic today. A few years ago there were only a few specialized and small service providers who strategically focused on this market. Large service providers generally treated this market and clients more opportunistically. Their product engineering service capability was relatively small and often sat inside a larger ADM practice. Overall the attractiveness of ISV market was not high enough for large service providers to make investments to serve this market in detail. Now the market attractiveness has increased because of two reasons. First, as ISVs (Independent Software Vendor) are moving to As-a-Service, they need help. Second, as more and more products are software driven in IoT world, enterprises need help too. Traditional software product engineering outsourcers were ISVs. Later internet companies who faced similar challenges of scalability, reliability as ISVs also became a major customer segment. What we are now witnessing is an emerging trend with the rise of IoT that all products and industries are becoming smart and will need software solutions for scalability, reliability and connectivity. The traditional ISV market had limited potential and was driven by the R&D spend of ISVs but this much greater market for software products beyond ISVs has huge potential. Consequently, service providers both large and specialized are increasing their attention on and capabilities to serve this market. We have observed new specialized service providers have also emerged in this space in the last few years.

And how did the Blueprint analysis turn out?

Pareekh Jain is Research Director, HfS (Click for Bio)

This Blueprint analysis was interesting. First we researched how service providers are making investments in helping ISVs transition to As-a-Service economy and used these criteria also in evaluating service provider capabilities.

The scope of this Blueprint was software product engineering services for ISVs and internet companies. We excluded software product engineering work for enterprises because it is still an emerging area and there is a lack of a common understanding among service providers of what enterprise work will qualify as ADM versus SPE.

We evaluated 13 service providers for this study. These service providers include providers which are China centric, Eastern Europe centric, Latin America centric, and 100% domestic US sourcing centric in addition to India centric service providers. This is much geographically dispersed than most other outsourcing markets we research.

There are five service providers in our Winner’s Circle – Cognizant, HARMAN, HCL, EPAM, and TCS (in alphabetical order). They all have the scale and are making investments in technologies, design and IP capabilities to push this market forward.

High Performers and other service providers are also capable of delivering high-quality services.

I was also impressed by three small service providers Belatrix, Happiest Minds and Nexient which are new age software product engineering service providers without any legacy hangover. Their scale is very small, and practice areas are still evolving, but their direction is good. They all have a promising future if they are able to scale up with systems and process and able to maintain their focus.

In this Blueprint, we also focused on benchmarking and operations improvement. This is first of its kind of software product engineering services study where we tried to collect important operating data from software product engineering service providers and arrived at the aggregate or the average software product engineering services industry metrics. This should help each software product engineering service provider and captive to benchmark their operations and identify their strengths as well as areas or levers of improvement.

Pareekh, what regions are excelling at providing affordable software engineering services? Is this still all about India, or are we seeing new regions emerge, such as Romania, Russia and China. And is onshore in the picture?

The majority of software product engineering work is still being done out of India, but we have found of pockets of excellence in Central and Eastern Europe (mainly Ukraine, Romania, and Russia) and China. The buy-side customers have highlighted that the cost of doing work from Eastern Europe is slightly higher than that of India. In addition, we are seeing some increased delivery investments in Israel and Silicon Valley becoming increasingly important for several customers, as it helps to leverage synergies with their innovation ecosystems, especially with several of the leading service providers making augmenting their delivery center capabilities in these locations.

So what are your key takeaways from this study and what should we be watching for in the next few years?

There are five key takeaways. First, there is renewed interest in this market and technology developments are creating interesting market opportunities. Second, for buy-side access to skills and time-to-market are most important drivers for software product outsourcing. Earlier it was cost and time-to-market. Now new technology developments have increased the importance of access to skills relative to the cost. Third, ISVs are facing disruption and need the help of software product engineering service providers in their “As-a-Service” journey. Fourth, scale is becoming important for service providers to make investments. Fifth, New service providers are entering this market and some service providers which were ignoring this market are making investments.

We will be watching four key trends. First, how will the software product engineering services revenue grow for service providers? Does it grow faster than overall IT services revenue? Will new service providers enter this market? Second, how will service providers build their scale organically and through mergers and acquisitions? Third, how will service providers augment their capabilities and service offerings? How some of the critical areas identified by us such as DevOps, product management, automation, design thinking become prevalent? Finally, will we hear examples of successful software product outsourcing case studies from new disruptors and Unicorn companies which are important and growing segments but still under-penetrated for software product outsourcing.

If you haven’t been bored silly listening to all the rampant change we are about to endure from literally every information outlet (and we are also complicit), then this data point from our recent

If you haven’t been bored silly listening to all the rampant change we are about to endure from literally every information outlet (and we are also complicit), then this data point from our recent